Kernel-weighted specification testing under general distributions

Abstract

Kernel-weighted test statistics have been widely used in a variety of settings including non-stationary regression, survival analysis, propensity score and panel data models. We develop the limit theory for a kernel-weighted specification test of a parametric conditional mean when the law of the regressors may not be absolutely continuous to the Lebesgue measure and admits non-trivial singular components. In the special case of absolutely continuous measures, our approach weakens the usual regularity conditions. This result is of independent interest and may be useful in other applications that utilize kernel smoothed statistics. Simulations illustrate the non-trivial impact of the distribution of the conditioning variables on the power properties of the test statistic.

keywords:

1 Introduction

Kernel-weighted statistics are widely used for inference on the functional form of a density, conditional distribution and conditional mean. In testing for a parametric specification of a conditional mean, kernel-based tests have been used in the traditional regression context [40, 14, 16]. Those types of statistics are also employed in various extensions such as regression quantiles [41, 25], semi-parametric models [4], propensity score [35], panel data [22], non-stationary regression [10, 39] and survival analysis [29]. If represents the law of the regressors, it can always be expressed in its Lebesgue decomposition:

| (1) | |||

where is a discrete measure, is absolutely continuous to the Lebesgue measure and is a singular continuous measure. While kernel-weighted statistics have been investigated in several distinct applications, not much is known about the statistical properties of procedures based on these statistics when the distribution is “contaminated” with non-trivial singular components. To the best of our knowledge, all the available analyses in the literature have assumed that the Lebesgue decomposition of does not admit any singular components, usually with additional smoothness regularity conditions imposed on the density function.

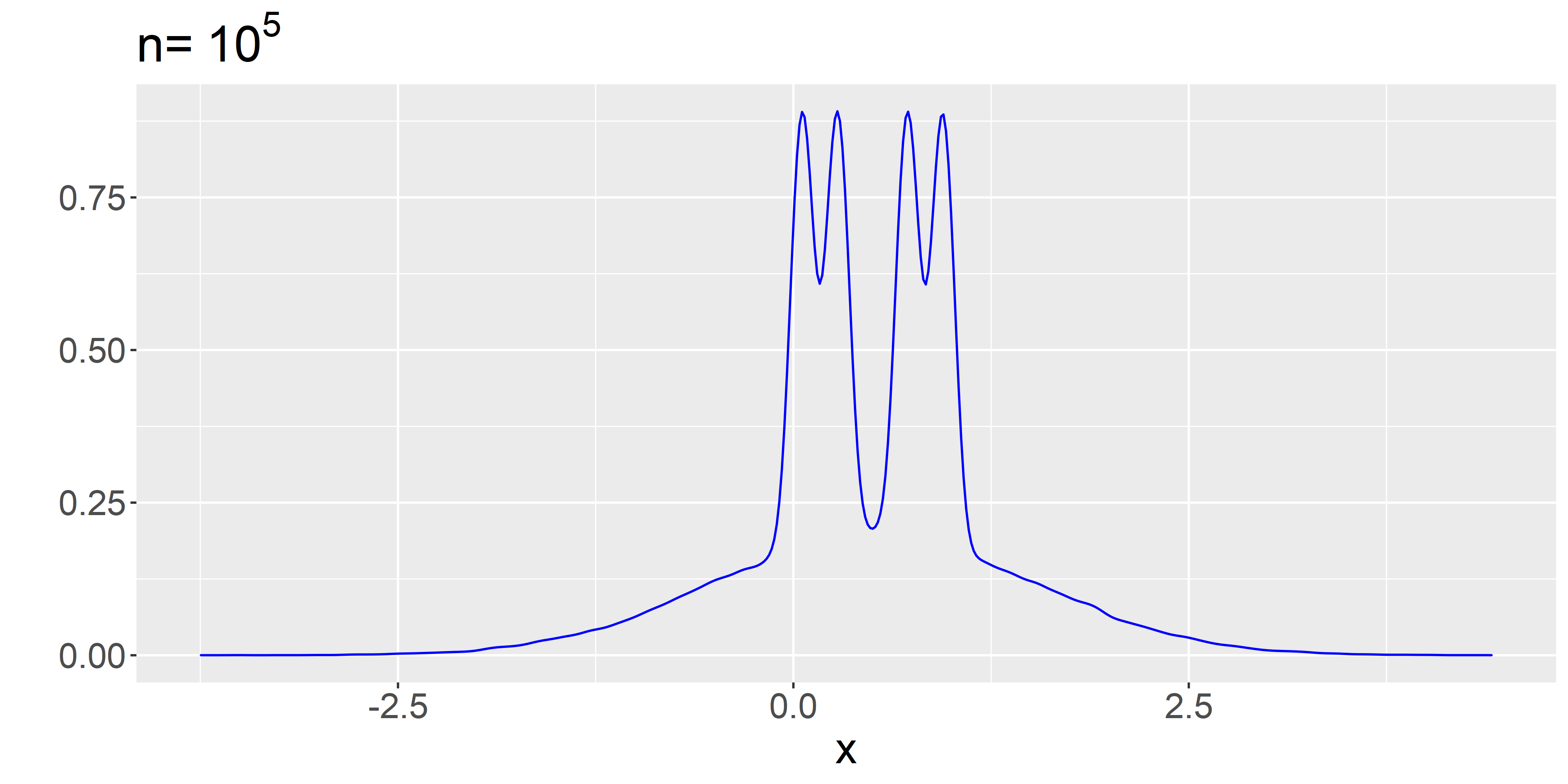

In this paper, we study a class of kernel-weighted U-statistics that frequently arise in the analysis of goodness-of-fit testing. A general limit theory is provided that allows for the Lebesgue decomposition of to contain singular components. Our generalization of the standard limit theory is partially motivated by a desire to understand the finite sample properties of these statistics when the distribution is absolutely continuous with a density that is either non-smooth or possesses large derivatives. Indeed, in finite samples, singular distributions tend to exhibit characteristics similar to such measures. For example, the claw and its variants in [26] are Gaussian mixtures with a density that exhibits sharp continuous “spikes” at several points in the support. While these distributions are absolutely continuous with a smooth density, the derivatives may be so large as to make them resemble distributions with singular components in finite samples.

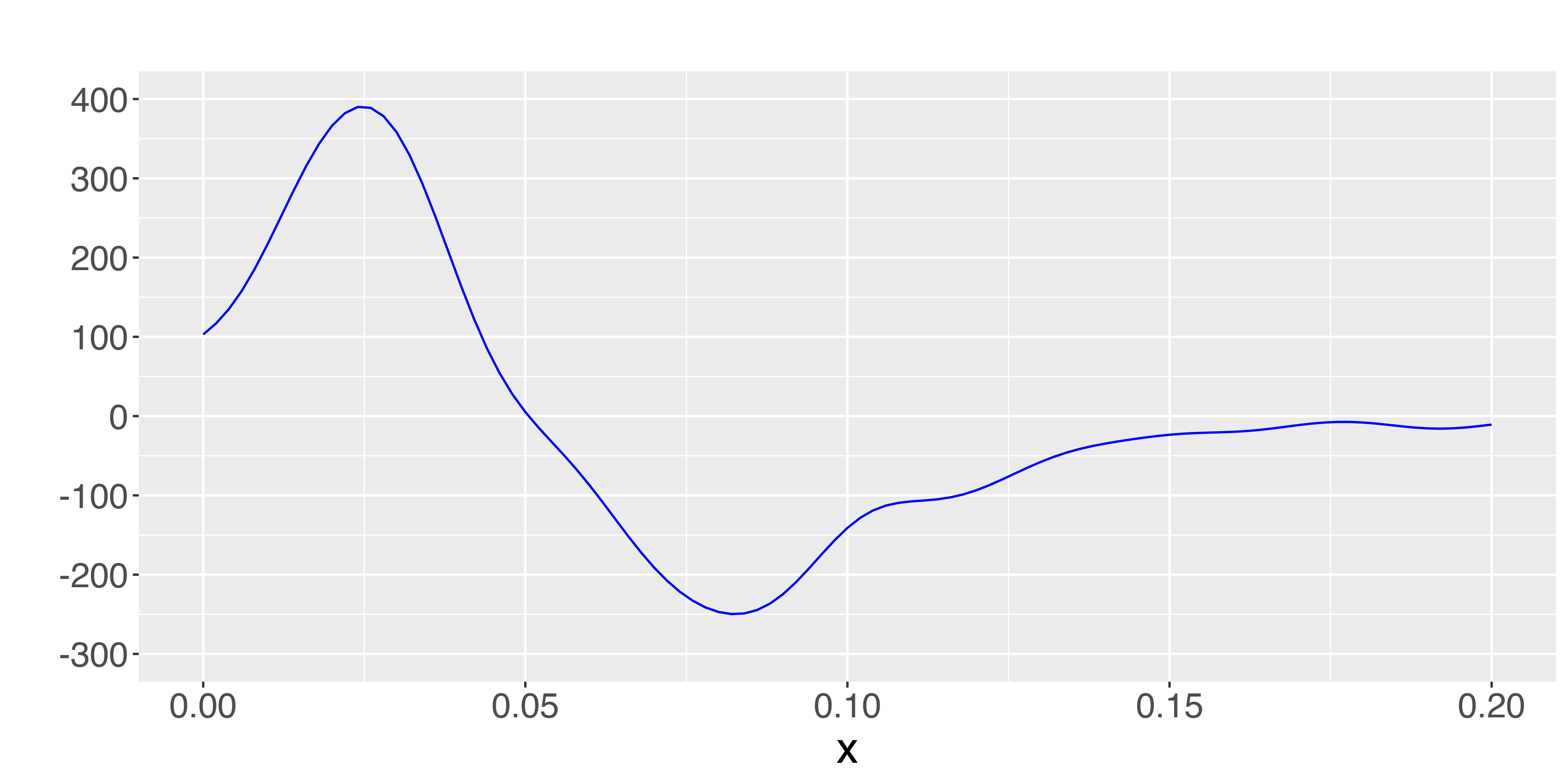

As illustrated in Figure 1, the estimated density derivative of covariates may be quite large: within the same data set, the budget shares for alcohol, travel and leisure were significantly more volatile and exhibited estimated derivatives in the thousands. While the standard limit theory can account for this phenomenon by imposing an arbitrarily large upper bound on the density and/or its derivative, we find it more appropriate to model these situations with the possibility of a non-trivial singular component.

The main results of this paper develop the limit theory for kernel-based inference statistics when the distribution of the conditioning variables admits a Lebesgue decomposition with singular components. The class of distributions that our theory covers include absolutely continuous measures with a bounded density, measures supported on lower dimensional subspaces, continuous measures that contain discrete marginals (e.g. mixed variables and discrete regressors), normalized Hausdorff measures on self-similar fractals and any Ahlfors-David regular measure. All our main results also apply to countable mixtures generated by such measures. Even in the special case where is absolutely continuous, our analysis only requires a bounded density and avoids imposing any further regularity conditions.

Denote by a vector of ones and the probability of a cube of radius and centred at by . Our approach provides interpretable conditions that are based on local features of the underlying distribution through the expected small ball probability:

| (2) |

If is a probability measure on with a bounded density, as but the rate is always slower when the Lebesgue decomposition admits singular components. The idea behind our results is to utilize a version of integration by parts to extract local features of that depend on when the density does not exist (at the cost of using sufficiently differentiable kernels). This approach is of independent interest and may be useful in other applications that utilize kernel-based statistics.

Theorem 3.8 establishes the general result for asymptotic normality of a degenerate kernel-weighted U-statistic. For some mixture subclasses that include singular distributions of reduced Hausdorff dimension for some , exact rates of convergence for the U-statistic are obtained. These results form the basis for the study of self-normalizing statistics that arise in goodness-of-fit tests of a parametric regression function. In Theorem 3.9, we establish the limit distribution for such statistics under the null hypothesis. In Theorem 3.10, we develop the local power analysis of the test statistic under a Pitman sequence of local alternatives

where and is a fixed drift function that determines the direction of approach to the null model. We characterize the fastest possible rate at which alternatives can approach and yet remain distinguishable from the null. If the Lebesgue decomposition of contains singular components, we show that it is possible for the alternatives to approach the null at a rate faster than in the fully absolutely continuous case. The novel feature of the result is the interplay between the rate of approach , the direction of approach to the null model and the singular components of the distribution. In particular, power does not exist at the fastest possible rate if the support of does not sufficiently “touch” areas where the local singularity of the measure (the rate at which decays) coincides with . In Theorem 3.11, we provide further details on the mechanism through which this interplay can influence the local power of the test statistic.

The paper is organized as follows. Section 2 provides the model framework and assumptions. Section 3 develops the main limit results. Section 4 provides simulation evidence on the sensitivity of the kernel test statistic to the distribution of the conditioning variables. Section 5 concludes. The supplemental file [19] contains additional proofs and technical results that were omitted in the main text.

2 Framework and assumptions

Consider the nonlinear regression model

| (3) |

where is a vector of regressors, is a scalar dependent variable and is an unobserved error. Given a family of parametric regression functions indexed by a finite dimensional parameter , we address the common problem of testing the null hypothesis

Denote by the vector of estimated residuals (e.g. using non-linear least squares or maximum likelihood). To test , we make use of the kernel smoothed statistic

| (4) |

where is a non-negative symmetric kernel function and is a deterministic bandwidth sequence. The usual goodness-of-fit statistic (see e.g. [10, 39, 40]) uses a self-normalized form

| (5) |

where is an estimator of the variance of . In the literature, this test statistic falls under the class of smoothing-based tests (see [11] for a comprehensive review). Let denote the version of obtained by replacing with the unobserved error:

| (6) |

2.1 Notation

Denote by a vector of ones and a vector of . For any vector , denote the coordinate components by . Let and denote the Euclidean, infinity and operator norm, respectively. For positive sequences , we use to denote and to denote . Let denote the usual equivalence class of integrable (with respect to ) functions that are measurable with respect to the algebra generated by . Denote the absolute continuity of a measure with respect to a measure by . Let and denote the usual expectation and probability operators. In the special case where can be expressed as a mixture that includes component , the notation and will be used to indicate that the operators are defined with respect to . We use to denote convergence in distribution.

2.2 Assumptions

Assumption 1.

is a sequence of independent and identically distributed (i.i.d) random vectors.

Assumption 2.

(i) . (ii) The functions and are bounded away from infinity: for some and . (iii) The function is bounded away from zero: for some .

Assumption 3.

(i) The function is a product kernel: for every . (ii) The kernel function is non-negative, continuous, symmetric around zero, strictly decreasing on and has support . (iii) is twice continuously differentiable on the interior and the derivatives admit a continuous extension to .

Assumption 1 could be generalized but is made here to facilitate the focus on the distribution of the conditioning variables. Assumptions 1 and 2(i) imply that the statistic in is degenerate. Assumptions 2(ii) and 2(iii) are made for convenience and could be weakened further. Of course, Assumption 2(ii-iii) applies under homoscedasticity.

Assumptions 3(i-iii) are standard and satisfied by e.g. the Epanechnikov kernel and Quartic kernel . The support assumption on could be modified to allow for any compact interval without changing any of our main results. This could be generalized even further to admit a wider class of kernel functions (e.g. Gaussian kernels) where the assumption of compact support is replaced with a rate of decay. However, such an analysis will typically involve some interplay between the decay rate of the kernel and the tails of the distribution. Here, we simplify to highlight the impact of the distribution. Assumption 3(iii) is satisfied if exist and are uniformly continuous on . It ensures that in the event a density does not exist, one can use (as we explain below) integration by parts to find the local behavior of moments of the U-statistic.

3 Main results

In Section 3.1, we provide results about the moments of kernel smoothed statistics. In Section 3.2 and 3.3, a class of distributions is defined over which asymptotic normality for the U-statistics in (4, 6) is subsequently established. Section 3.4 develops the limit theory and local power analysis within the context of specification testing.

3.1 Derivations and bounds for moments

From the seminal work of Hall [12, 13], it is known that limit theory for (6) can be established by appealing to a version of the martingale central limit theorem. Indeed, by defining

| (7) | |||

| (8) |

it is shown in [12, Theorem 1] that , provided that the moments satisfy

| (9) |

As noted in the literature (e.g. [20, pp. 154-155]), Condition (9) (or its variants in other applications) is typically difficult to interpret as it depends non-trivially on the underlying distribution of the regressors. It is shown in [40] (see also [14, 25, 35] for related applications) that when the distribution is absolutely continuous and certain smoothness regularity conditions hold on the density, Condition (9) reduces to the usual restriction on the bandwidth: and .

Our starting point in generalizing beyond absolutely continuous measures is to derive the distributional restrictions that are implicitly imposed through Condition (9). This requires us to express and bound the moments that appear in (7, 8) in terms of interpretable functionals of . This will be the subject of several subsequent Lemmas that appear below.

Definition 3.1.

Let where denote open intervals of finite length. We say a function is sufficiently differentiable on if the mixed partials

exist and admit continuous extensions to the closure of . In this case, we denote

Given , a straightforward application of Fubini’s theorem shows that integration (with respect to ) of a compactly supported sufficiently differentiable function admits a representation as a standard integral with respect to the Lebesgue measure. The integrand in this case is the -weighted measure of a Euclidean cube.

Lemma 3.2.

Let and denote open intervals of finite length. Suppose is bounded, continuous, sufficiently differentiable on and has support contained in the closure of . Additionally, for and every , suppose that the mixed partial

vanishes at for . Then

| (10) |

where denotes

| (11) |

The next Lemma aims to interpret the moments appearing in Condition (9) through repeated applications of Lemma 3.2. We begin by introducing some convenient notation. Let be as in Assumption 2. Given , we define the cube centered at with directions to be

Define

| (12) | |||

| (13) |

The following Lemma expresses the moments in terms of functionals of .

Proof of Lemma 3.3.

Define

Let denote the coordinate of . Conditional on , satisfy the hypothesis of Lemma 3.2 with . Applying Lemma 3.2 yields

where the last equality follows from the change of variables . It follows that

Define to be the partitioned vector with . For any fixed choice of , we have

where the second equality follows from the change of variables and ( is a symmetric function). Iterating this procedure from to yields

The expression for follows from substituting . The derivation for is similar. The derivation for follows from repeated applications of Lemma 3.2 (further details provided in the supplementary file [19]). ∎

Given the form of the integrand that defines in Lemma 3.3, it is expected (by Lebesgue’s differentiation theorem) that whenever Lebesgue measure. If the Lebesgue decomposition of admits singular components, the following Corollary shows that may at least be used as a conservative lower bound on the rate.

Corollary 3.4.

In particular, Corollary 3.4 extends the standard result (see e.g. [40]) for the limiting behavior of when the Lebesgue density exists (although here we do not assume that it is continuous) and demonstrates that diverges when there are singular components. The next Lemma provides bounds on the moments that will be instrumental in verifying Condition (9) and as a consequence the limit behavior of the U-statistic in .

Lemma 3.5.

Proof of Lemma 3.5.

Note that for every . Fix any . From the expression defining in Lemma 3.3, we obtain that

where is as in Assumption 2 and . The derivations for the other bounds are provided in the supplementary file [19].

∎

The bounds on the moments derived in this section are in terms of the expected small ball probability . We next turn to defining classes of distributions where these bounds can be used to provide limit properties of the statistic.

3.2 Classes of distributions

We begin by making an assumption that delineates a class of distributions for which the asymptotic normality of the kernel statistic will be established. As we show below, this class encompasses some well-known distributions. We will refer to as a continuous measure if as for every in the support of .

Assumption 4.

is a continuous measure that satisfies

A stronger pointwise version of Assumption 4(i) is commonly known as the “doubling” condition in the literature (see e.g. [23, 38]). Specifically, doubling measures are exactly those that satisfy

| (14) |

for some universal constant and all sufficiently small .

A stronger condition which implies both parts of Assumption 4 is that be Ahlfors-David regular (see e.g. [24]) on the support of . These are precisely the measures where there exists a for which

| (15) |

holds for some universal constants and all sufficiently small .

We note that while conditions (14, 15) are sufficient for Assumption 4 to hold, they are not necessary. In particular, the existence of a universal that satisfies (14, 15) may be excessively restrictive when is not compactly supported. Nonetheless, Assumption 4 may still hold in this case as the assumption only depends on expectations of the distribution. To expand on this point, we introduce a rich class of distributions that extends beyond the absolutely continuous and Ahlfors-David regular subclass. Define

Definition 3.6.

For every , let denote the class of probability measures that satisfy

| (16) |

for some constant and all sufficiently small . By varying the singularity exponent , we denote the class of all such distributions by .

The following four examples demonstrate that the class includes a wide range of distributions that may underlie various cases of interest in economics, finance and natural sciences.

Example 1 (Absolutely continuous measures).

Suppose is absolutely continuous with respect to the Lebesgue measure on and admits a density function . By Lebesgue’s differentiation theorem, we obtain that

almost everywhere with respect to the Lebesgue measure. As a consequence, where (16) holds with .

In particular, Example 1 allows for absolutely continuous measures that admit a discontinuous density function.

Example 2 (Self-Similar Fractals).

Consider a contraction mapping such that for all and some fixed . Let denote a family of contraction maps with contraction ratios . There is a unique compact set (see e.g. [21, Proposition 2.30]) that is invariant with respect to , in the sense that . Denote the similarity dimension of by the unique for which . is said to satisfy the open set condition (OSC) if there exists a nonempty open set such that and for . For any that satisfies the OSC, it is known (see e.g. [18, Section 5]) that the Hausdorff dimension of is the similarity dimension and the probability measure induced from the restriction of the -dimensional Hausdorff measure to is Ahlfors-David regular (15) with . Frequently referenced examples include the Cantor set (the Cantor measure is the restriction of the Hausdorff measure), Sierpiński’s Triangle () and the Koch Snowflake ().

Fractal measures are useful for modelling data that describe processes that are similar at different scales, used frequently in the natural sciences and the analysis of spatial data (see e.g. [3, 5]).

Example 3 (Measures supported on a low dimensional subspace).

Example 3 can be generalized further to allow for a general -rectifiable (see e.g. [30, 6, 28]) measure.111A measure on is -rectifiable if there exists a Borel measurable function and a countable collection of -dimensional submanifolds such that for every Borel set , where is the natural -dimensional volume measure that a submanifold inherits as a subset of . These are low dimensional measures in the sense that there exists a countable collection of -dimensional submanifolds such that .

Example 4 (Discrete Regressors and mass points).

Suppose where the law of is a continuous measure on for some and the law of assigns positive mass to some . Suppose admits a density and the conditional distribution measure admits a density . For any fixed , we have that

From Example 1, it follows that the first requirement of (16) holds with . For the second requirement, we note that if is in the support of , then

Denote the conditional (at ) measure of a cube with radius and centered at by . Since the conditional measure admits a density, the second requirement of (16) follows from

In Example 4, may be fully discrete (the support of is a countably infinite set ) or where is fully discrete and is a mixture of a continuous and discrete variable. Example 4 can be generalized in a straightforward way to allow for the continuous measure to contain singular components (the argument is identical if we insist that and are elements of for some ). To the best of our knowledge, Example 4 extends the known results in the literature (e.g. [17]) to allow for discrete regressors with countably infinite support, mixed regressors and continuous regressors whose joint law may have singular components . In this case, our approach also highlights that there are possible advantages to viewing the joint distribution of mixed data containing discrete and continuous variables as a continuous singular measure (which can be analyzed directly).

The next result shows that every satisfies Assumption 4. Moreover, is closed under mixtures, so that any mixture combination of its elements (such as the distributions in Example 1-4) satisfies Assumption 4 as well.

Lemma 3.7.

In particular, by mixing absolutely continuous measures with elements of , we obtain a large class of distributions that admit a non-trivial Lebesgue decomposition and satisfy Assumption 4. Finally, we remark that it is not necessary to argue for Assumption 4 through membership in . In more complicated setups, a measure may not charge cubes in a way that satisfies Definition 3.6. In such cases, Assumption 4 should be verified directly.

3.3 Limit theory

In the next result, we establish asymptotic normality for the U-statistic in (6) for every distribution that satisfies Assumption 4. For the remainder of Section 3, we assume that the bandwidth sequence satisfies and .

Proof of Theorem 3.8.

The result follows from Theorem of [12] if Condition (9) holds. We aim to verify that

From Assumption 4(i), there exists and such that

| (17) |

holds for all .

- (a)

- (b)

∎

Remark 1 (On the existence of ).

Let denote the Lebesgue measure on . Suppose Assumption 2 holds and for some . By Lemma 3.3, we have that

This suggests that may be well defined whenever

| (18) |

exists almost everywhere (with respect to . For absolutely continuous measures and low dimensional measures such as in Example 3, this follows immediately from an application of Lebesgue’s differentiation theorem. In the general case, it is known from [30] that if exists almost everywhere with , then for some integer and there exists a countable collection of -dimensional submanifolds such that . In particular, when is not an integer, the limit in (18) does not always exist and in this case typically oscillates between its limit inferior and superior.

Remark 2 (On bandwidth constraints).

Our limit theory depends on the assumption that the bandwidth sequence satisfies . While this is standard for the absolutely continuous case, a closer inspection of our proofs reveal that all our main results go through under the assumption that . From the general bound (with strict dominance in the presence of singular components), we see that this is a weaker requirement on the bandwidth. In particular, when singular components exist, the bandwidth can approach zero at a faster rate than in the fully absolutely continuous case. In most cases, this more relevant bandwidth restriction cannot be used directly as the exact rate depends on knowledge of the singular contamination. One situation where the weaker constraint can be interpreted directly is the case of mixed data with absolutely continuous and discrete regressors (Example 4). In this case, it reduces to (where denotes the dimension of the absolutely continuous regressors).

Remark 3 (On discrete measures and Assumption 4).

As illustrated in Example 4, Assumption 4 allows for discrete distributions and mass points in a subset of the marginals, provided that at least one of the marginals is a continuous distribution. If there is a mass point in the entire distribution (equivalently the Lebesgue decomposition of contains a discrete measure), Assumption 4(ii) will be violated. In this case, the limit distribution of the U-statistic in (6) is typically Non-Gaussian. Indeed, suppose where and is a discrete measure with finite support . First, we observe that scaling by does not provide any additional rate self-normalization as it converges to a positive limit:

It is straightforward to verify that the U-statistic can be expressed as

The first term on the right is non-trivial when the Lebesgue decomposition of contains a discrete measure. Moreover, it can be viewed as a degenerate U-statistic with a fixed symmetric kernel function . From [36, Theorem 12.10], it follows that where and are eigenvalues corresponding to the integral operator defined by .

3.4 Specification Testing

Consider the feasible statistic in (4) that differs from in that the residuals replace the true errors . To construct the goodness-of-fit test statistic in (5), we will also require a feasible analog of . To that end, define

| (19) |

Let and denote the Gradient and Hessian of (with respect to ), respectively. To derive the limit theory under , we impose the following regularity conditions on the model and parameter estimator.

Assumption 5.

(i) . (ii) In a neighborhood of , the map is twice continuously differentiable for every in the support of . (iii) In a neighborhood of , and are dominated by functions and , respectively.

Assumption 5 is commonly imposed in the literature (e.g. [40, 39]). For distributions in , all our results in this section also hold under the weaker requirement that . The theorem below establishes the limiting distribution for the self-normalized goodness-of-fit statistic in (5) under .

Theorem 3.9.

Thus, the test statistic converges weakly to a standard Gaussian and does not depend on any nuisance parameters. When singular components exist, the rate at which the distribution of the statistic approaches the limit Gaussian could be quite slow, in particular for converging to zero slowly (e.g. for small in . If knowledge of the singular components is assumed, one can in principle choose a bandwidth sequence that approaches zero at a faster rate than usual (see Remark 2) to improve on the rates.

To investigate the asymptotic power of the test, we consider the sequence of local alternative models

| (20) |

where is a deterministic sequence of constants and is a real-valued drift function that determines the direction of approach to the null model.

We will continue to assume (as is standard) that Assumption 5(i) holds under . Indeed, when the residuals are computed using non-linear least squares (NLS) and the usual regularity conditions to ensure consistency under hold, the estimator continues to admit (under ) the asymptotic linear expansion

To facilitate the derivation we make an assumption on the moments additional to Assumption 4.

Assumption 6.

is a continuous measure that satisfies

This assumption is similar to Assumption 4(ii). By arguing as in Lemma 3.7, it is straightforward to deduce that Assumption 6 holds for every distribution in the class .

The next theorem provides the local power analysis of the specification test. In general, it depends on the interplay between the rate at which the local alternatives approach the null, the drift function that determines the direction of approach to the null model and the distribution .

Theorem 3.10.

Thus, under a sequence of local alternatives, the fastest rate at which asymptotic power may exist is . Clearly (21) is satisfied whenever is bounded away from zero (up to a null set). If is absolutely continuous with density , we have and (21) reduces (by Lebesgue differentiation) to the usual condition

The implications of Theorem 3.10 are more complex for distributions with singular components when is not bounded away from zero. Loosely speaking, (21) says that the support of must intersect nontrivially with a subset of the support of the distribution where the local singularity is maximized (support points where the decay rate of coincides with the rate for ). The following example illustrates the essential idea of how the direction of approach may influence the local power properties of the test statistic.

Example 5 (On the direction of approach).

Suppose where is standard Gaussian and denotes the usual Cantor measure on . Let and denote the support of by . In this case, and . If there exists such that , then for any sequence we have that

In particular, condition (22) holds and there is no power for alternatives that approach at rate in the direction.

Remark 4 (On the power with singular components).

If is absolutely continuous, it is well known (see e.g. [40, Theorem 3]) that the fastest possible rate of approach to the null model is given by . If contains singular components, we have . By Theorem 3.10, it then follows that for measures with singular components, the alternative sequence can approach the null at a rate faster than in the fully absolutely continuous case (provided that the support of sufficiently “touches” the singular measures support for (21) to hold).

We now examine the situation where (22) holds. In this case, there is no power for alternatives that approach the null model in the direction with rate

| (23) |

A natural question then is what is the minimum rate for which power exists? In general depends non-trivially on the interaction between the support of and the local singularity of the measure. To illustrate the essential idea, we consider the case where can be represented as a finite mixture of distributions from . That is, there exists a finite index set such that

| (24) |

In this case, where . We consider the case where concentrates away from the support of the components or equivalently, the support of does not interact with areas where the local singularity of the measure is at its maximum.

Given a distribution , its support can always be expressed as

| (25) |

Let and denote the common support of by . For the mixture distribution in (24), denote by a subset of the index set for which

| (26) | |||

| (27) |

holds for all sufficiently small . Condition (26) restricts the support of to lie outside of . Condition (27) essentially states that is well-separated from for every that has a sharper singularity than that of . In particular, if there exists such that for every and , then (27) holds for every (for a one dimensional illustration, see Example 5).

Denote the restricted -singularity coefficient of by and the probability measure induced from the restriction by . The following theorem illustrates that for directions that satisfy (26-27) with no power at rate , there may be power when the alternatives approach at a slower rate , provided that the support of intersects nontrivially with some subset of the mixture components support.

Theorem 3.11.

Suppose the alternative hypothesis and Assumptions (1, 2, 3, 5) hold. Let be as in (24) and be such that (26-27) holds. Suppose is uniformly continuous on the support of and either or and Assumption 5(iii) holds with for some .

-

(i)

If , then

-

(ii)

If and

(28) then there exists a deterministic sequence of constants such that

In the special case where , we have . By Lemma 3.7, and . Therefore, the hypothesis and conclusion of Theorem 3.11 is identical to Theorem 3.10 in this setting. Moreover, when , boundedness of can be replaced with integrability and the existence of sufficient moments for the envelope function appearing in Assumption 5. Other variations on these assumptions are possible as well.

When and , Condition (21) of Theorem 3.10 will fail as the ratio has rate . Condition (28) corrects for this by using only the mixture components where has support and the appropriate rate for the denominator. If (28) holds, there will be power for alternatives that approach in the direction at rate

As an application, let be as in Example 5. We take to be the subcomponent that contains only the distribution. Then (28) holds whenever . In this case, Theorem 3.11 implies that power exists at the rate

Thus, under the null, the goodness-of-fit statistic in (5) converges weakly to a standard Gaussian for a large class of continuous measures. However, the usual local power analysis is complicated by possible singularities and their interplay with the direction of approach to the null model.

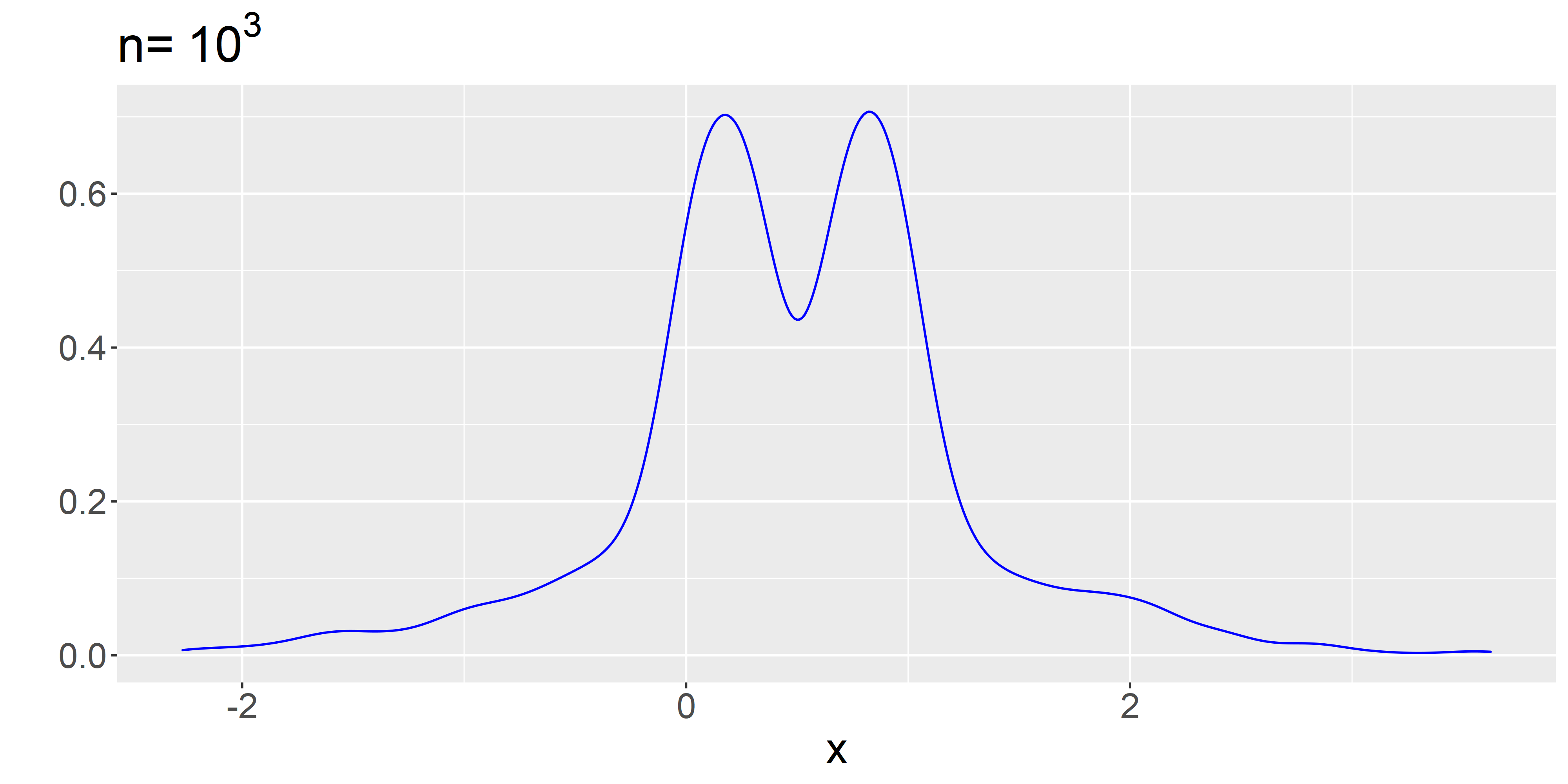

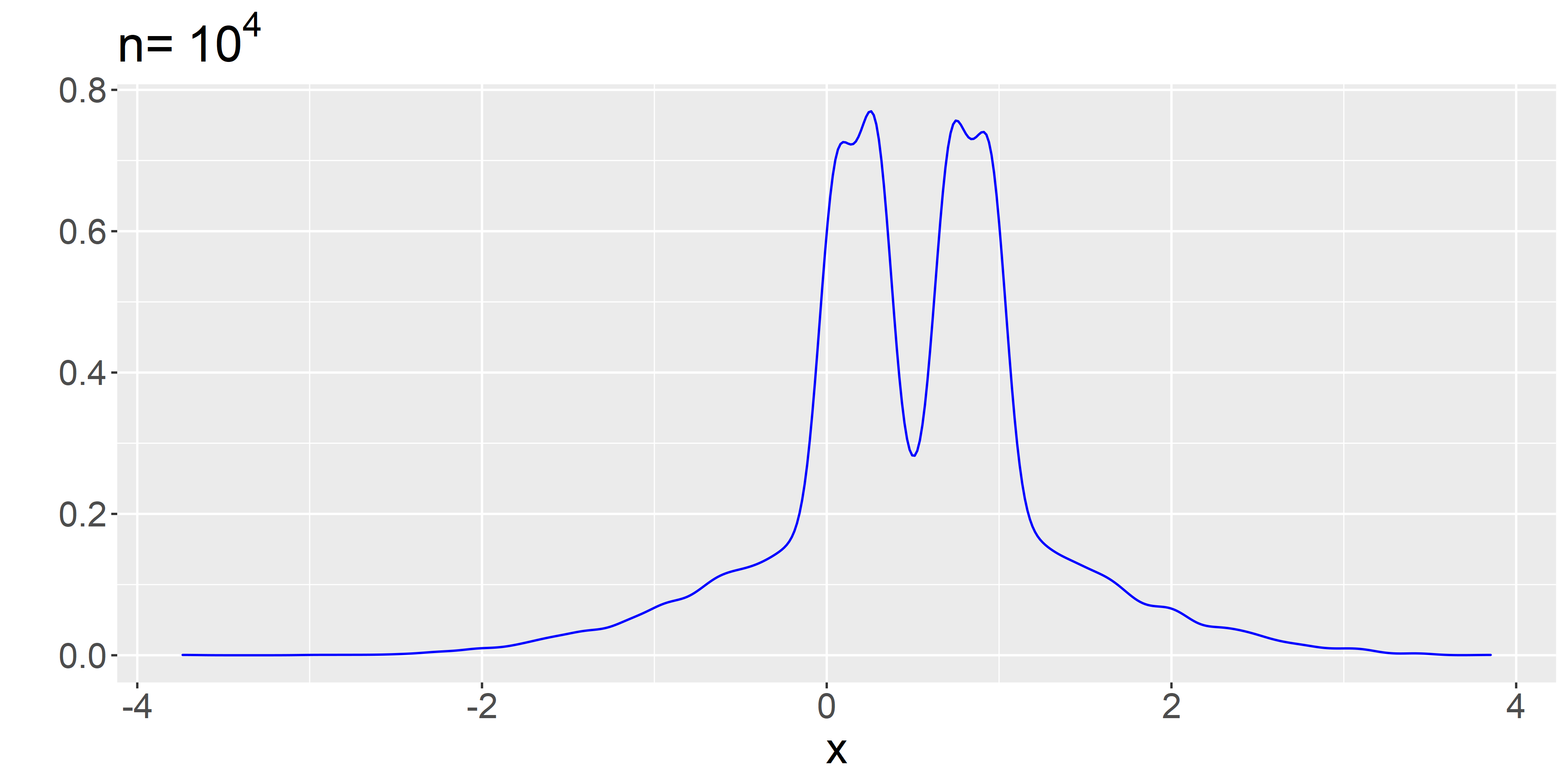

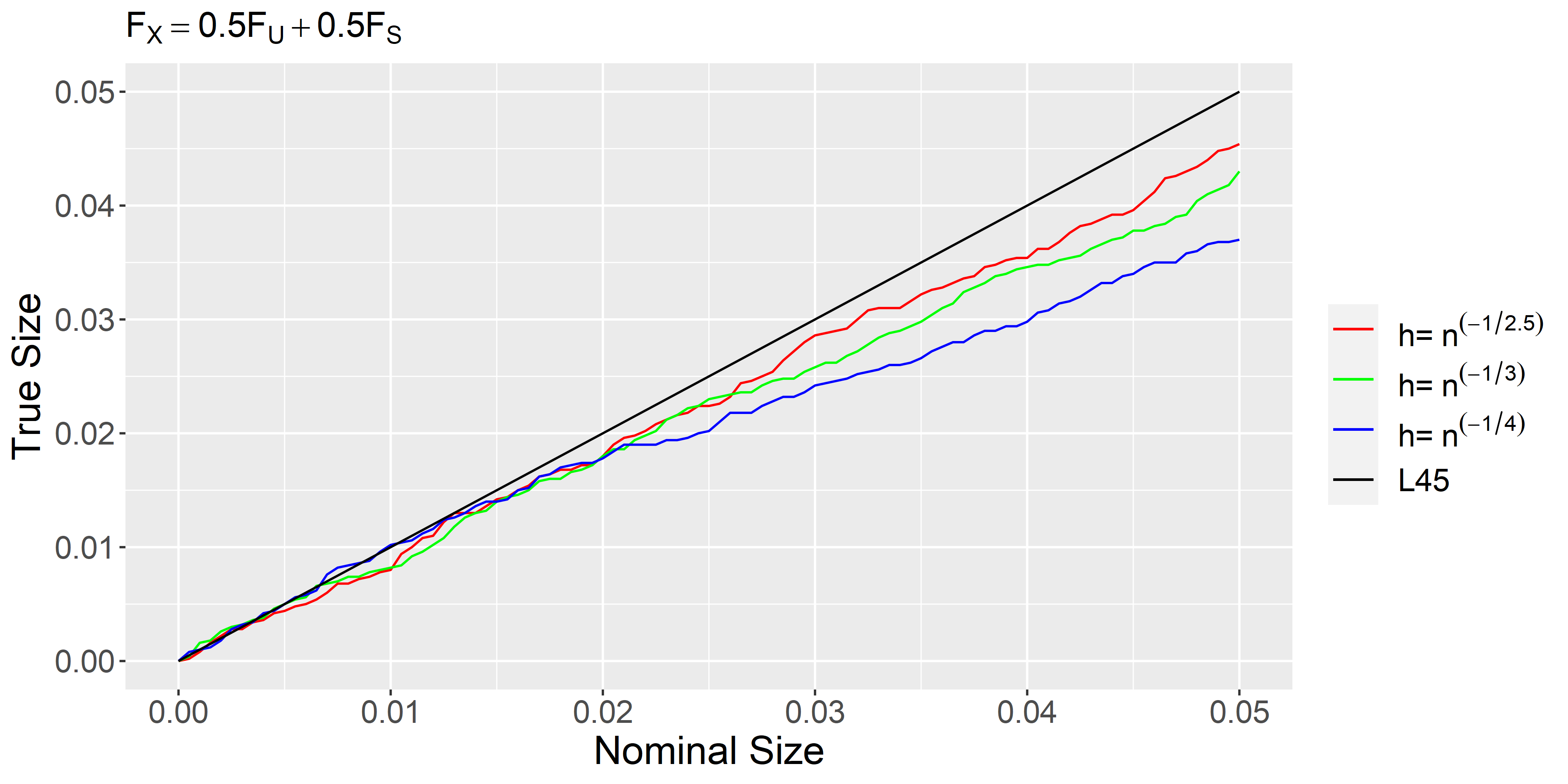

4 Simulations

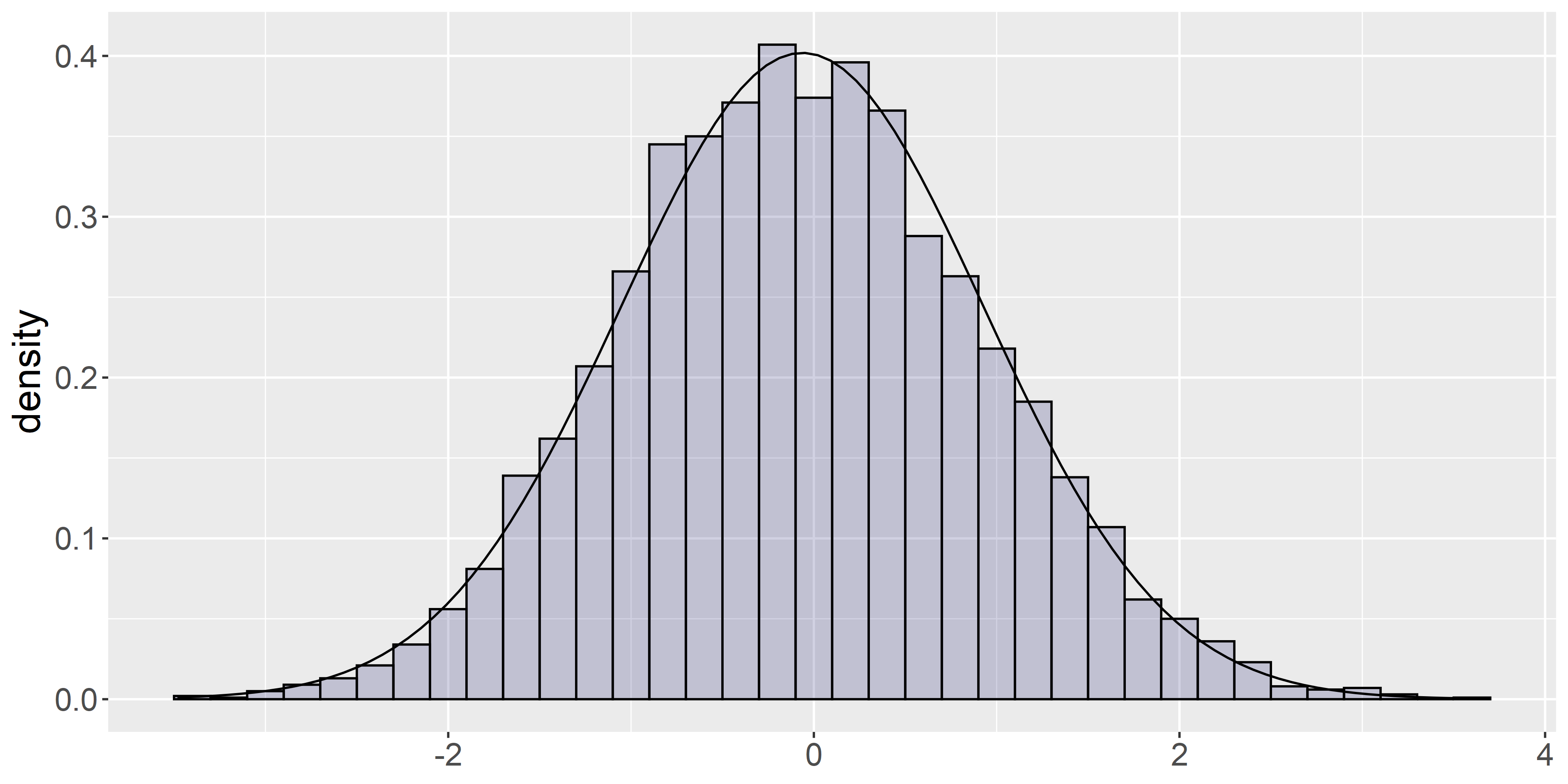

In this section, we provide simulation evidence on the asymptotic normality of the goodness-of-fit test statistic under the null hypothesis. Additionally, we illustrate the sensitivity of the test to the distribution of the conditioning variables. We use the Epanechnikov kernel and the number of replications in all cases is (population quantities defined through use the empirical analog from the simulation draws).

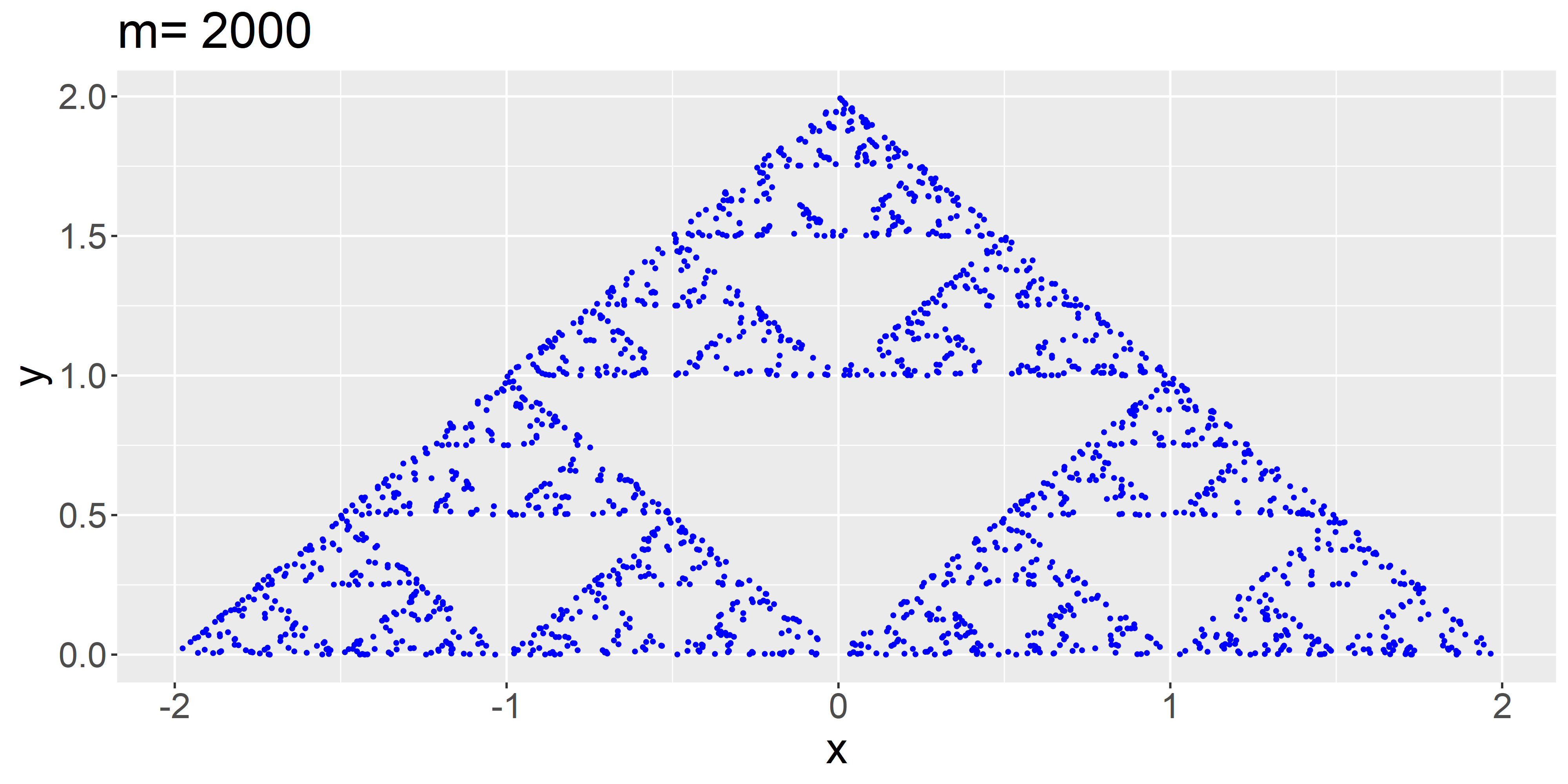

In the interest of working with a distribution that admits a non-trivial singular component, we make use of the fact that there exists a well developed theory (see e.g. [21]) for approximating a random sample from the normalized Hausdorff measure of any self-similar fractal. We focus on a two dimensional regressor with mixture distribution

| (29) |

where is the uniform distribution on and is the normalized Hausdorff measure on Sierpiński’s Triangle (with vertices at ).

A random sample from can be approximated using the Markov chain generated by the chaos game (see e.g. [21, Chapter 2.4]) on the iterated function system (the family of contraction maps in Example 2) associated with . In all cases, the initial draws are discarded as a Markov chain burn-in and the remaining draws are used as the observed sample of size .

Denote the coordinates of by . We consider the null model

| (30) |

The data is generated with . We use the feasible goodness-of-fit statistic where and are as in (4) and (19), respectively. The estimated residuals are computed using ordinary least squares on the regression in (30).

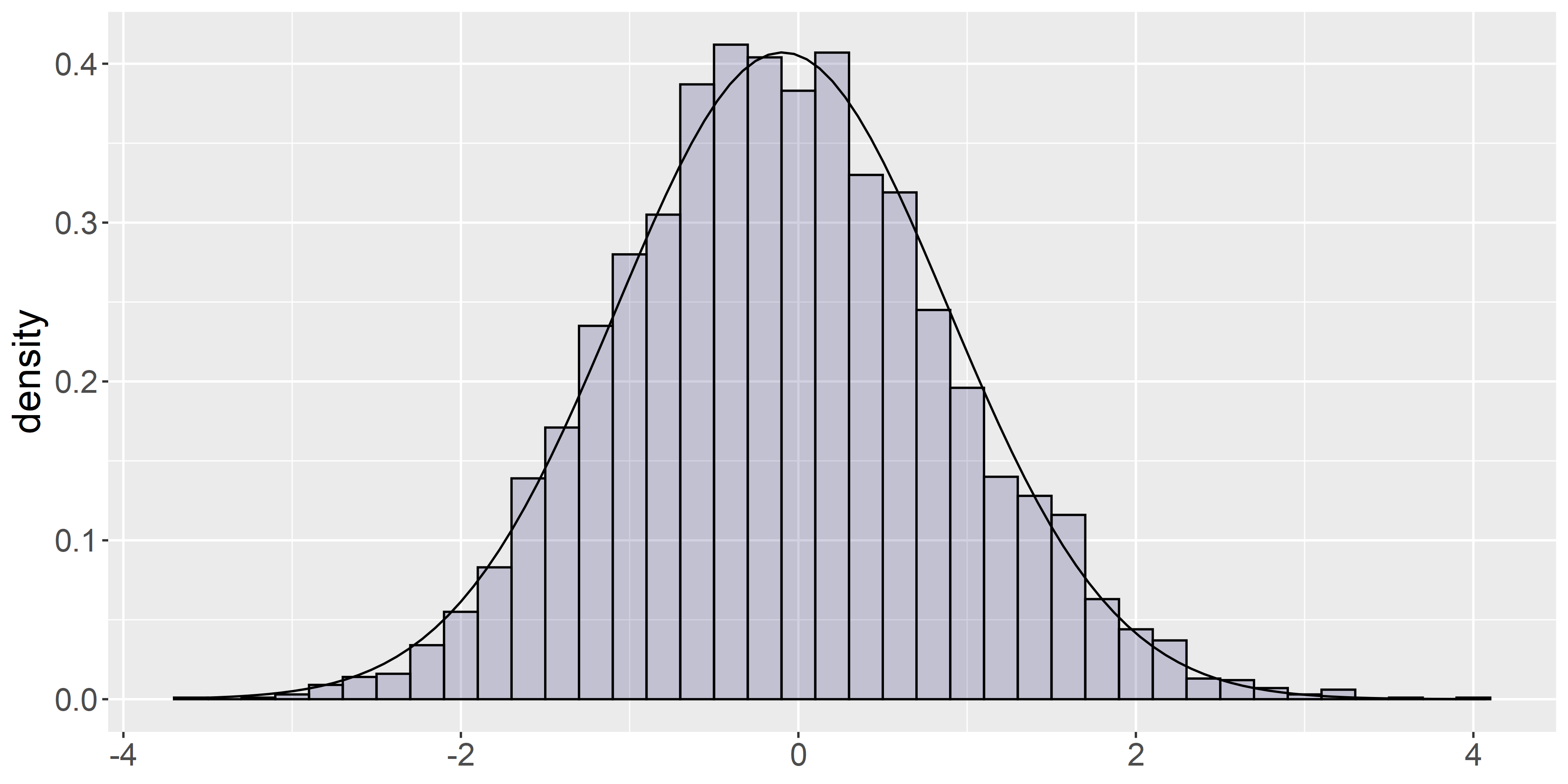

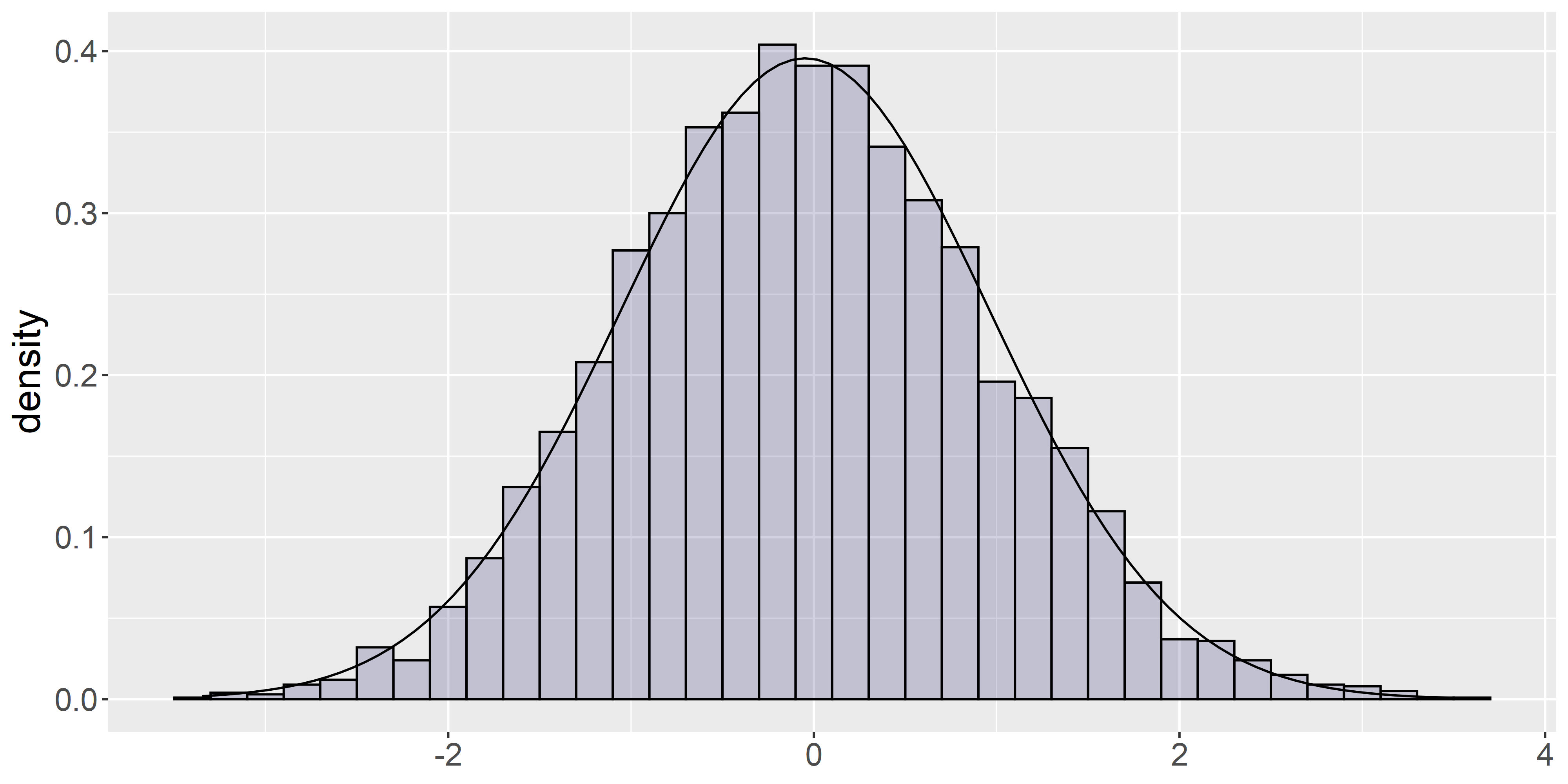

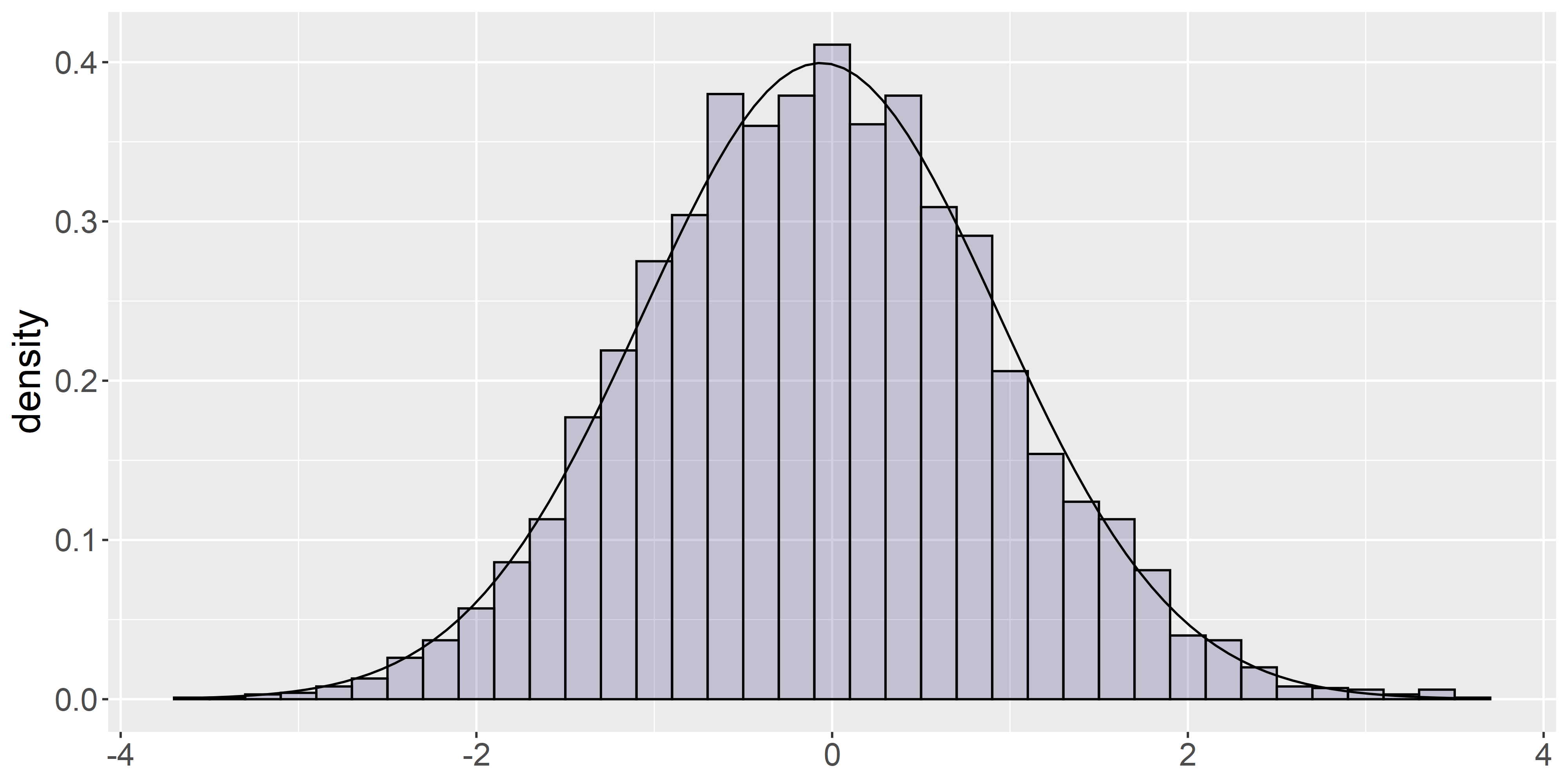

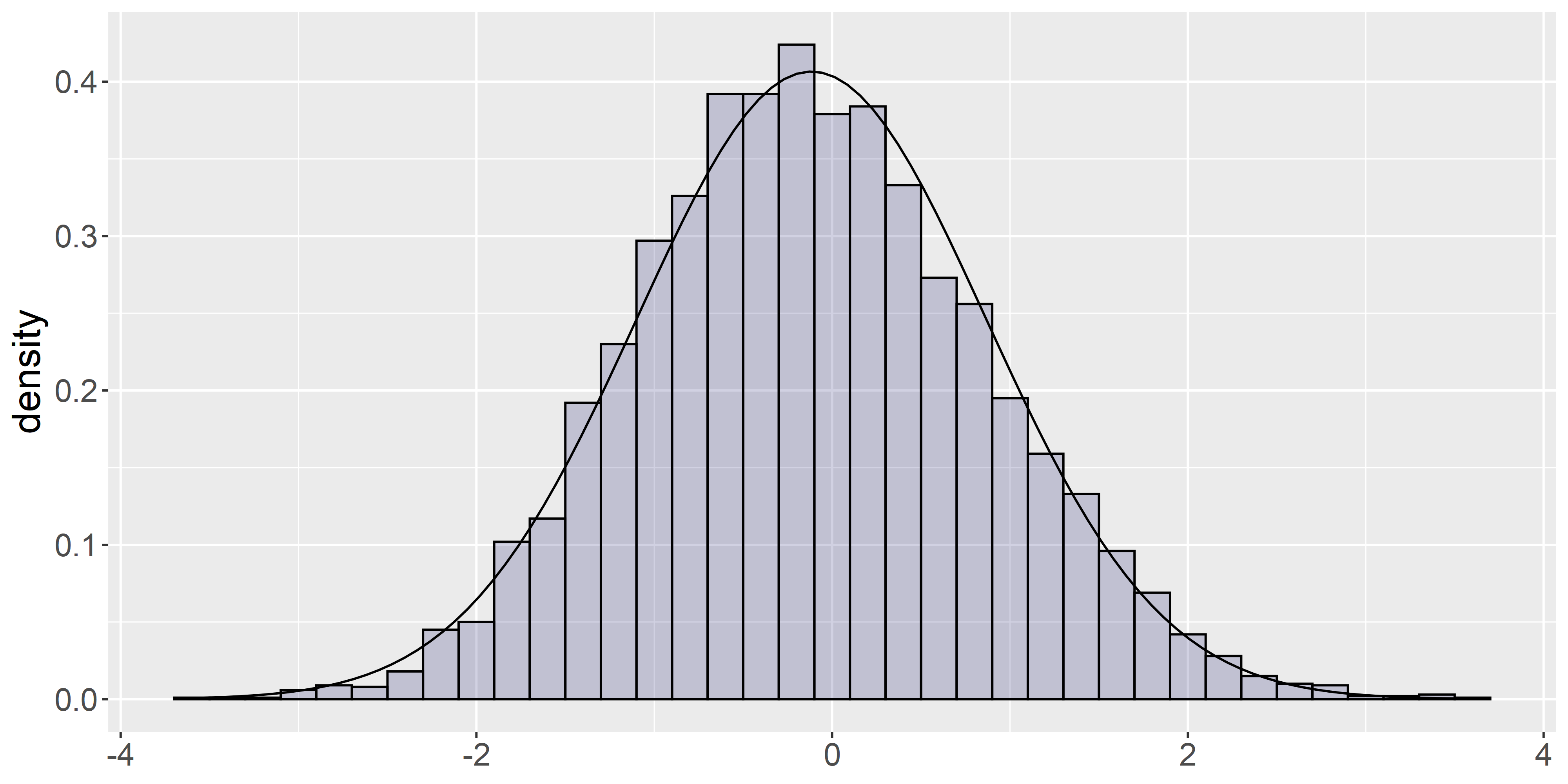

Figure 4 illustrates the approximate normality of the test statistic under the null. As noted in the literature (e.g. [14]), even with absolutely continuous regressors, the finite sample distribution of the test statistic typically places more mass on the negative axis. In particular, a test computed with the usual one-tailed Gaussian critical value may be slightly undersized in finite samples.

Next, we examine the sensitivity of the test statistic’s power as the level of singular contamination increases. This is incorporated into the data generating process through the mixture coefficient that appears in (29). We consider alternative models

| Nominal Size 1% | Nominal Size 5% | |||||

|---|---|---|---|---|---|---|

| 0.504 | 0.230 | 0.103 | 0.714 | 0.448 | 0.259 | |

| 0.728 | 0.431 | 0.208 | 0.876 | 0.657 | 0.422 | |

| 0.905 | 0.673 | 0.388 | 0.963 | 0.847 | 0.619 | |

| Nominal Size 1% | Nominal Size 5% | |||||

|---|---|---|---|---|---|---|

| 0.474 | 0.222 | 0.104 | 0.687 | 0.441 | 0.265 | |

| 0.678 | 0.411 | 0.204 | 0.839 | 0.643 | 0.423 | |

| 0.859 | 0.658 | 0.390 | 0.945 | 0.841 | 0.623 | |

As Tables 2 and 2 illustrate, the power exhibits a relevant dependence on the bandwidth. This is true even in the fully absolutely continuous case (see e.g. Table 2-4 in [40]). Denote by , the trigonometric functions appearing in the alternative models and above. From expanding (as in the proof of Theorem 3.10), the term that provides the positive bias under the alternative hypothesis is given by

Intuitively, as , the terms in this sum are nonzero only when is small and by uniform continuity this implies .

At all bandwidth levels, the test exhibits higher power as the weight on the singular component increases. The expected small ball probability increases as the weight on the singular component increases. The interpretation of this in finite samples is that, given any observation , there is a higher frequency of for which (and hence ) as the weight on the singular component increases. A larger bandwidth has a similar effect on the small ball probability, although it also influences the statistic through other factors, such as its interaction with the uniform continuity of .

Finally, we note that the situation in small to moderate samples also depends on the choice of used to construct the alternative. The trigonometric functions have comparable magnitude everywhere, thereby allowing us to focus more closely on the effects of singular contamination. By contrast, using a drift function that is large in magnitude away from the support of the singular component could result in a power loss as contamination increases (although, by Remark 4, this effect is expected to vanish in large samples, provided that the support of intersects the support of the singular component).

5 Discussion

This paper develops the limit theory for a class of kernel-weighted statistics when the underlying distribution of the conditioning variables admits a non-trivial Lebesgue decomposition. The limit theory for these statistics centers around the behavior of the expected small ball probability. Under the null, the usual kernel smoothed goodness-of-fit statistic converges weakly to a standard Gaussian for a large class of continuous measures. However, in contrast to the absolutely continuous case, the usual local power analysis of these statistics depends non-trivially on the direction of approach to the null model. We expect that our analysis has similar implications for the more complicated setups that make use of kernel smoothed statistics.

The results could be extended in future work in a number of directions. In this paper, we focus primarily on the goodness-of-fit statistic proposed in [40]. The results could be extended to other applications (e.g. [39, 10, 35, 22, 41]) that make use of an identical form of the statistic. As discussed in [11], this statistic is motivated by the moment condition . By contrast, the kernel-based goodness-of-fit statistics in [14] and [7] are motivated by the moment conditions and , respectively. In all cases, the test statistic is asymptotically equivalent to a quadratic form, and so an appropriately debiased version of the statistic has similar asymptotics to that of a degenerate U-statistic. We expect that our analysis could be extended to these cases. A more ambitious avenue would be to expand the investigation to accommodate the more complicated setups beyond goodness-of-fit testing that make use of kernel smoothed statistics.

Acknowledgments

The authors are grateful to Donald Andrews, Xiaohong Chen, Yuichi Kitamura, Renaud Raquépas, Michael R Sullivan and Edward Vytlacil for their suggestions and constructive comments.

Supplement to “Kernel-weighted specification testing under general distributions”. \sdescriptionThis supplemental file contains additional proofs and technical results omitted in the main text.

References

- [1] {barticle}[author] \bauthor\bsnmBierens, \bfnmHerman J\binitsH. J. and \bauthor\bsnmPloberger, \bfnmWerner\binitsW. (\byear1997). \btitleAsymptotic theory of integrated conditional moment tests. \bjournalEconometrica \bvolume65 \bpages1129–1151. \endbibitem

- [2] {barticle}[author] \bauthor\bsnmBlundell, \bfnmRichard\binitsR., \bauthor\bsnmChen, \bfnmXiaohong\binitsX. and \bauthor\bsnmKristensen, \bfnmDennis\binitsD. (\byear2007). \btitleSemi-nonparametric IV estimation of shape-invariant Engel curves. \bjournalEconometrica \bvolume75 \bpages1613–1669. \endbibitem

- [3] {barticle}[author] \bauthor\bsnmBurrough, \bfnmPeter A\binitsP. A. (\byear1981). \btitleFractal dimensions of landscapes and other environmental data. \bjournalNature \bvolume294 \bpages240–242. \endbibitem

- [4] {barticle}[author] \bauthor\bsnmChen, \bfnmSong Xi\binitsS. X. and \bauthor\bsnmVan Keilegom, \bfnmIngrid\binitsI. (\byear2009). \btitleA goodness-of-fit test for parametric and semi-parametric models in multiresponse regression. \bjournalBernoulli \bvolume15 \bpages955–976. \endbibitem

- [5] {barticle}[author] \bauthor\bsnmDavies, \bfnmSteve\binitsS. and \bauthor\bsnmHall, \bfnmPeter\binitsP. (\byear1999). \btitleFractal analysis of surface roughness by using spatial data. \bjournalJournal of the Royal Statistical Society: Series B (Statistical Methodology) \bvolume61 \bpages3–37. \endbibitem

- [6] {barticle}[author] \bauthor\bsnmDe Lellis, \bfnmCamillo\binitsC. (\byear2006). \btitleLecture notes on rectifiable sets, densities, and tangent measures. \bjournalPreprint \bvolume23. \endbibitem

- [7] {barticle}[author] \bauthor\bsnmDette, \bfnmHolger\binitsH. (\byear1999). \btitleA consistent test for the functional form of a regression based on a difference of variance estimators. \bjournalThe Annals of Statistics \bvolume27 \bpages1012–1040. \endbibitem

- [8] {barticle}[author] \bauthor\bsnmFan, \bfnmYanqin\binitsY. and \bauthor\bsnmLi, \bfnmQi\binitsQ. (\byear2000). \btitleConsistent model specification tests: Kernel-based tests versus Bierens’ ICM tests. \bjournalEconometric Theory \bvolume16 \bpages1016–1041. \endbibitem

- [9] {barticle}[author] \bauthor\bsnmGao, \bfnmJiti\binitsJ. and \bauthor\bsnmGijbels, \bfnmIrene\binitsI. (\byear2008). \btitleBandwidth selection in nonparametric kernel testing. \bjournalJournal of the American Statistical Association \bvolume103 \bpages1584–1594. \endbibitem

- [10] {barticle}[author] \bauthor\bsnmGao, \bfnmJiti\binitsJ., \bauthor\bsnmKing, \bfnmMaxwell\binitsM., \bauthor\bsnmLu, \bfnmZudi\binitsZ. and \bauthor\bsnmTjøstheim, \bfnmDag\binitsD. (\byear2009). \btitleSpecification testing in nonlinear and nonstationary time series autoregression. \bjournalThe Annals of Statistics \bvolume37 \bpages3893–3928. \endbibitem

- [11] {barticle}[author] \bauthor\bsnmGonzález-Manteiga, \bfnmWenceslao\binitsW. and \bauthor\bsnmCrujeiras, \bfnmRosa M\binitsR. M. (\byear2013). \btitleAn updated review of goodness-of-fit tests for regression models. \bjournalTest \bvolume22 \bpages361–411. \endbibitem

- [12] {barticle}[author] \bauthor\bsnmHall, \bfnmPeter\binitsP. (\byear1984). \btitleCentral limit theorem for integrated square error of multivariate nonparametric density estimators. \bjournalJournal of multivariate analysis \bvolume14 \bpages1–16. \endbibitem

- [13] {bbook}[author] \bauthor\bsnmHall, \bfnmPeter\binitsP. and \bauthor\bsnmHeyde, \bfnmChristopher C\binitsC. C. (\byear2014). \btitleMartingale limit theory and its application. \bpublisherAcademic press. \endbibitem

- [14] {barticle}[author] \bauthor\bsnmHardle, \bfnmWolfgang\binitsW. and \bauthor\bsnmMammen, \bfnmEnno\binitsE. (\byear1993). \btitleComparing nonparametric versus parametric regression fits. \bjournalThe Annals of Statistics \bpages1926–1947. \endbibitem

- [15] {barticle}[author] \bauthor\bsnmHärdle, \bfnmWolfgang\binitsW., \bauthor\bsnmMarron, \bfnmJames S\binitsJ. S. and \bauthor\bsnmWand, \bfnmMatten P\binitsM. P. (\byear1990). \btitleBandwidth choice for density derivatives. \bjournalJournal of the Royal Statistical Society: Series B (Methodological) \bvolume52 \bpages223–232. \endbibitem

- [16] {barticle}[author] \bauthor\bsnmHorowitz, \bfnmJoel L\binitsJ. L. and \bauthor\bsnmSpokoiny, \bfnmVladimir G\binitsV. G. (\byear2001). \btitleAn adaptive, rate-optimal test of a parametric mean-regression model against a nonparametric alternative. \bjournalEconometrica \bvolume69 \bpages599–631. \endbibitem

- [17] {barticle}[author] \bauthor\bsnmHsiao, \bfnmCheng\binitsC., \bauthor\bsnmLi, \bfnmQi\binitsQ. and \bauthor\bsnmRacine, \bfnmJeffrey S\binitsJ. S. (\byear2007). \btitleA consistent model specification test with mixed discrete and continuous data. \bjournalJournal of Econometrics \bvolume140 \bpages802–826. \endbibitem

- [18] {barticle}[author] \bauthor\bsnmHutchinson, \bfnmJohn E\binitsJ. E. (\byear1981). \btitleFractals and self similarity. \bjournalIndiana University Mathematics Journal \bvolume30 \bpages713–747. \endbibitem

- [19] {barticle}[author] \bauthor\bsnmKankanala, \bfnmSid\binitsS. and \bauthor\bsnmZinde-Walsh, \bfnmVictoria\binitsV. \btitleSupplement to “Kernel-weighted specification testing under general distributions”. \endbibitem

- [20] {barticle}[author] \bauthor\bsnmKoltchinskii, \bfnmVladimir\binitsV. and \bauthor\bsnmLounici, \bfnmKarim\binitsK. (\byear2017). \btitleNormal approximation and concentration of spectral projectors of sample covariance. \bjournalThe Annals of Statistics \bvolume45 \bpages121–157. \endbibitem

- [21] {bbook}[author] \bauthor\bsnmKunze, \bfnmHerb\binitsH., \bauthor\bsnmLa Torre, \bfnmDavide\binitsD., \bauthor\bsnmMendivil, \bfnmFranklin\binitsF. and \bauthor\bsnmVrscay, \bfnmEdward R\binitsE. R. (\byear2011). \btitleFractal-based methods in analysis. \bpublisherSpringer Science & Business Media. \endbibitem

- [22] {barticle}[author] \bauthor\bsnmLin, \bfnmZhongjian\binitsZ., \bauthor\bsnmLi, \bfnmQi\binitsQ. and \bauthor\bsnmSun, \bfnmYiguo\binitsY. (\byear2014). \btitleA consistent nonparametric test of parametric regression functional form in fixed effects panel data models. \bjournalJournal of Econometrics \bvolume178 \bpages167–179. \endbibitem

- [23] {barticle}[author] \bauthor\bsnmLuukkainen, \bfnmJouni\binitsJ. and \bauthor\bsnmSaksman, \bfnmEero\binitsE. (\byear1998). \btitleEvery complete doubling metric space carries a doubling measure. \bjournalProceedings of the American Mathematical Society \bvolume126 \bpages531–534. \endbibitem

- [24] {bbook}[author] \bauthor\bsnmMackay, \bfnmJohn M\binitsJ. M. and \bauthor\bsnmTyson, \bfnmJeremy T\binitsJ. T. (\byear2010). \btitleConformal dimension: theory and application \bvolume54. \bpublisherAmerican Mathematical Soc. \endbibitem

- [25] {barticle}[author] \bauthor\bsnmMammen, \bfnmEnno\binitsE., \bauthor\bsnmVan Keilegom, \bfnmIngrid\binitsI. and \bauthor\bsnmYu, \bfnmKyusang\binitsK. (\byear2019). \btitleExpansion for moments of regression quantiles with applications to nonparametric testing. \bjournalBernoulli \bvolume25 \bpages793–827. \endbibitem

- [26] {barticle}[author] \bauthor\bsnmMarron, \bfnmJ Steve\binitsJ. S. and \bauthor\bsnmWand, \bfnmMatt P\binitsM. P. (\byear1992). \btitleExact mean integrated squared error. \bjournalThe Annals of Statistics \bvolume20 \bpages712–736. \endbibitem

- [27] {barticle}[author] \bauthor\bsnmMeilán-Vila, \bfnmAndrea\binitsA., \bauthor\bsnmOpsomer, \bfnmJean D\binitsJ. D., \bauthor\bsnmFrancisco-Fernández, \bfnmMario\binitsM. and \bauthor\bsnmCrujeiras, \bfnmRosa M\binitsR. M. (\byear2020). \btitleA goodness-of-fit test for regression models with spatially correlated errors. \bjournalTEST \bvolume29 \bpages728–749. \endbibitem

- [28] {barticle}[author] \bauthor\bsnmMoore, \bfnmEdward F\binitsE. F. (\byear1950). \btitleDensity Ratios and (/phi, 1) Rectifiability in n-Space. \bjournalTransactions of the American Mathematical Society \bvolume69 \bpages324–334. \endbibitem

- [29] {barticle}[author] \bauthor\bsnmMüller, \bfnmUrsula U\binitsU. U. and \bauthor\bsnmVan Keilegom, \bfnmIngrid\binitsI. (\byear2019). \btitleGoodness-of-fit tests for the cure rate in a mixture cure model. \bjournalBiometrika \bvolume106 \bpages211–227. \endbibitem

- [30] {barticle}[author] \bauthor\bsnmPreiss, \bfnmDavid\binitsD. (\byear1987). \btitleGeometry of measures in Rn: distribution, rectifiability, and densities. \bjournalAnnals of Mathematics \bpages537–643. \endbibitem

- [31] {bbook}[author] \bauthor\bsnmRudin, \bfnmWalter\binitsW. (\byear1986). \btitleReal and Complex Analysis. \bpublisherMcGraw-Hill. \endbibitem

- [32] {barticle}[author] \bauthor\bsnmSant’Anna, \bfnmPedro HC\binitsP. H. and \bauthor\bsnmSong, \bfnmXiaojun\binitsX. (\byear2019). \btitleSpecification tests for the propensity score. \bjournalJournal of Econometrics \bvolume210 \bpages379–404. \endbibitem

- [33] {barticle}[author] \bauthor\bsnmSen, \bfnmArnab\binitsA. and \bauthor\bsnmSen, \bfnmBodhisattva\binitsB. (\byear2014). \btitleTesting independence and goodness-of-fit in linear models. \bjournalBiometrika \bvolume101 \bpages927–942. \endbibitem

- [34] {barticle}[author] \bauthor\bsnmShah, \bfnmRajen D\binitsR. D. and \bauthor\bsnmBühlmann, \bfnmPeter\binitsP. (\byear2018). \btitleGoodness-of-fit tests for high dimensional linear models. \bjournalJournal of the Royal Statistical Society: Series B (Statistical Methodology) \bvolume80 \bpages113–135. \endbibitem

- [35] {barticle}[author] \bauthor\bsnmShaikh, \bfnmAzeem M\binitsA. M., \bauthor\bsnmSimonsen, \bfnmMarianne\binitsM., \bauthor\bsnmVytlacil, \bfnmEdward J\binitsE. J. and \bauthor\bsnmYildiz, \bfnmNese\binitsN. (\byear2009). \btitleA specification test for the propensity score using its distribution conditional on participation. \bjournalJournal of Econometrics \bvolume151 \bpages33–46. \endbibitem

- [36] {bbook}[author] \bauthor\bparticleVan der \bsnmVaart, \bfnmAad W\binitsA. W. (\byear2000). \btitleAsymptotic statistics. \bpublisherCambridge university press. \endbibitem

- [37] {barticle}[author] \bauthor\bsnmVerzelen, \bfnmNicolas\binitsN. and \bauthor\bsnmVillers, \bfnmFanny\binitsF. (\byear2010). \btitleGoodness-of-fit tests for high-dimensional Gaussian linear models. \bjournalThe Annals of Statistics \bvolume38 \bpages704–752. \endbibitem

- [38] {barticle}[author] \bauthor\bsnmVolberg, \bfnmAlexander L’vovich\binitsA. L. and \bauthor\bsnmKonyagin, \bfnmSergei Vladimirovich\binitsS. V. (\byear1987). \btitleOn measures with the doubling condition. \bjournalMathematics of the USSR \bvolume51 \bpages666–675. \endbibitem

- [39] {barticle}[author] \bauthor\bsnmWang, \bfnmQiying\binitsQ. and \bauthor\bsnmPhillips, \bfnmPeter CB\binitsP. C. (\byear2012). \btitleA specification test for nonlinear nonstationary models. \bjournalThe Annals of Statistics \bvolume40 \bpages727–758. \endbibitem

- [40] {barticle}[author] \bauthor\bsnmZheng, \bfnmJohn Xu\binitsJ. X. (\byear1996). \btitleA consistent test of functional form via nonparametric estimation techniques. \bjournalJournal of Econometrics \bvolume75 \bpages263–289. \endbibitem

- [41] {barticle}[author] \bauthor\bsnmZheng, \bfnmJohn Xu\binitsJ. X. (\byear1998). \btitleA consistent nonparametric test of parametric regression models under conditional quantile restrictions. \bjournalEconometric theory \bvolume14 \bpages123–138. \endbibitem

Supplement to “Kernel-weighted specification testing under general distributions”

This supplemental file contains additional proofs and technical details omitted in the main text. For convenience, we first list some of the notation that was introduced in the main text and is frequently encountered in the proofs. Section 6 details a number of technical auxiliary lemmas that are used for the proofs of the main results. Section 7 contains the proofs of the statements appearing in the main text.

Given , we define the cube centered at with directions to be

Given any , define

| (S1) |

If and are defined as in Assumption , we denote the special case of by and , respectively. Additionally, we denote the case by

| (S2) |

Given a sufficiently differentiable function (in the sense of Definition ), we define

The sequence of local alternatives used in the local power analysis is denoted by

| (S3) |

The support of is denoted by . When can be expressed as a mixture that includes component , the notation and is used to indicate that the operators are defined with respect to .

6 Auxiliary Lemmas

Lemma 6.1.

Suppose with . Suppose has support contained in and is twice continuously differentiable on . Then the function

| (S4) |

is continuous on , has support contained in and is continuously differentiable on .

Proof of Lemma 6.1.

Since has support contained in and , it is straightforward to deduce that for and that . Let and denote by , the derivative of with respect to . From the hypothesis on , the functions and are uniformly continuous on the compact set . In the interior of , a straightforward application of the Leibniz rule yields

| (S5) |

Since , it follows that is continuous on and it admits a continuous extension to with

∎

Lemma 6.2.

Fix any and suppose Assumptions (1,3) hold. Then for every , there exists a universal constant such that

| (S6) |

holds for every . In particular, with we obtain that

| (S7) |

Proof of Lemma 6.2.

Without loss of generality, we take and to be non-negative.

Define

Let denote the coordinate of . Conditional on , satisfy the hypothesis of Lemma 3.2 with . Applying Lemma 3.2 yields

where the last equality follows from the change of variables . It follows that

where . The claim follows from repeating the argument with the roles of and reversed. ∎

Lemma 6.3.

Fix any non-negative functions and suppose Assumption 4(ii) holds. Then as , we have that

Proof of Lemma 6.3.

-

(i)

Let denote a fixed sequence of constants.

Clearly . For , Hölder’s inequality and Assumption 4(ii) yield

(S8) where

(S9) For the first term on the right side of (S8) we further obtain that

Combining the bounds yield

The result follows with .

-

(ii)

Let denote a fixed sequence of constants. Define

It follows that

For , monotonicity of the norm and Assumption 4(ii) yields

where

For , Cauchy-Schwarz yields

From combining the bounds, we obtain that

The result follows by letting sufficiently slowly, for e.g.

-

(iii)

The result follows immediately from part (ii) and an application of Cauchy-Schwarz.

∎

Lemma 6.4.

Define

| (S10) |

Suppose Assumptions 1-4 hold and . Then

Proof of Lemma 6.4.

By Markov’s inequality it suffices to verify that

where

The expression in the sum is equal to when the indices are all distinct. When the indices are not all distinct, Cauchy-Schwarz yields

In the sum, there are terms that correspond to distinct indices and terms otherwise. It follows that

By Lemma 3.5 and Assumption 4(i) we have that . This and Corollary 3.4(ii) imply

Since , we obtain that

∎

Lemma 6.5.

Let Assumptions 1-5 hold and . Suppose further that the alternative hypothesis in (S3) holds with and . Then

Proof of Lemma 6.5.

Observe that

where is as in (S10). By Lemma 6.4, . Therefore, it suffices to verify that . The mean value theorem implies that there exists a on the line segment connecting and such that

| (S11) |

Since , it suffices to work under the setting where and lie in the neighborhood of Assumption 5. Let be as in Assumption 5. Write the estimator as

We will verify that . The argument for is completely analogous and omitted. Observe that

| (S12) |

From this bound, we obtain

From (S19) and Cauchy-Schwarz we have that

| (S13) | |||

| (S14) |

From substituting this into the previous bound, we obtain that

where

We will verify that for . Before proceeding with the bounds, we state a few preliminary facts. By Lemma 3.5 and Assumption 4(i) we have . By Corollary 3.4(ii) we have .

-

(1)

Markov’s Inequality and imply

By assumption . It follows, by Lemma 6.2, that all the expectations above are . Substituting yields

Since and , it follows that .

-

(2)

Markov’s Inequality, Assumption 2(ii) and imply

By Lemma 6.2, the first three expectations are . For the last expectation, we use Lemma 6.2 and to obtain

Substituting yields

Since and , it follows that .

-

(3)

Markov’s Inequality, Assumption 2(ii) and imply

-

(4)

The argument to show is completely analogous to the one used for .

-

(5)

Markov’s Inequality, Assumption 2(ii) and imply

-

(6)

Substituting yields

Since and , it follows that .

∎

Lemma 6.6.

Suppose the conditions of Theorem hold and . Assume the alternative hypothesis in (S3) holds with and . Then

Proof of Lemma 6.6.

The proof is analogous to that of Lemma 6.5. The main difference being that we allow for and that the upper bound on the rate in this Lemma may be larger than allowed for in Lemma 6.5.

Let be as defined in the proof of Lemma 6.5. We will verify that for . Before proceeding with the bounds, we state a few preliminary facts. As shown in the proof of Theorem , there exists a such that

| (S15) |

holds for all sufficiently small . By Lemma 3.7, we have for some and . Assumptions (4, 6) are automatically satisfied. Then, by Lemma 3.5 and Assumption 4(i), we have as well.

-

(1)

Markov’s Inequality and imply

By assumption . It follows, by Lemma 6.2, that all the expectations above are . Substituting yields

Since and , it follows that .

-

(2)

Markov’s Inequality, Assumption 2(ii) and imply

By Lemma 6.2, the first three expectations are and

By Cauchy-Schwarz, we obtain

From this bound and (S15) it follows that

Substituting yields

Since and , it follows that .

-

(3)

Markov’s Inequality, Assumption 2(ii) and imply

-

(4)

The argument to show is completely analogous to the one used for .

-

(5)

Markov’s Inequality, Assumption 2(ii) and imply

Substituting yields

Since and , it follows that .

-

(6)

Markov’s Inequality, Assumption 2(ii) and imply

Substituting yields

Since and , it follows that .

∎

7 Proofs

7.1 Lemma 3.2

Proof of Lemma 3.2.

The function is a finite Borel measure on , which we will refer to as . Since has support contained in the closure of , the expectation can be expressed as

At the boundary of , we define the mixed partials of through continuous extension. Fix any . The assumed hypothesis on and its mixed partials imply that

Substitution of this identity and an application of Fubini’s Theorem yields

∎

7.2 Lemma 3.3

Proof of Lemma 3.3.

The proof of part is provided in the main text. We focus on and here.

-

(ii)

The proof follows the same steps as in part .

Define

Let denote the coordinate of . Conditional on , satisfy the hypothesis of Lemma 3.2 with . Applying Lemma 3.2 yields

where the last equality follows from the change of variables . It follows that

Define to be the partitioned vector with . For any fixed choice of , we have

where the second equality follows from the change of variables and ( is a symmetric function). Iterating this procedure from to yields

The expression for follows from substituting .

-

(iii)

Define

Conditional on , satisfy the hypothesis of Lemma 3.2 with . Applying Lemma 3.2 yields

where the last equality follows from the change of variables . By using Hölder’s inequality on the final expression above we obtain

Note that from which we obtain

Define

Let denote the coordinate of . Since is a product kernel, we have that

By Lemma 6.1 with , , the function is continuously differentiable on . It follows that satisfy the hypothesis of Lemma 3.2 with . Applying Lemma 3.2 yields

where the last equality follows from the change of variables .

∎

7.3 Corollary 3.4

Proof of Corollary 3.4.

-

(i)

The support of can be represented as . By Lemma 3.3 we obtain

Denote the maximal function associated to by

(S16) The integrand of the expectation can be dominated (up to a constant) by

It is well known (see for e.g. [2]) that the maximal operator is strong type bounded so that . By Cauchy-Schwarz, . Dominated convergence and Lebesgue’s differentiation theorem [1, Theorem 7.10] yield

where the second-last equality follows noting that is an even function and the last equality follows from univariate integration by parts.

-

(ii)

Note that for every so that the integrand defining in Lemma 3.3 is non-negative. The case where is absolutely continuous (but not necessarily with a bounded density) follows from Fatou’s Lemma and expressing the limit as in part (i).

If is not absolutely continuous, then the singular measure in the Lebesgue decomposition of is non-trivial. Define the probability measure and let be defined the same way as in (S2) but with replacing . By Lemma 3.3 and Assumption 2(iii), we obtain

Fix any . Then Assumption 3 implies and a straightforward application of [1, Theorem 7.15] yields almost everywhere with respect to . As this measure is non-trivial and the integrand is non-negative, Fatou’s lemma yields

∎

7.4 Lemma 3.5

Proof of Lemma 3.5.

-

(i)

The lower bound was provided in the main text. Here, we bound the moment from above. Note that for every . From the expression defining in Lemma 3.3 we obtain that

where is as in Assumption 2 and .

-

(ii)

The bound follows from the same argument as in part (i) by replacing with .

-

(iii)

By Lemma 3.3(iii), we have that

for some universal constant . Since the outer integral is over , we further obtain that

for some universal constant . The claim follows from using Assumption 2(ii) to bound the expression on the right.

∎

7.5 Lemma 3.7

Proof of Lemma 3.7.

-

(i)

Fix any . From the definition of and an application of Fatou’s Lemma, we obtain that as

Assumption 4 follows immediately.

-

(ii)

The second condition of Definition 3.6 follows from

From Definition 3.6, there exist constants such that

(S17) We claim that the mixture measure satisfies the first condition of Definition 3.6 with . Let denote the set where (S17) holds under the measure . In particular, we have that . Therefore, it suffices to verify

Fix any . If , we have that

Fix any such that . Then either the set is non-empty or (because ). In the former case, we have for any fixed the inclusion and the bound

Since this holds for every , we obtain that

Since this holds for every , we obtain that

∎

7.6 Theorem 3.9

Proof of Theorem 3.9.

The null hypothesis is a special case of the alternative with the choices and . Hence, by an application of Lemma 6.5, we have that . Therefore, it suffices to verify

| (S18) |

The mean value theorem implies that there exists a on the line segment connecting and such that

| (S19) |

Since , it suffices to work under the setting where and lie in the fixed neighborhood of Assumption 5.

The statistic can be expressed as

The result follows from Theorem 3.8 if for .

-

(i)

We verify that . From (S19) we obtain

Observe that and

Since , the desired result follows if we can verify that

By Lemma 3.5 and Assumption 4(i), we have and the claim follows.

-

(ii)

We verify that . A second order Taylor expansion of around yields

where is on the line segment connecting and . Since , it suffices to verify that

(S20) For , the triangle inequality and Assumptions (2, 5) yield

By Lemma 6.2, we obtain

From Hölder’s inequality and Assumption 4(ii), it follows that

where

(S21) The bound for in (S20) now follows from substituting .

For , let and denote respectively, the coordinate of the vectors and . The bound for in (S20) follows if we can show that for every coordinate . From the definition of , we obtain

For the second term, since is bounded and , we have that . By Corollary 3.4, and we obtain

For the first term, since are i.i.d, we obtain that

(S22) Define

Let denote the coordinate of . Conditional on , satisfy the hypothesis of Lemma 3.2 with . Applying Lemma 3.2 yields

(S23) where the third equality follows from the change of variables and the support of . The last equality follows from Lemma 6.3. From substituting , we obtain that .

∎

7.7 Theorem 3.10

Proof of Theorem 3.10.

By Lemma 6.5, we have that . Therefore, it suffices to study the limiting behavior of . The numerator of the statistic can be expressed as

where

From the proof of Theorem 3.8 and 3.9, we have that

| (S24) |

It remains to derive the asymptotics for and . The mean value theorem implies that there exists a on the line segment connecting and such that

| (S25) |

Since , it suffices to work under the setting where and lie in the neighborhood of Assumption 5.

- (a)

-

(b)

We verify that under both parts (i) and (ii) of Theorem 3.10. From Assumption 2 we obtain

From and Lemma 6.2 we obtain

By an analogous argument to ((c)) we obtain

By Markov’s inequality and we obtain

From substituting it follows that

By Corollary 3.4(ii), . As the first term on the right is . The second term is by Assumption 6.

-

(c)

We aim to show that

(S26) (S27) An analogous argument to the one used for Lemma 3.3 yields

The support of can be expressed as

Define

It follows that

For every we have that

uniformly over . Hence

Since is uniformly continuous on and , the preceding bound implies (S26).

-

(d)

It remains to prove the statement of the theorem. Combining the bounds derived in shows that

where

Define

Note that

From substituting , it follows that

In particular , provided that

Additionally, if is as in Assumption 4, we have that

In particular , provided that

∎

7.8 Theorem 3.11

Proof of Theorem 3.11.

First, we claim that there exists a such that

| (S28) |

holds for all sufficiently small . Since and for every , (S28) follows if we can verify that there exists a such that

| (S29) |

Fix any . If and , this follows from Condition (27) in the main text. For any with , let denote the set where the first condition of Definition 3.6 holds (with constant ). If , then because . If , then either or there exists some such that (because ). We have the inclusion and it follows that

because .

From combining the cases, we obtain (S28).

With (S28) established, the majority of the proof is analogous to the proof of Theorem 3.10, with some arguments modified to take into account the weaker requirement that . We provide the details for the main changes in the argument.

By Lemma 6.6, we have that . Therefore, it suffices to study the limiting behavior of . Let be as in the proof of Theorem 3.10. Define . By Lemma 3.7, we have and . Assumptions (4, 6) are automatically satisfied. By Lemma 3.5 and Assumption 4(i) we have as well.

- (a)

-

(b)

We verify that under both parts (i) and (ii) of Theorem 3.11. Suppose . From the argument in Theorem 3.10, we obtain

(S30) where

Without loss of generality, we take to be non-negative so that the absolute values can be dropped. From Lemma 6.2 and (S28) we obtain

For , we note that

By an analogous argument to the expansion of in Lemma 3.3 and (S28) we obtain

Given a positive sequence , define

From an application of Cauchy-Schwarz on , we obtain

Substituting this into the expectation and using (S28) yields

Letting sufficiently slowly, for e.g. , yields . From substituting the bounds for and into (S30) we obtain

This second term is because and the first is because and .

-

(c)

We aim to show that

(S31) (S32) Suppose . A derivation with steps similar to the proof of Lemma 3.3(i) yields

Define, as in the proof of Theorem , the quantity

It follows that

where the last equality follows from (S28).

We now verify (S32). Let and define

To show (S32), it suffices to verify

The result for follows immediately from the assumption that . Indeed, for any , we have that

Next, we verify the estimate for . Note that

By arguing in an analogous way to the derivation of in (S31), we obtain

Similarly, we obtain that

Substituting , we obtain

Finally, we verify the estimate for . By arguing analogously as in the proof of Theorem 3.10, the variance of has order

where

By Lemma 6.2 and (S28), we obtain

Since are i.i.d we obtain that

(S33) Define

Let denote the coordinate of . Conditional on , satisfy the hypothesis of Lemma 3.2 with . Applying Lemma 3.2 yields

where the third equality follows from the change of variables and the support of . It follows that

By Cauchy-Schwarz, and we obtain using (S28) that

By substituting , it follows that

This term is because and .

-

(d)

It remains to prove the statement of the theorem. Combining the bounds derived in shows that

where

Define

Note that by (S28) we have

It follows that

For any fixed , we have that

The result follows from substituting .

∎

References

- [1] Walter, Rudin. Real and Complex Analysis. McGraw Hill, 1987.

- [2] Journé, J-L. The Hardy-Littlewood Maximal Operator. In Calderón-Zygmund Operators, Pseudo-Differential Operators and the Cauchy integral of Calderón. pp. 7-15. Springer, 1983.