Forecast Evaluation for Data Scientists: Common Pitfalls and Best Practices

Abstract

Machine Learning (ML) and in particular Deep Learning (DL) methods nowadays are increasingly replacing traditional methods in many different domains involved with important decision making activities. Sophisticated DL techniques tailor-made for specific tasks such as image recognition, signal processing, or speech analysis are being introduced at a fast pace with many improvements. However, for the domain of time series forecasting, the current state in the ML community is perhaps where other domains such as Natural Language Processing and Computer Vision were at several years ago. The field of forecasting has mainly been fostered by statisticians/econometricians; consequently the related concepts are not the mainstream knowledge among general ML practitioners. The different forms of non-stationarities associated with time series challenge the capabilities of data-driven ML models. Nevertheless, recent trends in the domain have demonstrated that with the availability of massive amounts of time series, ML and DL techniques are quite competent in time series forecasting, when related pitfalls are properly handled. Therefore, in this work we provide a tutorial-like compilation of the details of one of the most important steps in the overall forecasting process, namely the evaluation. This way, we intend to impart the information associated with forecast evaluation to fit the context of ML, as means of bridging the knowledge gap between traditional methods of forecasting and current state-of-the-art ML techniques. We elaborate the details of the different problematic characteristics of time series such as non-normalities and non-stationarities and how they are associated with common pitfalls in forecast evaluation. Best practices in forecast evaluation are outlined with respect to the different steps such as data partitioning, error calculation, statistical testing, and others. Further guidelines are also provided along selecting valid and suitable error measures depending on the specific characteristics of the dataset at hand.

1 Introduction

In the present era of Big Data, Machine Learning (ML) and Deep Learning (DL) based techniques are driving the automatic decision making in many domains such as Natural Language Processing (NLP) or Time Series Classification (TSC, Bagnall et al., 2016; Fawaz et al., 2019). Although fields such as NLP and Computer Vision have heavily been dominated by ML and DL based techniques for decades by now, this has hardly been the case for the field of forecasting, until very recently. Forecasting was traditionally the field of statisticians and econometricians. However, nowadays, with many companies hiring data scientists, often these data scientists are tasked with forecasting. Therefore, now in many situations practitioners are tasked with forecasting that have a good background in ML and data science, but that are not aware of the decades of research in the forecasting space. This involves many aspects of the process of forecasting, from the point of data pre-processing, building models to final forecast evaluation. Due to the self-supervised and sequential nature of forecasting tasks, it is often associated with many pitfalls that usual ML practitioners are not aware of. Out of all these aspects, in this particular work, we focus on the evaluation of point forecasts as a key step in the overall process of forecasting.

Evaluating the performance of models is key to the development of concepts and practices in any domain. The general process involves employing a number of models having different characteristics, training them on a training dataset and then applying them on a validation set afterwards. Then, model selection may be performed by evaluating on the validation set to select the best models. Otherwise, ensemble models may be developed instead, by combining the forecasts from all the different models, and usually a final evaluation is then performed on a test set. In research areas such as classification and regression, there are well-established standard practices for evaluation. Data partitioning is performed by using a standard k-fold Cross-Validation (CV) to tune the model hyperparameters based on the error on a validation sets, the model with the best hyperparameter combination is tested on the testing set, standard error measures such as squared errors, absolute errors or precision, recall, area under curve are computed and finally the best models are selected. These best methods may continue to deliver reasonable predictions for a certain problem task, i.e., they generalise well, under the assumption that there are no changes of the distribution of the underlying data, which otherwise would need to be addressed as concept drift (Webb et al., 2016; Ghomeshi et al., 2019; Ikonomovska et al., 2010) or non-stationarity.

In contrast, evaluating forecasting models can be a surprisingly complicated task. Data partitioning and model selection have many different options in the context of forecasting, including fixed origin, rolling origin evaluation and other CV setups as well as controversial arguments associated with them. Due to the inherent non-independence, non-stationarities and non-normalities of time series, these choices are complex. Also, most error measures are susceptible to break down under certain of these conditions. Other considerations are whether to summarise errors across all available time series or consider different steps of the forecast horizon separately etc. As a consequence, without wanting to call them out here, we regularly come across papers in top AI/ML conferences and journals (even winning best paper awards) that use inadequate and miss-leading benchmark methods for comparison (e.g., non-seasonal models for long-term forecasting on seasonal series), others that use mean absolute percentage error (MAPE) for evaluation with series, e.g., with values in the interval because the authors think the MAPE is a somewhat generic “time series error measure”, even though MAPE is clearly inadequate in such settings. Other works make statements along the lines of ARIMA being able to tackle non-stationarity whereas ML models can’t, neglecting that the only thing ARIMA does is a differencing of the series as a pre-processing step to address non-stationarity. A step that can easily be done as preprocessing for any ML method as well. In other works, we see methods compared using MAE as the error measure, and only the proposed method by those authors is trained with L1 loss, all other competitors with L2 loss, which leads to unfair comparisons as the L1 loss optimises towards MAE, whereas the L2 loss optimises towards RMSE. Many other works evaluate on a handfull of somewhat randomly picked time series and then show plots of forecasts versus actuals as “proof” of how well their method works, without considering simple benchmarks or meaningful error measures, and other similar problems. Also, frequently forecasting competitions and research works introduce new evaluation measures and methodologies, sometimes neglecting the prior research, e.g., by seemingly not understanding that dividing a series by its mean will not solve scaling issues for many types of non-stationarities (e.g., strong trends). Thus, there is no generally accepted standard for forecast evaluation in every possible scenario. This gap has harmed progress in ML methods for forecasting significantly in the past. It is damaging the area currently, with spurious results in many papers, with researchers new to the field not being able to distinguish between methods that work and methods that don’t, and the associated slower progress and waste of resources.

Overall, this article makes an effort in the direction of raising awareness among ML practitioners regarding the best practices and pitfalls associated with the different steps of the point forecast evaluation process. Similar exhaustive efforts have been taken in the literature to review, formally define and categorise other important concepts in the ML domain such as concept drift (Webb et al., 2016) and mining statistically sound patterns from data (Hämäläinen and Webb, ). The rest of this paper is structured as follows. Section 2 first introduces terminology associated with the domain of forecasting. Next, Section 3 details the motivation for this article, including an introduction to the different forms of non-stationarities/non-normalities seen in time series data, along with common pitfalls related to using competitive benchmarks, visualisation of results using forecast plots and avoiding data leakage in forecast evaluation. Then, Section 4 presents an overview of the process of forecast evaluation. In Section 5, we provide a tutorial/guideline around how to best partition the data for a given forecasting problem such that it is not affecting the sequential nature or the non-stationarities involved with the problem. Section 6 first presents a comprehensive literature review of many different evaluation measures proposed over the years. This is supplemented by a critical analysis of how each of them can break/fail under different circumstances of the time series. This section also provides a guideline on selecting evaluation measures depending on the characteristics of the time series under consideration. In Section 7, we provide details of popular techniques used for statistical testing for significance of differences between models. Finally, Section 8 concludes the paper by summarising the overall content of the paper and highlighting the best practices for forecast evaluation.

2 Problem Definition and Terminology

The scope of the discussion in this article focusses on point forecasting, where the interest is to predict one particular statistic (mean/median) of the overall forecast distribution. However, we note that there are many works in the literature around predicting distributions and evaluating accordingly. In this section we provide a general overview of the terminology used in the context of time series forecasting.

Throughout this article, we focus on the task of univariate forecasting. Univariate forecasting is when future values of a time series are predicted using the past values of that same series as well as some other exogenous time varying variables which may affect the target series. This can be formulated as in Equation 1.

| (1) |

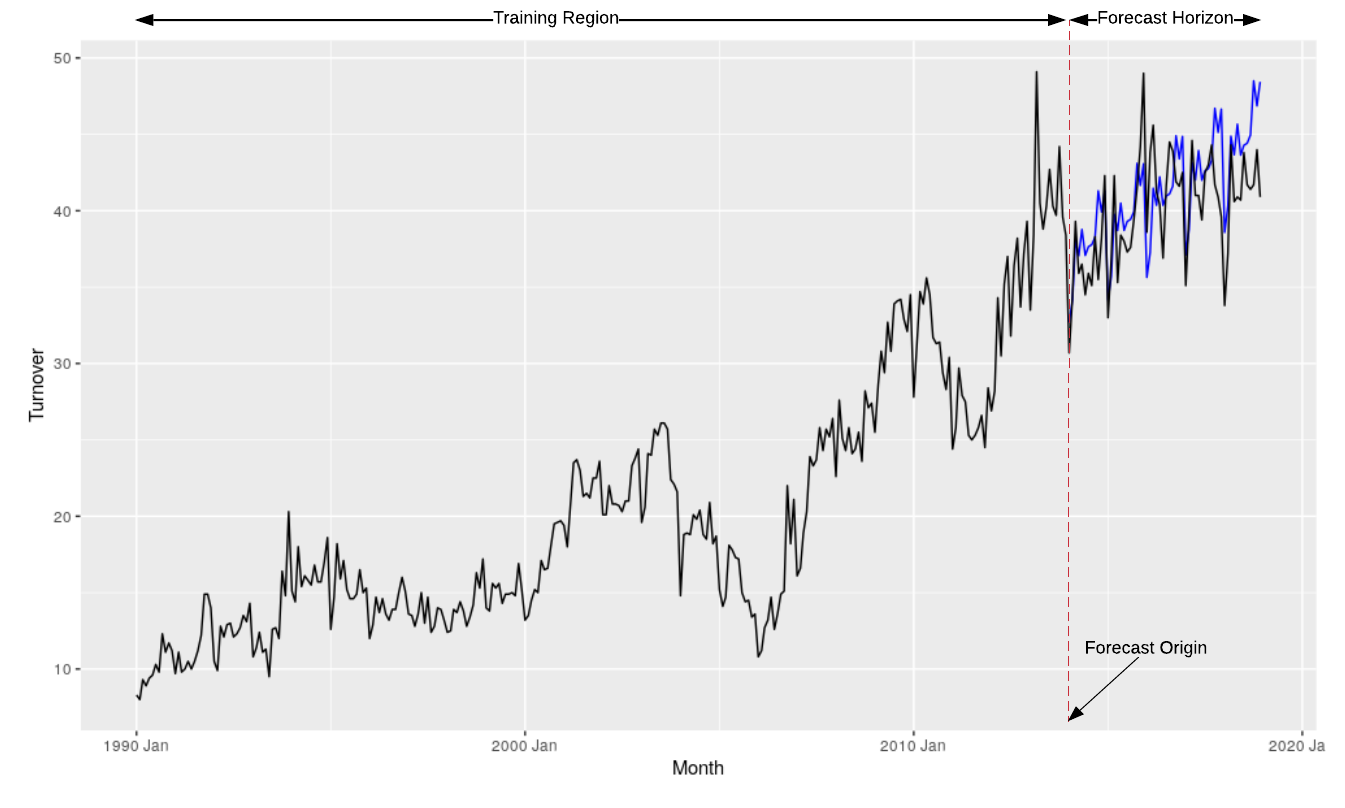

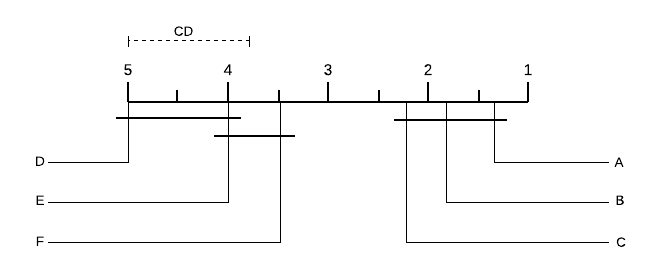

Here, is a (non-linear, non-parametric) function, for example an ML model and are its parameters. are all input data and information available to the model up until time where is the forecast origin. Therefore, forecast origin is the last known data point from which the forecasting begins. denotes the forecast horizon, i.e. the length of the time period into the future for which forecasting of the target value is performed. These are indicated in Figure 1.

Traditionally, in univariate forecasting without external variables, . With external variables, contains also the values of the external variables, up to time or also future values if known. We do not consider multivariate regression in this work, where to predict the future values of many target series together, past values of all series as well as other potentially available external variables are used.

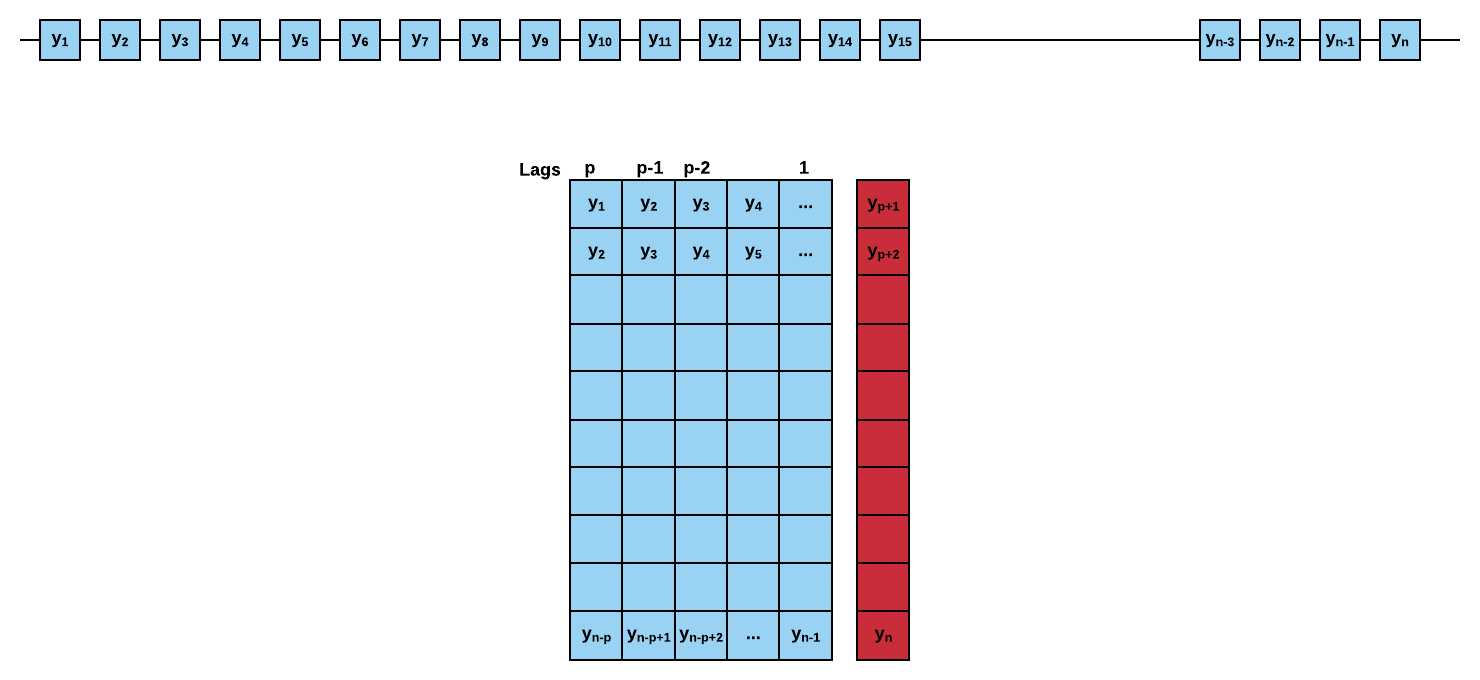

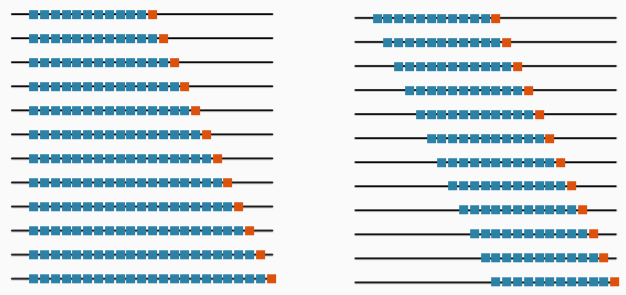

In a time series context, we define a lag with respect to a time step as the values of the series at previous time steps. For example, lag 1 is the value at time step and lag m is the value at time step . In a so-called Auto-Regression (AR), in Equation 1 only goes back a fixed amount of lags, usually called the model order. The very name indicates that the regression is performed against the values of the target series itself. An auto-regression of a time series uses an embedded matrix. In the embedded matrix in Figure 2, when the model order is , every row has consecutive observations from the time series. During model training, every row is considered a separate data instance, where values at lags are considered predictors for the target quantity of the time series at time step . The process goes through the whole series, shifting the target quantity by one time step in each row, to form a matrix. Therefore, in an AR setup of order on a series of length , the number of data instances for training is equivalent to .

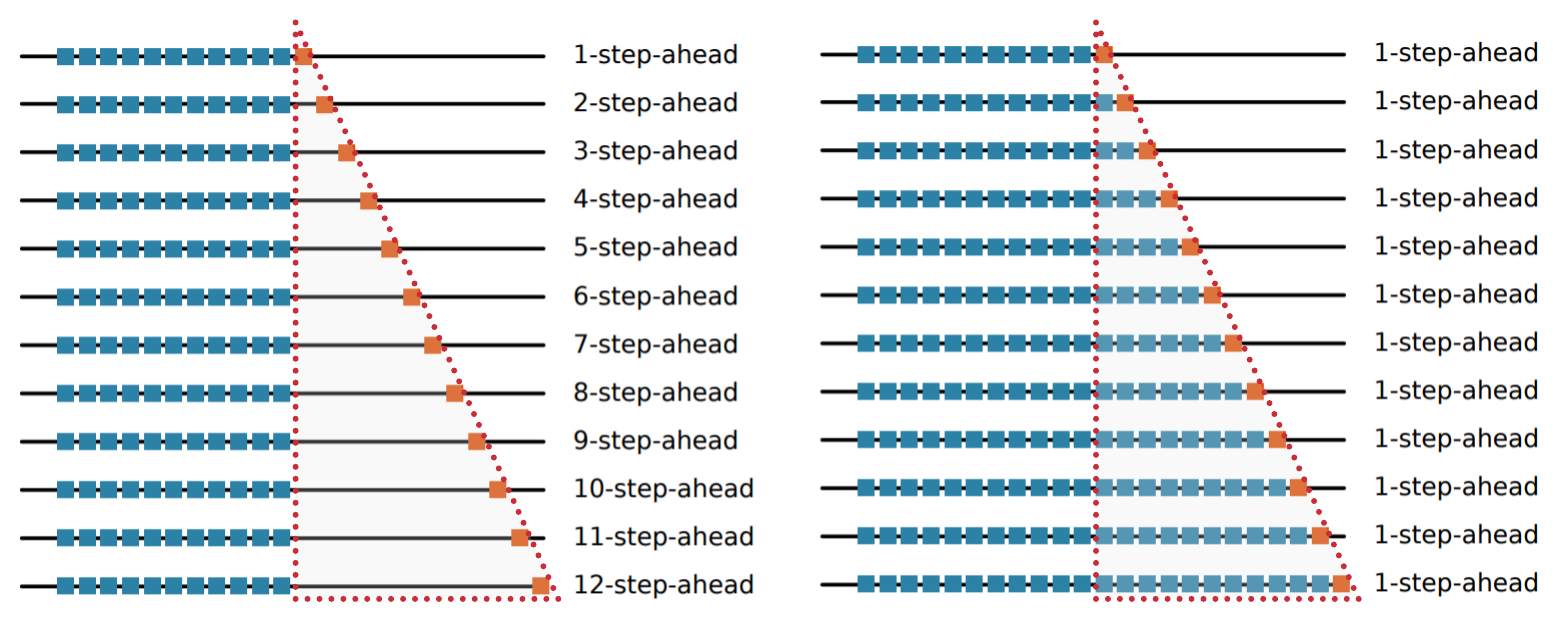

Using this notion of univariate forecasting, both local models and global models can be developed. For a local model, the parameters of the model are trained only using one series. Therefore, in the scenario where many time series are available, local models need to be developed as one per each series. On the other hand, for global models, the parameters are trained across time series, i.e., using data from all the series. Thus, the embedded matrix contains data instances from many series. However, for the prediction of a single series, in Equation 1 only considers the corresponding lags of that particular series (Januschowski et al., 2020). Similar to other ML tasks, validation and test sets are used for hyperparameter tuning of the models and for testing. Evaluations on validation and test sets are often called out-of-sample (OOS) evaluations in forecasting. The two main setups for OOS evaluation in forecasting are fixed origin evaluation and rolling origin evaluation (Tashman, 2000). Figure 3 shows the difference between the two setups. In the fixed origin setup, the forecast origin is fixed as well as the training region, and the forecasts are computed as one-step ahead or multi-step ahead depending on the requirements. In the rolling origin setup, the size of the forecast horizon is fixed, but the forecast origin changes over the time series (rolling origin), thus effectively creating multiple test periods for evaluation. With every new forecast origin, new data becomes available for the model which can be used for re-fitting of the model. However, as seen on Figure 3, since the rolling origin setup allows the data to pass on from the testing set to the training set of the next consecutive evaluation step, this setup, if not used properly, is naturally susceptible to data leakage dangers, where information of the future may leak to the model training phase using past data (further discussed in Section 3.4). The rolling origin setup is also called time series cross-validation (tsCV) and prequential evaluation in the literature (Hyndman and Athanasopoulos, 2018; Gama et al., 2013). Further details of these approaches are discussed in Section 5.

3 Motivation and Common Pitfalls

This section is devoted to provide the motivation of our work and we discuss the general problems faced in forecasting, in comparison to a usual ML task.

3.1 Characteristics of Time Series

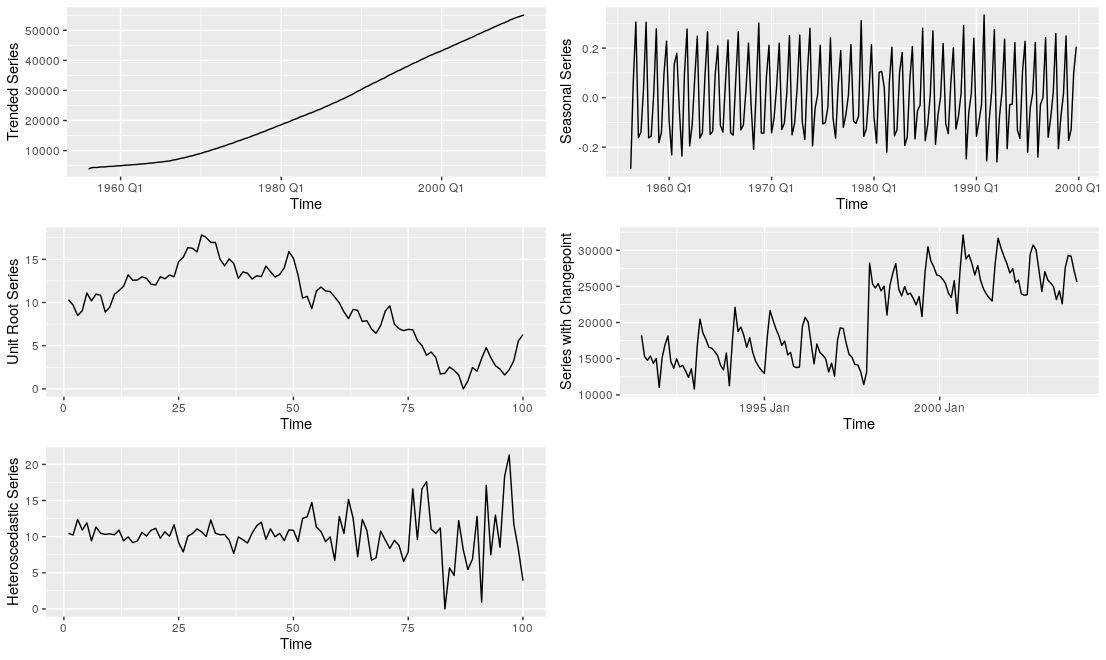

What makes time series forecasting a more difficult problem in comparison to other ML tasks, are the different non-stationarities and non-normalities commonly embedded in time series. Listed below are some of such possibly problematic characteristics of time series.

-

1.

Non-stationarities.

-

(a)

Seasonality

-

(b)

Trends (Deterministic, e.g., Linear/Exponential)

-

(c)

Stochastic Trends / Unit Roots

-

(d)

Heteroscedasticity

-

(e)

Structural Breaks (sudden changes, often with level shifts)

-

(a)

-

2.

Non-normality

-

(a)

Non-symmetric distributions

-

(b)

Fat tails

-

(c)

Intermittency

-

(d)

Outliers

-

(a)

-

3.

Series with very short history

Non-stationarity in general means that the distribution of the data in the time series is not constant, but it changes depending on the time (see, e.g., Salles et al., 2019). What we refer to as non-stationarity in this work is the violation of strong stationarity defined as in Equation 2 (Cox and Miller, 1965). Strong stationarity is defined as the distribution of a finite window (sub-sequence) of a time series (discrete-time stochastic process) remaining the same as we shift the window across time. In Equation 2, refers to the time series value at time step ; is the size of the shift of the window and is the size of the window. refers to the cumulative distribution function of the joint distribution of . Hence, according to Equation 2, is not a function of time, it does not depend on the shift of the window. In the rest of this paper, we refer to the violation of strong stationarity simply as non-stationarity.

| (2) |

Figure 4 gives an example of possible problems when building ML models on such data, where the models fail to produce reasonable forecasts as the range of values is different in the training and test sets. Different types of non-stationarities are illustrated in Figure 5. Seasonality usually means that the mean of the series changes periodically over time, with a fixed length periodicity. Trends can be twofold; 1) deterministic trends - change the mean of the series 2) stochastic trends (resulting from unit roots) - change both the mean and variance of the series (Salles et al., 2019). Note that neither trend nor seasonality are concepts that have precise formal definitions. They are usually merely defined as smoothed versions of the time series, where for the seasonality the smoothing occurs over particular seasons (e.g., in a daily series, the series of all Mondays needs to be smooth, etc.). Heteroscedasticity changes the variance of the series and structural breaks can change the mean or other properties of the series. Structural break is a term used in Econometrics and Statistics in a time series context to describe a sudden change in the series. It therewith has considerable overlap with the notion of sudden concept drift in an ML environment, where a sudden change of the data distribution is observed (Webb et al., 2016).

On the other hand, data can be far from normality, for example having fat tails, or when conditions such as outliers or intermittency are observed in the series. Non-stationarities and non-normalities are both seen quite commonly in many real-world time series and the decisions taken during forecast evaluation depend on which of these characteristics the series have. There is no single universal rule that applies to every scenario.

3.2 Benchmarks for Forecast Evaluation

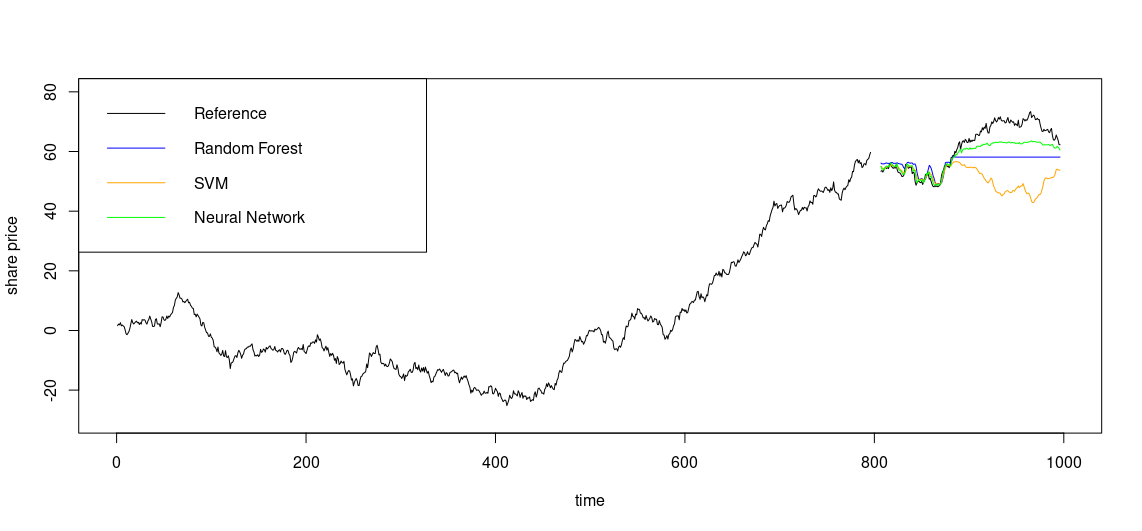

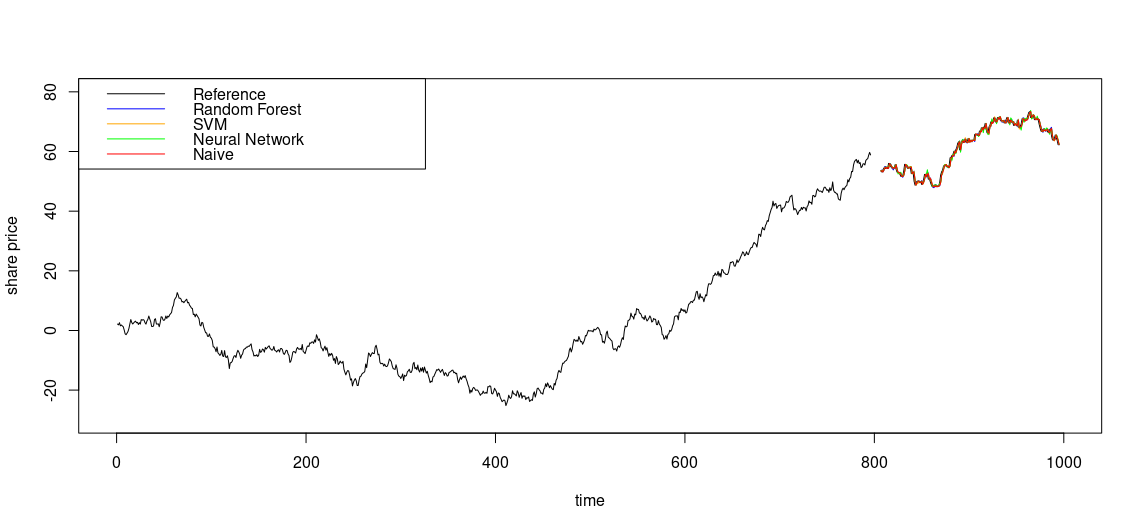

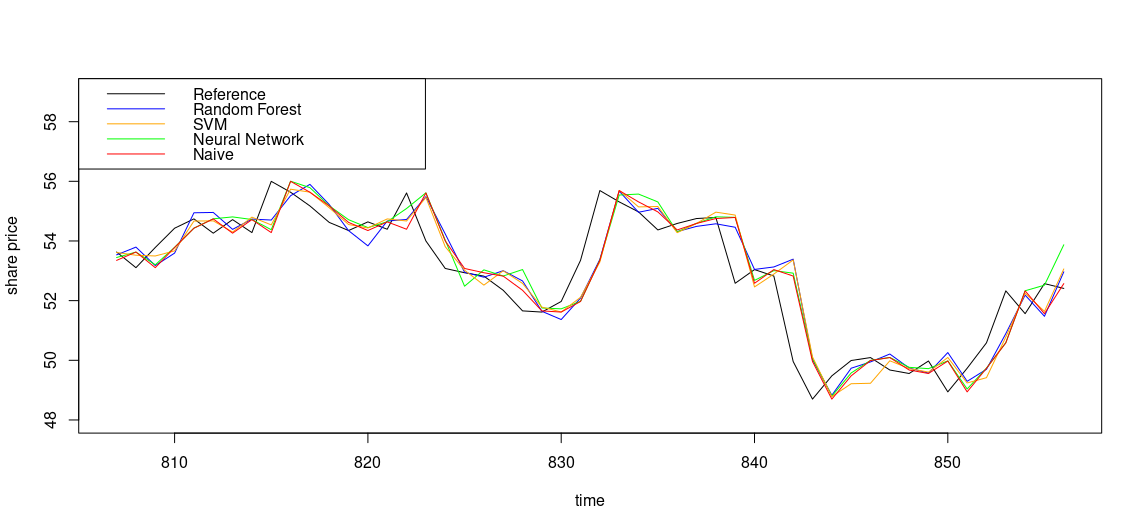

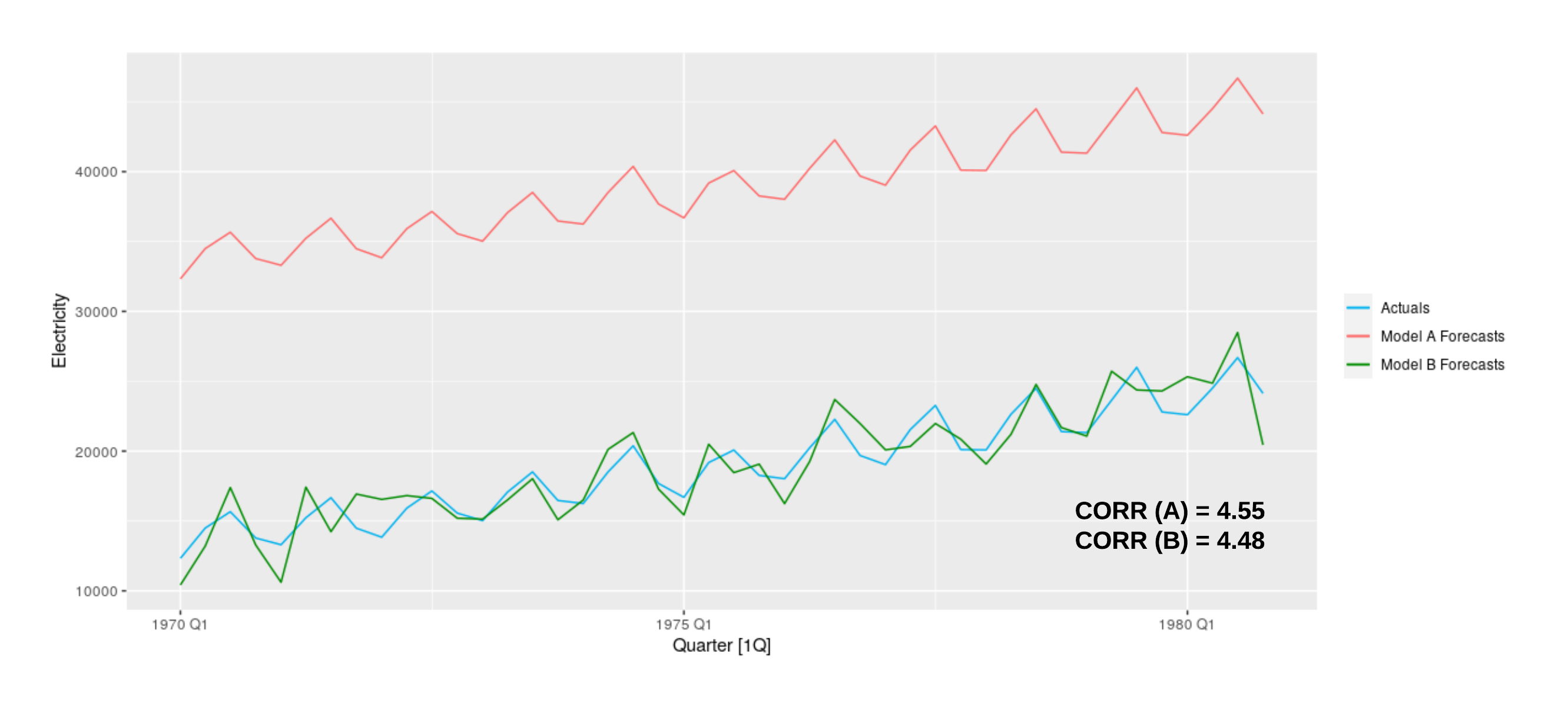

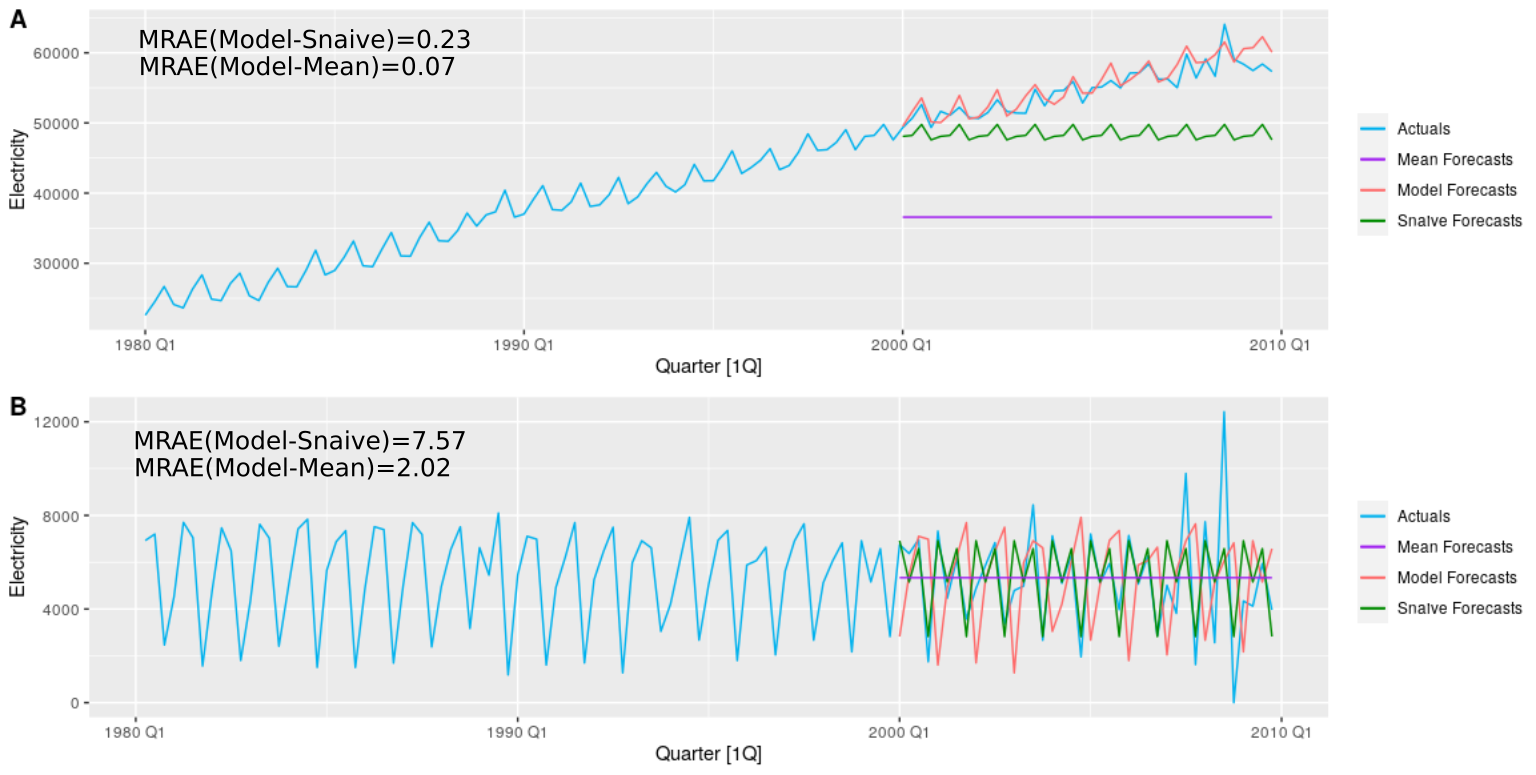

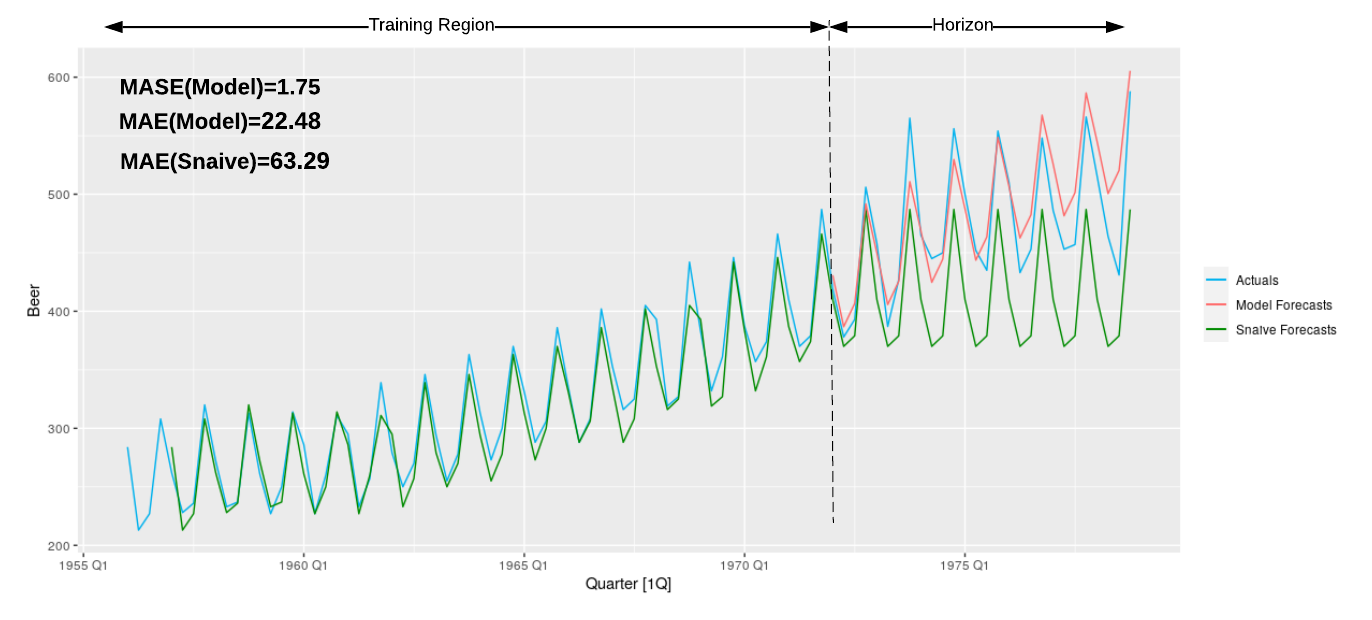

Benchmarks are an important part of forecast evaluation. Comparison against the right benchmarks and especially the simpler ones is essential. Arguably the simplest benchmark that is commonly employed in forecasting is the naïve forecast, also called persistence model or no-change model, that simply uses the last known observation as the forecast. It has demonstrated competitive performance in many scenarios (Armstrong, 2001). Figure 6 illustrates the behaviour of different models that have been trained with differencing as appropriate preprocessing on a series that has a unit root based non-stationarity. If the series has no further predictable properties above the unit root, i.e., it is a random walk where the innovation added to the last observation follows a normal distribution with a mean of zero, the naïve forecast is the theoretically best forecast. Other, more complex forecasting methods in this scenario will have no true predictive power beyond the naïve method, and any superiority, e.g., in error evaluations is by pure chance, and should be able to be identified as a spurious result on sufficiently large datasets.

Equation 3 shows the definition of a random walk, where is white noise; i.e. sampled from a normal distribution. Accordingly, the naïve forecast at any time step in the horizon can be defined as in Equation 4. As the naïve forecast is the last known observation, the forecast is a shifted version of the time series where the forecast simply follows the actuals (see Figure 6(b)).

| (3) |

| (4) |

In many practical applications, we find series that show strongly integrated behaviour and therewith are close to random walks (such as stock market data, wind power, wind speed). Here, a naïve forecast is a trivial yet competitive benchmark and without comparing against it, quality of more complex models cannot be meaningfully assessed. Furthermore, also more complex methods will in such series usually show a behaviour where they mostly follow the series in the same way as the naïve forecast, and improvements are often small percentages over the performance of the naïve benchmark.

As such, the benchmarks and the error measure used play an important role in such a setting. For instance, by using a relative error measure (detailed further in Section 6) that lets us directly compare against a simple benchmark such as the naïve, we can be certain of the competitiveness of the model against simple methods. On series that have clear seasonal patterns, models should accordingly be benchmarked against the seasonal naïve model as the most simplistic benchmark, and also other simple benchmarks are commonly used in forecasting.

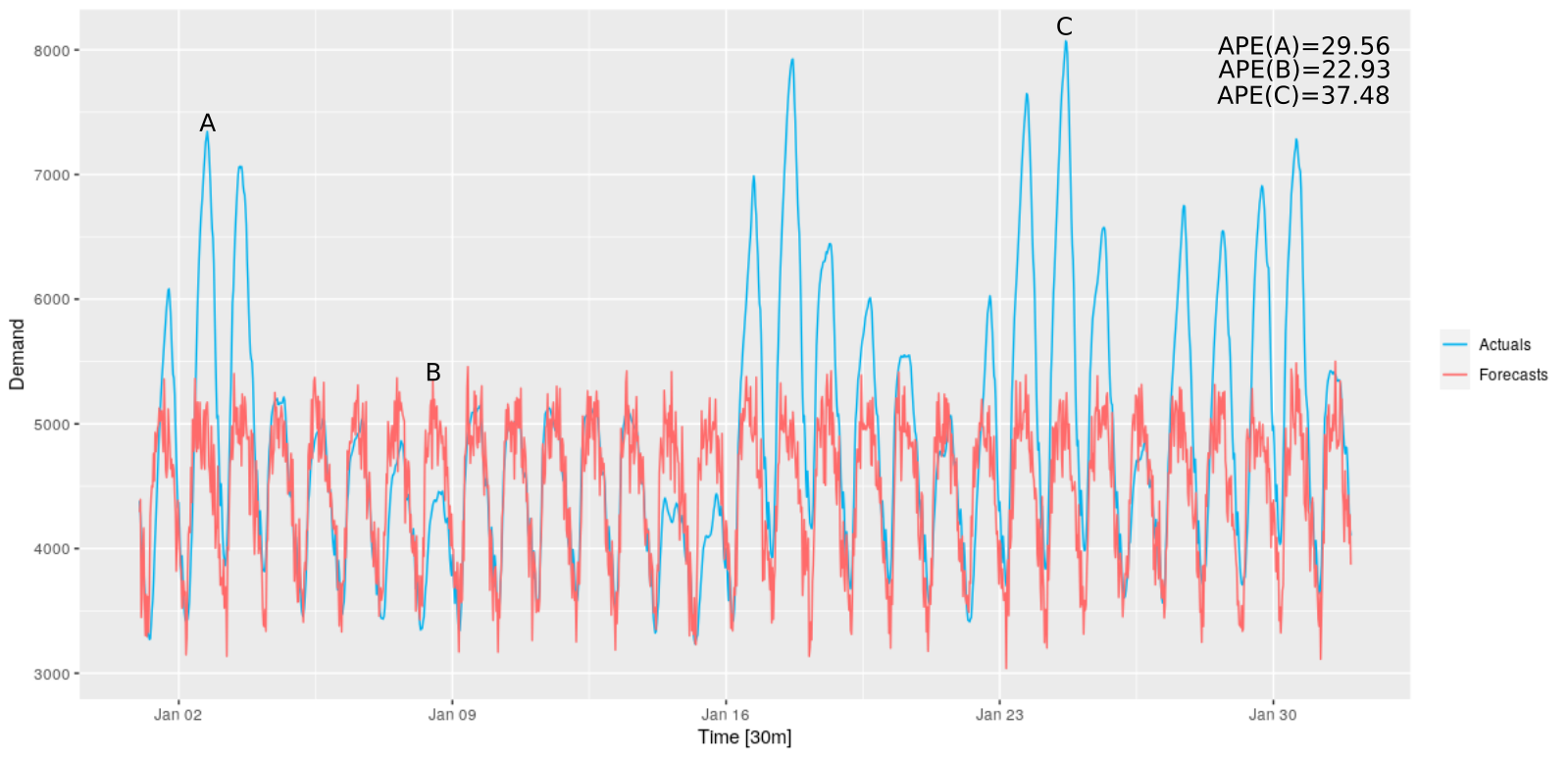

3.3 Forecast Plots

Plots with time series forecasting results can be quite misleading and should be used with caution. Analysing plots of forecasts from different models along with the actuals and concluding that they seem to fit well can lead to wrong conclusions. It is important to use benchmarks and evaluation metrics that are right for the context. Even with good error measures, in a scenario like a random walk series as in Figure 6, as stated before, our models may achieve better accuracy than the naïve method, but it will be a spurious result.

The visual appeal of a generated forecast or the possibility of such a forecast to happen in general are not good criteria to judge forecasts.

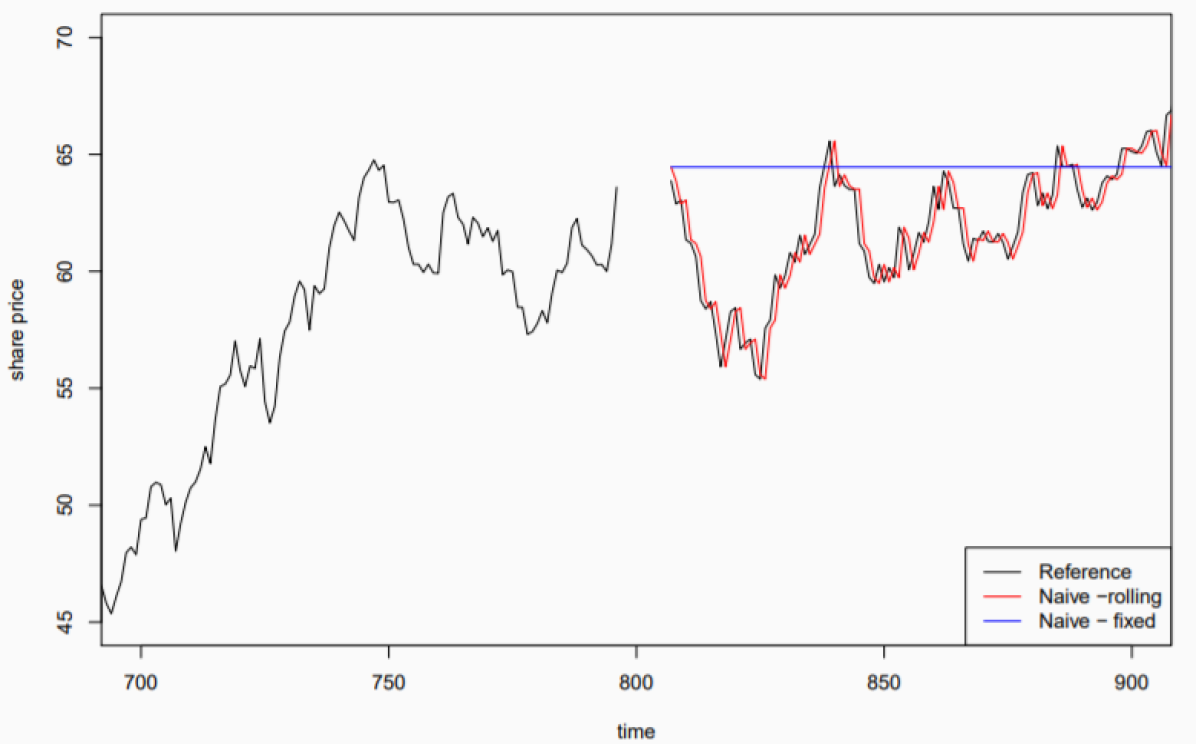

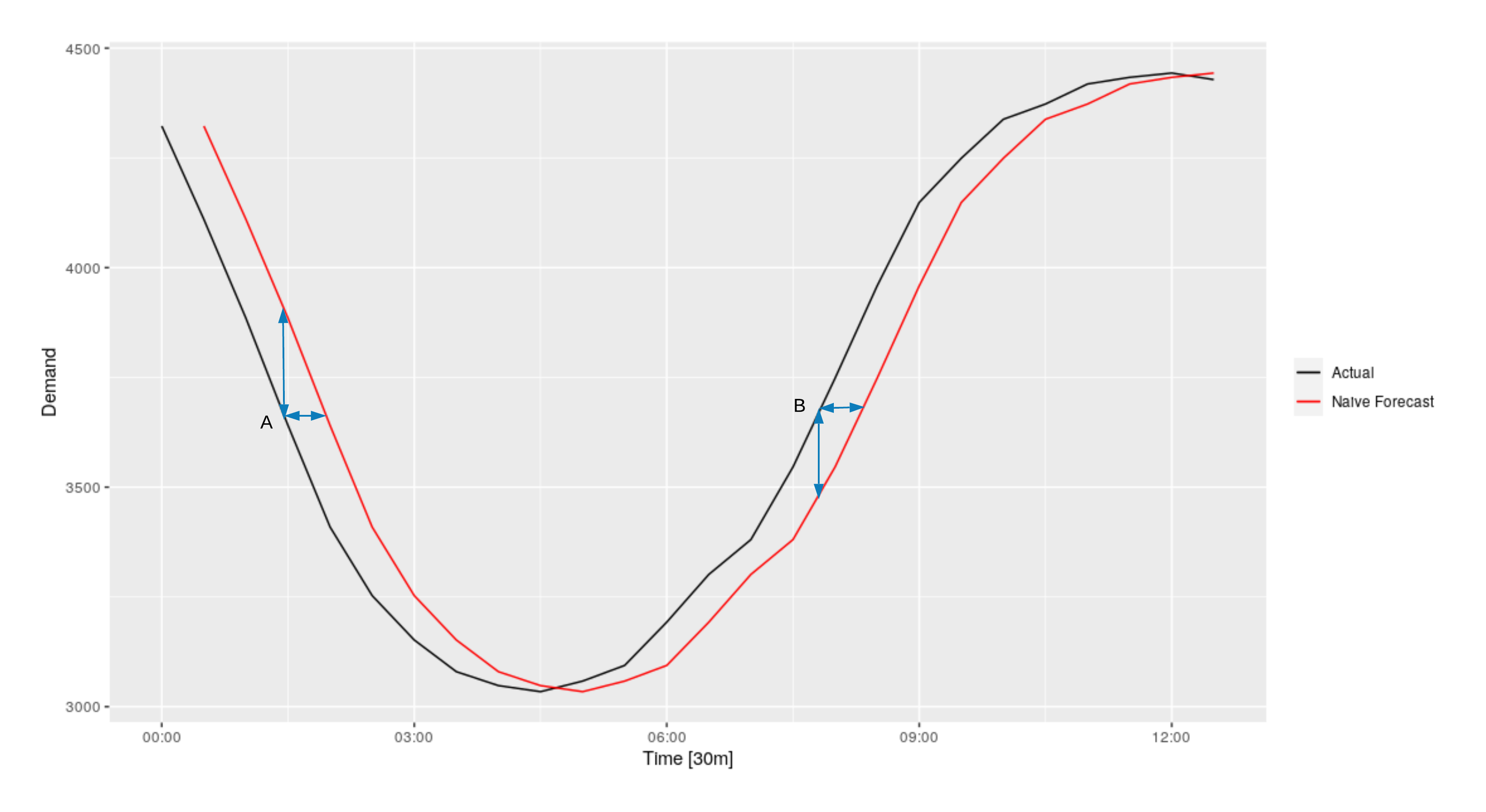

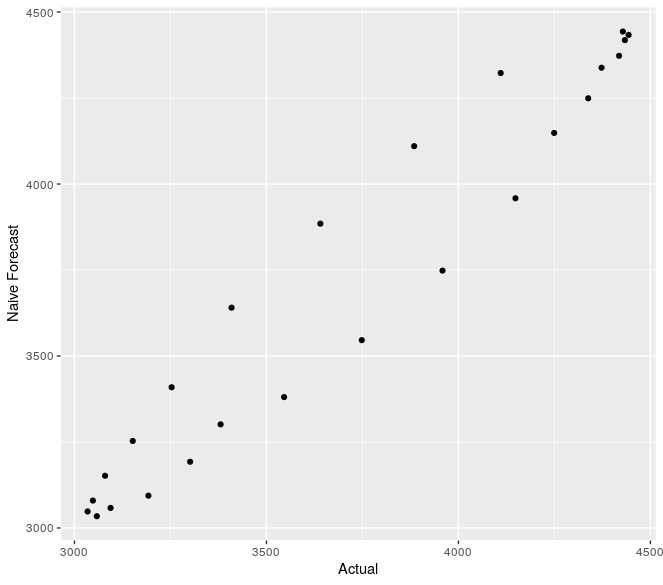

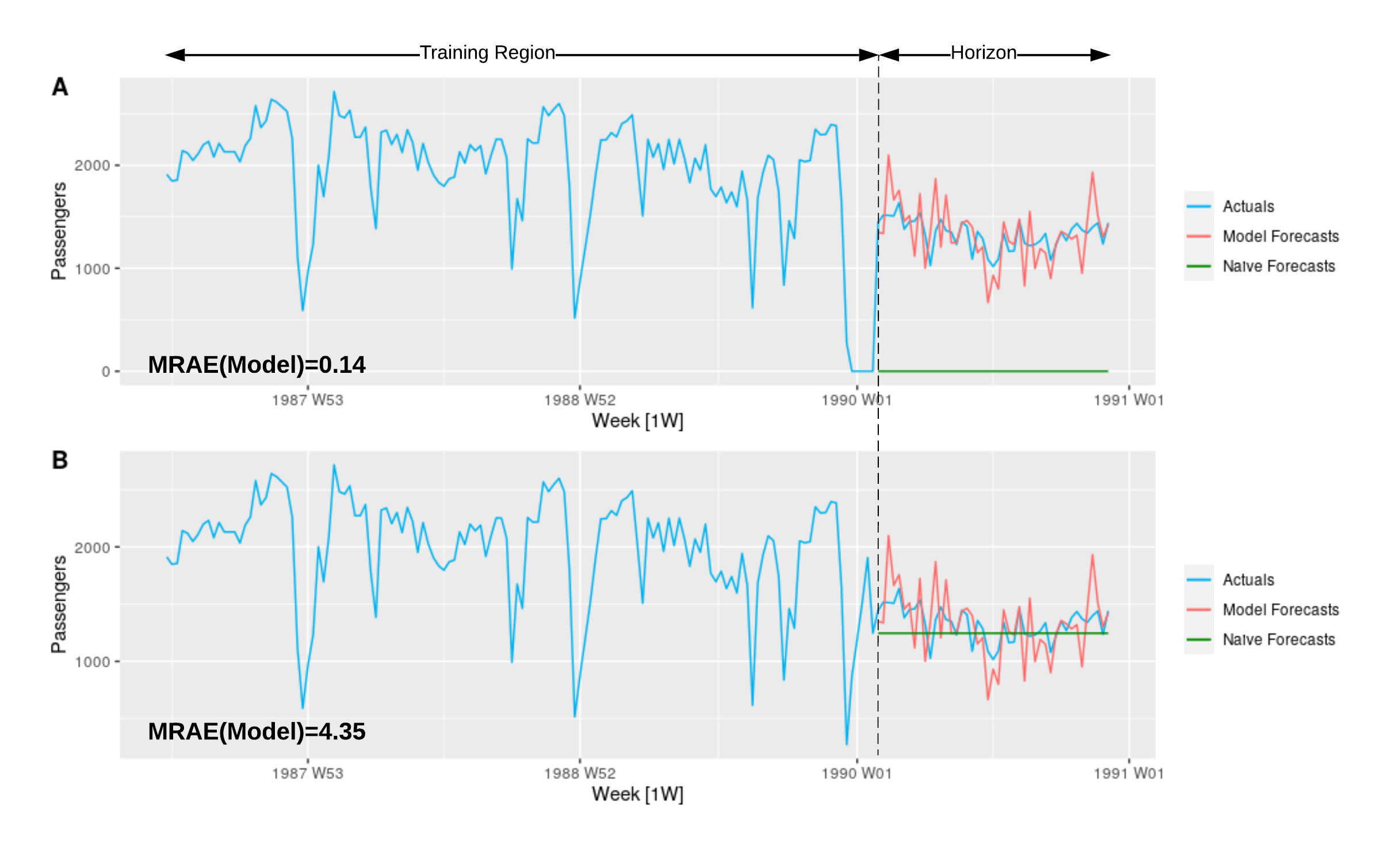

Figure 7(a) shows another random walk series, with the naïve forecast as the best forecast by definition of the Data Generating Process (DGP). The figure furthermore shows the forecasts under fixed origin and rolling origin data partitioning schemes. When periodic re-fitting is done with new data coming in as in a rolling origin setup, the naïve forecast gets continuously updated with the last observed value. For the fixed origin context on the other hand, the naïve forecast remains constant as a straight line corresponding to the last seen observation in the training series. We see that with a rolling-origin naïve forecast, the predictions tend to look visually very appealing, as the forecasts follow the actuals and our eyes are deceived by the smaller horizontal distances instead of the vertical distances that are relevant for evaluation. Figure 7(b) illustrates this behaviour. It is clear how the horizontal distance between the actuals and the naïve forecast at both points A and B are much less compared to the vertical distances which are the relevant ones for evaluation. If a scatter-plot of the actuals against the forecasts as in Figure 7(c) can be used instead, it may give a much better picture of where the forecasts stand with respect to reality, by discarding the time domain. On the other hand, on a series with integrated behaviour, the naïve method is a strong benchmark and other competitive methods on such a series will also tend to show behaviours of following the actuals. In these situations we need to rely on the error measures, as the plots do not give us much information.

Figure 7(a) shows another issue with forecasts, as the naïve forecast for fixed origin is a constant. Although this does not look realistic, and in most application domains we can be certain that the actuals will not be constant, practitioners may mistakenly identify such behaviour as a potential problem with the models, where this forecast is indeed the best possible forecast in the sense that it minimises the error based on the information available at present.

In summary, plots of the forecasts can be deceiving and should be used mostly for sanity checking. Decisions should mostly be made based on evaluations with error measures and not based on plots.

3.4 Data Leakage in Forecast Evaluation

Data leakage refers to the inadvertent use of data from the test set, or more generally data not available during inference, while training a model. It is always a potential problem in any ML task. For example, Kaufman et al. (2012) present an extensive review on the concept of data leakage for data mining and potential ways to avoid it. Arnott et al. (2019) discuss this in relation to the domain of finance. Hannun et al. (2021) propose a technique based on Fisher information that can be used to detect data leakage of a model with respect to various subsets of the dataset. Brownlee (2020) also provide a tutorial overview on data preparation for common ML applications while avoiding data leakage in the process. However, in forecasting data leakage can happen easier and can be harder to avoid than in other ML tasks such as classification/regression.

Forecasting is usually performed in a self-supervised manner with rolling origin evaluations where periodic re-training of models is performed, and within this re-training, it is normal that data travels from the test to the training set. As such, it is often difficult and not practical to separate training and evaluation code bases. As such, we often have to trust the software provider that everything is implemented correctly, and an external evaluation is difficult.

Also, more indirect forms of data leakage can happen in forecasting. In analogy to classification/regression, where data leakage sometimes happens by normalising data before partitioning for cross-validation, in forecasting, data leakage can happen by performing smoothing, decomposition (mode decomposition), normalisation etc. over the whole series before partitioning for training and testing. Data leakage can happen even when extracting features such as tsfeatures (Hyndman et al., 2019), catch22 (Lubba et al., 2019) that are not constant over time, to feed as inputs to the model. Thus, features can be extracted only from the training set data, and may need to be re-calculated either periodically or over the specific input windows. However, this can be computationally expensive.

Another type of leakage especially when training global models that learn across series, which is common practice nowadays for ML models, is when one series in the dataset contains information about the future of another series. For example with an external shock like COVID-19 or a global economy collapse, all the series in the dataset can be equally affected. Therefore, if the series in the dataset are not aligned and one series contains the future values with respect to another, when splitting the training region, future information can be already included within the training set. However, in real world application series are usually aligned so that this is not a big problem. On the other hand, in a competition setup such as the M3 and M4 forecasting competitions (Makridakis and Hibon, 2000; Makridakis et al., 2020b), where the series are not aligned, this can easily happen.

Data leakage can also happen simply due to using the wrong forecast horizon. This can happen by using data that in practice will become available later. For example, we could build a one-day-ahead model, but use summary statistics over the whole day. This means that we cannot run the model until midnight, when we have all data from that day available. If the relevant people who use the forecasts work only from 9am-5pm, it becomes effectively a same-day model. The other option is to set the day to start and end at 5pm everyday, but that may lead to other problems.

In conclusion, data leakage dangers are common in self-supervised forecasting tasks. It is important to avoid leakage problems 1) in rolling origin schemes by being able to verify and trust the implementation, as external evaluation can be difficult 2) during preprocessing of the data (normalising, smoothing etc.) and extracting features such as tsfeatures by splitting the data into training and test sets beforehand 3) by making sure that within a set of series, one series does not contain in its training period potential information about the future of another series.

4 Overview of the Forecast Evaluation Process

Forecast model building and evaluation typically encompasses the following steps.

-

1.

Data partitioning

-

2.

Forecasting

-

3.

Error Calculation

-

4.

Error Measure Calculation

-

5.

Statistical Tests for Significance (optional)

-

6.

Model Selection (optional)

The process of evaluation in a usual regression problem is quite straightforward. The models fitted to the training dataset output a prediction for a single target value in the validation set, an error such as the quadratic loss is computed for each prediction and target value combination, and finally the errors from all the predictions in the validation set are summarised using some error measure such as the Root Mean Squared Error (RMSE). The best model out of the pool of fitted models is selected based on the value of this final error measure on the validation set. The relevant error measures used etc. are standard and established as best practices in these domains.

However, when it comes to forecast evaluation, many different options are available for each of the aforementioned steps and no standards have been established thus far, although several pitfalls associated with certain evaluation setups have been identified. Two other optional activities related to forecast evaluation are Statistical Tests for Significance and Model Selection. They are not performed always by practitioners. Instead of selecting one best model, we may sometimes be interested in deploying an ensemble of all the models. Out of these different steps in evaluation, in this article we discuss the approaches commonly used for Data Partitioning, Model Selection, Error and Error Measure Calculation as well as Statistical Tests for Significance.

5 Data Partitioning

When performing OOS evaluation in forecasting (using a validation or test set), we can either evaluate for every individual forecast step separately (one-step-ahead error, two-step-ahead error) or the whole test period on average depending on the forecasting scheme of the underlying models. In this section, we explain the details of different data partitioning techniques for evaluations performed in the context of forecasting. We also explain the options for model selection based on these different data partitioning strategies.

5.1 Fixed Origin Setup

Fixed origin setup is a faster and easier to implement evaluation setup. Fixed origin setup is the usual setup used in many academic contexts such as forecasting competitions since this can effectively avoid data leakage problems as the test set is not disclosed in any way. In fact for competition scenarios where the dates of the series are not aligned (like the M3, M4 competitions), a fixed origin setup may be sufficient. However, for many practical scenarios, a fixed origin setup is problematic and may not be a sufficient evaluation. With a single series, the fixed origin setup only provides one forecast per each forecast step in the horizon. According to Tashman (2000), a preferred characteristic of OOS forecast evaluation is to have sufficient forecasts at each forecast step. Furthermore, for a single series, the testing period is short unless a long forecast horizon is used. However, with a long forecast horizon, the problem is that we are mixing very different forecasts. For example, for a 400-step-ahead forecast, short-term dynamics due to autocorrelation may be irrelevant, and trend and seasonality may matter the most, where for a one-step-ahead forecast short-term dynamics may be the dominating factor. Thus, a one-step-ahead forecast may have totally different characteristics, in terms of possible accuracy, useful input features, well-performing methods, than a 400-step-ahead forecast (Petropoulos et al., 2014).

Another requirement of OOS forecast evaluation is to make the forecast error measures insensitive to specific phases of business (Tashman, 2000). However, with a fixed origin setup, the errors may be the result of particular patterns only observable in that particular region of the horizon (Tashman, 2000), and evaluations will not generalise well to other phases such as Christmas sales, Holiday seasons, etc.. This poses a gap between what practitioners are really interested in and how forecasting is done often in academic settings. Having multiple forecasts for the same forecast step allows to produce a forecast distribution per each step for further analysis. Therefore, the following multi period evaluation setups are introduced as opposed to the fixed origin setup.

5.2 Rolling Origin, Time Series Cross-Validation and Prequential Evaluation Setups

Armstrong and Grohman (1972) are among the first researchers to give a descriptive explanation of the rolling origin evaluation setup. Although the terms rolling origin setup and tsCV are used interchangeably in the literature, in addition to the forecast origin rolling forward, tsCV also allows to skip origins, effectively rolling forward by more than one step at a time (analogously to the difference between a leave-one-out CV and a k-fold CV). In the field of stream data mining and concept drift, this form of evaluation is furthermore known as interleaved-test-then-train or prequential evaluation (Gama et al., 2013; Ghomeshi et al., 2019) as means of online evaluation. For streaming data, prequential evaluation allows to continuously monitor the performance of a model that evolves over time, and thus detect and act upon concept drifts (Gama et al., 2009; Kiran Bhowmick, 2020). With such multi period evaluations, each time the forecast origin updates, the model encounters new actual data. Hence, a rolling origin setup is typically the more practical evaluation setup in real-world application. For instance, in a task of forecasting the daily sales of a particular product, the number of actual sales can be obtained at the end of each day and can be incorporated in the model to better predict the next day’s demand.

With new data becoming available, we have the options to – in the terminology of Tashman (2000) – either update the model or recalibrate it. Recalibration here refers to either retraining the model weights from scratch or incremental learning as new data comes in. Updating on the other hand means just using the trained model to predict with new data. Although for some of the traditional models such as Exponential Smoothing (ETS) and Auto-Regressive Integrated Moving Average (ARIMA), the usual practice (and the implementation in the forecast package) in a rolling origin setup is to recalibrate (refit) the models, for general ML models it is more common to mostly just accept new data as inputs and only periodically retrain the model. While this is quite straightforward with a stateless ML model, on a model with a state such as a Recurrent Neural Network (RNN), updating still requires stepping through the whole series to construct the state. In this sense, the (updating-based) rolling origin setup comes more natural to many ML methods than to the traditional forecasting methods. Also, as ML methods tend to work better with higher granularities, re-fitting is not an option (for example, a monthly series predicted with ETS vs. a 5-minutely series predicted with Light Gradient Boosting Models). Therefore, retraining as the most recent data becomes available happens in ML methods mostly only when some sort of concept drift (change of the underlying data generating process) is encountered (Webb et al., 2016).

Rolling origin evaluation can be conducted in two ways; 1) Expanding window setup 2) Rolling window setup. Figure 8 illustrates the difference between the two approaches. In the expanding window setup, the training region of the series for the model expands as the forecast origin rolls forward, thus effectively increasing the length of the training data per each evaluation. The expanding window method is a good setup for small datasets/short series (Bell and Smyl, 2018). However, in the rolling window setup, the size of the training region is kept constant; thus as the forecast origin rolls forward, so does the start of the training period, dropping the oldest observations as new data becomes available (Cerqueira et al., 2020). The rolling window setup removes the oldest data from training. This will not make a difference with forecasting techniques that only minimally attend the distant past, such as ETS, but may be beneficial with pure autoregressive ML models, that have no notion of time beyond the windows. In a streaming data context as well, the most common methods of performing prequential evaluation are by using a sliding window or by using fading factors which tend to forget instances in the further past and focus on the current window (Mulinka et al., 2018). This is because the usual prequential evaluation approach with expanding window is known to provide overestimation for the validation error (Gama et al., 2009). Hidalgo et al. (2019) have empirically demonstrated that prequential evaluation with sliding window is the best approach for validation in comparison to fading factors and expanding window. A potential problem of the rolling origin setup is that the first folds may not have much data available. However, the size of the first folds is not an issue when dealing with long series, thus making rolling origin setup a good choice with sufficient amounts of data. On the other hand, with short series it is also possible to perform a combination of the aforementioned two rolling origin setups where we start with an expanding window setup and then move to a rolling window setup.

5.3 (Randomised) Cross-Validation

The aforementioned two techniques of data partitioning preserve the temporal order of the time series when splitting and using the data. Another form of data partitioning is to use a common randomised CV scheme as first proposed by Stone (1974). This scheme is visualised in Figure 9. The dataset is initially shuffled randomly and then partitioned into non-overlapping train and validation sets. Often a k-fold CV scheme is used for this purpose. For example, in a 5-fold CV strategy, the whole training dataset is randomly split into 5 partitions and 4 of them are used to train the model and the remaining partition held out for validation. This is done in iterations until all partitions are considered for validation separately. The set of validation scores produced this way are finally summarised. Leave-One-Out-Cross-Validation (LOOCV) is the extreme case of the k-fold CV where k is equal to the number of data points in the dataset. Therefore, compared to the aforementioned validation schemes which preserve the temporal order of the data, this form of randomised CV strategy can make efficient use of the data, since all the data is used for both model training as well as evaluation in iterations (Hastie et al., 2009). This helps to make a more informed estimation about the generalisation error of the model.

However, this form of random splitting of a time series does not preserve the temporal order of the data, and is therefore oftentimes not used and seen as problematic. The common points of criticism for this strategy are that, 1) it can make it difficult for a model to capture serial correlation between data points (autocorrelation) properly, 2) potential non-stationarities in time series can cause problems (for example, depending on the way that the data is partitioned, if all data from Sundays happen to be in the test set but not the training set in a series with weekly seasonality, then the model will not be able to produce accurate forecasts for Sundays since it has never seen data of Sundays before), 3) the training data contains future observations and the test set contains past data due to the random splitting and 4) since evaluation data is reserved randomly across the series, the forecasting problem shifts to a missing value imputation problem which certain time series models are not capable of handling (Petropoulos et al., 2020).

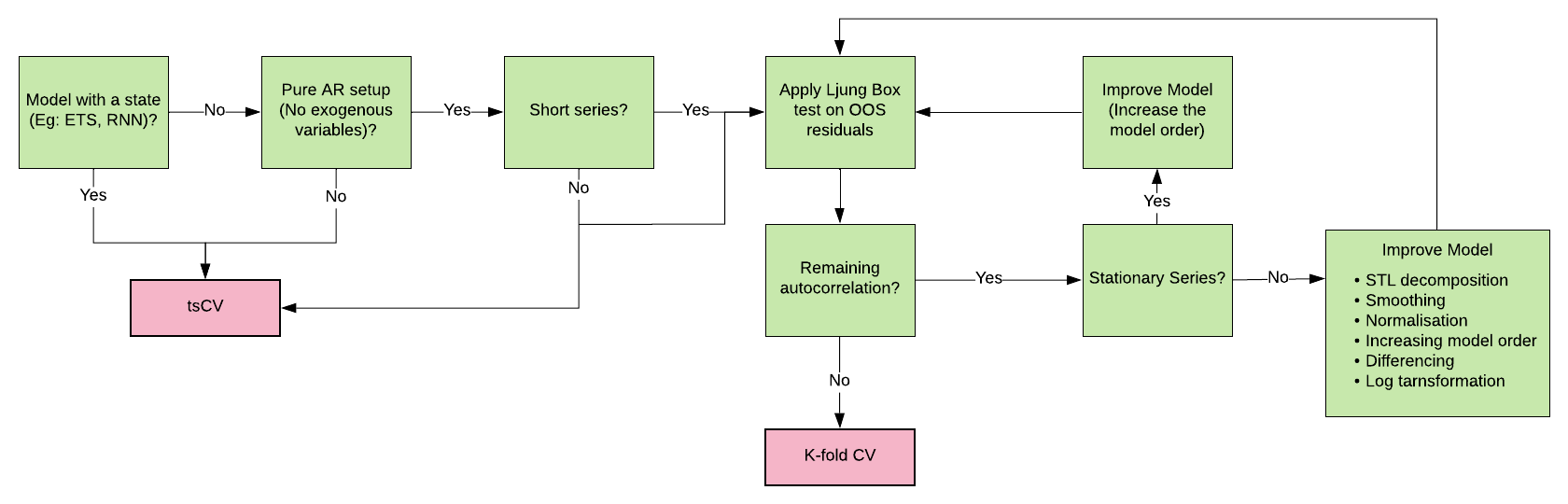

Out of these problems, to address the serial correlation issues, researchers have proposed a few variations of CV. Different forms of blocked CV have been introduced for this purpose, where the folds are selected in blocks, without initial shuffling and preserving the temporal order of the data within the folds (Racine, 2000; Bergmeir and Benítez, 2012). Further non-dependent CV techniques have also been proposed, where a sufficiently sized block of instances surrounding the test instances are discarded to ensure independence between the training and test sets (Burman et al., 1994; Racine, 2000). Nonetheless, randomised CV can be applied to pure AR models without a problem. Bergmeir et al. (2018) theoretically and empirically show that CV performs well in a pure AR setup, as long as the models nest or approximate the true model, as then the errors are uncorrelated, leaving no dependency between the individual windows. To check this, it is important to estimate the serial correlation of residuals. For this, the Ljung-Box test (Ljung and Box, 1978) can be used on the OOS residuals of the models. While for overfitting models there will be no autocorrelation left in the residuals, if the models are underfitted, some autocorrelation will be left in the OOS residuals. If there is autocorrelation left, then the model still does not use all the information available in the data, which means there will be dependencies between the separate windows. In such a scenario, CV of the time series dataset will not hold valid, and underestimate the true generalisation error. The existence of significant autocorrelations anyway means that the model should be improved to do better on the respective series (increase the AR order to capture autocorrelation etc.), since the model has not captured all the available information. Once the models are sufficiently competent in capturing the patterns of the series, for pure AR setups (without exogenous variables), standard k-fold CV is a valid strategy. Therefore, in situations with short series and small amounts of training data, where it is not practically feasible to apply the aforementioned tsCV techniques due to the initial folds involving very small lengths of the series, the standard CV method with some control of underfitting of the models is a better choice with efficient use of data.

The aforementioned problem that the testing windows can contain future observations, is also addressed by Bergmeir et al. (2018). With the CV strategy, the past observations not in the training data but existing in the test set can be considered missing observations, and the task is seen more as a missing value imputation problem rather than a forecasting problem. Many forecasting models such as ETS (in its implementation in the forecast package (Hyndman and Athanasopoulos, 2018)), which iterate throughout the whole series, cannot properly deal with missing data. For RNNs as well, due to their internal states that are propagated forward along the series, standard k-fold CV which partitions data randomly across the series is usually not applicable. Therefore, for such models, the only feasible validation strategy is tsCV. Models such as ETS can anyway train competitively with minimal amounts of data (as is the case with the initial folds of the tsCV technique) and thus, are not quite problematic with tsCV. However, for reasonably trained pure AR models, where the forecasts for one window do not in any way depend on the information from other windows (due to not underfitting and having no internal state), it does not make a difference between filling the missing values in the middle of the series and predicting future values, where both are performed OOS. Nevertheless, the findings by Bergmeir et al. (2018) are restricted to only stationary series. Cerqueira et al. (2020)’s work on the same area has concluded that for stationary series, using a pure AR setup, a blocked CV strategy works the best, and they also perform an analysis on non-stationary data, discussed in the following section.

5.4 Data partitioning for non-stationary data

Cerqueira et al. (2020) experimented using non-stationary series, where they have concluded that OOS validation procedures preserving the temporal order (such as tsCV), are the right choice when non-stationarities exist in the series. However, a possible criticism of that work is the choice of models. We have seen in Section 3 that ML models are oftentimes not able to address certain types of non-stationarities out of the box. More generally speaking, ML models are non-parametric, data-driven models. As such, the models are typically very flexible and the function fitted depends heavily on the characteristics of the observed data. Though recently challenged (Balestriero et al., 2021), a common notion is that ML models are typically good at interpolation and lack extrapolation capabilities. The models used by Cerqueira et al. (2020) include several ML models such as a Rule-based Regression (RBR) model, a Random Forest (RF) model and a Generalised Linear Model (GLM), without in any way explicitly tackling the non-stationarity in the data (similar to our example in Section 3). Thus, if a model is poor and not producing good forecasts, performing a validation to select hyperparameters, using any of the aforementioned CV strategies, will be of limited value. Furthermore, and more importantly, non-stationarity is a broad concept and it will depend both for the modelling and the evaluation on the type of non-stationarity which procedures will perform well. For example, with abrupt structural breaks and level shifts occurring in the unknown future, but not in the training and test set, it will be impossible for the models to address this change and none of the aforementioned evaluation strategies would do so either. In this situation, even tsCV would grossly underestimate the generalisation error. For a more gradual underlying change of the DGP, a validation set at the end of the series would be more appropriate since in that case, the data points closer to the end of the series may be already undergoing the change of the distribution. On the other hand, if the series has deterministic trend or seasonality, which are straightforward to forecast, they can be simply extracted from the series and predicted separately whereas the stationary remainder can be handled using the model. In such a setup, the k-fold CV scheme will work well for the model, since the remainder complies with the stationarity condition. For other non-deterministic trends, there are several data pre-processing steps mentioned in the literature such as lag-1 differencing, logarithmic transformation (for exponential trends), Seasonal and Trend Decomposition using Loess (STL Decomposition), local window normalisation (Hewamalage et al., 2021), moving average smoothing, percentage change transform, wavelet transform etc. (Salles et al., 2019). Salles et al. (2019) have conducted an extensive empirical study to investigate the impact of the choice of the data transformation technique on the accuracy of the model, using a linear ARMA model. Their findings have concluded that there is no single universally best transformation technique across all datasets; rather it depends on the characteristics of the individual datasets. However, for the particular datasets used in their study, differencing and moving average smoothing have generally worked the best for addressing trend. If appropriate data pre-processing steps are applied to enable models to handle non-stationarities, with a pure AR setup, the CV strategy still holds valid after the data transformation, if the transformation achieves stationarity. As such, to conclude, for non-stationarities, tsCV seems the most adequate as it preserves the temporal order in the data. However, there are situations where also tsCV will be misleading, and the forecasting practitioner will already for the modeling need to attempt to understand the type of non-stationarity they are dealing with. This information can subsequently be used for evaluation, which may render CV methods for stationary data applicable after transformations of the data to make them stationary.

5.5 Other model selection methods

The aforementioned data partitioning schemes are quite important when it comes to model selection based on the performance of the models on the validation sets. Apart from the CV strategies discussed above, other model selection techniques exist such as information criteria (IC) or techniques like minimum message length (Fitzgibbon et al., 2004). The advantage of these techniques over data partitioning is typically that all data can be used for training and no validation set is needed.

For example, let us consider Akaike’s Information Criterion (AIC, Akaike, 1974), but similar considerations hold for other IC. For time series models, it has been found that minimising AIC is asymptotically equivalent to minimising the MSE of OOS one-step ahead forecasts (Inoue and Kilian, 2006). However, using AIC has several downsides. To use it to compare across models, the respective likelihoods need to be computed the same way, using the same data. Therefore, it cannot be used to compare across models, with different model orders, from different model families such as ETS and ARIMA (since likelihoods for those models are computed in different ways), with and without differencing, since differencing effectively reduces the amount of data points available for the model. Apart from that, AIC is in general used when getting access to a separate test set is expensive (due to limited data), which is often not the case with data-abundant scenarios where ML models are applicable. Therefore, AIC is more suitable for small datasets and this is why models such as ETS and ARIMA that are not very data-intensive, use AIC and other IC internally. Moreover, the definition of AIC uses (an estimation of) the number of parameters of the model, which is not straightforward for complex ML models, since simply counting the number of parameters does not represent well the complexity of such models. Due to these reasons, generally AIC and other IC are not used for ML models that work on large datasets. For such situations, the data partitioning methods discussed before are usually preferable.

5.6 Summary and guidelines for data partitioning and model selection

It is important to identify which out of the above data partitioning strategies most closely estimates (without under/overestimation) the final error of a model for the test set under the given scenario (subject to different non-stationarities/serial correlations/amount of data of the given time series). In particular, in the M5 competition as well, it was re-emphasised that a reliable CV strategy is essential, to be able to assess the generalisation error of models (Makridakis et al., 2020a).

The gist of the guidelines for model selection is visualised by the flow chart in Figure 10. If the series are not short, tsCV is usually preferrable over k-fold CV, if there are no practical considerations such as that an implementation of an algorithm is used that is not primarily intended for time series forecasting, and that internally performs a certain type of cross-validation. If series are short, then k-fold CV should be used, accounting adequately for non-stationarities and autocorrelation in the residuals.

6 Error Measures for Forecast Evaluation

Once the predictions are obtained from models, the next requirement is to compute errors of the predictions to assess the model performance. Belt (2017) argue in their work that a bias-variance decomposition of the error measure should be considered. Bias and variance of forecasts may yield different business decisions. Bias in predictions occurs due to errors from wrong model assumptions, which result in a weak model not having captured the exact patterns of the data. This happens mostly due to the selected sample of data (used for model training) being under-representative of the whole distribution, which is also called as the selection bias. Because of this reason, a model can be very accurate (forecasts being very close to actuals), but consistently produce more overestimations than underestimations, which may be concerning from a business perspective. Therefore, forecast bias is calculated with a sign, as opposed to absolute errors, so that it indicates the direction of the forecast errors, either positive or negative. For example, scale-dependent forecast bias can be assessed with the Mean Error (ME) as defined in Equation in 5. Here, indicates the true value of the series, the forecast and , the number of all available errors (across series, across horizons, etc.). The scale-dependent standard deviation (Std) of the errors for the population is defined in Equation 6, assuming a 0 population mean of the errors, i.e., an unbiased model. Note that the Std of the errors for an unbiased model is identical to the Root Mean Squared Error (RMSE) defined later in Equation 10. Therefore, RMSE produces an estimate of the Std of the distribution of forecast errors. Other scale-free versions of bias and Std can be defined by scaling with respect to appropriate scaling factors, such as actual values of the series.

| (5) |

| (6) |

Two other popular and simple error measures used in a usual regression context are Mean Squared Error (MSE) and Mean Absolute Error (MAE) defined in Equations 7 and 8 respectively.

| (7) |

| (8) |

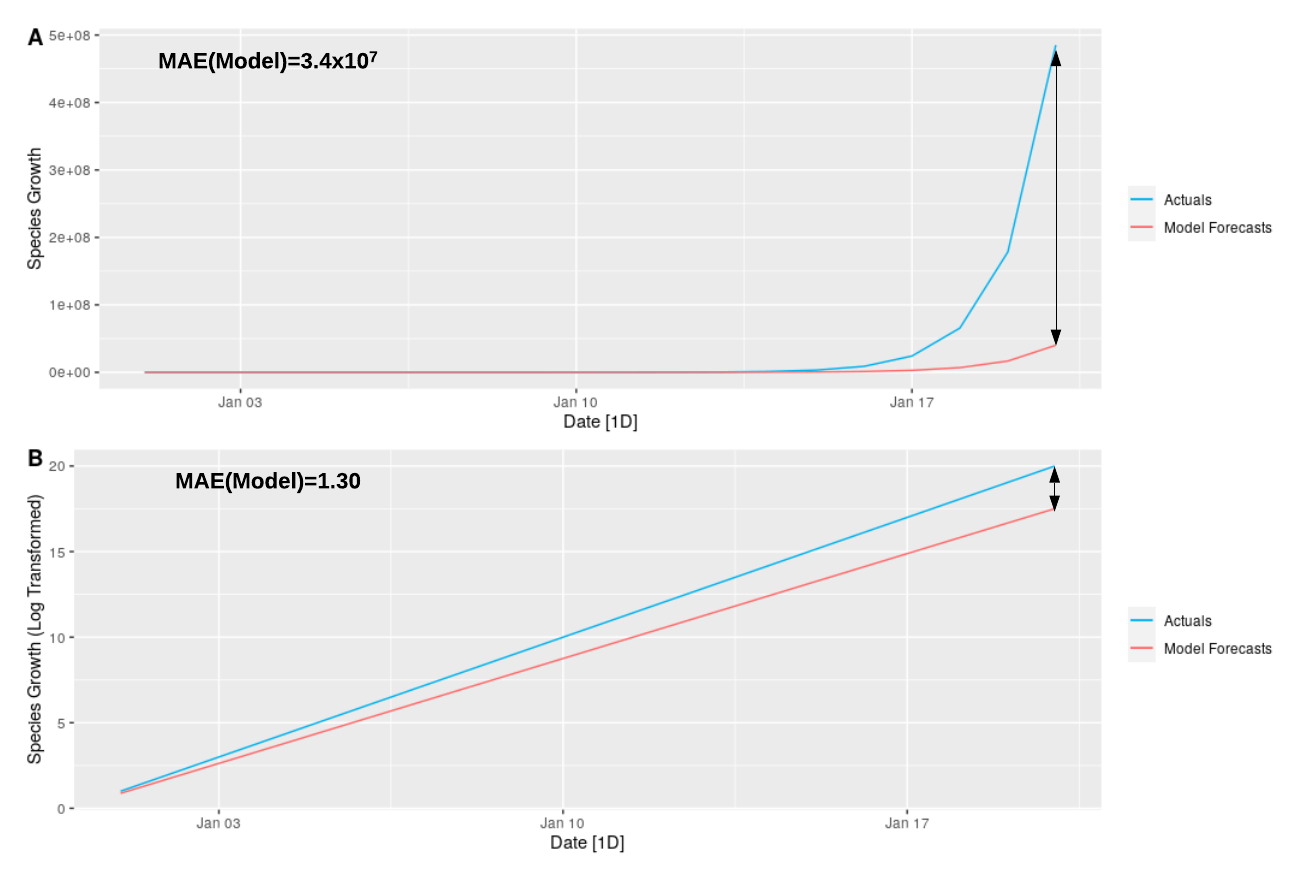

Apart from these simple measures used as in usual ML tasks such as regression, for forecasting a wide variety of error measures have been proposed by researchers over the years. The main reason for this is the need to have measures that allow for comparisons across series. For this, the measures need to be scaled, and it has turned out to be next to impossible to develop a scaling procedure that works for any type of possible non-stationarity and non-normality in a time series. Eventually we encounter a particular condition of the time series in the real world, that makes the proposed error measure fail (Svetunkov, 2021). Thus, new measures usually either focus on specific business needs or have the intention of addressing issues of previously used measures, but have new issues then. This has led to a large pool of proposals in the literature. Researchers/practitioners very often have particular series in mind when evaluating in a certain way (using specific measures) in their work, but these preconditions are often never stated. For example, smart meter or wind power production series do not usually have exponential trends, and they hardly have level shifts or long-term trends etc. On the other hand, growing businesses such as tech start-ups or ride-share providers often have strong trends in any business related time series that they have collected. The key to selecting a particular error measure for forecast evaluation is that it is mathematically and practically robust under the given data. From a business point of view there can be other requirements for an error measure such as being interpretable (easy to communicate) and reflecting on the key performance indicators of the underlying business application such as the net profit; which we do not focus on in this work.

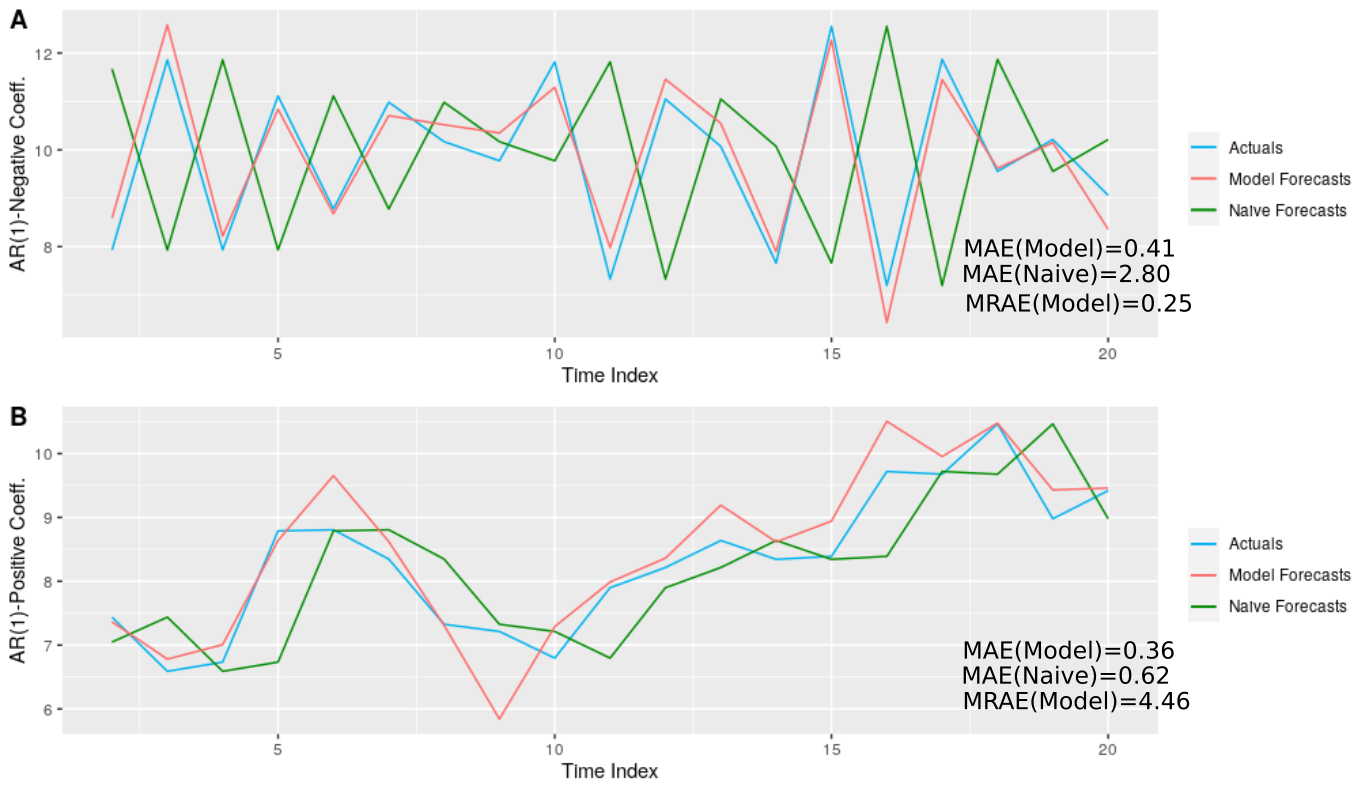

Point forecasting which is the main focus of this work is about predicting a particular statistic of interest from the future distribution of values, such as mean or median. Therefore, different point forecast evaluation measures are also targeted towards optimising for a specific statistic of the distribution and it is important to distinguish which statistic it is for each error measure. For example, measures with squared base errors such as MSE and RMSE optimise for the mean whereas others with absolute value base errors such as MAE and Mean Absolute Scaled Error (MASE) optimise for the median. Although the mean and median are the same for a symmetric distribution, that does not hold for skewed distributions as with intermittent series. There exist numerous controversies in the literature regarding this. Petropoulos et al. (2020) suggest that it is not appropriate to evaluate the same forecasts using many different error measures, since each one optimises for a different statistics of the distribution. Also according to Kolassa (2020), if different point forecast evaluation measures are considered, multiple point forecasts for each series and time point also need to be created. Kolassa (2020) further argues that, if the ultimate evaluation measure is, e.g., MAE which focusses on the median of the distribution, it does not make sense to optimise the models using an error measure like MSE (which accounts for the mean). It is more meaningful to consider MAE also during model training as well. However, these arguments hold only if it is not an application requirement for the same forecasts to perform generally well under all these measures. Koutsandreas et al. (2021) have empirically shown that, when the sample size is large, a wide variety of error measures agree on the most consistently dominating methods as the best methods for that scenario. They have also demonstrated that using two different error measures for optimising and final evaluation has an insignificant impact on the final accuracy of the models. Bermúdez et al. (2006) have developed a fuzzy ETS model optimised via a multi-objective function combining three error measures MAPE, RMSE and MAE. Empirical results have demonstrated that using such a mix of error measures instead of just one for the loss function leads to overall better, robust and generalisable results even when the final evaluation is performed with just one of those measures. Fry and Lichtendahl (2020) also assess their same forecasts across numerous error measures in a business context.

On the other hand, Kolassa (2016) also argues that point forecast evaluation alone is not sufficient. This is due to all the pitfalls associated with every point forecast evaluation measure as discussed in the rest of this section. Also, according to that author, evaluating only individual statistics of a distribution is not adequate and the overall predictive distributions need to be considered instead, in order to estimate the uncertainty of the produced point forecasts with a reasonable confidence. Although not the main point of focus in this article, different evaluation measures have been proposed in this respect. Kolassa (2016) explains most of them including randomised probability integral transform (rPIT) and several proper scoring rules such as logarithmic score, Brier score, ranked probability score etc.

Furthermore, depending on different data partitioning schemes, we may obtain many errors for the same model either for a fixed forecast origin or rolling forecast origin etc. In the context of global forecasting models, we train using many different series and also often evaluate on that same set of series. Thus, the number of series further increases the amount of errors available for a single model. For summarising errors across all available series as well as the different steps in the forecast horizon, we can consider a number of statistics such as median, arithmetic mean or geometric mean etc. Using medians and geometric means instead of arithmetic means helps with avoiding sensitivity to outlier series in a set of time series. However, this means that using the arithmetic mean identifies the existence of such outlier errors for certain series. The problem specifically with geometric mean based measures is that a model can perform perfectly (0 or error) on one series and quite bad on all the others but still become the best (as the overall error becomes 0 or quite small due to multiplication) (Boylan and Syntetos, 2006). Thus, Svetunkov (2021) mentions that the use of several summary operators on the same errors can raise awareness regarding these issues of the individual errors. Summarising across series and across the horizon can be done using the same or different statistical operators. We can also change the order of summarising the errors; for instance we can first summarise the errors for the different time steps separately and then summarise those per time step error measures. When summarising across the horizon, weights can be assigned to different time steps to get a weighted measure as well. Different terminology has been introduced by researchers for these base errors, statistical operators etc. For instance, in the work by Kunst (2016), the base error functions are named as local distance functions and the statistical operators to summarise base errors are denoted as link functions. The resulting final error functions are known as metrics or distance functions. According to the terminology introduced by Hyndman and Koehler (2006), which we follow in this paper, the base errors are called Errors, and summarised by using different statistical operators into Error Measures.

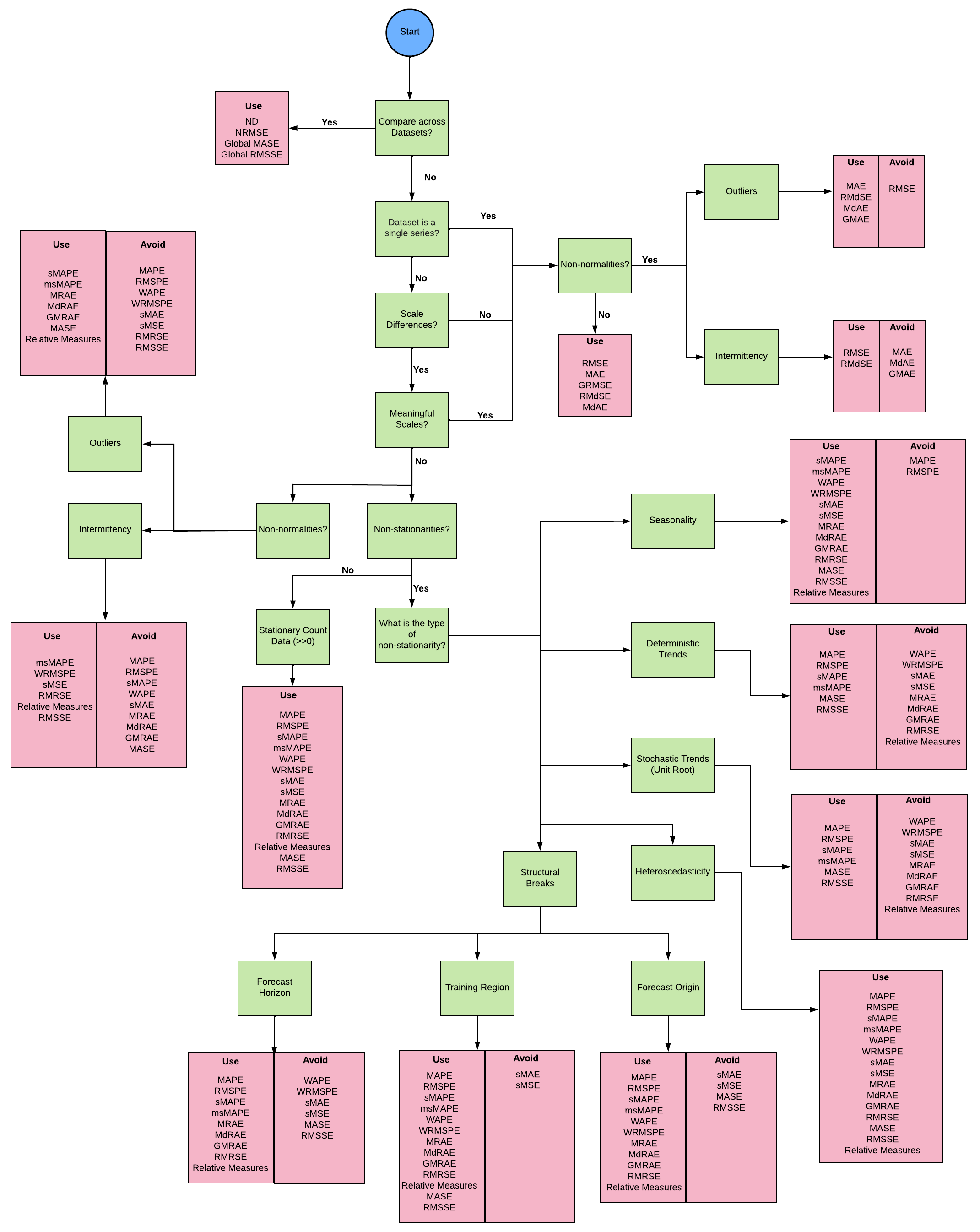

There are many different point forecast error measures available in the forecasting literature categorised based on 1) whether squared or absolute errors are used 2) techniques used to make them scale-free and 3) the operator such as mean, median used to summarise the errors (Koutsandreas et al., 2021). In the rest of this section, we first introduce, define, and categorise all different error measures introduced in the literature. We also provide the formulae for these measures and their general mathematical issues (not relevant to specific characteristics of the series). Then, we move on to provide an overview of certain types of data and possible problems that the error measures can have with them. We discuss which error measures are preferrable or should be avoided depending on each of the characteristics of time series as also stated in Section 3.1.

Summarising all these details, the main results of this section are then Table 1 and Figure 11. Table 1 can be used to choose error measures under given characteristics of the data. In Table 1, the scaling column indicates the type of scaling associated with each error measure mentioned in the previous column. This includes no scaling, scaling based on actual values, scaling based on benchmark errors as well as the categorisation such as per-step, per-series and all-series (per-dataset) scaling. The sign in Table 1 indicates that the respective error measures need to be used with caution under the given circumstances as explained in the above discussions. The flow chart in Figure 11 provides further support for forecast evaluation measure selection based on user requirements and other characteristics in the data. In Figure 11, the error measures selected to be used with outlier time series are in the context of being robust against outliers, not capturing them.

| Stationary Count Data (>>0) | Seasonality | Trend (Linear/Exp.) | Unit Roots | Heteroscedasticity |

|

Intermittence | Outliers | Error Measures | Scaling | |||||

|

|

|

||||||||||||

| ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✗ | RMSE | None | |||

| ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✗ | ✓ | MAE | ||||

| ✓ | ✗ | ✓ | ✓† | ✓† | ✓ | ✓ | ✓ | ✗ | ✗ | MAPE | OOS Per Step | Actual Values | ||

| ✓ | ✗ | ✓ | ✓† | ✓† | ✓ | ✓ | ✓ | ✗ | ✗ | RMSPE | ||||

| ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✗ | ✓ | sMAPE | ||||

| ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | msMAPE | ||||

| ✓ | ✓ | ✗ | ✗ | ✓ | ✗ | ✓ | ✓ | ✗ | ✗ | WAPE | OOS Per Series | |||

| ✓ | ✓ | ✗ | ✗ | ✓ | ✗ | ✓ | ✓ | ✓† | ✗ | WRMSPE | ||||

| ✓ | ✓ | ✗ | ✗ | ✓ | ✗ | ✗ | ✗ | ✗ | ✗ | sMAE | In-Sample Per Series | |||

| ✓ | ✓ | ✗ | ✗ | ✓ | ✗ | ✗ | ✗ | ✓† | ✗ | sMSE | ||||

| ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✗ | ✓ | ND | OOS All Series | |||

| ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✗ | NRMSE | ||||

| ✓† | ✓† | ✗ | ✗ | ✓ | ✓ | ✓† | ✓ | ✗ | ✓† | MRAE | OOS Per Step | Benchmark Errors | ||

| ✓† | ✓† | ✗ | ✗ | ✓ | ✓ | ✓† | ✓ | ✗ | ✓† | MdRAE | ||||

| ✓† | ✓† | ✗ | ✗ | ✓ | ✓ | ✓† | ✓ | ✗ | ✓† | GMRAE | ||||

| ✓† | ✓† | ✗ | ✗ | ✓ | ✓ | ✓† | ✓ | ✓† | ✗ | RMRSE | ||||

| ✓† | ✓† | ✗ | ✗ | ✓ | ✓ | ✓† | ✓ | ✓† | ✓† | Relative Measures |

|

|||

| ✓† | ✓† | ✓ | ✓ | ✓ | ✗ | ✓† | ✗ | ✗ | ✓ | MASE | In-Sample Per Series | |||

| ✓† | ✓† | ✓ | ✓ | ✓ | ✗ | ✓† | ✗ | ✓† | ✗ | RMSSE | ||||

| ✓† | ✓† | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ |

|

||||

| ✓ | ✓ | ✓† | ✓ | ✓† | ✓ | ✓ | ✓ | ✓ | ✓ |

|

None | |||

6.1 Categorisation of Error Measures

Different error measures in the literature are categorised as detailed in the following. We follow the categorisation of error measures introduced by Hyndman and Koehler (2006) and adopted by many successive works in this space.

6.1.1 Scale-Dependent Error Measures

Scale-dependent measures as the name suggests, are dependent on the scale of the series. In all the scale-dependent measures defined below, the scale-dependent base error used is as defined in Equation 9.

| (9) |

Apart from MSE and MAE as defined in Equations 7 and 8, other examples of scale-dependent measures which use as the base error are as defined below.

-

1.

Root Mean Squared Error (RMSE)

(10) -

2.

Root Median Squared Error (RMdSE)

(11) -

3.

Median Absolute Error (MdAE)

(12) -

4.

Geometric Root Mean Squared Error (GRMSE) - Proposed by Syntetos and Boylan (2005).

(13) Geometric Mean Absolute Error (GMAE)

(14)

Since RMSE is on the same scale as the original data (due to the square and the square-root), it is often preferred over MSE. Squared errors are known to lead to unbiased point forecasts since they predict the mean when used as a loss function (Kolassa, 2016). Although the definitions are slightly different, mathematically both GMAE and GRMSE are equivalent. The problem specifically with these geometric mean based measures is that a model can perform perfectly (0 or error) on one series and quite bad on all the others but still become the best (as the overall error becomes 0 or quite small due to multiplication) (Boylan and Syntetos, 2006).

Scale-invariant measures on the other hand are introduced for the requirement to be able to compare across series having different scales. Traditionally in forecasting, one series was mostly considered as a single dataset by practitioners in the domain. Therefore, scaling errors was limited to scales computed per each series or even each time step (to be able to compare errors across series). These approaches had several issues as explained next. However, in the current context of Big Data and global forecasting models, we are now in the situation where we want to compare models across datasets or select models that perform generally well on many datasets each having many series. Consequently, the error measures being introduced have also shifted from computing a scale per-series to a scale for the whole dataset. Such global scaling based error measures can address some of the issues with the per-step or per-series scaling. Nevertheless, Chen et al. (2017) state that despite the type of scaling used, the resulting error measure values need to be closely related to the scale of the series at the specific observation points. Hence, those authors opt for those measures that compute a per-step scaling. Due to the non-stationarities and non-normalities that are inherent in many time series, a constant estimator for scale (along the series or for the whole dataset) has been shown as a comparatively poor form of scaling for time series (Chen et al., 2017).

6.1.2 Measures based on Percentage Errors

In percentage error based measures, base errors are scaled by actual time series values. This means that the time series values get scaled with respect to the actual scale of the series. Percentage based measures were invented for inventory based series (having very high volumes, no intermittency) since they are more meaningful as indicating the percentage loss and thus easy to communicate. The percentage error is usually defined as in Equation 15, where is the scale-dependent error and is the actual value at the time step.

| (15) |

Examples of percentage errors are as follows.

-

1.

Mean Absolute Percentage Error (MAPE)

(16) -

2.

Median Absolute Percentage Error (MdAPE)

(17) -

3.

Root Mean Square Percentage Error (RMSPE) - Used in the Rossmann Store Sales Forecasting Competition111https://www.kaggle.com/c/rossmann-store-sales (Bojer and Meldgaard, 2020)

(18) -

4.

Root Median Square Percentage Error (RMdSPE)

(19)

Percentage based measures have the issue that is not symmetric since exchanging with changes the value of the error measure. Moreover, percentages can be above 100% sometimes, which makes a flat forecast of all 0’s a better forecast with a 100% MAPE (Kolassa, 2017). Apart from that, percentage based measures only make sense with the existence of a meaningful zero (where divisions and ratios are meaningful). Other forms of percentage based measures have been introduced with different scaling factors.

-

5.

Symmetric Mean Absolute Percentage Error (sMAPE) - Idea first proposed by Makridakis (1993)222The original definition of sMAPE used at the M3 forecasting competition did not use absolute values of and in the denominator, since all series had only positive values there.

(20) -

6.

Symmetric Median Absolute Percentage Error (sMdAPE)

(21)

sMAPE fixes the type of asymmetry seen with MAPE that the penalisation is different if and are exchanged. Hence, it was used heavily in most early forecasting competitions. However, sMAPE is not as symmetric as its name suggests (Goodwin and Lawton, 1999); it is arguably even less symmetric. It penalises the underestimates more than the overestimates for the same value of . Thus, it may tend towards selecting a slightly overestimating model. Nevertheless, this kind of asymmetry may be of interest to certain domains where underestimates are considered to be more costly than overestimates (Armstrong, 2001). sMAPE is also in general further criticised for its lack of interpretability (Hyndman and Koehler, 2006).

-

7.

Modified Symmetric Mean Absolute Percentage Error (msMAPE)

(22)

This was introduced by Suilin (2017), to address issues with sMAPE, as detailed in the next Section. In Equation 22, by default. msMAPE assigns the same scaling factor (0.6 in this case) for all less than or equal a certain threshold (0.5 in this case). This means that in this range, all errors are simply divided by a fixed constant, irrespective of the actual value or the forecast of the series. This idea is similar to the concept of winsorising of error distributions suggested by Armstrong and Collopy (1992), which is to clip extreme values/outliers (tails of the distribution) of the errors and replace them with certain limits/thresholds. Arnott et al. (2019) discuss the same idea of winsorisation for the purpose of excluding outliers from the data in the first place. In this sense, msMAPE can be considered as a winsorised version of sMAPE.

However, the exact threshold at which to cut off the errors/data, depends on the scale of the series. For example, this threshold cannot be the same (say 0.5) on two series where one goes to a maximum value of 1000 and the other has values only in-between 0-1. Also, winsorising basically skews the error measure/data since all values in the distribution are cut off at a certain threshold. Therefore, msMAPE is rather ad-hoc and it does not estimate any statistic like the mean or median of the distribution; it is rather a biased version of mean/median. Apart from that, the issues arising from symmetry in sMAPE are still there in msMAPE as well, but only for larger actuals and forecasts that exceed the threshold. Due to these reasons, msMAPE is often disapproved by researchers, as it has no theoretical foundation and its statistical properties have not been explored.

Kim and Kim (2016) introduced the Mean Arctangent Absolute Percentage Error (MAAPE), which retains the original scaling factor of percentage based measures, and thus its associated intuitive interpretation.

-

8.

Mean Arctangent Absolute Percentage Error (MAAPE)

(23)

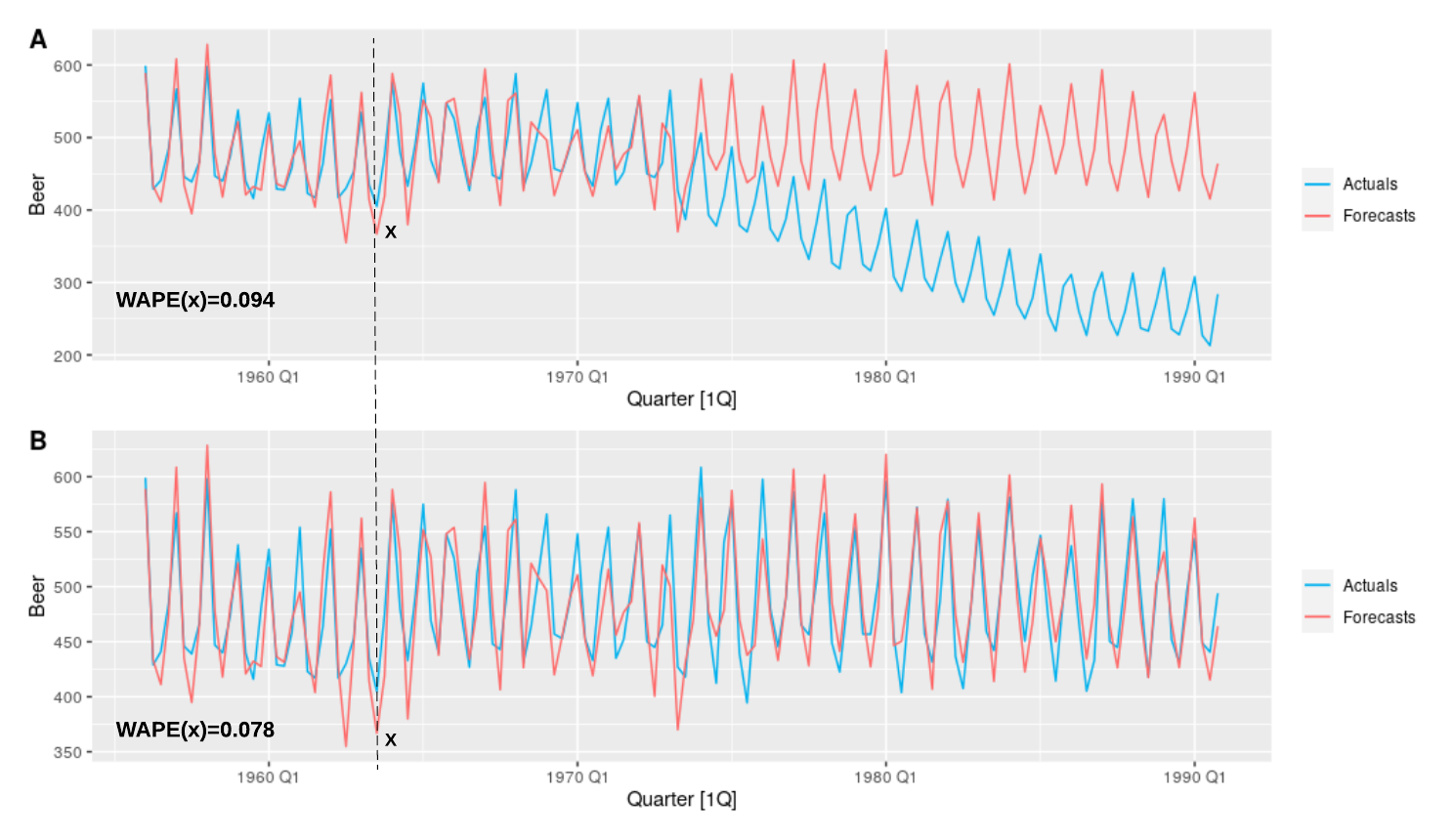

The Weighted Absolute Percentage Error (WAPE) is defined as in Equation 24 and performs the scaling based on the OOS values of the series in the whole forecast horizon.

-

9.

Weighted Absolute Percentage Error (WAPE)

(24)

Similar to the modification on MAPE to obtain sMAPE, WAPE can also be modified in the denominator to form the Symmetric Weighted Absolute Percentage Error (sWAPE) measure, although this has not been defined previously in the literature, to the best of our knowledge. Similar to sMAPE, sWAPE also avoids the problem of the final error being different when and are exchanged.

-

10.

Symmetric Weighted Absolute Percentage Error (sWAPE)

(25)

A similar version can be defined as follows, using squared errors in the numerator as opposed to absolute errors.

-

11.

Weighted Root Mean Squared Percentage Error (WRMSPE)

(26)

WAPE and WRMSPE defined above are for a single series, whereas for multiple series, the per-series errors can be summarised using mean, median etc. In the denominator of WAPE and WRMSPE, is the length of the training part of the series whereas is the size of the forecast horizon. A different version of the OOS scaling of WAPE was proposed by Wong (2019) as in Equation 27.

-

12.

Relative Total Absolute Error (RTAE)

(27)

RTAE above is defined for a single series. In Equation 27, refers to a regularisation constant to ensure that the denominator does not fall below the threshold . In this sense, RTAE also follows the concept of winsorising discussed above for msMAPE and thus, all the associated issues hold here as well. However, as opposed to WAPE and RTAE where the aggregation of the values in the denominator is done OOS, this aggregation can be done in-sample as well. Petropoulos and Kourentzes (2015) use a set of error measures in their work that follow this idea. The base error for these measures is defined as in Equation 28 where stands again for the length of the training part of the series.

| (28) |

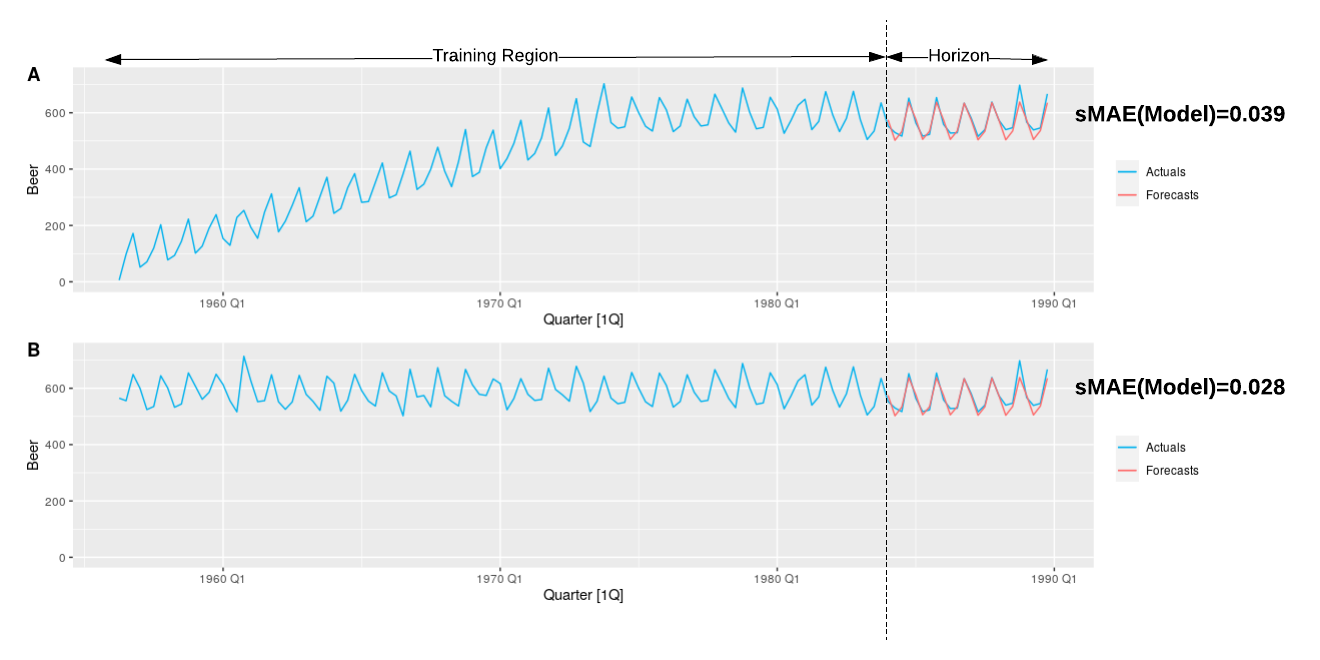

In the work by Petropoulos and Kourentzes (2015), is named as the scaled Error (sE) and is named as the scaled Squared Error (sSE). Similarly the scaled Absolute Error (sAE) is defined in Equation 29.

| (29) |

In both and , the error at time step in the forecast horizon is scaled by the mean of the actual values in the whole training region of the series. They are named as scaled errors to indicate similarity to the scaled errors discussed further in Section 6.1.5, where error measures are scaled by a scaling factor dependent on the time series to make them scale-free. However, in this case, since actual values of the series are used to compute the scale, they can be interpreted similar to the aforementioned percentage based measures. The error measures by using these as the base errors can be defined as below.

-

13.

Scaled Mean Error (sME)

(30) -

14.

Scaled Mean Squared Error (sMSE)

(31) -

15.

Scaled Mean Absolute Error (sMAE)

(32)

Another option for scaling based on actual values is to consider the OOS values (in the forecast horizon) as in the WAPE error measure mentioned above, but aggregated over all the series in the dataset. Salinas et al. (2020) use such error measures in their work as defined below.

-

16.

Normalised Deviation (ND)

(33) -

17.

Normalised Root Mean Squared Error (NRMSE)

(34)

6.1.3 Measures based on Relative Errors

In Relative Errors, scaling is done through dividing by errors from a benchmark method. This scaling is done per each time step (the error of the model at a particular time step is divided by the error from a benchmark method such as the naïve or the seasonal naïve for the same time step). The idea is to measure the performance of the forecasting model with respect to this benchmark method. On top of being scale-independent (errors scaled with respect to the scale of the series), relative measures are useful when necessary to average over series that differ in forecastability. These measures can standardise the series for their degree of difficulty in forecasting since the models are compared against a benchmark method on the same series (Armstrong et al., 2001). The relative error is defined as in Equation 35 where denotes the error of a benchmark method, commonly the naïve method.

| (35) |

Measures based on relative errors are as defined below.

-

1.

Mean Relative Absolute Error (MRAE)

(36) -

2.

Median Relative Absolute Error (MdRAE)

(37) -

3.

Root Mean Relative Squared Errors (RMRSE)

(38) -

4.

Geometric Mean Relative Absoluate Error (GMRAE)

(39) Relative Geometric Root Mean Squared Error (RGRMSE)

(40) Although the definitions are slightly different, mathematically both GMRAE and RGRMSE are equivalent.

The biggest advantage of these measures is that they are more interpretable, and directly comparable across datasets unlike those unbounded measures mentioned before. For instance, a MAPE value of 1% in itself gives no indication whether it is a high or a low value for the particular series without any explicit benchmark comparisons. On the other hand, measures which scale based on benchmark errors give direct interpretation of how good or bad the model is with respect to the benchmark, and thus also become comparable across datasets. However, with these relative measures the relative magnitude of the overall errors that we get depends on the competence of the underlying benchmark method on the respective series. Large errors from the benchmark methods tend to lessen the impact of the errors from our models. The opposite can happen too, where the underlying benchmark method is extremely good on one of the series in the dataset (very low benchmark errors), and thus overly exaggerates the errors from the forecasting model for that particular series, compared to the others. Thus, it becomes hard to capture models that do well on such series. Therefore, the choice of the benchmark method plays an important role for relative errors.

6.1.4 Relative Measures