Interval Dominance based Structural Results for Markov Decision Process

Abstract

Structural results impose sufficient conditions on the model parameters of a Markov decision process (MDP) so that the optimal policy is an increasing function of the underlying state. The classical assumptions for MDP structural results require supermodularity of the rewards and transition probabilities. However, supermodularity does not hold in many applications. This paper uses a sufficient condition for interval dominance (called ) proposed in the micro-economics literature, to obtain structural results for MDPs under more general conditions. We present several MDP examples where supermodularity does not hold, yet holds, and so the optimal policy is monotone; these include sigmoidal rewards (arising in prospect theory for human decision making), bi-diagonal and perturbed bi-diagonal transition matrices (in optimal allocation problems). We also consider MDPs with TP3 transition matrices and concave value functions. Finally, reinforcement learning algorithms that exploit the differential sparse structure of the optimal monotone policy are discussed.

KEYWORDS. MDP, Interval Dominance, monotone policy, supermodularity, differentially sparse policies, reinforcement learning

1 Introduction

Markov decision processes (MDPs) are controlled Markov chains. Brute force numerical solution to compute the optimal policy of an MDP with a large state and action space is expensive and yields little insight into the structure of the controller. Structural results for MDPs are widely studied in stochastic control, operations research and economics (Topkis, 1998; Amir, 2005; Puterman, 1994; Heyman and Sobel, 1984). They impose sufficient conditions on the parameters of an MDP model so that there exists an optimal policy that is increasing111We use increasing in the weak sense to mean non-decreasing. in the state , denoted as . Such monotone optimal policies are useful as they yield insight into the structure of the optimal controller of the MDP. Put simply, they provide a mathematical justification for rule of thumb heuristics such as choose a “larger” control action for a “larger” state. Also, since monotone optimal policies are differentially sparse (see Sec.5), optimization algorithms and reinforcement learning algorithms that exploit this sparsity can solve the MDP efficiently (Krishnamurthy, 2016; Mattila et al., 2017).

The textbook proof (Puterman, 1994; Heyman and Sobel, 1984) for the existence of a monotone policy in a MDP relies on supermodularity. By imposing sufficient conditions on the rewards and transition probabilities of the MDP, the classical proof shows that the function in Bellman’s dynamic programming equation is supermodular. (These conditions are reviewed in Section 2.) With denoting a finite state space and action space, recall Topkis (1998) that a generic function is supermodular222More generally supermodularity applies to lattices with a partial order (Topkis, 1998). In our simple setup of (1), Puterman (1994) uses the terminology ‘superadditive’ instead of supermodular. if it has increasing differences:

| (1) |

Topkis’ theorem then states that supermodularity is a sufficient condition for

| (2) |

So if it can be shown for an MDP that its function is supermodular, then Topkis theorem implies that there exists an optimal policy that is monotone:

However, supermodularity can be a restrictive sufficient condition for the existence of a monotone optimal policy; it imposes conditions on the rewards and transition probabilities that may not hold in many cases.

More recently, Quah and Strulovici (2009) introduced the Interval Dominance condition which is necessary and sufficient for (2) to hold. For the purposes of our paper, Quah and Strulovici (2009, Proposition 3) gives the following useful sufficient condition333If is a fixed constant independent of , then (3) is sufficient for the single crossing property (Milgrom and Shannon, 1994), namely, RHS of (1) implies LHS of (1) . Supermodularity implies single crossing which in turn implies interval dominance; see also Amir (2005) for a tutorial exposition. The condition (3) is sufficient for interval dominance and is the main condition that we will use in this paper. for to satisfy interval dominance:

| (3) |

where the scalar valued function (strictly non-negative) is increasing in .

We symbolically denote (3) as the condition

.

Comparing

supermodularity (1) with

in (3), we see that supermodularity is a special case of when .

An important property of is that it compares adjacent actions and . A

more restrictive

condition would be to replace with any action in (3). However, this stronger condition (which in analogy to (1) can be called -supermodularity) is highly restrictive and does not hold for MDP examples considered below.

Main Results. This paper shows how in (3) applies to obtain structural results for MDPs under more general conditions than the textbook supermodularity conditions. Theorems 1 and 2 are our main results. To avoid technicalities we consider finite state, finite action MDPs which are either finite horizon or discounted reward infinite horizon. We present several MDP examples where the functions satisfies but not supermodularity, and the optimal policy is monotone. One important class comprises MDPs with sigmoidal and concave rewards; since a sigmoidal function comprises convex and concave segments, supermodularity rarely holds. Such sigmoidal rewards arise in prospect theory (behavioral economics) based models for human decision making (Kahneman and Tversky, 1979). A second important class of examples we will consider involves perturbed bi-diagonal transition matrices for which the standard supermodularity assumptions do not hold. Bi-diagonal transition matrices arise in optimal allocation with penalty costs (Derman et al., 1976; Ross, 1983). The result in Sec. B complements this classical result for possibly non-submodular costs. Finally, a third class of examples comprises MDPs with integer concave value functions. Theorem 2 and Corollary 5 impose TP3 Theorem 2 and Corollary 5 impose TP3 (totally positive of order 3) assumptions along with to show that the optimal policy is monotone. An extension of the classical TP3 result of Karlin (1968, pg 23) is proved to characterize the condition for MDPs with bi-diagonal and tri-diagonal transition matrices. Such MDPs model controlled random walks (Puterman, 1994) and arise in the control of queuing and manufacturing systems.

2 Background. Supermodularity based Results

An infinite horizon discounted reward MDP model is the tuple . Here denotes the finite state space, and we will denote as the state at time . Also is the action space, and we will denote as the action chosen at time . are stochastic matrices with elements , are dimensional reward vectors with elements denoted , and is the discount factor.

The action at each time is chosen as where denotes a stationary policy . The optimal stationary policy is the maximizer of the infinite horizon discounted reward :

| (4) |

The optimal stationary policy satisfies Bellman’s dynamic programming equation

| (5) |

An MDP with finite horizon is the tuple where is the -dimensional terminal reward vector. (In general and can depend on time ; for notational convenience we suppress this time dependency.) The optimal policy sequence is given by Bellman’s recursion: , , and for ,

| (6) |

Monotone Policies using Supermodularity

For an MDP, the textbook sufficient conditions for in (5) or (6) to be supermodular are

-

(A1)

Rewards is increasing in for each .

-

(A2)

for each , where is the -th row of matrix . 444 denotes first order stochastic dominance, namely, , .

-

(A3)

is supermodular in .

-

(A4)

is supermodular in for each .

-

(A5)

The terminal reward .

The following textbook result establishes and are supermodular; so the optimal policy is monotone:

Proposition 1 ((Puterman, 1994; Heyman and Sobel, 1984))

(i) For a discounted reward MDP, under (A1)-(A4), the optimal policy satisfying (5)

is increasing555More precisely, there exists a version of the optimal policy that is non-decreasing in . Recall that (4) uses the notation since the optimal policy is not necessarily unique. in .

(ii) For a finite horizon MDP, under (A1)-(A5), the

optimal policy sequence , , satisfying (6) is increasing in .

3 MDP Structural Results using Interval Dominance

The supermodular conditions (A3), (A4) on the rewards and transition probabilities, are restrictive. We relax these with the interval dominance condition defined in (3) as follows:

-

(A6)

For and increasing in , the rewards satisfy

(7) -

(A7)

For each , the transition probabilities satisfy

(8) where and is increasing in . ( is not allowed to depend on .)

Equivalently, (8) can be expressed in terms of first order stochastic dominance as(9) - (A8)

Remark. If and , then (A6) and (A7) are equivalent to the supermodularity conditions (A3) and (A4). Then (A8) holds trivially. Note that (A8) is sufficient for the sum of two functions to be .

Main Result. The following is our main result.

Theorem 1

(i) For a discounted reward MDP, under (A1), (A2), (A6), (A7), (A8), there exists an optimal stationary policy satisfying (5) which is increasing in . (ii) For a finite horizon MDP, under (A1), (A2), (A5), (A6), (A7), (A8), there exists an optimal policy sequence , satisfying (6) which is increasing in .

Remark. Theorem 1 also holds for average reward MDPs that are unichain Puterman (1994) so that a stationary optimal policy exists. This is because our proof uses the value iteration algorithm, and for average reward problems, the same ideas directly apply to the relative value iteration algorithm.

Proof: The standard textbook proof (Puterman, 1994) shows via induction that for the finite horizon case, (A1), (A2), (A5) imply that is increasing in for each , and therefore is increasing in . The induction step also constitutes the value iteration algorithm for the infinite horizon case, and shows that and are increasing in .

Assumption (A6) implies the rewards satisfy . Finally, (A8) implies for ,

| (11) |

for . Thus implying that (2) holds.

3.1 Example 1. MDPs with Interval Dominant Rewards

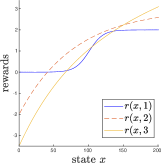

Our first example considers MDPs with sigmoidal and concave666Throughout this paper convex (concave) means integer convexity (concavity). Since , integer convex means . We do not consider higher dimensional discrete convexity such as multimodularity; see Sec.5. rewards. Supermodularity is difficult to ensure since a sigmoidal reward comprises a convex segment followed by a concave segment. In Figure 1(a), reward is sigmoidal, while and are concave in . Since concave reward intersects sigmoidal reward multiple times, the single crossing condition and therefore supermodularity (A3) does not hold. Also is not increasing and so not supermodular. But condition (A6) holds. Specifically, is single crossing, and is single crossing. Note that does not require to be single crossing.

Consider a discounted reward MDP. Assume:

-

(Ex1.1)

For each pair of actions , assume there is state such that , for . Also , for .

Compared to textbook Proposition 1, Statement 1 of Corollary 1 does not impose supermodularity conditions on the rewards or transition probabilities. (Ex1.1) is weaker than the single crossing condition.

First consider . Since , and , (A6) holds for all for some . Also implies (A7) holds for all for some . So we can choose independent of so that (A8) holds.

Next consider . Then (A6) holds for all for some . Also implies (A7) holds for all for some . Therefore, we can choose independent of so that (A8) holds. Finally, for and , (A6) and (A7) hold for all . So Theorem 1 applies and .

Example (i). Sigmoidal777Sigmoidal rewards/costs are ubiquitous. They arise in logistic regression, prospect theory in behavioral economics, and wireless communications. and Concave Rewards

The following MDP parameters satisfy the assumptions of Corollary 1: , . The action dependent transition matrices are

Here denotes the unit -dimension row vector with 1 in the -th position.

Example (ii). Prospect Theory based rewards

In prospect theory (Kahneman and Tversky, 1979), an agent (human decision maker) has utility that is asymmetric sigmoidal in . This asymmetry reflects a human decision maker’s risk seeking behavior (larger slope) for losses and risk averse behavior (smaller slope) for gains. With an even integer, the prospect theory rewards are

| (13) |

so they cross zero at . The shape parameter determines the slope of the reward curve .

Suppose the agents (investment managers) range from (cautious) to (aggressive); so the shape parameter . The value of an investment evolves according to Markov chain with transition probabilities based on agent . Since agent is more aggressive (risk seeking) than agent in losses and gains, it incurs higher volatility. So the -th row of and satisfy

| (14) |

The aim is to choose the optimal agent at each time to maximize the discounted infinite horizon reward. Since is single crossing but not supermodular, (A3) does not apply.

Corollary 2

The proof follows from Corollary 1 with .

3.2 Example 2. Interval Dominant Transition Probabilities

Corollary 3

Consider the discounted reward MDP with where is increasing and non-negative in . Suppose the -th row of transition matrix is

| (15) |

Here denotes the unit -dimension row vector with 1 in the -th position. is an arbitrary -dimensional probability row vector. Also , are increasing in , and satisfy (3). (Also, to ensure is valid transition matrix.) Then Theorem 1 holds.

Compared to supermodularity (A4) of the transition probabilities, Corollary 3 imposes weaker conditions: satisfy (3) and can be any probability vector. Since only needs to satisfy (suitably scaled and shifted to ensure valid probabilities), (15) offers considerable flexibility in choice of the transition matrices.

Proof: Reward satisfies (A1), (A6) for all . Also implies (A2) holds. Next let us verify (A7). Using (15), we need to verify

| (16) |

where is increasing in . Since , clearly satisfying (3) for some increasing in is a sufficient condition for (16) to hold. Since the choice of is unrestricted, we can choose . Hence (A8) holds. Thus Theorem 1 holds.

3.3 Example 3. Discounted MDP with Perturbed Bi-diagonal Transition Matrices

This section illustrates the condition in MDPs with perturbed bi-diagonal transition matrices. The E-companion discusses an example in optimal allocation problems with penalty costs (Ross, 1983; Derman et al., 1976). It also has applications in wireless transmission control (Ngo and Krishnamurthy, 2010).

Consider an infinite horizon discounted reward MDP. The action-dependent transition matrices specified by parameter are

| (17) |

where is a small positive real. We assume that is increasing in . When , are bi-diagonal transition matrices; so can be viewed as a perturbation probability of a bi-diagonal transition matrix.

Supermodularity (A4) of the transition matrices (17) holds if . In this section we assume is a small parameter with , so that (A4) does not hold. Therefore, textbook Proposition 1 does not hold. We show how the condition and Theorem 1 apply.

Remark. In our result below, to show condition holds, we choose . If is differentiable wrt , then as , i.e., for an MDP with bi-diagonal transition matrices, this can be interpreted as choosing .

Corollary 4

Proof: We verify that the assumptions in Theorem 1 hold. (A1) holds by assumption. From the structure of in (17) it is clear that (A2) holds. Considering actions and , it is verified that (A7) holds for all . Next by assumption (18), (A6) holds for . Finally, we can choose , and so (A8) holds.

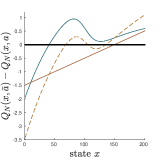

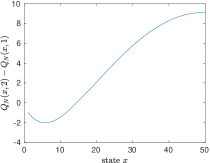

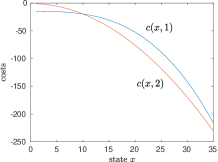

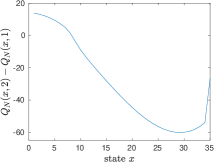

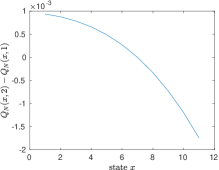

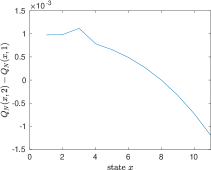

Example. , , , , , , . Given the transition probabilities, we choose . Also for the rewards, we choose in (18). So Corollary 4 holds. Figure 2 shows is not supermodular, yet the optimal policy is monotone with for and for .

4 Example 4. MDPs with Concave Value Functions

Theorem 1 used first order dominance and monotone costs to establish and therefore monotone optimal policies. In comparison, this section extends Theorem 1 to MDPs where the value function is concave. We use second order stochastic dominance and concave costs to establish and therefore monotone optimal policies. The results below assume a TP3 transition matrix; see Karlin (1968) for the rich structure involving their diminishing variation property. For convenience we minimize costs instead of maximize rewards.

-

(C1)

Costs are increasing and concave in for each .

-

(C2)

is TP3with increasing and concave in . Totally positive of order 3 means that each 3rd order minor of is non-negative.

-

(C3)

For and increasing in , .

-

(C4)

For and increasing in , where denotes second order stochastic dominance.888If are probability vectors, then if for each . Equivalently, iff for vector increasing and concave. Recall ′ denotes transpose.

-

(C5)

Terminal cost is increasing and concave in .

Remarks. (i) As shown in the proof, (C1) (concavity), (C2), (C5) imply the value function is concave and increasing. These together with (C3), (C4) and (A8) imply holds and so the optimal policy is monotone.

(ii) (C2) generalizes the assumption that is linear increasing in . The classical result in Karlin (1968, pg 23) states: Suppose is a TP3 transition matrix and is linear increasing in . If vector is concave, then vector is concave. However, for bi-diagonal and tri-diagonal transition matrices, is concave (or convex) and not linear in (see examples below). This is why we introduced (C2). Since the classical result requires being linear in , it no longer applies. So we will prove a small generalization that handles the case where is concave in (see Lemma 1 below).

Theorem 2

Corollary 5

Consider the modified assumptions: (C1): increasing replaced by decreasing; (C2) concave replaced with convex; (C3): inequality involving costs reversed; (C4): replaced by convex dominance999If are probability vectors, then if for each . Equivalently, iff for increasing and convex. ; (C5): increasing replaced by decreasing. Under these assumptions and (A8), Theorem 2 holds with the modification and , are increasing in .

Proof: (Theorem 2) We prove statement (ii). The proof of statement (i) is similar and omitted.

First we show by induction that is increasing in for . By (C5), is increasing. Assume is increasing in . TP3 assumption (C2) implies TP2 which preserves monotone functions (Karlin, 1968, pg 23), (Lehmann and Casella, 1998), namely, is increasing in . This together with (C1) implies is increasing. Thus is increasing in .

Next we show by induction that is concave in . By (C5), is concave. Assume is concave. Then (C2) implies is concave in (see Lemma 1 below). Since is concave by (C1), it follows that is concave in . Since concavity is preserved by minimization, is concave. Finally, increasing and concave in and (C4) implies (10) holds for all . Then with (C3),(A8), the proof is identical to (11) in Theorem 1.

The following lemma used in the proof of Theorem 2 slightly extends the result in Karlin (1968, pg 23).

Lemma 1

Suppose satisfies (C2). If is concave and increasing, then is concave and increasing.

Proof: First TP3 preserves monotonicity, so is increasing. Next, since is concave and increasing, then for any and , has two or fewer sign changes in the order as increases from 1 to . Let . Since is TP3, the diminishing variation property of TP3 implies also has two or fewer sign changes in the order as increases from 1 to . Assume two sign changes occur; then for some , for . Since is integer concave in by (C2), it lies above the line segment that connects to . So , Finally, for arbitrary , we can choose and so that at . Clearly, for arbitrary and for implies is concave.

Example (i). Bi-diagonal Transition Matrices and Non-supermodular Costs

Theorem 2 applies to bi-diagonal transition matrices with possibly non-supermodular costs; this is in contrast to Sec. 3.3 where we considered perturbed bi-diagonal matrices. Consider an MDP with bi-diagonal transition matrices . Then for and for ; so is increasing and concave in ((C2) holds). Assume . Then (C4) is equivalent to . Since , it follows that (C4) holds for all . If (C1), (C3) hold for some , then Theorem 2 holds.

Remarks. (i) For , and concave increasing costs , the following useful single crossing characterization satisfies (C3).

Suppose and the curves and intersect once at . For , the curve grows faster than , i.e., is supermodular for .

For , the difference between and can be arbitrary. Figure 3(i) illustrates this.

(ii) To motivate Theorem 2, (A4) does not hold for bi-diagonal matrices. Since , supermodularity (A3) does not hold. Also, Theorem 1 does not apply since (A7) does not hold.

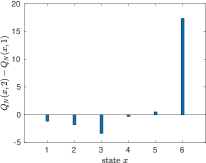

Numerical example. Consider a discounted cost MDP with , , , , , , , . It can be verified that the cost is not supermodular, but the conditions of Theorem 2 are satisfied. So the value function is concave and optimal policy is decreasing. Figure 3(ii) shows is not submodular.

Example (ii). Tri-diagonal Transition Matrices and Non-submodular Costs

Corollary 5 applies to MDPs with tri-diagonal transition matrices where . If is TP3 and , hold, then is increasing and convex in ; so modified (C2) holds. Also, if , , , , then convex dominance (modified (C4)) holds for all . Then if the costs are chosen so that modified (C1), and modified (C3) hold for some , then Corollary 5 holds and the optimal policy is monotone (even though the costs are not submodular when ).

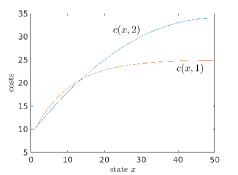

Numerical example. Consider a discounted cost MDP with , , tri-diagonal transition matrices with . Also , , where . The cost is not submodular (see Figure 4(i)), but Corollary 5 holds. Figure 4(ii) shows the non-submodular .

5 Summary and Discussion

Summary. The textbook structural result for MDPs uses supermodularity to establish the existence of monotone optimal policies. This paper shows how supermodularity can be relaxed by formulating a sufficient condition for interval dominance, which we call the condition. We presented several examples of MDPs which satisfy including sigmoidal costs, and bi-diagonal/perturbed bi-diagonal transition matrices. The structural results in Sec.3, namely, Theorem 1, Corollaries 1, 3, 4 and Theorem 3 used first order stochastic dominance to establish for several examples. of MDPs. In comparison, Theorem 2 in Sec.4 discussed examples of in MDPs with concave value functions; we used TP3 assumptions and second order (convex) stochastic dominance to prove the existence of monotone optimal policies.

Discussion 1. Reinforcement Learning (RL) and Differential sparse Policies: Once the existence of a monotone optimal policy has been established, RL algorithms that exploit this structure can be constructed. Q-learning algorithms that exploit the condition can be obtained by generalizing the supermodular Q-learning algorithms in Krishnamurthy (2016). The second approach is to develop policy search RL algorithms. In particular, when is small and is large, then since , it is differentially sparse, that is is positive only at values of , and zero for all other . In Mattila et al. (2017), LASSO based methods are developed to exploit this sparsity and significantly accelerate search for ; they build on the nearly-isotonic regression techniques in Tibshirani et al. (2011). The idea is to add a rectified -penalty to the cost in the optimization problem (here is the estimate of the optimal policy at iteration of the optimization algorithm). Intuitively, this modifies the cost surface to be more steep in the direction of monotone policies resulting in faster convergence of an iterative optimization algorithm.

Discussion 2. Convex Value Functions: Can Theorem 2 be extended to MDPs with convex value functions? Since convexity is not preserved by minimization, we need multimodularity assumptions to show the value function is convex. However, since multimodularity implies supermodularity, we are unable to exploit the weaker condition. Multimodularity is sufficient (but not necessary) for convexity to be preserved by minimization; so it is worthwhile exploring relaxed based versions that do not require supermodularity.

References

- Amir [2005] R. Amir. Supermodularity and complementarity in economics: An elementary survey. Southern Economic Journal, 71(3):636–660, 2005.

- Derman et al. [1976] C. Derman, G. J. Lieberman, and S. M. Ross. Optimal system allocations with penalty cost. Management Science, 23(4):399–403, December 1976.

- Heyman and Sobel [1984] D. P. Heyman and M. J. Sobel. Stochastic Models in Operations Research, volume 2. McGraw-Hill, 1984.

- Kahneman and Tversky [1979] D. Kahneman and A. Tversky. Prospect theory: An analysis of decision under risk. Econometrica, 47(2):263–291, 1979.

- Karlin [1968] S. Karlin. Total Positivity, volume 1. Stanford Univ., 1968.

- Krishnamurthy [2016] V. Krishnamurthy. Partially Observed Markov Decision Processes. From Filtering to Controlled Sensing. Cambridge University Press, 2016.

- Lehmann and Casella [1998] E. Lehmann and G. Casella. Theory of Point Estimation. Springer-Verlag, 2nd edition, 1998.

- Mattila et al. [2017] R. Mattila, C. R. Rojas, V. Krishnamurthy, and B. Wahlberg. Computing monotone policies for markov decision processes: a nearly-isotonic penalty approach. IFAC-PapersOnLine, 50(1):8429–8434, 2017.

- Milgrom and Shannon [1994] P. Milgrom and C. Shannon. Monotone comparative statics. Econometrica, 62(1):157–180, 1994.

- Ngo and Krishnamurthy [2010] M. H. Ngo and V. Krishnamurthy. Monotonicity of constrained optimal transmission policies in correlated fading channels with ARQ. IEEE Transactions on Signal Processing, 58(1):438–451, 2010.

- Puterman [1994] M. Puterman. Markov Decision Processes. John Wiley, 1994.

- Quah and Strulovici [2009] J. Quah and B. Strulovici. Comparative statics, informativeness, and the interval dominance order. Econometrica, 77(6):1949–1992, 2009.

- Ross [1983] S. Ross. Introduction to Stochastic Dynamic Programming. Academic Press, San Diego, California., 1983.

- Tibshirani et al. [2011] R. J. Tibshirani, H. Hoefling, and R. Tibshirani. Nearly-isotonic regression. Technometrics, 53(1):54–61, 2011.

- Topkis [1998] D. M. Topkis. Supermodularity and Complementarity. Princeton University Press, 1998.

Appendix A Toy Example Illustrating Rewards

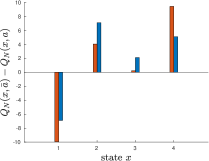

Sec. 3.1 discussed an intuitive visualization of property of rewards for a MDP in terms of the reward curves vs state. We now provide a second intuitive visualization displayed in Figure 5(a) in terms of the reward curves vs actions . This is similar to the discussion in Quah and Strulovici [2009]. For supermodular rewards, increases with . Examining Figure 5(a), for (where ), the differences between the reward curves can be arbitrary, as long as as required by (A1). Also the curve satisfies that , while the curve satisfies ; so the single crossing property is violated. Yet condition , namely, (A6) holds.

The following MDP satisfies Theorem 1: , , , ,

Note that while . Jointly, these violate both supermodularity and also single crossing. But the condition (3) holds since it compares action 1 with action 2, and action 2 with action 3. Indeed, (A6) holds for and . Also (A7) holds for all . Figure 5(b) plots and . Clearly is not supermodular. But the optimal policy is monotone by Theorem 1.

Appendix B Optimal Allocation MDP with Penalty Cost

This section discusses a finite horizon penalty-cost MDP with perturbed bi-diagonal transition matrices (17). This has applications in optimal allocation problems with penalty costs [Ross, 1983, Derman et al., 1976] and wireless transmission control [Ngo and Krishnamurthy, 2010]. We assume ; so as discussed in Sec. 3.3 supermodularity condition (A4) does not hold.

As in Example 4.2 in Ross [1983, pg.8] and Derman et al. [1976], we consider an -horizon MDP model. There are -stages to construct components sequentially. If effort is allocated then the component is constructed with successfully with probability . Our transition matrices are specified by the perturbed bi-diagonal matrices (17). At the end of stages, the penalty cost incurred is if we are components short, where , with . Ross [1983] considers a continuous action space as the closed interval , where and bi-diagonal matrices (). Although the condition yields degenerate policies for , it applies to non-supermodular cost structures with perturbed bi-diagonal matrices. Such cases cannot be handled by the convexity based supermodularity approach.

We consider the discrete action space corresponding to discretization of the continuous valued actions: . Recall are perturbation probabilities of the bi-diagonal transition matrices in (17). The costs and transition probability parameter in terms of the discretized actions are

| (19) |

We make the following assumptions; they are discussed after Theorem 3 below.

-

(A9)

and . (The can be relaxed, see remark below.)

-

(A10)

Terminal cost convex and with . Cost . (More generally, in (20) .)

Main Result. We will work with the modified value function . This is convenient since the terminal condition is for all . The dynamic programming recursion (6) expressed in terms of and minimizing the cumulative cost (rather than maximizing the cumulative reward) is

| where | (20) | |||

Theorem 3

Remarks. 1. Theorem 3 can be viewed as complementary result to the structural result in Ross [1983], Derman et al. [1976]. On the one hand, if we choose the same instantaneous cost as Ross [1983], namely for some constant , then (21) becomes . But terminal costs satisfying this condition yield monotone policies that are degenerate, namely, for all . So for , the condition does not yield a useful result. It is necessary to exploit convexity of the value function, as in Ross [1983], to obtain non-degenerate optimal policies.

On the other hand, the condition (21) allows for non-submodular

costs and yields monotone policies (see examples below).

For such cases, it is not clear how to extend the convexity based submodularity proof in Ross [1983] (which applies when ) to the MDP (17) for arbitrary .

2. Regarding the assumptions,

(A9) is equivalent to and convex.

(A9) can be relaxed to by imposing stronger conditions on (21), see (22) below.

The convexity (A10) of terminal costs implies in (20) is decreasing. Recall decreasing costs (A1) is used to show submodularity (and Theorem 1).

3. Theorem 3 considers costs (negative of rewards) whereas Theorem 1 considers rewards. Note (A1) is equivalent to the cost decreasing in the state. Also inequality (A6) is reversed in terms of costs.

Examples. We chose the MDP parameters in (17), (19)

as , , , ,

. Figure 6 displays for two cases: (i)

, , (ii)

, , .

In case (ii), is not submodular; see Figure 6(b).

But Theorem 3 holds; so optimal policy .

Proof of Theorem 3 Using the modified dynamic programming recursion (20), we verify the assumptions in Theorem 1. Examining the transformed cost in (20), (A1) holds for , , if is convex and increasing, and is decreasing in , i.e, (A10) holds. From the structure of in (17), (A2) holds. The terminal cost in (20) is for all states; so (A5) holds trivially. Next by (A9), . So for actions and , it is easily verified that (A7) holds for . So .