Tests of Linear Hypotheses using Indirect Information

Tests of Linear Hypotheses using Indirect Information

Abstract

In multigroup data settings with small within-group sample sizes, standard -tests of group-specific linear hypotheses can have low power, particularly if the within-group sample sizes are not large relative to the number of explanatory variables. To remedy this situation, in this article we derive alternative test statistics based on information-sharing across groups. Each group-specific test has potentially much larger power than the standard -test, while still exactly maintaining a target type I error rate if the hypothesis for the group is true. The proposed test for a given group uses a statistic that has optimal marginal power under a prior distribution derived from the data of the other groups. This statistic approaches the usual -statistic as the prior distribution becomes more diffuse, but approaches a limiting “cone” test statistic as the prior distribution becomes extremely concentrated. We compare the power and -values of the cone test to that of the -test in some high-dimensional asymptotic scenarios. An analysis of educational outcome data is provided, demonstrating empirically that the proposed test is more powerful than the -test.

Keywords: empirical Bayes, -test, frequentist testing, hierarchical model, invariant test, multilevel data, small area estimation.

1 Introduction

Multigroup data analysis often occurs through the lens of separate but related linear regression models for each of several groups. For example, letting be a real-valued outcome and be a vector of features for the th subject in group , the relationship between and is often explored via the assumption that where the ’s are standard normal random variables, independent within and across groups. Letting be the vector of outcomes in group , and be the matrix of explanatory variables, this model can be expressed as

| (1) |

independently across groups .

Estimators of can be broadly categorized as being either “direct” or “indirect”. A direct estimator of is one that makes use of data only from group , such as the ordinary least squares (OLS) estimator . While has minimum variance among unbiased estimators, if is small then it may be preferable to reduce variance further by introducing bias in the form of “indirect” information from the other groups. Such estimators are often derived by imagining a normal model for across-group variation,

| (2) |

This across-group model is sometimes referred to as a “linking model” in the small area estimation literature, as it “links” the group-specific parameters together through the parameters . For given values of , the mean squared estimation error for each , on average with respect to (2), is minimized by the conditional expectation . This estimator can be interpreted as a Bayes estimator when (2) is thought of as a prior distribution [13] and is sometimes referred to as the “best linear unbiased predictor” (BLUP) when (2) is thought of as a sampling model for the groups [10], despite the fact that is biased as an estimator of (the “U” in “BLUP” refers to average bias with respect to (2) - essentially the across-group average bias of ). In practice, values of are estimated from and then plugged into the equation for each , yielding a so-called empirical Bayes estimator that is an “indirect estimator” in the sense that it combines direct information from group with indirect information from other groups, via the estimates of . While the empirical Bayes estimator for a given group has potentially higher mean squared error than the corresponding OLS estimator, the across-group average mean squared error of the empirical Bayes estimators is typically lower than that of the OLS estimators, even if the linking model (2) is incorrect or only a conceptual device - for example if the groups are not randomly selected.

Analogously, we may consider direct and indirect methods for hypothesis testing. The most widely used frequentist level- direct test of a linear hypothesis about is the standard -test, whose test statistic is a function of data only from group . In contrast, a frequentist level- indirect test is one where the test statistic for group is allowed to depend on the data from the other groups. In particular, data from groups other than might suggest that the vector lies in a particular direction. We can use this indirect information to select a level- test of that has more power than the -test in this particular direction, at a cost of having less power in other directions. As long as the data are independent across-groups, such a procedure will maintain a type I error rate of if the hypothesis is true, while having having increased power as compared to the -test if the hypothesis is false and the indirect information from the other groups is reasonably accurate.

In comparison to methods for indirect estimation, methods for indirect hypothesis testing are relatively undeveloped. Notable work in this area by O’Gorman [14, 15] examines adaptive procedures for testing subsets of regression coefficients in a linear model. When the errors are non-normal, such procedures have higher power than the -test for a variety of error distributions. Recently, Hoff [12] proposed an indirect analogue to the standard -test and corresponding -value for a univariate parameter based on a normally distributed estimator and indirect data from groups other than group . The indirect test of has a rejection region that is asymmetric around zero and is chosen to maximize expected power with respect to a “prior distribution” that is derived from indirect data that is independent of . Such a test is “frequentist”, as it maintains an exact level- type I error rate, but is also Bayesian in that it minimizes a Bayes risk (one minus the prior expected power) and so it is referred to as being “frequentist and Bayesian”, or FAB. Inversions of such tests were used by Yu and Hoff [20] to construct indirect confidence intervals for means in multiple normal populations. Their confidence intervals are essentially a multigroup extension of the interval proposed by Pratt [16] who obtained the confidence interval for the mean of a normal population that has minimum prior expected width among those having frequentist coverage. These Bayes-optimal frequentist procedures can be derived from various likelihood ratios, and so in this sense, they are related to methods that use Bayes factors as statistics in frequentist hypothesis tests [5, 8]. Such an approach has been applied to testing hypotheses about multinomial probabilities [7] and for evaluating nonparametric goodness of fit [1].

In this article we develop FAB alternatives to the -test for evaluating group-specific linear hypotheses in multigroup regression settings. Essentially, the proposed FAB test for is a level- test that has maximum expected power with respect to the “prior” distribution , where are estimated from models (1), (2) and data from groups other than . In the next section, we derive the form of the optimal FAB statistic and obtain a numerical approximation to facilitate its calculation. A theoretical power comparison of a simplified version of the FAB test, which we call the cone test, and the -test appears in Section 3. It is shown that the -statistic is a special case of the FAB statistic. It is also shown that the ratio of the -test -value to the cone test -value may range from zero to infinity. Asymptotic power comparisons between the -test and the cone test are also provided, where it is shown that the cone test can have higher power than the -test in certain high-dimensional scenarios. In Section 4 we describe in greater detail how the FAB statistic can be used in multigroup settings, and review some methods for obtaining estimates of the linking model parameters. A data analysis example considering educational test scores from multiple schools appears in Section 5. The FAB tests that share information across schools lead to a substantially greater number of null hypotheses being rejected. A discussion follows in Section 6. All of the proofs of theoretical results presented in this article can be found in the Appendix.

2 A FAB test for linear hypotheses

Consider testing a linear hypothesis for the parameter based on an observation of from the linear model , where is a known matrix of predictors and and are unknown. For the moment it is assumed that has full-rank. Recall that linear hypotheses of the form may be expressed as for a transformed linear model with mean (Seber & Lee, 2003) so without loss of generality we consider the null hypothesis . Note that the null and alternative models are invariant under data rescalings of the form for scalars . For this reason, we restrict attention to tests based on statistics that are invariant with respect to the group of rescalings of . Any such statistic must be a function of a maximal invariant statistic such as the unit vector . A test statistic based on has the advantage that its null distribution does not depend on any unknown parameters, as is uniformly distributed on the sphere if .

One scale invariant statistic is the usual -statistic, where is the total sum of squares and is the residual sum of squares, with being the OLS estimator. To see that this depends on only through , let be the projection matrix onto the space spanned by the columns of . Then we can write

Note that If then and is constant in , and so in this case any test based on (such as the -test) has power equal to its level. Even if , since the distribution of the -statistic depends on only through , its power is constant on level-sets of . In this sense the -test is “looking” in all directions equally for evidence against the null hypothesis.

If prior information about the direction of is available, it may be preferable to use a test that has more power in this direction, at the cost of having lower power in the opposite direction. Specifically, suppose prior information about is available in the form of a prior density . Letting be the density of implied by the normal model (1). The prior expected power of a test function is given by

where is the marginal density density of induced by , with respect to the uniform measure on . The Bayes-optimal level- test is the test that maximizes among all level- tests. Since the null distribution of is uniform on , by the Neyman-Pearson lemma the optimal test is given by

where is chosen so that has a type I error rate equal to .

Primarily for computational reasons we consider the case that corresponds to a normal distribution for and a point-mass distribution on for . The marginal distribution of under this prior is , and the corresponding distribution for is the angular Gaussian distribution with and . The density of with respect to the uniform probability distribution on the sphere is derived in Pukkila & Rao (1988) and is given by where , , and , approximation and computation of which is described below. Therefore, the Bayes-optimal test of based on rejects the hypothesis when is large, or equivalently, for large values of the FAB test statistic

| (3) |

The function can be computed recursively as

where is the standard normal CDF [17]. While the recursion can be performed quite quickly, it can be numerically unstable if is negative and is large. Alternatively, for large we have the following approximation:

This is based on a Taylor series expansion and then applying Rocktaeschel’s [18] approximation to the gamma function. Based on this approximation, an approximately optimal test statistic is

| (4) |

The null distributions of and may be easily obtained via Monte Carlo simulation, because under the null hypothesis , the distribution of is uniform on and so it is free of any unknown parameters. Furthermore, an approximation to the -value corresponding to any test statistic based on may be obtained as follows:

-

1.

Simulate ;

-

2.

Compute for ;

-

3.

Compute

This Monte-Carlo approximation to the actual -value can be made arbitrarily accurate by increasing the Monte Carlo sample size .

We remind the reader that the power of the test statistics and depend on , the normality of and the prior distribution , but the frequentist validity of the tests depend only on the distribution of being uniform under the null hypothesis. This means that the tests described above are also valid for testing in any linear regression model where the distribution of is spherically symmetric. This includes non-Gaussian heavy-tailed error distributions, such as the and Cauchy distributions. If spherical symmetry under the null distribution is suspect, an alternative technique would be to obtain the null distribution of via randomization. Such a randomization test may be obtained by replacing in step 1 above with independent permutations of the elements of the observed data vector .

Another desirable feature of the FAB test is that, unlike the -test, when the FAB test has non-trivial power against certain alternative hypotheses, meaning that the power of the test is strictly greater than the level of the test. In contrast, the -test has power equal to the level of the test when . If the null hypothesis is false and the FAB prior distribution is concentrated around the true parameter values, the FAB test will have non-trivial power. This is especially useful in settings where the sample size is small or when there are a large number of predictor variables. Conceptually, when the FAB test is comparable to ridge regression, where a prior distribution is used to add additional structure to an otherwise degenerate inference problem. Regardless of the rank of , both the and FAB tests maintain the correct level. It should be noted that if is not full-rank, there does not exist an unbiased test of the hypothesis due to the lack of identifiability of the regression model. In the next section we provide some additional insight on the performance of the FAB test relative to the -test as a function of the values of and .

3 Theoretical power comparisons

In this section we first examine the FAB test statistic under the prior distribution . In the extreme cases where either or the FAB test is equivalent to the -test. In another extreme case where , the FAB test is equivalent to a test which we call the cone test. When both and are non-zero the FAB test can be seen as an interpolation between the simpler and cone tests. As such, in the remainder of this section we compare the asymptotic performance of the and cone tests. In particular, it will be shown that the cone test, if correctly specified, can significantly outperform the -test when the dimension of the regression subspace is large. This suggests that the FAB test is especially useful in settings with a large number of predictor variables, in which the -test has low power.

3.1 The FAB, F and cone tests

Suppose that the prior distribution is used in the FAB test statistic (3). Under this prior distribution, the marginal distribution of is , where is the orthogonal projection matrix onto . This marginal distribution has the property that and the distribution of is rotationally invariant for all orthogonal transformations that fix the subspace . This class of prior distributions with covariance matrices of the form is useful in situations where it is not feasible to model the entire prior covariance matrix of . Moreover, intuition for the behaviour of the FAB test statistic can be obtained by using this class of prior distributions. We have that where . Expanding the expression (3), the FAB test statistic in this case takes the form

| (5) |

The last term in (5) is simply an expansion of the term in (3). This expression for the FAB test statistic shows that is a function of and . For a fixed value of , is a strictly increasing function of , while for a fixed, positive value of , is a strictly decreasing function of . Consequently, the FAB test statistic is large when is simultaneously close to the vector and close to the subspace . From (5) it is immediate that when , is a strictly decreasing function of and so it results in a test that is equivalent to the -test. Similarly, if the prior distribution becomes diffuse and the FAB test statistic converges pointwise to a limiting test statistic that is a strictly decreasing function of . It is shown in the Appendix that the FAB test is asymptotically equivalent to the -test as .

Another extreme case occurs when so that and is a strictly increasing function of . We call the resulting test with the cone test with test direction . When the level of the cone test is less than , the test has the rejection region

| (6) |

where the number is chosen to make this a level- test. We call the test with rejection region a cone test because the set forms a cone in that is rotationally symmetric about the the ray extending in the direction from the origin. By construction, the cone test is identical to the likelihood ratio test of against the simple alternative hypothesis .

3.2 Power and -value comparisons of the and cone tests

The feature of the test statistic (5) that differentiates the FAB test from the -test is the dependence of the FAB test statistic on . The quantity is the cosine of the angle between the scaled data and the direction of the cone test. As the prior distribution becomes more concentrated about the FAB test can be approximated by the cone test. Below we compare the asymptotic properties of the -test and the cone test with rejection region given by (6).

Our first lemma compares the -value functions of the -test and cone test. In the univariate setting, it is shown in Hoff [12] that for a given observation , the -value function of the -test (or equivalently the -value function of the two-sided -test) at can be at most twice as large as the -value function of the FAB test . However, the ratio can be arbitrarily close to , meaning that it is possible for the FAB -value to be significantly larger than the -test -value if the true points in a direction opposite to that of . The following lemma shows that in a multivariate setting the -value ratio instead of being bounded above by two, is also unbounded. In particular, for observations where , the -value ratio of such an observation can be expressed as a ratio of probabilities of Dirichlet random variables.

Lemma 1.

Lemma 1 Let be the -value function for the cone test with rejection region (6) for testing the null hypothesis where with . If the observation is of the form with , then

where and . In particular, for such a the -value ratio can be bounded below by

which tends to as if .

From this lemma it is seen that for any observation with , the -value of the -test is larger than the -value of the cone test. Moreover, for such an observation, the -value ratio converges to infinity as when . Therefore, unlike in the univariate setting, the -value of the cone test can be orders of magnitude smaller than the corresponding -test -value when is close to . In practice, it is not realistic to observe a with . However, since the -value ratio is continuous at as long as , the conclusion of Lemma 1 can be extended to observations with . For instance, if then there is a neighbourhood of where this inequality holds for within this neighbourhood.

As the cone test only depends on the regression subspace through , the performance of the cone test is independent of the dimension of the regression subspace. This contrasts with the power of the -test which deteriorates as grows. Formalizing this, consider the sequence of models

| (7) |

Define to be the power of a level- test ( will be the power of either the -test or the cone test) of the null hypothesis under the alternative hypothesis that has . It is of interest to assess the impact of and on the power functions of the and cone tests. Table 1 summarizes the limiting power of both the -test and the cone test under various asymptotic regimes, when the test direction of cone test is correctly specified. The cone test direction is correctly specified when the null hypothesis does not hold and . These asymptotic regimes differ based on whether is taken to be fixed as increases or as increases. Summarizing Table 1, the correctly specified cone test will have higher limiting power than the -test in settings with a large number of predictor variables.

| -test | Cone test | |

|---|---|---|

| , | ||

| , | ||

| , | ||

| , |

A more complete description of the asymptotics of the -test is provided in the following lemma. This lemma shows that under the regime where as , the value of needs to diverge from at a rate of if the power of the -test is to be greater than its level.

Lemma 2.

Lemma 2 Let denote the power of the level- -test in the sequence of models (7). If and are constants then . If then and if then the -test has limiting power .

Similarly, the results in Table 1 regarding the cone test are described in the following lemma, where these results are extended to cone tests that are not correctly specified.

Lemma 3.

Lemma 3 Let denote the power of the level- cone test with rejection region in the sequence of models (7), where is an appropriate level- quantile, and . If is constant and the mean direction of the cone test is nearly correctly specified so that then where the power function does not depend on . If and if for some then and if then .

This lemma implies that the performance of a mispecified cone test depends on the dimension , where the test direction must converge to the direction of the mean vector under the alternative at a rate of if the test is to have limiting power that is greater than . If is the angle between and then this condition is equivalent to . Essentially, if is constant, the power of the cone test diminishes as increases but does not depend on , while the power of the -test diminishes as increases but it is not significantly altered by .

In both lemmas 2 and 3, it is not unrealistic to assume that when the null hypotheses do not hold. One common such scenario is where independent replications are observed, each with design matrix so that, and are constant while . In this case and the and correctly specified cone tests will have limiting power by the above lemmas. A related case is when , for all and the entries of are independent standard normal random variables. Then and . Therefore, the rate appearing in lemmas 2 and 3 has the alternative hypothesis diverging away from the null hypothesis at a rate that is slower than the -rate that occurs in the above replication scenarios.

It is not realistic to assume that the cone test direction is correctly specified in practice. In the multigroup setting to be considered in the following section, even as the amount of auxiliary information from other groups increases, it will generally not be true that the test direction of the cone test can be estimated consistently from the auxiliary information. Therefore we do not recommend using the cone test on its own. Rather, we recommend using the FAB test statistic (3) or (4), which provides a principled compromise between the and cone tests. If the prior information about is precise and accurate, the resulting FAB test will look similar to the cone test. If instead only weak prior information is available, the FAB test will behave similarly to the -test.

4 FAB testing in multigroup settings

4.1 The multigroup FAB Test

Thus far, the prior distribution used in the FAB test was assumed to known at the outset. In this section we demonstrate how to choose the prior distribution in a data dependent manner in a multigroup setting. Specifically, we consider the model (1) where , and . We construct different FAB tests for the each of the separate hypotheses in this model. To ease notation, we focus on testing the hypothesis , where any of the other hypotheses can be tested in a similar manner by relabelling the groups.

Given the multigroup regression model (1), the prior distribution in (2), which assumes that the regression coefficients are drawn from a common multivariate normal distribution, is used as a device to share information across the different groups in our multigroup FAB test. Such a prior distribution will also be referred to as a linking model. If the parameters and in the linking model (2) were known, the FAB test introduced in Section 2 could be directly applied. As this is generally not the case, the data from groups through will be used to obtain estimates of and . A level- multigroup FAB procedure can be constructed as follows:

-

1.

Obtain estimates and of the linking model parameters using observations from every group but the first group.

-

2.

Plug-in the values of and into the FAB test statistic in (3), where and . Denote the observed FAB test statistic by .

-

3.

Reject the null hypothesis if where is the quantile of where . This quantile can be found by Monte Carlo simulation.

This procedure results in a level- test since the independence of and implies that when ,

We emphasize that this FAB test will be a level- test, regardless of the validity of the linking model. All that is required for this test to have level- is that must be independent of and it must be uniformly distributed over the unit sphere.

Another desirable feature of the multigroup FAB test is that it approximately has the Bayes-optimal power if the linking model holds and if the the parameter estimates are close to . This follows by construction, since the likelihood ratio test that the multigroup FAB test approximates is the most powerful test marginally over the linking model. Conversely, mispecification of the linking model or poor estimates of can result in a multigroup FAB test with sub-optimal power.

4.2 Constructing a Data Dependent Prior Distribution

In this section we review some standard methods for obtaining estimates of and from the random effects model

| (8) |

For simplicity, assume that , where we denote the common value by . The marginal distribution of is with . Under this marginal model for the ’s, the maximum likelihood estimator of is

| (9) |

where is the maximum likelihood estimator of . The maximum likelihood estimators of and have to be found numerically using, for example, the R package lme4 [2]. As a simpler alternative, moment based estimates of and can be found which then can be substituted into the values of appearing in (9). If is the projection matrix onto , the residual maximum likelihood estimate (REML) of is given by

| (10) |

A simple moment based estimate of is

| (11) |

As depends on which in turn depends on , an iterative procedure is needed to find suitable estimates. Such an iterative procedure can be initialized by taking in (9).

In summary, there is flexibility as to what estimates of and are used in the multigroup FAB procedure, as long as such estimates are independent of . If the values of the ’s and are large, the estimates in (10) and (11) may be easier to compute than the maximum likelihood estimates. The restriction that can also be lifted at the expense of additional computational effort. In this case either the MLE or direct analogues of the estimators in (10) and (11) could be used. Lifting this restriction may result in better estimates of the linking model parameters and if the error variances across groups are different. However, the FAB test remains a level- test regardless of the particular linking model parameter estimates chosen.

4.3 Modelling the Error Variances

As discussed in Section 3, the FAB test can approximately be viewed as a combination of the cone and -tests. Roughly, if is given the prior distribution , the prior mean determines the test direction of the cone test while the relative magnitudes of and determine the how similar the FAB test is to either the -test or the cone test. Recall that was the location of the point mass prior distribution placed on . In this section we pursue a more sophisticated FAB test that adds to (8) the following linking model for the error variances :

| (12) |

Two additional steps are needed to incorporate this linking model into the multigroup FAB test previously discussed. First, the FAB test statistic (3) is altered to account for the new linking model (12). Second, the observations in groups through are used to obtain estimates of and to be used in this modified FAB test statistic.

As before, by the Neyman-Pearson lemma, the FAB test statistic is the likelihood ratio test of the densities of under the new linking model and under the null hypothesis. Under the null hypothesis, remains uniformly distributed over the sphere, while under the linking model we have with , and . Therefore, the FAB test statistic is

| (13) |

where and are defined as in Section 2 and is the density of an distribution. This statistic can be found via Monte Carlo approximation or numerical integration over the inverse gamma distribution.

Parameter estimates of and based on the data in groups through can be substituted into (13). One strategy for obtaining such estimates is to estimate and via equations (9) and (11) as described in the previous section. Estimates of and can be obtained by noting that . To ease notation, define and . For , the mean and variance of , marginally over the distribution of , are given by

If and , then method of moments estimators for and are found by solving the equations

yielding and . These estimates are straightforward to compute. They tend to be more accurate when the are large as then and thus . Other estimators for and can also be used, however, they generally must be solved for numerically.

The FAB test can have low power relative to the -test if the estimate of is poor. If this low power is a concern, a more conservative FAB test can be constructed by choosing estimates of and so that is large.

4.4 Testing Other Linear Hypotheses

In this section we describe how to test linear hypotheses in the multigroup regression model that are more general than the hypothesis . For instance, in (1) it may be of interest to test if a subset of components of are , or to test the hypothesis that the regression coefficients of two different groups are equal.

Define for and let , with . A FAB procedure for testing the linear hypothesis on the regression coefficients of the first groups in the model (1) is described below. We make the extra assumption in (1) that the error variances are all equal to . Define and . The multigroup regression model (1) under the homoskedasticity assumption can be rewritten as

| (14) |

Let and take to be a full-rank orthonormal matrix whose rows span the subspace . Also take to be a solution to the equation where we define . By the definition of , the value of is independent of the particular solution chosen. Moreover, if the hypothesis is holds, this implies that the hypothesis also holds. When is full-rank, or more generally when is full-rank, these hypotheses are equivalent, meaning that is true if and only if is true.

As , the hypothesis is identical to the hypothesis considered in Section 2, namely testing that the mean of the isotropic, multivariate normal random vector is . Applying the results from Section 2, if is given the prior distribution , the FAB test of is exactly the likelihood ratio test with test statistic where and and are the marginal mean and variance of . We note that the common variance assumption is crucial in this setting to ensure that the distribution of under the null hypothesis is pivotal.

A data dependent prior distribution over is obtained by finding estimates for and in the linking model (2). Such estimates are found exactly as in Section 4.2, using the observations that are not from the first groups. This procedure does not utilize any information from the portion of that lies in . If is a full-rank matrix with rows that span , then marginally under the prior distribution (2), . The vector therefore does provide some useful information about the covariance structure of . This information is most easily incorporated into a maximum likelihood approach for estimating and . However, in hypotheses where , such as the hypothesis that a subset of the components of are when a large number of groups are present, we recommend using the simpler prior parameter estimates based on the observations .

5 Example: Evaluating Standardized Test Scores

5.1 Overview of the ELS Data

In this section we demonstrate the efficacy of the multigroup FAB test on educational outcome data. The 2002 educational longitudinal study (ELS) dataset includes demographic information of 15362 students from a collection of 751 schools across the United States in an effort to inform educational policy. We identify schools with ethnic disparities in educational outcomes by testing for mean differences in test scores by ethnicity after accounting for other variables. As some schools had only a small number of students who were surveyed, sharing information between the schools can help to improve the sensitivity of within-school testing procedures. On average, 20 students were surveyed per school, however 34 of the schools had less than 10 students who were surveyed.

The response variable that we analyze is a (nationally) standardized composite math and reading score that is recorded for each student in the study. For each student we model the relationship between their test score and the following dependent variables: ethnicity, native language, sex, parental education and a composite index of the student’s socio-economic status. Ethnicity is aggregated into four broad categories: Asian, Black, Hispanic and White. A separate linear regression model with the aforementioned predictor variables is used for each school. Independently across schools , we take

| (15) |

where is the vector of test scores for the students in school , represents the regression coefficients for the ethnicity variables and represents the regression coefficients for the non-ethnicity variables in school . For every school , we test the hypotheses by projecting out the non-ethnicity variables in (15), a process which was described Section 4.4.

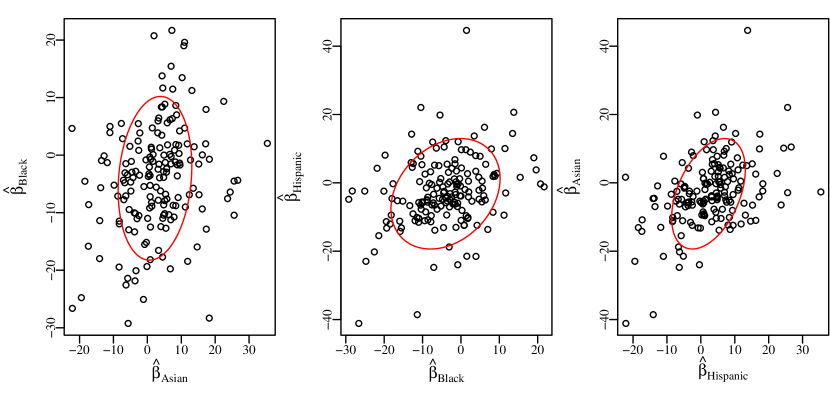

Figure 5 in the Appendix illustrates normal QQ-plots of the residuals in the projected models for 9 different schools. These plots suggest that the projected regression model is a reasonable model for the ELS data. Figure 1 shows the distribution of the least square estimates of the coefficients for schools with full-rank projected design matrices. From this figure, we conclude that it is not unrealistic to assume that the ’s follow the multivariate normal linking model in (2). The confidence ellipses for in Figure 1 are based on a method of moments estimate of .

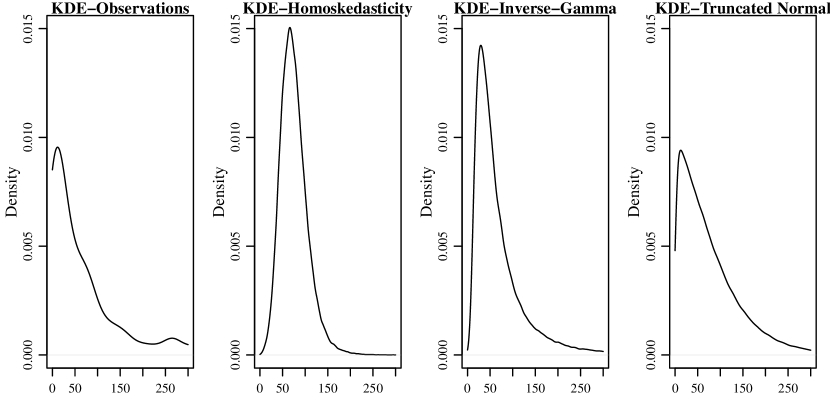

Lastly, we examine the empirical distribution of the scaled squared-residuals , to determine a suitable linking model for the error variances. A kernel density estimate of the marginal density of is shown in Figure 2. Under a linking model that assumes homoskedasticity, , and has a chi-squared marginal distribution scaled by the constant . The second plot in Figure 2 sets and displays a kernel density estimate of the marginal distribution of where this distribution is found by simulating . It is apparent that the kernel density estimate of this marginal distribution does not match the kernel density estimate of the observed marginal distribution. Two other possible linking models are the inverse-gamma linking model and the truncated normal linking model . Fitting both of these models, it is seen in Figure 2 that the marginal density of , under the truncated normal linking model with matches the observed marginal density more closely than the marginal density under the inverse-gamma linking model.

5.2 Methodology

We test the hypothesis in the model (15) by projecting out the non-ethnicity variables as described in Section 4.4. That is, if is a full-rank orthonormal matrix whose rows span , the problem of testing is reduced to testing this same hypothesis in the model . The FAB or -tests in the reduced model will have power greater than the level against some alternatives as long as , a condition which holds for 634 of the 751 schools. Out of these 634 schools, 169 of them have full-rank projected design matrices . In the FAB tests we construct, the multivariate normal linking model (2) is used to model . Parameter estimates of and are obtained using only the 169 schools that have the full-rank design matrices. The method of moments estimates of described in Section 4.2 are used as estimates of these linking model parameters. As there are a sufficiently large number of observations from which to obtain parameter estimates, other estimation procedures will produce similar estimates.

Two different linking model assumptions on the error variances are used, resulting in two different FAB testing procedures. The first is simply the homoskedastic linking model that uses the FAB test statistic (3), where the parameter is estimated by the mean squared error of the reduced model, pooled across schools. The second truncated normal linking model assumption assumes that . We refer to these tests as FAB-HS and FAB-TN respectively. Again, the pooled mean squared error is used to estimate in the truncated normal linking model. Denoting the marginal distribution of by , analogous to equation (13), the FAB test statistic for school is given by the equation

| (16) |

where and and are defined as in Section 2 based on the data from school . The integral in (16) is approximated via Monte Carlo by drawing observations of from the truncated normal distribution.

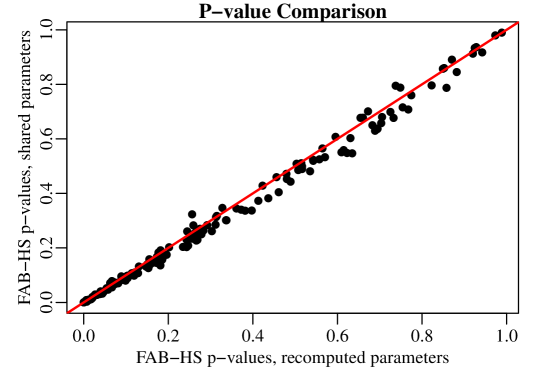

To obtain the correct level when testing the hypothesis for school , theoretically, all of the estimates should be computed by leaving out the data from school . For instance, when testing the hypothesis for school , should be of the form . However, as these parameter estimates are not significantly altered by leaving out school , it is not necessary in practice to recompute these estimates for each school. Figure 6 in the Appendix displays the -values for the homoskedastic FAB test where the linking model parameter estimates are either recomputed when testing each hypothesis or the same parameter estimates are used for testing every hypothesis. It is seen that the -values are nearly identical in these two cases, showing that at least when a large number of groups are present, it is not necessary to recompute the linking model parameter estimates for each hypothesis under consideration.

5.3 Results

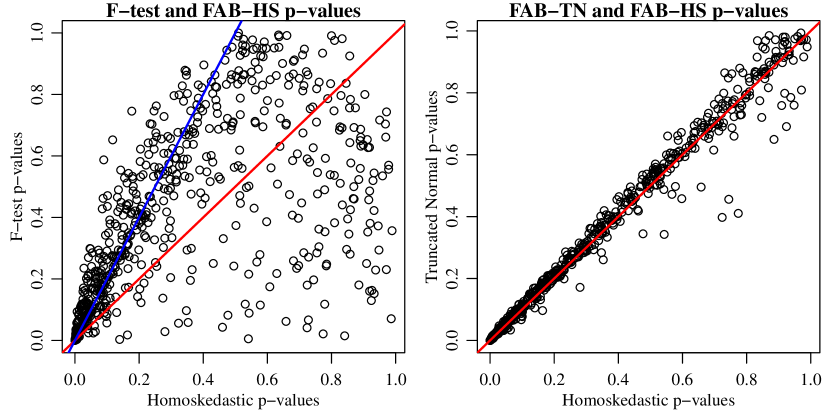

We compare the empirical performance of three tests: the -test, the homoskedastic FAB test and the truncated normal FAB test. In the second plot in Figure 3 it is shown that the -values for the homoskedastic and truncated normal FAB tests are nearly identical. This provides some evidence that the choice of the linking model over the ’s is not of critical importance. In the first plot, when the -values of the -test are small, the -values for the homoskedastic FAB test are typically less than the -test -values. These -values are concentrated near the blue line with slope when the -values of the FAB test are less than .

Table 2 quantifies the extent to which the power of the FAB tests is greater than the power of the -test. Across all of the 634 schools with non-zero projected design matrices, at a level of , the FAB test rejects nearly twice as many hypotheses as the -test. At a level of , the relative improvement is even greater, with the FAB tests rejecting approximately times as many hypotheses. The average number of hypotheses rejected is higher on average for the 169 schools that have full-rank projected design matrices than for schools that do not. If is not full-rank then the full vector is not identifiable in (15), rather only certain linear functions of are identifiable. Therefore, if a school does not have a full-rank projected design matrix, not as much prior information can be leveraged in the FAB test. Effectively, prior information can only be used to directly inform the identifiable “portion” of . For instance, if the first column of happened to be , the FAB test would not directly utilize the information from the other schools about the marginal distribution of the first component of .

| -test | FAB-HS | FAB-TN | |

|---|---|---|---|

| , All Schools | 0.103 | 0.188 | 0.186 |

| , All Schools | 0.019 | 0.059 | 0.054 |

| , Full-rank Schools | 0.118 | 0.237 | 0.219 |

| , Full-rank Schools | 0.030 | 0.095 | 0.083 |

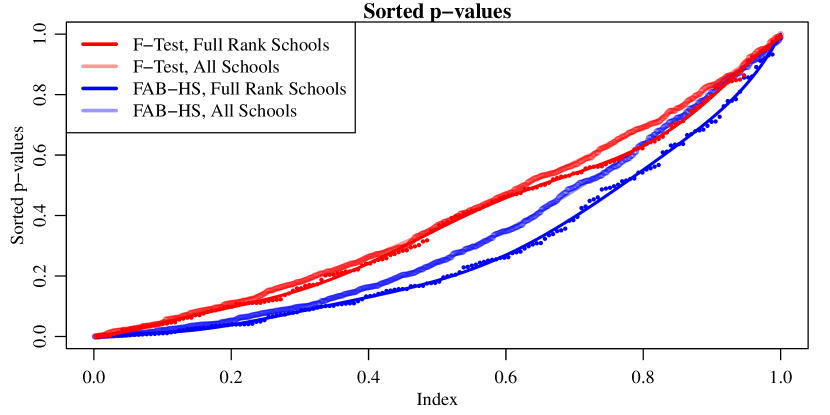

Lastly, we examine the performance of the FAB tests relative to the -test after controlling the false discovery rate (FDR). The Benjamini- Hochberg procedure controls the FDR at a level by sorting the observed -values and rejecting all hypotheses , where is the largest for which [3]. This procedure is valid for -values that are independent, as in the -test, or for -values that satisfy certain types of positive dependence [4]. As the -values obtained from the FAB test are constructed from estimates of the linking model parameters that are correlated, we expect the -values to be positively dependent and the Benjamini-Hochberg procedure to be approximately valid for the FAB tests. Table 3 in the Appendix compares the average number of hypotheses that are rejected for the -test and FAB-HS test, controlling the FDR at various levels by the Benjamini-Hochberg procedure. The plot of the sorted -values for the -test and the FAB-HS test in Figure 4 demonstrates that the empirical distribution of the FAB-HS -values is stochastically smaller than the empirical distribution of the -test -values. In conclusion, whether controlling for size or for the FDR, the FAB tests in this setting are seen to be more powerful than the -test.

6 Discussion

In multigroup data analyses, inferences about one group can often be made more precise by utilizing data from the other groups. In this article, we have shown how a FAB test for a linear hypothesis involving one group may be constructed with the aid of data from the other groups, via a linking model that describes relationships among group-specific parameters. If the data from different groups are informative about each other’s parameters, then such a test will have higher power than a direct test that does not make use of this information. Additionally, even if the linking model is incorrect or non-informative, the FAB test maintains exact type I error rate control.

The FAB test statistic we have proposed is a function of the scale-invariant statistic which has a distribution that does not depend on . Effectively, by only considering scale-invariant test statistics, the null hypothesis has been reduced to a simple null hypothesis. This reduction to test statistics that are pivotal under the null hypothesis can be applied more broadly to test a wide variety of hypotheses. An interesting future direction is to develop FAB tests for nonparametric hypotheses, by restricting the test statistic to be a function of a pivotal quantity. One such example is to test the hypothesis that two distributions are equal using test statistics based on empirical distributions.

In nonparametric settings it may also be necessary to to consider more sophisticated prior distributions than the multivariate normal prior used in this article. In fact, the FAB prior distribution can itself be nonparametrically estimated. The possible utility of doing so is suggested by the ELS example where kernel density estimates of the scaled, squared-residuals are shown in Figure 2. Rather than using the parametric truncated normal or inverse-gamma linking models, a kernel density estimate of the density of the variance parameter could instead be used. However, if the model under consideration is parametric, for computational reasons it is preferable to keep the linking model as simple as possible.

This article is focused entirely on testing the values of regression coefficients. In theory, the FAB test presented could be inverted to provide a confidence region for each vector of regression coefficients. Hoff and Yu [11] examine related confidence intervals for the elements of in a regression model for a single group using shrinkage prior distributions. In the multigroup setting, properties such as the connectedness or convexity of such a confidence region found by inverting the FAB test warrant further study.

Another aspect of the multigroup FAB test that warrants further study are the multiple testing properties of this test. The multigroup FAB test controls the type I error rate for each group and thus controls the per-comparison error rate, but it does not control the family-wise error rate [6]. Standard methods, such as the Bonferonni correction, can be used to control the family-wise error rate, although such methods may produce tests with low power. Similarly, it also is of interest to study methods for controlling the false discovery rate of the multigroup FAB test.

References

- [1] Aerts, M., Claeskens, G. & Hart, J. D. (2004). Bayesian-motivated tests of function fit and their asymptotic frequentist properties. The Annals of Statistics, 32, 2580–2615.

- [2] Bates, D., Machler M., Bolker, B., & Walker, S. (2015). Fitting Linear Mixed-Effects Models Using lme4. Journal of Statistical Software, 67, 1–48.

- [3] Benjamini, Y. & Hocherberg, Y. (1995). Controlling the false discovery rate: a practical and powerful approach to multiple testing. Journal of the Royal Statistical Society. Series B, 57, 289–300.

- [4] Benjamini, Y. & Yekutieli, D. (2001). The control of the false discovery rate in multiple testing under dependency. The Annals of Statistics, 29, 1165–1188.

- [5] Chacon, J. E., Montanero, J., Nogales, A. G. & Perez, P. (2007). On the Use of Bayes factor in Frequentist Testing of a Precise Hypothesis. Communications in Statistics. Theory and Methods. 36, 2251–2261.

- [6] Dudoit, S. & van der Laan, M. J. (2008). Multiple Testing Procedures with Applications to Genomics. Springer, New York.

- [7] Good, I. J. & Crook, J. F. (1974). The Bayes/Non-Bayes Compromise and the Multinomial Distribution. Journal of the American Statistical Association, 69, 711–720.

- [8] Good, I. J. (1992). The Bayes/Non-Bayes Compromise: A Brief Review. Journal of the American Statistical Association, 87, 597-606.

- [9] Hart, J. D. (2009). Frequentist-Bayes lack-of-fit tests based on Laplace approximations. Journal of Statistical Theory and Practice, 3, 681–704.

- [10] Henderson, C. R. (1974). Best linear unbiased estimation and prediction under a selection model. Biometrics, 423–447.

- [11] Hoff, P. D. & Yu, C. (2019). Exact adaptive confidence intervals for linear regression coefficients. Electronic Journal of Statistics, 13, 94-119.

- [12] Hoff, P. D. (2021). Smaller -values via Indirect Information. Journal of the American Statistical Association, 0, 1–16.

- [13] Lindley, D. V. & Smith, A. F. M. (1972). Bayes estimates for the linear model. Journal of the Royal Statistical Society. Series B, 24, 1–41.

- [14] O’Gorman, T. W. (2002). An adaptive test of significance for a subset of regression coefficients. Statistics in Medicine, 21, 3527–3542.

- [15] O’Gorman, T. W. (2006). An adaptive test for a subset of coefficients in a multivariate regression model. Biometrical Journal, 48, 849–859.

- [16] Pratt, J. W. (1963). Shorter confidence intervals for the mean of a normal distribution with known variance. The Annals of Mathematical Statistics, 34, 574–586.

- [17] Pukkila, T. M. & Rao, C. R. (1988). Pattern recognition based on scale invariant discriminant functions. Information Sciences, 46, 379–389.

- [18] Rocktaschel, O. R. (1922). Methods for Computing the Gamma Function for Complex Arguments. PhD Thesis.

- [19] Seber, G. A. F. & Lee, A. J. (2003). Linear Regression Analysis. Wiley, New Jersey.

- [20] Yu, C. & Hoff, P. D. (2018) Adaptive multigroup confidence intervals with constant coverage. Biometrika, 105, 319–335.

7 Appendix

7.1 Proofs

Lemma 1.

This is a theorem. Let be the -value function for the cone test with rejection region (6) for testing the null hypothesis where with . If the observation is of the form with , then

where and . In particular, for such a the -value ratio can be bounded below by

which tends to as if .

Proof.

Without loss of generality the regression subspace can be assumed to be equal to where is the ’th standard basis vector and can be taken to be . Thus and can be taken to be since both the and cone test statistics only depend on through the values of and . At the and cone test statistics are and respectively.

Under the null hypothesis and the vector has . The -test -value at therefore has the form

since . The conical test -value is

We bound this ratio of beta probabilities below by

∎

Lemma 2.

Consider the sequence of models where . Define to be the power of the level -test of the null hypothesis under the alternative hypothesis that has . If and are constants then . If then and if then the -test has limiting power .

Proof.

The statistic is

In the first regime where and this statistic converges in probability to a distribution under the null hypothesis and a distribution under the alternative hypothesis since the denominator converges in probability to and the numerator follows a chi-squared distribution. If then as needed.

Next, consider the case where . Under the alternative hypothesis the numerator of the -statistic has a distribution with the stochastic representation where . Define . As , and consequently, where is the standard normal quantile. Consequently,

If then , while if then and the claims follow. ∎

Lemma 3.

Consider the sequence of models where . Define to be the power of the level- cone test of the null hypothesis with rejection region where is an appropriate level- quantile, and under the alternative hypothesis. If is constant and the mean direction of the cone test is nearly correctly specified so that then where the power function does not depend on . If and if for some then and if then .

Proof.

Define and without loss of generality we assume that , where is the first standard basis vector. Under the alternative hypothesis the conical test statistic has the stochastic representation

where , and is the ’th component of . Thus

By the law of large numbers and thus where is a standard normal quantile. Then assuming that and is constant

Next assume that and so that

The result for immediately follows as well since . ∎

Lemma 4.

Under the prior distribution , the FAB test is asymptotically equivalent to the F-test as . That is, the probability that the F and FAB tests lead to the same conclusion under the null hypothesis or any alternative hypothesis tends to as .

Proof.

Let and be the rejection regions for the F and FAB tests respectively ). It suffices to show that has Lebesgue measure , where is the symmetric difference of sets.

As , if , then

| (17) |

where an appeal to the dominated convergence theorem is used to take the limit inside the integral in (5). Call the statistic on the right hand side of (17) . If then for any sequence since . If is the -quantile of then it is claimed that for any , . If this were not the case then there would exist a sequence with for all . However, this is not possible since and has a continuous distribution with positive density on the interior of its support (implying that its quantiles are unique).

We have shown above that if then for all with . As if and only if , all must satisfy . As this set has Lebesgue measure (assuming that ) this completes the proof.

∎

7.2 Tables and Figures

| FAB-HS, All | FA-HS, full-rank | -test, All | -test, full-rank | |

|---|---|---|---|---|

| 0.01 | 0.11 | 0.00 | 0.01 | |

| 0.09 | 0.24 | 0.00 | 0.02 | |

| 0.52 | 0.68 | 0.12 | 0.28 |