Rough volatility: fact or artefact?

Abstract

We investigate the statistical evidence for the use of ‘rough’ fractional processes with Hurst exponent for modeling the volatility of financial assets, using a model-free approach. We introduce a non-parametric method for estimating the roughness of a function based on discrete sample, using the concept of normalized -th variation along a sequence of partitions. Detailed numerical experiments based on sample paths of fractional Brownian motion and other fractional processes reveal good finite sample performance of our estimator for measuring the roughness of sample paths of stochastic processes. We then apply this method to estimate the roughness of realized volatility signals based on high-frequency observations. Detailed numerical experiments based on stochastic volatility models show that, even when the instantaneous volatility has diffusive dynamics with the same roughness as Brownian motion, the realized volatility exhibits rough behaviour corresponding to a Hurst exponent significantly smaller than . Comparison of roughness estimates for realized and instantaneous volatility in fractional volatility models with different values of Hurst exponent shows that, irrespective of the roughness of the spot volatility process, realized volatility always exhibits ‘rough’ behaviour with an apparent Hurst index . These results suggest that the origin of the roughness observed in realized volatility time-series lies in the estimation error rather than the volatility process itself.

Keywords— roughness, variation index, -th variation, realized volatility, instantaneous volatility, fractional Brownian motion, Hurst exponent, high-frequency data

1 Introduction

1.1 Fractional processes in finance: from long-range dependence to ‘rough volatility’

Beginning with Mandelbrot and Van Ness, (1968), fractional Brownian motion and fractional Gaussian noise have been used as building blocks of stochastic models of various phenomena in physics, engineering (Lévy-Véhel et al., , 2005) and finance (Baillie et al., , 1996; Bollerslev and Ole Mikkelsen, , 1996; Comte and Renault, , 1998; Cont, , 2007; Gatheral et al., , 2018; Rogers, , 1997; Willinger et al., , 1999). Fractional Brownian motion has two remarkable properties which have contributed towards its adoption as a building block in stochastic models: first, its ability to model long-range dependence, as measured by the slow decay of auto-correlation functions of increments, where is the Hurst exponent; second, its ability to generate trajectories which have varying levels of Hölder regularity (‘roughness’). The former is a property that manifests itself over long time scales while the latter manifests itself over short time scales and, in general, these two properties are unrelated. But in the case of fractional Brownian motion, the two properties are linked through self-similarity and governed by the Hurst exponent : for one obtains long-range dependence in increments and trajectories smoother than Brownian motion while for one obtains ‘anti-correlated’ increments and trajectories rougher than Brownian motion333Incidentally, Hurst and Hölder happen to have the same initials, adding to the confusion…. Processes driven by fractional Gaussian noise with are thus sometimes referred to as ‘rough processes’.

In early applications to financial data (Baillie et al., (1996); Bollerslev and Ole Mikkelsen, (1996); Comte and Renault, (1998); Willinger et al., (1999)), fractional processes were adopted in order to model long range dependence effects in financial time series Cont, (2005). More specifically, statistical evidence of volatility clustering Cont, (2007) - positive dependence of the amplitude of returns over long time scales - led to the development of stochastic volatility models driven by fractional Brownian motion. A well-known example of such a fractional stochastic volatility model is the one proposed by Comte and Renault, (1998) who modelled the dynamics of the (instantaneous) volatility of an asset as:

| (1) |

where is a fractional Brownian motion (fBM) with Hurst exponent . This long-range dependence in volatility is modelled by choosing (Comte and Renault, (1998); Bollerslev and Ole Mikkelsen, (1996); Breidt et al., (1998); Hurvich et al., (2005); Lahiri and Sen, (2020)).

A recent strand of literature, starting with Gatheral et al., (2018), has suggested the use of fractional Brownian models with for modelling volatility. Unlike previous studies based on auto-correlations of various volatility estimators over long time scales (Baillie et al., , 1996; Bollerslev and Ole Mikkelsen, , 1996; Cont, , 2005), Gatheral et al., (2018) rely on the analysis of the behaviour of volatility estimators over short intraday time scales in order to assess the ‘roughness’ of these signals and concluded that volatility is ‘rough’ i.e. has paths with a Hölder regularity which is strictly less than , suggest to use stochastic models with sample paths rougher than Brownian motion.

However, it has not been lost on experts working in this area that previous estimation results for fractional models in the literature on long-range dependence in volatility, pointed towards Hurst exponents (and around ) (Baillie et al., , 1996; Comte and Renault, , 1998; Lahiri and Sen, , 2020)while the recent ‘rough volatility’ literature indicates Hurst exponents much smaller than and closer to . Together with the well-known statistical issues plaguing the estimation of Hurst exponents (Beran, , 1994; Rogers, , 2019), these conflicting results call for a critical examination of the empirical evidence for ‘rough volatility’.

Compounding this issue is the fact that (spot) volatility is not directly observed but estimated from price series, with an inherent estimation error which has been the subject of many studies (Barndorff-Nielsen and Shephard, , 2002; Jacod and Protter, , 2012; Lahiri and Sen, , 2020). This estimation error is far from i.i.d.: it is known to possess path-dependent features (see Jacod and Protter, (2012)). As a result, measures of roughness for realized volatility indicators may be quite different from those of the underlying ‘spot volatility’. This is simply because the convergence of high-frequency volatility estimators in norms does not imply in any way their functional convergence in Hölder norms or other norms related to roughness.

As already pointed out by Rogers, (1997), these two properties, namely the short-range behaviour which determines the roughness of the path, and the long-range dependence property, can (and should) be modeled through different mechanisms. Bennedsen et al., (2022) discuss several such approaches.

The focus of the literature on parametric models based on fractional Brownian motion or fractional Gaussian noise concentrates these two, very different, properties in a single parameter: the Hurst exponent (Bolko et al., , 2022; Fukasawa et al., , 2022; Gatheral et al., , 2018). Such parametric approaches proceed as follows: one estimates a parametric model for volatility dynamics based on some fractional Gaussian driving noise with Hurst exponent using a MLE (Fukasawa et al., , 2022) or method of moments (Bolko et al., , 2022). Then, based on the estimated value of this parameter , one concludes that “volatility is rough” if .

The validity of such approaches hinges on the assumption that the class of models used is well-specified. As pointed out by Bennedsen et al., (2022), this is unlikely to be the case for SDEs driven by fractional Gaussian noise if one wants to accommodate both (long-range) dependence properties and (short-range) roughness properties.

To avoid this caveat, we propose a model-free non-parametric method which focuses solely on the roughness properties of sample paths. Although less ambitious in its scope -we only focus on roughness properties rather than developing a full model for volatility dynamics- our approach is robust to the specification errors and estimation biases which plague parametric methods.

1.2 Contribution

We address these questions in detail by re-examining the statistical evidence from high-frequency financial data in an attempt to clarify whether the assertion that ‘volatility is rough’ (i.e. rougher than typical paths of Brownian motion) is supported by empirical evidence. We investigate the statistical evidence for the use of ‘rough’ fractional processes with Hurst exponent for the modelling of volatility of financial assets, using a non-parametric, model-free approach.

We introduce a non-parametric method for estimating the roughness of a function/path based on a (high-frequency) discrete sample, using the concept of normalized -th variation along a sequence of partitions, and discuss the consistency of our estimator in a pathwise setting. We investigate the finite sample performance of our estimator for measuring the roughness of sample paths of stochastic processes using detailed numerical experiments based on sample paths of fractional Brownian motion and other fractional processes. We then apply this method to estimate the roughness of realized volatility signals based on high-frequency observations. Through a detailed numerical experiment based on a stochastic volatility model, we show that even when the instantaneous (spot) volatility has diffusive dynamics with the same roughness as Brownian motion, the realized volatility exhibits rough behaviour corresponding to a Hurst exponent significantly smaller than . Similar behavior is observed in financial data as well, which suggests that the origin of the roughness observed in realized volatility time-series lie in the estimation error rather than the volatility process itself. Comparison of roughness estimates for realized and instantaneous volatility in fractional volatility models for different values of Hurst parameter shows that whatever the value of for the (spot) volatility process, realized volatility always exhibits ‘rough’ behaviour.

Our results are broadly consistent with the observations by Rogers, (2019), but we pinpoint more precisely the origin of the apparent ‘rough’ behaviour of volatility as being the estimation error inherent in the estimation of realized volatility (sometimes known as microstructure noise). In particular, our results question whether the empirical evidence presented from high-frequency volatility estimates supports the ‘rough volatility’ hypothesis.

2 Measuring the roughness of a path

Determining the roughness of realized volatility from a sample path plays a crucial role in model specification Gatheral et al., (2018); Fukasawa et al., (2022). In practice, we observe only a single price path so one is faced with the problem of determining the roughness of a process from a single price path sampled at high frequency. We present in this section several concepts for measuring the roughness of a path and discuss how they may be used to design estimators from high-frequency observations.

2.1 -th variation and roughness index of a path

Consider a sequence of partitions of where

| (2) |

represents observation times ‘at frequency ’. We denote to be the number of intervals in the partition . Denote respectively by and the size of the largest and the smallest interval of . In this paper, we will always assume

The concept of -th variation along a sequence of partitions with is defined following Cont and Perkowski, (2019):

Definition 1.

(-th variation along a sequence of partitions) has finite -th variation along the sequence of partitions if there exists a continuous increasing function such that

| (3) |

If this property holds, then the convergence in (3) is uniform. We call the -th variation of along the sequence of partitions . We denote the set of all continuous paths with finite -th variation along .

Remark 1.

For we have . If

for all then we will write .

To formalize the concept of roughness, we introduce the notion of variation index and roughness index of a path:

Definition 2 (Variation index).

The variation index of a path along a partition sequence is defined as the smallest for which has finite -th variation along :

Definition 3 (Roughness index).

The roughness index of a path (along ) is defined as

When the underlying sequence of partitions is clear, we will omit and denote these indices as and . A similar roughness index was introduced by Han and Schied, (2021).

For a (real-valued) stochastic process the roughness index of each sample path may be different in principle. Nevertheless there are many important classes of stochastic processes which have an almost-sure roughness index. For example, the roughness index of fractional Brownian motion (fBM) matches with the corresponding Hurst parameter/ Hölder exponent:

Example 1.

Brownian motion has variation index and roughness index along any refining partition sequence or any partition with Dudley, (1973).

Fractional Brownian motion has variation index and roughness index along the dyadic partition sequence .

In general, the existence of a variation index is not obvious. For further details see Cont and Das, (2022)

2.2 Normalized -th variation

It is not easy to use -th variation directly on empirical data for estimating roughness based on discrete observations, as this involves checking convergence to an unknown limit. We introduce a normalized version of -th variation which has better asymptotic properties Cont and Das, (2022):

Definition 4 (Normalized -th variation along a sequence of partitions).

Let be a sequence of partitions of with mesh and . is said to have normalized -th variation along if there exists a continuous function such that:

| (4) |

We denote the class of all continuous functions for which the normalized -th variation444For we will call this quantity as ‘normalized quadratic variation’. exists.

The terminology is justified by the following result Cont and Das, (2022) which shows that, for a large class of functions with th variation, the normalized -th variation exists and is linear:

Theorem 2.1.

Let for some where be a sequence of partitions of with vanishing mesh . Furthermore, if the -th variation is absolutely continuous then:

Proof.

See Appendix. ∎

The following result shows that normalized -th variation is a ‘sharp’ statistic: if a function has finite -th variation along a sequence of partitions then for all the normalized -th variation is either infinite or zero.

Theorem 2.2.

Let be a sequence of partitions of with mesh . Let with for some .

-

(i)

For all and for all ; .

-

(ii)

For all and for all ;

Proof.

The proof is provided in Appendix. ∎

In particular, Brownian motion almost surely has linear normalized quadratic variation.

Example 2 (Normalized quadratic variation for Brownian motion).

Let be a Wiener process on a probability space , and be a sequence of partitions of with . Then:

Proof.

The proof is provided in the Appendix. ∎

Remark 2.

In the above example, instead of taking any partition sequence with , we can also take any refining sequence of partitions. The proof is then different and uses the martingale convergence theorem.

Example 3 (Stochastic integrals).

Let where is an adapted process with . Then, for any refining partition sequence with vanishing mesh,

Proof.

This is an immediate consequence of Theorem 2.1. ∎

Remark 3.

In the statement of Example 3, we can replace the assumption of refining partitions with partitions satisfying .

Example 4 (Normalized -th variation for fractional Brownian motion).

Let be a fractional Brownian motion with Hurst index , on a probability space . has normalized p-th variation along the dyadic partition for almost-surely:

Proof.

The proof is a consequence of (Viitasaari, , 2019, Proposition 4.1). ∎

2.3 Estimating roughness from discrete observations

Given observations on a refining time partition , we define the ‘normalized -th variation statistic’ which is the discrete counterpart of the normalized p-th variation:

| (5) |

The definition of the statistic (5) involves two frequencies: a ‘block’ frequency and a sampling frequency . As the partition is refining, is a subpartition of . The denominator is estimated by grouping the sample of size into many groups, where each group contains consecutive data points.

The statistic (5) converges to the normalized -th variation (4) as the sampling frequency and block frequency increase:

It is thus natural to define roughness estimators for a discretely sampled signal in terms of (5).

The variation index estimator associated with the signal sampled on is then obtained by computing for different values of and solving the following equation for ,

| (6) |

One can either fix a window length or solve (6) in a least squares sense across several values of .

An estimator for the roughness index is subsequently defined as:

| (7) |

We will denote the roughness estimator (7) as when the underline dataset and the corresponding partition sequence are clear. Asymptotic properties of these estimators under high-frequency sampling are studied in Cont and Das, (2022).

2.4 Finite sample behaviour of the roughness estimator

We will now study the finite sample behaviour of the roughness estimator using high-frequency simulations of fractional Brownian motions. In the simulation examples unless mentioned otherwise we will use a uniform partition sequence of with:

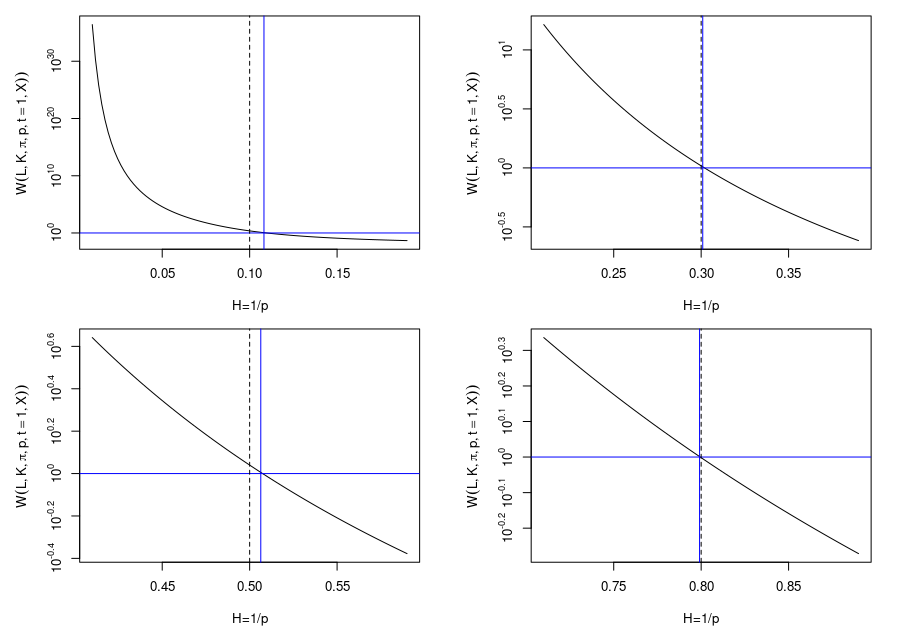

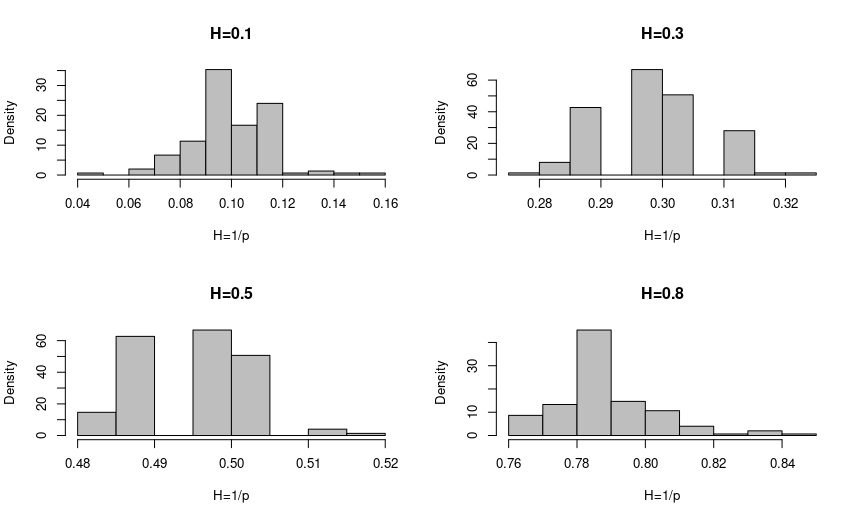

To assess the finite sample accuracy of the estimator we compare the roughness index estimator with the underlying Hurst exponent . For every simulated path we compute for different values of , in order to estimate . In figure 1, the black line is the value of plotted against roughness index in log-scale. The blue horizontal line represents the estimated roughness index whereas the dotted horizontal line represents the Hurst parameter. Figure 2 shows the histograms of the estimator generated from independent paths. We observe that for datasets with length our roughness estimator has satisfactory accuracy. Table 1 provides summary statistics for roughness index of simulated fractional Brownian motions.

|

Figure 3 represents a similar plot for simulated fractional Brownian motion with Hurst parameter . In Figure 3, in left, similar to Figure 1, is plotted against and the right plot represents the histograms of the estimator . The summary statistics for the esimator are provided in Table 2.

|

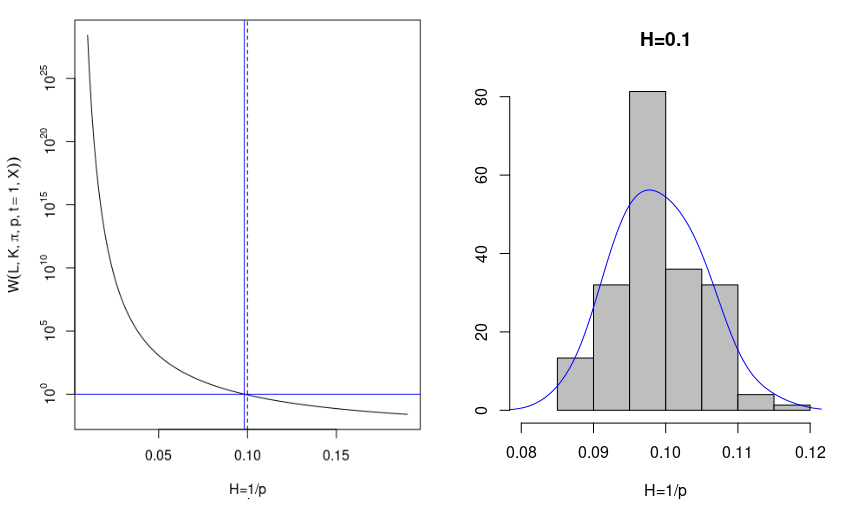

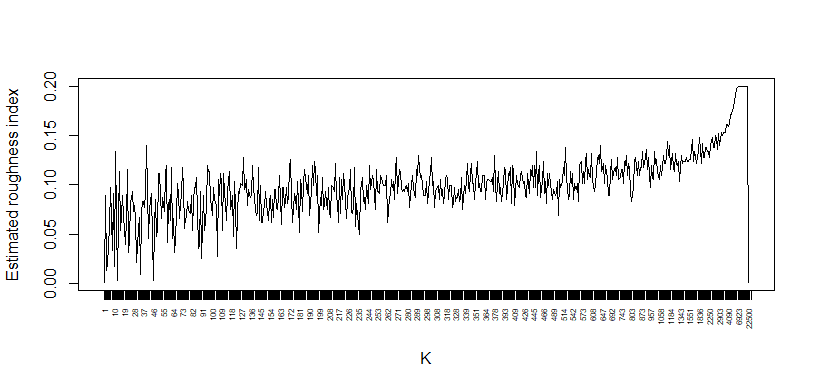

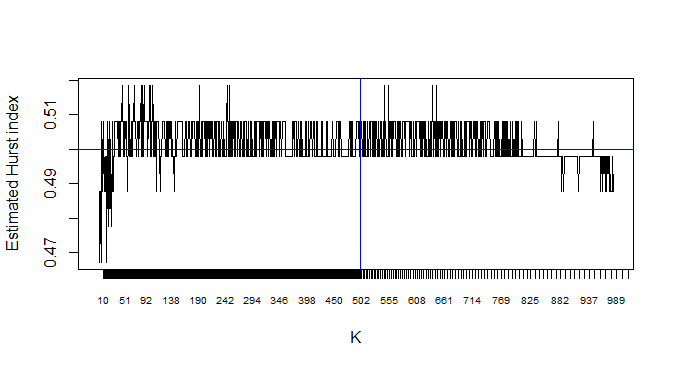

To compute the estimator we have different possible choices of . Figure 4 shows how the estimator varies with for fractional Brownian motion with Hurst parameter . The black line represents the plotted against different values of whereas the blue vertical line represents the value for . We observe that when we vary in the neighbourhood the estimator performs reasonably well and is not very sensitive to the choice of in this vicinity.

In summary, we observe that for realistic sample sizes and frequencies encountered in high-frequency financial data, the estimator is quite accurate and not sensitive to the block size in the range .

3 Spot volatility and realized volatility

Contrary to prices of an asset which may be observed and sampled directly from market data, (spot) volatility is not directly observable and as a consequence must be estimated from prices. Stochastic volatility models represent the price of a financial asset as the solution of a stochastic differential equation driven by a Brownian motion:

| (8) |

where the coefficient represents the instantaneous or ‘spot’ volatility. In general, is represented as a random process itself driven by fractional processes.

In a practical situation, the price at time , is usually observed over a non-uniform time grids of :

| (9) |

In order to study high-frequency asymptotics of roughness estimators, we assume as increases; here the index may be thought of as a ‘sampling frequency’. An example to keep in mind is the dyadic partition sequence: but none of the results below requires a uniform grid.

The spot volatility process may then be recovered from the quadratic variation of the log-price along this particular grid:

| (10) |

where the quadratic variation of the log-price

is computed as a high-frequency limit of the realized variance (Barndorff-Nielsen and Shephard, , 2002; Andersen et al., , 2003) along the sampling grid , defined as

| (11) |

The realized volatility is defined as the square root of the realized variance.

Definition 5 (Realized volatility).

The realized volatility of a price process over time interval sampled along the time partition is defined as:

| (12) |

where .

If the price follows a stochastic volatility model (8) with instantaneous volatility then realized variance converges to the quadratic variation of (also called ‘integrated variance’) as sampling frequency increases (Barndorff-Nielsen and Shephard, , 2002; Jacod and Protter, , 2012):

| (13) |

Along a single price path observed at high-frequency, we can compute the realized variance (12) and the realized volatility in (13) may be used as a practical indicator of volatility:

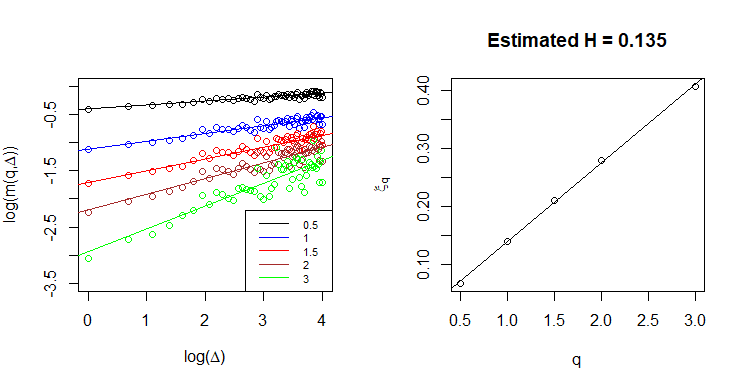

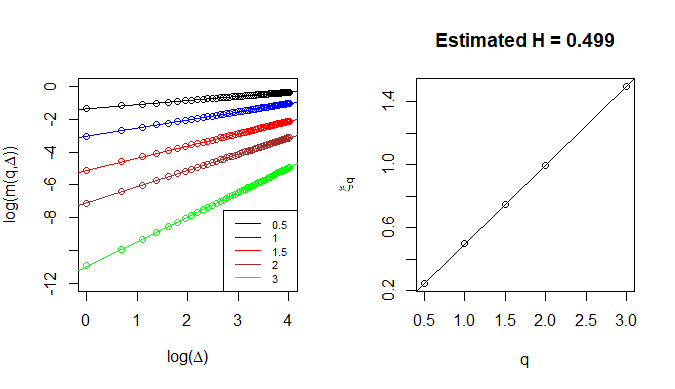

Several empirical studies have attempted to estimate the roughness of ‘realized volatility’ signals using high-frequency data, i.e. Andersen et al., (2003); Barndorff-Nielsen and Shephard, (2002); Cont and Mancini, (2011); Jacod and Protter, (2012); Podolskij and Vetter, (2009). A well-known reference is the study of Gatheral et al., (2018) where the authors estimate the roughness index of S&P500 realized volatility by performing the following logarithmic regression to :

| (14) |

The coefficients are also shown to behave linearly in :

Regression of on yields an estimate of Hurst/Hölder index, for which Gatheral et al., (2018) report the value . Based on these observations, they propose a fractional SDE for (spot) volatility:

As we see from Equation 14, the method used in Gantert, (1994) actually uses -th variation of the to calculate the roughness of the underlying volatility process. Figure 5 is a replication of the log-regression model described above to estimate the roughness index of the volatility of -min S&P 500. However, in an interesting simulation study using paths simulated from a Brownian OU volatility process, Rogers, (2019) showed that the scaling behavior claimed as evidence for ‘rough volatility’ is also observed in a Brownian OU model over a range of time scales, and that estimators of the roughness index based on log-regression of empirical -th variation have poor accuracy.

Similar evidence for the lack of accuracy of such estimators based on log-regression of -th variation is shown by Fukasawa et al., (2022).

4 Numerical experiments

We now compare various estimators of the roughness index for instantaneous volatility with those obtained from realized volatility using price trajectories simulated from stochastic volatility models with varying degrees of “roughness”.

4.1 Stochastic volatility diffusion models

Let us first consider the following stochastic volatility where volatility is simply (the modulus of) a Brownian motion:

Example 5.

| (15) |

where are two independent Brownian motions.

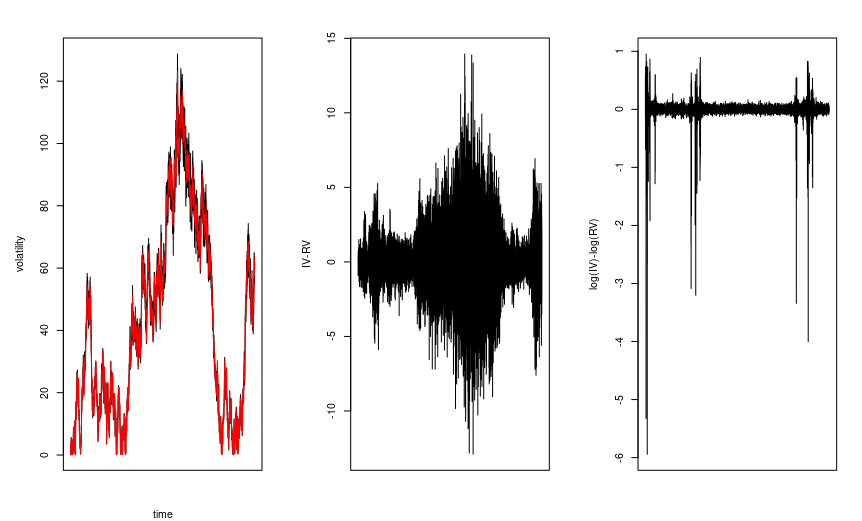

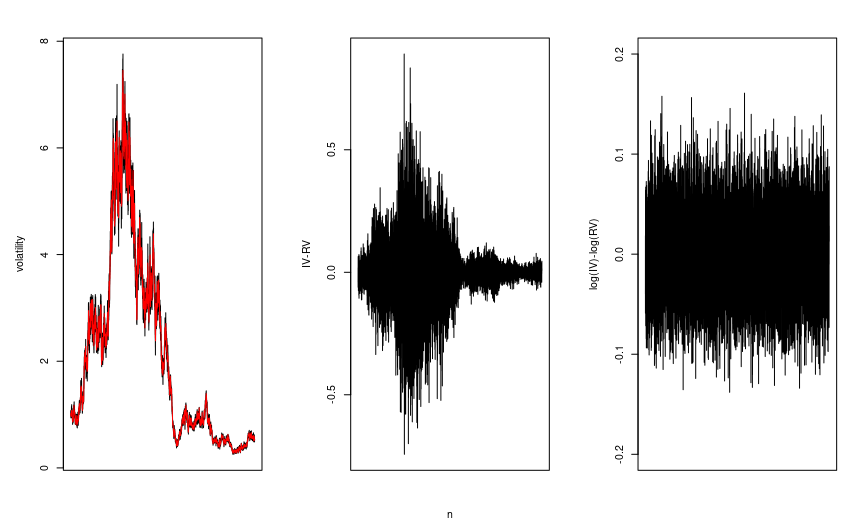

Figure 6 represents a path of the instantaneous volatility and the realized volatility computed as in Equation 12 by taking 300 consecutive data-points, which corresponds to a 5-minute moving window. The right plot of Figure 6 represents the estimation error, which is defined as the difference of instantaneous and realized volatility. The ACF of the estimation error shows a complex time-dependent pattern which rules out IID behavior and indicates a complex dependence structure.

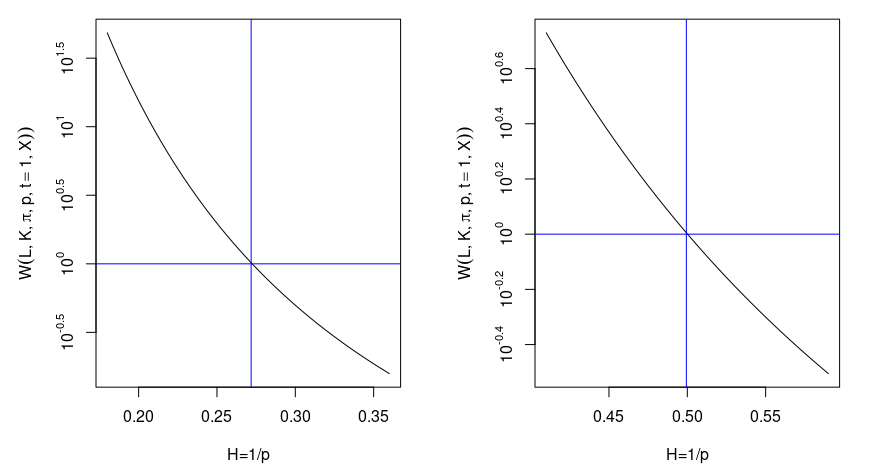

The estimated roughness index of instantaneous and realized volatility are observed to be very different. In the left graph of Figure 7 we plot against for the realized volatility. On the other hand, the right graph is the same plot with the same set of parameters but for instantaneous volatility. The estimated roughness index for realized volatility () is significantly smaller than the roughness index of the instantaneous volatility () suggesting rougher behaviour of realized volatility. As in our simulation study we do not have any measurement errors, this roughness behaviour purely comes from estimation error. In some studies it is assumed that the estimation error or the log-estimation error is I.I.D. (see for example Fukasawa et al., (2022)) but as one can see from this diffusion example, both the estimation error and the log-estimation error is far from I.I.D. and hence the assumptions put forth for example in Fukasawa et al., (2022), is not very realistic for general diffusion models.

The solid black lines in Figure 8 and Figure 9 respectively represent the estimated roughness index plotted against different values of for the realized and instantaneous volatility (model 15). The blue vertical line represents for . From the figures, we can observe that irrespective of the choice of for the finite sample dataset of length , the realized volatility is significantly rougher than the instantaneous volatility.

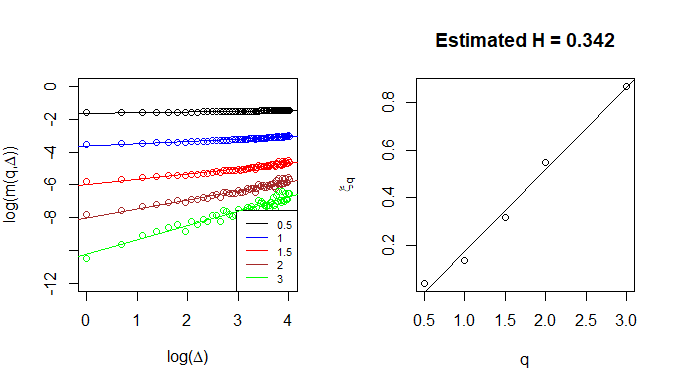

We now compare our roughness estimator with the log-regression method suggested in Gatheral et al., (2018) for the model 15. It turns out that even with the log-regression model, similar ‘rougher’ realized volatility is observed even if the instantaneous volatility has Brownian diffusive behaviour. Figure 10 and Figure 11 show that the realized volatility has a significant smaller roughness index than the instantaneous volatility even with respect to the log regression method. In this example it is clear that the roughness observed in realized volatility is attributable to the discretization error (‘estimation error’) and not the roughness of the spot volatility process, which is Brownian.

Next we consider a more realistic mean-reverting volatility model in which the volatility follows a Brownian Ornstein–Uhlenbeck process:

Example 6 (OU-SV model).

| (16) |

where and are two independent Brownian motions.

In the simulation, we use and . The left plot of Figure 12 represents the realized volatility (respectively instantaneous volatility) of the price process in black (respectively red) simulated from the above stochastic volatility model 16. The middle plot of Figure 12 represents the corresponding estimation error, which is the difference between the realized and the instantaneous volatility. Visually the middle plot suggests the estimation error has a complicated dependence structure. But unlike the plot for Example 5, the log error on the right plot of Figure 12 has an I.I.D. Gaussian structure (This is supported by the theory provided in Fukasawa et al., (2022)).

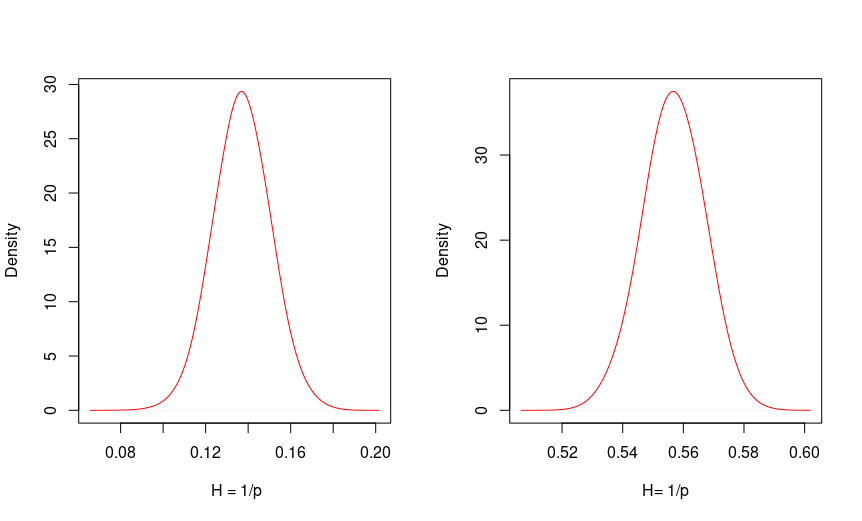

Now we compare the distribution of the estimator with for realized and instantaneous volatility across independent paths drawn from (16). The left plot in Figure 13 is the distribution of for the realized volatility while the right plot corresponds to the same for instantaneous volatility. The following table provides summary statistics for the estimator with across independent sample paths for realized volatility and instantaneous volatility respectively.

|

4.2 A fractional Ornstein-Uhlenbeck model

In both previous examples, instantaneous volatility follows a diffusive behaviour similar to Brownian motion with , yet the realized volatility exhibits ”rough” behaviour with an estimated roughness index significantly smaller than .

We now consider the more general case of a price process generated by a stochastic volatility model of the type (1) where instantaneous volatility has a general roughness index and explore how the roughness index of the instantaneous volatility reflects on the roughness index of realized volatility and the corresponding estimation error.

Example 7.

[Fractional OU process] Consider the following price process, where the volatility is described by a fractional Ornstein–Uhlenbeck process:

| (17) |

where , is a Brownian motion and fractional Brownian motion with Hurst index .

We compute the realized volatility and compare the estimated roughness index (with, ) of instantaneous and realized volatility in the following table.

|

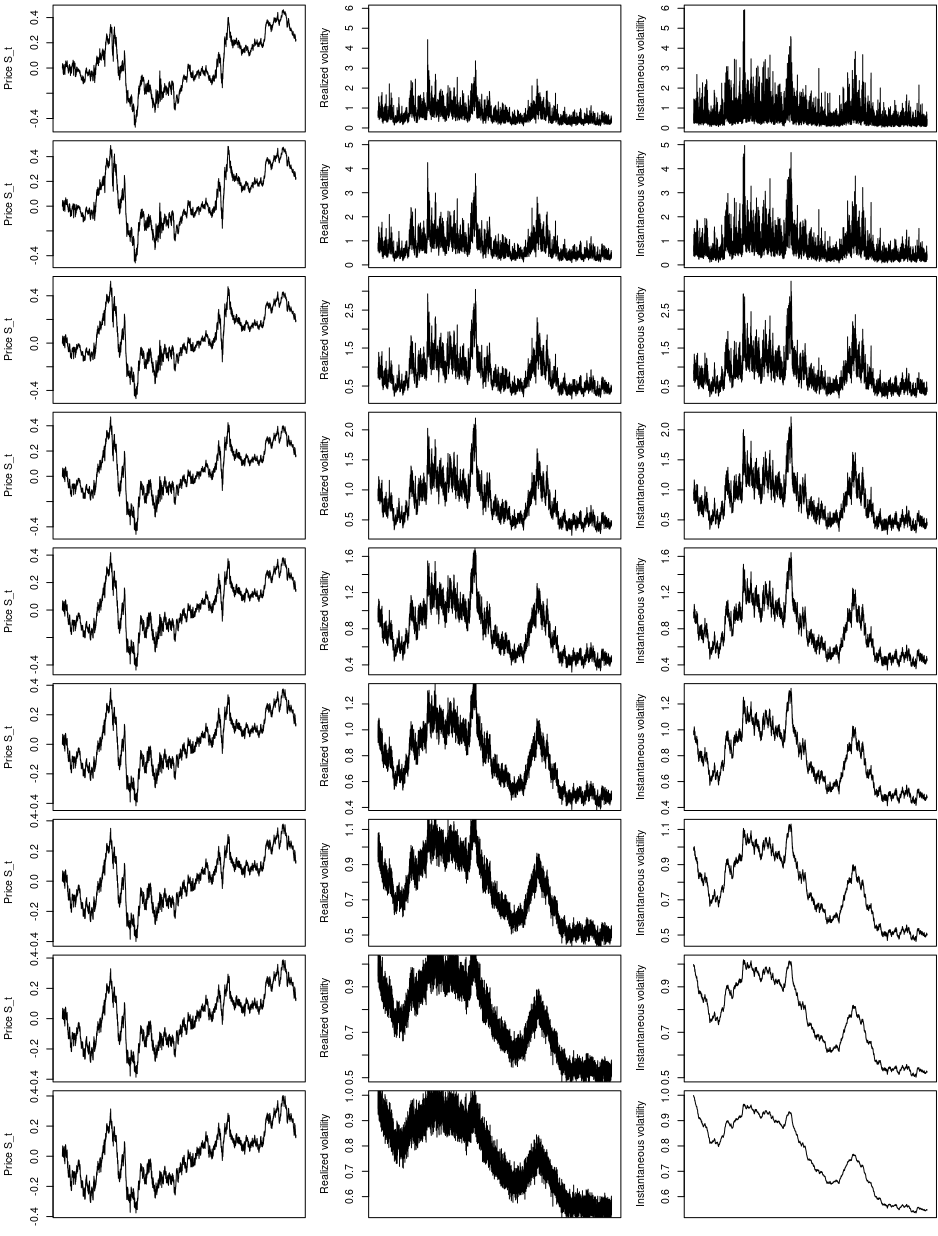

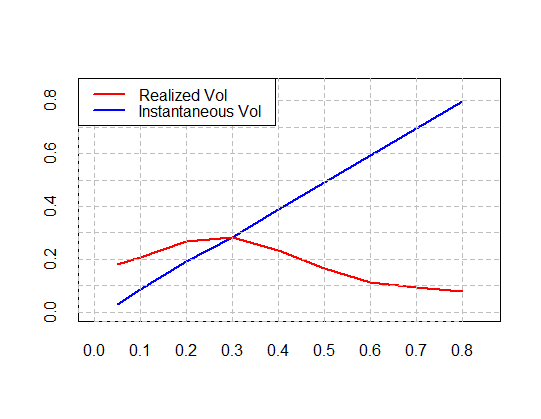

The corresponding pictures for price process, realized volatility and the instantaneous volatility from Model 17 with Hurst index respectively are presented in Figure 14. Visually we can observe that for smaller , the instantaneous volatility is rougher than realized volatility but as we increase the realized volatility shows significantly rougher behaviour than the instantaneous volatility. In Figure 15 for the simulated models in Figure 14, we plot the estimated roughness index and respectively in the red and blue line. Though the estimated roughness index of instantaneous volatility (represented in blue line) gives an accurate estimate of Hurst index , the roughness index for realized volatility always stays below . In particular, when the instantaneous volatility exhibits smoother behaviour (corresponding to ) the estimated roughness index of realized volatility turns out to be a poor estimate for the Hurst index.

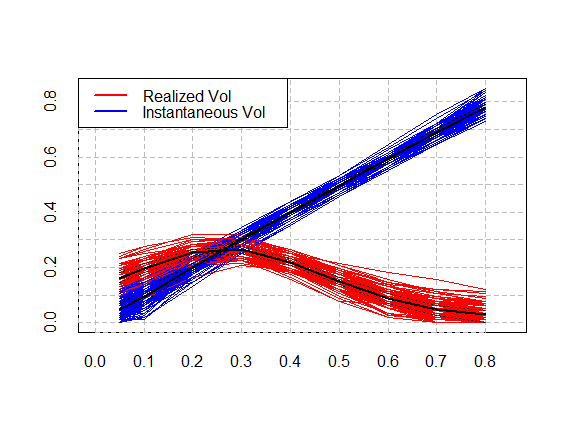

Figure 16 shows the corresponding estimators and for independent simulated price paths from (17). The bold black lines represent the mean across independent simulations whereas the dotted lines represent the corresponding and confidence intervals. For the price process (17), no matter what the value of the Hurst exponent for instantaneous volatility, the roughness index of realized volatility is always estimated to be between to .

These examples illustrate our point: one cannot draw the conclusion that (spot) ‘volatility is rough’ i.e. reject the null hypothesis just because realized volatility exhibits ‘rough’ behaviour with or , even when these estimators exhibit values well below .

H={0.05,0.1,0.2,0.3,0.4,0.5,0.6,0.7,0.8} respectively, Center: Realized volatility, Right: Instantaneous volatility.

5 Application to high-frequency financial data

Having extensively explored the performance of our roughness estimator based on the normalized -th variation statistic for spot and realized volatility on simulated price paths, we now apply it to high-frequency financial time series.

5.1 AAPL

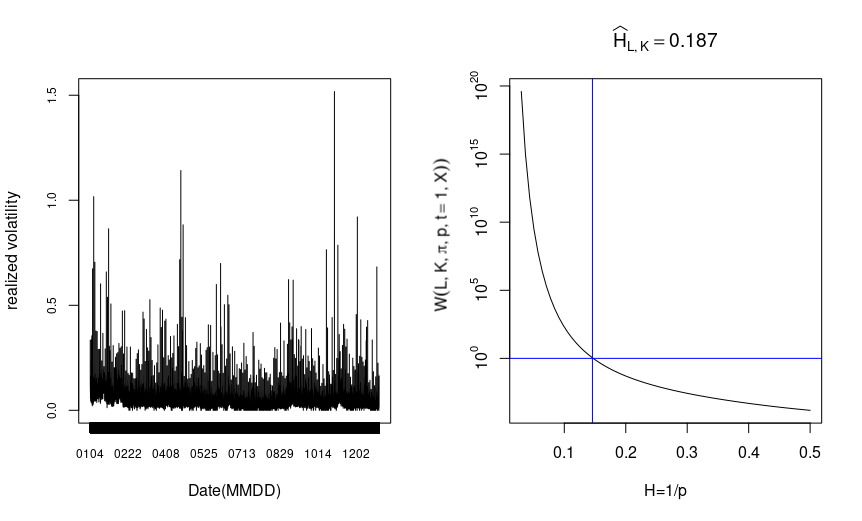

Figure 17 (left) shows the second-by-second record of AAPL stock price. The right graph of Figure 17 is plotted against Hurst parameter for ‘AAPL’ price.

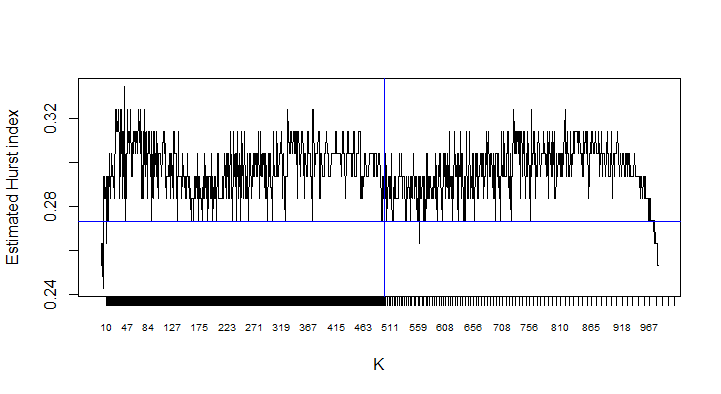

The left plot of Figure 18 represents -minute realized volatility of ‘AAPL’ in . The right graph of Figure 18 is plotted against for the 1-min AAPL realized volatility. Fixing the value of , if we deviate the value of a little, then the estimated roughness index varies between to . This is consistent with the results of Gatheral et al., (2018) regarding realized volatility. But as our simulation study suggests, the roughness index of realized volatility may be very different from that of spot volatility which is the quantity modelled in continuous-time stochastic volatility models.

5.2 SP500

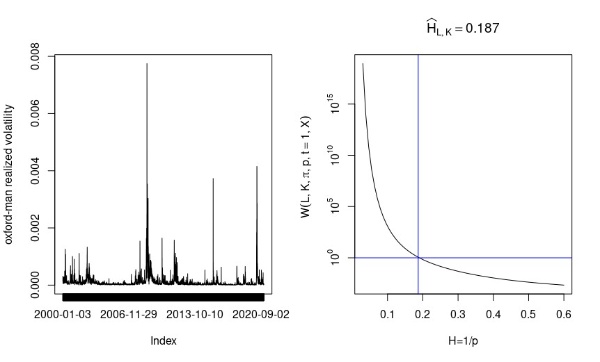

Several studies on rough volatility, including the original study Gatheral et al., (2018), are based on the Oxford-Man Institute Realized Volatility dataset 555https://realized.oxford-man.ox.ac.uk/data. Figure 19 represents the plot of 5-minute realized volatility of SP500. The X-axis represents date. The right graph of Figure 19 is plotted against Hurst parameter for the 5-min Oxford-Man institute realized volatility data. Fixing the value of , if we deviate the value of a little, the estimated roughness index varies between to . This finding is again consistent with the findings in Gatheral et al., (2018).

Overall, the picture that emerges from SP500 and AAPL data is quite similar to the one observed in simulations of diffusion-type stochastic volatility models discussed in Section 4.1. As observed in Section 2.4, these observations are fully compatible with a diffusion-type stochastic volatility model such as (16) and one cannot reject the null hypothesis just because realized volatility exhibits ‘rough’ behaviour with or , even though these estimators exhibit values around .

6 Rough volatility … or estimation error?

Given the large literature on ‘rough volatility’ in quantitative finance, it is somewhat surprising that the initial claim Gatheral et al., (2018) that one needs to model the spot volatility process using a ‘rough’ fractional noise with Hurst exponent has not been examined more closely, especially given that several follow-up studies (Fukasawa et al., , 2022; Rogers, , 2019) point to the fact that the observations in Gatheral et al., (2018) may well be compatible with a Brownian diffusion model for volatility.

Our detailed examples illustrate that, for stochastic-volatility diffusion models driven by Brownian motion as described in Examples 5 and 6, the realized volatility has a roughness index so exhibits an ‘apparent roughness’ which instantaneous volatility does not have, both in terms of normalized -th variation statistics and also in terms of the log- regression method used by Gatheral et al., (2018). Clearly in these simulation examples this is entirely due to the discretization error or ‘estimation error’.

These results suggest that one cannot hastily conclude that the roughness observed in realized volatility is an indicator of similar behaviour in spot volatility, as implicitly assumed in the ‘rough volatility’ literature; the observations in high-frequency financial data are in fact compatible with a stochastic volatility model drive by Brownian motion and the origin of this apparent roughness may very well lie in estimation error rather than the noise process driving spot volatility.

Also, as shown in Example 7, the rough behaviour of realized volatility does not lead us to reject the hypothesis that the underlying spot volatility may be modeled with a Brownian diffusion model or even a smoother model with long-range dependence and . This observation, together with “Occam’s razor”, pleads for the use of Markovian stochastic volatility models which seem compatible with the empirical evidence but are far more tractable.

We are thus drawn to concur with Rogers, (2019) that “the notion that volatility is rough, that is, governed by a fractional Brownian motion (with ), is not an incontrovertible established fact; simpler models explain the observations just as well.”

References

- Andersen et al., (2003) Andersen, T. G., Bollerslev, T., Diebold, F. X., and Labys, P. (2003). Modeling and forecasting realized volatility. Econometrica, 71(2):579–625.

- Baillie et al., (1996) Baillie, R. T., Bollerslev, T., and Mikkelsen, H. O. (1996). Fractionally integrated generalized autoregressive conditional heteroskedasticity. Journal of Econometrics, 74(1):3–30.

- Barndorff-Nielsen and Shephard, (2002) Barndorff-Nielsen, O. E. and Shephard, N. (2002). Econometric analysis of realized volatility and its use in estimating stochastic volatility models. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 64(2):253–280.

- Bennedsen et al., (2022) Bennedsen, M., Lunde, A., and Pakkanen, M. S. (2022). Decoupling the short-and long-term behavior of stochastic volatility. Journal of Financial Econometrics, 20(5):961–1006.

- Beran, (1994) Beran, J. (1994). Statistics for long-memory processes, volume 61 of Monographs on Statistics and Applied Probability. Chapman and Hall, New York.

- Bolko et al., (2022) Bolko, A. E., Christensen, K., Pakkanen, M. S., and Veliyev, B. (2022). A GMM approach to estimate the roughness of stochastic volatility. Journal of Econometrics, in press.

- Bollerslev and Ole Mikkelsen, (1996) Bollerslev, T. and Ole Mikkelsen, H. (1996). Modeling and pricing long memory in stock market volatility. Journal of Econometrics, 73(1):151–184.

- Breidt et al., (1998) Breidt, F., Crato, N., and de Lima, P. (1998). The detection and estimation of long memory in stochastic volatility. Journal of Econometrics, 83(1):325–348.

- Comte and Renault, (1998) Comte, F. and Renault, É. (1998). Long memory in continuous-time stochastic volatility models. Mathematical Finance, 8:291–323.

- Cont, (2005) Cont, R. (2005). Long range dependence in financial markets. In Lévy-Véhel, J. and Lutton, E., editors, Fractals in Engineering, pages 159–179, London. Springer London.

- Cont, (2007) Cont, R. (2007). Volatility clustering in financial markets: Empirical facts and agent-based models. In Teyssière, Gilles and Kirman, Alan P. (eds.): Long Memory in Economics, pages 289–309. Springer, Berlin, Heidelberg.

- Cont and Das, (2022) Cont, R. and Das, P. (2022). Measuring the roughness of a signal. Working Paper.

- Cont and Mancini, (2011) Cont, R. and Mancini, C. (2011). Nonparametric tests for pathwise properties of semimartingales. Bernoulli, 17(2):781 – 813.

- Cont and Perkowski, (2019) Cont, R. and Perkowski, N. (2019). Pathwise integration and change of variable formulas for continuous paths with arbitrary regularity. Transactions of the American Mathematical Society, 6:134–138.

- Dudley, (1973) Dudley, R. M. (1973). Sample functions of the gaussian process. Ann. Probab., 1(1):66–103.

- Fukasawa et al., (2022) Fukasawa, M., Takabatake, T., and Westphal, R. (2022). Consistent estimation for fractional stochastic volatility model under high-frequency asymptotics. Mathematical Finance, 32(4):1086–1132.

- Gantert, (1994) Gantert, N. (1994). Self-similarity of Brownian motion and a large deviation principle for random fields on a binary tree. Prob. Th. Rel. Fields, 98(1):7–20.

- Gatheral et al., (2018) Gatheral, J., Jaisson, T., and Rosenbaum, M. (2018). Volatility is rough. Quantitative Finance, 18:933–949.

- Han and Schied, (2021) Han, X. and Schied, A. (2021). The hurst roughness exponent and its model-free estimation.

- Hurvich et al., (2005) Hurvich, C. M., Moulines, E., and Soulier, P. (2005). Estimating long memory in volatility. Econometrica, 73(4):1283–1328.

- Jacod and Protter, (2012) Jacod, J. and Protter, P. (2012). Discretization of processes, volume 67 of Stochastic Modelling and Applied Probability. Springer, Heidelberg.

- Lahiri and Sen, (2020) Lahiri, A. and Sen, R. (2020). Fractional brownian markets with time-varying volatility and high-frequency data. Econometrics and Statistics, 16:91–107.

- Lévy-Véhel et al., (2005) Lévy-Véhel, J., Lutton, E., and Tricot, C. (2005). Fractals in Engineering. Springer, Berlin.

- Mandelbrot and Van Ness, (1968) Mandelbrot, B. B. and Van Ness, J. W. (1968). Fractional Brownian motions, fractional noises and applications. SIAM Review, 10(4):422–437.

- Podolskij and Vetter, (2009) Podolskij, M. and Vetter, M. (2009). Estimation of volatility functionals in the simultaneous presence of microstructure noise and jumps. Bernoulli, 15(3):634 – 658.

- Rogers, (2019) Rogers, L. (2019). Things we think we know. . https://www.skokholm.co.uk/wp-content/uploads/2019/11/TWTWKpaper.pdf.

- Rogers, (1997) Rogers, L. C. G. (1997). Arbitrage with fractional Brownian motion. Mathematical Finance, 7:95–105.

- Viitasaari, (2019) Viitasaari, L. (2019). Necessary and sufficient conditions for limit theorems for quadratic variations of gaussian sequences. Probab. Surveys, 16:62–98.

- Willinger et al., (1999) Willinger, W., Taqqu, M. S., and Teverovsky, V. (1999). Stock market prices and long-range dependence. Finance and stochastics, 3(1):1–13.

Proof of Theorem 2.2 (i).

We will prove the result for , for general the proof generalizes without further complication. Since and the function has finite -variation along , the pathwise -th variation for all . Hence given any fixed we have . Now given any and any , we will show that . For fix we have:

Define the ‘unfeasible estimator’

Since for some , for fix large enough , we have . So we get the lower bound of as follows.

Since for all , we can conclude the following:

Proof of Theorem 2.2(ii).

We will prove the result for , for general the proof follows exactly the same way. Since the function has finite -variation along and from the assumption, the pathwise -th variation for all . Hence, given any fixed we have . Now given any and any , we will show that by showing that for all large . For fix we have:

Since for all , ;

Proof of Theorem 2.1

For convenience, assume . Since the -th variation is strictly increasing we have . Since is continuous in a compact interval , it is also bounded. So for all , we have . So as a consequence of mean value theorem,

where for all and for all . Finally, using properties of Riemann integral we can conclude:

Since the limit always exists we can conclude the proof.

Proof of Example 2

Let be a Wiener process on the canonical Wiener space , i.e and is the Wiener measure. Let be a sequence of partitions of satisfying . Then the results of Dudley Dudley, (1973) imply that

So if we set then and any satisfies . Now for any we also have the following:

So for Brownian motion, normalized quadratic variation is almost surely equal to .

Remark 4.

From Lemma 2 we know that, for any partition sequence with , there exists with such that:

We also have the following relation between quadratic variation and normalized-QV for Brownian paths in the class .

i.e. the null set for quadratic variation and normalized-quadratic variation of Brownian motion are the same.