Generating Independent Replicates Directly from the Posterior Distribution for a Class of Spatial Latent Gaussian Process Models

Jonathan R. Bradley111(to whom correspondence should be addressed) Department of Statistics, Florida State University, 117 N. Woodward Ave., Tallahassee, FL 32306-4330, jrbradley@fsu.edu and Madelyn Clinch222Department of Statistics, Florida State University, 117 N. Woodward Ave., Tallahassee, FL 32306-4330

Abstract

Markov chain Monte Carlo (MCMC) allows one to generate dependent replicates from a posterior distribution for effectively any Bayesian hierarchical model. However, MCMC can produce a significant computational burden. This motivates us to consider finding expressions of the posterior distribution that are computationally straightforward to obtain independent replicates from directly. We focus on a broad class of Bayesian latent Gaussian process (LGP) models that allow for spatially dependent data. First, we derive a new class of distributions we refer to as the generalized conjugate multivariate (GCM) distribution. The GCM distribution’s theoretical development is similar to that of the CM distribution with two main differences; namely, (1) the GCM allows for latent Gaussian process assumptions, and (2) the GCM explicitly accounts for hyperparameters through marginalization. The development of GCM is needed to obtain independent replicates directly from the exact posterior distribution, which has an efficient projection/regression form. Hence, we refer to our method as Exact Posterior Regression (EPR). Illustrative examples are provided including simulation studies for weakly stationary spatial processes and spatial basis function expansions. An additional analysis of poverty incidence data from the U.S. Census Bureau’s American Community Survey (ACS) using a conditional autoregressive model is presented.

Keywords: Bayesian hierarchical model; Big data; Gibbs sampler; Log-Linear Models; Markov chain Monte Carlo; Non-Gaussian; Nonlinear.

1 Introduction

MCMC has become an invaluable tool in statistics and is covered in standard text books (Robert and Casella,, 2004). MCMC is an all purpose strategy that allows one to obtain dependent samples from a generic posterior distribution. There are several theoretical considerations that one needs to consider when implementing MCMC to obtain samples from the posterior distribution including, ergodicity, irreducibility, and positive recurrence of the MCMC. In addition to theoretical considerations, practical implementation issues arise, including, a potential for high computational costs, assessing convergence (Gelman and Rubin,, 1992; Cowles and Carlin,, 1996), tuning the MCMC (Roberts and Rosenthal,, 2009), and computing the effective sample size of the Markov chain (Vats et al.,, 2019), among other considerations. One of the current state-of-the-art techniques in MCMC is Hamiltonian Monte Carlo (HMC, Neal,, 2011). HMC is a MetropolisHastings algorithm, where Hamiltonian dynamic evolution is used to propose a new value. In general, HMC leads to “fast mixing” (i.e., converges relatively quickly to the posterior distribution) because it provides a sample from the joint posterior distribution of all processes and parameters, and moreover, has been optimized efficiently using the software Stan (Carpenter et al.,, 2017).

Of course, MCMC is not needed if one can obtain independent replicates directly from the posterior distribution efficiently. In this article, we revisit the problem of generating independent replicates directly from the posterior distribution for a broad class of spatial latent Gaussian process models (LGP, e.g., see Gelfand and Schliep,, 2016). Much of the current literature does not consider solving this problem, since obtaining independent replicates directly from the exact posterior distribution for Bayesian spatial LGPs is a difficult problem, and MCMC can easily be adapted to many settings. We consider Bayesian spatial LGPs for Gaussian distributed data, Poisson distributed data, and binomial distributed data. The samples from our proposed model are independently drawn, and hence avoid issues with convergence, tuning, and positive autocorrelations in a MCMC. Moreover, our exact replicates have an interpretable projection formulation. This regression-type projection can be computed efficiently using known block matrix inversion formulas (Lu and Shiou,, 2002). Thus, we refer to our method as Exact Posterior Regression (EPR), which is the one of the contributions of this article.

Conjugate prior distributions are often restricted to the data type. For example, for binomial, negative binomial, Bernoulli, and multinomial distributed data, the fixed and random effects are conjugate with the multivariate logit-beta distribution (Gao and Bradley,, 2019; Bradley et al.,, 2019), which is the special case of the conjugate multivariate (CM) distribution. Similarly, Poisson and Weibull distributed data are conjugate with the multivariate log-gamma distribution (Bradley et al.,, 2018; Hu and Bradley,, 2018; Xu et al.,, 2019; H.-C.Yang et al.,, 2019; Parker et al.,, 2020, 2021), another special case of the CM distribution. Finally, mixed effects models for Gaussian distributed data regularly make use of Gaussian priors for fixed and random effects (Gelman et al.,, 2013), which is also a type of CM distribution. Thus, our second major contribution is to extend the conjugate multivariate (CM) distribution (Bradley et al.,, 2020a) to LGPs. Additionally, conjugate prior distributions and the CM distribution do not allow one to explicitly account for hyperparameters without the use of MCMC or approximate Bayesian techniques. Thus, in our extension of the CM to LGPs we marginalize across hyperparameters. We call this new distribution the generalized CM (GCM) distribution, which allows for standard latent Gaussian process model specifications of spatial LGPs (e.g., see Gelfand and Schliep,, 2016, for a recent discussion). Furthermore, we develop conditional distributions for GCM distributed random vectors.

A key step in our formulation is the incorporation of what we call “discrepancy term,” which are simply additive term introduced into a mixed effects model similar to that of Bradley et al., (2020b) and Bradley et al., (2023). Classical spatial LGP models set these parameters equal to zero. When these terms are not set equal to zero and instead given a type of improper prior then we show that the implied posterior distribution for fixed and random effects is of the form of a GCM, which we can directly sample from (bypassing the need for MCMC). However, we show that posterior replicates from this GCM can overfit the latent process. Thus, we suggest including these discrepancy parameters in the model to bypass MCMC, and then marginalize them from the posterior distribution and estimate them to be zero.

We emphasize the high potential impact of the contributions of EPR and GCM, since much of the literature places a high consistent emphasis on using MCMC strategies to obtain asymptotically exact correlated samples from the posterior distribution. For example, at the time of writing this manuscript the following papers use MCMC in a spatial LGP setting: Kang et al., (2023), Konomi et al., (2023), Porter et al., (2023), Vranckx et al., (2023), and Zhang et al., (2023a), among others. All of these analyses can easily be adapted to be implemented using EPR, which completely avoids MCMC.

EPR allows one to efficiently analyze several types of correlated spatial data. In particular, we consider modeling three “types of data,” namely, conditionally Gaussian, Poisson, and binomial distributed spatial data. Computationally expensive MCMC techniques have become a standard for modeling spatial data (Robert and Casella,, 2011; Gelfand and Schliep,, 2016). Also, a common approximate Bayesian technique used frequently in the spatial statistics literature is referred to as integrated nested Laplace approximations (INLA, Lindgren et al.,, 2022). In this article, we compare MCMC and INLA to EPR.

To summarize, the contributions of this article can be classified into two groups:

-

1.

The first group of contributions of this article develops the GCM distribution. This includes integral expressions for the GCM distribution and the conditional GCM distribution up to a proportionality constant. The key literature on conjugate modeling began with Diaconis and Ylvisaker, (1979)’s seminal paper which formally developed univariate conjugate models for the exponential family. Then Chen and Ibrahim, (2003) developed Diaconis and Ylvisaker, (1979)’s work in the context of fixed effects models and Bradley et al., (2020a) developed Diaconis and Ylvisaker, (1979)’s work in the context of mixed effects models. However, all of these papers require one to match the form of the prior distribution with that of the likelihood. The use of the GCM allows one to consider LGPs. Moreover, this literature often does not emphasize hyperparameters; however, our development explicitly addresses hyperparameters through marginalization. It should be noted that the theoretical development of the GCM is similar to that of the CM distribution (Bradley et al.,, 2020a). However, the GCM has an enormous practical advantage over the CM by allowing one to use a more standard class (i.e., LGP) of process and prior distributions for spatial data and avoids MCMC updates of hyperparameters. For example, when using the CM for a Poisson data settings, one uses multivariate log-gamma priors for fixed and random effects and updates shape/rate parameters in an MCMC. When using the GCM one can use Gaussian priors and avoid sampling hyperparameters in an MCMC.

-

2.

The second group of contributions of this article allows one to use the GCM in a Bayesian LGP context to produce what we call exact posterior regression (EPR). Much of the Bayesian literature is shifting its’ focus on avoiding MCMC through the use of approximate Bayesian methods (e.g., see Wainwright and Jordan,, 2008; Rue et al.,, 2009) or through direct sampling of the posterior distributions in special cases for Gaussian data (Zhang et al.,, 2021; van Erven and Szabó,, 2021; Shirota et al.,, 2023; Zhang et al.,, 2023b). Recently, Bradley et al., (2023) developed an exact sampler from the posterior distribution for a deep Bayesian statistical model for Gaussian and non-Gaussian spatio-temporal data referred to as the deep hierarchical generalized transformation model. EPR adds to this growing literature by allowing one to independently sample from the posterior from a broad class of spatial LGPs. By “broad” we mean that many existing spatial LGPs can be written in terms of our formulation. We show that the posterior distribution for fixed and random effects are GCM. Furthermore, we use matrix algebra techniques to aid in the computation of EPR (see Theorems 3.3 and 3.4).

The remainder of the article proceeds as follows. Before we introduce our proposed LGP, we will first provide derivations of the GCM and conditional GCM distribution in Section 2. We emphasize that that GCM random vectors are derived through how they are simulated. Then, in Section 3 we show that our proposed model’s posterior distribution is GCM, and we describe how to efficiently sample independent replicates directly from the marginal posterior of the fixed effects, and random effects (which we call EPR). Illustrations are provided in Section 4, which includes several simulations/comparisons (15 in total) including common models used in spatial statistics: weakly stationary spatial processes, spatial basis function expansions, and conditional autoregressive models. The main goal of our illustrations is to compare to several common existing strategies for Bayesian spatial LGPs. Proofs are given in the Appendix, and a discussion is given in Section 5.

2 Preliminary Derivations: The Generalized Conjugate Multivariate Distribution

We now derive the generalized conjugate multivariate (GCM) distribution. This development is similar to the development of the CM distribution from Bradley et al., (2020a). We give a review of the CM distribution in Appendix A. The difference between the GCM and CM is that the GCM drops the assumption of identical classes of DY random variables, and marginalizes across a generic -dimensional real-valued parameter vector . The GCM is needed for our main contribution of EPR in Section 4.

The GCM is defined by the transformation,

| (1) |

where the -dimensional random vector , -dimensional random vector , the -dimensional random vector with -th element , “DY” is a shorthand for the well known Diaconis-Ylvisaker random variable (Diaconis and Ylvisaker,, 1979) (see Appendix A for a review), the subscript “M” stands for “Multi-type,” the real-valued matrix is an invertable covariance parameter matrix, and is an unknown -dimensional real-valued location parameter vector. The function is referred to as the unit log partition function, and we consider , , and for real-valued . It is known that is normally distributed with mean and variance , is the log of a gamma random variable with shape and rate , and is the logit of a beta random variable with shape parameters and rate (Bradley et al.,, 2020a).

Let be a known matrix valued function, such that exists for every -dimensional for a generic real-valued set . Let be distributed according to the proper density , where is independent of , , , and . Sampling from the marginal distribution (marginalizing across ) is straightforward; namely, first sample from and then compute the transformation in (1) to produce a sample from . The pdf is stated in Theorem 2.1.

Theorem 2.1.

Let y be defined as in (1). Then the pdf for y is given by,

| (2) |

where , , , , ,

, the matrix , is an matrix of zeros, is an identity matrix, the -dimensional vector , and the -dimensional vector .

Proof: See Appendix B.

We use the shorthand for the density in (2.1).

Sampling directly from a GCM distribution requires two items:

-

1.

One must be able to sample the random vector directly from its prior distribution .

-

2.

One must be able to the sample independent DY random variables contained in the vector .

In this article, the parameter vector typically consists of variance parameters and spatial range parameters. These parameters will be given independent inverse gamma prior or uniform prior distributions, which one can sample from directly. Additionally, the class of LGPs in Section 3 lead to DY random variables that are either independent univariate normal, beta, or gamma random variables, which are straightforward to simulate from directly using standard software. The fact that we can sample independent replicates of a GCM random vector directly is crucial in Section 3, where we show that a certain class of LGPs leads to a posterior distribution that is GCM (i.e., is of the form in Theorem 2.1), and hence, one can directly sample from it.

We now provide the integral expression for the conditional GCM in Theorem 2.2 up to a proportionality constant.

Theorem 2.2.

Let , where is -dimensional and is -dimensional. Also, let , where H is a and Q is . Then, it follows

where .

Proof: See Appendix B.

We use the shorthand cGCM for the conditional GCM in Theorem 2.2. It is not known how to simulate directly from a cGCM.

3 Methodology

In this section, we outline how to sample from the posterior distribution of fixed and random effects from a general class of spatial LGPs. We define EPR in Section 3.1 for areal spatial data, define the extension to spatial process models in Section 3.2, and discuss computational issues in Section 3.3.

3.1 Exact Posterior Regression for Regional Data

Suppose we observe data from the exponential family, let the total number of observations be denoted with , and denote the -dimensional data vector with . Let represent the data at region (e.g., counties, census tracts, etc.). Then assume belongs to a member of the exponential family of distributions. In particular, we assume one of the following:

| (3) |

where “EF” is a shorthand for the natural exponential family (see Appendix A for more details), and is the log-partition function. For example, when with and we have that is normally distributed with mean and variance . When and we have that is Poisson distributed with mean . Similarly, when with integer and we have that is binomial distributed with sample size and probability of success . In this article, we consider these three cases (i.e., normal, Poisson and binomial distributed cases), and note that binomial distributed data allows for Bernoulli distributed data as a special case (i.e., ), and multinomial distributed data when using a stick-breaking representation of the multinomial (e.g., see Bradley et al.,, 2019, for stick-breaking in the context of CM prior distributions).

Now, organize the latent random variable into the -dimensional vector . Consider the following linear model assumption for y (McCullagh and Nelder,, 1989):

| (4) |

where X is a matrix of known covariates, and is an unknown -dimensional vector of regression coefficients. Let have a Gaussian prior with -dimensional location vector , and covariance matrix , where . Let G be a matrix of coefficients for the -dimensional random effects . In this article, G will be set equal to a known pre-specified matrix of basis functions (e.g., splines (Wahba,, 1990), wavelets (Novikov et al.,, 2005), Moran’s I basis functions (Hughes and Haran,, 2013), etc.), or a matrix square root of a known spatial covariance matrix. We assume is Gaussian with -dimensional location vector and covariance matrix , where . Let be a generic -dimensional parameter vector with prior distribution .

Traditionally, the fine-scale variability term is assumed to be Gaussian (Cressie and Wikle,, 2011). In our framework, it will prove to be useful to specify the distribution for to be a cGCM that is “close” to a Gaussian distribution. Specifically, let the distribution for be proportional to a cGCM, where the -dimensional discrepancy parameter , and are -dimensional real-vectors, and matrix-valued precision parameter . The -dimensional shape parameter when the data is assumed Gaussian, and when the data is assumed to be distributed according to the Poisson or binomial distributions, where and is a matrix of ones. The -dimensional shape parameter when the data is assumed to be either Gaussian or Poisson distributed, and when the data is assumed to be distributed according to the binomial distribution. Let with . The unit-log partition function is,

for any . It is straightforward to verify that when we have that cGCM is proportional to a Gaussian distribution with mean and covariance with . This choice of cGCM with will ensure that the implied posterior distribution has parameters that do not lie on the boundary of the parameter space.

The terms , , and are covered in standard textbooks in spatio-temporal statistics (Cressie and Wikle,, 2011), and are referred to as large-scale variability, small-scale variability, and fine-scale variability, respectively. In more recent literature a fourth term has been considered (Bradley et al.,, 2020b, 2023); that is, the -dimensional vector discrepancy parameter. These discrepancy parameters often lead to more efficient procedures to sample from the posterior distribution. In our case, a particular form of leads the fixed and random effects to be distributed according to a GCM, which from Section 2, we know how to sample from directly without approximations and without MCMC. Specifically, let , where Q are the eigenvectors of the orthogonal complement of the matrix,

| (5) |

so that and , where recall that idempotent matrices have eigenvalues equal to zero or one. Let , where “blkdiag” be the block diagonal operator. The free parameter q is now referred as the “discrepancy term,” which is assumed unknown. Several LGPs in the literature set . However, if one instead assumes an improper prior on q then the posterior distribution of and q is GCM, as seen in Theorem 3.1 below. In Appendix C, we derive the posterior distribution up to a proportionality constant when these discrepancy parameters are set equal zero, which can not be simulated from directly.

Theorem 3.1.

Suppose are independently distributed according to (3). For , let the prior for be an inverse gamma distribution with shape and scale . Assume the model for y in (4), the improper prior , , and let the hyperparameters have a proper prior distribution where “c” denotes the set complement. Let with inverse gamma with shape and scale . Then

where is defined by (5), , the -dimensional unit-log partition function for -dimensional real-valued vector , and the -dimensional location and shape/scale parameter vectors are defined as follows: and when the data is normally distributed; and when the data is Poisson distributed; and and when the data is binomial distributed.

Proof: See Appendix B.

In Theorem 3.1 the presence of make components of and strictly positive when elements of the Poisson or binomial data vectors z are zero-valued. Hence, the presence of a cGCM (chosen to be close to a Gaussian) fine-scale term allows one to avoid the boundaries of the parameter space, leading to a well-defined GCM. Theorem 3.1 allows one to obtain replicates directly from the posterior distribution using a familiar projection expression, as seen below in Theorem 3.2.

Theorem 3.2.

Proof: See Appendix A

The vector -dimensional vector , where is easy to generate since it consists of independent DY random variables, is -dimensional, is -dimensional, and is -dimensional consisting of independent Gaussian random variables with mean zero and variance . Note that and are simply samples from the respective marginal prior distributions for and after marginalizing across and with location vector zero. Thus, it is straightforward to compute w when it is straightforward to sample from the marginal prior distributions for and . To do this one can, for example, sample from the joint distribution of and , where first one samples from then samples from . The projection can be computed on the order of operations with storage on the order of , when G is dense. When G is identity with , can be computed on the order of operations with storage on the order of . For the details on computing see Section 3.3.

The solution in the Gaussian special case is very similar to that in Murphy, (2007) and Zhang et al., (2023b). Namely, a different regression arises in (6) from Murphy, (2007) and Zhang et al., (2023b) due to our incorporation of a fine-scale variability term. Recall that the presence of fine-scale terms is particularly important for non-Gaussian data, since shape parameters and rate parameters in and are non-zero when count-valued observations are zero (i.e., the first stack components of and ) leading to a proper GCM. Thus, one exciting feature of Theorem 3.2 is that we obtain Gaussian like simulations of posterior replicates from the posterior distribution for non-Gaussian data. Equation (6) can also be seen as a parsimonious special case of the sampler in Bradley et al., (2023) with considerably fewer parameters.

Theorem 3.2 provides the motivation for including the discrepancy parameter q. Namely, this discrepancy parameter leads to easy-to-compute direct simulations from the posterior distribution. However, the incorporation of q leads to a model that is clearly overparameterized. Thus, a simple solution is to perform inference on using exact replicates from (6), which generates values from the marginal distribution . Then use the estimator of . This is the general strategy used in the CM literature (Bradley et al.,, 2020a) implemented using a type of block Gibbs sampler. Let represent the profile of y using the plug-in estimator , so that , where . Moreover, one might similarly use for inference on y, which would implicitly estimate both q and to be zero after marginalizing them from the posterior distribution.

The random vector has a very important interpretation. If one assumes is distributed according to the natural exponential family in (3), and is independently distributed according to the DY distribution in (16) then we have that the implied posterior distribution for in (17) is equal in distribution to in Theorem 3.2. Thus, represents a replicate from the posterior distribution from a saturated model. Recall in the goodness-of-fit literature that saturated models define a separate parameter for each datum and is meant to overfit the data, and then, measures of deviance from the saturated model are used to select more parsimonious models (e.g., see Bradley,, 2022, for a recent paper). This provides additional motivation for using the marginal distribution and (or ) to perform inference on y, which implies the use of the estimator of (and ). In the recent literature is referred to as “discrepancy error,” and hence we refer to as a discrepancy term (Bradley et al.,, 2020b, 2023).

3.2 Spatial Process Modeling with Exact Posterior Regression

The mixed effects model specification in Section 4.1 may be deceptively simple; however, we emphasize that several modern statistical models can use EPR including process models (e.g., spatial and spatio-temporal statistical models). See Hodges, (2013) for an thorough treatment of how spatial and temporal statistical models can be written as a richly parameterized mixed effects model. Although, of course, process models are different from mixed effects models, implementation of additive process models are similar to that of mixed effects models for a given collection of location/times. For example, consider locations , where is a generic spatial domain (e.g., a lattice or subset of ). We introduce process into our notation functionally so that, for example, is written as , where . Consider the following multivariate spatial statistical model,

where is a -dimensional vector of spatially varying covariates, is a -dimensional vector of spatial basis functions, be a random process, and be an unknown mean function. Suppose we are interested in estimation and prediction at the observed locations and an additional locations . Let . Then stacking over locations in yields,

| (9) |

where “” is the set union, -dimensional vector , and the matrix , where we note that X can be computed by pre-multiplying the covariates stacked over by a incidence matrix with -dimensional vector and denoting the indicator function. That is , where the matrix . In a similar manner let the matrix , where the matrix . Here, we let be the matrix square root of a parameterized covariance matrix (e.g., may be the Cholesky of a covariance matrix with -th element defined by the exponential covariogram). We let , , , and in (9) have the same specifications as in Section 3 with . Comparing our mixed effects model setup in (4) and the process model specification in (9) we see that process modeling can be implemented with EPR. That is, Theorem 3.1 (i.e., EPR) can be applied to the stacked expression in Equation (9). We illustrate this with spatial basis function expansions, weakly stationary spatial processes, and the conditional autoregressive model (Besag et al.,, 1991) in Section 4. To predict the process at both observed and prediction locations, posterior summaries of will be used

In practice, EPR may not always be scale-able for process modeling with large and , since it is not always straightforward to simulate directly from the prior distribution, nor is it always straightforward to compute G. In this article, we consider one example with a reduced rank assumption (Cressie and Johannesson,, 2008; Banerjee et al.,, 2008; Hughes and Haran,, 2013) by defining G to consist of spatially referenced basis functions (e.g., see Section 4.1). Although we consider to achieve scalability, there are options to consider when implementing EPR with . In particular, one might consider the “data subset model” from (Bradley,, 2021) to achieve scale-able inference, or sparse matrix Cholesky decompositions (e.g., see Datta et al.,, 2016).

3.3 Computational Considerations

For large the EPR formulation may not look practically feasible. However, standard block matrix inversion techniques can be used to reduce the order of operations to inverses of matrices, matrices, and diagonal matrices (Lu and Shiou,, 2002).

Theorem 3.3.

The following expression holds,

| (10) |

where , the matrix , the matrix

| (11) |

the matrix

the matrix , the matrix , the matrix , and the matrix .

Proof: See Appendix B.

Theorem 3.3 allows us to reduce the inverse of the matrix to the inverse of the matrix , and the matrix . When and are both “small,” these inverses are computationally efficient.

Simulation from the posterior using EPR does not necessarily require first computing a matrix of the form , storing this matrix, and then computing a -dimensional vector of the form . In fact this order of operations may require impractical storage, since the matrix may be high-dimensional. To avoid these issues one can instead compute/store the -dimensional vector of the form that avoids storage of high-dimensional matrices.

Theorem 3.4.

Let , , , , and . Then the following expression holds,

| (12) |

where the -dimensional vector , the -dimensional vector , the matrix , the matrix , the matrix , and the matrix

The matrix,

where the matrix , the matrix , the matrix , the matrix , the matrix , the matrix

, the matrix , and the matrix .

Proof: See the Appendix.

Careful examination of the order of operations show that Theorem (3.4) allows one to compute the vector by storing/computing the matrix X, the matrix G (when we set ), the matrix , the matrix , the matrix , and the matrix . These computations are straightforward when and are “small” or when is small and G is diagonal.

3.4 Implementation of Exact Posterior Regression

The following gives step-by-step instructions on obtaining efficient independent replicates directly from the posterior distribution of fixed effects and random effects using Theorem 3.1, which we refer to as EPR. We consider Gaussian data with unknown non-constant variance, Poisson data, binomial data, and Gaussian priors on and . Minor adjustments to these steps are needed for other settings (e.g., jointly modeling just two data types, etc.).

-

1.

Store/compute the matrix X, the matrix G, the matrix , the matrix , the matrix , and the matrix .

-

2.

Simulate w according to Theorem 3.2.

-

3.

Use the matrices computed in Step 1 and w in Step 2 to compute , , , and according to Theorem 3.4.

-

4.

Repeat Steps 23 times when G does not consist of unknown parameters. Repeat Steps 1 3 times when G is parameterized.

When using known basis function expansions to define G, repeated matrix operations that one might see in a Gibbs sampler are avoided, since matrix inversions are only required a single time in Step 1. Additionally, does not have to be as large as what one requires for an MCMC, since one does not require a burn-in period, thinning, or have concerns of mixing and positive autocorrelations in the MCMC.

|

|

|

|

|

|

|

|

|

4 Illustrations

We provide several illustrations in several standard spatial statistical model settings. In particular, we compare the use of spatial basis function expansions, weakly stationary spatial processes, and conditional autoregressive models, all of which are covered in standard text books on spatial and spatio-temporal modeling (e.g., see Cressie,, 1993; Rue and Held,, 2005; Cressie and Wikle,, 2011; Banerjee et al.,, 2015, among others).

4.1 Spatial Basis Function Expansions

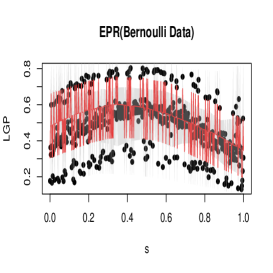

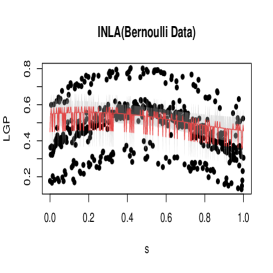

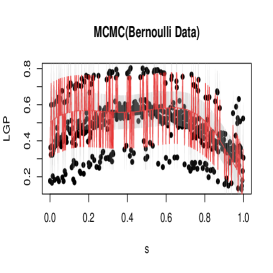

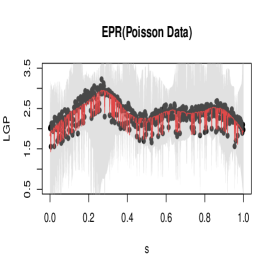

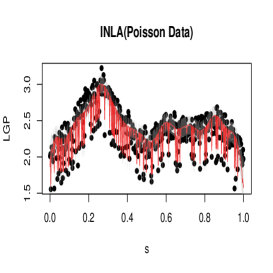

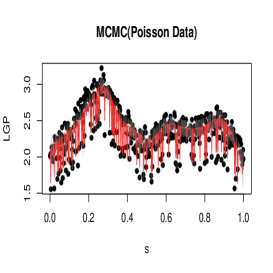

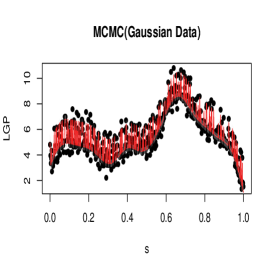

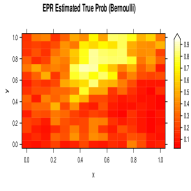

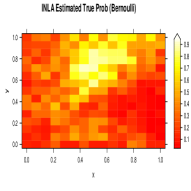

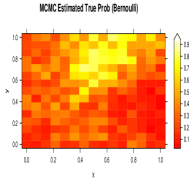

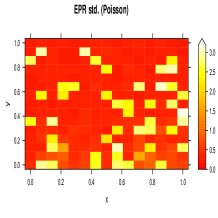

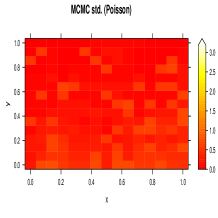

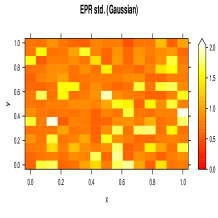

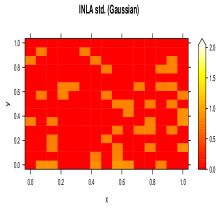

Spatial basis function expansions have become a standard in spatial statistics, with common classes of basis functions including Fourier basis functions, wavelet basis functions (Huang and Cressie,, 1999), radial basis functions (Cressie and Johannesson,, 2008), and splines (Wahba,, 1990), among others. In this section, we compare EPR, INLA, and MCMC implemented using the Pólya-Gamma technique from (Polson et al.,, 2013; D’Angelo and Canale,, 2022) using Gaussian radial basis function. EPR assumes an inverse gamma prior on all variance parameters with shape 1 and rate parameter given a gamma hyperprior with shape and rate set to 1. The range parameter is given a uniform zero to 0.5 prior. The default prior specifications are used for both INLA and spBayes. The Pólya-Gamma technique is a particularly efficient approach to fit latent Gaussian process models using MCMC, and is one of the more computationally competitive techniques in MCMC. In the Poisson MCMC implementation we make use of a new extremely efficient algorithm by D’Angelo and Canale, (2022). MCMC was implemented with 3,000 replicates with a burn-in of 1,000. We assume

| (13) |

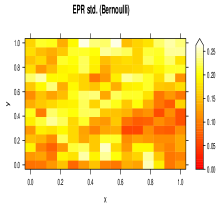

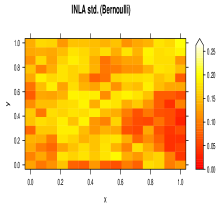

where are independently distributed according to a normal distribution with mean zero and variance 0.04, , we observe randomly selected locations, is an independent Bernoulli random variable with probability , is an independent Bernoulli random variable with probability , , are equally spaced across the spatial domain, and is the Euclidean distance. The default prior specifications are used for INLA. In Figure 1, we see that each method is fairly comparable in terms of predictive performance, expect in the case of Bernoulli data, where EPR is preferable for this particular dataset. Moreover, EPR tends to give larger measures of uncertainty than INLA and MCMC, both of which produce credible intervals that do not contain the true values of the latent process. The fact that the predictions are similar is notable since, INLA and MCMC are both approximate methods (MCMC is exact in the limit), whereas EPR is an exact method. Moreover, EPR (and INLA) does not require the additional overhead of MCMC diagnostics.

To assess the performance over multiple replicates, we use the central processing unit (CPU) time (seconds), the mean squared error (MSE) between the estimated regression coefficients and and true values, the mean squared prediction error (MSPE) between the latent process and predicted latent process (using ), and the continuous rank probability score (CRPS) (Gneiting and Katzfuss,, 2014) averaged over missing locations and scaled so that small values are preferable. The CRPS is useful since it is metric that evaluates the entire predictive distribution so that uncertainty in the predictions considered. In Table 1, we provide the average MSPE, MSE, CRPS, and CPU plus or minus two standard deviations over 50 independent replicates by method and data type.

| Method | Type | MSPE | MSE | CRPS | CPU | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| EPR | Logistic |

|

|

|

|

||||||||

| INLA | Logistic |

|

|

|

|

||||||||

| MCMC | Logistic |

|

|

|

|

||||||||

| EPR | Poisson |

|

|

|

|

||||||||

| INLA | Poisson |

|

|

|

|

||||||||

| MCMC | Poisson |

|

|

|

|

||||||||

| EPR | Normal |

|

|

|

|

||||||||

| INLA | Normal |

|

|

|

|

||||||||

| MCMC | Normal |

|

|

|

|

In Table 1, we see that the MSPE and CRPS are comparable in magnitude for EPR, INLA, and MCMC. In general, for EPR is preferable in terms of MSPE in the logistic regression setting, and INLA and MCMC produces smaller MSPE for Poisson and Normal regression. EPR and INLA have smaller CRPS (with CI that overlap) than MCMC in the logistic regression setting, and EPR is preferable in terms of CRPS than INLA and MCMC for Poisson and Normal data. EPR is consistently and considerably preferable in terms of MSE and CPU time in all settings. The performance in CPU time is especially notable, since INLA and MCMC are both approximate methods (MCMC is exact in the limit), whereas EPR is an exact MCMC free method. That is, EPR produces comparable predictions and superior regression estimates in a faster time than that of the state-of-the-art approximate Bayes and MCMC based methods in this study.

| Method | Type | MSPE | MSE | CRPS | CPU | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| EPR | Logistic |

|

|

|

|

||||||||

| INLA | Logistic |

|

|

|

|

||||||||

| MCMC | Logistic |

|

|

|

|

||||||||

| EPR | Poisson |

|

|

|

|

||||||||

| INLA | Poisson |

|

|

|

|

||||||||

| MCMC | Poisson |

|

|

|

|

||||||||

| EPR | Normal |

|

|

|

|

||||||||

| INLA | Normal |

|

|

|

|

||||||||

| MCMC | Normal |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4.2 Weakly Stationary Spatial Processes

A classical assumption for spatially referenced data is that the latent spatial process is weakly stationary. In particular, weakly stationary spatial processes have mean zero and the covariance of the process at any two locations is a positive definite function evaluated at the spatial lag, where this covariance function is referred to as a covariogram. In this section, we compare EPR, INLA, and MCMC implemented using the R package spBayes (Finley et al.,, 2012) using the exponential covariogram. The exponential covariogram is a well-known choice, but there are several other choices available (e.g, see Cressie,, 1993, among others). The simulated data are generated as follows,

|

|

|

|

|

|

|

|

|

| (14) |

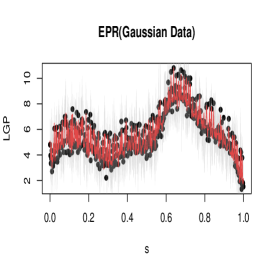

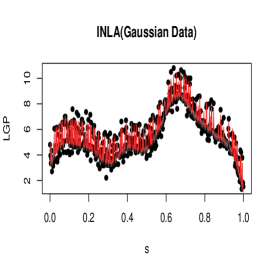

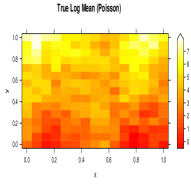

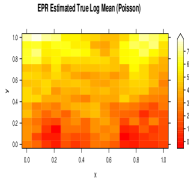

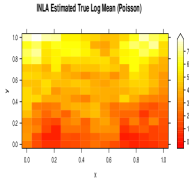

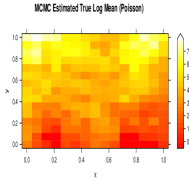

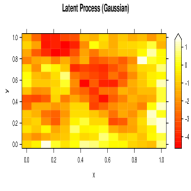

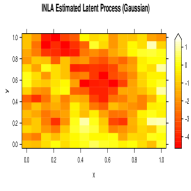

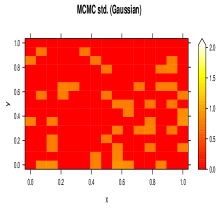

where are generated from a standard uniform distribution of a grid of the unit square, and is generated as a weakly stationary spatial process with exponential covariogram with range parameter 0.25, nugget variance 0.3, and variance 2 on a grid of the unit square. The slope and the intercept for the Poisson example was chosen so that the percent of zero count-valued observations to be small (roughly one percent) to avoid zero inflation. EPR assumes an inverse gamma prior on all variance parameters with shape 1 and rate parameter given a gamma hyperprior with shape and rate set to 1. The range parameter is given a uniform zero to 0.5 prior. The default prior specifications are used for both INLA and spBayes. In Figure 2, we provide plots of one simulated replicate and fitted means computed using EPR, INLA, and MCMC. The fitted posterior standard deviations for this example are provided in Figure 3. In general, we see that all methods perform similarly for this example, however, EPR tends to have larger posterior standard deviation. These patterns are consistent with the example in Section 4.1. The fact that the predictions are similar is again notable since, INLA and MCMC are both approximate methods (MCMC is exact in the limit), whereas EPR is an exact MCMC free method.

In Table 2, we provide the MSPE, MSE, CRPS, and CPU time across computational method and regression type. For logistic regression EPR, INLA, and MCMC perform similarly in terms of MSPE, CRPS, and MSE, since the confidence intervals (CI) over the 50 simulated replicates tend to overlap. In the Poisson data setting, we see similar values of MSPE, MSE, and CRPS, however, there are cases where one approach has a CI that does not overlap. In particular, when comparing CIs for Poisson data, implementation with MCMC leads to a significantly lower MSPE than EPR, implementation with INLA leads to a significantly lower MSE than EPR, and implementation with EPR leads to a significantly lower CRPS than MCMC. In all other cases the CIs overlap in the Poisson data setting. For all three types of spatial linear mixed models MCMC has a considerably larger CPU time than INLA and EPR, and INLA has moderately smaller CPU time than EPR. EPR performs marginally slower than it did in Section 4.1, since needs to be computed every step of the sampler, whereas the radial basis function in Section 4.1 only needed to computed once.

4.3 Intrinsic Conditional Autoregressive Model for American Community Survey Poverty Estimates

The U.S. Census Bureau’s ACS provides demographic statistics over several geographies and over 1-year and 5-year time periods (Torrieri,, 2007). As such, it has become a very useful tool for poverty estimation (Molina and Rao,, 2010). Small area estimation of poverty is a crucial and standard problem in both demography and official statistics (Rao,, 2003), since it is a key variable for determining economic disparities, public policy, and monitoring the financial circumstances at various levels of geography (e.g., see Theil,, 1996). Considering the wide-applicability of EPR, it is important to investigate its performance in standard settings such as poverty estimation. Consequently, in this section, we compare EPR to INLA and MCMC for poverty estimation over U.S. counties in Florida in 2019 using ACS 1-year period estimates.

Standard demographic related covariates are used; namely, ACS five year period estimates of the median age, the ratio of the population of males to females, and the population (on the log scale) of those who identify as white alone, black or African American alone, and Asian alone. We assume the population of those under the poverty status as binomial distributed with representing the -th county’s population. EPR assumes (chosen with cross validation), and the default prior specifications are used for INLA for the Besag, York, and Mollié (BYM, Besag et al.,, 1991) model are used. Let A be the row normalized first order binary adjacency matrix. When implementing EPR we define G to be the value such that , which is the Cholesky square root of the covariance matrix implied by the intrinsic conditional autoregressive model with precision (chosen using cross-validation). We fit EPR according to Section 3.4 with independent replicates from the posterior distribution and MCMC using the R package CARBayes with 20,000 replicates with a burn-in of 10,000 (Lee,, 2013).

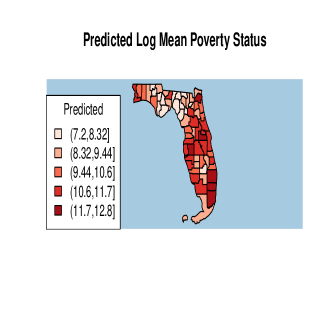

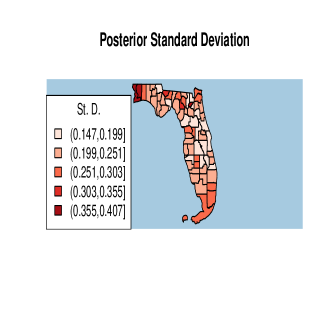

Plots of the predicted mean and standard deviation of versus the log-data using EPR are provided in Figure 4. In general, we see predictions that reflect the pattern of the data with spatial smoothing. Table 3 contains several metrics comparing the predictive performance of EPR, INLA, and MCMC. The leave-one-out cross validation error (Wahba,, 1990) is used to assess the predictive performance. Specifically, an observation is left out, and the model is used to predict this value. We compute the relative cross-validation (CV) error and the leave-one-out CRPS. The relative CV suggest that leave-one-out predictions are roughly within 15 of the hold-out proportion for EPR and INLA, and MCMC has a large relative CV at 70. These results suggest that EPR and INLA are comparable in terms of CV and CRPS. In general, INLA and EPR produce more similar estimates of the regression coefficients (MSE between these two estimated regression coefficients is 0.1921), and MCMC and INLA produce the most dissimilar regression estimates (MSE between these two estimated regression coefficients is 0.7286). Computationally, EPR is preferable in terms of CPU time followed closely by INLA. MCMC took considerably longer to implement the leave-one-out analysis.

| Method | CRPS | CPU | |

|---|---|---|---|

| EPR | 0.1529 | 0.1668 | 18.93 |

| INLA | 0.1589 | 0.1787 | 83.77 |

| MCMC | 0.6988 | 0.9858 | 449.65 |

5 Discussion

|

|

|

This paper describes how to efficiently sample independent replicates directly from the posterior distribution for data modeled using a broad class of spatial latent Gaussian process models. This development required the introduction of the GCM distribution and the conditional GCM distribution. The use of the GCM allows one to consider any class of CM’s for their prior distributions on fixed and random effects. Our development explicitly addresses hyperparameters through marginalization. We make use of the GCM in a LGP context to produce what we call exact posterior regression, which represents an efficiently generated independent sample from the posterior distribution. We show that the posterior distribution for fixed and random effects in this LGP are GCM, which we can directly sample from. Furthermore, we use matrix algebra techniques to aid in the computation of EPR.

The results in this paper solve an important problem for Bayesian analysis that is regularly overlooked (i.e., obtaining efficient independent replicates directly from the posterior distribution in Bayesian spatial LGPs). One might also consider empirical Bayesian variations of EPR as our solution also allows one to sample independent replicates directly from the posterior predictive distribution when using point mass specification of (i.e.,point mass on an estimate), which avoids MCMC in empirical Bayesian settings as well. Specifically, Theorems 3.1 3.3 can be used with a plug-in estimator of . However, plug-in estimators have unchecked sampling variability (provided that the plug-in estimator is a non-constant function of the data), and the development of the GCM provides a straightforward solution that accounts for all sources of variability.

While we feel that the results in this manuscript represent a significant advancement in Bayesian modeling of spatial LGPs, it is important to state that MCMC and INLA will always be a standard tool. This is because the spatial LGP specification we consider does not represent the wide variety of LGPs used in the literature (e.g., allowing for mixture components, inference on hyperparameters, data models outside the class of distributions we consider, etc.). Moreover, inference using EPR is limited to summaries of and , since is marginalized. However, we hope the theory developed in this article leads to further theoretical developments that allows one to sample independent replicates from the posterior distribution in other settings.

Acknowledgments

Jonathan R. Bradley’s research was partially supported by the U.S. National Science Foundation (NSF) under NSF grant SES-1853099. The authors are deeply appreciative to several helpful discussions from Drs. Scott H. Holan and Christopher K. Wikle at the University of Missouri.

Appendix A: Review of the Conjugate Multivariate Distribution

In this section, we give the reader a review of the CM distribution from Bradley et al., (2020a). Suppose the observed data is distributed according to the natural exponential family (Diaconis and Ylvisaker,, 1979; Lehmann and Casella,, 1998). That is, suppose that the probability density function/probability mass function (pdf/pmf) of the observed datum is given by,

| (15) |

where denotes a generic pdf/pmf, is the support of , is the support of the unknown parameter , is a possibly known real-value, both and are known real-valued functions, and is used to index the specific member of the exponential family (e.g., Gaussian, Poisson, binomial, etc.). The function is often called the log partition function (Lehmann and Casella,, 1998). We focus on Gaussian responses, which sets , , , and with ; Poisson responses, which sets , , , and ; and binomial responses, which sets , , , and with a strictly positive integer.

It follows from Diaconis and Ylvisaker, (1979) that the conjugate prior distribution for (when it exists) is given by,

| (16) |

where is a normalizing constant. Let denote a shorthand for the pdf in (16). Here “DY” stands for “Diaconis-Ylvisaker.” Of course, there are several special cases of the DY distribution other than the Gaussian (), log-gamma (), and logit-beta () distributions; however, we focus our attention on these standard conjugate cases.

By conjugate we mean that the posterior distribution is from the same family of distributions as the prior distribution. In the case of (15) and (16), we obtain conjugacy as

| (17) |

Bradley et al., (2020a) derived a multivariate version of . Define the -dimensional random vector y using the following transformation:

| (18) |

where is an -dimensional real-valued vector called the “location vector,” V is an real-valued invertible “covariance parameter matrix,” the elements of the -dimensional random vector w are mutually independent, and the -th element of w is with and shape/scale (depending on ) , respectively. Straightforward change-of-variables of the transformation in (18) yields the following expression for the pdf of y:

| (19) |

where the -th element of contains evaluated at the -th element of the -dimensional vector , “det” denotes the determinant function, , and . The density in (19) is referred to as the CM distribution, and we use the shorthand .

Appendix B : Proofs

Proof Theorem 2.1

We first derive . Upon multiplying independent DY random variables we see that the distribution of is,

The inverse transform is , and the corresponding Jacobian is . By standard change-of-variables (e.g., see Casella and Berger,, 2002), we have that,

| (20) |

From our independence assumption,

which upon substituting (20) completes the result.

Proof Theorem 2.2

From Theorem 2.1, the conditional distribution is given by

Integrating across completes the result.

Proof Theorem 3.1

Our strategy is to show that is the GCM stated in Theorem 3.1. The data model can be written as:

where for the Gaussian setting, and in the binomial and Poisson setting. Recall , and when z is Gaussian distributed, when z is Poisson or binomial distributed, when z is Gaussian distributed, and when z is Poisson or binomial distributed. The density is proportional to the product

where recall . Now,

| (25) | |||

| (30) |

with and known, when z is Gaussian distributed, when z is Poisson or binomial distributed, when z is Gaussian or Poisson distributed, and when z is binomial distributed. Let for -dimensional real-valued vector . The product,

| (35) | |||

| (40) |

where when z is Gaussian distributed, when z is Poisson or binomial distributed, when z is Gaussian distributed, when z is Poisson distributed, and when z is binomial distributed.

Notice that the implied shape/scale parameters and are not on the boundary of the parameter space (when zero counts are present), which is a motivation for including in the LGP. Multiplying by , and stacking vector and matrices leads to

| (49) | |||

| (58) |

Substituting and integrating with respect to leads to

| (63) | |||

which completes the result.

Proof Theorem 3.2

Equations (6) and 7) from the main text follows from (1) from the main text, Theorem 3.1, and that

Let consist of independent DY random variables with respective shape and scale parameters in and . Let

where recall is a block diagonal matrix with first block diagonal equaling the identity matrix. It follows from Theorem 2.1 that w has the stated GCM distribution in Theorem 3.2. Then

From Theorem 2.1 it follows that is the GCM stated in Theorem 3.2. Equation (8) in the main text follows from the fact that so that

Proof Theorem 3.3

From (Lu and Shiou,, 2002) the inverse of a 22 block matrix is,

for generic real-valued matrix , matrix , matrix , and matrix . Equation (13) of the main text follows from applying this known inverse of 22 block matrices(Lu and Shiou,, 2002) to,

Similarly, Equation (14) from the main text follows from applying the same inverse identity to

Proof Theorem 3.4

(Lu and Shiou,, 2002) gave two identities for the inverse of a 22 block matrix,

and

for generic real-valued matrix , matrix , matrix , and matrix . Apply this second identity to,

to produce

Since, we have that , Equation (12) from the main text follows immediately. Apply the first block inverse identity to to obtain , , , and . Apply the Sherman-Morrison Woodbury identity (Cressie and Johannesson,, 2008) to obtain .

Appendix C: Enforcing Sparse Discrepancy Parameters Instead of Marginalizing Discrepancy Parameters

Theorem 3.1 shows that posterior inference on can be interpreted as a type of regression when using for inference, which marginalizes across q. Another choice is to enforce sparsity on the discrepancy parameter (i.e., setting q equal to zero) before marginalizing it out instead of after, which we do in this article. That is, one might instead use the informative point mass prior of leading one to use for inference (McCulloch et al.,, 2008).

Result: Suppose is independently distributed according to either (3) of the main text with . Let y be defined as in Theorem 3.1 of the main text with the added assumption that . Then is cGCM, with , and , , H, D, and defined in Theorem 3.1.

Proof: We have from Theorem 3.1,

| (64) |

and when integrating across we obtain the cGCM in the statement above.

The result above shows that is a conditional GCM, however, it is currently unknown how to simulate from the conditional GCM in many settings.

References

- Banerjee et al., (2015) Banerjee, S., Carlin, B. P., and Gelfand, A. E. (2015). Hierarchical Modeling and Analysis for Spatial Data. London, UK: Chapman and Hall.

- Banerjee et al., (2008) Banerjee, S., Gelfand, A. E., Finley, A. O., and Sang, H. (2008). “Gaussian predictive process models for large spatial data sets.” Journal of the Royal Statistical Society, Series B, 70, 825–848.

- Besag et al., (1991) Besag, J. E., York, J. C., and Molliè, A. (1991). “Bayesian image restoration, with two applications in spatial statistics (with discussion).” Annals of the Institute of Statistical Mathematics, 43, 1–59.

- Bradley et al., (2018) Bradley, J., Holan, S., and Wikle, C. (2018). “Computationally Efficient Distribution Theory for Bayesian Inference of High-Dimensional Dependent Count-Valued Data.” Bayesian Analysis, 13, 253–302.

- Bradley, (2021) Bradley, J. R. (2021). “An Approach to Incorporate Subsampling Into a Generic Bayesian Hierarchical Model.” Journal of Computational and Graphical Statistics, 30, 4, 889–905.

- Bradley, (2022) — (2022). “Joint Bayesian Analysis of Multiple Response-Types Using the Hierarchical Generalized Transformation Model.” Bayesian Analysis, 17, 127–164.

- Bradley et al., (2020a) Bradley, J. R., Holan, S. H., and Wikle, C. K. (2020a). “Bayesian Hierarchical Models with Conjugate Full-Conditional Distributions for Dependent Data from the Natural Exponential Family.” Journal of the American Statistical Association, 115, 2037–2052.

- Bradley et al., (2019) Bradley, J. R., Wikle, C. K., and Holan, S. H. (2019). “Spatio-temporal models for big multinomial data using the conditional multivariate logit-beta distribution.” Journal of Time Series Analysis, 40, 3, 363–382.

- Bradley et al., (2020b) — (2020b). “Hierarchical Models for Spatial Data with Errors that are Correlated with the Latent Process.” Statistica Sinica, 30, 80–109.

- Bradley et al., (2023) Bradley, J. R., Zhou, S., and Liu, X. (2023). “Deep hierarchical generalized transformation models for spatio-temporal data with discrepancy errors.” Spatial Statistics, 100749.

- Carpenter et al., (2017) Carpenter, B., Gelman, A., Hoffman, M. D., Lee, D., Goodrich, B., Betancourt, M., Brubaker, M., Guo, J., Li, P., and Riddell, A. (2017). “Stan: A probabilistic programming language.” Journal of Statistical Software, 76, 1, 1–32.

- Casella and Berger, (2002) Casella, G. and Berger, R. (2002). Statistical Inference. Pacific Grove, CA: Duxbury.

- Chen and Ibrahim, (2003) Chen, M. H. and Ibrahim, J. G. (2003). “Conjugate priors for generalized linear models.” Statistica Sinica, 13, 2, 461–476.

- Cowles and Carlin, (1996) Cowles, M. K. and Carlin, B. P. (1996). “Markov chain Monte Carlo convergence diagnostics: a comparative review.” Journal of the American Statistical Association, 91, 434, 883–904.

- Cressie, (1993) Cressie, N. (1993). Statistics for Spatial Data, rev. edn. New York, NY: Wiley.

- Cressie and Johannesson, (2008) Cressie, N. and Johannesson, G. (2008). “Fixed rank kriging for very large spatial data sets.” Journal of the Royal Statistical Society, Series B, 70, 209–226.

- Cressie and Wikle, (2011) Cressie, N. and Wikle, C. K. (2011). Statistics for Spatio-Temporal Data. Hoboken, NJ: Wiley.

- D’Angelo and Canale, (2022) D’Angelo, L. and Canale, A. (2022). “Efficient posterior sampling for Bayesian Poisson regression.” Journal of Computational and Graphical Statistics, 1–10.

- Datta et al., (2016) Datta, A., Banerjee, S., Finley, A. O., and Gelfand, A. E. (2016). “Hierarchical nearest-neighbor Gaussian process models for large geostatistical datasets.” Journal of the American Statistical Association, 111, 514, 800–812.

- Diaconis and Ylvisaker, (1979) Diaconis, P. and Ylvisaker, D. (1979). “Conjugate priors for exponential families.” The Annals of Statistics, 17, 269–281.

- Finley et al., (2012) Finley, A. O., Banerjee, S., and Carlin, B. (2012). “Package ‘spBayes’.” http://cran.r-project.org/web/packages/spBayes/spBayes.pdf. Retrieved January, 2013.

- Gao and Bradley, (2019) Gao, H. and Bradley, J. R. (2019). “Bayesian analysis of areal data with unknown adjacencies using the stochastic edge mixed effects model.” Spatial Statistics, 31, 100357.

- Gelfand and Schliep, (2016) Gelfand, A. E. and Schliep, E. M. (2016). “Spatial statistics and Gaussian processes: a beautiful marriage.” Spatial Statistics, 18, 86–104.

- Gelman et al., (2013) Gelman, A., Carlin, J. B., Stern, H. S., Dunson, D. B., Vehtari, A., and Rubin, D. B. (2013). Bayesian Data Analysis, 3rd edn.. Boca Raton, FL: Chapman and Hall/CRC.

- Gelman and Rubin, (1992) Gelman, A. and Rubin, D. (1992). “Inference from iterative simulation using multiple sequences.” Statistical Science, 7, 473–511.

- Gneiting and Katzfuss, (2014) Gneiting, T. and Katzfuss, M. (2014). “Probabilistic forecasting.” Annual Review of Statistics and Its Application, 1, 125–151.

- H.-C.Yang et al., (2019) H.-C.Yang, Hu, G., and Chen, M.-H. (2019). “Bayesian Variable Selection for Pareto Regression Models with Latent Multivariate Log Gamma Process with Applications to Earthquake Magnitudes.” Geosciences, 9, 4, 169.

- Hodges, (2013) Hodges, J. S. (2013). Richly parameterized linear models: additive, time series, and spatial models using random effects. CRC Press.

- Hu and Bradley, (2018) Hu, G. and Bradley, J. R. (2018). “A Bayesian spatial–temporal model with latent multivariate log-gamma random effects with application to earthquake magnitudes.” Stat, 7, 1, e179.

- Huang and Cressie, (1999) Huang, H. and Cressie, N. (1999). “Empirical Bayesian Spatial Prediction Using Wavelets.” Bayesian Inference in Wavelet Based Models, eds P. Mueller and B. Vidakovich., , 141.

- Hughes and Haran, (2013) Hughes, J. and Haran, M. (2013). “Dimension reduction and alleviation of confounding for spatial generalized linear mixed model.” Journal of the Royal Statistical Society, Series B, 75, 139–159.

- Kang et al., (2023) Kang, H. B., Jung, Y. J., and Park, J. (2023). “Fast Bayesian Functional Regression for Non-Gaussian Spatial Data.” Bayesian Analysis, 1, 1, 1–32.

- Konomi et al., (2023) Konomi, B. A., Kang, E. L., Almomani, A., and Hobbs, J. (2023). “Bayesian Latent Variable Co-kriging Model in Remote Sensing for Quality Flagged Observations.” Journal of Agricultural, Biological and Environmental Statistics, 1–19.

- Lee, (2013) Lee, D. (2013). “CARBayes: an R package for Bayesian spatial modeling with conditional autoregressive priors.” Journal of Statistical Software, 55, 13, 1–24.

- Lehmann and Casella, (1998) Lehmann, E. and Casella, G. (1998). Theory of Point Estimation. 2nd ed. New York, NY: Springer.

- Lindgren et al., (2022) Lindgren, F., Bolin, D., and Rue, H. (2022). “The SPDE approach for Gaussian and non-Gaussian fields: 10 years and still running.” Spatial Statistics, 50, 100599.

- Lu and Shiou, (2002) Lu, T.-T. and Shiou, S.-H. (2002). “Inverses of 2 2 block matrices.” Computers & Mathematics with Applications, 43, 1-2, 119–129.

- McCullagh and Nelder, (1989) McCullagh, P. and Nelder, J. (1989). Generalized Linear Models. London, UK: Chapman and Hall.

- McCulloch et al., (2008) McCulloch, C. E., Searle, S. R., and Neuhaus, J. M. (2008). Generalized, Linear, and Mixed Models. NJ: Wiley.

- Molina and Rao, (2010) Molina, I. and Rao, J. (2010). “Small area estimation of poverty indicators.” Canadian Journal of statistics, 38, 3, 369–385.

- Murphy, (2007) Murphy, K. P. (2007). “Conjugate Bayesian analysis of the Gaussian distribution.” https://www.cs.ubc.ca/ murphyk/Papers/bayesGauss.pdf.

- Neal, (2011) Neal, R. M. (2011). “MCMC using Hamiltonian dynamics.” Handbook of Markov chain Monte Carlo, 2, 11, 2.

- Novikov et al., (2005) Novikov, I. Y., Protasov, V. Y., and Skopina, M. A. (2005). Wavelet Theory. US: American Mathematical Society.

- Parker et al., (2020) Parker, P. A., Holan, S. H., and Janicki, R. (2020). “Conjugate Bayesian unit-level modelling of count data under informative sampling designs.” Stat, 9, 1, e267.

- Parker et al., (2021) Parker, P. A., Holan, S. H., and Wills, S. A. (2021). “A general Bayesian model for heteroskedastic data with fully conjugate full-conditional distributions.” Journal of Statistical Computation and Simulation, 1–21.

- Polson et al., (2013) Polson, N. G., Scott, J. G., and Windle, J. (2013). “Bayesian inference for logistic models using Pólya-Gamma latent variables.” Journal of the American Statistical Association, 108, 1339–1349.

- Porter et al., (2023) Porter, E. M., Franck, C. T., and Ferreira, M. A. (2023). “Objective Bayesian Model Selection for Spatial Hierarchical Models with Intrinsic Conditional Autoregressive Priors.” Bayesian Analysis, 1, 1, 1–27.

- Rao, (2003) Rao, J. K. (2003). Small area estimation. John Wiley & Sons.

- Robert and Casella, (2011) Robert, C. and Casella, G. (2011). “A short history of MCMC: Subjective recollections from incomplete data.” Handbook of markov chain monte carlo, 49.

- Robert and Casella, (2004) Robert, C. P. and Casella, G. (2004). Monte Carlo Statistical Methods. New York, NY: Springer.

- Roberts and Rosenthal, (2009) Roberts, G. O. and Rosenthal, J. S. (2009). “Examples of adaptive MCMC.” Journal of computational and graphical statistics, 18, 2, 349–367.

- Rue and Held, (2005) Rue, H. and Held, L. (2005). Gaussian Markov random fields: theory and applications. CRC press.

- Rue et al., (2009) Rue, H., Martino, S., and Chopin, N. (2009). “Approximate Bayesian inference for latent Gaussian models using integrated nested Laplace approximations.” Journal of the Royal Statistical Society, Series B, 71, 319–392.

- Shirota et al., (2023) Shirota, S., Finley, A. O., Cook, B. D., and Banerjee, S. (2023). “Conjugate sparse plus low rank models for efficient Bayesian interpolation of large spatial data.” Environmetrics, 34, 1, e2748.

- Theil, (1996) Theil, H. (1996). Studies in global econometrics. Springer Science & Business Media.

- Torrieri, (2007) Torrieri, N. (2007). “America is changing, and so is the census: The American Community Survey.” American Statistician, 61, 16–21.

- van Erven and Szabó, (2021) van Erven, T. and Szabó, B. (2021). “Fast exact Bayesian inference for sparse signals in the normal sequence model.” Bayesian Analysis, 16, 3, 933–960.

- Vats et al., (2019) Vats, D., Flegal, J. M., and Jones, G. L. (2019). “Multivariate output analysis for Markov chain Monte Carlo.” Biometrika, 106, 2, 321–337.

- Vranckx et al., (2023) Vranckx, M., Faes, C., Molenberghs, G., Hens, N., Beutels, P., Van Damme, P., Aerts, J., Petrof, O., Pepermans, K., and Neyens, T. (2023). “A spatial model to jointly analyze self-reported survey data of COVID-19 symptoms and official COVID-19 incidence data.” Biometrical Journal, 65, 1, 2100186.

- Wahba, (1990) Wahba, G. (1990). Spline Models for Observational Data. Philadelphia, PA: Society for Industrial and Applied Mathematics.

- Wainwright and Jordan, (2008) Wainwright, M. J. and Jordan, M. I. (2008). Graphical models, exponential families, and variational inference. Now Publishers Inc.

- Xu et al., (2019) Xu, Z., Bradley, J. R., and Sinha, D. (2019). “Latent multivariate log-gamma models for high-dimensional multi-type responses with application to daily fine particulate matter and mortality counts.” arXiv preprint arXiv:1909.02528.

- Zhang et al., (2023a) Zhang, B., Sang, H., Luo, Z. T., and Huang, H. (2023a). “Bayesian clustering of spatial functional data with application to a human mobility study during COVID-19.” The Annals of Applied Statistics, 17, 1, 583–605.

- Zhang et al., (2021) Zhang, L., Banerjee, S., and Finley, A. O. (2021). “High-dimensional multivariate geostatistics: A Bayesian matrix-normal approach.” Environmetrics, 32, 4, e2675.

- Zhang et al., (2023b) Zhang, L., Tang, W., and Banerjee, S. (2023b). “Exact Bayesian Geostatistics Using Predictive Stacking.” arXiv preprint arXiv:2304.12414.