Split Conformal Prediction for Dependent Data

Abstract

Split conformal prediction is a popular tool to obtain predictive intervals from general statistical algorithms, with few assumptions beyond data exchangeability. We show that coverage guarantees from split CP can be extended to dependent processes, such as the class of stationary -mixing processes, by adding a small coverage penalty. In particular, we show that the empirical coverage bounds for some -mixing processes match the order of the bounds under exchangeability. The framework introduced also extends to non-stationary processes and to other CP methods, and experiments corroborate our split CP’s coverage guarantees under dependent data.

1 Introduction

Modern machine-learning methods often achieve significant predictive performance. However, oftentimes that is not enough: one needs a measure of uncertainty associated to the prediction. Conformal prediction (CP), introduced by Vovk, Gammerman and Shafer [36, 33], is a set of techniques for quantifying uncertainty in the predictions of any model, under very general assumptions on the data-generating distribution. CP has been applied in a variety of settings, ranging from regression [26, 32] to classification [9], and has generated much recent interest [33, 1].

Most works on CP crucially rely on the assumption of data exchangeability: the data-generating distribution is invariant under permutations of sample points. This is enough to cover the important setting of independent and identically distributed (iid) data. Deviations from exchangeability, however, have received significantly less attention, and only recently. Examples include methods for covariate shift [34] and tools for more general, but gradual shifts in the data distribution [4].

This paper considers CP guarantees for a broad class of dependent data distributions. In the simplest such setting, one has a time series consisting of stationary, but temporally dependent, points; in this case, the order of sample points matters. This is the situation, for instance, for many climate and financial data. Here, CP is appealing as it applies even to complex models, such as neural networks, that are sometimes employed in these applications [15, 31].

Several CP methods have been developed specifically for such dependent setting. They include the block-based construction of Chernozhukov et al. [11]; methods based on ensembling regressors over bootstrapped samples by Xu and Xie [37] and Jensen et al. [22]; and the general online adaptive method of Gibbs and Candès [19].

The main message of this paper, however, is that on many occasions there is no need to introduce specific CP methods for dependent data. Split conformal prediction [36, 26] — perhaps the most popular methodology for CP with iid data — is shown here to work well over a general class of dependent stochastic processes called absolutely regular or -mixing [7]. Split CP, along with the guarantees we provide, are very appealing in this setting:

-

•

It is exactly the same method that is used for iid data, with nearly the same guarantees.

- •

- •

-

•

Our split CP guarantees also work in the conditional setting proposed in [17], where one wants good performance conditioned on the covariates belonging to a given set.

- •

See §1.3.3 for a more detailed comparison with previous work.

1.1 Split conformal prediction

To explain our results, we briefly describe split CP in a regression setting. We follow Lei et al. [26], with modifications described in Remark 1.1.

Consider a regression setting where the data is a random sample consisting of covariate/response pairs . Split CP proceeds as follows:

-

1.

Divide the data indices in three parts: a training set , a calibration set , and a test set .

-

2.

Use to train a conformity score function . Note could be the residual function of an arbitrary model trained on ; a normalized version thereof; or any other function of the user’s choosing.

-

3.

Compute the empirical -quantile of over .

-

4.

For each , define a confidence set for :

The standard theory of conformal prediction over exchangeable data [36, 33, 1, 26] guarantees that the sets have good marginal coverage over the test set; that is, for any ,

| (1) |

Additionally, for iid data and , Lei et al. [26] prove empirical coverage over the test set; that is,

| (2) |

for some positive .

Remark 1.1.

Our presentation above differs from [26] and other references such as [1] in two points. Because of the dependent setting to be considered later, training, test and calibration sets are defined explicitly, and are allowed to have arbitrary sizes. Additionally, we use the ()-empirical quantile rather than the corrected quantile in [26, Section 2] that would give coverage at level in the iid setting (1). This is because, under dependence, there is no obvious correction to the quantile achieving the same result as for iid data.

1.2 Our contribution, and some key ideas

Roughly speaking, -mixing processes are stochastic processes in which far away points are approximately independent in a quantifiable manner (see Section 3). This is a general assumption that is satisfied by many popular stochastic processes, such as hidden Markov models, Markov chains, and ARMA and GARCH models [8, 30, 16].

Our theoretical results show that the marginal and empirical coverage properties in (1) and (2) also hold approximately for stationary -mixing stochastic processes. This approximation is better the weaker the dependence structure, but CP guarantees hold well for even fairly dependent processes. The fact that we only have approximate guarantees is shared by all other approaches to non-exchangeable data [4, 11, 37, 19], and, to a degree, it is unavoidable. Importantly, our experiments show that the effect of this approximation for split CP is relatively small. In particular, when the -mixing coefficients decrease geometrically, we show that the empirical coverage bounds for the -mixing process match the order of the iid bounds (see Remark 3.5).

The fundamental difficulty in our analysis of split CP is that -mixing processes can be far from exchangeable. Our main mathematical contribution is to develop a general methodology for analyzing CP that is based on concentration of measure and decoupling inequalities instead of exchangeability. For this reason, our methods may apply to other dependent random processes beyond the -mixing class.

To further emphasize the generality of our approach, we also consider popular extensions of split CP. For instance, we study dependent-data guarantees for the conditional version of CP, where one wants valid coverage for conditionally on . This version of CP was discussed in detail by Barber et al. [17] and gives coverage guarantees for subsets of the population. Additionally, we sketch how to obtain guarantees for non-stationary (but still -mixing) processes, and for other CP methods such as rank-one-out [26, Algorithm 4] and risk-controlling prediction sets [6].

Finally, we provide experiments and applications to back up our theoretical claims.

1.3 Related work

We give a concise overview of some of the relevant literature on CP. We will be especially brief on the general topic of conformal prediction (§1.3.1) and of different coverage guarantees (§1.3.2), while spending more time discussing papers on non-exchangeable data that are directly relevant to our results (§1.3.3).

1.3.1 General conformal prediction

The field of conformal prediction started with the seminal work of Vovk, Gammerman and Shafer [36]; see [33] for a survey of early work in the topic. Lei et al. [26] helped popularize CP in the Statistics community. Since then, there has been an explosion of work on the topic: see, e.g., [32, 9, 6, 2, 17] for significant recent examples, and the survey [1] for an introduction and additional references. We emphasize that the focus of this literature is on exchangeable data.

1.3.2 Marginal, pointwise and conditional guarantees

An important point about guarantees such as (1) is that they give marginal coverage. This means that coverage might be better than for certain “easy” values of and much worse for “hard” values. In fact, experiments in [9] confirm this possibility.

The harder goal of pointwise coverage,

for small , was discussed by Chernozhukov et al. [12, 11]. They prove that pointwise coverage can be achieved asymptotically when it is possible to learn the conditional distribution of given .

On the other hand, Barber et al. [17] show that pointwise coverage is not possible in general, even for iid data. On the positive side, they show that if is a family of subsets of of finite VC dimension, and the data is iid, then one obtains conditional guarantees

for all with not too small. One of our results is that such conditional guarantees can be extended to dependent data.

1.3.3 Non-exchangeable data

CP methodologies for non-exchangeable data have been considered since [36]. In recent years, a few different papers have appeared on this topic.

Gibbs and Candès [19] developed a general adaptive approach to conformal prediction that requires no distributional assumptions. Their method is very different in spirit from split CP: it requires the predictive sets to be updated online at each step. While [19] achieves empirical coverage under minimal assumptions, they give no guarantee of marginal coverage as in (1).

The issue of distributional shift has been considered in some detail. Tibshirani et al. [34] consider the setting where the distributions of the covariates in the training and calibration sets differ. If their likelihood ratio is known, or can be estimated well, their method achieves good guarantees. By contrast, Barber et al. [4] consider CP methods that give approximately correct marginal coverage under gradual changes in the data distribution. Their method does not seem applicable to time series, as it requires the distribution of the data to be approximately invariant under permutations between points “close” to the current test value.

We now consider methods that are specific to time series. The first work of this kind seems to be Chernozhukov et al [11], which employs a slightly convoluted block-based method reminiscent of the block bootstrap. Their results for non-exchangeable data, [11, Section 3.2], require that an “oracle score function” (a population object) be learned consistently from the data in the training phase. This is contrast to the guarantees of split CP, which are agnostic to the quality of the trained model. On the other hand, they require that the time series be strongly mixing, which is weaker than our -mixing assumption.

Xu and Xie [37] consider another approach to time series, based on ensembling regressors that are trained over bootstrapped subsamples. Like [11], their theoretical guarantees require the strong assumption that the population regression function is consistently learned from the training data [37, Assumption 2]. Also like [11], they require a weaker mixing assumption than we do. We note in passing that ensembling (which may be desired on its own) can be easily incorporated into the training phase of split CP.

Finally, Jensen et al [22] consider a time-series variant of conformalized quantile regression (see Romano et al. [32]). Like [37], the approach of Jensen et al. also involves training an ensemble of methods over bootstrapped samples. No theoretical guarantees are given in [22], but our framework can be used to obtain approximate versions of the bounds in [32].

1.4 Organization

The remainder of the paper is organized as follows. Section 2 describes a general setup for split conformal prediction. Precise non-asymptotic bounds for stationary -mixing processes are given in Section 3. Extensions beyond split CP and to non-stationary data are presented in Section 4. Experiments with real and synthetic data are discussed in Section 5. The appendix contains all mathematical proofs.

2 General setup for split conformal prediction

In this section we present a general setup for analyzing split conformal prediction. For simplicity, we consider only the setting of conformal prediction for regression via a conformity score (see [1, §1.1]).

In §2.1 we give our basic assumptions and state the goals of split conformal prediction. In §2.2.2 we give additional concentration and decoupling assumptions on the data distribution, which allow us to obtain guarantees for split CP in §2.2.3.

Throughout the paper, we use the notation

for the set of integers from to . In using this notation, is assumed to be a positive integer.

2.1 Basic assumptions

We detail the assumptions used in §1.1, starting with the data distribution.

Assumption 1 (Dependent data with stationary marginals).

The sample consists of random covariate/response pairs with stationary marginals: , where and are measurable spaces. An additional random pair , independent from the sample , will also be considered, and we assume for all .

In our second assumption, we fix the training, test and calibration data, and also a conformity score trained on data.

Assumption 2 (Training, test, and calibration data; trained conformity score).

We assume is a sum of three positive integers. We partition the indices

where corresponds to the training data, corresponds to calibration data, and corresponds to test data. Consider any function . For , we use the notation:

to denote the values of when the first pairs in the input correspond to the training data; is called a conformity score trained on the (training) data.

Intuitively, the role of will be to measure how “atypical” a data point is. Importantly, the choice of conformity score function is completely arbitrary. Some examples that have been considered in the literature include:

-

•

Regression residuals [26]: here and , where is some regression model trained on ;

-

•

Weighted regression residuals [26]: where is an estimate of the mean absolute deviation that was learned from the training data;

- •

-

•

Plug-in prediction interval error [32]: , where is any regression model trained to estimate the conditional -quantile.

2.2 Standard split conformal prediction

We now detail the split CP method and the assumptions needed to guarantee its coverage properties.

2.2.1 Definitions and goals

The split conformal prediction method chooses an empirical quantile for the score on the calibration data, which in turn defines the predictive sets.

Definition 2.1 (Empirical quantiles and predictive sets).

Given , let denote the empirical -quantile of over ; that is:

For , the predictive sets are then defined via:

Now, fix a confidence level . We wish to prove that the predictive sets above have adequate coverage over , in the following two senses:

| Marginal coverage: | (3) | |||

| Empirical coverage: | (4) |

for suitably small and .

2.2.2 Concentration and decoupling assumptions

The next assumptions will give us conditions on the data that suffice for (approximate) marginal and empirical coverage as in (3) and (4). To state the assumptions, we make the following definition.

Definition 2.2.

Given (assumed measurable), define and

The first assumption needed below is about the calibration data. Intuitively, it requires that the empirical and population cumulative distribution functions of are close over calibration data. A key point here, however, is that this closeness should hold even when the c.d.f. is computed over a point depending on test data.

Assumption 3 (Concentration over calibration data).

There exist and such that the following holds: if and , are as in Definition 2.2, then

The next two assumptions are on the test data. The first means that for essentially behaves like , i.e., a data point that is independent of training data.

Assumption 4 (Marginal decoupling of test data).

There exists such that, if and , are as in Definition 2.2, then, for ,

Finally, we require concentration of the empirical c.d.f. of the conformity score over the test data.

Assumption 5 (Concentration over test data).

There exist such that, if and , are as in Definition 2.2, then

2.2.3 Theoretical guarantees

We now combine our assumptions to obtain general coverage guarantees for split conformal prediction under dependent data. The first theorem achieves the goal of marginal coverage (3).

Theorem 2.3 (Marginal coverage over test data).

Additionally, if almost surely has a continuous distribution conditionally on the training data, then:

The second general theorem gives empirical coverage over the test data.

2.3 Split conformal prediction with conditional guarantees

The results from the previous subsection extend naturally to the conditional setting given suitably adapted assumptions.

2.3.1 Definitions and goals

Consider the problem proposed by Barber et al. [17], where one wants good coverage for conditionally on belonging to a subset . As explained in [17], it is not possible to obtain guarantees for completely general (measurable) sets . We will thus restrict to a family of subsets of . For the sake of notation, given a measurable set , let:

| (5) | |||||

| (6) | |||||

| (7) | |||||

| (8) |

We now introduce the corresponding empirical quantiles and predictive sets.

Definition 2.5 (Empirical conditional quantiles and predictive sets).

Remark 2.6.

Our definition of predictive set depends on the set , and only involves points in the calibration data with . By contrast, the definition in [17, Section 4] takes the following form in our notation:

Here, is a parameter. In all cases below, we will consider sets that occur often in the data, and it will always happen that . It follows that all coverage lower bounds we obtain also apply to the construction in [17].

Fix a confidence level and a parameter . We wish to prove that predictive sets have adequate coverage over . Here, however, we must restrict ourselves to sets that have sufficiently large measure. Thus, we require that, for each with and any :

| Marginal coverage: | (9) | |||

| Empirical coverage: | (10) |

with suitably small and and a quantile depending on the set .

2.3.2 Conditional concentration and decoupling

The assumptions below are the analogues for the conditional coverage setting to those of §2.2.2. To state them, we require the following analogue of Definition 2.2.

Definition 2.7.

Given (assumed measurable) and with , define as in Definition 2.2 and

The following assumptions are analogous to Assumptions 3, 4 and 5. Recall the notation for and introduced in (5) and (6), respectively.

Assumption 6 (Concentration over calibration data).

There exist such that for all , letting and be as in Definition 2.7,

Assumption 7 (Marginal decoupling from test data).

There exists such that, for all , letting and be as in Definition 2.7,

Assumption 8 (Concentration over test data).

There exist such that for all , letting and be as in Definition 2.7,

2.3.3 Theoretical guarantees under conditioning

We now combine our assumptions to obtain general conditional coverage guarantees for split conformal prediction under dependent data. The first theorem achieves the goal of marginal coverage (9).

Theorem 2.8 (Conditional coverage over test data).

Additionally, if almost surely has a continuous distribution conditionally on the training data, then:

The second general theorem gives empirical conditional coverage over the test data.

2.4 Application to the iid case

As an example, we sketch how the framework above applies to iid data. For the marginal coverage of Theorem 2.3 and empirical coverage of Theorem 2.4, Assumptions 3, 4 and 5 need to be checked. First, note that, in the iid case, when ,

showing that Assumption 4 holds with .

Moreover, using the fact that is an iid sample of bounded random variables, by Hoeffding’s inequality, with probability at least

Therefore, taking

| (11) |

3 Results for stationary -mixing processes

This section shows how the marginal and empirical coverage results in Section 2 extend to the class of stationary -mixing processes. This class is broad enough to cover many important applications while still allowing for the generalization of coverage results available in the iid setting. In this direction, it is useful to first limit the scope of the dependence by considering stationary processes.

Definition 3.1 (Stationary Processes).

A sequence of random variables is stationary if, for any and ,

That is, the finite-dimensional distributions of a stationary process are time-invariant.

We define next a natural condition for dependent data.

Definition 3.2 (-mixing).

For a stationary stochastic process and index , the -mixing coefficient of the process at is defined as

where denotes the total variation norm, and is the joint distribution of the blocks . The process is -mixing if when .

Intuitively, the -mixing coefficient measures how close, in total variation distance, the law of two blocks of random variables units apart is from being independent. Many natural classes of stochastic processes satisfy this property, including ARMA and GARCH models [8, 30] and more general Markov processes [16]. In particular, the -mixing coefficients decay exponentially fast for ARMA and GARCH models, and likewise for stationary geometrically ergodic Markov chains.

The -mixing condition allows us to replace independence with asymptotic independence and still retain some important concentration results. The so-called Blocking Technique [38, 29, 25] allows one to compare a -mixing process with another process made of independent blocks. The results below generally follow from combining the Blocking Technique with decoupling arguments and Bernstein’s concentration inequality.

Remark 3.3.

Our theoretical bounds are in terms of “optimal block sizes”. However, this is a purely mathematical device: while they appear in the performance bounds below, the split CP method is not dependent on this optimization (or even the definition of block sizes; this is in contrast with, e.g., [11]).

3.1 Standard coverage guarantees

We now argue that Assumptions 3, 4 and 5 hold for stationary -mixing processes. As is standard with the Blocking Technique, the error bounds obtained will depend on an optimization of block sizes (cf. Remark 3.3).

The sets of parameters we optimize over are defined as follows:

and

These two sets correspond to block size choices in the calibration and test sets, respectively. For the calibration set, define the error term as follows:

| (12) | ||||

where

| (13) |

Similarly, we define the test error correction factor for a stationary -mixing process as

| (14) | ||||

With defined as above, Theorem 2.3 yields the following result for stationary -mixing processes:

Theorem 3.4 (Marginal coverage: stationary -mixing processes).

Suppose that is stationary -mixing. Then given and , for ,

with where is as in (12) and Additionally, if almost surely has a continuous distribution conditionally on the training data, then:

Remark 3.5.

Additionally, with as above, Theorem 2.4 yields the following:

Theorem 3.6 (Empirical coverage: stationary -mixing processes).

Remark 3.7.

The expression in (12) follows from a stationary -mixing version of Bernstein’s inequality, proved in the appendix, which might be of independent interest. The factor of that appears in the variance term is due to the fact that for any , we have

However, given a confidence level , it is possible to improve on this bound by considering , where is a slight adaptation of the -quantile, such that

provided, for example, that almost surely has a continuous distribution conditionally on the training data. Therefore, our calibration adjustment becomes

| (15) | ||||

and the test adjustment becomes,

| (16) | ||||

where

| (17) |

which is never worse than (12) since . Nonetheless, as shown in Remark 3.5, our original bound (12) is enough to recover the same asymptotic order of the iid case.

Finally, note that in the iid case, using the fact that for any

and applying a similar argument as before, it is possible to show that, provided that almost surely has a continuous distribution conditionally on the training data and , we can take

| (18) |

3.2 Conditional guarantees

To apply Theorems 2.8 and 2.9 for stationary -mixing processes, we need to specify a family of Borel measurable sets in satisfying certain conditions that allow us to verify Assumptions 6, 7 and 8. In the remaining of this section we assume the following:

Assumption 9 (Family complexity).

For a fixed value , the family of Borel measurable sets in has finite VC dimension and for all .

The assumption that has finite VC dimension allows us to obtain concentration bounds for the empirical processes in Assumptions 6 and 8. Moreover, the condition is important to ensure the conditioned empirical quantile is well defined.

Now, given and , we define the calibration error correction factor for a stationary -mixing process conditioned to the family as

| (19) | ||||

where

Note the factor in : for to be small, we need to be small and consequently has to be large. This is quite natural, since if is too small, the probability can be close to zero, and thus a larger sample is necessary to estimate the empirical quantile well.

Similarly, we define the test error correction factor for a stationary -mixing process conditioned to the family as

| (20) | ||||

where

Finally, Theorem 2.8 yields the following result.

Theorem 3.8 (Conditional coverage: stationary -mixing processes).

Suppose that is stationary -mixing. Then given , and , for each and any

with , where is as in (19) and

Additionally, if almost surely has a continuous distribution conditionally on the training data, then:

And Theorem 2.9 yields the following:

4 Extensions

We discuss extensions of our theoretical framework beyond the cases covered by Sections 2 and 3. For simplicity, we focus only on non-conditional coverage.

In §4.1 we present an analysis of the rank-one-out conformal prediction method of Lei et al. [26]. That method calibrates the quantile used for each test data point by looking at the remaining test points. We give a complete analysis of that method following the general framework of Section 2. Additionally, we sketch how one can obtain explicit error terms via the -mixing assumption from Section 3.

In §4.2 we consider Risk-Controlling Prediction Sets, a very general uncertainty quantification technique due to Bates et al. [6] that goes beyond the regression setting. That method is implicitly based on the same data-splitting strategy as split CP. Using this, we sketch how our analysis extends to this technique.

Finally, §4.3 considers what happens when we drop the data stationarity assumption. We explain how a combination of our techniques with recent ideas of Barber et al. [4] can be used to analyze this case.

4.1 Rank-one-out conformal prediction

Rank-one-out (ROO) conformal prediction, introduced by Lei et al. [26], is different from split CP in that the test data is also used to calibrate the method. Specifically, a different quantile is used for each test point, and that quantile is calibrated using the remainder of the test set. This requires replacing Assumption 2.

Assumption 10 (Training, test, and calibration data; trained conformity score).

Assume is a sum of two positive integers, with , and partition the indices

where corresponds to the training data and corresponds to the test data. For each , the calibration set for is . The function and are as in Assumption 2.

We now define empirical quantiles and test sets for each .

Definition 4.1 (ROO empirical quantiles and predictive sets).

Given and , let denote the empirical -quantile of over ; that is:

For , the rank-one-out predictive set for is then defined via:

Finally, we need a third assumption combining the concentration and decoupling assumptions in §2.2.2.

Assumption 11 (Concentration and decoupling on test data for ROO).

There exist , and with the following property: let , , and be as in Definition 2.2. Then for any ,

and moreover,

Our main result on rank-one-out is an analogue of Theorems 2.3 and 2.4. For simplicity, we do not prove the results guaranteeing coverage upper bounds.

Theorem 4.2 (Marginal and empirical coverage over test data for ROO).

One can adapt the analysis in Section 3 to bound the parameters , and in Assumption 11. In particular, one may take , and equal to the respective parameters in that section, but with replacing . This reflects the fact that the calibration set for each point of rank-one-out is essentially equal to the test set.

On the other hand, we note that marginal coverage might suffer somewhat over the first few test data, since may be large for small values . This is because, in contrast to split CP, there is no gap in ROO between training and test data. In particular, the first test points may be strongly correlated with the training.

4.2 Risk-controlling prediction sets

Risk-controlling prediction sets (RCPS), introduced by Bates et al. [6], give a very general methodology for uncertainty quantification that applies in a variety of settings, including regression, multiclass classification and image segmentation. Importantly, RCPS does not involve conformity scores, but rather, the construction of nested sets. The original theory of RCPS in [6] assumes independent data. In what follows, we sketch an analysis of this method in our framework.

RCPS requires a split of data into training and calibration. Because we want to explicitly account for dependencies between data points, we follow the setup in Section 2 and take tripartition of the data set. The following is an analogue of Assumption 2.

Assumption 12 (Training, and calibration data; tolerance regions and loss function).

Assume is a sum of three positive integers, and partition the indices

where corresponds to the training data, corresponds to calibration data, and corresponds to test data. Suppose is a family of sets, is a closed set, and a map

is given with the following property: for all choices of , and :

For , we use the notation

to denote the values of when the first pairs in the input correspond to the training data. We call a trained tolerance region. Finally, is a loss function that is decreasing in the component.

Remark 4.3.

There are measure-theoretic issues related to the definition of and above. For ease of exposition, we will implicitly assume that and are “well-behaved enough” to allow the ensuing discussion to make sense. This is known to be the case in the practical examples in [6].

The goal of RCPS is to compute a value from the calibration data that achieves (conditional) risk smaller than a prespecified level . The conditional risk is defined in the next assumption. First, we need a definition (compare with Definition 2.2).

Definition 4.4 (Conditional expected risk).

We assume that the map

is almost surely continuous. Moreover, given a measurable , we let , and define the conditional expected risk:

where is as in Assumption 1.

We now explain how a threshold will be chosen from calibration data in order to control the risk. In [6], this involves finding another function that can be computed from the calibration data and gives a pointwise high-probability upper bound on . Since we are interested in approximate guarantees, we can allow for a that only bounds the risk up to a small error. Under suitable assumptions, the empirical risk will play this role.

Definition 4.5 (Empirical risk; empirical threshold).

The empirical risk over calibration data is defined as:

Given , define the empirical threshold:

Finally, we give conditions that guarantee that controls the risk with high probability. For simplicity, we focus on the marginal version of this condition. The following are analogues of Assumptions 3 and 4.

Assumption 13 (Concentration of the empirical risk on calibration data).

We assume that there exist , such that, for any as in Definition 4.4,

Assumption 14 (Decoupling over test data).

There exists a such that for all and all as in Definition 4.4,

We now state a result on the performance of RCPS over a single test point. The proof is essentially the same as that of [6, Theorem A.1].

Theorem 4.6 (Approximate marginal risk control for ).

Thus the expected loss at any test point is controlled by plus an error term that can be shown to be small under a -mixing assumption. Importantly, and similarly to [6], our result is achieved via assumptions that only bound the behavior of the loss over individual thresholds that are obtained from the training data. In particular, there is no need to require uniform control of the loss over a range of , which would require stronger (and looser) concentration bounds. The uniform bound on can be replaced by a moment assumption, at the cost of a messier bound.

4.3 Dealing with non-stationary data

As our final extension, we give a rough sketch how one could analyze split CP in a setting where there is dependent data with a marginal distribution that changes slowly over time. For clarity, we focus on marginal coverage. Our analysis is partly inspired by the recent preprint of Barber et al. [4].

Let empirical quantiles and predictive sets still be as in Definition 2.1, so the method is still the usual split CP. Assumption 1 is modified by replacing the pair with an auxiliary process , that is simply an independent copy of the original data .

Now define a random number that is uniformly distributed over , independently of the problem data and auxiliary process. The quantity:

measures how far the distribution of is to that of a randomly chosen point in the calibration dataset. This can be taken as a measure of distributional drift.

For marginal coverage, we go back to Definition 2.2, and take the random variable as before, but replace by a time-inhomogeneous version,

Letting be as in Definition 2.2, Assumptions 3 and 4 are also replaced with time-inhomogeneous versions, that is:

With these assumptions, marginal coverage result holds: for any ,

where is the same error term appearing in Theorem 2.3. In particular, we recover that theorem up to an error depending on how much distributional drift there is between and the calibration set. This is quite similar to the main result in [4], except that there the authors consider weighted calibration sets. Finally, it is possible to show that these assumptions hold for the nonstationary -mixing case.

Remark 4.7.

In practice, a reasonable way to deal with distribution drift is to occasionally (or always) update the training and calibration sets. Experiments with real data in §5.3 showcase online CP, even though data is assumed stationary there. Our finite-sample methods can also be used to analyze this case, at least when the -mixing coefficients decay fast enough. Note, however, that in the present setting we do not wish to assume stationarity.

5 Experiments

In this section, we display how our coverage guarantees fare in synthetic and real datasets, showing that, unless the dependence in the data is extreme, split CP works well even for non-exchangeable data. The synthetic experiments consider stationary -mixing sequences where can be found explicitly or numerically, while for the real data we consider financial series that can be assumed stationary after suitable transformations.

In the experiments below, data may be thought of as a time series, and the feature set to predict each data point is comprised of 11 lagged observations. Prediction is done via gradient boosting [18] with fixed hyperparameters and trained with the pinball loss [24] on training sets. The conformity scores are calculated over the calibration sets and conformalized following split conformal quantile regression [32]. Nominal coverage is set to and quantiles are calculated in accordance to the procedure outlined in Subsection 1.1. Since monotonicity of estimated quantiles is not guaranteed in this setting (see [5]), we follow [10] in swapping upper and lower quantiles in the rare cases where crossings occur.

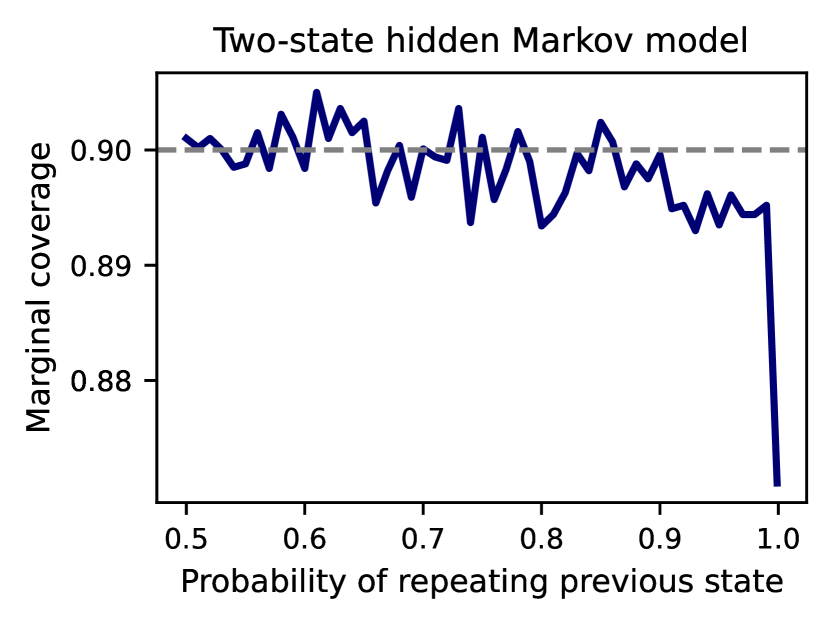

5.1 Two-state hidden Markov model

Let be a Markov chain with state space , probabilities and , and stationary distribution with , with and .

Homogeneous recurrent Markov chains are known to be absolutely regular and their -mixing coefficients can be directly calculated [14, 27, 35]. In particular, for two-state Markov chains with transition matrix , , so the -mixing coefficients can be calculated explicitly.

When , for all , indicating that in such cases the Markov chain reduces to a sequence of iid Bernoulli trials. On the other hand, as and tend towards zero, becomes large for every and dependence increases.

A hidden Markov model can be constructed from the Markov chain above by adding a Gaussian noise with small variance. The coefficients of the Markov chain are upper bounds on the coefficients for the hidden Markov model [38], and stationarity is still ensured by sampling the initial state from .

Figure 1(a) shows how marginal coverage (3), calculated through simulations, is affected by increasing levels of dependence. Marginal coverage observed is close to nominal iid value of 90% for the independent case () and weak to medium dependence, measured by the probabilities and of repeating the previous state. Coverage remains above 89% even for large values of dependence, and falls below 88% only after .

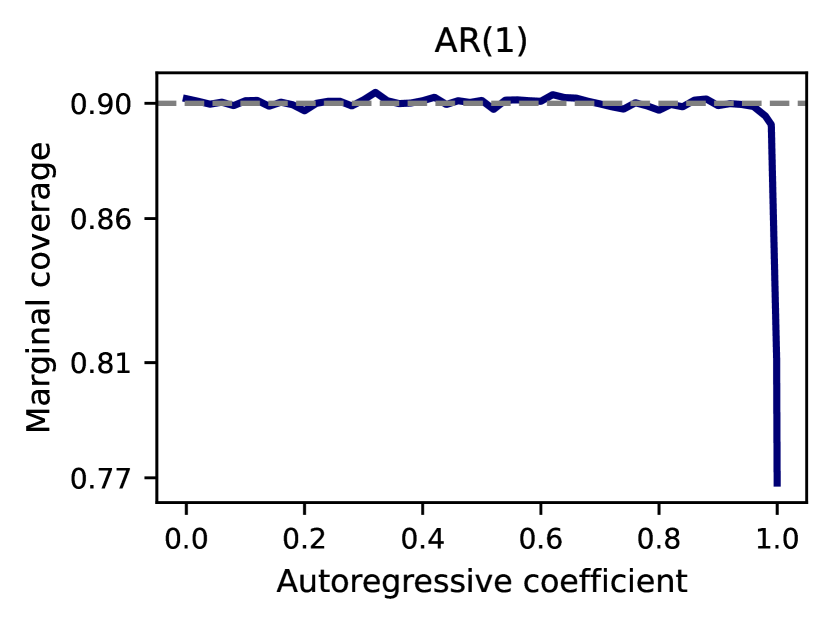

5.2 Autoregressive process

Consider the autoregressive process of order one (AR(1)), defined by the recurrence , with , , and independent normally distributed random variables with mean zero and variance one. The sequence is stationary as long as , and iid for . Although the -mixing coefficients cannot be calculated explicitly, it is possible to numerically integrate to approximate it, as in [27].

Figure 1(b) shows that the gap between marginal and iid nominal coverages is extremely tight even for highly dependent data following an process. Autoregressive coefficients up to achieve coverage higher than 89%. In particular, a significant loss of coverage only occurs when (81%) and (77%).

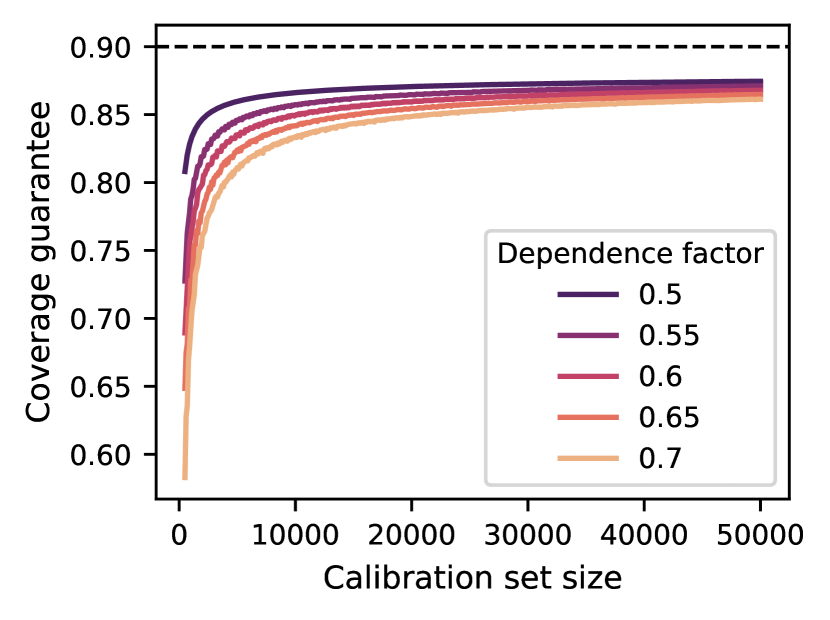

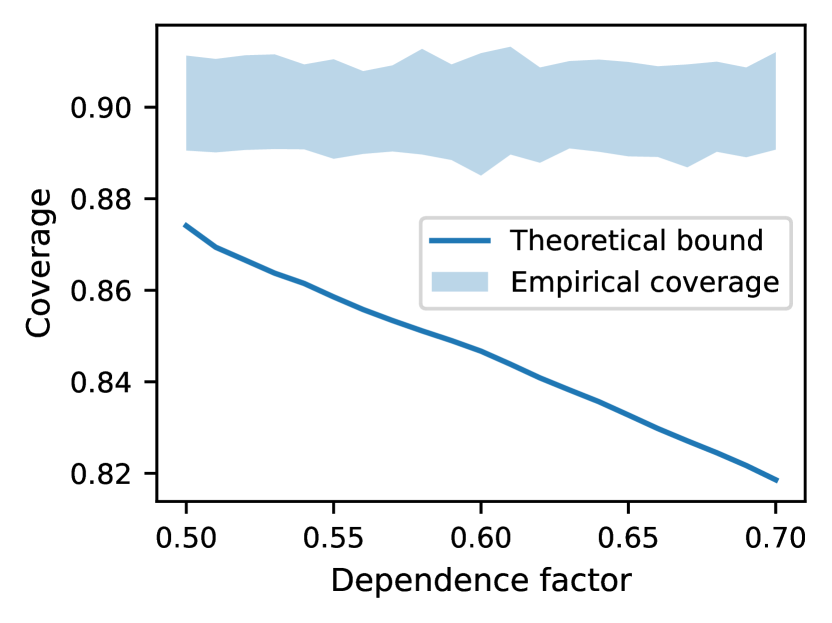

Figure 2 illustrates our marginal and theoretical coverage guarantees for the two-state hidden Markov model. Figure 2(a) shows how the correction in Theorem 3.4 depends on the calibration set sizes for the two-state hidden Markov model, quickly converging to the iid limit, even for moderately dependent data. Figure 2(b) illustrates Theorem 3.6 for and . Note the empirical coverage over simulations (blue region) is consistently high for varying levels of small to medium dependence. In particular, it is always above the theoretical guarantee (solid line), which naturally decreases as the data becomes more dependent.

5.3 Financial data

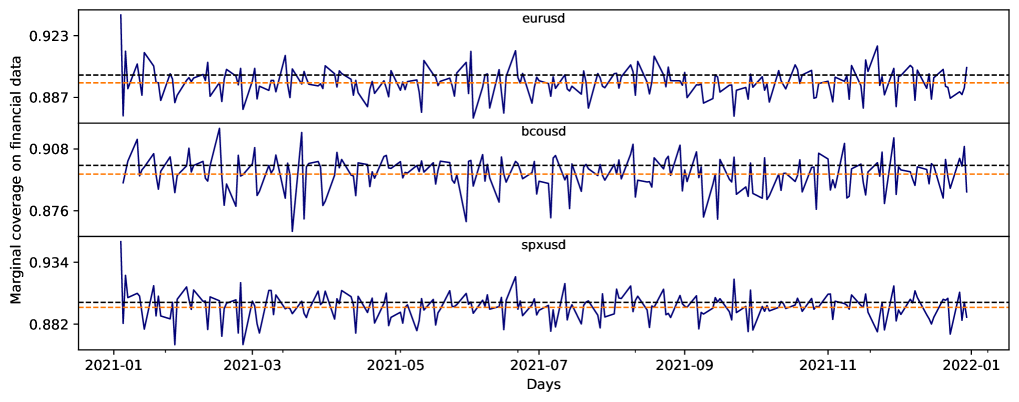

Consider predicting three distinct financial time series: Euro spot exchange rate (eurusd), Brent crude oil future (bcousd) and S&P 500 stock index future (spxusd). Minute-by-minute prices are available from HistData [21]. The data should be understood from a buyer’s perspective, with the typical spread between bid and ask not being too large in general, but with occasional periods of high volatility. As series of prices are highly nonstationary in general, we compute linear returns by dividing a price at time by the preceding price, at , and subtracting 1 from the result. Augmented Dickey-Fuller tests show the resulting series is sufficiently stationary. On the other hand, assessing -mixing is more delicate [27, 23]. However, previous works in the financial literature have argued that the autocorrelation of time series similar to the ones we consider have quickly vanishing autocorrelation [13], which we take as a reasonable indicator of -mixing.

We performed online conformal prediction over a sliding window of 1000 training points, 500 calibration points and 1 single test point for the entire year of 2021, each point corresponding to a minute. Figure 3 shows the daily marginal coverage (3) of the method from Mondays through Thursdays, as market operation is limited in other days of the week. The dashed black line represents the iid nominal coverage of 90% and the dashed orange one the marginal coverage over the entire year. For all three time series, marginal coverage is slightly below 90%, but never drastically so. It is possible to use the guarantees provided in Section 3 to adjust the quantile according to the desired nominal levels.

| Dataset | Cal. set size | Conditional coverage | |||

|---|---|---|---|---|---|

| Uptrend | Downtrend | High vol. | Low vol. | ||

| eurusd | 500 | 88.76% | 88.82% | 87.64% | 90.07% |

| 1000 | 89.19% | 89.17% | 88.38% | 90.19% | |

| 5000 | 90.03% | 89.98% | 89.85% | 90.08% | |

| bcousd | 500 | 88.94% | 88.72% | 87.10% | 89.43% |

| 1000 | 89.35% | 89.04% | 87.65% | 89.95% | |

| 5000 | 89.78% | 89.77% | 89.33% | 89.98% | |

| spxusd | 500 | 89.12% | 89.01% | 88.87% | 89.68% |

| 1000 | 89.53% | 89.48% | 88.84% | 90.03% | |

| 5000 | 90.04% | 89.73% | 89.53% | 90.30% | |

Table 1 presents the conditional coverage (9) on four distinct events of interest for all three financial datasets. Uptrend (respectively, downtrend) stands for two consecutive observations of positive (negative) returns. High (low) volatility events are taken to be those in which the standard deviation of the previous 10 returns observed is above (below) a given threshold. Note that conditioning on all such events still yields coverage close to the nominal iid level, on all three datasets. Following the results in Section 3, larger calibration sets have an important effect in improving coverage.

6 Conclusion

The main result of this paper is that many of the appealing properties of split conformal prediction hold approximately well even when the data exhibits some degree of dependence. This is reflected by Theorems 3.4 and 3.6, which give marginal and empirical coverage guarantees for stationary -mixing sequences, and Theorems 3.8 and 3.9, for conditional coverage. To prove these results, we introduced a general framework for split CP, which can be extended in many directions, for example, beyond stationarity and to other CP methods, as shown in Section 4. Future directions for our framework include considering weaker mixing assumptions and other uncertainty quantification methods such as the jackknife+ [3].

Acknowledgements

RIO is supported by CNPq grants 432310/2018-5 (Universal) and 304475/2019-0 (Produtividade em Pesquisa), and FAPERJ grants 202.668/2019 (Cientista do Nosso Estado) and 290.024/2021 (Edital Inteligência Artificial).

References

- [1] Anastasios Nikolas Angelopoulos and Stephen Bates. A gentle introduction to conformal prediction and distribution-free uncertainty quantification. arXiv preprint arXiv:2107.07511, 2021.

- [2] Anastasios Nikolas Angelopoulos, Stephen Bates, Michael Jordan, and Jitendra Malik. Uncertainty sets for image classifiers using conformal prediction. In International Conference on Learning Representations, 2021.

- [3] Rina Foygel Barber, Emmanuel J Candes, Aaditya Ramdas, and Ryan J Tibshirani. Predictive inference with the jackknife+. The Annals of Statistics, 49(1):486–507, 2021.

- [4] Rina Foygel Barber, Emmanuel J Candes, Aaditya Ramdas, and Ryan J Tibshirani. Conformal prediction beyond exchangeability. arXiv preprint arXiv:2202.13415, 2022.

- [5] Gilbert Bassett Jr and Roger Koenker. An empirical quantile function for linear models with iid errors. Journal of the American Statistical Association, 77(378):407–415, 1982.

- [6] Stephen Bates, Anastasios Angelopoulos, Lihua Lei, Jitendra Malik, and Michael Jordan. Distribution-free, risk-controlling prediction sets. Journal of the ACM (JACM), 68(6):1–34, 2021.

- [7] Richard C. Bradley. Basic Properties of Strong Mixing Conditions. A Survey and Some Open Questions. Probability Surveys, 2(none):107–144, 2005.

- [8] Marine Carrasco and Xiaohong Chen. Mixing and moment properties of various garch and stochastic volatility models. Econometric Theory, 18(1):17–39, 2002.

- [9] M Cauchois, S Gupta, and J. Duchi. Knowing what you know: valid and validated confidence sets in multiclass and multilabel prediction. Journal of machine learning research, 22(81), 2021.

- [10] Victor Chernozhukov, Iván Fernández-Val, and Alfred Galichon. Quantile and probability curves without crossing. Econometrica, 78(3):1093–1125, 2010.

- [11] Victor Chernozhukov, Kaspar Wüthrich, and Yinchu Zhu. Exact and robust conformal inference methods for predictive machine learning with dependent data. In Sébastien Bubeck, Vianney Perchet, and Philippe Rigollet, editors, Conference On Learning Theory, COLT 2018, Stockholm, Sweden, 6-9 July 2018, volume 75 of Proceedings of Machine Learning Research, pages 732–749. PMLR, 2018.

- [12] Victor Chernozhukov, Kaspar Wüthrich, and Yinchu Zhu. Distributional conformal prediction. Proceedings of the National Academy of Sciences, 118(48):e2107794118, 2021.

- [13] Rama Cont. Stylized properties of asset returns. In Encyclopedia of Quantitative Finance. Wiley, 2010.

- [14] Yu A Davydov. Mixing conditions for markov chains. Theory of Probability and Its Applications, 18(2):312–328, 1974.

- [15] Matthew F Dixon, Igor Halperin, and Paul Bilokon. Machine learning in Finance, volume 1170. Springer, 2020.

- [16] Paul Doukhan. Mixing: properties and examples, volume 85. Springer Science & Business Media, 2012.

- [17] Rina Foygel Barber, Emmanuel J Candès, Aaditya Ramdas, and Ryan J Tibshirani. The limits of distribution-free conditional predictive inference. Information and Inference: A Journal of the IMA, 10(2):455–482, 08 2020.

- [18] Jerome H. Friedman. Greedy function approximation: A gradient boosting machine. The Annals of Statistics, 29(5):1189–1232, 2001.

- [19] Isaac Gibbs and Emmanuel Candes. Adaptive conformal inference under distribution shift. In A. Beygelzimer, Y. Dauphin, P. Liang, and J. Wortman Vaughan, editors, Advances in Neural Information Processing Systems, 2021.

- [20] Yotam Hechtlinger, Barnabas Poczos, and Larry Wasserman. Cautious deep learning. arXiv preprint arXiv:1805.09460, 2019.

- [21] HistData, 2022. https://www.histdata.com/, Retrieved on 2022-01-27.

- [22] Vilde Jensen, Filippo Maria Bianchi, and Stian Norman Anfinsen. Ensemble conformalized quantile regression for probabilistic time series forecasting. arXiv preprint arXiv:2202.08756, 2022.

- [23] Azadeh Khaleghi and Gábor Lugosi. Inferring the mixing properties of an ergodic process. arXiv preprint arXiv:2106.07054, 2021.

- [24] Roger Koenker and Gilbert Bassett. Regression quantiles. Econometrica, 46(1):33–50, 1978.

- [25] Vitaly Kuznetsov and Mehryar Mohri. Generalization bounds for non-stationary mixing processes. Machine Learning, 106(1):93–117, 2017.

- [26] Jing Lei, Max G’Sell, Alessandro Rinaldo, Ryan J. Tibshirani, and Larry Wasserman. Distribution-free predictive inference for regression. Journal of the American Statistical Association, 113(523):1094–1111, 2018.

- [27] Daniel J. McDonald, Cosma Rohilla Shalizi, and Mark Schervish. Estimating beta-mixing coefficients via histograms. Electronic Journal of Statistics, 9:2855–2883, 2015.

- [28] Mehryar Mohri and Afshin Rostamizadeh. Rademacher complexity bounds for non-i.i.d. processes. In D. Koller, D. Schuurmans, Y. Bengio, and L. Bottou, editors, Advances in Neural Information Processing Systems, volume 21. Curran Associates, Inc., 2009.

- [29] Mehryar Mohri and Afshin Rostamizadeh. Stability bounds for stationary -mixing and -mixing processes. Journal of Machine Learning Research, 11(2), 2010.

- [30] Abdelkader Mokkadem. Mixing properties of arma processes. Stochastic processes and their applications, 29(2):309–315, 1988.

- [31] Suman Ravuri, Karel Lenc, Matthew Willson, Dmitry Kangin, Remi Lam, Piotr Mirowski, Megan Fitzsimons, Maria Athanassiadou, Sheleem Kashem, Sam Madge, et al. Skilful precipitation nowcasting using deep generative models of radar. Nature, 597(7878):672–677, 2021.

- [32] Yaniv Romano, Evan Patterson, and Emmanuel Candes. Conformalized quantile regression. In H. Wallach, H. Larochelle, A. Beygelzimer, F. d’Alché Buc, E. Fox, and R. Garnett, editors, Advances in Neural Information Processing Systems, volume 32. Curran Associates, Inc., 2019.

- [33] Glenn Shafer and Vladimir Vovk. A tutorial on conformal prediction. CoRR, abs/0706.3188, 2007.

- [34] Ryan J Tibshirani, Rina Foygel Barber, Emmanuel Candes, and Aaditya Ramdas. Conformal prediction under covariate shift. In H. Wallach, H. Larochelle, A. Beygelzimer, F. d’Alché Buc, E. Fox, and R. Garnett, editors, Advances in Neural Information Processing Systems, volume 32. Curran Associates, Inc., 2019.

- [35] Mathukumalli Vidyasagar and Rajeeva L. Karandikar. A learning theory approach to system identification and stochastic adaptive control. In Probabilistic and Randomized Methods for Design under Uncertainty, pages 265–302. Springer-Verlag, 2016.

- [36] Vladimir Vovk, Alex Gammerman, and Glenn Shafer. Algorithmic Learning in a Random World. Springer-Verlag, 2005.

- [37] Chen Xu and Yao Xie. Conformal prediction interval for dynamic time-series. In Marina Meila and Tong Zhang, editors, Proceedings of the 38th International Conference on Machine Learning, volume 139 of Proceedings of Machine Learning Research, pages 11559–11569. PMLR, 2021.

- [38] Bin Yu. Rates of Convergence for Empirical Processes of Stationary Mixing Sequences. The Annals of Probability, 22(1):94–116, 1994.

Appendix A Proofs of Section 2

For the proofs below, we need to introduce certain population quantiles for conditionally on the training data.

Definition A.1 (Conditional -quantile of the conformity score).

Remark A.2.

When the conditional law of given the training data is continuous, we have . Otherwise, it only holds that .

Proof of Theorem 2.3.

First we show that the event

satisfies Indeed, by Definitions 2.1, A.1 and Assumption 3, for any , with probability at least ,

This implies that the event

satisfies for all , and since , we have

where,

proving that . Therefore, given , using the fact that the function is increasing,

Hence, by Assumption 4 and a conditioning argument,

| (21) | ||||

proving the first part of the theorem.

For the second part, note that by Definition A.1 and Assumption 3 we have with probability at least

and since is the smallest possible value satisfying the expression above, the event

satisfies Then,

Hence, if almost surely has a continuous distribution conditionally on the training data, by Assumption 4

Putting this together with (21) concludes the second part. ∎

Proof of Theorem 2.4.

Using Assumptions 3 and 5 and a similar argument as we did in the proof of Theorem 2.3, it is easy to show that the event

satisfies But then,

proving the first part. For the second part, note that

also has probability at least , therefore the event

has probability at least

Hence, if almost surely has a continuous distribution conditionally on the training data, using the same argument as we did in the proof of Theorem 2.3 concludes the theorem. ∎

Appendix B Proofs of Section 3.1

Our goal is to check Assumptions 3, 4 and 5 when is a stationary -mixing process. As stated in the main text, the main tool we will use is the so-called Blocking Technique [38, 29, 25]. It allows one to measure the difference in expectation between a function of a -mixing process and the same function over an independent process, thereby transforming the original dependent problem into an independent one with the addition of a penalty factor.

Proposition B.1 (Blocking Technique).

Let be a sample of a stationary -mixing process. Split the sample into interleaved blocks, with even blocks of size and odd blocks of size , such that . Denote each block by , where and , so the set of odd blocks, each of size , is given by . Consider also the set where are independent for , and . If is a Borel-measurable function with for some , then

where is the -mixing coefficient of .

Using the Blocking Technique, we can prove that up to a error correction factor, we can transform our stationary -mixing problem into a iid one:

Lemma B.2 ([28]).

Let be a sample drawn from a stationary -mixing distribution. Split the sample into blocks, with blocks of size with . Denote the blocks by where and , with . Call the independent version of by , where are independent with , and let be their law. Then,

Finally, using Lemma B.2 and Bernstein’s Inequality, we are ready to prove a concentration inequality for stationary -mixing processes.

Lemma B.3.

Let be a sample drawn from a stationary -mixing distribution with and . Then, for any with , and , with probability at least it holds that

where

and

Proof.

By an application of Lemma B.2 and Bernstein’s inequality over the independent blocks, with probability at least

| (22) | ||||

| (23) | ||||

where To estimate , note that by stationarity,

Now, using the fact that is -mixing, we have

That is,

Plugging the above expression in (22) and using the fact that yields the result. ∎

Proposition B.4.

Proof.

We want to use Lemma B.3 for the random variables

however, since the random variables are dependent to and the quantile , we cannot simply apply the result. To fix this problem, it will be necessary to create a gap between our training and calibration data and use the Blocking Technique, Proposition B.1, to transpose our problem to an independent setting.

For and , let and define the event

we want to show that there exists such that Note that if holds, then

and since ,

that is, . Now, define

so under , we have that and are independent. Then, by Proposition B.1,

Note that by Lemma B.3, for any with and , using the fact that , taking

implies

hence,

which is equivalent to

if we take

Finally, since this is true for any choice of and with and , we can choose optimally such that the value of is minimized and there is no need to optimize in in this case.

∎

Proposition B.5.

If is stationary -mixing, then Assumption 4 holds with

Moreover, since , it is possible to find not depending on

Proof.

Given , define

so under the random variable is independent of the training data Then, if we have,

where the penalty follows from Proposition B.1. Note that the larger the the smaller the penalty incurred by the dependence in the -mixing process. Moreover, since

it is possible to define not depending on ∎

Proposition B.6.

Proof.

The proof is similar to the proof of Proposition B.4. Let the event be

Define,

so under we have that and are independent. By Proposition B.1 we have

Now we can apply Lemma B.3 and conclude that, just as we did in Proposition B.4, that for any , with and , it is true that , where

and

Finally, since this is true for any choice of and , with and , we can choose optimally such that the value of is minimized.

∎

Appendix C Proofs of Section 3.2

The proofs in this section are very similar to the proofs in Section 3.1, however, since we are dealing with a family of Borel measurable sets , we will need concentration results that allow us to uniformly control certain quantities over the family First, we state such classical results for iid sequences.

Theorem C.1 (Sauer-Shelah).

Let be a class of functions from to with finite VC dimension VC . Then, for any integer ,

Theorem C.2.

Let be iid random variables taking values on and be a class of functions from to . Then

Using the Blocking Technique, we can prove that up to a error correction factor, we can transform our stationary -mixing problem into a iid one. For example,

Lemma C.3 ([28]).

Let be a sample drawn from a stationary -mixing distribution and be a class of functions from to . Split the sample into blocks, with blocks of size with . Denote the blocks by where and , with . Call the independent version of by , where are independent with , and let be their law. Then,

Corollary C.4.

Let be a sample drawn from a stationary -mixing distribution and be a class of functions from to . Then, for any , with , and , it holds that

where

| (24) |

Proof.

By an application of Lemma C.3 and McDiarmids’s inequality over the independent blocks, it follows that

| (25) |

where

| (26) |

Denote by the th random variable of the th block , therefore the expectation in (26) can be written as

where the inequality comes from the triangular inequality and the monotonicity of the supremum.

Note that in we are considering only one element of each independent block , therefore this is a sum over iid random variables. Hence, by Theorem C.2

That is,

So taking and yields

∎

Corollary C.5.

Let be a sample drawn from a stationary -mixing distribution, be any deterministic function and be a family of Borel measurable sets in with finite VC dimension .

Lemma C.6.

Let be a sample drawn from a stationary -mixing distribution, and be a family of Borel measurable sets in with finite VC dimension such that for all . For with , and suppose that with as in (24). Then,

Lemma C.7.

Let be a sample drawn from a stationary -mixing distribution, be a deterministic function, and be a family of Borel measurable sets in with finite VC dimension such that for all . For with , and , if

then with probability at least

where as in (24).

Proof.

Define as in the lemma statement. We want to show that:

has probability at most . To this end, we define the following auxiliary event, which controls the random denominator term in :

By Lemma C.6, , so it suffices to show that:

| (27) |

Note that, if holds, then the quotient is well defined and

∎

Proof.

The proof is similar to the proof of Proposition B.4. For and , let

and

Define the events

and

and We want to show that there exists such that if then

Note that if holds, then for all

That is, . Now, define

so under we have that and are independent. By Proposition B.1 we have

But this implies that

For any with and , if we take

and assume that then

so Lemma C.7 tells us that

and Lemma C.6 tells us . That is,

which is equivalent to say that

if is as in the proposition statement. ∎

Proposition C.9.

Assumption 7 holds with

Proof.

Given , note that we can decompose

so under we have that is independent of Then, defining we have for all

where the penalty follows from Proposition B.1. But then, by a conditioning argument,

Finally, dividing by and using the fact that

yields the result. ∎

Proposition C.10.

Proof.

The proof is similar to the proof of Proposition C.8. Let the event be

Define,

so under we have that and are independent. By Proposition B.1 we have

Now we can apply Lemma C.7 and conclude that if , for any with and , it is true that , where

Finally, since this is true for any choice of with and , we can choose optimally such that the value of is minimized. ∎