A Bootstrap-Assisted Self-Normalization Approach to Inference in Cointegrating Regressions

Abstract

Traditional inference in cointegrating regressions requires tuning parameter choices to estimate a long-run variance parameter. Even in case these choices are “optimal”, the tests are severely size distorted. We propose a novel self-normalization approach, which leads to a nuisance parameter free limiting distribution without estimating the long-run variance parameter directly. This makes our self-normalized test tuning parameter free and considerably less prone to size distortions at the cost of only small power losses. In combination with an asymptotically justified vector autoregressive sieve bootstrap to construct critical values, the self-normalization approach shows further improvement in small to medium samples when the level of error serial correlation or regressor endogeneity is large. We illustrate the usefulness of the bootstrap-assisted self-normalized test in empirical applications by analyzing the validity of the Fisher effect in Germany and the United States.

Keywords: Sieve bootstrap, Size distortions, Tuning Parameters

JEL classification: C12, C13, C32

1 Introduction

Tuning parameter choices complicate statistical inference in cointegrating regressions and affect finite sample distributions of test statistics. Even in case these choices are “optimal”, hypothesis tests are often severely size distorted. In this paper we address this issue by proposing a novel self-normalized test statistic for general linear hypotheses, that itself is completely tuning parameter free.111The term “self-normalization” was coined in \citeasnounSh10, who extends the method of \citeasnounLo01 to inference for a general parameter in a stationary time series setting. The distinctive feature of “self-normalization” is that it leads to asymptotically pivotal test statistics without requiring the applied researcher to make tuning parameter choices. Its limiting distribution is non-standard but simulating asymptotically valid critical values is straightforward. In addition, we provide a resampling procedure to construct bootstrap critical values and justify their use by proving a bootstrap invariance principle that may be of independent interest.

Cointegration methods have been and are widely used to analyze long-run relationships between stochastically trending variables in many areas such as macroeconomics, environmental economics and finance, see, e. g., \citeasnounBLNW20, \citeasnounWa15 and \citeasnounRLF16 for recent examples. In addition to these classical fields of application, cointegration methods have recently proven to be useful to describe phenomena also in other contexts. For instance, \citeasnounDKN18 describe the close connection between cointegration and the theory of phase synchronization in physics and \citeasnounPLS20 apply cointegration-based methods to estimate Earth’s climate sensitivity.

Although the OLS estimator is consistent in cointegrating regressions, its limiting distribution is usually contaminated by second order bias terms, reflecting the correlation structure between regressors and errors. This makes the OLS estimator infeasible for conducting inference based on (simulated) quantile tables of (non)standard distributions. The literature provides several estimators which overcome this difficulty at the cost of tuning parameter choices: the number of leads and lags for the dynamic OLS (D-OLS) estimator of \citeasnounPhLo91, \citeasnounSa91 and \citeasnounStWa93, kernel and bandwidth choices for the fully modified OLS (FM-OLS) estimator of \citeasnounPhHa90 and the canonical cointegrating regression (CCR) estimator of \citeasnounPa92, or type and number of basis functions for the trend instrument variable (TIV) estimator of \citeasnounPh14. In addition, traditional hypothesis tests based on these estimators require kernel and bandwidth choices to estimate a long-run variance parameter. Such tuning parameters are often difficult to choose in practice and the finite sample performance of the estimators and tests based upon them often reacts sensitively to their choices. In particular, corresponding tests often suffer from severe size distortions.

In contrast to the aforementioned approaches, the integrated modified OLS (IM-OLS) estimator of \citeasnounVoWa14 avoids the choice of tuning parameters. However, standard asymptotic inference based on the IM-OLS estimator still involves estimating a long-run variance parameter. To capture the effects of the required kernel and bandwidth choices in finite samples, \citeasnounVoWa14 propose fixed- theory for obtaining critical values. However, their simulation results reveal that when endogeneity and/or error serial correlation is strong, a large sample size is needed for the procedure to yield reasonable sizes. Moreover, for small to medium samples, test performance still seems to be sensitive to the choice of . Similarly, \citeasnounHwSu18 develop “partial” fixed- theory for the TIV estimator, which captures the choice of the number of basis functions but ignores the impact of the basis functions itself.

Instead of trying to capture finite sample effects of tuning parameter choices, we propose a novel IM-OLS based test statistic for general linear hypotheses, which is completely tuning parameter free. The test statistic is based on a self-normalization approach that is similar in spirit to but different from the approach of \citeasnounKVB00 for stationary data. The limiting null distribution of the self-normalized test statistic is nonstandard but simulating asymptotic critical values is straightforward. The idea of inference based on self-normalized test statistics has been proven to be widely applicable in stationary time series analysis, see \citeasnounSh15 for a detailed review.222Self-normalization has also been applied to testing for a unit root in univariate time series, monitoring cointegrating relationships and the analysis of high-dimensional stationary time series, see \citeasnounBr02, \citeasnounKWG21 and \citeasnounWaSh20, respectively.

To further improve the performance of the self-normalized test in small to medium samples, we combine the self-normalization approach with a residual-based vector autoregressive (VAR) sieve resampling procedure to construct critical values.333The VAR sieve bootstrap is frequently used in related literature: \citeasnounPs01, inspired by the seminal work of \citeasnounLiMa97, shows the usefulness of the sieve bootstrap in cointegrating regressions and \citeasnounPa02 provides its asymptotic justification by proving an underlying invariance principle result. Subsequently, \citeasnounChPa03 and \citeasnounCPS06 apply the sieve bootstrap to unit root testing and to conduct D-OLS based inference in cointegrating regressions, respectively. Note, however, that the approach of \citeasnounCPS06 still requires the choice of leads and lags for estimation and additional kernel and bandwidth choices for inference. Moreover, \citeasnounPSU10 use the sieve bootstrap in the context of testing for cointegration in conditional error correction models. The VAR sieve bootstrap captures the second-order dependence structure of the original process in a simple manner. In particular, it only requires the selection of the order of the VAR, which is a straightforward and well understood task in practice.

To show consistency of the VAR sieve bootstrap in our context, we establish a bootstrap invariance principle result under relatively general conditions that may be of independent interest. Our framework allows for so-called weak white noises that are uncorrelated, but not necessarily independent, and also for various concepts to quantify such weak forms of dependence of the innovation process. In particular, we do not impose the assumption of a causal linear process with i.i.d. innovations as used in, e. g., \citeasnounPa02.

The theoretical analysis is complemented by a simulation study to assess the performance of the proposed methods benchmarked against competing approaches, including the traditional D-OLS and FM-OLS based Wald-type tests. The main result is that the traditional tests show severe size distortions, whereas our novel approach, which combines the concepts of self normalization and bootstrapping, proves to hold the prescribed level approximately at the expense of only small power losses. Given that large size distortions of hypothesis tests are the rule rather than the exception in the cointegrating literature, the small power losses may be accepted by the applied researcher.

We illustrate the usefulness of the bootstrap-assisted self-normalized test in empirical applications by analyzing the validity of the Fisher effect in Germany and the United States. The Fisher effect is backed by several theoretical models, but many empirical studies reject the hypothesis that inflation and the short-term nominal interest rate cointegrate with the slope of inflation being equal to one. The errors in this regression are likely to be highly persistent even in case cointegration between the two variables prevails. As a consequence, the Fisher effect might be rejected solely due to the adverse effects of highly persistent errors on the performance of the estimators and tests chosen by the applied researcher, see, e. g., \citeasnounCaPi04 and \citeasnounWe08 for a detailed discussion. The bootstrap-assisted self-normalized test remedies these shortcomings, as it leads to reliable inference even in the presence of highly persistent errors.

The rest of the paper is organized as follows: Section 2 introduces the model and its underlying assumptions. Section 3 constructs the self-normalized test statistic and derives its limiting null distribution. Section 4 presents the bootstrap procedure and derives its asymptotic validity. Section 5 assesses the finite sample performance of the proposed methods and Section 6 illustrates the usefulness of the bootstrap-assisted self-normalized test in empirical applications. Section 7 concludes. The Online Appendix contains additional theoretical and finite sample results, tabulated critical values and proofs.

We use the following notation. The integer part of a real number is denoted by . For a real matrix we denote its transpose by and its Frobenius norm by , where denotes the trace and for a vector the Frobenius norm becomes the Euclidean norm. The -dimensional identity matrix is denoted by and (or simply ) denotes a ()-dimensional matrix of zeros. With we denote a (block) diagonal matrix with diagonal elements specified throughout. Equality in distribution is signified by . With and we denote weak convergence and convergence in probability, respectively. Adding the superscript “” signifies convergence in the bootstrap probability space. The corresponding probability measure is denoted by and denotes the expectation with respect to . For notational simplicity, a Brownian motion is denoted by .

2 The Model and Assumptions

We consider the cointegrating regression model

| (2.1) | ||||

| (2.2) |

, where is a scalar time series and is an vector of time series.444We exclude deterministic regressors from (2.1) to ease exposition of the main arguments. However, it is straightforward to incorporate, e. g., the leading case of an intercept and polynomial time trends, , . Please note that the accompanying MATLAB code allows to handle this more general case. For brevity we set . For we assume the following:

Assumption 1.

Let be an -valued, strictly stationary and purely nondeterministic stochastic process of full rank555The process is of full rank, if the components of its innovation process are linearly independent. For more details we refer to \citeasnoun[p. 379]MeKr15, who study the range of validity of the VAR sieve bootstrap. with and, for some . The autocovariance matrix function of fulfills for some . For the spectral density matrix of we assume that there exists a constant such that for all frequencies , where denotes the spectrum of at frequency .

The short memory condition for some in Assumption 1 implies a continuously differentiable spectral density , which is particularly bounded from below and from above, uniformly for all frequencies . As shown in \citeasnounMeKr15, a process fulfilling Assumption 1 does always possess the one-sided representations

| (2.3) | ||||

| (2.4) |

where is a strictly stationary uncorrelated – but not necessarily independent – white noise process with positive definite covariance matrix , and , with and for the from Assumption 1. Moreover, it holds that and for all .

Assumption 2.

The process has absolutely summable cumulants up to order four. More precisely, we have for all and , with , that

where denotes the -th joint cumulant of and denotes the -th element of .

Let denote the long-run covariance matrix of , i. e.,

From and it follows that . In particular, positive definiteness of rules out cointegration among the elements of . As typical in the cointegration literature, we assume that fulfills an invariance principle.

Assumption 3.

Let fulfill

| (2.5) |

as , where is an -dimensional vector of independent standard Brownian motions and

where , such that . For later usage note that is a scalar and partition .

We emphasize that Assumption 1 does explicitly not ask for invertibility or causality of the process with respect to an independent white noise process, in contrast to the assumptions in related literature, compare, e. g., \citeasnounPa02, \citeasnounCPS06 and \citeasnounPSU10. In particular, in this paper, the innovation process resulting from the representations in (2.3) and (2.4) will generally be uncorrelated but not necessarily independent. Assumption 2 is of technical nature and satisfied if, e. g., is -mixing with strong-mixing coefficients such that and for some , see, e. g., \citeasnoun[p. 221]Sh10. In particular, Assumption 2 requires the existence of fourth moments of . To establish meaningful asymptotic theory, Assumptions 1 and 2 have to be complemented by an invariance principle in Assumption 3. This general formulation of an invariance principle allows for various concepts of choice to quantify weak forms of dependence of the innovation process . These include classical approaches sufficing to prove invariance principles, e. g., several variants of mixing properties, mixingale-type sequences, linear processes including all-pass filters and their multivariate extensions, or (Bernoulli) shift processes, see \citeasnounMPU06 for an overview.666All-pass filters, discussed for univariate times series in, e. g., \citeasnounADB07, lead to uncorrelated, but dependent white noise processes. \citeasnounLaSa13 propose their multivariate extensions based on non-causal and non-invertible vector-valued time series models. In addition, the general formulation also allows for more modern approaches that cover the general notion of weakly dependent stationary time series discussed in \citeasnounDoWi07 or physical dependence proposed by \citeasnounWu05 and employed in \citeasnounWu07 to prove (strong) invariance principles. Finally, note that Assumption 3 suffices to derive the limiting distribution of the self-normalized test statistic defined in Section 3. Assumptions 1 and 2 are required only to show bootstrap consistency in Section 4.

3 Testing General Linear Hypotheses

In cointegrating regressions the OLS estimator is consistent, but its limiting distribution is contaminated by second order bias terms. The bias terms reflect the correlation structure between the regressors and the errors and make the OLS estimator unsuitable for conducting asymptotic inference using (simulated) quantile tables of (non)standard distributions. The literature provides several modified estimators that allow for standard asymptotic inference, compare the discussion in the introduction. For our purposes, we choose the tuning parameter free and easy to implement IM-OLS approach of \citeasnounVoWa14.

3.1 The IM-OLS Estimator Revisited

VoWa14 propose to compute the partial sum of both sides of (2.1), then to add as a regressor to the partial sum regression and finally to estimate the regression coefficients by OLS.777Adding to the partial sums regression serves as an endogeneity correction, which is similar to the leads and lags augmentation in D-OLS estimation. Although similar in spirit, it is considerably simpler as it avoids choosing the numbers of leads and lags. That is, by computing the OLS estimator in the augmented partial sums regression

| (3.1) |

with , , and the -dimensional vector , the IM-OLS estimator for in (3.1) is obtained. As shown in \citeasnoun[Theorem 2]VoWa14 it holds under Assumption 3 that the limiting distribution of is given by

| (3.2) |

as , where and

| (3.3) |

with and .888Since both and are I(1) processes, all correlation – between and – is soaked up in the long-run population regression vector . Therefore, the correct centering parameter for in case of endogeneity is rather than the population value . For more details see \citeasnoun[p. 746]VoWa14. Conditional upon , the asymptotic distribution in (3.2) is normal with zero-mean and covariance matrix , where

| (3.4) | ||||

| (3.5) |

with implicitly defined by the last equality. Let and define

| (3.6) |

where and , with , for . Then,

| (3.7) |

as , compare \citeasnoun[Proof of Theorem 3]VoWa14.

Remark 1.

The IM-OLS estimator is rate- consistent, but its conditional asymptotic covariance matrix is always larger than (or equal to) the conditional asymptotic covariance matrix of the rate- consistent D- and FM-OLS estimators \citeaffixed[Proposition 2]VoWa14see. This stems from the fact that the error in the augmented partial sum regression is integrated rather than stationary. However, this comparison may be misleading, as the asymptotic covariance matrix of the D- and FM-OLS estimators does not account for the finite sample effects of tuning parameter choices required for the D- and FM-OLS estimators but not for the IM-OLS estimator. Simulation results in \citeasnounVoWa14 and in Section C.1 in Online Appendix C demonstrate that the IM-OLS estimator performs well relative to the two competitors. The IM-OLS estimator thus serves as a useful starting point for developing a self-normalized test statistic.

3.2 The Self-Normalized Test Statistic

The zero mean Gaussian mixture limiting distribution of the IM-OLS estimator in conjunction with (3.7) forms the basis for standard asymptotic inference based on the traditional Wald-type hypothesis test. To be more precise, for testing linearly independent restrictions on in (2.1), we consider the hypotheses

| (3.8) |

where has full row rank and . For deriving the limiting null distribution of the corresponding Wald-type test statistic, it is convenient to rewrite the null hypothesis in terms of the correct centering parameter for , given by . To this end, we define such that the null hypothesis in (3.8) reads as .999Note that the auxiliary coefficient vector is not restricted under the null hypothesis and, in particular, does not have to be estimated.

Under Assumption 3 it follows from \citeasnoun[Theorem 3]VoWa14 that the limiting distribution of the Wald-type test statistic

converges under the null hypothesis in distribution to

| (3.9) |

as , where is defined in (3.3) and denotes a chi-square distribution with degrees of freedom.101010In practical applications it might be more convenient to express this – and the following – test statistic(s) in terms of and , only. This can be achieved by noting that and , where denotes the upper left -dimensional block of the -dimensional matrix . The limiting null distribution of is contaminated by a nuisance parameter, .111111As pointed out in \citeasnoun[Remark 4.6(d)]Ph95, is the long-run variance of the regression error corrected for its conditional long-run mean given . The dependence of the limiting distribution on rather than on the long-run variance of the regression errors follows from the endogeneity correction within the IM-OLS procedure. The presence of the long-run variance parameter makes the limiting distribution highly case dependent and thus infeasible for inference based on tabulated critical values.121212Analogous results also hold for the Wald-type tests based on the D-OLS, FM-OLS and CCR estimators. To remedy this problem, the literature suggests to plug-in a consistent estimator of , say, such that the nuisance parameter is scaled out in the limit. For this purpose, we denote

| (3.10) |

with denoting a one-dimensional quantity. For we thus have . Hence, the literature typically considers Wald-type test statistics of the form

| (3.11) |

which converge under the null hypothesis in distribution to

as . As is nuisance parameter free, it allows for standard asymptotic inference based on tabulated critical values. However, estimation of is cumbersome, as it is typically based on non-parametric kernel estimators of the form

| (3.12) |

where

| (3.13) |

with and denoting the OLS residuals in (2.1) and the first differences of , respectively. The kernel function and the bandwidth parameter have to fulfill some common technical assumptions to ensure consistency of , see, e. g., \citeasnounAn91, \citeasnounNeWe94 and \citeasnounJa02 for details. As these kernel and bandwidth choices affect the finite sample distribution of , but are completely ignored in the conventional asymptotic framework, corresponding tests are usually prone to large size distortions. This is in particular the case, when the level of endogeneity and/or error serial correlation is large or the sample size is small.131313\citeasnounVoWa14 suggest to use fixed- critical values to capture the effects of tuning parameter choices. However, their simulation results reveal that in small to medium samples the observed test performance turns out to be sensitive to the choice of , and worsens as endogeneity and/or error serial correlation increases.

To avoid any tuning parameter choices, we propose a novel test statistic based on self-normalization. Instead of plugging-in a consistent estimator of in (3.10), we insert a quantity that is asymptotically proportional to but does not rely on any tuning parameters and can be directly computed from the data. To this end, we define the OLS residuals in the augmented partial sum regression given in (3.1) as , . For let and define the self-normalizer as

| (3.14) |

The proof of Theorem 1 below reveals that under the null hypothesis the self-normalizer converges weakly to , i. e., its limiting distribution is scale dependent on . Choosing thus removes the nuisance parameter asymptotically, without estimating it directly. Therefore, we introduce our self-normalized test statistic as

| (3.15) |

Its limiting null distribution is given in the following theorem.

Theorem 1.

The limiting null distribution of is nonstandard but free of any nuisance parameters and only depends on the number of restrictions under the null hypothesis and the number of integrated regressors. Although the distributed random variable in the numerator is correlated with the denominator (as both are driven by and ), simulating critical values is straightforward. Table D.4 in Online Appendix D provides critical values for various choices of and as well as for different deterministic regressors in (2.1).

Remark 2.

We have already mentioned in the introduction that our self-normalization approach is similar in spirit to but different from the approach of \citeasnounKVB00 in the stationary time series literature. As \citeasnounKiVo02 show that the approach of \citeasnounKVB00 is exactly equivalent to using HAC standard errors based on the Bartlett kernel with bandwidth equal to sample size, it is tempting to assume that the traditional kernel estimator of defined in (3.12) with the Bartlett kernel () and could also serve as a self-normalizer in our context. However, as depends on the OLS residuals in (2.1), several nuisance parameters other than enter the limiting distribution of . Thus, the resulting test statistic is not nuisance parameter free.141414In particular, this implies that our self-normalization approach is not a special case of standard long-run variance estimation based on the Bartlett kernel with bandwidth equal to sample size. Instead, in Online Appendix A, we show that is related to a a seemingly natural but inconsistent kernel estimator of based on the first differences of the residuals in the augmented partial sum regression. One way around this problem is to replace the OLS residuals in the construction of with FM-OLS residuals \citeaffixedJPS06see. However, the tuning parameter choices required for FM-OLS estimation may have adverse effects on the performance of the corresponding test in finite samples. Moreover, this approach does not fit to the tuning parameter free flavor of self-normalization. The discussion in Online Appendix A reveals some other possible choices of leading to a nuisance parameter free limiting distribution of . A large scale simulation study comparing all mentioned approaches might be interesting but beyond the scope of this paper.

Remark 3.

In the stationary time series literature local asymptotic power of self-normalized tests is often slightly smaller than local asymptotic power of traditional tests, see, e. g., \citeasnounKVB00 and \citeasnounSh15. Focusing on the single regressor case, we derive local asymptotic power of the self-normalized test and compare it with local asymptotic power of the traditional test in Online Appendix B. We find that local asymptotic power of the self-normalized test is similar to, but slightly below, local asymptotic power of the traditional test. Interestingly, the corresponding largest relative local asymptotic power loss is smaller than the largest relative local asymptotic power loss of a classical self-normalized test for a restriction on the mean of a stationary time series relative to the corresponding -type test \citeaffixed[p. 1800]Sh15compare.

4 Bootstrap Inference

In small to medium samples asymptotic critical values might not serve as good approximations of the quantiles of the self-normalized test statistic’s finite sample distribution. In this section, we combine our self normalization approach with a VAR sieve based resampling procedure to obtain more suitable critical values. We first describe the bootstrap scheme in detail in Section 4.1 and then show its consistency in Section 4.2.

4.1 Bootstrap Method

The representation given in (2.3) suggests to approximate by a sequence of VAR processes with increasing order as . These VAR approximations can be bootstrapped using the vector autoregressive sieve bootstrap. Applying the VAR sieve bootstrap in our context requires to fit a finite order VAR to , . However, while is simply given by the first difference of , the regression error in (2.1), , is unknown. We therefore fit a finite order VAR to , , instead, where denotes the IM-OLS residual in (2.1). In the following, let denote the solution of the sample Yule-Walker equations in the regression of on , , and denote the corresponding residuals by , .151515The Yule-Walker estimator is a natural choice, as any finite order VAR estimated by the Yule-Walker estimator is causal and invertible in finite samples. This will be particularly important in the proof of Theorem 2 below.

Bootstrap Scheme:

-

Obtain the bootstrap sample by randomly drawing times with replacement from the centered residuals , where , and construct recursively as , given initial values .161616Though irrelevant for developing asymptotic theory, it is advantageous in practical applications to eliminate the dependencies of the results on the initial values of , , to obtain a stationary sample. We suggest to generate a sufficiently large number of ’s and keep the last of them, only. Partition analogously to and define .

-

To generate data under the null hypothesis given in (3.8), define , where the restricted IM-OLS estimator of is given by

(4.1) with , such that .

-

Compute the OLS estimator in the bootstrap augmented partial sum regression

(4.2) where , , and , to obtain the bootstrap IM-OLS estimator of in (4.2). Define the corresponding residuals , , and let , , denote their first differences. Define

where and , with , for .

-

Define the bootstrap version of the test statistic as

where

-

Let denote the desired nominal size of the test. Repeat times, where is large and is an integer, to obtain realizations of the bootstrap test statistic . Reject the null hypothesis in (3.8) if the test statistic based on the original observations, , is greater than the -th largest realization of the bootstrap test statistic.

Note that we impose the null hypothesis when generating the bootstrap sample by using the restricted IM-OLS estimator, , instead of the unrestricted IM-OLS estimator, . However, we use the unrestricted residuals, , instead of the restricted residuals, , in the definition of . It is advantageous to use the restricted residuals in the definition of when the null hypothesis is true. However, the empirical distribution function of the restricted residuals will generally fail to mimic the population distribution under the alternative. This leads to a loss of power of the test relative to the case where is based on the unrestricted residuals, see, e. g., \citeasnounGiKi02 and \citeasnounPaPo05 for a detailed discussion.

4.2 Bootstrap Consistency

We now show the asymptotic validity of the testing approach proposed in the previous subsection. To this end, we first prove an invariance principle result to hold for the bootstrap innovations , which then enables us to show that an invariance principle result also holds for . To derive asymptotic results, the rate at which goes to infinity needs to fulfill a technical assumption.

Assumption 4.

Let and as .

For notational brevity, we suppress, as before, the dependence of on also in the following. We are now in the position to prove the following invariance principle for the bootstrap innovations.

The preceding result together with the Beveridge-Nelson decomposition [PhSo92] allows us to prove an invariance principle for that may be of independent interest.

Theorem 2.

Theorem 2 extends the bootstrap invariance principle of \citeasnoun[Theorem 3.3]Pa02 in the sense that the innovations in (2.3) and (2.4) have to be uncorrelated but not necessarily independent. Nevertheless, generating the bootstrap quantities by drawing independently with replacement from the centered residuals still allows to capture the entire second order dependence structure of , which is in our context both necessary and sufficient for the bootstrap to be consistent. This stems from the fact that the dependence structure in the limiting null distribution of depends only on the second moments of and, with respect to second moments, independence and uncorrelatedness are indistinguishable.

The invariance principle for is the key ingredient in showing that the bootstrap IM-OLS estimator in (4.2) has, conditional upon the original sample, the same limiting distribution as the IM-OLS estimator in (3.1).

Theorem 3.

Theorem 3 shows that the VAR sieve bootstrap described in Section 4.1 is consistent for the limiting distributions of the IM-OLS estimator and the self-normalized test statistic based upon it under the null hypothesis.171717Following the bootstrap literature, it would be more common to use rather than as the centering coefficient vector in (4.3). However, both versions lead to the same limiting distribution. As (an estimate of) is not needed to construct the bootstrap samples, we use as the centering coefficient vector in (4.3) to stress that estimating is not necessary for our procedure. Moreover, by construction, the bootstrap is consistent for the limiting null distribution of the self-normalized test statistic even under deviations from the null hypothesis. In particular, this implies that local asymptotic power of the bootstrap-assisted self-normalized test coincides with local asymptotic power of the asymptotic-version of the self-normalized test, compare the discussion in Remark 6 in Online Appendix B.

Remark 4.

The VAR sieve bootstrap scheme allows to capture the second-order dependence structure of in a simple manner. In particular, it only requires the selection of the order of the VAR, which is a straightforward and well understood task in practice. In contrast, choosing the block size for the residual-based block bootstrap proposed in \citeasnounPaPo03 for unit root testing seems to be difficult in applications.181818Although \citeasnounPoWh04 and \citeasnounPPW09 propose estimators of the optimal block size, these are tailor-made for the sample mean of a univariate time series. The dependent wild bootstrap (DWB), originally proposed in \citeasnounSh10 in a stationary setting and recently extended in \citeasnounRhSh19 to univariate unit root testing, might serve as a more non-parametric alternative to the VAR sieve bootstrap. However, it requires the choice of a kernel and a bandwidth parameter to capture dependencies across time. Extending the DWB to our setting and providing a – possibly data-driven – rule for selecting the bandwidth parameter for a given kernel seems to be non-trivial. We leave these interesting questions for future research.

5 Finite Sample Performance

We generate data according to (2.1) and (2.2) with regressors, i. e.,

| (5.1) | ||||

| (5.2) |

for . The regression errors and the first differences of the stochastic regressors are generated as

for . The period serves as a burn-in period to ensure stationarity of and . The parameters and control the level of serial correlation in the regression errors and the extent of endogeneity, respectively. For the error process contains a first order moving average component. To construct , and we first generate three independent univariate stationary GARCH(1,1) processes

, where i.i.d. across , with , and , such that and . We then set , where is the lower triangular matrix of the Cholesky decomposition of

such that . The parameter thus controls the level of correlation between the univariate GARCH(1,1) processes , and . In the following we set to impose weak correlation between the three process. We set and choose the order of the VAR sieve as the one that minimizes the Akaike information criterion (AIC) computed on the evaluation period , as suggested by \citeasnoun[p. 56]KiLu17.191919Results based on the Bayesian information criterion are similar and therefore not reported. We consider results for , and . To mimic typical empirical GARCH patterns, we set and \citeaffixed[p. 77]BJT16compare.202020The performance advantages of the (bootstrap-assisted) self-normalized test over the traditional tests, that will be apparent below, also prevail for other choices of , and . In particular, we observe similar results in case , and are i.i.d. standard normal and independent of each other (). We provide corresponding results in Table C.2 and Figure C.2 in Online Appendix C.2. In all cases, the number of Monte Carlo and bootstrap replications is and , respectively.

We present simulation results under the null hypothesis in Section 5.1 and under deviations from the null hypothesis in Section 5.2. Section C.1 in Online Appendix C compares the estimation performance of the IM-OLS estimator with the performance of the D- and FM-OLS estimators. Finally, Section C.3 in Online Appendix C compares the performance of the non-parametric (bootstrap-assisted) self-normalized test with the performance of \citenameJo95’s \citeyearJo95 parametric likelihood ratio test.

5.1 Test Performance Under the Null Hypothesis

We start with the performance of the (bootstrap-assisted) self-normalized test under the null hypothesis . The results are benchmarked against the traditional Wald-type tests based on the D-, FM- and IM-OLS estimators, in the following denoted by and , respectively. The traditional tests rely on a kernel estimator of the long-run variance parameter as defined in (3.12). We analyze results for the Bartlett kernel and the QS kernel together with the corresponding data-dependent bandwidth selection rules of \citeasnounAn91. In addition, we analyze the performance of the IM-OLS based test statistic that is neither divided by nor by , given by . In conjunction with corresponding bootstrap critical values the test is in the following denoted by .212121We obtain bootstrap critical values for using the scheme described in Section 4.1, with obvious modifications. We analyze the performance of to assess whether the bootstrap is able to approximate the limiting distribution of the tuning parameter free test statistic adequately. Moreover, we also present results of the IM-OLS based Wald-type test that relies on bootstrap rather than asymptotically valid chi-square critical values. We denote this test in the following as and refer to it as the IM-OLS based Wald-type bootstrap test.222222Again, we obtain bootstrap critical values for the IM-OLS based Wald-type statistic using the scheme described in Section 4.1, with obvious modifications. In particular, in each bootstrap iteration, the estimate of the long-run variance is based on the corresponding bootstrap sample rather than on the original sample, which has turned out to be beneficial in preliminary simulations. Table 1 displays the empirical null rejection probabilities – in the following referred to as (empirical) sizes – of the tests.

Overall, size distortions of the tests are the larger the larger or and decrease as increases. In line with \citeasnounVoWa14, we find that the traditional Wald-type test based on the IM-OLS estimator performs better than the Wald-type tests based on the D- and FM-OLS estimators, but is still severely size distorted. In addition, the following three key observations emerge: First, the self-normalized test performs much better than the traditional Wald-type tests for all sample sizes considered. The performance advantage of self-normalization over the traditional approach is the more pronounced the larger or . Second, the self-normalized test has only minor size-distortions for even for small sample sizes. However, for size distortions of – although considerably smaller than size distortions of the traditional tests – are less satisfactory in small to medium samples. In these cases, bootstrapping reduces the size distortions considerably. Third, for the bootstrap-assisted self-normalized test and the IM-OLS based Wald-type bootstrap test perform similarly. In case , however, outperforms , with the performance advantage being the more pronounced the larger and the smaller .

It is worth emphasizing that for the non-bootstrapped self-normalized test outperforms the IM-OLS based Wald-type bootstrap . In case , however, has smaller size distortions than , but the difference decreases considerably as or increase. This demonstrates that self-normalization itself, i. e., without bootstrap assistance, is already a useful tool to reduce size distortions observed for the traditional Wald-type tests in cointegrating regression. It is also interesting to note that for and the bootstrap version of the traditional IM-OLS Wald-type test based on the QS kernel has larger size distortions than the version based on the Bartlett kernel. This indicates that the bootstrap is unable to capture the effects of tuning parameter choices on the performance of the traditional tests in small to medium samples. Finally, we note that both the self-normalized test and the bootstrap-assisted self-normalized test outperform . The performance advantage of self-normalization over the traditional Wald-type tests based on thus seems to result from the ability of the self-normalizer to converge in distribution to a limit that is scale dependent on the true long-run variance parameter rather than from avoiding estimating completely.

Traditional Wald-type tests Self-normalized tests Bartlett kernel QS kernel Panel A: 0 0.10 0.03 0.07 0.16 0.15 0.11 0.07 0.19 0.20 0.14 0.07 0.3 0.12 0.05 0.08 0.18 0.21 0.14 0.08 0.19 0.23 0.14 0.08 0.6 0.16 0.08 0.08 0.34 0.40 0.19 0.09 0.33 0.43 0.18 0.09 0.9 0.53 0.36 0.19 0.69 0.83 0.69 0.25 0.77 0.88 0.77 0.28 0 0.11 0.04 0.07 0.18 0.18 0.13 0.07 0.20 0.21 0.15 0.07 0.3 0.13 0.06 0.07 0.22 0.23 0.15 0.08 0.22 0.25 0.15 0.08 0.6 0.18 0.09 0.09 0.39 0.41 0.22 0.10 0.40 0.44 0.23 0.09 0.9 0.54 0.35 0.20 0.72 0.81 0.69 0.25 0.82 0.89 0.80 0.29 0 0.16 0.05 0.09 0.23 0.19 0.15 0.10 0.24 0.23 0.16 0.08 0.3 0.19 0.07 0.10 0.29 0.26 0.18 0.11 0.31 0.30 0.19 0.09 0.6 0.24 0.10 0.11 0.46 0.41 0.26 0.13 0.50 0.49 0.31 0.11 0.9 0.55 0.33 0.20 0.77 0.79 0.70 0.27 0.88 0.90 0.83 0.31 Panel B: 0 0.08 0.04 0.07 0.13 0.13 0.10 0.07 0.15 0.17 0.12 0.06 0.3 0.10 0.05 0.07 0.14 0.18 0.13 0.08 0.14 0.20 0.13 0.07 0.6 0.13 0.07 0.07 0.26 0.35 0.16 0.09 0.25 0.35 0.16 0.08 0.9 0.44 0.29 0.15 0.61 0.77 0.59 0.19 0.68 0.82 0.65 0.21 0 0.09 0.04 0.06 0.14 0.16 0.12 0.07 0.15 0.18 0.13 0.06 0.3 0.11 0.06 0.07 0.16 0.20 0.14 0.08 0.16 0.21 0.14 0.07 0.6 0.15 0.08 0.08 0.29 0.35 0.19 0.10 0.29 0.38 0.19 0.09 0.9 0.44 0.29 0.16 0.64 0.76 0.59 0.20 0.73 0.84 0.69 0.22 0 0.13 0.05 0.08 0.16 0.18 0.13 0.09 0.17 0.19 0.14 0.08 0.3 0.16 0.06 0.09 0.19 0.23 0.16 0.10 0.20 0.25 0.17 0.09 0.6 0.20 0.08 0.10 0.33 0.36 0.22 0.11 0.35 0.42 0.25 0.11 0.9 0.47 0.27 0.17 0.69 0.74 0.60 0.22 0.81 0.86 0.74 0.24 Panel C: 0 0.06 0.04 0.06 0.09 0.09 0.07 0.06 0.09 0.10 0.08 0.06 0.3 0.07 0.05 0.06 0.10 0.12 0.09 0.06 0.09 0.11 0.08 0.06 0.6 0.08 0.06 0.06 0.14 0.21 0.10 0.07 0.13 0.19 0.10 0.06 0.9 0.19 0.12 0.08 0.30 0.58 0.26 0.09 0.34 0.60 0.29 0.10 0 0.06 0.05 0.06 0.10 0.10 0.08 0.06 0.09 0.10 0.08 0.06 0.3 0.07 0.06 0.06 0.11 0.13 0.10 0.06 0.10 0.12 0.09 0.06 0.6 0.09 0.06 0.06 0.15 0.21 0.11 0.07 0.14 0.21 0.11 0.07 0.9 0.20 0.13 0.08 0.35 0.56 0.29 0.10 0.40 0.60 0.34 0.10 0 0.08 0.05 0.07 0.11 0.12 0.09 0.07 0.10 0.11 0.09 0.07 0.3 0.10 0.06 0.07 0.12 0.15 0.11 0.07 0.12 0.14 0.10 0.07 0.6 0.12 0.07 0.07 0.18 0.22 0.13 0.08 0.17 0.23 0.13 0.07 0.9 0.25 0.14 0.10 0.41 0.54 0.32 0.11 0.48 0.62 0.41 0.12 Panel D: 0 0.05 0.04 0.05 0.07 0.07 0.07 0.05 0.07 0.07 0.07 0.05 0.3 0.06 0.05 0.05 0.08 0.09 0.08 0.06 0.07 0.08 0.07 0.06 0.6 0.06 0.05 0.05 0.10 0.14 0.08 0.06 0.09 0.13 0.07 0.05 0.9 0.09 0.05 0.05 0.15 0.38 0.11 0.05 0.15 0.38 0.12 0.06 0 0.06 0.04 0.05 0.08 0.08 0.08 0.06 0.07 0.08 0.07 0.06 0.3 0.06 0.05 0.05 0.09 0.10 0.09 0.06 0.08 0.09 0.08 0.05 0.6 0.06 0.05 0.05 0.11 0.14 0.09 0.06 0.10 0.13 0.08 0.06 0.9 0.10 0.06 0.05 0.18 0.37 0.13 0.06 0.20 0.39 0.15 0.06 0 0.06 0.04 0.05 0.08 0.09 0.08 0.06 0.07 0.08 0.07 0.06 0.3 0.07 0.05 0.05 0.09 0.11 0.09 0.06 0.09 0.10 0.08 0.06 0.6 0.07 0.05 0.05 0.12 0.15 0.10 0.06 0.11 0.14 0.09 0.06 0.9 0.13 0.08 0.06 0.23 0.36 0.17 0.07 0.26 0.40 0.20 0.07 • Notes: Superscript “” signifies the use of bootstrap critical values. The asymptotic critical value for the self-normalized test is given in Table D.4 in Online Appendix D (; Panel A, , ).

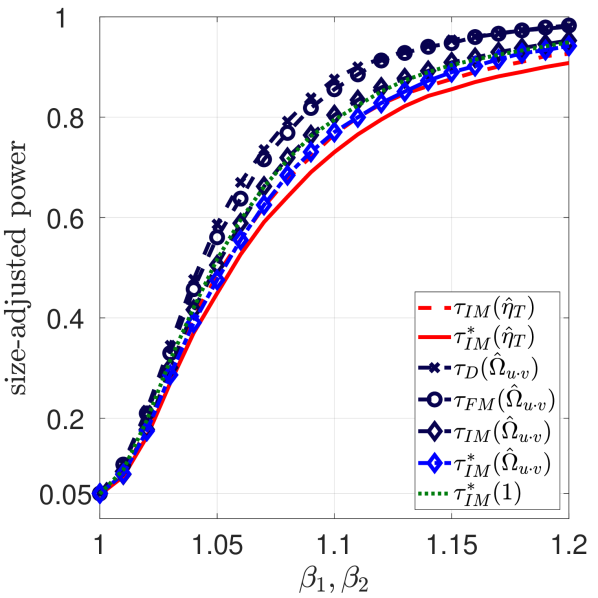

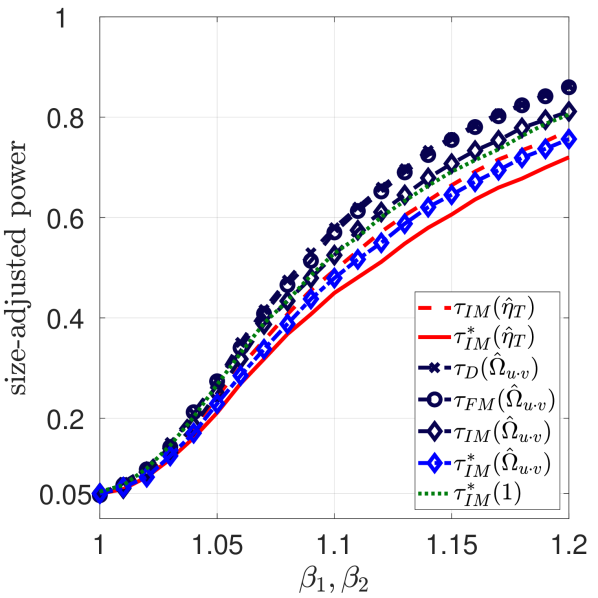

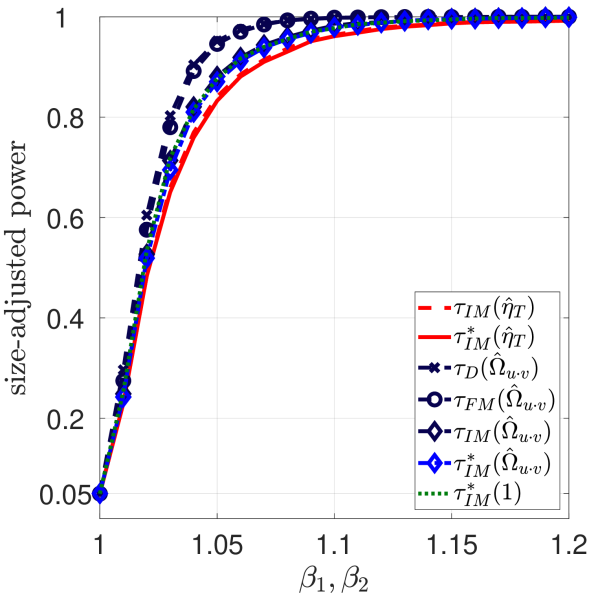

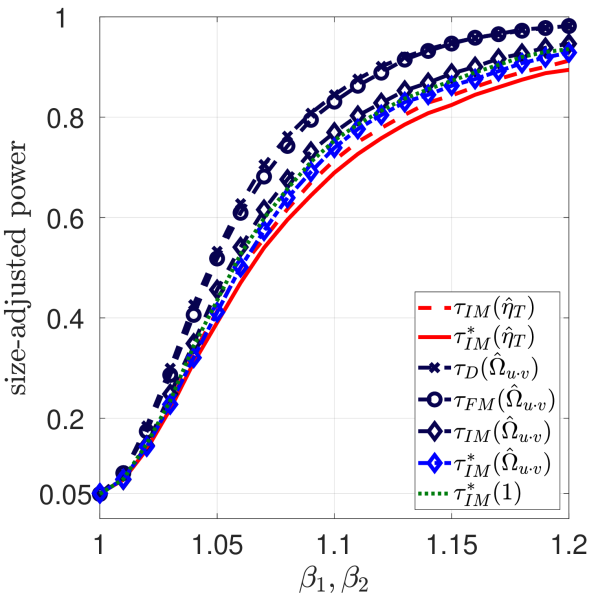

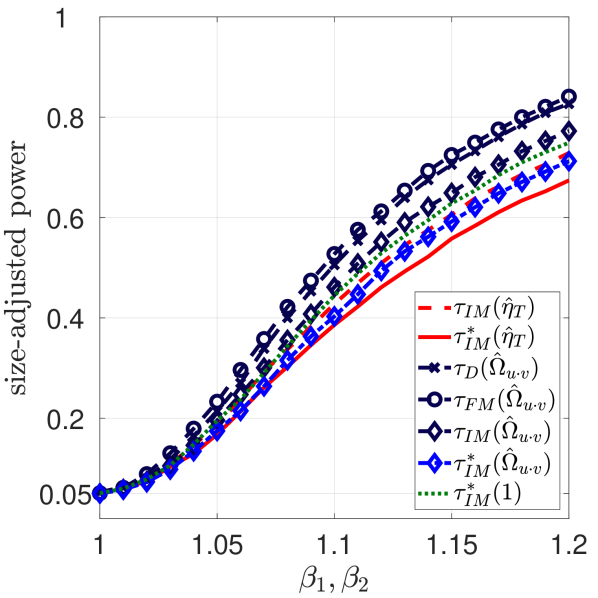

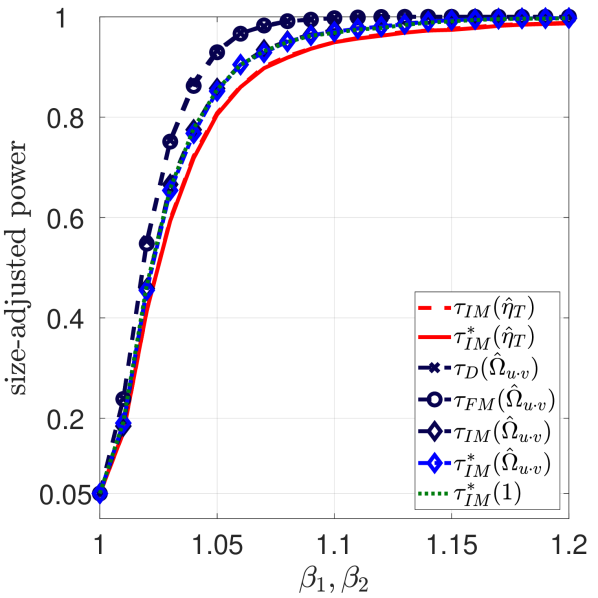

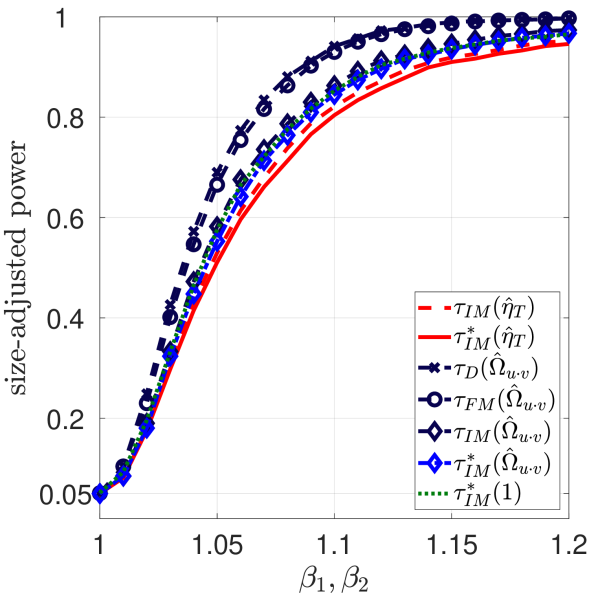

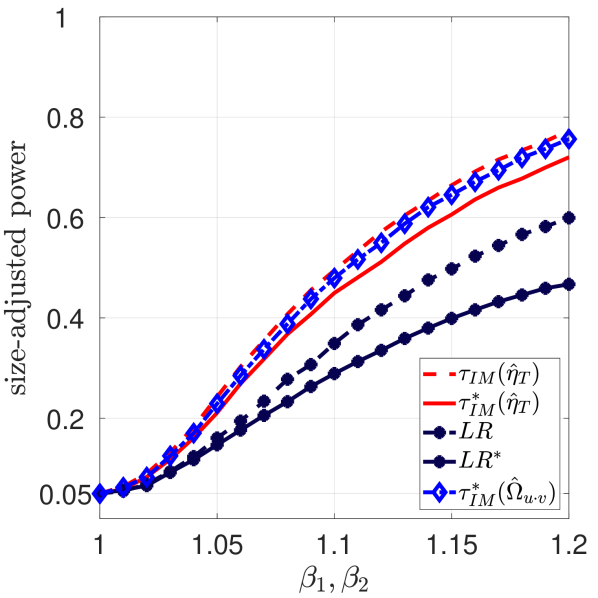

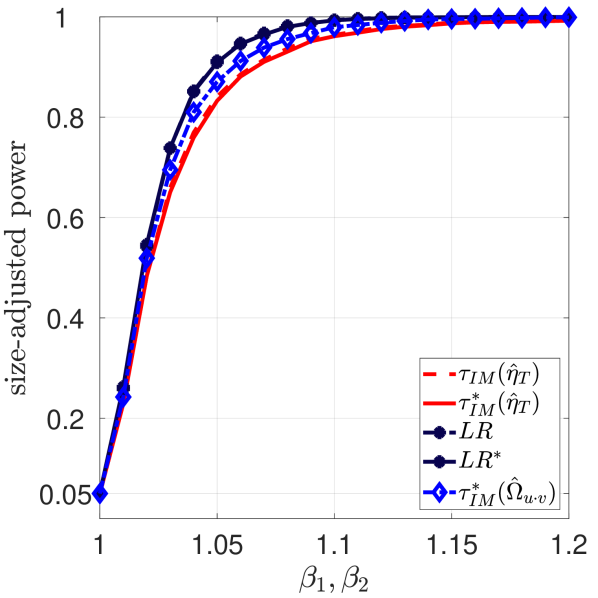

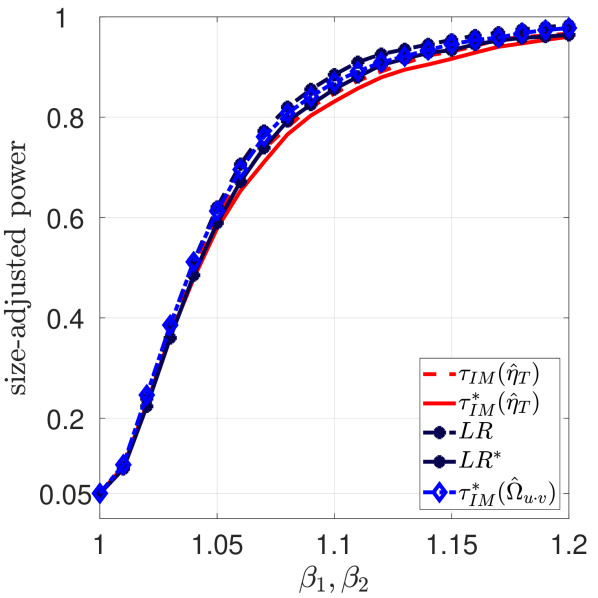

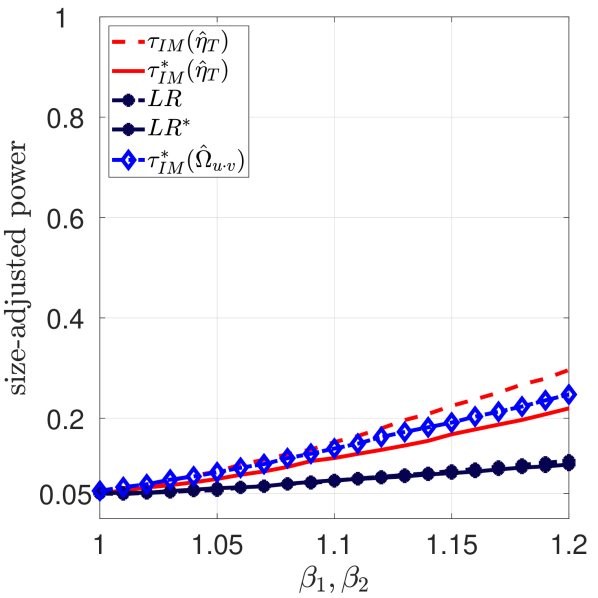

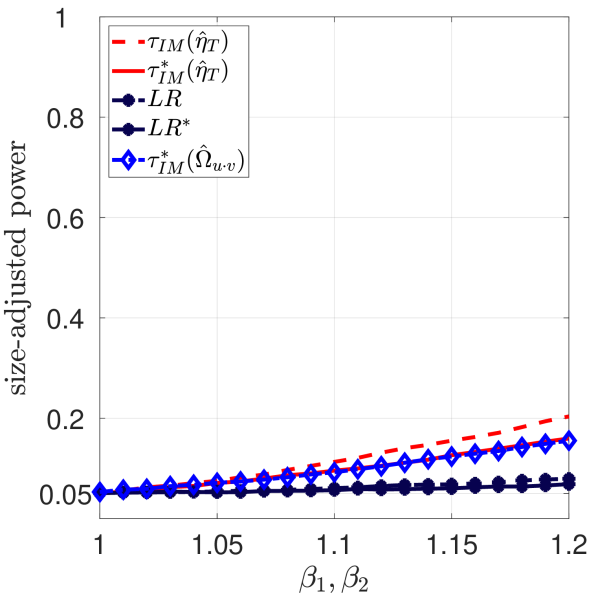

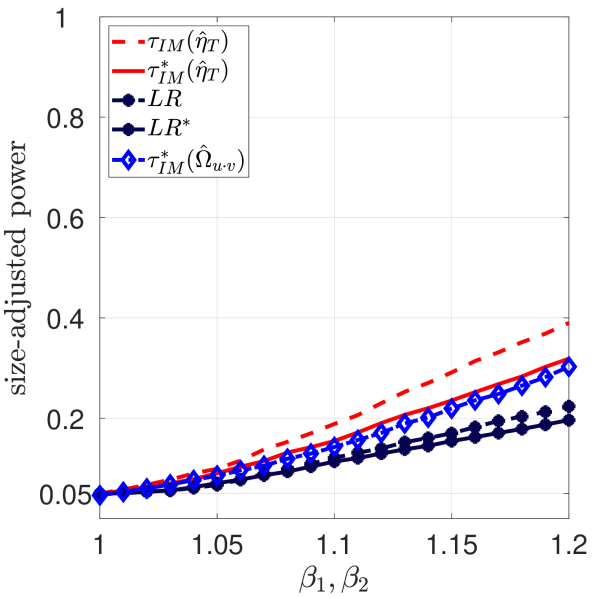

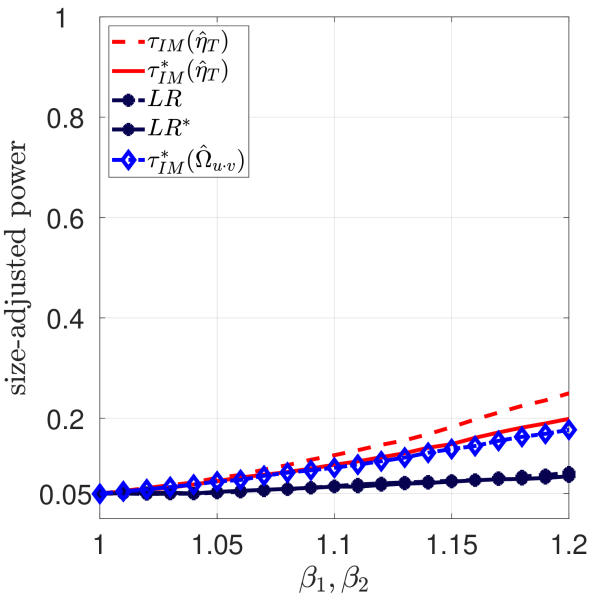

5.2 Size-Adjusted Power

To analyze the properties of the tests under deviations from the null hypothesis, we generate data for using values on a grid with mesh size . The large differences in sizes (i. e., under the null hypothesis), however, make a meaningful comparison of the performances under the alternative difficult. To enable a “fair” comparison, we follow \citeasnoun[p. 826]CNR15 and first simulate under the null hypothesis and record for each test the nominal size that yields an empirical size equal to the desired . We then use critical values corresponding to in the simulations under deviations from the null hypothesis.

Figure 1 displays illustrative results for , and , where, whenever necessary, we use the Bartlett kernel to estimate long-run variance parameters. Results for the QS kernel and other choices of , and are qualitatively similar.232323Because of the enormous size distortions of under the null hypothesis in case and , constructing the size-adjusted power curves for this test requires a much larger number of bootstrap replications. In general, we find that size-adjusted power of the tests increases with sample size, but larger values of and lead to smaller size-adjusted power. In line with \citeasnounVoWa14 we find that the traditional Wald-type test based on the IM-OLS estimator has slightly smaller size-adjusted power than the tests based on the D- and FM-OLS estimators, with the difference vanishing as the sample size increases. Moreover, size-adjusted power of is similar to size-adjusted power of . With respect to self-normalization, we observe that size-adjusted power of is very similar to size-adjusted power of the traditional tests for small deviations from the null hypothesis, but then becomes slightly lower for larger deviations from the null. This finding is in line with the power properties of self-normalized tests in the stationary time series literature \citeaffixedSh15see, e. g., and with the local asymptotic power properties of the self-normalized test analyzed in detail in Online Appendix B. However, given the enormous size improvement of the self-normalized test with respect to the traditional tests under the null hypothesis, the observed loss in power is difficult to deem relevant. The bootstrap versions of the self-normalized test and the traditional Wald-type test have slightly smaller power than the versions based on asymptotic critical values. In this respect, we note that size-adjusted power of the IM-OLS based Wald-type bootstrap test seems to be slightly larger than size-adjusted power of the bootstrap-assisted self-normalized test. However, there are some exceptions, e. g., for and , compare Figure C.4 in Online Appendix C.3. Thus, in this case, the bootstrap-assisted self-normalized test performs better than the IM-OLS based Wald-type bootstrap test both under the null hypothesis and in terms of size-adjusted power.

6 Empirical Illustration: The Fisher Effect

In this section we briefly illustrate the usefulness of the self-normalized test developed in this paper in applications. Many empirical studies suggest that inflation and the short-term nominal interest rate do not cointegrate with the slope of inflation being equal to one, a finding at odds with the so-called Fisher effect that is backed by many theoretical models.242424For a brief description of the underlying economic theory we refer to \citeasnoun[pp. 195]We08. The errors in the Fisher equation

| (6.1) |

, are likely to be highly persistent even in case cointegration between inflation and the short-term nominal interest rate prevails, \citeaffixed[pp. 217]We08see, e. g.,. As demonstrated in our simulation study (and in many simulation studies before), highly persistent errors are well known to have adverse effects on the performance of estimators and tests in cointegrating regressions. Consequently, the Fisher effect might be rejected, even if it exists, solely due to the poor performance of the methods chosen by the applied researcher \citeaffixed[for a detailed analysis of this phenomenon]CaPi04see. \citeasnounWe08 shows that this problem can be tackled by using suitable panel methods, i. e., at the cost of including a large number of additional countries into the analysis. This may be undesirable for the applied researcher originally interested in analyzing the existence of the Fisher effect for a particular country only. Given its superior finite sample performance demonstrated in Section 5 compared to the traditional tests, the bootstrap-assisted self-normalized test developed in this paper seems to be useful to address this problem in the time series setting.

We investigate the validity of the Fisher effect for Germany and the United States between 1965Q1 and 2021Q1, using quarterly data () obtained from the OECD databases Economic Outlook and Main Economic Indicators.252525The inflation rates and short-term interest rates are available on https://data.oecd.org/price/inflation-cpi.htm and https://data.oecd.org/interest/short-term-interest-rates.htm, respectively (Accessed: March 24, 2022). Before estimating (6.1) for both countries separately, we first assess whether the short-term interest rate and inflation are indeed non-stationary and cointegrated. To this end, we employ \citenameBr02’s \citeyearBr02 self-normalized variance ratio unit root test and a Shin-type cointegration test based on the IM-OLS residuals allowing for a potentially non-zero mean. To estimate the long-run variance parameter required for the cointegration test, we use the Bartlett kernel and the corresponding data-dependent bandwidth selection rule of \citeasnounAn91. All tests in this section are carried out at the nominal level. For both countries, the unit root test fails to reject the null hypothesis of non-stationarity of the interest rate and inflation and the cointegration test fails to reject the null hypothesis of cointegration between the two variables.

These preliminary results justify to estimate (6.1) on the individual country level using the IM-OLS estimator and to test whether is indeed equal to one using the bootstrap-assisted self-normalized test developed in this paper. We set the number of bootstrap replications to and determine the order of the VAR sieve as described in Section 5.262626Note again that ready-to-use MATLAB code for empirical applications is available on www.github.com/kreichold/CointSelfNorm. For comparison, we also estimate (6.1) using the FM-OLS estimator and test unity of using the corresponding traditional Wald-type test. For the FM-OLS estimator and the test statistic based upon it we use the Bartlett kernel and the corresponding data-dependent bandwidth selection rule of \citeasnounAn91 to estimate the long-run parameters. The results are reported in Table 2, which also presents the OLS estimates as a benchmark.

Estimates of Test statistics for Persistence Country OLS IM-OLS FM-OLS Germany 1.36 1.68 1.53 26.72 (102.57) 2.85 (2.71) 0.92 United States 0.99 1.39 1.14 24.29 (102.32) 0.47 (2.71) 0.91 • Notes: All tests are carried out at the nominal level and reject the null hypothesis if the test statistic is larger than the corresponding critical value. Bootstrap critical values for the bootstrap-assisted self-normalized test and chi-square critical values for the traditional test in parenthesis. The measure of persistence in the regression errors in (6.1) is obtained by regressing the OLS residuals on their first lag.

The OLS estimate of is given by for Germany and for the United States, with the modified estimators yielding slightly larger estimates. The estimated values of compare well with the estimates obtained in \citeasnoun[Table VII]We08 for the subperiod 1980Q1–2004Q4. To assess the persistence of the errors in (6.1), we regress the OLS residuals on their first lag. The resulting estimates of the AR(1) parameter are for Germany and for the United States, showing that the regression errors are indeed highly persistent. With respect to testing unity of , Table 2 shows that the traditional FM-OLS based test accepts the hypothesized value of one for for the United States, but rejects the null hypothesis for Germany. In contrast, the bootstrap-assisted self-normalized test does not reject the hypothesis that is equal to one for both countries. Interestingly, the realizations of the self-normalized test statistic and the corresponding bootstrap critical values are very similar for Germany and the United States. This indicates that the validity of the Fisher effect is equally likely in both countries, although the estimates of are slightly closer to one for the United States. The traditional test thus gives misleading results.272727It is worth mentioning that the asymptotic critical value for the self-normalized test statistic is given by (see Table D.4 in Online Appendix D, Panel B, , ). This implies that also the self-normalized test based on the asymptotic critical value does not reject the validity of the Fisher effect for the two countries.

Although our results show the importance of accounting for highly persistent regression errors, a more careful analysis is needed to assess the validity of the Fisher effect for the full period, as the link between inflation and the short-term interest rate might have weakened in the aftermath of the global financial crisis.

7 Conclusion

We propose a novel self-normalized test statistic for general linear restrictions in cointegrating regressions avoiding direct estimation of a long-run variance parameter. Its limiting null distribution is nonstandard, but we provide asymptotic critical values. Combining the self-normalization approach with a VAR sieve bootstrap to construct critical values further improves the performance of the self-normalized test in small to medium samples when the level of error serial correlation or regressor endogeneity is large. Constructing bootstrap critical values requires the choice of a single tuning parameter, the order of a VAR, which is a straightforward and well understood task in practice.

Simulation results and local asymptotic power analyses demonstrate that the bootstrap-assisted self-normalized test is considerably less prone to size distortions than the traditional tests at the cost of only small power losses. From a practical point of view, these small power losses are difficult to deem relevant in cointegrating regressions, given the enormous size improvements under the null hypothesis. An empirical application analyzing the validity of the Fisher effect in Germany and the United States exemplifies the advantage of the bootstrap-assisted self-normalized test over the traditional tests. Given that the bootstrap-assisted self-normalized test is easy to implement, we conclude that it should become a serious competitor to the traditional tests in practice.

Bootstrap-assisted self-normalized inference may also be a promising approach to address the enormous size distortions of hypothesis tests often observed in, e. g., cointegrated panels, cointegrating polynomial regressions and non-linear cointegrating regressions. We leave these interesting extensions for future research.

Acknowledgements

Karsten Reichold gratefully acknowledges partial financial support by the German Research Foundation via the Collaborative Research Center SFB 823 Statistical Modelling of Nonlinear Dynamic Processes. The authors are grateful to Katharina Hees, Fabian Knorre and participants at the Econometrics Colloquium at the University of Konstanz, the IAAE 2021 Annual Conference, the 2021 Asian Meeting of the Econometric Society and the 2021 North American Summer Meeting of the Econometric Society for helpful comments.

References

- [1] \harvarditem[Andrews]Andrews1991An91 Andrews, D.W.K. (1991). Heteroskedasticity and Autocorrelation Consistent Covariance Matrix Estimation. Econometrica 59, 817–858.

- [2] \harvarditem[Andrews et al.]Andrews et al.2007ADB07 Andrews, B., Davis, R.A., Breidt, F.J. (2007). Rank-Based Estimation for All-Pass Time Series Models. Annals of Statistics 35, 844–869.

- [3] \harvarditem[Benati et al.]Benati et al.2020BLNW20 Benati, L., Lucas Jr., R.E., Nicolini, J.P., Weber, W. (2020). International Evidence on Long-Run Money Demand. Journal of Monetary Economics. Forthcoming.

- [4] \harvarditem[Breitung]Breitung2002Br02 Breitung, J. (2002). Nonparametric Tets for Unit Roots and Cointegration. Journal of Econometrics 108, 343–363.

- [5] \harvarditem[Brüggemann et al.]Brüggemann et al.2016BJT16 Brüggemann, R., Jentsch, C., and Trenkler, C. (2016). Inference in VARs with Conditional Heteroskedasticity of Unknown Form. Journal of Econometrics 191, 69–85.

- [6] \harvarditem[Caporale and Pittis]Caporale and Pittis2004CaPi04 Caporale, G.M., Pittis, N. (2004). Estimator Choice and Fisher’s Paradox: A Monte Carlo Study. Econometric Reviews 23, 25–52.

- [7] \harvarditem[Cavaliere et al.]Cavaliere et al.2015CNR15 Cavaliere, G., Nielsen, H.B., Rahbek, A. (2015). Bootstrap Testing of Hypotheses on Co-Integration Relations in Vector Autoregressive Models. Econometrica 83, 813–831.

- [8] \harvarditem[Chang and Park]Chang and Park2003ChPa03 Chang, Y., Park, J.Y. (2003). A Sieve Bootstrap for the Test of a Unit Root. Journal of Time Series Analysis 24, 379–400.

- [9] \harvarditem[Chang et al.]Chang et al.2006CPS06 Chang, Y., Park, J.Y., Song, K. (2006). Bootstrapping Cointegrating Regressions. Journal of Econometrics 133, 703–739.

- [10] \harvarditem[Dahlhaus et al.]Dahlhaus et al.2018DKN18 Dahlhaus, R., Kiss, I.Z., Neddermeyer, J.C. (2018). On the Relationship Between the Theory of Cointegration and the Theory of Phase Synchronization. Statistical Science 33, 334–357.

- [11] \harvarditem[Doukhan and Wintenberger]Doukhan and Wintenberger2007DoWi07 Doukhan, P., Wintenberger, O. (2007). An Invariance Principle for Weakly Dependent Stationary General Models. Probability and Mathematical Statistics 27, 45–73.

- [12] \harvarditem[Hwang and Sun]Hwang and Sun2018HwSu18 Hwang, J., Sun, Y. (2018). Simple, Robust, and Accurate and Tests in Cointegrated Systems. Econometric Theory 34, 949–984.

- [13] \harvarditem[Jansson]Jansson2002Ja02 Jansson, M. (2002). Consistent Covariance Matrix Estimation for Linear Processes. Econometric Theory 18, 1449–1459.

- [14] \harvarditem[Jin et al.]Jin et al.2006JPS06 Jin, S., Phillips, P.C.B., Sun, Y. (2006). A New Approach to Robust Inference in Cointegration. Economics Letters 91, 300–306.

- [15] \harvarditem[Johansen]Johansen1995Jo95 Johansen, S. (1995). Likelihood-Based Inference in Cointegrated Vector Auto-Regressive Models. Oxford University Press, Oxford.

- [16] \harvarditem[Kiefer and Vogelsang]Kiefer and Vogelsang2002KiVo02 Kiefer, N.M., Vogelsang, T.J. (2002). Heteroskedasticity-Autocorrelation Robust Standard Errors Using the Bartlett Kernel Without Truncation. Econometrica 70, 2093–2095.

- [17] \harvarditem[Kiefer et al.]Kiefer et al.2000KVB00 Kiefer, N.M., Vogelsang, T.J., Bunzel, H. (2000). Simple Robust Testing of Regression Hypotheses. Econometrica 68, 695–714.

- [18] \harvarditem[Kilian and Lütkepohl]Kilian and Lütkepohl2017KiLu17 Kilian, L., Lütkepohl, H. (2017). Structural Vector Autoregressive Analysis. Cambridge University Press, Cambridge.

- [19] \harvarditem[Knorre et al.]Knorre et al.2021KWG21 Knorre, F., Wagner, M., Grupe, M. (2021). Monitoring Cointegrating Polynomial Regressions: Theory and Application to the Environmental Kuznets Curves for Carbon and Sulfur Dioxide Emissions. Econometrics 9, 12.

- [20] \harvarditem[Lanne and Saikkonen]Lanne and Saikkonen2013LaSa13 Lanne, M., Saikkonen, P. (2013). Noncausal Vector Autoregression. Econometric Theory 29, 447–481.

- [21] \harvarditem[Li and Maddala]Li and Maddala1997LiMa97 Li, H., Maddala, G.S. (1997). Bootstrapping Cointegrating Regressions. Journal of Econometrics 80, 297–318.

- [22] \harvarditem[Lobato]Lobato2001Lo01 Lobato, I.N. (2001). Testing that a Dependent Process is Uncorrelated. Journal of the American Statistical Association 96, 1066–1076.

- [23] \harvarditem[Merlevède et al.]Merlevède et al.2006MPU06 Merlevède, F., Peligrad, M., Utev, S. (2006). Recent Advances in Invariance Principles for Stationary Sequences. Probability Surveys 3, 1–36.

- [24] \harvarditem[Meyer and Kreiss]Meyer and Kreiss2015MeKr15 Meyer, M., Kreiss, J.-P. (2015). On the Vector Autoregressive Sieve Bootstrap. Journal of Time Series Analysis 36, 377 – 397.

- [25] \harvarditem[Newey and West]Newey and West1994NeWe94 Newey, W.K., West, K.D. (1994). Automatic Lag Selection in Covariance Matrix Estimation. Review of Economic Studies 61, 631–653.

- [26] \harvarditem[Palm et al.]Palm et al.2010PSU10 Palm, F.C., Smeekes, S., Urbain, J.-P. (2010). A Sieve Bootstrap Test for Cointegration in a Conditional Error Correction Model. Econometric Theory 26, 647 – 681.

- [27] \harvarditem[Paparoditis and Politis]Paparoditis and Politis2003PaPo03 Paparoditis, E., Politis, D.N. (2003). Residual-Based Block Bootstrap for Unit Root Testing. Econometrica 71, 813 – 855.

- [28] \harvarditem[Paparoditis and Politis]Paparoditis and Politis2005PaPo05 Paparoditis, E., Politis, D.N. (2005). Bootstrap Hypothesis Testing in Regression Models. Statistics & Probability Letters 74, 356 – 365.

- [29] \harvarditem[Park]Park1992Pa92 Park, J.Y. (1992). Canonical Cointegrating Regressions. Econometrica 60, 119–143.

- [30] \harvarditem[Park]Park2002Pa02 Park, J.Y. (2002). An Invariance Principle for Sieve Bootstrap in Time Series. Econometric Theory 18, 469–490.

- [31] \harvarditem[Patton et al.]Patton et al.2009PPW09 Patton, A., Politis, D.N., White, H. (2009). Correction to “Automatic Block-Length Selection for the Dependent Bootstrap” by D. Politis and H. White. Econometric Reviews 28, 372–375.

- [32] \harvarditem[Phillips]Phillips1995Ph95 Phillips, P.C.B. (1995). Fully Modified Least Squares and Vector Autoregression. Econometrica 63, 1023–1078.

- [33] \harvarditem[Phillips]Phillips2014Ph14 Phillips, P.C.B. (2014). Optimal Estimation of Cointegrated Systems With Irrelevant Instruments. Journal of Econometrics 178, 210–224.

- [34] \harvarditem[Phillips and Hansen]Phillips and Hansen1990PhHa90 Phillips, P.C.B., Hansen, B.E. (1990). Statistical Inference in Instrumental Variables Regression with I(1) Processes. Review of Economic Studies 57, 99–125.

- [35] \harvarditem[Phillips et al.]Phillips et al.2020PLS20 Phillips, P.C.B., Leirvik, T., Storelvmo, T. (2020). Econometric Estimates of Earth’s Transient Climate Sensitivity. Journal of Econometrics 214, 6 – 32.

- [36] \harvarditem[Phillips and Loretan]Phillips and Loretan1991PhLo91 Phillips, P.C.B., Loretan, M. (1991). Estimating Long Run Economic Equilibria. Review of Economic Studies 58, 407–436.

- [37] \harvarditem[Phillips and Solo]Phillips and Solo1992PhSo92 Phillips, P.C.B., Solo, V. (1992). Asymptotics for Linear Processes. Annals of Statistics 20, 971–1001.

- [38] \harvarditem[Politis and White]Politis and White2004PoWh04 Politis, D.N., White, H. (2004). Automatic Block-Length Selection for the Dependent Bootstrap. Econometric Reviews 23, 53-70.

- [39] \harvarditem[Psaradakis]Psaradakis2001Ps01 Psaradakis, Z. (2001). On Bootstrap Inference in Cointegrating Regressions. Economics Letters 72, 1–10.

- [40] \harvarditem[Rad et al.]Rad et al.2016RLF16 Rad, H., Low, R.K.Y., Faff, R. (2016). The Profitability of Pairs Trading Strategies: Distance, Cointegration and Copula Methods. Quantitative Finance 16, 1541–1558.

- [41] \harvarditem[Rho and Shao]Rho and Shao2019RhSh19 Rho, Y., Shao, X. (2019). Bootstrap-Assisted Unit Root Testing With Piecewise Locally Stationary Errors. Econometric Theory 35, 142–166.

- [42] \harvarditem[Saikkonen]Saikkonen1991Sa91 Saikkonen, P. (1991). Asymptotically Efficient Estimation of Cointegrating Regressions. Econometric Theory 7, 1–21.

- [43] \harvarditem[Shao]Shao2010Sh10 Shao, X. (2010). The Dependent Wild Bootstrap. Journal of the American Statistical Association 105, 218–235.

- [44] \harvarditem[Shao]Shao2015Sh15 Shao, X. (2015). Self-Normalization for Time Series: A Review of Recent Developments. Journal of the American Statistical Association 110, 1797–1817.

- [45] \harvarditem[Stock and Watson]Stock and Watson1993StWa93 Stock, J.H., Watson, M.W. (1993). A Simple Estimator of Cointegrating Vectors in Higher Order Integrated Systems. Econometrica 61, 783–820.

- [46] \harvarditem[van Giersbergen and Kiviet]van Giersbergen and Kiviet2002GiKi02 van Giersbergen, N.P.A., Kiviet, J.F. (2002). How to Implement the Bootstrap in Static or Stable Dynamic Regression Models: Test Statistic Versus Confidence Region Approach. Journal of Econometrics 108, 133–156.

- [47] \harvarditem[Vogelsang and Wagner]Vogelsang and Wagner2014VoWa14 Vogelsang, T.J., Wagner, M. (2014). Integrated Modified OLS Estimation and Fixed- Inference for Cointegrating Regressions. Journal of Econometrics 178, 741–760.

- [48] \harvarditem[Wagner]Wagner2015Wa15 Wagner, M. (2015). The Environmental Kuznets Curve, Cointegration and Nonlinearity. Journal of Applied Econometrics 30, 948–967.

- [49] \harvarditem[Wang and Shao]Wang and Shao2020WaSh20 Wang, R., Shao, X. (2020). Hypothesis Testing for High-Dimensional Time Series via Self-Normalization. Annals of Statistics 48, 2728–2758.

- [50] \harvarditem[Westerlund]Westerlund2008We08 Westerlund, J. (2008). Panel Cointegration Tests of the Fisher Effect. Journal of Applied Econometrics 23, 193–233.

- [51] \harvarditem[Wu]Wu2005Wu05 Wu, W. (2005). Nonlinear System Theory: Another Look at Dependence. Proceedings of the National Academy of Sciences of the USA 102, 14150–14154.

- [52] \harvarditem[Wu]Wu2007Wu07 Wu, W. (2007). Strong Invariance Principles for Dependent Random Variables. Annals of Probability 35, 2294–2320.

- [53]

Online Appendix to

“A Bootstrap-Assisted Self-Normalization Approach to Inference in Cointegrating Regressions”

Karsten Reichold and Carsten Jentsch

March 11, 2024

Equation, Table and Figure numbers not preceded by a letter refer to the main article.

A Other Possible Choices for

Our particular choice for in (3.10), the self-normalizer , is closely related to a seemingly natural kernel estimator of defined as

where, as before, is a kernel function and is a bandwidth parameter. In contrast to the traditional estimator defined in (3.12), is inconsistent for under common kernel and bandwidth assumptions. Nevertheless, serves as a useful starting point to motivate our choice of as the self-normalizer.

We first note that under traditional kernel and bandwidth assumptions , as , where denotes the vector of the last components of the -dimensional vector defined in (3.3), see \citeasnoun[Proof of Theorem 3]VoWa14. That is, the limiting distribution of is nuisance parameter free up to its scale-dependence on , which leads to a nuisance parameter free limiting distribution of the test statistic . However, is not a self-normalizer in the original sense, as its construction requires tuning parameter choices, which may have adverse effects on the performance of in finite samples. In particular, unreported preliminary simulation results indicate that is less successful in reducing the size distortions of the traditional test relative to .

In the special case where is the Bartlett kernel () and , it follows from algebraic arguments used in \citeasnoun[Proof of Lemma 1]CaSh06 in combination with similar arguments as used in the proof of Theorem 1 that

as . The quantity is thus closely related to and its limiting distribution is again nuisance parameter free up to its scale-dependence on . Unreported preliminary simulation results show that performs similarly to under the null hypothesis. However, has smaller (local asymptotic) power than under the alternative.

Remark 5.

There is another interesting relation we want to highlight. If we assume for a moment that , which does not hold in general, we obtain . This relation fits well to the finding of \citeasnounKiVo02 in the stationary time series literature. The authors show that the self-normalization approach of \citeasnounKVB00 is exactly equivalent to using HAC standard errors based on the Bartlett kernel with bandwidth equal to sample size. From this perspective, choosing as the self-normalizer seems to be the natural extension of the approach of \citeasnounKVB00 from the stationary time series literature to cointegrating regressions.

B Local Asymptotic Power

In this section we compare the asymptotic power properties of the self-normalized test and the traditional test under local alternatives. The results hold under Assumption 3, with and generated by (2.1) and (2.2), respectively. To ease exposition of the main arguments, we restrict attention to the single regressor case (), which suffices to illustrate the main similarities and differences between the two tests. For the regression model becomes , with being a one-dimensional parameter. We are interested in testing the null hypothesis . In this case, defined in (3.10) simplifies to

| (B.1) |

where denotes the upper-left element of the ()-dimensional matrix defined in (3.6). Straightforward calculations reveal that under the local alternative , with , the limiting distribution of is given by

| (B.2) |

where denotes the upper-left element of the nuisance parameter free ()-dimensional matrix defined in (3.1) and denotes the first element in the two-dimensional vector defined in (3.3). Analogously, the limiting distribution of under the local alternative is given by

| (B.3) |

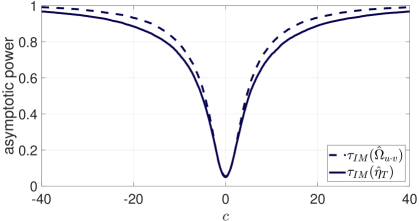

Naturally, for the limiting distributions in (B.2) and (B) coincide with the chi-square distribution with one degree of freedom and the distribution defined in (1), respectively. It follows that local asymptotic power of at the nominal level is given by , where denotes the -quantile of the chi-square distribution with one degree of freedom. Analogously, local asymptotic power of at the nominal level is given by , where denotes the corresponding -quantile for the self-normalized test statistic given in Table D.4 in Online Appendix D (; Panel A, , ). Local asymptotic power of both tests depends on . For a given , local asymptotic power of the tests thus depends on both the long-run variance of the first differences of the regressor and the long-run variance of the regression error corrected for its conditional long-run mean given . In particular, it follows from the definition of that local asymptotic power of the tests decreases as the variability in the regression errors increases. To assess the effect of the location parameter , we plot the two power curves as a function of in Figure B.1 for fixed and using simulations. In particular, we set and approximate the stochastic terms using similar methods to those used to generate the critical values in Online Appendix D.

Figure B.1 shows that both tests have asymptotic power against local alternatives, with local asymptotic power increasing symmetrically as moves away from zero. Local asymptotic power of the self-normalized test is similar to, but slightly below, local asymptotic power of the traditional Wald-type test. To quantify the local power loss, we consider two measures: the absolute local power loss, i. e., the difference in local power between the traditional test and the self-normalized test, and the relative local power loss, i. e., the absolute local power loss divided by local power of the traditional test. The largest absolute local power loss is about and occurs at around , whereas the largest relative local power loss is about and occurs at around . The results are consistent with the findings in the stationary time series literature, where local asymptotic power of self-normalized tests is well known to be often slightly below that of traditional tests, see, e. g., \citeasnounKVB00 and \citeasnounSh15.303030For comparison, note that \citeasnoun[p. 1800]Sh15 analyzes local asymptotic power of a self-normalized test for testing a hypothesis on the mean of a strictly stationary time series . He reports that under suitable moment and weak dependence conditions, the largest relative local power loss of the self-normalized test statistic compared to the -type test based on an estimator of the long-run variance of is around . In this light, the largest relative local power loss of our self-normalized test compared to the traditional test seems to be relatively small.

Remark 6.

Given the results in Theorem 3, it follows from consistency of the IM-OLS estimator of and imposing the null hypothesis when constructing the bootstrap data that the VAR sieve bootstrap is consistent for the limiting null distribution of the self-normalized test statistic even when the null hypothesis is incorrect. In the limit, the bootstrap critical value for the self-normalized test statistic thus coincides with the asymptotic critical value even under deviations from the null hypothesis. Consequently, local asymptotic power of the bootstrap-assisted self-normalized test coincides with local asymptotic power of the asymptotic version of the self-normalized test.

C Additional Finite Sample Results

C.1 Estimator Performance

We briefly compare the IM-OLS estimator with the D- and FM-OLS estimators in terms of bias and root mean squared error (RMSE). Implementing the D-OLS estimator requires choosing the numbers of leads and lags of the first differences of the integrated regressors. To this end, we use the Bayesian information criterion (BIC) analyzed in \citeasnounChKu12, as it appears to be the most successful criterion – among those considered by the authors – in reducing the mean squared error of the D-OLS estimator. The FM-OLS estimator is based on an estimator of the long-run covariance matrix of as defined in (3.13). We analyze the results for the Bartlett kernel and the Quadratic Spectral (QS) kernel, together with the corresponding data-dependent bandwidth selection rules of \citeasnounAn91. Table C.1 displays results for .313131Results for are similar and therefore not reported. Although asymptotically unbiased, the D-, FM- and IM-OLS estimators are biased in finite samples. Generally, bias and RMSE increase in and and decrease in . In terms of bias the IM-OLS estimator performs similar to the D-OLS estimator and clearly outperforms the FM-OLS estimator. In terms of RMSE the results show that overall the D-OLS estimator performs best, followed by the FM-OLS estimator based on the Bartlett kernel. RMSE of the IM-OLS estimator is comparable to the RMSE of the FM-OLS estimator based on the QS kernel, which is often slightly larger than RMSE of the FM-OLS estimator based on the Bartlett kernel. We conclude that the IM-OLS estimator performs relatively well and serves as a good starting point for self-normalized inference in cointegrating regressions.

FM-OLS FM-OLS IM-OLS D-OLS Bartlett QS QML IM-OLS D-OLS Bartlett QS QML Panel A: 0 0.25 0.27 0.04 0.11 0.05 5.15 3.52 3.28 3.42 15.31 0.3 0.25 0.08 0.66 0.79 0.45 7.29 4.91 5.02 5.38 19.79 0.6 0.88 1.65 3.64 3.70 6.82 12.72 11.68 11.12 11.97 374.48 0.9 19.63 12.69 24.93 25.00 606.33 58.08 46.22 48.09 55.54 31796.03 0 0.28 0.18 0.13 0.19 0.39 6.67 4.46 4.24 4.42 20.65 0.3 0.28 0.10 0.87 1.00 0.42 9.46 7.43 6.50 6.93 23.56 0.6 0.91 1.52 4.16 4.30 1.25 16.45 16.59 13.63 14.75 77.59 0.9 20.44 12.89 26.44 26.37 75.50 68.99 58.15 54.10 88.03 6141.08 0 0.35 0.09 0.34 0.41 0.66 9.74 8.06 6.27 6.56 20.00 0.3 0.33 0.35 1.37 1.51 0.95 13.83 12.87 9.56 10.16 76.13 0.6 0.96 1.60 5.14 5.59 3.55 23.95 26.29 18.48 19.82 354.12 0.9 22.08 13.54 29.43 29.69 31.68 92.30 83.42 66.97 122.62 4171.58 Panel B: 0 0.07 0.15 0.05 0.09 0.13 3.91 2.37 2.38 2.46 6.22 0.3 0.03 0.03 0.45 0.51 0.14 5.55 3.25 3.55 3.72 9.96 0.6 0.74 1.53 2.48 2.44 2.05 9.71 6.63 7.76 8.25 115.53 0.9 14.76 11.97 20.06 20.35 54.65 45.30 33.92 39.03 42.27 3497.87 0 0.07 0.07 0.12 0.15 0.02 5.07 2.97 3.09 3.18 3.97 0.3 0.01 0.19 0.60 0.65 0.09 7.20 4.21 4.62 4.84 11.40 0.6 0.83 1.71 2.92 2.94 5.09 12.56 8.85 9.67 10.28 289.60 0.9 15.60 12.88 21.49 22.36 12.16 53.98 42.04 44.37 50.19 903.93 0 0.06 0.12 0.30 0.31 0.24 7.39 4.42 4.56 4.71 9.54 0.3 0.03 0.49 1.00 1.05 0.06 10.51 6.40 6.84 7.18 21.90 0.6 1.01 2.04 3.72 3.86 1.24 18.27 13.33 13.42 14.37 168.09 0.9 17.27 14.19 24.28 25.81 123.50 72.40 58.58 55.89 66.60 4255.25 Panel C: 0 0.01 0.06 0.02 0.02 0.01 1.59 0.91 0.91 0.92 0.95 0.3 0.03 0.02 0.12 0.12 0.01 2.27 1.25 1.33 1.35 1.38 0.6 0.21 0.46 0.79 0.69 0.04 3.96 2.38 2.80 2.84 2.50 0.9 5.01 4.25 8.83 8.67 0.17 17.71 11.78 17.39 18.36 15.07 0 0.02 0.03 0.04 0.04 0.01 2.07 1.14 1.18 1.19 1.25 0.3 0.05 0.10 0.17 0.16 0.00 2.95 1.61 1.74 1.77 1.83 0.6 0.24 0.55 0.93 0.84 0.01 5.14 3.06 3.54 3.63 3.33 0.9 5.32 4.98 9.64 9.82 1.37 21.88 14.73 19.96 21.40 36.14 0 0.04 0.08 0.09 0.09 0.02 3.02 1.67 1.74 1.77 1.91 0.3 0.07 0.25 0.30 0.29 0.07 4.30 2.41 2.58 2.65 2.87 0.6 0.31 0.75 1.21 1.15 0.03 7.50 4.44 5.01 5.19 6.09 0.9 5.95 6.43 11.20 11.85 5.25 30.54 20.66 25.18 27.23 290.19 Panel D: 0 0.01 0.01 0.01 0.01 0.01 0.77 0.45 0.45 0.46 0.46 0.3 0.02 0.02 0.05 0.05 0.01 1.10 0.63 0.66 0.67 0.66 0.6 0.08 0.21 0.30 0.25 0.03 1.93 1.16 1.33 1.33 1.17 0.9 1.59 1.72 3.77 3.45 0.02 8.22 5.38 8.33 8.54 5.14 0 0.02 0.00 0.02 0.02 0.01 1.00 0.58 0.59 0.59 0.60 0.3 0.03 0.06 0.07 0.06 0.02 1.43 0.82 0.86 0.87 0.86 0.6 0.09 0.24 0.35 0.28 0.02 2.50 1.50 1.70 1.72 1.54 0.9 1.71 2.05 4.11 3.92 0.07 10.41 6.82 9.64 10.07 6.86 0 0.03 0.05 0.04 0.04 0.02 1.46 0.84 0.87 0.87 0.91 0.3 0.04 0.13 0.12 0.10 0.01 2.09 1.21 1.28 1.29 1.33 0.6 0.12 0.31 0.45 0.39 0.01 3.65 2.18 2.43 2.47 2.34 0.9 1.96 2.73 4.82 4.82 0.08 14.87 9.69 12.35 13.12 10.14 • Notes: The terms “Bartlett” and “QS” signify the kernel used to apply the FM-OLS estimator. QML denotes the quasi maximum likelihood estimator of \citeasnounJo95, as described in Section C.3.

C.2 Results in the i.i.d. Innovations Case ()