Department of Computer Science

Investigating transactions in cryptocurrencies

Abstract

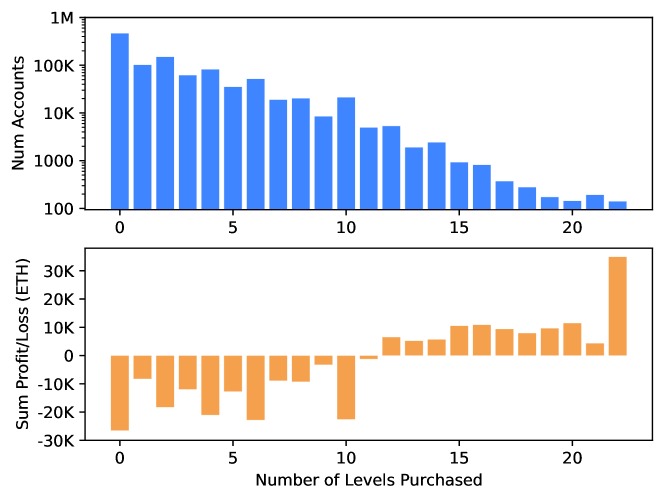

This thesis presents techniques to investigate transactions in uncharted cryptocurrencies and services. Cryptocurrencies are used to securely send payments online. Payments via the first cryptocurrency, Bitcoin, use pseudonymous addresses that have limited privacy and anonymity guarantees. Research has shown that this pseudonymity can be broken, allowing users to be tracked using clustering and tagging heuristics. Such tracking allows crimes to be investigated. If a user has coins stolen, investigators can track addresses to identify the destination of the coins. This, combined with an explosion in the popularity of blockchain, has led to a vast increase in new coins and services. These offer new features ranging from coins focused on increased anonymity to scams shrouded as smart contracts. In this study, we investigated the extent to which transaction privacy has improved and whether users can still be tracked in these new ecosystems. We began by analysing the privacy-focused coin Zcash, a Bitcoin-forked cryptocurrency, that is considered to have strong anonymity properties due to its background in cryptographic research. We revealed that the user anonymity set can be considerably reduced using heuristics based on usage patterns. Next, we analysed cross-chain transactions collected from the exchange ShapeShift, revealing that users can be tracked as they move across different ledgers. Finally, we present a measurement study on the smart-contract pyramid scheme Forsage, a scam that cycled $267 million USD (of Ethereum) within its first year, showing that at least 88% of the participants in the scheme suffered a loss. The significance of this study is the revelation that users can be tracked in newer cryptocurrencies and services by using our new heuristics, which informs those conducting investigations and developing these technologies.

The work presented in this thesis is intended to inform those conducting cryptocurrency investigations and may facilitate the design and development of projects within distributed ledger ecosystems, particularly with respect to privacy and security.

The work shown in Chapter 4 was responsibly disclosed to the founders of Zcash, who responded with updated privacy recommendations and best practices for users [150, 157]. It was covered by multiple media outlets [38, 50, 21, 1] and is mentioned in the later revisions of the Zcash protocol specification [69].

The work in Chapter 5 was responsibly disclosed to ShapeShift and was covered by the MIT Technology Review[111]. The work introduces new tracing heuristics and highlights criminal activity with case studies. These heuristics can be applied not just to ShapeShift, but to platforms which offer cross-currency trading. Weeks before we published the research, The Wall Street Journal published an investigation into ShapeShift which paralleled our work [132], and which was responded to by ShapeShift’s CEO[45]. When the work was originally published, the ShapeShift exchange did not have a Know-Your-Customer (KYC)/Anti-money laundering policy, however this has since been introduced.

The analysis in Chapter 6 will inform those investigating cryptocurrency scams. The work presents a multi-angled analysis of a large pyramid scheme operating on the Ethereum cryptocurrency. Since publication, we have been contacted by a law enforcement investigator requesting advice on how to proceed with active investigations on similar scams.

All the work published in this thesis has been uploaded to open conference proceedings and open access repositories. As of November 27, 2021 the work in this thesis had over 147 citations. The relevant source code for each project has been shared publicly to Github [githubsourcecode]. Talks at each of the conference proceedings are freely available to view online. This will facilitate impact for those researching into improving privacy and combatting scams in distributed ledgers.

Acknowledgements.

This thesis would not have been possible without support from my primary supervisor, Professor Sarah Meiklejohn. Since our first run-in at Euston Station, there was never a discussion where I was not left with increased motivation and knowledge. I am truly indebted for all the support. A special thanks to my closest collaborator, George Kappos. I have been privileged to work with many across the globe and would also like to thank all of my co-authors and contributors (in alphabetical order): Sarah Allen, Sarah Azouvi, Ben Steer, Sergi Delgado-Segura, Bernhard Haslhofer, Alex Hicks, Ari Juels, Sanket Kanjalkar, Tyler Kell, Mary Maller, Andrew Miller, Ania Piotrowska, Pierre Reibel, Sofia Rollet and Rainer Stuetz. This research was funded with a PhD scholarship which I would like to thank the European Commission and The Initiative For Cryptocurrencies & Contracts (IC3) for providing. Finally, I would like to especially thank my parents, Farzana and Muhammad Yousaf, for keeping my stomach full, my head dry and letting me skip years of chores in the name of science. Without their support, I would not have come this far. It is true when they say that no one is self-made.Chapter 1 Introduction

Bitcoin alleviates the problems of centralisation and censorship within a financial system. Anyone has the freedom to create a cryptocurrency wallet and have coins sent to them, simply by providing their public key. No user identification, passport or verification is needed to create such a wallet. This bypasses traditional financial Know Your Customer (KYC) principles, which inform a set of rules used by financial services in order to identify users prior to conducting business, and thereby anticipate and prevent crime. With this freedom, coins can be freely sent to any address without discrimination and free from censorship. These coins cannot be returned or reversed (unless the new owner explicitly does so). By default the system offers pseudonymity, as mentioned in the Bitcoin white paper, transaction privacy is supposedly preserved [106].

Notably, users in oppressed circumstances can purchase and freely send coins without the fear of banks or governments impeding the transaction, and have done so with Bitcoin [13, 123]. There is no risk from hyper-inflation as there is only a fixed number of mintable coins. Donations to charitable organisations can be made without the sender revealing who they are [16, 74]. However, such a system has flaws, and some may argue that those flaws are within its pseudonymity, which allows users to obscure their identity.

For some, this acts as a layer of privacy, preventing their financial transactions from being monitored. For others, this acts as a shroud which allows them to conceal their crimes, such as stealing coins or selling illegitimate goods. Such crimes may need to be investigated. For example, a victim wants to track coins stolen from them to discover if they were sent to an exchange, in the hopes of identifying the criminal and collecting their funds. However, if KYC has not been adopted by that particular exchange, it is much more difficult to discover the identity of the criminal. Alternatively, cryptocurrency exchanges may want to ensure the coins they accept from users were neither stolen nor gained nefariously. These instances, amongst many others, illustrate the need to be able to track coins.

Scientific research has shown that Bitcoin is not private, and entities can be identified and tracked through the use of clustering and wallet identification techniques [95, 63, 108, 121]. This, combined with the openness of the Bitcoin source code, has inspired others to create so called privacy coins. Privacy coins are alternative cryptocurrencies to Bitcoin which improve the underlying user privacy with new features. For example: Zcash has introduced the notion of a shielded pool which uses zero-knowledge proofs to obscure the properties of transactions [156]; Dash uses Coinjoins (as PrivateSpend) which allows users to perform transactions together, to make it difficult to identify which sender paid which recipient [41, 91]; and Monero uses ring signatures to create mix-ins allowing users to include keys of other users within their own transaction to increase their anonymity set [101, 107].

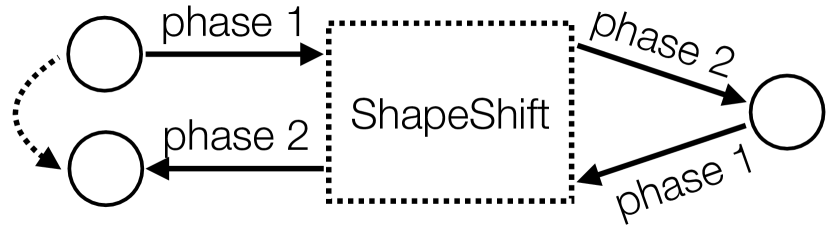

Parallel to privacy coins, the ecosystem has seen an introduction in companies allowing users to freely trade between different coins. July 2014 saw the announcement of cryptocurrency exchange ShapeShift, a service that allowed users to trade coins across different cryptocurrency ledgers without the need for KYC. The service officially launched in 2015, and for the first three years operated without any identity checks, until forced to do so by regulators [147]. In 2017, the Wannacry ransomware hackers reportedly used ShapeShift to move their illicitly acquired cryptocurrencies [42].

With respect to privacy coins, one should also ask whether the claims by the developers of these hold true. Given the avenue for cross-currency trading and potential for crime, one must ask whether cross-currency trading has any affect on user privacy.

The advancements of cryptocurrency technology has resulted in an increase in new coins and services in the ecosystem. As of June 15, 2021, CoinMarketCap lists over 10,000 different cryptocurrencies [39]. Given these opportunities, criminals are quick to exploit new technologies to scam those who are not as technologically literate. For example, Bitconnect, a ponzi scheme, was introduced in 2016 and sold a blockchain-based coin that claimed to offer a high rate of return [49, 72]. The scheme was ultimately closed after regulators ruled that it was a scam, causing the value of the coin to tumble by 92% [4]. Similarly Wotoken, a ponzi scheme claiming large profits due to advanced trading bots, raised over $1.1 billion USD before being shutdown by law enforcement [61]. As scams continue to appear, it becomes important to understand the magnitude and dynamics of these schemes.

In this thesis, we empirically analyse transactions in new cryptocurrencies and services. We investigate transaction privacy on the blockchain by empirically measuring the privacy coin Zcash, developing strategies to trace coins on the cross-trading service ShapeShift, and reveal the scale of a modern day smart-contract pyramid scheme, Forsage. We question whether coins offer the privacy they promise and, if not, what techniques can be introduced to defeat them.

1.1 Scope and Contributions

Our study analysed public transactions that occurred on-chain within the public ledger. Off-chain privacy, for example in software such as the lightning network [117] (an off-chain payment protocol), has been implemented but was beyond the scope of this research. At the start of this study there was no evidence of any published techniques that analysed Zcash [79], cross-currency trading [155] or thoroughly investigated pyramid schemes in cryptocurrencies [81].

First, this work offers the reader a foundation in (Chapter 2). We start with presenting a background on cryptocurrencies, in particular Bitcoin and its relevant components. Then we explain the anonymity of Bitcoin and state-of-the-art techniques used to defeat anonymity/privacy via address clustering, along with countermeasures proposed by the community. We end with some of the core concepts used in privacy coins.

In Chapter 3 we present a literature review of the ecosystem. We start with an overview of the research that preceded cryptocurrencies. We then discuss the literature used to defeat and improve anonymity in both Bitcoin and privacy coins and end with a review of the various aspects of crime in the blockchain ecosystem.

Our first contribution to analysing transaction privacy is presented in Chapter 4. Here we analyse the privacy coin Zcash, finding that address clustering and tagging is a very viable technique, privacy guarantees are severely limited due to a small anonymity set, and users perform unwise transactions with traceable patterns that damage the privacy of themselves and others. We end with a case study of a prominent hacker collective that used the coin to sell security vulnerabilities.

With the rise of alternative cryptocurrencies, exchanges began to provide trading services, allowing users to directly swap coins between different cryptocurrencies. In Chapter 5 we present one of the first academic analyses of cross-currency trading. We show techniques for tracing users moving across chains, heuristics clustering cross-chain user addresses and multiple case studies showcasing criminal use.

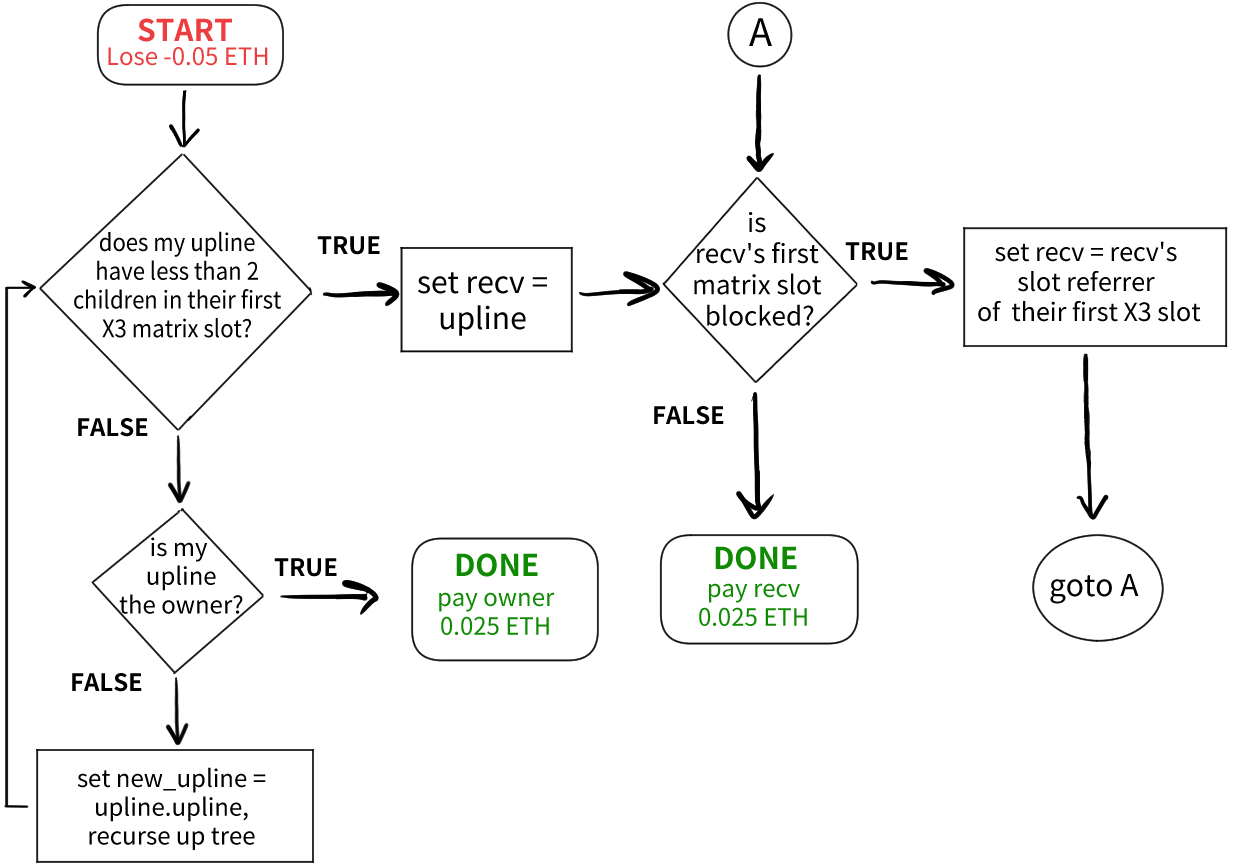

Having been around for over a century, pyramid schemes have scammed users out of billions of dollars [64]. In Chapter 6 we contribute to other analyses of this crime in blockchain and present an in-depth empirical study of Forsage, a smart-contract pyramid scheme on Ethereum. We explain how the obfuscated smart contract , using a purpose-built transaction simulator, quantify the gains and losses, and study the promotional videos showing how the promoters leverage the new technology of smart contracts to lure users.

The question that then arises is about who are the ’others’ who would implement such work. We define ’others’ as the following; Fellow scientists who discover and implement mediation’s which would improve user privacy, thus thwarting our attacks. Scientists who produce follow-up work with even more attacks, as well as investigators who use our heuristics to measure risk in their services, or trace transactions to combat crime.

1.2 Included Work

Parts of this thesis have been published in the following papers. All papers are joint work unless otherwise stated.

-

•

George Kappos, Haaroon Yousaf, Mary Maller, and Sarah Meiklejohn. An Empirical Analysis of Anonymity in Zcash. In 27th USENIX Security Symposium (USENIX Security 18), pages 463–477, Baltimore, MD, 8 2018, USENIX Association, https://www.usenix.org/conference/usenixsecurity18/presentation/kappos. Source code: https://github.com/manganese/zcash-empirical-analysis/. Included in Chapter 4.

-

•

Haaroon Yousaf, George Kappos, and Sarah Meiklejohn. Tracing Transactions Across Cryptocurrency Ledgers. In 28th USENIX Security Symposium (USENIX Security 19), pages 837–850, Santa Clara, CA, 8 2019. USENIX Association. Paper: https://www.usenix.org/conference/usenixsecurity19/presentation/yousaf. Source code: https://github.com/manganese/tracingTransactionsAcrossCryptocurrencyLedgers. Included in Chapter 5.

Other parts of the thesis are under submission to conferences, and have been published in pre-print.

-

•

Tyler Kell, Haaroon Yousaf, Sarah Allen, Sarah Meiklejohn and Ari Juels. Forsage: Anatomy of a Smart-Contract Pyramid Scheme. In: arXiv preprint arXiv:2105.04380, 2021. Paper: https://arxiv.org/abs/2105.04380. Source code: https://github.com/initc3/forsage. Included in Chapter 6.

1.3 Additional Work

The following papers were published, as part of my research, and are not included in this thesis.

-

•

George Kappos, Haaroon Yousaf, Ania M. Piotrowska, Sanket Kanjalkar, Sergi Delgado-Segura, Andrew Miller, and Sarah Meiklejohn. An Empirical Analysis of Privacy in the Lightning Network. In International Conference on Financial Cryptography and Data Security. Springer, 2021. Paper: https://fc21.ifca.ai/papers/130.pdf.

-

•

Pierre Reibel, Haaroon Yousaf, and Sarah Meiklejohn. Short Paper: An Exploration of Code Diversity in the Cryptocurrency Landscape. In International Conference on Financial Cryptography and Data Security, pages 73–83. Springer, 2019. Paper: http://fc19.ifca.ai/preproceedings/134-preproceedings.pdf.

-

•

George Kappos, Haaroon Yousaf, Rainer Stuetz, Sofia Rollet, Bernhard Haslhofer and Sarah Meiklejohn. How to Peel a Million: Validating and Expanding Bitcoin Clusters. arXiv pre-print 2021, TBC.

1.4 Work Done in Collaboration

A large part of the work in this thesis was completed in collaboration with researchers across the globe, all of whom are listed in Section 1.2.

In Chapter 4, Sarah Meiklejohn discovered that the Zcash shielded pool was leaking non-trivial information that could damage the privacy of users. I managed and processed blockchain data used for the project, general statistics, tagging analysis and leading the case study on the hacker collective with Mary Maller. Joint work includes the clustering heuristic with Sarah Meiklejohn and tag collection with Mary Maller. George Kappos analysed the interactions with the pool and shielded pool.

In Chapter 5, I wrote the scraping tool to collect all data (including all blockchain nodes and exchanges), statistics, cross-currency tracing via pass-through and patterns of ShapeShift Usage (excluding Trading bots). With regards to joint work, all authors contributed to identifying blockchain transactions and I worked on the clustering analysis with Sarah Meiklejohn. George Kappos worked on tracking cross-currency u-turns, round trip and the trading bots.

In Chapter 6, I processed the data from the Ethereum nodes and performed the contract measurements study. All authors contributed to the proposed solutions. Tyler Kell worked on contract deconstruction. Sarah Allen and Tyler Kell worked on the community-dynamics study.

With regards to work not included in this thesis. In the paper, Why is a Ravencoin Like a TokenDesk? An Exploration of Code Diversity in the Cryptocurrency Landscape [120], I came up with the study and proposed the breakdown of work. Sarah Meiklejohn led and wrote the paper and worked with Pierre Rebel who performed the scraping and analysis.

In the paper, An Empirical Analysis of Privacy in the Lightning Network [80], I ran and managed our Bitcoin and lightning nodes, created and performed the property heuristic and extended the previous version of the balance discovery attack based upon the original from Sergi Delgado-Segura.

In the paper, How to Peel a Million: Validating and Expanding Bitcoin Clusters (under re-submission), I worked on identifying the transaction and address features, and jointly worked on the algorithms with George Kappos.

Chapter 2 Background

2.1 Cryptocurrencies

This chapter details the basic components needed to gain an understanding of cryptocurrencies.

2.1.1 Bitcoin

The first decentralised electronic cryptocurrency, Bitcoin, was created by Satoshi Nakamoto in 2008 [106]. A white paper explaining the architecture and design was originally sent as a link to the metzdowd cryptography email list in October 2008, and was shortly followed by the release of Bitcoin open source software in January 2009 [105]. That paper lays the foundation for a decentralised financial system through a digital asset class called cryptocurrencies.

By definition, cryptocurrencies are a form of digital currency coupled with cryptography and a blockchain. A blockchain is a distributed ledger which contains a record of all transactions. In Bitcoin, the complete record is public, viewable and verifiable by all participants and thus reduces the need for a central authority. All participants can choose to have a copy of the ledger, allowing it to be decentralised. Public key cryptography is used in Bitcoin to maintain the integrity and authenticity of each transaction.

Digital coins are used as a medium of exchange and allowed to be freely traded between users without fear of censorship. All coins are stored in wallets each of which has one or many public key(s), or wallet address(es), and has one or many private key(s). Users can generate as many wallets and keys as needed, without the requirement for any verification of identity.

Coin minting and supply is fixed within the protocol, and awarded to users who maintain security by mining. Transaction finality is protected by this consensus of miners.

This was the first system of its kind that allows users to transfer digital cash without the fear of double spending and need for any intermediaries, effectively a non-custodial, trustless and decentralised global payments network. On 8th November 2021, the value of Bitcoin soared to the highest currently recorded: $67,566.83 USD per Bitcoin. This innovation has led to the development of new research fields and new cryptocurrencies (e.g., Ethereum, ZCash and Monero). According to CoinMarketCap, as of November 27th 2021 there are over 14,000 cryptocurrencies with a total market capitalisation of 2.4 trillion USD [39].

2.1.2 Blockchain components

In this section we explore the core foundational components used in blockchain technologies. We begin with Keys and Wallets which are responsible for holding, sending and receiving coins. Then we discuss the format of transactions which are used to send and receive coins. Finally, we discuss the structure of blocks and role of miners. Further information about the cryptography can be found in various textbooks [narayanan2016bitcoin, boneh2017graduate].

Keys and Wallets

Bitcoin’s foundation is built with its use of public key cryptography. This allows the user to create two related but different keys: a private key and a (derived) public key.

The private key is the secret component that controls and signs transactions, akin to a bank PIN code which is used to authorise money that is spent. However, unlike a PIN code, the private key also acts as the vault to store coins, and if leaked allows all coins to be compromised. If a user looses their private key, this would also mean a loss of access to the coins belonging to that key.

Public keys are derived from private keys. These are the user’s Bitcoin address and digital fingerprint, with workings akin to a bank account number. 19Yq6pRM3mRUZMbWZoBpRWhNehiQHqznGR is an example of a public key used in Bitcoin. Users send coins to public keys, similar to the way in which cash is transferred to bank account numbers. When sending coins, the user must sign the transaction with a unique signature created from the associated private key. The transaction, signature and public address combination is then verified by users of the network to ensure the user owns the coins being spent. Both keys, public and private, are generated using the Elliptic Curve Digital Signature Algorithm (ECDSA) [75]. Key management is performed via digital wallets. Just like a physical wallet which can hold one or more cards/cash, digital wallets hold private and public keys. The wallet is controlled by the software the user chooses to run, for example in Bitcoin this is done via the bitcoind program.

A user can spend funds from multiple private keys in the same transaction, and thus signs the transaction which each of the corresponding keys. The signature is stored within the transaction inside the input field, which allows the network to verify that the coins have been rightly spent. Keys are pseudonymous and are not tied to any physical identity. However, if the identity of a public key is revealed, then blockchain analytics and heuristics can be used to identify all transactions that involved the said key, thus tying and identifying the financial habits of the user.

Transactions

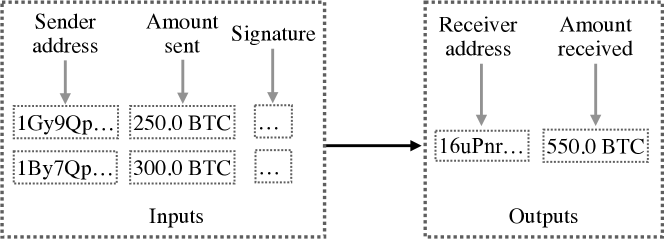

A transaction is the structure used to transfer coins. It has inputs, outputs and features. Inputs are the addresses from which coins are received, and outputs are addresses to which coins are sent. The number of inputs and outputs is determined by the user, but there must be at least one input and one output in a transaction. Features are attributes on transactions which trigger certain conditions. For example, a Bitcoin transaction can set a feature called locktime which means the transaction is only valid once the specific time has passed.

Figure 2.1 illustrates a simple example of a two input and one output transaction. On the input side, two addresses 1Gy9Qp… and 1By7Qp… are sending 250 BTC and 300 BTC respectively to address 16uPnr…, the output. In this instance a single entity may own both of the input addresses or it may be two users performing a transaction together to send coins to the same recipient. Only public addresses are shown on the blockchain and only public addresses are used to send and receive coins. The sending user(s) sign the transaction with the corresponding private key. This produces signature(s) to be included within the transaction to allow for verification. Once the transaction is confirmed and verified by the network, it is stored on the blockchain within blocks.

In order to maintain security and incentivise miners to validate and publish transactions, users can optionally add a transaction fee. This fee represents a portion of the bitcoins transferred, calculated by deducting the total bitcoins in the output the total bitcoins in the input. The fee is collected by the miner who publishes the transaction onto the chain. As space within a block is limited, miners can choose the transactions they would like to include in their block. Thus, there is an economic incentive to choose transactions with high fees. This creates a market for transaction fees, and thus users must be aware of the current fees being accepted to ensure their transaction is published.

Blocks and Miners

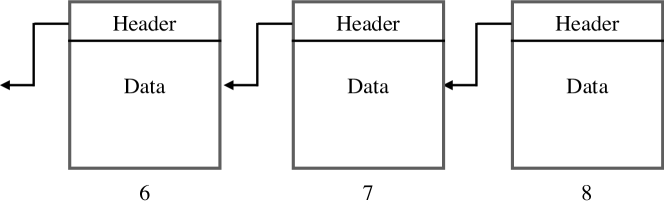

A block is a data structure that contains both a header and block data. The data in a block is made of newly confirmed transactions (can hold zero or more transactions). The header contains block metadata and a cryptographic hash of the previous block. As shown in Figure 2.2, multiple blocks are chained together with their respective hashes forming a block chain. This is akin to a linked list, using hash pointers instead of traditional pointers.

As Bitcoin is an append-only ledger, the cryptographic hash pointers of previous blocks are a vital and necessary core component of maintaining security. Any modification to the data in any part of the chain changes the cryptographic hash of the modified block, subsequently causing all following hashes to change. Thus, data is only appended to the end in the form of new blocks. Each block is stamped with a block number indicating its position in the chain. This, combined with the chain of hashes, makes blocks immutable to change.

All blocks are created (in blockchain terminology mined) by miners who follow the Nakamoto consensus [106]. One part is a proof-of-work (PoW) algorithm which uses a set of rules that govern the network and the another is the heavy emphasis on following the longest chain.

In the case of Bitcoin, miners solve a difficult mathematical puzzle in return for the reward of newly minted coins and transaction fees. This ensures that nodes generate proof to show they have spent some computational power/energy. The difficulty of the puzzle prevent miners from spamming the network with fake blocks to quickly obtain new coins/fees as puzzle solutions require some computational power to generate but are very easy to verify. This allows block generation and transaction confirmation to be secure and decentralised within a trustless network, as trust is obtained from verifying a miners puzzle and the process incentivizes nodes to behave honestly in order to obtain the rewards.

In Bitcoin proof-of-work, the puzzles are difficult to solve, easy to verify and have varying levels of difficulty depending on the overall power of the network, with the answer to the puzzle being a hash within the target difficulty. To generate this hash, miners use the hash of the previous block, data from transactions they choose to validate, a time stamp and a nonce. The nonce is the value that is iterated in order to find the hash. Once found, the miner then enters their public key and pushes the block to the network. Full nodes in the network verify the block contents and the answer to the puzzle. If no issues are found, this new block is added to their chain, the miner earns the reward containing both newly minted coins and transaction fees from pending transactions they included (which are now marked as confirmed) and the entire process repeats. Rewards and fees act as incentives for miners to follow the rules and participate in the network.

On average this routine takes 10 minutes which provides proof that the majority of the power in the network participated. In the case where two miners find a block at the same time, causing a chain split, the miners are all programmed to follow the longest chain which removes the need for a third party to direct the system. The system is protected against double spend attacks, as the attackers would require more than 50% of the network hash power to take control of the chain.

The longest chain rule, states that nodes in the network must follow and build upon the blockchain with the most blocks as this is the most legitimate as it has had the most computational power spent upon it. New users in the network simply follow the longest chain and begin to mine on top of it, allowing users to join and leave the network without having any negative impacts. This also prevents the network from needing to delegate authority, as by default all nodes follow the authority of the longest chain.

2.1.3 Accounting models

In this section we explain the two accounting models used in the blockchain technologies we explored, these being the Unspent Transaction Output model (used in systems such as Bitcoin, Dash and Zcash) and Account-based model (used in smart-contract based cryptocurrencies such as Ethereum).

Unspent Transaction Output

In the Unspent Transaction Output (UTXO) accounting model transactions have one or more inputs and one or more outputs. The outputs determine the receiving amount (the coins) and condition. Each output is a UTXO.

The receiving condition is a script, that when true, allows the coins to be spent. In Bitcoin, one example of this script consists of the address of the recipient who can spend the coins, provided they can sign the follow-on transaction with the associated private key. At a high level, this output is seen simply as the address. For example, a user who mined a block would receive newly minted coins sent to a script only redeemable with their address. To spend this coin, the user must turn this into an input within a new transaction.

The input contains a signature which proves the corresponding output to be true. For example, a user wants to send their newly minted coins to a cryptocurrency exchange. With their private key they create a signature that solves the script that was sent to them, thus allowing them to spend their coins, and also marking the output as spent. With this they repeat the process by creating a new output with the recipient amount and condition. The spent input combined with the new output creates a transaction.

Inputs cannot be split; when spent, the entire input is used. This ensures that each is spent only once. If users want to partially spend their UTXO, they would create an additional change output to themselves. This process of change is usually handled by the wallet software. This process is akin to spending physical cash. For example, to spend a £20 note one must give the note in its whole physical form to the recipient, who then keeps the note and in exchange returns any change. One does not physically tear a note.

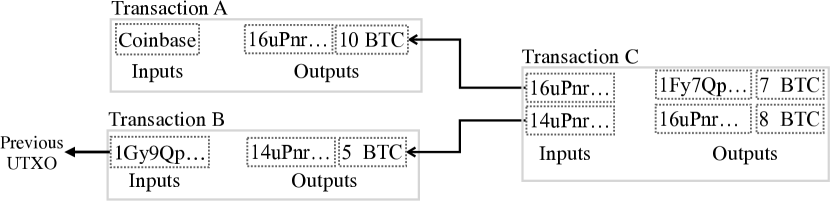

Figure 2.3 shows a high level diagram of three UTXO-based transactions. Here, user Alice has received two transactions: Transaction A with newly minted coins sent to address 16uPnr… and Transaction B with 5 BTC sent to her second address 14uPnr…. She spends both of these in Transaction C by spending both as inputs, sending 7 BTC to Bob 1Fy7Qp… and the remainder to herself as change.

The UTXO model ensures that no user is able to double spend, as every UTXO can only be spent once and must be completely used. Users can spend UTXOs independently of one another. The network can determine who owns what coins by simply taking a list of all UTXOs. From an analytics perspective, UTXOs make it easier for users to trace coins to their source.

Account-Based

Account-based models are an alternative and used in cryptocurrencies such as Ethereum, a smart-contract-based blockchain. An address acts as an account (with a private and public key) and coins are deposited directly to the address. Accounts have a balance and keep a record of all transactions. In Ethereum, accounts can be controlled by a user or by code within a smart-contract.

When a user wants to send funds, the transaction reduces their (sender) balance and increases the recipient’s balance. Each account has a public nonce which acts as a protection against malicious users attempting to replay transactions. This nonce is incremented and attached to each transaction sent from the sending account. Compared to UTXOs, coins in accounts can be split and do not need to be fully spent. This means account-based blockchains do not create change as in Bitcoin.

2.2 Anonymity

As previously mentioned, Bitcoin is designed to operate with pseudonymity on an open ledger that maintains the public history of all transactions. This transparency allows transactions to be monitored. By analysing transaction patterns, researchers have created heuristics able to reduce the effectiveness of pseudonymity by linking transactions and addresses to real world entities.

2.2.1 Multi-input heuristic

A multi-input (also known as co-spend or clustering) heuristic is the foundational process used to cluster Bitcoin addresses, linking together addresses that may be owned by the same entity. This, when combined with address tagging, reveals the real world identity behind the transactions. The effectiveness of this technique has been demonstrated by many researchers [EvaluatingUserPrivacy, 95, 121, 124] and has formed the basis for commercial cryptocurrency analytics and surveillance companies (e.g., Chainalysis and Elliptic).

A user must have access to the private key in order to spend coins. Inputs in a transaction are spent as the owner(s) signs the transaction(s). It can therefore be deduced that addresses spent together in the same inputs are probably owned or at least controlled by the same entity. By cascading this process across all transactions, one is left with clusters of addresses that have been used together.

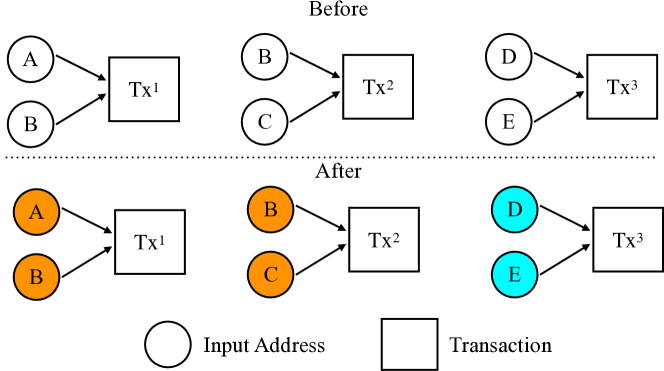

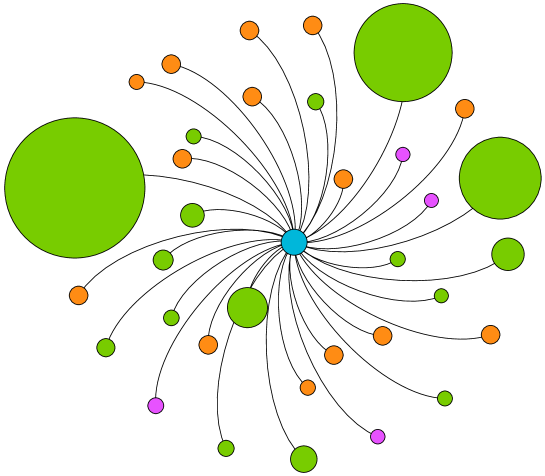

Figure 2.4 shows a visual example of this process, with three transactions that each have two input addresses. Before, we can see unclustered transactions, indicated by a white circle. To conduct the heuristic we execute the following steps. We look at the inputs of the first transaction and label these addresses, A and B, with the colour orange. In the next transaction, we look at the inputs and check if they have been coloured (allocated a cluster) before, if so we give them the existing colour, if not we assign a new colour. In this instance the second transaction has input B, which was labelled previously. Thus these inputs are given the colour orange. We repeat this process until all transactions have been labelled. Finally, we can see that in the final transaction input addresses D and E have not been labelled before and are given a new colour, cyan. This completes the heuristic and the ”after” section shows the final result containing two clusters, cluster orange with addresses A, B and C and cluster cyan with addresses D and E.

In practise this algorithm can be modelled in a number of ways. The method mentioned above is akin to the disjoint set (union find) algorithm [124]. Alternatively this can be modelled by extracting clusters from connected components [126] within a graph, where nodes are addresses and are connected by edges to other nodes if they were involved as inputs in a transaction.

2.2.2 Countermeasures

A variety of counter-measures have arisen since the development of the clustering heuristic, namely coin mixing and privacy coins.

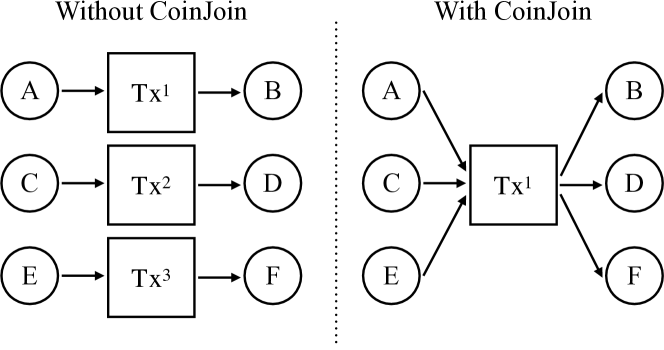

Mixing is the process of combining coins with users to attain increased privacy and anonymity. CoinJoin, a form of mixing, was proposed by Maxwell in the Bitcoin forums in 2013 [91]. They present a method for users to mix their coins together in a single transaction. This obfuscates coin movement by severing the link between inputs and outputs. Clusters are then combined, triggering incorrect results when using clustering techniques.

For example, let us say that user Alice wants to pay Bob, Charlie wants to pay Dennis and Eve wants to pay Francis. This can either be recorded as three separate transactions on the chain, shown in ‘without CoinJoin‘ in Figure 2.5. This approach makes it trivial to identify payees and recipients. Alternatively, users can perform a CoinJoin together and join their coins in a single transaction. This would appear as Alice, Charlie and Eve are sending coins to Bob, Dennis and Francis and hides the intricate details of exactly who paid whom.

Alternatively, let us say that Alice, Bob and Charlie unfortunately had their wallet addresses leaked and tied to their real-world identity, or had stolen Bitcoins and wanted to hide their trail. They could perform multiple CoinJoins one after the other with other users, in an attempt to pool and mix all their tainted coins together with non-tainted coins. This can be performed using a tumbler or mixing service, which given a transaction fee, would automate the entire process and allow the user to select a degree of privacy, e.g. mix and return funds after 10 CoinJoins.

In practice, performing CoinJoins is cumbersome. Users need to find other willing users and perform the advanced task of signing and merging their transactions. Developers have created tools that automate this by automatically finding users and performing the CoinJoin, such as Wasabi Wallet [148] and Samourai Wallet [129]. Tumblers, such as Bitcoin.Fog, allow users to mix their coins, but services like this are often shutdown by law enforcement agencies due to criminal usage and money laundering [88].

2.3 Privacy Coins

Bitcoins pseudonymity was short lived as two years after release the attacks on its protocol came to fruition [95, 124] Since there has been an increase in privacy-preserving coins (privacy coins) which attempt to solve the privacy flaws of Bitcoin, such as Dash [41, 91]), Zcash [156, 15] and Monero [101, 128], each of which provide different guarantees of anonymity.

2.3.1 ZCash

Zcash (ZEC) is an alternative cryptocurrency developed as a (code) fork of Bitcoin that aims to break the link between senders and recipients in a transaction. In Bitcoin, recipients receive funds into addresses (referred to as the vOut in a transaction), and when they spend them they do so from these addresses (referred to as the vIn in a transaction). The act of spending bitcoins thus creates a link between the sender and recipient, and these links can be followed as bitcoins continue to change hands. It is thus possible to track any given bitcoin from its creation to its current owner.

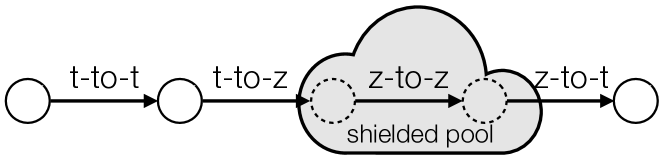

Any transaction which interacts with the so-called shielded pool in Zcash does so through the inclusion of a vJoinSplit, which specifies where the coins are coming from and where they are going. To receive funds, users can provide either a transparent address (t-address) or a shielded address (z-address). Coins that are held in z-addresses are said to be in the shielded pool.

To specify where the funds are going, a vJoinSplit contains (1) a list of output t-addresses with funds assigned to them (called zOut), (2) two shielded outputs, and (3) an encrypted memo field. The zOut can be empty, in which case the transaction is either shielded (t-to-z) or private (z-to-z), depending on the inputs. If the zOut list contains a quantity of ZEC not assigned to any address, then we still consider it to be empty (as this is simply the allocation of the miner’s fee). Each shielded output contains an unknown quantity of ZEC as well as a hidden double-spending token. The shielded output can be a dummy output (i.e., it contains zero ZEC) to hide the fact that there is no shielded output. The encrypted memo field can be used to send private messages to the recipients of the shielded outputs.

To specify where the funds are coming from, a vJoinSplit also contains (1) a list of input t-addresses (called zIn), (2) two double-spending tokens, and (3) a zero-knowledge proof. The zIn can be empty, in which case the transaction is either deshielded (z-to-t) if zOut is not empty, or private (z-to-z) if it is. Each double-spending token is either a unique token belonging to some previous shielded output, or a dummy value used to hide the fact that there is no shielded input. The double-spending token does not reveal to which shielded output it belongs. The zero-knowledge proof guarantees two things. First, it proves that the double-spending token genuinely belongs to some previous shielded output. Second, it proves that the sum of (1) the values in the addresses in zIn plus (2) the values represented by the double-spending tokens is equal to the sum of (1) the values assigned to the addresses in zOut plus (2) the values in the shielded outputs plus (3) the miner’s fee. A summary of the different types of transactions is in Figure 2.6.

2.3.2 Dash

As in Zcash, the “standard” transaction in Dash is similar to a Bitcoin transaction in terms of the information it reveals. Its main anonymity feature PrivateSend transactions are a type of CoinJoin [91].

A CoinJoin is specifically designed to invalidate the multi-input clustering heuristic described in Section 2.2.2, as it allows multiple users to come together and send coins to different sets of recipients in a single transaction. If each sender in a CoinJoin sends the same number of coins to their recipient, then it is difficult to determine which input address corresponds to which output address, thus severing the link between an individual sender and recipient.

In a traditional CoinJoin, users must find each other in some offline manner (e.g., an IRC channel) and form the transaction together over several rounds of communication. This process is often centralised, as users become aware of one another and may use a service to find each other. Dash aims to simplify this for users by automatically finding other users for them and chaining multiple mixes together. In order to ensure that users cannot accidentally de-anonymize themselves by sending uniquely identifiable values, these PrivateSend transactions are restricted to specific denominations: 0.01, 0.1, 1, and 10 DASH.

Chapter 3 Literature Review

3.1 Cryptocurrencies

3.1.1 Early digital cash

One of the earliest research publications on digital cash is eCash, created in 1983 by David Chaum [30]. Banks issue eCash to users, who are able to store it on their local machines. eCash uses a concept called blind signatures, introduced in 1983, which blinds contents of message before being signed, hiding the contents from the signer. In the context of eCash, this allows users to hide their identities from banks, and anonymises the links between spend and withdrawal transactions. However, key issues with the system are that it requires banks to both participate and act as the central authority, and banks have the power to mint digital cash as well as the ability to refuse deposits.

Following this, in 1998 Wei Dais proposed B-money an anonymous and distributed cash system [40]. B-money is similar to Bitcoin, whereby, new transactions are broadcast to all users, who also keep a complete record of the ledger. Users are represented by public keys, and mint coins via completing computational puzzles. This solved the previous issues raised by eCash as the new features alleviated the need for an issuing bank. However, B-money raised a number of other issues. One was with the protocol for creating new coins, which required account keepers to decide on the cost of computations. This at the time was not feasible, due to the rapid advancement of technology. Wei did propose an alternative way to mint money with a four step process, however this seemed complicated. Secondly, B-money was entirely conceptual, having only been written on paper with no code or tests to support its claims.

In 2005, Szabo introduced bit gold [138, 115], which used a proof-of-work scheme to mint new coins. In this scheme, users would compete to solve computational puzzles and in doing so would earn bit gold. Each puzzle solution became a part of the next one, and thus would form a chain. However, similarly to B-money, bit gold remained as a concept and was not turned into working code.

3.1.2 Bitcoin and the alt-coins

In November 2008, Satoshi Nakamoto revealed the Bitcoin white paper to the metzdowd’s cryptography mailing list [105, 106]. This system solved previous problems by creating a distributed shared public ledger that prevented double spending, did not include any third parties, allowed pseudonymous user accounts and used a modified version of Hashcash’s proof-of-work scheme to generate new coins [10]. As of today, Bitcoin is one of the most valuable cryptocurrencies with a market capitalisation of many billions of dollars (USD) [39, 23]. Researchers and companies have examined and evolved the underlying software, forking the source code into many new coins or developing new software based on the presented ideas. These coins are named alternative coins or alt-coins, and examples include Litecoin [85], Dash [41], Zcash [156] and Ethereum [28].

Litecoin, an alt-coin forked from Bitcoin, has some changes such as different proof-of-work algorithm, decreased block generation times and an increased maximum number of coins. Dash offers faster transaction confirmations and is packaged with a coin mixing service. Zcash builds upon Bitcoin by adding privacy preserving transactions that make use of zero-knowledge proofs [miers2013zerocoin, 15, 69]. Ethereum is a blockchain proposed by Buterin in 2013, is not a fork of Bitcoin but it carries many of the same principles. The main differences include: an introduction of a Turing-complete (limited by execution costs) programming language named Solidity, allowing user created smart contracts to be published on-chain, introduction of custom user created tokens on-chain and an account-based accounting model. As of July 2021, Ethereum is the second most valuable cryptocurrency, just after Bitcoin.

3.2 Privacy

The openness of the ledger allows the transaction flows of the network to be monitored. A large volume of work is dedicated to analysing the privacy of Bitcoin, including improving its anonymity and analysing the privacy of alt-coins. Here, we outline the most relevant works.

3.2.1 Anonymity of Bitcoin

Reid et al. presented one of the first anonymity analyses on Bitcoin in 2011 [121]. Their work analyses nearly two-years-worth of data across multiple angles. Firstly, they model both transaction and wallets as two separate network graphs, revealing that the network has been increasing over time and that the user network is cyclic with users sending coins to previously-owned addresses rather than treating addresses as one-time use. By focusing on privacy, they also discovered that public-keys can be linked with others via passively analysing the monetary flow between addresses, Using this, they performed one of the first academic analysis of a theft of bitcoins, tracing some of the stolen funds to an online wallet provider. However, some of the limitations of this study are that the analysis was conducted very early in the Bitcoin timeline and therefore was performed on a small graph, with potential users who were early adopters, and thus, this may not have represented a mature graph.

In 2012, Ron and Shamir [Ron2013] analysed statistics across the entire blockchain, from genesis until May 2012. Compared to previous analysis, the Bitcoin graph had since grown by a factor of three. Using the union-find algorithm, Ron and Shamir cluster 3M addresses as 1.8M entities, identifying that some of the most active clusters belong to exchange or wallet providers. Furthermore, Ron and Shamir identified that many bitcoins remained unused in sink addresses, and most transactions moved only small quantities of the total bitcoin in circulation, and users created transaction chains in an attempt to hide and weaken the links between their addresses. In their paper, the researchers could have made further efforts to identify the larger entities, as only three out of a million or so entities are revealed. Their reasoning and usage of the union-find algorithm is largely unclear, as is the method used to identify clusters.

In the same conference as Ron and Shamir (Financial Cryptography and Data Security, 2013), Androulakil et al. presented an evaluation of user privacy [8]. They offered a short evaluation of privacy using two heuristics: a multi-input heuristic and a change heuristic, as well as a longer evaluation on an account-based behaviour simulator. Using the first heuristic they are able classify 1.6M addresses into 1M entities, and this is further reduced to 693k entities when using the second heuristic. With the simulator, they identify that Bitcoin does not do enough to protect the privacy of its users, as despite following the recommended guidelines, behaviour-based clustering can profile 40% of participants. The evaluation of the two heuristics is very short, and the paper largely focuses on the data from the simulation rather then the ground truth data from their defined heuristics.

Meiklejohn et al. [95] performed an in-depth measurement study on Bitcoin and its anonymity. They significantly expanded upon previous clustering efforts and examined the network from creation to April 2013, revealing network statistics, usage and account heuristics, attacks on pseudo-anonymity and the role of entities in the wider ecosystem. They interacted with a wide variety of services, manually obtaining tags for 1,070 addresses. Using both the multi-input, and introducing, a peel-chain heuristic, they analysed the entire network and expanded their tags across clusters covering over 1.8M addresses. Their work demonstrates the effectiveness of such clustering techniques. In addition, they presented multiple real world case studies tracking criminal activities, finding that funds from a Bitcoin ponzi scheme were distributed to a variety of services, and tracking multiple thefts to exchanges. However, Meiklejohn et al. also presented progressive enhancements, as both heuristics had been previously published in some form. The effectiveness of the reidentification attack can be reduced if users use mixing services. Their clusters were not compared against ground truth, however, during this time period in the Bitcoin ecosystem, ground truth data was likely only obtainable by directly contacting exchanges and services that may not have wanted to share their sensitive data.

Spagnuolo et al. presented BitIodine [136], a modular analytic framework which parses, clusters, classifies and visualises Bitcoin data. In their work they describe the workings of the system which uses a variety of open-source tools, including the C\+\+ programming language, Neo4J (a graph database) and Gephi (an open source visualiser). They implement both the the multi-input and change heuristic, and test these on real-world use cases. Notably, they argue that they find a connection between an address belonging to the owner of a dark market and a separate address which at one point contained over 111k BTC. In addition, they analysed addresses that sent and received coins from the CryptoLocker ransomware. Using their tool they estimate the scammers obtained over 1.1M USD worth of BTC and identify what is claimed to be a potential ”test” transaction that occurred days before the first ransom was paid. There are however some limitations with both the work and tool. With regard to the work, the case studies are very short, and stating an address has a ”meaningful connection” to another is not indicative of holding any real significance. The tool itself stores all transactions and clusters in memory, which makes the process memory-intensive and costly, given the increasing size of the Bitcoin ledger. It is limited to exporting static graphs and is not bundled with a user interface. Thus the tool requires users to have a high level of technical knowledge to operate.

Kalodner et al. have presented an open-source blockchain analytics tool BlockSci [77]. Their paper describes in detail the design choices, and architectural challenges, and then presents multiple real-world case studies. When compared to standard graph analytic platforms, the BlockSci program is significantly faster and easier to use than BitIodine, as it is bundled with documentation and a python interface. The tool itself features an extensive analytics engine, allowing clustering and tracing across UTXO cryptocurrencies and their corresponding forks. Within their use-cases, the authors demonstrate that anonymity is affected by usage patterns in multi-signature wallets, identifying that 5% of Bitcoin addresses have their privacy affected as users cash out their coins on corresponding forks, such as Bitcoin Cash. By clustering these transactions across Bitcoin forks, they reveal information about users that can be linked back to their wallets. The paper does not compare the tool against previous blockchain analytics programs such as BitIodone, but instead against graph analytics tools. Since the release of the paper, development of the tool has since discontinued. The tool also requires a machine with very large memory in order to cluster the blockchain.

The research above demonstrates that Bitcoin’s anonymity can be breached, since there have been new proposals to resolve these issues and improve privacy without major changes to the protocol. One process is CoinJoin [91], where users create a transaction together, merging their inputs and outputs in order to reduce the linkability within their transaction. This process is one of the foundational features of the cryptocurrency Dash [41] which automates the entire procedure. This CoinJoin mechanism is explained in more detail in Chapter 2.2.2.

Analysis around the anonymity of CoinJoin [94, 102, 90, 96, 9] presents many issues. Atlas affirms that inputs and outputs of a CoinJoin can be linked through brute-forcing all possible summations and more so, if denominations can be uniquely identified [9]. However, the process can quickly become computationally expensive as CoinJoin is a variant of the Knapsack problem [125, 90]. Dash [41] improves the usability of Maxwell’s CoinJoin [91] through automating the process of finding participants to mix with using fixed denominations, further explained in Chapter 2.3.2. However this adds a time delay to transactions, as users must wait to find others with whom to mix.

3.2.2 Anonymity of privacy coins

In Bitcoin transactions information is entirely public and, as previously shown, allows any entities to freely track the movement of coins. Protocols have since been developed to integrate anonymity. Many of these have been implemented into alternative coins marketed with a privacy focus.

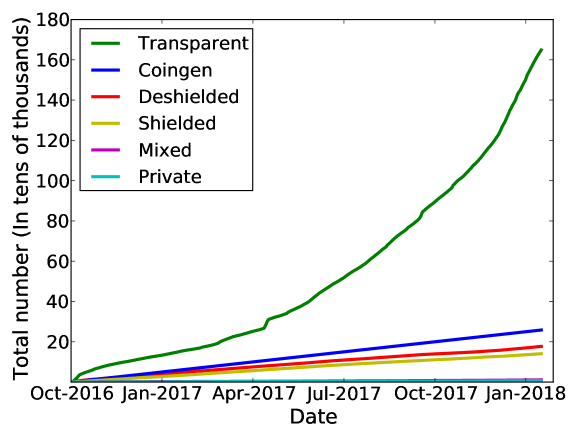

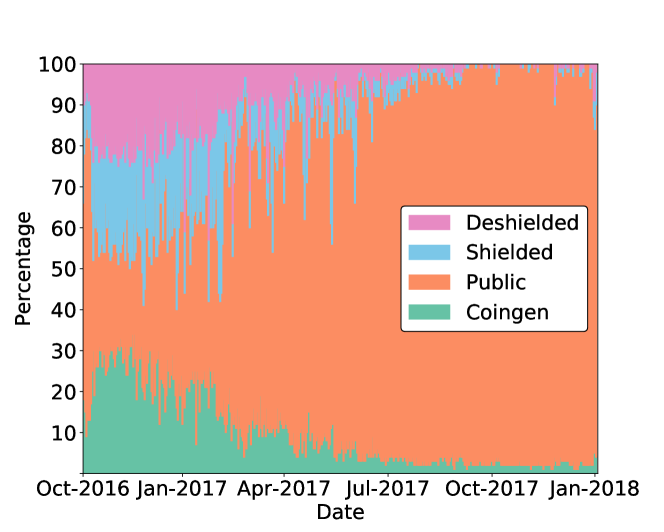

Zerocash is a protocol, forked from Bitcoin, that adds privacy-preserving transactions [97, 15]. These use zero-knowledge proofs to ”shield” coins, adding an anonymity layer that hides the amount, sender and receiver. Thus, when coins are spent, no information about the transaction is revealed other than a potential fee. Users have the option to use this feature, for anonymous coins they utilise zerocoins, also known as shielded coins/transactions, and for non-anonymous coins they can spend basecoins, also known as transparent coins/transactions. Coins can be converted to either type at the users preference. This concept is further explained in Chapter 2.3.1. Zerocash was subsequently commercialised into the cryptocurrency ZCash. The initial downsides of ZCash were that the original versions required a significant amount of processing power (3GB of RAM and several minutes) to construct the zero-knowledge proof required for a single shielded transaction. This was not suitable for sending quick transaction, nor were users able to perform such computations on their mobile devices. They originally needed to run a full ZCash node, as most wallet software only supported transparent transactions. In doing so, this led to the second issue, whereby running a node and performing shielded transactions required some familiarity with the command-line, as even the software did not come with a user interface. Given that this type of transaction was optional, not enabled by default or the above issues, the anonymity set of the shielded pool was thus confined to users who were technically advanced. Recent advancements have since solved these issue such as reducing the memory usage by 98%, reducing transaction times by 80% [24], and introducing mobile wallets which support all types of transactions such as Zecwallet Lite [161].

Prior to the above advancements, researchers had revealed the short-comings of the shielded pool. In 2018, we published the first peer-reviewed study discussing the limitations and privacy flaws that were then present in Zcash. This is explained in detail in Chapter 4. Whilst we conducted this research, others published studies that had parallels with our work.

In late 2017, Quesnelle [119] also published a short study analysing the privacy of Zcash. They revealed that transaction meta-data can be used to link coins between deshielding and shielded transactions. They identified that the vast majority of coins were not used within the shielded pool, given that only 19.6% of transactions used some form of a privacy-preserving feature and that 57.7% of these were used to deshield coins. Although Quesnelle is credited with creating round-trip transactions, this is also a concept that we discovered during our research. In this process transparent coins are sent to a shielded address, and then a similar or identical number of shielded coins is returned to a public address within a close time frame. Around 31.5% of shielded coin transactions were conducted within round-trips. Using these, Quesnelle linked coins belonging to miners after their respective mining pool had deshielded newly minted coins. Quesnelle believes the reasons for these short-comings are due to lack of support within third-party wallets and high computational costs. The study has limitations because the work exclusively focuses on brief statistics and round-trips. The background does not clearly explain the workings of Zcash, and the transparent transactions which account for the majority of transactions in Zcash have not been fully discussed.

Birkyukov et al. [18] published heuristics analysing the behaviour of miners in both transparent and shielded pools. They extended previous work [79] by presenting heuristics targeting the two payout strategies deployed by mining pools. The first strategy identifies users of mining pools by following transactions that pay users with public addresses, whereas the second strategy identifies mining pools that directly pay users from a shielded address. Combined, their heuristics are able to link 88.4% of all mining rewards to shielded addresses. When combined with the Founder heuristic from previous work, presented in Section 4.5.1, they are able to link over 84% of all de-shielded transactions. In terms of downsides, the work does not focus any analysis on transparent transactions and their heuristics primarily target de-anonymising mining pool transactions.

In 2014, developers created Monero [101], a privacy focused cryptocurrency based on Nicolas van Saberhagen’s whitepaper on CryptoNote [128, 29]. Monero uses ring signatures, which are a digital signature that can be created by a user from a group of users that each have keys. When creating a signature, it is computationally impracticable to identify which member of the group created the signature. When a user wants to spend their coins in Monero, they generate a ”min-in”, which is a ring signature using their output as a key with other public keys taken from previous outputs in the blockchain. These all act as decoys within the new transaction, and when created the inputs appear to be equally likely to have been originally spent, which masks the origin of the transaction. All aspects of the transaction are obfuscated, hiding the senders, receivers and amounts.

Multiple research projects in 2017 identified issues which can disrupt the anonymity of the system [83, 98, tramer2020remote]. Kumar et al. presented three heuristics that were used to trace 87% of inputs [83]. By using temporal analytics, they identify that it is not as difficult to predict the correct output in a ring signature. Given that over time it is more likely a UTXO had already been spent and thus the most recent output is very likely to be the real one being spent. Secondly, by using a technique called leveraging output merging, they analyse user behaviour in transactions where two outputs belong to the same entity. Thirdly, they present that users themselves can disrupt the anonymity of others by choosing to do a mix with zero mix-ins, damaging the anonymity set of others who may have referenced their coins. Moser et al. presented similar work, by detailing issues surrounding the coin selection algorithm [98]. Similarly, they found it more likely to select more recently generated outputs.

These works all reveal that, despite best efforts, so called ”privacy coins” are vulnerable to attack. Over time, scientific advancements will identify weak points in systems that were previously thought to be secure. Therefore, it is pertinent to develop new techniques in order to strengthen current practices and create better mitigations.

3.3 Blockchain crime

The decentralised, pseudonymous and uncensorable transaction system has attracted a wide range of users, some of whom exploit the system for nefarious reasons. Bitcoin’s ability to transfer coins across borders (regardless of location), combined with misleading claims that Bitcoin offers anonymity, have attracted those involved in crime. Such crimes range from operating a dark market, theft, and ransomware, to scams and money laundering. This section details the literature that analyses transactions linked to misdeeds.

3.3.1 Dark markets

Underground markets are those which sell goods or services that may or may not be forbidden by law. Historically, there have been many examples with some predating the second world war [43, 143]. With the advancement of technology, these markets have naturally made an online appearance, with the earliest cyber markets selling information about goods and services (e.g., credit card numbers, viruses, botnets) via internet relay chats (IRC) [54, 140]. Following take downs by law enforcement, this activity moved to online forums, marketplaces and registration-only websites with research analysing their appearances in China [163]. The underground economy is now considered to be an integral piece of cybercrime, due to servicing criminal enterprises with illicit goods and services [62].

Silk Road, a notorious and commonly known underground market attributed to Bitcoin launched in 2011 [33]. It operates similarly to Amazon and eBay, where anonymous sellers are able to sell goods and services to anonymous consumers [70]. The market ran as a Tor hidden service using Bitcoin as the medium of exchange [19]. The market sold a large variety of goods, such as unlicensed firearms and drugs (both legitimate and illegitimate), and services such as assassination, botnets, malware and targeted hacking. The initial version, 1.0, operated for over two years and the second version, 2.0, for a year before both being shut down by the FBI [7, 37].

In 2013, Christin [33] published an in-depth measurement study of Silk Road, analysing the types of products sold, the evolution of sellers including their countries of origin, and economic indicators, including the use of Bitcoin and sales volume. With regards to Bitcoin, they estimated that over a 29-day span the marketplace transacted 1.3M BTC (1.22M USD), which they believe corresponded to between 4.5% and 9% of all exchange trades. The Bitcoin analytics in the paper are very short and the authors make no attempts to trace the illicit funds, however this is acknowledged as not being the primary focus. In 2014, Spagnuolo et al. [136] used their Bitcoin tracing, classification, and verification system to analyse crime and perform an analysis of potential connections between the Silk Road cold wallet and its founder, and measured on-chain crime from the CryptoLocker ransomware. We discuss this paper earlier in Chapter 3.2.1.

Many new anonymous market places have been created since the closure of Silk Road, with recent crime studies reporting an increasing trend in dark market revenues and competition. In 2015, Soska et al. [135] performed a long term measurement analysis of 35 marketplaces across two years, detailing the growth of the underground ecosystems. In their study they scraped and parsed the data from these market places across multiple snapshots to analyse how the system evolved over time. Through analysing sales volumes in Silk Road, they projected the marketplace produced $100M USD a year, which was in accordance with the amounts projected by the US government. Overall, they estimate that the ecosystem transacts over $500,000 USD per day. Market place closures and shutdowns resulted in users moving their business elsewhere, and that, interestingly, the ecosystem was resilient to scams and law enforcement take-downs. In terms of limitations, it is unclear whether the researchers have made their datasets available for others to use in their own research. Some of the datasets are censored due to insufficient amounts of data collected. The authors did not appear to directly interact with the services as estimated sales volume is predicted based on user feedback instead of real transactions.

Markets are, however, actively shut down, either voluntarily (Sheep Market place [130]) or forcefully by law enforcement (Utopia [57]). Further analysis of underground markets includes the following works [66, 67, 86, 137, 20], however these do not focus on cryptocurrency transactions but demonstrate techniques used to collect data.

3.3.2 Thefts, Ransomware and Sextortion

Cryptocurrency exchanges and user accounts have been subjected to numerous cases of theft. Opened in July 2010, Mt Gox was one of the worlds largest digital asset exchanges, allowing users to trade via standardised market methods [142]. At its peak the service was responsible for handling over 70% of all bitcoin transactions [55]. In 2011, it was reported that someone had been gradually stealing coins from the exchange-owned wallets, siphoning 750,000 bitcoins ($330 million USD) which subsequently caused the company to file for bankruptcy [154].

In 2015, the Bitstamp exchange was breached and hackers stole 19,000 bitcoins ($5 million USD) [65]. Employees from Bitstamp were targeted through phishing campaigns which ran for weeks. The attackers distributed malware via Skype and email channels, compromising internal machines. In 2016, Bitfinex, a Hong Kong based exchange, was also breached with hackers stealing 119,756 BTC ($72 million USD) causing a 20% drop in the Bitcoin price when announced [22, 31].

Lazarenko et al. [84] list and classify 48 attacks on blockchain projects which had lead to theft of coins. These attacks are grouped into eight categories, some of which include insider attacks, phishing and malware. For each project attacked, they list the number of coins lost and detail the cause. Their analysis shows that the number of attacks on blockchain projects has increased annually, likely due to the increase in available technologies. Exchanges had been subject to the most thefts and attacks on Bitcoin, whereas Ethereum Initial Coin Offerings (when an unregulated entity raises money through distribution of cryptocurrency assets) had the most Ether stolen. Overall the report finds that 59% of blockchain related projects are closed after a cyber attack. The analysis in the paper is very brief, and the paper simply lists out a number of attacks, however this is due to the research being classified as a survey rather than an in-depth study.

Since 2012 a new type of malware has emerged: ransomware. It is malicious software that prevents a user from accessing their computer until they pay a certain amount to the operator. The payloads are spread through a variety of ways, for example through malicious email attachments [2] or via exploited vulnerabilities [100]. In May 2017 the ransomware WannaCry attacked Windows Machines worldwide, encrypting user data and holding it as ransom, requiring users to pay with bitcoin to regain access. Some of the infected machines belonged to national hospitals and telecommunication companies [82]. The ransomware caused an estimated $4 billion USD worth of damage [17]. After the outbreak, it was discovered that the attackers had used the cross-currency exchange ShapeShift to convert their tainted Bitcoins into Monero, which was reported to then ’disappear’ [56].

Conti et al. published an in-depth study of ransomware on Bitcoin, presenting techniques to identify, collect and analyse transaction data [36]. They present an identification framework to identify extorted ransom transactions which consists of three components. First is the identification of addresses from online resources, removal guides and threat reports. These are then clustered using both the multi-input and change heuristics. Next is the extraction of all transactions which contain these addresses, and finally, the classification of the amounts received as ransom if at least one of their payment conditions is satisfied. This methodology is applied to twenty ransomware cases, and for each they detail payment strategies, methods of infection and ransoms extorted. Overall ransomware operators earned an excess of 3M USD, and the operators of WannaCry earned 238 payments averaging a total of 86k USD (47 BTC), compared to the operators of CryptoWall who obtained 2.2M USD (5,351 BTC). The work is very thorough and the appendices list all the addresses used in the initial portions of the investigation, which is useful for future research. Limitations of the work include that the ransom addresses are collected from public sources and such data quality cannot be guaranteed, however they compare their results and find that it is similar to previous works.

Paquet-Clouston et al. [113] present methods identifying illicit Bitcoin transactions by focusing on 35 ransomware families. The work obtains, clusters and filters a set of seed addresses obtained from researchers and online sources. By following the flow of money, they found that multiple ransomware families interacted with the same actor. Across four years they reveal a lower bound of over 22k BTC ($12M USD) in ransomware payments, with the Locky ransomware receiving over $7.8M USD and more than 50% of payments. The researchers concluded that a small number of actors, just three families, dominated this genre of crime and were accountable for 86% of the marketshare.

Huang et al. [71] created a framework to track ransomware end-to-end and applied this to real-world cases across a two-year period. They first obtained a list of addresses from public ransomware infection reports, seed addresses and a form of synthetic address (victims they created and tracked by sending operators micro-payments). These were turned into clusters using co-spend heuristics, and transactions to and from the clusters were filtered and analysed. Overall, they estimated that operators from 10 ransomware attackers obtained $16M USD from 20k potential victims. Through looking at inflows to clusters, it is found that exchanges account for 40% of payments. They also revealed that BTC-e, a Russian exchange, prior to being seized by US law enforcement, was a key exit point used for criminals in the Locky and CryptoDefense ransomwares, as they saw $3M USD flow through their exchange.

Some scams feed on the fear, gullibility and technical infancy of the target users. Paquet-Clouston et al. [114] analysed emails sent by criminals to victims of sextortion scams requesting bitcoin as payment. Sextortion is a spam scheme whereby an attacker emails victims, claiming that sensitive and private photos or videos will be leaked to their contacts unless they are paid some bitcoins. The researchers analysed 4.3M emails, bucketing emails into 15 campaigns and extracted all bitcoin addresses. They extracted 245 addresses from the emails, which when clustered and filtered came to 485 payment addresses that had received coins. Their analysis revealed that scammers attempt to extort higher amounts of coins based on the language used in the emails, Emails written in the English language asked for a mean of $745 USD whereas Spanish language scams were asked for $249, indicating that attackers adjusted their prices based on the victims’ perceived language and location. By following cash flows from the spam clusters, they discovered that entities were moving coins to known exchanges. However, this part of tracing is very limited as tags were obtained from an open source website. By analysing the campaigns they identified that multiple clusters appeared across multiple campaigns, suggesting that the majority of revenue was collected by a single real world entity. Untagged clusters were sent 48 BTC (17% of revenue), and these were mentioned to possibly be potential cash-out services. In conclusion, they estimated that one entity may be responsible for the majority of crimes, with scammers harnessing a lower bound of over $1 million USD within 11-months. In terms of limitations, the addresses were obtained from a data set which was caught by a spam filter, and thus may not have reached most recipients, thus the estimations are a lower bound and only cover a small section of this ecosystem. The multi-input heuristic may have clustered in addressess belonging to the same author but perhaps different scams. The source of the tags is extremely limited, and thus it is unclear exactly how many of the coins were sent to and from exchanges.

3.3.3 Investment Programs and Money Laundering

Past research has quantified and described crime and scams running on blockchain ecosystems that use high return investment programs and ponzi schemes as well as mixing services as a form of money laundering.

Vasek et al. [146] presented analysis of four types of scams (ponzi schemes, mining scams, scam wallets and exchanges) that used Bitcoin, identifying 192 scams and tracking their payments. By collecting scams from various data sets online, and after a cleaning process, they extracted all relevant transactions from the Bitcoin blockchain. They modelled 42 scams into four categories and analysed each. One class of scams they analysed was high yield investment programs (HYIPs). These are schemes that promise investors a high rate of return. Previous investors are paid by new investors, and this process repeats until the scheme closes or collapses. By comparing traditional HYIPs to Bitcoin based HYIPs, they found that Bitcoin was not yet widely accepted. However, some act more traditionally using fiat currency and then transitioning into Bitcoin. From these, they identified a user who earned 1.6M USD. Another category they analysed was scam wallets. These are online wallets that claim to host Bitcoin for users, but the operators, in-fact, steal the coins that have been deposited. One scam wallet in particular earned 4,100 BTC ($1M USD). Overall, they found that scammers earned $11 million USD from 13,000 victims. The research within this paper is very thorough, covering a wide variety of scams including economic perspectives. The work however only focuses on how many coins were received and they do not track the illicit funds after they have been received.

In 2018, Bartoletti et al. [11] applied data mining techniques and machine learning algorithms to detect Ponzi schemes in Bitcoin. Ponzi schemes are a form of HYIP where users of the schemes are paid only by other new users that join the scheme. They collected 32 addresses belonging to ponzis and through clustering obtained 1211 addresses. Analyses revealed that these received $10M USD worth of deposits. Using these clusters they derived and extracted features (e.g., statistics, measures of inequality) from both these and random addresses. By testing a range of supervised binary classifiers, they found that the random forest algorithm was correctly able to identify 96% of addresses as ponzi schemes. This experiment is very thorough, and the authors released addresses and features used and tested across multiple classifiers and ponzi schemes. The limitations are that this approach was only tested against ponzi schemes, so it would be interesting to see whether it is applicable to other types of scams.

Bitcoin is not the only cryptocurrency prone to being targeted by crime; this behaviour also occurs on Ethereum. Chen et al. [32] used data mining and machine learning to detect Ponzi schemes, scams that fraudulently promise high returns by generating income for previous investors by taking money from later investors. They first analyse a known smart contract ponzi scheme by studying the transactions betwen the contract and participants. With this they developed sets of features that are key to ponzi schemes. The first set of features looks at statistics, including the number of payments into and out, and the proportion of users who sent money to the coin before ever receiving anything in return. The second set analyses the use of opcodes, assembly like commands used by contracts extracted from the Ethereum Virtual Machine. These features were tested with a machine learning algorithm that classified whether the contract resembled a ponzi scheme. The classifier was tested on 54 previously known ponzi schemes and was able to detect 45 schemes. The undetected 9 were manually investigated and found not to be ponzi schemes. Out of 280k contracts on Ethereum, they estimate that 434 ponzi scheme smart contracts exist. In terms of limitations, the reasoning for the machine learning algorithm is not convincing, it would be clearer to compare this against other algorithms to justify the decision. The results detected 386 algorithms that were not checked, and it would have been helpful to take a random sample to manually check whether they could be confirmed.