[1]\fnmShunan \surYao

[1]\orgdivDepartment of Mathematics, \orgnameUniversity of Southern California, \orgaddress\street3620 S. Vermont Ave, \cityLos Angeles, \postcode90007, \stateCalifornia, \countryUSA

Median of Means Principle for Bayesian Inference

Abstract

The topic of robustness is experiencing a resurgence of interest in the statistical and machine learning communities. In particular, robust algorithms making use of the so-called median of means estimator were shown to satisfy strong performance guarantees for many problems, including estimation of the mean, covariance structure as well as linear regression. In this work, we propose an extension of the median of means principle to the Bayesian framework, leading to the notion of the robust posterior distribution. In particular, we (a) quantify robustness of this posterior to outliers, (b) show that it satisfies a version of the Bernstein-von Mises theorem that connects Bayesian credible sets to the traditional confidence intervals, and (c) demonstrate that our approach performs well in applications.

keywords:

Robustness, Bayesian inference, posterior distribution, median of means, Bernstein-von Mises theorem1 Introduction.

00footnotetext: Authors gratefully acknowledge support by the National Science Foundation grants DMS CAREER-2045068 and CIF-1908905.Modern statistical and machine learning algorithms typically operate under limited human supervision, therefore robustness - the ability of algorithms to properly handle atypical or corrupted inputs - is an important and desirable property. Robustness of the most basic algorithms, such as estimation of the mean and covariance structure that serve as “building blocks” of more complex methods, have received significant attention in the mathematical statistics and theoretical computer science communities; the survey papers by Lugosi and Mendelson (2019a); Diakonikolas and Kane (2019) provide excellent overview of the recent contributions of these topics as well as applications to a variety of statistical problems. The key defining characteristics of modern robust methods are (a) their ability to operate under minimal model assumptions; (b) ability to handle high-dimensional inputs and (c) computational tractability. However, many algorithms that provably admit strong theoretical guarantees are not computationally efficient. In this work, we rely on a class of methods that can be broadly viewed as risk minimization: the output (or the solution) provided by such methods is always a minimizer of the properly defined risk, or cost function. For example, estimation of the mean of a square-integrable random variable can be viewed as minimization of the risk over . Since the risk involves the expectation with respect to the unknown distribution, its exact computation is impossible. Instead, risk minimization methods introduce a robust data-dependent “proxy” of the risk function, and attempt to minimize it instead. The robust empirical risk minimization method by Brownlees et al (2015), the “median of means tournaments” developed by Lugosi and Mendelson (2019b) and a closely related method due to Lecué and Lerasle (2020) are the prominent examples of this approach. Unfortunately, the resulting problems are computationally hard as they typically involve minimization of general non-convex functions. In this paper, we propose a Bayesian analogue of robust empirical risk minimization that allows one to replace non-convex loss minimization by sampling that can be readily handled by many existing MCMC algorithms. Moreover, we show that for the parametric models, our approach preserves one of the key benefits of Bayesian methods - the “built-in” quantification of uncertainty - and leads to asymptotically valid confidence sets. At the core of our method is a version of the median of means principle, and our results demonstrate its potential beyond the widely studied applications in the statistical learning framework.

Next, we introduce the mathematical framework used throughout the text. Let be a random variable with values in some measurable space and unknown distribution . Suppose that are the training data – N i.i.d. copies of . We assume that the sample has been modified in the following way: an “adversary” replaces a random set of observations by arbitrary values, possibly depending on the sample. Only the corrupted values are observed.

Suppose that has a density with respect to a -finite measure (for instance, the Lebesgue measure or the counting measure). We will assume that belongs to a family of density functions , where is a compact subset, and that for some unknown in the interior of . We will also make the necessary identifiability assumption stating that is the unique minimizer of over , where is the negative log-likelihood, that is, . Clearly, an approach based on minimizing the classical empirical risk of leads to familiar maximum likelihood estimator (MLE) . At the same time, the main object of interest in the Bayesian approach is the posterior distribution, which is a random probability measure on defined via

| (1) |

for all measurable sets . Here, is the prior distribution with density with respect to the Lebesgue measure. The following result, known as the Bernstein-von Mises (BvM) theorem that is due to L. Le Cam in its present form (see the book by Van der Vaart (2000) for its proof and discussion), is one of the main bridges connecting the frequentist and Bayesian approaches.

Theorem (Bernstein-von Mises).

Under the appropriate regularity assumptions on the family ,

where is the MLE, stands for the total variation distance, is the Fisher Information matrix and denotes convergence in probability (with respect to the distribution of the sample ).

In essence, BvM theorem implies that for a given the credible set, i.e. the set of posterior probability, coincides asymptotically with the set of probability under the distribution , which is well-known to be an asymptotically valid “frequentist” confidence interval for , again under minimal regularity assumptions111For instance, these are rigorously defined in the book by Van der Vaart (2000).. It is well known however that the standard posterior distribution is, in general, not robust: if the sample contains even one corrupted observation (referred to as an “outlier” in what follows), the posterior distribution can concentrate arbitrarily far from the true parameter that defines the data-generating distribution. A concrete scenario showcasing this fact is given in Baraud et al (2020); another illustration is presented below in example 2). The approach proposed below addresses this drawback: the resulting posterior distribution (a) admits natural MCMC-type sampling algorithms and (b) satisfies quantifiable robustness guarantees as well as a version of the Bernstein-von Mises theorem that is similar to its classical counterpart in the outlier-free setting. In particular, the credible sets associate with the proposed posterior are asymptotically valid confidence intervals that are also robust to sample contamination.

Many existing works are devoted to robustness of Bayesian methods, and we attempt to give a (necessarily limited) overview of the state of the art. The papers by Doksum and Lo (1990) and Hoff (2007) investigated approaches based on “conditioning on partial information,” while a more recent work by Miller and Dunson (2015) introduced the notion of the “coarsened” posterior; however, non-asymptotic behavior of these methods in the presence of outliers has not been explicitly addressed. Another line of work on Bayesian robustness models contamination by either imposing heavy-tailed likelihoods, like the Student’s t-distribution, on the outliers (Svensen and Bishop, 2005), or by attempting to identify and remove them, as was done by Bayarri and Berger (1994).

As mentioned before, the approach followed in this work relies on a version of the median of means (MOM) principle to construct a robust proxy for the log-likelihood of the data and, consequently, a robust version of the posterior distribution. The original MOM estimator was proposed by Nemirovsky and Yudin (1983) and later, independently, by Jerrum et al (1986); Alon et al (1999). Its versions and extensions were studied more recently by many authors including Lerasle and Oliveira (2011); Lugosi and Mendelson (2019b); Lecué and Lerasle (2020); Minsker (2020); we refer the reader to the surveys mentioned in the introduction for a more detailed literature overview. The idea of replacing the empirical log-likelihood of the data by its robust proxy appeared previously the framework of general Bayesian updating described by Bissiri et al (2016), where, given the data and the prior, the posterior is viewed as the distribution minimizing the loss expressed as the sum of a “loss-to-data” term and a “loss-to-prior” term. In this framework, Jewson et al (2018) adopted different types of f-divergences (such as the one corresponding to the Hellinger distance), to the loss-to-prior term to obtain a robust analogue of the posterior; this approach has been investigated further in Knoblauch et al (2019). Asymptotic behavior of related types of posteriors was studied by Miller (2021), though the framework in that paper is not limited to parametric models while imposing more restrictive regularity conditions than the ones required in the present work. Various extensions for this class of algorithms were suggested, among others, by Hooker and Vidyashankar (2014, based on so-called “robust disparities”), Ghosh and Basu (2016, based on -density power divergence), Nakagawa and Hashimoto (2020), Bhattacharya et al (2019), and Matsubara et al (2021, who used kernel Stein discrepancies in place of the log-likelihood). Yet another interesting idea for replacing the log-likelihood by its robust alternative, yielding the so-called “-Bayes” posterior, was proposed and rigorously investigated by Baraud et al (2020). However, sampling from the -posterior appears to be computationally difficult, while most of the other works mentioned above impose strict regularity conditions on the model that, unlike our results, exclude popular examples like the Laplace likelihood.

1.1 Proposed approach.

Let be an arbitrary fixed point in the relative interior of . Observe that the density of the posterior distribution is proportional to ; indeed, this is evident from equation 1 once the numerator and the denominator are divided by . The key idea is to replace the average by its robust proxy denoted 222Since is fixed, we will suppress the dependence on in the notation for brevity. and defined formally in equation (3) below, which gives rise to the robust posterior distribution

| (2) |

defined for all measurable sets .

Remark 1.

While it is possible to work with the log-likelihood directly, it is often easier and more natural to deal with the increments . For instance, in the Gaussian regression model with , with likelihood and , which is more manageable than itself: in particular, the increments do not include the terms involving .

Note that the density of is maximized for . For instance, if the prior is the uniform distribution over , then corresponds exactly to the robust risk minimization problem which, as we’ve previously mentioned, is hard due to non-convexity of the function . At the same time, sampling from is possible, making the “maximum a posteriori” (MAP) estimator as well as the credible sets associated with accessible. The robust risk estimator employed in this work is based on the ideas related to the median of means principle. The original MOM estimator was proposed by Nemirovsky and Yudin (1983) and later by Jerrum et al (1986); Alon et al (1999). Its versions and extensions were studied more recently by many researchers including Audibert et al (2011); Lerasle and Oliveira (2011); Brownlees et al (2015); Lugosi and Mendelson (2019b); Lecué and Lerasle (2020); Minsker (2020). Let be a positive integer and be disjoint subsets (“blocks”) of of equal cardinality , . For every , define the block average

which is the (increment of) empirical log-likelihood corresponding to the subsample indexed by . Next, let be a convex, even, strictly increasing smooth function with bounded first derivative; for instance, a smooth (e.g. convolved with an infinitely differentiable kernel) version of the Huber’s loss is an example of such function. Furthermore, let be a non-decreasing sequence such that and . Finally, define

| (3) |

which is clearly a solution to the convex optimization problem. Robustness and non-asymptotic performance of can be quantified as follows. Let , and ; then for all , and number of outliers such that for some absolute constant ,

| (4) |

with probability at least , where as . Put simply, under very mild assumptions on , admits sub-Gaussian deviations around , moreover, it can absorb the number of outliers that is of order . We refer the reader to Theorem 3.1 in Minsker (2018) for a uniform over version of this bound as well as more details. We end this section with two technical remarks.

Remark 2.

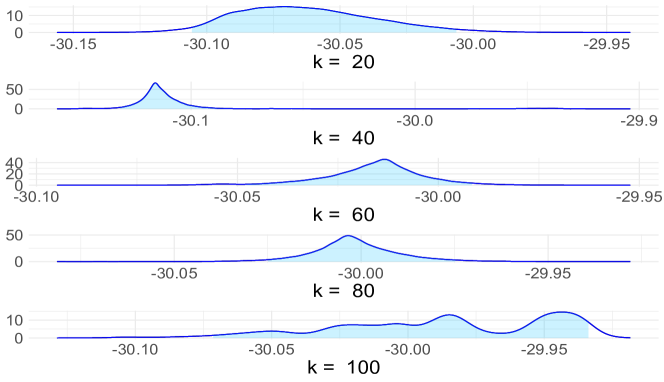

The classical MOM estimator corresponds to the choice which is not smooth but is scale-invariant, in a sense that the resulting estimator does not depend on the choice of . While the latter property is often desirable, we conjecture that the posterior distribution based on such “classical” MOM estimator does not satisfy the Bernstein-von Mises theorem, and that smoothness of is important beyond being just a technical assumption. This, perhaps surprising, conjecture is so far only supported by our simulation results explained in Example 1.

Example 1.

Let be i.i.d. with normal distribution , and the prior distribution for is . Furthermore, let . We sample from the robust posterior distribution for the values of and . The resulting plots are presented in Figure 1. The key observation is that the posterior distributions are often multimodal and skewed, unlike the expected “bell shape.”

Remark 3.

Let us mention that the posterior distribution is a valid probability measure, meaning that . By the definition at display (2), it suffices to show the denominator, , is finite. Indeed, note that for all where , hence

Therefore, a sufficient condition for being finite is a.s. This is guaranteed by the fact that under mild regularity assumptions, for any , , - almost surely.

2 Main results.

We are ready to state the main theoretical results for the robust posterior distribution . First, we will state them in a way that avoids technical assumptions which can be found in the latter part of the section. Recall that where , and let and . The following theorem characterizes robustness properties of the mode of the posterior defined as

| (5) |

Theorem 1.

Under the appropriate regularity conditions on the function , prior and the family , with probability at least ,

as long as for some absolute constants . Here, is a function that converges to as .

In particular, stated inequality implies that as long as the number of blocks containing outliers, whose cardinality is , is not too large, the effect of these outliers on the squared estimation error is limited, regardless of their nature and magnitude. While the fact that the mode of is a robust estimator of is encouraging, one has to address the ability of the method to quantify uncertainty to fully justify the title of the “posterior distribution.” This is exactly the content of the following result. Let ; it can be viewed as a mode of the posterior distribution corresponding to the uniform prior on .

Theorem 2.

Assume the outlier-free framework. Under appropriate regularity conditions on the prior and the family ,

Moreover, .

The message of this result is that in the ideal, outlier-free scenario, the robust posterior distribution asymptotically behaves like the usual posterior distribution , and that the credible sets associated with it are asymptotically valid confidence intervals. Technical requirements include a condition on the growth of the number of blocks of data, namely for some defined below. The main novelty here is the first, “BvM part” of the theorem, while asymptotic normality of has been previously established by Minsker (2020).

We finish this section by listing and discussing the complete list of regularity conditions that are required for the stated results to hold. The norm refers to the standard Euclidean norm everywhere below.

Assumption 1.

The function is convex, even, and such that

-

(i)

for and for .

-

(ii)

is nondecreasing on ;

-

(iii)

is bounded and Lipschitz continuous.

One example of such is the smoothed Huber’s loss: let

Moreover, set . Then , where denotes the convolution, satisfies assumption 1. Condition (iii) on the higher-order derivatives is technical in nature and can likely be avoided at least in some examples; in numerical simulations, we did not notice the difference between results based on the usual Huber’s loss and its smooth version. Next assumption is a standard requirement related to the local convexity of the loss function at its global minimum .

Assumption 2.

The Hessian exists and is strictly positive definite.

In particular, this assumption ensures that in a sufficiently small neighborhood of , for some constants . The following two conditions allow one to control the “complexity” of the class .

Assumption 3.

For every , the map is differentiable at for -almost all (where the exceptional set of measure can depend on ), with derivative . Moreover, , the envelope function of the class satisfies for some and a sufficiently small .

An immediate implication of this assumption is the fact that the function is locally Lipschitz. It other words, for any , there exists a ball of radius such that for all . In particular, this condition suffices to prove consistency of the estimator .

The following condition is related to the modulus of continuity of the empirical process indexed by the gradients . It is similar to the typical assumptions required for the asymptotic normality of the MLE, such as Theorem 5.23 in the book by Van der Vaart (2000). Define

where is the empirical distribution by .

Assumption 4.

The following relation holds:

Moreover, the number of blocks satisfies as .

Limitation on the growth of is needed to ensure that the bias of the estimator is of order , a fact that we rely on in the proof of Theorem 2. Finally, we state a mild requirement imposed on the prior distribution; it is only slightly more restrictive than its counterpart in the classical BvM theorem (for example, Theorem 10.1 in the book by Van der Vaart (2000)).

Assumption 5.

The density of the prior distribution is positive and bounded on , and is continuous on the set for some positive constant .

Remark 4.

Most commonly used families of distributions satisfy assumptions 2-4. For example, this is easy to check for the normal, Laplace or Poisson families in the location model where . Other examples covered by our assumptions include the linear regression with Gaussian or Laplace-distributed noise. The main work is usually required to verify assumption 4; it relies on the standard tools for the bounds on empirical processes for classes that are Lipschitz in parameter or have finite Vapnik-Chervonenkis dimension. Examples can be found in the books by Van der Vaart (2000) and Van Der Vaart et al (1996).

3 Numerical examples and applications.

We will illustrate our theoretical findings by presenting numerical examples below. The loss function that we use is Huber’s loss defined before. While, strictly speaking, it does not satisfy the smoothness requirements, we found that it did not make a difference in our simulations. Algorithm for sampling from the posterior distributions was based on the “No-U-Turn sampler” variant of Hamiltonian Monte Carlo method (Hoffman and Gelman, 2014). Robust estimator of the log-likelihood are approximated via the gradient descent algorithm at every . Our first example demonstrates that using Huber’s loss in the framework of Example 1 is enough for BvM theorem to hold.

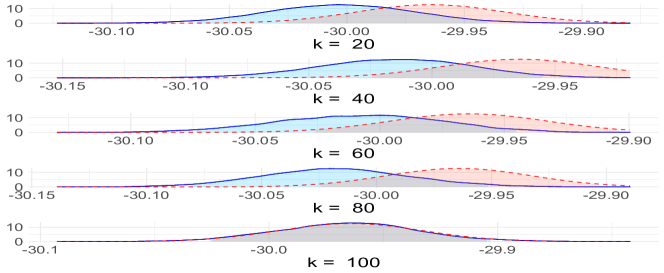

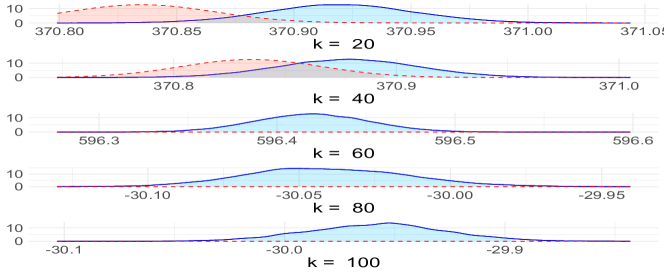

Example 2.

We consider two scenarios: in the first one, the data are i.i.d. copies of random variables. In the second scenario, data are generated in the same way except that randomly chosen observations are replaced with i.i.d. copies of distributed random variables. Results are presented in figures 3 and 3, where the usual posterior distribution is plotted as well for comparison purposes. The main takeaway from this simple example is that the proposed method behaves as expected: as long as the number of blocks is large enough, robust posterior distribution concentrates most of its “mass” near the true value of the unknown parameter, while the usual posterior distribution is negatively affected by the outliers. At the same time, in the outlier-free regime, both posteriors perform similarly.

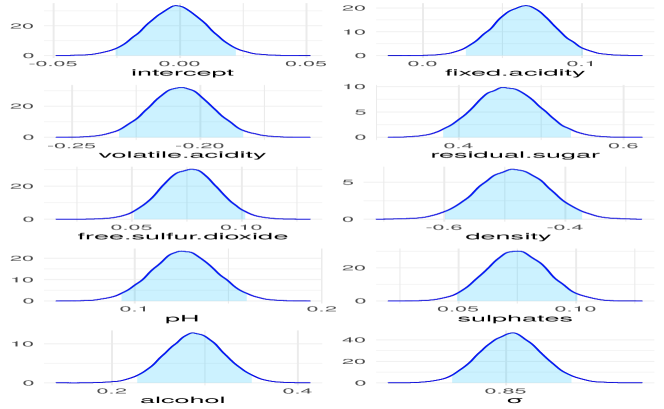

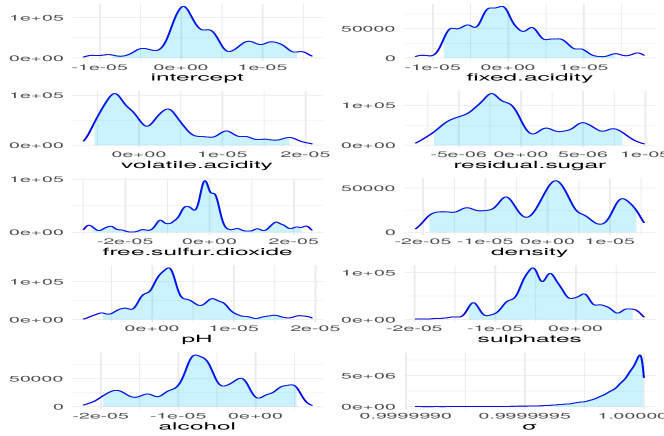

Example 3.

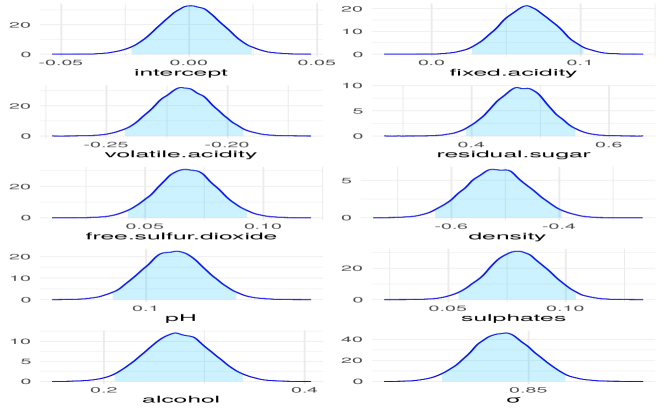

In this example, we consider a non-synthetic dataset in the linear regression framework. The dataset in question was provided by Cortez et al (2009) and describes the qualities of different samples of red and white wine. It contains “subjective” features such as fixed acidity, pH, alcohol, etc., and one “objective” feature, the scoring of wine quality; white wine samples are selected to perform the linear regression where the objective feature is the response and the subjective features are the regressors. It is assumed that the data is sampled from the model

where is the intercept, is the response, are the chosen regressors (see detailed variable names in Table 1) along with the corresponding coefficients , and is the random error with distribution. Here we remark that, for simplicity only out of “subjective” features are selected such that this model agrees with the OLS linear regression model generated by best subset selection with minimization of BIC. In the second experiment, randomly chosen response variables are replaced with random outliers. In both cases, the priors for are set to be for every , and the prior for is the uniform distribution on . The block size is set to be and the number of blocks is . The MAP estimates of ’s and , as well as the two end points of the credible intervals are reported in Table 1. These plots yet again demonstrate that the posterior , unlike its standard version, shows stable behavior when the input data are corrupted.

| variable name | |

|---|---|

| intercept | |

| fixed.acidity | |

| volatile.acidity | |

| residual.sugar | |

| free.sulfur.dioxide | |

| density | |

| pH | |

| sulphates | |

| alcohol | |

4 Discussion.

The proposed extension of the median of means principle to Bayesian inference yields a version of the posterior distribution possessing several desirable characteristics, such as (a) robustness, (b) valid asymptotic coverage and (c) computational tractability. In addition, the mode of this posterior distribution serves as a robust alternative to the maximum likelihood estimator. The computational cost of our method is higher compared to the usual posterior distribution as we need to solve a one-dimensional convex optimization problem to estimate the expected log-likelihood, however, the method is still practical and, unlike many existing alternatives with similar theoretical properties, can be implemented with many off the shelf sampling packages. As with many MOM-based methods, the main “tuning parameter” is the number of blocks : while larger increases robustness, smaller values reduce the bias in the estimation of the likelihood. In many examples however, this bias is far from the worst case scenario, and we observed that in our simulations, the method behaves well even when the size of each “block” is small. As a practical rule of a thumb, we recommend setting if no prior information about the number of outliers is available.

Now, let us discuss the drawbacks. First of all, the requirement for to be compact is quite restrictive, and is typically necessary to ensure that the quantity appearing in our bounds is finite. This root of this requirement is related to the fact that , viewed as an estimator of the mean, is not scale-invariant. At the same time, compactness assumption is satisfied if one has access to some preliminary, “low-resolution” proxy of such that for some, possibly large, . Second, our method is currently tailored only for the case of i.i.d. data and the parametric models, which is the most natural setup that is natural for demonstrating the “proof of concept.” At the same time, it would be interesting to obtain practical and theoretically sound extensions that are applicable in more challenging frameworks.

5 Proofs.

This section explains the key steps behind the proofs of our mains results. The complete argument leading to Theorem 2 is rather long and technical. Here, we will outline the main ideas of the proof and the reduction steps that are needed to transform the problem into an easier one, while the missing details are included in the supplementary material.

6 Proof of Theorem 1.

In view of assumption 2, whenever is sufficiently small. Hence, if we show that satisfies this requirement, we would only need to estimate . To this end, denote , and observe that

If , the last term above can be dropped without changing the inequality. On the other hand, is bounded and , , whence the last term is at most . Given , assumption 2 implies that there exists such that . Let be large enough so that , whence . It follows from Lemma 2 in Minsker (2020) (see also Theorem 3.1 in Minsker (2018)) that under the stated assumptions,

with probability at least as long as are large enough and is sufficiently small. Here, is a function that tends to as . This shows consistency of . Next, we will provide the required explicit upper bound on . As we’ve demonstrated above, it suffices to find an upper bound for . We will apply the result of Theorem 2.1 in Mathieu and Minsker (2021) to deduce that for large enough, with probability at least . To see this, it suffices to notice that in view of Lemma 6 in the supplementary material, where may depend on and the class .

6.1 Proof of Theorem 2 (sketch).

The high-level idea of the proof is fairly standard and consists in obtaining a proper (quadratic) local approximation of in the neighborhood of , coupled with careful control of the remainder terms. However, the difficulty that one has to overcome is the fact that, unlike the empirical log-likelihood, the robust estimator is not linear in . To do so, we develop the technical tools that are based on the existing results in the papers by Minsker (2020, 2018).

In view of the well-known property of the total variation distance,

Next, let us introduce the new variable , multiply the numerator and the denominator on the posterior by , and set

| (6) |

and . The total variation distance can then be equivalently written as . The function can be viewed a pdf of a new probability measure . Thus it suffices to show that

Since is the unique minimizer of , . Next, define ; it is twice differentiable since both and are. It is shown in the proof of Lemma 4 in Minsker (2020) that with high probability. Therefore, a unique mapping exists around the neighborhood of and so do and . Denote . The following result, proven in the supplementary material, essentially establishes stochastic differentiability of at .

Lemma 1.

The following relation holds:

In view of the lemma, the total variation distance between the normal laws and converges to in probability. Hence one only needs to show that . Let

| (7) |

and observe that as long as one can establish that

| (8) |

we will be able to conclude that

so that . This further implies that

and the desired result would follow. Therefore, it suffices to establish that relation (8) holds. Moreover, since outside of a compact set , it is equivalent to showing that

| (9) |

where . Note that

An argument behind the proof of Lemma 1 yields (again, we present the missing details in the technical supplement) the following representation for defined in (6):

| (10) |

Let us divide into 3 regions: , and where is a sufficiently small positive number and is a sufficiently large so that contains . Finally, is chosen such that , and that satisfies an additional growth condition specified in Lemma 8 in the supplement. The remainder of the proof is technical and is devoted to proving that each part of the integral (9) corresponding to converges to . Details are presented in the supplementary material.

References

- \bibcommenthead

- Alon et al (1999) Alon N, Matias Y, Szegedy M (1999) The space complexity of approximating the frequency moments. Journal of Computer and system sciences 58(1):137–147

- Audibert et al (2011) Audibert JY, Catoni O, et al (2011) Robust linear least squares regression. The Annals of Statistics 39(5):2766–2794

- Baraud et al (2020) Baraud Y, Birgé L, et al (2020) Robust Bayes-like estimation: Rho-Bayes estimation. Annals of Statistics 48(6):3699–3720

- Bayarri and Berger (1994) Bayarri MJ, Berger JO (1994) Robust Bayesian bounds for outlier detection. Recent Advances in Statistics and Probability pp 175–190

- Bhattacharya et al (2019) Bhattacharya A, Pati D, Yang Y (2019) Bayesian fractional posteriors. The Annals of Statistics 47(1):39–66

- Bissiri et al (2016) Bissiri PG, Holmes CC, Walker SG (2016) A general framework for updating belief distributions. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 78(5):1103–1130

- Brownlees et al (2015) Brownlees C, Joly E, Lugosi G (2015) Empirical risk minimization for heavy-tailed losses. Annals of Statistics 43(6):2507–2536

- Cortez et al (2009) Cortez P, Cerdeira A, Almeida F, et al (2009) Modeling wine preferences by data mining from physicochemical properties. Decision support systems 47(4):547–553

- Diakonikolas and Kane (2019) Diakonikolas I, Kane DM (2019) Recent advances in algorithmic high-dimensional robust statistics. arXiv preprint arXiv:191105911

- Doksum and Lo (1990) Doksum KA, Lo AY (1990) Consistent and robust Bayes procedures for location based on partial information. The Annals of Statistics pp 443–453

- Ghosh and Basu (2016) Ghosh A, Basu A (2016) Robust Bayes estimation using the density power divergence. Annals of the Institute of Statistical Mathematics 68(2):413–437

- Hoff (2007) Hoff PD (2007) Extending the rank likelihood for semiparametric copula estimation. The Annals of Applied Statistics pp 265–283

- Hoffman and Gelman (2014) Hoffman MD, Gelman A (2014) The No-U-Turn sampler: adaptively setting path lengths in Hamiltonian monte carlo. J Mach Learn Res 15(1):1593–1623

- Hooker and Vidyashankar (2014) Hooker G, Vidyashankar AN (2014) Bayesian model robustness via disparities. Test 23(3):556–584

- Jerrum et al (1986) Jerrum MR, Valiant LG, Vazirani VV (1986) Random generation of combinatorial structures from a uniform distribution. Theoretical computer science 43:169–188

- Jewson et al (2018) Jewson J, Smith JQ, Holmes C (2018) Principles of Bayesian inference using general divergence criteria. Entropy 20(6):442

- Knoblauch et al (2019) Knoblauch J, Jewson J, Damoulas T (2019) Generalized variational inference: Three arguments for deriving new posteriors. arXiv preprint arXiv:190402063

- Lecué and Lerasle (2020) Lecué G, Lerasle M (2020) Robust machine learning by median-of-means: theory and practice. Annals of Statistics 48(2):906–931

- Lerasle and Oliveira (2011) Lerasle M, Oliveira RI (2011) Robust empirical mean estimators. arXiv preprint arXiv:11123914

- Lugosi and Mendelson (2019a) Lugosi G, Mendelson S (2019a) Mean estimation and regression under heavy-tailed distributions: A survey. Foundations of Computational Mathematics 19(5):1145–1190

- Lugosi and Mendelson (2019b) Lugosi G, Mendelson S (2019b) Risk minimization by median-of-means tournaments. Journal of the European Mathematical Society 22(3):925–965

- Mathieu and Minsker (2021) Mathieu T, Minsker S (2021) Excess risk bounds in robust empirical risk minimization. Information and Inference: A Journal of the IMA

- Matsubara et al (2021) Matsubara T, Knoblauch J, Briol FX, et al (2021) Robust generalised Bayesian inference for intractable likelihoods. arXiv preprint arXiv:210407359

- Miller (2021) Miller JW (2021) Asymptotic normality, concentration, and coverage of generalized posteriors. Journal of Machine Learning Research 22(168):1–53

- Miller and Dunson (2015) Miller JW, Dunson DB (2015) Robust Bayesian inference via coarsening. arXiv preprint arXiv:150606101

- Minsker (2018) Minsker S (2018) Uniform bounds for robust mean estimators. arXiv preprint arXiv:181203523

- Minsker (2020) Minsker S (2020) Asymptotic normality of robust risk minimizers. arXiv preprint arXiv:200402328

- Nakagawa and Hashimoto (2020) Nakagawa T, Hashimoto S (2020) Robust Bayesian inference via -divergence. Communications in Statistics-Theory and Methods 49(2):343–360

- Nemirovsky and Yudin (1983) Nemirovsky AS, Yudin DB (1983) Problem complexity and method efficiency in optimization. Wiley-Interscience

- Svensen and Bishop (2005) Svensen M, Bishop CM (2005) Robust Bayesian mixture modelling. Neurocomputing 64:235–252

- Van der Vaart (2000) Van der Vaart AW (2000) Asymptotic statistics, vol 3. Cambridge university press

- Van Der Vaart et al (1996) Van Der Vaart AW, van der Vaart AW, van der Vaart A, et al (1996) Weak convergence and empirical processes: with applications to statistics. Springer Science & Business Media

Appendix A Preliminary results.

In this section, we introduce some of the technical tools that will be used in the proofs of our main results. Lemmas 2 - 5 stated below were established in Minsker (2020), and therefore will be given without the proofs. Let be a compact set, and define

The following lemma provides a high probability bound for that holds uniformly over .

Lemma 2.

Let be a class of functions mapping to , and assume that for some . Then there exist absolute constants and a function satisfying such that for all and satisfying

the following inequality holds with probability at least :

This lemma implies that as long as and ,

Next, Lemma 3 below establishes consistency of the estimator that is a necessary ingredient in the proof of the Bernstein-von Mises theorem.

Lemma 3.

in probability as .

The following lemma establishes the asymptotic equicontinuity of the process at (recall that the existence of at the neighborhood around has bee justified in the proof of Theorem 2).

Lemma 4.

For any ,

This result combined with Lemma 3 yields a useful corollary. Note that due to consistency of ,

| (11) |

On the other hand,

| (12) |

where . Note that for any ,

The first term converges to in probability by Lemma 4 the second term converges to in probability by Lemma 3. Therefore,

Under assumptions of the following Lemma 5, is asymptotically (multivariate) normal, therefore, . Moreover, is non-singular by Assumption 2. It follows that , and we conclude that

| (13) |

Lemma 5.

The following asymptotic relations hold:

The following lemma demonstrates that empirical processes indexed by classes that are Lipschitz in parameter (for example, satisfying assumption 3) are “well-behaved.” This fact is well-known but we outline the proof for reader’s convenience.

Lemma 6.

Let be a class of functions that is Lipschitz in parameter, meaning that . Moreover, assume that for some . Then

Proof: Symmetrization inequality yields that

As the process is sub-Gaussian conditionally on , its (conditional) -norms are equivalent to norm. Hence, Dudley’s entropy bound implies that

where , and is the diameter of with respect to the distance . As is Lipschitz in , we have that , implying that and

| (14) |

Therefore,

and

| (15) |

Next are three lemmas that we rely on in the proof of Theorem 2. Define

Lemma 7.

For any ,

where and are two functions such that for any satisfying ,

as .

Let where and note that . Then

| (16) |

The first integral equals . For the second integral, note that the reasoning similar to the one behind equation (11) yields that for any

where is a vector-valued function such that as . Therefore, for any

implying that

Denoting the last two terms and respectively, and combining the previous display with equation (16), we deduce that

Moreover,

Therefore, for such that , Furthermore,

and

Thus, which converges to as .

Lemma 8.

Proof: [Proof of Lemma 8.] Let be a sequence such that and . In view of Lemma 4,

where is given in Lemma 7. Moreover, let be a sequence such that , and

Lemma 7 implies that

Similarly, let be a sequence such that and . Lemma 7 yields that

Finally, let be the sequence such that , and

Then

Finally, take , and conclude using the triangle inequality.

Lemma 9.

Let be a sequence of random vectors that converges to weakly, where is a standard random vector of dimension and is a invertible matrix. Furthermore, let be a symmetric positive definite matrix and - a sequence of positive numbers converging to infinity. Then

Proof: [Proof of Lemma 9.] Note that

where is the smallest eigenvalue of . Let be an arbitrary positive constant and , then on the set ,

for any as . Note that , where is the smallest eigenvalue of . For an arbitrary , select such that . Then

with probability at least , thus the assertion holds.

Appendix B Proof of Theorem 2.

We begin by filling in the details omitted in the sketch given in Section 6.1. First, Lemma 1 is implied directly by display (13) and display (10) is given by Lemma 7. For the integral over the set , observe that

To estimate the first term, recall the definition of in display (7) and note that

Therefore, recalling that can be written as in display (10), we have that

hence

Here, by the continuity of while

by Lemma 8. Moreover, by the definition of (see equation (7)), the integral factor equals . Therefore, the first integral converges to in probability. For the second integral, observe that

by Assumption 5. Next, to estimate the integral over , note that

For the first term, consider again the representation of as

Since is a positive definite matrix, and, in view of Lemma 7,

with probability close to , for sufficiently small . Then

where and converges to weakly with and and being a -dimensional identity matrix respectively. Therefore, for any positive increasing sequence ,

It is easy to see that converges to in probability by Lemma 9. Then choosing such that

guarantees that the first term converges to . Meanwhile, the second term is with probability . Note that for any ,

is positive for large enough by tightness and converges to by weak convergence. Thus, for large enough, for any . Since and are symmetric and positive definite, so is . Note that for arbitrary , one can select a sufficiently large such that Therefore,

Thus, for large enough,

equals with probability at least for any , hence the above term converges to in probability. We have so far shown that converges to in probability. Another application of Lemma 9 implies that

which shows the integral over converges to in probability. For the final part, the integral over , observe again that

As before, the second integral converges to in probability by Lemma 9. The first integral can be further estimated as

On the compact set , attains a minimum positive value . Moreover,

By Lemma 2, the terms in the first and third pair of brackets converge to in probability. Thus,

with probability approaching 1. Therefore,

with probability approaching 1. This establishes the relation (8), and therefore completes the proof.