High-Dimensional Vector Autoregression with Common Response and Predictor Factors

Abstract

The reduced-rank vector autoregressive (VAR) model can be interpreted as a supervised factor model, where two factor modelings are simultaneously applied to response and predictor spaces. This article introduces a new model, called vector autoregression with common response and predictor factors, to explore further the common structure between the response and predictors in the VAR framework. The new model can provide better physical interpretations and improve estimation efficiency. In conjunction with the tensor operation, the model can easily be extended to any finite-order VAR model. A regularization-based method is considered for the high-dimensional estimation with the gradient descent algorithm, and its computational and statistical convergence guarantees are established. For data with pervasive cross-sectional dependence, a transformation for responses is developed to alleviate the diverging eigenvalue effect. Moreover, we consider additional sparsity structure in factor loading for the case of ultra-high dimension. Simulation experiments confirm our theoretical findings and a macroeconomic application showcases the appealing properties of the proposed model in structural analysis and forecasting.

Keywords: Factor model, High-dimensional time series, Gradient descent, Matrix factorization, Tensor decomposition

1 Introduction

Due to recent developments in information technologies, high-dimensional data, especially time-dependent data, have been routinely collected from a wide range of scientific areas, including economics, finance, neuroscience, and meteorology, among others (Gorrostieta et al.,, 2012; Hallin and Lippi,, 2013; Dowell and Pinson,, 2016). The well-developed statistical methodology for fixed-dimensional data may not be directly applicable to high-dimensional cases, and large-scale data sets often also require scalable and efficient computational algorithms. As a result, it becomes an emerging area of research to develop new statistical methodology and theoretically justified algorithms to analyze the high dimensional data (Wainwright,, 2019; Chi et al.,, 2019). In addition, more efforts are needed for high-dimensional time series data due to its complex dynamic dependency; see Peña and Tsay, (2021).

The vector autoregressive (VAR) model, arguably the most widely used model in multivariate time series applications, has been a primary workhorse for analyzing serially dependent data. Consider a VAR(1) model for a -dimensional mean-zero time series ,

| (1.1) |

where is a white noise process with mean zero and the covariance matrix , and is the parameter matrix providing a straightforward characterization of the interactions between the response and predictor ; see Tsay, (2014). Note that the number of parameters in increases quadratically with the dimension , making it difficult to apply VAR models to high-dimensional data. To overcome it, a commonly used solution is to assume sparsity in parameter matrices, and many sparsity-imposing or inducing methods can then be employed for estimation and variable selection, including regularization (Basu and Michailidis,, 2015; Han et al.,, 2015) and linear restrictions (Guo et al.,, 2016; Wang and Tsay,, 2023).

Despite its popularity in the literature, there are two concerns about sparse VAR modeling. First, the general sparsity structure cannot guarantee the spectral radius condition for stationarity, so a sparse estimate may result in a non-stationary VAR model. Second, for financial and economic time series, one often observes strong dependence among the scalar series, which often is investigated via factor models by assuming that the variables can be decomposed into two parts, factors and errors. In the vast literature of econometrics and statistics, there are two classes of factor models under various assumptions on factors and errors. The first class assumes that factors are common cross-sectionally and allows for serially dependent idiosyncratic errors (Stock and Watson,, 2002; Bai and Ng,, 2002, 2008); while the second class assumes that the dynamic structures along the temporal direction are summarized in the factors, and the errors are temporally uncorrelated (Peña and Box,, 1987; Lam and Yao,, 2012; Gao and Tsay,, 2022).

Another solution for handling high dimensionality is to impose some low-rank structure on the parameter matrices of VAR models, and it leads to the reduced-rank model (Velu and Reinsel,, 2013) or the multilinear low-rank model (Wang et al.,, 2022). This method can circumvent the two concerns mentioned above, and especially for financial and economic data, the fitted models can be interpreted from the perspective of the second class of factor models. Specifically, assume that is of rank with and, hence, it admits a singular value decomposition (SVD) , where and are -by- orthonormal matrices. Accordingly, model (1.1) can then be rewritten as

| (1.2) |

and this motivates us to interpret and as -dimensional response and predictor factors, respectively, where and are the factor loading matrices. The factors defined here can summarize the temporal dynamics in responses and predictors, and should be understood in the sense of the second class of factor models, in which the factors capture all dynamic dependency in the data. Along this line, we reformulate the VAR model with a low-rank parameter matrix into a form of supervised factor modeling in Section 2.1. Specifically, it is equivalent to simultaneously conducting two factor modelings for the financial or economic variables in a market, where the latent response factors can summarize the whole market as in the traditional factor modeling, while the latent predictor factors are the driving forces of the market; see Section 2 for more details.

Although the factor model cannot directly be used for forecasting, a common practice is to apply a low-dimensional model to the factor processes, and then use predictions of the factors and the loading matrices to obtain forecasts of the high-dimensional time series (Lam and Yao,, 2012; Gao and Tsay,, 2022). For example, for a -dimensional time series , consider the factor model in Gao and Tsay, (2022), which can be written as with being a low-dimensional factor process and a -dimensional white noise, and the loading matrix being orthonormal. Assuming a VAR(1) model for , say , it can be shown that follows a VAR(1) process

| (1.3) |

In comparison with model (1.2), the spaces spanned by the response and predictor factors in model (1.3) are identical; see Section 2.1 for more discussions on its relationship to VAR models. As shown by the empirical example in Section 8, the setting of factor models may be too restrictive, while the spaces spanned by and from VAR models in (1.2) may be overlapped, i.e., there may exist common factors in responses and predictors. The first main contribution of this article is to propose a VAR model with common response and predictor factors in Section 2.2, where dynamic dependence in time series is summarized into three types of factors: response-specific, predictor-specific, and common factors. This enables a better physical interpretation and facilitates the development of more efficient estimation.

We then consider the high-dimensional estimation method and algorithm. A form of matrix or tensor decomposition is considered for the proposed model. However, as the decomposition is not unique and the optimization problem is non-convex, it is challenging to derive computational and statistical guarantees. To this end, the second contribution of this article is to develop a complete modeling procedure for estimation and parameter selection in Section 3 and further to provide theoretical justifications for both computational and statistical convergence in Section 4. Specifically, a regularized estimation framework is proposed for high-dimensional VAR models with common response and predictor factors, and a scalable and efficient gradient descent algorithm with spectral initialization is developed accordingly. From the computational and statistical convergence analysis, the proposed procedure can effectively and efficiently achieve a statistically optimal rate for estimation errors. Moreover, a data-driven procedure is suggested to determine the numbers of common and specific factors, and its theoretical justifications are also established.

To adequately address the strong cross-sectional dependence of time series data in the many real applications, in Section 5, we further investigate the case where the largest eigenvalue of may diverge to infinity as increases. The third contribution of this article is to provide the first solution to deal with the diverging eigenvalue effect, or pervasive cross-sectional dependency, in high-dimensional VAR estimation. Additionally, in Section 6, for the case of , we consider an additional sparsity structure on the factor loading matrices to improve estimation efficiency and to perform variable selection. Finally, some simulation results and an empirical example are presented in Sections 7 and 8, respectively. Section 9 gives a short conclusion with discussion. All technical proofs, codes, data, and additional simulation results are given in appendices.

This work is also related to the vast literature on Bayesian VAR models. Bańbura et al., (2010) studied the shrinkage prior for large Bayesian VAR models, and Koop, (2013) applied it to the macroeconomic data of medium and large sizes. Bayesian variable selection method for VAR processes was first proposed by Korobilis, (2013). Ghosh et al., (2019) and Ghosh et al., (2021) studied posterior estimation consistency and strong variable selection consistency of large Bayesian VAR models, respectively.

Throughout this article, we denote vectors by boldface lower case letters, e.g., , matrices by boldface capital letters, e.g., , and third-order tensors by Euler script letters, e.g., . For any vector , denote by its Euclidean norm. For any matrix , denote by , , , , and its transpose, Frobenius norm, -th largest singular value, column space, and orthogonal complement of column space, respectively. For a symmetric matrix , denote by and its largest and smallest eigenvalue, respectively. For two matrices and , denote by and their column-wise matrix concatenation and inner product, respectively. For positive integers , denote the set of orthonormal matrices by . For a third-order tensor , denote by the Frobenius norm and by its mode- matricization, for . For a tensor and matrix , denote by the mode- tensor-matrix multiplication, for . Let denote a generic positive constant. For two real-valued sequences and , if there exists a such that for all . In addition, we write if and . Some preliminaries of tensor notation and tensor algebra are presented in Appendix D.

2 VAR with Common Response and Predictor Factors

2.1 Relationship between reduced-rank VAR and factor models

Consider the VAR(1) model in (1.1). Assume that the parameter matrix has a low rank , which is much smaller than , and admits the SVD , where are orthonormal matrices, and is a diagonal matrix. As a result, the reduced-rank VAR model can be formulated into

| (2.1) |

where are i.i.d. with mean zero and finite variance matrix; see Velu and Reinsel, (2013). Note that the singular vectors and are not unique, as sign switches and column exchanges can be applied. Also, when some of the singular values are identical, their corresponding singular vectors are also not unique. However, the column spaces and , as well as the corresponding subspace projectors and , can be uniquely defined. In fact, and are the column and row spaces of , respectively.

From model (2.1), we can interpret and , respectively, as the response and predictor factors, which correspond to two different factor modelings. On one hand, for dimension reduction on the response factor space, can be projected onto and , where these two parts can be verified to have completely different dynamic structures,

| (2.2) |

All information of related to temporal dynamic structures is collected into , and the projection of onto is serially uncorrelated. In fact, model (2.1) can also simply be rewritten as with . Consequently, the time series generated by model (2.1) admits a form of static factor models, and the corresponding factor space is exactly the response factor space .

On the other hand, if we project onto and , it holds that

All information of that can contribute to predicting is summarized into the space , and the predictor factors contain all driving forces of the market. Following the existing work considering dynamically dependent factors and white noise errors (Lam and Yao,, 2012), we may treat model (2.1) as a supervised factor model, where two different factor modelings are conducted simultaneously and the dynamic dependence of time series is driven by these two types of factors.

Factor modeling, with dynamically dependent factors and white noise errors, is another method to forecast high-dimensional time series in the statistics literature; see Lam et al., (2011), Lam and Yao, (2012), Gao and Tsay, (2022), among others. Specifically, consider the factor model in Gao and Tsay, (2022), and assume that has a latent structure of

| (2.3) |

where is a dynamic factor, is a white noise, and and are full-rank loading matrices for factors and white noise components, respectively. For the sake of identification, and are assumed to be orthonormal, i.e., and , and is of full rank such that is nonsingular. Furthermore, suppose that the factors in (2.3) follow a VAR model, , where is a coefficient matrix, and is a white noise uncorrelated with in all leads and lags.

Denote , which is serially uncorrelated. Note that and, for the projection of onto , it holds that , which is also serially uncorrelated. The projection of onto follows

| (2.4) |

i.e. a form of vector autoregressive and moving average (VARMA) models (Tsay,, 2014). Moreover, when , it reduces to a VAR(1) process. In comparison with (2.2), the response and predictor spaces in (2.4) are identical, and this may be too restrictive; see Section 8 for empirical evidence.

We finally consider model (2.1) with the same response and predictor spaces, i.e., . There exists an orthogonal matrix such that . As a result, model (2.1) can be rewritten as , where ,

| (2.5) |

which remarkably coincide with dynamic structures of the above-mentioned dynamic factor model with , , , and .

2.2 Common response and predictor factors

For model (2.1), consider its response and predictor spaces, and , and suppose that their intersection is of dimension , i.e. , with . As a result, when , there exist two orthogonal matrices such that

| (2.6) |

where the orthonormal matrices represent the response-specific and predictor-specific subspaces of dimension , respectively, the orthonormal matrix represents the common subspace of dimension , and is orthogonal to and .

Let , and model (2.1) can be rewritten as

| (2.7) |

Let , , and . Then model (2.7) implies

| (2.8) |

We call the model in (2.7) or equivalently in (2.8) the vector autoregression with common response and predictor factors, and , , and are referred to as the common, response-specific, and predictor-specific factors, respectively.

The proposed model in (2.7) can provide a better physical interpretation, especially for financial and economic series, than reduced-rank VAR models in (2.1) by distinguishing these three types of factors; see Section 8 for empirical evidence. Moreover, the reduced-rank model in (2.1) has parameters, whereas the proposed model has parameters. When and are much smaller than , the model complexity is roughly reduced from to , and hence the corresponding estimation efficiency can be improved; see simulation experiments in Section 7.

Using tensor operations, we extend the proposed model to general VAR() processes,

| (2.9) |

The parameter matrices are first rearranged into a tensor such that its mode-1 matricization is , and its mode-2 matricization assumes the form . Note that the column spaces of and are the column and row spaces of all parameter matrices, respectively. Suppose that they are of dimensions and , respectively; that is, and , where and may not be equal. We have a Tucker decomposition via higher-order singular value decomposition (HOSVD) (De Lathauwer et al.,, 2000),

where and consist of the top and left singular vectors of and , respectively, the core tensor , and is the tensor-matrix mode- multiplication defined in Appendix D.

Split the mode-1 matricization of into with each , and then model (2.9) becomes

| (2.10) |

where and are the response and predictor factors, respectively. Note that and are not unique, but the subspaces and , together with their projectors and , can be uniquely defined. As in VAR(1), we can interpret model (2.10) as a supervised factor model with and being the response and predictor factor spaces, respectively.

Remark 1.

Let and , and then model (2.10) can be rewritten into , i.e. it admits a generalized dynamic factor modeling form in Forni et al., (2000, 2005). Note that the proposed model is for a supervised problem, while the generalized dynamic factor modeling is fundamentally for an unsupervised one. In addition, the factors and errors in Forni et al., (2000, 2005) are assumed to be uncorrelated in all leads and lags, but those in our model are not.

Suppose that the response and predictor subspaces share a common subspace of dimension , i.e., , with . Then there exist two matrices, and , such that , , and , where , , and are the response-specific, predictor-specific, and common subspaces of dimensions , , and , respectively. As a result, the parameter tensor can be formulated into , where . Furthermore, let , , and , and then model (2.10) has the form

| (2.11) |

where each is a -by- matrix such that . The model (2.11) defines a general vector autoregression with common response and predictor factors, and , , and are the common, response-specific, and predictor-specific factors, respectively.

For the parameter tensor , dimension reduction is conducted along the first two modes, and when the lag order is large, it is also of interest to further restrict the parameter space along the third mode. Specifically, assume that , and we have the Tucker decomposition: and

| (2.12) |

where is the core tensor and is the lag factor matrix. Similarly, this additional low-rankness along the third mode would lead to a lag-specific factor. The number of parameters under the low-rank structure is , while model (2.9) has parameters.

3 High-Dimensional Estimation Methods

3.1 Regularized estimation and gradient descent algorithm

Consider the observed sequence, , generated by the VAR(1) model in (2.7), and suppose that both and are known. Our aim is to estimate the parameter matrix

where , , , and are four blocks of . Let and , and the squared loss function is

| (3.1) |

With being regularization parameters, the components in (2.7) can be estimated by

| (3.2) |

The above estimation method is motivated by Han et al., (2021) for low-rank tensor estimation, and the regularization terms and are used to keep and from being singular and to balance the scaling of these components. It is noteworthy that . Moreover, the estimated parameter matrix is not sensitive to the choices of regularization parameters and , and they are set to one in all our numerical analysis.

We use the gradient descent method to solve the optimization problem in (3.2). Specifically, the partial derivatives can be calculated as

| (3.3) |

where . Given an initial estimator and a step size , we can then design a gradient descent algorithm to search for the minimizer of (3.2); see Algorithm 1.

1: Input: , , step size , number of iteration , initial values , , , and

2: for

3:

4:

5:

6:

7: end for

8: Return:

3.2 Initialization of the algorithm

The problem in (3.2) is non-convex, and the initial values play important roles in the algorithm. Hence, we provide a simple spectral initialization method.

Consider model (2.1) with and its equivalent form in (2.7) with and being orthonormal matrices. It then holds that , , and . Moreover, since is orthogonal to and , we have and . It implies that and are the subspaces spanned by the first left singular vectors of and . In addition, and .

The above finding motivates us to use a reduced-rank VAR estimation (Velu and Reinsel,, 2013) to construct an initialization. Specifically, denote by the first eigenvectors of , corresponding to the largest eigenvalues in the decreasing order, and then the reduced-rank VAR estimation has an explicit form of

| (3.4) |

As a result, the following procedure is suggested for initialization:

-

(i.)

Conduct SVD to the reduced-rank VAR estimator: ;

-

(ii.)

Calculate the top left singular vectors of and , and denote them by and , respectively;

-

(iii.)

Calculate the top eigenvectors of , and denote it by ;

-

(iv.)

Calculate ;

-

(v.)

Set the initialization to , , , and .

3.3 Rank selection and common dimension selection

The rank and common dimension are assumed to be known in the previous two subsections, but they are unknown in most real applications. Here we propose a two-stage selection procedure to select them and relegate its theoretical justification to Section 4.

A ridge-type ratio method (Xia et al.,, 2015) is first introduced to select the rank , regardless of the existence of the common subspace. Specifically, we first give a pre-specified upper bound for some , and then calculate the estimate in (3.4). Denote by its singular values, and then the rank can be selected by

| (3.5) |

where the ridge parameter is a positive sequence depending on and .

The proposed method is not sensitive to the choice of as long as it is greater than . Thus, for large datasets with a large dimension , we can choose the upper bound to be reasonably large but much smaller than . When is small, we may even simply set to . On the other hand, the ridge parameter is essential for consistent rank selection. We suggest using , according to Theorem 3 in Section 4.3, and its satisfactory performance is observed in our simulation experiments of Section 7.

Remark 2.

Next, we consider the selection of the common dimension in model (2.7). Denote by the estimator obtained from Algorithm 1 with the rank and common dimension , and then the Bayesian information criterion (BIC) can be constructed below,

| (3.6) |

where is the number of free parameters. As a result, given , the common dimension can be selected by . Note that the BIC in (3.6) can also be used to select and simultaneously, but it would be time-consuming in practice.

3.4 The case of VAR() models

This subsection extends the proposed methodology to VAR() models with common response and predictor factors. Suppose that and are known. To estimate the parameter tensor , the loss function is , where . With regularization parameters , we can use a gradient descent algorithm to find the following estimators

For initialization, consider the rank-constrained estimator (Wang et al.,, 2022)

and apply the similar initialization method in Section 3.2 to obtain . In addition, the ridge-type rank selection and the common dimension selection via BIC can also be extended to VAR() models. For brevity, the algorithm and implementation details are relegated to Appendix D.2.

4 Computational and Statistical Convergence Analysis

Sections 4.1 and 4.2 establish the computational and statistical convergence for the VAR(1) model, respectively. Section 4.3 studies the consistency of the rank and common dimension selection, and Section 4.4 provides the theoretical justification for the VAR() model. In what follows, we denote and as the ground truth of the parameter matrix and tensor.

4.1 Computational convergence analysis

The optimization problem in (3.2) is non-convex, and it is challenging to establish the convergence analysis of Algorithm 1. To solve it, we introduce some regulatory conditions.

Definition 1.

A function is restricted strongly convex with parameter and restricted strongly smooth with parameter , if for any matrices of rank ,

| (4.1) |

Definition 2.

For the given rank , common dimension , and the true parameter matrix , the deviation bound is defined as

| (4.2) |

The restricted strong convexity and smoothness of Definition 1 are essential in establishing the convergence analysis for many non-convex optimization problems; see Jain and Kar, (2017) and references therein. The deviation bound in Definition 2 characterizes the magnitude of statistical noises projected onto a low-dimensional space of matrices with rank and common dimension , and we can treat it as a statistical error as in Han et al., (2021).

For the true parameter matrix , denote its largest and smallest singular values and its condition number by , , and , respectively. Assuming that both and are known, we state the convergence analysis of Algorithm 1 below.

Theorem 1.

For the upper bound in Theorem 1, the first term corresponds to optimization errors, while the second term is related to statistical errors. From Theorem 1, the estimation error decreases toward a statistical limit exponentially with respect to iterations. Moreover, when the parameters , , and are bounded away from zero and infinity, the tuning parameters , , and would be at a constant level and, hence, do not depend on and .

4.2 Statistical convergence analysis

Assumption 1.

The parameter matrix has a spectral radius strictly less than one.

Assumption 2.

The error term is , where are random vectors with and . Moreover, the entries of are mutually independent and -sub-Gaussian, i.e. for any and .

Remark 3.

Assumption 1 is sufficient and necessary for the existence of a unique strictly stationary solution to model (2.1) with any finite , and this is consistent with the non-asymptotic framework used in this article. For the case with , we may refer to Zhu et al., (2017) for the definition of strict stationarity, which is given via a mechanism similar to the Cramer-Wold device. Moreover, the Gaussian condition is commonly used in the literature of high-dimensional time series (Basu and Michailidis,, 2015), while the sub-Gaussian condition in Assumption 2 is more general.

In the decomposition in (2.7), intuitively, the response-specific and predictor-specific subspaces and cannot be too close so that we can separate the common subspace out successfully. Here we use the distance for two spaces. Specifically, let be the singular values of . Then, the canonical angles between and can be defined as for . The following condition is added to the smallest canonical angle between and .

Assumption 3.

There exists a constant such that .

Furthermore, we quantify the temporal and cross-sectional dependency as in Basu and Michailidis, (2015). For any , let be the matrix polynomial, where is the set of all complex numbers. Let and , where is the conjugate transpose of . Moreover, denote

| (4.4) |

Based on them, we have the following statistical convergence analysis for Algorithm 1.

Theorem 2.

The above theorem gives an estimation error bound after a sufficiently large number of iterations. When the quantities of and are bounded away from zero and infinity, the required number of iterations does not depend on the dimension or the sample size , and this makes sure that the proposed algorithm can be applied to large datasets without any difficulty. Moreover, the estimated parameter matrix from Algorithm 1 has the convergence rate of , while the reduced-rank VAR estimation has the rate of (Negahban and Wainwright,, 2011). Note that roughly equals to when both and are much smaller than . This efficiency improvement is due to the fact that the proposed methodology takes into account the possible common subspace.

4.3 Rank and common dimension selection consistency

In this section, we provide theoretical justifications for rank and common dimension selection. First, we establish the rank selection consistency for the ridge-type ratio in (3.5).

The conditions in this theorem reduce to and as , when , , , , and are bounded. Moreover, the required sample size in Theorem 3 is the same as that for the estimation consistency in Theorem 2.

Given that the rank is known, the following theorem provides theoretical justifications for the proposed BIC in (3.6).

Theorem 4.

Suppose the conditions in Theorem 2 hold. Then, as .

4.4 Convergence analysis for VAR() models

This subsection extends the convergence analysis of the gradient descent algorithm for VAR(1) to VAR(). We refer the readers to Appendix D for the detailed algorithm and implementation. The computational convergence analysis can be extended from that in Section 4.1, and is omitted to save space. Here, we focus on the statistical convergence.

For the VAR () model in (2.9), define the matrix polynomial , where , and its stationarity condition is given below.

Assumption 4.

The determinant of is not equal to zero for all .

Denote by , , and the largest and smallest singular values and the condition number of the true parameter tensor, respectively. As in Section 4.2, we can similarly define the quantities, , , , , and . The statistical convergence analysis is given below.

Theorem 5.

From the theorem, the estimation efficiency can be achieved by considering the common structure between and . We can also establish the consistency for rank and common dimension selection, but it is omitted for brevity.

5 Diverging Eigenvalue Effect

5.1 Diverging eigenvalue and elimination transformation

In many high-dimensional time series data, it is common to observe the diverging eigenvalue effect in : all diagonal entries in are bounded, but the leading eigenvalues of are diverging to infinity with increasing. This phenomenon implies the pervasive cross-sectional dependency and has been well studied in the econometrics literature of factor modeling with common factors and idiosyncratic errors (Bai and Ng,, 2008).

If we model the data with the diverging eigenvalue effect via a VAR(1) model in (1.1), the relationship between and , namely , implies that the diverging eigenvalues of may be splitted into the autoregression part and white noise part. In other words, at least one of the conditional expectation of the response and white noise have strong cross-sectional dependence. Under Assumption 1 for the eigenvalues of , some singular values of are allowed to diverge. However, if is diverging, the estimation error bound in Theorem 2 is , resulting in a much larger sample size requirement. To this end, we propose an elimination transformation to remove the diverging eigenvalue effect in white noise errors.

Remark 4.

For , the diverging singular values exist typically when is pervasive such that the response factor is related to most or even all of the variables, but the predictor loading is highly sparse. For example, consider the rank-1 , where and the nonzero eigenvalue of is 0.9. In this case, the diverging eigenvalues in may come from the pervasive dependence on the conditional expectation of the response; see the empirical evidence in Section 8.

Based on the decomposition in (2.2), is involved in the low-dimensional autoregressive model, and , where such that , is not related to the parameter matrix . Hence, when estimating , it is beneficial to eliminate the diverging eigenvalue effect in and preserve information in to avoid model bias. Suppose has diverging eigenvalues, i.e., , where and contains the diverging and bounded eigenvalues, respectively, and and are the corresponding eigenvectors. The transformation can remove the diverging eigenvalue effect in , since

| (5.1) |

In order to preserve the informative factor loading in when estimating , we consider the -preserved transformation and denote such that

| (5.2) |

If the eigenvalues of are bounded, all eigenvalues of are bounded. In other words, the diverging eigenvalue effects of in can be removed. By the -preseved property of the transformation , we have that . Thus, the reduced-rank VAR model in (2.1) implies that , in which the diverging eigenvalue effects in the white noise innovations are alleviated.

5.2 Estimation methodology

First, the reduced-rank VAR(1) model can be formulated to the factor model in (2.3)

| (5.3) |

where is an -dimensional dynamic factor and is a white noise. Following the literature of factor models with dynamically dependent factors and white noise errors (Lam and Yao,, 2012; Gao and Tsay,, 2022), we consider the autocovariance matrices , for . It follows from (5.3) that , for , where and . For a prespecified integer , define , and is the subspace spanned by the first eigenvectors of . Given , the covariance matrix of is and its first eigenvectors are .

Therefore, we can first obtain the estimates and by calculating the first and last eigenvectors of , respectively, where each sample autocovariance is calculated via . The diverging eigenvalues and the corresponding eigenvectors of can be estimated by the first eigenvalues and eigenvectors of , denoted by and . Then, we can obtain the estimated transformations and , and apply the transformation to obtain . Let the matrix collect all transformed response vectors, and we can use the transformed response and the original predictor in the methods described in Section 3 to complete the estimation procedure.

When the number of factors in (5.3) is unknown, we may use the eigenvalue ridge-type ratios (Xia et al.,, 2015) of to estimate it numerically. To determine the number of diverging eigenvalues , we may also calculate the eigenvalue ridge-type ratios of , or select the diverging eigenvalues based on a threshold for some .

Finally, for the general VAR() model, we can also use the same factor model estimation method to obtain and , and apply the transformed response and the original predictors to the proposed estimation procedure in Section 3.4.

5.3 Theoretical results

In this subsection, we focus on the VAR(1) model, as the results can easily be extended to the general VAR() models. When the singular values of are diverging, the spectral measurements and may be diverging as well. In the setting with diverging eigenvalue effect, representing the cross-sectional and temporal dependency in by the spectral measurements in Section 4 may result in a loose result. As we assume the leading eigenvalues of are diverging, it is more natural to impose the following assumptions on the explicit diverging rates of the specific components in the model.

Assumption 5.

All nonzero singular values of scale as for some .

Assumption 6.

The first eigenvalues of scale as for some . The first eigenvalues of scale as for some , and the other eigenvalues are bounded. In addition, the first eigenvalues of scale as for some .

The term in Assumption 5 characterizes the strength of diverging singular values in . Note that it is possible that but diverges to infinity. However, when , we must have to ensure stationarity. The terms and in Assumption 6 represent the diverging eigenvalue effects of the white noise errors in the response subspace and its orthogonal complement, respectively. The term characterizes the signal strength in the predictor factor . Based on these diverging rates, denote , and as the variants of , and defined in Section 4. These quantities are related to the explicit diverging rates and are more suitable to derive the theory here.

Suppose that the number of diverging eigenvalues are known, we present the theoretical guarantees for the estimation procedures with and used in Algorithm 1.

Theorem 6.

Theorem 6 presents the statistical convergence rate of the proposed estimator for the data with the diverging eigenvalue effect. First, the additional signal strengh condition, , implies that the signal strength in the low-dimensional dynamic part is not weaker than that in the white noise part , such that the proposed factor modeling method can work. Second, if is fixed, the upper bound scales as . If , i.e., the strength of the predictor factors is stronger than the that of white noise errors in , the rate is even faster than that in Theorem 2. Third, if we ignore the diverging effect in the data and apply the standard estimation procedure in Section 3, the resulting rate in Theorem 2, scaling as , can be much larger than that in Theorem 6, which confirms the efficacy of the proposed transformation method in removing the diverging effect. Finally, when , i.e., diverges with , we may also consider the relative estimation error for the estimation consistency of factor loadings.

6 Sparsity on Factor Loading Matrices

The convergence analysis in Sections 4 and 5 requires or ; however, the number of series could be comparable to or even larger than the sample size for some real applications. For this case, the common and specific factors are related to only a small subset of variables, while many other variables have no contribution in extracting factors. Thus, in order to improve the estimation efficiency and model interpretation, it is of interest to further consider additional row-wise sparsity structure to factor loading matrices. If the factor loadings are sparse, it is unlikely to have strong cross-sectional dependence, so in this section, the diverging eigenvalue effect is not considered.

We consider the case of VAR(1) models and the result can be extended to that of general VAR() models. Suppose that there are at most , , and variables related to the common, response-specific, and predictor-specific factors, respectively. Let . We can extend the regularized estimation method in (3.2) to encourage the row-wise sparsity on , , and ,

| (6.1) |

Accordingly, for the row-wise sparsity constraint, the hard thresholding operation can be added to the gradient descent algorithm, where projects the matrix onto by keeping the top largest rows of in terms of Euclidean norm and truncating the rest to zeros; see Algorithm 2. Note that the row-wise sparsity structure is invariant with respect to rotation.

1: Input: , , , , , , , , and sparsity level .

2: for

3: Use lines 3-6 in Algorithm 1 to obtain , , , and

4: , , and

5: end for

6: Return:

For initialization of Algorithm 2, we conduct the regularized least squares estimation . Denote by and the first left and right singular vectors of , respectively, and then the spectral initialization method in Section 3.2 can be used to obtain . Finally we set , , , and . The rank and common dimension can similarly be selected by the proposed methods in Section 3.3. The sparsity level can be determined by the domain knowledge or estimated based on .

Assume that the numbers of nonzero rows in the ground truth , , and are , , and , respectively, and the sparsity levels in Algorithm 2 satisfy that , , and , for some constant .

Theorem 7.

From the above theorem, the estimation efficiency of the sparsity-constrained estimator is improved significantly. Specifically, when both and are much smaller than , the required sample size is reduced from to . In other words, the proposed sparsity-constrained method can be applied to the case with .

7 Simulation Studies

7.1 VAR with common factors

We conduct two simulation experiments to evaluate the finite-sample performance of the proposed estimation methods. The number of replications is set to 500 for each experiment.

In the first experiment, the VAR(1) model in (2.7) is considered with , , and . The dimension is or 100, and we consider for and for . The orthonormal matrices and are generated randomly in each replication such that . Moreover, let with each in each replication. As a result, from (2.1) and (2.7), the parameter matrix assumes the form .

The proposed methodology in Sections 3.1-3.3 is applied to the generated data. The ridge-type ratio method with and is used to select , and BIC in (3.6) is used to select . Table 1 lists the percentages of correct rank and common dimension selection. It can be seen that both can be correctly selected almost for all cases, and the percentages of correct selection in rank and common dimension both increase as the sample size increases. This confirms the selection consistency derived in Section 4.3.

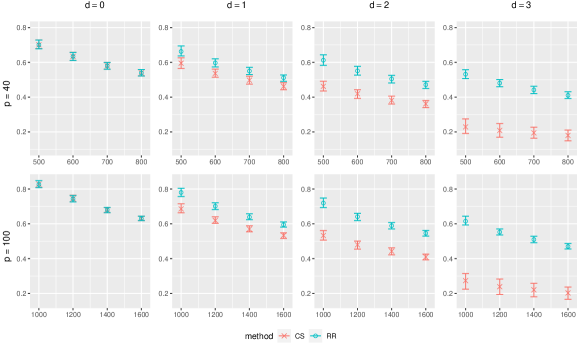

We next compare the estimation efficiency between two models: the proposed model with a common subspace (CS) in (2.7) and the reduced-rank (RR) model in (2.1). The median of estimation errors, , over 500 replications is presented in Figure 1, and the 0.75- and 0.25-th quantiles are also given in terms of error bars. The two models have similar performances when . However, when , the proposed model is more efficient, and the efficiency gain increases as the common dimension becomes larger. This result shows that it pays to explore the common subspace between response and predictor spaces.

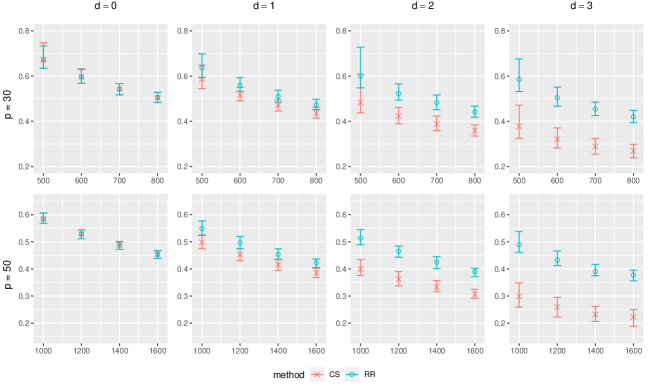

The data generating process of the second experiment is a VAR() model in (2.9) with , and its parameter tensor is in the form of (2.12) with ranks and common dimension . The dimension is or 50, and we consider for and for . We generate the orthonormal matrices, , , , , , and , randomly for each replication. Let be a super-diagonal tensor with diagonal entries , and ’s are generated by the same method as that of the first experiment. The parameter tensor has the form , where . The proposed methodology in Section 3.4 and Appendix D.2 is applied to each generated sample.

Table 2 gives the percentages of correct rank and common dimension selection, respectively, and Figure 2 presents the median, 0.75- and 0.25-th quantiles of estimation errors, , from our model (CS) in (2.12) and the reduced-rank model (RR) in Wang et al., (2022). From Table 2, the percentages of correct rank selection are obviously smaller than those of correct common dimension selection. This is mainly due to the fact that, when tensor ranks are over-selected, the proposed method may still correctly select the common dimension. All other findings are similar to those of the first experiment.

7.2 VAR with diverging eigenvalue effect

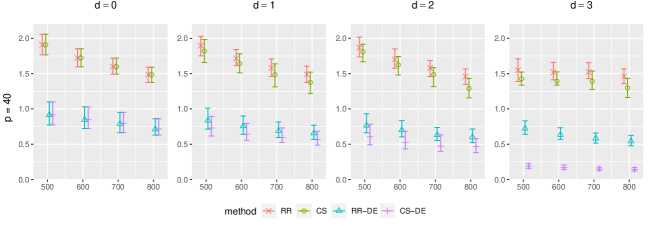

Next, we conduct a simulation experiment to investigate how the diverging eigenvalues may affect the estimation procedure and support the proposed methodology in Section 5. The DGP is the same as the first experiment with , except for , where is the -dimensional vector whose entries are all one. Hence, has one diverging eigenvalue as .

In this experiment, we apply the proposed estimation procedure with diverging eigenvalue effect, including common subspace with diverging eigenvalues (CS-DE) and reduced-rank with diverging eigenvalues (RR-DE), and compare them with the standard versions CS and RR. Table 3 contains the percentages of correct rank and common dimension selection for CS and CS-DE. When has a diverging eigenvalue, the CS method fails to find the correct rank while CS-DE can consistently estimate the rank and common dimension. The estimation errors over 500 replications are presented in Figure 3. In all cases of , the errors of RR-DE and CS-DE are significantly smaller than those of the standard methods. When , the CS-DE performs better than RR-DE, which supports the theoretical results in Section 5.

8 An Empirical Example

We apply the proposed methodology to a macroeconomic time series data set with variables of the United States. The data consist of quarterly economic series from Q3-1959 to Q4-2007 with the length . These macroeconomic variables, selected by Koop, (2013), can be classified into eight categories: GDP decomposition, NAPM indices, industrial production, housing, interest rates, employment, prices, and others. All series have been transformed to stationary series and standardized, and seasonal adjustment has also been conducted to all variables except the financial series. More information of these macroeconomic series can be found in Appendix H.

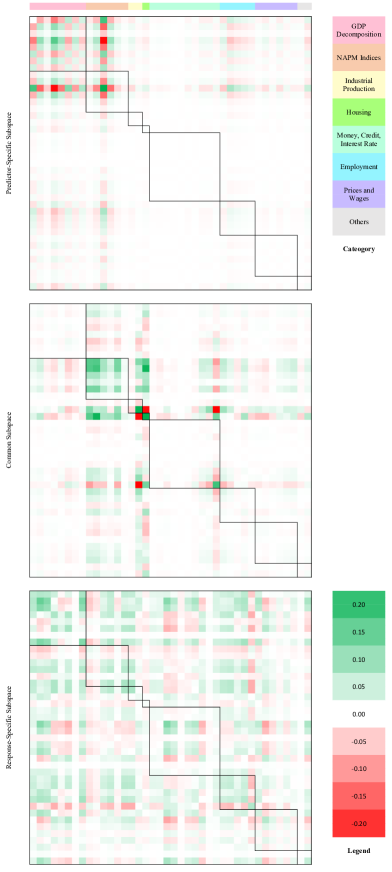

This dataset has been well studied in various factor models, and the largest eigenvalues of the sample covariance matrix is 11.68. Hence, we first apply the factor modeling procedure in Gao and Tsay, (2022), but no diverging eigenvalue in the white noise is found. Following Koop, (2013), we consider a VAR(4) model and the parameter tensor is specified as in (2.12). The modeling procedure in Section 3.4 is applied to the above high-dimensional macroeconomic time series. The estimated ranks are , while the selected common dimension is , i.e., there are two common, two response-specific, and one predictor-specific factors. The singular values of are 8.87, 3.70, 1.15, and 0.56, and the first two singular values can explain the diverging eigenvalue in . For the factor interpretation, since the tensor decomposition in (2.12) is not unique, we standardize the matrices , and to be orthonormal, and calculate their projection matrices , and , which are uniquely defined and can be used to represent the subspaces , , and , respectively; see Section 2 for more details.

Figure 4 plots the calculated projection matrices , and . It can be seen that both and are highly sparse, and these nonzero entries exhibit certain clustering pattern, which is consistent with the classification of macroeconomic variables. Specifically, almost all significant entries in the projection matrix of predictor-specific factors can be observed for the first two categories of variables, GDP decomposition and NAPM indices, while those of common factors are from NAMP indices, industrial production, and housing. We may argue that the three fitted predictor factors mainly extract information from four classes of variables, including GDP, NAPM indices, industrial production and housing, for the sake of predicting the future values of all series. The predictability of these variables is consistent with our empirical experience: GDP is the most important measure of the current status of an economy, and purchasing manager indices, industrial production indices, and housing starts are widely recognized as leading indicators of economic activities. Nevertheless, the estimated response-specific projection matrix is much denser, indicating that almost all economic variables are related to the response-specific factors. The patterns in these projection matrices can also help us interpret the diverging eigenvalues in . Since the response-specific loading is pervasive, strong cross-sectional dependency may exist in the conditional expectation of the response, but the common and predictor-specific factors are only related to a small subset of variables. As discussed in Remark 4, the pervasive response loadings and sparse predictor loadings may lead to the large singular values of .

On the other hand, it is interesting to observe that the upper left corner of the common projection matrix is almost sparse, while those in predictor-specific and response-specific projection matrices are not. We may argue that the information of GDP extracted for predictors and responses are different in general. The GDP components in the responses are positively correlated, as shown in the green upper-left block in the response-specific projection matrix, whereas in the predictor-specific projection matrix, the first variable, real GDP, is negatively correlated to real personal consumption, private domestic investment, real exports, and government consumption and investment. By definition, as the real GDP is the summation of its decomposition, the negative relationship in the predictor subspace partially cancels out the double counting.

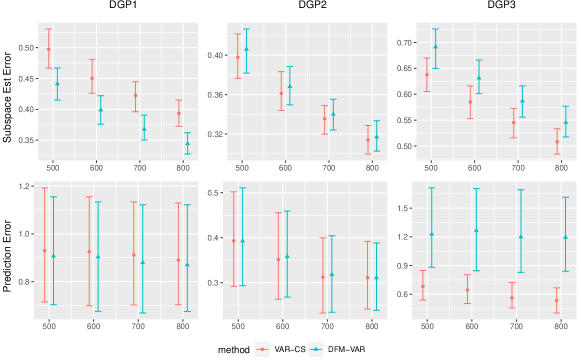

Finally, we compare the proposed model with two other commonly used models, the rank-constrained VAR(4) model (VAR-RR) in Wang et al., (2022) with ranks and the dynamic factor model in Lam and Yao, (2012) with a low-dimensional VAR(4) for factors (DFM-VAR), in terms of rolling forecast. Specifically, from the time point of Q1-2000 () to Q2-2007 (), we fit these three models utilizing all available historical data until time and obtain one-, two- and three-step-ahead forecasts. We consider two forecasting tasks: one is to predict all forty variables, and the other is to only forecast the 34th series, CPI for all items, as the inflation rate is one of the typical macroeconomic variables of interest in forecasting. The average rolling forecast errors for both tasks are summarized in Table 4, and it can be seen that our model has the smallest errors in both tasks, especially the overall forecasting. This is due to the fact that, compared to the dynamic factor modeling, our model is able to flexibly extract useful information for responses and predictors. In the meanwhile, in the proposed model, substantial dimension reduction can be further achieved by exploring the possible common subspace between response and predictor factor spaces of the rank-constrained model. The CPI forecasting errors of both methods are quite close, possibly because CPI is only involved in response-specific factor loading and DFM can also estimate it consistently.

9 Conclusion and Discussion

Vector autoregressive and factor models are two mainstream modeling frameworks for high-dimensional time series, and they have their own strengths in real applications. This article proposed a new model by focusing on the dependent factor structure of the series, and it was shown by simulation experiments and an empirical example that the proposed model enjoys advantages over both VAR and factor models. Theoretical justifications are established for both computational and statistical convergence of the new model.

The research of this article can be extended in two directions. Firstly, heavy-tailed distributions and outliers are commonly observed in empirical data sets, which violates Assumption 2. Robust estimation methods against the heavy-tailed distribution for high-dimensional VAR models have been investigated recently (Wang and Tsay,, 2023), and it is of practical importance to investigate the robust methods for the proposed model. Secondly, inspired by the emerging literature on matrix and tensor-valued time series (Chen et al.,, 2021, 2022; Wang et al.,, 2021), we may generalize the proposed model, methodology, and theory to autoregressive models for matrix and tensor-valued time series.

References

- Bai and Ng, (2002) Bai, J. and Ng, S. (2002). Determining the number of factors in approximate factor models. Econometrica, 70:191–221.

- Bai and Ng, (2008) Bai, J. and Ng, S. (2008). Large dimensional factor analysis. Now Publishers Inc.

- Bańbura et al., (2010) Bańbura, M., Giannone, D., and Reichlin, L. (2010). Large Bayesian vector auto regressions. Journal of Applied Econometrics, 25(1):71–92.

- Basu and Michailidis, (2015) Basu, S. and Michailidis, G. (2015). Regularized estimation in sparse high-dimensional time series models. Annals of Statistics, 43:1535–1567.

- Cai and Zhang, (2018) Cai, T. T. and Zhang, A. (2018). Rate-optimal perturbation bounds for singular subspaces with applications to high-dimensional statistics. Annals of Statistics, 46:60–89.

- Candès and Plan, (2011) Candès, E. J. and Plan, Y. (2011). Tight oracle inequalities for low-rank matrix recovery from a minimal number of noisy random measurements. IEEE Transactions on Information Theory, 57:2342–2359.

- Chen et al., (2021) Chen, R., Xiao, H., and Yang, D. (2021). Autoregressive models for matrix-valued time series. Journal of Econometrics, 222:539–560.

- Chen et al., (2022) Chen, R., Yang, D., and Zhang, C.-H. (2022). Factor models for high-dimensional tensor time series. Journal of the American Statistical Association, 117:94–116.

- Chi et al., (2019) Chi, Y., Lu, Y. M., and Chen, Y. (2019). Nonconvex optimization meets low-rank matrix factorization: An overview. IEEE Transactions on Signal Processing, 67:5239–5269.

- De Lathauwer et al., (2000) De Lathauwer, L., De Moor, B., and Vandewalle, J. (2000). A multilinear singular value decomposition. SIAM Journal on Matrix Analysis and Applications, 21:1253–1278.

- Dowell and Pinson, (2016) Dowell, J. and Pinson, P. (2016). Very-short-term probabilistic wind power forecasts by sparse vector autoregression. IEEE Transactions on Smart Grid, 7:763–770.

- Forni et al., (2000) Forni, M., Hallin, M., Lippi, M., and Reichlin, L. (2000). The generalized dynamic-factor model: Identification and estimation. Review of Economics and Statistics, 82:540–554.

- Forni et al., (2005) Forni, M., Hallin, M., Lippi, M., and Reichlin, L. (2005). The generalized dynamic factor model: one-sided estimation and forecasting. Journal of the American Statistical Association, 100:830–840.

- Gao and Tsay, (2022) Gao, Z. and Tsay, R. S. (2022). Modeling high-dimensional time series: a factor model with dynamically dependent factors and diverging eigenvalues. Journal of the American Statistical Association, 117:1398–1414.

- Ghosh et al., (2019) Ghosh, S., Khare, K., and Michailidis, G. (2019). High-dimensional posterior consistency in Bayesian vector autoregressive models. Journal of the American Statistical Association, 114:735–748.

- Ghosh et al., (2021) Ghosh, S., Khare, K., and Michailidis, G. (2021). Strong selection consistency of Bayesian vector autoregressive models based on a pseudo-likelihood approach. Annals of Statistics, 49:1267–1299.

- Gorrostieta et al., (2012) Gorrostieta, C., Ombao, H., Bédard, P., and Sanes, J. N. (2012). Investigating brain connectivity using mixed effects vector autoregressive models. Neuroimage, 59:3347–3355.

- Guo et al., (2016) Guo, S., Wang, Y., and Yao, Q. (2016). High-dimensional and banded vector autoregressions. Biometrika, 103:889–903.

- Hallin and Lippi, (2013) Hallin, M. and Lippi, M. (2013). Factor models in high-dimensional time series: A time-domain approach. Stochastic Processes and their Applications, 123:2678–2695.

- Han et al., (2015) Han, F., Lu, H., and Liu, H. (2015). A direct estimation of high dimensional stationary vector autoregressions. Journal of Machine Learning Research, 16:3115–3150.

- Han et al., (2021) Han, R., Willett, R., and Zhang, A. (2021). An optimal statistical and computational framework for generalized tensor estimation. Annals of Statistics, 50:1–29.

- Jain and Kar, (2017) Jain, P. and Kar, P. (2017). Non-convex optimization for machine learning. Foundations and Trends® in Machine Learning, 10:142–336.

- Kolda and Bader, (2009) Kolda, T. G. and Bader, B. W. (2009). Tensor decompositions and applications. SIAM Review, 51:455–500.

- Koop, (2013) Koop, G. M. (2013). Forecasting with medium and large Bayesian VARs. Journal of Applied Econometrics, 28:177–203.

- Korobilis, (2013) Korobilis, D. (2013). VAR forecasting using Bayesian variable selection. Journal of Applied Econometrics, 28:204–230.

- Lam and Yao, (2012) Lam, C. and Yao, Q. (2012). Factor modeling for high-dimensional time series: Inference for the number of factors. Annals of Statistics, 40:694–726.

- Lam et al., (2011) Lam, C., Yao, Q., and Bathia, N. (2011). Estimation of latent factors for high-dimensional time series. Biometrika, 98:901–918.

- Li et al., (2016) Li, X., Arora, R., Liu, H., Haupt, J., and Zhao, T. (2016). Nonconvex sparse learning via stochastic optimization with progressive variance reduction. arXiv preprint arXiv:1605.02711.

- Li et al., (2019) Li, Z., Lam, C., Yao, J., and Yao, Q. (2019). On testing for high-dimensional white noise. Annals of Statistics, 47:3382–3412.

- Mirsky, (1960) Mirsky, L. (1960). Symmetric gauge functions and unitarily invariant norms. The Quarterly Journal of Mathematics, 11:50–59.

- Negahban and Wainwright, (2011) Negahban, S. and Wainwright, M. J. (2011). Estimation of (near) low-rank matrices with noise and high-dimensional scaling. Annals of Statistics, 39:1069–1097.

- Nesterov, (2003) Nesterov, Y. (2003). Introductory lectures on convex optimization: A basic course, volume 87. Springer Science & Business Media.

- Peña and Box, (1987) Peña, D. and Box, G. E. (1987). Identifying a simplifying structure in time series. Journal of the American statistical Association, 82:836–843.

- Peña and Tsay, (2021) Peña, D. and Tsay, R. S. (2021). Statistical learning for big dependent data. John Wiley & Sons, New Jersey.

- Stock and Watson, (2009) Stock, J. H. and Watson, M. (2009). Forecasting in dynamic factor models subject to structural instability. The Methodology and Practice of Econometrics. A Festschrift in Honour of David F. Hendry, 173:205.

- Stock and Watson, (2002) Stock, J. H. and Watson, M. W. (2002). Forecasting using principal components from a large number of predictors. Journal of the American Statistical Association, 97:1167–1179.

- Tsay, (2014) Tsay, R. S. (2014). Multivariate time series analysis: with R and financial applications. John Wiley & Sons, Hoboken, New Jersey.

- Tsay, (2020) Tsay, R. S. (2020). Testing serial correlations in high-dimensional time series via extreme value theory. Journal of Econometrics, 216:106–117.

- Tucker, (1966) Tucker, L. R. (1966). Some mathematical notes on three-mode factor analysis. Psychometrika, 31:279–311.

- Velu and Reinsel, (2013) Velu, R. and Reinsel, G. C. (2013). Multivariate reduced-rank regression: theory and applications, volume 136. Springer Science & Business Media.

- Vershynin, (2018) Vershynin, R. (2018). High-dimensional probability: An introduction with applications in data science, volume 47. Cambridge university press.

- Wainwright, (2019) Wainwright, M. J. (2019). High-dimensional statistics: A non-asymptotic viewpoint. Cambridge University Press.

- Wang et al., (2020) Wang, D., Huang, F., Zhao, J., Li, G., and Tian, G. (2020). Compact autoregressive network. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 34, pages 6145–6152.

- Wang and Tsay, (2023) Wang, D. and Tsay, R. S. (2023). Rate-optimal robust estimation of high-dimensional vector autoregressive models. Annals of Statistics. To appear.

- Wang et al., (2021) Wang, D., Zheng, Y., and Li, G. (2021). High-dimensional low-rank tensor autoregressive time series modeling. arXiv preprint arXiv:2101.04276.

- Wang et al., (2022) Wang, D., Zheng, Y., Lian, H., and Li, G. (2022). High-dimensional vector autoregressive time series modeling via tensor decomposition. Journal of the American Statistical Association, 117:1338–1356.

- Xia et al., (2015) Xia, Q., Xu, W., and Zhu, L. (2015). Consistently determining the number of factors in multivariate volatility modelling. Statistica Sinica, 25:1025–1044.

- Yu et al., (2015) Yu, Y., Wang, T., and Samworth, R. J. (2015). A useful variant of the davis–kahan theorem for statisticians. Biometrika, 102:315–323.

- Zhu et al., (2017) Zhu, X., Pan, R., Li, G., Liu, Y., and Wang, H. (2017). Network vector autoregression. Annals of Statistics, 45:1096–1123.

| Rank selection | Common dimension selection | ||||||||

| 0 | 1 | 2 | 3 | 0 | 1 | 2 | 3 | ||

| dimension | |||||||||

| 97.8 | 97.2 | 96.2 | 98.4 | 98.6 | 97.6 | 95.8 | 98.4 | ||

| 600 | 99.8 | 99.6 | 98.6 | 99.8 | 99.4 | 98.8 | 98.4 | 99.8 | |

| 700 | 99.8 | 99.8 | 99.8 | 100 | 100 | 99.8 | 99.8 | 100 | |

| 800 | 99.8 | 100 | 100 | 100 | 100 | 100 | 99.8 | 99.8 | |

| dimension | |||||||||

| 94.8 | 92.4 | 92.2 | 93.0 | 93.4 | 91.8 | 85.8 | 93.0 | ||

| 1200 | 96.6 | 96.6 | 95.8 | 98.0 | 98.4 | 95.8 | 95.6 | 98.0 | |

| 1400 | 99.0 | 99.4 | 97.8 | 99.6 | 99.8 | 99.2 | 97.6 | 99.2 | |

| 1600 | 99.4 | 98.6 | 98.8 | 99.8 | 100 | 98.6 | 98.8 | 99.8 | |

| Rank selection | Common dimension selection | ||||||||

| 0 | 1 | 2 | 3 | 0 | 1 | 2 | 3 | ||

| dimension | |||||||||

| 76.6 | 75.6 | 71.4 | 68.8 | 89.0 | 87.0 | 77.6 | 80.4 | ||

| 600 | 88.0 | 89.4 | 88.4 | 84.8 | 96.6 | 94.4 | 92.0 | 90.6 | |

| 700 | 97.6 | 94.8 | 93.6 | 91.6 | 98.6 | 97.4 | 95.0 | 94.4 | |

| 800 | 98.0 | 97.4 | 98.2 | 97.2 | 99.2 | 99.0 | 98.6 | 98.4 | |

| dimension | |||||||||

| 94.6 | 91.6 | 94.6 | 86.8 | 98.2 | 96.0 | 95.8 | 90.8 | ||

| 1200 | 98.2 | 97.4 | 97.4 | 98.2 | 99.2 | 98.2 | 98.4 | 99.0 | |

| 1400 | 99.0 | 99.6 | 99.2 | 99.8 | 99.8 | 99.8 | 99.6 | 99.8 | |

| 1600 | 99.8 | 100 | 99.8 | 100 | 100 | 100 | 100 | 100 | |

| Rank selection | Common dimension selection | ||||||||

| 0 | 1 | 2 | 3 | 0 | 1 | 2 | 3 | ||

| Method: CS | |||||||||

| 0.4 | 0.2 | 0.0 | 0.0 | 100 | 76.0 | 73.8 | 49.6 | ||

| 600 | 0.2 | 0.0 | 0.2 | 0.0 | 100 | 78.0 | 76.6 | 66.4 | |

| 700 | 0.8 | 0.2 | 0.0 | 0.0 | 100 | 80.6 | 84.8 | 84.4 | |

| 800 | 1.2 | 0.4 | 1.6 | 0.0 | 99.8 | 88.6 | 83.2 | 89.4 | |

| Method: CS-DE | |||||||||

| 99.6 | 98.8 | 97.8 | 99.4 | 100 | 84.2 | 84.8 | 81.6 | ||

| 600 | 99.4 | 99.8 | 98.8 | 99.8 | 100 | 85.0 | 84.4 | 82.8 | |

| 700 | 99.8 | 99.4 | 98.8 | 100 | 100 | 84.2 | 86.6 | 89.8 | |

| 800 | 100 | 99.6 | 98.2 | 100 | 100 | 86.8 | 89.0 | 90.4 | |

| Model | Overall forecast | CPI forecast | |||||

|---|---|---|---|---|---|---|---|

| One-step | Two-step | Three-step | One-step | Two-step | Three-step | ||

| VAR-CS | 4.889 | 5.156 | 5.254 | 0.958 | 0.929 | 0.967 | |

| VAR-RR | 5.622 | 5.702 | 5.593 | 1.087 | 1.006 | 1.019 | |

| DFM-VAR | 5.104 | 5.283 | 5.330 | 0.967 | 0.997 | 0.980 | |

lemmasection \AtAppendixdefinitionsection

Appendix A Computational convergence analysis of gradient descent

In this appendix, we present the proof of Theorem 1 and necessary lemmas for the deterministic convergence analysis.

A.1 Proof of Theorem 1

Proof.

The proof consists of five steps. In the first step, we introduce some notations and conditions essential to the convergence analysis. In the second to fourth steps, we provide a deterministic convergence result for the iterates, given that some regulatory conditions are satisfied. Finally, in the last step, we show that these regulatory conditions hold iteratively.

Step 1. (Notations and conditions)

We begin by introducing some notations and conditions for the convergence analysis.

Denote the empirical least squares loss function as

| (A.1) |

As the matrix decomposition is not unique, for the iterate at the step , define the combined estimation errors of up to the optimal rotations as

| (A.2) |

and the corresponding optimal rotations as . For simplicity in presentation, denote and .

By Definition 1, for the given sample size , is restricted strongly convex (RSC) with parameter and restricted strongly smooth (RSS) with parameter , such that for any rank- matrices ,

| (A.3) |

The -RSC condition implies that

| (A.4) |

and as in Nesterov, (2003), the convexity and -RSS condition jointly imply that

| (A.5) |

Combining these two inequalities, we have that

| (A.6) |

which is also known as the restricted correlated gradient condition in Han et al., (2021). Moreover, by definition, we immediately have that .

In addition, by Definition 2, we assume that given the sample,

| (A.7) |

For simplicity, we assume and , and the proof can readily be extended to the case with . Before starting the proof, we also assume that the following conditions hold and will verify them in the last step. For any , we assume that

| (A.8) |

which obviously implies that

| (A.9) |

Note that the constant 1.1 can be replaced by any arbitrary constant greater than 1. In addition, we assume that for any , .

Step 2. (Upper bound of )

By definition,

| (A.10) |

Step 2.1. ( and steps)

By definition, . Thus, we have

| (A.11) |

First, for the second term in the right hand side of (A.11), by Cauchy’s inequality,

| (A.12) |

where the first term can be bounded by mean inequality

| (A.13) |

By the duality of the Frobenius norm, we have

| (A.14) |

and the first term can be bounded as

| (A.15) |

the second term can be bounded as

| (A.16) |

and the third term can be bounded as

| (A.17) |

Thus, we have

| (A.18) |

For the fourth and fifth terms in (A.11), denote

| (A.20) |

Therefore, we can rewrite the last three terms in (A.11) as

| (A.21) |

Combining the bounds for the terms in (A.11), we have

| (A.22) |

Similarly, for , we can define similar quantities and , and show that

| (A.23) |

Step 2.2. ( step)

For , note that

| (A.24) |

Thus, we have

| (A.25) |

where

| (A.26) |

First, we have

| (A.27) |

where the first term can be bounded as

| (A.28) |

and the other three terms can be bounded as

| (A.29) |

| (A.30) |

| (A.31) |

Thus, the second term in (A.25) can be bounded as

| (A.32) |

For the third term in (A.25),

| (A.33) |

For the fourth and fifth terms in (A.25), denote

| (A.34) |

Step 2.3. ( step)

For , we consider the following decomposition

| (A.37) |

For the third term, we have

| (A.38) |

In addition,

| (A.39) |

Hence, we have

| (A.40) |

Together, we have that

| (A.41) |

Step 3. (Lower bound of )

In the third step, we develop a lower bound for . By definition,

| (A.42) |

Note that

| (A.43) |

where

| (A.44) |

By Lemma 1, since , , , and , we can derive an upper bound for ,

| (A.45) |

By the -RSC and -RSS conditions, the first term on the right hand side of (A.42) can be bounded as

| (A.46) |

In addition, we have that for any

| (A.47) |

and

| (A.48) |

for any . Combining these inequalities, we have

| (A.49) |

Applying Lemma 2 with , we can obtain an upper bound for ,

| (A.50) |

For the second term on the right-hand side of (A.42), note that

| (A.51) |

Denote and . Note that

| (A.52) |

In addition, by the fact that and , we have

| (A.53) |

and

| (A.54) |

Therefore, we have

| (A.55) |

Combining these inequalities, and since ,

| (A.56) |

Letting and since

| (A.57) |

Step 4. (Convergence analysis of )

In the following, we combine all the results in the previous steps to establish the error bound for and . Plugging in and to , , and , we have

| (A.58) |

Combining the upper bound for and the lower bound for , we have

| (A.59) |

Letting , with , since , the coefficients of the second, third, and fourth term in (A.59) are

| (A.60) |

| (A.61) |

and

| (A.62) |

as , and . Therefore, we can derive the following recursive inequality

| (A.63) |

By induction, we have that for any ,

| (A.64) |

For the error bound of , by Lemma 2,

| (A.65) |

Step 5. (Verification of conditions)

Finally, we show that conditions and (A.8) hold.

Since and , by Lemma 2 and initialization bound , we have

| (A.66) |

Based on the recursive relationship in (A.63), by induction it is easy to check that for all . In other words, as and , we have for all , which further implies that

| (A.67) |

and

| (A.68) |

which completes the deterministic analysis.

∎

A.2 Auxiliary lemmas

The first lemma follows from Lemma E.3 in Han et al., (2021) with the tensor order changed from 3 to 2.

Lemma 1.

Suppose that , with , , , , , , and . Let

| (A.69) |

Then, defining

| (A.70) |

we have

| (A.71) |

where

| (A.72) |

Proof.

Since , we have

| (A.73) |

For , since and , we have

| (A.74) |

where . For , we have

| (A.75) |

where . Hence, and

| (A.76) |

∎

The following lemma shares similar ideas and techniques as those of Lemma E.2 in Han et al., (2021) with the common subspace structure included.

Lemma 2.

Suppose that , , , , and . Let with , and for some constant . Define

| (A.77) |

Then, we have

| (A.78) |

and

| (A.79) |

where .

Proof.

Denote and . Note that . We have the decomposition

| (A.80) |

By mean inequality,

| (A.81) |

Hence, it follows that

| (A.82) |

where .

Let be the SVD of . Then, we have

| (A.83) |

Similarly to Lemma E.2 in Han et al., (2021), we have

| (A.84) |

Let be the perpendicular orthonormal matrix of . As and are orthonormal matrices spanning left singular subspaces of and , we have

| (A.85) |

By Lemma 1 in Cai and Zhang, (2018),

| (A.86) |

These imply that

| (A.87) |

For the second inequality, denote the optimal rotation matrices by

| (A.88) |

Let , , and . Then,

| (A.89) |

and

| (A.90) |

Hence,

| (A.91) |

∎

Appendix B Statistical convergence analysis of gradient descent

In this appendix, we present the stochastic properties of the time series data.

Proof of Theorem 2.

The proof of Theorem 2 consists of two steps. In the first step, we show that the RSC, RSS and deviation bound conditions defined in the deterministic computational convergence analysis hold with high probability, and proofs of these conditions are presented in Appendix B.1. Given these regularity conditions, it suffices to show the statistical properties of the initial values, which will be discussed in Appendix B.2.

By Lemmas 3 and 4, with probability at least , the empirical loss function satisfies the RSC- and RSS- conditions, and

| (B.1) |

By Theorem 1, we have that, for all ,

| (B.2) |

Hence, when

| (B.3) |

the statistical error will absorb the optimization error, so

| (B.4) |

Moreover, by Lemma 6, with probability at least ,

| (B.5) |

Combining these results, we have that when

| (B.6) |

with probability at least ,

| (B.7) |

∎

B.1 Proofs of RSC, RSS and deviation bound

We first prove the restricted strong convexity (RSC) and restricted strong smoothness (RSS) conditions. For the least squares loss function , it is easy to check that for any ,

| (B.8) |

Lemma 3.

Assume the conditions in Theorem 2 hold. Suppose that . For any rank- matrix , with probability at least ,

| (B.9) |

where and .

Proof of Lemma 3.

For any , denote . Note that .

Based on the moving average representation of VAR(1), we can rewrite as a VMA() process,

| (B.10) |

Let , , and . Note that , where is defined as

| (B.11) |

Then, we have

| (B.12) |

where

| (B.13) |

Thus, .

As , by the sub-multiplicative property of the Frobenius norm and operator norm, we have

| (B.14) |

and

| (B.15) |

For any and any , by Hanson-Wright inequality,

| (B.16) |

Considering an -covering net of , by Lemma 9, we can easily construct the union bound for ,

| (B.17) |

Letting , for , we have

| (B.18) |

where .

Therefore, with probability at least ,

| (B.19) |

Similarly, and . Additionally, the upper bound in (B.18) can easily be expanded to , and the upper bound of follows.

Finally, since is related to the VMA() process, by the spectral measure of ARMA process discussed in Basu and Michailidis, (2015), we may replace and with and , respectively.

∎

We next prove the deviation bound for . For the least squares loss function , it is clear that

| (B.20) |

Lemma 4.

Proof of Lemma 4.

Denote . By definition,

| (B.22) |

First, we consider an -net for . For any matrix , there exists a matrix such that . Obviously, is a rank- matrix with common dimension . Based on the SVD of , we can split the first pairs of left and right singular vectors into two equal-size groups such that the dimension of left and right singular vectors is in each group. By the splitting of SVD, we can write , where both and are rank- matrix with common dimension and .

By Cauchy’s inequality, as , we have . Moreover, since ,

| (B.23) |

which implies that

| (B.24) |

Next, for any fixed such that , , and we denote and , for . Similar to Wang et al., (2021), by the standard Chernoff bound, for any and ,

| (B.25) |

Similar to Lemma 3, with probability at least ,

| (B.26) |

Therefore, for any ,

| (B.27) |

By Lemma 8, . Thus, if we take and , when , we have

| (B.28) |

Finally, by the spectral measure of ARMA processes, we can replace with .

∎

B.2 Properties of initial value

We present some statistical properties of the initial value of the gradient descent algorithm, the reduced-rank estimator and the corresponding , , , and . Consider the reduced-rank estimator

| (B.29) |

where contains the leading eigenvectors of .

Proof.

Denote , then by the optimality of the reduced-rank estimator

| (B.31) |

Since the rank of both and is , is at most rank . Denote the set of matrices . Then, we have

| (B.32) |

By Lemma 4, with probability at least ,

| (B.35) |

Combining these results, we have that with probability at least ,

| (B.36) |

∎

Next, we derive the estimation error rate for the resulting initial estimator , , , and .

Proof.

Throughout this proof, we assume that the true values , and satisfy that and .

We begin with the rate of and . Based on Lemma 5, we have that . By Lemma 11, we have that

| (B.38) |

and

| (B.39) |

By triangle inequality,

| (B.40) |

For , by triangle inequality,

| (B.43) |

Denote

| (B.46) |

and let and . For and ,

| (B.47) |

In summary, when , we have that

| (B.48) |

B.3 Auxiliary lemmas

We first present a deviation bound inequality for the quadratic term . This is Lemma 6 in Wang et al., (2021)

Lemma 7.

For any such that and any ,

| (B.50) |

where is defined as

| (B.51) |

The following lemma is the covering number of . The proof essentially follows that of the Lemma 3.1 in Candès and Plan, (2011).

Lemma 8.

Let be an -net of , where . Then

| (B.52) |

Proof.

For any , where and , we construct an -net for by covering the set of , , , and .

By Lemma 9, we take to be an -net for with .

Next, to cover , we consider the norm, defined as

| (B.53) |

where is the -th column of . Let . It can be easily checked that , and thus an -net for obeying .

Denote and we have

| (B.54) |

It suffices to show that for any , there exists a such that .

For any fixed , decompose it as . Then, there exist satisfying that , , , and . This gives

| (B.55) |

∎

The next lemma is the covering number of the -dimensional unit sphere, which follows directly from Corollary 4.2.13 of Vershynin, (2018).

Lemma 9.

Let be an -net of the unit sphere , where . Then,

| (B.56) |

The following two lemmas are variants of the Davis-Kahan theorem for eigenvector perturbation for symmetric matrices and singular vector perturbation for generic matrices. These results are Theorems 2 and 4 in Yu et al., (2015). To make the proof self-contained, they are presented below.

Lemma 10.

Let , be symmetric, with eigenvalues and , respectively. Fix and assume that , where and . Let , and let and contain the eigenvectors corresponding to the eigenvalues. Then

| (B.57) |

Lemma 11.

Let , have singular values and , respectively. Fix and assume that , where and . Let , and let and contain the right singular vectors. Then,

| (B.58) |

Appendix C Determination of rank and common dimension

We start from the proof of rank selection consistency in Theorem 3.

Proof of Theorem 3.

Following the proof of Lemma 5, if , then with probability approaching one,

| (C.1) |

Obviously, . By definition,

| (C.2) |

By Mirsky’s singular value inequality (Mirsky,, 1960),

| (C.3) |

As the norm of any vector is smaller than the norm, it follows the same upper bound

| (C.4) |

For any , note that . For , and , provided that . Hence, is the dominating term in , when . When , as , and .

Hence, for , as ,

| (C.5) |

For ,

| (C.6) |

For ,

| (C.7) |

∎

Next, we prove the common dimension selection consistency of the BIC.

Proof of Theorem 4.

To show the consistency of common dimension selection via BIC, it suffices to show that

| (C.8) |

Consider the under-parameterized case first. Note that

| (C.9) |

and

| (C.10) |

Thus, by for , we have

| (C.11) |

and it follows that , as , provided that .

For the cases , using the similar arguments in the proof of Theorem 2, we can show that . It follows that

| (C.12) |

which implies that , since as .

∎

Appendix D Supplementary materials for VAR() models

Appendix D presents the supplementary materials of modeling, estimation and theory for the VAR(). It begins with some preliminaries of tensor notation and tensor operation.

D.1 Some basics of tensor algebra

We follow the notations in Kolda and Bader, (2009) to denote tensors of order three or higher by Euler script boldface letters, e.g., . For a generic -th order tensor , denote its elements by and unfolding of along the -mode by , where the columns of are the -mode vectors of , for . The Frobenius norm of a tensor is defined as . The mode- multiplication of a tensor and a matrix is defined as

| (D.1) |

for , respectively.

The tensor ranks considered in this paper are defined as the matrix ranks of the unfoldings of along all modes, namely , for . If the tensor ranks of are , where , there exists a tensor and matrices , such that

| (D.2) |

which is well known as Tucker decomposition (Tucker,, 1966). With the Tucker decomposition, the -mode unfolding of can be written as

| (D.3) |

where denotes the Kronecker product for matrices.