Partially Linear Models under Data Combination††thanks: We thank the Editor, Francesca Molinari, three anonymous referees, Federico Bugni, Nathael Gozlan, Jinyong Hahn, Jim Heckman, Matt Masten, David Pacini, Adam Rosen, Andres Santos, Jörg Stoye, Martin Weidner, Daniel Wilhelm, Joachim Winter and conference and seminar participants at Aarhus, Duke, Munich, Oxford, Séminaire Palaisien, Tilburg, UCLA, the 2021 European Winter Meeting of the Econometric Society, the 2021 Bristol Econometric Study Group, the 2023 IAAE Annual Conference, Econometrics and Optimal Transport Workshop, and the Monash/Princeton/SJTU/SMU Econometrics Conference for useful comments and suggestions. We also thank Hongchang Guo, Zhangchi Ma and Frank Yan for capable research assistance.

Abstract

We study partially linear models when the outcome of interest and some of the covariates are observed in two different datasets that cannot be linked. This type of data combination problem arises very frequently in empirical microeconomics. Using recent tools from optimal transport theory, we derive a constructive characterization of the sharp identified set. We then build on this result and develop a novel inference method that exploits the specific geometric properties of the identified set. Our method exhibits good performances in finite samples, while remaining very tractable. We apply our approach to study intergenerational income mobility over the period 1850-1930 in the United States. Our method allows us to relax the exclusion restrictions used in earlier work, while delivering confidence regions that are informative.

Keywords: Partially Linear Model; Data combination; Partial Identification; Intergenerational Mobility.

1 Introduction

In this paper, we derive partial identification and inference results for a partially linear model, in a context where the outcome of interest and some of the covariates are observed in two different datasets that cannot be merged. Relevant situations include cases where the researcher is interested in the effect of a particular variable that is not observed jointly with the outcome variable, as well as cases where the outcome and covariates of interest are jointly observed but some of the potential confounders are observed in a different dataset.

Our analysis focuses on a partially linear model of the following form:

| (1) |

in a data combination environment where and are supposed to be identified, but the joint distribution is not. The variable is thus common to both datasets, whereas the variable is only observed in one of the two datasets. In this setup, is generally not point-identified, and as a result we focus on the identified set of either or for some ; the identified set of can then be deduced from that of .

We first derive a tractable characterization of the identified set of . Unlike many other models considered in the partial identification literature, our setup does not deliver a tractable characterization of the identified set through the support function (see Bontemps and Magnac, 2017; Molinari, 2020, for detailed discussions of support functions). However, using Strassen’s theorem (Strassen, 1965), a recent result in optimal transport by Backhoff-Veraguas et al. (2019), and a convenient characterization of second-order stochastic dominance, we show that this set is convex, compact, includes the origin and can be simply constructed from its radial function.111The radial function of a closed, compact convex set including the origin is defined, for any on the unit sphere, by . The identified set of , then, can also be computed at low computational cost by solving an unconstrained convex minimization problem.

The characterization of the identified set also implies that point identification may be achieved if , or under a restriction on the unobserved term . While the latter condition is not directly testable, we show how to assess its plausibility when one has access to a validation sample in which the outcome and covariates are jointly observed.

In the partially identified case, the identification region may be reduced by adding restrictions on . The two-sample two-stage least squares estimator (TSTSLS) relies on the assumption for some and . In this context, (resp. ) corresponds to the excluded (resp. included) instruments. This is a leading example that results in point identification. But the exclusion restriction that does not depend on may not be credible. We show that alternative restrictions, such as imposing a lower bound on the of the “long regression” of on and (in a similar spirit as Oster, 2019) or shape restrictions such as monotonicity or convexity of , may in practice dramatically reduce the identified set, and allow to, e.g., identify the sign of .

Our identification result is constructive, and readily leads to a simple, plug-in estimator of the identified sets for or . A difficulty arises, however, as the estimator of the radial function is generally not asymptotically normal. To construct asymptotically valid confidence regions on or confidence intervals on , we propose to use subsampling (Politis et al., 1999).

Our method is based on a specific characterization of the identified set, and one may wonder whether alternative characterizations would be more convenient. In particular, the identified set can also be expressed through an infinite collection of moment inequalities. Therefore, general approaches for such problems such as that developed by Andrews and Shi (2017) could in principle be used instead. We show through simulations the key computational advantage of relying on the method we propose. With a univariate , confidence regions are typically computed in seconds, whereas they take up to 30 seconds with a bivariate . Compared to the method of Andrews and Shi (2017), this corresponds to a dramatic reduction by a factor of more than 1,000 in computational time.

We apply our method to study intergenerational income mobility over the period 1850 to 1930 in the United States, revisiting the analysis of Olivetti and Paserman (2015). In this context where the main variable and outcome of interest are observed in two different datasets that cannot be linked, we show that the confidence sets obtained using our method are quite informative in practice, while allowing us to relax the exclusion restrictions underlying the TSTSLS approach used in Olivetti and Paserman (2015). In the appendix, we consider another application where a key control variable is observed in a separate database. When incorporating sign constraints, our bounds are again very informative.

Related literatures

The method we develop in this paper can be used in a broad set of data combination environments. Two such contexts have attracted much attention in the empirical literature.

One can use our method to conduct inference on the relationship between a particular covariate and an outcome variable, in situations where both variables are not jointly observed. A large literature on intergenerational income mobility often faces the unavailability of linked income data across generations and relies on exclusion restrictions, as in the application we revisit (see Santavirta and Stuhler, 2022, for a recent survey). Data combination issues are also common in consumption research, where income (or wealth) and consumption are often measured in two different datasets (Crossley et al., 2022). More generally, this type of data combination environment frequently arises in various subfields of empirical microeconomics, including in education and returns to skill estimation (Rothstein and Wozny, 2013; Piatek and Pinger, 2016; Garcia et al., 2020; Hanushek et al., 2021), health (Manski, 2018; Robbins et al., 2022) and labor (Athey et al., 2020). A leading example that has attracted much interest in the literature is one where the researcher seeks to combine experimental data with another observational dataset, in particular situations where data on long-term outcomes is not available in the experimental data.

Our approach can also be used to conduct inference on the causal effect of a variable of interest, in a setup where some of the confounders are observed in an auxiliary dataset. As such, our paper expands the range of data environments in which unconfoundedness is a credible assumption, complementing a literature that focuses on evaluating its reasonableness in the absence of data combination (see, e.g., Altonji et al., 2005; Oster, 2019; Diegert et al., 2022).

From a methodological standpoint, our paper is connected to the seminal article of Cross and Manski (2002) and subsequent work by Molinari and Peski (2006). They consider the issue of identifying the “long regression”, in our context , in the same data combination set-up as here. Importantly though, these two papers focus on deriving the identification region for , but do not address the issue of inference. They also consider a setup where the covariates have a discrete distribution with finite support, while we allow to be continuously distributed. On the other hand their setup is entirely nonparametric, whereas we focus on a model that is linear in the covariates and without interaction terms with . The linearity assumption plays an important role in our ability to derive a tractable inference method. The absence of interaction further implies that in our set-up, and in contrast with these two papers, the identified set shrinks as one considers different values of .

Our paper is also related to Pacini (2019) and Hwang (2022). Both papers construct bounds on the best linear predictor of on in a similar data combination framework as here. We show that if one is ready to impose the usual assumption that the model is partially linear, large identification gains may be achieved, possibly up to point identification. Hwang (2022) also considers a set-up where some of the ’s are only observed with but not with , a case we do not study in this paper.

More generally speaking, our paper relates to the broader literature on data combination problems in econometrics and statistics. We refer the reader to Ridder and Moffitt (2007) for a survey of this literature and to Fan et al. (2014), Fan et al. (2016), Buchinsky et al. (2022), and Athey et al. (2020) for recent contributions. Contrary to ours, most of these papers impose restrictions that entail point identification.

Within the data combination literature, our paper is technically closest to D’Haultfoeuille et al. (2021). Though that paper considered the entirely different context of rational expectation testing, we also relied therein on Strassen’s theorem to obtain a characterization of the null hypothesis of rational expectations. Importantly, we extend here our previous main result in a highly non-trivial way, by relying in particular on Backhoff-Veraguas et al. (2019) to handle multivariate . Also, we previously based our inference on Andrews and Shi (2017). In contrast, a key contribution of our paper lies in the novel and tractable inference method that we derive.

Finally, by developing in this data combination context a feasible inference method that can be implemented at a very limited computational cost, our paper also adds to the growing set of papers that propose tractable computational methods for partially identified models (see Bontemps and Magnac, 2017 and Molinari, 2020 for recent surveys). In particular, our paper fits into the strand of the literature that uses tools from optimal transport to devise computationally tractable identification and inference methods for partially identified models (Galichon and Henry, 2011; Galichon, 2016). By characterizing the sharp identified set based on the radial function, a novel approach in the partial identification literature, we show that it is possible to achieve very substantial tractability gains in this context, relative to a more standard characterization in terms of many moment inequalities.

Organization of the paper

The remainder of the paper is organized as follows. In Section 2 we present our main identification results for the two-sample partially linear model described above. Section 3 studies estimation and inference for this model. In Section 4, we apply our method to intergenerational income mobility in the United States. Section 5 concludes. The Appendix of the paper gathers additional results on robustness to measurement errors, identification in models with heterogeneous effects of on , and a test for point-identification. It also presents our second application to the black-white wage gap in the United States. Monte Carlo simulation results, additional material on the application, and the proofs are collected in the online Appendix. Some complements of the proofs appear in supplementary material available in our working paper version (see D’Haultfœuille et al., 2023). Finally, our inference method can be implemented using our companion R package, RegCombin, available at CRAN.R-project.org/package=RegCombin.

2 Identification

Before presenting our main identification results, we introduce some notation that will be used throughout the paper. We let , and denote respectively the usual Euclidean norm in , the vector and the unit sphere in ; we may omit the index in the absence of ambiguity. For any cumulative distribution function (cdf) defined on , we let denote its generalized inverse and be the corresponding survival function. For any random variable , we let be its support, denote its cdf. and its variance, if defined. We also let denote the convex ordering, namely, for two random variables and with and , if for all convex functions .222Even though we may have , is always well-defined because , since there exists such that for all , . We write when does not hold. Finally, for any sets and , we denote by the boundary of and by the Hausdorff distance between and , defined by

2.1 Identification without common regressors

2.1.1 A tractable characterization of the identified set

We first consider a linear model and derive the sharp identified set of in the absence of common regressors observed in both datasets. We suppose that we observe from two samples that can not be merged the distributions of the outcome, , and covariates, . We maintain the following assumption:

Assumption 1.

We have , , and is non-singular. Moreover, for some .

We focus hereafter on the identified set of . Since is the set of all vectors in that are compatible with the model and the marginal distributions of and , we have

| (2) |

where, for any random variable with , we let and we have used that for some is equivalent to . Now, our goal is to express to make it amenable to (simple) estimation. To this end, we define, for any , and cdfs with expectation 0, the following functions:

| (3) | ||||

These two functions play an important role in our analysis. Remark that, since and are cdfs of mean zero distributions, and are both positive, so that the ratio of superquantiles is well-defined, with and . Theorem 1 is our main identification result.

Theorem 1.

We now give a sketch of the proof of (4). Let denote the set on the right-hand side of (4). First, one can show that by definition of ,

This, in turn, is equivalent to dominating at the second order (see, e.g. De la Cal and Cárcamo, 2006), implying that

The inclusion then follows essentially from Jensen’s inequality. As a side remark, note that we can also express through infinitely many moment inequality restrictions:

| (5) |

This equality directly follows from Fubini-Tonelli, applied to the standard characterization of the second-order stochastic dominance condition, namely . We return to this alternative characterization of the identified set in Subsections C.1 and C.4 of the online appendix, where we document the computational advantages of using our characterization instead.

The inclusion is more intricate to prove. Assume . By what precedes, . Then, by Strassen’s theorem (Theorem 8 in Strassen, 1965),

| (6) |

This result was already used in D’Haultfoeuille et al. (2021) to characterize the restrictions on and entailed by the rational expectation hypothesis , where denotes the subjective expectations on an outcome . Importantly though, when is multivariate, (6) is not sufficient to conclude that , as the -algebras generated by and are not equal in general. Nonetheless, we prove, using in particular Theorem 1.3 in Backhoff-Veraguas et al. (2019), that for ,333We thank Nathael Gozlan for his help in obtaining (7).

| (7) |

Together, (6), (7), and the existence of a minimizer on the left-hand side of (7) (Theorem 1.2 in Backhoff-Veraguas et al., 2019), imply that we can find random variables and such that , and . Thus, .

Turning to the second part of the theorem, follows by noting that one can always rationalize, from the sole knowledge of their marginal distributions, that and are independent. That comes from the inclusion , combined with the fact that implies . Hence, is included in a bounded ellipsoid. The equality occurs for instance when and are normally distributed. Otherwise, may be substantially smaller than , as we illustrate below. In such cases, remains a natural benchmark as it is very simple to characterize using and only, and straightforward to estimate.

Remark 2.1.

Using the exact same reasoning as above, one can prove that without any linear restriction on the conditional expectation, the identified set for is . Similarly, if we only impose that belongs to a linear space of functions, then the identified set for is .444We thank a referee for pointing out this extension.

Radial vs. support function characterization of the identified set.

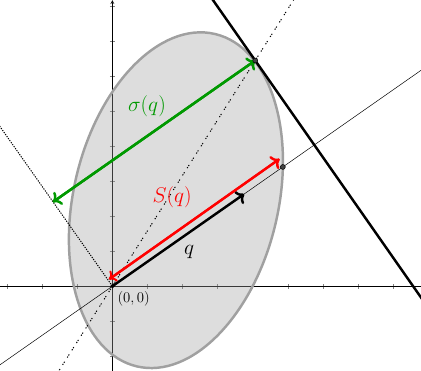

A key takeaway from Equation (4) is that the identified set admits a very simple expression as a function of , which is the inverse of the Minkowski gauge function of (see, e.g., Definition 1.2.4 p.137 and Proposition 3.2.4 p.157 Hiriart-Urruty and Lemaréchal, 2012), also known as the radial function of . This function differs from the support function of , defined by . The difference between these two functions is illustrated in Figure 1.

The partial identification literature has largely relied on support functions, as these are powerful tools that uniquely characterize their convex sets. But the radial function also uniquely characterizes convex sets if, as is the case here, these sets include the origin.555More generally, star-shaped sets are fully characterized by the radial function (and a given point, in our setup). See Molchanov (2017), p.156, for more details on this point. Importantly, this approach allows us to characterize the sharp identified set by minimizing a simple function over the interval . In contrast, the support function approach will generally be significantly less tractable in our context as it would require solving a high-dimensional constrained optimization problem. Namely, using the characterization of the identified set given in Equation (5) above, the support function can be obtained by solving the following program:

| (8) |

where the constraint itself involves an optimization problem. Simulation results indicate that using the radial function rather than the support function approach does result in very large computational gains, see Online Appendix C.4 for details on this.

Partial identification of subcomponents of .

The support function still plays a key role in our context when one is interested in a component of , say . The following result shows that we can actually recover this function at a low computational cost once is known. Hereafter, we let denotes the -th element of the canonical basis in and use the convention and .

Corollary 1.

Suppose that Assumption 1 holds. Then, the identified set of satisfies . Moreover,

| (9) |

The same holds with , after replacing by .

We use the expression (9) of the support function, rather than the simpler expression , because is convex (see the proof of Proposition 6, which also applies when ), whereas may not be concave. It follows that one can recover the support function , and in turn the sharp bounds on , by simply minimizing a convex function over .

2.1.2 Point identification

In some cases, our approach yields point identification of the parameters of interest, or subcomponents of it. Proposition 1 below presents two such cases under which the identified sets and , respectively, boil down to a singleton.

Proposition 1.

Suppose that Assumption 1 holds and let be a convex function such that . Then:

-

1.

If for all , , then .

-

2.

If for all and for all , then .

Recall from our main identification result above that the identified set always includes the origin. The first point of Proposition 1 further establishes point identification of when, basically, has lighter tails than any linear index of . The second point is similar but focuses on a subcomponent instead: if and have lighter tails than , then is point identified. As an example of function for which Proposition 1 holds, one might consider for instance for some (in which case or have heavy tails), or for some (in which case or have exponential tails).

To illustrate Point 1 of Proposition 1, suppose that , follows a Laplace distribution (with density on ) and . Then, by using , it follows from Point 1 of Proposition 1 that is point identified in this case. On the other hand, the variance restrictions only set identify , with an identified set given by . This example illustrates the (in this case point-) identifying power of higher-order moments of the distributions of and .

2.2 Identification with common regressors

We now turn to the frequent situation where some regressors are observed in both datasets. Namely, suppose we observe regressors that are common to both datasets, and assume that the partially linear model (1) holds:

The key here is to note, following Robinson (1988), that this case is equivalent to the previous setup without common regressors once we compute the following residuals, for all in the support of :

It directly follows that satisfies , which allows us to use the characterization of the identified set without common regressors obtained in Section 2.1.

Let and denote the identified sets of and , respectively. We have the following characterization of and :

Proposition 2.

Suppose that , for all , is nonsingular and (1) holds. Then:

where . includes , is compact and convex.

It is possible to extend (1) by including interaction terms. Notably, such specification allows for heterogeneous effects of on , which can be important in practice (see, e.g., Hausman, 2016, pp.1110-1111). We consider this extension in Appendix A.2. Another interesting extension corresponds to cases where and we observe in a first dataset and in a second dataset, . This setup leads to qualitatively different results. For instance, if there is no common regressors and and are Gaussian, one can show that the sharp identified set of is not convex and does not include (with the dimension of ). We refer the reader to Hwang (2022) for outer bounds on the best linear predictor in this setup and leave its study for future research.

2.3 Identifying power of additional restrictions

We now consider additional restrictions that may reduce the identified set, in some cases resulting in point identification of the parameters of interest.

2.3.1 Lower bound on the of the long regression

A first way to reduce the identified set is to use a lower bound on the predictive power of and with respect to . To formalize this idea, we assume that , the coefficient of determination of the “long” regression of on and is higher than a certain threshold. This threshold may be absolute (e.g., 0.1) or relative to , the of the “short” regression of on , which is directly identified from the data. This is in the same spirit as Oster (2019), who suggests fixing to 1.3. Note that

and the two components on the right-hand side are uncorrelated. Thus,

Then, if one imposes a lower bound on such that , the identified set on becomes

provided that is nonsingular. This restriction has three key attractive features. First, one can in practice motivate this restriction based on a “validation sample”, namely a subset of the population or another population (e.g., a different country than that under investigation), for which we identify the joint distribution of the outcome and covariates, and thus the of the “long” regression. Second, imposing a lower bound such that allows one to exclude from the identified set. Third, the identified set still admits a very simple expression.

2.3.2 Linear shape restrictions

Another way to narrow the identified set with common regressors is to impose some constraints on . Shape restrictions such as monotonicity or convexity often follow from economic theory; see Matzkin (1994) and Chetverikov et al. (2018) for econometric reviews, and Tripathi (2000) and Abrevaya and Jiang (2005) for their use and testability with partially linear models. We characterize here the identified set when we impose such restrictions on .

We model these restrictions by for all , with a known linear operator, a known, real function and the domain of and . For instance, if is discrete such that , with and , considering for (resp. for with ) and corresponds to imposing that is non-decreasing (resp. convex). When is continuous, the same two constraints can be imposed by considering and , with .

This framework also accommodates restrictions on the magnitude of the effect of on . Namely, suppose for simplicity that is binary and consider with and . The extreme case corresponds to having no effect on , as in the two-sample two-stage least squares strategy (see the next subsection for a related, more general point identification result in this context). More generally, this corresponds to the constraint that the magnitude of the effect of is bounded by the cutoff , .666If has points of support, the same idea can be generalized by imposing restrictions on for specific pairs , . By increasing , one can therefore study how the identified set varies when relaxing the exclusion restriction, in a similar spirit to, e.g., Masten and Poirier (2018).

Hereafter, we denote by , and

where we let and we note that the two functions above may be infinite. We introduce limits to deal with the cases where . Proposition 3 characterizes the identified sets of and under such shape restrictions.

Proposition 3.

Suppose that the conditions of Proposition 2 hold and for all . Then, the identified sets and of and satisfy

where and

is compact, convex but does not include if for some , .

In contrast to our baseline identification results in the absence of additional restrictions, the resulting identified set may exclude the origin. This illustrates the practical importance of imposing these types of shape restrictions in contexts where these are likely to hold. Suppose for instance that , is binary (), and , namely we impose that is non-decreasing. If , then . As a result, . The condition holds for instance if is decreasing and is positive and large enough.

Remark 2.2.

While we focus here on the identifying power of each type of restrictions considered separately, researchers may in some contexts want to jointly impose several of these restrictions and consider the intersection of the associated identified sets. In the particular cases of the shape restrictions and the restrictions on the considered above, the identified sets share the same structure. Thus, the identified set resulting from both types of constraints can be simply computed by replacing the lower bound on by the maximum of the lower bounds of the initial sets, and proceeding symmetrically for the upper bound.

2.3.3 Functional form restrictions involving common regressors

One may alternatively be willing to impose functional form restrictions on . The following proposition shows that this may yield point identification.

Proposition 4.

Suppose that , and belongs to a vector space . Then, if for all , , and are point identified.

This proposition encompasses several popular restrictions. We consider in particular three such restrictions, for which the key point-identifying condition has a simple interpretation:

-

1.

, with . This restriction, which is implicit in, and central to the two-sample two-stage least squares strategy, states that conditional on , is mean-independent of . In such a case, for all basically means that varies with . To see this, consider the simple case where , for some function and a matrix . Then, is equivalent to having rank , which is the usual rank condition in linear instrumental variable models.

-

2.

. Under this linearity restriction on , for all basically means that is nonlinear in (the two notions are actually equivalent if ). Note that this point identification result fully relies on the linearity of combined with the nonlinearity of , and is thus akin to, e.g., the identification of sample selection models without instruments exploiting the nonlinearity of the inverse Mill’s ratio. Also, this result does not apply when is binary, since in this case is necessarily linear in .

-

3.

, with . Under this additivity restriction on , for all means that is not additive in . If for instance with both binary, for all holds if in the regression of on and , the coefficient of is not zero.

2.3.4 Tail conditions

Finally, if one is ready to impose a relative tail condition between the error term and , the identified set is considerably reduced. For simplicity, we assume here that there are no common regressors but Proposition 5 readily extends to accomodate such regressors.

Proposition 5.

Suppose that Assumption 1 holds. Then:

-

1.

If there exists a convex function such that for all , the identified set of is included in ;

-

2.

, for all and it is known that , is point identified.

With , the condition for all holds for instance if for some . More generally, the condition basically imposes that has fatter tails than . In this sense, this condition is similar to those in Proposition 1 above.

Testability.

Note that we cannot test the condition for some convex function and all , simply because is not identified. On the other hand, we can assess the plausibility of using a validation sample, as defined above. Denoting by the variables corresponding to this validation sample, it becomes possible to test whether the corresponding parameter is at the boundary of the identified set one would get from the sole knowledge of and . Provided that , this condition is indeed equivalent to or, in simpler terms,

We consider a statistical test of this condition in Appendix A.3, and apply it in Section 4 below.

2.4 Numerical illustration

We illustrate the previous results by considering the following model:

We set the coefficients as follows: , , and . The variables are transformations of , which is supposed to follow a multivariate normal distribution with mean 0 and covariance matrix

Specifically, the common regressor is given by , , , , are respectively the quantiles of order 0.1, 0.37, 0.67 and 0.9 of the standard normal, and . We consider two cases for the regressors that are observed in one of the datasets only, . In the first case, and in the second, .

Figure 2 displays several identified sets for each of the two data-generating processes (DGPs) described above, each of them being associated with particular restrictions. Namely, the set in red, denoted by , is obtained from the variance restrictions only:

where and are defined as in Section 2.2. Hence, is the intersection of two ellipses. The set in green, , is obtained as in Proposition 2 and relies on the restrictions for . Finally, the set in blue, , is a subset of that imposes both convexity and monotonicity constraints on .

A couple of comments are in order. In case (a) the restrictions implied by the model are much more informative than the variance restrictions, because of the non-normality of , and in particular the fact that it has fatter tails than the residuals . The true point is at the boundary of , illustrating Proposition 1 applied conditional on and . In this case, the shape restrictions are sufficient to imply that but also to rule out that as well as . The identified set is reduced further in case (b), as a result of the fatter tails of both and . Like in case (a), the shape constraints on allow to reduce dramatically the identified set.

Figure 3 presents convexity constraints and different constraints on the on the first DGP. While unlike case (a) of Figure 2, convexity constraints alone fail to reject , imposing a constraint of the form with rejects it by definition. In the latter case, the identified set is no longer convex, allowing to exclude some directions from the identified set and providing an informative lower bound on . Overall, that the sharp identified sets are much more informative than the identified set based on the variance restrictions highlights the importance of using all of the restrictions implied by the model. Another takeaway from these numerical illustrations is that sign constraints can be very informative in practice, resulting in significant shrinkage of the identified set.

2.5 Regularization

An issue for estimation and inference on is that when or , is a ratio of two terms tending to 0. It follows that its plug-in estimator may become very unstable. To regularize the problem, we consider an outer set of based on the removal of extreme values of . We will focus on this outer set when we turn to estimation and inference in Section 3. Specifically, we define, for any ,

| (10) | ||||

Note that for all , is continuous on . Thus, the minimum in (10) is well-defined. Proposition 6 below describes some properties of and relates it to the sharp identified set .

Proposition 6.

Suppose that Assumption 1 holds. Then:

-

1.

For all , includes , is compact and convex;

-

2.

For all , and ;

-

3.

Suppose that is continuous and satisfies

(11) Then, there exists such that for all , .

The first part of Proposition 6 states that the regularized set , for all , preserves the compactness and convexity of the sharp identified set . The second part states that is always a superset of , which is arbitrarily close to as . The third part states that if, basically, the tails of are thinner than those of (Condition (11)), the set coincides with the sharp set for small enough. Condition (11) holds in particular if has a bounded support and , or if is symmetric and has a tail index larger than that of . Note that may hold even without (11). For instance, if both and are normally distributed, it is easy to check that for all .

On the other hand, when has thinner tails than , will be a strict superset of for large enough. In such cases, and under additional restrictions, we provide upper bounds on the Hausdorff distance between and in Proposition 7. Intuitively, these bounds inform us about the maximal possible loss, in terms of identification, that is due to regularization.

Proposition 7.

Suppose that Assumption 1 holds and let . Then:

-

1.

Assume that has an elliptical distribution with nonsingular variance matrix , a density with respect to the Lebesgue measure and for some . Suppose also that for some . Then, there exists such that for small enough,

-

2.

Assume that , and for some . Then, there exists such that for small enough,

The tail conditions imposed in Proposition 7 are basically the opposite as in Point 3 of Proposition 6, as they imply that has fatter tails than . The assumption that has an elliptical distribution in Point 1 allows us to relate , for any , with , but it is not necessary to obtain an upper bound on .

In the two cases of Proposition 7, we produce upper bounds on the Hausdorff distance between and that are, up to some constants, power of the regularization parameter . The upper bounds are close to 0 when is small, in line with Point 2 of Proposition 6. They are also closer to 0 the smaller is, i.e. the fatter the tails of (or ) are, or the larger is, i.e. the thinner the tails of are.

3 Inference

We now consider the estimation of the identified set, and how to conduct inference on the parameters of interest . As in the previous section, we first consider the case without common regressors before showing how to incorporate such regressors and combine them with additional constraints. We conclude this section by discussing some computational aspects of our procedure. We illustrate the finite sample performances of our inference method in Online Appendix C.

3.1 No common regressors

3.1.1 Estimation of the identification region and confidence region

We rely on random samples from the distributions of and .

Assumption 2.

We observe and , two independent samples of i.i.d. variables with the same distribution as and , respectively.

For any , let and denote the empirical cdf of and and let and . We simply estimate and by their empirical counterpart and . It turns out that these functions can be computed quickly, as detailed in Section 3.3 below. We then also simply estimate the identified set by plug-in:

Next, we build confidence regions on . The asymptotic distribution of is not Gaussian in general, so we rely on subsampling (Politis et al., 1999). One could alternatively use the numerical bootstrap, see the discussion pp. 18-19 in the first version of D’Haultfœuille et al. (2023).

Let and let denote the size of the subsample. For any estimator , let denotes its subsampling counterpart. For a nominal coverage of , the confidence region on we consider is given by

where is the quantile of order of the distribution of , conditional on the data.

Inference on subcomponents of .

In practice, one is often interested in conducting inference on subcomponents of . In view of (9), the identified (outer) set of corresponding to satisfies

| (12) |

where denotes the support function associated to and is the -th element of the canonical basis of . To construct confidence intervals on , we first estimate by

| (13) |

see Corollary 1. Then, denoting by the quantile of order of the distribution of , conditional on the data, the confidence interval we consider for is

where and . The rationale for using and is to ensure that : recall that without constraints, . The advantage, then, is that we can still use the quantiles of order while maintaining coverage even under point identification, as formally shown in Theorem 3 below.

Choice of the regularization parameter .

Because , the confidence regions and intervals above are conservative in general. To gain in efficiency, we suggest using several , and, basically, keep the one leading to the smallest confidence regions or intervals. We distinguish the cases , where we can adapt the choice to the direction while preserving the convexity of , from the case . When , let us define, for ,

| (14) |

where is a finite grid in . Hence, simply minimizes the boundary value of the confidence region in the direction . This idea is similar to that of Chernozhukov et al. (2013) in the context of intersection bounds.

Now consider the case . If one focuses on confidence intervals on , we need to choose the parameter that appears in . To this end, we simply use as given above, with . If we are interested instead in the set itself, we recommend using , where is a finite subset of .

3.1.2 Consistency and validity of the confidence region

The following theorem shows that is consistent for , in the sense of the Hausdorff distance, under mild regularity conditions.

Next, we establish the asymptotic validity of and , under Assumptions 3 and 4 respectively. Assumption 5 (resp. 6) is used to establish the asymptotic validity of (resp. ) using or (resp. ), as defined above, instead of a fixed .

Assumption 3.

(Regularity conditions for ) , . Also, for all , there exists such that and are continuous and strictly increasing on and respectively.

Assumption 4.

(Regularity conditions for ) , . Also, there exists such that for all , there exists a strictly increasing and continuous function such that and

| (15) | ||||

Finally, for all , either (i) , (ii) admits a unique maximizer on , or (iii) for all , admits a unique minimizer on .

Assumption 5.

(Regularity conditions for the validity of based on data-dependent ) For all , we either have (i) for all , or (ii) admits a unique minimizer on .

Assumption 6.

(Regularity conditions for the validity of based on data-dependent ) For all , we either have (i) for all or (ii) for all , admits a unique minimizer on , with and .

The second part of Assumption 3 holds if for all , the distributions of and are continuous with respect to the Lebesgue distribution and their support is a (possibly unbounded) interval. The first part of Assumption 4 is basically a reinforcement of Assumption 3 to ensure that some of our results hold uniformly over . This is needed when we consider the support function, as this function implies an optimization over . A sufficient condition for (15) is that, for all , admits a density with respect to the Lebesgue measure and . The conditions (ii) and (iii) in Assumption 4 are sufficient conditions for the continuity of the asymptotic distribution of , which is necessary for the validity of subsampling.

Assumption 5 can accomodate DGPs where the tails of are thinner than those of (which may correspond to admitting a unique minimum) but also DGPs for which the opposite holds (since in this case we can have for all and ). For instance, one can check that it holds if with , , and either follows a Laplace distribution while is uniform, or the other way around. But it fails to hold when both and are Gaussian, since then is actually constant. Assumption 6 is basically similar to Assumption 5 but somewhat more complicated, as we consider therein the support function instead of the radial function.

To prove (16)-(17), we first show the weak convergence of

seen as a process indexed by either or . The convergence in distribution of and , and in turn (16)-(17), then essentially follows by the Hadamard directional differentiability of the minimum and maximin maps, shown respectively by Cárcamo et al. (2020) and Firpo et al. (2023).

Our results for a fixed extend to the data-dependent and , under the additional conditions provided above. Note that one could avoid these conditions by using sample splitting, with one subsample used to choose or and the other to construct the confidence regions/intervals. One drawback of this alternative solution, though, is that it increases the size of confidence regions/intervals, to a point that we may lose the benefits of using a data-dependent rather than a fixed .

3.2 Common regressors and possible constraints

We now turn to inference on with common regressors . Recall from Proposition 2 that the identified set on is

with .

Let us first assume that has a finite support. Let and denote the empirical estimators of and , respectively. Following the same logic as above, we estimate by

Let be the quantile of order of the distribution of , conditional on the data. For a nominal coverage of , the confidence region on we consider is

With continuous common regressors, one can adapt the earlier arguments using sieve estimation. Specifically, suppose that Model (1) holds and consider a linear sieve approximation of by a step function for some partition of the support of and with tending to infinity at an appropriate rate. Then, one can construct a confidence region on by following a similar logic as above.777Establishing the asymptotic validity of such a confidence region would require to handle both the bias stemming from the approximation of and the increasing complexity of the approximation. We leave this analysis for future research.

We now discuss how to conduct inference under constraints on the or shape restrictions, as considered in Subsections 2.3.1 and 2.3.2 respectively. The main difference with above is that for a given direction , both the lower and upper bounds on the identified set need to be estimated. As before, we can estimate them with plug-in estimators. The only substantive difference is that in the confidence regions, we need to account for the variability of both bounds. For instance, with shape restrictions, we can consider the following confidence region:

where is the quantile of order of , conditional on the data and similarly for . We conjecture that with a finite number of constraints, finitely supported and if for all , is pointwise asymptotically conservative. Alternatively, one could use the formulation of our problem with shape constraints as a set of infinitely many moments inequalities. While generally far less tractable that our baseline approach, confidence intervals based on the inversion of the test of these many moment inequalities have uniformly correct asymptotic size (Andrews and Shi, 2017).

3.3 Computational aspects

We first discuss how to efficiently compute . Let represent the distinct, ordered values of the and let . Let us also define . We define similarly and . By construction, the numerator of is linear on all intervals (). Moreover, for any ,

| (18) |

The same holds for the denominator of . As a result, is of the form on intervals between two consecutive values of . Now, observe that the minimum of such a function is reached at one of the endpoints of the interval. As a result, we can compute using the following algorithm:

-

1.

Compute on using (18) and let . Proceed similarly with ;

-

2.

Interpolate linearly (resp. ) on (resp. ).

-

3.

Compute .

To compute , we solve (13), in which is also convex. In practice, we use the BFGS quasi-Newton method implemented in the R package optim, using as a starting point the considered direction .

Finally, the exact computation of and requires the computation of and for all , which is in practice infeasible if as is infinite. Instead, we suggest to (i) fix a grid ; (ii) compute and for each ; (iii) construct an approximation of and by computing the convex hulls of and , respectively.888The convex hull of points in can be computed efficiently by the quickhull algorithm (Barber et al., 1996), which requires around operations. The resulting sets, and say, are convex, inner approximations of and , and satisfy, as , and .

The computation of the estimated set, the confidence regions on and in the specification (where is the vector of all dummy variables associated with a finitely supported variable) and the confidence intervals on the corresponding subcomponents are implemented in our companion R package RegCombin. The package also handles shape restrictions and lower bound on the of the long regression, as well as combinations of these. The RegCombin vignette, available through the description of the package on CRAN, provides additional details about the implementation, including the choice of the tuning parameters and .

4 Application to intergenerational mobility in the United States

We now apply our method to conduct inference on the intergenerational income mobility over the period 1850 to 1930 in the United States, revisiting the influential analysis of Olivetti and Paserman (2015) on this question. We follow their paper and focus on the father-son and father-son-in-law intergenerational income elasticities. We conduct our analysis using 1 percent extracts from the decennial censuses of the United States, over the period 1850 to 1930 (1850-1930 IPUMS).999We refer the reader to Section 2 of Olivetti and Paserman (2015) for a detailed discussion of the data used in the analysis. Note that they estimate the evolution of the intergenerational income mobility over a longer time window (1850 to 1940) than we do. We confine our analysis to the period 1850-1930 as the 1940 portion of the data (1% extract of the IPUMS Restricted Complete Count Data) is not publicly available.

An important feature of the historical Census data used in this analysis is that father’s and son’s (as well as son-in-law’s) incomes are not jointly observed. Olivetti and Paserman (2015) address this measurement issue by predicting, for any given child (John, say) observed in one of the Census datasets, their father’s log earnings using the mean log earnings of fathers whose children have the same first name (namely, John). Olivetti and Paserman then estimate in a second step the intergenerational elasticity by regressing son’s log earnings on the predicted father’s log earnings computed from the previous step. This procedure boils down to a two-sample two-stage least squares estimator (TSTSLS).101010Another limitation of the data used in Olivetti and Paserman (2015) and in this application is that it does not allow us to directly calculate the intergenerational elasticity in income. Instead, we follow the baseline specification of Olivetti and Paserman (2015) and proxy income using an index of occupational standing available from IPUMS (OCCSCORE), which is constructed as the median total income of the persons in each occupation in 1950. The corresponding exclusion restriction that the son’s first name does not predict his log earnings, once we control for his father’s log earnings, may nonetheless be problematic; see Santavirta and Stuhler (2022) for a critical review of the empirical literature using TSTSLS in this context of intergenerational mobility. For the periods 1860-1880 and 1880-1900 only, the IPUMS Linked Representative Samples link fathers and sons using information on first and last names, which allows us to estimate more directly the father-son elasticity using OLS.

Using our notation and consistent with Olivetti and Paserman (2015), the population parameter of interest here is given by

where denotes the son’s (or son-in-law’s) log-income, the father’s log-income and the vector of indicators corresponding to the son’s (or son-in-law’s) first names observed in both datasets. The second equality follows from (1), since is discrete and thus for some . In what follows, we report the upper bound of the estimated identified set and confidence interval on .

Even though the sample sizes as well as the number of common regressors are quite large, our method can still be implemented at a very reasonable computational cost. For instance, for the sample of sons over the first period (1850-1870), the computation of the confidence intervals only takes less than 4 minutes with our R package. As expected, computational time is highest for the period 1910-1930 associated with the largest number of observations, with for both samples of and . Nonetheless, our inference procedure remains tractable in this case too, with a computational time of about 11 minutes.111111These CPU times are obtained using our companion R package, parallelized on 20 CPUs on an Intel Xeon Gold 6130 CPU 2.10GHz with 382Gb of RAM. Overall, this illustrates the applicability of our method, which can be easily implemented even in this type of rich and high-dimensional data environment.

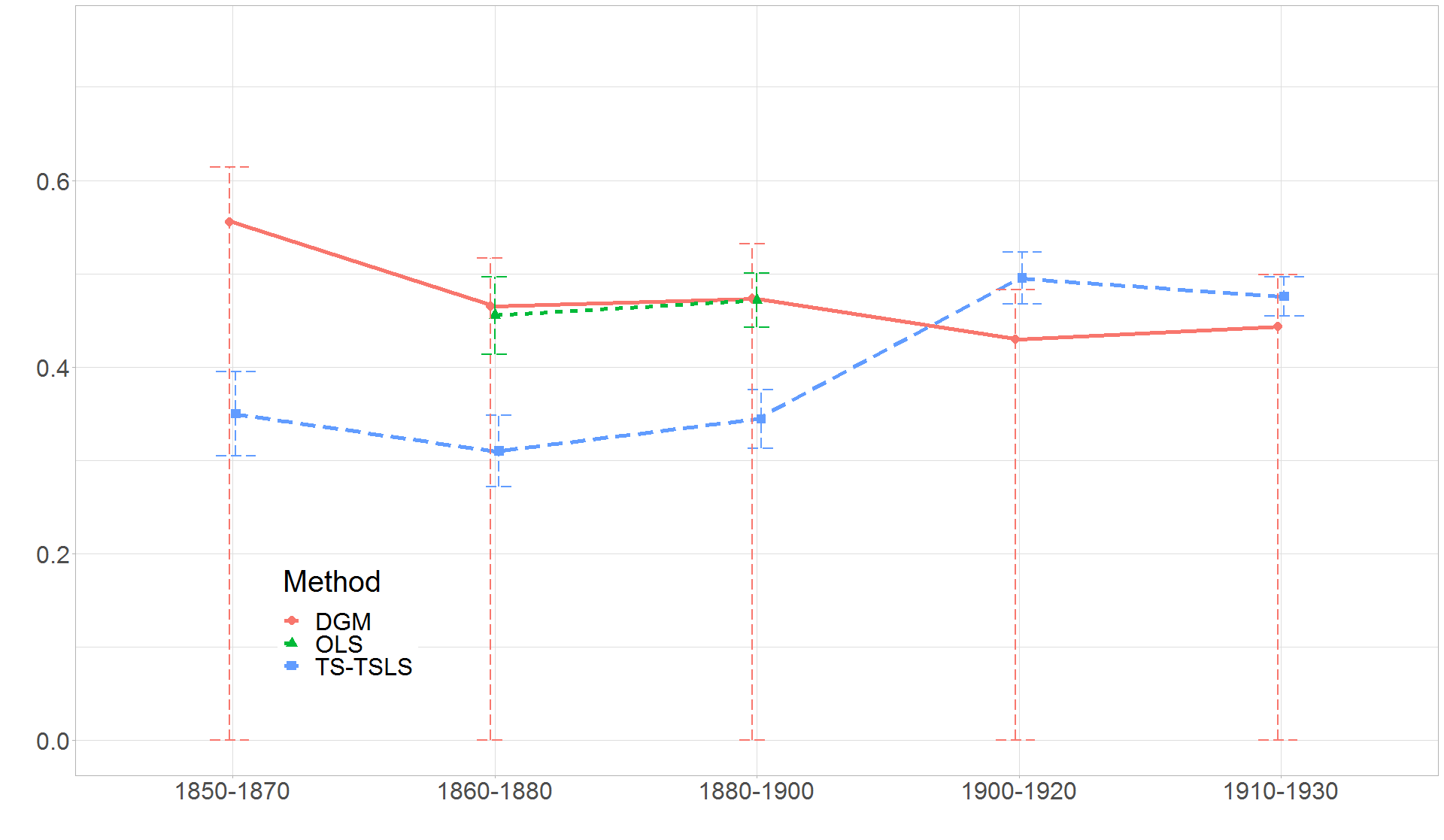

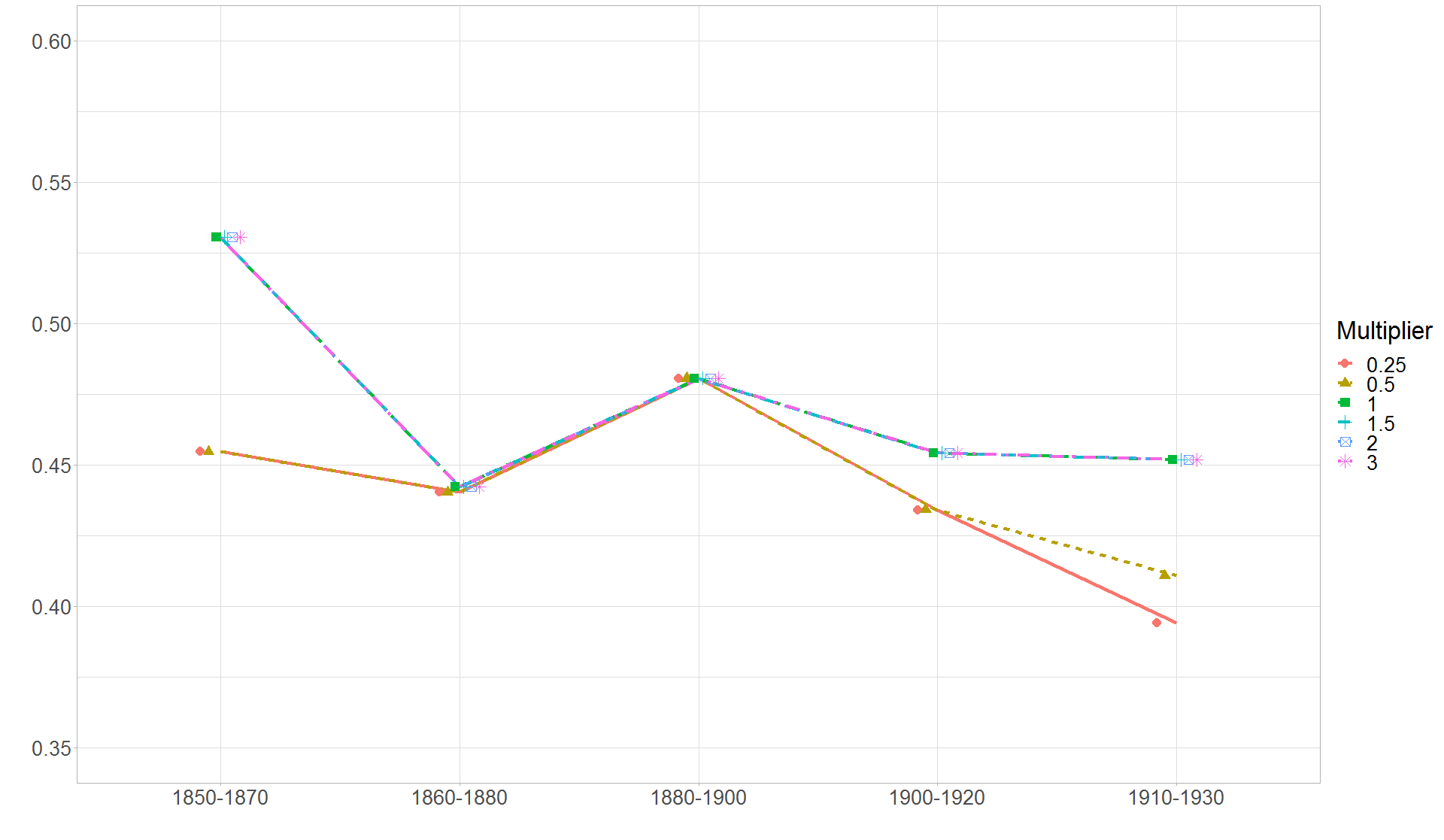

Figures 4(a)-4(b) and Table 1 below display the results, for the father-son as well as father-son-in-law elasticities, obtained using our approach, the TSTSLS and, for the sample of sons over the years 1860-1880 and 1880-1900, the OLS.121212In practice we need to restrict the set of first names included in to avoid very uncommon occurrences that are perfect predictors of the outcome variable . In our baseline specification, we implement this by restricting to the set of first names that account for at least 0.01% of the observations in the pooled sample, and appear at least 10 times in either of the samples. We discuss in the following the robustness of our results to alternative cutoffs. Specifically, we report in Figures 4(a)-4(b) the estimated upper bounds of the identified sets (in solid red) and the confidence intervals (dashed red) obtained with our method, the TSTSLS estimates and confidence intervals (solid and dashed blue, resp.) as well as, for 1860-1880 and 1880-1900 and the sample of sons only, the OLS estimates and confidence intervals (solid and dashed green, resp.).

A first conclusion from these results is that the upper bounds of the confidence intervals associated with our method range, depending on the periods, between 0.48 and 0.61 (0.51 and 0.6) for the sample of sons (sons-in-law). These values of the intergenerational coefficient are all well below the natural upper bound of 1. Also, even though the estimates vary depending on the data and econometric specification being used, most of the existing point estimates of the father-son income elasticity range between 0.40 and 0.50 (Olivetti and Paserman, 2015). Overall, this clearly indicates that our method leads to informative inference on the parameter of interest.

Second, consider the two cases where the linked data is available (1860-1880 and 1880-1900 for the sample of sons). Results in Table 1 indicate that the corresponding OLS estimates of the intergenerational income elasticities are quantitatively very close to the estimated upper bound of our identified set. Recall that, from Proposition 5 in Section 2.3.4, the upper bound of our identified set (, say) plays a special role: under an additional restriction on the distributions of and the error term, is actually point identified and equal to .131313Proposition 5 is obtained without . Yet, it can be combined with Proposition 2 to show that , and in turn (and thus here) are point identified with such . In other words, the results from these two periods support the hypothesis that the restriction on the distributions of and the error term guaranteeing point identification of by hold.

Note: for readability and because 0 is a natural lower bound, the y-axis starts at 0, even though the lower bounds of our confidence intervals without restrictions are negative (see Table 1).

| Sample: | 1850-1870 | 1860-1880 | 1880-1900 | 1900-1920 | 1910-1930 | ||||

| Sons | |||||||||

| DGM, set | [-0.555,0.555] | [-0.465,0.465] | [-0.473,0.473] | [-0.430,0.430] | [-0.443,0.443] | ||||

| DGM, CI. | [-0.614,0.614] | [-0.517,0.517] | [-0.532,0.532] | [-0.483,0.483] | [-0.499,0.499] | ||||

| DGM, , set | [0.081,0.555] | [0.075,0.465] | [0.075,0.473] | [0.076,0.430] | [0.071,0.443] | ||||

| DGM, , CI. | [0.033,0.617] | [0.034,0.519] | [0.039,0.527] | [0.044,0.477] | [0.047,0.491] | ||||

| DGM, , set | [0.163,0.555] | [0.151,0.465] | [0.153,0.473] | [0.164,0.430] | [0.159,0.443] | ||||

| DGM, , CI. | [0.095,0.601] | [0.093,0.506] | [0.102,0.513] | [0.127,0.459] | [0.132,0.477] | ||||

| TSTSLS, pt. | 0.350 | 0.310 | 0.344 | 0.495 | 0.476 | ||||

| TSTSLS, CI. | [0.305,0.395] | [0.272,0.348] | [0.313,0.376] | [0.468,0.523] | [0.454,0.497] | ||||

| Test of equality, p-value | 0.001 | 0.001 | 0.001 | 0.999 | 0.014 | ||||

| (Stat.; critical val. 95%) | (28.52; 15.16) | (25.21; 12.37) | (25.92; 28.30) | (15.09; 17.69) | (8.18; 6.79) | ||||

| OLS, pt. | 0.455 | 0.472 | |||||||

| OLS, CI. | [0.414,0.497] | [0.443,0.501] | |||||||

| Test pt identification, p-value | 0.147 | 0.003 | |||||||

| (Stat.; critical val. 95%) | (9.21,17.03) | (23.06,6.33) | |||||||

| Number of names | 225 | 261 | 382 | 514 | 598 | ||||

| Sample sizes and | (39,734; 34,603) | (55,728; 47,014) | (85,340; 73,999) | (116,986; 102,053) | (131,089; 116,328) | ||||

| Sample: | 1850-1870 | 1860-1880 | 1880-1900 | 1900-1920 | 1910-1930 | ||||

| Sons-in-law | |||||||||

| DGM, set | [-0.531,0.531] | [-0.442,0.442] | [-0.481,0.481] | [-0.454,0.454] | [-0.452,0.452] | ||||

| DGM, CI. | [-0.601,0.600] | [-0.507,0.507] | [-0.554,0.555] | [-0.515,0.515] | [-0.513,0.513] | ||||

| DGM, , set | [0.089,0.531] | [0.085,0.442] | [0.075,0.481] | [0.073,0.454] | [0.062,0.452] | ||||

| DGM, , CI. | [0.030,0.605] | [0.036,0.505] | [0.029,0.552] | [0.037,0.513] | [0.033,0.509] | ||||

| DGM, , set | [0.186,0.531] | [0.178,0.442] | [0.159,0.481] | [0.164,0.454] | [0.146,0.452] | ||||

| DGM, , CI. | [0.115,0.596] | [0.114,0.490] | [0.105,0.534] | [0.122,0.499] | [0.113,0.496] | ||||

| TSTSLS, pt. | 0.340 | 0.400 | 0.400 | 0.493 | 0.414 | ||||

| TSTSLS, CI. | [0.299,0.381] | [0.364,0.436] | [0.365,0.434] | [0.469,0.518] | [0.395,0.433] | ||||

| Test of equality, p-value | 0.001 | 0.998 | 0.012 | 1 | 1 | ||||

| (Stat.; critical val. 95%) | (23.12; 9.67) | (5.87; 18.53) | (13.08; 12.94) | (8.03; 13.28) | (8.33; 13.07) | ||||

| Number of names | 155 | 212 | 323 | 468 | 545 | ||||

| Sample sizes and | (25,760; 33,256) | (32,970; 45,800) | (49,068; 71,141) | (73,425; 99,871) | (85,122; 112,763) | ||||

| Notes: Dependent variable is son’s (or son-in-law’s) log income. Common regressors are dummies for the first names appearing more than 0.01% in the pooled dataset and 10 times in both datasets. “DGM, set” and “DGM, CI.” refer to the estimated identified set and 95% confidence interval, respectively, obtained with our method. “TSTSLS, pt.” and “TSTSLS, CI.” refer to the TSTSLS point estimate and 95% confidence interval, respectively. The test of equality between the TSTSLS () estimates and DGM () upper bound estimates is performed using subsampling with 1,000 replications. The statistic (“Stat.”) is , where and , and being the respective sample sizes of and . The critical value corresponds to the quantile of the distribution of , where is a subsampled version of and is the subsample size. The sample sizes where the joint distribution is observed for both periods 1860-1880 and 1880-1900 are respectively 3,947 and 9,076. The on the short and long regressions are respectively 0.04 and 0.18 for 1860-1880, and 0.02 and 0.17 for 1880-1900. The test for point identification is performed with the selected in (14), however this choice appears conservative on simulations. Taking yields p-values of 0.69 for the period 1860-1880 and 0.04 for 1880-1900. | |||||||||

Besides, the fact that we do not reject at standard levels the null hypothesis of point identification with our formal test described in Section A.3 for the period 1860-1880 (p-value of 0.147) provides suggestive evidence in this direction.141414Simulation results available from the authors upon request indicate that our choice of tends to be conservative for the test of point identification. One would not reject either at the 1% level the null hypothesis for the period 1880-1900 with a less conservative choice of (e.g. we obtain a p-value of 0.04 using ). Under this assumption, our results are informative not only on the maximal father-son elasticity coefficient for a given period of time, but also on its evolution. It follows in particular that our estimates point to a mild decrease in this elasticity coefficient for sons between 1850 and 1930.

Third, the results from the equality test reported in Table 1 indicate that the TSTSLS estimates are in several cases statistically distinguishable from the estimated upper bounds of our identified sets. This includes, for the sample of sons, all periods except 1900-1920, and the periods 1850-1870 and 1880-1900 for the sample of sons-in-law. Besides, for the sample of sons in particular, the TSTSLS estimates exhibit a sharp increase, while our estimated upper bound decreases between the periods 1880-1900 and 1900-1920. In that sense, our results offer suggestive evidence that the intergenerational income correlation might have been more stable at the beginning of the 20th century than what one would infer from the TSTSLS estimates.

Fourth, we also report in Table 1 the estimated identified set and confidence intervals associated with our method when we impose a lower bound on the of the long regression, namely or . Imposing any of these restrictions, which are satisfied for the periods 1860-1880 and 1880-1900 for which the linked data is available, results in substantially tighter confidence intervals. In particular, for the sample of sons, the confidence intervals obtained under the restriction allow us to reject values of the intergenerational income elasticity coefficient smaller than 0.13 and larger than 0.48 for the years 1910-1930.

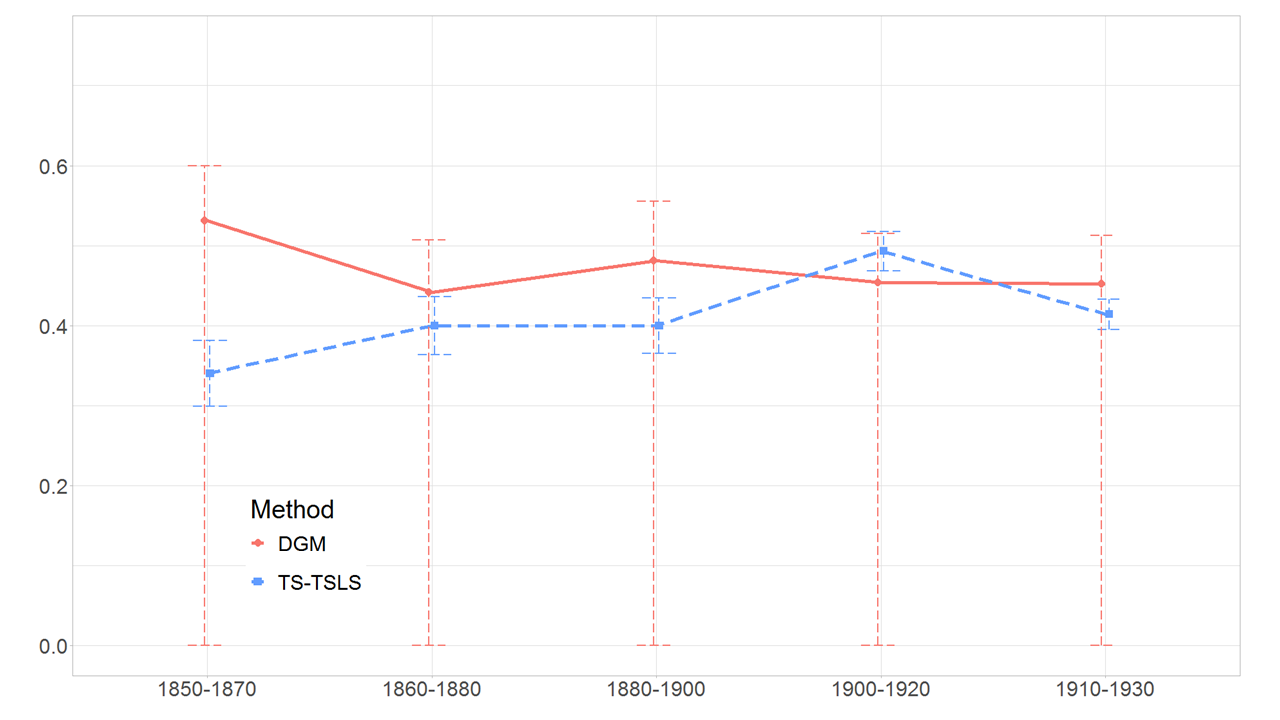

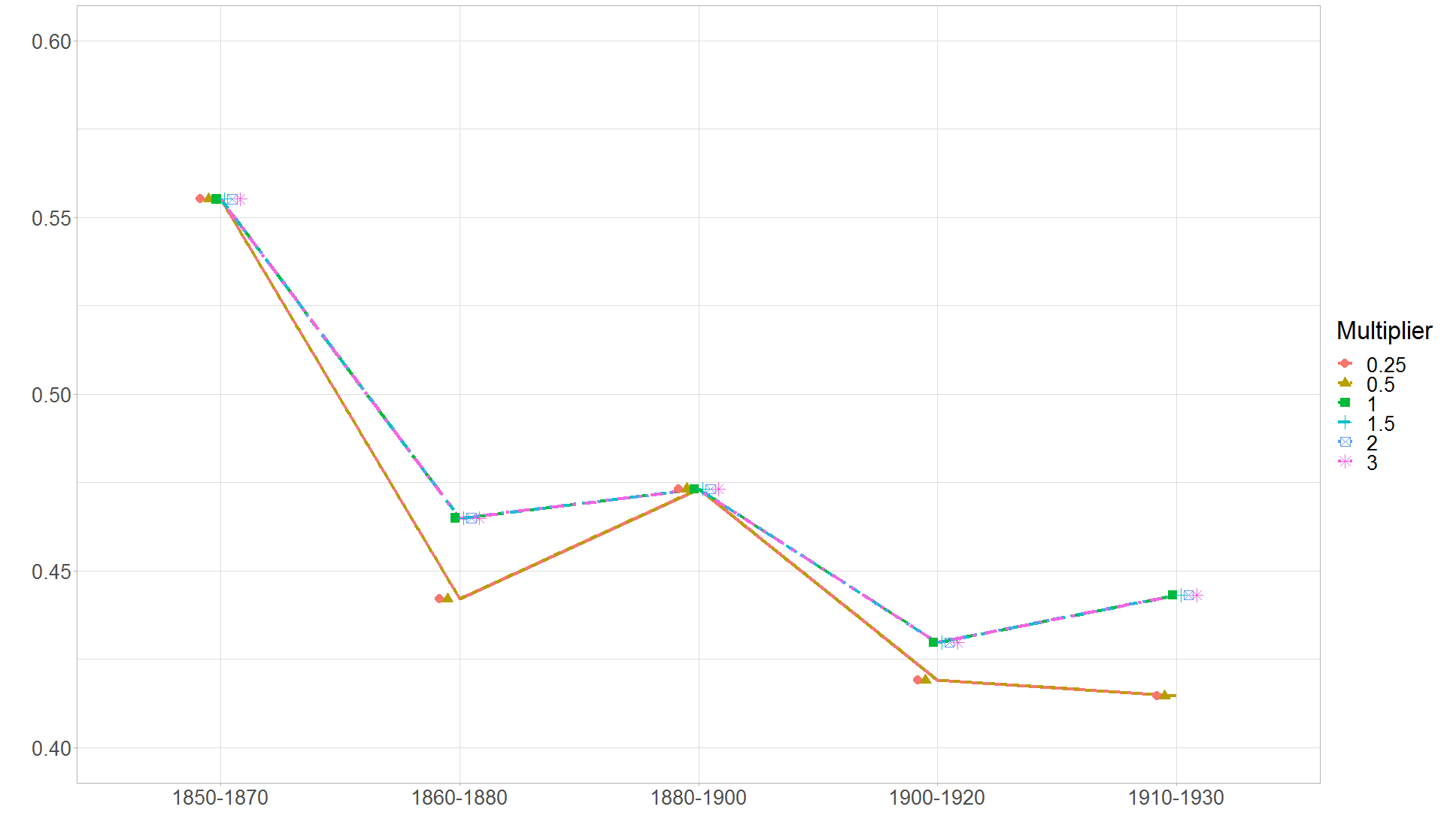

We consider in Tables 8 and 9, and Figure 5(b) in online Appendix D several robustness checks. They relate to the set of first names that we include as controls in our estimation procedure (Panel A), the choice of (Panel B and Figure 5(b)), and restrictions of the sample to the set of individuals whose first name is included in the set of controls (Panel C). Throughout the tables, we focus on the upper bound of the estimated identified set (“DGM, set”) and of the confidence interval (“DGM, CI.”).

The main takeaway from Table 8 and Figure 5(b) is that, for the sample of sons, the results from our inference procedure are qualitatively, and in most cases quantitatively, robust to these different sensitivity analyses. The one case that exhibits more sensitivity is the specification where we control for the first names that account for at least 0.02% of the sample, instead of 0.01% in our baseline specification. The upper bound of our confidence interval for the period 1900-1920 increases in this case from 0.48 to 0.58, the results remaining, however, stable for the other periods. The results for the sample of sons-in-law (Table 9) are also, for most periods at the exception of the same limit for 1900-1920, qualitatively, and in some cases quantitatively similar across specifications. The main difference with the sample of sons is that the choice of does appear to matter more for the sons-in-law, a limitation that one should keep in mind when interpreting the findings for this subgroup. Nonetheless, to the extent that our baseline choice of (see Section 3.3) is motivated by the theory and is found to perform well in our Monte Carlo simulation exercises, we do not view this as particularly worrisome.

5 Conclusion

We study the identification of and inference on partially linear models, in an environment where the outcome of interest and some of the covariates are observed in two different datasets that can not be matched. This setup arises in particular when one is interested in the effect of a variable that is not observed jointly with the outcome variable, or in cases where potential confounders are observed in a different dataset from the one including the outcome and regressor of interest. In such situations, researchers often rely on strong assumptions to point identify their parameters of interest. Our approach offers a useful alternative when such assumptions are debatable. The application shows that in addition to its tractability, our method is able to deliver informative bounds. Finally, beyond the model considered in this paper, our analysis suggests that the radial function is an appealing tool in partial identification problems where the support function proves difficult to compute.

References

- Abrevaya and Jiang (2005) Abrevaya, J. and W. Jiang (2005). Unobservable selection and coefficient stability: theory and evidence. Journal of Business and Economic Statistics 23(1), 1–19.

- Altonji et al. (2005) Altonji, J. G., T. E. Elder, and C. R. Taber (2005). Selection on observed and unobserved variables: Assessing the effectiveness of catholic schools. Journal of Political Economy 113(1), 151–184.

- Andrews and Shi (2017) Andrews, D. W. and X. Shi (2017). Inference based on many conditional moment inequalities. Journal of Econometrics 196(2), 275–287.

- Athey et al. (2020) Athey, S., R. Chetty, and G. W. Imbens (2020). Combining experimental and observational data to estimate treatment effects on long term outcomes. arXiv preprint arXiv:2006.09676v1.

- Backhoff-Veraguas et al. (2019) Backhoff-Veraguas, J., M. Beiglböck, and G. Pammer (2019). Existence, duality, and cyclical monotonicity for weak transport costs. Calculus of Variations and Partial Differential Equations 58(6), 1–28.

- Barber et al. (1996) Barber, C. B., D. P. Dobkin, and H. Huhdanpaa (1996). The quickhull algorithm for convex hulls. ACM Transactions on Mathematical Software (TOMS) 22(4), 469–483.

- Bontemps and Magnac (2017) Bontemps, C. and T. Magnac (2017). Set identification, moment restrictions, and inference. Annual Review of Economics 9, 103–129.

- Buchinsky et al. (2022) Buchinsky, M., F. Li, and Z. Liao (2022). Estimation and inference of semiparametric models using data from several sources. Journal of Econometrics 226(1), 80–103.

- Cárcamo et al. (2020) Cárcamo, J., A. Cuevas, and L.-A. Rodríguez (2020). Directional differentiability for supremum-type functionals: Statistical applications. Bernoulli 26(3), 2143–2175.

- Chernozhukov et al. (2013) Chernozhukov, V., S. Lee, and A. M. Rosen (2013). Intersection bounds: estimation and inference. Econometrica 81(2), 667–737.

- Chetverikov et al. (2018) Chetverikov, D., A. Santos, and A. M. Shaikh (2018). The econometrics of shape restrictions. Annual Review of Economics 10(1), 31–63.

- Cross and Manski (2002) Cross, P. J. and C. F. Manski (2002). Regressions, short and long. Econometrica 70(1), 357–368.

- Crossley et al. (2022) Crossley, T. F., P. Levell, and S. Poupakis (2022). Regression with an imputed dependent variable. Journal of Applied Econometrics 37(7), 1277–1294.

- Davydov et al. (1998) Davydov, Y. A., M. A. Lifshits, and N. V. Smorodina (1998). Local properties of distributions of stochastic functionals. American Mathematical Society.

- De la Cal and Cárcamo (2006) De la Cal, J. and J. Cárcamo (2006). Stochastic orders and majorization of mean order statistics. Journal of Applied Probability 43(3), 704–712.

- Del Barrio et al. (1999) Del Barrio, E., E. Giné, and C. Matrán (1999). Central limit theorems for the wasserstein distance between the empirical and the true distributions. Annals of Probability 31, 1009–1071.

- D’Haultfoeuille et al. (2021) D’Haultfoeuille, X., C. Gaillac, and A. Maurel (2021). Rationalizing rational expectations: Characterizations and tests. Quantitative Economics 12(3), 817–842.

- D’Haultfœuille et al. (2023) D’Haultfœuille, X., C. Gaillac, and A. Maurel (2023). Partially linear models under data combination. arXiv preprint arXiv:2204.05175.

- Diegert et al. (2022) Diegert, P., M. A. Masten, and A. Poirier (2022). Assessing omitted variable bias when the controls are endogenous. arXiv preprint arXiv:2206.02303.

- Embrechts and Wang (2015) Embrechts, P. and R. Wang (2015). Seven proofs for the subadditivity of expected shortfall. Dependence Modeling 3(1), 126–140.

- Fan et al. (2014) Fan, Y., R. Sherman, and M. Shum (2014). Identifying treatment effects under data combination. Econometrica 82(2), 811–822.

- Fan et al. (2016) Fan, Y., R. Sherman, and M. Shum (2016). Estimation and inference in an ecological inference model. Journal of Econometric Methods 5(1), 17–48.

- Firpo et al. (2023) Firpo, S., A. F. Galvao, and T. Parker (2023). Uniform inference for value functions. Journal of Econometrics 235, 1680–1699.

- Galichon (2016) Galichon, A. (2016). Optimal transport methods in economics. Princeton University Press.

- Galichon and Henry (2011) Galichon, A. and M. Henry (2011). Set identification in models with multiple equilibria. The Review of Economic Studies 78(4), 1264–1298.

- Garcia et al. (2020) Garcia, J., J. Heckman, L. D.E., and M. Prados (2020). Quantifying the life-cycle benefits of an influential early-childhood program. Journal of Political Economy 128(7), 2502–2541.

- Gozlan et al. (2018) Gozlan, N., C. Roberto, P.-M. Samson, Y. Shu, and P. Tetali (2018). Characterization of a class of weak transport-entropy inequalities on the line. Annales de l’IHP 54(3), 1667–1693.

- Hanushek et al. (2021) Hanushek, E. A., L. Kinne, P. Lergetporer, and L. Woessmann (2021). Culture and student achievement: The intertwined roles of patience and risk-taking. Economic Journal 132(646), 2290–2307.

- Hausman (2016) Hausman, J. K. (2016). Fiscal policy and economic recovery: The case of the 1936 veterans’ bonus. American Economic Review 106(4), 1100–1143.

- Hiriart-Urruty and Lemaréchal (2012) Hiriart-Urruty, J.-B. and C. Lemaréchal (2012). Fundamentals of convex analysis. Springer Science & Business Media.

- Horowitz and Manski (1995) Horowitz, J. L. and C. F. Manski (1995). Identification and robustness with contaminated and corrupted data. Econometrica: Journal of the Econometric Society 63(2), 281–302.

- Hwang (2022) Hwang, Y. (2022). Bounding omitted variable bias using auxiliary data with an application to estimate neighborhood effects. SSRN 3866876.

- Manski (2018) Manski, C. F. (2018). Credible ecological inference for medical decisions with personalized risk assessment. Quantitative Economics 9(2), 541–569.

- Masten and Poirier (2018) Masten, M. A. and A. Poirier (2018). Identification of treatment effects under conditional partial independence. Econometrica 86(1), 317–351.

- Matzkin (1994) Matzkin, R. (1994). Restrictions of economic theory in nonparametric methods. In R. Engle and D. McFadden (Eds.), Handbook of Econometrics, Volume 4, Volume 4 of Handbook of Econometrics, pp. 2523–58. Elsevier.

- Milgrom and Segal (2002) Milgrom, P. and I. Segal (2002). Envelope theorems for arbitrary choice sets. Econometrica 70(2), 583–601.

- Molchanov (2017) Molchanov, I. (2017). Theory of Random Sets, Volume 87. Springer, Probability Theory and Stochastic Modelling.

- Molinari (2020) Molinari, F. (2020). Microeconometrics with partial identification. In S. N. Durlauf, L. P. Hansen, J. J. Heckman, and R. L. Matzkin (Eds.), Handbook of Econometrics, Volume 7A, Volume 7 of Handbook of Econometrics, pp. 355–486. Elsevier.

- Molinari and Peski (2006) Molinari, F. and M. Peski (2006). Generalization of a result on “regressions, short and long”. Econometric Theory 22(1), 159–163.

- Neal and Johnson (1996) Neal, D. A. and W. R. Johnson (1996). The role of premarket factors in black-white wage differences. Journal of Political Economy 104(5), 869–895.

- Olivetti and Paserman (2015) Olivetti, C. and M. D. Paserman (2015). In the name of the son (and the daughter): Intergenerational mobility in the united states, 1850-1940. American Economic Review 105(8), 2695–2724.

- Oster (2019) Oster, E. (2019). Unobservable selection and coefficient stability: theory and evidence. Journal of Business and Economic Statistics 37(2), 187–204.

- Pacini (2019) Pacini, D. (2019). Two-sample least squares projection. Econometric Reviews 38(1), 95–123.

- Piatek and Pinger (2016) Piatek, R. and P. Pinger (2016). Maintaining (locus of) control? data combination for the identification and inference of factor structure models. Journal of Applied Econometrics 31, 734–755.

- Politis et al. (1999) Politis, D. N., J. P. Romano, and M. Wolf (1999). Subsampling. Springer Science & Business Media.

- Pollard (1991) Pollard, D. (1991). Asymptotics for least absolute deviation regression estimators. Econometric Theory 7(2), 186–199.

- Ridder and Moffitt (2007) Ridder, G. and R. Moffitt (2007). The econometrics of data combination. Handbook of Econometrics 6, 5469–5547.

- Robbins et al. (2022) Robbins, M. W., S. Bauhoff, and L. Burgette (2022). Data fusion for predicting long-term program impacts. arXiv preprint arXiv:2205.01904v1.

- Robinson (1988) Robinson, P. (1988). Root-n-consistent semiparametric regression. Econometrica 56(4), 931–954.

- Rothstein and Wozny (2013) Rothstein, J. and N. Wozny (2013). Permanent income and the black-white test score gap. Journal of Human Resources 48(3), 510–544.

- Santavirta and Stuhler (2022) Santavirta, T. and J. Stuhler (2022). Name-based estimators of intergenerational mobility. Mimeo.

- Strassen (1965) Strassen, V. (1965). The existence of probability measures with given marginals. The Annals of Mathematical Statistics 36(2), 423–439.

- Sundaram (1996) Sundaram, R. K. (1996). A first course in optimization theory. Cambridge university press.

- Tripathi (2000) Tripathi, G. (2000). Local semiparametric efficiency bounds under shape restrictions. Econometric Theory 16(5), 729–739.

- Van der Vaart (2000) Van der Vaart, A. W. (2000). Asymptotic statistics. Cambridge University Press.

- Van der Vaart and Wellner (1996) Van der Vaart, A. W. and J. A. Wellner (1996). Weak convergence and empirical processes. Springer.

- Wijsman (1966) Wijsman, R. A. (1966). Convergence of sequences of convex sets, cones and functions. ii. Transactions of the American Mathematical Society 123(1), 32–45.

Appendix A Additional theoretical results

A.1 Measurement errors

We have assumed so far that the outcome and covariates are perfectly observed. However, measurement errors are pervasive in survey data. We now explore the robustness of the identified set proposed earlier to measurement errors on the outcome and covariates, which we denote by and . Specifically, consider a situation where both the covariates and the outcome are measured with error, such that:

| (19) |

We introduce a new set, , which is defined as the original identified set after replacing the observed measurement error-ridden covariates and outcome by their latent counterparts .

The proof is in our supplementary material. This proposition establishes that the identified set is robust to measurement errors in the following sense: if (centered) measurement errors on the outcome second-order stochastically dominate those on the linear index for all , the identified set based on the observed covariates and outcome always contains the true value of the parameter of interest.151515 This result and underlying assumptions are closely related to the robustness to measurement errors on the beliefs of the test of rational expectations proposed in D’Haultfoeuille et al. (2021) (Subsection 2.2.4). To better understand the above domination condition, suppose that , and . Then, recalling that any satisfies the variance restriction , a sufficient condition for the dominance condition is . In our application for instance, and are the log earnings of fathers and sons (or sons-in-law), respectively, so and seem credible. This suggests that the key domination condition from Proposition 8 is likely to hold in this context.

A.2 Identification of a model with interaction terms

Let and . We consider here the following model

First define, for and (),

Proposition 2 applied to the subpopulation implies that for all , , where . Because the converse also holds, the identified set of is

| (20) |

The sets are convex and include . Hence, is convex too, and also includes . Moreover, because are compact, any satisfies, for any , ,

| (21) |

for some . Moreover,

which implies that is also compact. Thus, can also be described by its radial function, which we denote by . Moreover, it follows from (20) that

A.3 Test for point-identification

We develop here a statistical test that can be used to check whether . Following the discussion in Subsection 2.3.4, this boils down to testing for

| (22) |

where we recall that the joint distribution of the validation data is observed and . We consider a statistical test based on i.i.d. data . The test statistic is

where is the OLS estimator of . The critical value is then , the quantile of order (defined conditional on the data) of

where , and are the subsampling counterpart of , and , respectively. We establish the asymptotic properties of the test under the following assumption.

Assumption 7.

for some , , and . Also, there exists , compact and including a ball of positive radius centered at , and such that for all , there exists and a strictly increasing and continuous function such that and

Up to the condition on which we come back below, Assumption 7 is very close to the first part of Assumption 4, but it is weaker as we require that it holds over instead of .

Proposition 9.

The proof is in our supplementary material. Note that if holds but , will tend to infinity and will be rejected. Because we are testing here the validation of the tail condition described above, failing to reject under the alternative is more of an issue than wrongly rejecting . Thus, potential over-rejection is arguably not as problematic as in other more standard contexts, such as testing the null of no effect of a treatment.

Appendix B Application to the black-white wage gap

We apply our method to estimate the black-white wage gap among young males in the United States using the 1979 panel of the National Longitudinal Survey of Youth (NLSY79), revisiting the seminal work of Neal and Johnson (1996) on this question. Considering the same restrictions as Neal and Johnson (1996) leads to a sample of size .161616We refer the reader to Neal and Johnson (1996) for a detailed discussion on the data. We focus on the following model :

where is the mean log wage in 1990-1991, denotes the AFQT and , are dummy variables for being black or Hispanic. While is jointly observed in the NLSY79 dataset, we proceed in the following as if AFQT, which is used in Neal and Johnson (1996) to control for pre-market factors, was not observed jointly with wages. This setup, which mimics the data environments in several other countries, allows us to directly compare the confidence intervals based on our partial identification approach with the ones obtained from the oracle OLS specification.

Results in Table 2 below show the effect on our bounds when we impose different sets of constraints, namely i) a negative sign constraint on the coefficient associated with the black indicator as well as a positive sign constraint on the coefficient associated with the AFQT, ii) the latter constraints combined with the constraint , and iii) the sign constraints i) combined with a less conservative bound . Focusing on the main coefficient of interest , these results indicate that imposing these constraints on the results in an identified set and confidence interval that are quite informative. Notably, the lower bound of the confidence interval is equal to and respectively in cases ii) and iii), against (i.e. a 17 log points wage penalty) for the OLS estimator. Taken together, these results show that our method is able to deliver confidence intervals that are very informative in practice.