Local optimisation of Nyström samples

through stochastic gradient descent

Abstract

We study a relaxed version of the column-sampling problem for the Nyström approximation of kernel matrices, where approximations are defined from multisets of landmark points in the ambient space; such multisets are referred to as Nyström samples. We consider an unweighted variation of the radial squared-kernel discrepancy (SKD) criterion as a surrogate for the classical criteria used to assess the Nyström approximation accuracy; in this setting, we discuss how Nyström samples can be efficiently optimised through stochastic gradient descent. We perform numerical experiments which demonstrate that the local minimisation of the radial SKD yields Nyström samples with improved Nyström approximation accuracy.

Keywords: Low-rank matrix approximation; Nyström method; reproducing kernel Hilbert spaces;

stochastic gradient descent.

1 Introduction

In Data Science, the Nyström method refers to a specific technique for the low-rank approximation of symmetric positive-semidefinite (SPSD) matrices; see e.g. [5, 11, 18, 10, 4]. Given an SPSD matrix , with , the Nyström method consists of selecting a sample of columns of , generally with , and next defining a low-rank approximation of based on this sample of columns. More precisely, let be the columns of , so that , and let denote the indices of a sample of columns of (note that is a multiset, i.e. the indices of some columns might potentially be repeated). Let be the matrix defined from the considered sample of columns of , and let be the principal submatrix of defined by the indices in , i.e. the entry of is , the entry of . The Nyström approximation of defined from the sample of columns indexed by is given by

| (1) |

with the Moore-Penrose pseudoinverse of . The column-sampling problem for Nyström approximation consists of designing samples of columns such that the induced approximations are as accurate as possible (see Section 1.2 for more details).

1.1 Kernel Matrix Approximation

If the initial SPSD matrix is a kernel matrix, defined from a SPSD kernel and a set or multiset of points (and with a general ambient space), i.e. the entry of is , then a sample of columns of is naturally associated with a subset of ; more precisely, a sample of columns , indexed by , naturally defines a multiset , so that the induced Nyström approximation can in this case be regarded as an approximation induced by a subset of points in . Consequently, in the kernel-matrix framework, instead of relying only on subsets of columns, we may more generally consider Nyström approximations defined from a multiset . Using matrix notation, the Nyström approximation of defined by a subset is the SPSD matrix , with entry

| (2) |

where is the kernel matrix defined by the kernel and the subset , and where

We shall refer to such a set or multiset as a Nyström sample, and to the elements of as landmark points; the notation emphasises that the considered Nyström approximation of is induced by . As in the column-sampling case, the landmark-point-based framework naturally raises questions related to the characterisation and the design of efficient Nyström samples (i.e. leading to accurate approximations of ). As an interesting feature, Nyström samples of size may be regarded as elements of , and if the underlying set is regular enough, they might be directly optimised on ; the situation we consider in this work corresponds to the case , with , but may more generally be a differentiable manifold.

Remark 1.1.

1.2 Assessing the Accuracy of Nyström Approximations

In the classical literature on the Nyström approximation of SPSD matrices, the accuracy of the approximation induced by a Nyström sample is often assessed through the following criteria:

-

(C.1)

, with the trace norm;

-

(C.2)

, with the Frobenius norm;

-

(C.3)

, with the spectral norm.

Although defining relevant and easily interpretable measures of the approximation error, these criteria are relatively costly to evaluate. Indeed, each of them involves the inversion or pseudoinversion of the kernel matrix , with complexity . The evaluation of the criterion (C.1) also involves the computation of the diagonal entries of , leading to an overall complexity of . The evaluation of (C.2) involves the full construction of the matrix , with an overall complexity of , and the evaluation of (C.3) in addition requires the computation of the largest eigenvalue of an SPSD matrix, leading to an overall complexity of . If , then the evaluation of the partial derivatives of these criteria (regarded as maps from to ) with respect to a single coordinate of a landmark point has a complexity similar to the complexity of evaluating the criteria themselves. As a result, a direct optimisation of these criteria over is intractable in most practical applications.

1.3 Radial Squared-Kernel Discrepancy

As a surrogate for the criteria (C.1)-(C.3), and following the connections between the Nyström approximation of SPSD matrices, the approximation of integral operators with SPSD kernels and the kernel embedding of measures, we consider the following radial squared-kernel discrepancy criterion (radial SKD, see [9, 7]), denoted by and given by, for ,

| (3) |

and if ; the notation stands for . We may note that . In (3), the evaluation of the term has complexity ; nevertheless, this term does not depend on the Nyström sample , and may thus be regarded as a constant. The complexity of the evaluation of the term , i.e. of the radial SKD up to the constant , is , and the same holds for the complexity of the evaluation of the partial derivative of with respect to a coordinate of a landmark point, see equation (5) below. We may in particular note that the evaluation of the radial SKD criterion or its partial derivatives does not involve the inversion or pseudoinversion of the matrix .

Remark 1.2.

From a theoretical standpoint, the radial SKD criterion measures the distance, in the Hilbert space of all Hilbert-Schmidt operators on , between the integral operator corresponding to the initial matrix , and the projection of this operator onto the subspace spanned by an integral operator defined from the kernel and a uniform measure on . The radial SKD may also be defined for non-uniform measures, and the criterion in this case depends not only on , but also on a set of relative weights associated with each landmark point in ; in this work, we only focus on the uniform-weight case. See [9, 7] for more details.

The following inequalities hold:

which, in complement to the theoretical properties enjoyed by the radial SKD, further support the use of the radial SKD as a numerically affordable surrogate for (C.1)-(C.3) (see also the numerical experiments in Section 4).

From now on, we assume that . Let , with , be the -th coordinate of in the canonical basis of . For , we denote by (assuming they exist)

| (4) |

the partial derivatives of the maps and at and with respect to the -th coordinate of , respectively; the notation indicates that the left entry of the kernel is considered, while refers to the diagonal of the kernel; we use similar notations for any kernel function on .

For a fixed number of landmark points , the radial SKD criterion can be regarded as a function from to . For a Nyström sample , and for and , we denote by the partial derivative of the map at with respect to the -th coordinate of the -th landmark point . We have

| (5) | ||||

In this work, we investigate the possibility to use the partial derivatives (5), or stochastic approximations of these derivatives, to directly optimise the radial SKD criterion over via gradient or stochastic gradient descent; the stochastic approximation schemes we consider aim at reducing the burden of the numerical cost induced by the evaluation of the partial derivatives of when is large.

The document is organised as follows. In Section 2, we discuss the convergence of a gradient descent with fixed step size for the minimisation of over . The stochastic approximation of the gradient of the radial SKD criterion (3) is discussed in Section 3, and some numerical experiments are carried out in Section 4. Section 5 consists of a concluding discussion, and the Appendix contains a proof of Theorem 2.1.

2 A Convergence Result

We use the same notation as in Section 1.3 (in particular, we still assume that ), and by analogy with (4), for and , and for , we denote by the partial derivative of the map with respect to the -th coordinate of . Also, for a fixed , we denote by the gradient of at ; in matrix notation, we have

with for .

Theorem 2.1.

We make the following assumptions on the squared-kernel , which we assume hold for all and , and all and , uniformly:

-

(C.1)

there exists such that ;

-

(C.2)

there exists such that and ;

-

(C.3)

there exists such that , and

.

Let and be two Nyström samples; under the above assumptions, there exists such that

with the Euclidean norm of ; in other words, the gradient of is Lipschitz-continuous with Lipschitz constant .

Since is bounded from below, for and independently of the considered initial Nyström sample , Theorem 2.1 entails that a gradient descent from , with fixed stepsize for the minimisation of over , produces a sequence of iterates that converges to a critical point of . Barring some specific and largely pathological cases, the resulting critical point is likely to be a local minimum of , see for instance [12]. See the Appendix for a proof of Theorem 2.1.

The conditions considered in Theorem 2.1 ensure the existence of a general Lipschitz constant for the gradient of ; they, for instance, hold for all sufficiently regular Matérn kernels (thus including the Gaussian or squared-exponential kernel). These conditions are only sufficient conditions for the convergence of a gradient descent for the minimisation of . By introducing additional problem-dependent conditions, some convergence results might be obtained for more general squared kernels and adequate initial Nyström samples . For instance, the condition (C.1) simply aims at ensuring that for all ; this condition might be relaxed to account for kernels with vanishing diagonal, but one might then need to introduce ad hoc conditions to ensure that remains large enough during the minimisation process.

3 Stochastic Approximation of the Radial SKD Gradient

The complexity of evaluating a partial derivative of is , which might become prohibitive for large values of . To overcome this limitation, stochastic approximations of the gradient of might be considered (see e.g. [2]).

The evaluation of (5) involves, for instance, terms of the form , with and . Introducing a random variable with uniform distribution on , we can note that

and the mean may then, classically, be approximated by random sampling. More precisely, if are copies of , we have

so that we can easily define unbiased estimators of the various terms appearing in (5). We refer to the sample size as the batch size.

Let and ; the partial derivative (5) can be rewritten as

with and , and

The terms and are the only terms in (5) that depend on . From a uniform random sample , we define the unbiased estimators of , and of , as

In what follows, we discuss the properties of some stochastic approximations of the gradient of that can be defined from such estimators.

One-Sample Approximation.

Using a single random sample of size , we can define the following stochastic approximation of the partial derivative (5):

| (6) |

An evaluation of has complexity , as opposed to for the corresponding exact partial derivative. However, due to the dependence between and , and to the fact that involves the square of , the stochastic partial derivative will generally be a biased estimator of .

Two-Sample Approximation.

To obtain an unbiased estimator of the partial derivative (5), instead of considering a single random sample, we may define a stochastic approximation based on two independent random samples and , consisting of and copies of (i.e. consisting of uniform random variables on ), with . The two-sample estimator of (5) is then given by

| (7) |

and since and , we have

Although being unbiased, for a common batch size , the variance of the two-sample estimator (7) will generally be larger than the variance of the one-sample estimator (6). In our numerical experiments, the larger variance of the unbiased estimator (7) seems to actually slow down the descent when compared to the descent obtained with the one-sample estimator (6).

Remark 3.1.

While considering two independent samples and , the two terms and appearing in (7) are dependent. This dependence may complicate the analysis of the properties of the resulting SGD; nevertheless, this issue might be overcome by considering four independent samples instead of two.

4 Numerical Experiments

Throughout this section, the matrices are defined from multisets and from kernels of the form , with and where is the Euclidean norm of (Gaussian kernel). Except for the synthetic example of Section 4.1, all the multisets we consider consist of the entries of data sets available on the UCI Machine Learning Repository; see [6].

Our experiments are based on the following protocol: for a given , we consider an initial Nyström sample consisting of points drawn uniformly at random, without replacement, from . The initial sample is regarded as an element of , and used to initialise a GD or SGD, with fixed stepsize , for the minimisation of over , yielding, after iterations, a locally optimised Nyström sample . The SGDs are performed with the one-sample estimator (6) and are based on independent and identically distributed uniform random variables on (i.e. i.i.d. sampling), with batch size ; see Section 3. We assess the accuracy of the Nyström approximations of induced by and in terms of radial SKD and of the classical criteria (C.1)-(C.3).

For a Nyström sample of size , the matrix is of rank at most . Following [10, 4], to further assess the efficiency of the approximation of induced by , we introduce the approximation factors

| (8) |

where denotes an optimal rank- approximation of (i.e. the approximation of obtained by truncation of a spectral expansion of and based on of the largest eigenvalues of ). The closer , and are to , the more efficient the approximation is.

4.1 Bi-Gaussian Example

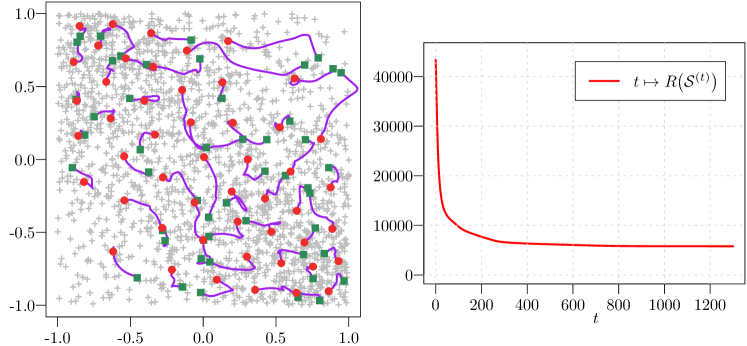

We consider a kernel matrix defined by a set consisting of points in (i.e. ); for the kernel parameter, we use . A graphical representation of the set is given in Figure 1; it consists of independent realisations of a bivariate random variable whose density is proportional to the restriction of a bi-Gaussian density to the set (the two modes of the underlying distribution are located at and , and the covariance matrix of the each Gaussian density is , with the identity matrix).

The initial samples are optimised via GD with stepsize and for a fixed number of iterations . A graphical representation of the paths followed by the landmark points during the optimisation process is given in Figure 1 (for and ); we observe that the landmark points exhibit a relatively complex dynamic, some of them showing significant displacements from their initial positions. The optimised landmark points concentrate around the regions where the density of points in is the largest, and inherit a space-filling-type property in accordance with the stationarity of the kernel .

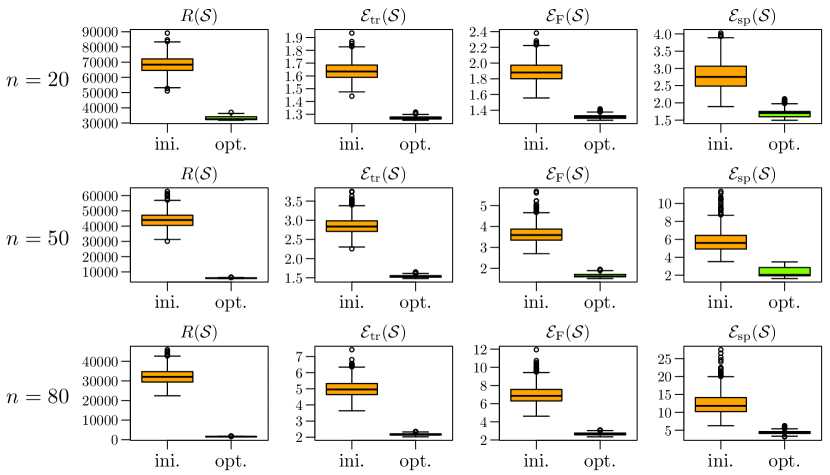

To assess the improvement yielded by the optimisation process, for a given number of landmark points , we randomly draw an initial Nyström sample from (uniform sampling without replacement) and compute the corresponding locally optimised sample (GD with and ). We then compare with , and compute the corresponding approximation factors with respect to the trace, Frobenius and spectral norms, see (8). We consider three different values of , namely , and , and each time perform repetitions of this experiment. Our results are presented in Figure 2; we observe that, independently of , the local optimisation produces a significant improvement of the Nyström approximation accuracy for all the criterion considered; the improvements are particularly noticeable for the trace and Frobenius norms, and slightly less for the spectral norm (which of the three, appears the coarsest measure of the approximation accuracy). Remarkably, the efficiencies of the locally optimised Nyström samples are relatively close to each other, in particular in terms of trace and Frobenius norms, suggesting that a large proportion of the local minima of the radial SKD induce approximations of comparable quality.

4.2 Abalone Data Set

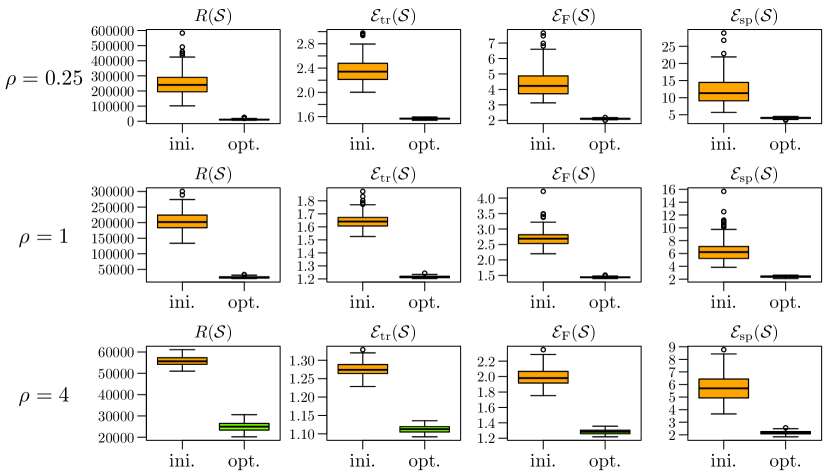

We now consider the attributes of the Abalone data set. After removing two observations that are clear outliers, we are left with entries. Each of the features is standardised such that it has zero mean and unit variance. We set and consider three different values of the kernel paramater , namely , , and ; this values are chosen so that the eigenvalues of the kernel matrix exhibit sharp, moderate and shallower decays, respectively. For the Nyström sample optimisation, we use SGD with i.i.d. sampling and batch size , and ; these values were chosen to obtain relatively efficient optimisations for the whole range of values of we consider. For each value of , we perform repetitions. The results are presented in Figure 3.

We observe that regardless of the values of and in comparison with the initial Nyström samples, the efficiencies of the locally optimised samples in terms of trace, Frobenius and spectral norms are significantly improved. As observed in Section 4.1, the gains yielded by the local optimisations are more evident in terms of trace and Frobenius norms, and the impact of the initialisation appears limited.

4.3 MAGIC Data Set

We consider the attributes of the MAGIC Gamma Telescope data set. In pre-processing, we remove the duplicated entries in the data set, leaving us with data points; we then standardise each of the features of the data set. For the kernel parameter, we use .

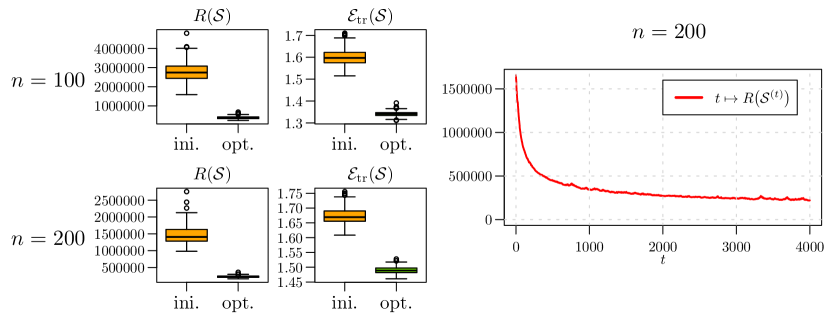

In Figure 4, we present the results obtained after the local optimisation of random initial Nyström samples of size and . Each optimisation was performed through SGD with i.i.d. sampling, batch size and stepsize ; as number of iterations, for , we used , and for . The optimisation parameters were chosen to obtain relatively efficient but not fully completed descents, as illustrated in Figure 4. Alongside the radial SKD, we only compute the approximation factor corresponding to the trace norm (the trace norm is indeed the least costly to evaluate of the three matrix norms we consider, see Section 1.2). As in the previous experiments, we observe a significant improvement of the initial Nyström samples obtained by local optimisation of the radial SKD.

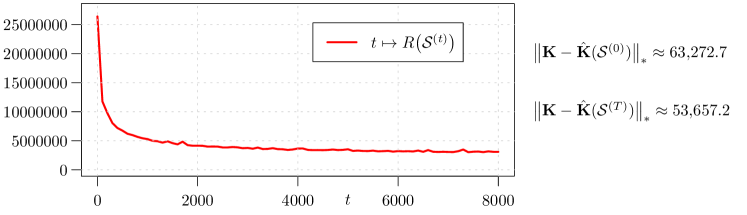

4.4 MiniBooNE Data Set

In this last experiment, we consider the attributes of the MiniBooNE particle identification data set. In pre-processing, we remove the entries in the data set with missing values, and entry appearing as a clear outlier, leaving us with data points; we then standardise each of the features of the data set. We use (kernel parameter).

We consider a random initial Nyström sample of size , and optimise it through SGD with i.i.d. sampling, batch size , stepsize ; the descent is stopped after iterations. The resulting decay of the radial SKD is presented in Figure 5 (the cost is evaluated every iterations), and the trace norm of the Nyström approximation error for the initial and locally optimised samples are reported. In terms of computation time, on our machine (endowed with an 3.5 GHz Dual-Core Intel Core i7 processor, and using a single-threaded C implementation interfaced with R), for , an evaluation of the radial SKD (up to the constant ) takes , while an evaluation of the term takes ; performing the optimisation reported in Figure 5 without checking the decay of the cost takes . This experiment illustrates the ability of the considered framework to tackle relatively large problems.

5 Conclusion

We demonstrated the relevance of the radial-SKD-based framework for the local optimisation, through SGD, of Nyström samples for SPSD kernel-matrix approximation. We studied the Lipschitz continuity of the underlying gradient and discussed its stochastic approximation. We performed numerical experiments illustrating that local optimisation of the radial SKD yields significant improvement of the Nyström approximation in terms of trace, Frobenius and spectral norms.

In our experiments, we implemented SGD with i.i.d. sampling, fixed stepsize and fixed number of iterations; although already bringing satisfactory results, to improve the time efficiency of the approach, the optimisation strategy could be accelerated by considering for instance adaptive stepsize, parallelisation or momentum-type techniques (see [16] for an overview). The initial Nyström samples we considered were draw uniformly at random without replacement; while our experiments suggest that the local minima of the radial SKD often induce approximations of comparable quality, the use of more efficient initialisation strategies may be investigated (see e.g. [13, 11, 18, 3, 4]).

As a side note, when considering the trace norm, the Nyström sampling problem is intrinsically related to the integrated-mean-squared-error design criterion in kernel regression (see e.g. [15, 8, 17]); consequently the approach considered in this paper may be used for the design of experiments for such models.

Appendix

Proof of Theorem 2.1.

We consider a Nyström sample and introduce

| (9) |

In view of (5), the partial derivative of at with respect to the -th coordinate of the -th landmark point can be written as

| (10) |

For and with , and for and , the second-order partial derivatives of at , with respect to the coordinates of the landmark points in , verify

| (11) | ||||

| (12) | ||||

where the partial derivative of with respect to the -th coordinate of the -th landmark point is given by

| (13) |

From (C.1), we have

| (14) |

By the Schur product theorem, the squared kernel is SPSD; we denote by the RKHS of real-valued functions on for which is reproducing. For and , we have , with the inner product on , and where is such that , for all . From the Cauchy-Schwartz inequality, we have

| (15) |

By combining (9) with inequalities (14) and (15), we obtain

| (16) |

Let and let . From equation (13), and using inequalities (14) and (16) together with (C.2), we obtain

| (17) |

In addition, let and ; from equations (11), (12), (16) and (17), and conditions (C.2) and (C.3), we get

| (18) |

and

| (19) |

For , we denote by the matrix with entry given by (11) if , and by (12) otherwise. The Hessian can then be represented as a block-matrix, that is

The entries of the diagonal blocks of are of the form (11), and the entries of the off-diagonal blocks of are the form (12). From inequalities (18) and (19), we obtain

with

For all , the constant is an upper bound for the spectral norm of the Hessian matrix , so the gradient of is Lipschitz continuous over , with Lipschitz constant . ∎

References

- [1] Alain Berlinet and Christine Thomas-Agnan. Reproducing Kernel Hilbert Spaces in Probability and Statistics. Springer Science, 2004.

- [2] Léon Bottou, Frank E Curtis, and Jorge Nocedal. Optimization methods for large-scale machine learning. Siam Review, 60(2):223–311, 2018.

- [3] Difeng Cai, Edmond Chow, Lucas Erlandson, Yousef Saad, and Yuanzhe Xi. SMASH: Structured matrix approximation by separation and hierarchy. Numerical Linear Algebra with Applications, 25, 2018.

- [4] Michal Derezinski, Rajiv Khanna, and Michael W. Mahoney. Improved guarantees and a multiple-descent curve for Column Subset Selection and the Nyström method. In Advances in Neural Information Processing Systems, 2020.

- [5] Petros Drineas and Michael W. Mahoney. On the Nyström method for approximating a Gram matrix for improved kernel-based learning. Journal of Machine Learning Research, 6:2153–2175, 2005.

- [6] Dheeru Dua and Casey Graff. UCI machine learning repository, 2019.

- [7] Bertrand Gauthier. Nyström approximation and reproducing kernels: embeddings, projections and squared-kernel discrepancy. Preprint, 2021.

- [8] Bertrand Gauthier and Luc Pronzato. Convex relaxation for IMSE optimal design in random-field models. Computational Statistics and Data Analysis, 113:375–394, 2017.

- [9] Bertrand Gauthier and Johan Suykens. Optimal quadrature-sparsification for integral operator approximation. SIAM Journal on Scientific Computing, 40:A3636–A3674, 2018.

- [10] Alex Gittens and Michael W. Mahoney. Revisiting the Nyström method for improved large-scale machine learning. Journal of Machine Learning Research, 17:1–65, 2016.

- [11] Sanjiv Kumar, Mehryar Mohri, and Ameet Talwalkar. Sampling methods for the Nyström method. Journal of Machine Learning Research, 13:981–1006, 2012.

- [12] Jason D Lee, Max Simchowitz, Michael I Jordan, and Benjamin Recht. Gradient descent only converges to minimizers. In Conference on learning theory, pages 1246–1257. PMLR, 2016.

- [13] Harald Niederreiter. Random Number Generation and Quasi-Monte Carlo Methods. SIAM, 1992.

- [14] Vern I. Paulsen and Mrinal Raghupathi. An Introduction to the Theory of Reproducing Kernel Hilbert Spaces. Cambridge University Press, 2016.

- [15] C.E. Rasmussen and C.K.I. Williams. Gaussian Processes for Machine Learning. MIT press, Cambridge, MA, 2006.

- [16] Sebastian Ruder. An overview of gradient descent optimization algorithms. arXiv preprint arXiv:1609.04747, 2016.

- [17] Thomas J. Santner, Brian J. Williams, and William I. Notz. The Design and Analysis of Computer Experiments. Springer, 2018.

- [18] Shusen Wang, Zhihua Zhang, and Tong Zhang. Towards more efficient SPSD matrix approximation and CUR matrix decomposition. Journal of Machine Learning Research, 17:7329–7377, 2016.