Your Policy Regularizer is Secretly an Adversary

Abstract

Policy regularization methods such as maximum entropy regularization are widely used in reinforcement learning to improve the robustness of a learned policy. In this paper, we unify and extend recent work showing that this robustness arises from hedging against worst-case perturbations of the reward function, which are chosen from a limited set by an implicit adversary. Using convex duality, we characterize the robust set of adversarial reward perturbations under kl- and -divergence regularization, which includes Shannon and Tsallis entropy regularization as special cases. Importantly, generalization guarantees can be given within this robust set. We provide detailed discussion of the worst-case reward perturbations, and present intuitive empirical examples to illustrate this robustness and its relationship with generalization. Finally, we discuss how our analysis complements previous results on adversarial reward robustness and path consistency optimality conditions.

1 Introduction

Regularization plays a crucial role in various settings across reinforcement learning (rl), such as trust-region methods (Peters et al., 2010; Schulman et al., 2015; 2017; Bas-Serrano et al., 2021), offline learning (Levine et al., 2020; Nachum et al., 2019a; b; Nachum & Dai, 2020), multi-task learning (Teh et al., 2017; Igl et al., 2020), and soft -learning or actor-critic methods (Fox et al., 2016; Nachum et al., 2017; Haarnoja et al., 2017; 2018; Grau-Moya et al., 2018). Various justifications have been given for policy regularization, such as improved optimization (Ahmed et al., 2019), connections with probabilistic inference (Levine, 2018; Kappen et al., 2012; Rawlik et al., 2013; Wang et al., 2021), and robustness to perturbations in the environmental rewards or dynamics (Derman et al., 2021; Eysenbach & Levine, 2021; Husain et al., 2021).

In this work, we use convex duality to analyze the reward robustness which naturally arises from policy regularization in rl. In particular, we interpret regularized reward maximization as a two-player game between the agent and an imagined adversary that modifies the reward function. For a policy regularized with a convex function and regularization strength , we investigate statements of the form

| (1) |

where indicates a modified reward function chosen from an appropriate robust set (see Fig. 1-2). Eq. 1 suggests that an agent may translate uncertainty in its estimate of the reward function into regularization of a learned policy, which is particularly relevant in applications such as inverse rl (Ng et al., 2000; Arora & Doshi, 2021) or learning from human preferences (Christiano et al., 2017).

This reward robustness further implies that regularized policies achieve a form of ‘zero-shot’ generalization to new environments where the reward is adversarially chosen. In particular, for any given and a modified reward within the corresponding robust set, we obtain the following performance guarantee

| (2) |

Eq. 2 states that the expected modified reward under , with as in Fig. 1, will be greater than the value of the regularized objective with the original, unmodified reward. It is in this particular sense that we make claims about robustness and zero-shot generalization throughout the paper.

Our analysis unifies recent work exploring similar interpretations (Ortega & Lee, 2014; Husain et al., 2021; Eysenbach & Levine, 2021; Derman et al., 2021) as summarized in Sec. 5 and Table 1. Our contributions include

-

•

A thorough analysis of the robustness associated with kl and -divergence policy regularization, which includes popular Shannon entropy regularization as a special case. Our derivations for the -divergence generalize the Tsallis entropy rl framework of Lee et al. (2019).

-

•

We derive the worst-case reward perturbations corresponding to any stochastic policy and a fixed regularization scheme (Prop. 2).

-

•

For the optimal regularized policy in a given environment, we show that the corresponding worst-case reward perturbations match the advantage function for any -divergence. We relate this finding to the path consistency optimality condition, which has been used to construct learning objectives in (Nachum et al., 2017; Chow et al., 2018), and a game-theoretic indifference condition, which occurs at a Nash equilibrium between the agent and adversary (Ortega & Lee, 2014).

-

•

We visualize the set of adversarially perturbed rewards against which a regularized policy is robust in Fig. 1-2, with details in Prop. 1. Our use of divergence instead of entropy regularization to analyze the robust set clarifies several unexpected conclusions from previous work. In particular, similar plots in Eysenbach & Levine (2021) suggest that MaxEnt rl is not robust to the reward function of the training environment, and that increased regularization strength may hurt robustness. Our analysis in Sec. 5.1 and App. F.4 establishes the expected, opposite results.

-

•

We perform experiments for a sequential grid-world task in Sec. 4 where, in contrast to previous work, we explicitly visualize the reward robustness and adversarial strategies resulting from our theory. We use the path consistency or indifference conditions to certify optimality of the policy.

| Ortega & Lee (2014) | Eysenbach & Levine (2021) | Husain et al. (2021) | Derman et al. (2021) | Ours | |

|---|---|---|---|---|---|

| Multi-Step Analysis | ✗ | ✓ | ✓ | ✓ | ✓ |

| Worst-Case | policy form | policy form | value form | policy (via dual lp Eq. 11) | policy value forms |

| Robust Set | ✗ | ✓ (see our App. F.4) | ✗ | ✓(flexible specification) | ✓ |

| Divergence Used | KL () | Shannon entropy (Sec. 5.1) | any convex | derived from robust set | any convex , -Div examples |

| or Reg.? | Both | Both | |||

| Indifference | ✓ | ✗ | ✗ | ✗ | ✓ |

| Path Consistency | ✗ | ✗ | ✗ | ✗ | ✓ |

2 Preliminaries

In this section, we review linear programming (lp) formulations of discounted Markov Decision Processes (mdp) and extensions to convex policy regularization.

Notation

For a finite set , let denote the space of real-valued functions over , with indicating restriction to non-negative functions. We let denote the probability simplex with dimension equal to the cardinality of . For , indicates the inner product in Euclidean space.

2.1 Convex Conjugate Function

We begin by reviewing the convex conjugate function, also known as the Legendre-Fenchel transform, which will play a crucial role throughout our paper. For a convex function which, in our context, has domain , the conjugate function is defined via the optimization

| (3) |

where . The conjugate operation is an involution for proper, lower semi-continuous, convex (Boyd & Vandenberghe, 2004), so that and is also convex. We can thus represent via a conjugate optimization

| (4) |

Differentiating with respect to the optimization variable in Eq. 3 or (4) suggests the optimality conditions

| (5) |

Note that the above conditions also imply relationships of the form . This dual correspondence between values of and will form the basis of our adversarial interpretation in Sec. 3.

2.2 Divergence Functions

We are interested in the conjugate duality associated with policy regularization, which is often expressed using a statistical divergence over a joint density (see Sec. 2.3). In particular, we consider the family of -divergences (Amari, 2016; Cichocki & Amari, 2010), which includes both the forward and reverse kl divergences as special cases. In the following, we consider extended divergences that accept unnormalized density functions as input (Zhu & Rohwer, 1995) so that we may analyze function space dualities and evaluate Lagrangian relaxations without projection onto the probability simplex.

KL Divergence

The ‘forward’ kl divergence to a reference policy is commonly used for policy regularization in rl. Extending the input domain to unnormalized measures, we write the divergence as

| (6) |

Using a uniform reference , we recover the Shannon entropy up to an additive constant.

-Divergence

The -divergence over possibly unnormalized measures is defined as

| (7) |

Taking the limiting behavior, we recover the ‘forward’ kl divergence as or the ‘reverse’ kl divergence as .

To provide intuition for the -divergence, we define the deformed -logarithm as in Lee et al. (2019), which matches Tsallis’s -logarithm (Tsallis, 2009) for . Its inverse is the -exponential, with

| (8) |

where ensures fractional powers can be taken and suggests that for . Using the -logarithm, we can rewrite the -divergence similarly to the kl divergence in Eq. 6 For a uniform reference , the -divergence differs from the Tsallis entropy by only the factor and an additive constant (see App. F.1).

| Divergence | Conjugate | Conjugate Expression | Optimizing Argument ( or ) |

|---|---|---|---|

2.3 Unregularized MDPs

A discounted mdp is a tuple consisting of a state space , action space , transition dynamics for , , initial state distribution in the probability simplex, and reward function . We also use a discount factor (Puterman (1994) Sec 6).

We consider an agent that seeks to maximize the expected discounted reward by acting according to a decision policy for each . The expected reward is calculated over trajectories , which begin from an initial and evolve according to the policy and mdp dynamics

| (9) |

We assume that the policy is stationary and Markovian, and thus independent of both the timestep and trajectory history.

Linear Programming Formulation

We will focus on a linear programming (lp) form for the objective in Eq. 9, which is common in the literature on convex duality. With optimization over the discounted state-action occupancy measure, , we rewrite the objective as

| (10) | ||||

We refer to the constraints in the second line of Eq. 10 as the Bellman flow constraints, which force to respect the mdp dynamics. We denote the set of feasible as . For normalized and , we show in App. A.2 that implies is normalized.

It can be shown that any feasible induces a stationary , where and is normalized by definition. Conversely, any stationary policy induces a unique state-action visitation distribution (Syed et al. (2008), Feinberg & Shwartz (2012) Sec. 6.3). Along with the definition of above, this result demonstrates the equivalence of the optimizations in Eq. 9 and Eq. 10. We will proceed with the lp notation from Eq. 10 and assume is induced by whenever the two appear together in an expression.

Importantly, the flow constraints in Eq. 10 lead to a dual optimization which reflects the familiar Bellman equations (Bellman, 1957). To see this, we introduce Lagrange multipliers for each flow constraint and for the nonnegativity constraints. Summing over , and eliminating by setting yields the dual lp

| (11) |

where we have used as shorthand for and reindexed the transition tuple from to compared to Eq. 10. Note that the constraint applies for all and that . By complementary slackness, we know that for such that .

2.4 Regularized MDPs

We now consider regularizing the objective in Eq. 10 using a convex penalty function with coefficient . We primarily focus on regularization using a conditional divergence between the policy and a normalized reference distribution , as in Sec. 2.2 and (Ortega & Braun, 2013; Fox et al., 2016; Haarnoja et al., 2017; 2018). We also use the notation to indicate regularization of the full state-action occupancy measure to a normalized reference , which appears, for example, in Relative Entropy Policy Search (reps) (Peters et al., 2010; Belousov & Peters, 2019). The regularized objective is then defined as

| (12) |

where contains an expectation under as in Eq. 6-(7). We can also derive a dual version of the regularized lp, by first writing the Lagrangian relaxation of Eq. 12

| (13) |

Swapping the order of optimization under strong duality, we can recognize the maximization over as a conjugate function , as in Eq. 3, leading to a regularized dual optimization

| (14) |

which involves optimization over dual variables only and is unconstrained, in contrast to Eq. 11. Dual objectives of this form appear in (Nachum & Dai, 2020; Belousov & Peters, 2019; Bas-Serrano et al., 2021; Neu et al., 2017). We emphasize the need to include the Lagrange multiplier , with when the optimal policy has , since an important motivation for -divergence regularization is to encourage sparsity in the policy (see Eq. 8, Lee et al. (2018; 2019); Chow et al. (2018)).

Soft Value Aggregation

In iterative algorithms such as (regularized) modified policy iteration (Puterman & Shin, 1978; Scherrer et al., 2015), it is useful to consider the regularized Bellman optimality operator (Geist et al., 2019). For given estimates of the state-action value , the operator updates as

| (15) |

Note that this conjugate optimization is performed in each state and explicitly constrains each to be normalized. Although we proceed with the notation of Eq. 12 and Eq. 14, our later developments are compatible with the ‘soft-value aggregation’ perspective above. See App. C for detailed discussion.

3 Adversarial Interpretation

In this section, we interpret regularization as implicitly providing robustness to adversarial perturbations of the reward function. To derive our adversarial interpretation, recall from Eq. 4 that conjugate duality yields an alternative representation of the regularizer

| (16) |

Using this conjugate optimization to expand the regularization term in the primal objective of Eq. 12,

| (17) |

We interpret Eq. 17 as a two-player minimax game between an agent and an implicit adversary, where the agent chooses an occupancy measure or its corresponding policy , and the adversary chooses reward perturbations subject to the convex conjugate as a penalty function (Ortega & Lee, 2014).

To understand the limitations this penalty imposes on the adversary, we transform the optimization over in Eq. 17 to a constrained optimization in Sec. 3.1. This allows us to characterize the feasible set of reward perturbations available to the adversary or, equivalently, the set of modified rewards to which a particular stochastic policy is robust. In Sec. 3.2 and 3.4, we interpret the worst-case adversarial perturbations corresponding to an arbitrary stochastic policy and the optimal policy, respectively.

3.1 Robust Set of Modified Rewards

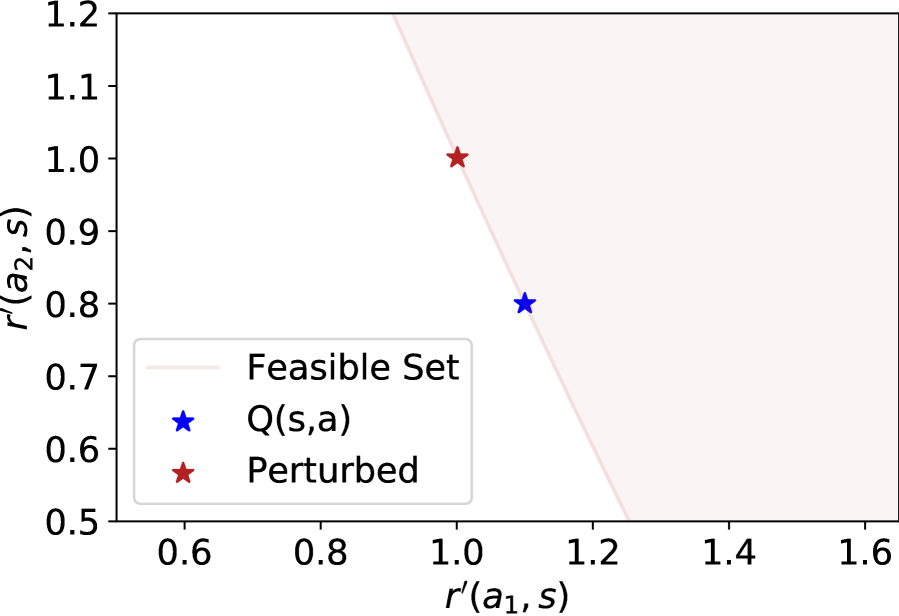

In order to link our adversarial interpretation to robustness and zero-shot generalization as in Eq. 1-(2), we characterize the feasible set of reward perturbations in the following proposition. We state our proposition for policy regularization, and discuss differences for regularization in App. D.2.

Proposition 1.

Assume a normalized policy for the agent is given, with . Under -divergence policy regularization to a normalized reference , the optimization over in Eq. 17 can be written in the following constrained form

| (18) |

We refer to as the feasible set of reward perturbations available to the adversary. This translates to a robust set of modified rewards for the given policy. These sets depend on the -divergence and regularization strength via the conjugate function.

For kl divergence regularization, the constraint is

| (19) |

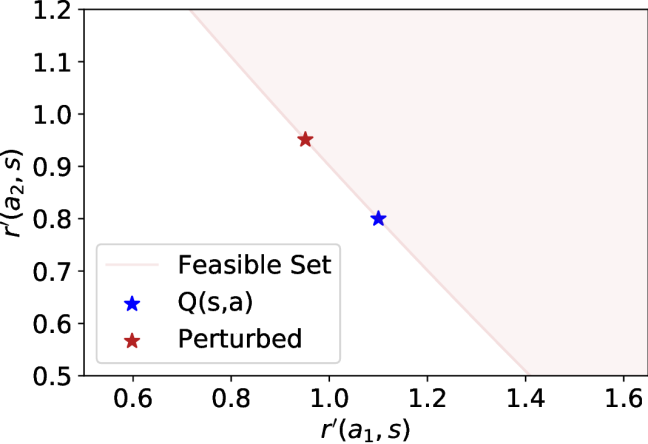

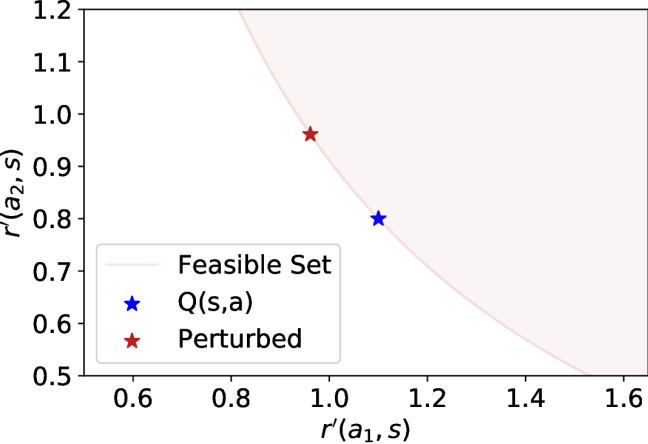

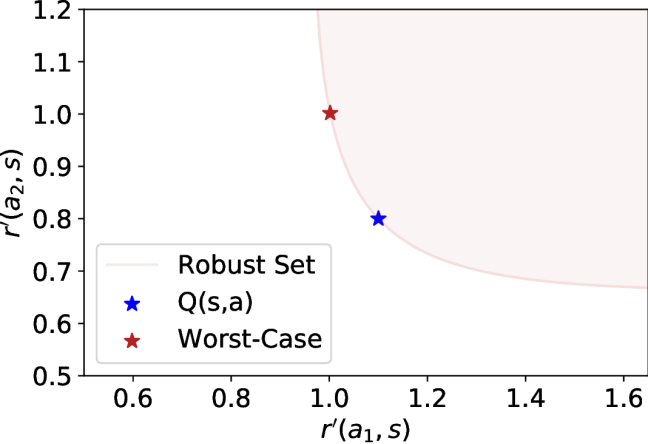

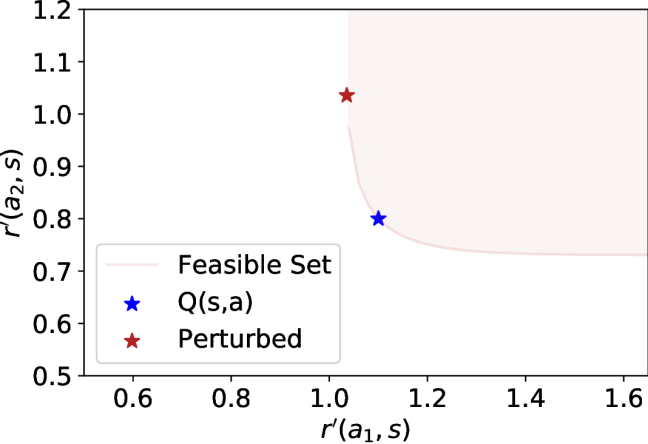

See App. D.1 for proof, and Table 2 for the convex conjugate function associated with various regularization schemes. The proof proceeds by evaluating the conjugate function at the minimizing argument in Eq. 17 (see Sec. 3.2), with for normalized and . The constraint then follows from the fact that is convex and increasing in (Husain et al., 2021). We visualize the robust set for a two-dimensional action space in Fig. 2, with additional discussion in Sec. 4.1.

As in Eq. 2, we can provide ‘zero-shot’ performance guarantees using this set of modified rewards. For any perturbed reward in the robust set , we have , so that the policy achieves an expected modified reward which is at least as large as the regularized objective. However, notice that this form of robustness is sensitive to the exact value of the regularized objective function. Although entropy regularization and divergence regularization with a uniform reference induce the same optimal , we highlight crucial differences in their reward robustness interpretations in Sec. 5.1.

3.2 Worst-Case Perturbations: Policy Form

From the feasible set in Prop. 1, how should the adversary select its reward perturbations? In the following proposition, we use the optimality conditions in Eq. 5 to solve for the worst-case reward perturbations which minimize Eq. 17 for an fixed but arbitrary stochastic policy .

Proposition 2.

For a given policy or state-action occupancy , the worst-case adversarial reward perturbations or associated with a convex function and regularization strength are

| (20) |

See App. A.1 for proof. We now provide example closed form expressions for the worst-case reward perturbations under common regularization schemes. We emphasize that the same stochastic policy or joint occupancy measure can be associated with different adversarial perturbations depending on the choice of -divergence and strength .111One exception is that a policy with s.t. can only be represented using kl regularization if .

KL Divergence

-Divergence

For kl divergence regularization, the worst-case reward perturbations had a similar expression for conditional and joint regularization. However, we observe notable differences for the -divergence in general. For policy regularization to a reference ,

| (22) |

where we define as

| (23) |

As we discuss in App. B.3, plays the role of a normalization constant for the optimizing argument in the definition of (see Eq. 3, Table 2). This term arises from differentiating with respect to instead of from an explicit constraint. Assuming the given and reference are normalized, note that . With normalization, we also observe that for kl divergence regularization (), which confirms Eq. 21 is a special case of Eq. 22.

For any given state-action occupancy measure and joint -divergence regularization to a reference , the worst-case perturbations become

| (24) |

with detailed derivations in App. B.4. In contrast to Eq. 22, this expression lacks an explicit normalization constant, as this constraint is enforced by the Lagrange multipliers and (App. A.2).

3.3 Worst-Case Perturbations: Value Form

In the previous section, we analyzed the implicit adversary corresponding to any stochastic policy for a given and . We now take a dual perspective, where the adversary is given access to a set of dual variables across states and selects reward perturbations . We will eventually show in Sec. 3.4 that these perturbations match the policy-form perturbations at optimality.

Our starting point is Theorem 3 of Husain et al. (2021), which arises from taking the convex conjugate of the entire regularized objective , which is concave in . See App. E.1.

Theorem 1 (Husain et al. (2021)).

Rearranging the equality constraint to solve for and substituting into the objective, this optimization recovers the regularized dual problem in Eq. 14. We can also compare Eq. 25 to the unregularized dual problem in Eq. 11, which does not include an adversarial cost and whose constraint implies an unmodified reward, or . Similarly to Sec. 3.2, the adversary incorporates the effect of policy regularization via the reward perturbations .

3.4 Policy Form Value Form at Optimality

In the following proposition, we provide a link between the policy and value forms of the adversarial reward perturbations, showing that for the optimal policy and value . As in Eysenbach & Levine (2021), the uniqueness of the optimal policy implies that its robustness may be associated with an environmental reward for a given regularized mdp.

Proposition 3.

For the optimal policy and value function corresponding to -divergence policy regularization with strength , the policy and value forms of the worst-case adversarial reward perturbations match, , and are related to the advantage function via

| (26) |

where we define and recall by complementary slackness. Note that depends on the regularization scheme via the conjugate function in Eq. 25.

Proof.

See App. A.3. We consider the optimal policy in an mdp with -divergence policy regularization , which is derived via similar derivations as Lee et al. (2019) or by eliminating in Eq. 13.

| (27) |

We prove Prop. 3 by plugging this optimal policy into the worst-case reward perturbations from Eq. 22, . We can also use Eq. 26 to verify is normalized, since ensures normalization for the policy corresponding to . In App. C.3, we also show , where is a Lagrange multiplier enforcing normalization in Eq. 15. ∎

Path Consistency Condition

The equivalence between and at optimality matches the path consistency conditions from (Nachum et al., 2017; Chow et al., 2018) and suggests generalizations to general -divergence regularization. Indeed, combining Eq. 22 and (26) and rearranging,

| (28) |

for all and . This is a natural result, since path consistency is obtained using the kkt optimality condition involving the gradient with respect to of the Lagrangian relaxation in Eq. 13. Similarly, we have seen in Prop. 2 that . See App. A.4.

Indifference Condition

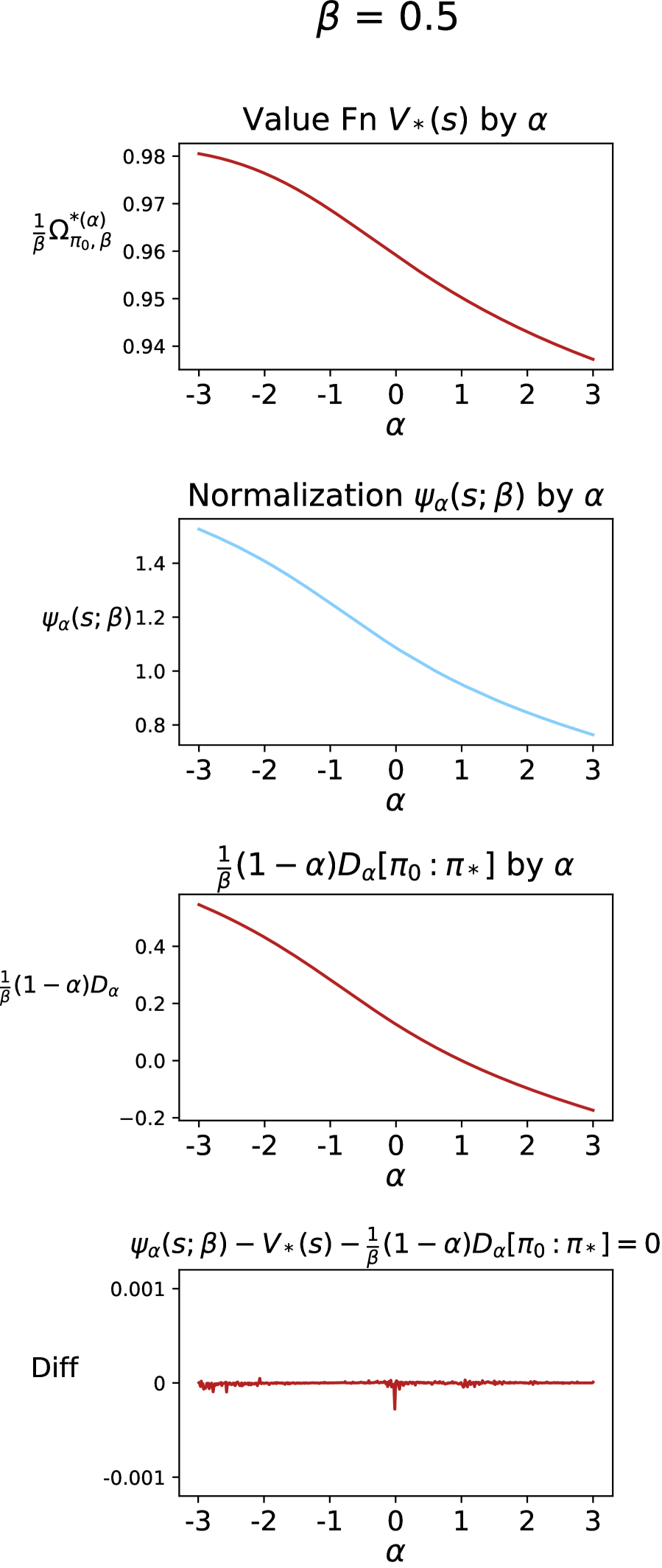

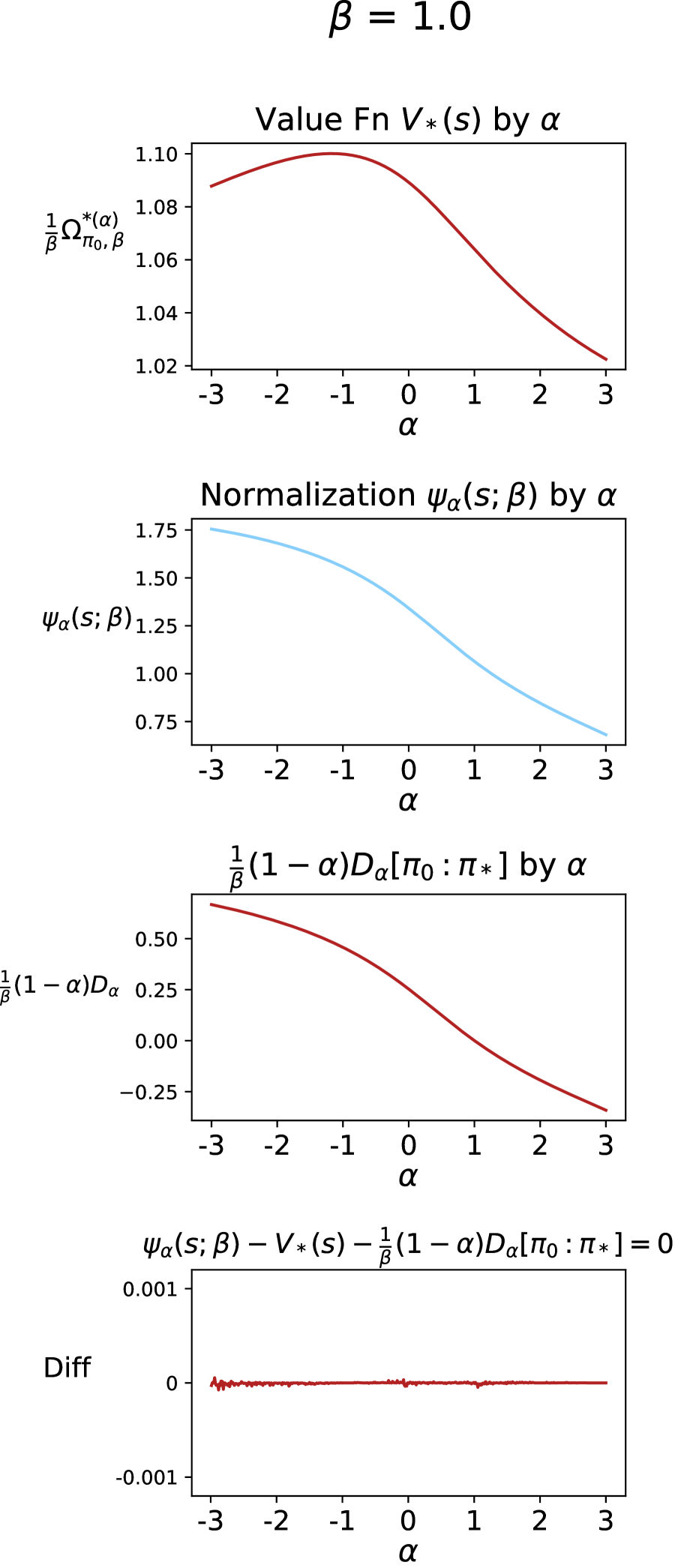

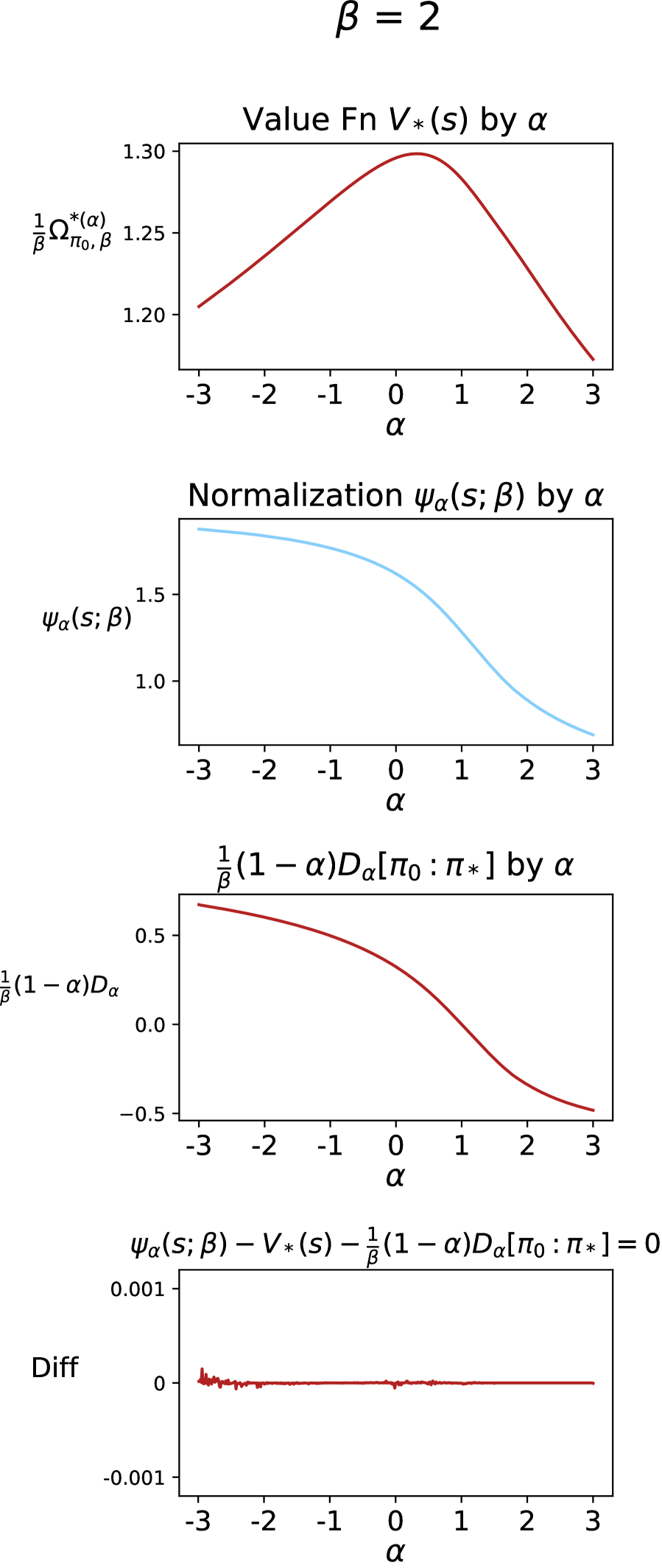

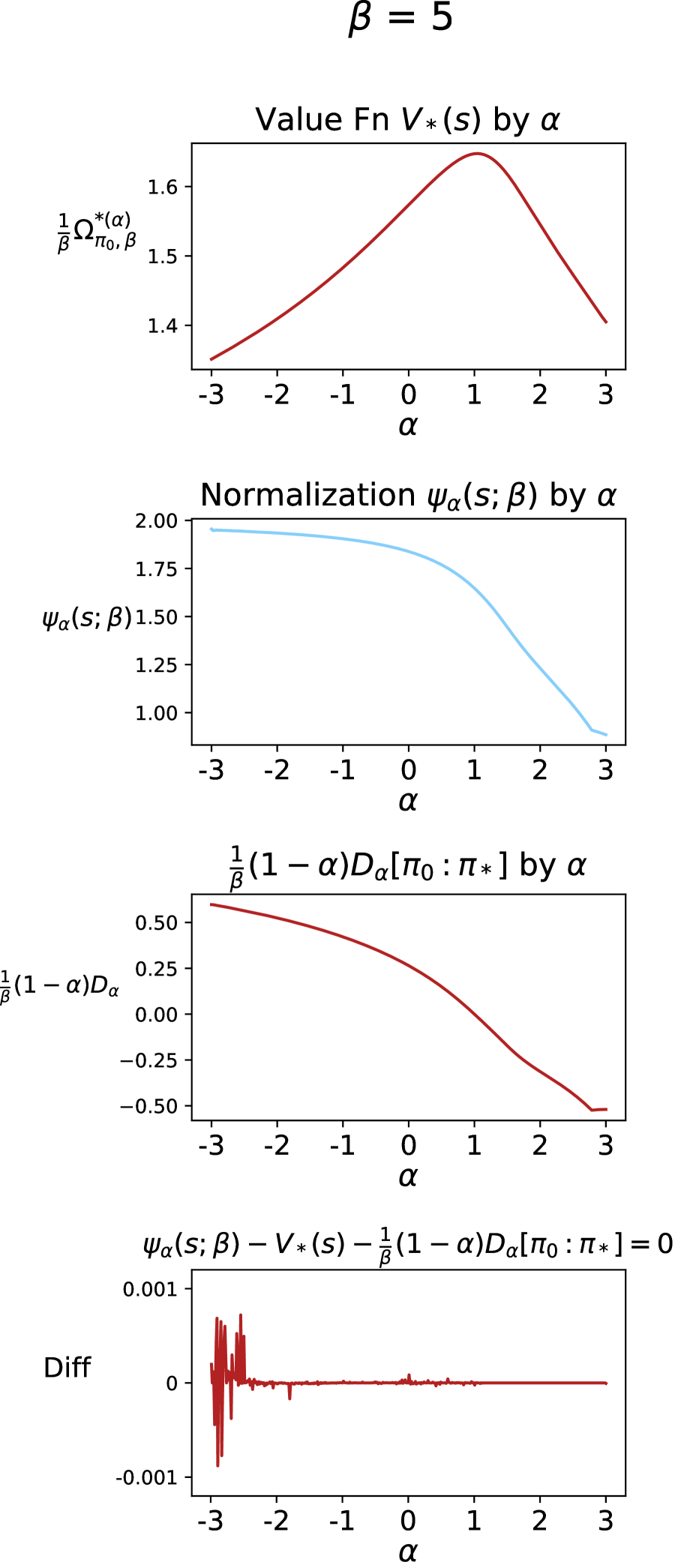

As Ortega & Lee (2014) discuss for the single step case, the saddle point of the minmax optimization in Eq. 17 reflects an indifference condition which is a well-known property of Nash equilibria in game theory (Osborne & Rubinstein, 1994). Consider to be the agent’s estimated payoff for each action in a particular state. For the optimal policy, value, and worst-case reward perturbations, Eq. 28 shows that the pointwise modified reward is equal to a constant.222This holds for actions with and . Note that we treat as the reward in the sequential case. Against the optimal strategy of the adversary, the agent becomes indifferent between the actions in its mixed strategy. The value or conjugate function (see App. C) is known as the certainty equivalent (Fishburn, 1988; Ortega & Braun, 2013), which measures the total expected utility for an agent starting in state , in a two-player game against an adversary defined by the regularizer with strength . We empirically confirm the indifference condition in Fig. 3 and 7.

4 Experiments

In this section, we visualize the robust set and worst-case reward perturbations associated with policy regularization, using intuitive examples to highlight theoretical properties of our adversarial interpretation.

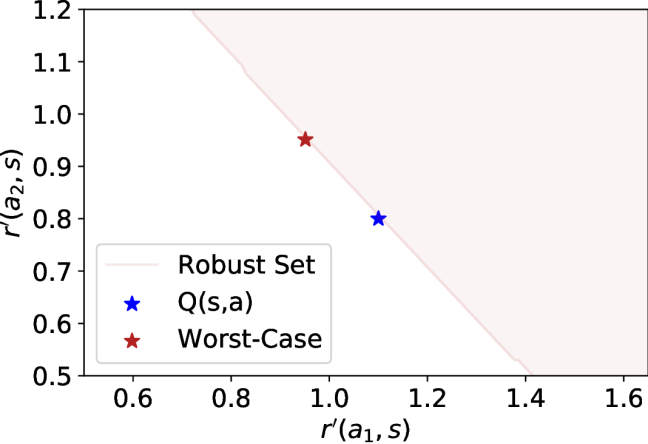

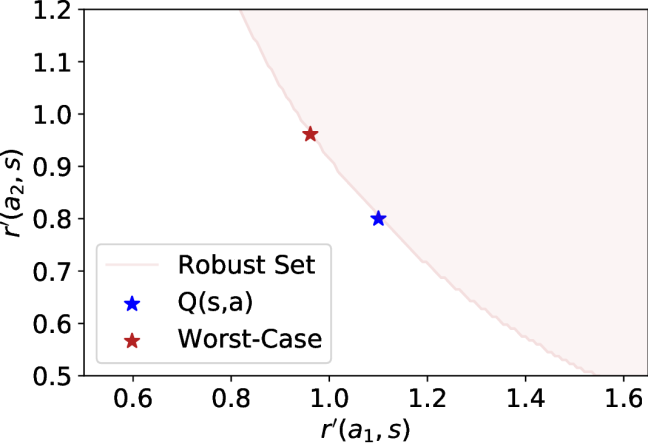

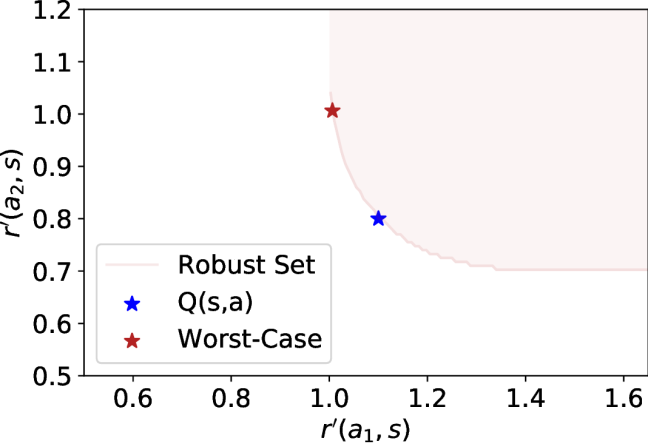

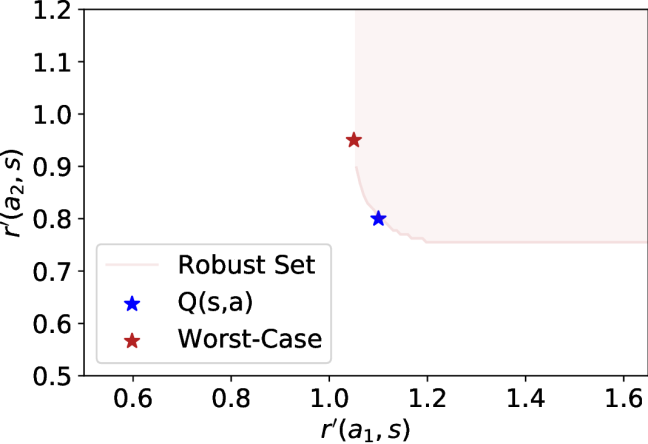

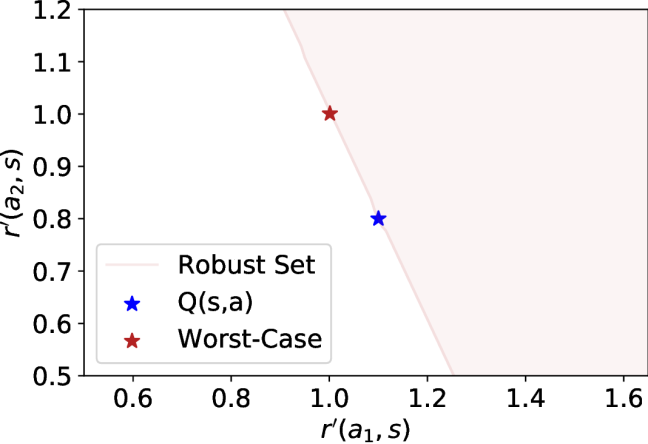

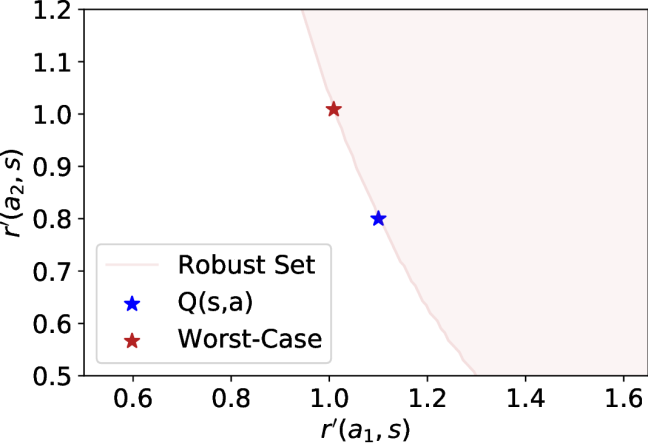

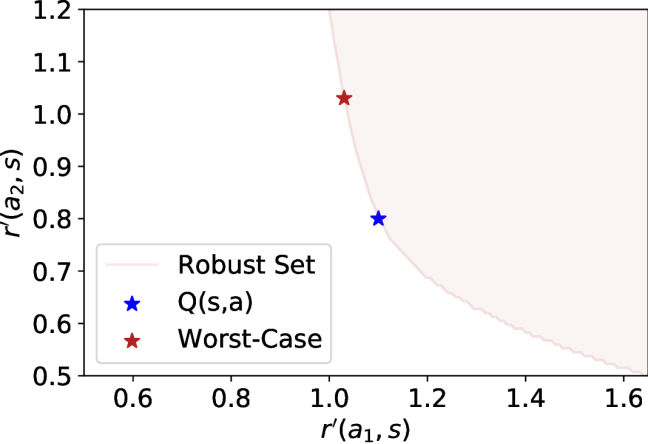

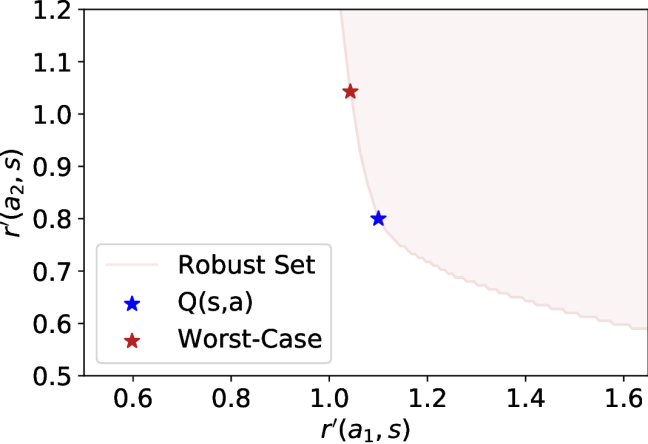

4.1 Visualizing the Robust Set

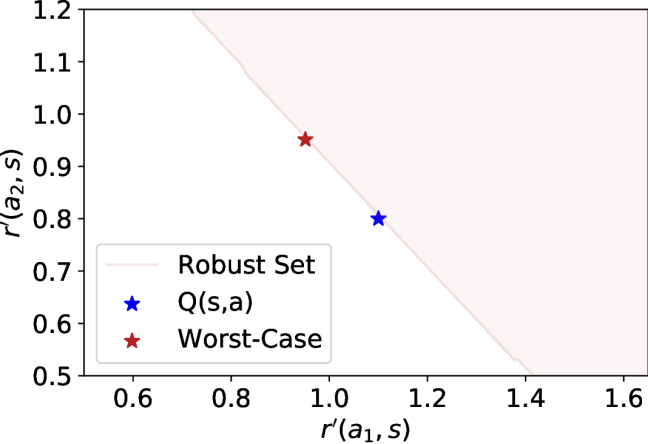

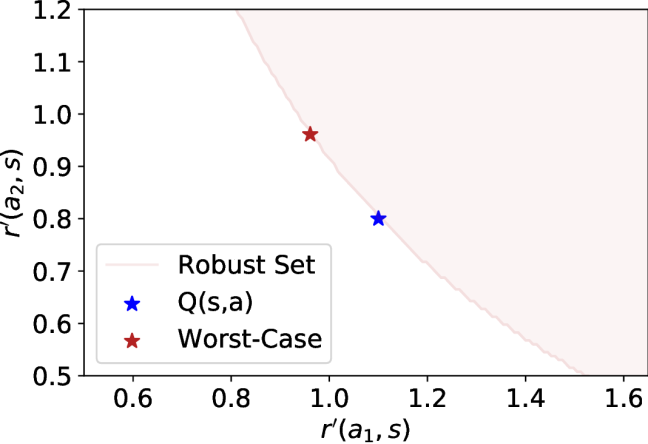

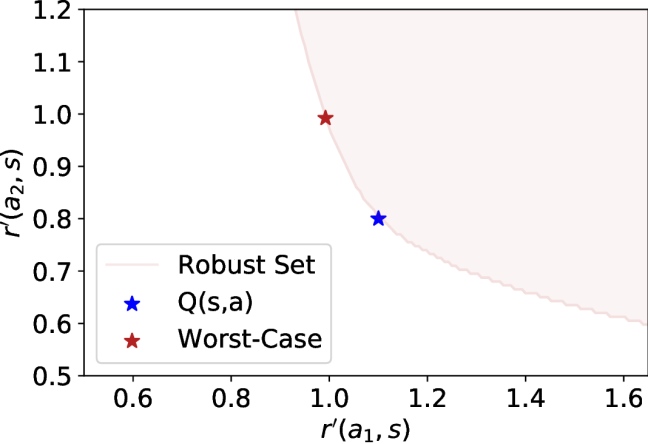

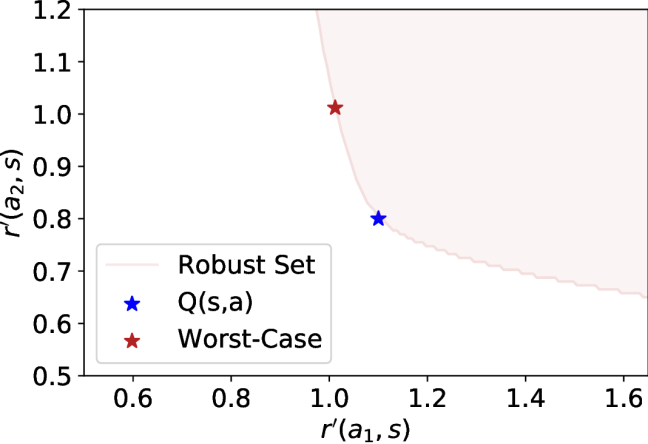

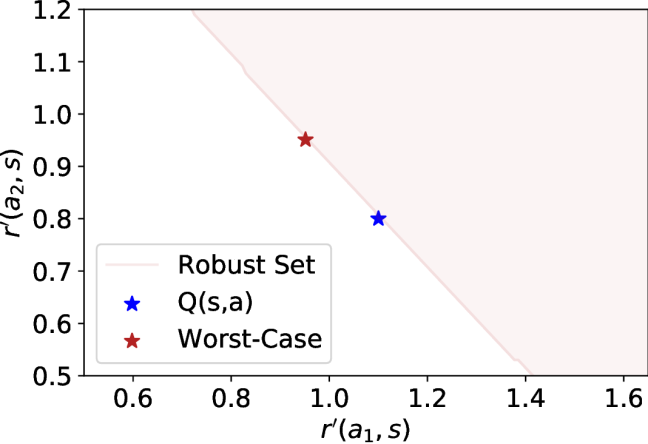

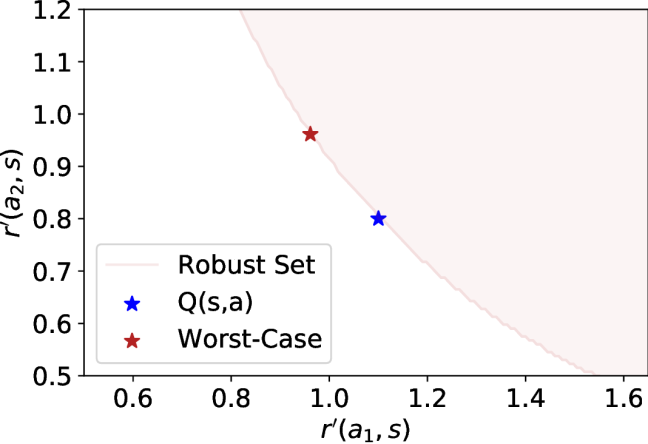

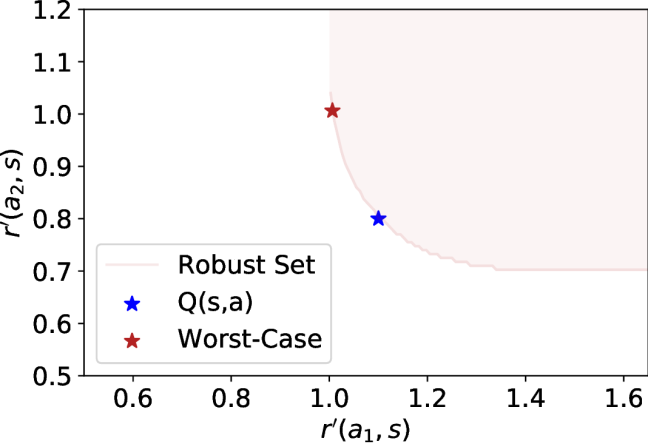

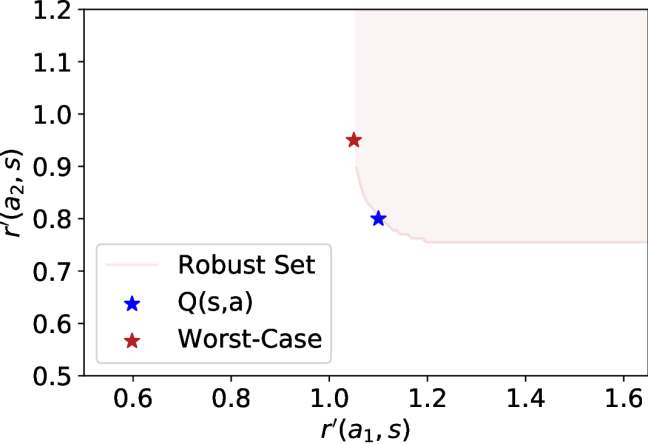

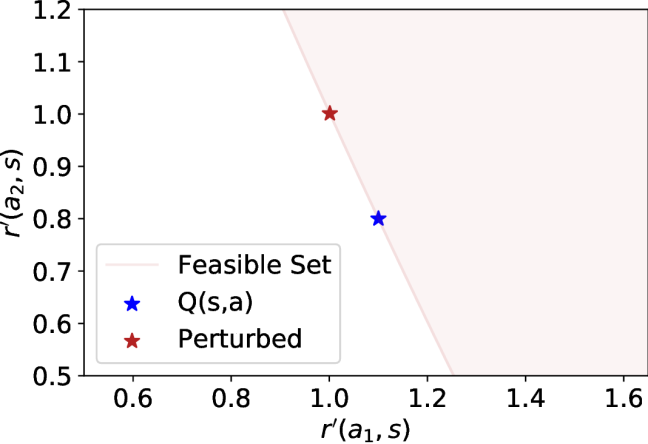

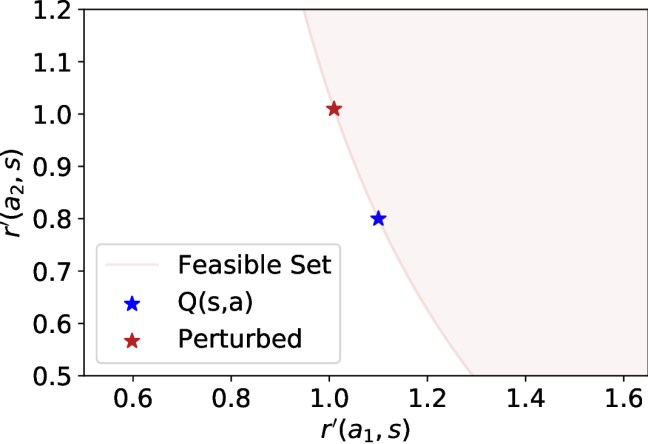

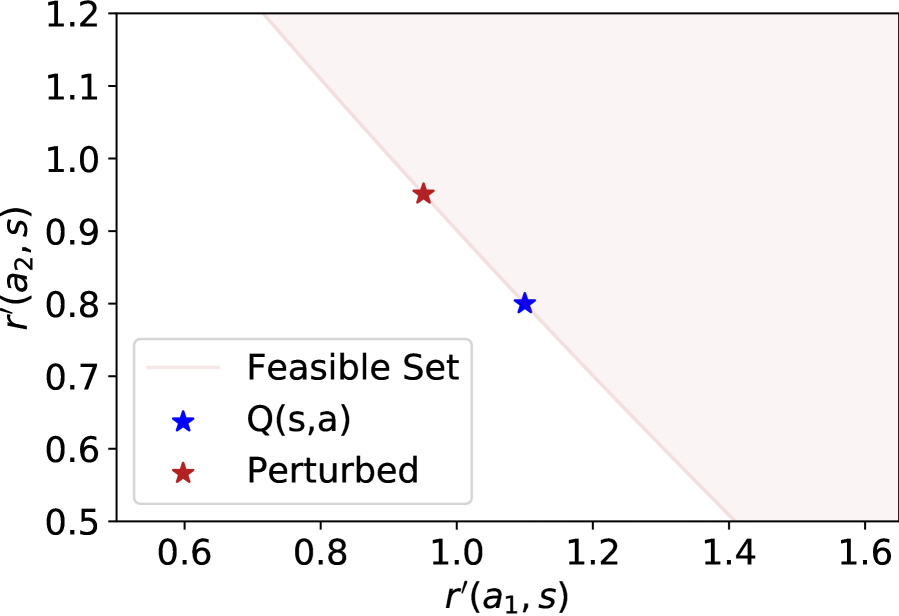

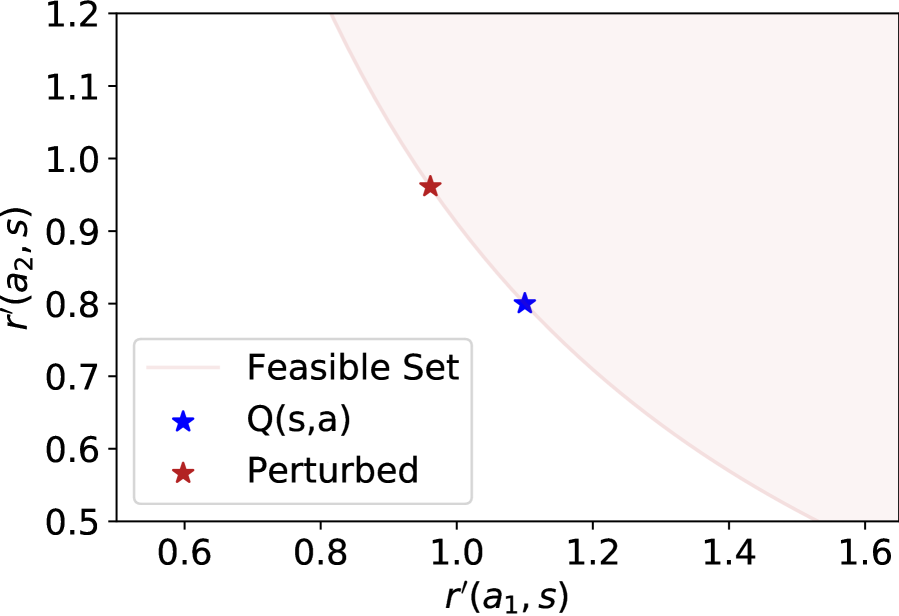

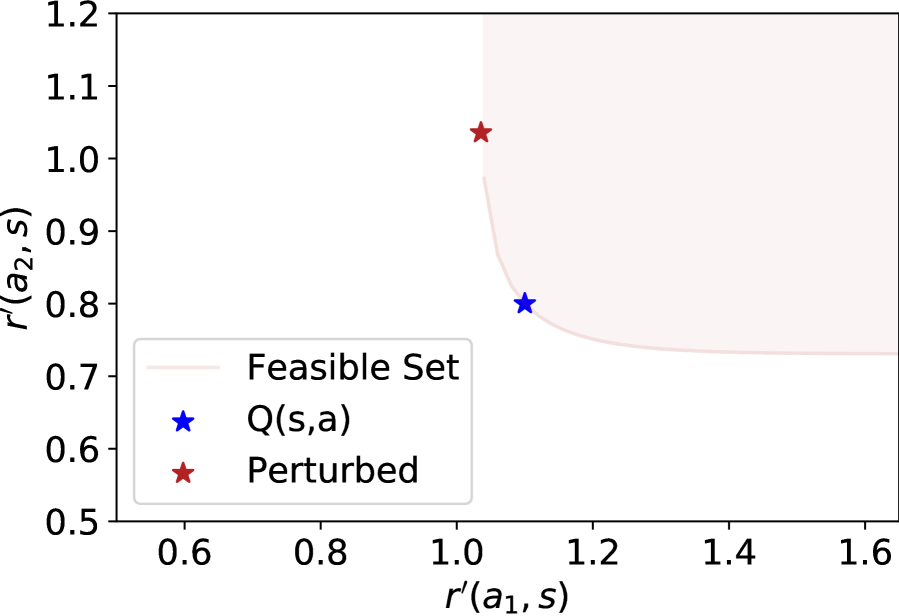

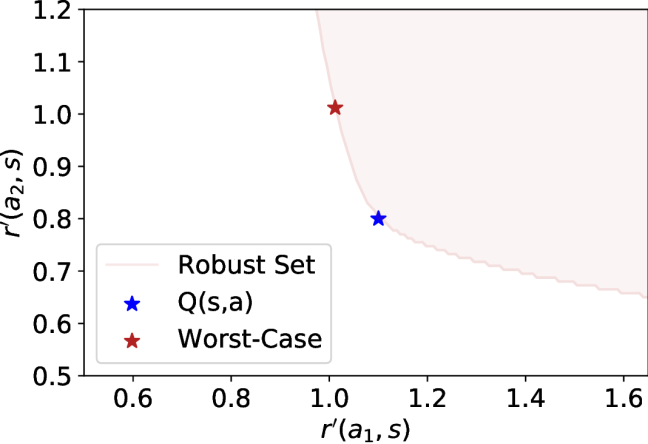

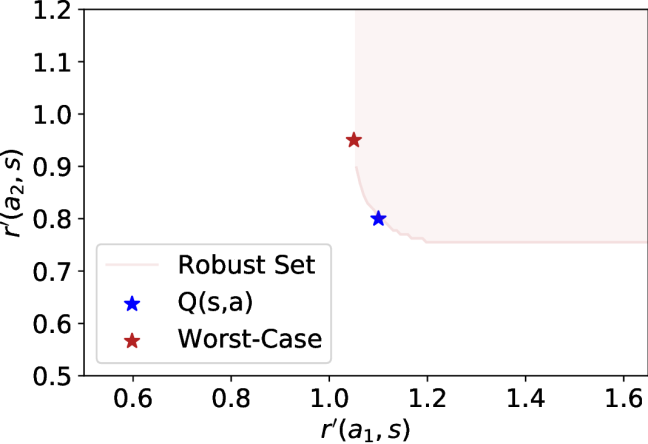

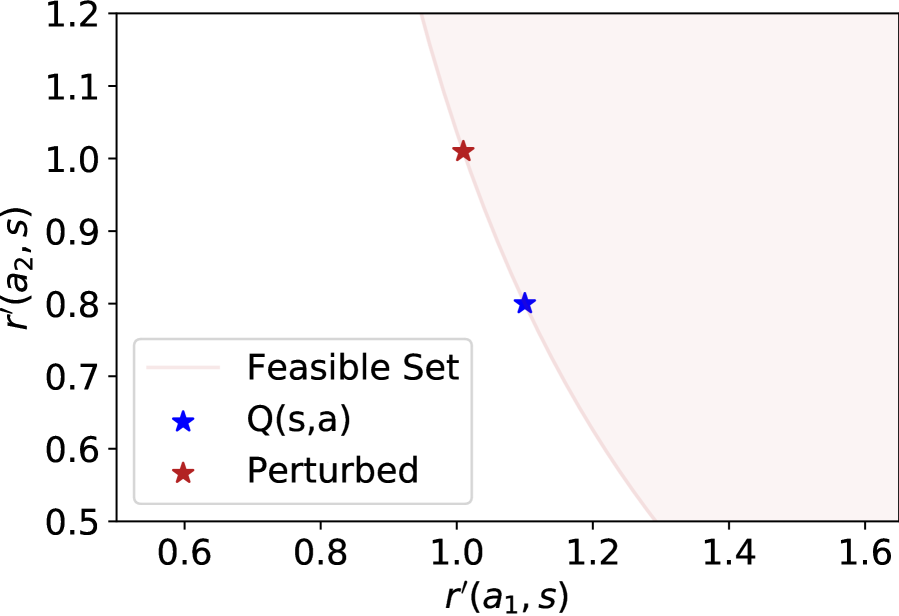

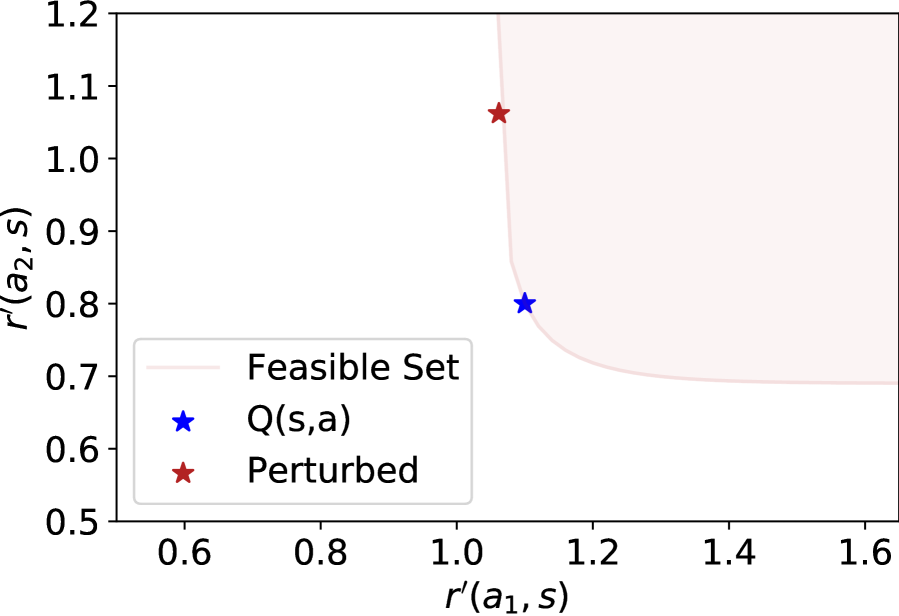

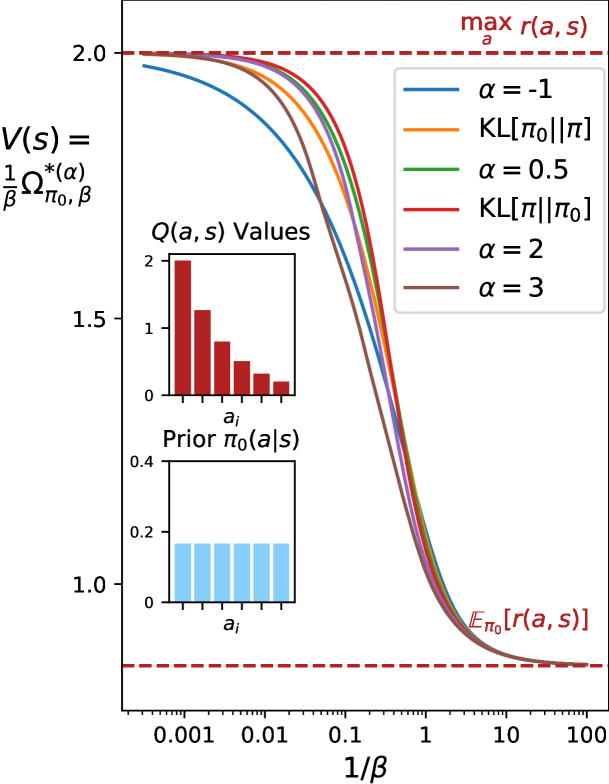

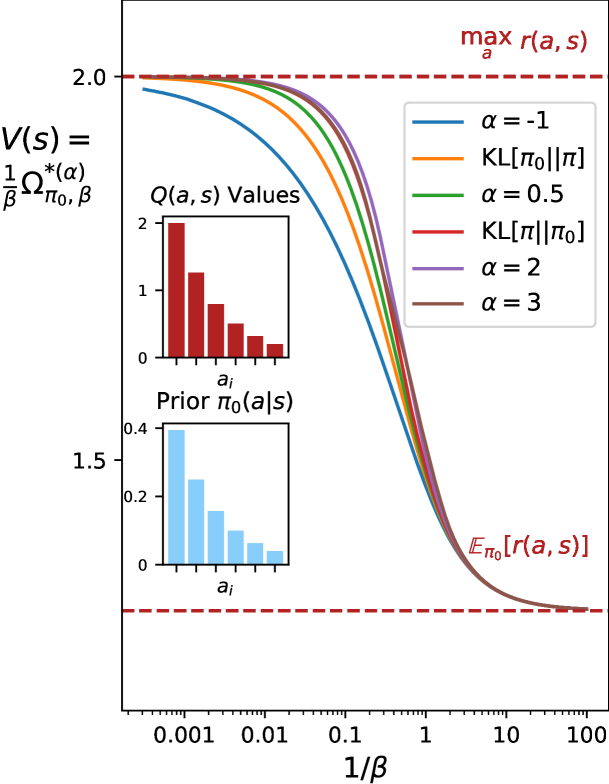

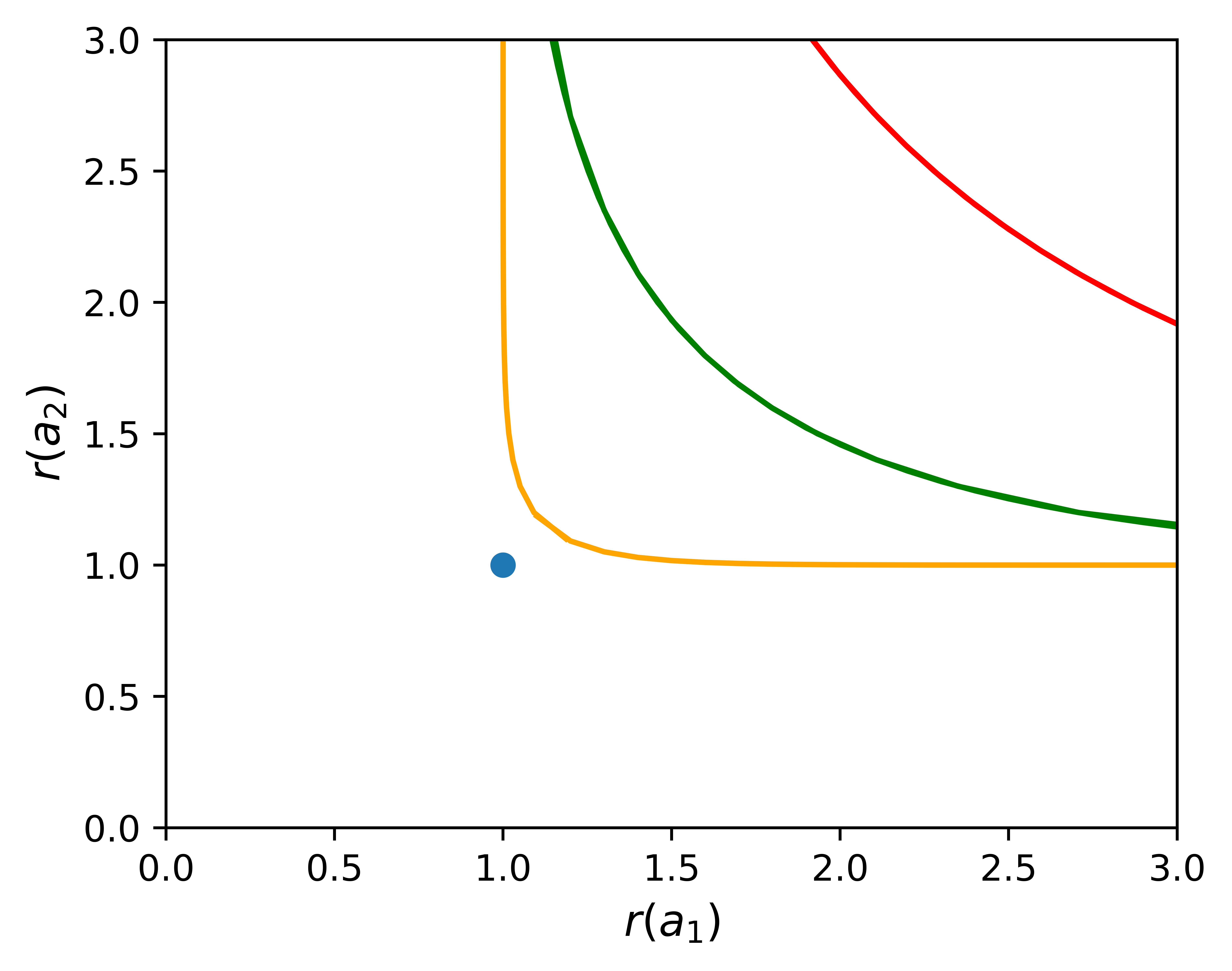

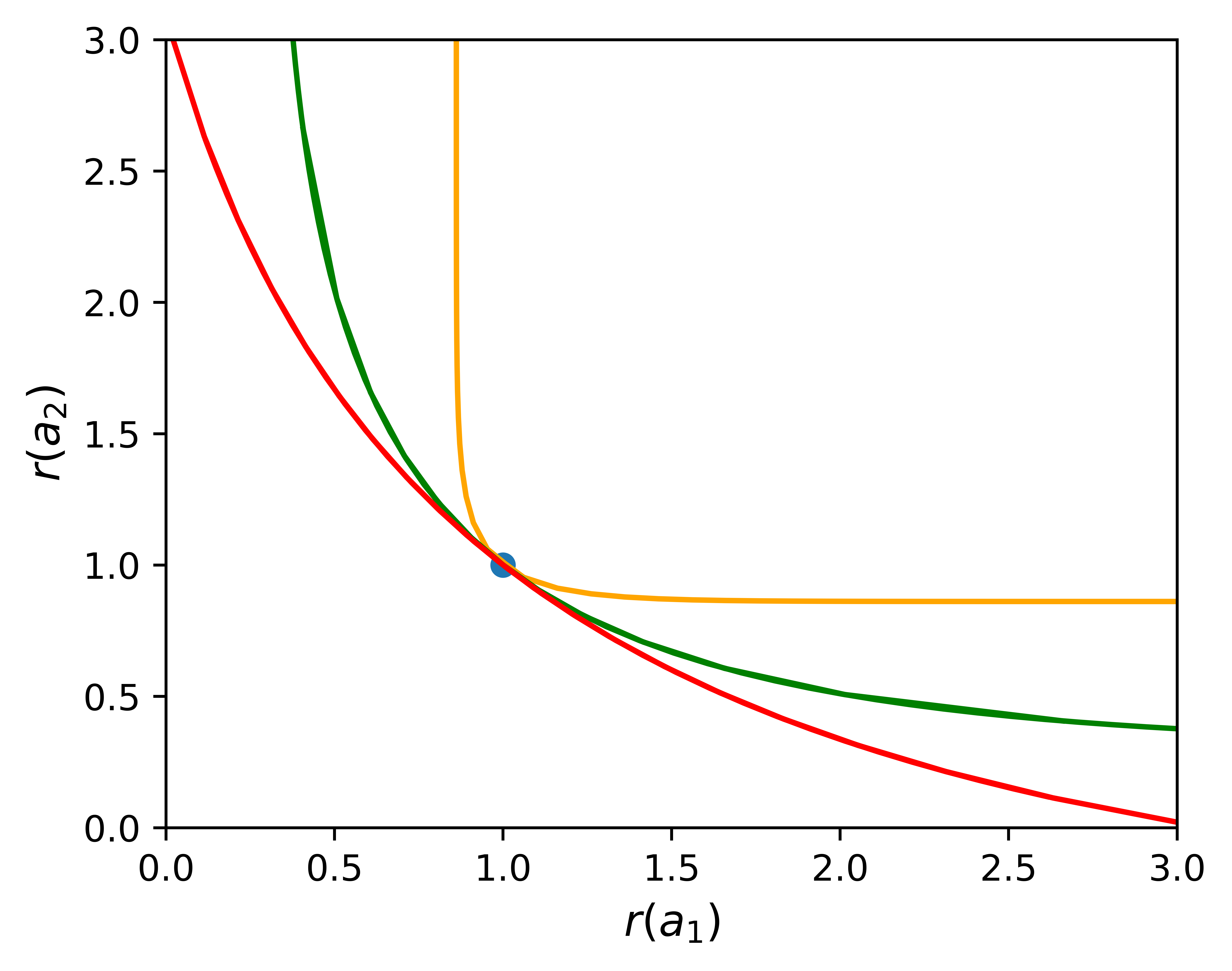

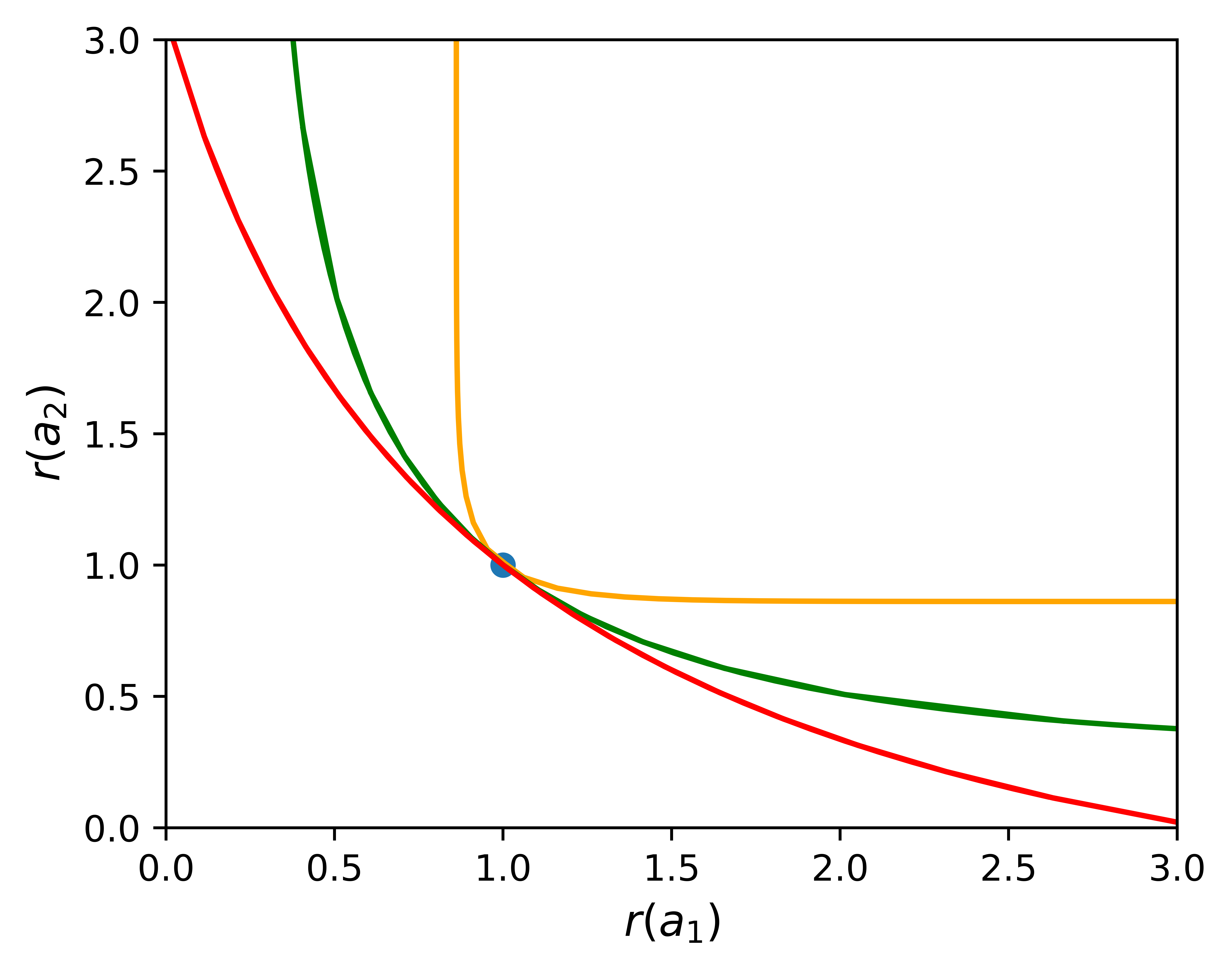

In Fig. 2, we visualize the robust set of perturbed rewards for the optimal policy in a two-dimensional action space for the kl or -divergence, various , and a uniform or non-uniform prior policy . Since the optimal policy can be easily calculated in the single-step case, we consider fixed and show the robustness of the optimal , which differs based on the choice of regularization scheme using Eq. 27. We determine the feasible set of using the constraint in Prop. 1 (see App. D.3 for details), and plot the modified reward for each action.

Inspecting the constraint for the adversary in Eq. 19, note that both reward increases and reward decreases contribute non-negative terms at each action, which either up- or down-weight the reference policy . The constraint on their summation forces the adversary to trade off between perturbations of different actions in a particular state. Further, since the constraints in Prop. 1 integrate over the action space, the rewards for all actions in a particular state must be perturbed together. While it is clear that increasing the reward in both actions preserves the inequality in Eq. 2, Fig. 2 also includes regions where one reward decreases.

For high regularization strength (), we observe that the boundary of the feasible set is nearly linear, with the slope based on the ratio of action probabilities in a policy that matches the prior. The boundary steepens for lower regularization strength. We can use the indifference condition to provide further geometric insight. First, drawing a line from the origin with slope will intersect the feasible set at the worst-case modified reward (red star) in each panel, with . At this point, the slope of the tangent line yields the ratio of action probabilities in the regularized policy, as we saw for the case. With decreasing regularization as , the slope approaches or for a nearly deterministic policy and a rectangular feasible region.

Finally, we show the -divergence robust set with and in Fig. 2 (d)-(e) and (i)-(j), with further visualizations in App. H. Compared to the kl divergence, we find a wider robust set boundary for . For and , the boundary is more strict and we observe much smaller reward perturbations as the optimal policy becomes deterministic () for both reference distributions. However, in contrast to the unregularized deterministic policy, the reward perturbations are nonzero. We provide a worked example in App. G, and note that indifference does not hold in this case, , due to the Lagrange multiplier .

4.2 Visualizing the Worst-Case Reward Perturbations

In this section, we consider kl divergence regularization to a uniform reference policy, which is equivalent to Shannon entropy regularization but more appropriate for analysis, as we discuss in Sec. 5.1.

Single Step Case

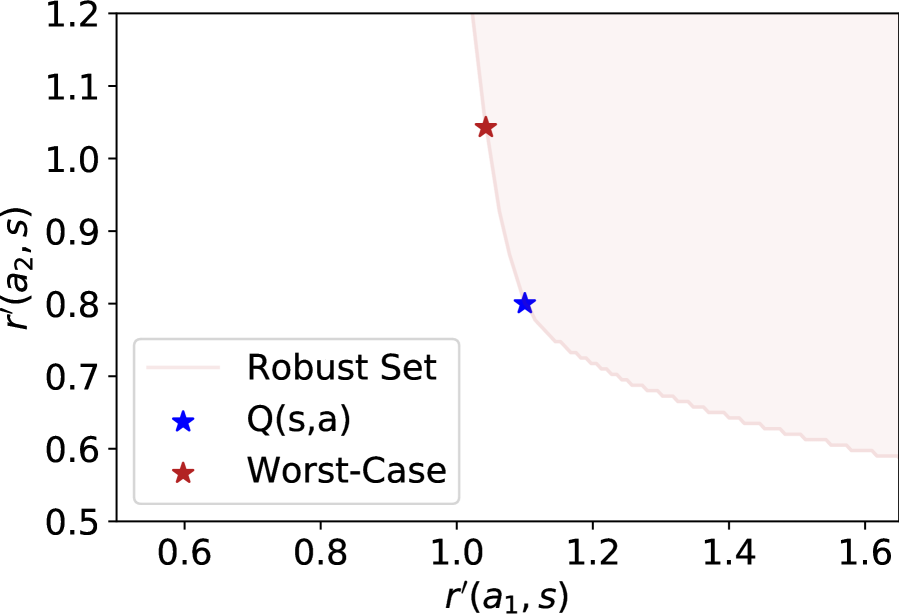

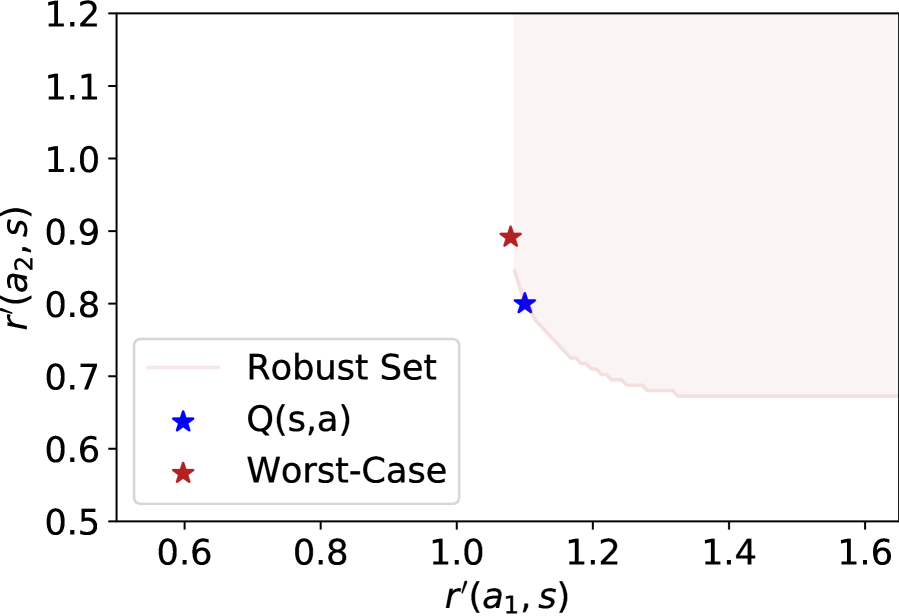

In Fig. 3, we plot the negative worst-case reward perturbations and modified reward for a single step decision-making case. For the optimal policy in Fig. 3(a), the perturbations match the advantage function as in Eq. 26 and the perturbed reward for all actions matches the value function . While we have shown in Sec. 3.2 that any stochastic policy may be given an adversarial interpretation, we see in Fig. 3(b) that the indifference condition does not hold for suboptimal policies.

The nearly-deterministic policy in Fig. 3(a)(ii) also provides intuition for the unregularized case as . Although we saw in Sec. 3.3 that in the unregularized case, Eq. 11 and (26) suggest that plays a similar role to the (negative) reward perturbations in Fig. 3(a)(ii), with and for all other actions.

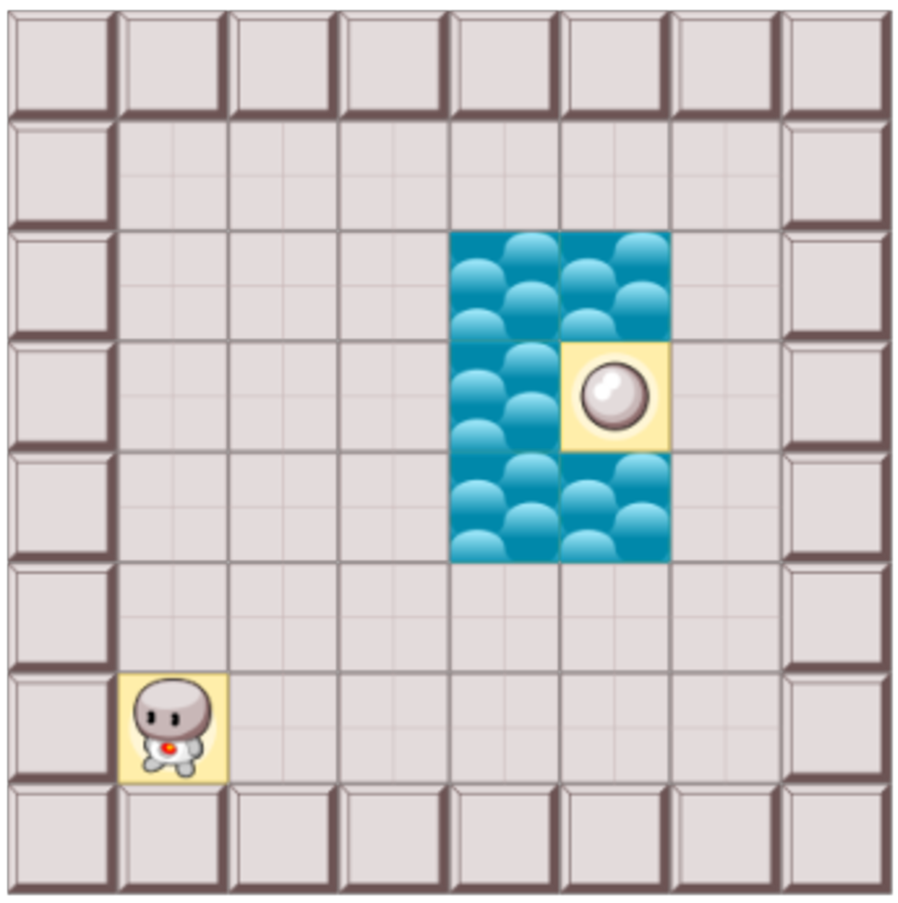

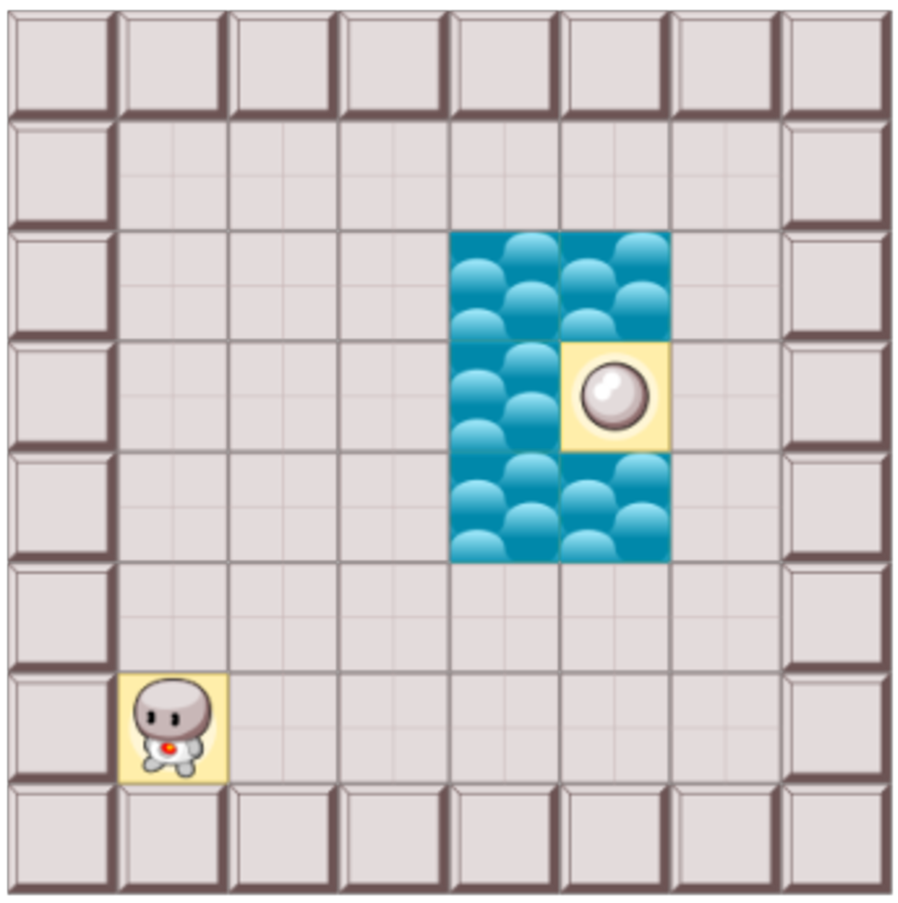

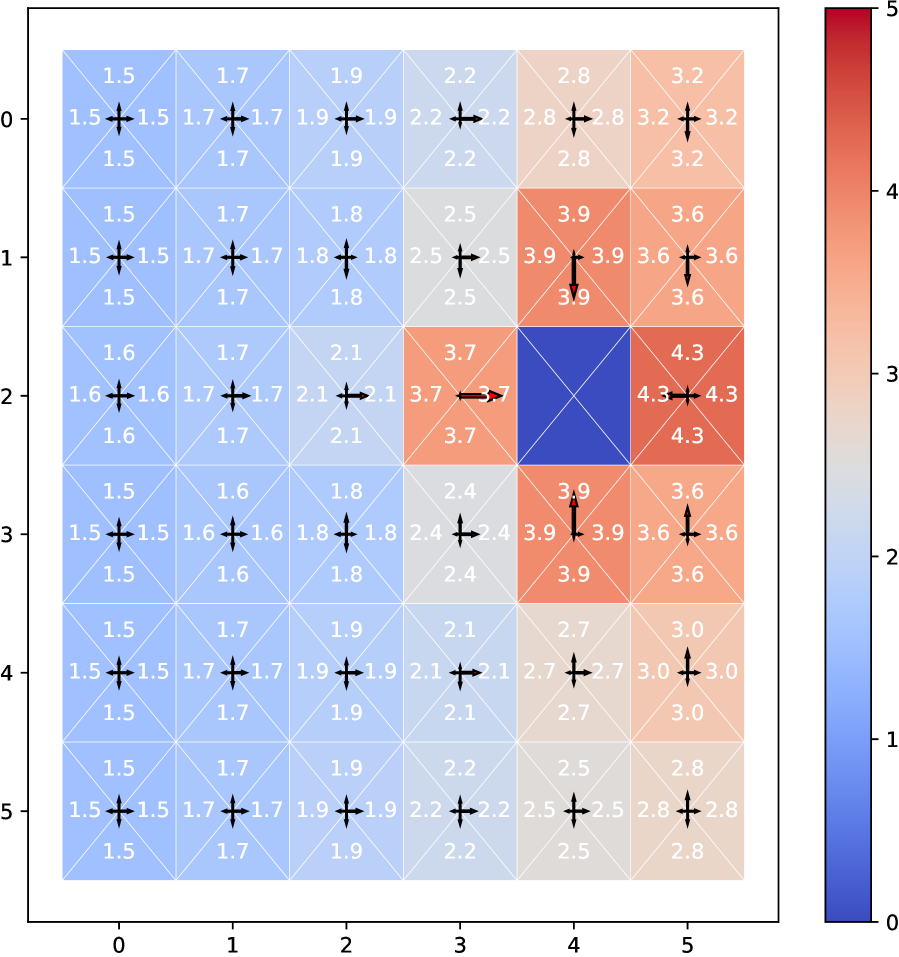

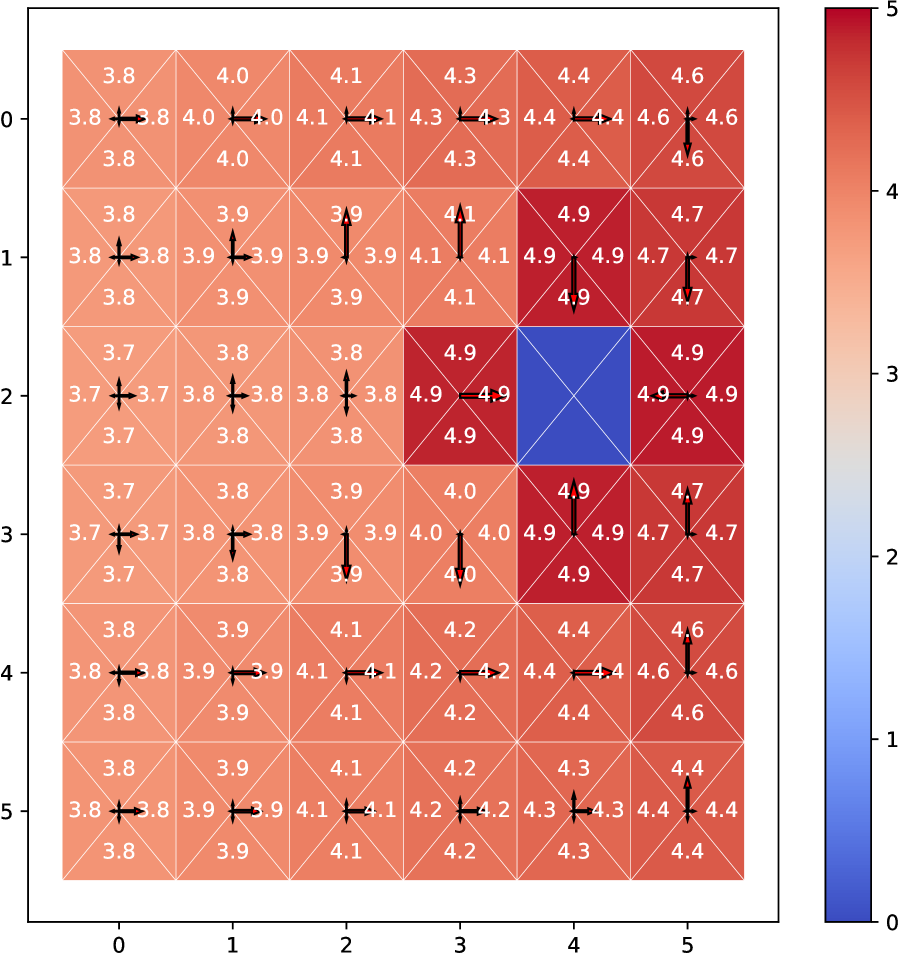

Sequential Setting

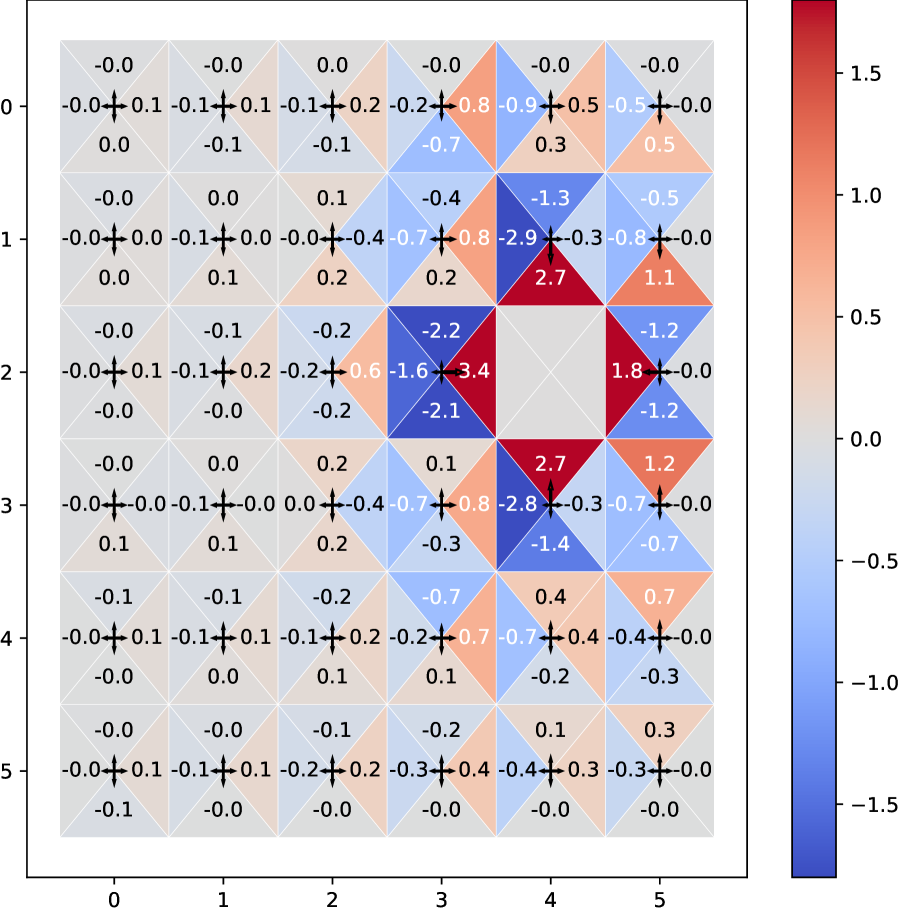

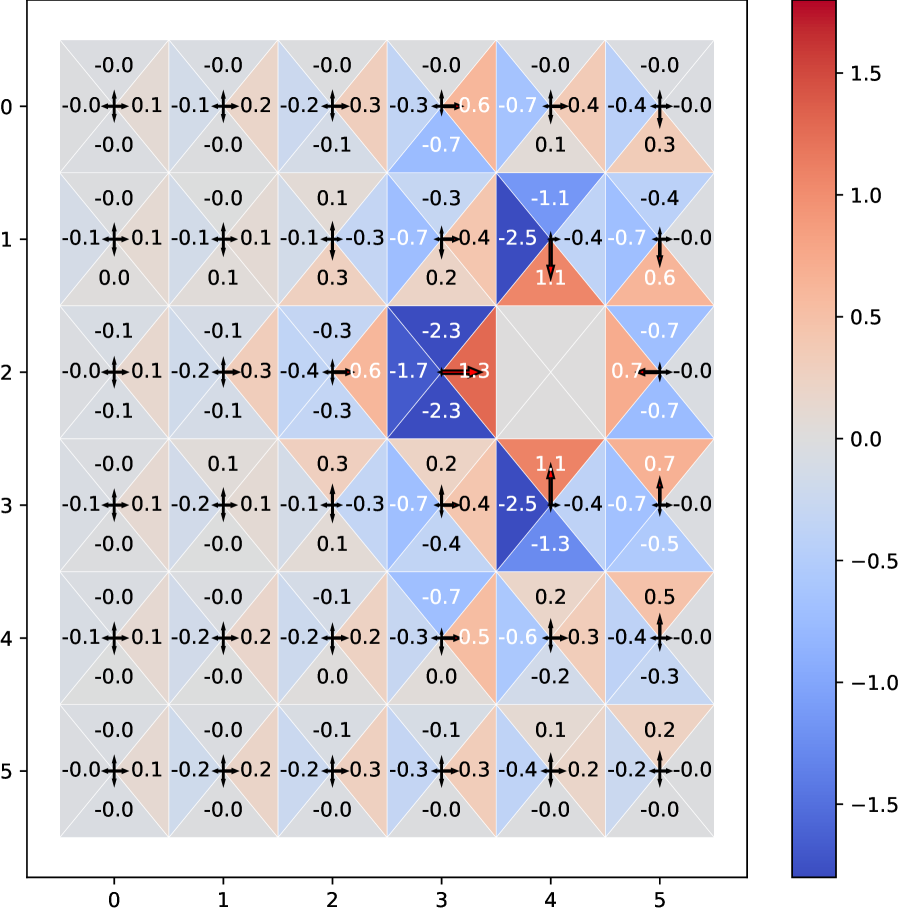

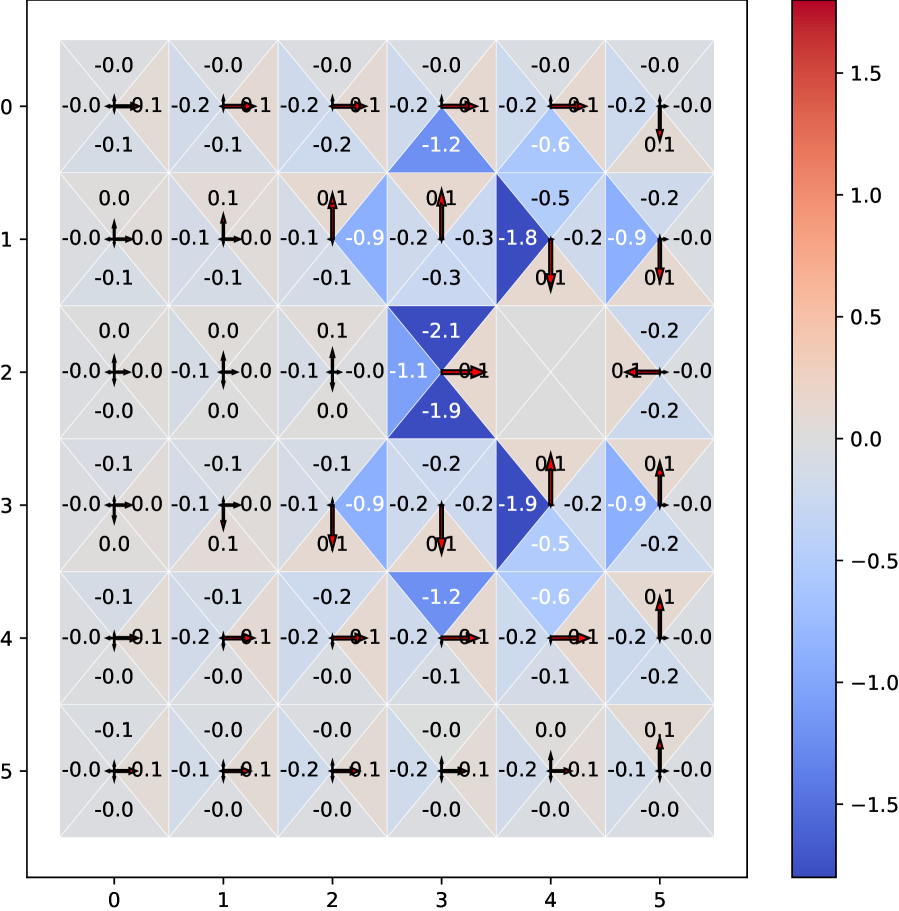

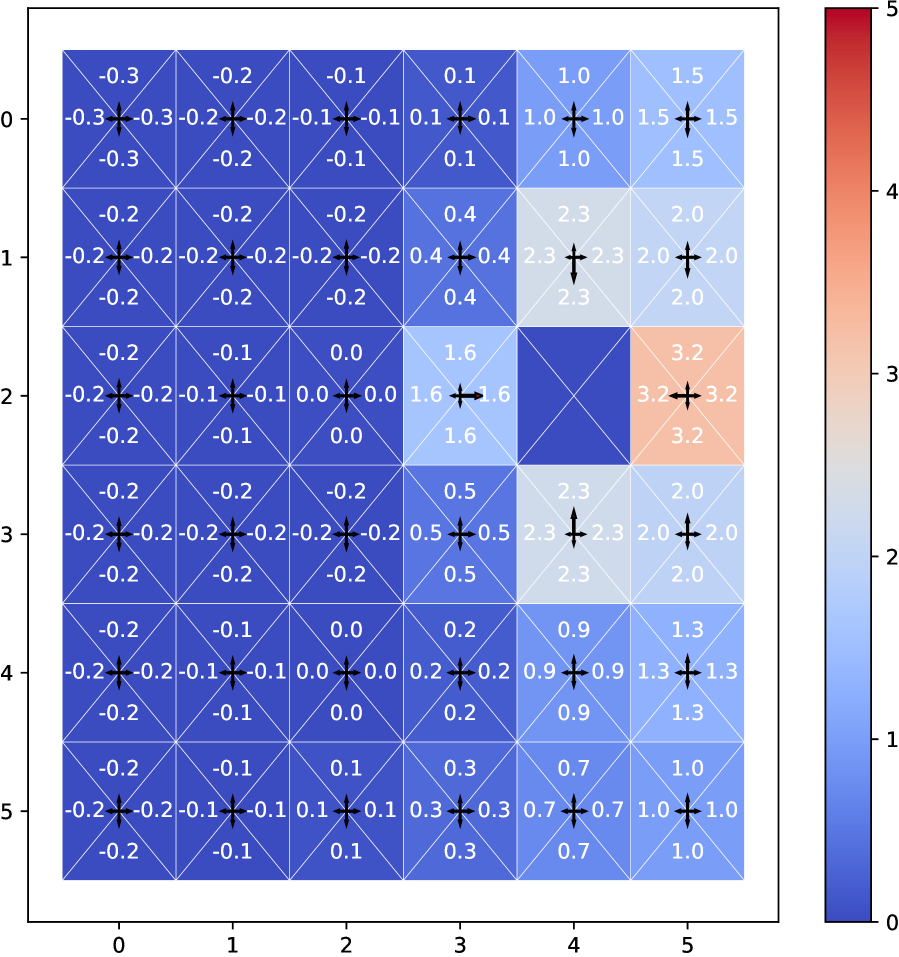

In Fig. 4(a), we consider a grid world where the agent receives for picking up the reward pill, for stepping in water, and zero reward otherwise. We train an agent using tabular -learning and a discount factor . We visualize the worst-case reward perturbations in each state-action pair for policies trained with various regularization strengths in Fig. 4(b)-(d). While it is well-known that there exists a unique optimal policy for a given regularized mdp, our results additionally display the adversarial strategies and resulting Nash equilibria which can be associated with a regularization scheme specified by , , , and in a given mdp.

Each policy implicitly hedges against an adversary that perturbs the rewards according to the values and colormap shown. For example, inspecting the state to the left of the goal state in panel Fig. 4(b)-(c), we see that the adversary reduces the immediate reward for moving right (in red, ). Simultaneously, the adversary raises the reward for moving up or down towards the water (in blue). This is in line with the constraints on the feasible set, which imply that the adversary must balance reward decreases with reward increases in each state. In App. E.4 Fig. 7, we certify the optimality of each policy using the path consistency conditions, which also confirms that the adversarial perturbations have rendered the agent indifferent across actions in each state.

Although we observe that the agent with high regularization in Fig. 4(b) is robust to a strong adversary, the value of the regularized objective is also lower in this case. As expected, lower regularization strength reduces robustness to negative reward perturbations. With low regularization in Fig. 4(d), the behavior of the agent barely deviates from the deterministic policy in the face of the weaker adversary.

(uniform ,

for water,

for goal)

5 Discussion

Our analysis in Sec. 3 unifies and extends several previous works analyzing the reward robustness of regularized policies (Ortega & Lee, 2014; Eysenbach & Levine, 2021; Husain et al., 2021), as summarized in Table 1. We highlight differences in the analysis of entropy-regularized policies in Sec. 5.1, and provide additional discussion of the closely-related work of Derman et al. (2021) in Sec. 5.2.

5.1 Comparison with Entropy Regularization

As argued in Sec. 3, the worst-case reward perturbations preserve the value of the regularized objective function. Thus, we should expect our robustness conclusions to depend on the exact form of the regularizer.

When regularizing with the Tsallis or Shannon () entropy, the worst-case reward perturbations become

| (29) |

See App. F.2, we also show that for , these perturbations cannot decrease the reward, with and . In the rest of this section, we argue that this property leads to several unsatisfying conclusions in previous work (Lee et al., 2019; Eysenbach & Levine, 2021), which are resolved by using the kl and -divergence for analysis instead of the corresponding entropic quantities.333Entropy regularization corresponds to divergence regularization with the uniform reference distribution .

First, this means that a Shannon entropy-regularized policy is only ‘robust’ to increases in the reward function. However, for useful generalization, we might hope that a policy still performs well when the reward function decreases in at least some states. Including the reference distribution via divergence regularization resolves this issue, and we observe in Fig. 2 and Fig. 4 that the adversary chooses reward decreases in some actions and increases in others. For example, for the kl divergence, implies robustness to reward decreases when or .

Similarly, Lee et al. (2019) note that for any ,

where and the Tsallis entropy equals the Shannon entropy for . This soft value aggregation yields a result that is larger than any particular -value. By contrast, for the -divergence, we show in App. F.3 that for fixed and ,

| (30) |

This provides a more natural interpretation of the Bellman optimality operator as a soft maximum operation. As a function of , we see in App. C.4 and F.3 that the conjugate ranges between .

Finally, using entropy instead of divergence regularization also affects interpretations of the feasible set. Eysenbach & Levine (2021) consider the same constraint as in Eq. 19, but without the reference

| (31) |

This constraint suggests that the original reward function () is not feasible for the adversary. More surprisingly, Eysenbach & Levine (2021) App. A8 argues that increasing regularization strength (with lower ) may lead to less robust policies based on the constraint in Eq. 31. In App. F.4, we discuss how including in the constraint via divergence regularization (Prop. 1) avoids this conclusion. As expected, Fig. 2 shows that increasing regularization strength leads to more robust policies.

5.2 Related Algorithms

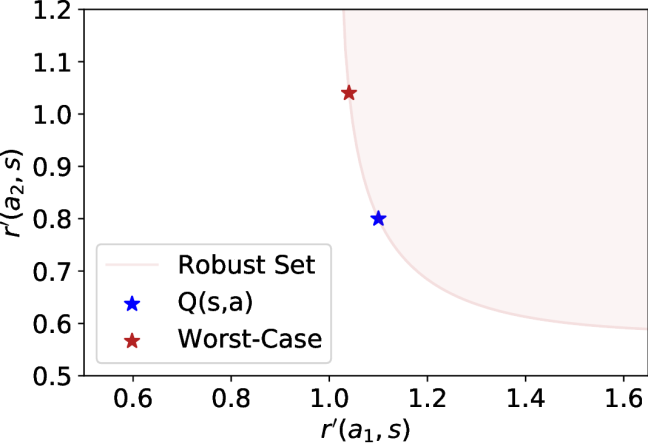

Several recent works provide algorithmic insights which build upon convex duality and complement or extend our analysis. Derman et al. (2021) derive practical iterative algorithms based on a general equivalence between robustness and regularization, which can be used to enforce robustness to both reward perturbations (through policy regularization) and changes in environment dynamics (through value regularization). For policy regularization, Derman et al. (2021) translate the specification of a desired robust set into a regularizer using the convex conjugate of the set indicator function. In particular, Derman et al. (2021) associate kl divergence or (scaled) Tsallis entropy policy regularization with the robust set . Our analysis proceeds in the opposite direction, from regularization to robustness, using the conjugate of the divergence. While the worst-case perturbations result in the same modified objective, our approach yields a larger robust set with qualitatively different shape (see Fig. 1).

Zahavy et al. (2021) analyze a general ‘meta-algorithm’ which alternates between updates of the occupancy measure and modified reward in online fashion. This approach highlights the fact that the modified reward or worst-case perturbations change as the policy or occupancy measure is optimized. The results of Zahavy et al. (2021) and Husain et al. (2021) hold for general convex mdp s, which encompass common exploration and imitation learning objectives beyond the policy regularization setting we consider.

As discussed in Sec. 3.4, path consistency conditions have been used to derive practical learning objectives in (Nachum et al., 2017; Chow et al., 2018). These algorithms might be extended to general -divergence regularization via Eq. 28, which involves an arbitrary reference policy that can be learned adaptively as in (Teh et al., 2017; Grau-Moya et al., 2018).

Finally, previous work has used dual optimizations similar to Eq. 14 to derive alternative Bellman error losses (Dai et al., 2018; Belousov & Peters, 2019; Nachum & Dai, 2020; Bas-Serrano et al., 2021), highlighting how convex duality can be used to bridge between policy regularization and Bellman error aggregation (Belousov & Peters, 2019; Husain et al., 2021).

6 Conclusion

In this work, we analyzed the robustness of convex-regularized rl policies to worst-case perturbations of the reward function, which implies generalization to adversarially chosen reward functions from within a particular robust set. We have characterized this robust set of reward functions for kl and -divergence regularization, provided a unified discussion of existing works on reward robustness, and clarified apparent differences in robustness arising from entropy versus divergence regularization. Our advantage function interpretation of the worst-case reward perturbations provides a complementary perspective on how -values appear as dual variables in convex programming forms of regularized mdp s. Compared to a deterministic, unregularized policy, a stochastic, regularized policy places probability mass on a wider set of actions and requires state-action value adjustments via the advantage function or adversarial reward perturbations. Conversely, a regularized agent, acting based on given -value estimates, implicitly hedges against the anticipated perturbations of an appropriate adversary.

References

- Ahmed et al. (2019) Zafarali Ahmed, Nicolas Le Roux, Mohammad Norouzi, and Dale Schuurmans. Understanding the impact of entropy on policy optimization. In International Conference on Machine Learning. PMLR, 2019.

- Amari (2016) Shun-ichi Amari. Information geometry and its applications, volume 194. Springer, 2016.

- Arora & Doshi (2021) Saurabh Arora and Prashant Doshi. A survey of inverse reinforcement learning: Challenges, methods and progress. Artificial Intelligence, 297:103500, 2021.

- Banerjee et al. (2005) Arindam Banerjee, Srujana Merugu, Inderjit S Dhillon, Joydeep Ghosh, and John Lafferty. Clustering with bregman divergences. Journal of machine learning research, 6(10), 2005.

- Bas-Serrano et al. (2021) Joan Bas-Serrano, Sebastian Curi, Andreas Krause, and Gergely Neu. Logistic q-learning. In International Conference on Artificial Intelligence and Statistics, pp. 3610–3618. PMLR, 2021.

- Bellman (1957) Richard Bellman. A markovian decision process. Journal of mathematics and mechanics, 6(5):679–684, 1957.

- Belousov (2017) Boris Belousov. Bregman divergence of alpha-divergence. Blog post, 2017. URL http://www.boris-belousov.net/2017/04/16/bregman-divergence/.

- Belousov & Peters (2019) Boris Belousov and Jan Peters. Entropic regularization of markov decision processes. Entropy, 21(7), 2019.

- Boyd & Vandenberghe (2004) Stephen Boyd and Lieven Vandenberghe. Convex optimization. Cambridge university press, 2004.

- Chow et al. (2018) Yinlam Chow, Ofir Nachum, and Mohammad Ghavamzadeh. Path consistency learning in tsallis entropy regularized mdps. In International Conference on Machine Learning, pp. 979–988. PMLR, 2018.

- Christiano et al. (2017) Paul F Christiano, Jan Leike, Tom Brown, Miljan Martic, Shane Legg, and Dario Amodei. Deep reinforcement learning from human preferences. Advances in neural information processing systems, 30, 2017.

- Cichocki & Amari (2010) Andrzej Cichocki and Shun-ichi Amari. Families of alpha-beta-and gamma-divergences: Flexible and robust measures of similarities. Entropy, 12(6):1532–1568, 2010.

- Dai et al. (2018) Bo Dai, Albert Shaw, Lihong Li, Lin Xiao, Niao He, Zhen Liu, Jianshu Chen, and Le Song. Sbeed: Convergent reinforcement learning with nonlinear function approximation. In International Conference on Machine Learning, pp. 1125–1134. PMLR, 2018.

- Derman et al. (2021) Esther Derman, Matthieu Geist, and Shie Mannor. Twice regularized mdps and the equivalence between robustness and regularization. In Thirty-Fifth Conference on Neural Information Processing Systems, 2021.

- Diamond & Boyd (2016) Steven Diamond and Stephen Boyd. CVXPY: A Python-embedded modeling language for convex optimization. Journal of Machine Learning Research, 17(83):1–5, 2016.

- Eysenbach & Levine (2021) Benjamin Eysenbach and Sergey Levine. Maximum entropy RL (provably) solves some robust RL problems. In International Conference on Learning Representations, 2021.

- Feinberg & Shwartz (2012) Eugene A Feinberg and Adam Shwartz. Handbook of Markov decision processes: methods and applications, volume 40. Springer Science & Business Media, 2012.

- Fishburn (1988) Peter C Fishburn. Nonlinear preference and utility theory. Number 5. Johns Hopkins University Press, 1988.

- Fox et al. (2016) Roy Fox, Ari Pakman, and Naftali Tishby. Taming the noise in reinforcement learning via soft updates. In Proceedings of the Thirty-Second Conference on Uncertainty in Artificial Intelligence, pp. 202–211, 2016.

- Geist et al. (2019) Matthieu Geist, Bruno Scherrer, and Olivier Pietquin. A theory of regularized markov decision processes. In ICML 2019-Thirty-sixth International Conference on Machine Learning, 2019.

- Grau-Moya et al. (2018) Jordi Grau-Moya, Felix Leibfried, and Peter Vrancx. Soft q-learning with mutual-information regularization. In International Conference on Learning Representations, 2018.

- Haarnoja et al. (2017) Tuomas Haarnoja, Haoran Tang, Pieter Abbeel, and Sergey Levine. Reinforcement learning with deep energy-based policies. In Proceedings of the 34th International Conference on Machine Learning, volume 70 of Proceedings of Machine Learning Research, pp. 1352–1361. PMLR, 06–11 Aug 2017.

- Haarnoja et al. (2018) Tuomas Haarnoja, Aurick Zhou, Pieter Abbeel, and Sergey Levine. Soft actor-critic: Off-policy maximum entropy deep reinforcement learning with a stochastic actor. In International Conference on Machine Learning, pp. 1861–1870. PMLR, 2018.

- Husain et al. (2021) Hisham Husain, Kamil Ciosek, and Ryota Tomioka. Regularized policies are reward robust. International Conference on Artificial Intelligence and Statistics, 2021.

- Igl et al. (2020) Maximilian Igl, Andrew Gambardella, Jinke He, Nantas Nardelli, N Siddharth, Wendelin Böhmer, and Shimon Whiteson. Multitask soft option learning. In Conference on Uncertainty in Artificial Intelligence, pp. 969–978, 2020.

- Kappen et al. (2012) Hilbert J Kappen, Vicenç Gómez, and Manfred Opper. Optimal control as a graphical model inference problem. Machine learning, 87(2):159–182, 2012.

- Lee et al. (2018) Kyungjae Lee, Sungjoon Choi, and Songhwai Oh. Sparse markov decision processes with causal sparse tsallis entropy regularization for reinforcement learning. IEEE Robotics and Automation Letters, 3(3):1466–1473, 2018.

- Lee et al. (2019) Kyungjae Lee, Sungyub Kim, Sungbin Lim, Sungjoon Choi, and Songhwai Oh. Tsallis reinforcement learning: A unified framework for maximum entropy reinforcement learning. arXiv preprint arXiv:1902.00137, 2019.

- Levine (2018) Sergey Levine. Reinforcement learning and control as probabilistic inference: Tutorial and review. arXiv preprint arXiv:1805.00909, 2018.

- Levine et al. (2020) Sergey Levine, Aviral Kumar, George Tucker, and Justin Fu. Offline reinforcement learning: Tutorial, review, and perspectives on open problems. arXiv preprint arXiv:2005.01643, 2020.

- Nachum & Dai (2020) Ofir Nachum and Bo Dai. Reinforcement learning via fenchel-rockafellar duality. arXiv preprint arXiv:2001.01866, 2020.

- Nachum et al. (2017) Ofir Nachum, Mohammad Norouzi, Kelvin Xu, and Dale Schuurmans. Bridging the gap between value and policy based reinforcement learning. arXiv preprint arXiv:1702.08892, 2017.

- Nachum et al. (2019a) Ofir Nachum, Yinlam Chow, Bo Dai, and Lihong Li. Dualdice: Behavior-agnostic estimation of discounted stationary distribution corrections. Reinforcement Learning for Real Life Workshop (ICML), 2019a.

- Nachum et al. (2019b) Ofir Nachum, Bo Dai, Ilya Kostrikov, Yinlam Chow, Lihong Li, and Dale Schuurmans. Algaedice: Policy gradient from arbitrary experience. arXiv preprint arXiv:1912.02074, 2019b.

- Naudts (2011) Jan Naudts. Generalised thermostatistics. Springer Science & Business Media, 2011.

- Neu et al. (2017) Gergely Neu, Anders Jonsson, and Vicenç Gómez. A unified view of entropy-regularized markov decision processes. arXiv preprint arXiv:1705.07798, 2017.

- Ng et al. (2000) Andrew Y Ng, Stuart J Russell, et al. Algorithms for inverse reinforcement learning. In International Conference on Machine Learning, 2000.

- Ortega & Lee (2014) Pedro Ortega and Daniel Lee. An adversarial interpretation of information-theoretic bounded rationality. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 28, 2014.

- Ortega & Braun (2013) Pedro A Ortega and Daniel A Braun. Thermodynamics as a theory of decision-making with information-processing costs. Proceedings of the Royal Society A: Mathematical, Physical and Engineering Sciences, 469(2153), 2013.

- Osborne & Rubinstein (1994) Martin J Osborne and Ariel Rubinstein. A course in game theory. 1994.

- Peters et al. (2010) Jan Peters, Katharina Mulling, and Yasemin Altun. Relative entropy policy search. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 24, 2010.

- Puterman (1994) Martin L Puterman. Markov Decision Processes: Discrete Stochastic Dynamic Programming. John Wiley & Sons, Inc., 1994.

- Puterman & Shin (1978) Martin L Puterman and Moon Chirl Shin. Modified policy iteration algorithms for discounted markov decision problems. Management Science, 24(11), 1978.

- Rawlik et al. (2013) Konrad Rawlik, Marc Toussaint, and Sethu Vijayakumar. On stochastic optimal control and reinforcement learning by approximate inference. In International Joint Conference on Artificial Intelligence, 2013.

- Scherrer et al. (2015) Bruno Scherrer, Mohammad Ghavamzadeh, Victor Gabillon, Boris Lesner, and Matthieu Geist. Approximate modified policy iteration and its application to the game of tetris. Journal of Machine Learning Research, 16(49):1629–1676, 2015.

- Schulman et al. (2015) John Schulman, Sergey Levine, Pieter Abbeel, Michael Jordan, and Philipp Moritz. Trust region policy optimization. In International conference on machine learning, pp. 1889–1897. PMLR, 2015.

- Schulman et al. (2017) John Schulman, Filip Wolski, Prafulla Dhariwal, Alec Radford, and Oleg Klimov. Proximal policy optimization algorithms. arXiv e-prints, pp. arXiv–1707, 2017.

- Syed et al. (2008) Umar Syed, Michael Bowling, and Robert E Schapire. Apprenticeship learning using linear programming. In Proceedings of the 25th international conference on Machine learning, pp. 1032–1039, 2008.

- Teh et al. (2017) Yee Whye Teh, Victor Bapst, Wojciech Marian Czarnecki, John Quan, James Kirkpatrick, Raia Hadsell, Nicolas Heess, and Razvan Pascanu. Distral: robust multitask reinforcement learning. In Proceedings of the 31st International Conference on Neural Information Processing Systems, pp. 4499–4509, 2017.

- Tsallis (2009) Constantino Tsallis. Introduction to nonextensive statistical mechanics: approaching a complex world. Springer Science & Business Media, 2009.

- Wang et al. (2021) Ziyi Wang, Oswin So, Jason Gibson, Bogdan Vlahov, Manan S Gandhi, Guan-Horng Liu, and Evangelos A Theodorou. Variational inference mpc using tsallis divergence. arXiv preprint arXiv:2104.00241, 2021.

- Zahavy et al. (2021) Tom Zahavy, Brendan O’Donoghue, Guillaume Desjardins, and Satinder Singh. Reward is enough for convex mdps. Advances in Neural Information Processing Systems, 2021.

- Zhu & Rohwer (1995) Huaiyu Zhu and Richard Rohwer. Information geometric measurements of generalisation. Technical report, Aston University, 1995.

Appendix

Appendix A Implications of Conjugate Duality Optimality Conditions

In this section, we show several closely-related results which are derived from the conjugate optimality conditions. We provide additional commentary in later Appendix sections which more closely follow the sequence of the main text.

First, recall from Section 2.1 the definition of the conjugate optimizations for functions over . We restrict to be a nonnegative function over , so that

| (32) |

and the implied optimality conditions are

| (33) |

A.1 Proof of Prop. 2 : Policy Form Worst-Case Reward Perturbations

See 2

Proof.

A.2 Optimal Policy in a Regularized MDP

In Lemma 1 below, we show that the Bellman flow constraints Eq. 10, which are enforced by the optimal Lagrange multipliers , ensure that the optimal is normalized. This suggests that an explicit normalization constraint is not required. In Prop. 4, we then proceed to derive the optimal policy in a regularized mdp using the conjugate optimality conditions in Eq. 33.

Lemma 1 (Flow Constraints Ensure Normalization).

Assume that the initial state distribution and transition dynamics are normalized, with and . If a state-occupancy measure satisfies the Bellman flow constraints , then it is a normalized distribution .

Proof.

Starting from the Bellman flow constraints , we consider taking the summation over states ,

where uses the normalization assumption on and the distributive law, and uses the normalization assumption on . Finally, we rearrange the first and last equality to obtain

| (34) |

which shows that is normalized as a joint distribution over , as desired. ∎

Proposition 4 (Optimal Policy in Regularized MDP).

Given the optimal value function and Lagrange multipliers , the optimal policy in the regularized mdp is given by

This matches the conjugate conditions in Eq. 33 using the arguments .

Proof.

In Sec. 2.4, we moved from the regularized primal optimization (Eq. 12) to the dual optimization (Eq. 14) via the regularized Lagrangian

Note that the Lagrange multipliers enforce while enforces the flow constraints and thus, by Lemma 1, normalization of . We recognized the final two terms as a conjugate optimization

| (35) |

to yield a dual optimization over and only in Eq. 14. After solving the dual optimization for the optimal , , we can recover the optimal policy in the mdp using the optimizing argument of Eq. 35. Differentiating Eq. 35 and solving for yields which we invert to obtain Prop. 4. The other equality follows from the conjugate optimality conditions in Eq. 33. ∎

For -divergence regularization, the optimal policy or state-action occupancy is given by the ‘optimizing argument’ column of Table 2, up to reparameterization of as the dual variable. In this case, note that the argument to the conjugate function accounts for the flow and nonnegativity constraints via and . In particular, we have

| Policy Reg., App. B.3 Eq. 63 | |||

| (36) | |||

| Occupancy Reg., App. B.4 Eq. 68 | |||

| (37) |

where appears from differentiating as in Eq. 23 or App. B.3. This means that the optimal policy is only available in self-consistent fashion, with the normalization constant inside the , which can complicate practical applications (Lee et al., 2019; Chow et al., 2018).

A.3 Proof of Prop. 3: Policy Form Worst-Case Perturbations match Value Form at Optimality

The substitution above already anticipates the result in Prop. 3, which links the reward perturbations for the optimal policy or state-action occupancy to the advantage function. See the proof of Thm. 1 in App. E.1 for additional context in relation to the value-form reward perturbations .

See 3

A.4 Path Consistency and KKT Conditions

A.5 Modified Rewards and Duality Gap for Suboptimal Policies

We can also use the conjugate duality of state-action occupancy measures and reward functions ( or ) to express the optimality gap for a suboptimal . Consider the regularized primal objective as a (constrained) conjugate optimization,

| (40) | ||||

| (41) |

where the inequality follows from the fact that any feasible provides a lower bound on the objective. We use the notation to anticipate the fact that, assuming appropriate domain considerations, we would like to associate this occupancy measure with a modified reward function using the conjugate optimality conditions in Eq. 33 (with as the dual variable). In particular, for a given , we use the fact that to recognize the conjugate duality gap as a Bregman divergence. Rearranging Eq. 41,

| (42) | ||||

| (43) | ||||

| (44) | ||||

| (45) |

where the last line follows from the definition of the Bregman divergence (Amari, 2016). For example, using the kl divergence , one can confirm that the Bregman divergence generated by is also a kl divergence, (Belousov, 2017; Banerjee et al., 2005).

Appendix B Convex Conjugate Derivations

In this section, we derive the convex conjugate associated with kl and -divergence regularization of the policy or state-action occupancy . We summarize these results in Table 2, with equation references in Table 3. In both cases, we treat the regularizer as a function of and optimize over all states jointly,

| (46) |

These conjugate derivations can be used to reason about the optimal policy via , as argued in App. A.2, or the worst case reward perturbations using . We use as the argument or dual variable throughout this section.

In App. C, we derive alternative conjugate functions which optimize over the policy in each state, where is constrained to be a normalized probability distribution. This conjugate arises in considering soft value aggregation or regularized iterative algorithms as in Sec. 2.4. See Table 4 for equation references.

B.1 KL Divergence Policy Regularization:

The conjugate function for kl divergence from the policy to a reference has the following closed form

| (47) |

Proof.

Worst-Case Reward Perturbations

Optimizing Argument

Conjugate Function

We plug this back into the conjugate optimization Eq. 48, with . Assuming is normalized, we also have and

| (52) |

as desired. Note that the form of the conjugate function also depends on the regularization strength .

Finally, we verify that our other conjugate optimality condition , or holds for this conjugate function. Indeed, differentiating with respect to above, we see that matches via Eq. 51. ∎ Although our regularization applies at each , we saw that performing the conjugate optimization over led to an expression for a policy that is normalized by construction . Conversely, for a given normalized , the above conjugate conditions yield such that Eq. 51 is also normalized.

B.2 KL Divergence Occupancy Regularization:

Nearly identical derivations as App. B.1 apply when regularizing the divergence between the joint state-action occupancy and a reference . This leads to the following results

| Worst-Case Perturbations: | (53) | ||||

| Optimizing Argument: | (54) | ||||

| Conjugate Function: | (55) |

Such regularization schemes appear in reps (Peters et al., 2010), while Bas-Serrano et al. (2021) consider both policy and occupancy regularization.

B.3 -Divergence Policy Regularization:

The conjugate for -divergence regularization of the policy to a reference takes the form

| (56) |

where is a normalization constant for the optimizing argument corresponding to .

We provide explicit derivations of the conjugate function instead of leveraging -divergence duality (Belousov & Peters, 2019; Nachum & Dai, 2020) in order to account for the effect of optimization over the joint distribution . We will see in App. C.2 see that the conjugate in Eq. 56 takes a similar to form as the conjugate with restriction to normalized , where this constraint is not captured using -divergence function space duality.

Proof.

We begin by writing the -divergence as a function of the occupancy measure , with . As in Prop. 2, the conjugate optimization implies an optimality condition for .

| (57) | ||||

| (58) |

Worst-Case Reward Perturbations

We now differentiate with respect to , using similar derivations as in Lee et al. (2019). While we have already written Eq. 58 using , we again emphasize that depends on . Differentiating, we obtain

| (59) | ||||

| (60) |

where we have rewritten in terms of the policy and assumed is normalized.

Letting indicate the policy which is in dual correspondence with , we would eventually like to invert the equality in Eq. 60 to solve for in each . However, the final term depends on a sum over all actions. To handle this, we define

| (61) |

Since is normalized by construction, the constant with respect to actions has appeared naturally when optimizing with respect to . In App. C.2-C.3, we will relate this quantity to the Lagrange multiplier used to enforce normalization when optimizing over .

Finally, we use Eq. 60 to write as

| (62) |

Optimizing Argument

Solving for the policy in Eq. 62 and denoting this as ,

| (63) |

Note that is defined in self-consistent fashion due to the dependence of on in Eq. 61. Further, does not appear as a divisive normalization constant for general , which is inconvenient for practical applications (Lee et al., 2019; Chow et al., 2018).

Conjugate Function

Finally, we plug this into the conjugate optimization Eq. 57. Although we eventually need to obtain a function of only, we write in initial steps to simplify notation.

| (64) | ||||

where in we note that . In , we add and subtract the term in blue, which will allow to factorize an additional term of and obtain a function of only

| (65) |

where in we have used Eq. 63 and , along with . ∎

Confirming Conjugate Optimality Conditions

B.4 -Divergence Occupancy Regularization:

The conjugate function for -divergence regularization of the state-action occupancy to a reference can be written in the following form

| (66) |

Note that this conjugate function can also be derived directly from the duality of general -divergences, and matches the form of conjugate considered in (Belousov & Peters, 2019; Nachum & Dai, 2020).

Proof.

Worst-Case Reward Perturbations

| (67) | ||||

Optimizing Argument . Solving for ,

| (68) |

Conjugate Function . Plugging this back into the conjugate optimization, we finally obtain

| (69) | ||||

| (70) | ||||

| (71) |

where, to obtain the exponent in the last line, note that . ∎

Appendix C Soft Value Aggregation

Soft value aggregation (Fox et al., 2016; Haarnoja et al., 2017) and the regularized Bellman optimality operator (Neu et al., 2017; Geist et al., 2019) also rely on the convex conjugate function, but with a slightly different setting than our derivations for the optimal regularized policy or reward perturbations in App. B. In particular, in each state we optimize over the policy using an explicit normalization constraint (Eq. 74).

We derive the regularized Bellman optimality operator from the primal objective in Eq. 12. Factorizing , we can imagine optimizing over and separately,

| (72) |

Eliminating (by setting ) leads to a constraint on the form of , since both may be viewed as enforcing the Bellman flow constraints.

| (73) |

We define and write moving forward.

As an operator for iteratively updating , Eq. 73 corresponds to the regularized Bellman operator and may be used to perform policy evaluation for a given (Geist et al., 2019). The regularized Bellman optimality operator , which can be used for value iteration or modified policy iteration (Geist et al., 2019), arises from including the maximization over from Eq. 72

| (74) |

Comparison of Conjugate Optimizations

Eq. 74 has the form of a conjugate optimization (Geist et al., 2019). However, in contrast to the setting of App. A.2 and App. B, we optimize over the policy in each state, rather than the state-action occupancy . Further, we must include normalization and nonnegativity constraints , which can be enforced using Lagrange multipliers and . We derive expressions for this conjugate function for the kl divergence in App. C.1 and -divergence in App. C.2, and plot the value as a function of and in App. C.4.

C.1 KL Divergence Soft Value Aggregation:

We proceed to derive a closed form for the conjugate function of the kl divergence as a function of , which we write using the -values as input

| (75) |

Optimizing Argument

Solving for yields the optimizing argument

| (76) |

where we can ignore the Lagrange multiplier for the nonnegativity constraint since ensures We can pull the normalization constant out of the exponent to solve for

| (77) |

Plugging Eq. 76 into the conjugate optimization,

Conjugate Function

We finally recover the familiar log-mean-exp form for the kl-regularized value function

| (78) |

Notice that the conjugate or value function is exactly equal to the normalization constant of the policy . We will show in App. C.2 that this property does not hold for general -divergences, with example visualizations in App. C.3 Fig. C.3.

C.2 -Divergence Soft Value Aggregation:

We now consider soft value aggregation using the -divergence, where in contrast to App. B.3, we perform the conjugate optimization over in each state, with Lagrange multipliers and to enforce normalization and nonnegativity.

| (79) | ||||

| (80) |

Optimizing Argument

Solving for yields the optimizing argument for the soft value aggregation conjugate,

| (81) |

Unlike the case of the standard exponential, we cannot easily derive a closed-form solution for .

Note that the expressions in Eq. 80 and Eq. 81 are similar to the form of the worst-case reward perturbations in Eq. 62 and optimizing policy in Eq. 63, except for the fact that arises as a Lagrange multiplier and does not have the same form as as in Eq. 23 and Eq. 61. We will find that and differ by a term of in App. C.3 (Eq. 86).

Conjugate Function

Plugging Eq. 81 into the conjugate optimization, we use similar derivations as in Eq. 64-Eq. 65 to write the conjugate function, or regularized Bellman optimality operator as

| (82) | ||||

Comparison with KL Divergence Regularization Note that for general , the conjugate or value function in Eq. 82 is not equal to the normalization constant of the policy . We discuss this further in the next section.

We also note that the form of the conjugate function is similar using two different approaches: optimizing over with an explicit normalization constraint, as in Eq. 82, or optimizing over with regularization of but no explicit normalization constraint, as in App. B.3 or Table 2. This is in contrast to the kl divergence, where the normalization constraint led to a log-mean-exp conjugate in Eq. 75 which is different from App. B Eq. 47.

C.3 Relationship between Normalization Constants , , and Value Function

In this section, we analyze the relationship between the conjugate optimizations that we have considered above, either optimizing over as in deriving the optimal policy, or optimizing over as in the regularized Bellman optimality operator or soft-value aggregation. Using ,

| Optimal Policy (or Worst-Case Reward Perturbations) (App. B.3) | (83) | ||

| (84) | |||

Note that the arguments differ by a term of . We ignore the apparent difference in the term, which can be considered as an argument of the conjugate in Eq. 84 since a linear term of appears when enforcing . Evaluating the optimizing arguments,

| Optimal Policy (or Worst-Case Reward Perturbations) (App. B.3, Eq. 63, Table 2) | ||||

| (85) | ||||

For the optimal and , the two policies match. This can be confirmed using similar reasoning as in Lee et al. (2019) App. D-E or (Geist et al., 2019) to show that iterating the regularized Bellman optimality operator leads to the optimal policy and value.

Relationship between and

This implies the condition which is the main result of this section.

| (86) |

In Fig. C.3 we empirically confirm this identity and inspect how each quantity varies with and (App. C.4)444 Note that appears from differentiating with respect to (App. B.3 Eq. 61). We also write this as for normalized and .

Eq. 86 highlights distinct roles for the value function and the Lagrange multiplier enforcing normalization of in soft-value aggregation ( Eq. 79 or Eq. 84). It is well known that these coincide in the case of kl divergence regularization, with as in App. C.1. We can also confirm that vanishes for kl regularization () and normalized and the normalized optimal policy .

However, in the case of -divergence regularization, optimization over the joint in Eq. 83 introduces the additional term , which is not equal to 0 in general.

Relationship between Conjugate Functions

We might also like to compare the value of the conjugate functions in Eq. 83 and Eq. 84, in particular to understand how including as an argument and optimizing over versus affect the optima. We write the expressions for the conjugate function in each case, highlighting the terms from Eq. 86 in blue.

| Optimal Policy (or Worst-Case Reward Perturbations) (App. B.3, Eq. 56, Table 2) | |||

| (87) | |||

| (88) | |||

Note that we have rewritten directly as . To further simplify, note that the optimal policy matches as in Eq. 85, with

Since , we can write terms of the form in Eq. 87-(88) as , where the exponents of add to 1. Finally, we use this expression to simplify the value function expression in Eq. 88, eventually recovering the equality in Eq. 86

| (89) | ||||

| (90) |

In the second line, we use the fact that from Eq. 61. We can use the same identity to show that the conjugate in Eq. 87 evaluates to zero,

| (91) |

In Lemma 2, we provide a more detailed proof and show that this identity also holds for suboptimal policies and their worst-case reward perturbations, , where Eq. 91 is a special case for .

Finally, note that the condition in Eq. 91 implies that for the optimal , the regularized dual objective in Eq. 14 reduces to the value function averaged over initial states, . This is intuitive since measures the regularized objective attained from running the optimal policy for infinite time in the discounted mdp.

C.4 Plotting Value Function as a Function of Regularization Parameters

Confirming Relationship between Normalization , and Value Function

In Fig. C.3, we plot both and for various values of (x-axis) and (in each panel). We also plot in the third row, and confirm the identity in Eq. 86 in the fourth row.

Value as a Function of ,

In Fig. 6, we visualize the optimal value function , for kl or -divergence regularization and different choices of regularization strength . The choice of divergence particularly affects the aggregated value at low regularization strength, although we do not observe a clear pattern with respect to .555See Belousov & Peters (2019); Lee et al. (2018; 2019), or Section C.4 for additional discussion of the effect of -divergence regularization on learned policies. In all cases, the value function ranges between for an unregularized deterministic policy as , and the expectation under the reference policy for strong regularization as . We also discuss this property in Sec. 5.1.

Appendix D Robust Set of Perturbed Rewards

In this section, we characterize the robust set of perturbed rewards to which a given policy or is robust, which also provides performance guarantees as in Eq. 2 and also describes the set of strategies available to the adversary. For proving Prop. 1, we focus our discussion on policy regularization with kl or -divergence regularization and compare with state-occupancy regularization in App. D.2.

D.1 Proof of Prop. 1: Robust Set of Perturbed Rewards for Policy Regularization

We begin by stating two lemmas, which we will use to characterize the robust set of perturbed rewards. All proofs are organized under paragraph headers below the statement of Prop. 1.

Lemma 2.

For the worst-case reward perturbation associated with a given, normalized policy and - or kl-divergence regularization, the conjugate function evaluates to zero,

| (92) |

Lemma 3.

The conjugate function is increasing in . In other words, if for all , then

See 1

Proof.

Recall the adversarial optimization in Eq. 17 for a fixed

| (93) |

which we would like to transform into a constrained optimization. From Lemma 2, we know that for the optimizing argument in Eq. 93, but it is not clear whether this should appear as an equality or inequality constraint. We now show that the constraint changes the value of the objective, whereas the constraint does not change the value of the optimization.

Inequality First, consider the optimization subject to . From the optimizing argument , consider an increase in the reward perturbations where s.t. and . By Lemma 3, we have . However, the objective now satisfies for fixed , which is a contradiction since provides a global minimum of the convex objective in Eq. 93.

Inequality We would like to show that this constraint does not introduce a different global minimum of Eq. 93. Assume there exists with and for the occupancy measure associated with the given policy . By convexity of , we know that a first-order Taylor approximation around everywhere underestimates the function, . Noting that by the conjugate optimality conditions (Eq. 5, App. A), we have . This now introduces a contradiction, since we have assumed both that , and that provides a global minimum, where implies Thus, including the inequality constraint cannot introduce different minima.

This constraint is consistent with the constrained optimization and generalization guarantee in Eq. 1-(2), where it is clear that increasing the modified reward away from the boundary of the robust set (i.e. decreasing and ) is feasible for the adversary and preserves our performance guarantee. See Eysenbach & Levine (2021) A2 and A6 for alternative reasoning. ∎

Proof of Lemma 2 For -divergence policy regularization and a given , we substitute the worst-case reward perturbations (Eq. 22 or Eq. 62) in the conjugate function (Eq. 56 or Table 2). Assuming , we have

Proof of Lemma 3

See Husain et al. (2021) Lemma 3.

D.2 Robust Set for -Divergence under Regularization

For state-action occupancy regularization and kl divergence, Lemma 2 holds with for normalized and . However, the reasoning in App. D no longer holds for -divergence regularization to a reference . Substituting the worst-case reward perturbations (Eq. 24 or (67)) into the conjugate function (Eq. 66 or Table 2)

| (94) | ||||

whose value is not equal to in general and instead is a function of the given . This may result in the original environmental reward not being part of the robust set, since substituting into Eq. 94 results in .

D.3 Plotting the -Divergence Feasible Set

To plot the boundary of the feasible set in the single step case, for the kl divergence regularization in two dimensions, we can simply solve for the which satisfies the constraint for a given

| (95) |

The interior of the feasible set contains and that are greater than or equal to these values.

However, we cannot analytically solve for the feasible set boundary for general -divergences, since the conjugate function depends on the normalization constant of . Instead, we perform exhaustive search over a range of and values. For each pair of candidate reward perturbations, we use cvx-py (Diamond & Boyd, 2016) to solve the conjugate optimization and evaluate . We terminate our exhaustive search and record the boundary of the feasible set when we find that within appropriate precision.

Appendix E Value Form Reward Perturbations

E.1 Proof of Thm. 1 (Husain et al. (2021))

We rewrite the derivations of Husain et al. (2021) for our notation and setting, where represents a convex regularizer. Starting from the regularized objective in Eq. 12,

| (96) |

note that the objective is concave, as the sum of a linear term and the concave . Since the conjugate is an involution for convex functions, we can rewrite , which yields

| (97) |

where applies the definition of the conjugate of , reparameterizes the optimization in terms of , is the conjugate for , and uses the definition of the regularized RL objective for occupancy measure with the reward . Finally, recognizes the inner maximization as the conjugate function for a modified reward and swaps the order of and assuming the problem is feasible.

Note that Eq. 97 is a standard unregularized rl problem with modified reward . As in Sec. 2, introducing Lagrange multipliers to enforce the flow constraints and for the nonnegativity constraint,

| (98) |

Now, eliminating yields the condition

| (99) |

Letting , we can consider Eq. 99 as a constraint and rewrite Eq. 98 as

| (100) | ||||

which matches Theorem 1. See Husain et al. (2021) for additional detail.

E.2 Path Consistency (Comparison with Nachum et al. (2017); Chow et al. (2018))

We have seen in Sec. 3.3 and App. E.2 that the path consistency conditions arise from the kkt conditions. For kl divergence regularization, Nachum et al. (2017) observe the optimal policy and value satisfy

| (101) |

where the Lagrange multiplier is not necessary since the unless or the rewards or values are infinite. This matches our condition in Eq. 39, where we can also recognize as the identity from Prop. 3. Nachum et al. (2017) use Eq. 101 to derive a learning objective, with the squared error used as a loss for learning and (or simply , Nachum et al. (2017) Sec. 5.1) using function approximation.

Similarly, Chow et al. (2018) consider a (scaled) Tsallis entropy regularizer, . For , the optimal policy and value function satisfy

| (102) |

where is a Lagrange multiplier whose value is learned in Chow et al. (2018). However, inspecting the proof of Theorem 3 in Chow et al. (2018), we see that this multiplier is obtained via the identity (see Eq. 23, App. C.3). Our notation in Eq. 102 differs from Chow et al. (2018) in that we use as the regularization strength (compared with their ). We have also written Eq. 102 to explicitly include the constant factors appearing in the -divergence.

In generalizing the path consistency equations, we will consider the -divergence, with . Note that this includes an additional factor which multiplies the term, compared to the Tsallis entropy considered in Chow et al. (2018). In particular, this scaling will change the additive constant term in Eq. 102, to a term of .

E.3 Indifference Condition

In the single step setting with kl divergence regularization, Ortega & Lee (2014) argue that the perturbed reward for the optimal policy is constant with respect to actions

| (104) |

when are obtained using the optimal policy . Ortega & Lee (2014) highlight that this is a well-known property of Nash equilibria in game theory where, for the optimal policy and worst-case adversarial perturbations, the agent obtains equal perturbed reward for each action and thus is indifferent between them.

In the sequential setting, we can consider as the analogue of the single-step reward or utility function. Using our advantage function interpretation for the optimal policy in Prop. 3, we directly obtain an indifference condition for the sequential setting

| (105) |

for actions with and nonzero probability under . Observe that is a constant with respect to for a given state . Recall that our notation for omits its dependence on and . This indifference condition indeed holds for arbitrary regularization strengths and choices of -divergence, since our proof of the advantage function interpretation in App. A.3 is general. Finally, we emphasize that the indifference condition holds only for the optimal policy with a given reward (see Fig. 3).

( for water,

for goal)

E.4 Confirming Optimality using Path Consistency and Indifference

In Fig. 4, we plotted the regularized policies and worst-case reward perturbations for various regularziation strength and kl divergence regularization. In Fig. 7, we now seek to certify the optimality of each policy using the path consistency or indifference conditions. In particular, we confirm the following equality holds

| (106) |

which aligns with the path consistency condition in (Nachum et al., 2017). Compared with Eq. 28 or Eq. 103, Eq. 106 uses the fact that and in the case of kl divergence regularization. This equality also confirms the indifference condition since the right hand side is a constant with respect to actions. Finally, we can recognize our advantage function interpretation in Eq. 106, by substituting and for kl divergence regularization.

In Fig. 7, we plot for each state-action pair to confirm that it yields a constant value and conclude that the policy and values are optimal. Note that this constant is different across states based on the soft value function , which also depends on the regularization strength.

Appendix F Comparing Entropy and Divergence Regularization

In this section, we provide proofs and discussion to support our observations in Section 5.1 on the benefits of divergence regularization over entropy regularization.

F.1 Tsallis Entropy and -Divergence

To show a relationship between the Tsallis entropy and the -divergence, we first recall the definition of the -exponential function (Tsallis, 2009). We also define , with , so that our use of matches Lee et al. (2019) Eq. (5)

| (107) |

The Tsallis entropy of order (Tsallis, 2009; Naudts, 2011) can be expressed using either or

| (108) | ||||

| (109) |

Eq. 108 and Eq. 109 mirror the two equivalent ways of writing the Shannon entropy for . In particular, we have and . See Naudts (2011) Ch. 7 for discussion of these two forms of the deformed logarithm.

To connect the Tsallis entropy and the -divergence in Eq. 7, we can consider a uniform reference measure . For normalized ,

| (110) | ||||

| (111) | ||||

| (112) |

which recovers the negative Tsallis entropy of order , up to an multiplicative factor and additive constant. Note that including this constant factor via -divergence regularization allows us to avoid an inconvenient factor in optimal policy solutions (Eq. 27) compared with Eq. 8 and 10 of Lee et al. (2019).

F.2 Non-Positivity of for Entropy Regularization

We first derive the worst-case reward perturbations for entropy regularization, before analyzing the sign of these reward perturbations for various values of in Prop. 5. In particular, we have for entropy regularization with , which includes Shannon entropy regularization at . This implies that the modified reward for all .

Lemma 4.

The worst-case reward perturbations for Tsallis entropy regularization correspond to

| (113) |

with limiting behavior of for Shannon entropy regularization as .

Proof.

We can write the Tsallis entropy using an additional constant , with mirroring the -divergence

| (114) |

Note that we use negative Tsallis entropy for regularization since the entropy is concave. Thus, the worst case reward perturbations correspond to the condition . Differentiating with respect to using similar steps as in App. B.3 Eq. 59-(60), we obtain

| (115) |

For and , we obtain Eq. 113. ∎

Proposition 5.

For and , the worst-case reward perturbations with Tsallis entropy regularization from Lemma 4 are non-positive, with . This implies that the entropy-regularized policy is robust to only pointwise reward increases for these values of .

Proof.

We first show for and any . Note that we may write

| (116) |

Since is a non-negative function for , then .

To analyze the second term, consider . We know that for , so that . Thus, we have and implies . Since both terms are non-positive, we have for as desired.

However, for or , we cannot guarantee the reward perturbations are non-positive. Writing the second term in Eq. 113 as , we first observe that that . Now, or implies that , so that the second term is non-negative, compared to the first term, which is non-positive. ∎

F.3 Bounding the Conjugate Function

Conjugate for a Fixed : We follow similar derivations as Lee et al. (2019) to bound the value function for general -divergence regularization instead of entropy regularization. We are interested in providing a bound for with fixed . To upper bound the conjugate, consider the optimum over each term separately

where we let .

We can also lower bound the conjugate function in terms of . Noting that any policy provides a lower bound on the value of the maximization objective, we consider . For evaluating , we assume for and undefined otherwise. Thus, we restrict our attention to to derive the lower bound

where uses and simplifies terms in the -divergence. One can confirm that for . Combining these bounds, we can write

| (117) |