An Illustrative Industry Architecture

to Mitigate Potential Fragmentation across

Central Bank Digital Currency and Commercial Bank Money

Abstract

Central banks are actively exploring central bank digital currencies (CBDCs) by conducting research, proofs of concept and pilots. However, adoption of a CBDC can risk fragmenting both payments markets and retail deposits. In this paper, we aim to provide a mitigation to this fragmentation risk by presenting an illustrative industry architecture which places CBDCs and commercial bank money on a similar footing. We introduce the concept of ecosystems providing a common programmability layer that interfaces with the account systems at both commercial banks and the central bank. We focus on a potential United Kingdom (UK) CBDC, including industry ecosystems interfacing with commercial banks using Open Banking application programming interfaces (APIs).

1 Introduction

A central bank digital currency (CBDC) is a digital payment instrument, denominated in a national unit of account, that is a direct liability of a central bank [9]. Central banks are actively exploring CBDCs [10, 1] with various motivations such as: (i) continuing access to central bank money, (ii) improving resilience, (iii) increasing payments diversity, (iv) encouraging financial inclusion, (v) improving cross-border payments, (vi) supporting privacy, and (vii) facilitating fiscal transfers [13]. The design of a CBDC and its underlying system could potentially lead to significant risks, ranging from cyber security risks [9] to financial stability risks [12]. In addition, we identify a further risk of fragmentation in payments markets and retail deposits unless there is interoperability between CBDCs and existing forms of money.

In the UK, the Bank of England and HM Treasury have established the CBDC Taskforce to coordinate the exploration of a potential UK CBDC and two external engagement groups, the CBDC Engagement Forum and the CBDC Technology Forum, to gather input on non-technology and technology aspects respectively of CBDC [5]. The Bank of England and HM Treasury will also launch a consultation in 2022, which will set out their assessment of the case for a UK CBDC [8]. In this paper, we focus on a potential UK CBDC and describe an illustrative industry architecture based on the Bank of England’s ‘platform model’ [4]. Our contribution is the concept of ecosystems that provide a common programmability layer across both CBDC and commercial bank money and thereby place both forms of money on a similar footing. We hope the architecture presented in this paper will stimulate discussion and look forward to ongoing industry engagement on CBDC.

2 CBDC Models and Architectures

Central banks have described, proposed and piloted several models and architectures for CBDCs. The Bank for International Settlements (BIS) has described a range of CBDC architectures including a single-tier ‘direct’ architecture, two-tier ‘hybrid’ and ‘intermediated’ architectures, and an ‘indirect’ architecture [2]. BIS has also described models for multi-CBDC arrangements to make cross-border payments more efficient, namely ‘compatible’ CBDC systems, ‘interlinked’ CBDC systems, and a ‘single’ CBDC system [3]. The People’s Bank of China has initiated a CBDC pilot that uses a two-tier architecture with the central bank issuing digital fiat currency to authorised operators who take charge of exchange and circulation [16]. The Estonian Central Bank is experimenting with a bill-based CBDC money scheme built on a partitioned blockchain architecture [14]. The Federal Reserve Bank of Boston and the Massachusetts Institute of Technology have prototyped two CBDC systems with a central transaction processor, one with an ‘atomizer’ architecture and another with a ‘two-phase commit’ architecture [11].

The Bank of England has described several potential models for CBDC provision including a ‘platform model’, a ‘pooled account model’, an ‘intermediated token model’, and a ‘bearer instrument model’ [6]. The ‘platform model’ (see Figure 1), which we adopt in this paper, comprises the Bank of England operating a core ledger and providing access via application programming interfaces (APIs) to authorised and regulated Payment Interface Providers (PIPs) that provide users with access to CBDC.

3 Illustrative Industry Architecture

In this section, we describe an illustrative industry architecture for a potential UK CBDC by identifying initial requirements, describing the logical architecture, and analysing how it meets the requirements. We adopt the Bank of England’s platform model, i.e. we do not consider other models in the remainder of this paper.

3.1 Initial Requirements

We first identify the following initial requirements as a basis for developing the architecture:

-

•

Characteristics: Support the characteristics of a CBDC system identified by the Bank of England, namely: (i) reliable and resilient, (ii) fast and efficient, and (iii) innovative and open to competition [7].

-

•

Technology choices: Align to the Bank of England’s current views on potential technology choices on topics such as ledger design, privacy, simplicity and programmability [7].

-

•

Interoperability: Avoid fragmentation by ensuring CBDCs and commercial bank money are interoperable and have similar operational capabilities.

3.2 Logical Architecture

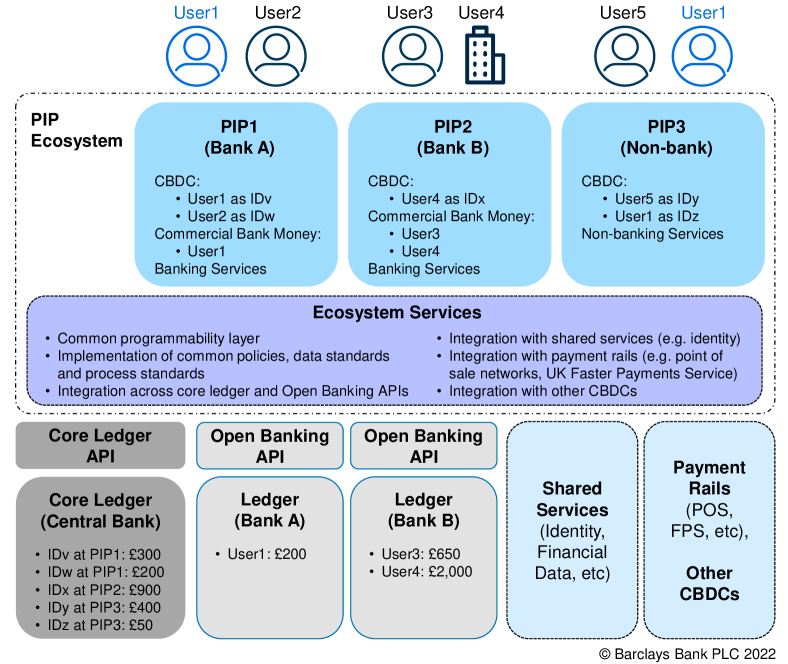

We next present the logical architecture as shown in Figure 2.

Key aspects of the architecture, which extends the platform model, are summarised below:

-

•

The Bank of England: (i) operates the core ledger that records CBDC value and processes the payment transactions made using CBDC, and (ii) provides access to the core ledger via APIs. Users are linked to their CBDC balances and payment transactions on the core ledger with pseudonymous identities. We highlight that the core ledger APIs could potentially be similar to Open Banking APIs [15] with some enhancements such as new APIs for opening and closing CBDC accounts.

-

•

We introduce PIP ecosystems that provide competing services including: (i) implementation of common policies, data standards and process standards, (ii) integration across the core ledger APIs provided by the Bank of England and Open Banking APIs provided by commercial banks, (iii) integration with shared services such as identity providers and financial data vendors, (iv) integration with other payment rails such as the UK Faster Payments Service (FPS) and point of sale (POS) networks, (v) integration with other CBDC systems, and (vi) a programmability layer that operates across all of these services and provides a foundation for creating new automated behaviours and innovative products.

-

•

PIPs are authorised and regulated firms, which can include both commercial banks and non-banks. They onboard retail and business users, provide customer services, and fulfil regulatory requirements such as know-your-customer (KYC) and anti-money laundering (AML). PIPs also pseudonymise user identity and intermediate user access to the CBDC system. Note that PIPs could potentially deliver these capabilities by leveraging ecosystem services.

3.3 Analysis

We now analyse the architecture against the initial requirements and present our summary findings in Table LABEL:table:key-principle-analysis.

| Requirements | Analysis |

|---|---|

|

Characteristics:

(i) reliable and resilient (ii) fast and efficient (iii) innovative and open to competition |

(i) The Bank of England can exercise control and

oversight over the core ledger to ensure it is secure, compliant and private.

Well-designed platforms can deliver resiliency, scalability and

availability at the core ledger and ecosystem layers.

(ii) The architecture introduces ecosystems as a layer between PIPs and the core ledger API, but the overhead of this indirection should be minimal and ecosystems can provide significant benefits including operational efficiencies. (iii) PIP ecosystems can build competing and innovative services while using common policies and standards to ensure interoperability. |

|

Technology choices:

(i) ledger design (ii) privacy (iii) simplicity (iv) programmability |

(i) The API-based layered architecture allows the technology choices

for the core ledger to be generally independent of the

technology choices for other layers such as the ecosystems.

(ii) The use of pseudonymous identities ensures only appropriate parties are aware of user identities, which facilitates privacy while retaining the ability to conduct KYC and AML. (iii) The core ledger infrastructure can be kept relatively simple because more complex functionality is provided by PIP ecosystems instead. (iv) Implementing programmability in the PIP ecosystems layer, instead of in the core ledger, should reduce security risks and complexity at the core ledger. Programs running in PIP ecosystems would leverage the core ledger acting as the authoritative data store. Each ecosystem could implement programmability using its platform of choice. |

| Interoperability | The PIP ecosystems would provide common policies, data standards and process standards across both CBDC and commercial bank money. This would avoid fragmentation by ensuring CBDCs and commercial bank money are interoperable and have similar operational capabilities. |

4 Summary and Further Work

This paper focussed on a potential UK CBDC and presented an illustrative industry architecture that:

-

•

adopts and extends the Bank of England’s platform model for CBDC provision,

-

•

aligns to the Bank of England’s currently-identified system characteristics and views on potential technology choices for CBDC infrastructure, and

-

•

mitigates the risk of fragmentation in payments markets and retail deposits by introducing the concept of ecosystems that provide a common programmability layer across CBDC and commercial bank money.

Barclays is currently developing a prototype based on the illustrative industry architecture. Potential further work includes analysis of any changes needed to Open Banking APIs in order to integrate with the common programmability layer, prototyping the specification of the Core Ledger APIs, and elaborating key customer journeys using the architecture. We hope this architecture paper will stimulate discussion, particularly regarding methods to reduce fragmentation risk by placing CBDCs and commercial bank money on a similar footing, and look forward to ongoing industry engagement on CBDC.

Acknowledgements: We would like to thank Vikram Bakshi (Barclays) for his helpful feedback.

References

- [1] Atlantic Council. Central Bank Digital Currency Tracker, 2021. https://www.atlanticcouncil.org/cbdctracker/. Accessed 23 February 2022.

- [2] Raphael Auer and Rainer Böhme. Central bank digital currency: the quest for minimally invasive technology. BIS Working Papers 948, BIS, June 2021. https://www.bis.org/publ/work948.pdf.

- [3] Raphael Auer, Philipp Haene, and Henry Holden. Multi-CBDC arrangements and the future of crossborder payments. BIS Papers 115, BIS, March 2021. https://www.bis.org/publ/bppdf/bispap115.pdf.

- [4] Bank of England. Central Bank Digital Currency - Opportunities, challenges and design. Discussion Paper, March 2020. https://www.bankofengland.co.uk/-/media/boe/files/paper/2020/central-bank-digital-currency-opportunities-challenges-and-design.pdf.

- [5] Bank of England. Central bank digital currencies, 2021. https://www.bankofengland.co.uk/research/digital-currencies. Accessed 23 February 2022.

- [6] Bank of England. Item 2 - Models of CBDC Provision. In Minutes of the CBDC Technology Forum, November 2021. https://www.bankofengland.co.uk/-/media/boe/files/minutes/2021/meeting-slides-cbdc-technology-forum-meeting-november-2021.

- [7] Bank of England. Item 2 - Recap of some assumptions around CBDC technology. In Minutes of the CBDC Technology Forum, September 2021. https://www.bankofengland.co.uk/-/media/boe/files/minutes/2021/meeting-slides-cbdc-technology-forum-meeting-september-2021.

- [8] Bank of England. Statement on Central Bank Digital Currency next steps, 2021. https://www.bankofengland.co.uk/news/2021/november/statement-on-central-bank-digital-currency-next-steps. Accessed 23 February 2022.

- [9] BIS. CBDCs: an opportunity for the monetary system. In BIS Annual Economic Report, chapter III, pages 65–95. June 2021. https://www.bis.org/publ/arpdf/ar2021e3.pdf.

- [10] Codruta Boar and Andreas Wehrli. Ready, steady, go? – Results of the third BIS survey on central bank digital currency. BIS Papers 114, BIS, January 2021. https://www.bis.org/publ/bppdf/bispap114.pdf.

- [11] Anders Brownworth et al. Project Hamilton Phase 1: A High Performance Payment Processing System Designed for Central Bank Digital Currencies. Report, Boston Fed and MIT DCI, February 2022. https://www.bostonfed.org/-/media/Documents/Project-Hamilton/Project-Hamilton-Phase-1-Whitepaper.pdf.

- [12] Group of Central Banks. Central bank digital currencies: financial stability implications. Report 4, BIS, September 2021. https://www.bis.org/publ/othp42_fin_stab.pdf.

- [13] Group of Central Banks. Central bank digital currencies: system design and interoperability. Report 2, BIS, September 2021. https://www.bis.org/publ/othp42_system_design.pdf.

- [14] Group of European Central Banks. Work stream 3: A New Solution – Blockchain & eID, July 2021. https://www.ecb.europa.eu/paym/digital_euro/investigation/profuse/shared/files/deexp/ecb.deexp211011_3.en.pdf.

- [15] Open Banking Implementation Entity. Open Banking API Specifications, 2020. https://standards.openbanking.org.uk/api-specifications/. Accessed 23 February 2022.

- [16] Working Group on E-CNY Research and Development. Progress of Research & Development of E-CNY in China. Report, People’s Bank of China, July 2021. http://www.pbc.gov.cn/en/3688110/3688172/4157443/4293696/2021071614584691871.pdf.