1]School of Mathematics and Statistics, Xi’an Jiaotong University, Xi’an, China. 2,*]School of Mathematics and Statistics, Xi’an Jiaotong University, Xi’an, China.

[*]Dandan Jiang, School of Mathematics and Statistics, Xi’an Jiaotong University, Xi’an, China. Email: jiangdd@mail.xjtu.edu.cn

Determining the number of factors in a large-dimensional generalised factor model

Abstract

This paper proposes new estimators of the number of factors for a generalised factor model with more relaxed assumptions than the strict factor model. Under the framework of large cross-sections and large time dimensions , we first derive the bias-corrected estimator of the noise variance in a generalised factor model by random matrix theory. Then we construct three information criteria based on , further propose the consistent estimators of the number of factors. Finally, simulations and real data analysis illustrate that our proposed estimations are more accurate and avoid the overestimation in some existing works.

keywords:

Factor model; Noise estimation; Number of factors; Information criteria1991 Mathematics Subject Classification:

C13, C38, C431. Introduction

With the rapid development of information technology, the factor models with large cross-sections and time-series dimensions have emerged more intensively in the fields of economy and finance. For example, it can be used to determine the tick-by-tick transaction prices of a large number of assets, and to depict the leading eigenvalues of the coincident indexes in macroeconomics, and so on. The factor model reveals the intricate relationship of the mass of variables through several common factors and simplifies the model structure.

A critical problem of factor models is to determine the number of static factors or dynamic factors. “Dynamic” refers to whether the common factor itself is modeled as a dynamic process. If it is assumed that does not have an auto-correlation structure, i.e. , the dynamic factor is transformed into a static factor. There is a lot of literature on this issue for both static and dynamic factor models. On one hand, Bai and Ng (2002), Onatski (2006, 2010), Alessi et al. (2010), Ahn and Horenstein (2013), Caner and Han (2014) studied on the estimation of the number of static factors. On the other hand, Forni et al. (2000), Hallin and Liska (2007), Amengual and Watson (2007), Bai and Ng (2007), Onatski (2009), etc. investigated on the determination of the the number of dynamic factors. Moreover, the factor models are closely related to principal component analysis (PCA) models and spiked models in random matrix theory. Many related works to determine the number of factors/principal components/spikes are developed, such as Kritchman and Nadler (2008), Ulfarsson and Solo (2008), Johnstone and Lu (2009), Passemier and Yao (2012), Passemier et al. (2017), etc.

In this paper, we focus on the static factor model and propose new estimators of the number of factors by random matrix theory, as both the cross-section units and time series observations go to infinity. Within this context, a pioneering work is developed by Bai and Ng (2002), which provided some information criteria for estimating the number of factors and established the consistency of the estimators of the number of factors as simultaneously. Following their work, Alessi et al. (2010) improved their criteria by introducing a tuning multiplicative constant in the penalty. More recently, Passemier et al. (2017) modified the information criteria to determine the number of factors for the strict factor model.

However, these existing works are constrained by different reasons. Practical analysis shows that the information criteria developed by Bai and Ng (2002) often led to non-robust estimations, i.e. the number of factors may be overestimated (see e.g. the application on U.S. macroeconomic data in Forni et al. (2009)). Alessi et al. (2010) considered a factor model with the idiosyncratic components only being mildly cross-correlated. Passemier et al. (2017) required the idiosyncratic components to be independent and the population covariance of the observations to be a finite-rank perturbation matrix on the identity matrix.

The main contributions of our work are reflected in the following points. First, we relax the independent distributed assumptions of in Passemier et al. (2017), and generalise the strict factor model to a more general form. Thus, for our target model, the population covariance matrix of the observations can be regarded as a more generalised spiked population covariance matrix as mentioned in Jiang and Bai (2021a). Second, we establish the new information criteria by random matrix theory, and propose more accurate estimators of the number of factors. Compared with the existing works, our proposed estimators provide the smaller standard errors as illustrated in the simulations. Moreover, we also prove the consistency of our estimators as and approach infinity. Finally, although our method is constructed under the framework of large and , the estimations of the number of factors are still robust even if both and are small. As shown in simulation study, when and , our estimations are much closer to the true number of factors, while the estimations in Bai and Ng (2002) fail for finite samples.

The arrangement of this article is as follows. First, we generalise the strict factor model and introduce the bias-corrected estimator of the noise variance in Section 2. Then we construct three new information criteria based on the above bias-corrected noise estimator, and give the new estimators of the number of factors for a generalised factor model in Section 3. As a by-product, we also prove the consistency of our proposed estimators as simultaneously. In Section 4, the Monte Carlo simulations are conducted to evaluate the performance of the proposed estimators of the number of factors. In Section 5, we apply our proposed methods to some real data sets to illustrate their feasibility in practice.

2. Estimation on the variance of the noise in a generalised factor model

2.1. A bias-corrected estimation of the noise variance

We consider the generalised factor model with the following form

| (1) |

where is an -dimensional cross-section vector at time , is an matrix of factor loading, is an -dimensional vector of common factors, represents the general mean and is an idiosyncratic error vector. Compared with the strict factor model, which assumes that the covariance matrix of in the model (1) is , we extend this assumption to a general case of , where the matrix is a general Hermitian matrix. The matrix satisfies the following points: First, the eigenvalues of are scatted into spaces of several bulks of the general population eigenvalues. Second, the independent assumption of can be removed. Thus the model in (1) is so-called a generalised factor model.

To develop meaningful asymptotic theory in the large-dimensional setting, we assume that both and go to infinity proportionally, i.e. , as . Therefore, the population covariance matrix of is

| (2) |

To ensure the identification of the model, we impose some assumptions on the model parameters, as mentioned in Anderson (2003) : {assumption} and {assumption} is diagonal matrix of distinct diagonal eigenvalues. Then the population covariance matrix in (2) is exactly the generalised spiked population covariance proposed in (Jiang and Bai, 2021a), which has the spectrum form as

| (3) |

where are spikes with multiplicity , , respectively, satisfying with the fixed integer . The rest are non-spiked eigenvalues, where is a fixed small number. Moreover, we assume that the empirical spectral distribution (ESD) of converges weakly to a nonrandom probability distribution on the real line as , which follows a probability distribution and takes the value in probability and .

The spiked model describes a phenomenon of a few perturbations to a positively definite matrix, see the references such as Johnstone (2001),Bai and Yao (2008, 2012), Jiang and Bai (2021a), etc. By the close relationship between the factor model and the spiked model, to determine the number the factors is equivalent to find the number of the spikes in the spiked covariance matrix . Thus we focus on the study of the spiked eigenvalues of the matrix . Following the works in Passemier et al. (2017), it is necessary to get an accurate estimation of before estimating the number of factors (or spikes). Then, we refer the work of Jiang (2022), which provided a bias-corrected estimation based on random matrix theory.

Before introducing it, we first provide some preliminary knowledge. Decompose the population covariance matrix as , where ∗ denotes conjugate transposition. Let , then can be seen as random samples from the population covariance matrix . And the corresponding sample covariance matrix of is

| (4) |

which is the generalised spiked sample covariance matrix. It is should be noted that if the mean parameter is unknown, the sample covariance matrix (4) needs to be replaced by an unbiased form, and the corresponding ratio should be replaced by .

We denote the set of ranks of with multiplicity among all the eigenvalues of as , and represent the eigenvalues of sorted in descending order as . According to the classical statistical theory, the maximum likelihood estimator of can be obtained as

| (5) | ||||

which can be viewed as an appropriate estimation of the noise variance . However, it is well known that the sample eigenvalues do not converge to the population ones when the cross-section dimension is large compared to the time dimension . Therefore, the estimator (5) will underestimate the true noise variance .

To this end, Jiang (2022) established the central limit theorem of in the large-dimensional setting, and gave the corresponding bias-corrected estimation. To refer this work, we define with for real case and 0 for complex, where is the first element of . We denote as the LSD of the sample matrix , and further as the Stieltjes Transform of Then the bias-corrected estimator of the noise variance is given in the following proposition.

2.2. Monte Carlo experiments

Since Jiang (2022) only performed the simulations for the case of equal non-spikes, we design the following simulation to verify the feasibility of Proposition 2.1 in our model for more complex cases. We first set up the following models:

- Model 1.:

-

Assuming that , where , is an matrix with spikes of the multiplicity (1, 2, 1) and non-spikes 2 of time, non-spikes 1 of time.

- Model 2.:

-

Assuming that , where is defined in Model 1, is composed of eigenvectors of an matrix with the entries of being independently sampled from standard Gaussian population.

Moreover, for each model, the Gaussian and Gamma populations are studied to show the conclusion is extensively utilisable without the limitations of population.

- Gaussian Assumption.:

-

are samples from standard Gaussian population;

- Gamma Assumption.:

-

are samples from .

Next we will compare with and several other existing noise variance estimators. The definitions of these estimators are given below.

-

(a)

The estimator in Passemier et al. (2017) is also a bias correction of the maximum likelihood estimation of the noise, but for the case where the non-spikes are all 1 and are independent, which is defined as

where is the maximum likelihood estimation of the noise given in their work.

-

(b)

The estimator in Kritchman and Nadler (2008) is described as the solution of the following system of nonlinear equations with unknowns,

and

-

(c)

The estimator in Ulfarsson and Solo (2008) is defined as the ratio of the median of the non-spike sample eigenvalues to the the median of the Marčenko-Pastur distribution ,

where is the median of .

-

(d)

The estimator in Johnstone and Lu (2009) is defined as the median of the variances across all dimensions of the samples,

where are the centralised data of the original samples .

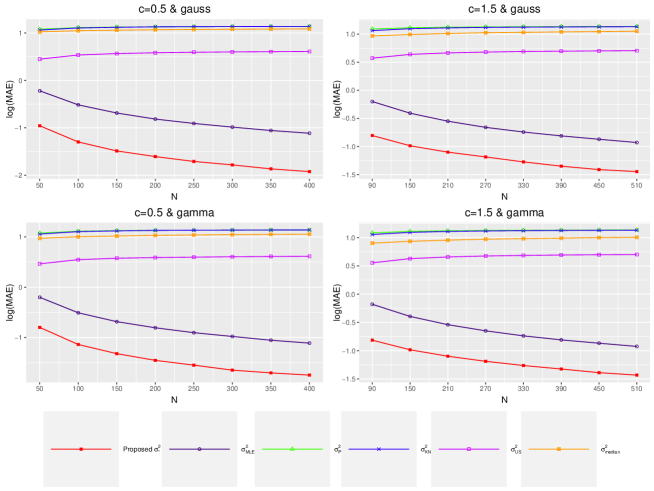

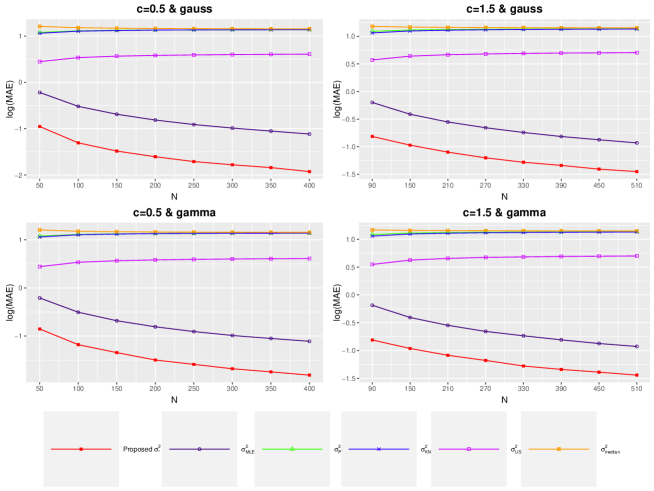

We respectively simulate the numerical logarithm transformed mean absolute error (MAE) with 1,000 replications as increases for and . When the ratio is set to be , the value of is set to , respectively. And when the ratio is set to , the value of is set to , respectively.

The results are reported in Figure 1 and 2 . Under different models and distributions, the proposed bias-corrected estimator has the smallest logarithm transformed MAE. As the increases, the logarithm transformed MAE of becomes smaller and smaller. However, the estimator , and obviously fail to estimate in our model. In addition, the numerical results of and are so close that their corresponding curves are not easy to distinguish on the Figure. To show the results more accurately, we put the original simulation values in the Appendix.

3. Estimation on the number of factors in a generalised large-dimensional factor model

In this section, we will construct the new information criteria based on , and propose the estimators of the number of factors for our generalised factor model. Recall the work in Bai and Ng (2002), the common factor and the factor loading can be estimated by the asymptotic principal components method in a large panel. The asymptotic principal component method minimises

| (7) |

subject to the normalisation , where is the factor loading matrix, is factor matrix, respectively. To be specific, under the normalisation of , we adopt as the estimated factor matrix minimising , where is the eigenvector corresponding to the th largest eigenvalue of . Then, applying the least square method, we can obtain the corresponding factor loading matrix, .

According to the knowledge of the linear model, the formula (7) is a decreasing function of . With the increasing integer , we will get the smaller squared error loss . But selecting the excessive number of factors will lose the efficiency of the model, and the simplicity of the model cannot be guaranteed. For this reason, Bai and Ng (2002) developed the penalty function relied on both and , and avoided over fitting. Let , then a loss function can be used to determine the number of factors. In order to balance the goodness of fit and simplicity of the model, Bai and Ng (2002) generalised the criterion of Mallows (1973) and suggested three criteria under the framework of large and as follows:

| (8) |

where , is a consistent estimator of , and ’s are different penalty functions

with .

All of these penalty functions satisfy two conditions: (i) , (ii) as .

The in (8) plays a role as an appropriate scaling parameter for the penalty term. Bai and Ng (2002) recommended replacing it with , where is a bounded integer such that . The estimators of the number of factors corresponding to the three information criteria are .

As mentioned in the Introduction, the method proposed by Bai and Ng (2002) often overestimate the number of factors. To improve this problem, we construct the new information criteria based on the bias-corrected noise estimator in proposition 2.1. In fact, and are indeed estimations of the noise variance in model (1). Then we substitute in (8) by , where is the function of with definition in Proposition 2.1. Moreover, we substitute by . Thus, our proposed new information criteria and the estimators of the number are obtained in the following theorem.

Theorem 3.1.

For the determination of the number of factors in the generalised factor model (1), we propose three information criteria as follows

| (9) | ||||

and the corresponding estimators of the number of factors are

Furthermore, we establish the consistency of the corresponding estimators of as and give the proof as follows.

Theorem 3.2.

Let and . Then we have , where is the true number of factors .

Proof 3.3.

We are going to prove that for all and , where stands for all , because they have the same limiting properties. Since

it is sufficient to prove

| (10) |

or

| (11) |

as

Since both and are bounded positive values, the right-hand side of (12) is bounded. The inequality (10) will hold if the penalty satisfies

| (13) |

for large and . And we have , the right part of inequality expression (13) is a bounded value, and the conclusion follows.

Next, for , we have

| (14) |

where represents the maximum likelihood estimation of when the population covariance matrix has spikes.

The first and the third terms on the right side of expression (14) are both . Next, consider the second term. When the number of real population spikes is and , there is only a difference of spikes between the two populations. We retain Assumption B about the factor loadings in Bai and Ng (2002), that the factor loadings grow to with the dimension .

It implies that the second term is a positive bounded value. Since as , the inequality (11) holds.

The conclusion follows.

4. Simulation study

To check the improvement performance of our proposed information criteria, Monte Carlo simulations are conducted. we refer the data generating process in Bai and Ng (2002), which is expressed as

with the factors being variates and . Different from simulated design in Bai and Ng (2002) and Passemier et al. (2017), we generalised the settings as and , where , is diagonal or off-diagonal matrix listed in Model 3 to 5, and are random variables such that .

- Model 3.:

-

Assuming that , where is an identity matrix.

- Model 4.:

-

Assuming that , and , where eigenvalues 2 and 1 are half and half.

- Model 5.:

-

Assuming that , where is defined in Model 4, and is defined in Model 2.

By the generalised settings, we relax the independent or mild cross-correlated assumptions of the error sequence than previous works. Furthermore, we reuse the two population assumptions of in subsection 2.2

| () | ||||||

|---|---|---|---|---|---|---|

| Mode3 under Gaussian assumption | ||||||

| 4.00 | 4.00 | 4.32(0.48) | 4.00 | 4.00 | 4.00 | |

| 4.00 | 4.00 | 4.16(0.37) | 4.00 | 4.00 | 4.00 | |

| 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | |

| 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | |

| 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | |

| 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | |

| 4.00 | 4.00 | 4.72(0.57) | 4.00 | 4.00 | 4.00 | |

| 4.00 | 4.00 | 4.27(0.46) | 4.00 | 4.00 | 4.00 | |

| 4.00 | 4.00 | 4.16(0.36) | 4.00 | 4.00 | 4.00 | |

| 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | |

| 8.00 | 8.00 | 8.00 | 4.01(0.60) | 3.98(0.61) | 4.05(0.60) | |

| 8.00 | 8.00 | 8.00 | 3.92(0.36) | 3.91(0.36) | 3.93(0.33) | |

| 5.50(0.66) | 4.92(0.64) | 6.78(0.66) | 4.00 | 4.00 | 4.00 | |

| 5.53(0.65) | 4.95(0.61) | 6.79(0.65) | 4.32(0.50) | 4.11(0.32) | 5.32(0.77) | |

| Model3 under Gamma assumption | ||||||

| 4.00(0.03) | 4.00 | 4.69(0.57) | 4.00 | 4.00 | 4.01(0.11) | |

| 4.00 | 4.00 | 4.47(0.54) | 4.00 | 4.00 | 4.00 | |

| 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | |

| 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | |

| 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | |

| 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | |

| 4.00 | 4.00 | 5.11(0.60) | 4.00 | 4.00 | 4.00 | |

| 4.00(0.03) | 4.00 | 4.69(0.59) | 4.00 | 4.00 | 4.00 | |

| 4.00 | 4.00 | 4.49(0.54) | 4.00 | 4.00 | 4.00 | |

| 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | |

| 8.00 | 8.00 | 8.00 | 4.04(0.47) | 3.97(0.43) | 4.11(0.53) | |

| 8.00 | 8.00 | 8.00 | 3.93(0.25) | 3.93(0.26) | 3.94(0.24) | |

| 5.93(0.67) | 5.35(0.65) | 7.13(0.65) | 4.00 | 4.00 | 4.00 | |

| 5.92(0.66) | 5.35(0.67) | 7.11(0.62) | 4.73(0.66) | 4.38(0.55) | 5.82(0.80) | |

| () | ||||||

|---|---|---|---|---|---|---|

| Mode4 under Gaussian assumption | ||||||

| 4.00(0.03) | 4.00 | 4.82(0.58) | 4.00 | 4.00 | 4.01(0.09) | |

| 4.00 | 4.00 | 4.81(0.59) | 4.00 | 4.00 | 4.00 | |

| 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | |

| 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | |

| 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | |

| 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | |

| 4.00 | 4.00 | 6.08(0.65) | 4.00 | 4.00 | 4.00 | |

| 4.00 | 4.00 | 5.54(0.66) | 4.00 | 4.00 | 4.00 | |

| 4.00 | 4.00 | 5.25(0.62) | 4.00 | 4.00 | 4.00 | |

| 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | |

| 8.00 | 8.00 | 8.00 | 4.067(0.69) | 3.96(0.62) | 4.26(0.82) | |

| 8.00 | 8.00 | 8.00 | 3.90(0.42) | 3.87(0.41) | 3.94(0.44) | |

| 6.98(0.63) | 6.41(0.66) | 7.86(0.38) | 4 | 4.00(0.04) | 4 | |

| 5.85(0.67) | 5.26(0.62) | 7.08(0.64) | 4.67(0.63) | 4.31(0.49) | 5.73(0.80) | |

| Model4 under Gamma assumption | ||||||

| 4.02(0.13) | 4.00(0.03) | 5.22(0.64) | 4.00 | 4.00 | 4.08(0.27) | |

| 4.00 | 4.00 | 5.19(0.61) | 4.00 | 4.00 | 4.02(0.13) | |

| 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | |

| 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | |

| 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | |

| 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | |

| 4.00 | 4.00 | 6.52(0.68) | 4.00 | 4.00 | 4.01(0.09) | |

| 4.12(0.32) | 4.01(0.11) | 5.91(0.67) | 4.00 | 4.00 | 4.00(0.03) | |

| 4.00(0.04) | 4.00 | 5.64(0.66) | 4.00 | 4.00 | 4.00(0.04) | |

| 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | |

| 8.00 | 8.00 | 8.00 | 4.30(0.83) | 4.18(0.76) | 4.50(0.92) | |

| 8.00 | 8.00 | 8.00 | 3.98(0.56) | 3.94(0.53) | 4.04(0.62) | |

| 7.08(0.64) | 6.56(0.69) | 7.91(0.29) | 4.00 | 4.00(0.03) | 4.01(0.10) | |

| 6.23(0.69) | 5.68(0.66) | 7.36(0.61) | 5.12(0.75) | 4.66(0.63) | 6.19(0.80) | |

| () | ||||||

|---|---|---|---|---|---|---|

| Model5 under Gaussian assumption | ||||||

| 4.00 | 4.00 | 4.85(0.63) | 4.00 | 4.00 | 4.01(0.11) | |

| 4.00 | 4.00 | 4.78(0.58) | 4.00 | 4.00 | 4.00 | |

| 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | |

| 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | |

| 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | |

| 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | |

| 4.00 | 4.00 | 6.09(0.65) | 4.00 | 4.00 | 4.00 | |

| 4.02(0.13) | 4.00 | 5.52(0.64) | 4.00 | 4.00 | 4.00 | |

| 4.00 | 4.00 | 5.26(0.64) | 4.00 | 4.00 | 4.00 | |

| 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | |

| 8.00 | 8.00 | 8.00 | 4.11(0.73) | 4.00(0.65) | 4.29(0.85) | |

| 8.00 | 8.00 | 8.00 | 3.96(0.40) | 3.90(0.39) | 3.97(0.44) | |

| 6.99(0.63) | 6.39(0.63) | 7.87(0.34) | 4.00(0.03) | 4.00(0.04) | 4.00(0.03) | |

| 5.87(0.66) | 5.31(0.65) | 7.13(0.64) | 4.68(0.64) | 4.29(0.47) | 5.76(0.79) | |

| Model5 under Gamma assumption | ||||||

| 4.01(0.12) | 4.00 | 5.19(0.65) | 4.00 | 4.00 | 4.06(0.24) | |

| 4.00 | 4.00 | 5.15(0.64) | 4.00 | 4.00 | 4.00(0.08) | |

| 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | |

| 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | |

| 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | |

| 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | |

| 4.00 | 4.00 | 6.41(0.67) | 4.00 | 4.00 | 4.00(0.05) | |

| 4.08(0.27) | 4.00(0.06) | 5.86(0.67) | 4.00 | 4.00 | 4.00 | |

| 4.00 | 4.00 | 5.58(0.64) | 4.00 | 4.00 | 4.00 | |

| 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | 4.00 | |

| 8.00 | 8.00 | 8.00 | 4.27(0.79) | 4.11(0.71) | 4.50(0.90) | |

| 8.00 | 8.00 | 8.00 | 3.98(0.50) | 3.95(0.49) | 4.05(0.57) | |

| 7.15(0.62) | 6.62(0.64) | 7.92(0.28) | 4.00 | 4.00 | 4.0090.06) | |

| 6.23(0.68) | 5.67(0.65) | 7.36(0.60) | 5.07(0.71) | 4.63(0.63) | 6.20(0.79) | |

Reported in Tables 1 to 3 are the empirical means of the estimations of the number of factors over 1,000 replications, corresponding to Model 3 to 5 respectively. The standard errors are also given in parentheses following the estimations. If the standard error is 0, no further annotations will be made. Refer to Passemier et al. (2017), for these six scenarios, the predetermined maximum number of factors is set to 8.

As shown in the simulated results, our proposed information criteria have an overall better performance than in Bai and Ng (2002) for different models and populations. When , both information criteria and can obtain satisfactory estimation of the number of factors. But our estimation are more accurate with smaller standard errors. When , the original information criteria almost report the predetermined maximum value 8, but the estimation of our method is closer to the true value 4. In addition, when the population assumption is gamma distribution, the efficiency of detecting the true number of factors of in Bai and Ng (2002) is lower than that of Gaussian distribution, but our new information criteria perform still well for the non-Gaussian assumptions. When the error sequence no longer satisfy the independent assumption, our method also outperforms in Bai and Ng (2002).

5. Real data analysis

The proposed information criteria seem to work rather well in the simulated experiments. We now apply the new procedure of determining the number of the factors to two real data sets. Both data sets are downloaded from https://www.oecd.org. The first is the OECD Composite Leading Indicators (CLI) data set, which is constructed by weighting indicator data in various fields of the national economy according to certain standards. It is a leading indicator reflecting a country’s macroeconomic development cycle. And this data set consists of CLI for 32 OECD countries, 6 non-member economies and 8 zone aggregates () observed monthly from June 1998 to October 2020 (). The second data set contains OECD Business Confidence Indicators (BCI) data for 36 OECD countries, 6 non-member economies and 6 zone aggregates () observed monthly from November 2003 to May 2021 ().

In practice analysis, we need to pay attention to the chosen of , which will effect the robustness of estimations. Since the matrix has only non-zero spiked eigenvalues, but the rest tailed eigenvalues are all zero, so that we only need to select an arbitrary large integer , and then we can obtain the robust estimations. But in practical applications, except the spiked eigenvalues, the tailed eigenvalues of are not all zeros, but most of them are relatively small values close to zero. Due to this reason, should be selected to sufficiently ensure the inclusion of the most of non-zero eigenvalues. According to practical experience, we adopt the selection of in the range of to .

Then, we apply the information criteria of Bai and Ng (2002) and our proposed criteria to estimate the number of factors for the real data sets. The estimate results on the two data sets are shown in Table 4 and 5. The three rows of the tables correspond to the estimations when is selected as , and , respectively. It suggests that the original criteria ’s seriously overestimate for the two data sets. In contrast, when , our proposed information criteria ’s estimate the number of factors for both data sets to be 10 or 11, and the corresponding cumulative contribution rate can reach 95%. It implies that 10 or 11 is a reasonable estimation of the number of factors for both data sets.

| 24 | 23 | 27 | 8 | 8 | 9 | |

| 32 | 32 | 32 | 10 | 10 | 11 | |

| 37 | 37 | 37 | 13 | 13 | 14 |

| 23 | 22 | 27 | 8 | 8 | 9 | |

| 34 | 34 | 34 | 10 | 10 | 11 | |

| 38 | 38 | 38 | 12 | 12 | 13 |

6. Conclusion

This paper aimed to determine the number of factors in a large-dimensional generalised factor model with more relaxed assumptions than that of previous works. For the target model, we introduced the bias-corrected noise estimator by random matrix theory, further construct the information criteria based on , and estimate the number of factors consistently. The good performance of our method is demonstrated by simulations and empirical applications. This paper only focused on the static factor models. Further we will improve the information criteria to accommodate the dynamic factor models in the future work.

Appendix A The logarithm transformed MAEs among several noise estimators

| Estimators | ||||||

|---|---|---|---|---|---|---|

| Under Gaussian assumption and | ||||||

| -0.95594 | -0.21996 | 1.079281 | 1.061465 | 0.448425 | 1.023963 | |

| -1.29808 | -0.51528 | 1.113894 | 1.105469 | 0.535754 | 1.04767 | |

| -1.48663 | -0.68761 | 1.124752 | 1.119236 | 0.565924 | 1.059354 | |

| -1.60601 | -0.81515 | 1.130371 | 1.129887 | 0.582757 | 1.067715 | |

| -1.70851 | -0.90724 | 1.133389 | 1.133012 | 0.59349 | 1.074012 | |

| -1.78126 | -0.98528 | 1.13551 | 1.135202 | 0.600825 | 1.078858 | |

| -1.86527 | -1.05624 | 1.137166 | 1.136905 | 0.605671 | 1.082972 | |

| -1.92219 | -1.11401 | 1.138295 | 1.138069 | 0.609859 | 1.086277 | |

| Under Gaussian assumption and | ||||||

| -0.80542 | -0.2007 | 1.089998 | 1.062031 | 0.571411 | 0.967804 | |

| -0.98767 | -0.40775 | 1.112526 | 1.095778 | 0.638532 | 0.992417 | |

| -1.10124 | -0.55065 | 1.122464 | 1.110508 | 0.664882 | 1.010448 | |

| -1.18679 | -0.66006 | 1.128019 | 1.11872 | 0.679631 | 1.024954 | |

| -1.27469 | -0.74316 | 1.131205 | 1.123598 | 0.690476 | 1.030937 | |

| -1.35075 | -0.81195 | 1.13339 | 1.12695 | 0.695654 | 1.039021 | |

| -1.41206 | -0.87197 | 1.135046 | 1.129465 | 0.700718 | 1.043806 | |

| -1.44716 | -0.93001 | 1.136531 | 1.131607 | 0.704886 | 1.050749 | |

| Under Gamma assumption and | ||||||

| -0.7978 | -0.20039 | 1.074523 | 1.056506 | 0.465334 | 0.972263 | |

| -1.13773 | -0.50752 | 1.113048 | 1.104576 | 0.547863 | 1.003191 | |

| -1.31941 | -0.68424 | 1.124514 | 1.118972 | 0.57605 | 1.017331 | |

| -1.45258 | -0.80535 | 1.129859 | 1.129375 | 0.589596 | 1.031058 | |

| -1.548 | -0.9029 | 1.133208 | 1.132832 | 0.597788 | 1.038072 | |

| -1.64719 | -0.97789 | 1.135253 | 1.134946 | 0.605367 | 1.044539 | |

| -1.70155 | -1.05285 | 1.137067 | 1.136807 | 0.61079 | 1.050343 | |

| -1.74588 | -1.11015 | 1.138197 | 1.137971 | 0.614225 | 1.055111 | |

| Under Gamma assumption and | ||||||

| -0.81382 | -0.17868 | 1.084367 | 1.056048 | 0.5545 | 0.902996 | |

| -0.98342 | -0.3935 | 1.110467 | 1.093598 | 0.628851 | 0.935026 | |

| -1.09768 | -0.53948 | 1.121347 | 1.109331 | 0.658228 | 0.955865 | |

| -1.18749 | -0.64851 | 1.12714 | 1.117806 | 0.675449 | 0.973028 | |

| -1.262 | -0.73747 | 1.130854 | 1.123223 | 0.685124 | 0.982414 | |

| -1.32379 | -0.80877 | 1.133225 | 1.126769 | 0.692978 | 0.99098 | |

| -1.38851 | -0.86749 | 1.134844 | 1.12925 | 0.697477 | 1.000551 | |

| -1.43185 | -0.92462 | 1.136319 | 1.131384 | 0.701558 | 1.00541 | |

| Estimators | ||||||

|---|---|---|---|---|---|---|

| Under Gaussian assumption and | ||||||

| -0.95278 | -0.2181 | 1.07884 | 1.061015 | 0.448869 | 1.208373 | |

| -1.30545 | -0.51772 | 1.114157 | 1.105739 | 0.535016 | 1.180092 | |

| -1.4831 | -0.68824 | 1.124797 | 1.119282 | 0.566147 | 1.169562 | |

| -1.60578 | -0.81338 | 1.130279 | 1.129795 | 0.582211 | 1.16414 | |

| -1.70975 | -0.91001 | 1.133503 | 1.133127 | 0.592704 | 1.160719 | |

| -1.77951 | -0.98689 | 1.135565 | 1.135257 | 0.600081 | 1.158251 | |

| -1.84042 | -1.0515 | 1.137028 | 1.136767 | 0.605395 | 1.156618 | |

| -1.926 | -1.11542 | 1.13833 | 1.138105 | 0.609938 | 1.155565 | |

| Under Gaussian assumption and | ||||||

| -0.81416 | -0.19829 | 1.0894 | 1.061424 | 0.572178 | 1.178899 | |

| -0.971 | -0.41135 | 1.113034 | 1.096288 | 0.640573 | 1.16716 | |

| -1.09756 | -0.5519 | 1.122587 | 1.11063 | 0.666064 | 1.161364 | |

| -1.20135 | -0.65616 | 1.127725 | 1.118427 | 0.680227 | 1.157876 | |

| -1.2806 | -0.74153 | 1.131106 | 1.123497 | 0.689871 | 1.155746 | |

| -1.33833 | -0.81492 | 1.133544 | 1.127105 | 0.696498 | 1.154434 | |

| -1.40564 | -0.874 | 1.135137 | 1.129555 | 0.700147 | 1.1532 | |

| -1.45006 | -0.9301 | 1.136534 | 1.13161 | 0.703742 | 1.152568 | |

| Under Gamma assumption and | ||||||

| -0.85259 | -0.20869 | 1.076574 | 1.058641 | 0.442791 | 1.204876 | |

| -1.17927 | -0.50421 | 1.112681 | 1.104226 | 0.533345 | 1.176478 | |

| -1.34406 | -0.68147 | 1.124317 | 1.118785 | 0.565031 | 1.167195 | |

| -1.49708 | -0.80743 | 1.129969 | 1.129485 | 0.582381 | 1.162066 | |

| -1.58779 | -0.90644 | 1.133356 | 1.132979 | 0.594179 | 1.159008 | |

| -1.67897 | -0.98786 | 1.135598 | 1.13529 | 0.601305 | 1.156902 | |

| -1.74402 | -1.04957 | 1.136971 | 1.136711 | 0.606059 | 1.155449 | |

| -1.81112 | -1.10866 | 1.138159 | 1.137933 | 0.610654 | 1.154233 | |

| Under Gamma assumption and | ||||||

| -0.81058 | -0.18644 | 1.086393 | 1.058178 | 0.548338 | 1.168817 | |

| -0.96384 | -0.40608 | 1.11229 | 1.095475 | 0.625941 | 1.159911 | |

| -1.08621 | -0.54748 | 1.12215 | 1.110156 | 0.656867 | 1.156134 | |

| -1.17893 | -0.65703 | 1.127791 | 1.118473 | 0.675113 | 1.154124 | |

| -1.27892 | -0.73578 | 1.130749 | 1.123124 | 0.683333 | 1.15202 | |

| -1.34049 | -0.80886 | 1.133229 | 1.126779 | 0.691245 | 1.151347 | |

| -1.38994 | -0.87447 | 1.135158 | 1.129571 | 0.696488 | 1.150754 | |

| -1.44307 | -0.9276 | 1.136436 | 1.131505 | 0.700241 | 1.150307 | |

References

- Ahn and Horenstein (2013) Ahn, S.C. and Horenstein, A.R. (2013). ‘Eigenvalue ratio test for the number of factors’, Econometrica, vol. 81(3), pp. 1203–1227.

- Alessi et al. (2010) Alessi, L., Barigozzi, M. and Capasso, M. (2010). ‘Improved penalization for determining the number of factors in approximate factor models’, Statist. Probab. Lett., vol. 80(23), pp. 1806–1813.

- Amengual and Watson (2007) Amengual, D. and Watson M. W. (2007). ‘Consistent Estimation of the Number of Dynamic Factors in a Large and Panel’, Journal of Business & Economic Statistics, vol. 25(1), pp. 91–96.

- Anderson (2003) Anderson, T. W. (2003). ‘An Introduction to Multivariate Statistical Analysis, 3rd edition’, Hoboken: Wiley–Interscience.

- Bai and Ng (2002) Bai, J. and Ng, S. (2002). ‘Determining the number of factors in approximate factor models’, Econometrica, vol. 70(1), pp. 191–221.

- Bai and Ng (2007) Bai, J. and Ng, S. (2007). ‘Determining the Number of Primitive Shocks in Factor Models’, Journal of Business & Economic Statistics, vol. 25(1), pp. 52–60.

- Bai and Yao (2008) Bai, Z. D. and Yao, J. F. (2008). ‘Central limit theorems for eigenvalues in a spiked population model’, Annales de l’Institut Henri Poincar–Probabilits et Statistiques, vol. 44(3), pp. 447–474.

- Bai and Yao (2012) Bai, Z. D. and Yao, J. F. (2012). ‘On sample eigenvalues in a generalized spiked population model’, Journal of Multivariate Analysis, vol. 106, pp. 167–177.

- Caner and Han (2014) Caner, M. and Han, X. (2014). ‘Selecting the Correct Number of Factors in Approximate Factor Models: The Large Panel Case With Group Bridge Estimators’, Journal of Business & Economic Statistics, vol. 32(3), pp. 359–374.

- Forni et al. (2000) Forni, M., Hallin, M., Lippi, M. and Reichlin, L. (2000). ‘The generalized Dynamic Factor Model: Identification and Estimation’, The Review of Economics and Statistics, vol. 82(4), pp. 540–554.

- Forni et al. (2009) Forni, M., Gannone, D., Lippi, M., and Reichlin,L. (2009). ‘Opening the black box: Structuralfactor models versus structural VARs’, Econometric Theory, vol. 25(5), pp. 1319–1347.

- Hallin and Liska (2007) Hallin, M. and Liska, R. (2007). ‘Determining the Number of Factors in the generalized Dynamic Factor Model’, Journal of the American Statistical Association, vol. 102, pp. 603–617.

- Jiang and Bai (2021a) Jiang, D. D. and Bai, Z. D. (2021a). ‘Generalized four moment theorem and an application to CLT for spiked eigenvalues of large-dimensional covariance matrices’, Bernoulli, vol. 27(1), pp. 274–294.

- Jiang (2022) Jiang, D. D. (2022). ‘A universal test on the number of spikes in a high-dimensional generalized spiked model and its applications’, https://arxiv.org/abs/2203.06924.

- Johnstone (2001) Johnstone, I. M. (2001). ‘On the distribution of the largest eigenvalue in principal components analysis’, Ann. Statist., vol. 29(2), pp. 295–327.

- Johnstone and Lu (2009) Johnstone, I. M. and Lu, A. Y. (2009). ‘On consistency and sparsity for principal components analysis in high dimensions’, J. Am. Statist. Ass., vol. 104(486), pp. 682–693.

- Kapetanios (2004) Kapetanios, G. (2004). ‘ A New Method for Determining the Number of Factors in Factor Models With Large Datasets’, Working Paper no. 525, Queen Mary, University of London.

- Kritchman and Nadler (2008) Kritchman, S. and Nadler, B. (2008). ‘Determining the number of components in a factor model from limited noisy data’, Chem. Int. Lab. Syst., vol. 94(1), pp. 19–32.

- Onatski (2006) Onatski, A. (2006). ‘A Formal Statistical Test for the Number of Factors in Approximate Factor Models’, Preprint, Columbia University, Economics Dept.

- Onatski (2009) Onatski, A. (2009). ‘Testing hypotheses about the number of factors in large factor model’, Econometrica, vol. 77(5), pp. 1447–1479.

- Onatski (2010) Onatski, A. (2010). ‘Determining the number of factors from empirical distribution of eigenvalues’, Rev. Econ. Stat, vol. 92(4), pp. 1004–1016.

- Passemier and Yao (2012) Passemier, D. and Yao, J. F. (2012). ‘On determining the number of spikes in a high-dimensional spiked population model’, Rand. Matr. Theor. Appl., vol. 1(1), article 1150002.

- Passemier et al. (2017) Passemier, D., Li, Z. Y. and Yao, J. F. (2017). ‘On estimation of the noise variance in high-dimensional probabilistic principal component analysis’, Journal of the Royal Statistical Society Series B (Statistical Methodology), vol. 79(1), pp. 51–67.

- Paul (2007) Paul, D. (2007). ‘Asymptotics of sample eigenstructure for a large dimensional spiked covariance model’, Statistica Sinica, vol. 17(4), pp. 1617–1642.

- Ulfarsson and Solo (2008) Ulfarsson, M. O. and Solo, V. (2008). ‘Dimension estimation in noisy PCA with SURE and random matrix theory’, IEEE Trans. Signal Process., vol. 56(12), pp. 5804–5816.