Economic Networks:

Theory and Computation

QuantEcon Book I

Preface

The development and use of network science has grown exponentially since the beginning of the 21st century. The ideas and techniques found in this field are already core tools for analyzing a vast range of phenomena, from epidemics and disinformation campaigns to chemical reactions and brain function.

In economics, network theory is typically taught as a specialized subfield, available to students as one of many elective courses towards the end of their program. However, we are rapidly approaching the stage where every aspiring scientist—including social scientists and economists—wants to know the foundations of this field. It is arguably the case that, just as every well-trained economist learns the basics of convex optimization, maximum likelihood and linear regression, so too should every graduate student in economics learn the fundamental ideas of network theory.

This textbook is an introduction to economic networks, intended for students and researchers in the fields of economics and applied mathematics. The textbook emphasizes quantitative modeling, with the main underlying tools being graph theory, linear algebra, fixed point theory and programming. Most mathematical tools are covered from first principles, with the two main technical results—the Neumann series lemma and the Perron–Frobenius theorem—playing a central role.

The text is suitable for a one-semester course, taught either to advanced undergraduate students who are comfortable with linear algebra or to beginning graduate students. (For example, although we define eigenvalues, an ideal student would already know what eigenvalues and eigenvectors are, so that concepts like “eigenvector centrality” or results like the Neumann series lemma are readily absorbed.) The text will also suit students from mathematics, engineering, computer science and other related fields who wish to learn about connection between economics and networks.

Several excellent textbooks on network theory in economics and social science already exist, including Jackson, (2010), Easley et al., (2010), and Borgatti et al., (2018), as well as the handbook by Bramoullé et al., (2016). These textbooks have broad scope and treat many useful applications. In contrast, our book is narrower and more technical. It provides mathematical, computational and graph-theoretic foundations that are required to understand and apply network theory, along with a treatment of some of the most important network applications in economics, finance and operations research. It can be used as a complementary resource, or as a preliminary course that facilitates understanding of the alternative texts listed above, as well as research papers in the area.

The book contains a mix of Python and Julia code. The majority is in Python because the libraries are somewhat more stable at the time of writing, although Julia also has strong graph manipulation and optimization libraries. Code for figures is available from the authors. There are many solved exercises, ranging from simple to quite hard. At the end of each chapter we provide notes, informal comments and references.

We are greatly indebted to Jim Savage and Schmidt Futures for generous financial support, as well as to Shu Hu and Chien Yeh for their outstanding research assistance. QuantEcon research fellow Matthew McKay generously lent us his time and remarkable expertise in data analysis, networks and visualization. QuantEcon research assistant Mark Dawkins turned a messy collection of code files into an elegant companion Jupyter book. For many important fixes, comments and suggestions, we thank Quentin Batista, Rolf Campos, Fernando Cirelli, Rebekah Dix, Saya Ikegawa, Fazeleh Kazemian, Dawie van Lill, Simon Mishricky, Pietro Monticone, Flint O’Neil, Zejin Shi, Akshay Shanker, Arnav Sood, Natasha Watkins, Chao Wei, and Zhuoying Ye. Finally, Chase Coleman, Alfred Galichon, Spencer Lyon, Daisuke Oyama and Jesse Perla are collaborators at QuantEcon, and almost everything we write has benefited from their input. This text is no exception.

Common Symbols

| implies | |

| and | |

| the set | |

| is defined as equal to | |

| function is everywhere equal to | |

| the power set of ; that is, the collection of all subsets of given set | |

| , and | the natural numbers, integers and real numbers respectively |

| the set of complex numbers (see §6.1.1.8) | |

| , , etc. | the nonnegative elements of , , etc. |

| all matrices | |

| the diagonal matrix with on the principle diagonal | |

| the probability distribution concentrated on point | |

| the absolute value of | |

| the cardinality of (number of elements in) set | |

| is a function from set to set | |

| the set of all functions from to | |

| all -tuples of real numbers | |

| the norm (see §2.3.1.1) | |

| the norm (see §2.3.1.1) | |

| when | the operator norm of (see §2.3.2.3) |

| the inner product of and | |

| function (or vector) is everwhere strictly less than | |

| vector of ones or function everywhere equal to one | |

| indicator, equal to 1 if statement is true and 0 otherwise | |

| iid | independent and identically distributed |

| in-degree of node | |

| out-degree of node | |

| set of direct predecessors of node | |

| set of direct successors of node | |

| node is accessible from node | |

| and have the same distribution | |

| has distribution | |

| the set of all couplings of |

Chapter 1 Introduction

Relations are the fundamental fabric of reality.

Michele Coscia

1.1 Motivation

Alongside the exponential growth of computer networks over the last few decades, we have witnessed concurrent and equally rapid growth in a field called network science. Once computer networks brought network structure into clearer focus, scientists began to recognize networks almost everywhere, even in phenomena that had already received centuries of attention using other methods, and to apply network theory to organize and expand knowledge right throughout the sciences, in every field and discipline.

The set of possible examples is vast, and sources mentioning or treating hundreds of different applications of network methods and graph theory are listed in the reading notes at the end of the chapter. In computer science and machine learning alone, we see computational graphs, graphical networks, neural networks and deep learning. In operations research, network analysis focuses on minimum cost flow, traveling salesman, shortest path, and assignment problems. In biology, networks are a standard way to represent interactions between bioentities.

In this text, our interest lies in economic and social phenomena. Here, too, networks are pervasive. Important examples include financial networks, production networks, trade networks, transport networks and social networks. For example, social and information networks affect trends in sentiments and opinions, consumer decisions, and a range of peer effects. The topology of financial networks helps to determine relative fragility of the financial system, while the structure of production networks affects trade, innovation and the propagation of local shocks.

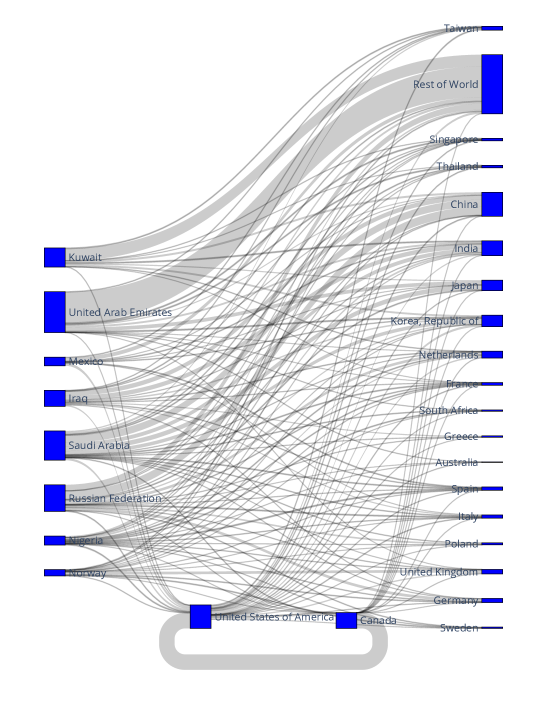

Figures 1.1–1.2 show two examples of trade networks. Figure 1.1 is called a Sankey diagram, which is a kind of figure used to represent flows. Oil flows from left to right. The countries on the left are the top 10 exporters of crude oil, while the countries on the right are the top 20 consumers. The figure relates to one of our core topics: optimal (and equilibrium) flows across networks. We treat optimal flows at length in Chapter 3.111This figure was constructed by QuantEcon research fellow Matthew McKay, using International Trade Data (SITC, Rev 2) collected by The Growth Lab at Harvard University.

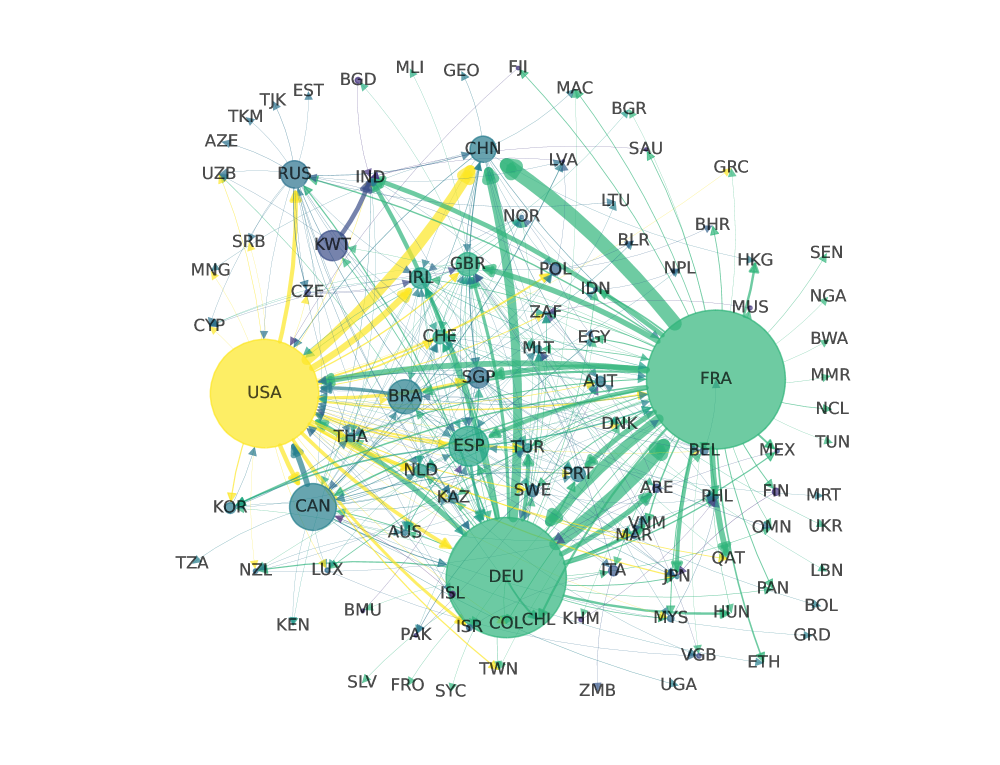

Figure 1.2 shows international trade in large commercial aircraft in 2019.222This figure was also constructed by Matthew McKay, using data 2019 International Trade Data SITC Revision 2, code 7924. The data pertains to trade in commercial aircraft weighted at least 15,000kg. It was sourced from CID Dataverse. Node size is proportional to total exports and link width is proportional to exports to the target country. The US, France and Germany are revealed as major export hubs.

While some readers viewing Figures 1.1–1.2 might at first suspect that the network perspective adds little more than an attractive technique for visualizing data, it actually adds much more. For example, in Figure 1.2, node colors are based on a ranking of “importance” in the network called eigenvector centrality, which we introduce in §1.4.3.4. Such rankings and centrality measures are an active area of research among network scientists. Eigenvector and other forms of centrality feature throughout the text. For example, we will see that these concepts are closely connected to—and shed new light on—fundamental ideas first developed many years ago by researchers in the field of input-output economics.

In addition, in production networks, it turns out that the nature of shock propagation is heavily dependent on the underlying structure of the network. For example, for a few highly connected nodes, shocks occurring within one firm or sector can have an outsized influence on aggregate-level fluctuations. Economists are currently racing to understand these relationships, their interactions with various centrality measures, and other closely related phenomena.

To understand this line of work, as well as other applications of network methods to economics and finance, some technical foundations are required. For example, to define eigenvector centrality, we need to be familiar with eigenvectors, spectral decompositions and the Perron–Frobenius theorem. To work with Katz centrality, which also features regularly in network science and economics, we require a sound understanding of the Neumann series lemma. The Perron–Frobenius theorem and the Neumann series lemma form much of the technical foundation of this textbook. We review them in detail in §1.2 and develop extensions throughout remaining chapters.

One reason that analysis of networks is challenging is high-dimensionality. To see why, consider implementing a model with economic agents. This requires times more data than one representative agent in a setting where agents are atomistic or coordinated by a fixed number of prices. For example, Carvalho and Grassi, (2019) model the dynamics of firms, all of which need to be tracked when running a simulation. However, if we wish to model interactions between each pair (supply linkages, liabilities, etc.), then, absent sparsity conditions, the data processing requirement grows like .333See §6.1.3 for a discussion of big O notation. In the Carvalho and Grassi, (2019) example, is , which is very large even for modern computers. One lesson is that network models can be hard to solve, even with powerful computers, unless we think carefully about algorithms.

In general, to obtain a good grasp on the workings of economic networks, we will need computational skills plus a firm understanding of linear algebra, probability and a field of discrete mathematics called graph theory. The rest of this chapter provides relevant background in these topics. Before tackling this background, we recommend that readers skim the list of common symbols on page Common Symbols, as well the mathematical topics in the appendix, which start on page 6. (The appendix is not intended for sequential reading, but rather as a source of definitions and fundamental results to be drawn on in what follows.)

1.2 Spectral Theory

In this section we review some linear algebra needed for the study of graphs and networks. Highlights include the spectral decomposition of diagonalizable matrices, the Neumann series lemma, and the fundamental theorem of Perron and Frobenius.

1.2.1 Eigendecompositions

Our first task is to cover spectral decompositions and the spectral theorem. We begin with a brief review of eigenvalues and their properties. (If you are not familiar with eigenvalues and eigenvectors, please consult an elementary treatment first. See, for example, Cohen, (2021).)

1.2.1.1 Eigenvalues

Fix in . A scalar is called an eigenvalue of if there exists a nonzero such that . A vector satisfying this equality is called an eigenvector corresponding to the eigenvalue . (Notice that eigenvalues and eigenvectors are allowed to be complex, even though we restrict elements of to be real.) The set of all eigenvalues of is called the spectrum of and written as . As we show below, has at most distinct eigenvalues.

In Julia, we can check for the eigenvalues of a given square matrix via eigvals(A). Here is one example

Running this code in a Jupyter cell (with Julia kernel) or Julia REPL produces

Here im stands for , the imaginary unit (i.e., ).

Using pencil and paper, confirm that Julia’s output is correct. In particular, show that

with corresponding eigenvectors and .

For , we have

Similarly for , we have

If and is an eigenvector for , then is called an eigenpair.

Prove: if is an eigenpair of and is a nonzero scalar, then is also an eigenpair of .

Fix an eigenpair of and a nonzero scalar . We have

Hence is an eigenvector and is an eigenvalue, as claimed.

Lemma 1.2.1.

is an eigenvalue of if and only if .

Proof.

If , then Lemma 1.2.1 follows directly from Theorem 6.1.14 on page 6.1.14, since is equivalent to existence of nonzero vector such that , which in turn says that is an eigenvalue of . The same arguments extend to the case because the statements in Theorem 6.1.14 are also valid for complex-valued matrices (see, e.g., Jänich, (1994)). ∎

It can be shown that is a polynomial of degree .444See, for example, Jänich, (1994), Chapter 6. This polynomial is called the characteristic polynomial of . By the Fundamental Theorem of Algebra, there are roots (i.e., solutions in to the equation ), although some may be repeated as in the complete factorization of . By Lemma 1.2.1,

-

(i)

each of these roots is an eigenvalue, and

-

(ii)

no other eigenvalues exist besides these roots.

If appears times in the factorization of the polynomial , then is said to have algebraic multiplicity . An eigenvalue with algebraic multiplicity one is called simple. A simple eigenvalue has the property that its eigenvector is unique up to a scalar multiple, in the sense of Exercise 1.2.1.1. In other words, the linear span of (called the eigenspace of ) is one-dimensional.

For , show that iff for all .

Fix and . If , then , or . Hence . To obtain the converse implication, multiply by .

A useful fact concerning eigenvectors is that if the characteristic polynomial has distinct roots, then the corresponding eigenvectors form a basis of . Prove this for the case where all eigenvectors are real—that is show that the (real) eigenvectors form a basis of . (Bases are defined in §6.1.4.2. Proving this for is also a good effort.)

If has distinct roots, then . For each , let be a corresponding eigenvector. It suffices to show that is linearly independent. To this end, let be the largest number such that is independent. Seeking a contradiction, suppose that . Then for suitable scalars . Hence, by , we have

Since is independent, we have for all . At least one is nonzero, so for some . Contradiction.

1.2.1.2 The Eigendecomposition

What are the easiest matrices to work with? An obvious answer to this question is: the diagonal matrices. For example, when with ,

-

•

the linear system reduces to completely independent scalar equations,

-

•

the -th power is just , and

-

•

the inverse is just , assuming all ’s are nonzero.

While most matrices are not diagonal, there is a way that “almost any” matrix can be viewed as a diagonal matrix, after translation of the usual coordinates in via an alternative basis. This can be extremely useful. The key ideas are described below.

is called diagonalizable if

We allow both and to contain complex values. The representation is called the eigendecomposition or the spectral decomposition of .

One way to think about diagonalization is in terms of maps, as in

Either we can map directly with or, alternatively, we can shift to via , apply the diagonal matrix , and then shift back to via .

The equality can also be written as . Decomposed across column vectors, this equation says that each column of is an eigenvector of and each element along the principal diagonal of is an eigenvalue.

Confirm this. Why are column vectors taken from nonzero, as required by the definition of eigenvalues?

Suppose to the contrary that there is one zero column vector in . Then is not nonsingular. Contradiction.

The trace of a matrix is equal to the sum of its eigenvalues, and the determinant is their product. Prove this fact in the case where is diagonalizable.

Let be as stated, with . Using elementary properties of the trace and determinant, we have

and

The asymptotic properties of are determined by the eigenvalues of . This is clearest in the diagonalizable case, where . To illustrate, use induction to show that

| (1.1) |

When does diagonalizability hold?

While diagonalizability is not universal, the set of matrices in that fail to be diagonalizable has “Lebesgue measure zero” in . (Loosely speaking, only special or carefully constructed examples will fail to be diagonalizable.) The next results provide conditions for the property.

Theorem 1.2.2.

A matrix is diagonalizable if and only if its eigenvectors form a basis of .

This result is intuitive: for to hold we need to be invertible, which requires that its columns are linearly independent. Since is -dimensional, this means that the columns form a basis of .

Corollary 1.2.3.

If has distinct eigenvalues, then is diagonalizable.

Proof.

See Exercise 1.2.1.1. ∎

Give a counterexample to the statement that the condition in Corollary 1.2.3 is necessary as well as sufficient.

If is the identity and for some nonzero , then and hence . Hence . At the same time, is diagonalizable, since when .

There is another way that we can establish diagonalizability, based on symmetry. Symmetry also lends the diagonalization certain properties that turn out to be very useful in applications. We are referring to the following celebrated theorem.

Theorem 1.2.4 (Spectral theorem).

If is symmetric, then there exists a real orthonormal matrix such that

Since, for the orthonormal matrix , we have (see Lemma 6.1.15), one consequence of the spectral theorem is that is diagonalizable. For obvious reasons, we often say that is orthogonally diagonalizable.

1.2.1.3 Worker Dynamics

Let’s study a small application of the eigendecomposition. Suppose that, each month, workers are hired at rate and fired at rate . Their two states are unemployment (state 1) and employment (state 2). Figure 1.3 shows the transition probabilities for a given worker in each of these two states.

We translate these dynamics into the matrix

-

•

Row 1 of gives probabilities for unemployment and employment respectively when currently unemployed.

-

•

Row 2 of gives probabilities for unemployment and employment respectively when currently employed.

Using Lemma 1.2.1, show that the two eigenvalues of are and . Show that, when ,

are two corresponding eigenvectors, and that and are simple.

Show that, when , the eigenvalue is not simple.

Below we demonstrate that the -th power of provides -step transition probabilities for workers. Anticipating this discussion, we now seek an expression for at arbitrary . This problem is simplified if we use diagonalization.

Assume that . (When , computing the powers of is trivial.) Show that

Using (1.1), prove that

| (1.2) |

for every .

1.2.1.4 Left Eigenvectors

A vector is called a left eigenvector of if is an eigenvector of . In other words, is nonzero and there exists a such that . We can alternatively write the expression as , which is where the name “left” eigenvector originates.

Left eigenvectors will play important roles in what follows, including that of stochastic steady states for dynamic models under a Markov assumption. To help distinguish between ordinary and left eigenvectors, we will at times call (ordinary) eigenvectors of right eigenvectors of .

If is diagonalizable, then so is . To show this, let with . We know from earlier discussion that the columns of are the (right) eigenvectors of .

Let . Prove that and .

The results of the last exercise show that, when , the columns of coincide with the left eigenvectors of . (Why?) Equivalently, where is the matrix with -th column equal to the -th left eigenvector of .

Let be right eigenvectors of and let be the left eigenvectors. Prove that

| (1.3) |

(Hint: Use the results of Exercise 1.2.1.4.)

Continuing with the notation defined above and continuing to assume that is diagonalizable, prove that

| (1.4) |

for all . The expression for on the left hand side of (1.4) is called the spectral representation of .

Prove that each matrix in the sum is rank 1.

1.2.1.5 Similar Matrices

Diagonalizability is a special case of a more general concept: is called similar to if there exists an invertible matrix such that . In this terminology, is diagonalizable if and only if it is similar to a diagonal matrix.

Prove that similarity between matrices is an equivalence relation (see §6.1.1.2) on .

The fact that similarity is an equivalence relation on implies that this relation partitions into disjoint equivalence classes, elements of which are all similar. Prove that all matrices in each equivalence class share the same eigenvalues.

Prove: If is similar to , then is similar to . In particular

The last result is a generalization of (1.1). When is large, calculating the powers can be computationally expensive or infeasible. If, however, is similar to some simpler matrix , then we can take powers of instead, and then transition back to using the similarity relation.555The only concern with this shift process is that can be ill-conditioned, implying that the inverse is numerically unstable.

1.2.2 The Neumann Series Lemma

Most high school students learn that, if is a number with , then

| (1.5) |

This geometric series representation extends to matrices: If is a matrix satisfying a certain condition, then (1.5) holds, in the sense that . (Here is the identity matrix.) But what is the “certain condition” that we need to place on , which generalizes the concept to matrices? The answer to this question involves the “spectral radius” of a matrix, which we now describe.

1.2.2.1 Spectral Radii

Fix . With indicating the modulus of a complex number , the spectral radius of is defined as

| (1.6) |

Within economics, the spectral radius has important applications in dynamics, asset pricing, and numerous other fields. As we will see, the same concept also plays a key role in network analysis.

Remark 1.2.1.

For any square matrix , we have . This follows from the fact that and always have the same eigenvalues.

Example 1.2.1.

As usual, diagonal matrices supply the simplest example: If , then the spectrum is just and hence .

1.2.2.2 Geometric Series

We can now return to the matrix extension of (1.5) and state a formal result.

Theorem 1.2.5 (Neumann series lemma (NSL)).

If is in and , then is nonsingular and

| (1.7) |

The sum is called the power series representation of . Convergence of the matrix series is understood as element-by-element convergence.

A full proof of Theorem 1.2.5 can be found in Cheney, (2013) and many other sources. The core idea is simple: if then . Reorganizing gives , which is equivalent to (1.7). The main technical issue is showing that the power series converges. The full proof shows that this always holds when .

Fix . Prove the following: if , then, for each the linear system has the unique solution given by

| (1.8) |

Fix and where . We can write as . Since , is invertible and hence the linear system has unique solution . The expression follows from the Neumann series lemma.

1.2.3 The Perron–Frobenius Theorem

In this section we state and discuss a suprisingly far reaching theorem due to Oskar Perron and Ferdinand Frobenius, which has applications in network theory, machine learning, asset pricing, Markov dynamics, nonlinear dynamics, input-output analysis and many other fields. In essence, the theorem provides additional information about eigenvalues and eigenvectors when the matrix in question is positive in some sense.

1.2.3.1 Order in Matrix Space

We require some definitions. In what follows, for , we write

-

•

if all elements of are nonnegative and

-

•

if all elements of are strictly positive.

It’s easy to imagine how nonnegativity and positivity are important notions for matrices, just as they are for numbers. However, strict positivity of every element of a matrix is hard to satisfy, especially for a large matrix. As a result, mathematicians routinely use two notions of “almost everywhere strictly positive,” which sometimes provide sufficient positivity for the theorems that we need.

Regarding these two notions, for , we say that is

-

•

irreducible if and

-

•

primitive if there exists an such that .

Evidently, for we have

A nonnegative matrix is called reducible if it fails to be irreducible.

By examining the expression for in (1.2), show that is

-

(i)

irreducible if and only if ; and

-

(ii)

primitive if and only if and .

((i), ()) Suppose that is irreducible and yet . Then, by the expression for in (1.2), we have for all . This contradicts irreducibility, so must hold. A similar argument shows that .

((i), ()) If , then the diagonal elements are strictly positive whenever is even. A small amount of algebra shows that the off-diagonal elements are strictly positive whenever is odd. Hence and is irreducible.

((ii), ()) Suppose that is primitive. Then is irreducible, so it remains only to show that . Suppose to the contrary that . Then has zero diagonal elements when is even and zero off-diagonal elements when is odd. This contradicts the primitive property, so must hold.

((ii), ()) Suppose that and . Some algebra shows that . The same is true when and . Hence is primitive.

In addition to the above notation, for , we also write

-

•

if and if ,

-

•

if , etc.

Show that is a partial order (see §6.1.2.1) on .

The partial order discussed in Exercise 1.2.3.1 is usually called the pointwise partial order on . Analogous notation and terminology are used for vectors.

The following exercise shows that nonnegative matrices are order-preserving maps (see §6.1.2.3) on vector space under the pointwise partial order—a fact we shall exploit many times.

Show that the map is order-preserving (see §6.1.2.3) whenever (i.e., implies for any conformable vectors ).

Fix with , along with . From we have , so . But then , or .

1.2.3.2 Statement of the Theorem

Let be in . In general, is not an eigenvalue of . For example,

But is always an eigenvalue when . This is just one implication of the following famous theorem.

Theorem 1.2.6 (Perron–Frobenius).

If , then is an eigenvalue of with nonnegative real right and left eigenvectors:

| (1.9) |

If is irreducible, then, in addition,

-

(i)

is strictly positive and a simple eigenvalue,

-

(ii)

the eigenvectors and are everywhere positive, and

-

(iii)

eigenvectors of associated with other eigenvalues fail to be nonnegative.

If is primitive, then, in addition,

-

(i)

the inequality is strict for all eigenvalues of distinct from , and

-

(ii)

with and normalized so that , we have

(1.10)

The fact that is simple under irreducibility means that its eigenvectors are unique up to scalar multiples. We will exploit this property in several important uniqueness proofs.

In the present context, is called the dominant eigenvalue or Perron root of , while and are called the dominant left and right eigenvectors of , respectively.

Why do we use the word “dominant” here? To help illustrate, let us suppose that is primitive and fix any . Consider what happens to the point as grows. By (1.10) we have for large , where . In other words, asymptotically, the sequence is just scalar multiples of , growing at rate . Thus, dominates other eigenvalues in controlling the growth rate of , while dominates other eigenvectors in controlling the direction of growth.

The matrix in (1.10) is called the Perron projection of . Prove that (a property that is often used to define projection matrices) and . Describe the one-dimensional space that projects all of into.

Example 1.2.2.

Fix . If , then is not invertible. To see this, observe that, by Theorem 1.2.6, since is an eigenvalue of , there exists a nonzero vector such that . The claim follows. (Why?)

1.2.3.3 Worker Dynamics II

We omit the full proof of Theorem 1.2.6, which is quite long and can be found in Meyer, (2000), Seneta, 2006b or Meyer-Nieberg, (2012).666See also Glynn and Desai, (2018), which provides a new proof of the main results, based on probabilistic arguments, including extensions to infinite state spaces. Instead, to build intuition, let us prove the theorem in a rather simple special case.

The special case we will consider is the class of matrices

This example is drawn from the study of worker dynamics in §1.2.1.3.

You might recall from that and . Clearly , so is an eigenvalue, as claimed by the first part of the Perron–Frobenius theorem.

From now on we assume that , which just means that we are excluding the identity matrix in order to avoid some tedious qualifying remarks.

The two right eigenvectors () and two left eigenvectors () are, respectively,

Verify these claims. (The right eigenvectors were treated in §1.2.1.3.)

Recall from Exercise 1.2.3.1 that is irreducible if and only if both and are strictly positive. Show that all the claims about irreducible matrices in the Perron–Frobenius theorem are valid for under this irreducibility condition.

1.2.3.4 Bounding the Spectral Radius

Using the Perron–Frobenius theorem, we can provide useful bounds on the spectral radius of a nonnegative matrix. In what follows, fix and set

-

•

the -th row sum of and

-

•

the -th column sum of .

Lemma 1.2.7.

If , then

-

(i)

and

-

(ii)

.

Proof.

Let be as stated and let be the right eigenvector in (1.9). Since is nonnegative and nonzero, we can and do assume that . From we have for all . Summing with respect to gives . Since the elements of are nonnegative and sum to one, is a weighted average of the column sums. Hence the second pair of bounds in Lemma 1.2.7 holds. The remaining proof is similar (use the left eigenvector). ∎

1.3 Probability

Next we review some elements of probability that will be required for analysis of networks.

1.3.1 Discrete Probability

We first introduce probability models on finite sets and then consider sampling methods and stochastic matrices.

1.3.1.1 Probability on Finite Sets

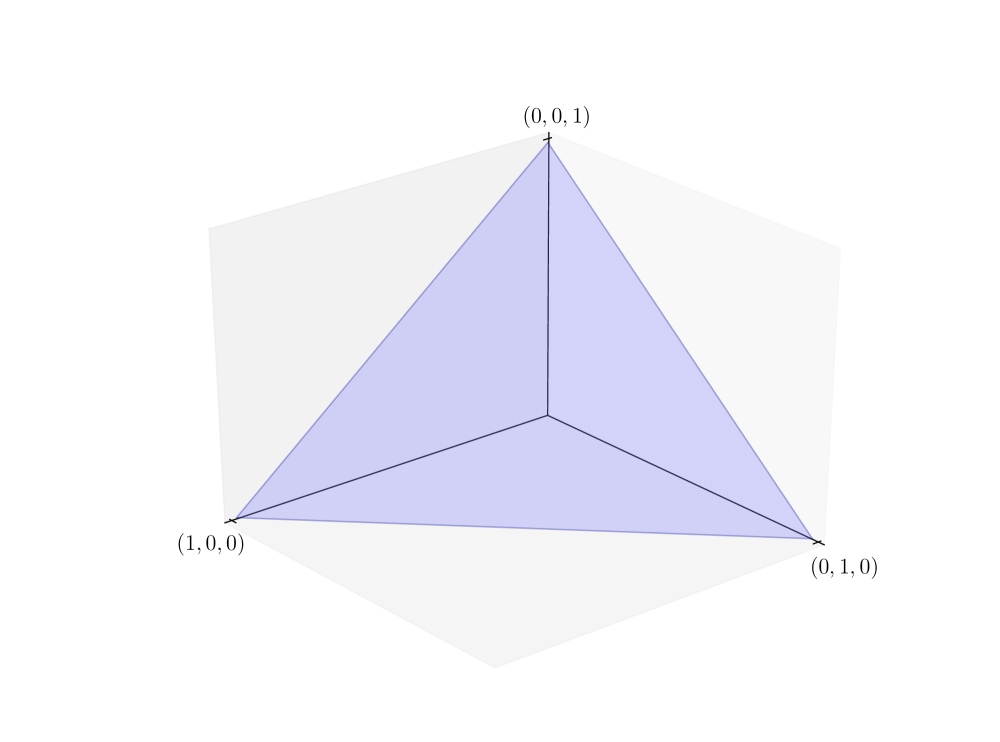

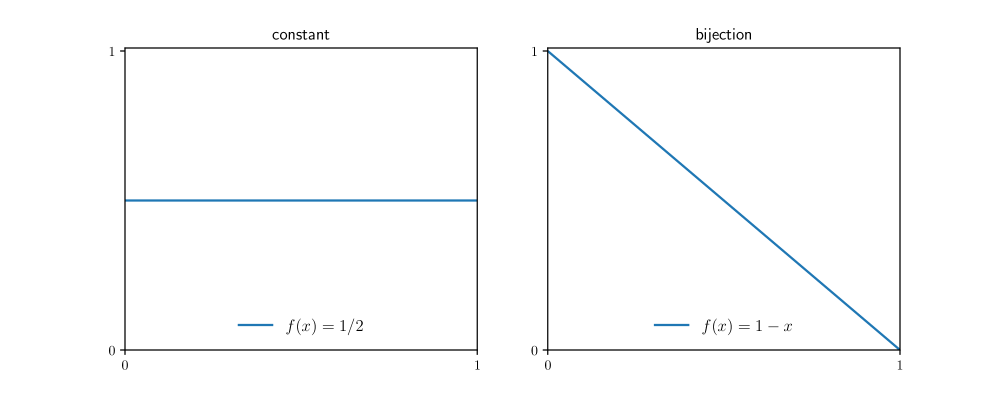

Throughout this text, if is a finite set, then we set

and call the set of distributions on . We say that a random variable taking values in has distribution and write if

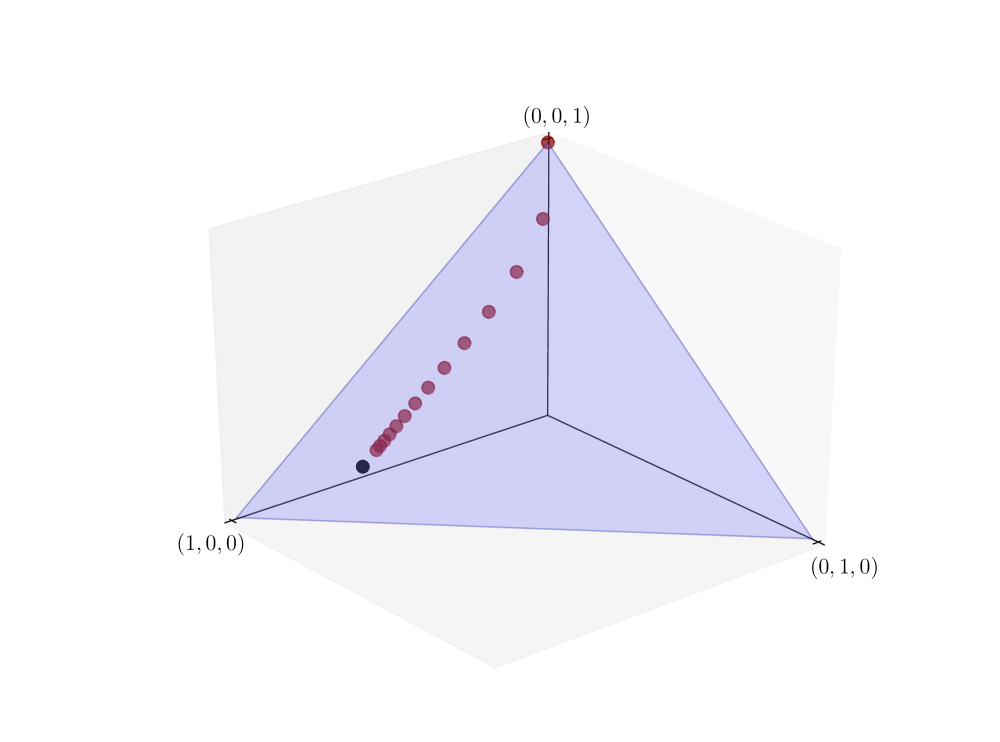

A distribution can also be understood as a vector (see Lemma 6.1.2 in §6.1.1.3). As a result, can be viewed as a subset of . Figure 1.4 provides a visualization when . Each is identified by the point in .

More generally, if , then can be identified with the unit simplex in , which is the set of all -vectors that are nonnegative and sum to one.

Throughout, given , we use the symbol to represent the element of that puts all mass on . In other words, for all . In Figure 1.4, each is a vertex of the unit simplex.

We frequently make use of the law of total probability, which states that, for a random variable on and arbitrary ,

| (1.11) |

where is a partition of (i.e., finite collection of disjoint subsets of such that their union equals ).

Prove (1.11) assuming for all .

1.3.1.2 Inverse Transform Sampling

Let be a finite set. Suppose we have the ability to generate random variables that are uniformly distributed on . We now want to generate random draws from that are distributed according to arbitrary .

Let be uniformly distributed on , so that, for any , we have , which is the length of the interval .777The probability is the same no matter whether inequalities are weak or strict. Our problem will be solved if we can create a function from to such that has distribution . One technique is as follows. First we divide the unit interval into disjoint subintervals, one for each . The interval corresponding to is denoted and is chosen to have length . More specifically, when , we take

You can easily confirm that the length of is for all .

Now consider the function defined by

| (1.12) |

where is one when and zero otherwise. It turns out that has the distribution we desire.

Prove:

-

(i)

For all , we have if and only if .

-

(ii)

The random variable has distribution .

For the first claim, fix and . If , then, since all elements of are distinct, the definition of implies . Conversely, if , then, since all intervals are disjoint, we have .

For the second claim, pick any , and observe that, by the first claim, the precisely when . The probability of this event is the length of the interval , which, by construction, is . Hence for all as claimed.

Let , and be as defined above. Prove that holds for all . {Answer} Fix . Observe that is Bernoulli random variable. The expectation of such a equals . As , this is .

Using Julia or another language of your choice, implement the inverse transform sampling procedure described above when and . Generate (quasi) independent draws from and confirm that for .

The last exercise tells us that that the law of large numbers holds in this setting, since, under this law, we expect that

with probability one as . In view of Exercise 1.3.1.2, the right hand side equals .

Suppose that, on a computer, you can generate only uniform random variables on , and you wish to simulate a flip of a biased coin with heads probability . Propose a method.

Draw uniformly on and set the coin to heads if . The probability of this outcome is .

Suppose that, on a computer, you are able to sample from distributions and defined on some set . The set can be discrete or continuous and, in the latter case, the distributions are understood as densities. Propose a method to sample on a computer from the convex combination , where .

For the solution we assume that is finite, although the argument can easily be extended to densities. On the computer, we flip a biased coin with and then

-

(i)

draw from if , or

-

(ii)

draw from if .

With this set up, by the law of total probability,

In other words, .

1.3.1.3 Stochastic Matrices

A matrix is called a stochastic matrix if

In other words, is nonnegative and has unit row sums.

We will see many applications of stochastic matrices in this text. Often the applications are probabilistic, where each row of is interpreted as a distribution over a finite set.

Let be stochastic matrices. Prove the following facts.

-

(i)

is also stochastic.

-

(ii)

.

-

(iii)

There exists a row vector such that and .

Let and be as stated. Evidently . Moreover, , so is stochastic. That follows directly from Lemma 1.2.7. By the Perron–Frobenius theorem, there exists a nonzero, nonnegative row vector satisfying . Rescaling to gives the desired vector .

The vector in part (iii) of Exercise 1.3.1.3 is called the PageRank vector by some authors, due to its prominence in Google’s PageRank algorithm. We will call it a stationary distribution instead.888Stationary distributions of stochastic matrices were intensively studied by many mathematicians well over a century before Larry Page and Sergey Brin patented the PageRank algorithm, so it seems unfair to allow them to appropriate the name. Stationary distributions play a key role in the theory of Markov chains, to be treated in §4.1. Ranking methods are discussed again in §1.4.3. PageRank is treated in more detail in §4.2.3.3.

1.3.2 Power Laws

Next we discuss distributions on the (non-discrete) sets and . We are particularly interested in a certain class of distributions that are apparently non-standard and yet appear with surprising regularity in economics, social science, and the study of networks. We refer to the distributions that are said to obey a “power law.”

In what follows, given a real-valued random variable , the function

is called the cumulative distribution function (cdf) of . The counter cdf (ccdf) of is the function .

A useful property that holds for any nonnegative random variable and is the identity

| (1.13) |

See, for example, Çınlar, (2011), p. 63.

1.3.2.1 Heavy Tails

Recall that a random variable on is said to be normally distributed with mean and variance , and we write , if has density

One notable feature of the normal density is that the tails of the density approach zero quickly. For example, goes to zero like as , which is extremely fast.

A random variable on is called exponentially distributed and we write if, for some , has density

The tails of the exponential density go to zero like as , which is also relatively fast.

When a distribution is relatively light-tailed, in the sense that its tails go to zero quickly, draws rarely deviate more than a few standard deviations from the mean. In the case of a normal random variable, the probability of observing a draw more than 3 standard deviations above the mean is around 0.0014. For 6 standard deviations, the probability falls to .

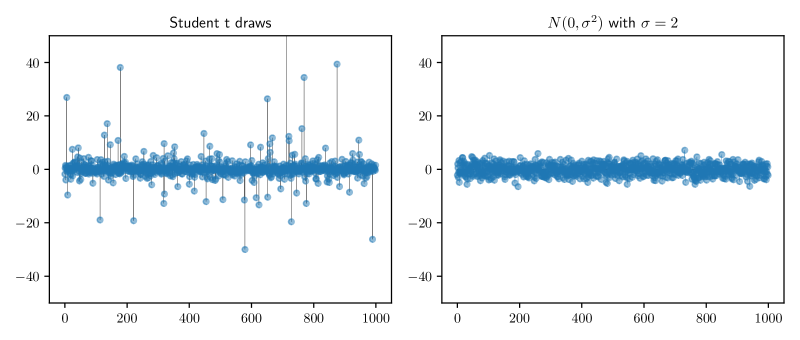

In contrast, for some distributions, “extreme” outcomes occur relatively frequently. The left panel of Figure 1.5 helps to illustrate by simulating 1,000 independent draws from Student’s t-distribution, with degrees of freedom. For comparison, the right subfigure shows an equal number of independent draws from the distribution. The Student’s t draws reveal tight clustering around zero combined with a few large deviations.

Formally, a random variable on is called light-tailed if its moment generating function

| (1.14) |

is finite for at least one . Otherwise is called heavy-tailed.999Terminology on heavy tails varies across the literature but our choice is increasingly standard. See, for example, Foss et al., (2011) or Nair et al., (2021).

Example 1.3.1.

If , the the moment generating function of is known to be

Hence is light tailed.

Example 1.3.2.

A random variable on is said to have the lognormal density and we write if . The mean and variance of this distribution are, respectively,

The moment generating function is known to be infinite for all , so any lognormally distributed random variable is heavy-tailed.

For any random variable and any , the (possibly infinite) expectation called the -th moment of .

Lemma 1.3.1.

Let be a random variable on . If is light-tailed, then all of its moments are finite.

Proof.

Pick any . We will show that . Since is light-tailed, there exists a such that . For a sufficiently large constant we have whenever . As a consequence, with as the distribution of , we have

Prove that the lognormal distribution has finite moments of every order.

Fix and let be . We have

Since , we can apply the formula for the mean of a lognormal distribution to obtain .

1.3.2.2 Pareto Tails

Given , a nonnegative random variable is said to have a Pareto tail with tail index if there exists a such that

| (1.15) |

In other words, the ccdf of satisfies

| (1.16) |

If has a Pareto tail for some , then is also said to obey a power law.

Example 1.3.3.

A random variable on is said to have a Pareto distribution with parameters if its ccdf obeys

| (1.17) |

It should be clear that such an has a Pareto tail with tail index .

Regarding Example 1.3.3, note that the converse is not true: Pareto-tailed random variables are not necessarily Pareto distributed, since the Pareto tail property only restricts the far right hand tail.

Show that, if has a Pareto tail with tail index , then for all . [Hint: Use (1.13).]

Let have a Pareto tail with tail index and let be its ccdf. Fix . Under the Pareto tail assumption, we can take positive constants and such that whenever . Using (1.13) we have

But whenever . Since , we have .

From Exercise 1.3.2.2 and Lemma 1.3.1, we see that every Pareto-tailed random variable is heavy-tailed. The converse is not true, since the Pareto tail property (1.15) is very specific. Despite this, it turns out that many heavy-tailed distributions encountered in the study of networks are, in fact, Pareto-tailed.

Prove: If for some , then does not obey a power law.

Fix and suppose . A simple integration exercise shows that . Now fix . Since , the random variable does not obey a power law.

1.3.2.3 Empirical Power Law Plots

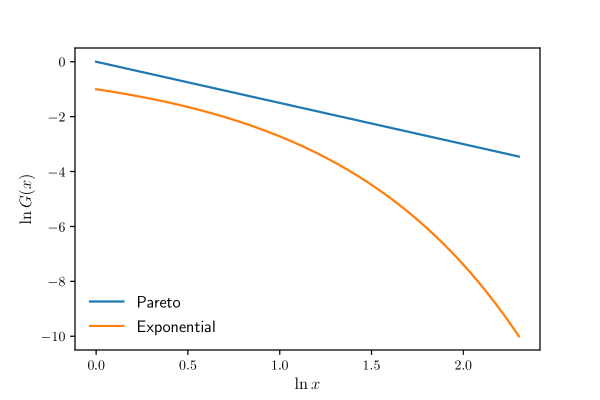

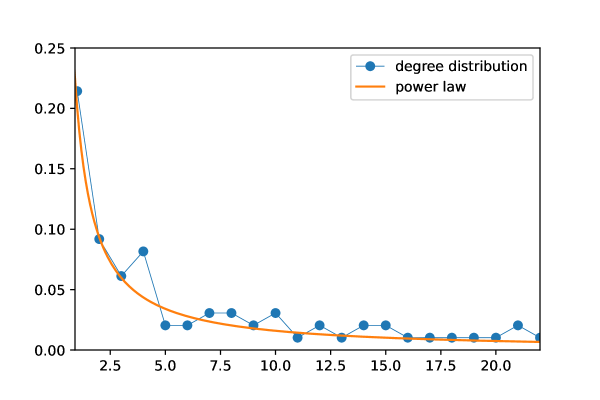

When the Pareto tail property holds, the ccdf satisfies for large . In other words, is eventually log linear. Figure 1.6 illustrates this using a Pareto distribution. For comparison, the ccdf of an exponential distribution is also shown.

If we replace the ccdf with its empirical counterpart—which returns, for each , the fraction of the sample with values greater than —we should also obtain an approximation to a straight line under the Pareto tail assumption.

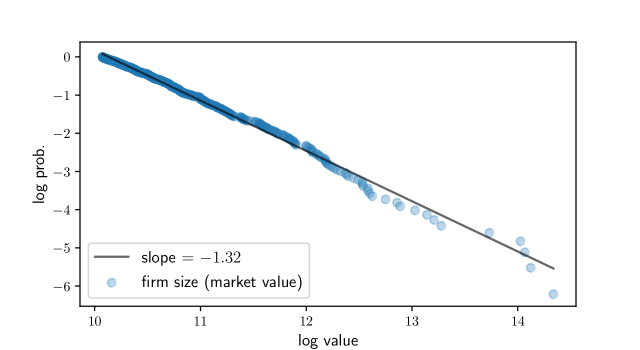

For example, consider the cross-sectional distribution of firm sizes. While the precise nature of this distribution depends on the measure of firm size, the sample of firms and other factors, the typical picture is one of extreme heavy tails. As an illustration, Figure 1.7 shows an empirical ccdf log-log plot for market values of the largest 500 firms in the Forbes Global 2000 list, as of March 2021. The slope estimate and data distribution are consistent with a Pareto tail and infinite population variance.

1.3.2.4 Discrete Power Laws

Let be a random variable with the Pareto distribution, as described in Example 1.3.3. The density of this random variable on the set is with and . The next exercise extends this idea.

Let be a random variable with density on . Suppose that, for some constants , and , we have

| (1.18) |

Prove that is Pareto-tailed with tail index .

Let and the constants and be as described in the exercise. Pick any . By the usual rules of integration,

With , we then have , and is Pareto-tailed with tail index .

The discrete analog of (1.18) is a distribution on the positive integers with

| (1.19) |

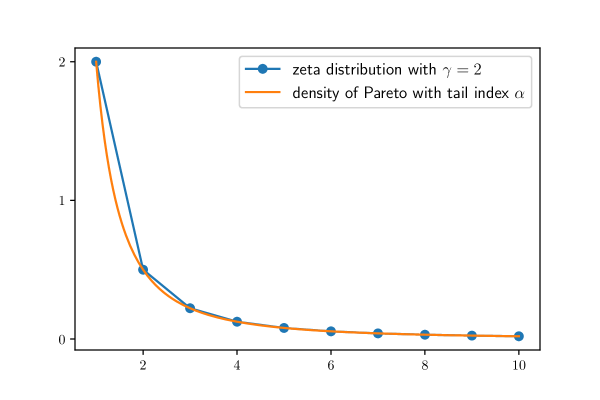

for large . In the special case where this equality holds for all , and is chosen so that , we obtain the zeta distribution.101010Obviously the correct value of depends on , so we can write for some suitable function . The correct function for this normalization is called the Riemann zeta function.

In general, when we see a probability mass function with the specification (1.19) for large , we can identify this with a Pareto tail, with tail index . Figure 1.8 illustrates with .

1.4 Graph Theory

Graph theory is a major branch of discrete mathematics. It plays an essential role in this text because it forms the foundations of network analysis. This section provides a concise and fast-moving introduction to graph theory suitable for our purposes.111111Graph theory is often regarded as originating from work by the brilliant Swiss mathematician Leonhard Euler (1707–1783), including his famous paper on the “Seven Bridges of Königsberg.”

Graph theory has another closely related use: many economic models are stochastic and dynamic, which means that they specify states of the world and rates of transition between them. One of the most natural ways to conceptualize these notions is to view states as vertices in a graph and transition rates as relationships between them.

We begin with definitions and fundamental concepts. We focus on directed graphs, where there is a natural asymmetry in relationships (bank lends money to bank , firm supplies goods to firm , etc.). This costs no loss of generality, since undirected graphs (where relationships are symmetric two-way connections) can be recovered by insisting on symmetry (i.e., existence of a connection from to implies existence of a connection from to ).

1.4.1 Unweighted Directed Graphs

We begin with unweighted directed graphs and examine standard properties, such as connectedness and aperiodicity.

1.4.1.1 Definition and Examples

A directed graph or digraph is a pair , where

-

•

is a finite nonempty set called the vertices or nodes of , and

-

•

is a collection of ordered pairs in called edges.

Intuitively and visually, is understood as an arrow from vertex to vertex .

Two graphs are given in Figures 1.9–1.10. Each graph has three vertices. In these cases, the arrows (edges) could be thought of as representing positive possibility of transition over a given unit of time.

For a given edge , the vertex is called the tail of the edge, while is called the head. Also, is called a direct predecessor of and is called a direct successor of . For , we use the following notation:

-

•

the set of all direct predecessors of

-

•

the set of all direct successors of

Also,

-

•

the in-degree the number of direct predecessors of , and

-

•

the out-degree the number of direct successors of .

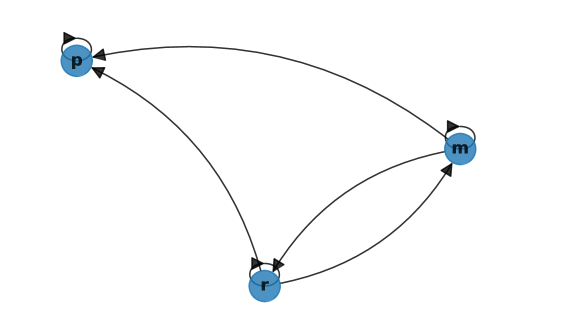

If and , then is called a source. If either or , then is called a sink. For example, in Figure 1.10, “poor” is a sink with an in-degree of 3.

1.4.1.2 Digraphs in Networkx

Both Python and Julia provide valuable interfaces to numerical computing with graphs. Of these libraries, the Python package Networkx is probably the most mature and fully developed. It provides a convenient data structure for representing digraphs and implements many common routines for analyzing them. To import it into Python we run

In all of the code snippets shown below, we assume readers have executed this import statement, as well as the additional two imports:

As an example, let us create the digraph in Figure 1.10, which we denote henceforth by . To do so, we first create an empty DiGraph object:

Next we populate it with nodes and edges. To do this we write down a list of all edges, with poor represented by p and so on:

Finally, we add the edges to our DiGraph object:

Adding the edges automatically adds the nodes, so G_p is now a correct representation of . For our small digraph we can verify this by plotting the graph via Networkx with the following code:

DiGraph objects have methods that calculate in-degree and out-degree of vertices. For example,

prints 3.

1.4.1.3 Communication

Next we study communication and connectedness, which have important implications for production, financial, transportation and other networks, as well as for dynamic properties of Markov chains.

A directed walk from vertex to vertex of a digraph is a finite sequence of vertices, starting with and ending with , such that any consecutive pair in the sequence is an edge of . A directed path from to is a directed walk from to such that all vertices in the path are distinct. For example, in Figure 1.12, is a directed walk from to , while is a directed path from to .

As is standard, the length of a directed walk (or path) counts the number of edges rather than vertices. For example, the directed path from to in Figure 1.12 is said to have length 2.

Vertex is called accessible (or reachable) from vertex , and we write , if either or there exists a directed path from to . A set is called absorbing for the directed graph if no element of is accessible from .

Example 1.4.1.

Let be a digraph representing a production network, where elements of are sectors and means that supplies to . Then sector is an upstream supplier of sector whenever .

Example 1.4.2.

The vertex in the Markov digraph displayed in Figure 1.10 is absorbing, since is not accessible from .

Two vertices and are said to communicate if and .

Let be a directed graph and write if and communicate. Show that is an equivalence relation (see §6.1.1.2).

Since communication is an equivalence relation, it induces a partition of into a finite collection of equivalence classes. Within each of these classes, all elements communicate. These classes are called strongly connected components. The graph itself is called strongly connected if there is only one such component; that is, is accessible from for any pair . This corresponds to the idea that any node can be reached from any other.

Example 1.4.3.

Figure 1.12 shows a digraph with strongly connected components and . The digraph is not strongly connected.

Example 1.4.4.

Networkx can be used to test for communication and strong connectedness, as well as to compute strongly connected components. For example, applied to the digraph in Figure 1.12, the code

prints [{1}, {2, 3}].

1.4.1.4 Aperiodicity

A cycle of a directed graph is a directed walk in such that (i) the first and last vertices are equal and (ii) no other vertex is repeated. The graph is called periodic if there exists a such that divides the length of every cycle. A graph that fails to be periodic is called aperiodic.

Example 1.4.5.

In Figure 1.13, the cycles are , , , , and . Hence the length of every cycle is and the graph is periodic.

An obvious sufficient condition for aperiodicity is existence of even one self-loop. The digraphs in Figures 1.9–1.12 are aperiodic for this reason.

The next result provides an easy way to understand aperiodicity for connected graphs. Proofs can be found in Häggström et al., (2002) and Norris, (1998).

Lemma 1.4.1.

Let be a digraph. If is strongly connected, then is aperiodic if and only if, for all , there exists a such that, for all , there exists a directed walk of length from to .

It is common to call a vertex satisfying the condition in Lemma 1.4.1 aperiodic. With this terminology, Lemma 1.4.1 states that a strongly connected digraph is aperiodic if and only if every vertex is aperiodic.

Networkx can be used to check for aperiodicity of vertices or graphs. For example, if G is a DiGraph object, then nx.is_aperiodic(G) returns True or False depending on aperiodicity of G.

1.4.1.5 Adjacency Matrices

There is a simple map between edges of a graph with fixed vertices and a binary matrix called an adjacency matrix. The benefit of viewing connections through adjacency matrices is that they bring the power of linear algebra to the analysis of digraphs. We illustrate this briefly here and extensively in §1.4.2.

Let be a digraph and let . If we enumerate the elements of , writing them as , then the adjacency matrix corresponding to is defined by121212Note that, in some applied fields, the adjacency matrix is transposed: if there is an edge from to , rather than from to . We will avoid this odd and confusing definition (which contradicts both standard graph theory and standard notational conventions in the study of Markov chains).

| (1.20) |

For example, with poor, middle, rich mapped to , the adjacency matrix corresponding to the digraph in Figure 1.10 is

| (1.21) |

An adjacency matrix provides us with enough information to recover the edges of a graph. More generally, given a set of vertices , an matrix with binary entries generates a digraph with vertices and edges equal to all with . The adjacency matrix of this graph is .

A digraph is called undirected if implies . What property does this imply on the adjacency matrix?

If is undirected, then the adjacency matrix is symmetric.

Remark 1.4.1.

The idea that a digraph can be undirected, presented in Exercise 1.4.1.5, seems contradictory. After all, a digraph is a directed graph. Another way to introduce undirected graphs is to define them as a vertex-edge pair , where each edge is an unordered pair, rather than an ordered pair . However, the definition in Exercise 1.4.1.5 is essentially equivalent and more convenient for our purposes, since we mainly study directed graphs.

Like Networkx, the QuantEcon Python library quantecon supplies a graph object that implements certain graph-theoretic algorithms. The set of available algorithms is more limited but each one is faster, accelerated by just-in-time compilation. In the case of QuantEcon’s DiGraph object, an instance is created via the adjacency matrix. For example, to construct a digraph corresponding to Figure 1.10 we use the corresponding adjacency matrix (1.21), as follows:

Let’s print the set of strongly connected components, as a list of NumPy arrays:

The output is [array([0]), array([1, 2])].

1.4.2 Weighted Digraphs

Early quantitative work on networks tended to focus on unweighted digraphs, where the existence or absence of an edge is treated as sufficient information (e.g., following or not following on social media, existence or absence of a road connecting two towns). However, for some networks, this binary measure is less significant than the size or strength of the connection.

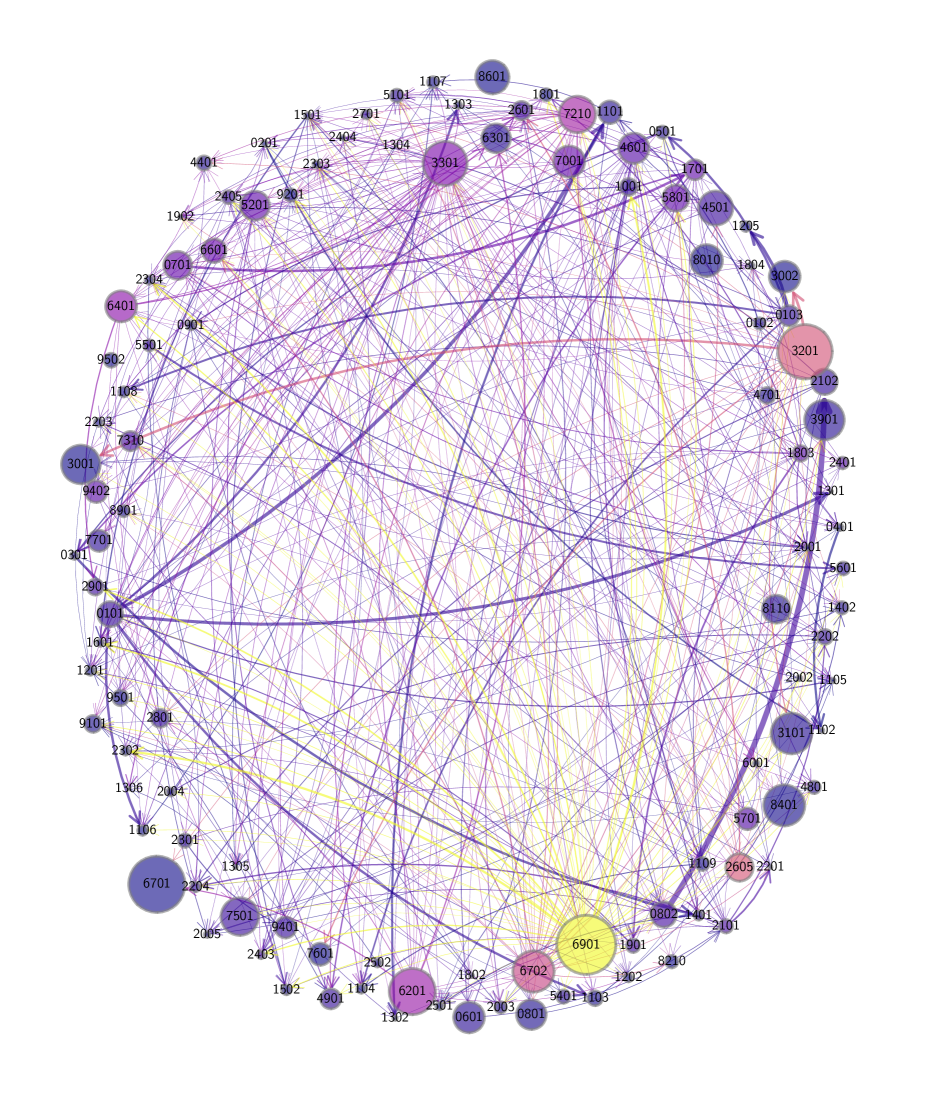

As one illustration, consider Figure 1.14, which shows flows of funds (i.e., loans) between private banks, grouped by country of origin. An arrow from Japan to the US, say, indicates aggregate claims held by Japanese banks on all US-registered banks, as collected by the Bank of International Settlements (BIS). The size of each node in the figure is increasing in the total foreign claims of all other nodes on this node. The widths of the arrows are proportional to the foreign claims they represent.131313Data for the figure was obtained from the BIS consolidated banking statistics, for Q4 of 2019. Our calculations used the immediate counterparty basis for financial claims of domestic and foreign banks, which calculates the sum of cross-border claims and local claims of foreign affiliates in both foreign and local currency. The foreign claim of a node to itself is set to zero. The country codes are given in Table 1.1.

| AU | Australia | DE | Germany | CL | Chile | ES | Spain |

|---|---|---|---|---|---|---|---|

| PT | Portugal | FR | France | TR | Turkey | GB | United Kingdom |

| US | United States | IE | Ireland | AT | Austria | IT | Italy |

| BE | Belgium | JP | Japan | SW | Switzerland | SE | Sweden |

In this network, an edge exists for almost every choice of and (i.e., almost every country in the network).141414In fact arrows representing foreign claims less than US$10 million are cut from Figure 1.14, so the network is even denser than it appears. Hence existence of an edge is not particularly informative. To understand the network, we need to record not just the existence or absence of a credit flow, but also the size of the flow. The correct data structure for recording this information is a “weighted directed graph,” or “weighted digraph.” In this section we define this object and investigate its properties.

1.4.2.1 Definitions

A weighted digraph is a triple such that is a digraph and is a function from to , called the weight function.

Remark 1.4.2.

Weights are traditionally regarded as nonnegative. In this text we insist that weights are also positive, in the sense that for all . The reason is that the intuitive notion of zero weight is understood, here and below, as absence of a connection. In other words, if has “zero weight,” then is not in , so is not defined on .

Example 1.4.6.

As suggested by the discussion above, the graph shown in Figure 1.14 can be viewed as a weighted digraph. Vertices are countries of origin and an edge exists between country and country when private banks in lend nonzero quantities to banks in . The weight assigned to edge gives total loans from to as measured according to the discussion of Figure 1.14.

Example 1.4.7.

Figure 1.15 shows a weighted digraph, with arrows representing edges of the induced digraph (compare with the unweighted digraph in Figure 1.9). The numbers next to the edges are the weights. In this case, you can think of the numbers on the arrows as transition probabilities for a household over, say, one year. For example, a rich household has a 10% chance of becoming poor.

The definitions of accessibility, communication, periodicity and connectedness extend to any weighted digraph by applying them to . For example, is called strongly connected if is strongly connected. The weighted digraph in Figure 1.15 is strongly connected.

1.4.2.2 Adjacency Matrices of Weighted Digraphs

In §1.4.1.5 we discussed adjacency matrices of unweighted digraphs. The adjacency matrix of a weighted digraph with vertices is the matrix

Clearly, once the vertices in are enumerated, the weight function and adjacency matrix provide essentially the same information. We often work with the latter, since it facilitates computations.

Example 1.4.8.

With poor, middle, rich mapped to , the adjacency matrix corresponding to the weighted digraph in Figure 1.15 is

| (1.22) |

In QuantEcon’s DiGraph implementation, weights are recorded via the keyword weighted:

One of the key points to remember about adjacency matrices is that taking the transpose “reverses all the arrows” in the associated digraph.

Example 1.4.9.

The digraph in Figure 1.16 can be interpreted as a stylized version of a financial network, with vertices as banks and edges showing flow of funds, similar to Figure 1.14 on page 1.14. For example, we see that bank 2 extends a loan of size 200 to bank 3. The corresponding adjacency matrix is

| (1.23) |

The transposition is

| (1.24) |

The corresponding network is visualized in Figure 1.17. This figure shows the network of liabilities after the loans have been granted. Both of these networks (original and transpose) are useful for analysis of financial markets (see, e.g., Chapter 5).

It is not difficult to see that each nonnegative matrix can be viewed as the adjacency matrix of a weighted digraph with vertices equal to . The weighted digraph in question is formed by setting

We call the weighted digraph induced by .

The next exercise helps to reinforce the point that transposes reverse the edges.

Let be a nonnegative matrix and let and be the weighted digraphs induced by and , respectively. Show that

-

(i)

if and only if .

-

(ii)

in if and only if in .

Let , so that for each . By definition, we have

which proves (i). Regarding (ii), to say that is accessible from in means that we can find vertices that form a directed path from to under , in the sense that such that , , and each successive pair is in . But then, by (i), provides a directed path from to under , since and each successive pair is in .

1.4.2.3 Application: Quadratic Network Games

Acemoglu et al., (2016) and Zenou, (2016) consider quadratic games with agents where agent seeks to maximize

| (1.25) |

Here , is a symmetric matrix with for all , is a parameter and is a random vector. (This is the set up for the quadratic game in §21.2.1 of Acemoglu et al., (2016).) The -th agent takes the decisions as given for all when maximizing (1.25).

In this context, is understood as the adjacency matrix of a graph with vertices , where each vertex is one agent. We can reconstruct the weighted digraph by setting and letting be all pairs in with . The weights identify some form of relationship between the agents, such as influence or friendship.

A Nash equilibrium for the quadratic network game is a vector such that, for all , the choice of agent maximizes (1.25) taking as given for all . Show that, whenever , a unique Nash equilibrium exists in and, moreover, .

Recalling that , the first order condition corresponding to (1.25), taking the actions of other players as given, is

Concatenating into a row vector and then taking the transpose yields , where we used the fact that is symmetric. Since , the condition implies that , so, by the Neumann series lemma, the unique solution is .

The network game described in this section has many interesting applications, including social networks, crime networks and peer networks. References are provided in §1.5.

1.4.2.4 Properties

In this section, we examine some of the fundamental properties of and relationships among digraphs, weight functions and adjacency matrices. Throughout this section, the vertex set of any graph we examine will be set to . This costs no loss of generality, since, in this text, the vertex set of a digraph is always finite and nonempty.

Also, while we refer to weighted digraphs for their additional generality, the results below connecting adjacency matrices and digraphs are valid for unweighted digraphs. Indeed, an unweighted digraph can be mapped to a weighted digraph by introducing a weight function that maps each element of to unity. The resulting adjacency matrix agrees with our original definition for unweighted digraphs in (1.20).

As an additional convention, if is an adjacency matrix, and is the -th power of , then we write for a typical element of . With this notation, we observe that, since , the rules of matrix multiplication imply

| (1.26) |

( is the identity.) The next proposition explains the significance of the powers.

Proposition 1.4.2.

Let be a weighted digraph with adjacency matrix . For distinct vertices and , we have

Proof.

( ). The statement is true by definition when . Suppose in addition that holds at , and suppose there exists a directed walk of length from to . By the induction hypothesis we have . Moreover, is part of a directed walk, so . Applying (1.26) now gives .

(). Left as an exercise (just use the same logic). ∎

Example 1.4.10.

In this context, the next result is fundamental.

Theorem 1.4.3.

Let be a weighted digraph. The following statements are equivalent:

-

(i)

is strongly connected.

-

(ii)

The adjacency matrix generated by is irreducible.

Proof.

Let be a weighted digraph with adjacency matrix . By Proposition 1.4.2, strong connectedness of is equivalent to the statement that, for each , we can find a such that . (If then set .) This, in turn, is equivalent to , which is irreducibility of . ∎

Example 1.4.11.

We will find that the property of being primitive is valuable for analysis. (The Perron–Frobenius Theorem hints at this.) What do we need to add to strong connectedness to obtain primitiveness?

Theorem 1.4.4.

For a weighted digraph , the following statements are equivalent:

-

(i)

is strongly connected and aperiodic.

-

(ii)

The adjacency matrix generated by is primitive.

Proof of Theorem 1.4.4.

Throughout the proof we set . First we show that, if is aperiodic and strongly connected, then, for all , there exists a such that whenever . To this end, pick any in . Since is strongly connected, there exists an such that . Since is aperiodic, we can find an such that implies . Picking and applying (1.26), we have

Thus, with , we have whenever .

((i) (ii)). By the preceding argument, given any , there exists an such that whenever . Setting over all yields .

((ii) (i)). Suppose that is primitive. Then, for some , we have . Strong connectedness of the digraph follows directly from Proposition 1.4.2. It remains to check aperiodicity.

Aperiodicity will hold if we can establish that for all . To show this, it suffices to show that for all . Moreover, to prove the latter, we need only show that , since the claim then follows from induction.

To see that , observe that, for any given , the relation (1.26) implies

where . The proof will be done if . But this must be true, since otherwise vertex is a sink, which contradicts strong connectedness. ∎

Example 1.4.12.

In Exercise 1.2.3.1 we worked hard to show that is irreducible if and only if , using the approach of calculating and then examining the powers of (as shown in (1.2)). However, the result is trivial when we examine the corresponding digraph in Figure 1.3 and use the fact that irreducibility is equivalent to strong connectivity. Similarly, the result in Exercise 1.2.3.1 that is primitive if and only if and becomes much easier to establish if we examine the digraph and use Theorem 1.4.4.

1.4.3 Network Centrality

When studying networks of all varieties, a recurring topic is the relative “centrality” or “importance” of different nodes. One classic application is the ranking of web pages by search engines. Here are some examples related to economics:

-

•

In which industry will one dollar of additional demand have the most impact on aggregate production, once we take into account all the backward linkages? In which sector will a rise in productivity have the largest effect on national output?

-

•

A negative shock endangers the solvency of the entire banking sector. Which institutions should the government rescue, if any?

-

•

In the network games considered in §1.4.2.3, the Nash equilibrium is . Players’ actions are dependent on the topology of the network, as encoded in . A common finding is that the level of activity or effort exerted by an agent (e.g., severity of criminal activity by a participant in a criminal network) can be predicted from their “centrality” within the network.

In this section we review essential concepts related to network centrality.151515Centrality measures are sometimes called “influence measures,” particularly in connection with social networks.

1.4.3.1 Centrality Measures

Let be the set of weighted digraphs. A centrality measure associates to each in a vector , where the -th element of is interpreted as the centrality (or rank) of vertex . In most cases is nonnegative. In what follows, to simplify notation, we take .

(Unfortunately, the definitions and terminology associated with even the most common centrality measures vary widely across the applied literature. Our convention is to follow the mathematicians, rather than the physicists. For example, our terminology is consistent with Benzi and Klymko, (2015).)

1.4.3.2 Authorities vs Hubs

Search engine designers recognize that web pages can be important in two different ways. Some pages have high hub centrality, meaning that they link to valuable sources of information (e.g., news aggregation sites) . Other pages have high authority centrality, meaning that they contain valuable information, as indicated by the number and significance of incoming links (e.g., websites of respected news organizations). Figure 1.19 helps to visualize the difference.

Similar ideas can and have been applied to economic networks (often using different terminology). For example, in production networks we study below, high hub centrality is related to upstreamness: such sectors tend to supply intermediate goods to many important industries. Conversely, a high authority ranking will coincide with downstreamness.

In what follows we discuss both hub-based and authority-based centrality measures, providing definitions and illustrating the relationship between them.

1.4.3.3 Degree Centrality

Two of of the most elementary measures of “importance” of a vertex in a given digraph are its in-degree and out-degree. Both of these provide a centrality measure. In-degree centrality is defined as the vector . Out-degree centrality is defined as . If is expressed as a Networkx DiGraph called G (see, e.g., §1.4.1.2), then can be calculated via

This method is relatively slow when is a large digraph. Since vectorized operations are generally faster, let’s look at an alternative method using operations on arrays.

To illustrate the method, recall the network of financial institutions in Figure 1.16. We can compute the in-degree and out-degree centrality measures by first converting the adjacency matrix, which is shown in (1.23), to a binary matrix that corresponds to the adjacency matrix of the same network viewed as an unweighted graph:

| (1.27) |

Now if and only if points to . The out-degree and in-degree centrality measures can be computed as

| (1.28) |

respectively. That is, summing the rows of gives the out-degree centrality measure, while summing the columns gives the in-degree measure.

The out-degree centrality measure is a hub-based ranking, while the vector of in-degrees is an authority-based ranking. For the financial network in Figure 1.16, a high out-degree for a given institution means that it lends to many other institutions. A high in-degree indicates that many institutions lend to it.

Notice that, to switch from a hub-based ranking to an authority-based ranking, we need only transpose the (binary) adjacency matrix . We will see that the same is true for other centrality measures. This is intuitive, since transposing the adjacency matrices reverses the direction of the edges (Exercise 1.4.2.2).

For a weighted digraph with adjacency matrix , the weighted out-degree centrality and weighted in-degree centrality measures are defined as

| (1.29) |

respectively, by analogy with (1.28). We present some intuition for these measures in applications below.

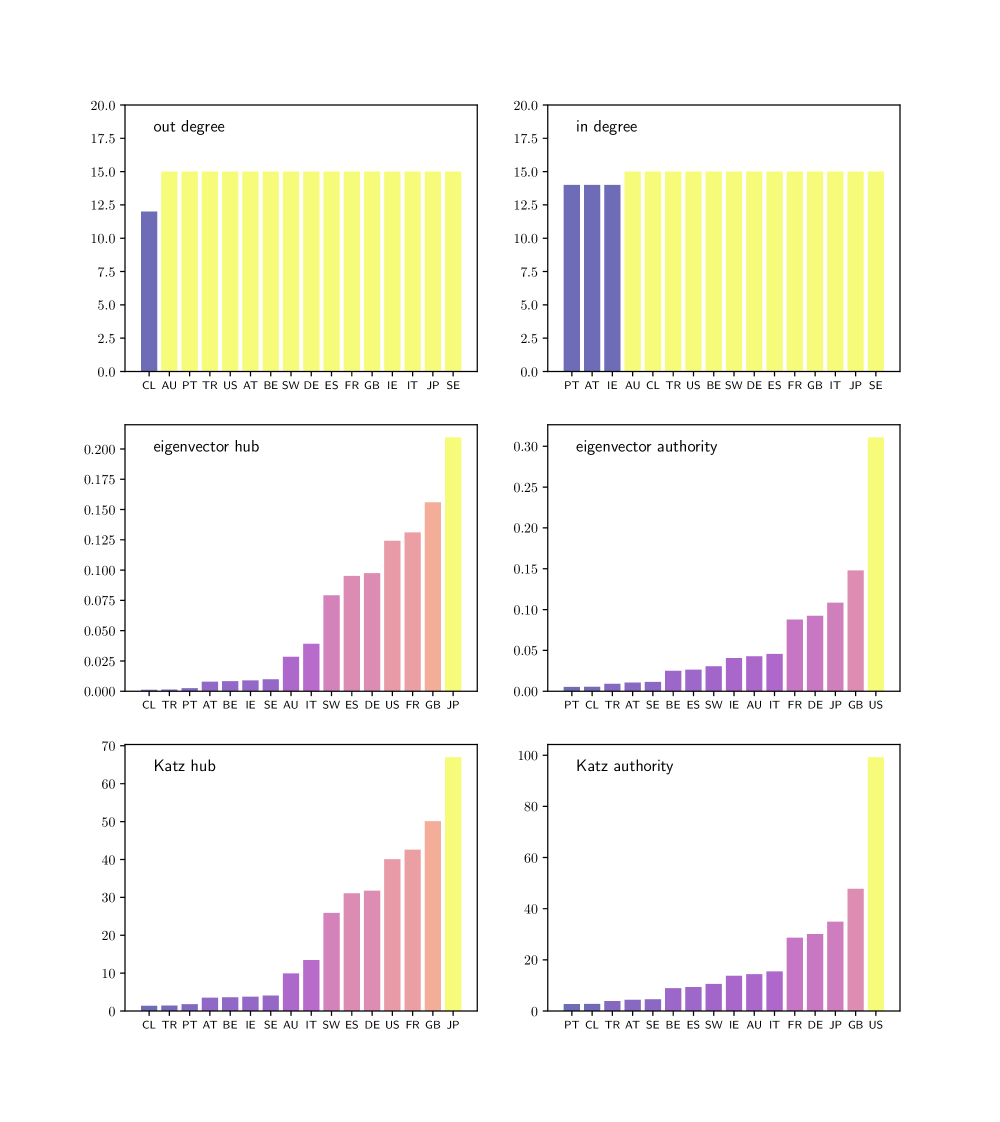

Unfortunately, while in- and out-degree measures of centrality are simple to calculate, they are not always informative. As an example, consider again the international credit network shown in Figure 1.14. There, an edge exists between almost every node, so the in- or out-degree based centrality ranking fails to effectively separate the countries. This can be seen in the out-degree ranking of countries corresponding to that network in the top left panel of Figure 1.20, and in the in-degree ranking in the top right.

There are other limitations of degree-based centrality rankings. For example, suppose web page A has many inbound links, while page B has fewer. Even though page A dominates in terms of in-degree, it might be less important than web page B to, say, a potential advertiser, when the links into B are from more heavily trafficked pages. Thinking about this point suggests that importance can be recursive: the importance of a given node depends on the importance of other nodes that link to it. The next set of centrality measures we turn to has this recursive property.

1.4.3.4 Eigenvector Centrality

Let be a weighted digraph with adjacency matrix . Recalling that is the spectral radius of , the hub-based eigenvector centrality of is defined as the that solves

| (1.30) |

Element-by-element, this is

| (1.31) |

Note the recursive nature of the definition: the centrality obtained by vertex is proportional to a sum of the centrality of all vertices, weighted by the “rates of flow” from into these vertices. A vertex is highly ranked if (a) there are many edges leaving , (b) these edges have large weights, and (c) the edges point to other highly ranked vertices.

When we study demand shocks in §2.1.3, we will provide a more concrete interpretation of eigenvector centrality. We will see that, in production networks, sectors with high hub-based eigenvector centrality are important suppliers. In particular, they are activated by a wide array of demand shocks once orders flow backwards through the network.

Show that (1.31) has a unique solution, up to a positive scalar multiple, whenever is strongly connected.

When is strongly connected, the Perron–Frobenius theorem tells us that and has a unique (up to a scalar multiple) dominant right eigenvector satisfying . Rearranging gives (1.31).161616While the dominant eigenvector is only defined up to a positive scaling constant, this is no reason for concern, since positive scaling has no impact on the ranking. In most cases, users of this centrality ranking choose the dominant eigenvector satisfying .

As the name suggests, hub-based eigenvector centrality is a measure of hub centrality: vertices are awarded high rankings when they point to important vertices. The next two exercises help to reinforce this point.

Show that nodes with zero out-degree always have zero hub-based eigenvector centrality.

To compute eigenvector centrality when the adjacency matrix is primitive, we can employ the Perron–Frobenius Theorem, which tells us that as , where and are the dominant left and right eigenvectors of . This implies

| (1.32) |

Thus, evaluating at large returns a scalar multiple of . The package Networkx provides a function for computing eigenvector centrality via (1.32).

One issue problem with this method is the assumption of primitivity, since the convergence in (1.32) can fail without it. The following function uses an alternative technique, based on Arnoldi iteration, which generally works even when primitivity fails. (The authority option is explained below.)

Show that the digraph in Figure 1.21 is not primitive. Using the code above or another suitable routine, compute the hub-based eigenvector centrality rankings. You should obtain values close to . Note that the sink vertex (vertex 4) obtains the lowest rank.

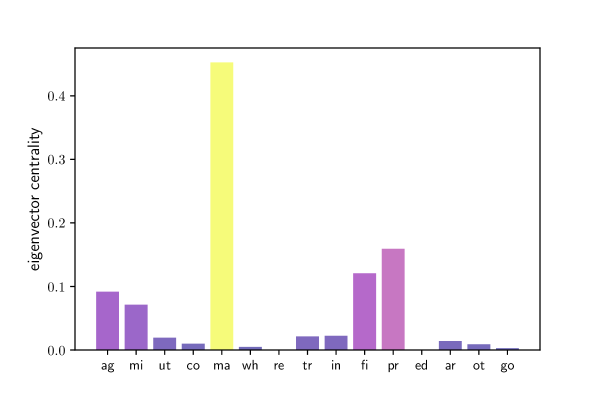

The middle left panel of Figure 1.20 shows the hub-based eigenvector centrality ranking for the international credit network shown in Figure 1.14. Countries that are rated highly according to this rank tend to be important players in terms of supply of credit. Japan takes the highest rank according to this measure, although countries with large financial sectors such as Great Britain and France are not far behind. (The color scheme in Figure 1.14 is also matched to hub-based eigenvector centrality.)

The authority-based eigenvector centrality of is defined as the solving

| (1.33) |

The difference between (1.33) and (1.31) is just transposition of . (Transposes do not affect the spectral radius of a matrix.) Element-by-element, this is

| (1.34) |

We see will be high if many nodes with high authority rankings link to .

The middle right panel of Figure 1.20 shows the authority-based eigenvector centrality ranking for the international credit network shown in Figure 1.14. Highly ranked countries are those that attract large inflows of credit, or credit inflows from other major players. The US clearly dominates the rankings as a target of interbank credit.

Assume that is strongly connected. Show that authority-based eigenvector centrality is uniquely defined up to a positive scaling constant and equal to the dominant left eigenvector of .

1.4.3.5 Katz Centrality

Eigenvector centrality can be problematic. Although the definition in (1.31) makes sense when is strongly connected (so that, by the Perron–Frobenius theorem, ), strong connectedness fails in many real world networks. We will see examples of this in §2.1, for production networks defined by input-output matrices.

In addition, while strong connectedness yields strict positivity of the dominant eigenvector, many vertices can be assigned a zero ranking when it fails (see, e.g., Exercise 1.4.3.4). This zero ranking often runs counter to our intuition when we examine specific networks.

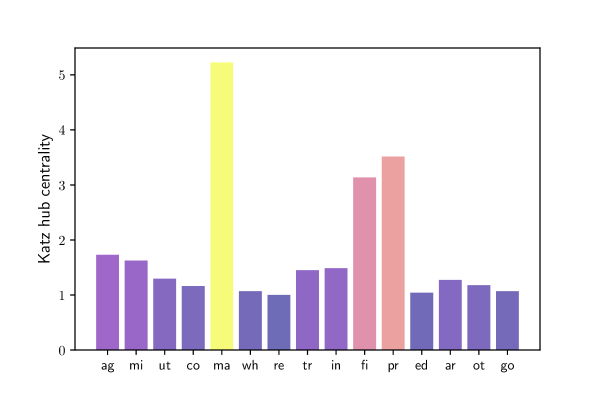

Considerations such as these encourage use of an alternative notion of centrality for networks called Katz centrality, originally due to Katz, (1953), which is positive under weaker conditions and uniquely defined up to a tuning parameter. Fixing in , the hub-based Katz centrality of weighted digraph with adjacency matrix , at parameter , is defined as the vector that solves

| (1.35) |

The intuition is very similar to that provided for eigenvector centrality: high centrality is conferred on when it is linked to by vertices that themselves have high centrality. The difference between (1.35) and (1.31) is just in the additive constant .

Show that, under the stated condition , hub-based Katz centrality is always finite and uniquely defined by

| (1.36) |

where is a column vector of ones.

When we have . Hence, we can express (1.35) as and employ the Theorem 1.2.5 to obtain the stated result.

We know from the Perron–Frobenius theorem that the eigenvector centrality measure will be everywhere positive when the digraph is strongly connected. A condition weaker than strong connectivity is that every vertex has positive out-degree. Show that the Katz measure of centrality is strictly positive on each vertex under this condition.

The attenuation parameter is used to ensure that is finite and uniquely defined under the condition . It can be proved that, when the graph is strongly connected, hub-based (resp., authority-based) Katz centrality converges to the hub-based (resp., authority-based) eigenvector centrality as .171717See, for example, Benzi and Klymko, (2015). This is why, in the bottom two panels of Figure 1.20, the hub-based (resp., authority-based) Katz centrality ranking is seen to be close to its eigenvector-based counterpart.

When , we use as the default for Katz centrality computations.

Compute the hub-based Katz centrality rankings for the simple digraph in Figure 1.21 when . You should obtain . Hence, the source vertex (vertex 1) obtains equal highest rank and the sink vertex (vertex 4) obtains the lowest rank.

Analogously, the authority-based Katz centrality of is defined as the that solves

| (1.37) |

Show that, under the restriction , the unique solution to (1.37) is given by

| (1.38) |

(Verify the stated equivalence.)