Decision-Focused Learning without

Differentiable Optimization:

Learning Locally Optimized Decision Losses

Abstract

Decision-Focused Learning (DFL) is a paradigm for tailoring a predictive model to a downstream optimization task that uses its predictions in order to perform better on that specific task. The main technical challenge associated with DFL is that it requires being able to differentiate through the optimization problem, which is difficult due to discontinuous solutions and other challenges. Past work has largely gotten around this this issue by handcrafting task-specific surrogates to the original optimization problem that provide informative gradients when differentiated through. However, the need to handcraft surrogates for each new task limits the usability of DFL. In addition, there are often no guarantees about the convexity of the resulting surrogates and, as a result, training a predictive model using them can lead to inferior local optima. In this paper, we do away with surrogates altogether and instead learn loss functions that capture task-specific information. To the best of our knowledge, ours is the first approach that entirely replaces the optimization component of decision-focused learning with a loss that is automatically learned. Our approach (a) only requires access to a black-box oracle that can solve the optimization problem and is thus generalizable, and (b) can be convex by construction and so can be easily optimized over. We evaluate our approach on three resource allocation problems from the literature and find that our approach outperforms learning without taking into account task-structure in all three domains, and even hand-crafted surrogates from the literature.

1 Introduction

Predict-then-optimize Donti et al. (2017); Elmachtoub and Grigas (2021) is a framework for using machine learning to perform decision-making. As the name suggests, it proceeds in two stages—first, a predictive model takes as input features and makes some predictions using them, then second, these predictions are used to parameterize an optimization problem that outputs a decision. A large number of real-world applications involve both prediction and optimization components and can be framed as predict-then-optimize problems—for e.g., recommender systems in which missing user-item ratings need to be predicted Isinkaye et al. (2015), portfolio optimization in which future performance needs to be predicted Markowitz and Todd (2000), or strategic decision-making in which the adversary behavior needs to be predicted Kar et al. (2017).

In addition to wide applicability, this framework also formalizes the relationship between prediction and decision-making. This is important because such predictive models are typically learned independently of the downstream optimization task in Machine Learning-based decision-making systems, and recent work in the predict-then-optimize setting Elmachtoub and Grigas (2021); Mandi et al. (2020); Wilder et al. (2019a); Ferber et al. (2020); Amos et al. (2019); Wilder et al. (2019a); Xie et al. (2020); Wilder et al. (2019b); Demirović et al. (2019) has shown that it is possible to achieve better task-specific performance by tailoring the predictive model to the downstream task. This is often done by differentiating through the entire prediction and optimization pipeline end-to-end, leading to a family of approaches that we will refer to as decision-focused learning (DFL) Wilder et al. (2019a). Optimizing directly for the quality of decisions induced by the predictive model in this end-to-end manner yields a loss function we call the decision loss.

However, training with the decision loss can be challenging because the solutions to optimization problems are often discontinuous in the predictions (see Section 2.1). This results in an uninformative loss function with zero or undefined gradients, neither of which are useful for learning a predictive model. To address this, DFL approaches often leverage handcrafted surrogate optimization tasks that provides more useful gradients. These surrogate problems may be constructed by relaxing the original problem Elmachtoub and Grigas (2021); Mandi et al. (2020); Wilder et al. (2019a); Ferber et al. (2020), adding regularization to the objective Amos et al. (2019); Wilder et al. (2019a); Xie et al. (2020), or even using entirely an different optimization problem that shares the same decision space Wilder et al. (2019b).

Designing good surrogates is an art, requiring manual effort, insight into the optimization problem of interest. In addition, there are no guarantees that the surrogates induce convex decision losses, leading to local optima that further complicate training. Instead, we propose a fundamentally different approach: to learn a decision loss directly for a given task, circumventing surrogate problem design entirely. Our framework represents the loss as a function in a particular parametric family and selects parameters which provide an informative loss for the optimization task. We call the resulting loss a locally optimized decision loss (LODL).

Our starting point is the observation that a good decision loss should satisfy 3 properties: it should (i) be faithful to the original task, i.e., the decision quality is consistent with the original problem; (ii) provide informative gradients everywhere (i.e., defined and non-zero); and (iii) be convex in prediction space to avoid local minima. These demands are in tension—the first requirement prevents the loss function from being modified too much to achieve the other two. It is not obvious apriori that any tractable parametric family should be able to simultaneously satisfy all three properties for the complex structure induced by many optimization tasks. We resolve this tension by separately modeling the loss function locally for the neighborhood around each individual training example. Faithful representation of the decision loss is easier to accomplish locally in each individual neighborhood than globally across instances, allowing us to introduce convex parametric families of loss functions which capture structural intuitions about properties important for optimization. To fit the parameters, we sample points in the neighborhood of the true labels, evaluate the decision loss associated with these sampled points, and then train a loss function to mimic the decision loss.

We evaluate LODLs on three resource allocation domains from the literature Hughes et al. (2018); Wilder et al. (2019a); Wang et al. (2020). Perhaps surprisingly, we find that LODLs outperform handcrafted surrogates in two out of the three. In our analysis, we discover a linear correlation between the agreement of the learned LODL with the decision loss and the decision loss of a predictive model learned using said LODL. Our approach motivates a new line of research on decision-focused learning.

2 Background

In predict-then-optimize, a predictive model first takes as input features and produces predictions . These predictions are then used to parameterize an optimization problem that is solved to yield decisions :

| (1) |

Note that, unlike typical machine learning problems, the dimensionality of is likely to be large as it consists of all predictions needed to parameterize the optimization problem. Given the large dimensionality, and the similarity in the role of all the predictions, the predictive model typically predicts individual components of , i.e. .

Predictions are evaluated with respect to the decision loss (DL) of the decision that they induce, i.e., the value under the objective function of the optimization under the ground truth parameters :

Thus, for a dataset , we aim to learn a model that generates predictions that minimize the decision loss :

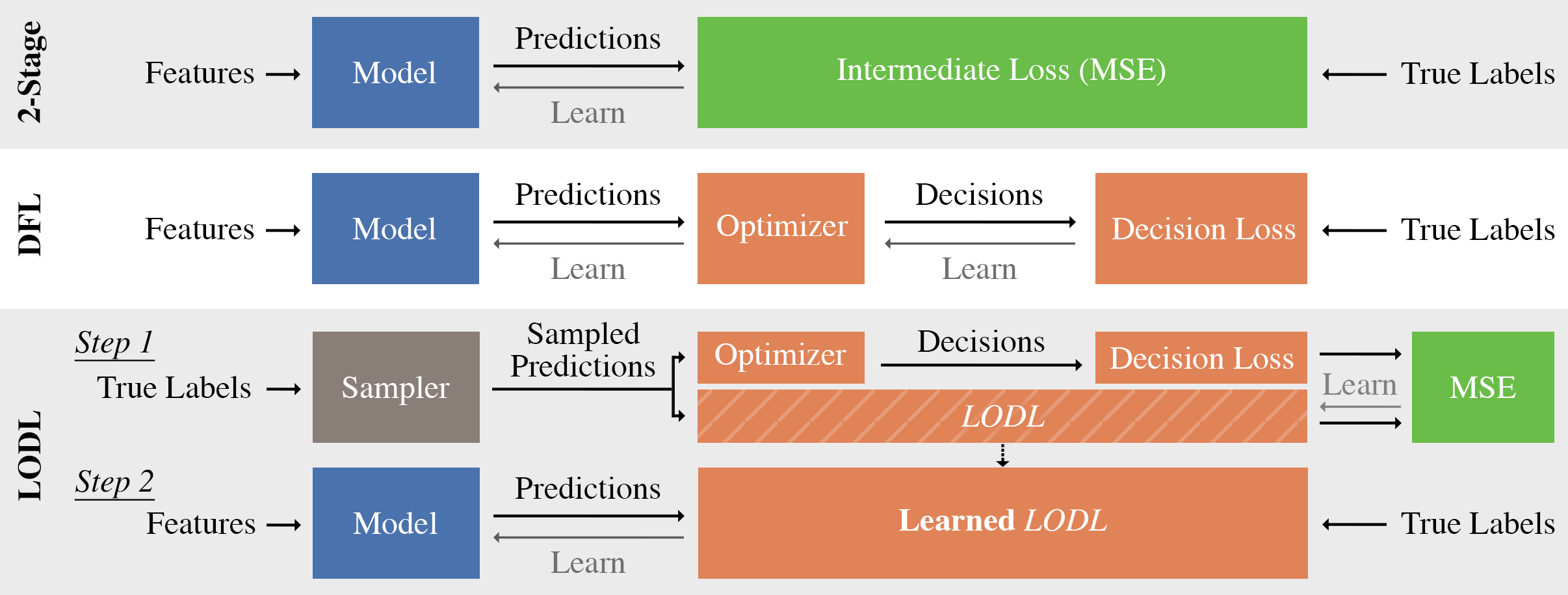

This is in contrast with standard supervised learning approaches in which the quality of a prediction is measured by a somewhat arbitrary intermediate loss (e.g., mean squared error) that does not contain information about the downstream decision-making task. In this paper, we refer to models that use an intermediate loss as 2-stage and those that directly optimize for as decision-focused learning (DFL). Figure 1 outlines how a predictive model is learned using these different approaches.

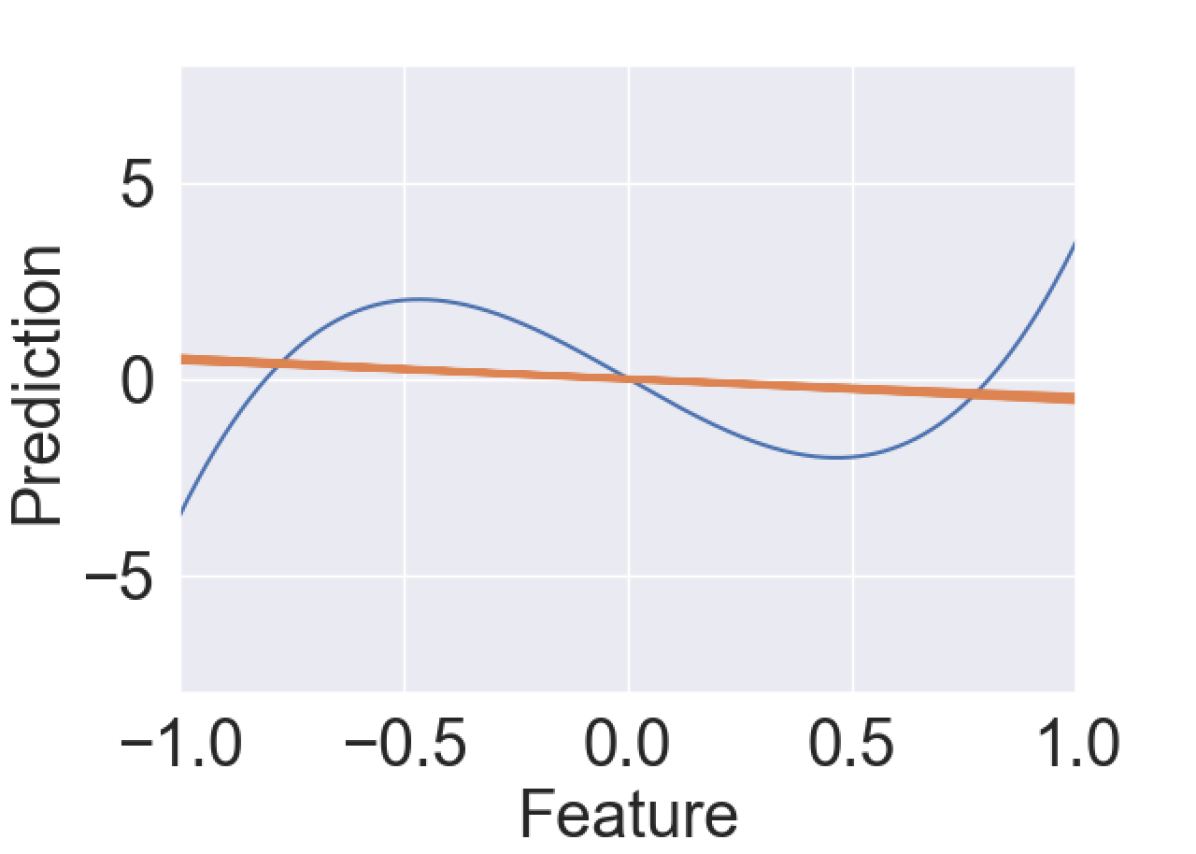

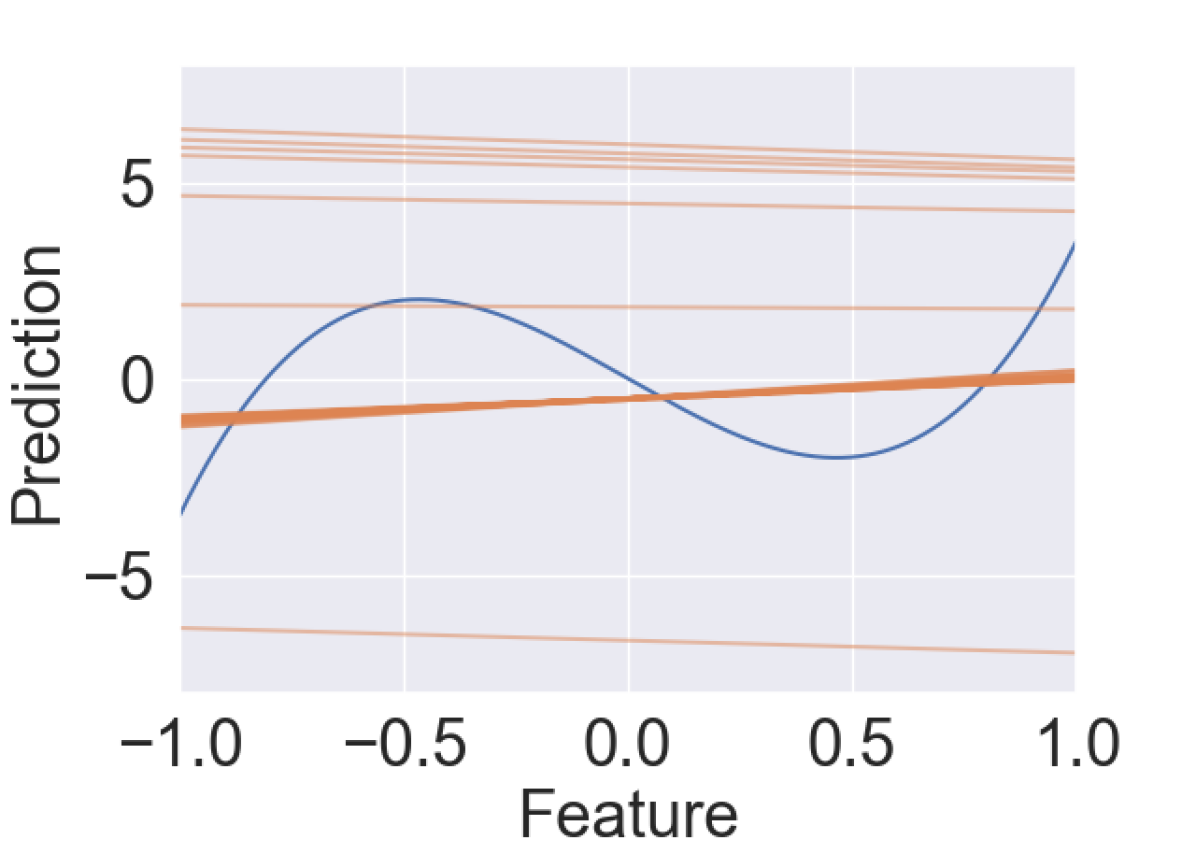

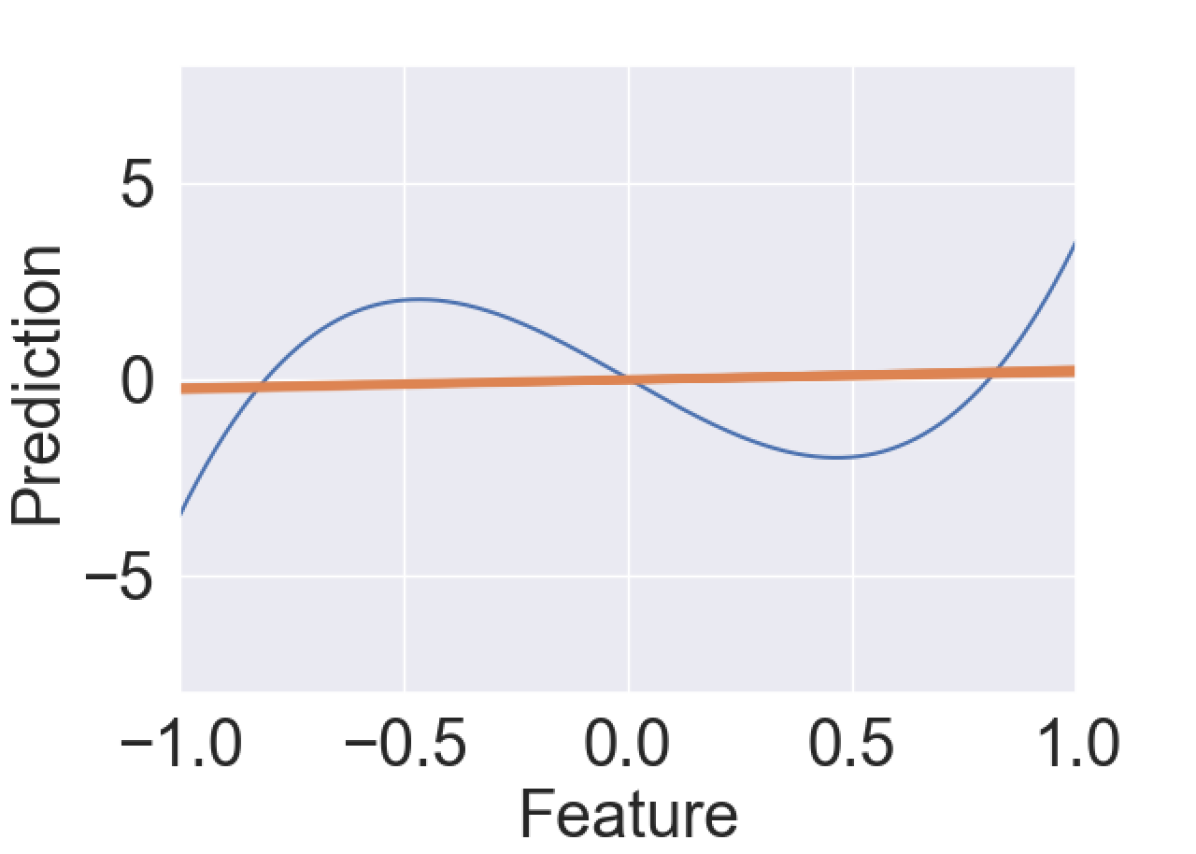

2.1 Motivating Example

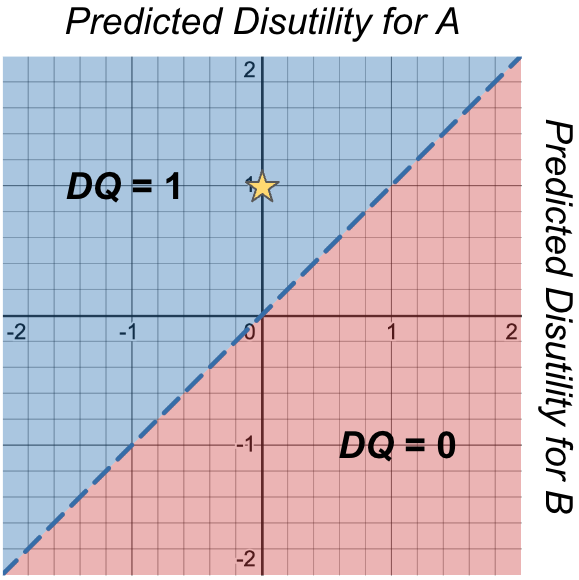

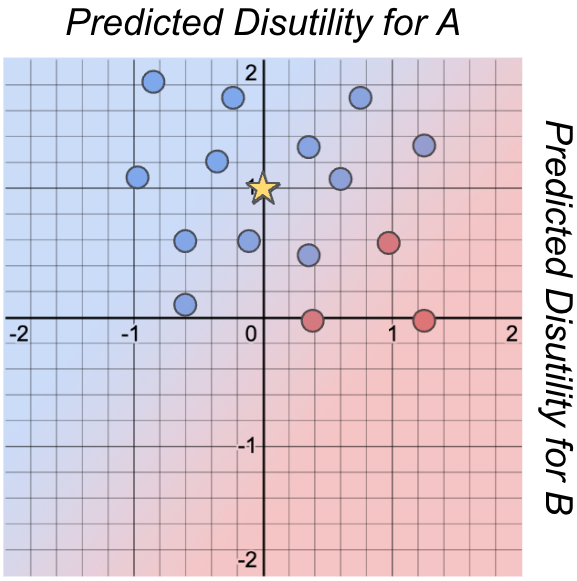

Consider an optimization where the goal is to predict the disutility of 2 agents (A, B), e.g., . Now, if these parameters are predicted perfectly, the decision is “Pick A”, and the decision loss is the true disutility of agent A, i.e., .

On the other hand, consider the set of predictions for . Any prediction in this set will yield the decision ‘Pick B” and a decision loss of 1. Given that the decision loss is constant in this region, the gradients are all zero, i.e., . As a result, if a predictive model makes such a prediction, it cannot improve its predictions by gradient descent. Therefore, although is what we want to minimize, we don’t want to fit it perfectly.

If instead of minimizing directly, we minimized a surrogate loss , gradient descent would lead to the model to predict regardless of the initialization (see Figure 2). While isn’t the true set of disutilities, it does lead to the optimal decision, i.e., “Pick A” and is thus effective from a predict-then-optimize perspective.

The challenge is then coming up with such surrogates. Although it is easy for the problem above, it becomes more complicated as the number and types of variables and constraints grows. Below, we propose an approach to automatically learn good surrogates. Figure 2(c) shows what our method looks like for the example above.

3 Related Work

A great deal of recent work on decision-focused learning and related topics aims to incorporate information about a downstream optimization problem into the training of a machine learning models. Some optimization problems (especially strongly convex ones) can be directly differentiated through Donti et al. (2017); Amos et al. (2018); Agrawal et al. (2019). For others, particularly discrete optimization problems with ill-defined gradients, a variety of approaches have been proposed. Most of these construct surrogate loss functions via smoothing the optimization problem Mensch and Blondel (2018); Wilder et al. (2019a); Ferber et al. (2020); Wilder et al. (2019b); Tschiatschek et al. (2018); Mandi and Guns (2020). Alternatively, Elmachtoub and Grigas (2021) propose a closed-form convex surrogate loss with desirable theoretical properties; however, this loss applies only when the optimization problem has a linear objective function. Similarly, Mulamba et al. (2021) provide a contrastive learning-based surrogate which does not require differentiation through optimization, but which is also developed specifically for linear objectives. When the predictive model is itself a linear function, Guler et al. (2022) propose an approach to search directly for the best model.

Perhaps the most related work to ours is by Berthet et al. (2020). They differentiate through linear optimization problems during training by adding randomized perturbations to smooth the induced loss function. Specifically, they randomly perturb the predictions with random noise and solve for , which can be interpreted as replacing the decision loss with its averaged value in a neighborhood around , where the averaging smooths the function and ensures differentiability. There are two key differences between our approach and theirs. First, they apply random perturbations to optimization in the training loop in order to produce a smoother surrogate loss. By contrast, we use random perturbations to learn a loss function prior to training; during training optimization is removed entirely. This allows us to use the same random samples to inform each training iteration instead of drawing new samples per iteration. Second, their approach applies only to linear objective functions while ours applies to arbitrary optimization problems.

4 Locally Optimized Decision Losses (LODL)

In this paper, we do away with the need for custom task-specific relaxations of the optimization problem by instead translating task-specific information from the decision loss into a loss function that (i) approximates the behavior of , and (ii) is convex by construction.

Our broad strategy to do this is to learn the function using supervised machine learning. Specifically, we proceed in 3 steps:

-

1.

We simplify the learning problem in two ways (Section 4.1). First, we learn a separate LODL for every () pair in the dataset to make our learning problem easier. Second, we note that there’s a chicken-and-egg problem associated with learning LODLs—to train the LODL we need inputs of the form , but to produce we need a predictive model trained on said LODL. To resolve this, we make the assumption that our predictive model will get us sufficiently close to the true labels . This means:

-

2.

Given these simplifications, we propose convex-by-construction parametric forms for (Section 4.2). We subtract a constant from the target to ensure that the function to be learned has a minima at and that the result can be modeled well by a convex function:

- 3.

4.1 Local Loss Functions

We introduce a separate set of parameters for each in the training set. We take this step because learning a global approximation to (for arbitrary ) is hard; it requires learning a closed-form approximation to the general optimization problem which may not always exist. Introducing separate parameters per-instance gives two key advantages.

-

1.

Learning for a specific : Instead of learning a function to imitate , we instead learn different functions that imitate for each . Doing this significantly reduces the dimensionality of the learning problem—this is especially relevant when is not very large in comparison to (as in our experiments). It also circumvents the need to enforce invariance properties on the global loss. For example, many optimization problems are invariant to permutations of the ordering of dimensions in , making it difficult to measure the quality of ’s across different instances. In a local loss, the ordering of the dimensions is fixed and so this issue is no longer relevant.

-

2.

Learning for only : In addition to the simplification above, we don’t try to learn a faithful approximation —we instead limit ourselves to learning an approximation of only when is in the neighborhood of . We assume that our predictive model will always get us in the neighborhood of the true labels, and the utility of LODL is in helping distinguish between these points.

The combination of these two choices makes the learned a “local” surrogate for , rather than a global one.

4.2 Representing the

The key design choice in instantiating our framework is choice of the parametric family used to represent the LODL. Optimization problems can induce a complex loss landscape which is not easily summarized in a closed-form function with concise parameterization. Accordingly, we design a set of families which capture phenomena particularly important for common families of predict-then-optimize problems.

Parametric families for the local losses

Having made the decision to allow separate parameters for each training instance, the second design choice is how to represent each local loss, i.e., the specific parametric family to use. Our choice must be sufficiently expressive to capture the local dynamics of the optimization problem while remaining sufficiently efficient to be replicated across the training instances. We propose that the structure of the loss function should capture the underlying rationale for why decision-focused learning provides an advantage over 2-stage in the first place; this is the key behavior which will underpin improved decision quality. We identify three key phenomena which motivate the design of the family of loss functions:

-

1.

Relative importance of different dimensions: Typically, the different dimensions of a prediction problem are given equal weight, e.g., the MSE weights errors in each coordinate of equally. However, there may be some dimensions along which is more sensitive to local perturbations. For example, a knapsack problem may be especially sensitive to errors in the value of items which are on the cusp of being chosen. In such cases, DFL can capture the relative importance of accurately predicting different dimensions.

-

2.

Cost of correlation: Given the possibly large dimensionality of , in practice, the predictive model does not typically predict directly. Instead, the the structure of the optimization is exploited to make multiple predictions that are then combined to create . For example, in a knapsack problem, we might train a model which separately predicts the value of each item (i.e., predicts each entry of separately) using features specific to that item, instead of jointly predicting the entire set of values using the features of all of the items. However, Cameron et al. (2022) show that ignoring the correlation between different sub- scale predictions (as in 2-stage) can result in poor optimization performance, and that DFL can improve by propagating information about the interactions between entries of to the predictive model.

-

3.

Directionality of predictions: In the example from the introduction, the prediction produces the same decision as . On the other hand, the prediction leads to a different decision. As a result, over-predicting and under-predicting often have different associated costs for some optimization problems. Predictive models trained with DFL can take into account this behavior while those trained by typical symmetric 2-Stage losses like MSE cannot.

Given these insights, we propose three corresponding families of loss functions for , each of which is convex by design and has a global minima at the true label , a desirable property because also has its minima at .

-

1.

WeightedMSE: To take into account the relative importance of different dimensions, we propose a weighted version of MSE:

where ‘weights’ are the parameters of the LODL, i.e., (for convexity).

-

2.

Quadratic: To take into account the effect of correlation of different dimensions on each other, we propose learning a quadratic function that has terms of the form :

where is a learned low-rank symmetric Positive semidefinite (PSD) matrix. This family of functions is convex as long as is PSD, which we enforce by parameterizing , where is a low-rank triangular matrix of dimension and is the desired rank.

This loss function family has an appealing interpretation because learning LODL is similar to estimating the partial derivative of with respect to its first input . Specifically, consider the first three terms of the Taylor expansion of with respect to at :

Quadratic can be seen as a -order Taylor-series approximation of at where the learned approximates the Hessian of . Note that WeightedMSE is a special case of this Quadratic loss when .

-

3.

DirectedWeightedMSE and DirectedQuadratic: To take into account the fact that overpredicting and underpredicting can have different consequences, we propose modifications to the two loss function families above. For WeightedMSE, we redefine the weight vector as below, and learn both and . Similarly for Quadratic, we define 4 copies of the parameter based on the directionality of the predictions.

4.3 Learning

Given families proposed in Section 4.1, our goal is to learn some for every such that for “close” to . We propose a supervised approach to learning which proceeds in two steps (Figure 1): (1) we build a dataset mapping in the region of , and then (2) we use this dataset to estimate by minimizing the mean squared error to the true decision loss:

| (2) |

This framework has the key advantage of reducing the design of good surrogate tasks (a complex problem requiring in-depth knowledge of each optimization problem) to supervised learning (for which many methods are available). Indeed, future advances, e.g. in representation learning, can simply be plugged into our framework.

The major remaining step is to specify the construction of the dataset for supervised learning of . We propose to construct this dataset by sampling a set of points in the vicinity of and calculate for each. In this paper, we consider three sampling strategies:

-

1.

All-Perturbed: Add zero-mean Gaussian noise to the true label :

where is a normalization factor and is a identity matrix.

-

2.

1-Perturbed or 2-Perturbed: Estimating the behavior of for small can alternatively be interpreted as estimating (i.e., the partial derivative of w.r.t. its first input ) at because all the dimensions of are being varied simultaneously. While computing is computationally challenging, it can be estimated using the simpler 1st or 2nd partial derivatives. This corresponds to perturbing only one or two dimensions at a time.

4.4 Time Complexity of Learning LODLs

The amount of time taken by each of the methods using gradient descent is:

-

•

2-Stage = , where is the amount of time taken to run one forward and backwards pass through the model for one optimization instance, is the number of optimization instances, and is the number of time-steps is trained for.

-

•

DFL = , where is the time taken to solve the forward pass of one optimization instance and is the time taken to compute the backward pass.

-

•

LODL = , where is the number of samples needed to train the LODL, and is the amount of time taken to run one forward and backwards pass through the LODL. The three terms correspond to (i) generating samples, (ii) training LODLs, and (iii) training using the trained LODLs.

In practice, we find that . As a result, the difference in complexity of DFL and LODL is roughly vs. . Further, the calculation above assumes that LODLs are trained in the same way as . However, in practice, they can often be learned much faster, sometimes even in closed form (e.g., WeightedMSE and DirectedWeightedMSE), leading to an effective runtime of . Then, the difference between DFL and LODL boils down to vs. , i.e., the number of time-steps needed to train vs. the number of samples needed to train the LODL.

While our approach can be more computationally expensive, it typically isn’t for two reasons:

-

•

Amortization: We need only sample candidate predictions once, to then train any number of LODLs (e.g., WeightedMSE, DirectedQuadratic) without ever having to call an optimization oracle. Once the LODLs have been learned, you can train any number of predictive models based on said LODLs—in contrast to DFL, which requires calling the oracle to train each model. DFL is thus more expensive when training a large number of models (e.g., for hyperparameter/architecture search, trading-off performance vs. inference time vs. interpretability, etc.). In the future, we imagine that datasets could be shipped with not only features and labels, but also LODLs associated with downstream tasks!

-

•

Parallelizability: The sample generation process for LODL is completely parallelizable, resulting in an lower-bound wall-clock complexity for our approach. In contrast, the calls to the optimization oracle in DFL are interleaved with the training of and, as a result, cannot be parallelized with respect to , resulting in an wall-clock complexity.

We demonstrate this empirically in Section 5.3.

5 Experiments

To validate the efficacy of our approach, we run experiments on three resource allocation tasks from the literature. We use the term decision quality (higher is better) instead of because these are all maximization problems.

Linear Model This domain involves learning a linear model when the underlying mapping between features and predictions is cubic. Such problems are common in the explainable AI literature Narayanan et al. (2021); Futoma et al. (2020); Hughes et al. (2018) where predictive models must be interpretable.

-

•

Predict: Given a feature , use a linear model to predict the utility of resource , where the true utility is . Combining predictions yields .

-

•

Optimize: Choose the out of resources with highest utility:

-

•

Surrogate: Because the operation is piecewise constant, DFL requires a surrogate—we use the soft Top-K proposed by Xie et al. (2020). Although this surrogate is convex in the decision variables, it is not convex in the predictions.

Web Advertising This is a submodular optimization task taken from Wilder et al. (2019a). The aim is to determine on which websites to advertise given features about different websites.

-

•

Predict: Given features associated with some website , predict the click-through rates (CTRs) for a fixed set of users on websites . To obtain the features for each website , true CTRs from the Yahoo! Webscope Dataset Yahoo! (2007) are scrambled by multiplying with a random matrix , i.e., .

-

•

Optimize: Given the matrix of CTRs, determine on which (budget) websites to advertise such that the expected number of users that click on the ad at least once is maximized, i.e., , where all the .

-

•

Surrogate: Instead of requiring that , the multi-linear relaxation from Wilder et al. (2019a) allows fractional values. The induced by the relaxation is non-convex.

Portfolio Optimization This is a Quadratic Programming domain Donti et al. (2017); Wang et al. (2020) in which the aim is to choose a distribution over stocks that maximizes the expected profit minus a quadratic risk penalty. We choose this domain as a stress test—it is highly favorable for DFL because the optimization problem naturally provides informative gradients and thus requires no surrogate.

-

•

Predict: Given historical data about stock , predict the future stock price . We use historical data from 2004 to 2017 for a set of stocks from the QuandlWIKI dataset Quandl (2022).

-

•

Optimize: Given a historical correlation matrix between pairs of stocks, choose a distribution over stocks that maximizes , where is the risk aversion constant.

More experimental setup details are provided in Appendix A.

5.1 Results

| Loss Function | Normalized On Test Data | ||

| Linear Model | Web Advertising | Portfolio Optimization | |

| Random | 0 | 0 | 0 |

| Optimal | 1 | 1 | 1 |

| 2-Stage (MSE) | -0.95 ± 0.00 | 0.48 ± 0.15 | 0.32 ± 0.02 |

| DFL | 0.83 ± 0.38 | 0.85 ± 0.10 | 0.35 ± 0.02 |

| NN | 0.96 ± 0.00 | 0.81 ± 0.14 | -0.11 ± 0.08 |

| WeightedMSE | -0.93 ± 0.06 | 0.58 ± 0.15 | 0.31 ± 0.02 |

| DirectedWeightedMSE | 0.96 ± 0.00 | 0.53 ± 0.14 | 0.32 ± 0.02 |

| Quadratic | -0.75 ± 0.38 | 0.93 ± 0.04 | 0.27 ± 0.02 |

| DirectedQuadratic | 0.96 ± 0.00 | 0.91 ± 0.04 | 0.33 ± 0.01 |

We train either a linear model (for the Linear Model domain) or a 2-layer fully-connected neural network with 500 hidden units (for the other domains) using LODLs and compare it to:

-

1.

Random: The predictions are sampled uniformly from .

-

2.

Optimal: The predictions are equal to the true labels .

-

3.

2-Stage: The model is trained on the standard MSE loss ().

-

4.

DFL: Decision-focused learning using the specified surrogate.

-

5.

NN: To determine how important convexity is for LODL we define in which is a 4-layer fully-connected Neural Network (NN) with 100 hidden units.

Table 1 shows the main results. We find that, in all domains, training predictive models with LODL outperforms training them with a task-independent 2-stage loss. Surprisingly, it also outperforms DFL, which has the benefit of handcrafted surrogates, in two of the three. This is strong evidence in favor of our hypothesis that we can automate away the need for handcrafting surrogates. We first analyze the results in terms of the domains:

-

1.

Linear Model: In this domain, the directionality of predictions is very important. As we describe in Section 2.1, predicting values higher than the true utilities for the resources with highest utility, does not change the decision. However, if their predicted utility is lower than that of the th best resource, the decision quality is affected. As a result, we see that the “Directed” methods perform significantly better than their competition.

-

2.

Web Advertising: In this domain, Wilder et al. (2019a) suggest that the decision quality is linked to being able to predict the quantity (the sum of CTRs across all users for a given website ). However, because the input features for every are the same , the errors can be correlated and so the sum can be biased. As a result, the ability to penalize the correlations between two predictions and is important to being able to perform well on this task—which results in the Quadratic methods outperforming the others.

-

3.

Portfolio Optimization: Given that this stress-test domain was built to be favorable to , it outperforms all other approaches with statistical significance. While the directed LODL methods do not outperform DFL, they nonetheless significantly outperform 2-stage at .

We now analyze the results in terms of the methods:

-

1.

Our DirectedQuadratic consistently does well: In addition to consistently high expected values (always better than 2-stage), the associated variance is lower as well.

-

2.

Lack of convexity can cause inconsistent results: While NN does well in the first two domains, it fails catastrophically in the Portfolio Optimization domain.

-

3.

DFL has a large variance in performance: In both the ”Web Advertising” and ”Linear Model” domain, DFL has higher variation than the best performing LODLs. We posit that this is also because of the lack of convexity of the surrogates that DFL uses in these two domains.

5.2 Ablations

We study the impact of the sampling strategy and number of samples on the performance of the LODL methods in the Web Advertising domain in Table 3. We find:

-

1.

Sampling strategy (Table 4(d)): The best sampling strategy is loss family-specific. Specifically, NN and DirectedWeightedMSE perform best with the “2-Perturbed” strategy, while the remaining LODLs perform best with the “All-Perturbed” strategy.

-

2.

Number of samples (Table 4(e)): All models perform better with more samples. In addition, the variance reduces as the number of samples increases (especially for Quadratic), suggesting that better approximations of lead to more consistent outcomes.

5.3 Computational Cost of Learning with LODLs

We measure the time taken to learn predictive models with LODLs in the Web Advertisement domain. We train each LODL for 100 gradient descent steps using 5000 samples and train the predictive model for 500 steps (the same as the setup as Table 1). We find:

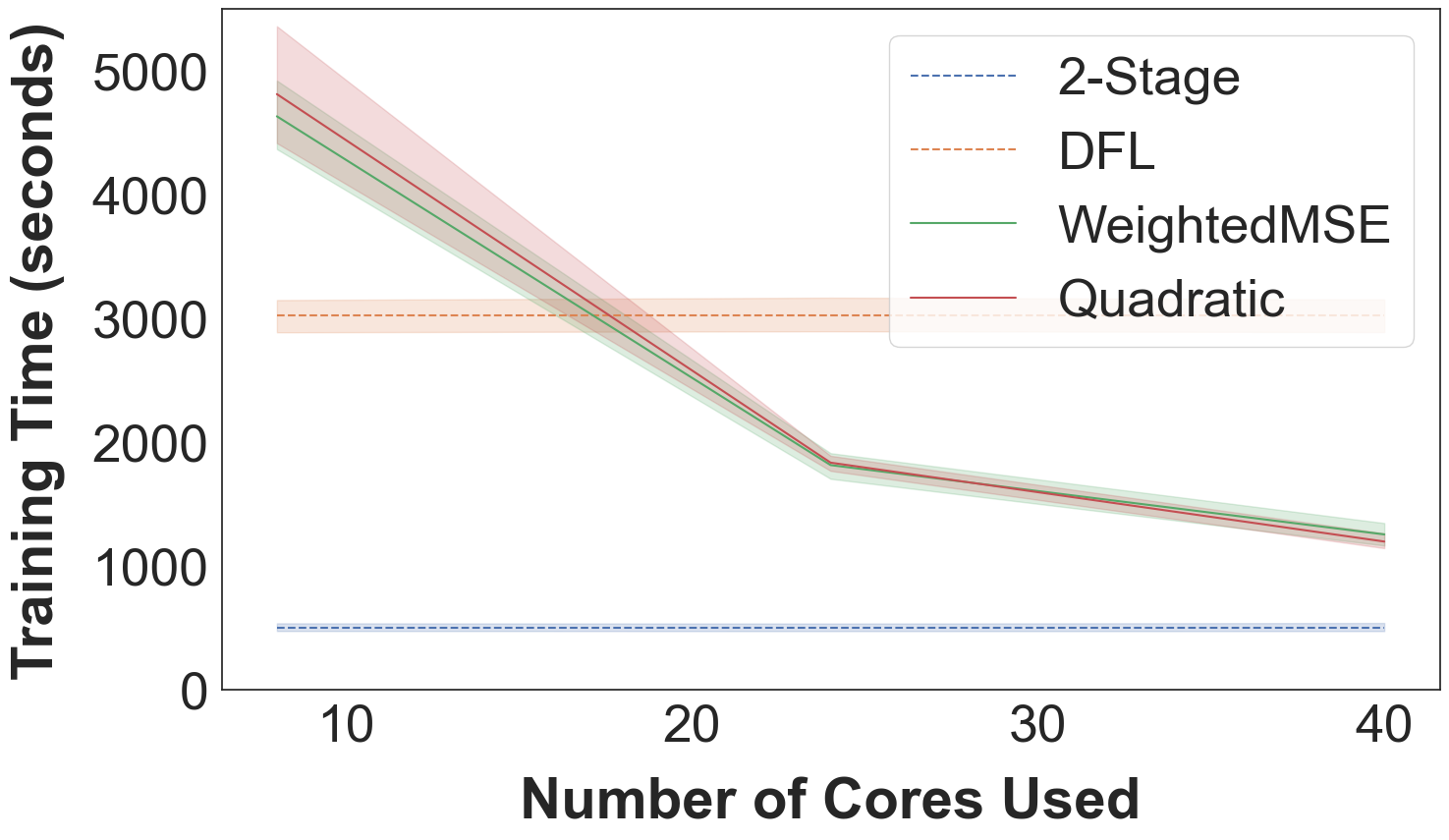

-

1.

Learning LODLs is parallelizable: Figure 3(a) shows that the cost of training a predictive model using LODLs decreases near-linearly in the number of cores used. With more than 20 cores, training with LODLs can be cheaper than training with DFL for this domain.

-

2.

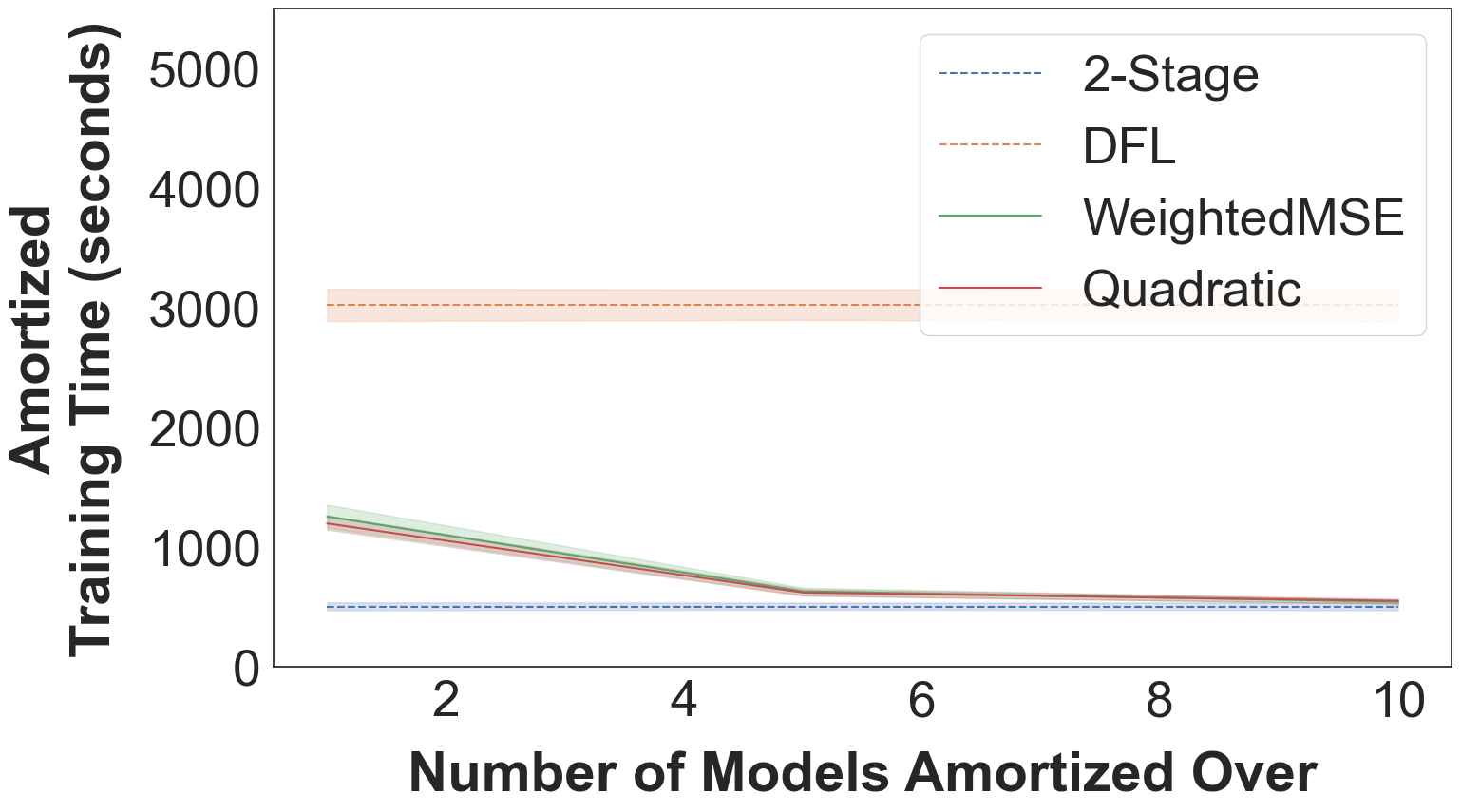

If LODLs can be reused, their (already low) overhead quickly diminishes: From Figure 3(b) we see that even for a modest amount of amortization (over 5-10 predictive models), the training time using LODLs converges to that of two-stage (shown using parallelization with 40 cores).

5.4 Correlation between the ‘quality’ of LODL and decision quality

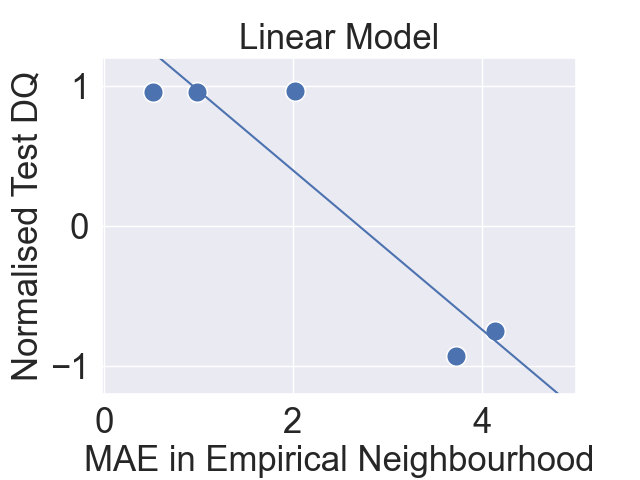

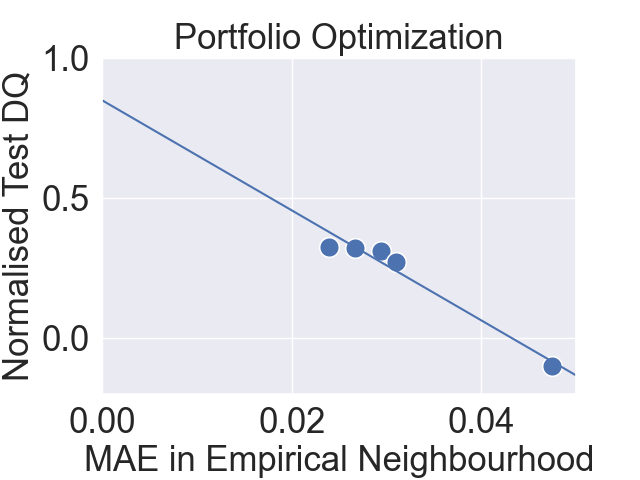

Recall that LODL losses are fit using a Gaussian sampling strategy centered around the true labels. It is natural to ask how well this proxy loss correlates with the decision quality on test data. We do this by measuring the mean absolute error (MAE) of LODL relative to the ground truth decision loss for points in the Gaussian neighborhood around the true labels.

This Gaussian neighborhood is only an approximation of the true distribution of interest—the distribution of predictions generated by the predictive model that is trained using the LODL loss. We can measure the MAE on this distribution, which we call the empirical neighborhood.

| Approach | MAE in Gaussian | MAE in Empirical | Normalized DQ |

|---|---|---|---|

| Neighborhood | Neighborhood | on Test Data | |

| (x ) | (x ) | ||

| NN | |||

| WeightedMSE | |||

| DirectedWeightedMSE | |||

| Quadratic | |||

| DirectedQuadratic |

![[Uncaptioned image]](/html/2203.16067/assets/budget_allocation.png)

Table 2 shows the results for the Budget Allocation domain, while the remaining graphs are in Appendix B.3. All methods are able to approximate the comparably well in the Gaussian neighborhood, but this does not correlate well with decision quality. In contrast, the error on the empirical neighborhood is tightly linearly correlated with decision quality. Furthermore, if we extrapolate the line of best fit to where the MAE is 0, i.e., when there is no discrepancy LODL and , we find that the trend predicts the normalized would be .

6 Discussion and Conclusion

Our work proposes a conceptual shift from hand-crafting surrogate losses for decision problems to automatically learning them, and demonstrates experimentally that the LODL paradigm enables us to learn high-quality models without such manual effort. Nevertheless, our current instantiation of this framework has limitations which are areas for future work.

We considered LODLs that additively decompose across the dimensions of , allowing us to isolate the effects of fit to from the generalization performance across the dimensions of . Future work may learn models that generalize across dimensions, allowing for even greater scalability.

We demonstrate that the fit of a LODL to the empirical neighborhood around the ground truth label is highly correlated with the eventual decision quality. While the Gaussian neighborhood method does yield models that perform well, it does not correlate well with the decision quality across LODL parameterizations. It would be valuable to study the empirical neighborhood to better understand the reasons for this discrepancy and potentially develop LODLs with even stronger performance.

In summary, LODL provides an alternate framework for machine learning which informs decision making, opening up new avenues towards models which are both high-performing and easily trained.

Acknowledgments and Disclosure of Funding

Research was sponsored by the ARO and was accomplished under Grant Number: W911NF-18-1-0208. Wilder was supported by the Schmidt Science Fellows program.

References

- Agrawal et al. [2019] Akshay Agrawal, Brandon Amos, Shane Barratt, Stephen Boyd, Steven Diamond, and J Zico Kolter. Differentiable convex optimization layers. Advances in Neural Information Processing Systems, 32, 2019.

- Amos et al. [2018] Brandon Amos, Ivan Jimenez, Jacob Sacks, Byron Boots, and J. Zico Kolter. Differentiable mpc for end-to-end planning and control. In Advances in Neural Information Processing Systems, volume 31, 2018.

- Amos et al. [2019] Brandon Amos, Vladlen Koltun, and J Zico Kolter. The limited multi-label projection layer. arXiv preprint arXiv:1906.08707, 2019.

- Berthet et al. [2020] Quentin Berthet, Mathieu Blondel, Olivier Teboul, Marco Cuturi, Jean-Philippe Vert, and Francis Bach. Learning with differentiable pertubed optimizers. Advances in Neural Information Processing Systems, 33:9508–9519, 2020.

- Cameron et al. [2022] Chris Cameron, Jason Hartford, Taylor Lundy, and Kevin Leyton-Brown. The perils of learning before optimizing. Proceedings of the AAAI Conference on Artificial Intelligence, 36, 2022.

- Demirović et al. [2019] Emir Demirović, Peter J Stuckey, James Bailey, Jeffrey Chan, Chris Leckie, Kotagiri Ramamohanarao, and Tias Guns. An investigation into prediction+ optimisation for the knapsack problem. In International Conference on Integration of Constraint Programming, Artificial Intelligence, and Operations Research, pages 241–257. Springer, 2019.

- Donti et al. [2017] Priya Donti, Brandon Amos, and J Zico Kolter. Task-based end-to-end model learning in stochastic optimization. Advances in Neural Information Processing Systems, 30, 2017.

- Elmachtoub and Grigas [2021] Adam N Elmachtoub and Paul Grigas. Smart “predict, then optimize”. Management Science, 2021.

- Ferber et al. [2020] Aaron Ferber, Bryan Wilder, Bistra Dilkina, and Milind Tambe. MIPaaL: Mixed integer program as a layer. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 34, pages 1504–1511, 2020.

- Futoma et al. [2020] Joseph Futoma, Michael Hughes, and Finale Doshi-Velez. POPCORN: Partially observed prediction constrained reinforcement learning. In International Conference on Artificial Intelligence and Statistics, pages 3578–3588. PMLR, 2020.

- Guler et al. [2022] Ali Ugur Guler, Emir Demirovic, Jeffrey Chan, James Bailey, Christopher Leckie, and Peter J Stuckey. Divide and learn: A divide and conquer approach for predict+ optimize. Proceedings of the AAAI Conference on Artificial Intelligence, 36, 2022.

- Hughes et al. [2018] Michael Hughes, Gabriel Hope, Leah Weiner, Thomas McCoy, Roy Perlis, Erik Sudderth, and Finale Doshi-Velez. Semi-supervised prediction-constrained topic models. In Proceedings of the Twenty-First International Conference on Artificial Intelligence and Statistics, pages 1067–1076, 2018.

- Isinkaye et al. [2015] Folasade Olubusola Isinkaye, Yetunde O Folajimi, and Bolande Adefowoke Ojokoh. Recommendation systems: Principles, methods and evaluation. Egyptian Informatics Journal, 16(3):261–273, 2015.

- Kar et al. [2017] Debarun Kar, Benjamin Ford, Shahrzad Gholami, Fei Fang, Andrew Plumptre, Milind Tambe, Margaret Driciru, Fred Wanyama, Aggrey Rwetsiba, Mustapha Nsubaga, and Joshua Mabonga. Cloudy with a chance of poaching: Adversary behavior modeling and forecasting with real-world poaching data. In Proceedings of the 16th Conference on Autonomous Agents and MultiAgent Systems, page 159–167, 2017.

- Mandi and Guns [2020] Jayanta Mandi and Tias Guns. Interior point solving for LP-based prediction+optimisation. Advances in Neural Information Processing Systems, 33:7272–7282, 2020.

- Mandi et al. [2020] Jayanta Mandi, Peter J Stuckey, Tias Guns, et al. Smart predict-and-optimize for hard combinatorial optimization problems. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 34, pages 1603–1610, 2020.

- Markowitz and Todd [2000] Harry M Markowitz and G Peter Todd. Mean-variance analysis in portfolio choice and capital markets. John Wiley & Sons, 2000.

- Mensch and Blondel [2018] Arthur Mensch and Mathieu Blondel. Differentiable dynamic programming for structured prediction and attention. In International Conference on Machine Learning, pages 3462–3471. PMLR, 2018.

- Michaud [1989] Richard O Michaud. The Markowitz optimization enigma: Is ‘optimized’ optimal? Financial Analysts Journal, 45(1):31–42, 1989.

- Mulamba et al. [2021] Maxime Mulamba, Jayanta Mandi, Michelangelo Diligenti, Michele Lombardi, Victor Bucarey, and Tias Guns. Contrastive losses and solution caching for predict-and-optimize. In Proceedings of the International Joint Conferences on Artificial Intelligence, 2021.

- Narayanan et al. [2021] Sanjana Narayanan, Abhishek Sharma, Catherine Zeng, and Finale Doshi-Velez. Prediction-focused mixture models. arXiv preprint arXiv:2110.13221, 2021.

- Quandl [2022] Quandl. WIKI various end-of-day data, 2022. URL https://www.quandl.com/data/WIKI.

- Tschiatschek et al. [2018] Sebastian Tschiatschek, Aytunc Sahin, and Andreas Krause. Differentiable submodular maximization. In Proceedings of the 27th International Joint Conference on Artificial Intelligence, pages 2731–2738, 2018.

- Wang et al. [2020] Kai Wang, Bryan Wilder, Andrew Perrault, and Milind Tambe. Automatically learning compact quality-aware surrogates for optimization problems. Advances in Neural Information Processing Systems, 33:9586–9596, 2020.

- Wilder et al. [2019a] Bryan Wilder, Bistra Dilkina, and Milind Tambe. Melding the data-decisions pipeline: Decision-focused learning for combinatorial optimization. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 33, pages 1658–1665, 2019a.

- Wilder et al. [2019b] Bryan Wilder, Eric Ewing, Bistra Dilkina, and Milind Tambe. End to end learning and optimization on graphs. Advances in Neural Information Processing Systems, 32:4672–4683, 2019b.

- Xie et al. [2020] Yujia Xie, Hanjun Dai, Minshuo Chen, Bo Dai, Tuo Zhao, Hongyuan Zha, Wei Wei, and Tomas Pfister. Differentiable top-k with optimal transport. Advances in Neural Information Processing Systems, 33:20520–20531, 2020.

- Yahoo! [2007] Yahoo! Webscope dataset, 2007. URL https://webscope.sandbox.yahoo.com/. ydata-ysm-advertiser-bids-v1.0.

Checklist

The checklist follows the references. Please read the checklist guidelines carefully for information on how to answer these questions. For each question, change the default [TODO] to [Yes] , [No] , or [N/A] . You are strongly encouraged to include a justification to your answer, either by referencing the appropriate section of your paper or providing a brief inline description. For example:

-

•

Did you include the license to the code and datasets? [Yes] See Section LABEL:gen_inst.

-

•

Did you include the license to the code and datasets? [No] The code and the data are proprietary.

-

•

Did you include the license to the code and datasets? [N/A]

Please do not modify the questions and only use the provided macros for your answers. Note that the Checklist section does not count towards the page limit. In your paper, please delete this instructions block and only keep the Checklist section heading above along with the questions/answers below.

-

1.

For all authors…

-

(a)

Do the main claims made in the abstract and introduction accurately reflect the paper’s contributions and scope? [Yes]

-

(b)

Did you describe the limitations of your work? [Yes] See Section 6

-

(c)

Did you discuss any potential negative societal impacts of your work? [N/A]

-

(d)

Have you read the ethics review guidelines and ensured that your paper conforms to them? [Yes]

-

(a)

-

2.

If you are including theoretical results…

-

(a)

Did you state the full set of assumptions of all theoretical results? [N/A]

-

(b)

Did you include complete proofs of all theoretical results? [N/A]

-

(a)

-

3.

If you ran experiments…

-

(a)

Did you include the code, data, and instructions needed to reproduce the main experimental results (either in the supplemental material or as a URL)? [Yes] As supplemental material.

-

(b)

Did you specify all the training details (e.g., data splits, hyperparameters, how they were chosen)? [Yes] In the appendix

-

(c)

Did you report error bars (e.g., with respect to the random seed after running experiments multiple times)? [Yes] In all tables.

-

(d)

Did you include the total amount of compute and the type of resources used (e.g., type of GPUs, internal cluster, or cloud provider)? [Yes] In the appendix

-

(a)

-

4.

If you are using existing assets (e.g., code, data, models) or curating/releasing new assets…

-

(a)

If your work uses existing assets, did you cite the creators? [Yes]

-

(b)

Did you mention the license of the assets? [No] It isn’t clear exactly what the license is, but all the datasets are publicly available.

-

(c)

Did you include any new assets either in the supplemental material or as a URL? [No]

-

(d)

Did you discuss whether and how consent was obtained from people whose data you’re using/curating? [N/A]

-

(e)

Did you discuss whether the data you are using/curating contains personally identifiable information or offensive content? [No]

-

(a)

-

5.

If you used crowdsourcing or conducted research with human subjects…

-

(a)

Did you include the full text of instructions given to participants and screenshots, if applicable? [N/A]

-

(b)

Did you describe any potential participant risks, with links to Institutional Review Board (IRB) approvals, if applicable? [N/A]

-

(c)

Did you include the estimated hourly wage paid to participants and the total amount spent on participant compensation? [N/A]

-

(a)

Appendix A Extended Experimental Setup

We provide an extended version of the Experimental Setup from Section 5 below.

Linear Model

This domain involves learning a linear model when the underlying mapping between features and predictions is cubic. Concretely, the aim is to choose the top out of resources using a linear model. The fact that the features can be seen as 1-dimensional allows us to visualize the learned models (as seen in Figure 4).

Predict: Given a feature , use a linear model to predict the utility of choosing resource , where the true utility is given by . Combining predictions yields . There are 200 pairs in each of the training and validation sets, and 400 pairs in the test set.

Optimize: Given these predictions, choose the (budget) resources with the highest utility:

Surrogate: Because the operation is piecewise constant, DFL requires a surrogate—we use the soft Top-K proposed by Xie et al. [2020] that reframes the Top-K problem with entropy regularization as an optimal transport problem. Note that this surrogate is not convex in the predictions.

Intuition: With limited model capacity, you cannot model all the data accurately. Better performance can be achieved by modeling the aspects of the data that are most relevant to decision-making—in this case, the behavior of the top of resources. Such problems are common in the explainable AI literature Narayanan et al. [2021], Futoma et al. [2020], Hughes et al. [2018] where predictive models must be interpretable and so model capacity is limited.

Web Advertising

This is a submodular optimization task taken from Wilder et al. [2019a]. The aim is to determine on which websites to advertise given features about different websites. The predictive model being used is a 2-layer feedforward neural network with an intermediate dimension of 500 and ReLU activations.

Predict: Given features associated with some website , predict the clickthrough rates (CTRs) for a fixed set of users . These CTR predictions for each of the websites are stitched together to create an matrix of CTRs . The task is based on the Yahoo! Webscope Dataset Yahoo! [2007] which contains multiple CTR matrices. We randomly sample rows and columns from each matrix and then split the dataset such that the training, validation and test sets have 80, 20 and 500 matrices each. To generate the features for some website , the true CTRs for the website are scrambled by multiplying with a random matrix , i.e., .

Optimize: Given this matrix of CTRs, determine on which (budget) websites to advertise such that the expected number of users that click on the advertisement at least once is maximized:

Surrogate: Instead of requiring that , the multi-linear relaxation suggested in Wilder et al. [2019a] allows fractional values. However, while this relaxation may allow for non-zero gradients, the induced is non-convex because the term in the objective is non-convex in the predictions.

Intuition: In practice, the CTR values are so small that you can approximate because the product terms are almost zero, i.e., . As a result, the goal is to accurately predict , the sum of CTRs across all the users for a given website. However, because the input features for every are the same , the errors are correlated. As a result, when you add up the values the errors do not cancel out, leading to biased estimates.

Portfolio Optimization

This is a Quadratic Programming domain popular in the literature Donti et al. [2017], Wang et al. [2020] because it requires no relaxation in order to run DFL. The aim is to choose a distribution over stocks in a Markowitz portfolio optimization setup Markowitz and Todd [2000], Michaud [1989] that maximizes the expected profit minus a quadratic risk penalty. The predictive model being used is a 2-layer feedforward neural network with a 500-dimensional intermediate layer using ReLU activations, followed by an output layer with a ‘tanh’ activation.

Predict: Given historical data about some stock at time-step , predict the stock price at time-step . Combining the predictions across a consistent set of stocks together yields . We use historical price and volume data of S&P500 stocks from 2004 to 2017 downloaded from the QuandlWIKI dataset Quandl [2022] to generate and . There are 200 pairs in each of the training and validation sets, and 400 pairs in the test set.

Optimize: Given a historical correlation matrix between pairs of stocks, choose a distribution over stocks such that the future return is maximized subject to a quadratic risk penalty :

where is the risk aversion constant. The intuition behind the penalty is that if two stocks have strongly correlated historical prices, the penalty will be higher, forcing you to hedge your bets.

Intuition Along the lines of Cameron et al. [2022], DFL is able to take into account the correlations in predictions between the different stocks, while 2-stage is not.

Computation Infrastructure

We ran 100 samples for each pair—we used 10 different random seeds to generate the domain, and for each random seed we trained the s and the predictive model for 10 random intializations. We ran all the experiments in parallel on an internal cluster. Each individual experiment was performed on an Intel Xeon CPU with 64 cores and 128 GB memory.

Appendix B Detailed Experimental Results

B.1 Visualizing the Linear Model Domain

B.2 Ablations

| Approach | Normalized Test | ||

|---|---|---|---|

| 1-Perturbed | 2-Perturbed | All-Perturbed | |

| NN | |||

| WeightedMSE | |||

| DirectedWeightedMSE | |||

| Quadratic | |||

| DirectedQuadratic | |||

| Approach | Normalized Test | ||

|---|---|---|---|

| 50 samples | 500 samples | 5000 samples | |

| NN | |||

| WeightedMSE | |||

| DirectedWeightedMSE | |||

| Quadratic | |||

| DirectedQuadratic | |||

B.3 Extending the Results from Section 5.4 to Different Domains

Figure 5 extends the observation that the LODL’s goodness of fit in the Empirical Neighborhood linearly correlates to improved ‘Decision Quality’ to the different domains considered in this paper.