Testing the identification of causal effects in observational data

Martin Huber* & Jannis Kueck+

*University of Fribourg, Department of Economics

+University of Düsseldorf, Faculty of Business Administration and Economics

Abstract

This study demonstrates the existence of a testable condition for the identification of the causal effect of a treatment on an outcome in observational data, which relies on two sets of variables: observed covariates to be controlled for and a suspected instrument. Under a causal structure commonly found in empirical applications, the testable conditional independence of the suspected instrument and the outcome given the treatment and the covariates has two implications. First, the instrument is valid, i.e. it does not directly affect the outcome (other than through the treatment) and is unconfounded conditional on the covariates. Second, the treatment is unconfounded conditional on the covariates such that the treatment effect is identified. We suggest tests of this conditional independence based on machine learning methods that account for covariates in a data-driven way and investigate their asymptotic behavior and finite sample performance in a simulation study. We also apply our testing approach to evaluating the impact of fertility on female labor supply when using the sibling sex ratio of the first two children as supposed instrument, which by and large points to a violation of our testable implication for the moderate set of socio-economic covariates considered.

JEL Classification: C12, C21, C26

Keywords: treatment effects, causality, conditional independence, instrument, covariates, hypothesis test, double machine learning.

The authors are grateful to Joachim Freyberger, Christoph Rothe, and conference/seminar participants at the Causal Data Science Meeting (2022), the Annual Meetings of the German Economic Association (2022; Basel), the Conference on Counterfactual Methods for Policy Impact Evaluation (2022; Mannheim), and the research seminars at the Luxembourg Institute of Socio-Economic Research (2022) and the University of Tübingen (2022) for their valuable comments. Addresses for correspondence: Martin Huber, University of Fribourg, Bd. de Pérolles 90, 1700 Fribourg, Switzerland; martin.huber@unifr.ch. Jannis Kueck, University of Hamburg, Moorweidenstraße 18, 20148 Hamburg, Germany; jannis.kueck@uni-hamburg.de.

1 Introduction

Causal inference methods for assessing the effect of a treatment or policy intervention (e.g. a training or a marketing campaign) on an outcome variable (e.g. earnings or sales) typically make use of identifying assumptions that are deemed untestable. For instance, the popular selection-on-observables, unconfoundedness, conditional independence, or ignorability assumption imposes that the treatment is as good as randomly assigned after controlling for observed covariates, see e.g. ImWo08 for a review of evaluation approaches in this context. Whether the set of covariates is sufficient for this assumption to hold is conventionally motivated based on theory, intuition, domain knowledge, or previous empirical findings.

In this paper, we demonstrate that the existence of a testable condition for the satisfaction of the selection-on-observables assumption in observational data in empirically relevant causal models, which implies that identification can be tested in the data. This condition relies on two types of observed characteristics, namely covariates to be controlled for and a suspected instrument. The condition arises if the following assumptions hold: First, there is no reverse causality from the outcome to the treatment, covariates, or the suspected instrument and from the treatment to the covariates or the suspected instrument. Second, the suspected instrument is statistically associated with the treatment conditional on the covariates, e.g. through a first stage effect of the suspected instrument on the treatment. If the suspected instrument is conditionally independent of the outcome given the treatment and the covariates in this context, then the instrument and the treatment satisfy the following two conditions: (A) the instrument is valid, i.e. does not directly affect the outcome (other than through the treatment) and is not associated with unobservables affecting the outcome conditional on the covariates and (B) the treatment is not associated with unobservables affecting the outcome conditional on the covariates. The latter means that the selection-on-observables assumption holds. Therefore, the conditional independence of the suspected instrument points to the identification of treatment effects. When focusing on average causal effects like the average treatment effects (ATE), it is sufficient to test mean (rather than full) conditional independence of the outcome and the suspected instrument.

There is an extensive literature on conditional independence tests of variables. Closely related to our testing problem, fan1996consistent, racine1997consistent and racine2006testing provide methods to test the significance of regressors using kernel methods in semi- and nonparametric regression models. Further specification tests have been suggested in bierens1982consistent, hardle1993comparing, horowitz1994testing and wooldridge1992test. All of these methods assume the regressors to be fixed (i.e. a priori chosen by the researcher), while the testing approaches suggested in this paper permit selecting important control variables in a data-driven way. More specifically, we construct tests for the conditional independence of the instrument using doubly robust (DR) methods, see Robins+94 and RoRo95. In our context, these DR approaches are based on statistical models for both the instrument and the outcome. We apply the double machine learning (DML) framework of Chetal2018, in which the models for the instrument and the outcome are learned in a data-driven way based on machine learning. This appears particularly attractive in high-dimensional settings where the number of available covariates is relatively large.

Under specific regularity conditions, testing is root-n-consistent despite the use of flexible machine learning methods. Following AtheyImbens2016, WagerAthey2018, AtheyTibshiraniWager2019, and leeetal2020, we also suggest a machine learning-based algorithm for detecting heterogeneity in the violations of the conditional independence as a function of the covariates. This permits detecting subgroups in which the violations are particularly large, in order to increase (asymptotic) testing power. Finally, we propose a test based on the average squared violation across all covariate values, which represents a global testing approach to account for covariate-dependent heterogeneity in violations. We show that under the null hypothesis, this test (similarly to DML) satisfies so-called Neyman1959-orthogonality, implying that we may account for covariates by machine learning without compromising on a desirable asymptotic behavior, given that specific regularity conditions hold. In a simulation study with 50 covariates, we find that the various tests perform decently in terms of empirical size and power even under moderate sample sizes of 1000 or 4000 observations.

As an empirical illustration, we apply our testing approach to US census data previously considered in Angrist+98 for assessing the impact of fertility, which is the treatment, on female labor supply when using the sex ratio of the first two children as instrument. The intuition for this instrumental variable (IV) strategy is that if parents tend to have a preference for mixed sex children, then having two children of the same sex, which is arguably randomly assigned by nature, increases the chances of getting a third child. Based on findings in RoWo00 and Lee07f, one might, however, challenge whether all identifying assumptions required for the IV-based identification of causal effects are satisfied. Here, we do not impose any IV assumptions a priori, but use the sibling sex ratio to test the joint satisfaction of IV validity and the selection-on-observables assumption. Our results point to a violation of the conditional independence of the instrument under our moderate set of covariates, which consists of several socio-economic characteristics like mother’s age and father’s income. Therefore, testing suggests that the treatment does not satisfy the selection-on-observables assumption, or the sex ratio is no conditionally valid instrument, or both.

This paper connects to several strands of the causal inference literature. Most closely related are studies assuming an instrument that is conditionally valid given covariates, in order to test the selection-on-observables assumption on the treatment based on the very same condition as in this paper, see deLunaJohansson2012 and BlackJooLaLondeSmithTaylor2015.111Angrist2004, BrinchMogstadWiswall2012, and Huber2013 consider related tests when instrument validity is assumed to hold unconditionally, i.e. without controlling for covariates, in order to test the unconditional independence of the treatment and potential outcomes. BertanhaImbens2015 focus on a fuzzy regression discontinuity design (RDD), where instrument validity is assumed to hold at a specific threshold of a running variable which discontinuously affects treatment assignment. These contributions have in common that they a priori assume some form of IV validity like in condition (A) to test treatment exogeneity, e.g. the selection-on-observables condition (B). Here, we highlight that (A) and (B) can be tested jointly, such that one need not impose the existence of a valid instrument prior to testing. This is conceptually distinct from the previous approaches, as it implies that under some causal structure, we can test for identification in the data by checking a condition that implies the satisfaction of both (A) and (B).

Furthermore, our approach relates to angrist2015wanna, who consider the opposite scenario of a treatment satisfying a selection-on-observables assumption (B) in order to test whether a further variable is a valid instrument (A).222In the absence of a selection-on-observables assumption on the treatment, specific instrument assumptions are only partially testable, see for instance the methods proposed by Kitagawa2008, HuMe11, MoWa2014, and Guber2018. More concisely, they consider the sharp RDD, in which the treatment is a deterministic function of a threshold in a running variable and therefore by design not associated with unobservables affecting the outcome. For instance, the admission to a college, which is the treatment, might be conditional on reaching a specific threshold in the score of an entrance exam, the running variable. Because admission is exclusively determined by passing the score’s threshold, it is unconfounded conditional on the score. RDD identification relies on comparing the outcomes of treated and non-treated subjects close to the threshold, i.e. with comparable values in the running variable. However, for subjects with scores further away from the threshold, the treatment effect is confounded if the running variable directly affects the outcome or is associated with unobservables affecting the outcome. For this reason, angrist2015wanna test whether the score is independent of the outcome given the treatment and observed covariates. If this is the case, the running variable is (conditional on the covariates) a valid instrument, not a confounder. This permits identifying treatment effects away from the threshold, as one need not control for the running variable.

Our study is also related to CaetanoCaetanoFeNielsen2021, who consider a treatment with multiple values and bunching at a specific value. For instance, schooling laws may impose a minimum number of years of eduction, such that all subjects who would otherwise have acquired a lower level of eduction bunch at this minimum. For this reason, also the subjects’ unobserved characteristics affecting the treatment bunch at this point, which might for instance imply a comparably low level of ability at the minimum education requirement relative to other educational levels. One may then verify the selection-on-observables assumption by testing whether a dummy variable for the bunching point, which is a function of the unobserved characteristics, is conditionally independent of the outcome given the treatment and the covariates. Therefore, the dummy variable at the bunching point of the unobservables has the same role as the supposed instrument in our context, under the condition that the outcome model as a function of the treatment and covariates is correctly specified.

Our method of testing identification addresses in some sense a statistical problem ‘in between’ classical treatment evaluation, where both the treatment and the identifying assumptions are predetermined, and causal discovery, see e.g. KalischB2014, peters2017elements, Glymouretal2019, or breunig2021testability. Causal discovery does typically not predefine the treatment and outcome, but aims at learning the causal relations between two or more variables in a data-driven way, possibly under parametric restrictions or the assumption that all relevant variables in the causal system (apart from random error terms) are observed. Here, we do not rely on such assumptions, but instead impose more causal structure to distinguish the treatment, outcome, covariates, and the supposed instrument. This structure appears realistic in many empirical contexts with information about the timing of variable measurement. For instance, a treatment taking place in an earlier period can affect and outcome measured in a later period, but not vice versa. In contrast to classical treatment evaluation, we do, however, not pre-impose specific identifying assumptions, but test them in the data.333One subfield of causal discovery related to our study is so-called Y-learning, see e.g. mani2012theoretical and SevillaMayn2021. Conditional on covariates, Y-learning implies that if two variables are (1) independent of each other when not controlling for the treatment, (2) statistically associated with each other when controlling for the treatment, and (3) both independent of the outcome when controlling for the treatment, then these two variables are valid instruments. A further implication is that the selection-on-observables assumption holds, in analogy to the satisfaction of our testable implication under a single instrument. The difference to Y-learning is that here, we impose more structure by predefining a supposed instrument that must not be causally affected by the treatment. In contrast, testing identification by Y-learning hinges on detecting two instruments in a data-driven way, rather than predefining an instrument and ruling out causality from the treatment to the instrument.

The remainder of this study is organized as follows. Section 2 discusses a set of identifying assumptions. The latter are used in Section 3 to derive a testable implication of the joint satisfaction of IV validity and selection-on-observables assumptions, implying the identifiability of treatment effects. Section 4 provides a modified testable implication when assuming that the IV validity and selection-on-observables assumptions hold with respect to the mean potential outcomes, rather than the entire potential outcome distributions. Section 5 discusses the null hypotheses to be tested. Section 6 proposes tests based on DML to control for (possibly high dimensional) covariates in a data-driven way. DML permits verifying whether the testable implication holds on average in the total sample or within subsamples defined as a function of the covariates. Section 7 proposes a test based on average squared violations, i.e. squared differences in conditional mean outcomes, which jointly tests for violations of the testable implication across all covariate values. Section 8 provides a simulation study. Section LABEL:application presents an application to the evaluation of the impact of fertility on female labor supply. Section LABEL:co concludes.

2 Assumptions

We are interested in the causal effect of a treatment on an outcome , and both variables might be discretely or continuously distributed. In our discussion of causality, we will make use of the potential outcome framework as for instance advocated in Neyman23 and Rubin74. We denote by the potential outcome when exogenously setting the treatment of a subject to some value in the support of the treatment. More generally, we will use capital and lower case letters for referring to random variables and specific values thereof, respectively. Importantly, denoting the potential outcome as a function of a subject’s treatment status alone implicitly imposes that (i) someone’s potential outcomes are not affected by the treatment status of others and (ii) there are no different versions of any treatment level across individuals. This is known as the ‘Stable Unit Treatment Value Assumption’ (SUTVA), see for instance the discussion in Rubin80 and Cox58, and is imposed throughout this paper. Furthermore, we denote by a vector of observed covariates to be used as control variables and by one or several observed instrumental variables, whose properties are yet to be defined. Finally, let , , , and denote the support of , , , and , respectively. We will subsequently discuss the assumptions which permit testing identification.

Our first assumption imposes some structure concerning which variables may causally affect other variables. It also states that any two variables which are associated with each other via causal paths (possibly conditional on other variables) are necessarily statistically dependent, which is known as causal faithfulness.

Assumption 1 (Causal structure and faithfulness).

| Only variables which are d-separated in some causal model are statistically independent. |

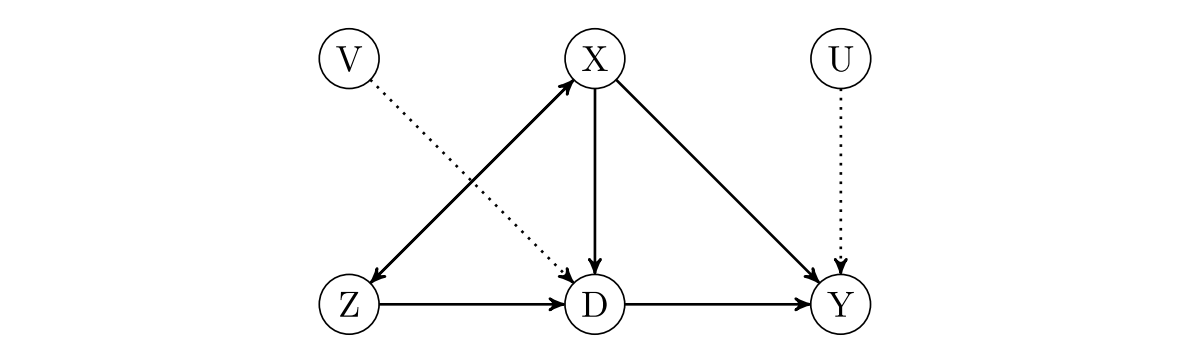

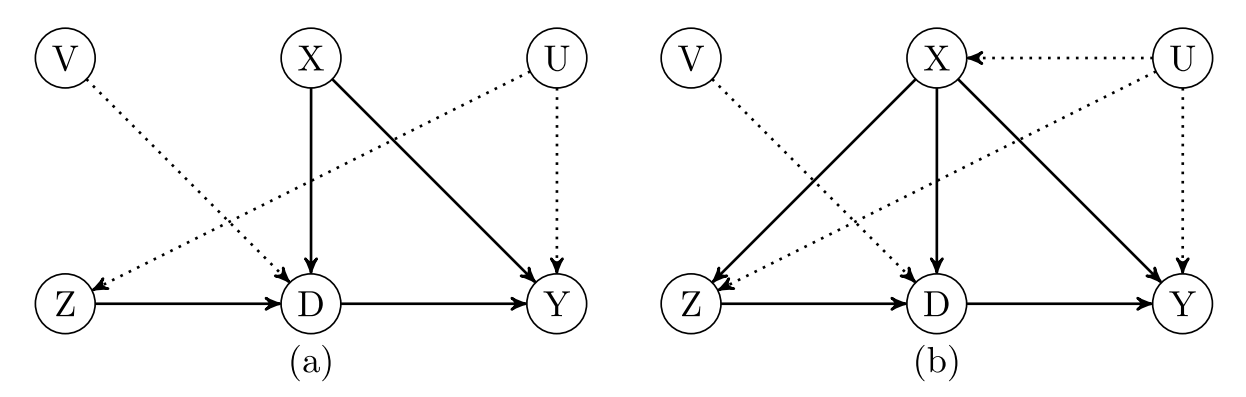

The first line of Assumption 1 rules out reverse causal effects of outcome on , , or . It also states that the treatment must not causally affect or , while both and might affect , , or each other. These conditions are satisfied in the causal framework in Figure 1, which represents the causal associations between instrument , treatment , and outcome by arrows in a directed acyclic graph (DAG), as e.g. considered in Pearl00 or Cunningham2021. In the DAG, and affect and and affect . Furthermore, might affect or vice versa, as indicated by the bidirectional causal arrow. This scenario is in line with the practice of measuring covariates and instruments prior to treatment assignment, which rules out reverse causality of and on the pre-treatment and . The DAG also includes the unobserved terms and which affect and , respectively, with the dashed arrows indicating that these effect cannot be observed.

The second line of Assumption 1 imposes causal faithfulness, meaning that only variables which are d-separated, i.e. not associated with each other via some causal paths (possibly conditional on other variables) are statistically independent (or conditionally independent). More formally, the d-separation criterion of pearl1988probabilistic implies that two (sets of) variables and are d-separated when conditioning on a (set of) control variable(s) if and only if

-

1.

the path between and contains a triple (causal chain) or (confounding) such that variable (set) is in (i.e. controlled for),

-

2.

the path between and contains a collider such that variable (set) or any variable (set) causally affected by is not in (i.e. not controlled for).

d-separation is sufficient for the (conditional) independence of two variables, which will be useful for proving Theorems 1 and 2. Causal faithfulness imposes that d-separation is also a necessary condition, such that two variables are statistically independent if and only if d-separation holds.

One scenario in which faithfulness fails is that one variable affects another one via several causal paths (or mechanisms) which exactly cancel out such that the variables are independent, see e.g. the discussion in spirtes2000causation. In the context of Figure 1, faithfulness rules for instance out that affects via multiple causal mechanisms that fully offset each other. A further example is that one variable causally affects another one, but both variables are affected by a third factor in a way that exactly offsets the association of the first two variables such that they are independent. The implications of faithfulness for our testable condition will become apparent in the discussion in Section 3.

Our second assumption requires that for any values of in the population, any possible combination of treatment and instrument values exists, which is known as common support.

Assumption 2 (Common support).

Assuming discretely distributed treatments and instruments, Assumption 2 implies that the joint probabilities of any and conditional on are larger than zero. In the case of continuously distributed treatments and/or instruments, the joint probabilities are to be replaced by joint density functions conditional on . By applying basic probability theory, , where is the conditional treatment probability given , known as treatment propensity score, and is conditional instrument probability given , i.e. the instrument propensity score. Therefore, Assumption 2 requires that both the treatment and instrument propensity scores are larger than zero, i.e. and and .444Common support in the treatment propensity score ensures that causal effects are identified conditional on any value of in the population, which is a precondition that aggregate treatment effects like the average treatment effect (ATE) given by for any , are well defined. Under a violation of common support in the treatment propensity score for some values of , one may identify causal effects only for subpopulations whose covariate values satisfy . Common support in the instrument propensity score ensures that the testable implication suggested further below can be verified at any value of in the population and for any treatment value . A violation of common support in the instrument propensity score implies that one may test the implication only among those covariate and treatment combinations satisfying . Assumption 2 is therefore strictly speaking not required for implementing our testing approach yet to be defined, if we contend ourselves with considering a subpopulation satisfying common support, which may, however, come with the potential caveat of reduced testing power.

Our third assumption requires the treatment and the instrument to be statistically dependent conditional on the covariates, where denotes statistical dependence.

Assumption 3 (Conditional dependence between the treatment and instrument).

Together with Assumption 1, which rules out effects of on , Assumption 3 either implies that causally affects , which is known as first stage effect in the IV literature, or that some (unobserved) characteristics jointly affect and given . This assumption is satisfied in Figure 1, where the instrument has an impact on the treatment.

Our fourth assumption invokes the conditional independence of the treatment and the potential outcomes given the covariates, with denoting statistical independence. This popular assumption in the treatment evaluation literature is also known as selection-on-observables, exogeneity, or unconfoundedness, see e.g. Im04 and ImWo08.

Assumption 4 (Conditional independence of the treatment).

Assumption 4 implies that conditional on covariates , there exist no unobserved confounders jointly affecting outcome and treatment .

Our fifth assumption invokes IV validity, requiring that the instrument is conditionally independent of the outcome give the covariates .

Assumption 5 (Conditional independence of the instrument).

Assumption 5 has two implications. First, does not directly affect the outcome other than through the treatment conditional on , such that potential outcome is a function of alone, rather than the instrument, too. For this reason, an IV exclusion restriction holds such that conditional on , for any instrument values and , otherwise the conditional independence would be violated. Second, there exist no unobserved confounders jointly affecting and when controlling for , which is analogous to Assumption 4, but now concerning the instrument rather than the treatment. We note that Assumption 5 is not sufficient for identifying causal effects based on the instrument, like the local average treatment effect (LATE) on the subpopulation whose treatment reacts to (or complies with) the instrument, see Imbens+94 and Angrist+96. The IV-based assessment of the LATE hinges on further assumptions, like e.g. the (conditional) monotonicity of in , which we do not consider here, because it is not required for our identification test.

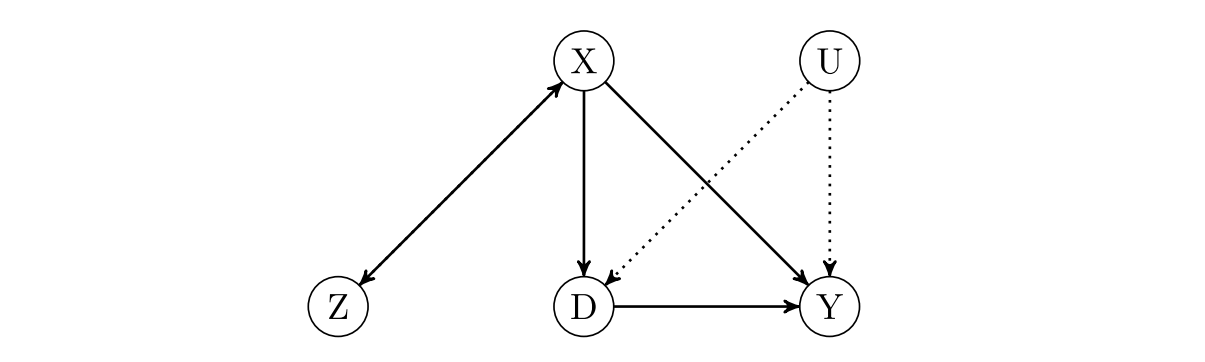

To provide an example where Assumption 5 is violated, consider the following nonparametric outcome model: , where is an unknown function and denotes unobserved variables affecting the outcome. directly affects the outcome, as considered in Figure 2. In this case, the potential outcome is not independent of conditional on . Let us now alternatively assume that the outcome model is , such that . In this case, does not directly affect and Assumption (5) is satisfied if holds such that the unobservables and the instrument are conditionally independent. This is satisfied in Figure 1, where is a conditionally valid instrument for , as it neither directly shifts the outcome nor is associated with unobservables affecting the outcome.

3 Testable implication for identification

In the subsequent discussion, we use the assumptions introduced in Section 2 to derive a testable implication for the identification of causal effects. Assuming the causal structure and faithfulness condition imposed by Assumption 1, we note that if Assumption 4 holds, then the additional satisfaction of Assumption 5 implies for some potential outcome that

| (3.1) |

That is, controlling for in addition to cannot introduce statistical dependence between and , because the treatment and the potential outcomes are independent given . This follows from the d-separation criterion of pearl1988probabilistic, which under our model assumptions rules out such a spurious dependence between and , known as collider bias (see Pearl00) or sample selection bias (see He79), when controlling for and .555Indeed, when substituting by , by , and by in the d-separation criterion established at the beginning of Section 2, we can verify that and are d-separated conditional on . This is the case because and are d-separated conditional on alone and furthermore, is not a collider and may therefore be included in the conditioning set , too. As d-separation implies conditional independence, it follows that (3.1) holds under our assumptions.

Next, we note that when setting in the conditioning set of (3.1), the potential outcome corresponds to the observed outcome if SUTVA holds, because conditional on . For this reason, (3.1) implies that

| (3.2) |

As the conditional independence (3.2) is based on observed (rather than potential) outcomes, it provides a testable implication of the joint satisfaction of Assumptions 4 and 5 for the potential outcome under the (f)actually assigned treatment . It appears important to point out the implications of causal faithfulness in this context, see Assumption 1. If it fails, then a violation of (3.2) might in particular parametric models not go together with a violation of Assumptions 4 and/or 5, respectively. For instance, deLunaJohansson2012 consider a direct effect of on (violating the exclusion restriction) and an association of with unobservables affecting which exactly offset each other in a linear model. In this case, Assumption 5 holds, while (3.2) may be violated. In more general (nonparametric) models, however, a violation of (3.2) necessarily points to a violation of Assumptions 4 and/or 5. Causal faithfulness, also referred to as stability in Pearl00, rules out parametric models for which this is not the case.

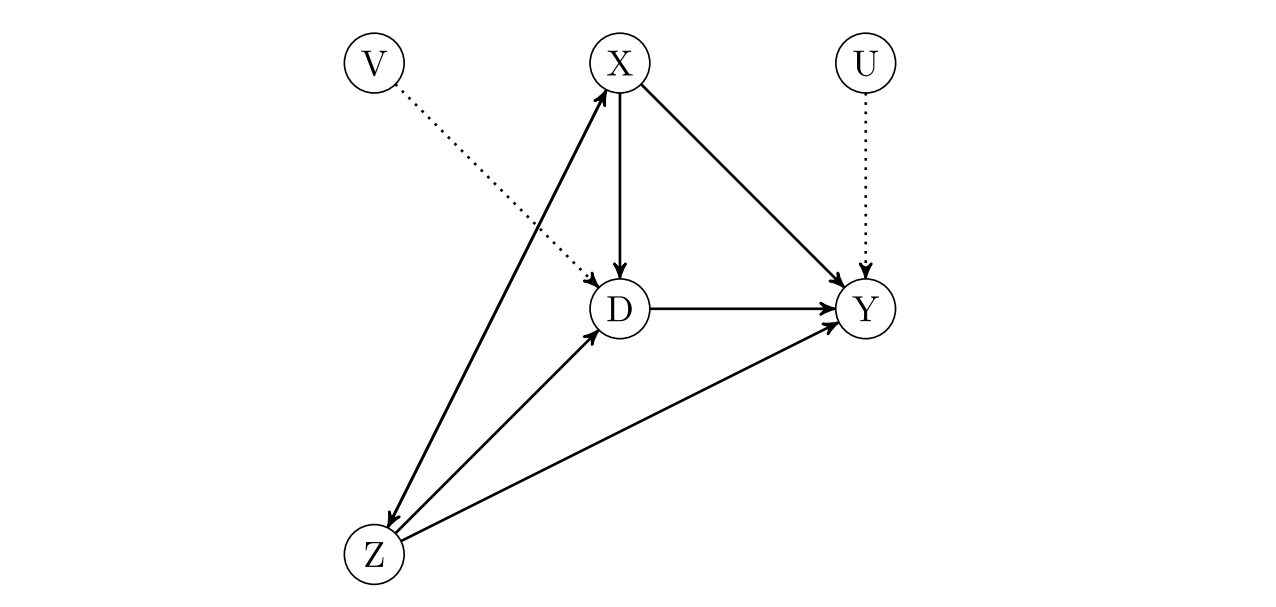

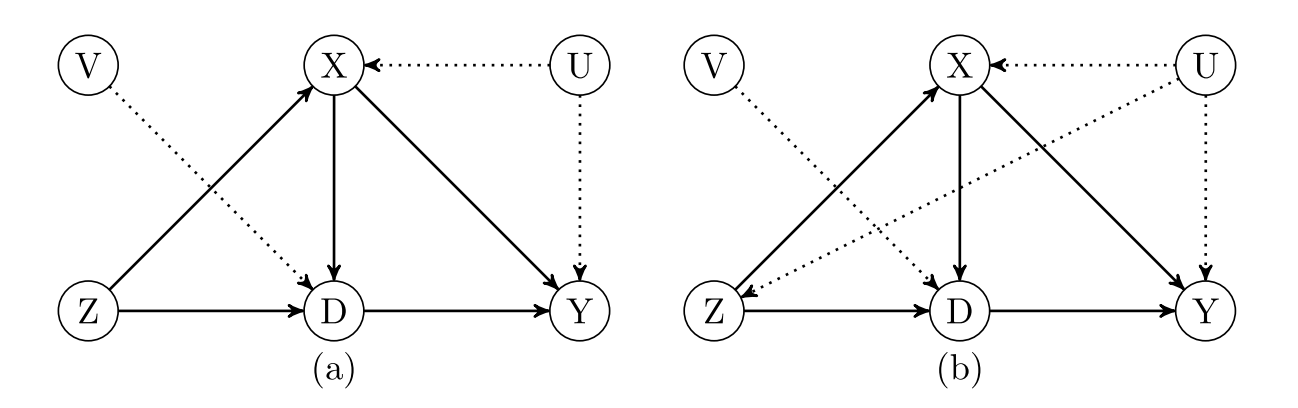

It is worth noting that if and are conditionally independent given , i.e. , condition (3.2) can hold even under a violation of Assumption 4, implying a lack of testing power. This follows from d-separation: If Assumption 5 holds such that is conditionally independent of given , then controlling for an endogenous treatment will not introduce a spurious dependence (or collider bias) between and if and are conditionally independent given . Under the causal structure postulated in Assumption 1, it holds that and imply and , even if . Figure 3 provides a causal model satisfying this framework. is not associated with given , as neither affects , nor affects and no variables jointly affect and conditional on . Therefore, (3.2) holds even if (4) is violated, due to confounding by which jointly affects and .

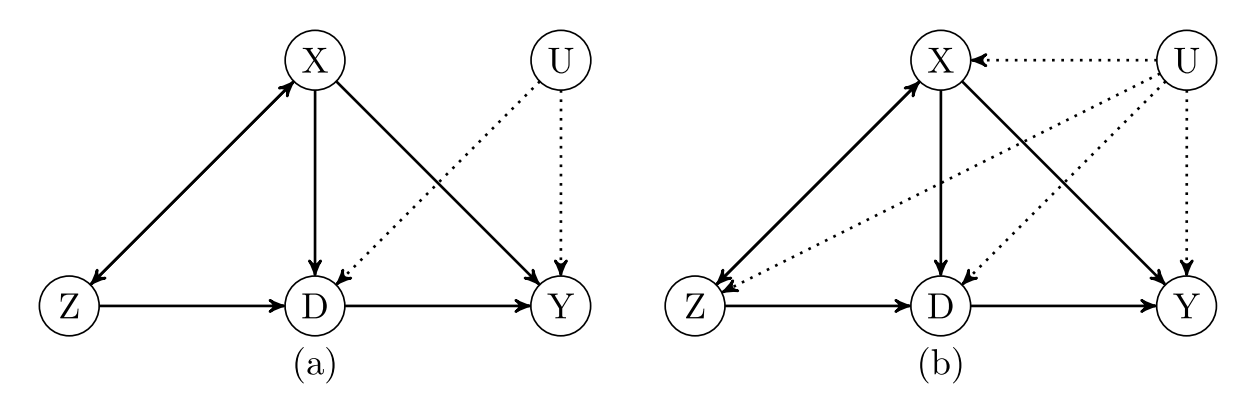

For this reason, we additionally impose Assumption 3, i.e. conditional dependence between and , to guarantee that (3.2) can be considered as a condition for the joint satisfaction of Assumptions 4 and 5. Under both Assumptions 1 and 3, (3.2) no longer holds if Assumption 4 is violated. Figure 4 provides several examples for such a causal framework, in which affects such that Assumption 3 holds. However, the treatment-outcome association is confounded by unobservables given . For this is reason, controlling for introduces a spurious dependence between and even conditional on . This in turn introduces statistical dependence (or collider bias) between and , because affects . This issue arises in both graphs (a) and (b), implying that the causal effect of on is not identified conditional on . It is not identified conditional on both and either, as additionally controlling for does not tackle the confounding of the treatment-outcome relation due to .

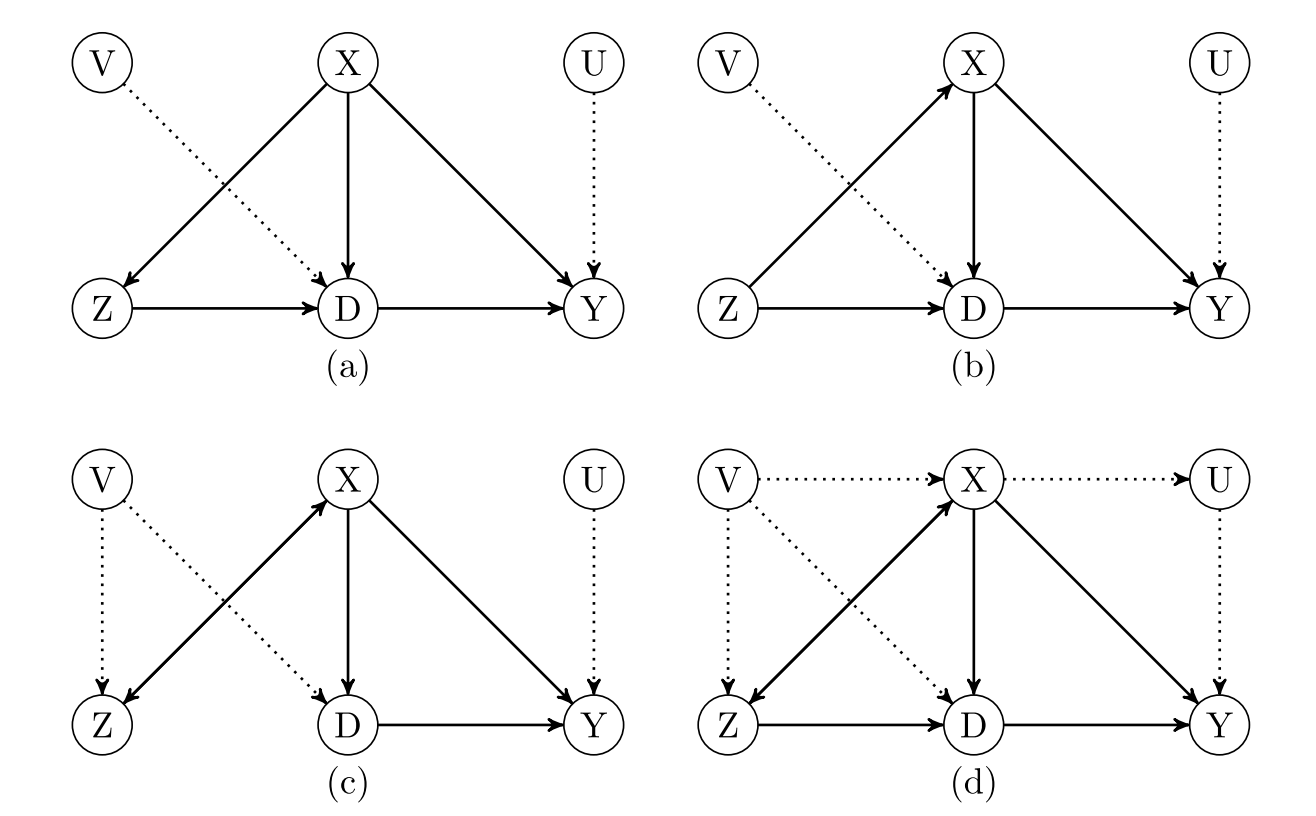

The previous discussion demonstrates that under the satisfaction of Assumptions 1, 5, and 3, a violation of Assumption 4, implying that the treatment effect is not identified conditional on , entails a violation of (3.2). Such a violation also occurs under the satisfaction of Assumptions 1, 4, and 3, but a violation of Assumption 5: entails and thus . Figure 5 provides two examples for such a causal framework, in which the unobserved characteristics that affect are not associated with . While and is confounded by in graphs (a) and (b) such that Assumption 5 is violated, controlling for permits identifying the causal effect of on such that Assumption 4 holds. In this case, identification is obtained conditional on but cannot be revealed through a satisfaction of (3.2) due to the invalidity of the instrument.

To gain further intuition about the conditional independence (3.2), Figure 6 provides two causal scenarios in which both Assumptions 4 and 5 are violated. In graphs (a) and (b), conditioning on alone introduces so-called M-bias, a form of collider bias. Because is influenced by both and , controlling for introduces a spurious association between (which affects ) and (which affects ), such that the treatment-outcome association is confounded. Nevertheless, the causal effect of is identified based on observed variables, namely when controlling for both and . In graph (a), this approach simultaneously avoids M-bias by conditioning on the instrument and confounding of the treatment-outcome relation by conditioning on the covariates. In graph (b), the same strategy additionally blocks the direct impact of on . For this reason, a violation of (3.2) does not necessarily imply non-identification, as treatment effects might be just identified when controlling for both and . However, if (3.2) is violated, we cannot distinguish non-identification from identification in a data-driven way but need to rely on untestable assumptions.

Finally, Figure 7 provides several causal graphs in which both Assumptions 4 and 5 are satisfied (in addition to Assumptions 1 and 3), such that (3.2) holds. In all cases considered, controlling for is sufficient for the conditional independence of both the treatment and the instrument on the one hand and the potential outcomes on the other hand. In contrast to Figure 6, conditioning on the covariates does not introduce M-bias. Therefore, is conditionally independent of given both and and (3.2) provides a testable condition for the identification of the treatment effect of on given .

In Theorem 1, we formalize the findings of our previous discussion. More concisely, we show that conditional on Assumptions 1 and 3, is a necessary and sufficient condition for the joint satisfaction of and . The latter two conditions correspond to Assumptions 4 and 5 when considering potential outcomes that match the factual treatment assignment . This implies that in practice, we may test Assumptions 4 and 5 only for factual outcomes, e.g. for the potential outcomes of subjects with and of subjects with . However, one cannot construct tests based on counterfactual outcomes, e.g. for potential outcomes of subjects with and of subjects with . For this reason, our approach tests a necessary, but not a sufficient condition. If violations of Assumptions 4 and 5 solely concern counterfactual outcomes, i.e. of treated individuals and of non-treated individuals, testing cannot detect such violations. From a practical perspective, however, it seems unlikely that violations exclusively occur among counterfactual, but not among factual outcomes, because this would imply very specific modeling constraints.

Theorem 1.

The proof of the theorem is provided in Appendix LABEL:proofth1 and is related to, but yet different from that in deLunaJohansson2012, who consider the same testable implication under a different conceptual framework: They a priori impose Assumption 5 to test Assumption 4, i.e. selection-on-observables. That is, the same testable implication as considered in Theorem 1 also arises when imposing conditional IV validity and testing the selection-on-observables assumption w.r.t. treatment, see also BlackJooLaLondeSmithTaylor2015. Taking in some sense the opposite approach, one may alternatively assume a treatment that is unconfounded to test IV validity, which entails the same testable implication. angrist2015wanna consider this approach in an RDD context to test whether the running variable is a conditionally valid instrument. The latter implies the identification of causal effects away from the running variable’s threshold determining treatment assignment, at which the treatment is locally unconfounded by design.

In contrast to these contributions, Theorem 1 demonstrates that we can jointly test Assumptions 4 and 5, i.e. the conditional independence of both the treatment and the instrument, given that the two variables are conditionally dependent. We need not be convinced a priori that conditional instrument validity holds in order to test the selection-on-observables assumption, or vice versa. By jointly testing both assumptions, we conceptually move away from pre-imposing one specific set of identifying assumptions and towards verifying identification in the data. This idea is related to CaetanoCaetanoFeNielsen2021, who test whether conditional on the treatment and the covariates, the outcome is statistically independent of a function of unobservables. The latter function corresponds to a dummy variable for a specific treatment value under the conditions that bunching (i.e. a mass point) in the treatment occurs at that value and that the outcome model is correctly specified. In other words, the function of the unobservables is the instrument in Theorem 1. Also in CaetanoCaetanoFeNielsen2021, it is a priori not clear whether the unobservables are valid instruments or whether the selection-on-observables assumption holds, but both assumptions are tested jointly based on the dummy variable at the bunching point.

Our approach of jointly testing several assumptions is also related to classical specification tests, like the Hausman78 test for comparing the results from an IV regression with those of a method relying on selection-on-observables, e.g. OLS. Also in this case, one may assume conditional IV validity to test the selection-on-observables assumption or vice versa. And as in our setting, both assumptions could be tested jointly. However, as the Hausman test relies on comparing the causal effects obtained under IV and selection-on-observables methods, one disadvantage is that its behavior is generally affected by misspecification of the models underlying effect estimating. Even when basing testing on nonparametric models that allow for heterogeneous effects across subpopulations as in DoHsLi2014, IV-based identification has to rely on further identifying assumptions like monotonicity of in . Because such functional form restrictions compromise on the generality of the model and the robustness of the tests, directly testing the conditional independence in Theorem 1 as in our approach seems preferable.

4 Conditional mean independence

The conditional independence assumptions 4 and 5 refer to the entire distributions of potential outcomes and permit the evaluation of distributional effects such as the quantile treatment effect (QTE), see for instance fir07. For assessing the average treatment effect (ATE), we may consider somewhat weaker conditional independence assumptions w.r.t. the means of potential outcomes. More formally, we may replace Assumption 4 by the following condition.

Assumption 6 (Conditional mean independence of the treatment).

Assumption 6 is weaker than Assumption 4 as it only imposes the conditional mean independence of and given , but not that of other moments. Analogously, we can weaken Assumption 5 to conditional mean independence of the instrument, see Assumption 7.

Assumption 7 (Conditional mean independence of the instrument).

When considering Assumptions 6 and 7 rather than 4 and 5, Assumption 3 on the conditional dependence of and needs to be replaced, too, by conditional mean dependence.

Assumption 8 (Conditional mean dependence between the treatment and instrument).

Assumption 8 imposes a nonzero first-stage effect of in a regression of on a constant, , and . It is stronger than the previously imposed Assumption 3, because it requires that the conditional dependence of and necessarily affects the mean of these variables. Any conditional dependence in other moments (like the variance) is irrelevant for this assumption.

Theorem 2 states that conditional on Assumptions 1 and 8, the conditional mean independence of and given and implies that and is implied by and , where is the potential outcome associated with the factual treatment . Therefore, Assumptions 6 and 7 are testable for potential outcomes that match the factual treatment assignment. The proof is provided in Appendix LABEL:proofth2.

5 Testable hypotheses

This section presents the hypotheses for testing the conditional mean independence in (2), which implies the identification of average effects. We assume that the supposed instrument to be a scalar, while is a vector of observed covariates. To ease notation, we henceforth denote the conditional mean outcome as . Considering a discretely distributed instrument , the conditional mean independence (2) is equivalent to the following null hypothesis :

| (5.1) |

Under the null hypothesis, the mean conditional outcome is constant across given any value of and . For a binary instrument, (5.1) for instance corresponds to . For a continuous instrument , (2) implies the following null hypothesis:

| (5.2) |

That is, the first derivative of the conditional mean outcome w.r.t. the instrument must be zero given any value of , , and .

Under a linear regression model for the outcome with homogeneous effects, we can test the null hypotheses (5.1) or (5.2) based on regressing on a constant, , , and and verifying whether the coefficient on is statistically significantly different from zero. However, when assuming a more flexible nonparametric model, the conditional statistical association of and is allowed to be heterogeneous across different values of , , and . In theory, one then might want to verify the respective null hypothesis at all values of the instrument, the treatment, and the covariates, to check for any possible violation. However, if some or all of these variables are continuously distributed, this implies an infinite number of hypotheses to be tested. Even under (mostly) discretely distributed variables, statistical power in finite samples quickly decreases in the conditioning set as a function of the dimension and support of . Therefore, a test statistic must necessarily involve an aggregate measure over its domain (or support), see e.g. racine1997consistent and racine2006testing who provide a nonparametric significance test based on an aggregate -norm that is related to our approach in Section 7.

Another way to circumvent such issues of limited finite sample power and multiple hypothesis testing is to verify whether the null hypothesis holds on average. For a binary instrument as considered in our application in Section LABEL:application, this amounts to testing the following condition:

| (5.3) |

We henceforth denote this average difference in conditional means by . may be estimated by treatment evaluation methods for assessing the ATE, such as propensity score matching, see rosenbaum1983 and RosenbaumRubin1985, inverse probability weighting (IPW), see Horvitz52 and Hirano+00, or doubly robust (DR) methods, see Robins+94 and RoRo95.

6 Testing based on doubly robust estimation

We henceforth suggest a testing approach based on doubly robust (DR) estimation, and to this end consider vectors such that

| (6.1) | ||||

| (6.2) |

with denoting the conditional instrument probability or instrument propensity score and as well as denoting deviations from the conditional mean of and , respectively. The DR approach exploits both propensity scores and conditional means to estimate the following expression for (which is equivalent to ):

| (6.3) |

with

| (6.4) |

is the efficient (and Neyman-orthogonal) score function, into which and enter as first-step or nuisance parameters. The sample analog of (6.3) consistently estimates if either the model for or for is correctly specified, which is known as DR property.

In particular when the set of covariates is large, one might estimate and by machine learning (ML) algorithms, in order to control for important confounders in a data-driven way (rather than using an ad-hoc rule which may introduce pre-testing issues). This double machine learning (DML) approach is typically combined with cross-fitting, which consists of estimating the the nuisance parameter models and the score function in non-overlapping subsets of the data, with the roles of the subsets for the estimation steps being sequentially swapped. As no observation enters both estimation steps at the same time, cross-fitting avoids correlations between the estimation of the models of and on the one hand and of the score function on the other hand and thus, overfitting bias. Finally, taking the sample average of the estimated score function yields an estimate of , in analogy to the population average in (6.3). Under specific regularity conditions, e.g. the convergence rate of ML-based estimators of and being faster than , DML is root--consistent, see the discussion in Chetal2018.

However, verifying the condition (5.3) rather than (5.1) has its caveats. By averaging over values of and (and , if it is non-binary) when testing the null hypothesis, there is a risk of averaging out violations of the conditional mean independence (2) such that they cannot be detected. By aiming at increasing finite sample power through averaging, we sacrifice asymptotic power as we do not test the hypotheses separately for distinct values of our conditioning set. To more optimally trade off asymptotic and finite sample power, we outline a further testing approach, which borrows from the literature on estimating conditional average treatment effects (CATE) and investigating effect heterogeneity across observed characteristics based on ML, see e.g. WagerAthey2018. Denoting the conditional mean difference by , we use the score function for assessing whether is heterogeneous across values of and thus necessarily non-zero for some values of the conditioning set.

A practical issue is that we would like to focus on those variables in the set which importantly predict the effect heterogeneity of and thus, drive the statistical power of our test. This suggests the use of ML for determining the crucial predictors of the estimate of . However, if the ML-based detection of important predictors of and hypothesis testing e.g. of (5.1) based on those predictors proceeds in the very same data, this may entail overfitting bias. This can entail spurious rejections of the null hypothesis due to a correlation of the estimation steps of predictor selection and testing, in analogy to the discussion in AtheyImbens2016. For this reason, we apply a sample splitting approach which avoids such correlations, see e.g. leeetal2020, by randomly partitioning our sample into two non-overlapping subsamples. In the first subsample, we apply the previously discussed DML procedure to estimate the efficient score function, henceforth denoted by . Still in the first subsample, is predicted as a function of the predictors using ML, for instance based on a so-called decision tree, see MorganSonquist1963 and Breimanetal1984. A decision tree consists of recursively splitting the covariate space into subsets (or leaves), such that predictive power w.r.t. is maximized. In the second subsample, we first estimate based on DML and then conduct the hypotheses tests conditional on the covariates that have been found to importantly predict the score in the first subsample.

More formally, let denote the total sample size (i.e. the sum of observations in the first and second subsample) and be the index of observations in the sample, i.e. . Furthermore, denote by a specific leaf or subset and by the total number of leaves defined by the regression tree (or any other machine learning algorithm) in the first subsample, such that . The average of within the respective leaf is denoted by

Hypothesis testing amounts to verifying whether the averages in the various leaves are statistically significantly different from zero. A leaf-specific null hypotheses is defined as follows:

| (6.5) |

Under specific regularity conditions, the estimated parameters are root-n-consistent and asymptotically normally distributed with a variance which is not affected by the fact that is a ML-based estimate of the true (but unknown) score function . As discussed in SemenovaChernozhukov2020, such a favorable behavior can be attained if the ML-based estimators of the nuisance parameters converge to the respective true models with a rate faster than and if the number of leaves is small relative to the sample size . In this case, we can directly consider the t-statistics for testing the null hypothesis in specific leaves. To account for multiple hypothesis testing issues due to running the test in several leaves, we may apply a statistical correction which controls for the expected proportion of spurious rejections among the rejected hypotheses, the so-called false discovery rate, as e.g. suggested BenjaminiHochberg1995, or the standard Bonferroni correction.666Alternatively, we can run an F-test for the joint satisfaction of the null hypothesis (6.5) across all leaves if we assume a linear form of the regression function .

One drawback of such corrections for multiple testing is that they can drastically reduce testing power if the number of leaves is non-negligible. To mitigate this issue, we base testing on uniformly valid confidence intervals for all target parameters , obtained by the multiplier bootstrap. The target parameter equals zero if and only if , given that . To construct uniformly valid confidence intervals, we consider the -dimensional score function with

| (6.6) |

for all with .

To derive the large sample behavior of this approach, we introduce further notation. Let be sequences of positive constants approaching . Furthermore, let and be fixed strictly positive constants with . In the following, we rely on cross-fitted DML and split the observations in the second subsample (used for testing) into folds , , of size as described in Definition 3.2 in doubleML. For simplicity, assume that is an integer. For each , we obtain

which is an ML-based estimate of . We then estimate the target parameter by , which solves

where is the empirical expectation over the kth fold of the data. We now impose a set of regularity conditions required for the construction of uniform confidence intervals and the asymptotic normality of our testing approach, which is stated in Theorem 3.

Assumption 9 (Uniform confidence intervals).

The following assumptions need to hold for all , and :

-

i)

It holds , for all and .

-

ii)

It holds, for all .

-

iii)

Given a random subset of of size , the nuisance parameter estimator obeys the following conditions: With -probability not less than , , , and .

Theorem 3.

Conditional on Assumptions 9, under , it holds that

| (6.7) |

uniformly over , where with diagonal elements , . Moreover, the result continues to hold if is replaced by

The proof of Theorem 3 is provided in Appendix LABEL:proofDR and we note that its result also holds under the alternative hypothesis if the variance of the score is non-degenerate. Theorem 3 can be used to construct confidence regions for any scalar parameter for some vector . Using for instance the multiplier bootstrap, we can also construct a confidence interval for to simultaneously test the hypotheses (6.5) for all . To this end, we define the process

where are standard normal random variables, which are independent of each other and of the data . , , are the diagonal elements of . The critical value obtained through the multiplier bootstrap corresponds to the ()-quantile of the conditional distribution of given the data . The null hypothesis is rejected if

It is worth noting that one can also construct hypothesis tests based on the -norm, , rather than the infinity norm of . In this case, we simultaneously reject (6.5) if

| (6.8) |

with being the ()-quantile of the conditional distribution of given the data . This can lead to more efficient confidence intervals with lower volume compared to standard multiple testing approaches and hence to tests with higher power, see e.g. https://doi.org/10.48550/arxiv.2105.09028 and 10.1093/biomet/asac030.

Finally, we note that since Theorem 3 also holds for any , we can reverse the role of the null and alternative hypotheses to construct hypotheses tests of the form

| (6.9) |

for a predefined threshold . In such a framework as e.g. advocated by bilinski2018nothing, the null hypothesis postulates a non-negligible violation of the testable implication, while the alternative hypothesis states that the violation is close to zero, i.e. smaller than the absolute value of . For this reason, a statistically significant test statistic suggests that violations exceeding the threshold can be ruled out in order to justify ATE estimation based on the selection-on-observables assumption.

7 Testing based on squared differences

In this section, we suggest a further testing approach based on squared differences in conditional mean outcomes. More concisely, we aim at testing for violations of hypothesis (5.1) globally, i.e. across all values of and , by verifying the following null hypothesis :

| (7.1) |

In contrast to equation (6.3), expression (7.1) uses an aggregate -type measure to test violations across values of and , which is a common approach in specification tests for nonparametric regression, see e.g. racine1997consistent, racine2006testing, hong1995consistent and wooldridge1992test. Here, we consider machine learning for estimating the regression function , to allow the covariate vector to be high-dimensional. To this end, we test (7.1) based on a moment condition which uses the following Neyman-orthogonal score function:

| (7.2) |

where are the data, are the true nuisance parameters, and is an independent mean-zero random variable, which satisfies for and has a variance of . In contrast to the DR approach discussed in Section 6, testing exclusively relies on the conditional mean outcome as nuisance parameter, while propensity score estimation is not required. The additional random variable is introduced to avoid a degenerate distribution of our estimator under , which is a common problem in specification tests, see e.g. hong1995consistent and wooldridge1992test. The variance acts like a tuning parameter and should be chosen as a function of the sample size . A relatively high variance should ensure that our test based on comes close to the nominal level in small samples. On the negative side, a high variance could importantly reduce testing power by whitewashing violations of the null hypothesis.

To estimate the target parameter , we rely on cross-fitting and split the data into subsamples of size . The cross-fitted estimator is given by

The following assumption imposes several regularity conditions required for the asymptotic normality of our test under null hypothesis, as postulated in Theorem 4.

Assumption 10 (Asymptotic Normality).

The following assumption needs to hold for all , and : Given a random subset of of size , the nuisance parameter estimator obeys , , and with -probability not less than .

Theorem 4.

Conditional on Assumptions 10, under , it holds

| (7.3) |

uniformly over , where . Moreover, the result continues to hold if is replaced by

Consequently, a test that rejects the null hypothesis if has asymptotic level .

It is important to point out that Theorem 4 only holds under . This is because Neyman orthogonality is only satisfied under , as shown in the proof of Theorem 4 in Appendix LABEL:proofth3. To provide theoretical power results under , one could orthogonalize the score (7.1) using the methodology introduced in chernozhukov2015post and doubleML. This is an open question for future research.

8 Simulation study

This section provides a simulation study to investigate the finite sample behavior of our testing approaches introduced in Section 6 and Section 7 based on the following data generating process:

with , , , , being independent of each other. Outcome is a linear function of (whose treatment effect is one), covariates (for ), the unobservables (for ) and , and the supposed instrument if the coefficient . The binary treatment is a function of , , and the unobservables and . While the supposed instrument is binary, the unobserved terms are normally distributed random variables that are independent of each other, of , and of with and . is a vector of covariates which follow a normal distribution with a zero mean and a covariance matrix that is obtained by setting the covariance of the th and th covariate in to . The coefficient vector gauges the effects of the covariates on and , respectively, and thus, the magnitude of confounding due to observables. The th element of the coefficient vector is set to for , implying a linear decay of covariate importance in terms of confounding.

We analyze the performance of our testing approach in simulations under two sample sizes of and when setting the number of covariates to . We estimate based on DML with cross-fitting using the default options of the ‘treatDML’ command in the ‘causalweight’ package by BodoryHuber2018 for the statistical software R. The command uses lasso regression, see Tibshirani96, as ML method for estimating the nuisance parameters, i.e. linear and logit specifications of the outcome and treatment equations (and more generally makes use of the ‘SuperLearner’ package by vanderLaanetal2007 for selecting ML algorithms). Observations whose instrument propensity scores are close to zero, namely smaller than a threshold of (or 1%), are dropped from the estimation in order to avoid an explosion of the propensity score-based weights, which might heavily increase the variance of estimating . We also analyze the test performance when using the score based on the squared difference in equation (7.2) to estimate in (7.1). In this case, we choose where the variance term decreases in the sample size, by setting in (7.2).

| Test based on | Test based on | |||||||

| sample size | est | std | mean se | rej. rate | est | std | mean se | rej. rate |

| Assumptions 6 and 7 hold (, ) | ||||||||

| 1000 | -0.0030 | 0.0069 | 0.0066 | 0.151 | 0.0034 | 0.0152 | 0.0158 | 0.097 |

| 4000 | 0.0016 | 0.0034 | 0.0033 | 0.135 | 0.0009 | 0.0077 | 0.0079 | 0.091 |

| Ass. 6 violated, Ass. 7 holds (, ) | ||||||||

| 1000 | -0.0695 | 0.0367 | 0.0328 | 0.657 | 0.0721 | 0.0192 | 0.0162 | 0.992 |

| 4000 | -0.0613 | 0.0170 | 0.0166 | 0.979 | 0.0232 | 0.0040 | 0.0020 | 1.000 |

| Ass. 6 holds, Ass. 7 violated (, ) | ||||||||

| 1000 | 0.0970 | 0.0069 | 0.0066 | 1.000 | 0.0126 | 0.0152 | 0.0158 | 0.186 |

| 4000 | 0.0984 | 0.0034 | 0.0033 | 1.000 | 0.0101 | 0.0020 | 0.0020 | 1.000 |

Notes: columns ‘est’, ‘std’, and ‘mean se’ provide the average estimate of and , respectively, its standard deviation, and the average of the estimated standard error across all samples. ‘rej. rate’ gives the empirical rejection rate when setting the level of statistical significance to 0.1 (or 10%).

Table 1 reports the simulation results. The top panel focusses on the case that , such that both Assumptions 6 and 7 are satisfied. Already under the smaller sample size of , the average estimate of (‘est’) across all simulations is close to zero, and quickly approaches this true value as the sample size increases. Accordingly, the empirical rejection rate amounts to 0.151 or 15.1% under the smaller sample size, which is only somewhat higher than the nominal rate of 10% when setting the level of statistical significance to . Under the larger sample size of , the rejection rate corresponds to 13.5% and, thus, appears to approach the nominal level. Furthermore, the average standard error across all simulations (‘mean se’) is generally close to the actual standard deviation (‘std’) of DML. We also see a root-n consistent behavior in the sense that the standard deviation of the estimator is cut by half when the sample size is quadrupled, while the bias is close to zero.

The intermediate panel presents the results when Assumption 6 does not hold (, ), such that the treatment is not conditionally mean independent. The DML estimates are substantially different from zero, amounting to and for and , respectively. Furthermore, the test’s statistical power to detect the violation quickly increases in the sample size, with a rejection rate amounting to 65.7% under the lower and 97.9% under the higher sample size. Similar conclusions apply to the violation of Assumption 7 (, ), such that the instrument is not conditionally mean independent. The lower panel of Table 1 shows that the rejection rates correspond to 100% for both sample sizes, and . Summing up, we find the empirical size and power of our test based on to be very decent in these simulation scenarios.

The empirical size of our test based on the squared difference is generally close to the nominal level of 10% under the null hypothesis, as indicated in the top panel of Table 1. Also the power is generally quite decent. Under a violation of Assumption 6 (, ), the rejection rate is close to 100% under either sample size, see the intermediate panel. Under a violation of Assumption 7 (, ), the power of the test based on is quite low for but increases fast in the sample size, with a rejection rate of 100% for , see the lower panel. In contrast to the estimation of , we do not observe a root- consistent behavior of the test based on in the intermediate and lower panel of Table 1, which is not surprising as orthogonality only holds under the null hypothesis, see Theorem 4.

In a next step, we consider a simulation setting with effect heterogeneity:

with , , , , being independent of each other and and denoting the first and second covariates in , respectively. For and , Assumptions 6 and 7, respectively, are violated, but in contrast to our previous simulation design, the violations are now heterogeneous in and . We also note that the violations cancel out when averaging over and , because the covariates are normally distributed and centered around zero.

| Test based on | Test based on | |||||||

| sample size | est | std | mean se | rej. rate | est | std | mean se | rej. rate |

| Assumptions 6 violated, 7 holds (, ) | ||||||||

| 1000 | 0.0015 | 0.0656 | 0.0584 | 0.139 | 0.1738 | 0.0369 | 0.0178 | 1.000 |

| 4000 | 0.0181 | 0.0320 | 0.0300 | 0.185 | 0.0582 | 0.0122 | 0.0080 | 1.000 |

| Ass. 6 holds, Ass. 7 violated (, ) | ||||||||

| 1000 | -0.0033 | 0.0089 | 0.0086 | 0.143 | 0.0336 | 0.0155 | 0.0159 | 0.678 |

| 4000 | -0.0017 | 0.0044 | 0.0043 | 0.120 | 0.0309 | 0.0077 | 0.0079 | 0.995 |

| Ass. 6 and Ass. 7 violated (, ) | ||||||||

| 1000 | 0.0013 | 0.0657 | 0.0586 | 0.139 | 0.2035 | 0.0519 | 0.0187 | 1.000 |

| 4000 | 0.0181 | 0.0321 | 0.0300 | 0.188 | 0.0864 | 0.0212 | 0.0082 | 1.000 |

Notes: columns ‘est’, ‘std’, and ‘mean se’ provide the average estimate of and , respectively, its standard deviation, and the average of the estimated standard error across all samples. ‘rej. rate’ gives the empirical rejection rate when setting the level of statistical significance to 0.1 (or 10%).

Table 2 provides the results for testing based on and under a violation of Assumption 6 (upper panel), Assumption 7 (intermediate panel), and both assumptions (lower panel). The DR estimator of has a low power in all settings and under either sample size, due to averaging out violations across values of . In contrast, the estimator based on the squared difference has a very high power in all settings investigated.

Finally, we investigate empirical size and testing power under effect heterogeneity when estimating violations based on DR in subsets of the data defined as a function of variables in that importantly predict such violations, as discussed in Section 6. To this end, we randomly split our data into two halves and use the first subsample to estimate the DR score functions based on cross-fitting and the random forest as implemented in the ‘grf’ package by TibshiraniAtheyWager2020grf for nuisance parameter estimation. We then apply yet another random forest for determining the importance of the variables in for predicting the estimated scores based on the mean squared error-criterion, using the ‘randomForest’ package by LiawWiener2002. According to variable importance, we pick those three variables which explain most of the heterogeneity in violations. In the second subsample, we split the data at the median of these variables, such that we obtain subsets in which we estimate the violation based on the DR score function (6). Finally, we control for multiple testing using the Bonferroni correction or the multiplier bootstrap based on the and norms.

| Multiple testing based on | |||

| sample size | Bonf. | ||

| Ass. 6 and Ass. 7 hold (, ) | |||

| 4000 | 0.164 | 0.173 | 0.247 |

| 12000 | 0.154 | 0.158 | 0.245 |

| Ass. 6 and Ass. 7 violated (, ) | |||

| 4000 | 0.302 | 0.308 | 0.408 |

| 12000 | 0.824 | 0.829 | 0.869 |

| Ass. 6 violated and Ass. 7 holds (, ) | |||

| 4000 | 0.365 | 0.377 | 0.458 |

| 12000 | 0.867 | 0.874 | 0.915 |

| Ass. 6 holds and Ass. 7 violated (, ) | |||

| 4000 | 1.000 | 1.000 | 1.000 |

| 12000 | 1.000 | 1.000 | 1.000 |

Notes: column ‘Bonf.’ corresponds to rejection rate using Bonferroni correction for multiple testing. The columns ‘’ and ‘’ correspond to rejection rate using the multiplier bootstrap procedure described in (6.8) based on the norms and , respectively. The level of statistical significance is 0.1 (or 10%).