Optimizing Randomized and Deterministic Saturation Designs under Interference

Abstract

Randomized saturation designs are a family of designs which assign a possibly different treatment proportion to each cluster of a population at random. As a result, they generalize the well-known (stratified) completely randomized designs and the cluster-based randomized designs, which are included as special cases. We show that, under the stable unit treatment value assumption, either the cluster-based or the stratified completely randomized design are in fact optimal for the bias and variance of the difference-in-means estimator among randomized saturation designs. However, this is no longer the case when interference is present. We provide the closed form of the bias and variance of the difference-in-means estimator under a linear model of interference and investigate the optimization of each of these objectives. In addition to the randomized saturation designs, we propose a deterministic saturation design, where the treatment proportion for clusters are fixed, rather than randomized, in order to further improve the estimator under correct model specification. Through simulations, we illustrate the merits of optimizing randomized saturation designs to the graph and potential outcome structure, as well as showcasing the additional improvements yielded by well-chosen deterministic saturation designs.

Keywords: Violations of SUTVA, Causal Inference, Potential Outcomes, Saturation Designs

1 Introduction

In many randomized experiments, the population of interest can be organized into groups (clusters) of units. In certain instances, the clustering of units is artificial. For instance, units are grouped according to their distance to the discontinuity point in a regression discontinuity design (Owen and Varian, 2020), or units can be grouped into subsets of data from the perspective of data fusion (Rosenman and Owen, 2021). A more common incentive for exploring the cluster structure of population is to discover interference between units (Toulis and Kao, 2013; Tchetgen and VanderWeele, 2012). As a violation of the stable unit treatment value assumption (SUTVA) (Imbens and Rubin, 2015), units within the same cluster are often assumed to have interference, that is the outcome of one unit can be affected by the treatment status of its group-mates. In certain cases, interference can also occur across clusters. Examples of such interference clusters include a class of students in educational studies (Rosenbaum, 2007), a group of people with a financial relationship (Banerjee et al., 2013), a social network group (Phan and Airoldi, 2015), or a block of crop field (Zaller and Köpke, 2004). In a two-sided market, interference can occur across both customer-side and listing-side (Johari et al., 2020), which provide a natural clustering. When the clusters representing interference are not immediately clear, Ugander et al. (2013) explores algorithmic clustering solutions.

Given a clustered population, three group-level experimental designs are commonly used: the stratified completely randomized design, the cluster-based randomized design and the randomized saturation design. The stratified—sometimes referred to as ‘blocked’—design extends the standard completely randomized design (Rubin, 1974) to groups of units such that in each cluster, an equal proportion of units is treated (Owen and Varian, 2020; Rosenman and Owen, 2021). In cluster-based designs, all units within the same cluster receive treatment or control (Eckles et al., 2017). When interference is present, compared to stratified design, it is generally believed that a cluster-based randomized design will be less biased (Eckles et al., 2017; Ugander and Backstrom, 2013), but will have higher variance than a completely-randomized design that assigns the same proportion of units to treatment. The complexity of finding balanced partitioning of a large set of experimental units (Andreev and Racke, 2006) is another aspect to take into consideration when choosing between both of these standard designs. An optimal cluster-based randomized design is tractable under monotonicity (Pouget-Abadie et al., 2018).

The randomized saturation design, proposed in Hudgens and Halloran (2008) as a compromise between the two previous designs, is a two-step procedure, where clusters are first assigned with treatment proportions, and then units within each group are assigned to treatment and control at random according to the assigned treatment proportion. Randomized saturation designs are often used in the context of interference because they allow the experimenter to infer a unit’s reaction to varying levels of treatment (Banerjee et al., 2012; Sinclair et al., 2012; Crépon et al., 2013). This is especially appropriate if we are willing to make an anonymous interference assumption (Manski, 2013) or an assumption of no peer-effect-heterogeneity (Athey et al., 2015). For an excellent reference on randomized saturation designs, we refer the reader to Baird et al. (2016).

Randomized saturation designs offer an interesting interpolation between stratified and cluster-based randomized designs. Both can be conceptualized as a randomized saturation design: the stratified completely randomized design corresponds to a randomized saturation design with identical treatment proportions across all clusters; the cluster-based randomized design corresponds to a randomized saturation design with full treatment or full control proportions.

Randomized saturation designs are an example of model-assisted designs (Basse and Airoldi, 2018). Indeed, the distribution of the treatment proportions can be chosen to optimize a particular objective under a set of model assumptions, without sacrificing the validity of the estimation procedure if our model of potential outcomes is misspecified. With high confidence in our modelling assumptions, we can further optimize the assignment of each treatment proportions within each cluster of experimental units. We refer to these designs as deterministic saturation designs and show that they yield additional improvements over their randomized saturation design counterparts under certain assumptions. Unlike general randomized saturation designs, which randomly assign treatment proportions to clusters in a first stage, deterministic saturation designs predetermine the treatment proportion for each cluster and forgo the initial randomization. Both of them randomly assign treatment within each cluster in the second stage; “deterministic” only refers to the first stage.

Our contribution

We conduct a complete analysis of the bias and variance of the difference-in-means estimator under any randomized saturation design. Furthermore, we provide general guidance for finding the optimal randomized saturation design in terms of bias, variance, or mean-squared error, particularly when a realistic linear interference model holds.

We start by assuming the stable unit treatment value assumption (SUTVA), where interference is absent. We show that, under SUTVA, all randomized saturation designs are unbiased and at least one of the stratified design and the cluster-based design has the minimum variance for the difference-in-means estimator among all randomized saturation designs.

When interference is present, we assume a linear interference model where interference occurs both within and across clusters and units can receive heterogeneous levels of interference depending on their local neighbors. This assumption of interference is more realistic than that of the previous study (Baird et al., 2016), which assumed isolated clusters and homogeneous interference. We show that the closed form of the bias, the variance, and the mean-squared error of the difference-in-means estimator can be optimized analytically within a symmetric proportion family of randomized saturation design. Under this interference structure, we find that the optimal randomized saturation design is not necessarily the cluster-based design or the stratified design, unlike in the SUTVA case.

In addition, we propose the optimal deterministic saturation design, which can further reduce the variance/mean-squared error of the difference-in-means estimator when interference is present. Finding the optimal deterministic saturation design requires more knowledge of certain population statistics than finding the optimal randomized saturation design does. Using an optimal deterministic saturation design takes advantage of additional information when available to better design the experiment.

The manuscript is organized as follows. In Section 2, we formally introduce randomized saturation designs and explore the bias and variance of the standard difference-in-means estimator under the stable unit treatment value (SUTVA) assumption, as well as under a heterogeneous linear model of interference. These results can be extended to random graph model setting and other model-assisted estimator as discussed in Section 2.5. In Section 3, we introduce and define optimal deterministic saturation designs and show that they can yield additional improvements over randomized saturation designs, even optimal randomized ones. The benefits from optimizing the randomized saturation design, as well as the additional improvement obtained from optimizing the deterministic saturation design, is demonstrated in Section 4 with simulations. We conclude this paper with practical considerations in Section 5.

2 Randomized Saturation Designs

In this section, we formally define randomized saturation designs, and study the bias and variance of the standard difference-in-means estimator under various potential outcome models.

2.1 Definitions

A randomized saturation design is any two-stage design that first assigns clusters of experimental units at random to treatment proportions, and then assigns the units within each cluster to treatment and control, respecting the assigned treatment proportion for each cluster. Let be the number of experimental units, let be their outcome vector, and let be the assignment vector stating whether each unit is in treatment () or control (). Let be the number of clusters of the experimental units; they partition the experimental cohort such that each unit belongs to exactly one cluster . There are many possible kinds of randomization saturation designs. We list two below, and show that they are equivalent when the number of clusters is large.

Definition 1.

The independently-sampled randomized saturation design is a two-stage design defined by a probability distribution on and the following procedure: for each cluster , sample and assign randomly-chosen units of cluster to treatment and the remainder units of cluster to control.

The independently-sampled randomized saturation design is entirely characterized by its distribution . The total number of treated units is a random variable, given by . Assuming the size of each cluster is large (), the expected number of treated units over the sampling of is the expectation of times the total number of experimental units : .

Definition 2.

The permutation-based randomized saturation design is a two-stage randomized design defined by a fixed vector of length and the following procedure: sample a random permutation of , letting be the corresponding permutation matrix of . For each block , assign randomly-chosen units of to treatment, and the remainder units of to control, where is the coordinate of the permuted vector .

The permutation-based design is entirely characterized by its vector . The total number of treated units is fixed when the clusters are of equal size: . For this reason, we will always refer to the second implementation of randomized saturation designs, unless stated otherwise. To simplify the analysis, we assume the clusters are of equal size throughout this paper so that the total number of treated units is fixed. This is the case when clusters of equal size are drawn from a super-population. A similar equal-sized cluster assumption was made in Baird et al. (2016). For further ease of exposition, we will assume that the number of units in each cluster is large enough to ignore the flooring function.

The treatment-proportions vector can be chosen explicitly by the experimenter or be the result of an optimization program; it can also be randomly sampled from a probability distribution. In the latter case, the independently-sampled and permutation-based randomized saturation designs are equivalent when the number of clusters is large. Assuming that the treatment proportions vector is sampled from a probability distribution , the moment of the number of units assigned to treatment in each the permutation-based design is equal asymptotically to its moment under the independently-sampled design by the law of large numbers: , where is the moment of the coordinate of , and is shown to be equivalent to the moment of the coordinate of sampled according to , , when the number of clusters is large.

Finally, both cluster-based randomized designs and stratified completely randomized designs are in fact instantiations of randomized saturation designs. The cluster-based randomized design is an example of a randomized saturation design where , assigning either all units in a cluster to treatment or to control, whereas a stratified completely randomized assignment, which assigns the same proportion of units to treatment in each cluster, corresponds to a randomized saturation design with constant vector .

In the subsequent sections, we adopt the following notational convention. The plain letter with subscript, , stands for the potential outcome of unit under treatment assignment . The plain letter with superscript, , is the cluster-level potential outcome for clusters such that . The bolded letters, and , denote the vector of all unit-level potential outcomes and the sub-vector restricted to cluster , such that and . We define to be the vector of all cluster-level potential outcomes under treatment assignment . Finally, for any vector , denotes its average, and for any two vectors , we define the sample covariance operator such that

| (1) |

We adopt the convention for the sample variance of vector . For example, is the sample within-cluster covariance between the potential outcomes with every unit treated and the potential outcomes with every unit untreated; is the sample variance of cluster-level potential outcomes under treatment .

2.2 Bias and variance under SUTVA

A starting point to understanding any class of designs is to consider the resulting bias and variance of the commonly used difference-in-means estimator under the Stable Unit Treatment Value Assumption (SUTVA) (Imbens and Rubin, 2015). Let denote the difference-in-means estimator, defined by

where is the total number of treated units and is the total number of control units.

We have defined the difference-in-means estimator under the assumption of equal cluster size. Without assuming equal cluster size, Hudgens and Halloran (2008) defined the difference-in-means estimator at the cluster-level such that

where , are the sample mean estimators for cluster . This definition of is identical to ours under a equal cluster size assumption, which we will make throughout the rest of this paper.

By the law of iterated expectations, the shorthand denotes , i.e. the expectation taken with respect to the permutation of the treatment proportions assignment to clusters, and with respect to the assignment of units to treatment and control , conditioned on the assignment of . We first show that, when SUTVA holds, the difference-in-means estimator is unbiased under a randomized saturation design for the total treatment effect .

Proposition 3.

IF SUTVA holds,

where is the cluster-level outcome of cluster .

A proof is included in the supplementary materials. From Proposition 3, the difference-in-means estimator is not guaranteed to be unbiased if we condition on a specific assignment of clusters to treatment proportions. Only by randomizing over the assignment of treatment proportion do we guarantee unbiasedness.

We can also give a concise formula of the variance of the difference-in-means estimator under SUTVA and a randomized saturation design.

Proposition 4.

When SUTVA holds, the variance of the difference-in-means estimator under a randomized saturation design is

| (2) |

where is a weighted average of the potential outcomes and , denote the vector of ’s in cluster and the vector of all cluster-level ’s correspondingly.

A proof can be found in the supplementary materials. The important takeaway from Equation 2 is that the variance of the difference-in-means estimator for a randomized saturation design under SUTVA is linear in the empirical variance of the treatment-proportions vector . Optimizing the variance of the difference-in-means estimator under SUTVA, and holding the number of treated units constant, can be reduced to choosing the optimal variance of the treatment proportions vector . This leads to the following simple characterization for which randomized saturation design will lead to the lowest variance of the difference-in-means estimator under SUTVA.

Corollary 5.

Assuming SUTVA and holding the number of treated units fixed, if , then is attained when , corresponding to a stratified completely randomized assignment with . Otherwise, is attained when , corresponding to a cluster-based randomized assignment with

In other words, if the variance of the cluster-level aggregate outcomes is higher than the average of the intra-cluster outcome variances, then a cluster-based randomized assignment will only exacerbate the variance of the difference-in-means estimator. Without any further assumptions, a cluster-based randomized assignment is appropriate only when the variance of the cluster-level aggregate outcomes is lower than the average of the intra-cluster outcome variances. Furthermore, only a stratified completely randomized design or a cluster-based randomized designs can be the variance-minimizing design in the class of randomized saturation designs for the difference-in-means estimator under SUTVA, unless , in which case, all randomized saturation designs will lead to the same variance and mean-squared error. A proof of Corollary 5 is included in the supplementary materials.

2.3 Bias under a linear interference model

In the previous section, we explored the bias and variance of the difference-in-means estimator under SUTVA. In this section, we seek to extend these results to a setting where interference is present. For the sake of exposition, we will focus on a commonly-used linear model of interference. Consider a network over the units of experimentation, such that an edge between two units indicates they are likely to interfere with one another. Let the neighborhood of unit be the set of all units linked by a direct edge to unit and let , such that the outcome of unit can be expressed as

| (3) |

where is the proportion of ’s neighborhood that is treated. The coefficient can be interpreted as a direct effect parameter, while the coefficient can be interpreted as an interference parameter: if , then SUTVA holds. The linear model of interference in Equation 3 is an example of an anonymous interaction model (Manski, 2013) for which randomized saturation designs are appropriate. For any two assignment vectors and , such that the treatment status of unit and the number of its treated neighbors is identical, unit ’s outcome is held constant: . See Eckles et al. (2017) and Forastiere et al. (2021) for more details on the linear interference model.

We adopt the same notational conventions for as we did for in Section 2.1 such that , , , and correspond to the unit-level value, the cluster-level value, the vector of unit-level values in cluster , the vector of all unit-level values, and the vector of cluster-level values of the parameter correspondingly. We begin by quantifying the total treatment effect for this linear model of interference, for which a proof is provided in the supplementary materials.

Proposition 6.

Under the model of interference in Equation 3, the total treatment effect is the sum of the average direct effect and the average interference effect: .

To write the bias of the classic difference-in-means estimator in closed-form, we introduce the following linear combination of the different components of , where each component is down-weighted by the proportion of each unit’s intra-cluster number of neighbors to its total number of neighbors: . can be interpreted as a measure of clustering quality and is contained in the segment . For a perfect clustering where no graph edges are cut (i.e. endpoints belong to different clusters), . For a random clustering, . For a clustering which places no unit in the same cluster as one of its neighbors, . The expectation, and by extension the bias, of the difference-in-means estimator under the linear interference model defined in Eq. 3, can be expressed using .

Theorem 7.

Assuming the linear interference model in Eq. 3, the expectation of the difference-in-means estimator is given by .

The important takeaway of Theorem 7 is that the expectation—and therefore bias—of the difference-in-means estimator under a randomized saturation design is linear in the empirical variance of the treatment-proportions vector . Much like in Proposition 4, optimizing the bias of a randomized saturation design under the linear model of interference in Eq. 3 can be reduced to choosing the optimal variance of the treatment-proportions vector. This leads to the following characterization of which randomized saturation design minimizes the bias of the difference-in-means estimator.

Corollary 8.

Assume that the linear interference model from Equation 3 holds. We can distinguish three cases. If , then the bias of the difference-in-means estimator under a randomized saturation design is minimized for a cluster-based randomized assignment . The bias is then equal to . If , then the bias of the difference-in-means estimator under a randomized saturation design is minimized for a constant treatment-proportions vector and is equal to . If , then both results hold: the bias is constant, such that every randomized saturation design minimizes the bias.

A proof is included in the supplementary materials. The significance of as the cut-off point is intuitive: when the graph is randomly-clustered, . Hence, the first regime corresponds to a “better-than-random” clustering of the experimental units, where cluster-based randomized designs will improve the bias of the difference-in-means estimator, while the second regime corresponds to a “worse-than-random” clustering. In conclusion, to optimize the bias of the difference-in-means estimator for a randomized saturation design under the linear interference model in Equation 3, the optimal randomized saturation design is either a stratified completely randomized design or a cluster-based randomized design—the parameter , an indicator of the quality of the clustering, being the deciding factor between the two.

2.4 Variance under a linear interference model

In the previous section, we discussed the bias of the difference-in-means estimator under a linear interference model, and provided a treatment-proportions vector which minimizes this bias. In certain circumstances, we may be more interested in minimizing the variance of the estimator instead of its bias. We explore this in the following section, under the same linear interference model from Eq. 3.

Under the asymptotic regime where both the number of clusters and the size of each cluster are large enough, we can express the variance of the difference-in-means estimator in closed-form, in terms of the centralized moments of , as shown in the following theorem.

Theorem 9.

Suppose and . The total variance of the difference-in-means estimator is given by

| (4) |

where is the variance of the vector , and and are the third and fourth central moments of the vector . All five coefficients to depend only on the potential outcomes as well as certain statistics of the interference graph.

The explicit formulas for to are provided in the supplementary materials so as to not overburden the reader with notation. Unlike previous results, which were linear in the variance of the treatment-proportions vectors , the total variance of the difference-in-means estimator depends on up to the fourth central moment of the treatment-proportions vector , as expressed in (4).

2.4.1 Simplifying assumptions

Before determining which treatment-proportions vector minimizes the variance of the difference-in-means estimator , we first introduce a set of common assumptions under which the expressions for the coefficients can be significantly simplified.

Assumption 10.

As and , we suppose

-

(a)

(Boundedness) There exists a constant such that .

-

(b)

(Dense Connection) There exists a constant such that .

-

(c)

(Proxy Edge Probability) There exists a constant such that for all , we have

where

is the observed edge-formation probability between cluster and .

-

(d)

(Unconfoundedness of Network) We assume the edge formation between units and is approximately independent with their potential outcome parameters in the sense that, for any fixed bounded function of potential outcome parameters , there exists a constant such that for any unit and for any cluster

Assumption 10(a) assumes the potential outcome parameters are uniformly bounded as the size of the network increases to infinity. Assumption 10(b) requires that the degree of each unit be at least of the same order as its cluster size , such that for unit , the individualistic interference effect in (3) can be well approximated by its expectation with a negligible deviation of order . In Assumption 10(c), () is the ratio of the number of observed edges to the maximum possible number of edges between clusters and . serves as a proxy edge-formation probability between clusters and , such that the proportion of observed edges formed with unit in cluster departs at most from the proxy probability . The factor in Assumption 10(c) comes from a union bound over all possible pairs of .

Finally, assumption 10(d) impose a bound on the sample covariance between the edge formations and the potential outcomes . When this upper-bound is small, the formation of edges with some unit in cluster is approximately independent from the potential outcome parameters of that unit , hence the name “unconfoundedness of network”.

In Section 2.5, we extend our results to graphs which are generated by a known random process. In particular, we will show that if the graph is generated under a stochastic block model, Assumption 10 is satisfied with high probability. While Assumptions 10(a)-10(c) are common assumptions in real applications, Assumption 10(d) may require further examination. In the stochastic block model example, Assumption 10(d) holds because the edge forming probability only depends on a predetermined probability matrix; it may fail under other random graph models that incorporate potential outcomes in the graph-generating process (e.g. a graphon model where the edge-forming probability is a bivariate function of the potential outcomes of the two nodes). Handling cases where the graph is confounded with the potential outcomes is out-of-scope for our paper.

To further simplify Eq. (4), we can assume that the interference effects are “block-fixed”, formalized in the following assumption—the full expression for Eq. (4) without this simplifying assumption can be found in the supplementary materials.

Assumption 11 (Block-fixed Interference Effect).

The interference effect is fixed within each cluster such that , , where is the common interference parameter in cluster .

Under Assumption 11, we can rewrite , where the common value of interference parameters in each cluster is down-weighted by the average proportion of intra-cluster edges per cluster.

2.4.2 Simplified form

We provide the simplified form of the coefficients in Theorem 9 under Assumption 10 and Assumption 11 (block-fixed interference effect) in the following corollary.

Corollary 12.

Under Assumption 10 and Assumption 11 , the coefficients in Eq. (4) can be simplified to

where is the harmonic mean of , is the row-normalized transformation of the proxy edge-forming probabilities , and is the vector of down-weighted cluster-level interference parameter, whose coordinates are . Recall that and are the sample variance and sample covariance operators introduced in (1).

It is also possible to compute these coefficients in closed-form under Assumption 10 without the block-fixed effect assumption (Assumption 11). To ease the notational burden on the reader, we defer this formula to the supplementary material, and present only their simplified form here.

By definition of the coefficients in Eq. 4, the coefficient corresponds to the variance of the difference-in-means estimator under a stratified completely randomized assignment, where , such that and . As expected, if , the expression for coincides with the variance of the difference-in-means estimator under SUTVA, found in Equation 2 of Proposition 4, for a stratified completely randomized assignment. Similarly, the expression for , the coefficient before the variance of , is almost identical to the expression found of the analog parameter in the SUTVA case, in Equation 2 of Proposition 4, except that the between-cluster sample covariance terms now appear with interference coefficients: .

The connection between the expressions for the coefficients and in the linear interference model and in the SUTVA case is salient when each unit has a sufficiently large number of neighbors. In that case, using the law of large numbers, the potential outcomes of unit can be approximated by

where . As a result, in the asymptotic regime where each unit has many neighbors in the graph, the coefficients and have the same expression as the SUTVA case by replacing with .

The coefficients do not have similar correspondences in the expression of the variance of the estimator under SUTVA. Recall that corresponds to the average proportion of neighbors, belonging to cluster , of units in cluster ; corresponds to the within-cluster proportion of neighbors in cluster . The coefficient can be described as the between-cluster second moment of , weighted by the proportions . The coefficient is the between-cluster sample covariance of the potential outcome combination and the interference parameter , down-weighted by the intra-cluster edge proportion . Similarly, is the sample covariance of interference parameters , down-weighted by . In the extreme case when the clusters are isolated, we have and in both and .

2.4.3 Choosing a variance-minimizing distribution of under interference

Previously, the statistics of interests—like the bias and variance under SUTVA, and the bias under interference—were linear in the variance of such that determining an optimal distribution of was straightforward. However, finding the optimal variance under interference over is more challenging as the variance depends on the first four central moments of the vector . It is an especially difficult problem when is large. In order to minimize in a tractable way, we consider optimizing it within the following set for the treatment proportions vector :

| (5) |

The set consists of all symmetric M-tuples bounded within and centered at . One benefit of considering is that it contains only symmetric distributions, which have zero skewness, such that the third moment term in (4) disappears. Another benefit of considering the set of distributions is the ability to optimize the variance with respect to the second moment and the fourth moment separately. To see this, we observe that fixes the mean at and that the vector can be entirely determined by its first half of coordinates . Define the square of the distance between each point and the mean as One can easily verify that and , which correspond to the mean and variance of respectively. To optimize the variance with respect to the second and fourth moments separately, we begin by maximizing (or minimizing) , depending on the sign of . The resulting optimization program is quadratic in , which we can set independently of to its optimal value. Finally, we set to its optimal value as suggested in the first step of the optimization, consider the case when and each element in is bounded between and , without loss of generality. For any given (or equivalently, a given ), is lower bounded by 0, attained when , and is upper bounded by , attained when -portion of are at and the rest stays at . This procedure is formalized in the following proposition.

Proposition 13.

Consider the optimization such that

where and are given by (4) and (5) correspondingly. Suppose, without loss of generality, . Then, we have the following optimal values .

-

(i)

if , the first half of ’s lie at and the second half of ’s lie at , where

-

(ii)

if , -portion of ’s lie at , -portion of ’s lie at , and -portion of ’s lie at , where

We considered optimizing the variance of the difference-in-means estimator under three different settings of clustering quality and interference effect structure as illustrating examples to the reader. For the sake of brevity, we relegated two of these examples to the appendix (cf. Examples 20 and Examples 21 in Section B of the appendix).

Example 14 (Perfect clustering and block-fixed interference).

Suppose Assumption 10 holds, interference effects are block-fixed and the graph is perfectly clustered such that

Assume .

(i) If the intra-cluster variance of potential outcomes dominates the inner-cluster one (), the optimal assignment vector is

for all . The optimal variance is

(ii) If the intra-cluster variance of potential outcomes dominates the inter-cluster one (), the optimal assignment vector is

The corresponding optimal variance is

When , in case (i) and case (ii) of Example 14, the optimal designs are the stratified design and cluster-based design, respectively. In Example 21, relegated to the appendix, we show the same is true even if the interference effects are not block-fixed. However, when the units are randomly clustered–with block-fixed interference effect—the optimal design is no longer one of the two extremes necessarily, as shown in case (ii) of Example 20, which can also be found in the appendix.

2.5 Extensions

There are some important extensions that can be made to the results presented here. For example, we focused thus far on the difference-in-means estimator, but other estimators may also be appropriate. While the difference-in-means estimator is agnostic to any model assumptions or validity of the clustering—and is unbiased if the stable unit treatment value assumption holds—we might benefit from using a stratified estimator if we believe that the clustering of units is representative of the potential outcomes in some way. When the stable unit treatment value assumptions holds, we can choose an appropriate configuration for the stratified estimator such that it becomes unbiased, conditionally on the assignment of treatment proportions to clusters , and in expectation over any randomized saturation assignment. We can also show that its variance depends only on the harmonic mean of and covariances of the potential outcomes. Finally, we can show that under the linear interference model introduced in Eq. 3, the expectation of the stratified estimator is a constant function of . To improve the brevity of our paper, we have relegated these initial extensions to the supplementary materials.

Furthermore, many of our results are implicitly conditioned on a fixed observed graph. In certain cases, it may be more appropriate to consider an underlying random graph model and include this randomness as an additional integration step in our results. Consider, for example, one of the simplest and well-studied random graph models: the stochastic block model (Holland et al., 1983; Anderson et al., 1992; Wasserman and Faust, 1994; Goldenberg et al., 2010). It states that the probability that an edge exists between two units in a graph depends only on the clusters they belong to. In other words, two units belonging to clusters and —with and possibly equal—are linked by an edge with probability . We define the block-matrix of the graph , such that . Under such a random graph model, the measure of clustering quality , introduced in Theorem 7, has expectation , with respect to the stochastic block-model with block-matrix . Because all other quantities in Theorem 7 are constant with respect to the graph, the expectation of the difference-in-means estimator can easily be extended to incorporate the random graph model by replacing with its expectation , computed above. Additionally, by considering a stochastic block model, we can ensure with high probability the validity of the assumptions made to simplify the expression of Equation 4.

Proposition 15.

Suppose that the interference graph is generated according to a stochastic block model with block-matrix , such that . Let , then Assumptions 10(b)-10(d) are satisfied with high probability. More specifically, for any constant , Assumption 10(b) is satisfied with probability at least ; for any constant , Assumption 10(c) is satisfied with probability at least ; for any constant , Assumption 10(d) is satisfied with probability at least .

A proof is included in the supplementary materials. A more thorough extension of our results to other random graph models is left for future work.

3 Deterministic Saturation Designs

In the previous section, we investigated randomized saturation designs, which assign random treatment proportions to clusters of the experimental cohort. We then analysed the bias and variance of the difference-in-means estimator for this class of randomized saturation design. From these results, we determined which randomized saturation design optimized these objectives, under a regime where SUTVA holds and a regime where a linear model of interference holds. We show that the bias and variance of these estimators can often be expressed in terms of moment of the treatment-proportions vector , therefore reducing the objective of finding the “optimal randomized saturation designs” among all possible vectors to optimizing over the moments of this vector instead.

This optimization is limited by the random assignment of coordinates of to each cluster. Optimal deterministic saturation designs, which we introduce below, go one step further in their optimization by removing the permutation step and choosing the optimal treatment proportion per cluster.

Definition 16.

Let be an objective function, taking as input a treatment-proportions vector , a clustering of the experimental units, and a set of parameters . Let be an allowable set of treatment-proportions vectors. An optimal deterministic design selects that minimizes

| (6) |

and, for each cluster , assigns randomly-chosen units to treatment and the remaining units to control.

It is up to the practitioner to choose which objective function is most relevant. Generally, she will choose to be the bias, variance, or mean-squared error of her estimator of choice, conditioned on the assignment of a specific treatment proportion to each cluster. In fact, many of these conditional expectations and variances were previously computed in Section 2, as a step in applying Adam’s law (law of iterated expectations) or Eve’s law (law of total variance). We list some common examples below, and show how each objective can be optimized in each scenario.

Example 17.

Let be the bias of the difference-in-means estimator under the stable unit treatment value assumption. Let be the set of treatment proportion vectors with fixed average , where is some fixed number of treated units.

| (7) |

The constant vector minimizes the objective function and belongs to :

In other words, the stratified completely randomized assignment is an optimal deterministic saturation design for , the bias of the difference-in-means estimator under the stable unit treatment value assumption.

A proof can be found in Section F.1. Practitioners may wish to choose an optimal deterministic saturation design that optimizes not just for the bias of an estimator, but its variance as well. A common objective is to optimize them jointly in the form of the mean-squared error, as is done in the following example.

Example 18.

Let be the mean-squared error of the difference-in-means estimator under the stable unit treatment value assumption. Let be the set of treatment proportion vectors with fixed average , where is some fixed number of treated units.

| (8) |

From Propositions 3 and 4, we can express this objective in closed-form:

where with defined in Proposition 4, is a vector of length , and is an diagonal matrix whose diagonals are . Therefore, the optimal proportion vector can be obtained by the following quadratic optimization.

| (9) | ||||

| subject to | (10) | |||

The feasible set defined by the constraints of (9) is a convex set with vertices belonging to , corresponding to the class of cluster-based randomized saturation designs.

When , the matrix is negative semi-definite, resulting in the concavity of the objective function (9), in which case, the optimal proportion vector must lie on the vertices of the feasible set , corresponding to a -valued proportion vector.

For general cases, when and is neither positive or negative semi-definite, the optimal proportion vector must lie on the boundary of , but not necessarily the vertices. In other words, the stratified randomized saturation design is never optimal. See Appendix F.2 for more details.

Beyond operating under the stable unit treatment value assumption, optimal deterministic saturation design can postulate a parametric model of potential outcomes with interference, like the one in Equation 3, which we do in the following final example.

Example 19.

Let be the conditional mean squared error of the difference-in-means estimator under the linear interference model in (3). Let be the set of treatment proportion vectors with fixed average , where is some fixed number of treated units.

| (11) |

Specifically, assuming Assumptions 10(a) and 10(b), if the units are perfectly clustered, we can rewrite the objective function as follows:

| (12) |

where is a constant term with respect to , , and . The objective function shown in (12) is quadratic in . In practice, one can find the optimal point of subject to through a quadratic programming solver (for example, the Sequential Least Squares Programming (SLSQP) algorithm).

Under certain additional assumptions, we can express the solution in closed-form. First, we assume there is no significant difference in the distributions of outcome parameters across different clusters such that Second, we assume that the interference effects are block-fixed and that the number of neighbors is identical for units in the same cluster such that and are constant in any cluster. When these two additional assumptions hold, the objective function (12) is a quadratic function of :

| (13) |

The support for is . The minimum value of the objective function (13) is attained when , i.e. when . From Corollary 8, when units are perfectly clustered such that , the bias is minimized for any -valued proportion vector. Similarly, the conditional variance term in (12) also obtains its minimum ( in this case) when for all . Therefore, the conditional mean squared error is minimized at any with .

4 Simulations

In order to validate the results of the previous section, we implement a small-scale simulation study to validate the bias-variance trade-offs available to randomized saturation designs. We also illustrate the potential upside of using deterministic saturation designs.

4.1 Optimal Randomized Saturation Designs

In Section 2, we presented several objectives for which, under certain assumptions on the potential outcomes, either the stratified randomized design ( is minimized) or the cluster-based randomized design ( is maximized) are optimal. This is the case in Corollary 5 and Corollary 8 for example. However, these designs are not always optimal, as we show in Section 2.4, notably when the variance—and consequently the mean-squared error—of the difference-in-means estimator under a linear model of interference is concerned. In this first simulation, we consider the variance of the difference-in-means estimator under a linear interference model where the stratified randomized design and the cluster-based randomized designs are not optimal, and illustrate the benefit of using an optimal randomized saturation design instead.

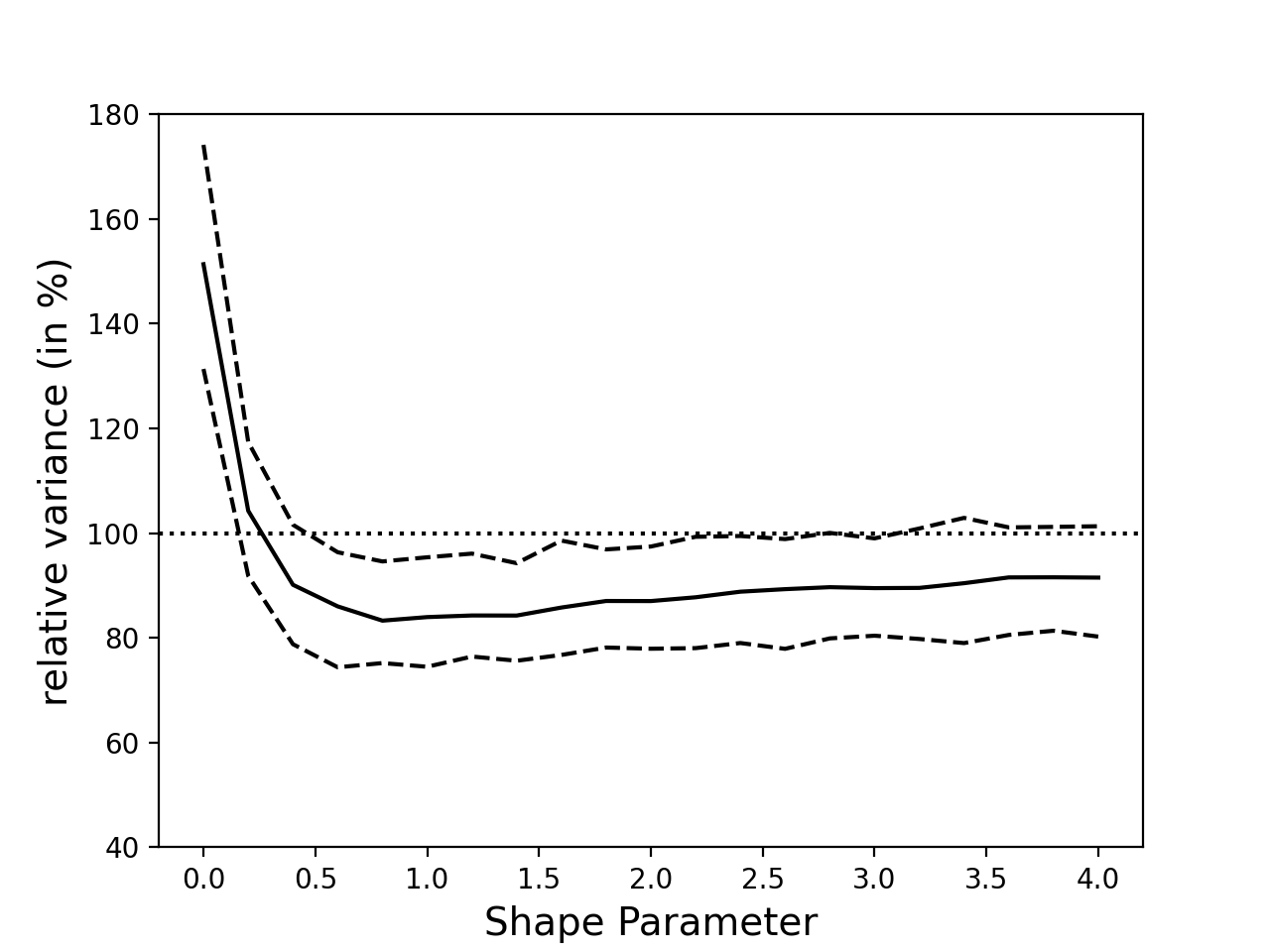

We consider a population of 2,000 units, grouped into 40 equally-sized clusters which are labeled through . The interference graph is generated according to a stochastic block model such that the probability of observing an edge between units and is The edge-formation probability is chosen so that different pairs of clusters have different forming probabilities in general. In particular, this increases the value of in the variance of the difference-in-means estimator in Theorem 9 by increasing the variance terms in the closed-form expression of , which can be found in the appendix. As a result, the variance of difference-in-means estimator will, in general, have a larger curvature as a function of the second moment of , as we show below.

The potential outcomes are randomly generated according to the following distributions:

After sampling these outcome parameters, we transform each to so that after the transformation. The normalization of fixes the inter-cluster variance of to , such that the variance coefficient in Theorem 9 can be tuned by a single parameter . Furthermore, we consider the proportion vector within the family of symmetric Beta distribution Beta such that

where is the shape parameter and is the c.d.f function of . Within the symmetric Beta distribution family, we recover our two baseline randomized designs. When , corresponds to the cluster-based randomized design where half of the clusters are assigned to treatment and all others to control. When , corresponds to the stratified completely randomized design where exactly half of the units in each cluster are treated.

Recall Theorem 9, where the variance of the difference-in-means estimator can be expressed as

by ignoring the fourth order term and by observing that for symmetric beta distributions. In the subsequent simulations, we carefully choose such that , making the optimal distribution for within symmetric Beta distributions.

Finally, we generated 100 realizations of the interference graph and outcome parameters according to the distributions described above. For each realization, we investigated the variance of the difference-in-means estimator under a randomized saturation design for 22 different shape parameters . For each shape parameter, the variance is estimated by the sample variance of difference-in-means estimates from 1000 random assignments. We report the relative change in variance over 100 realizations for each value of the shape parameters in Figure 1, where the relative change in variance= is calculated with respect to the variance of the estimator under a stratified randomized saturation design (). The lower 2.5% quantile and the upper 2.5% quantile are also reported in dashed lines.

Figure 1 shows that by fixing at , neither the cluster-based randomized design () nor the stratified randomized design achieve the minimum variance. The minimum average percentage of variance is obtained at about , which reduces the variance of the difference-in-means estimator in a stratified randomized design by roughly 17% in our simulations.

4.2 Optimal Deterministic Saturation Designs

In Section 3, we showed that, rather than randomizing over which treatment proportion gets assigned to which cluster—the first step of any randomized saturation design—we could also consider skipping this permutation step and directly optimize each coordinate of the treatment proportions vector . We referred to this latter category of designs as a deterministic saturation design in Definition 16. Because a deterministic saturation design can select the optimal treatment proportion for each cluster, as opposed to the optimal distribution of treatment proportions, we expect the statistical measure that is being optimized—like the bias and variance of the difference-in-means estimator—to improve when using a well-chosen deterministic saturation design over even the best possible randomized saturation design.

In this section, we demonstrate the benefits of using an optimal deterministic saturation design, as compared to various randomized saturation designs. More specifically, we will compare an optimally-chosen deterministic saturation design over the best possible randomized saturation design—including both the cluster-based and stratified completely randomized designs. Additionally, we will also compare our optimally-chosen deterministic saturation design with fixed treatment proportions vector to a randomized design which permutes . Naturally, we expect this re-randomized design to perform worse than the best possible randomized saturation design on the metric for which we are optimizing for.

We construct the following simulation using the setting presented in Example 19, which considers the mean-squared error of the difference-in-means estimator under a linear model of interference. We again consider 40 clusters, each containing 50 units. We assume the outcomes follow a linear interference model with the interference graph generated according to a stochastic block model with edge probability:

We consider the following distributions for the outcome parameters:

Recall that three designs will be simulated and compared:

-

•

The optimal randomized saturation design. Because the clustering is “perfect” (no edges are cut), we know from Corollary 8 that the bias of the difference-in-means estimator is minimized for a cluster-based randomized design. Specifically, the bias is given by . On the other hand, from Corollary 12, we have the expected coefficients are , and . When , the optimal design allocates on two points, or equivalently, has zero fourth central moment (see Proposition 13). Therefore the mean squared error of can be written in a quadratic form of as

up to some constant term. The MSE obtains its minimum at , corresponding to . As must be an integer, the closest possible assignment is . We use in this simulation for simplicity.

-

•

The optimal deterministic saturation design. Recall that for this category of designs, we fix the vector in the treatment assignment procedure. The optimal choice of the assignment-proportion is obtained by optimizing the conditional MSE in (12) in Example 19, subject to , using a quadratic programming solver. We expect this design to have the lowest mean-squared error, since it optimizes that objective for each coordinate of the treatment proportions vector, rather than optimizing over its distribution.

-

•

The re-randomized saturation design. Instead of fixing at as we did for the optimal deterministic saturation design, we permute when assigning treatment. Therefore, the suggested re-randomized saturation design is a special case of a randomized saturation design, which uses instead of . While we expect this design to perform the worse of the three suggested designs for the mean-squared error of the difference-in-means estimator, this comparison allows us to showcase that (i) the optimal deterministic randomized design does outperform a non-optimally-chosen randomized saturation design, (ii) the out-performance of the chosen deterministic saturation design is not due to the distribution of , but its ability to fix and optimize each coordinate of .

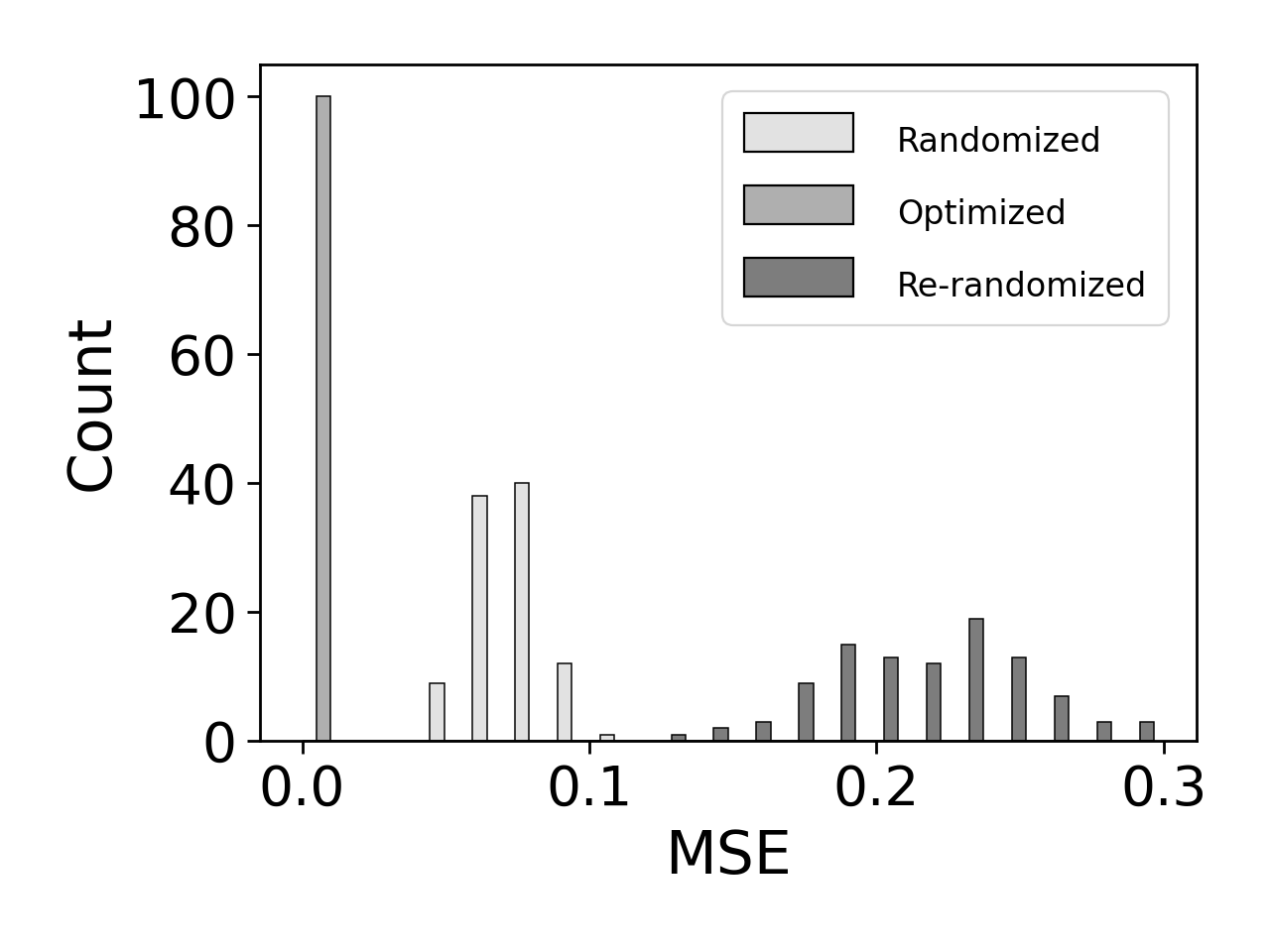

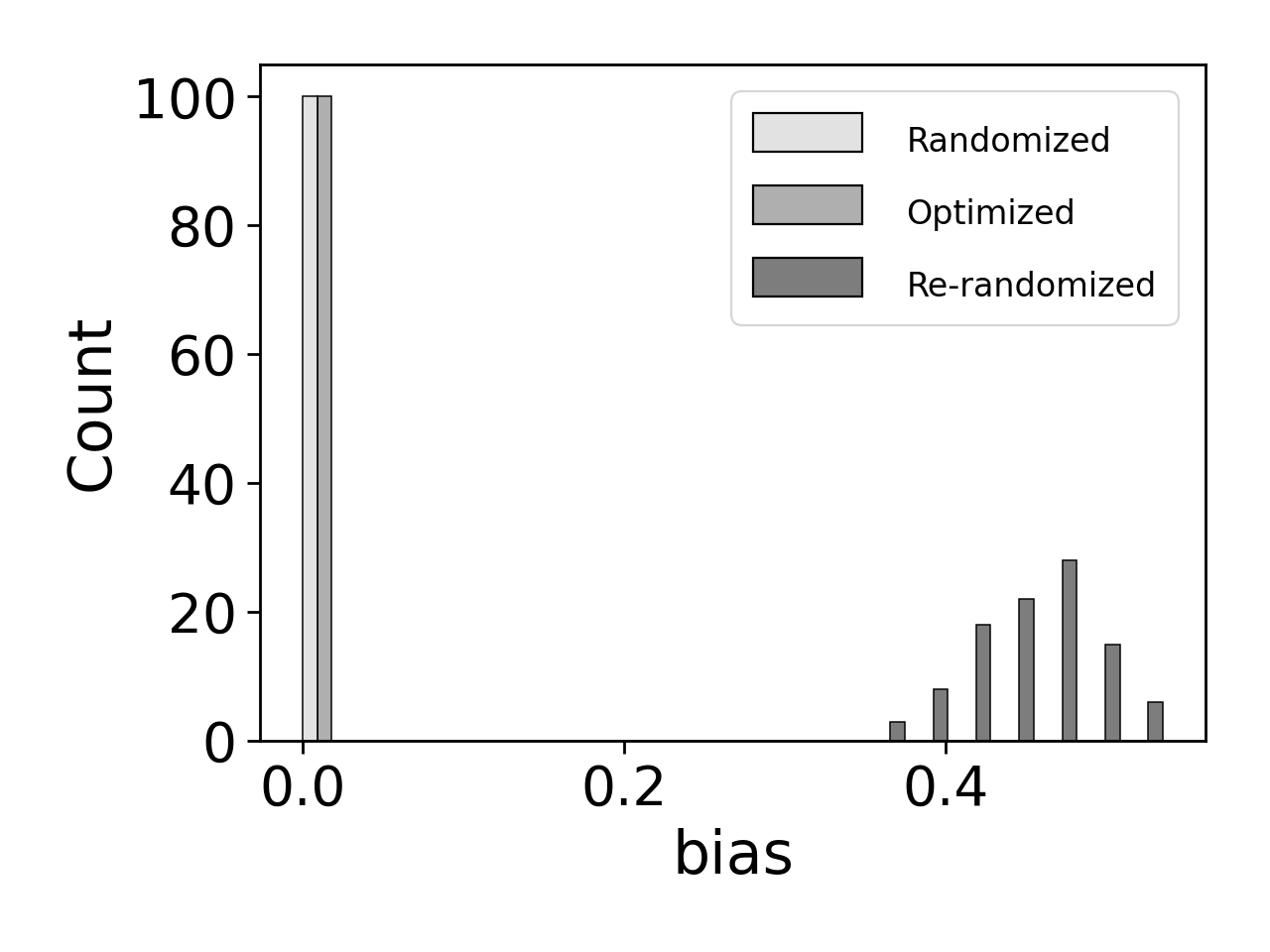

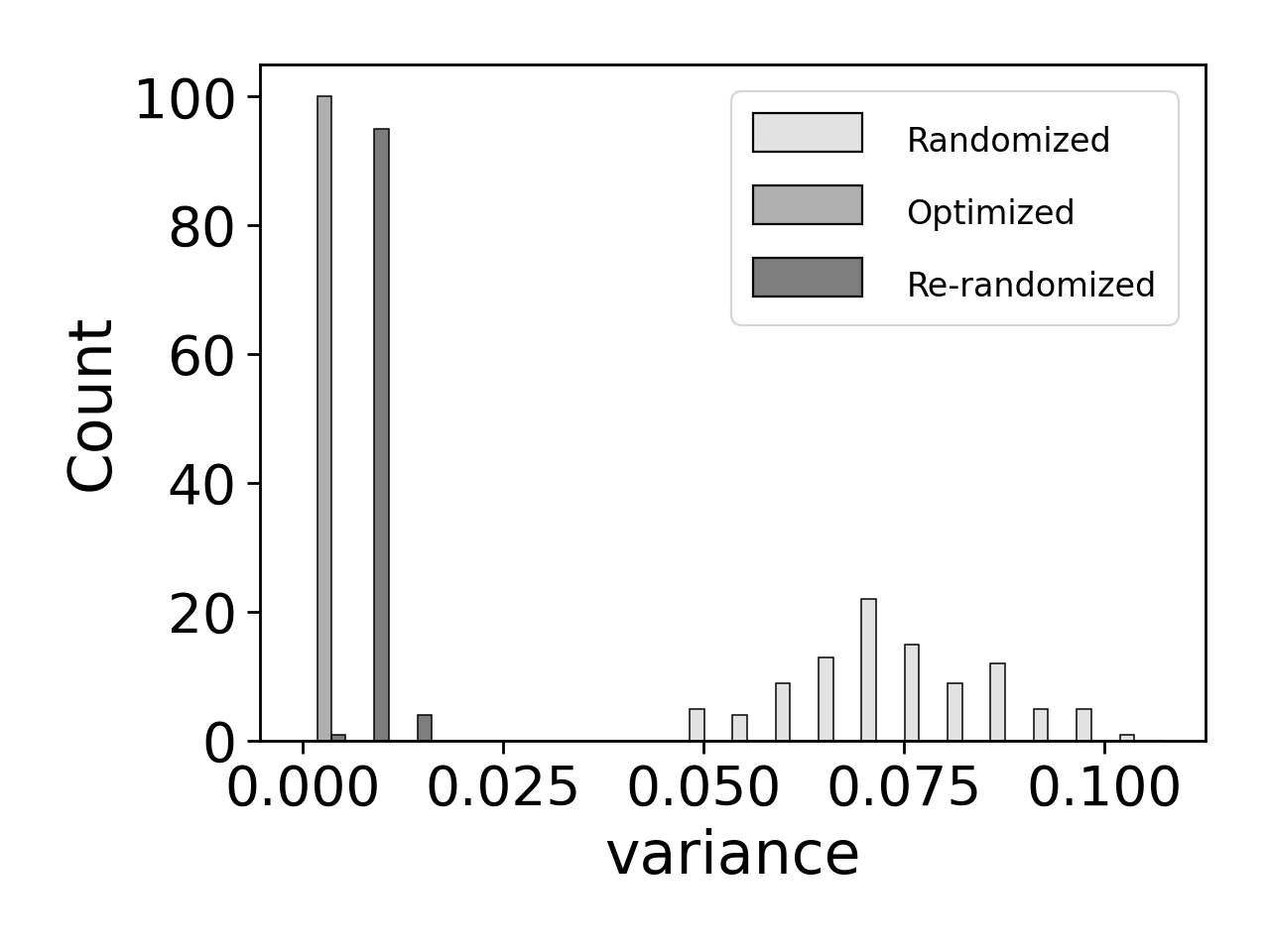

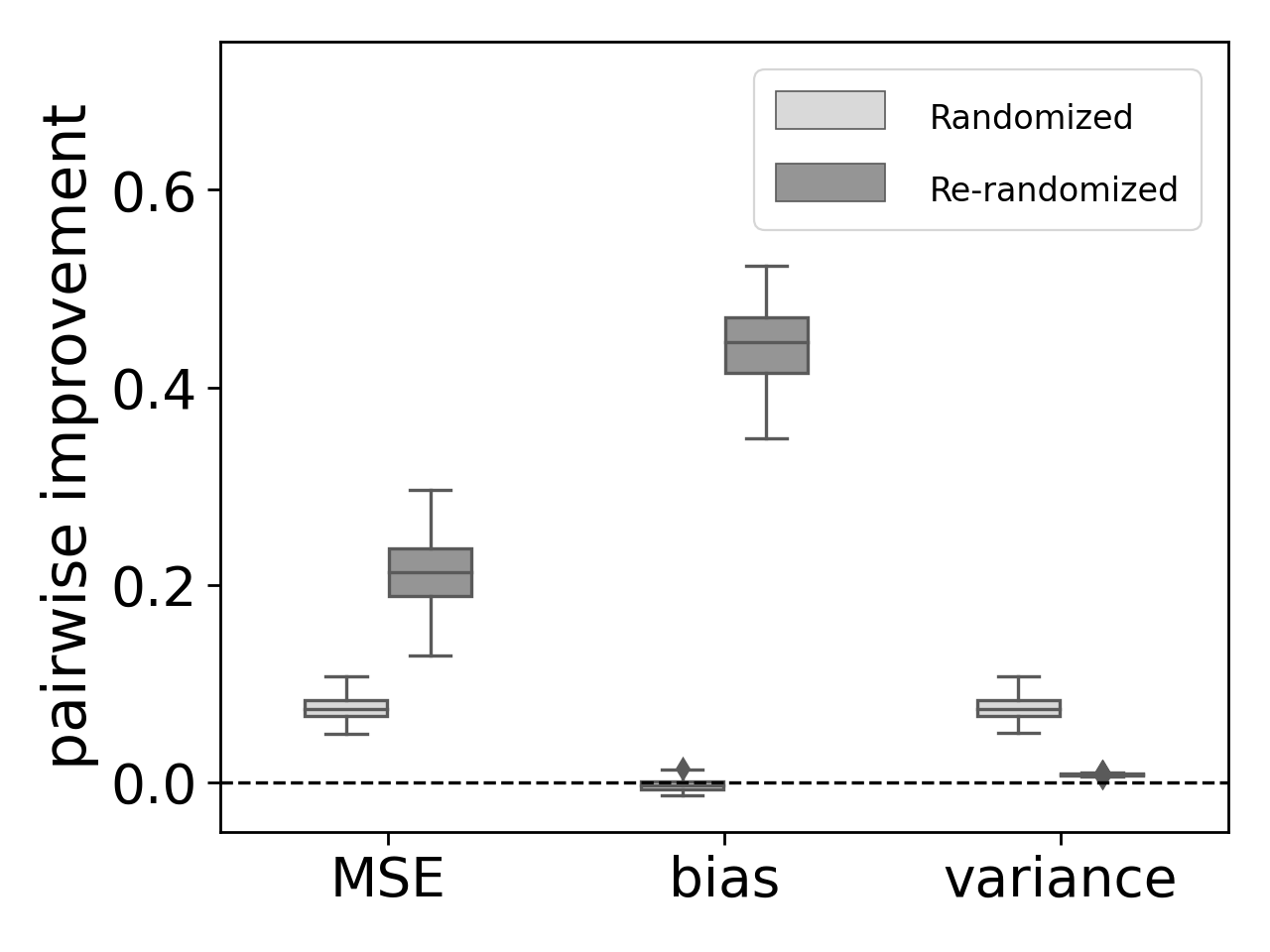

We simulated 100 realizations of interference graph and outcome parameters. For each realization, we estimate the bias, variance and mean squared error of the difference-in-means estimator from random assignments from the three suggested designs. The histogram in Figure 2 reports the distribution of bias, variance and mean squared error of the three designs.

As shown in Figure 2, the randomized saturation design optimized for the mean-squared error of the difference-in-means estimator achieves the best (lowest) value for that objective. Expectedly, the optimal deterministic randomized design performs the second best, since the re-randomized design is able to neither fix the optimal coordinate values for nor optimize its distribution. When examining the bias and the variance of each design separately, we notice that both the optimal deterministic saturation design and the optimal randomized saturation design have similar and small bias compared to the one of the re-randomized design, but the variance of the optimal randomized saturation design is significantly greater than the two others. Compared to the optimal randomized and the re-randomized saturation design, the optimal deterministic saturation design reduces the bias and variance simultaneously.

Figure 2 demonstrates the population comparison over 100 repetitions. Although the optimal deterministic saturation design outperforms the optimal randomized one on average, it is still necessary to check if there is any circumstance that the optimal deterministic saturation design is sub-optimal. A stronger assertion would be whether the optimal deterministic saturation design improves the optimal randomized saturation design on every single realization. Our answer is affirmative. Figure 3 demonstrates the improvement in bias, variance, and the mean-squared error of the optimal deterministic saturation design over the other two designs in each of the 100 realizations. One can observe that the optimal deterministic saturation design always improves over the re-randomized saturation design and consistently reduces the variance and MSE from the randomized saturation design.

5 Conclusion and Practical Considerations

This manuscript focuses on the randomized saturation designs, where each cluster of units is first assigned with a treatment proportion and then units within this cluster are randomly assigned to treatment. Depending on whether the treatment proportions assigned to clusters are randomized, we distinguish between two types of randomized saturation designs: the randomized saturation design and the deterministic saturation design. The stratified randomized saturation design, where the treatment proportions are constant, and the cluster-based randomized saturation design, where the treatment proportions are -valued are two well-studied special cases of the randomized saturation design.

When the potential outcomes satisfy SUTVA, the difference-in-means estimator is unbiased under all randomized saturation designs, and in terms of variance/mean squared error, either the stratified randomized saturation design or the cluster-based one is optimal, depending on the relative values of the inter-cluster variance of outcomes and the intra-cluster variance of outcomes.

When interference is present, we show the bias of the difference-in-means estimator is linear in the variance of the treatment proportion vector for a linear model of interference. In addition, the variance of the difference-in-means estimator is a linear function of the variance, the squared variance, the third central moment and the fourth central moment of the treatment proportion vector. The minimization of such a variance is tractable when we restrict the proportion vector to all symmetric distributed vectors around the fixed mean. It is possible that neither the cluster-based design nor the stratified design is optimal as demonstrated in Section 4.1.

The performance of the difference-in-means estimator can be further improved through the optimal deterministic saturation design, when the model is correctly specified. Specifically, the conditional mean squared error of the difference-in-means estimator under SUTVA or under the linear interference model can be optimized by choosing a fixed proportion vector as discussed in Examples 18 and 19. The benefits achieved from the optimal deterministic saturation design are demonstrated in the simulation in Section 4.2.

We note that, although our analysis on optimizing randomized saturation designs is based on the exact values of potential outcomes, it does not require full knowledge on all units’ potential outcomes to find the optimal proportion vector . As illustrated in Theorem 9 and its simplified form in Corollary 12, the knowledge of certain cluster-level statistics of potential outcomes (e.g., intra-cluster and inter-cluster variances) is sufficient for optimization. Therefore, if an experimenter has certain prior knowledge on these cluster-level statistics—perhaps a pilot experiment has been run on a small scale—an optimal deterministic saturation design can be generated using our approach by plugging in the pre-assumed/estimated potential outcome statistics. The resulting saturation designs are exactly optimal when the ‘plug-in’ parameters are accurate and may still improve over the two extreme designs (cluster-based and stratified) when these ‘plug-in’ parameters are misspecified. Furthermore, as one would expect, there is no free lunch on the performance improvement obtained from the optimal deterministic saturation designs. Optimizing the deterministic saturation design as shown in Definition 16 requires more cluster-specific statistics than finding the optimal randomized saturation design, resulting in compromising the robustness under model misspecification. In practice, one would choose the optimal randomized saturation design or the optimal deterministic design based on the feasibility of accurately estimating the necessary population-level statistics of the potential outcomes. The idea of using plug-in values to design optimal experiments is related to the model-assisted designs (Basse and Airoldi, 2018), where an artificial model is assumed to generate designs which are guaranteed to be optimal when properly specified.

References

- Anderson et al. [1992] Carolyn J Anderson, Stanley Wasserman, and Katherine Faust. Building stochastic blockmodels. Social networks, 14(1-2):137–161, 1992.

- Andreev and Racke [2006] Konstantin Andreev and Harald Racke. Balanced graph partitioning. Theory of Computing Systems, 39(6):929–939, 2006.

- Athey et al. [2015] Susan Athey, Dean Eckles, and Guido W Imbens. Exact p-values for network interference. Technical report, National Bureau of Economic Research, 2015.

- Baird et al. [2016] Sarah Baird, J Aislinn Bohren, Craig McIntosh, and Berk Özler. Optimal design of experiments in the presence of interference. Review of Economics and Statistics, 2016.

- Banerjee et al. [2013] Abhijit Banerjee, Arun G Chandrasekhar, Esther Duflo, and Matthew O Jackson. The diffusion of microfinance. Science, 341(6144), 2013.

- Banerjee et al. [2012] Abhijit V Banerjee, Raghabendra Chattopadhyay, Esther Duflo, Daniel Keniston, and Nina Singh. Can institutions be reformed from within? evidence from a randomized experiment with the rajasthan police. CEPR Discussion Paper DP8869, 2012.

- Basse and Airoldi [2018] Guillaume W Basse and Edoardo M Airoldi. Model-assisted design of experiments in the presence of network-correlated outcomes. Biometrika, 105(4):849–858, 2018.

- Crépon et al. [2013] Bruno Crépon, Esther Duflo, Marc Gurgand, Roland Rathelot, and Philippe Zamora. Do labor market policies have displacement effects? evidence from a clustered randomized experiment. The Quarterly Journal of Economics, 128(2):531–580, 2013.

- Eckles et al. [2017] Dean Eckles, Brian Karrer, and Johan Ugander. Design and analysis of experiments in networks: Reducing bias from interference. Journal of Causal Inference, 5(1), 2017.

- Forastiere et al. [2021] Laura Forastiere, Edoardo M Airoldi, and Fabrizia Mealli. Identification and estimation of treatment and interference effects in observational studies on networks. Journal of the American Statistical Association, 116(534):901–918, 2021.

- Goldenberg et al. [2010] Anna Goldenberg, Alice X Zheng, Stephen E Fienberg, Edoardo M Airoldi, et al. A survey of statistical network models. Foundations and Trends® in Machine Learning, 2(2):129–233, 2010.

- Holland et al. [1983] Paul W Holland, Kathryn Blackmond Laskey, and Samuel Leinhardt. Stochastic blockmodels: First steps. Social networks, 5(2):109–137, 1983.

- Hudgens and Halloran [2008] Michael G Hudgens and M Elizabeth Halloran. Toward causal inference with interference. Journal of the American Statistical Association, pages 832–842, 2008.

- Imbens and Rubin [2015] Guido W. Imbens and Donald B. Rubin. Causal Inference in Statistics, Social, and Biomedical Sciences. Cambridge University Press, 2015.

- Johari et al. [2020] Ramesh Johari, Hannah Li, and Gabriel Weintraub. Experiment design in two-sided platforms: An analysis of bias. In ACM Conference on Economics and Computation (EC), 2020.

- Manski [2013] Charles F Manski. Identification of treatment response with social interactions. The Econometrics Journal, 16(1):S1–S23, 2013.

- Mitchell [2004] Douglas W Mitchell. 88.27 more on spreads and non-arithmetic means. The Mathematical Gazette, 88(511):142–144, 2004.

- Owen and Varian [2020] Art B Owen and Hal Varian. Optimizing the tie-breaker regression discontinuity design. Electronic Journal of Statistics, 14(2):4004–4027, 2020.

- Phan and Airoldi [2015] Tuan Q Phan and Edoardo M Airoldi. A natural experiment of social network formation and dynamics. Proceedings of the National Academy of Sciences, 112(21):6595–6600, 2015.

- Pouget-Abadie et al. [2018] Jean Pouget-Abadie, Vahab Mirrokni, David C Parkes, and Edoardo M Airoldi. Optimizing cluster-based randomized experiments under monotonicity. In Proceedings of the 24th ACM SIGKDD International Conference on Knowledge Discovery & Data Mining, pages 2090–2099. ACM, 2018.

- Rosenbaum [2007] Paul R Rosenbaum. Interference between units in randomized experiments. Journal of the American Statistical Association, 102(477), 2007.

- Rosenman and Owen [2021] Evan Rosenman and Art B Owen. Designing experiments informed by observational studies. arXiv preprint arXiv:2102.10237, 2021.

- Rubin [1974] Donald B. Rubin. Estimating causal effects of treatments in randomized and nonrandomized studies. Journal of Educational Psychology, 66(5):688–701, 1974.

- Sinclair et al. [2012] Betsy Sinclair, Margaret McConnell, and Donald P. Green. Detecting spillover effects: Design and analysis of multilevel experiments. American Journal of Political Science, 56(4):1055–1069, 2012.

- Tchetgen and VanderWeele [2012] Eric J Tchetgen Tchetgen and Tyler J VanderWeele. On causal inference in the presence of interference. Statistical Methods in Medical Research, 21(1):55–75, 2012.

- Toulis and Kao [2013] Panos Toulis and Edward Kao. Estimation of Causal Peer Influence Effects. In ICML, 2013.

- Ugander and Backstrom [2013] Johan Ugander and Lars Backstrom. Balanced label propagation for partitioning massive graphs. In WSDM, 2013.

- Ugander et al. [2013] Johan Ugander, Brian Karrer, Lars Backstrom, and Jon Kleinberg. Graph cluster randomization: Network exposure to multiple universes. In KDD, 2013.

- Wasserman and Faust [1994] Stanley Wasserman and Katherine Faust. Social network analysis: Methods and applications, volume 8. Cambridge university press, 1994.

- Zaller and Köpke [2004] Johann G Zaller and Ulrich Köpke. Effects of traditional and biodynamic farmyard manure amendment on yields, soil chemical, biochemical and biological properties in a long-term field experiment. Biology and fertility of soils, 40(4):222–229, 2004.

Appendix A Analysis of the Difference-in-means Estimator under SUTVA

A.1 Proof of Proposition 3

The expectation of the difference-in-means estimator conditioned on the proportion of units assigned to treatment is given by:

We now introduce the permutation matrix .

This last quantity corresponds to the total treatment effect, hence the proof that the difference-in-means estimators is unbiased under the stable unit treatment value assumption for a randomized saturation design.

A.2 Proof of Proposition 4

Using Eve’s law, we have that

We first compute the variance of the estimator conditional on an assignment of the treatment proportions vector . We start from

where . Its conditional variance is given by

The expectation of the conditional variance is therefore

Next, from Proposition 3, the conditional expectation of is

where is the cluster-level averaged potential outcome. Its variance is

The total variance is now immediate.

A.3 Proof of Corollary 5

It suffices to prove that the variance of is maximized at with a constrained mean.

We show that the variance of the treatment proportions vector is maximized, constrained to verify , only for vectors assigning either all of a cluster to treatment or none, assuming that a solution in verifying the equality constraint exists. One direction is easy. Let be any assignment placing all of a cluster to treatment or none, and verifying the inequality constraint.

We prove the other direction. Consider . Consider increasing and decreasing by such that the total number of treated units is constant: , , and , such that:

Since , , which concludes the proof.

Appendix B Examples of variance-minimizing distributions of under interference

Example 20 (Random clustering and block-fixed interference).

Suppose Assumption 10 holds, interference effects are block-fixed and the graph is randomly clustered such that

Assume . Then and

(i) If , the optimal assignment vector is for all . The optimal variance is .

(ii) If , the optimal assignment vector is

(iii) If , the optimal assignment vector is

Example 21 (Perfect clustering and non-block-fixed interference).

Suppose Assumption 10 holds and the graph is perfectly clustered such that

Assume . Then

(i) If and , or and , the optimal assignment vector is for all .

(ii) If and , or and , the optimal assignment vector is

Appendix C Analysis for Linear Interference Model

C.1 Notation for Linear Interference Model

We define the interference coefficient from unit to unit by

such that the potential outcome of unit under treatment in a linear interference model can be expressed as

| (14) |

The corresponding difference-in-means estimator is therefore

| (15) |

where

are the weighted sum of potential outcomes coefficients of unit and the aggregated interference coefficients of the neighbors of correspondingly.

Note that is asymmetric in the sense that for . One can symmetrize by defining . In addition, we define the clustered aggregated interference coefficients by

The difference-in-means estimator in (15) can be rewritten to

| (16) |

so that the quadratic coefficients of is now symmetrized.

C.2 Proof of Proposition 6

When all units are treated, the observed outcome of unit is . In opposite, when all units are untreated, the observed outcome of unit is . Therefore, the total treatment effect for unit is . The average total treatment effect is hence , where and are population averages.

C.3 Proof of Theorem 7

Consider the expectation of the difference-in-means estimator under an observed treatment proportion vector . In additional to the idiosyncratic noise , the randomness also comes from the completely randomization of given for all .

According to the notation in (15), the conditional expectation is

| (17) |

Notice that under the permutation of , for all and

Then we have from (17),

where we utilize the fact that

C.4 Proof of Corollary 8

Theorem 7 reveals that the bias of the is . Since the dependence of bias on is linear, it suffices to provide lower and upper bound for when is fixed. On the one hand, the lower bound of is obviously zero, attained when for all . On the other hand, is bounded above by because for all . The upper bound is attained when since for all . Depending on the sign of , the minimal bias is achieved when takes the lower bound or upper bound. The corollary now is straightforward.

C.5 Proof of Theorem 9

By Eve’s law (or the law of total variance), the total variance of the difference-in-means estimator is decomposed to

The two terms on the right hand side are given by the following two lemmas.

Lemma 22.

The variance of the conditional expectation of difference-in-means estimator is given by

where , and , and are the second, third and fourth central moments of .

Lemma 23.

The conditional variance of the difference-in-means estimator is

where , and

Its expectation is

where .

Proofs of above lemmas are deferred to later sub-sections.

C.6 Proof of Corollary 12

We start from the explicit forms for the coefficients given in Section C.5 and do not assume the block-fixed effect assumption yet. With Assumptions 10(a) and 10(b), the sum of symmetrized interference coefficient can be bounded above by

where and are the constants in Assumptions 10.

Therefore, the terms involving summations of in is of order , which is negligible.

Next, we simplify . Recall that

From Assumption 10(c) and 10(d), we have

and

Then, we have

where .

Noticing that , the right hand side of above formula is negligible.

Simplify, for , we get

By plugging above simplifications, we have the reduced coefficients as follows (high order terms are not displayed).

Furthermore, if we assume the interference effect is block-fixed, all and vanish, which gives Coroallary 12.

C.7 Proof of Proposition 13

Within the distribution family , we have the objective function , where the third moment disappears. Suppose and define for . The support for is . Observe that

Noticing that is linear in when is fixed, we consider optimizing first. Depending on the sign of , it suffices to provide the lower and upper bound for . On the one hand, by Jensen’s inequality, we have , attained when for all . On the other hand, observe that

where the upper bound is attained when for all .

Specifically, if , the optimal allocation of is that

In this case, .

If , the optimal allocation of is that

In this case, .

When , either is optimal. The rest is to optimize as in a quadratic function.

C.8 Proof of Examples 14, 20 and 21

We proof Example 14 here and leave Examples 20 and 21 for the readers as they follow the same procedure. When the clustering is perfect and the interference is block-fixed, we adopt the result from Corollary 12 such that the coefficients are

In this case, we have and it falls to the first case in Proposition 13. Since the quadratic optimization of is simply a linear optimization. When , needs to be minimized. The correspnding case is all are at , resulting zero variance and zero four moment. When , needs to be maximized at , corresponding to a two-point distribution for with half points at and the other half at .

C.9 Proof of Lemma 22

We first rewrite the conditional expectation of in (17) in terms of the symmetrized interference coefficients such that

where

The conditional expectation above is now a quadratic function of . Its variance is given by

| (18) |

For , we have

where, in this proof, we use to denote and use to denote -th central moment of .

The first term in (18) is now

where denotes the sample variance of .

For , we define the following excessive covariance.

The above covariance are expressed in accordance with the inclusion-exclusion principle. The excessive covariance in addition to the preceding cases are presented. Therefore, the second term in (18) is now

Similarly, for , we have the following excess covariance.

Therefore, by the inclusion-exclusion principle, the third term in (18) is

Finally, by substituting the results back to (18), we have

C.10 Proof of Lemma 23

We start from the difference-in-means estimator

where . Its conditional variance is therefore,

We now calculate the three terms in above formula.

Term 1

Since for different cluster memberships of and , we have

then

Term 2

We consider the following cases for covaraince .

-Case 2-a

When , we have

The subtotal is

-Case 2-b

When and , we have

The subtotal is

where .

-Case 2-c

When , we have

The subtotal is

-Case 2-d

When and , we have

The subtotal is

By summing up to we have

where .

Term 3

We consider the following cases for covariance .

-Case 3-a

When and but , we have

The subtotal is

-Case 3-b

When and but , we have

The subtotal is

-Case 3-c

When and , we have

The subtotal is

-Case 3-d

When , and , we have

The subtotal is

-Case 3-e

When , , we have

The subtotal is

-Case 3-f

When , , and , we have

The subtotal is

-Case 3-g

When , we have

The subtotal is

-Case 3-h

When , , we have

The subtotal is

-Case 3-i

When , , we have

The subtotal is

-Case 3-j

When , , and , we have

The subtotal is

By summing up to , we have

where , and is the mean squared interaction defined by

for any matrix .

Finally, we have the conditional variance of the difference-in-means estimator

| (19) | ||||

| (20) |

with an relative error of order .

Next, we derive the expectation of (20) under the permutation of . Notice that depends on such that

Hence the first term in (20) is

The expectation of above equation involves higher moments of . Hence we denote the expectation terms as follows. For ,

Here -terms denotes the excessive expectation compared to a more general case.

Then we have

where we define

For the second term in (20), we have

By combining terms together, we have

The result is up to a relative error of .

Appendix D Analysis on Random Graph Extension

D.1 Proof of Proposition 15

For Assumption 10(b), let be an unit in . Then , where for , each is a Bernoulli random variable with probability . By Bernstein’s inequality, we have for ,

| (21) |

If we plug in , we have

Take the union bound over all units, we have

Therefore, one can choose with to control the probability that Assumption 10(b) is violated below . If , one can choose .

For Assumption 10(c), is a natural edge forming probability for . Similar to (21), we have the probability for the edges between unit and cluster to violate Assumption 10(c) as

which gives the union bound

Hence, as long as one choose , Assumption 10(c) is satisfied with probability at least . One such choice that does not depend on is .

Assumption 10(d) can be done in a very similar way by observing that , where is the averaged function value in cluster . Again, by Bernstein’s inequality, we have

which yields a union bound for the probability that Assumption 10(d) is not satisfied as . As long as , Assumption 10(d) is satisfied with probability at least . One can choose to remove dependence on .

Appendix E Analysis on the Stratified Estimator

E.1 Presentation of Initial Results

Recall the definition of the stratified estimator . Let be the total number of units in cluster and be the number of units assigned to treatment in that cluster. Let be a vector of positive coefficients, usually chosen to sum to , we define the stratified estimator as

In general, we recommend choosing , as evidenced by the following result on the bias of the stratified estimator under the stable treatment value assumption:

Proposition 24.

Assume that the standard unit treatment value assumption holds. The conditional expectation of the stratified estimator is

| (22) |

If , then the stratified estimator is unbiased for the total treatment effect, conditionally on the assignment of treatment proportions to clusters. The same holds true in expectation over a randomized saturation assignment.

A proof can be found in the following subsections. Similarly, the variance has an easily interpretable closed-form under the standard unit treatment value assumption. Recall , , and .

Proposition 25.

Assume that the stable unit value assumption holds. The variance of the stratified estimator under a randomized saturation design is

| (23) |

where is the harmonic mean of and is the harmonic mean of . Constrained to maintain , the stratified completely randomized design with minimizes the variance of the stratified estimator in Eq. 23, which is then equal to .

A proof can be found in the following subsections. In contrast to the variance of the difference-in-means estimator , which is linear in the variance of the treatment-proportions vector (cf. Prop 4), the variance of the stratified estimator depends on the variance of the treatment-proportions vector only through the inverse of the harmonic mean of , as stated in Proposition 25. Since any mean-preserving spread decreases the harmonic mean [Mitchell, 2004], when holding constant, any increase in the variance of the treatment-proportions vector increases the variance of the stratified estimator under the stable unit treatment value assumption.

We can also express the bias of the stratified estimator under the linear interference model of Equation 3. Recall that is the proportion of a unit’s neighborhood that also belongs to its cluster, averaged over all units.

Proposition 26.

Under the linear model of interference in Eq. 3, the expectation of the stratified estimator conditioned on the assignment of clusters to treatment-proportions is:

If the interference effects are constant, then the formula becomes .