tcb@breakable

33institutetext: 1 Centrum Wiskunde & Informatica, Department of Stochastics

Science Park 123

1098 XG, Amsterdam, Netherlands

44institutetext: 2 Vrije Universiteit, Department of Mathematics

De Boelelaan 1111

1081 HV, Amsterdam, Netherlands

55institutetext: 3 Vrije Universiteit, Department of Computer Science

De Boelelaan 1111

1081 HV, Amsterdam, Netherlands

The Dutch Draw: Constructing a Universal Baseline for Binary Prediction Models

Abstract

Novel prediction methods should always be compared to a baseline to know how well they perform. Without this frame of reference, the performance score of a model is basically meaningless. What does it mean when a model achieves an of 0.8 on a test set? A proper baseline is needed to evaluate the ‘goodness’ of a performance score. Comparing with the latest state-of-the-art model is usually insightful. However, being state-of-the-art can change rapidly when newer models are developed. Contrary to an advanced model, a simple dummy classifier could be used. However, the latter could be beaten too easily, making the comparison less valuable. This paper presents a universal baseline method for all binary classification models, named the Dutch Draw (DD). This approach weighs simple classifiers and determines the best classifier to use as a baseline. We theoretically derive the DD baseline for many commonly used evaluation measures and show that in most situations it reduces to (almost) always predicting either zero or one. Summarizing, the DD baseline is: (1) general, as it is applicable to all binary classification problems; (2) simple, as it is quickly determined without training or parameter-tuning; (3) informative, as insightful conclusions can be drawn from the results. The DD baseline serves two purposes. First, to enable comparisons across research papers by this robust and universal baseline. Secondly, to provide a sanity check during the development process of a prediction model. It is a major warning sign when a model is outperformed by the DD baseline.

Keywords:

Baseline Benchmark Evaluation Supervised learning Binary classification1 Introduction

A typical data science project can be crudely simplified to the following steps: (1) comprehending the problem context, (2) understanding the data, (3) preparing the data, (4) modeling, (5) evaluating the model, and (6) deploying the model (Wirth and Hipp, 2000). Before deploying a new model, it should be tested whether it meets certain predefined success criteria. A baseline plays an essential role in this evaluation, as it gives an indication of the actual performance of a model.

However, which baseline should be selected? A good baseline is desirable, but what explicitly makes a baseline ‘good’? Comparing with the latest state-of-the-art model is usually insightful. However, being state-of-the-art can change rapidly when newer models are developed. Reproducibility of a model is also often a problem, because code is not published or large amounts of computational resources are required to retrain the model. These aspects make it hard or even impossible to compare older results with newer research. Nevertheless, it is important to stress that the comparison with a state-of-the-art model still has merit. However, we are pleading for an additional universal baseline that can be computed quickly and can make it possible to compare results across research domains and papers. With that aim in mind, we outline three principal properties that any universal baseline should have: generality, simplicity, and informativeness.

Generality

In research, a new model is commonly compared to a limited number of existing models that are used in the same field. Although these are usually carefully selected, they are still subjectively chosen. Take binary classification, in which the objective is to label each observation either zero or one. Here, one could already select a decision tree (Min and Jeong, 2009), random forest (Couronné et al., 2018), variants of naive Bayes (Wang and Manning, 2012), -nearest neighbors (Araújo et al., 2017), support vector machine (Shahraki et al., 2017), neural network (Sundarkumar and Ravi, 2013), or logistic regression model (Sergioli et al., 2019) to evaluate the performance. These models are often trained specifically for a problem instance with parameters tuned for optimal performance in that specific case. Hence, these methods are not general. One could not take a decision tree that is used for determining bankruptcy (Min and Jeong, 2009) and use it as a baseline for a pathological voice detection problem (Muhammad and Melhem, 2014). At least structural adaptations and retraining are necessary. A good standard baseline should be applicable to all binary classification problems, irrespective of the domain.

Simplicity

An additional universal baseline should not be too complex. But, it is hard to determine for a measure if a baseline is too complex or not. Essentially, two components are critical in our view: (1) computational timeand (2) explainability. It is necessary for practical applications that the baseline can be determined relatively fast. For example, training a neural network many times to generate an average baseline or optimizing the parameters of a certain model could take too much valuable time. Secondly, if a baseline is very complex, it can be harder to draw meaningful conclusions. Is it expected that a new model is outperformed by this ingeniously complicated baseline, or is it exactly what one would expect? This leads to the last property of a good standard baseline.

Informativeness

Our baseline should be informative. When a method achieves a score higher or lower than the baseline, clear conclusions need to be drawn. Is it obvious that the baseline should be beaten? Consider the athletic event high jump, where an athlete needs to jump over a bar at a specific height. If the bar is set too low, anyone can jump over it. If the bar is too high, no one makes it. Both situations do not give us any additional information to distinguish a professional athlete from a regular amateur. The bar should be placed at a height where the professional could obviously beat it, but the amateur can not. Drawing from this analogy, a baseline should be obviously beaten by any developed model. If not, this should be considered a major warning sign.

Our research focuses on finding such a general, simple and informative baseline for binary classification problems. Although we focus on these type of problems, the three properties should also hold for constructing baselines in other supervised learning problems, such as multiclass classification and regression. Two methods that immediately come to mind are dummy classifiers and optimal threshold classifiers. They could be ideal candidates for our additional universal baseline.

Dummy classifier

A dummy classifier is a non-learning model that makes predictions following a simple set of rules. For example, always predicting the most frequent class label or predicting each class with some probability. A dummy classifier is simple and general, however it is not always informative. The information gained by performing better than a simple dummy classifier can even be zero. With the plethora of dummy classifiers, selection is also still arbitrary and questionable.

Optimal threshold classifier

Koyejo et al. (2014) determined for a large family of binary performance measures that the optimal classifier consists of a sign function with a threshold tailored to each specific measure. To determine the optimal classifier, it is necessary to know or approximate , which is the probability that the binary label is 1 given the features . Lipton et al. (2014) had a similar approach, but they only focus on the score. The conditional probabilities need to be learned from training data. However, this leads to arbitrary selections, as a model is necessary to approximate these probabilities. It is a clever approach, but unfortunately there is no clear-cut best approximation model for different research domains. If the approximation model is not accurate, the optimal classifier is based on wrong information, which makes it hard to draw meaningful conclusions from this approach.

Both the dummy classifier and the optimal threshold classifier have their strengths and weaknesses. In this paper, we introduce a novel baseline approach, called the Dutch Draw (DD). The DD eliminates these weaknesses, whilst keeping their strengths. The DD can be seen as a dummy classifier on steroids. Instead of arbitrarily choosing a dummy classifier, we mathematically derive which classifier, from a family of classifiers, has the best expected performance. Also, this expected performance can be directly determined, making it very fast to obtain the baseline. The DD baseline is: (1) applicable to any binary classification problem; (2) reproducible; (3) simple; (4) parameter-free; (5) more informative than any single dummy baseline; (6) and an explainable minimal requirement for any new model. This makes the DD an ideal candidate for a universal baseline in binary classification.

Our contributions are as follows: (1) we introduce the DD and explain why this method produces a universal baseline that is general, simple and informative for all binary classification problems; (2) we provide the mathematical properties of the DD for many evaluation measures and summarize them in several tables; (3) we demonstrate how the DD baseline can be used in practice to identify which models should definitely be reconsidered; (4) and we made the DD available in a Python package.111https://github.com/joris-pries/DutchDraw

2 Preliminaries

Before formulating the DD, we need to introduce necessary notation, and simultaneously, provide elementary information on binary classification. This is required to explain how binary models are evaluated. Then, we discuss how performance measures are constructed for binary classification and we examine the ones that are most commonly used.

2.1 Binary classification

The goal of binary classification is to learn (from a dataset) the relationship between the input variables and the binary output variable. When the dataset consists of observations, let be the set of observation indices. Each instance, denoted by , has explanatory feature values. These features can be categorical or numerical. Without loss of generality, we assume that for all . Moreover, each observation has a corresponding output value . Now, let denote the matrix with all observations and their explanatory feature values and let be the response vector. The complete dataset is then represented by . We call the observations with response value ‘positive’, while the observations with response value are ‘negative’. Let denote the number of positives and the number of negatives. Note that by definition must hold.

2.2 Evaluation measures

An evaluation measure quantifies the prediction performance of a trained model. We categorize the evaluation measures into two groups: base measures and performance measures (Canbek et al., 2017). Since there are two possible values for both the predicted and the true classes in binary classification, there are four base measures: the number of true positives (TP), false positives (FP), false negatives (FN) and true negatives (TN). Performance measures are a function of one or more these four base measures. To shorten notation, let and denote the number of positively and negatively predicted instances respectively.

All considered performance measures and base measures are shown in Table 1. Also their abbreviations, possibly alternative names, their definitions and corresponding codomains are presented in Table 1. The codomains show in what set the measure can theoretically take values (without considering the exact values of , , and ). In Sec. 3, the case-specific codomains are provided when we discuss the evaluation measures in more detail. Finally, note that the list is not exhaustive, but it contains most of the commonly used evaluation measures.

Measure Definition Codomain True Positives (TP) TP True Negatives (TN) TN False Negatives (FN) FN False Positives (FP) FP True Positive Rate (TPR), Recall, Sensitivity True Negative Rate (TNR), Specificity, Selectivity False Negative Rate (FNR), Miss Rate False Positive Rate (FPR), Fall-out Positive Predictive Value (PPV), Precision Negative Predictive Value (NPV) False Discovery Rate (FDR) False Omission Rate (FOR) score () Youden’s J Statistic/Index (J), (Bookmaker) Informedness Markedness (MK) Accuracy (Acc) Balanced Accuracy (BAcc) Matthews Correlation Coefficient (MCC) Cohen’s kappa () Fowlkes-Mallows Index (FM), G-mean 1 G-mean 2 () Prevalence Threshold (PT) Threat Score (TS), Critical Success Index

Ill-defined measures

Not every evaluation measure is well-defined. Often, the problem occurs due to division by zero. For example, the True Positive Rate (TPR) defined as cannot be calculated whenever . Therefore, we have made assumptions for the allowed values of , , and . These are shown in Table 2. One exception is the Prevalence Threshold (PT) (Balayla, 2020), where the denominator is zero if TPR is equal to the False Positive Rate (defined as ). Depending on the classifier, this situation could occur regularly. Therefore, PT is omitted throughout the rest of this research.

| Domain requirement for: | ||||

| Measure | ||||

| TP, TN, FN, FP, Acc, | - | - | - | - |

| TPR, FNR, TS | - | - | - | |

| TNR, FPR | - | - | - | |

| PPV, FDR | - | - | - | |

| NPV, FOR | - | - | - | |

| , FM | - | - | ||

| J, BAcc, | - | - | ||

| MK | - | - | ||

| MCC | ||||

3 Dutch Draw (DD)

In this section, we introduce the DD framework and discuss how this method is able to provide a universal baseline for any evaluation measure. This baseline is general, simple, and informative, which is crucial for a good baseline, as we explained in Sec. 1. First, we provide the family of DD classifiers, and thereafter explain how the optimal classifier generates the baseline.

3.1 Dutch Draw classifiers

The goal of our research is to provide a universal baseline for any evaluation measure in binary classification. The DD baseline comes from choosing the best DD classifier. Before we discuss what ‘best’ actually entails, we have to define the DD classifier in general. This is the function with input an evaluation dataset with observations and feature values per observation. The function generates the predictions for these observations by outputting a vector of binary predictions. It is described in words as:

| of rows from and assign to these observations and | |||

Here, is the function that rounds its argument to the nearest integer. The parameter controls what percentage of observations are predicted as positive. The mathematical definition of is given by:

with the vector with ones in the positions in and zeroes elsewhere. Note that a classifier does not learn from the features in the data, just as a dummy classifier. The set of all DD classifiers is the complete family of models that classify a random sample of any size as positive.

Given a DD classifier, the number of predicted positives depends on and is given by and the number of predicted negatives is . To be specific, these two numbers are integers, and thus, different values of can lead to the same value of . Therefore, we introduce the parameter as the discretized version of . Furthermore, we define:

as the set of all unique values that can obtain for all .

Next, we derive mathematical properties of the DD classifier for every evaluation measure in Table 1 (except PT). Note that the DD is stochastic, thus we examine the distribution of the evaluation measure. Furthermore, we also determine the range and expectation of a DD classifier.

3.1.1 Distribution

The distributions of the base measures (see Sec. 2.2) are directly determined by . Consider for example TP: the number of positive observations that are also predicted to be positive. In a dataset of observations with labeled positive, random observations are predicted as positive in the DD approach. This implies that is hypergeometrically distributed with parameters , and , as the classifier randomly draws samples without replacement from a population of size , where samples are labeled positive. Thus:

where is the domain of . The definition of this domain is given in Eq. (1).

The other three base measures are also hypergeometrically distributed following similar reasoning. This leads to:

Note that these random variables are not independent. In fact, they can all be written in terms of . This is a crucial effect of the DD approach, as it reduces the formulations to only a function of a single variable. Consequently, most evaluation measures can be written as a linear combination of only . With only one random variable, theoretical derivations and optimal classifiers can be determined. As mentioned before, and , and we also have , because this denotes the total number of positively predicted observations. These three identities are linear in , thus each base measure can be written in the form with . Additionally, let be the probability distribution of . Then, by combining the identities, we get:

| (B1) | ||||

| (B2) | ||||

| (B3) | ||||

| (B4) |

with .

Example: distribution score

To illustrate how the probability function can directly be derived, we consider the score (Chinchor, 1992). It is the weighted harmonic average between the True Positive Rate () and the Positive Predictive Value (). The latter two performance measures are discussed extensively in A.5 and A.9, respectively. The score balances predicting the actual positive observations correctly () and being cautious in predicting observations as positive (). The factor indicates how much more is weighted compared to . The score is commonly defined as:

By substituting and by their definitions (see Table 1) and using Eq. (B1) and (B2), we get:

Since is only defined when and is only defined when , we need for that both these restrictions hold. The definition of is linear in and can therefore be formulated as:

3.1.2 Range

The values that can attain depend on and , and of course, on the domain of . Without restriction, the maximum number that can be is . Then, all positive observations are also predicted to be positive. However, when is small enough such that , then only observations are predicted as positive. Consequently, can only reach the value in this case. Hence, in general, the upper bound of the domain of is . The same reasoning holds for the lower bound: when is small enough, the minimum number of is 0, since all positive observations can be predicted as negative. However, when gets large enough, positive observations have to be predicted positive even if all negative observations are predicted positive. Thus, in general, the lower bound of the domain is . Now, let be the domain of , then:

| (1) |

Consequently, the range of is given by

| (R) |

3.1.3 Expectation

The introduction of allows us to write its expected value in terms of and . This statistic is required to calculate the actual baseline. Since has a distribution, its expected value is known and given by

Next, we obtain the following general definition for the expectation of :

| () |

This rule is consistently used to determine the expectation for each measure.

Example: expectation score

To demonstrate how the expectation is calculated for a performance measure, we again consider . It is linear in with and , and so, its expectation is given by:

| (2) |

A full overview of the distribution and mean of all considered base and performance measures is given in Table 3. All the calculations performed to derive the corresponding distributions and expectations are provided in Appendix A.

| Distribution | |||

| Measure | Expectation | ||

| TP | |||

| TN | |||

| FN | |||

| FP | |||

| TPR | |||

| TNR | |||

| FNR | |||

| FPR | |||

| PPV | |||

| NPV | |||

| FDR | |||

| FOR | |||

| J | |||

| MK | |||

| Acc | |||

| BAcc | |||

| MCC | |||

| FM | |||

| - | Nonlinear in | Nonlinear in | |

| TS | - | Nonlinear in | Nonlinear in |

3.2 Optimal Dutch Draw classifier

Next, we discuss how the DD baseline will ultimately be derived. In order to do so, an overview is presented in Fig. 1. Starting with the definition of the DD classifiers in Sec. 3.1 and determining their expectations for commonly used measures (see Table 3), we are now able to identify the optimal DD classifier. Given a performance measure and dataset, the optimal DD classifier is found by optimizing (taking the minimum or maximum of) the associated expectation for .

3.2.1 Dutch Draw baseline

The optimal DD classifiers and the corresponding DD baseline can be found in Table 4. For many performance measures, it is optimal to always predict positive or negative. In some cases, this is not allowed due to ill-defined measures. Then, it is often optimal to only predict one sample differently. For several other measures, almost all parameter values give the optimal baseline. Next, we give an example to illustrate how the results of Table 4 are derived.

Example: DD baseline for the score

To determine the DD baseline, the extreme values of the expectation need to be identified. To do this, examine the following function defined as:

The relationship between and is given as . To find the extreme values, we have to look at the derivative of :

It is strictly positive for all in its domain, thus is strictly increasing in . This means is non-decreasing in and also in , because the term is non-decreasing in . Hence, the extreme values of the expectation of are its border values:

Note that is a restriction for , and hence the optima are taken over the interval . Furthermore, the optimization values and for the extreme values are given by

respectively. Following this reasoning, the discrete forms and are given by

The smallest is obtained when all observations except one are predicted negative, while predicting everything positive yields the largest .

| Measure | ||||

| TP | ||||

| TN | ||||

| FN | ||||

| FP | ||||

| TPR | ||||

| TNR | ||||

| FNR | ||||

| FPR | ||||

| PPV | ||||

| NPV | ||||

| FDR | ||||

| FOR | ||||

| J | ||||

| MK | ||||

| Acc | 222If , then . Note that Iverson brackets are used to simplify notation. | 2 | ||

| BAcc | ||||

| MCC | ||||

| 333If , then . | 3 | |||

| FM | ||||

| - | - | |||

| TS | ||||

4 Dutch Draw in Practice

Now that we have established how to derive the DD baseline, it is time to see it in action. As a demonstration, we determined the DD baseline for commonly used evaluation measures on eight datasets extracted from the UCI machine learning archive (Dua and Graff, 2021): Adult, Bank Marketing, Banknote Authentication, Cleveland Heart Disease, Haberman’s Survival, LSVT Voice Rehabilitation, Occupancy Detection, and Wisconsin Cancer. The resulting DD baselines are shown in Table 5. For some measures, the DD baseline already achieves the highest attainable score, such as for TPR and FNR. This suggests that these measures are not reliable indicators of the overall performance of a model. The problem is that these measures are only concerned with correctly predicting the positive instances. Always predicting positive therefore trivially gives the optimal performance. A less obvious DD baseline is the one for the score on the Bank Marketing dataset. The DD achieves an expected performance of approximately . Any new model for the Bank Marketing dataset should therefore surpass this score. Next, we want to discuss what conclusions can be drawn from such a comparison by examining the following example.

Measure Adult 444Dua and Graff (2021) Bank Marketing 555Moro et al. (2014) Banknote Authentication 4 Cleveland Heart Disease 4 Haberman’s Survival 4 LSVT Voice Rehabilitation 666Tsanas et al. (2014) Occupancy Detection 777Candanedo and Feldheim (2016) Wisconsin Cancer (Diagnostic) 4 TP 11687 5289 610 139 81 42 4750 212 TN 37155 39922 762 164 225 84 15810 357 FN 37155 39922 672 164 225 84 15810 357 FP 11687 5289 610 139 81 42 4750 212 TPR 1 1 1 1 1 1 1 1 TNR 1 1 1 1 1 1 1 1 FNR 1 1 1 1 1 1 1 1 FPR 1 1 1 1 1 1 1 1 PPV 0.239 0.117 0.445 0.459 0.265 0.333 0.231 0.373 NPV 0.761 0.883 0.555 0.541 0.735 0.667 0.769 0.627 FDR 0.761 0.883 0.555 0.541 0.735 0.667 0.769 0.627 FOR 0.239 0.117 0.445 0.459 0.265 0.333 0.231 0.373 0.386 0.209 0.616 0.629 0.419 0.5 0.375 0.543 J 0 0 0 0 0 0 0 0 MK 0 0 0 0 0 0 0 0 Acc 0.761 0.883 0.555 0.541 0.735 0.667 0.769 0.627 BAcc 0.5 0.5 0.5 0.5 0.5 0.5 0.5 0.5 MCC 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 FM 0.489 0.342 0.667 0.677 0.514 0.577 0.481 0.61 0.5 0.5 0.5 0.5 0.5 0.5 0.5 0.5 TS 0.239 0.117 0.445 0.459 0.265 0.333 0.231 0.373

4.1 Example: Cleveland Heart disease

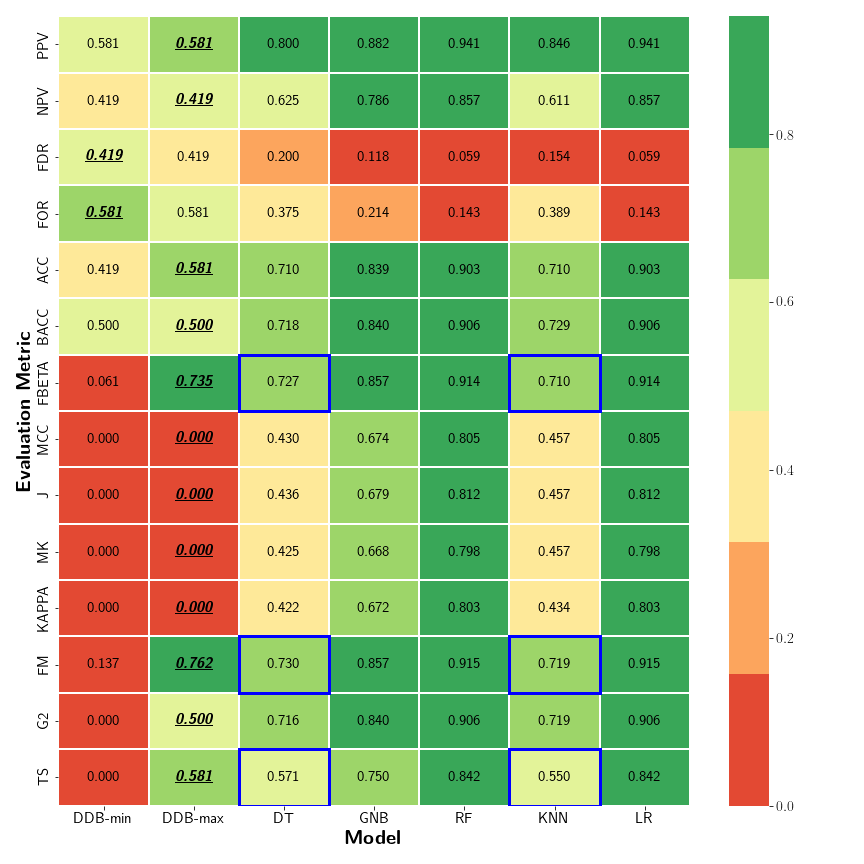

The objective of this dataset is to predict whether patients have a heart disease given several feature values. In order to do so, we used five commonly used machine learning algorithms to perform this binary classification task: logistic regression, decision tree, random forest, -nearest neighbors, and Gaussian naive Bayes. These algorithms all had their default parameters in scikit-learn (Pedregosa et al., 2011). The dataset was randomly split in a training (90%) and test set (10%). Fig. 2 shows the corresponding performance results.

Before applying a newly developed model to actual patients, its performance should at least be better than the DD baseline, as the latter does not learn anything from the feature values of the data. In Fig. 2, we see that some methods fail to beat the baseline and should therefore be reconsidered. For example, decision tree and -nearest neighbors underperform for the score (FBETA), Fowlkes-Mallows Index (FM), and Threat Score (TS). Note that the two methods were not trained to be optimal for the selected performance measures, whereas the DD does take the performance measure into account. However, this does not make the comparison unfair, since they are not competing for being the best prediction method. After all, the DD baseline is a minimal requirement for any new binary classification method. Even though a model is optimized for, say, the Accuracy, its performance should still beat the DD baseline for the score, as both the Accuracy and score provide indications of the overall prediction performance. To conclude, this example shows how the DD can be used in practice and why it is valuable in the evaluation process.

5 Discussion and Conclusion

In this research, we have proposed a new baseline methodology called the Dutch Draw (DD). The DD baseline is: (1) applicable to any binary classification problem; (2) reproducible; (3) simple; (4) parameter-free; (5) more informative than any single dummy baseline; (6) and an explainable minimal requirement for any new model. We have shown that for most commonly used measures the DD baseline can be theoretically determined (see Table 4). When the baseline cannot be derived directly, it can be identified quickly by computation. For most performance measures, the DD baseline reduces to one of the following three cases: (i) always predicting positive or negative; (ii) always predicting positive or negative, except for one instance; (iii) any DD classifier, except maybe for or . However, there are exceptions to these three cases. Examine the following example for the G-mean 2: and . We have previously seen (Table 4) that achieves the lowest expected score. To find the highest expected score, note that gives an expected score of , a score of , and a score of . This shows that the optimal parameter is not in , as . In this case, the maximum is achieved for . This shows that the DD does not always reduce to one of the three previously mentioned cases and does not always give straightforward results.

By introducing the DD baseline, we have simplified and improved the evaluation process of new binary classification methods. We consider it a minimal requirement for any novel model to at least beat the DD baseline. When this does not happen, the question is raised how much a new method has even learned from the data, since the DD baseline is derived from dummy classifiers. When the novel model has beaten the DD baseline, it should still be compared to a state-of-the-art method in that specific domain to obtain additional insights. In Sec. 4, we have shown how the DD should be used in practice and that commonly used approaches such as -nearest neighbors and a decision tree can underperform. Hence, using the Dutch Draw as a general, simple and informative baseline should be the new gold standard in any model evaluation process.

5.1 Further research

Our baseline is a stepping stone for further research, where multiple avenues should be explored. We discuss four possible research directions.

Firstly, we are now able to determine whether a binary classification model performs better than a universal baseline. However, we do not yet know how much it performs better (or worse). For example, let the baseline have a score of 0.5 and a new model a score of 0.9. How much better is the latter score? It could be that a tiny bit of extra information easily pushes the score from 0.5 to 0.9. Or, it is possible that a model needs a lot of information to understand the intricacies of the problem, making it very difficult to reach a score of 0.9. Thus, it is necessary to quantify how hard it is to reach any score. Also, when another model is added that achieves a score of 0.91, can the difference in performance of these models be quantified? Is it only a slightly better model or is it a leap forward?

Secondly, our DD baseline could be used to construct new standardized evaluation measures from their original versions. The advantage of these new measures would be that the interpretation of their scores is independent of the number of positive and negative observations in the dataset. In other words, the DD baseline would already be incorporated in the new measure, such that comparing a score to the baseline is not necessary anymore. There are many ways how the DD baseline can be used to scale a measure. Let and denote the maximum and minimum Dutch Draw baseline, respectively. As an example, a measure with range that needs to be maximized can be rescaled by

Everything below the lowest Dutch Draw baseline () gets value , because every Dutch Draw classifier is then performing better. This should be a major warning sign. A score between and is rescaled to . This value indicates that the performance is still worse than the best Dutch Draw baseline. All scores above are scaled to In this case, the performance at least performed better than the best Dutch Draw baseline.

Thirdly, another natural extension would be to drop the binary assumption and consider multiclass classification. This is more complicated than it seems, because not every multiclass evaluation measure follows automatically from its binary counterpart. However, we expect that for most multiclass measures it is again optimal to always predict a single specific class.

Fourthly, the essence of the DD could be used to create universal baselines for other prediction problems, such as for regression problems. This means an approach that also uses (almost) no information from the data and is able to generate a measure-specific baseline to which newly developed models could be compared.

As a final note, we have published the code for the DD, such that the reader can easily implement the baseline into their binary classification problems.888https://github.com/joris-pries/DutchDraw

Appendix A Mathematical Derivations

This section contains the complete theoretical analysis that is used to gather the information presented in Sec. 2 and 3, and more specifically, Table 2, 3 and 4. Each subsection is dedicated to one of the evaluation measures. The following definitions are frequently used throughout this section:

An overview of the entire Appendix can be viewed in Table 6.

A.1 Number of True Positives

The Number of True Positives is one of the four base measures that are introduced in Sec. 2.2. This measure indicates how many of the predicted positive observations are actually positive. Under the DD methodology, each evaluation measure can be written in terms of .

A.1.1 Definition and Distribution

Since we want to formulate each measure in terms of , we have for :

The range of this base measure depends on . Therefore, Eq. (R) yields the range of this measure:

A.1.2 Expectation

The expectation of using the DD is given by

| (3) |

A.1.3 Optimal Baselines

The DD baseline is given by the optimal expectation. Eq. (3) shows that the expected value depends on the parameter . Therefore, either the minimum or maximum of the expectation yields the baseline. They are given by

The values of that minimize or maximize the expected value are and , respectively, and are defined as

Equivalently, the discrete optimizers and are determined by

A.2 Number of True Negatives

The Number of True Negatives is also one of the four base measures and is introduced in Sec. 2.2. This base measure counts the number of negative predicted instances that are actually negative.

A.2.1 Definition and Distribution

Since we want to formulate each measure in terms of , we have for :

which corresponds to Eq. (B4). Furthermore,

and for its range

A.2.2 Expectation

is linear in with slope and intercept , so its expectation is given by

A.2.3 Optimal Baselines

To determine the range of the expectation of , and hence, obtain baselines, its extreme values are calculated:

The associated optimization values and are

The discrete equivalents and are then determined by

A.3 Number of False Negatives

The Number of False Negative is one of the four base measures that are introduced in Sec. 2.2. This base measure counts the number of mistakes made by predicting instances negative while the actual labels are positive.

A.3.1 Definition and Distribution

A.3.2 Expectation

As Eq. (B3) shows, is linear in with slope and intercept . Hence, the expectation of is given by

A.3.3 Optimal Baselines

The range of the expectation of determines the baselines. The extreme values are given by

The associated optimization values and are then

respectively. The discrete versions and of the optimizers are as follows:

A.4 Number of False Positives

The Number of False Positives is one of the four base measures that we discussed in Sec. 2.2. This base measure counts the number of mistakes made by predicting instances positive while the actual labels are negative.

A.4.1 Definition and Distribution

Each base measure can be expressed in terms of , thus we have for :

and for its range:

A.4.2 Expectation

As Eq. (B2) shows, is linear in with slope and intercept , thus the expectation of is defined as

A.4.3 Optimal Baselines

The baselines of are given by the extreme values of its expectation. Hence:

The corresponding optimization values and are

The discrete versions and of the optimization values are determined by

A.5 True Positive Rate

The True Positive Rate , Recall, or Sensitivity is the performance measure that presents the fraction of positive observations that are correctly predicted. This makes it a fundamental performance measure in binary classification.

A.5.1 Definition and Distribution

The True Positive Rate is commonly defined as

| (4) |

Hence, should hold, otherwise the denominator is zero. Now, is linear in and can therefore be written as

| (5) |

and for its range:

A.5.2 Expectation

Since is linear in with slope and intercept , its expectation is

A.5.3 Optimal Baselines

The range of the expectation of directly determines the baselines. The extreme values are given by

Furthermore, the corresponding optimization values and are given by

The discrete versions and of the optimizers are then

respectively.

A.6 True Negative Rate

The True Negative Rate , Specificity, or Selectivity is the measure that shows how relatively well the negative observations are correctly predicted. Hence, this performance measure is a fundamental measure in binary classification.

A.6.1 Definition and Distribution

The True Negative Rate is commonly defined as

Hence, should hold, otherwise the denominator is zero. By using Eq. (B4), can be rewritten as

Hence, it is linear in and can therefore be written as

| (6) |

and for its range:

A.6.2 Expectation

Since is linear in in terms of with slope and intercept , its expectation is

A.6.3 Optimal Baselines

The extreme values of the expectation of determine the baselines. The range is given by

Moreover, the optimization values and corresponding to the extreme values are defined as

respectively. The discrete versions and of the optimizers are given by

A.7 False Negative Rate

The False Negative Rate or Miss Rate is the performance measure that indicates the relative number of incorrectly predicted positive observations. Therefore, it can be seen as the counterpart to the True Positive Rate that is discussed in Sec. A.5.

A.7.1 Definition and Distribution

The False Negative Rate is commonly defined as

Hence, should hold, otherwise the denominator is zero. With the aid of Eq. (B3), can be reformulated to

Thus, it is linear in and can therefore be written as

and for its range:

A.7.2 Expectation

Because is linear in with slope and intercept , its expectation is

A.7.3 Optimal Baselines

The range of the expectation of determines the baselines. The extreme values are given by:

Furthermore, the optimizers and for the extreme values are as follows:

respectively. The discrete versions and of the optimization values are then:

A.8 False Positive Rate

The False Positive Rate or Fall-out is the performance measure that shows the fraction of incorrectly predicted negative observations. Hence, it can be seen as the counterpart to the True Negative Rate that is introduced in Sec. A.6.

A.8.1 Definition and Distribution

The False Positive Rate is commonly defined as

Hence, should hold, otherwise the denominator is zero. By using Eq. (B2), can be restated as

| (7) |

Note that it is linear in and can therefore be written as

with range:

A.8.2 Expectation

Since is linear in with slope and intercept , its expectation is given by

A.8.3 Optimal Baselines

The extreme values of the expectation of determine the baselines. The range is given by

Moreover, the optimizers and for the extreme values are determined by

respectively. The discrete forms and of these are then

A.9 Positive Predictive Value

The Positive Predictive Value or Precision is the performance measure that considers the fraction of all positively predicted observations that are in fact positive. Therefore, it provides an indication of how cautious the model is in assigning positive predictions. A large value means the model is cautious in predicting observations as positive, while a small value means the opposite.

A.9.1 Definition and Distribution

The Positive Predictive Value is commonly defined as

| (8) |

By using Eq. (B1) and (B2), this definition can be reformulated to

Note that this performance measure is only defined whenever , otherwise the denominator is zero. Therefore, we assume specifically for that . The definition of is linear in and can thus be formulated as

| (9) |

with range:

A.9.2 Expectation

Because is linear in with slope and intercept , its expectation is

A.9.3 Optimal Baselines

The baselines are determined by the extreme values of the expectation of :

because the expectation does not depend on . Hence, the optimization values and are simply all allowed values for :

Consequently, the discrete versions and of these optimizers are in the set of all allowed discrete values:

A.10 Negative Predictive Value

The Negative Predictive Value is the performance measure that indicates the fraction of all negatively predicted observations that are in fact negative. Hence, it shows how cautious the model is in assigning negative predictions. A large value means the model is cautious in predicting observations negatively, while a small value means the opposite.

A.10.1 Definition and Distribution

The Negative Predictive Value is commonly defined as

With the help of Eq. (B3) and (B4), this definition can be rewritten as

Note that this performance measure is only defined whenever , otherwise the denominator is zero. Therefore, we assume specifically for that . The definition of is linear in and can thus be formulated as

| (10) |

with range:

A.10.2 Expectation

Since is linear in with slope and intercept , its expectation is given by

A.10.3 Optimal Baselines

The extreme values of the expectation of determine the baselines. They are given by

because the expectation does not depend on . Consequently, the optimization values and are all allowed values for :

This also means the discrete forms and of the optimizers are in the set of all allowed discrete values:

A.11 False Discovery Rate

The False Discovery Rate is the performance measure that looks at the fraction of positively predicted observations that are actually negative. Therefore, it can be seen as the counterpart to the Positive Predictive Value that we discuss in Sec. A.9. Consequently, a small value means the model is cautious in predicting observations as positive, while a large value means the opposite.

A.11.1 Definition and Distribution

The False Discovery Rate is commonly defined as

With the help of Eq. (9), this definition can be rewritten as

Note that this performance measure is only defined whenever , otherwise the denominator is zero. Therefore, we assume specifically for that . The definition of is linear in and can thus be formulated as

with range:

A.11.2 Expectation

Since is linear in with slope and intercept , its expectation is given by

A.11.3 Optimal Baselines

The extreme values of the expectation of determine the baselines. Its range is given by

because the expectation does not depend on . Consequently, the optimization values and are all allowed values for :

This also means the discrete forms and of the optimizers are in the set of all allowed discrete values:

A.12 False Omission Rate

The False Omission Rate is the performance measure that considers the fraction of observations that are predicted negative, but are in fact positive. Hence, it can be seen as the counterpart to the Negative Predictive Value that is introduced in Sec. A.10. As a consequence, a small value means the model is cautious is predicting observations negatively, while a large value means the opposite.

A.12.1 Definition and Distribution

The False Omission Rate is commonly defined as

With the aid of Eq. (B3), this can be reformulated to

Note that this performance measure is only defined whenever , otherwise the denominator is zero. Therefore, we assume specifically for that . Now, is linear in and can therefore be written as

with range:

A.12.2 Expectation

Because is linear in with slope and intercept , its expectation is

A.12.3 Optimal Baselines

The range of the expectation of determines the baselines. The extreme values are defined as

because the expectation does not depend on . Consequently, the optimization values and are all allowed values for :

This also means the discrete forms and of the optimizers are in the set of all allowed discrete values:

A.13 Score

The score was introduced by Chinchor (1992). It is the weighted harmonic average between the True Positive Rate () and the Positive Predictive Value (). These two performance measures are discussed extensively in Sec. A.5 and A.9, respectively, and their summarized results are shown in Tables 3 and 4. The score balances predicting the actual positive observations correctly () and being cautious in predicting observations as positive (). The factor indicates how much more is weighted compared to .

A.13.1 Definition and Distribution

The score is commonly defined as

By using the definitions of and in Eq. (4) and (8), can be formulated in terms of the base measures:

Eq. (B1) and (B2) allow us to write the formulation above in terms of only :

Note that and , otherwise or is not defined, and hence, is not defined. Now, is linear in and can be formulated as

with range:

A.13.2 Expectation

Because is linear in with slope and intercept , its expectation is given by

| (11) |

A.13.3 Optimal Baselines

To determine the extreme values of the expectation of , and therefore the baselines, the derivative of the function defined as

is calculated. First note that . The derivative is given by

It is strictly positive for all in its domain, thus is strictly increasing in . This means given in Eq. (11) is non-decreasing in both and . This is because the term is non-decreasing in . Hence, the extreme values of the expectation of are its border values:

Consequently, the optimization values and for the extreme values are given by

respectively. Following this reasoning, the discrete forms and are given by

A.14 Youden’s J Statistic

The Youden’s J Statistic , Youden’s Index, or (Bookmaker) Informedness was introduced by Youden (1950) to capture the performance of a diagnostic test as a single statistic. It incorporates both the True Positive Rate and the True Negative Rate, which are discussed in Sec. A.5 and A.6, respectively. Youden’s J Statistic shows how well the model is able to correctly predict both the positive as the negative observations.

A.14.1 Definition and Distribution

The Youden’s J Statistic is commonly defined as

By using Eq. (5) and (6), which provide the definitions of and in terms of , the definition of can be reformulated as

Because needs , and needs , we have both these assumptions for . Consequently, . Now, is linear in and can therefore be written as

with range:

A.14.2 Expectation

Since is linear in with slope and intercept , its expectation is given by

A.14.3 Optimal Baselines

The extreme values of the expectation of determine the baselines. They are given by

because the expected value does not depend on . Consequently, the optimization values and can be any value in the domain of :

This also holds for the discrete forms and of the optimizers:

A.15 Markedness

The Markedness or deltaP is a performance measure that is mostly used in linguistics and social sciences. It combines both the Positive Predictive Value and the Negative Predictive Value. These two measures are discussed in Sec. A.9 and A.10, respectively. The Markedness indicates how cautious the model is in predicting observations as positive and also how cautious it is in predicting them as negative.

A.15.1 Definition and Distribution

The Markedness is commonly defined as

This definition of can be reformulated in terms of by using Eq. (9) and (10):

Note that is only defined for and , otherwise the denominator becomes zero. The assumption automatically follows from the assumptions and , which hold for and , respectively. In other words, there is at least one observation predicted positive and at least one predicted negative, thus . Now, is linear in and can therefore be written as

with range:

A.15.2 Expectation

By using slope and intercept , the expectation of can be calculated:

A.15.3 Optimal Baselines

The extreme values of the expectation of determine the baselines. Its range is given by:

since the expected value does not depend on . Therefore, the optimization values and are in the set of allowed values for :

This also means the discrete forms and of the optimizers are in the set of the allowed discrete values:

A.16 Accuracy

The Accuracy is the performance measure that assesses how good the model is in correctly predicting the observations without making a distinction between positive or negative observations.

A.16.1 Definition and Distribution

The Accuracy is commonly defined as

By using Eq. (B4), this can be restated as

Note that it is linear in and can therefore be written as

| (12) |

with range:

A.16.2 Expectation

Since is linear in with slope and intercept , its expectation can be derived:

| (13) |

A.16.3 Optimal Baselines

The range of the expectation of directly determines the baselines. To determine the extreme values of , the derivative of the function defined as

is calculated. First, note that . The derivative is given by

It does not depend on , but whether the derivative is positive or negative depends on and . Whenever , then is strictly increasing for all in its domain. If , then is strictly decreasing. When , is constant. Consequently, the same holds for given in Eq. (13). This is because the term is non-decreasing in . Thus, the extreme values of the expectation of are given by

This means that the optimization values and for these extreme values respectively are given by

| (14) | ||||

| (15) |

Consequently, the discrete versions and of the optimizers are given by

| (16) | ||||

| (17) |

respectively.

A.17 Balanced Accuracy

The Balanced Accuracy is the mean of the True Positive Rate and True Negative Rate, which are discussed in Sec. A.5 and A.6. It determines how good the model is in correctly predicting the positive observations and in correctly predicting the negative observations on average.

A.17.1 Definition and Distribution

A.17.2 Expectation

is linear in with slope and intercept , so its expectation can be derived:

A.17.3 Optimal Baselines

The baselines are directly determined by the ranges of the expectation of . Since the expectation is constant, its extreme values are the same:

This means that the optimization values and for these extreme values respectively are simply

Consequently, the discrete versions and of the optimizers are given by

respectively.

A.18 Matthews Correlation Coefficient

The Matthews Correlation Coefficient was established by Matthews (1975). However, its definition is identical to that of the Yule phi coefficient, which was introduced by Yule (1912). The performance measure can be seen as the correlation coefficient between the actual and predicted classes. Hence, it is one of the few measures that lies in instead of .

A.18.1 Definition and Distribution

The Matthews Correlation Coefficient is commonly defined as

By using Eq. (B2) and (B4), this definition can be reformulated as

| (18) |

As Table 2 shows, the assumptions , , , and must hold. If one of these assumptions is violated, then the denominator in Eq. (18) is zero, and is not defined. Therefore, we have for that and . Next, to improve readability we introduce the variable to replace the denominator in Eq. (18):

The definition of is linear in and can thus be formulated as

with range:

A.18.2 Expectation

is linear in with slope and intercept , so its expectation can be derived from Eq. ( ‣ 3.1.3):

A.18.3 Optimal Baselines

The baselines are directly determined by the ranges of the expectation of . Since the expectation is constant, its extreme values are the same:

This means that the optimization values and for these extreme values respectively are simply:

Consequently, the discrete versions and of the optimizers are given by:

A.19 Cohen’s Kappa

Cohen’s kappa is a less straightforward performance measure than the other measures that we discuss in this research. It is used to quantify the inter-rater reliability for two raters of categorical observations (Kvålseth, 1989). In our case, we compare the first rater, which is the DD classifier, with the perfect rater, which assigns the true label to each observation.

A.19.1 Definition and Distribution

Although there are several definitions for Cohen’s kappa, here we choose the following:

with the Accuracy as defined in Sec. A.16 and the probability that the shuffle approach assigns the true label by chance. These two values can be expressed in terms of the base measures as follows:

By using Eq. (12), (B1), (B2), (B3) and (B4) the above can be rewritten as

Note that for to be well-defined, we need . In other words,

This simplifies to

| (19) |

The left-hand side is by definition in the interval . For the right-hand side to be in that interval, we firstly need . Since , that means , and hence, . Secondly, . Since we know , we obtain . This inequality reduces to , because is always at most . Whenever , then Eq. (19) becomes

To summarize, when , then all are allowed in , but when , then .

Now, by using and in the definition of Cohen’s kappa, we obtain:

To improve readability, we introduce the variables and defined as

Hence, is linear in and can be written as

with range:

A.19.2 Expectation

As Cohen’s kappa is linear in , its expectation can be derived:

A.19.3 Optimal Baselines

The baselines are directly determined by the ranges of the expectation of . Since the expectation is constant, its extreme values are the same:

This means that the optimization values and for these extreme values respectively are simply all allowed values:

Consequently, the discrete versions and of the optimizers are given by

A.20 Fowlkes-Mallows Index

The Fowlkes-Mallows Index or G-mean 1 was introduced by (Fowlkes and Mallows, 1983) as a way to calculate the similarity between two clusterings. It is the geometric average between the True Positive Rate () and Positive Predictive Value (), which are discussed in Sec. A.5 and A.9, respectively. It offers a balance between correctly predicting the actual positive observations () and being cautious in predicting observations as positive ().

A.20.1 Definition and Distribution

A.20.2 Expectation

Because is linear in with slope and intercept , its expectation is

A.20.3 Optimal Baselines

The extreme values of the expectation of determine the baselines. They are given by:

because the expectation is a non-decreasing function in . Note that the minimum and maximum are equal to each other when . Consequently, the optimizers and for the extreme values are determined by:

respectively. The discrete forms and of these are given by:

A.21 G-mean 2

The G-mean 2 was established by (Kubat et al., 1998). This performance measure is the geometric average between the True Positive Rate () and True Negative Rate (), which we discuss in Sec. A.5 and A.6, respectively. Hence, it balances correctly predicting the positive observations and correctly predicting the negative observations.

A.21.1 Definition and Distribution

The G-mean 2 is defined as

Since needs the assumption and needs , we have these restrictions also for . Consequently, . Now, by using the definitions of and in terms of in, respectively, Eq. (5) and (6), we obtain:

This function is not a linear function of , and hence, we cannot write it in the form for some variables .

A.21.2 Expectation

Since is not linear in , we cannot easily use the expectation of to determine that for . However, we are able to determine the second moment of :

Of course, since the distribution of is known, the expectation of can always be numerically calculated.

A.21.3 Optimal Baselines

Since the function given by is a convex function, we have by Jensen’s inequality that

This means that

Therefore, whenever , then . Since , it must hold that . Hence, the set contains minimizers for . The continuous version of this set is the interval . To show that this interval contains the only possible values for the minimizers, consider the definition for the expectation of :

where is the domain of , i.e., the set of values such that . Now, let be such that . Furthermore, consider the summand corresponding to :

which is strictly positive in both cases. Hence, there is at least one term in the summation in the definition of that is larger than 0, thus the expectation is strictly positive for . Consequently, the minimization values are

Following this reasoning, the discrete form is given by

A.22 Prevalence Threshold (PT)

A relatively new performance measure named Prevalence Threshold () was introduced by (Balayla, 2020). We could not find many articles that use this measure, but it is included for completeness. However, this performance measure has an inherent problem that eliminates the possibility to determine all statistics.

A.22.1 Definition and Distribution

The Prevalence Threshold is commonly defined as

By using the definitions of and in terms of (see Equations (5) and (7)), we obtain:

| (20) |

It is clear that this performance measure is not a linear function of , therefore we cannot easily calculate its expectation. However, there are more fundamental problems with .

A.22.2 Division by Zero

Eq. (20) shows that is a problematic measure. When is the denominator zero? This happens when . In this case, the fraction is undefined, as the denominator is zero. Furthermore, also the numerator is zero in that case. The number of true positives can attain the value whenever the latter is also an integer. For example, this always happens for . But even when , is still only safe to use when and are coprime, i.e., when the only positive integer that is a divisor of both of them is 1. Otherwise, there are always values of that cause to be an integer and therefore to be undefined when attains that value.

One solution would be to say , , whenever both the numerator and denominator are zero. However, this is arbitrary and directly influences the optimization of the expectation. This makes the optimal parameter values dependent on , which is beyond the scope of this chapter. Thus, no statistics are derived for the Prevalence Threshold .

A.23 Threat Score (TS) / Critical Success Index (CSI)

The Threat Score (Palmer and Allen, 1949) or Critical Success Index (Schaefer, 1990) is a performance measure that is used for evaluation of forecasting binary weather events: it either happens in a specific location or it does not. It was already used in 1884 to evaluate the prediction of tornadoes (Schaefer, 1990). The Threat Score is the ratio of successful event forecasts () to the total number of positive predictions () and the number of events that were missed ().

A.23.1 Definition and Distribution

A.23.2 Expectation

Because is not linear in , determining the expectation is less straightforward than for other performance measures. The definition of the expectation is

Unfortunately, we cannot explicitly solve this sum, but it can be calculated numerically.

A.23.3 Optimal Baselines

Although no explicit formula can be given for the expectation, we are able to calculate the extreme values of the expectation and the corresponding optimizers.

Minimal Baseline

Firstly, we show that constitutes a minimum and that there are no outside this interval also yielding this minimum. To this end,

because . This is the lowest possible value, since is a non-negative performance measure, and hence, for any . Now, let , then there exists a such that . Consequently, and this means the interval contains the only values that constitute the minimum. In summary,

Since is the discretization of it corresponds to 0. More precisely:

Maximal Baseline

Secondly, to determine the maximum of and the corresponding parameter , we determine an upper bound for the expectation, show that this value is attained for a specific interval and that there is no outside this interval also yielding this value. To do this, assume that . This makes sense, because implies and such a would yield the minimum . Now,

Next, let , then

because . Hence, the upper bound is attained for , and thus, is a maximizer.

Now, specifically for , we show that the interval of maximizers is actually . Thus, let , then and

which is exactly the upper bound for .

Next, to show that the maximizers are only in for , assume there is a that also yields the maximum. Hence, there is a with such that . This means

Hence, there is a strict inequality and this means is not a maximizer of the expectation. Consequently, the maximizers are only in the interval for . In summary,

Since is the discretization of , we obtain:

Declarations

-

•

Funding: No funding was received for conducting this study.

-

•

Conflicts of interest/Competing interests: Not applicable.

-

•

Availability of data and material: All data used in this research is cited in the appropriate sections.

-

•

Code availability: The Dutch Draw code can be found at https://github.com/joris-pries/DutchDraw.

-

•

Authors’ contributions (Contributor Roles Taxonomy (CRediT)):

-

–

Etienne van de Bijl: Conceptualization, Methodology, Software, Validation, Formal analysis, Investigation, Data Curation, Writing - Original Draft, Writing - Review & Editing, Visualization, Project administration;

-

–

Jan Klein: Conceptualization, Methodology, Software, Validation, Formal analysis, Investigation, Data Curation, Writing - Original Draft, Writing - Review & Editing, Visualization, Project administration;

-

–

Joris Pries: Conceptualization, Methodology, Software, Validation, Formal analysis, Investigation, Data Curation, Writing - Original Draft, Writing - Review & Editing, Visualization, Project administration;

-

–

Sandjai Bhulai: Conceptualization, Validation, Writing - Review & Editing, Supervision;

-

–

Mark Hoogendoorn: Conceptualization, Validation, Writing - Review & Editing, Supervision;

-

–

Rob van der Mei: Conceptualization, Validation, Writing - Review & Editing, Supervision.

-

–

References

- Araújo et al. (2017) Araújo R. d. A., Oliveira A. L., Meira S. (2017) A morphological neural network for binary classification problems. Engineering Applications of Artificial Intelligence 65:12–28, DOI https://doi.org/10.1016/j.engappai.2017.07.014

- Balayla (2020) Balayla J. (2020) Prevalence threshold (e) and the geometry of screening curves. PLoS ONE 15(10):e0240215, DOI https://doi.org/10.1371/journal.pone.0240215

- Canbek et al. (2017) Canbek G., Sagiroglu S., Temizel T. T., Baykal N. (2017) Binary classification performance measures/metrics: A comprehensive visualized roadmap to gain new insights. In: 2017 International Conference on Computer Science and Engineering (UBMK), IEEE, DOI https://doi.org/10.1109/ubmk.2017.8093539

- Candanedo and Feldheim (2016) Candanedo L. M., Feldheim V. (2016) Accurate occupancy detection of an office room from light, temperature, humidity and CO 2 measurements using statistical learning models. Energy and Buildings 112:28–39, DOI https://doi.org/10.1016/j.enbuild.2015.11.071

- Chinchor (1992) Chinchor N. (1992) Muc-4 evaluation metrics. In: Proceedings of the 4th Conference on Message Understanding, Association for Computational Linguistics, USA, MUC4 ’92, p. 22–29, DOI https://doi.org/10.3115/1072064.1072067

- Couronné et al. (2018) Couronné R., Probst P., Boulesteix A.-L. (2018) Random forest versus logistic regression: a large-scale benchmark experiment. BMC Bioinformatics 19(1), DOI https://doi.org/10.1186/s12859-018-2264-5

- Dua and Graff (2021) Dua D., Graff C. (2021) UCI machine learning repository. URL http://archive.ics.uci.edu/ml

- Fowlkes and Mallows (1983) Fowlkes E. B., Mallows C. L. (1983) A method for comparing two hierarchical clusterings. Journal of the American Statistical Association 78(383):553–569, DOI https://doi.org/10.1080/01621459.1983.10478008

- Koyejo et al. (2014) Koyejo O., Natarajan N., Ravikumar P., Dhillon I. S. (2014) Consistent binary classification with generalized performance metrics. In: Proceedings of the 27th International Conference on Neural Information Processing Systems - Volume 2, MIT Press, Cambridge, MA, USA, NIPS’14, p. 2744–2752

- Kubat et al. (1998) Kubat M., Holte R. C., Matwin S. (1998) Machine learning for the detection of oil spills in satellite radar images. Machine Learning 30(2/3):195–215, DOI https://doi.org/10.1023/a:1007452223027

- Kvålseth (1989) Kvålseth T. O. (1989) Note on cohen’s kappa. Psychological Reports 65(1):223–226, DOI https://doi.org/10.2466/pr0.1989.65.1.223

- Lipton et al. (2014) Lipton Z. C., Elkan C., Naryanaswamy B. (2014) Optimal thresholding of classifiers to maximize f1 measure. In: Calders T., Esposito F., Hüllermeier E., Meo R. (eds) Machine Learning and Knowledge Discovery in Databases, Springer Berlin Heidelberg, Berlin, Heidelberg, pp. 225–239

- Matthews (1975) Matthews B. (1975) Comparison of the predicted and observed secondary structure of t4 phage lysozyme. Biochimica et Biophysica Acta (BBA) - Protein Structure 405(2):442–451, DOI https://doi.org/10.1016/0005-2795(75)90109-9

- Min and Jeong (2009) Min J. H., Jeong C. (2009) A binary classification method for bankruptcy prediction. Expert Systems with Applications 36(3):5256–5263, DOI https://doi.org/10.1016/j.eswa.2008.06.073

- Moro et al. (2014) Moro S., Cortez P., Rita P. (2014) A data-driven approach to predict the success of bank telemarketing. Decision Support Systems 62:22–31, DOI https://doi.org/10.1016/j.dss.2014.03.001

- Muhammad and Melhem (2014) Muhammad G., Melhem M. (2014) Pathological voice detection and binary classification using MPEG-7 audio features. Biomedical Signal Processing and Control 11:1–9, DOI https://doi.org/10.1016/j.bspc.2014.02.001

- Palmer and Allen (1949) Palmer W., Allen R. (1949) Note on the accuracy of forecasts concerning the rain problem. US Weather Bureau manuscript

- Pedregosa et al. (2011) Pedregosa F., Varoquaux G., Gramfort A., Michel V., Thirion B., Grisel O., Blondel M., Prettenhofer P., Weiss R., Dubourg V., Vanderplas J., Passos A., Cournapeau D., Brucher M., Perrot M., Duchesnay E. (2011) Scikit-learn: Machine learning in Python. Journal of Machine Learning Research 12:2825–2830

- Schaefer (1990) Schaefer J. T. (1990) The critical success index as an indicator of warning skill. Weather and Forecasting 5(4):570–575, DOI https://doi.org/10.1175/1520-0434(1990)005¡0570:tcsiaa¿2.0.co;2

- Sergioli et al. (2019) Sergioli G., Giuntini R., Freytes H. (2019) A new quantum approach to binary classification. PLoS ONE 14(5):e0216224, DOI https://doi.org/10.1371/journal.pone.0216224

- Shahraki et al. (2017) Shahraki H. R., Pourahmad S., Zare N. (2017) K important neighbors: A novel approach to binary classification in high dimensional data. BioMed Research International 2017:1–9, DOI https://doi.org/10.1155/2017/7560807

- Sundarkumar and Ravi (2013) Sundarkumar G. G., Ravi V. (2013) Malware detection by text and data mining. In: 2013 IEEE International Conference on Computational Intelligence and Computing Research, IEEE, pp. 1–6, DOI https://doi.org/10.1109/iccic.2013.6724229

- Tsanas et al. (2014) Tsanas A., Little M. A., Fox C., Ramig L. O. (2014) Objective automatic assessment of rehabilitative speech treatment in parkinson’s disease. IEEE Transactions on Neural Systems and Rehabilitation Engineering 22(1):181–190, DOI https://doi.org/10.1109/tnsre.2013.2293575

- Wang and Manning (2012) Wang S., Manning C. (2012) Baselines and bigrams: Simple, good sentiment and topic classification. In: Proceedings of the 50th Annual Meeting of the Association for Computational Linguistics (Volume 2: Short Papers), Association for Computational Linguistics, Jeju Island, Korea, pp. 90–94, URL https://www.aclweb.org/anthology/P12-2018

- Wirth and Hipp (2000) Wirth R., Hipp J. (2000) Crisp-dm: Towards a standard process model for data mining. Proceedings of the 4th International Conference on the Practical Applications of Knowledge Discovery and Data Mining URL http://cs.unibo.it/~danilo.montesi/CBD/Beatriz/10.1.1.198.5133.pdf

- Youden (1950) Youden W. J. (1950) Index for rating diagnostic tests. Cancer 3(1):32–35, DOI https://doi.org/10.1002/1097-0142(1950)3:1¡32::aid-cncr2820030106¿3.0.co;2-3

- Yule (1912) Yule G. U. (1912) On the methods of measuring association between two attributes. Journal of the Royal Statistical Society 75(6):579, DOI https://doi.org/10.2307/2340126