1 Introduction

This paper investigates the optimal design of brokerage fees in Almgren-Chriss model (see [1]). We consider a population of investors (a.k.a. potential clients or agents) who can either trade directly in the market (and be subject to trading costs due to their price impact) or to trade via a broker (i.e., to become broker’s clients) who charges a contingent fee for this service. The main goal of our investigation is a tractable characterization of the optimal brokerage fees and the optimal choice of a portfolio of clients.

This question is formulated as an optimal contract problem with multiple agents, where the broker plays the role of a principal who designs the fees.

The problem considered herein formally fits within the optimal contract theory, which is concerned with the design of compensation (or incentive) schemes, referred to as contracts. In the classical example of an optimal contract problem (see, among others, [9], [7]), a principal hires an agent to work on a project in exchange for a payment (contract). The payment depends on the information available to the principal which may be affected by the agent’s action. The agent chooses his action to maximize his objective, which depends on the payment promised by the principal and on the action itself (e.g., the agent may not like to work very hard). The principal aims to choose the contract so that it maximizes her objective, which also depends on the payment to the agent and on the agent’s action. This leads to a pair of nested optimization problems, also known as the Stackelberg game.

In the present setting, the broker observes the trading strategy of her client precisely, which leads to a so-called first best optimal contact problem between the broker and her individual client. Such optimal contract problems are known to have simple solutions (especially in the case of risk-neutral preferences, as herein), and this is confirmed by Proposition 1 which provides the optimal brokerage fees in the present setting. However, our setting implies the following additional challenges. First, the model considered herein includes multiple agents whose objectives are coupled via their price impact. Thus, a collective response of the agents to a contract chosen by the principal is given by a collection of strategies that form a Nash equilibrium among the agents. The principal, then, chooses a contract so as to maximize her objective that depends on the associated equilibrium strategies of the agents. The optimal contract problems with multiple agents are considered, for example, in [8], [5], [10]. It is worth mentioning that we consider heterogenous agents, as one of our goals is to study how the characteristics of the agents (i.e., their price impact coefficients) affect the optimal choice of the portfolio of clients.

Another important feature that makes the present problem non-standard is the fact that the reservation value of each agent (which represents the minimum objective value that the agent must be able to attain in order to accept a proposed contract) is determined endogenously. Indeed, we naturally assume that the reservation value of each agent equals his maximum objective value in case he decides to trade directly in the market. The latter value depends on the equilibrium strategies of other agents, which in turn depend on the contract chosen by the broker. The third distinctive feature of the present work is that, unlike the classical optimal contract problems, the broker is not constrained to offer a contract to every agent and choses her portfolio of clients strategically. In particular, one of our main questions is to determine the optimal portfolio of clients for the broker.

To the best of our knowledge, to date there exist no results on the optimal brokerage fees in the presence of price impact and multiple agents. The recent paper [2] studies a related problem in which a single agent hires a financial intermediary to trade a risky asset on his behalf, and pays a fee (chosen by the agent) for this service. This is also related to earlier literature on delegated portfolio management: see, e.g., [14], [15], [12], [4], [3], [6], [11]. Despite obvious similarities, the important conceptual differences between the latter works and the present one are that, herein, (i) the fee is designed by the broker, (ii) multiple agents are present, and (iii) ex ante the trading strategy is determined by the client as opposed to the broker, who nevertheless does observe the strategy.

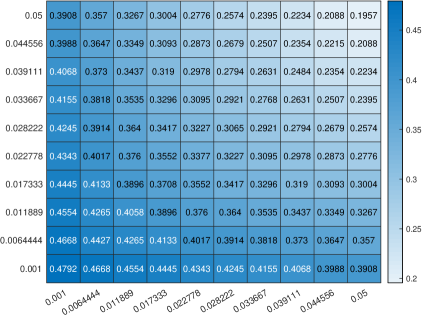

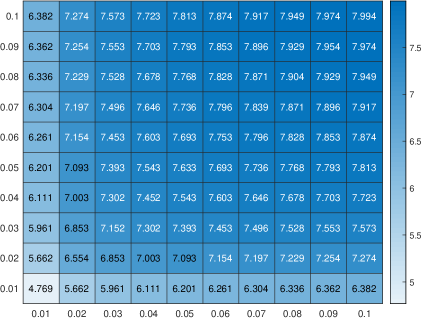

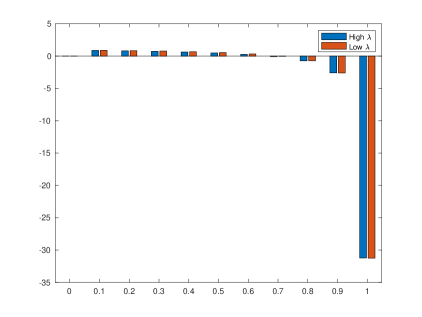

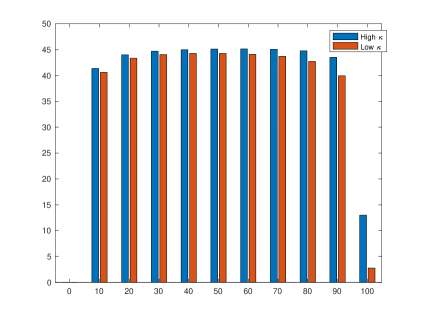

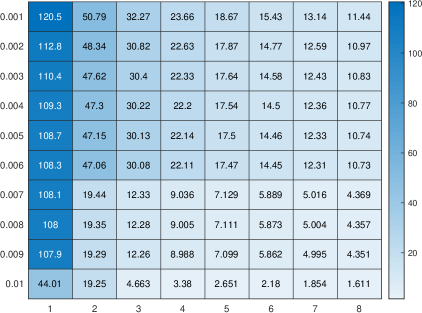

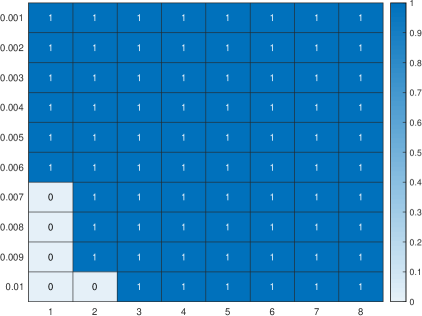

The rest of the paper is organized as follows. Section 2 introduces the model and the main objectives. Section 3 constructs optimal contracts (Proposition 1) given (arbitrary) reservation values of the agents and broker’s (arbitrary) choice of clients. Section 4 describes the unique equilibrium among those agents who are not offered a contract (i.e., among independent agents). Section 5 defines the reservation values of the agents endogenously (Definition 2) and shows how to compute the maximum objective value of the broker given an arbitrary portfolio of clients (Theorem 1). The latter result allows one to find an optimal portfolio of clients for the broker by solving a digital optimization problem. Section 6 considers several numerical experiments, where the aforementioned digital optimization problem is solved by exhaustive search and the broker’s optimal portfolio of clients, as well as the profits of the broker and of the agents, are analyzed as functions of the price impact parameters.

2 The setup

We consider agents, each of whom can trade a single risky asset that follows the Almgren-Chriss model over the time interval . In addition to the agents, we assume the presence of a single broker. Each agent makes a decision (once, before the trading starts) on whether he trades the asset directly or via the broker, and these decisions are represented by the vector : if and only if the -th agent trades via the broker. For convenience, we also denote by , , the indices of the agents that trade via broker. We refer to the agents who trade via the broker as clients and to those who trade directly in the market as independent. The trading activity of an independent agent affects the price of the asset via the impact coefficients of this agent. The trading of a client is done via the broker and hence affects the price of the asset via the impact coefficients of the broker. Of course, the broker may be able to offer lower price impact to her clients, but she also charges each of them a fee for this service. Even though we introduced as a vector of agents’ decisions, it is important to realize that these decisions are ultimately controlled by the broker, who decides whether to offer a contract to a particular agent or not (the acceptance of each offered contract is ensured by matching the reservation value of the associated agent). Therefore, in the remainder of the paper, we refer to as the choice of clients made by the broker.

We fix a probability space and consider a standard Brownian motion on this space. Let be the filtration generated by the Brownian motion . We define the set of admissible controls of a single agent as

|

|

|

(1) |

The (controlled) inventory of agent , who uses a control , is given by the process

|

|

|

Next, we recall the price process for the traded asset in the Almgren-Chriss model:

|

|

|

(2) |

where , are the coefficients of temporary and permanent price impacts of the agents, , are the corresponding coefficients of the broker, is the volatility of the asset price, and is its drift (i.e., trading signal). For convenience, we assume that for all , so that the temporary impacts of the agents do not affect the terminal price.

Let be the fees that the broker charges to her clients.

We assume that the fees are of the form , with measurable , where is the Sobolev space of order one, equipped with the natural norm. A client aims to maximize his expected profit:

|

|

|

(3) |

where denotes the trading rate of the rest of agents.

Similarly, an independent agent maximizes his expected profit:

|

|

|

(4) |

For a given combination of the strategies of other agents, we define the control problem of a client and of an independent agent , respectively, as:

|

|

|

(5) |

|

|

|

(6) |

Definition 1.

Given a choice of clients , as well as the associated indices and fees , we define as the set of all agents’ strategies that form Nash equilibria in the game defined by (5)–(6). Namely, if and only if the following two conditions hold:

|

|

|

(7) |

|

|

|

(8) |

The objective of the broker is given by the sum of expected fees in the best equilibrium attainable with these fees:

|

|

|

(9) |

In the above, we make the standard assumption that, given a set of admissible contracts, the agents will choose an equilibrium that is best for the principal among all attainable equilibria.

To ensure that and that the agents’ reservation values are met, we introduce the set of admissible fees of the broker:

|

|

|

(10) |

where is the reservation value of agent .

Thus, we obtain the following “local” maximization problem for the broker, given a choice of clients :

|

|

|

(11) |

The optimal contract that attains the above supremum is constructed in Section 3.

Note that, in the present setting we do not assume that is given endogenously, because there is in fact a very natural endogenous definition of the reservation value of each agent. However, as the above optimal contract problem is of first-best type, with risk-neutral preferences, the value of is not important for the form of the optimal contract we design in Section 3. Therefore, in order to ease the notation, we postpone the definition of to Section 5.

Note that the “global” optimization problem of the broker is to find an optimal and respective optimal fees , which amounts to solving

|

|

|

(12) |

The above is a discrete optimization problem. We do not provide a complete solution to this problem herein, assuming instead that it can be solved by an exhaustive search in case of a reasonably small or of a smaller subset of admissible (see Section 6). However, even to perform such an exhaustive search, one needs to have a numerically tractable representation of the value of for each . The latter representation is the main subject of Sections 4,5.

4 Equilibrium strategies of independent agents

Proposition 1 shows that, for any given , there exists a trivial choice of optimal contracts. This provides a solution to the broker’s local problem (11). Nevertheless, to find the optimal choice of that solves the global problem (12), we need to compute the value function for each . This, in turn, requires the knowledge of the equilibrium strategies of the agents that correspond to the fees constructed in Proposition 1, as well as the value of the broker in this Stackelberg game. The former is discussed in this section, and the latter is analyzed in Section 5.

The results of this section hold for an arbitrary fixed . However, for convenience, we assume that with some .

Notice that, with the fees given by (13), the objectives of the broker’s clients do not depend on their actions nor on the actions of the independent agents. Hence, any equilibrium in the sub-game among the independent agents can trivially be extended to an equilibrium among all agents. This observation is made precise in Theorem 1, and it is only brought up here to explain why it suffices to focus on the equilibria among independent agents, which is the main subject of the remainder of this section.

We begin by noticing that the objective (4) of an independent agent, by design, is only affected by the actions of the broker and of her clients through the total order flow of the broker’s clients, denoted

|

|

|

We refer to as the broker’s order flow.

In particular, for the fees constructed in Proposition 1, the objective (4) of an independent agent can be rewritten as

|

|

|

|

|

|

|

|

|

(16) |

where denotes the vector without the th element and .

The main goal of this section is to characterize all Nash equilibria among independent agents who solve

|

|

|

(17) |

for any given order flow of the broker .

Proposition 2.

For any , there exists a unique Nash equilibrium of (17), and it is given by

|

|

|

(18) |

where is the unique solution of the BSDE:

|

|

|

(19) |

and

|

|

|

Let us fix arbitrary , , , and describe an optimal strategy for the agent . Recall that the agent maximizes the right hand side of (16). We introduce his Hamiltonian:

|

|

|

Next, we observe that is concave in . Applying the stochastic maximum principle for the i-th agent’s problem (see, e.g., Theorem 6.4.6 in [13]), we conclude that the strategy defined by

|

|

|

(20) |

is optimal.

Moreover, as the objective of the agent is strictly concave, we conclude that (20) defines his unique optimal strategy, given .

Applying the same argument for every agent , we deduce that any solution of the system (20), for , defines a Nash equilibrium among the independent agents. By the strict concavity of the individual objectives we obtain that any Nash equilibrium is a solution to (20).

Summing up the first equation in (20) over , we obtain

|

|

|

(21) |

and, in turn,

|

|

|

Plugging the above in the second equation in (20), we obtain (19).

Thus, we have shown that any Nash equilibrium among the independent agents satisfies (18)–(19). It remains to notice that (19) is a standard linear BSDE, and its solution is unique. The latter, in particular, yields uniqueness of the solution to (20) and hence the uniqueness of equilibrium.

An immediate corollary of Proposition 2 is that, with and with the fees given by (13), the set of all equilibria among the agents (see Definition 1) is given by

|

|

|

where are given by (18).

5 Optimization problem of the broker

As in the previous section, the results of this section hold for an arbitrary fixed , but, for convenience, we assume that with some .

Herein, we turn to the control problem of the broker. Notice that, with the fees given by (13) and with the strategies of broker’s clients denoted by , the independent agents will necessarily adapt the strategies , given by (18) with , and the payoff of the broker can be written as

|

|

|

(22) |

|

|

|

where

|

|

|

This implies that the value of the broker’s objective (9), for the fees given by (13), can be written as

|

|

|

(23) |

where

|

|

|

Next, we use (18) to deduce

|

|

|

|

|

|

|

|

|

which leads to

|

|

|

|

|

|

where

is the unique solution to the linear BSDE (19).

Let us resolve the optimization over in (23), for each fixed and . Indeed, the latter amounts to solving the quadratic minimization problem with linear constraints:

|

|

|

|

|

|

where we recall that is known given . Constructing the Lagrangian and setting its derivatives to zero, we deduce that the above infimum equals

|

|

|

Thus, the broker’s objective for a fixed choice of clients can be written as

|

|

|

(24) |

where

|

|

|

|

|

|

(25) |

Let us denote .

The above expression can be viewed as a backward representation of as it involves that solved a BSDE.

The following lemma establishes a convenient forward representation for , which is used in the subsequent analysis.

Lemma 1.

For any , we have

|

|

|

(26) |

where , are defined by

|

|

|

(27) |

|

|

|

(28) |

and

|

|

|

(29) |

Integrating by parts and recalling (19), we obtain:

|

|

|

|

|

|

|

|

|

Plugging the above into the right hand side of (25), we obtain:

|

|

|

|

|

|

|

|

|

(30) |

Next, we recall that the linear BSDE (19) has a semi-explicit solution:

|

|

|

(31) |

Plugging the above expression into (30) and recalling the definition of in (29), we obtain

|

|

|

|

|

|

|

|

|

|

|

|

Using Fubini’s theorem and the tower property, we remove the conditional expectations in the right hand side of the above.

Finally, noticing that

|

|

|

and recalling the definition of (in (29)), we obtain the statement of the lemma.

Next, we introduce our main assumption.

Assumption 1.

The parameters are such that

|

|

|

(32) |

where is the 2-norm of a matrix, denotes the Euclidean norm in , and we recall

|

|

|

|

|

|

When verifying the above assumption, it is convenient to recall that , where

|

|

|

The next proposition shows that the broker’s optimization problem (24) is well-posed under Assumption 1.

Proposition 3.

Under Assumption 1, there exists a unique maximizer of over . Moreover, the optimal strategy is deterministic.

Using Lemma 1, we deduce that , where

|

|

|

Next, we observe:

|

|

|

(33) |

where we used Jensen’s inequality:

|

|

|

The above inequality also yields

|

|

|

Collecting the above, we conclude that

|

|

|

where .

Notice that the second and the third lines in the right hand side of the above display are linear in . In addition, Assumption 1 yields that the coefficient in front of is strictly negative, which implies that the above expression is strictly concave as a function of , where we introduced the set of deterministic strategies . As is linear-quadratic in , we conclude that it is also strictly concave (this can deduced easily by contradiction), which yields the statement of the proposition.

The above lemma shows that there is no loss of optimality in reducing the optimization problem (24) of the broker to the deterministic set of strategies . As the objective is linear-quadratic, we can find its maximizer by setting to zero its derivative.

Lemma 2.

The mapping is Fréchet-differentiable w.r.t. the -norm on , and its derivative is given by the following linear functional of :

|

|

|

|

where

is the unique solution of the (non-coupled) system of ODE:

|

|

|

(34) |

where , and are defined in (27)–(28).

For any we define , and we introduce defined as the unique solution of the ODE:

|

|

|

(35) |

where . Recall (35) can be written as

|

|

|

(36) |

Let . Then,

|

|

|

It is a standard exercise to check that the linear part (in ) of the right hand side of the above gives the desired Fréchet derivative:

|

|

|

(37) |

Next, we rewrite in a more convenient way. To this end, we observe:

|

|

|

Using the above, we deduce:

|

|

|

(38) |

Recalling (34), we obtain the statement of the lemma.

The above lemma allows us to characterize the optimal order flow of the broker in terms of the unique solution of a linear forward-backward system of ODEs, arising as a combination of (34) and

|

|

|

(39) |

Proposition 4.

Under Assumption 1, there exists a unique classical solution to (34), (39), and the optimal order flow of the broker is equal to .

By Proposition 3, we know that there exits a unique optimal control . Then, Lemma 2 implies that satisfies the second line of (39) for a.e. , with defined via (34) and the first line of (39). Noticing that are continuous, we conclude that is continuously differentiable and that it satisfies the second line of (39) for all . Finally, for any solution to (34), (39), the Frechet derivative of at is zero, which implies that and in turn that .

The following theorem summarizes all the results we have established.

Theorem 1.

For any and any , the set of fees given by (13) is optimal for the broker’s local optimization problem (11). Provided the broker chooses this set of fees, the following holds.

-

•

Any choice of equilibrium strategies that is optimal for the broker has the following structure: the strategies of independent agents, , are determined uniquely by (18)–(19), and the clients’ strategies can be chosen arbitrarily subject to

|

|

|

where is defined in Proposition 4.

-

•

The broker’s value for a given , defined in (11), satisfies

|

|

|

(40) |

where is given by (13), is defined in (25), and is defined in Proposition 4.

-

•

In any equilibrium , the value of the optimization problem (6) of each independent agent is given by the right hand side of (16), with replaced by .

In addition, is the same for any choice of that is optimal for the broker.

Let us now propose an endogenous definition of the clients’ reservation values.

Notice that these reservation values are needed in order to determine the broker’s value (via (40) and (25))

The latter, in turn, is needed to determine which is optimal.

Definition 2.

For every and every we define

|

|

|

(41) |

where all entries of are equal to those of , except for the -th entry which is equal to zero, and is given by the right hand side of (16), with replaced by and with a choice of equilibrium strategies that is optimal for the broker (see Theorem 1 and note that ).

Note that the above definition is consistent, in the sense that the right hand side of (41) does not depend on . Indeed, the right hand side of (16) depends only on and . In any equilibrium that is optimal for the broker, the latter quantities are determined uniquely by (18)–(19) and by Proposition 4, and they do not depend on .

The motivation for the above definition of a reservation value is clear. Namely, each client of the broker has an opportunity to trade directly in the market (i.e., to become an independent agent), hence, the reservation value of the client must equal the maximum objective value he can achieve by such trading.

The above definition and Theorem 1 give us a method for computing , for each . Then, an optimal can be found by maximizing . The latter is accomplished by an exhaustive search, in the next section, which is realistic for small or if the choices of are restricted to a small enough subset of .