High-dimensional time series segmentation via factor-adjusted vector autoregressive modelling

Abstract

Vector autoregressive (VAR) models are popularly adopted for modelling high-dimensional time series, and their piecewise extensions allow for structural changes in the data. In VAR modelling, the number of parameters grow quadratically with the dimensionality which necessitates the sparsity assumption in high dimensions. However, it is debatable whether such an assumption is adequate for handling datasets exhibiting strong serial and cross-sectional correlations. We propose a piecewise stationary time series model that simultaneously allows for strong correlations as well as structural changes, where pervasive serial and cross-sectional correlations are accounted for by a time-varying factor structure, and any remaining idiosyncratic dependence between the variables is handled by a piecewise stationary VAR model. We propose an accompanying two-stage data segmentation methodology which fully addresses the challenges arising from the latency of the component processes. Its consistency in estimating both the total number and the locations of the change points in the latent components, is established under conditions considerably more general than those in the existing literature. We demonstrate the competitive performance of the proposed methodology on simulated datasets and an application to US blue chip stocks data.

Keywords: data segmentation, vector autoregression, high dimensionality, factor model

1 Introduction

Vector autoregressive (VAR) models are popular for modelling cross-sectional and serial correlations in multivariate, possibly high-dimensional time series. With, for example, applications in finance (Barigozzi and Hallin,, 2017), biology (Shojaie and Michailidis,, 2010) and genomics (Michailidis and d’Alché Buc,, 2013). Within such settings, the importance of data segmentation is well-recognised, and several methods exist for detecting change points in VAR models in both fixed (Kirch et al.,, 2015) and high dimensions (Safikhani and Shojaie,, 2022; Wang et al.,, 2019; Bai et al.,, 2020; Maeng et al.,, 2022).

| (a) 18/03/2008–07/07/2009 | (b) 18/03/2008–07/07/2009 | (c) 18/03/2008–07/07/2009 |

|

|

|

| (d) 15/11/2003–07/06/2006 | (e) 08/06/2006–17/03/2008 | (f) 08/07/2009–28/07/2011 |

|

|

|

VAR modelling quickly becomes a high-dimensional problem as the number of parameters grows quadratically with the dimensionality. Accordingly, most existing methods for detecting change points in high-dimensional, piecewise stationary VAR processes assumes sparsity (Basu and Michailidis,, 2015). However, it is debatable whether highly sparse models are appropriate for some applications. For example, Giannone et al., (2021) note the difficulty of identifying sparse predictive representations for several macroeconomic applications.

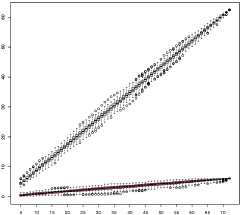

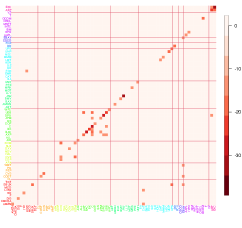

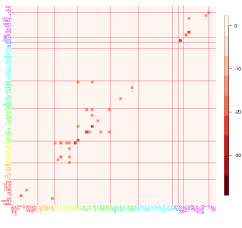

We illustrate the inadequacy of the sparsity assumption on a volatility panel dataset (see Section 5.3 for its description). Figure 1 (a) shows that as the dimensionality increases, the leading eigenvalue of the spectral density matrix at frequency (i.e. the long-run covariance) estimated from the data also increases linearly. This indicates the presence of strong serial and cross-sectional correlations that cannot be accommodated by sparse VAR models. In Figure 1 (b), we report the logged and truncated -values obtained from fitting a VAR() model to the same dataset (truncation level chosen at by Bonferroni correction with the significance level ) via ridge regression, see Cule et al., (2011). Strong dependence observed from most pairs of the variables further confirms that we cannot infer a sparse pairwise relationship from such data. On the other hand, Figure 1 (c) shows that once we estimate factors driving the strong correlations and adjust for their presence, there is evidence that the remaining dependence in the data can be modelled as being sparse. Together, the plots (d), (e), (c) and (f) display that the relationship between a pair of variables (after factor-adjustment) varies over time, particularly at the level of industrial sectors. Here, the intervals are chosen according to the data segmentation result reported in Section 5.3. This example highlights the importance of (i) accounting for the dominant correlations prior to fitting a model under the sparsity assumption, and (ii) detecting structural changes when analysing time series datasets covering a long period.

Motivated by the aforementioned characteristics of high-dimensional time series data, factor-adjusted regression modelling has increasingly gained popularity (Fan et al.,, 2020, 2021; Krampe and Margaritella,, 2021). The factor-adjusted VAR model proposed by Barigozzi et al., (2022) assumes that a handful of common factors capture strong serial and cross-sectional correlations, such that it is reasonable to assume a sparse VAR model on the remaining component to capture idiosyncratic, variable-specific dependence. We extend this framework by proposing a new, piecewise stationary factor-adjusted VAR model and develop FVARseg, an accompanying change point detection methodology. Below we summarise the methodological and theoretical contributions made in this paper.

Generality of the modelling framework.

We decompose the data into two piecewise stationary latent processes: one is driven by factors and accounts for dominant serial and cross-sectional correlations, and the other models sparse pairwise dependence via a VAR model. We adopt the most general approach to factor modelling and allow both components to undergo changes which, in the case of the latter, are attributed to shifts in the VAR parameters. To the best of our knowledge, such a general model simultaneously permitting the presence of common factors and change points, has not been studied in the literature previously. Accordingly, we are not aware of any method that can comprehensively address the data segmentation problem considered in this paper.

Methodological novelty.

The idea of scanning the data for changes over moving windows, has successfully been applied to a variety of data segmentation problems (Preuss et al.,, 2015; Eichinger and Kirch,, 2018; Chen et al.,, 2021). We propose FVARseg, a two-stage methodology that combines this idea with statistics carefully designed to have good detection power against different types of changes in the two latent components. In Stage 1 of FVARseg, motivated by that dominant factor-driven correlations appear as leading eigenvalues in the frequency domain, see e.g. Figure 1 (a), we propose a detector statistic that contrasts the local spectral density matrix estimators from neighbouring moving windows in operator norm, which is well-suited to detect changes in the factor-driven component.

In Stage 2 for detecting change points in the latent piecewise stationary VAR process, we deliberately avoid estimating the latent process which may incur large errors. Instead, we make use of (i) the Yule-Walker equation that relates autocovariances (ACV) and VAR parameters, and (ii) the availability of local ACV estimators of the latent VAR process after Stage 1. Combining these ingredients, we propose a novel detector statistic that enjoys methodological simplicity as well as statistical efficiency. Further, through sequential evaluation of the detector statistic, the second-stage procedure requires the estimation of local VAR parameters at selected locations only. Consequently it is highly competitive computationally when both the sample size and the dimensionality are large.

Theoretical consistency.

FVARseg achieves consistency in estimating the total number and locations of the change points in both of the piecewise stationary factor-driven and VAR processes. Our theoretical analysis is conducted in a setting considerably more general than those commonly adopted in the literature, permitting dependence across stationary segments and heavy-tailedness of the data. We also derive the rate of localisation for each stage of FVARseg where we make explicit the influence of tail behaviour and the size of changes. In particular, under Gaussianity, the estimators from Stage 1 nearly matches the minimax optimal rate derived for the simpler, covariance change point detection problem.

The rest of the paper is structured as follows. Section 2 introduces the piecewise stationary factor-adjusted VAR model. Section 3 describes the two stages of FVARseg, the proposed data segmentation methodology, and Section 4 establishes its theoretical consistency. Section 5 demonstrates the good performance of FVARseg empirically. R code implementing our method is available from https://github.com/haeran-cho/fvarseg.

Notation.

Let and denote an identity matrix and a matrix of zeros whose dimensions depend on the context. For a random variable and , denote . Given , we denote by its transposed complex conjugate. We define its element-wise , and -norms by , and , and its spectral and induced , -norms by , and , respectively. For positive definite , we denote its minimum eigenvalue by . For two real numbers, and . For two sequences and , we write if, for some constants , there exists such that for all .

2 Piecewise stationary factor-adjusted VAR model

2.1 Background

A zero-mean, -variate process follows a VAR() model if it satisfies

| (1) |

where , determine how future values of the series depend on their past. The -variate random vector has which are independently and identically distributed (i.i.d.) for all and with and . The positive definite matrix is the covariance matrix of the innovations for the VAR process.

A factor-driven component exhibits strong cross-sectional and/or serial correlations by ‘loading’ finite-dimensional factors linearly. Among many, the generalised dynamic factor model (GDFM, Forni et al.,, 2000, 2015) provides the most general approach (see Appendix D for further discussions), and defines the -variate factor-driven component as

| (2) |

For fixed , the -variate random vector contains the common factors which are shared across the variables and time, and are assumed to be i.i.d. for all and with and . The matrix of square-summable filters with the lag-operator and , serves the role of loadings under (2).

Barigozzi et al., (2022) propose a factor-adjusted VAR model, where the observations are assumed to be decomposed as a sum of the two latent components and in (1)–(2), with pervasive correlations in the data are accounted for by and the remaining dependence captured by . In the next section, we introduce its piecewise stationary extension where both the factor-driven and VAR processes are allowed to undergo structural changes.

2.2 Model

We observe a zero-mean, -variate piecewise stationary process where

| (5) |

Here, , denote the change points in the piecewise stationary factor-driven component such that at each , the filter of loadings undergoes a change. We permit the factor number to vary over time as , with the factor associated with being a sub-vector of . Similarly, , denote the change points in the piecewise stationary VAR process at which the VAR parameters undergo shifts; we permit the VAR innovation covariance matrix to vary as but our interest lies in detecting changes in VAR parameters, and the VAR order may vary over time as with for . By convention, we denote and . In line with the factor modelling literature, we assume that and are uncorrelated through having for any and .

The model (5) does not require that the change points in and are aligned, or that . Our goal is to estimate the total number and locations of the change points for both of the piecewise stationary latent processes. Importantly, we allow (resp. ) to be dependent across through sharing the innovations (resp. ). This makes our model considerably more general than those found in the literature on (high-dimensional) data segmentation under VAR models (Wang et al.,, 2019; Safikhani and Shojaie,, 2022; Bai et al.,, 2022) which assume independence across the segments. Data segmentation under factor models has been considered by Barigozzi et al., (2018) and Li et al., (2022) but they adopt a static approach to factor modelling.

2.3 Assumptions

We introduce assumptions that ensure the (asymptotic) identifiability of the two latent processes in (5) which are framed in terms of spectral properties, as well as controlling the degree of dependence in the data. Denote by the ACV matrix of at lag , and its spectral density matrix at frequency by with . Then, , denote the real, positive eigenvalues of ordered by decreasing size. We similarly define , and for .

Assumption 2.1.

For each , the following holds: There exist a positive integer , pairs of functions and for and , and satisfying such that for all ,

If for all as frequently assumed in the literature (Fan et al.,, 2013; Forni et al.,, 2015), we are in the presence of factors which are equally pervasive for the whole cross-sections of . If for some , we permit the presence of ‘weak’ factors. Since our primary interest lies in change point analysis, we later introduce a related but distinct condition on the size of change in in Assumption 4.2.

Assumption 2.2.

-

(i)

for all and .

-

(ii)

for some constants .

-

(iii)

Consider the Wold decomposition where . Then, there exist constants and such that we have , satisfying with which for all .

-

(iv)

for some fixed constant .

Assumption 2.3.

There exist constants and such that for all ,

Assumption 2.2 (i)–(ii) are standard conditions in the literature (Lütkepohl,, 2005; Basu and Michailidis,, 2015). Under condition (iii) and Assumption 2.3, we have time-varying serial dependence in (across all segments) decay at an algebraic rate according to the functional dependence measure of Zhang and Wu, (2021), which is required for controlling the error in locally estimating spectral density and ACV matrices of . Assumption 2.2 (iii) allows for mild cross-correlations in while ensuring that is uniformly bounded:

Proposition 2.1.

Under Assumption 2.2, uniformly over all , there exists some depending only on , and such that .

Remark 2.1.

Proposition 2.1, together with Assumption 2.2 (iv), establishes the boundedness of the eigenvalues of , which is commonly assumed in the high-dimensional VAR literature for the consistency of Lasso estimators. Assumption 2.2 (iv) holds if there exists some constant satisfying (Basu and Michailidis,, 2015). When , we have such that if , Assumption 2.2 (iii) is readily satisfied with .

3 Methodology

3.1 Stage 1: Factor-driven component segmentation

3.1.1 Change point detection

The spectral density matrix of is given by for , i.e. it varies over time in a piecewise constant manner with change points at . By Weyl’s inequality, Assumption 2.1 and Proposition 2.1 jointly indicate a gap in the eigenvalues of (time-varying) spectral density matrix of , i.e. those attributed to the factor-driven component diverges with while the remaining ones are bounded for all . This suggests an approach that looks for changes in from the behaviour of in the frequency domain which we further justify below.

Example 3.1.

Suppose that contains a single change point at at which a new factor is introduced, i.e. and with , which leads to . Then, from the uncorrelatedness between and and Proposition 2.1, the time-varying spectral density of , , satisfies . That is, the change in the spectral density of is detectable as a change in time-varying spectral density matrix of in operator norm, with the size of change diverging with as does so under Assumption 2.1.

Thus, we detect changes in by scanning for any large change in the spectral density matrix of measured in operator norm, and propose the following moving window-based approach. Given a bandwidth , we estimate the local spectral density matrix of by

| (6) |

where denotes the Bartlett kernel, the kernel bandwidth with , and

| (7) |

Then the following statistic

| (8) |

serves as a good proxy of the difference in local spectral density matrices of over and . To make it more precise, let denote a weighted average with weights corresponding to the proportion of , belonging to (see (F.1)). Then, , as a function of , linearly increases and then decreases around the change points with a peak of size formed at for all , provided that the bandwidth is not too large (in the sense of Assumption 4.2 (ii) below). The detector statistic is designed to approximate when is not directly observed, and thus is well-suited to detect and locate the change points therein. Unlike other methods for detecting changes in the factor structure (e.g. Li et al.,, 2022), we do not require the number of factors, either for each segment or for the whole dataset, as an input for the construction of .

Once is evaluated at the Fourier frequencies , we adapt the maximum-check of Eichinger and Kirch, (2018) for simultaneous detection of the multiple change points. Taking the pointwise maximum over the frequencies at each given location , we check if exceeds some threshold where denotes the frequency at which is maximised, i.e. . If so, it provides evidence that a change point is located near the time point , but some care is needed to avoid detecting duplicate estimators, since the detector statistic is expected to take a large value over an interval containing . Therefore, denoting by the set containing all time points at which , we regard as a change point estimator if it is a local maximiser of within an interval of radius centred at with some , i.e. . Once is added to the set of final estimators, say , in order to avoid the risk of duplicate estimators, we remove the interval of radius centred at from , and repeat the same procedure with the maximiser of at time points remaining in until the set is empty. Algorithm 1 in Appendix C outlines the steps of Stage 1 of FVARseg.

3.1.2 Post-segmentation factor adjustment

Following the detection of change points in , we are able to estimate the segment-specific quantities related to . In view of the second-stage of FVARseg detecting change points in , we describe how to estimate with which we can estimate the ACV of .

For each , we first estimate the spectral density of over the segment by as in (6) using the sample ACV computed from the segment (we use the same kernel bandwidth for simplicity). Then noting that the spectral density matrix of is of rank under (5), we estimate it from the eigendecomposition of by retaining only the largest eigenvalues, say , and the associated eigenvectors , and then estimate the ACV of by inverse Fourier transform, i.e.

| (9) |

The estimators in (9) require the factor number as an input. We refer to Hallin and Liška, (2007) for an information criterion (IC)-based estimator of that make use of the postulated eigengap in the spectral density matrix of .

3.2 Stage 2: Piecewise VAR process segmentation

Applying the existing VAR segmentation methods in our setting requires estimating the elements of the latent piecewise stationary VAR process , which introduces additional errors and possibly results in the loss of statistical efficiency. In addition, as discussed in Appendix A.2, the existing methods tend to be computationally demanding, e.g. by evaluating the Lasso estimators times in a dynamic programming algorithm, or solving a large fused Lasso objective function of dimension . Instead, since we can estimate the local AVC of from the post-segmentation factor-adjustment in Stage 1, our proposed methodology for segmenting the latent VAR component avoids estimating directly. Also, as described below, the proposed method evaluates the local VAR parameters at carefully selected locations only, and thus is computationally efficient.

Specifically, our approach makes use of the Yule-Walker equation (Lütkepohl,, 2005). Let contain all VAR parameters in the th segment. Then, it is related to the ACV matrices as , where

| (10) |

with being invertible due to Assumption 2.2 (iv). We propose to utilise this estimating equation in combination with the local ACV estimators of obtained as described below.

For a given bandwidth and the interval , we estimate the ACV of for , by . Here, is defined in (7) and is a weighted average of , the estimators of ACV of in (9), with the weights given by the proportion of covered by the th segment (see (F.16) for the precise definition). Replacing with , we obtain estimating a weighted average of , and similarly . Then, we propose to scan with some inspection parameter and a matrix norm . We motivate this statistic by considering , its population counterpart. With appropriately chosen (see Assumption 4.4 (ii) below), if is far from all the change points in , i.e. , while it is tent-shaped near the change points with a local maximum at , provided that

| (11) |

For the inspection parameter, we adopt an -regularised Yule-Walker estimator of the VAR parameters first considered by Barigozzi et al., (2022) in stationary settings. At given , we solve the constrained -minimisation problem

| (12) |

with a tuning parameter . The -constraint in (12) naturally leads to the choice , resulting in the following detector statistic:

For good detection power, the condition in (11) suggests using an estimator of or in place of for detecting . Therefore, we propose to evaluate for , with updated sequentially at locations strategically selected as below.

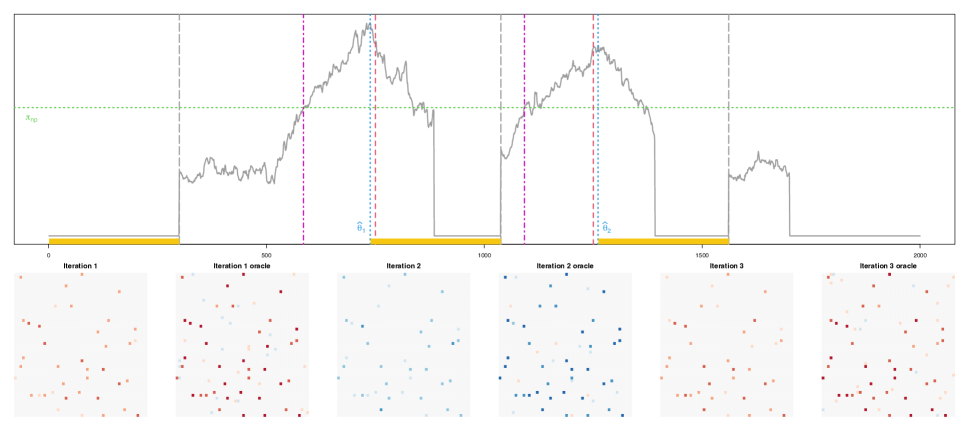

First we estimate by in (12) with and scan the data using . When exceeds some threshold, say , at for the first time, it signifies that a change has occurred in the neighbourhood. Reducing the search for a change point to , we identify a change point estimator as the local maximiser . Then updating with obtained at for some (i.e. only using an interval of length located strictly to the right of for its computation), we continue screening , until it next exceeds . These steps of screening and updating are repeated iteratively until the end of the data sequence is reached. Algorithm 2 in Appendix C outlines the steps of the Stage 2 methodology.

Figure 2 illustrates that although is latent, at each iteration, does as well as its oracle counterpart (obtained as in (12) with the sample ACV of replacing ). Computationally, this strategy benefits from that the costly solution to the -minimisation problem in (12) is required (at most) times with an appropriately chosen threshold (see Theorem 4.3 below). We further demonstrate numerically the competitiveness of Stage 2 as a standalone method for VAR time series segmentation in Section 5.2, and provide an in-depth comparative study with the existing methods in Appendix A.2.

4 Theoretical properties

4.1 Consistency of Stage 1 of FVARseg

We carry out our theoretical investigation under two different regimes with respect to the tail behaviour of and ; in particular, the weaker condition in Assumption 4.1 (i) permits heavy-tailed innovations, while the existing literature on (piecewise stationary) VAR modelling in high dimensions, commonly adopts the Gaussianity as in (ii).

Assumption 4.1.

We assume either of the following conditions.

-

(i)

There exists such that .

-

(ii)

and .

In establishing the consistency of Stage 1, we opt to measure the size of changes in using , , the difference in spectral density matrices of from neighbouring segments. As is Hermitian, we can always find the th largest (in modulus), real-valued eigenvalue of which we denote by , with . Recall that for some , denotes the bandwidth used in local spectral density estimation, see (6).

Assumption 4.2.

-

(i)

For each , the following holds: There exist a positive integer and pairs of functions and for and , and and satisfying , such that

for all . Besides, we assume that the functions are Lipschitz continuous with bounded Lipschitz constants. Then for , we have , where

(15) -

(ii)

The bandwidth satisfies as while fulfilling

(16)

Assumption 4.2 specifies the detection lower bound which is determined by and (through ), for all change points to be detectable by Stage 1. Condition (i) requires to be distinct from the rest. In fact, the remaining , are allowed to be exactly zero, which is the case in Example 3.1; here, we have where is a -variate vector of factor loading filters. The rate represents the bias-variance trade-off when estimating the local spectral density matrix of by (see Proposition F.6). It is possible to find the rate of kernel bandwidth that minimises this rate depending on the tail behaviour of (e.g. under Gaussianity), but we choose to explicitly highlight the role of this tuning parameter on our results.

Theorem 4.1.

Remark 4.1.

-

(i)

In Theorem 4.1 (b), reflects the difficulty associated with estimating the individual change point manifested by . In the Gaussian case (Assumption 4.1 (ii)), the localisation rate is always sharper than due to Assumption 4.2 (i). Considering the problem of covariance change point detection in independent, sub-Gaussian random vectors in high dimensions, Wang et al., (2021) derive the minimax lower bound on the localisation rate in their Lemma 3.2, and matches this rate up to ; here, the dependence on the kernel bandwidth is attributed to that we consider a time series segmentation problem, i.e. a change may occur in the ACV of at lags other than zero. If heavier tails are permitted (Assumption 4.1 (i)), can be tighter than , e.g. when , is fixed and for some .

- (ii)

Next, we establish the consistency of in (9) estimating the segment-specific ACV of under the following assumption on the strength of factors.

Assumption 4.3.

Assumption 2.1 holds with for all and .

Theorem 4.2.

It is possible to work under the weaker Assumption 2.1 and trace the effect of weak factors or bound estimation errors measured in different norms. Corollary C.16 of Barigozzi et al., (2022) derives such results in the stationary setting, where an additional multiplicative factor of appears in the -bound in Theorem (4.2). We work under the stronger Assumption 4.3 as it simplifies the presentation of Theorem 4.2 which plays an important role in the investigation into Stage 2 of FVARseg, and since only Assumption 4.3 is compatible with the cross-sectional ordering often being completely arbitrary.

4.2 Consistency of Stage 2 of FVARseg

Suppose that the tuning parameter for the -regularised Yule-Walker estimation problem in (12), is set with some constant and and defined in Theorem 4.2, as

| (20) |

This choice reflects the error in estimating the local ACV of over all and .

The following assumption imposes conditions on the size of the changes in VAR parameters and the minimum spacing between the change points.

Assumption 4.4.

-

(i)

For each , let . Then,

-

(ii)

The bandwidth fulfils (16), i.e. .

Remark 4.2.

We choose to measure the size of change using . From Assumption 2.2 (iv), we have iff . In the related literature, the -norm scaled by the global sparsity (given by the union of the supports of all ), is used to measure the size of change where this global sparsity may be much greater than that of when is large, see Appedix A.2. In some instances, we have , e.g. when and such that Assumption 4.4 (i) becomes . More generally, bounding implicitly assumes (approximate) sparsity on the second-order structure of . When , we have such that the boundedness of and follows when and are block diagonal with fixed block size (Wang and Tsay,, 2022). For general , we have bounded if are strictly diagonally dominant (see Definition 6.1.9 of Horn and Johnson, (1985) and Han et al., (2015)), which is met e.g. when are diagonal with their diagonal entries fulfilling (where ); this trivially holds when .

Theorem 4.3.

Suppose that Assumption 4.4 holds in addition to the assumptions made in Theorem 4.2. With chosen as in (20), we set to satisfy

Then, there exists a set with as , such that the following holds for returned by Stage 2 of FVARseg, on for large enough :

-

(a)

and for some with .

-

(b)

There exists a constant such that for all satisfying , we have , where

Due to the sequential nature of FVARseg, the success of Stage 2 is conditional on that of Stage 1 which occurs on an asymptotic one-set, see Theorem 4.1. Theorem 4.3 (a) establishes that Stage 2 of FVARseg consistently detects all change points within the distance of where can be made arbitrarily small as under Assumption 4.4 (i). Theorem 4.3 (b) shows that a further refined localisation rate can be derived for when it is sufficiently distanced away from the change points in the factor-driven component. If, say, lies close to , a change point in , the error from estimating the local ACV of due to the bias in , prevents applying the arguments involved in the refinement to such . The refined rate is always tighter than under Gaussianity.

It is of independent interest to consider the cases where is stationary (i.e. ) or where we directly observe the piecewise stationary VAR process (i.e. ). Consistency of the Stage 2 of FVARseg readily extends to such settings and the improved localisation rates in Theorem 4.3 (b) apply to all the estimators. Also, further improvement is attained in the heavy-tailed situations (Assumption 4.1 (i)) if is directly observable. For the full statement of the results, we refer to Corollary A.1 in Appendix A where we also provide a detailed comparison between Stage 2 of FVARseg and existing VAR segmentation methods (that do not take into the possible presence of factors), both theoretically and numerically.

5 Empirical results

5.1 Numerical considerations

Multiscale extension.

The bandwidth is required to be large enough to provide a good local estimators of spectral density of (Stage 1) and VAR parameters (Stage 2). However, if is too large, we may have windows that contain two or more changes when scanning the data for change points, which violates Assumptions 4.2 (ii) and 4.4 (ii). Cho and Kirch, (2022) note the lack of adaptivity of a single-bandwidth moving window procedure in the presence of multiscale change points (a mixture of large changes over short intervals and smaller changes over long intervals), and advocates the use of multiple bandwidths. Accordingly we also propose to apply FVARseg with a range of bandwidths and prune down the outputs using a ‘bottom-up’ method (Messer et al.,, 2014; Meier et al.,, 2021). Let denote the output from Stage 1 or 2 with a bandwidth . Given a set of bandwidths , we accept all estimators from the finest to the set of final estimators and sequentially for , accept iff . In simulation studies, we use for Stage 1, and generated as an equispaced sequence between and of length for Stage 2. The choice of is motivated by the simulation results of Barigozzi et al., (2022) under the stationarity, where the -regularised estimator in (12) was observed to performs well when the sample size exceeds .

Speeding up Stage 1.

The computational bottleneck of FVARseg is the computation of in Stage 1, which involves singular value decomposition (SVD) of a -matrix at multiple frequencies and over time. We propose to evaluate on a grid with . This may incur additional bias of at most in change point location estimation which is asymptotically negligible in view of Theorem 4.1, but reduce the computational load by the factor of .

Selection of thresholds.

The theoretically permitted ranges of and (see Theorems 4.1 and 4.3) depend on constants which are not accessible or difficult to estimate in practice. This is an issue commonly encountered by data segmentation methods which involve localised testing, and often a reasonable solution is found by large-scale simulations, an approach we also take. We use simulations to derive a simple rule for selecting the threshold as a function of , and . For this, we (i) propose a scaling for each of the two detector statistics adopted in Stages 1 and 2 which reduces its dependence on the data generating process, and (ii) fit a linear model for an appropriate percentile of the scaled detector statistics obtained from simulated datasets. Specifically, we simulate time series following (5) with using the models considered in Section 5.2, and record the maximum of the scaled detector statistics and over on each realisation. Here, the scaling terms are obtained from the first observations only, as

Generating the data with varying and repeating the above procedure with multple choices of , we fit a linear model to the th percentile of with and as regressors (), and use the fitted model to derive a threshold for given and that is then applied to the similarly scaled . Analogously, we regress the th percentile of onto , and (), and find a threshold applied to the scaled given , and from the fitted model. The choice of the regressors is motivated by the definitions of and which appear in Theorems 4.1 and 4.3. The high values of indicate the excellent fit of the linear models and consequently, that the threshold selection rule is insensitive to the data generating processes. When Stage 2 is used as a standalone method for segmenting observed VAR processes, a smaller threshold is recommended which is in line with Corollary A.1, and we find that works well with the proposed scaling.

Other tuning parameters.

While data-adaptive methods exist for selecting the kernel window size in (6) (Politis,, 2003), we find that setting it simply at for given , works well for the purpose of data segmentation. The results are not highly sensitive to the choice of in Stage 1 and use throughout. In Stage 2, we find that not trimming off the data when estimating the VAR parameters by setting , does not hurt the numerical performance. In factor-adjustment, we select the segment-specific factor number using the IC-based approach of Hallin and Liška, (2007). Krampe and Margaritella, (2021) propose to jointly select the (static) factor number and the VAR order using an IC but generally, the validity of IC is not well-understood for VAR order selection in high dimensions. In our simulations, following the practice in the literature on VAR segmentation, we regard as known but also investigate the sensitivity of FVARseg when is mis-specified. In analysing the panel of daily volatilities (Section 5.3), we use which has the interpretation of the number of trading days per week. Finally, we select in (12) via cross validation as in Barigozzi et al., (2022).

5.2 Simulation studies

In the simulations, we consider the cases when the factor-driven component is present () and when it is not (). For the former, we consider two models for generating with . In the first model, referred to as (C1), admits a static factor model representation while in the second model (C2), it does not; empirically, the task of factor structure estimation is observed to be more challenging under (C2) (Forni et al.,, 2017; Barigozzi et al.,, 2022). We generate as piecewise stationary Gaussian VAR() processes with and a parameter that controls the size of the change (with smaller indicating the smaller change). We refer to Appendix B.1 for the full descriptions of simulation models and Table 1 for an overview of the data generating processes which also contains information about the sets of change points and ; under each setting, we generate realisations. Below we provide a summary of the findings from the simulation studies, and Tables B.1–B.2 reporting the results can be found in Appendix B.2.

To the best of our knowledge, there does not exist a methodology that comprehensively addresses the change point problem under the model (5). Therefore under (M1)–(M2), we compare the Stage 1 of FVARseg with a method proposed in Barigozzi et al., (2018), referred to as BCF hereafter, on their performance at detecting changes in . While BCF has a step for detecting change points in the remainder component, it does so nonparametically unlike the Stage 2 of FVARseg, which may lead to unfair comparison. Hence we separately consider (M3) with where we compare the Stage 2 method with VARDetect (Safikhani et al.,, 2022), a block-wise variant of Safikhani and Shojaie, (2022).

Results under (M1)–(M2).

Overall, FVARseg achieves good accuracy in estimating the total number and locations of the change points for both and across different data generating processes. Under (M1) adopting the static factor model for generating , FVARseg shows similar performance as BCF in detecting when the dimension is small (), but the latter tends to over-estimate the number of change points as increases. Also, FVARseg outperforms the binary segmentation-based BCF in change point localisation. BCF requires as an input the upper bound on the number of global factors, say , that includes the ones attributed to the change points, and its performance is sensitive to its choice. In (M1), we have (which is supplied to BCF) while in (M2), does not admit a static factor representation and accordingly such does not exist (we set for BCF). Accordingly, BCF tends to under-estimate the number of change points under (M2). Generally, the task of detecting change points in is aggravated by the presence of change points in due to the sequential nature of FVARseg, and the Stage 2 performs better when both in terms of detection and localisation accuracy, which agrees with the observations made in Corollary A.1 (a).

Between (M1) and (M2), the latter poses a more challenging setting for the Stage 2 methodology. This may be attributed to (i) the difficulty posed by the data generating scenario (C2), which is observed to make the estimation tasks related to the latent VAR process more difficult (Barigozzi et al.,, 2022), and (ii) that where the estimation bias from Stage 1 has a worse effect on the performance of Stage 2 compared to when and do not overlap, see the discussion below Theorem 4.3.

Results under (M3).

Table B.2 shows that the Stage 2 of FVARseg outperforms VARDetect in all criteria considered, particularly as increases. VARDetect struggles to detect any change point when the change is weak (recall that is used when which makes the size of change at small) or when . FVARseg is faster than VARDetect in most situations except for when , sometimes more than times e.g. when and there is no change point in the data. Additionally, Stage 2 of FVARseg is insensitive to the over-specification of the VAR order ( is used when in fact ). When it is under-specified, there is slight loss of detection power as expected. Compared to the results obtained under (M1)–(M2), the localisation performance of the Stage 2 method improves in the absence of the factor-driven component, even though the size of changes under (M3) tends to be smaller. This confirms the theoretical findings reported in Corollary A.1 (b) in Appendix A. Although not reported here, when the full FVARseg methodology is applied to the data generated under (M3), the Stage 1 method does not detect any spurious change point estimators as desired.

5.3 Application: US blue chip data

We consider daily stock prices from US blue chip companies across industry sectors between January 3, 2000 and February 16, 2022 ( days), retrieved from the Wharton Research Data Services; the list of companies and their corresponding sectors can be found in Appendix E. Following Diebold and Yılmaz, (2014), we measure the volatility using where (resp. ) denotes the maximum (resp. minimum) log-price of stock on day , and set .

We apply FVARseg to detect change points in the panel of volatility measures . With denoting the number of trading days per year, we apply Stage 1 with bandwidths chosen as an equispaced sequence between and of length , implicitly setting the minimum distance between two neighbouring change points to be three months. Based on the empirical sample size requirement for VAR parameter estimation (see Section 5.1), we apply Stage 2 with bandwidths chosen as an equispaced sequence between and of length . The VAR order is set at which corresponds to the number of trading days in each week, and the rest of the tuning parameters are selected as in Section 5.1. Table 2 reports the segmentation results.

| returned by Stage 1 | returned by Stage 2 | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| 2002-06-06 | 2007-12-10 | 2008-09-12 | 2008-12-16 | 2002-02-04 | 2003-03-18 | 2003-11-25 | 2006-06-07 | 2008-03-17 | 2009-07-07 |

| 2009-05-11 | 2020-02-18 | 2020-05-20 | 2011-07-28 | 2013-05-30 | 2015-06-25 | 2017-10-03 | 2020-02-27 | ||

Stage 1 detects four change points around the Great Financial Crisis between 2007 and 2009, and the last two estimators from Stage 1 correspond to the onset (2020-02-20) and the end (2020-04-07) of the stock market crash brought in by the instability due to the COVID-19 pandemic. Given the clustering of change points between 2007 and 2009, an alternative approach is to adopt a locally stationary factor model as in Barigozzi et al., (2021). However, such a model does not allow for the number of factors to vary over time, whereas we observe the contrary to be the case when applying the IC-based method of Hallin and Liška, (2007) to each segment defined by , see Table 3. This supports that it is more appropriate to model the changes in the factor-driven component of this dataset as abrupt changes rather than as smooth transitions.

| Segment | 0 | 1 | 2 | 3 | 4 | 5 | 6 | 7 |

| 3 | 4 | 2 | 7 | 2 | 5 | 1 | 2 |

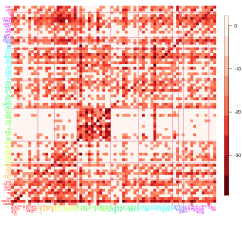

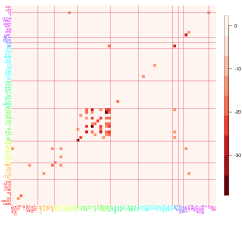

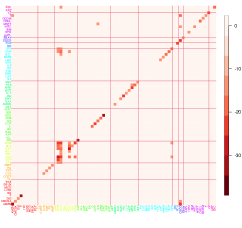

The estimators from Stage 2 are spread across the period in consideration. Figure 1 (c)–(f) illustrate how the linkages between different companies vary over the four segments identified between and particularly at the level of industrial sectors, although this information is not used by FVARseg.

| Forecasting method | Mean | SE | Mean | SE | |

|---|---|---|---|---|---|

| (F1) | Restricted | 0.7671 | 0.3729 | 0.9181 | 0.1898 |

| Unrestricted | 0.7746 | 0.4123 | 0.9204 | 0.2007 | |

| (F2) | Restricted | 0.7831 | 0.4011 | 0.9217 | 0.1962 |

| Unrestricted | 0.8138 | 0.4666 | 0.9279 | 0.2008 | |

To further validate the segmentation obtained by FVARseg, we perform a forecasting exercise. Two approaches, referred to as (F1) and (F2) below, are adopted to build forecasting models where the difference lies in how a sub-sample of , is chosen to forecast . Simply put, (F1) uses the observations belonging to the same segment as only, for constructing the forecast of (resp. ) according to the segmentation defined by (resp. ), while (F2) ignores the presence of the most recent change point estimator. We expect (F1) to give more accurate predictions if the data undergoes structural changes at the detected change points. On the other hand, if some of the change point estimators are spurious, (F2) is expected to produce better forecasts since it makes use of more observations. We select , the set of time points at which to perform forecasting, such that each does not belong to the first two segments (i.e. ), and there are at least of observations to build a forecast model separately for and , respectively. Denoting by the index of nearest to and strictly left of and similarly defining , this means that and for all . We have . For such , we obtain for some , where denotes an estimator of the best linear predictor of given , and is defined analogously. The difference between the two approaches we take lies in the selection of .

-

(F1)

We set and .

-

(F2)

We set and .

Barigozzi et al., (2022) propose two methods for estimating the best linear predictors of and under a stationary factor-adjusted VAR model, one based on a more restrictive assumption on the factor structure (‘restricted’) than the other (‘unrestricted’); we refer to the paper for their detailed descriptions. Both estimators are combined with the two approaches (F1) and (F2). Table 4 reports the summary of the forecasting errors measured as and , obtained from combining different best linear predictors with (F1)–(F2). According to all evaluation criteria, (F1) produces forecasts that are more accurate than (F2) regardless of the forecasting methods, which supports the validity of the change point estimators returned by FVARseg.

References

- Bai, (2003) Bai, J. (2003). Inferential theory for factor models of large dimensions. Econometrica, 71:135–171.

- Bai et al., (2021) Bai, P., Bai, Y., Safikhani, A., and Michailidis, G. (2021). Multiple change point detection in structured VAR models: the VARDetect R Package. arXiv preprint arXiv:2105.11007.

- Bai et al., (2020) Bai, P., Safikhani, A., and Michailidis, G. (2020). Multiple change points detection in low rank and sparse high dimensional vector autoregressive models. IEEE Trans. Signal Process., 68:3074–3089.

- Bai et al., (2022) Bai, P., Safikhani, A., and Michailidis, G. (2022). Multiple change point detection in reduced rank high dimensional vector autoregressive models. J. Amer. Statist. Assoc. (to appear).

- Barigozzi and Cho, (2020) Barigozzi, M. and Cho, H. (2020). Consistent estimation of high-dimensional factor models when the factor number is over-estimated. Electron. J. Stat., 14:2892–2921.

- Barigozzi et al., (2018) Barigozzi, M., Cho, H., and Fryzlewicz, P. (2018). Simultaneous multiple change-point and factor analysis for high-dimensional time series. J. Econometrics, 206:187–225.

- Barigozzi et al., (2022) Barigozzi, M., Cho, H., and Owens, D. (2022). FNETS: Factor-adjusted network estimation and forecasting for high-dimensional time series. arXiv preprint arXiv:2201.06110.

- Barigozzi and Hallin, (2017) Barigozzi, M. and Hallin, M. (2017). A network analysis of the volatility of high dimensional financial series. J. Roy. Statist. Soc. Ser. C, 66:581–605.

- Barigozzi et al., (2021) Barigozzi, M., Hallin, M., Soccorsi, S., and von Sachs, R. (2021). Time-varying general dynamic factor models and the measurement of financial connectedness. J. Econometrics, 222:324–343.

- Basu et al., (2019) Basu, S., Li, X., and Michailidis, G. (2019). Low rank and structured modeling of high-dimensional vector autoregressions. IEEE Trans. Signal Process., 67:1207–1222.

- Basu and Michailidis, (2015) Basu, S. and Michailidis, G. (2015). Regularized estimation in sparse high-dimensional time series models. Ann. Statist, 43:1535–1567.

- Cai et al., (2011) Cai, T., Liu, W., and Luo, X. (2011). A constrained minimization approach to sparse precision matrix estimation. J. Amer. Statist. Assoc., 106:594–607.

- Chen et al., (2021) Chen, L., Wang, W., and Wu, W. B. (2021). Inference of breakpoints in high-dimensional time series. J. Amer. Statist. Assoc. (to appear).

- Cho and Kirch, (2022) Cho, H. and Kirch, C. (2022). Two-stage data segmentation permitting multiscale change points, heavy tails and dependence. Ann. Inst. Stat. Math., 74(4):653–684.

- Cule et al., (2011) Cule, E., Vineis, P., and De Iorio, M. (2011). Significance testing in ridge regression for genetic data. BMC Bioinform., 12(1):1–15.

- Diebold and Yılmaz, (2014) Diebold, F. X. and Yılmaz, K. (2014). On the network topology of variance decompositions: Measuring the connectedness of financial firms. J. Econometrics, 182:119–134.

- Eichinger and Kirch, (2018) Eichinger, B. and Kirch, C. (2018). A MOSUM procedure for the estimation of multiple random change points. Bernoulli, 24:526–564.

- Fan et al., (2020) Fan, J., Ke, Y., and Wang, K. (2020). Factor-adjusted regularized model selection. J. Econometrics, 216:71–85.

- Fan et al., (2013) Fan, J., Liao, Y., and Mincheva, M. (2013). Large covariance estimation by thresholding principal orthogonal complements. J. R. Stat. Soc. Ser. B Stat. Methodol., 75(4):603–680.

- Fan et al., (2021) Fan, J., Masini, R., and Medeiros, M. C. (2021). Bridging factor and sparse models. arXiv preprint arXiv:2102.11341.

- Forni et al., (2009) Forni, M., Giannone, D., Lippi, M., and Reichlin, L. (2009). Opening the black box: Structural factor models with large cross sections. Econometric Theory, 25:1319–1347.

- Forni et al., (2000) Forni, M., Hallin, M., Lippi, M., and Reichlin, L. (2000). The Generalized Dynamic Factor Model: identification and estimation. Rev. Econ. Stat., 82:540–554.

- Forni et al., (2015) Forni, M., Hallin, M., Lippi, M., and Zaffaroni, P. (2015). Dynamic factor models with infinite-dimensional factor spaces: One-sided representations. J. Econometrics, 185:359–371.

- Forni et al., (2017) Forni, M., Hallin, M., Lippi, M., and Zaffaroni, P. (2017). Dynamic factor models with infinite-dimensional factor space: Asymptotic analysis. J. Econometrics, 199:74–92.

- Forni and Lippi, (2001) Forni, M. and Lippi, M. (2001). The Generalized Dynamic Factor Model: Representation theory. Econometric Theory, 17:1113–1141.

- Giannone et al., (2021) Giannone, D., Lenza, M., and Primiceri, G. E. (2021). Economic predictions with big data: The illusion of sparsity. ECB Working Paper 2542, European Central Bank.

- Hallin et al., (2018) Hallin, M., Hörmann, S., and Lippi, M. (2018). Optimal dimension reduction for high-dimensional and functional time series. Stat. Inference Stoch. Process., 21:385–398.

- Hallin and Liška, (2007) Hallin, M. and Liška, R. (2007). Determining the number of factors in the general dynamic factor model. J. Amer. Statist. Assoc., 102:603–617.

- Han et al., (2015) Han, F., Lu, H., and Liu, H. (2015). A direct estimation of high dimensional stationary vector autoregressions. J. Mach. Learn. Res., 16:3115–3150.

- Horn and Johnson, (1985) Horn, R. A. and Johnson, C. R. (1985). Matrix Analysis. Cambridge University Press.

- Kirch et al., (2015) Kirch, C., Muhsal, B., and Ombao, H. (2015). Detection of changes in multivariate time series with application to EEG data. J. Amer. Statist. Assoc., 110:1197–1216.

- Krampe and Margaritella, (2021) Krampe, J. and Margaritella, L. (2021). Dynamic factor models with sparse VAR idiosyncratic components. arXiv preprint arXiv:2112.07149.

- Li et al., (2022) Li, Y.-N., Li, D., and Fryzlewicz, P. (2022). Detection of multiple structural breaks in large covariance matrices. J. Bus. Econom. Statist. (to appear).

- Lütkepohl, (2005) Lütkepohl, H. (2005). New Introduction to Multiple Time Series Analysis. Springer Science & Business Media.

- Maeng et al., (2022) Maeng, H., Eckley, I., and Fearnhead, P. (2022). Collective anomaly detection in High-dimensional VAR Models. Statist. Sinica (to appear).

- Meier et al., (2021) Meier, A., Kirch, C., and Cho, H. (2021). mosum: A package for moving sums in change-point analysis. J. Stat. Softw., 97:1–42.

- Messer et al., (2014) Messer, M., Kirchner, M., Schiemann, J., Roeper, J., Neininger, R., and Schneider, G. (2014). A multiple filter test for the detection of rate changes in renewal processes with varying variance. Ann. Appl. Stat., 8:2027–2067.

- Michailidis and d’Alché Buc, (2013) Michailidis, G. and d’Alché Buc, F. (2013). Autoregressive models for gene regulatory network inference: Sparsity, stability and causality issues. Math. Biosci., 246:326–334.

- Politis, (2003) Politis, D. N. (2003). Adaptive bandwidth choice. J. Nonparametr. Stat., 15:517–533.

- Preuss et al., (2015) Preuss, P., Puchstein, R., and Dette, H. (2015). Detection of multiple structural breaks in multivariate time series. J. Amer. Statist. Assoc., 110:654–668.

- Safikhani et al., (2022) Safikhani, A., Bai, Y., and Michailidis, G. (2022). Fast and scalable algorithm for detection of structural breaks in big VAR models. J. Comput. Graph. Statist., 31:176–189.

- Safikhani and Shojaie, (2022) Safikhani, A. and Shojaie, A. (2022). Joint structural break detection and parameter estimation in high-dimensional nonstationary VAR models. J. Amer. Statist. Assoc., 117:251–264.

- Shojaie and Michailidis, (2010) Shojaie, A. and Michailidis, G. (2010). Discovering graphical granger causality using the truncating lasso penalty. Bioinformatics, 26:i517–i523.

- Stock and Watson, (2002) Stock, J. H. and Watson, M. W. (2002). Forecasting using principal components from a large number of predictors. J. Amer. Statist. Assoc., 97:1167–1179.

- Wang and Tsay, (2022) Wang, D. and Tsay, R. S. (2022). Rate-optimal robust estimation of high-dimensional vector autoregressive models. arXiv preprint arXiv:2107.11002.

- Wang et al., (2021) Wang, D., Yu, Y., and Rinaldo, A. (2021). Optimal covariance change point localization in high dimensions. Bernoulli, 27:554–575.

- Wang et al., (2019) Wang, D., Yu, Y., Rinaldo, A., and Willett, R. (2019). Localizing changes in high-dimensional vector autoregressive processes. arXiv preprint arXiv:1909.06359.

- Wu, (2005) Wu, W. B. (2005). Nonlinear system theory: Another look at dependence. Proceedings of the National Academy of Sciences, 102:14150–14154.

- Yu et al., (2015) Yu, Y., Wang, T., and Samworth, R. J. (2015). A useful variant of the Davis–Kahan theorem for statisticians. Biometrika, 102:315–323.

- Zhang and Wu, (2021) Zhang, D. and Wu, W. B. (2021). Convergence of covariance and spectral density estimates for high-dimensional locally stationary processes. Ann. Statist, 49:233–254.

Appendix A Further discussions on Stage 2 of FVARseg

A.1 Extension of Theorem 4.3

We consider the performance of the Stage 2 of FVARseg when applied to some special cases under the model (5) where (a) is stationary (i.e. ) and (b) we directly observe (i.e. ). Theorem 4.1 indicates that in both cases, the Stage 1 of FVARseg returns . The results reported in Theorem 4.3 readily extend to such settings.

Corollary A.1.

Suppose that the assumptions of Theorem 4.3 hold, including Assumption 4.4 (i) with specified below. Then, with defined as in Theorem 4.3, i.e.

there exist a set with as and constants such that on , we have

for large enough, in the following situations.

-

(a)

There is no change point in the factor-driven component, i.e. , and we set

-

(b)

We directly observe the piecewise stationary VAR process, i.e. for all , and we set with

(A.3)

When compared to the methods dedicated to the setting corresponding to Corollary A.1 (b), our Stage 2 methodology achieves comparative theoretical performance in terms of the detection lower bound imposed on the size of changes for their detection, and the rate of localisation achieved. We provide a comprehensive comparison of the Stage 2 methodology with the existing VAR segmentation methods in the next section, both on their theoretical and computational properties.

A.2 Comparison with the existing VAR segmentation methods

There are a few methods proposed for time series segmentation under piecewise stationary, Gaussian VAR models, a setting that corresponds to Corollary A.1 (b) under Gaussianity. In this setting, we compare the Stage 2 of FVARseg with those proposed by Wang et al., (2019) and Safikhani and Shojaie, (2022).

| Methods | Separation | Localisation | Complexity |

|---|---|---|---|

| Stage 2 of FVARseg | |||

| Wang et al., (2019) | |||

| Safikhani and Shojaie, (2022) | Not available |

Table A.1 summarises the comparative study in terms of their theoretical and computational properties. Denoting by the size of change between the th and the th segments (measured differently for different methods), the separation rate refers to some such that if , the corresponding method correctly detects all change points; for Stage 2, we set and for the others, (see the caption of Table A.1 for the definition of ). The localisation rate refers to some satisfying for the estimators returned by respective methods. For FVARseg, the weights reflect the difficulty associated with locating individual change points, i.e. , while for Wang et al., (2019) and Safikhani and Shojaie, (2022), the weights are global with and , respectively. Safikhani and Shojaie, (2022) further assume that is bounded away from zero. We suppose that , a sufficient condition for the boundedness of for each segment-specific VAR process (Basu and Michailidis,, 2015, Proposition 2.2), which is required by all the methods in consideration for their theoretical consistency.

Immediate comparison of the theoretical results is difficult due to different definitions of : Observe that

from Assumption 2.2 (iv), where denotes the element-wise -norm. Noting that , the requirement of Stage 2 of FVARseg may be stronger than that made in Wang et al., (2019) if . On the other hand, we can have much greater than if is large or when the sparsity pattern of varies greatly from one segment to another. The method proposed by Safikhani and Shojaie, (2022) is generally worse than the other two both in terms of separation and localisation rates.

The -regularised Yule-Walker estimation problem in (12) can be solved in parallel and further, it needs to be performed only times with large probability, which makes the Stage 2 methodology more attractive. By comparison, the dynamic programming methodology of Wang et al., (2019) requires the Lasso estimation to be performed times, and the multi-stage procedure of Safikhani and Shojaie, (2022) solves a fused Lasso problem of dimension to obtain pre-estimators of the change points, and then exhaustively searches for the final set of estimators which can be NP-hard in the worst case. In Section 5.2, we compare the Stage 2 methodology with a blockwise modification of Safikhani and Shojaie, (2022) that is implemented in the R package VARDetect (Bai et al.,, 2021).

Finally, we note that there are methods developed under piecewise stationary extensions of the low-rank plus sparse VAR() model proposed in Basu et al., (2019), see Bai et al., (2022). While they additionally permit a low rank structure in the parameter matrices, the spectrum of is assumed to be uniformly bounded which rules out pervasive (serial) correlations in the data and thus is distinguished from the piecewise stationary factor-adjusted VAR model considered in this paper.

Appendix B Further information on simulation studies

B.1 Data generating processes

We provide full details on how the data is generated for numerical experiments reported in Section 5.2. Firstly, the factor-driven component is generated according to the following two models.

-

(C1)

admits a static factor model representation, as

where with , and the MA coefficients are generated as for all and when . Then sequentially for , we draw with such that for all , when while when .

-

(C2)

does not admit a static factor model representation, as

where and the coefficients are drawn uniformly as with denoting a uniform distribution. The AR coefficients are generated as when and then sequentially for , we draw with such that for all , we have when and when .

For generating the piecewise stationary VAR() process , we consider , and . When , we generate , a directed Erdös-Rényi random graph on the vertex set with the link probability , set the entries of as if and otherwise, then rescale it such that . When , we rescale the thus-generated to have and similarly generate with . Then sequentially for , we set for and some .

B.2 Complete simulation results

Tables B.1 and B.2 report the complete results obtained for the simulation studies described in Section 5.2. In particular, Table B.1 compares the performance of FVARseg against BCF (Barigozzi et al.,, 2018) on datasets generated as in (M1)–(M2) of Table 1, and Table B.2 compares the Stage 2 methodology of FVARseg (i.e. Algorithm 2 applied with and ), against VARDetect (Safikhani and Shojaie,, 2022; Bai et al.,, 2021) on datasets generated under (M3) in Table 1. All tuning parameters are selected as described in Section 5.1.

Denoting by and the sets of estimated and true change points, respectively, we report the distributions of (with and ) and the (scaled) Hausdorff distance between and ,

| (B.1) |

averaged over realisations, as well as the average computation time (in seconds) in Table B.2.

| Method | 0 | 1 | 0 | 1 | |||||||||||

| (M1) | FVARseg | 0 | 0 | 100 | 0 | 0 | 0 | 0 | 98 | 2 | 0 | 0.000 | 0.018 | ||

| BCF | 0 | 0 | 95 | 5 | 0 | 0.007 | |||||||||

| FVARseg | 5 | 15 | 80 | 0 | 0 | 0 | 6 | 86 | 8 | 0 | 0.057 | 0.049 | |||

| BCF | 0 | 0 | 91 | 8 | 1 | 0.010 | |||||||||

| FVARseg | 0 | 0 | 100 | 0 | 0 | 0 | 0 | 100 | 0 | 0 | 0.000 | 0.018 | |||

| BCF | 0 | 0 | 95 | 4 | 1 | 0.012 | |||||||||

| FVARseg | 4 | 10 | 86 | 0 | 0 | 0 | 2 | 90 | 6 | 2 | 0.041 | 0.032 | |||

| BCF | 0 | 0 | 50 | 30 | 20 | 0.040 | |||||||||

| FVARseg | 0 | 0 | 100 | 0 | 0 | 0 | 0 | 100 | 0 | 0 | 0.000 | 0.018 | |||

| BCF | 0 | 0 | 92 | 7 | 1 | 0.011 | |||||||||

| FVARseg | 4 | 10 | 86 | 0 | 0 | 0 | 2 | 93 | 5 | 0 | 0.046 | 0.030 | |||

| BCF | 0 | 0 | 33 | 28 | 39 | 0.056 | |||||||||

| (M2) | FVARseg | 0 | 0 | 98 | 2 | 0 | 1 | 2 | 81 | 14 | 2 | 0.006 | 0.054 | ||

| BCF | 0 | 0 | 94 | 5 | 1 | 0.012 | |||||||||

| FVARseg | 0 | 0 | 99 | 1 | 0 | 7 | 20 | 57 | 12 | 4 | 0.006 | 0.141 | |||

| BCF | 0 | 1 | 91 | 8 | 0 | 0.013 | |||||||||

| FVARseg | 0 | 0 | 99 | 1 | 0 | 0 | 4 | 87 | 8 | 1 | 0.003 | 0.044 | |||

| BCF | 0 | 0 | 94 | 5 | 1 | 0.009 | |||||||||

| FVARseg | 0 | 0 | 99 | 1 | 0 | 3 | 10 | 67 | 20 | 0 | 0.004 | 0.101 | |||

| BCF | 0 | 0 | 90 | 10 | 0 | 0.013 | |||||||||

| FVARseg | 0 | 0 | 99 | 0 | 1 | 0 | 4 | 91 | 5 | 0 | 0.003 | 0.042 | |||

| BCF | 0 | 0 | 92 | 7 | 1 | 0.009 | |||||||||

| FVARseg | 0 | 0 | 100 | 0 | 0 | 3 | 9 | 78 | 9 | 1 | 0.005 | 0.086 | |||

| BCF | 0 | 0 | 91 | 8 | 1 | 0.011 | |||||||||

| Method | 0 | 1 | time | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

| 1 | FVARseg () | 0 | 0 | 99 | 1 | 0 | 0.001 | 11.14 | ||

| FVARseg () | 0 | 0 | 95 | 5 | 0 | 0.013 | 12.92 | |||

| VARDetect | 0 | 0 | 95 | 1 | 4 | 0.015 | 7.11 | |||

| FVARseg () | 0 | 0 | 98 | 2 | 0 | 0.012 | 20.20 | |||

| FVARseg () | 0 | 0 | 91 | 8 | 1 | 0.019 | 22.55 | |||

| VARDetect | 59 | 33 | 6 | 2 | 0 | 0.307 | 16.50 | |||

| FVARseg () | 0 | 0 | 100 | 0 | 0 | 0.00 | 26.98 | |||

| FVARseg () | 0 | 0 | 100 | 0 | 0 | 0.00 | 37.96 | |||

| VARDetect | 0 | 0 | 89 | 5 | 6 | 0.03 | 78.87 | |||

| FVARseg () | 0 | 1 | 98 | 1 | 0 | 0.013 | 47.71 | |||

| FVARseg () | 0 | 1 | 98 | 1 | 0 | 0.015 | 62.78 | |||

| VARDetect | 90 | 9 | 0 | 0 | 1 | 0.362 | 96.08 | |||

| FVARseg () | 0 | 0 | 100 | 0 | 0 | 0.00 | 55.82 | |||

| FVARseg () | 0 | 0 | 100 | 0 | 0 | 0.00 | 87.33 | |||

| VARDetect | 0 | 0 | 88 | 6 | 6 | 0.036 | 305.95 | |||

| FVARseg () | 0 | 1 | 98 | 1 | 0 | 0.014 | 98.96 | |||

| FVARseg () | 0 | 2 | 97 | 1 | 0 | 0.017 | 146.40 | |||

| VARDetect | 89 | 11 | 0 | 0 | 0 | 0.361 | 335.79 | |||

| 2 | FVARseg () | 0 | 0 | 82 | 18 | 0 | 0.054 | 13.52 | ||

| FVARseg () | 0 | 0 | 92 | 8 | 0 | 0.026 | 11.18 | |||

| VARDetect | 0 | 0 | 96 | 2 | 2 | 0.012 | 37.26 | |||

| FVARseg () | 0 | 4 | 88 | 8 | 0 | 0.031 | 20.90 | |||

| FVARseg () | 0 | 10 | 86 | 4 | 0 | 0.045 | 17.56 | |||

| VARDetect | 81 | 6 | 9 | 1 | 3 | 0.326 | 30.31 | |||

| FVARseg () | 0 | 0 | 98 | 2 | 0 | 0.008 | 37.96 | |||

| FVARseg () | 0 | 0 | 97 | 3 | 0 | 0.009 | 27.05 | |||

| VARDetect | 0 | 0 | 90 | 8 | 2 | 0.021 | 334.24 | |||

| FVARseg () | 0 | 12 | 87 | 1 | 0 | 0.044 | 57.77 | |||

| FVARseg () | 0 | 27 | 73 | 0 | 0 | 0.08 | 39.57 | |||

| VARDetect | 95 | 1 | 3 | 0 | 1 | 0.365 | 137.59 | |||

| FVARseg () | 0 | 0 | 97 | 3 | 0 | 0.01 | 89.06 | |||

| FVARseg () | 0 | 0 | 100 | 0 | 0 | 0.00 | 56.14 | |||

| VARDetect | 0 | 0 | 93 | 3 | 4 | 0.016 | 1063.33 | |||

| FVARseg () | 0 | 15 | 85 | 0 | 0 | 0.051 | 136.81 | |||

| FVARseg () | 1 | 28 | 71 | 0 | 0 | 0.085 | 86.51 | |||

| VARDetect | 97 | 1 | 0 | 0 | 2 | 0.371 | 389.86 | |||

Appendix C Pseudocodes for FVARseg

Appendix D Generalised dynamic factor model

D.1 GDFM as a representation

Forni and Lippi, (2001) show that the necessary and sufficient condition for any -dimensional, weakly stationary time series to admit the generalised dynamic factor model (GDFM) representation, is to have a finite number of the eigenvalues of its spectral density matrix diverge with (as in Assumption 2.1) while the remaining ones are bounded for all . In other words, GDFM itself (without the VAR model imposed on as in this paper) can be regarded as a representation of high-dimensional time series rather than a model. Overall, GDFM provides the most general framework for high-dimensional time series factor modelling and it encompasses other factor models found in the literature such as static factor models (Forni et al.,, 2009).

Static factor models are popularly adopted in both stationary (Stock and Watson,, 2002; Bai,, 2003; Fan et al.,, 2013; Barigozzi and Cho,, 2020) and piecewise stationary (Barigozzi et al.,, 2018; Li et al.,, 2022) time series modelling in high dimensions. Under stationary factor models, the factor-driven component permits a representation with some finite-dimensional vector processes as the common factors; here, ‘static’ refers to that loads contemporaneously and does not preclude serial dependence therein. The model in (2) includes such a static factor model by representing with , for some (see Remark R of Forni et al., (2009)). On the other hand, some models that have a finite number of factors under (2) cannot be represented with of finite dimension, the simplest example being the case where for some (Forni et al.,, 2015); see also (C2) in Section 5.2.

Hallin et al., (2018) observe that principal component analysis (PCA), typically accompanying static factor models as an estimation tool, does not enjoy the optimality property that guarantees their success in the i.i.d. case in the presence of serial correlations, unlike the dynamic PCA adopted for estimation under GDFM (see Section 3.1.2).

D.2 VAR representation of GDFM

For notational simplicity, let for all . Suppose that each th element of the filter in (5), say , is a ratio of finite-order polynomials in such that for some finite ,

for all and . Furthermore, assume the followings.

-

(a)

There exists such that

-

(b)

For all , and , we have for all .

Under such assumptions, Section 4 of Forni et al., (2015) establishes that for generic values of the parameters and (outside a countable union of nowhere dense subsets), admits a block-wise singular VAR representation

| (D.1) |

where and is of rank ; for convenience, we assume that for some . Here, each admits a finite-order VAR representation determined by with its degree , and for all .

The representation (D.1) gives the piecewise stationary factor-adjusted VAR model in (5) the interpretation of decomposing high-dimensional time series into two latent VAR processes with time-varying parameter matrices, one of low rank (singular) accounting for dominant dependence and the other modelling individual interdependence between the variables unaccounted for by the former.

Appendix E Information on the real dataset

Table E.1 provides the list of the companies included in the application presented in Section 5.3 along with their tickers and industry classifications .

| Ticker | Company name | Sector | Ticker | Company name | Sector |

|---|---|---|---|---|---|

| AMZN | Amazon.com | Cons. Disc. | AMGN | Amgen | Health Care |

| CMCSA | Comcast | Cons. Disc. | BAX | Baxter International | Health Care |

| DIS | Walt Disney | Cons. Disc. | BMY | Bristol-Myers Squibb | Health Care |

| F | Ford Motor | Cons. Disc. | JNJ | Johnson & Johnson | Health Care |

| HD | Home Depot | Cons. Disc. | LLY | Lilly (Eli) & Co. | Health Care |

| LOW | Lowes | Cons. Disc. | MDT | Medtronic | Health Care |

| MCD | McDonalds | Cons. Disc. | MRK | Merck & Co. | Health Care |

| SBUX | Starbucks | Cons. Disc. | PFE | Pfizer | Health Care |

| TGT | Target | Cons. Disc. | UNH | United Health | Health Care |

| CL | Colgate-Palmolive | Cons. Stap. | BA | Boeing Company | Industrials |

| COST | Costco | Cons. Stap. | CAT | Caterpillar | Industrials |

| CVS | CVS Caremark | Cons. Stap. | EMR | Emerson Electric | Industrials |

| PEP | PepsiCo | Cons. Stap. | FDX | FedEx | Industrials |

| PG | Procter & Gamble | Cons. Stap. | GD | General Dynamics | Industrials |

| WMT | Wal-Mart Stores | Cons. Stap. | GE | General Electric | Industrials |

| APA | Apache | Energy | HON | Honeywell Intl | Industrials |

| COP | ConocoPhillips | Energy | LMT | Lockheed Martin | Industrials |

| CVX | Chevron | Energy | MMM | 3M Company | Industrials |

| HAL | Halliburton | Energy | NSC | Norfolk Southern | Industrials |

| NOV | National Oilwell Varco | Energy | UNP | Union Pacific | Industrials |

| OXY | Occidental Petroleum | Energy | UPS | United Parcel Service | Industrials |

| SLB | Schlumberger Ltd. | Energy | DD | Du Pont | Materials |

| XOM | Exxon Mobil | Energy | FCX | Freeport-McMoran | Materials |

| AIG | AIG | Financials | CSCO | Cisco Systems | Technology |

| ALL | Allstate | Financials | EBAY | eBay | Technology |

| AXP | American Express Co | Financials | AAPL | Apple | Technology |

| BAC | Bank of America | Financials | HPQ | Hewlett-Packard | Technology |

| BK | Bank of New York | Financials | IBM | IBM | Technology |

| C | Citigroup | Financials | INTC | Intel | Technology |

| COF | Capital One Financial | Financials | MSFT | Microsoft | Technology |

| GS | Goldman Sachs | Financials | ORCL | Oracle | Technology |

| JPM | JPMorgan Chase | Financials | QCOM | QUALCOMM | Technology |

| SPG | Simon Property | Financials | T | AT&T | Technology |

| USB | U.S. Bancorp | Financials | VZ | Verizon | Technology |

| WFC | Wells Fargo | Financials | AEP | American Electric Power | Utilities |

| ABT | Abbott Laboratories | Health Care | EXC | Exelon | Utilities |

Appendix F Proofs

F.1 Preliminary lemmas

In the following lemmas, we operate under Assumptions 2.1, 2.2, 2.3 and 4.1. For notational convenience, we assume that for each , the filters have with appropriate zero columns such that we can write even when .

Recall that

| (F.1) |

with denoting the index of the change point nearest to and strictly left of a time point , and we define and analogously. Then, the local spectral density matrix of is defined as . Similarly, with and , we define the local ACV matrix of as

and analogously define . Then we define .

Zhang and Wu, (2021) extend the functional dependence measure introduced in Wu, (2005) for high-dimensional, locally stationary time series. Denote by and and -valued measurable functions such that for , and for . Then, and . Also let denote a coupled version of with an independent copy replacing . Then, the element-wise functional dependence measure is defined as

the uniform functional dependence measure as

the dependence adjusted norms as

and the overall and the uniform dependence adjusted norms as

Lemma F.1.

Proof.

By Minkowski inequality,

for all . Due to independence of , Assumption 2.3 and Lemma D.3 of Zhang and Wu, (2021), there exists that depends only on such that

for all , and

Similarly, from Assumption 2.2 and independence of , we have

for all . Then,

such that . Then, for some constant , we have

and setting ,

∎

Lemma F.2.

Proof.

The following lemma is a direct consequence of Lemma F.2.

Lemma F.3.

We adopt the notations and to denote the elements of the spectral density matrices, and similarly and .

Lemma F.4.

Denote by . Then, there exists such that .

Proof.

Lemma F.5.

For all and , the functions possess derivatives of any order and are of bounded variation, i.e. there exists such that uniformly in , , and any partition of , .

Proof.

From Lemma F.2,

for all , which implies that has derivatives of all orders. Moreover,

for some constant not depending on , or , which entails the bounded variation of . ∎

F.2 Proof of Proposition 2.1

Let . Under Assumption 2.2, we can find a constant which depends only on , and such that, uniformly over and ,

F.3 Proof of Theorem 4.1

Proposition F.6.

Under the assumptions made in Theorem 4.1, we have

For ease of notation, define and analogously define , and . By definition and Assumption 4.2 (ii), . Also, let and . Then, due to the Lipschitz continuity of (see Assumption 4.2 (i)), we have

| (F.2) |

for some small enough constant . In what follows, we omit the subscript from and for simplicity and throughout the proof, we operate on the set , where

with as in Theorem 4.1, and is defined in (F.8) below. By Proposition F.6, we have as and similarly, by Lemma F.8, such that .

Proof of Theorem 4.1 (a).

On , we have

| (F.3) |

for all . From (F.3), it follows that for any satisfying , we have since due to Assumption 4.2 (ii), and such does not belong to . Also, noting that by (F.2), (F.3) and the definition of and ,

we conclude that at least one change point is detected within distance from each . Next, suppose that satisfies . From that , we obtain

for some small constant and large enough under Assumption 4.2 (ii), i.e. we detect at least one change point within -distance from each . Finally, suppose that at some satisfying , we have . Then by (F.3) and the lower bound on ,

where , provided that , i.e. such cannot be a local maximiser of within its -radius. This, combined with how is updated at each iteration, makes sure that only a single estimator is added to for each change point. ∎

Proof of Theorem 4.1 (b).

WLOG, we consider the case when ; the following arguments apply analogously to the case when . We prove by contradiction that if , we have and thus cannot be the local maximiser of within its -environment as required.

From Theorem 4.1 (a), we have . Then from that and by (F.2) and (F.3), we have

| (F.4) |

for an arbitrarily small constant . Noting that and are Hermitian (and thus diagonalisable with real diagonal entries), we write

for some satisfying , for all . By Assumption 4.2 (ii), we have

Then on , there exists with and a constant such that

| (F.5) |

where the first inequality follows from Corollary 1 of Yu et al., (2015), and the second one from Assumption 4.2 (i), (F.3) and (F.4). WLOG, suppose that . Then,

From (F.3), (F.4) and Assumption 4.2 (i), for small enough ,

Also by (F.5),

for all under Assumption 4.2 (i), and is bounded analogously. Putting together the bounds on – together with the fact that , we have , and similarly we can show that . Then, we observe:

implies that

| (F.6) |

First, note that by (F.4),

| (F.7) |

and as applying the same arguments as those adopted in bounding and above, we have . Now we turn our attention to . Let with and , and when and when . Then,

By Lemma F.2, there exists constant that do not depend on such that

Similarly, noting that there are at most a single change point within any -interval, we have

for some constant , from that . Collecting the bounds on , and , we have for some constant ,

under Assumption 4.2 (i). Also, we observe that by Proposition 2.1,

Turning our attention to , note that

where the definitions of , , can be found in (F.11). Then by Lemma F.8 and Chebyshev’s inequality, there exists some constant such that , where

| (F.8) |

for some , where and is defined in the lemma. Setting (which itself does not depend on ), we have on ,

for large enough which, combined with the bounds on , contradicts the first inequality in (F.7). As these statements are deterministic on , the above arguments apply to all which concludes the proof. ∎

F.3.1 Supporting results

In what follows, we operate under the assumptions made in Theorem 4.1.

Lemma F.7.

Proof.

Noting that

| (F.9) |

we first address the first term in the RHS of (F.9). In Lemma F.1, for (as assumed in Assumptions 2.2 (iii) and 2.3), we can always set . Then, from the finiteness of shown therein and by Theorems 4.1 and 4.2 of Zhang and Wu, (2021), there exist universal constants and constants that depend only on their subscripts, such that for any ,

Noting that for any positive random variable , we have , we have for some constant independent of , thanks to Lemma F.1.

Turning our attention to the second term in the RHS of (F.9), let and define , , and , analogously. Then,

Then by Lemma F.2, for all , and ,

noting that under Assumption 4.2 (ii). Similarly, we yield under Assumption 4.4 (ii). Then,

| (F.10) |

From the bounds on and (which hold uniformly over and ) and that , there exists such that . Also from Lemma F.3 , there exists such that

and . Combining the bounds on –, the proof is complete. ∎

For and , define

| (F.11) |

Lemma F.8.

Proof.

Under Assumption 4.1 (i), Proposition 6.2 of Zhang and Wu, (2021), combined with the arguments adopted in the proof of their Theorem 4.1 (most notably, their Equation (B.15)) and Bonferroni correction, obtains that there exist universal constants and that depend only on their subscripts, such that

thanks to Lemma F.1. Then, as in the proof of Lemma F.7, we can find independent of and show the first part of the claim by Lemma F.1. Similarly, under Assumption 4.1 (ii), Lemma F.1 and Theorem 6.3 of Zhang and Wu, (2021) show that there exists a universal constant such that

which completes the proof. ∎

F.4 Proof of Theorem 4.2

We provide a series of supporting results under the assumptions made in Theorem 4.2, leading to the proof of the claims. In what follows, we operate in . We define

Also, let for , and for , such that .

Proposition F.9.

-

(a)

There exists a constant such that

-

(b)

Also, we have

Proof of (a).

Under Assumption 4.2 (ii), applying Proposition 6.2 and Theorem 6.3 of Zhang and Wu, (2021) with their (B.15), there exist universal constants not dependent on and constants that depend only on their subscripts, such that for any ,