plain

Fast Simulation-Based Bayesian Estimation of Heterogeneous and Representative Agent Models using Normalizing Flow Neural Networks

Abstract

This paper proposes a simulation-based deep learning Bayesian procedure for the estimation of macroeconomic models. This approach is able to derive posteriors even when the likelihood function is not tractable. Because the likelihood is not needed for Bayesian estimation, filtering is also not needed. This allows Bayesian estimation of HANK models with upwards of 800 latent states as well as estimation of representative agent models that are solved with methods that don’t yield a likelihood–for example, projection and value function iteration approaches. I demonstrate the validity of the approach by estimating a 10 parameter HANK model solved via the Reiter method that generates 812 covariates per time step, where 810 are latent variables, showing this can handle a large latent space without model reduction. I also estimate the algorithm with an 11-parameter model solved via value function iteration, which cannot be estimated with Metropolis-Hastings or even conventional maximum likelihood estimators. In addition, I show the posteriors estimated on Smets-Wouters 2007 are higher quality and faster using simulation-based inference compared to Metropolis-Hastings. This approach helps address the computational expense of Metropolis-Hastings and allows solution methods which don’t yield a tractable likelihood to be estimated.

JEL Codes: E27, E37, E47, C45, C11, C15

Keywords: Neural Networks, Bayesian Inference, Dynamic Estimation, Simulation-Based Estimators

I. Introduction

There are significant barriers to Bayesian or maximum likelihood estimation (MLE) in many situations outside one standard approach of estimating after perturbation. In spite of this, Bayesian methods have advantages. They allow the use of informative priors, perhaps derived by microdata to guide estimation and provide distributional information on parameters. They give distributional insight on parameters. In the case of MLE, it efficiency advantages over alternatives like method of simulated moments and modeling advantages over maximum simulated likelihood.

Discussing the barriers, first, MH-MCMC estimation of Bayesian posteriors, particularly of slow state-of-the-art models, is computationally inefficient. For example, even in a small HANK model, the size of the latent state space could be in the thousands making a filtering likelihood approach to Bayesian estimation intractable. For this reason, most heterogenous agent models are calibrated (Liu and Plagborg-Møller, 2021), but if they are estimated in a likelihood manner, state space dimension reduction techniques are used at the expense of accuracy (Ahn et al., 2018). Second, many popular solution methods, like value function iteration or projection, don’t yield complementary likelihood functions so conventional methods using Metropolis-Hastings Markov Chain Monte Carlo (MH-MCMC) and MLE are off the table.

Discussing the first barrier: the problem with heterogeneous agent model estimation is that the Kalman filter is a computational bottleneck when the state space is too large. Since heterogeneous agent models often divide up one or more distribution state variable into many quantiles, the size of the latent state space could be in the 1000s. Since Kalman filtering’s computational complexity scales with matrix multiplication, filtering something that is approximately 20x larger than the 40 parameter latent space in Smets and Wouters (2007) model takes approximately 4500x more compute. This means the traditional MH-MCMC or even maximum likelihood combined with a filtering approach may become computationally intractable, even for small heterogeneous agent models. The approach I propose estimates the posterior from simulations only, allowing one to avoid filtering and the likelihood function in general. Thus, this approach can estimate models with almost unbounded latent state space size with small increases in computational cost.

Likewise, discussing the second barrier: conventional approaches have downsides if the solution method doesn’t yield a complementary likelihood function. If one cannot estimate via perturbation, Bayesian and MLE estimation cannot be done with conventional MH-MCMC or even MLE. Thus options with less attractive qualities are used. In this case, solved models are either calibrated, estimated via method of simulated moments (MSM), or estimated in a simulated maximum likelihood fashion. Each approach has its own drawbacks. Calibration is not an algorithmic approach so it lacks both rigour and quantification tools like standard errors. MSM is not efficient unless the global identification criterion is met, which is both unverifiable and unlikely. Adding in measurement error for maximum simulated likelihood makes it less realistic as practitioners often want to assume the error comes from economic shocks and not measurement. Additionally, none of these alternatives can handle incorporating posterior distributions or prior information.

I propose a method from machine learning that allows Bayesian and full information estimation of models without a likelihood function. This also addresses filtering computational bottlenecks since avoiding the likelihood function avoids the use of filtering. Since the approach is likelihood-free, one can Bayesian/MLE estimate models solved via projection and value function iteration. This includes non-analytic models with kinks that often require these solution approaches. This approach allows the estimation of heterogeneous agent models whose large latent state spaces make filtering intractable without dimension reduction, even when the likelihood is available. Although the method is more general, this paper focuses on the case of dynamic macroeconomic structural models in a Bayesian setting. Finding the mode of the posterior with a uniform prior allows one to derive MLE estimation from the Bayesian procedure as well. Econometrically, this approach extends Kaji, Manresa and Pouliot (2020) to the Bayesian setting and when there is a time series component that is not iid.

I next will discuss briefly the Sequential Neural Posterior Estimation (SNPE) algorithm (Greenberg, Nonnenmacher and Macke, 2019), (Tejero-Cantero et al., 2020) that can perform this likelihood-free Bayesian and MLE estimation. SNPE uses a model little used in economics, the normalizing flow (Rezende and Mohamed, 2015), which is a powerful conditional density estimator. Flows facilitate Bayesian estimation by learning the posterior conditional distribution trained on samples from the joint, . One can think of SNPE as an extension of the Kristensen and Shin (2012) approach to likelihood estimation, where they simulate data from the joint via the prior and the likelihood simulations. Then they use a kernel density estimator (KDE) to estimate the likelihood function. In my case, I use a normalizing flow to replace their KDE, which allows me to extend their result to full Bayesian inference and accommodate data with a latent state space structure. The benefits of SNPE mainly stem from the use of the flow over traditional density estimators like the KDE. There are also alternative methods like SNRE (Durkan, Murray and Papamakarios, 2020) which is discussed in the appendix and simulation-based inference combined with variational inference (Glöckler, Deistler and Macke, 2021).

The general approach around simulation-based inference has gained popularity in many fields. The approach is often used for Bayesian inference in machine learning (Durkan, Murray and Papamakarios, 2020), (Greenberg, Nonnenmacher and Macke, 2019). The approach has been used in neuroscience (Boelts et al., 2021) and ecology (DiNapoli et al., 2021). The technique has also become one of the leading estimation methods in many fields of physics (Brehmer, 2021), (Cranmer, Brehmer and Louppe, 2020).

II. Literature Review

This literature review will cover three topics: simulation-based methods in economics, the literature on solving dynamic models, particularly with kinks and discontinuities, and solution and estimation of heterogenous agent models. I will discuss MH-MCMC and machine learning background in the following sections.

II.A. Simulation-Based Models in Economics

I will give an overview of current simulation-based estimation and related approaches. Most of the simulation-based likelihood and inference approaches are inspired by an approach like method of simulated moments (MSM) (McFadden, 1989), (Pakes and Pollard, 1989), (Duffie and Singleton, 1990). Due to the difficulty of verifying the global identification criterion there is a large interest in developing more efficient and robust estimators where this is not a problem. Techniques like maximum simulated likelihood, attempt to address this (Lerman and Manski, 1981), although these techniques both have simulation bias (Hajivassiliou et al., 1997), (Haan and Uhlendorff, 2006) and typically require the use of measurement error. There has also been work on using techniques from simulation-based likelihood estimation to solve dynamic models, particularly in industrial organization (Keane and Wolpin, 1994). There is also literature on efficient simulation techniques using both indirect inference (Smith Jr, 1993), (Gourieroux, Monfort and Renault, 1993), and efficient method of moments (Gallant and Tauchen, 1996).

Simulation-based techniques in economics are efficient when the model is well specified, so much of recent work has been done to improve robustness in misspecification. One such avenue is efficient method of moment estimators using a spectrum of moments so the data is guaranteed to be in the support of distributions spanned by the moments111There is also work in machine learning attempting to perform robust and efficient moment estimation by using a spectrum of moments, most well known is the Generative Moment Matching Network (Li, Swersky and Zemel, 2015) (Carrasco et al., 2007), (Altissimo and Mele, 2009). However, these methods have a difficult time dealing with models with latent time structure. Another approach is approximate Bayesian inference (Rubin, 1984) to estimate models solved via value function iteration techniques, to estimate these models. However, in a well specified model, this approach is only approximately Bayesian, unlike the set of algorithms I propose.

One could even consider a particle filter a simulation-based technique for deriving a likelihood function given an intractable integral (Fernández-Villaverde and Rubio-Ramírez, 2007), but this approach only works with dynamic models that yield complementary state space representations and requires a likelihood function at each point in time. Although the literature is more sparse, there are papers that also perform simulated Bayesian inference (Flury and Shephard, 2011) (Herbst and Schorfheide, 2014), extending particle filtering for Bayesian inference. Other machine learning approaches use techniques that have both robustness and efficiency guarantees like GANs. Most relevant to this paper, Kaji, Manresa and Pouliot (2020) whose GAN approach to structural modelling open the door to robust and near efficient point estimation using only simulations from the model and not a likelihood.

II.B. Solving Dynamic Models with Kinks

I will next discuss approaches to solve dynamic models, particularly models with kinks and nonlinearities.

There are a variety of ways to solve dynamic macroeconomic models: perturbation, projection, and value function iteration (Fernández-Villaverde, Rubio-Ramírez and Schorfheide, 2016), (Judd et al., 2017), of which only perturbation yields likelihood functions that allow Bayesian and MLE estimation using conventional techniques. Perturbation works well when the policy function looks like a linear or low degree polynomial function. For methods that are highly nonlinear, with large shocks (Terry, 2017), or even non-analytic, projection and value function iteration should be used. For a large set of models, almost anything that is solved via value function iteration (Hennessy and Whited, 2007), heterogeneous agent models with intractable likelihoods (Kukackaa and Barunika, n.d.), and most projection models the likelihood is intractable forcing the use of less efficient point estimate methods that have weaknesses compared to Bayesian and MLE estimation.

In order to estimate non-perturbation models, one has to resort to simulation-based inference approaches. As such, most of the time, these models are not estimated in a Bayesian or even full information manner and practitioners resort to, for example, method of simulated moments.

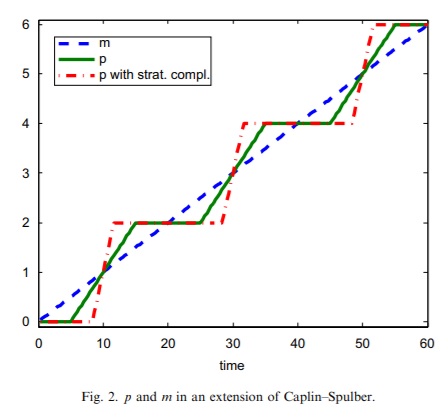

As an illustration of problems faced by a perturbation approach, below is an example of a s-S model policy function in Caballero and Engel (2007):

s-S models posits a fixed cost to changing a state variable which typically leads to kinks in the policy function. Often times modeling inventory or capital requires this assumption. The above example uses s-S costs with respect to menu prices assuming a linearly increasing money supply (blue). This is a modification of Caplin and Spulber (1987), which assumes there is a spectrum of firm prices from the s-S trigger point to zero. Caballero and Engel (2007) assume there is a spectrum of firms prices that only covers a portion of the range from the s-S trigger to zero. As the money supply increases linearly, at some time periods there will be no firms adjusting due to the fixed costs and at some time periods an above average number of firms will adjust to keep up with the price level. This is shown by the behavior in the the green and red line show. The kinks are where the policy function is non-differentiable and shows the transition where no firm is adjusting to when some firms are adjusting prices or vice versa. Thus a perturbation approach, which estimates a Taylor series approximation of the policy function, will not work as the policy function is non-analytic. This implies that one must solve the model via something like value function iteration, which leads to estimation problems mentioned above.

Papers which estimate s-S models include Arrow, Harris and Marschak (1951) and Caplin and Spulber (1987). In particular, Khan and Thomas (2008) assumes an s-S model for heterogeneous agent model for investment in capital. House and Leahy (2004) model the purchasing behavior for used durable goods given a fixed cost in addition to the price of the good. In particular, the good is priced under adverse selection (Akerlof, 1978). Likewise in finance there is a large literature estimating structural models (He, Whited and Guo, 2021), (Taylor, 2013). Like the s-S models, this literature often includes fixed adjustment costs or other approaches that yield kinks in the policy function. Terry, Whited and Zakolyukina (2022) finds a negative externality that comes regulation of public company disclosure. Although they find current disclosure regulations are low, if one is forced to disclose accurately, one will mis-invest so that the investments generate results that more closely resemble the the desired upon false disclosure results.

II.C. Heterogeneous Agent Models

I will now discuss the literature around full information estimation of heterogenous agent models. Much of the methodological interest in heterogeneous agent models is improving the speed of solution methods (Auclert et al., 2021a), (Winberry, 2018), (Khan and Thomas, 2008). However the computational bottleneck for estimation problems is not solution speed, but the intractability of the Kalman filter on large latent spaces. For this reason, while there is a large literature on heterogeneous agent model (Auclert et al., 2021b), (Ottonello and Winberry, 2020), (Caglio, Darst and Kalemli-Özcan, 2021), most practitioners resort to calibration because of this and other barriers to estimation. There have been approaches like Ahn et al. (2018), who propose a dimension reduction technique to reduce latent state space size to be manageable for filtering. However this approaches throws away information while still adding overhead compared to a pure simulation-based approach. Liu and Plagborg-Møller (2021) and Parra-Alvarez, Posch and Wang (2020) perform maximum likelihood estimation using micro data along with macroeconomic aggregates. Parra-Alvarez, Posch and Wang (2020) estimate an Aiyagari model (Aiyagari, 1994), (Huggett, 1993) and propose a diagnostic that finds that a sizable number of parameters are not well identified and they suggest calibrating those parameters. For my results, the choice to use uniform priors for all the estimation problems faces the same documented identification problem, however, uniform priors are still used for the sake of estimation transparency.

While there is a large literature dealing with simulation based estimators, both macroeconomists that work with heterogeneous agent and representative agent models have expressed a need to reduce the barriers to MLE and Bayesian estimation. The SNPE and related algorithms can help mitigate these barriers.

III. Background on Simulation Neural Posterior Estimation (SNPE) and Metropolis-Hastings

This section will discuss the background of the SNPE estimator and MH-MCMC. First, I will intuitively discuss the basics behind Bayesian estimation. Then I will move to a brief discussion of normalizing flows, which is a density estimator used to estimate the posteriors from samples drawn from the joint distribution. I will discuss the SNPE algorithm and finally conclude with some caveats and pathological examples.

When discussing the approach of simulation-based inference, it is useful to lay down a few definitions. The true data comes from the underlying data generating process. For macroeconomics, it would be economic data like output, consumption, etc. The simulator is the model being estimated, for this paper: a dynamic macro model. The only demand simulation-based inference puts on simulators is to be able to simulate data that has a 1-1 correspondence to the covariates in the true data.

III.A. Bayesian Basics

In this subsection, I will discuss the general paradigm of Bayesian estimation, then I will discuss MH-MCMC.

Bayesian estimation attempts to find the posterior given the likelihood and prior of a model using Bayes’ rule:

Here is the posterior, is the likelihood, and is the prior. All approaches that perform Bayesian inference, ranging from MH-MCMC, variational inference, to simulation-based inference concern techniques for calculating without calculating the partition function, .

The predominant technique for performing Bayesian inference in economics is to perform MH-MCMC (Herbst and Schorfheide, 2015), which I will describe next. In MH-MCMC, one concerns oneself with likelihood ratios between parameter values. For example, if one knows both the prior and the likelihood for any given point, one knows the relative likelihood of being in any point versus any other. One point in parameter space may be twice as likely to be visited in the posterior as another point, even if the actual probabilities are not known. Since one knows the relative probabilities, one can design a random walk so that a walker visits probabilities equivalent to the ratios of there probabilities. One way to do that is if a walker can choose to compare any point in the posterior to the point the walker is currently at, the walker will move to the second point with the likelihood according to the ratio of the unnormalized probabilities. If the second point is half as likely to be in the posterior, the walker will move with probability one half and probability one half stay in place. If the second point is more likely to be in the posterior, say twice as likely, the walker will move to the second point for sure, with the understanding that if the walker randomly selected to move back, the move back would be now with half the probability.

In this way, the walker moves across the space of the posterior with relative frequency according to ratio between points, which ultimately means that one is sampling from without calculating the normalizing partition function. In practice, MCMC is a little more complicated, as often the parameter space is unbounded, and one can’t sample the entire space with equal probability if the space is unbounded. Thus this involves the use of a proposal distribution and the use of importance sampling (see appendix for more information).

Alternatives like variational inference have been proposed which speed up the inference at the cost of some bias (Wainwright and Jordan, 2008), but it is beyond the scope of this paper. The approach I propose, simulation-based inference, does not require knowing the likelihood, , which often cannot be derived with commonly used solution methods, and scales computationally much better than MH-MCMC for larger state-of-the-art models, like HANK models. The backbone of the SNPE approach I proposes samples points from the joint distribution , then one estimates the posterior using a conditional density estimator. SNPE uses a normalizing flow as a density estimator which has a series of advantages over traditional KDEs. The normalizing flow and it’s advantages will be the next topic.

III.B. Normalizing Flows

sectionNormalizing Flows In this section, I will discuss how a particular normalizing flow, the neural autoregressive flow (Huang et al., 2018), is structured. Then I will discuss how to use the change of variables formula for a random variable to derive a likelihood of a sample under the flow. I will also attempt to highlight advantages flows have over KDEs that make the SNPE algorithm more powerful that the tradional Kristensen and Shin (2012) approach.

A flow is a composition of individual bijectors. Thus the first task is to define these intermediate changes in measure, , so that they can be composed with each other to form a invertable function. For example the output of becomes the input to giving the total composition much more flexibility. This is not trivial. For example take a polynomial regression. If one knows the input to this regression, one can calculate the output. However if one knows the output, the roots of a polynomial are not generally solvable and so polynomials aren’t invertable transformations. However one set of invertable transformations are affine operations. Given and going from 1…N indexing each element in the vector :

| (1) |

This is trivially invertable as one can derive from by shifting the negative of and scaling by the inverse of . While one can still add nonlinearities like a logit link function between bijective transformations, this still lacks expressivity. The standard way to extend this model is to allow for the shifts and scales to be dependent on at least some of the inputs. For example, earlier elements are only modified in an directly invertable manner (ie ), then condition the shifts and scales for the rest of the elements on inputs, , that weren’t transformed:

| (2) |

and are typically differentiable and flexible functions–typically feed-forward neural networks conditioned on earlier elements of the vector, that now output dynamic ”psuedo” parameters , that depend on the conditioning variables, . Next I will illustrate how a neural autoregressive bijector is defined that I use in my paper. Make the first element, the identity or affine map, then the second element an affine transformation in with psuedo-parameters and dependent only on . The third element, , has psuedo-parameters then dependent only on and enters only in an affine manner.

To make this model nonlinear, one typically adds a link function which is usually a Leaky ReLU (Xu et al., 2015). A Leaky ReLU is two lines of different slope intersecting at zero. This kink is often enough to make neural networks universal approximators of continuous functions (Cybenko, 1989).

Since is invertable as well as the rest of the flow, one can recover the inputs knowing only all elements in 222The procedure to recover from all the ’s is to know from the affine first equation. Then recover the affine parameters for the equation (which is only conditioned on ). Then one can invert to get knowing the affine parameters. Now that one knows one can repeat the procedure to get , etc.. This makes the bijector invertable in practice. This invertability is another advantage normalizing flows have over KDE. One can sample from them and calculate the pdf of any sample without the use of rejection sampling or other computationally heavy techniques. This will be exploited in the SNPE algorithm as the flow will be used both as a density estimator and as a proposal distribution for generating samples.

Additionally since each affine transformation is a function of variables that have an index smaller than the index in question, the Jacobian is lower triangular and the determinant is just the product on the diagonal. This makes the change in variable formula scale linearly with the number of parameters.

Furthermore, if one stacks multiple bijections on top of one another, one can permute the order of input elements () with a bijective operation so that different bijectors have different conditioning relationships among variables allowing the flow to universally approximate any distribution. If the functions for and are universal approximators (ie neural networks), one can show that a stack of bijectors (along with permutations), is also a universal approximator and thus can approximate any change of variable arbitrarily well. This will be discussed and proved in the theoretical section in the appendix following (Huang et al., 2018).

One can also condition and with additional arbitrary conditioning variables to form a flexible conditional density estimator. This ability to condition is one advantage it has over a KDE. Since the problem is to estimate the density of conditioned on , will take the role of . will be the true data and analogue of simulated data which will be differentiated by a lower case . Conditioning variable and real data will enter as additional conditioning varibles in the flow. In particular they will be included as conditioning variables in the neural networks that produces and . Thus, for example will be conditioned on as well as /, the simulated/real data.

Since these models can model any conditional distribution, and can calculate the likelihood of any sample point in the target space, one can fit this model on samples from arbitrary continuous densities and have the guarantees that come with a well specified maximum likelihood problem. Thus, normalizing flows are density estimators that are robust to misspecification and asymptotically efficient due to estimation with maximum likelihood.

Next I will discuss the change of variable formula for a flow. Given a density, with random vector realizations ; a normalizing flow is a function, mapping to a target random variable , which has density, such that the probability is related to the probability via:

| (3) |

This formula is simply the change of variable formula one learns in an introductory PhD econometrics class, with the first term representing the measure in the base distribution, and the Jacobian representing the change in measure due to the transformation to the target distribution . In the appendix, I show in more detail how to construct a flow so that it is both invertable and can approximate any continuous distribution. Assuming both these things, one can use the change of variable formula to derive the likelihood that a sample point was generated by the flow (Rezende and Mohamed, 2015). One uses the flow to transform the to and then one can use the change of variable formula to calculate . One can then perform maximum likelihood by modifying the parameters of the neural networks that govern the psuedo-parameters ( and in each layer to maximize for samples in the data.

III.C. Sequential Neural Posterior Estimation

First, I will discuss the procedure underlying Kristensen and Shin (2012), which is the same approach as the SNPE algorithm. Then I will discuss the role of the normalizing flow in extending the Kristensen and Shin (2012) approach as well as multi-round inference. I proceed by simulating from the prior. Then one simulates , simulated data, from the model likelihood, . Concatenating the two simulations together gives samples from the joint distribution . With these samples one can use the normalizing flow density estimator to estimate . Setting the conditioning variable in the flow, , to be the real data (note capitalized), allows one to have an estimate of the posterior.

One typically proceeds with SNPE in a multi-round fashion where a proposal distribution which has more alignment with the posterior takes the place of the sampling from the prior. Since the true posterior and the true prior might have limited overlap, to reduce variance, it’s often important to estimate the posterior in multiple rounds. In the first round, one samples from the prior. In later rounds, one samples from the current estimate of the posterior and performs importance sampling to correct from the distribution shift. More mathematically, given a proposed prior of , true prior of , the posterior, when trained on this data, will have to be importance sample adjusted by the factor of , to account for sampling from a distribution that isn’t the prior. Greenberg, Nonnenmacher and Macke (2019) perform the estimation in one step by recognizing the adjusted distribution , where is the posterior obtained by sampling from a proposal distribution different then the prior. Then if a normalizing flow is estimated in place of in the above equation, a fully flexible will return a unbiased estimator of the posterior. Importance sampling is more thoroughly discussed in the appendix.

III.D. Properties of SNPE

This section will briefly relay the proof for why the SNPE algorithm converges to the Bayesian posterior in the infinite Monte Carlo sampling limit.

Proposition 1 from Papamakarios and Murray (2016) proves that if is sampled from a proposal distribution with the true prior and the likelihood is sampled from than a normalizing flow that maximizes the likelihood of the simulated data will be proportional to , ie:

| (4) |

provided that the true parameterization is contained in the set of parameters of the normalizing flow. This restriction implies that the posterior is continuous and at least for instance because the flow can only approximate continuous and distributions.

The intuition behind the proof is that given enough samples from , maximum likelihood of estimation will converge to the distribution that minimizes the KL divergence between the distribution the sample comes from and the normalizing flow parameterization. Thus if the flow has parameters that would set the KL-divergence to 0, this would be the actual distribution that is the data generating process. When fitting distributions, since 4 implies the distribution that will converge too, if one estimates on the data, will converge to the posterior. The importance weights are inverted since this function is trained on data rather than the data being reweighted by the weights. See importance sampling discussion in appendix for details. This proof goes hand in hand with the proof that a flow is a universal approximator (proof in appendix), as given enough samples and a large enough flow, the true posterior will be arbitrarily close in a KL divergence sense to the best parameterization of the flow.

III.E. Caveats and Pathological Examples Using SNPE

There are two caveats regarding the theoretical proprieties of SNPE: the lack of smoothness in the posterior of kinked models and the issue of modeling stochastic singularities. Many, but not all, s-S models and other models with kinks, may have discontinuities in the posterior distribution. In particular the assumption that there is a normalizing flow parametrization that can generate the posterior is violated. This problem is not unique to flows, MSM will also have similar problems, but because it’s not a full information technique ignoring this information will allow for convergence. That being said, in practice, just like MSM, the flow will still converge. However, it will often learn a continuous function that approximates the discontinuity in the posterior. In the maximum likelihood case, a continuous function can approximate the discontinuity well, as dynamic models often have discontinuities in only a handful of points if that. Thus, the estimation result will generally be near the true likelihood, which is still an efficiency improvement over the MSM. That being said, if estimation with a kinked model is a problem, one can also add measurement error to smooth the problem out.

Stochastic singularities are the second pathological example that the model will have difficulty handling. This also leads to some estimation issues, not unique to flows, but also other MLE approaches, like maximum likelihood after solving with perturbation. When this happens, the dynamic model learns a sub-manifold on the entire space. Because a normalizing flow has to have positive support on the entire space of of the target distribution, this also violates the assumption that the normalizing flow parameterization can generate the posterior. Like in the previous case, the flow will just learn to put an asymptotically small probability on spaces not in the dynamic models support. That being said, in the cases where there are stochastic singularities and one uses real data that doesn’t lie on the sub-manifold of the model, the model will fail to match the data. MSM will typically still match the data, but this a weakness of the MSM. MSM will converge because it cannot discern that the model has no support in those region of the data. One can add more shocks, add measurement error, or a change in modeling like the generalized sS model (Caballero and Engel, 2007) to avoid a stochastic singularity. If the true data is on the submanifold, SNPE will work.

IV. Results

Each model has it’s own set of results. The first model is the RBC model where I estimate on simulated data and real data. The second model is toy corporate finance model solved via value function iteration and three different simulation-based approaches are used to estimate this model. The third model is the Lucas asset pricing model solved via projection. The forth model is the Smets and Wouters (2007) model estimated via both MH-MCMC and SNPE. The fifth model is a HANK model solved via Reiter’s method and time iteration. Finally the sixth model is a model of bequests which is solved via value function iteration. For more information on the details and construction of the models, refer to the appendix. All six models have been estimated using my simulation-based inference approach.

I will now discuss proper posterior behavior and how to inspect the accuracy of the posterior through inspection. While inspection is used for all of the models, for some that can be estimated reasonably, I will compare posteriors with MH-MCMC. Through the Bernstein-von Mises theorem, the posterior should converge to the true parameter given enough data samples. However, in finite sample sizes the correct posterior may not match the value of the true parameters. Nevertheless, it is a useful check to make sure that the posterior mode generally matches in at least some of the parameters and doesn’t put vanishing posterior mass at the true values.

IV.A. RBC Model

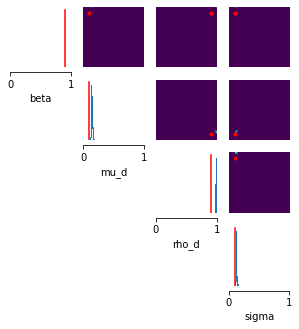

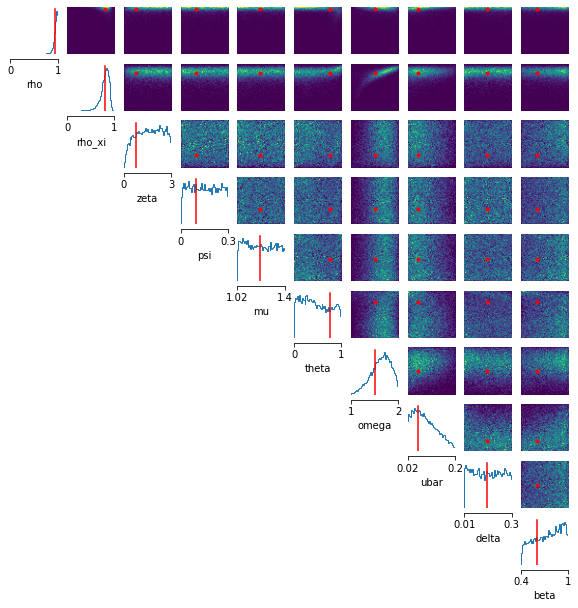

The first set of results deal with the RBC model. The RBC model has 4 parameters: , , , and as defined in the economic models section of the appendix. The CRRA elasticity, is set to 2. The model is simulated for 200 iterations and the first 100 iterations is dropped to get a steady state behavior. The results of the posterior with the parameters displayed in the same order as above is shown here:

The red bar indicates the true parameter values and the blue line indicates the posterior of the model as estimated by the simulation-based inference approach. Each of the density plots in the upper triangular portion of the graph indicates two way densities given by the corresponding row and column. Likewise the red dot indicates the true value of the parameter with respect to the two axis. In all models, uniform priors are used along the interval specified for all parameters.

Next I show a chart that displays the an approximate ground truth by running MH-MCMC for 2 million iterations. Although in the limit of time steps, given regularity conditions, the Bernstein-von Mises theorem implies that the Bayesian posterior converges to the maximum likelihood solution (which in this case is the true value given data simulated from a parameterization), with a set number of data points, the posterior may not concentrate around the true parameters. The fact that MH-MCMC concentrates around the true solution, indicates that the posterior obtained with SNPE is likely the true posterior.

As is clear, for MH-MCMC the simulation-based inference approach concentrates almost entirely on the true parameter value. This extremely close relationship is not entirely replicated on the other models, as the other models have flatter likelihoods and more parameters. In many cases the true posterior is not a delta function in the same way the simulated RBC model is.

The third chart is the same RBC model estimated on real data:

Here there is no available ground truth but the parameters derived are not realistic, which is not surprising for such a simple model. You can see that compared to the first chart, the method is more uncertain of ground truth. You can also see the model doesn’t estimate parameters close to what theory would suggest. This is not surprising given that the RBC model is too simple to work on real data and many of these parameters don’t agree with theory even in more complex models. Furthermore, to illustrate the accuracy of the model, all priors are uniform over the charted interval. In the model, it predicts the Cobb-Douglas parameter, should be very close to 1, which is reasonable since labor is fixed in this model and capital is highly correlated with labor, combined with the fact that a Cobbs-Douglas function is homogeneous with degree 1. The discount rate, , also doesn’t agree with theory, which is unsurprising as is often calibrated because it’s so difficult to pin down. Likewise the parameter on the productivity process, , is another variable that is often estimated but is difficult to pin down in this model. or the depreciation rate, is the only parameter where the model is relatively reasonable.

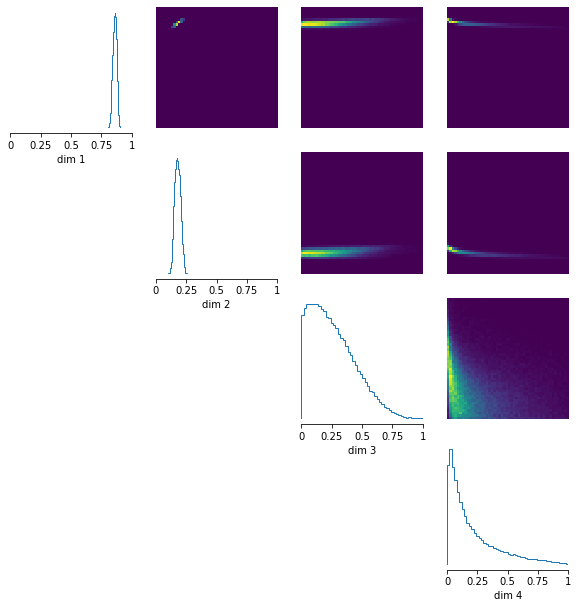

IV.B. Cash Flow Model

The next set of results deal with a partial equilibrium model of firm cash flow solved via value function iteration. The parameters here are , , , and . is the standard deviation of the productivity law of motion. The interest rate is set at 5 percent and is set as 1/(1+r). The cash flow model was estimated with three different methods, each of which obtaining nearly the same posterior, giving confidence the approach has converged to the right solution. The first chart will show the posterior for a simulation-based inference approach that uses a normalizing flow and a feed forward network as the embedding network (converting the high dimensional data into a lower dimensional conditioning variable). The second chart will show the same model and data, but using a RNN embedding network. The third chart will show a density estimator that is a GAN instead of a normalizing flow. This is an alternative simulation-based estimator: Sequential Neural Ratio Estimation which is discussed in the appendix.

Displaying the charts:

Despite using different inference techniques, the posteriors look fairly equivalent by visual inspection, suggesting the same distribution has been learned. Furthermore it does seem like the mode is fairly close to the actual parameterization. There some higher order considerations that are getting in the way of the dynamics of the model, but the model seems to be able to accurately recover the true parameters.

IV.C. Lucas Asset Pricing Projection Model

The following section shows the estimation procedure on a Lucas asset pricing model:

The model does seem to accurately fit reproduce the true values. the main error is on where the posterior seems to be higher than the true value for the autogregressive parameters. All other posteriors match very closely the actual data generating parameters. This model took under 10 hours to estimate on an 8 core Intel i7 machine.

IV.D. Smets-Wouters 2007 Model

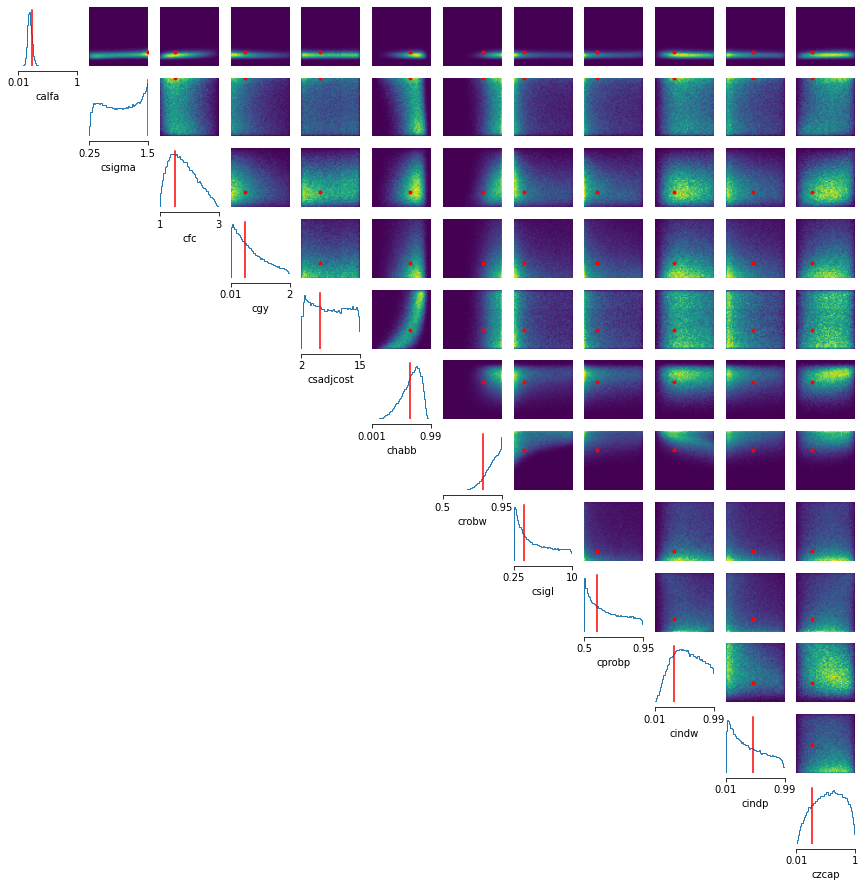

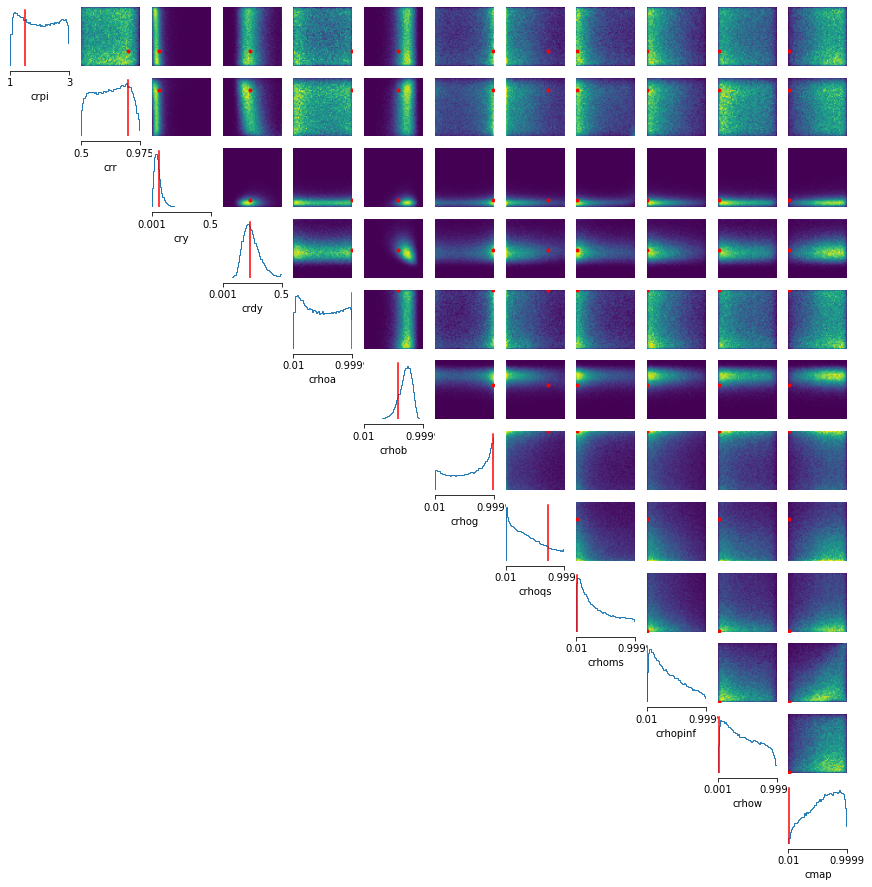

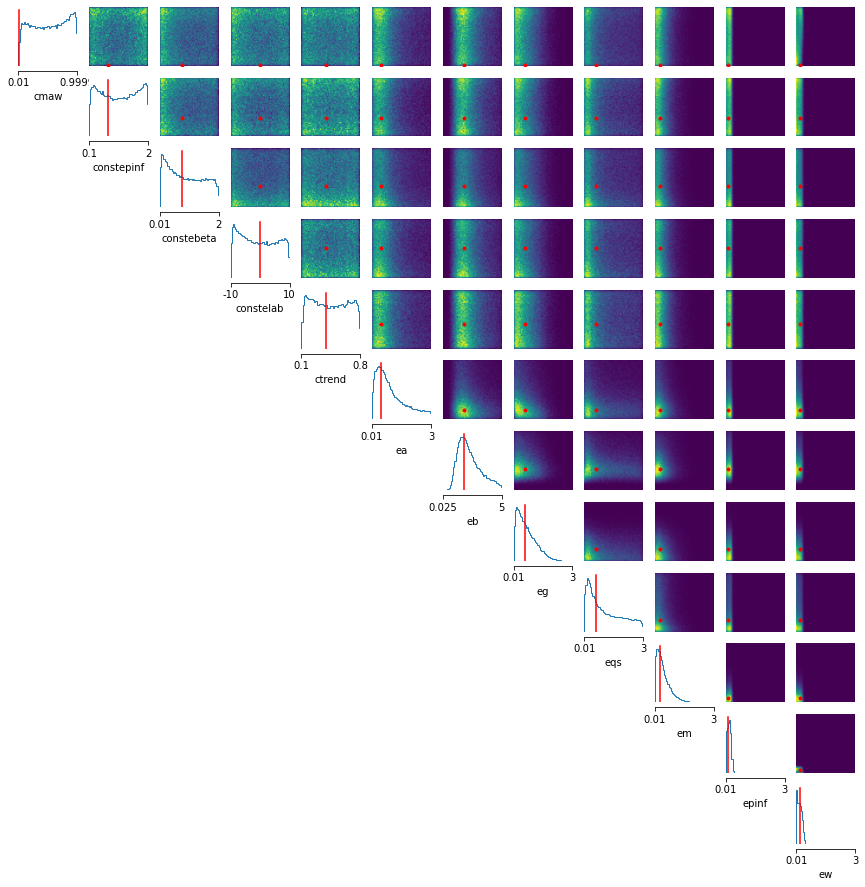

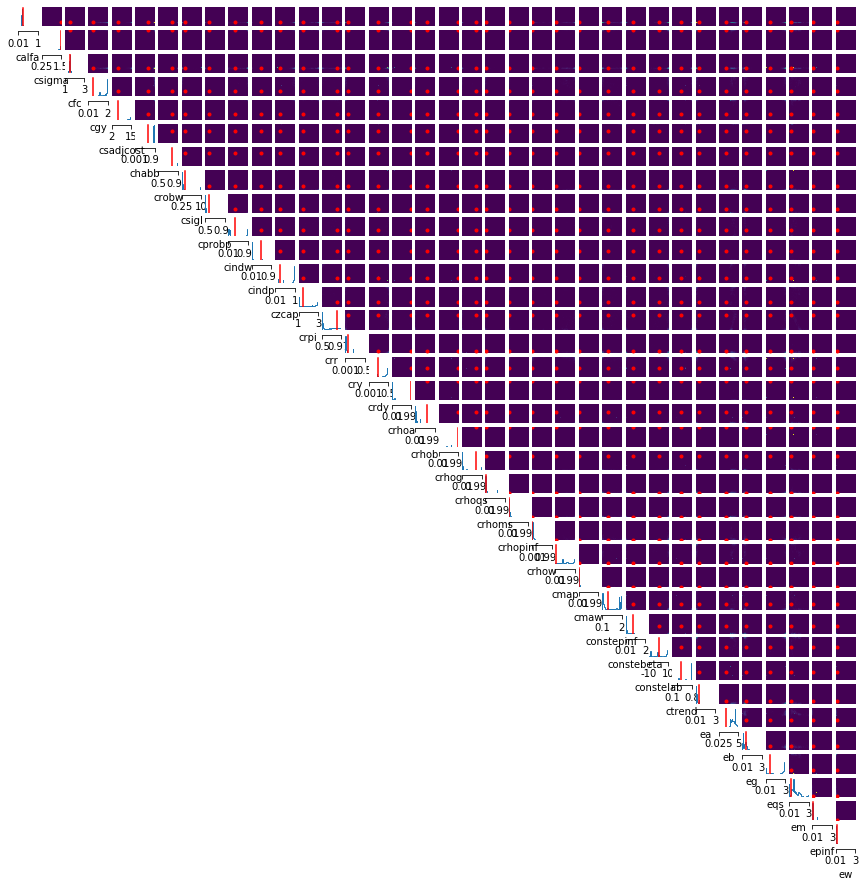

A description of the model can be found at Smets and Wouters (2007). The model is a representative agent New Keynesian model. The model has 8 shocks that interact with the rest of the model in a autoregressive manner and 8 observed variables. The model estimates a model of potential GDP with a flexible price economy, along with the true economy with sticky Calvo prices. The model is expressed in linearized form. For more information on the model see the paper and the appendix. Since there are 37 parameters in this model, the data are seperated into three different charts of 12,12,13 parameters each.

I will next discuss some of the parameters and the accuracy of the model. The model successfully estimates capital share (calpha). The model seems to have a difficult time estimating the elasticity of the adjustment costs (csadjcost) as the posterior is diffuse. Fixed costs (cfc) seems to be estimated well, with the mode corresponding to the data generating parameter. The wage stickiness posterior (cprobw) is generally in the right place but there is little probability mass in the location of the true parameter. The wage indexation parameter (cindw) seems to be well identified. The Taylor rule parameters for output (cry) and change in output (crdy) also agree with the ground truth, but the inflation Taylor rule parameter (crpi) does not. Some autoregressive parameters on shocks seem to be well estimated (crhob, crhoms, crhow), while others seem to be diffuse or in areas of low probability mass (crhoa, cmaw, crhoqs, cmap). Typically these parameters are hard to identify, but the model seems perform adequately in identifying some of these parameters. Surprisingly, the model seems to do a poor job in identifying the mean of the observed variables (ctrend, constepinf, conster, constelab, constebeta), but performs well in identifying the standard deviation of shock variables (ea, eb, eg, eqs, em, epinf, ew).

The algorithm can also find multimodal distributions. You can see this with a few of the parameters, namely crpi and constepinf among others. Since the model estimates posterior by estimating a density from joint distribution draws, there is no reason multi-modal distributions would be more problematic than uni-modal distributions. However with MH-MCMC, multi-modal distributions are a well documented problem (Pompe, Holmes and Łatuszyński, 2020), (Herbst and Schorfheide, 2015). A more elaborate discussion of the model structure which links up all the parameter names to the Smets-Wouters equations is found in the appendix.

I will now discuss the Smets-Wouters model estimated with MH-MCMC. Although the models were estimated on different computers, each model was solved 1 million times. While estimating the density from samples adds overhead for SNPE, the initial burn in period and the use of the Kalman filter also adds overhead for MH-MCMC. Despite the use of different computers, the amount of overhead is comparable for the two approaches with SNPE using slightly more computation. Below shows the posterior after MH-MCMC:

As you can see, the quality of the posterior compares poorly to SNPE. Many times the mode is far from the true parameter value. Additionally, quite a few parameters have negligible mass near the true parameter value and the distribution of the posterior looks much more scattered and disconnected than in the SNPE case. Nevertheless checks indicate the MH-MCMC algorithm is sampling from places of high likelihood, it’s just not sampling for the entire array of locations where this is the case.

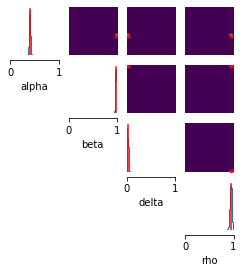

IV.E. HANK Model

The fifth model is the 10 parameter HANK model with the parameters discussed in the model section:

I will next discuss the estimation of the HANK model. This model has only two shocks and thus only two observable equations, the unemployment rate (which is linked to output via a labor only production function) and the interest rate. Since there were 810 latent variables in the model, it’s perhaps reasonable to expect that many of the parameters were difficult to identify. That being said the parameters the approach was confident in aggreed with the ground truth. This illustrates the the model can estimate HANK models with large latent state space–something that is computationally intractable for a likelihood based approach without dimension reduction. For the parameters rho, rho-xi, omega and ubar, the mode of the distribution is either at the true parameter value or in the case of omega, close to the true parameter value. The other parameters all exhibit flat likelihoods, which may not be surprising considering the limited impact of some of the parameters on the two chosen observed variables.

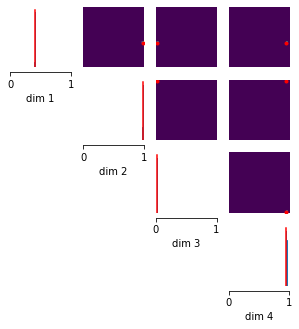

IV.F. Bequests Model

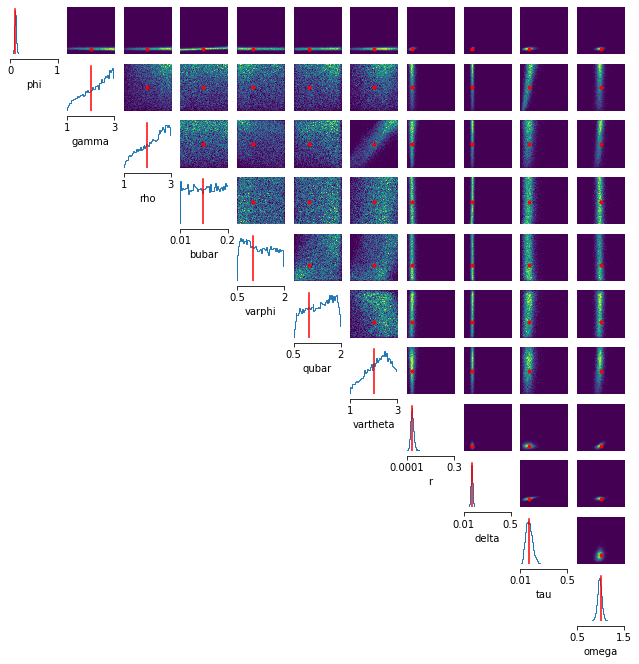

The sixth model is the 11 parameter bequests model with parameters displayed in the chart corresponding to the parameters in the model appendix section:

While many of the parameters have converged to the value of the true parameters, some of the parameters still have high uncertainty. This could be due to the fact that the parameters have very flat likelihoods. Regardless, this, the HANK model, and the Smets-Wouters models are all research scale, and the estimation of posteriors seems good in all cases. Many of the posterior distributions do concentrate around the true value, suggesting the model does have some discerning power with regard to the given parameters. Furthermore this is a reasonable sized model solved via value function iteration and the algorithm succeeds relatively well in calculating the posterior.

V. Conclusion

In this paper, I propose a method to estimate models in a Bayesian or MLE manner using simulations only, without a likelihood function. This works even on models that have a latent state space relationships across time. This model can Bayesian estimate HANK models with large latent state spaces and also can be applied to solution methods like value function iteration and projection which don’t yield a likelihood function. The model can be applied as broadly as MSM, with better gaurantees like efficiency and posterior estimation. Additionally, outside of macroeconomics, this approach can be applied to industrial organization, applied game theory, and econometrics. In industrial organization and game theory, this could be used to solve structural and dynamic models. In econometrics, general latent time series models can be estimated more effectively and efficiently, without likelihood functions. Additionally, the normalizing flow which is a bijective map that can perform arbitrary change of variables is a powerful technique that hasn’t been explored in depth. For example, normalizing flows can be applied to the identification in non-separable models literature and can be used as transport maps in optimal transport. Despite the focus on macroeconomic modeling, the application of this technique is more general and has much greater applications that is beyond the scope of this paper.

References

- (1)

- Ahn et al. (2018) Ahn, SeHyoun, Greg Kaplan, Benjamin Moll, Thomas Winberry, and Christian Wolf. 2018. “When inequality matters for macro and macro matters for inequality.” NBER macroeconomics annual, 32(1): 1–75.

- Aiyagari (1994) Aiyagari, S Rao. 1994. “Uninsured idiosyncratic risk and aggregate saving.” The Quarterly Journal of Economics, 109(3): 659–684.

- Akerlof (1978) Akerlof, George A. 1978. “The market for “lemons”: Quality uncertainty and the market mechanism.” In Uncertainty in economics. 235–251. Elsevier.

- Altissimo and Mele (2009) Altissimo, Filippo, and Antonio Mele. 2009. “Simulated non-parametric estimation of dynamic models.” The Review of Economic Studies, 76(2): 413–450.

- Arrow, Harris and Marschak (1951) Arrow, Kenneth J, Theodore Harris, and Jacob Marschak. 1951. “Optimal inventory policy.” Econometrica: Journal of the Econometric Society, 250–272.

- Auclert et al. (2021a) Auclert, Adrien, Bence Bardóczy, Matthew Rognlie, and Ludwig Straub. 2021a. “Using the sequence-space Jacobian to solve and estimate heterogeneous-agent models.” Econometrica, 89(5): 2375–2408.

- Auclert et al. (2021b) Auclert, Adrien, Hannes Malmberg, Frederic Martenet, and Matthew Rognlie. 2021b. “Demographics, wealth, and global imbalances in the twenty-first century.” National Bureau of Economic Research.

- Boelts et al. (2021) Boelts, Jan, Jan-Matthis Lueckmann, Richard Gao, and Jakob H Macke. 2021. “Flexible and efficient simulation-based inference for models of decision-making.” bioRxiv.

- Brehmer (2021) Brehmer, Johann. 2021. “Simulation-based inference in particle physics.” Nature Reviews Physics, 3(5): 305–305.

- Caballero and Engel (2007) Caballero, Ricardo J, and Eduardo MRA Engel. 2007. “Price stickiness in Ss models: New interpretations of old results.” Journal of monetary economics, 54: 100–121.

- Caglio, Darst and Kalemli-Özcan (2021) Caglio, Cecilia R, R Matthew Darst, and Sebnem Kalemli-Özcan. 2021. “Risk-taking and monetary policy transmission: Evidence from loans to smes and large firms.” National Bureau of Economic Research.

- Caplin and Spulber (1987) Caplin, Andrew S, and Daniel F Spulber. 1987. “Menu costs and the neutrality of money.” The Quarterly Journal of Economics, 102(4): 703–725.

- Carrasco et al. (2007) Carrasco, Marine, Mikhail Chernov, Jean-Pierre Florens, and Eric Ghysels. 2007. “Efficient estimation of general dynamic models with a continuum of moment conditions.” Journal of econometrics, 140(2): 529–573.

- Cranmer, Brehmer and Louppe (2020) Cranmer, Kyle, Johann Brehmer, and Gilles Louppe. 2020. “The frontier of simulation-based inference.” Proceedings of the National Academy of Sciences, 117(48): 30055–30062.

- Cybenko (1989) Cybenko, George. 1989. “Approximation by superpositions of a sigmoidal function.” Mathematics of control, signals and systems, 2(4): 303–314.

- DiNapoli et al. (2021) DiNapoli, Robert J, Enrico R Crema, Carl P Lipo, Timothy M Rieth, and Terry L Hunt. 2021. “Approximate Bayesian Computation of radiocarbon and paleoenvironmental record shows population resilience on Rapa Nui (Easter Island).” Nature Communications, 12(1): 1–10.

- Dixit and Stiglitz (1977) Dixit, Avinash K, and Joseph E Stiglitz. 1977. “Monopolistic competition and optimum product diversity.” The American economic review, 67(3): 297–308.

- Duffie and Singleton (1990) Duffie, Darrell, and Kenneth J Singleton. 1990. “Simulated moments estimation of Markov models of asset prices.”

- Durkan, Murray and Papamakarios (2020) Durkan, Conor, Iain Murray, and George Papamakarios. 2020. “On contrastive learning for likelihood-free inference.” 2771–2781, PMLR.

- Fernández-Villaverde and Rubio-Ramírez (2007) Fernández-Villaverde, Jesús, and Juan F Rubio-Ramírez. 2007. “Estimating macroeconomic models: A likelihood approach.” The Review of Economic Studies, 74(4): 1059–1087.

- Fernández-Villaverde, Rubio-Ramírez and Schorfheide (2016) Fernández-Villaverde, Jesús, Juan Francisco Rubio-Ramírez, and Frank Schorfheide. 2016. “Solution and estimation methods for DSGE models.” In Handbook of macroeconomics. Vol. 2, 527–724. Elsevier.

- Flury and Shephard (2011) Flury, Thomas, and Neil Shephard. 2011. “Bayesian inference based only on simulated likelihood: particle filter analysis of dynamic economic models.” Econometric Theory, 27(5): 933–956.

- Gallant and Tauchen (1996) Gallant, A Ronald, and George Tauchen. 1996. “Which moments to match?” Econometric theory, 12(4): 657–681.

- Glöckler, Deistler and Macke (2021) Glöckler, Manuel, Michael Deistler, and Jakob H Macke. 2021. “Variational methods for simulation-based inference.”

- Goodfellow et al. (2014) Goodfellow, Ian, Jean Pouget-Abadie, Mehdi Mirza, Bing Xu, David Warde-Farley, Sherjil Ozair, Aaron Courville, and Yoshua Bengio. 2014. “Generative adversarial nets.” Advances in neural information processing systems, 27.

- Gourieroux, Monfort and Renault (1993) Gourieroux, Christian, Alain Monfort, and Eric Renault. 1993. “Indirect inference.” Journal of applied econometrics, 8(S1): S85–S118.

- Greenberg, Nonnenmacher and Macke (2019) Greenberg, David, Marcel Nonnenmacher, and Jakob Macke. 2019. “Automatic posterior transformation for likelihood-free inference.” 2404–2414, PMLR.

- Haan and Uhlendorff (2006) Haan, Peter, and Arne Uhlendorff. 2006. “Estimation of multinomial logit models with unobserved heterogeneity using maximum simulated likelihood.” The Stata Journal, 6(2): 229–245.

- Hajivassiliou et al. (1997) Hajivassiliou, Vassilis A, et al. 1997. Some practical issues in maximum simulated likelihood. Suntory-Toyota International Centre for Economics and Related Disciplines ….

- He, Whited and Guo (2021) He, Li, Toni M Whited, and Ran Guo. 2021. “Relative Performance Evaluation and Strategic Competition.” Available at SSRN 3287143.

- Hennessy and Whited (2007) Hennessy, Christopher A, and Toni M Whited. 2007. “How costly is external financing? Evidence from a structural estimation.” The Journal of Finance, 62(4): 1705–1745.

- Herbst and Schorfheide (2014) Herbst, Edward, and Frank Schorfheide. 2014. “Sequential Monte Carlo sampling for DSGE models.” Journal of Applied Econometrics, 29(7): 1073–1098.

- Herbst and Schorfheide (2015) Herbst, Edward P, and Frank Schorfheide. 2015. Bayesian estimation of DSGE models. Princeton University Press.

- Hermans, Begy and Louppe (2020) Hermans, Joeri, Volodimir Begy, and Gilles Louppe. 2020. “Likelihood-free mcmc with amortized approximate ratio estimators.” 4239–4248, PMLR.

- House and Leahy (2004) House, Christopher L, and John V Leahy. 2004. “An sS model with adverse selection.” Journal of Political Economy, 112(3): 581–614.

- Huang et al. (2018) Huang, Chin-Wei, David Krueger, Alexandre Lacoste, and Aaron Courville. 2018. “Neural autoregressive flows.” 2078–2087, PMLR.

- Huggett (1993) Huggett, Mark. 1993. “The risk-free rate in heterogeneous-agent incomplete-insurance economies.” Journal of economic Dynamics and Control, 17(5-6): 953–969.

- Hyvärinen and Pajunen (1999) Hyvärinen, Aapo, and Petteri Pajunen. 1999. “Nonlinear independent component analysis: Existence and uniqueness results.” Neural networks, 12(3): 429–439.

- Judd et al. (2017) Judd, Kenneth L, Lilia Maliar, Serguei Maliar, and Inna Tsener. 2017. “How to solve dynamic stochastic models computing expectations just once.” Quantitative Economics, 8(3): 851–893.

- Kaji, Manresa and Pouliot (2020) Kaji, Tetsuya, Elena Manresa, and Guillaume Pouliot. 2020. “An adversarial approach to structural estimation.” arXiv preprint arXiv:2007.06169.

- Keane and Wolpin (1994) Keane, Michael P, and Kenneth I Wolpin. 1994. “The solution and estimation of discrete choice dynamic programming models by simulation and interpolation: Monte Carlo evidence.” the Review of economics and statistics, 648–672.

- Khan and Thomas (2008) Khan, Aubhik, and Julia K Thomas. 2008. “Idiosyncratic shocks and the role of nonconvexities in plant and aggregate investment dynamics.” Econometrica, 76(2): 395–436.

- Kristensen and Shin (2012) Kristensen, Dennis, and Yongseok Shin. 2012. “Estimation of dynamic models with nonparametric simulated maximum likelihood.” Journal of Econometrics, 167(1): 76–94.

- Kukackaa and Barunika (n.d.) Kukackaa, Jiri, and Jozef Barunika. n.d.. “Non-Parametric Simulated Maximum Likelihood Estimation of Parameters in Heterogeneous Agent ModelsI Preliminary Draft Version: May 19, 2015.”

- Lerman and Manski (1981) Lerman, Steven, and Charles Manski. 1981. “On the use of simulated frequencies to approximate choice probabilities.” Structural analysis of discrete data with econometric applications, 10: 305–319.

- Liu and Plagborg-Møller (2021) Liu, Laura, and Mikkel Plagborg-Møller. 2021. “Full-information estimation of heterogeneous agent models using macro and micro data.” arXiv preprint arXiv:2101.04771.

- Li, Swersky and Zemel (2015) Li, Yujia, Kevin Swersky, and Rich Zemel. 2015. “Generative moment matching networks.” 1718–1727, PMLR.

- Lucas Jr (1978) Lucas Jr, Robert E. 1978. “Asset prices in an exchange economy.” Econometrica: journal of the Econometric Society, 1429–1445.

- Matzkin (2003) Matzkin, Rosa L. 2003. “Nonparametric estimation of nonadditive random functions.” Econometrica, 71(5): 1339–1375.

- McFadden (1989) McFadden, Daniel. 1989. “A method of simulated moments for estimation of discrete response models without numerical integration.” Econometrica: Journal of the Econometric Society, 995–1026.

- Ottonello and Winberry (2020) Ottonello, Pablo, and Thomas Winberry. 2020. “Financial heterogeneity and the investment channel of monetary policy.” Econometrica, 88(6): 2473–2502.

- Pakes and Pollard (1989) Pakes, Ariel, and David Pollard. 1989. “Simulation and the asymptotics of optimization estimators.” Econometrica: Journal of the Econometric Society, 1027–1057.

- Papamakarios and Murray (2016) Papamakarios, George, and Iain Murray. 2016. “Fast -free inference of simulation models with bayesian conditional density estimation.” Advances in neural information processing systems, 29.

- Parra-Alvarez, Posch and Wang (2020) Parra-Alvarez, Juan Carlos, Olaf Posch, and Mu-Chun Wang. 2020. “Estimation of heterogeneous agent models: A likelihood approach.”

- Pompe, Holmes and Łatuszyński (2020) Pompe, Emilia, Chris Holmes, and Krzysztof Łatuszyński. 2020. “A framework for adaptive MCMC targeting multimodal distributions.” The Annals of Statistics, 48(5): 2930–2952.

- Rezende and Mohamed (2015) Rezende, Danilo, and Shakir Mohamed. 2015. “Variational inference with normalizing flows.” 1530–1538, PMLR.

- Rubin (1984) Rubin, Donald B. 1984. “Bayesianly justifiable and relevant frequency calculations for the applied statistician.” The Annals of Statistics, 1151–1172.

- Smets and Wouters (2007) Smets, Frank, and Rafael Wouters. 2007. “Shocks and frictions in US business cycles: A Bayesian DSGE approach.” American economic review, 97(3): 586–606.

- Smith Jr (1993) Smith Jr, Anthony A. 1993. “Estimating nonlinear time-series models using simulated vector autoregressions.” Journal of Applied Econometrics, 8(S1): S63–S84.

- Taylor (2013) Taylor, Lucian A. 2013. “CEO wage dynamics: Estimates from a learning model.” Journal of Financial Economics, 108(1): 79–98.

- Tejero-Cantero et al. (2020) Tejero-Cantero, Alvaro, Jan Boelts, Michael Deistler, Jan-Matthis Lueckmann, Conor Durkan, Pedro J. Gonçalves, David S. Greenberg, and Jakob H. Macke. 2020. “sbi: A toolkit for simulation-based inference.” Journal of Open Source Software, 5(52): 2505.

- Terry (2017) Terry, Stephen J. 2017. “Alternative methods for solving heterogeneous firm models.” Journal of Money, Credit and Banking, 49(6): 1081–1111.

- Terry, Whited and Zakolyukina (2022) Terry, Stephen J, Toni M Whited, and Anastasia A Zakolyukina. 2022. “Information versus investment.” National Bureau of Economic Research.

- Wainwright and Jordan (2008) Wainwright, Martin J, and Michael Irwin Jordan. 2008. Graphical models, exponential families, and variational inference. Now Publishers Inc.

- Winberry (2018) Winberry, Thomas. 2018. “A method for solving and estimating heterogeneous agent macro models.” Quantitative Economics, 9(3): 1123–1151.

- Xu et al. (2015) Xu, Bing, Naiyan Wang, Tianqi Chen, and Mu Li. 2015. “Empirical evaluation of rectified activations in convolutional network.” arXiv preprint arXiv:1505.00853.

Appendix A Economic Models

The models used to test these algorithms are disparate. I estimate a relatively standard RBC model via time iteration, a model of capital formation solved via value function iteration, a Lucas Tree model (Lucas Jr, 1978) solved with projection, the linearized Smets-Wouters 2007 model, a HANK model solved via Rieter’s method with time iteration and lastly a 11 parameter bequests model solved via value function iteration. I will now discuss each of these models sequentially.

AA. The RBC Model

This RBC model is standard and comes from Alisdair McKay’s note on heterogeneous agent models: https://alisdairmckay.com/Notes/HetAgents/index.html.

The utility function is a standard CRRA utility:

| (5) |

The production function is standard Cobb-Douglas with productivity:

| (6) |

Where is fixed labor and is productivity and is capital which evolves according to a standard law of motion:

| (7) |

Productivity evolves according to a AR(1) process in logs:

| (8) |

This model is solved via time iteration and matches consumption, investment, productivity to real data, interest rates and capital are the latent unobserved variables. This is done on data both synthetic and real.

AB. The Model of Capital Formation

This model is a straightforward infinite horizon partial equilibrium model with risk neutral managers choosing investment to maximize the present value of a stream of firm cash flows and comes from solution code written by Emil Lakkis and Toni Whited.

Utility/cash flows are give by this formula:

| (9) |

Where , , and are the same as in the RBC model–capital, productivity and investment respectively. is the profit function.

The capital law of motion is like the RBC model:

| (10) |

Productivity evolves according to a AR(1) process in logs:

| (11) |

Profit is defined as:

| (12) |

This model shares similarities with the RBC model, with the main difference being the utility function and the value function solution method. This estimation method matches capital levels generated by a parameterized model.

AC. Lucas Asset Pricing Projection Model

Each agent maximizes CRRA utility:

with set to 3. The law of motion is:

The state of the system is defined as dividends received plus price of the amount of assets owned:

Putting these three equations together one gets the pricing kernel:

Dividends evolve under an process:

Where is a shock with standard deviation . When behaving optimally, consumption also equals the dividends received. This model matches the expected return and risk free rate at a variety of dividend levels, which demonstrates the ability of this model to not only estimate on models solved via projection, but also to work on cross sectional problems as well.

AD. Smets-Wouters 2007 Model

This section will mainly illustrate the equations and the parameters so one can cross reference parameters shown in the diagram with the correct equation in the DSGE model. This model comes from the paper Smets and Wouters (2007). More details on the economics of the equations can be found there.

First, a brief discussion of the overview of the model. The model is a representative New Keynesian model with stickiness in both wages and prices. The model has a flexible price set of equations which determines potential GDP for monetary policy and a sticky price system with a price markup equation that determines the true economy. I will only be discussing the sticky price system of equations with an implicit understanding that there is a mirroring flexible price system. Shocks all have autoregressive components to more accurately match data. All equations are linearized.

The aggregate resource constraint is:

| (13) |

The Euler equation is given by:

| (14) | ||||

The investment Euler equations are:

| (15) |

The arbitrage equation for the value of the capital stock is:

| (16) | ||||

The linearized production function is:

| (17) |

Capital utilization:

| (18) |

Capital utilization is some function of the interest rate for capital:

| (19) |

Capital’s law of motion is:

| (20) |

The markup equation is:

| (21) |

This equation is the only set of economic equations that doesn’t have a flexible price counterpart. Note that the observed variable equations also will not have a flexible price counterpart.

The New Keynesian Phillips curve:

| (22) | ||||

The rental rate of capital equation:

| (23) |

The path of wages is:

| (24) | ||||

The Taylor rule followed by central banks is:

| (25) |

The observed variables equations are:

| (26) | |||

| (27) | |||

| (28) | |||

| (29) | |||

| (30) | |||

| (31) | |||

| (32) |

The autoregressive equations for shocks are:

| (33) | |||

| (34) | |||

| (35) | |||

| (36) | |||

| (37) | |||

| (38) | |||

| (39) | |||

| (40) | |||

| (41) |

Some of the higher level parameters in the above equations are also related to the parameters in my diagram by the following equations:

| (42) | |||

| (43) | |||

| (44) | |||

| (45) | |||

| (46) | |||

| (47) | |||

| (48) | |||

| (49) | |||

| (50) | |||

| (51) | |||

| (52) | |||

| (53) | |||

| (54) | |||

| (55) | |||

| (56) | |||

| (57) | |||

| (58) | |||

| (59) |

The seven observed equations , , , , , , , are matched using data simulated from a model with true parameters equal to the Smets-Wouters 2007 mean parameters, with slight modifications as some parameters were calibrated to 0.

AE. The HANK Model

The HANK model also comes from Alisdair McKay’s tutorial, which adds a heterogeneous distribution of wealth as a state variable for households combined with a New Keynesian backbone.

Preferences are still CRRA, like the RBC model. The firm side is now new Keynesian with intermediate goods produced via:

| (60) |

Here is aggregate productivity and is labor employed by firm j producing variety . The final good is produced via the Dixit-Stiglitz aggregator Dixit and Stiglitz (1977):

| (61) |

Here is the elasticity of substitution between intermediates.

Output is defined as,

Where is the labor for the individual intermediate goods. Additionally from the accounting identity, output is also,

Where the second term is hiring costs.

Government and bonds are defined by the following nominal and real budget constraint equations:

| (62) | |||

| (63) |

Labor market is a standard McCall Search model:

| (64) | |||

| (65) | |||

| (66) | |||

| (67) |

The household maximizes the CRRA utility like the RBC model. The households budget constraint in real money is:

| (68) |

Here is savings and is the interest rate as determined by the bond market clearing condition. Earnings are given by:

| (69) |

Here is wages, is dividend income and is unemployment benefits.

The stochastic matrix governing employment, unemployment transitions is given by:

| (70) |

Again is governed by the labor market equations above.

The firm solves the Dixit-Stiglitz cost problem:

| (71) |

with price index given by

| (72) |

The Calvo pricing adjustment parameter implies that the intermediate firm chooses price to maximize:

| (73) |

Here denotes employment at firm in time . denotes hiring and denotes the real interest rate discounted periods back to time . This model is solved using Reiter’s method in combination with time iteration. This model matches unemployment and interest rate to the same data generated by a parameterized model, only two observed variables are used as the model only had two shocks.

AF. The Value Function Iteration Bequests Model

Finally this is a model of bequests over time. The model illustrates the benefit of my approach as it cannot be estimated by perturbation because of the kink at the intersection of the consumption versus adjusting illiquid savings intersection. Thus one has to use simulation-based inference to estimate this model solved via value function iteration.

This model comes from Jeppe Druedahl’s open source model example: https://github.com/pkofod/vfi/blob/master/Fast%20VFI.ipynb. The utility function is:

| (74) |

Here is bequest or non-liquid savings. is consummation. are all parameters. The bequest utility function (end of life utility) is:

| (75) |

Here is liquid savings and are all parameters. The value function is give by:

| (76) | |||||

| (77) | s.t. | ||||

| (78) |

Here is beginning of period liquid savings (analogous to end of period ) and is beginning of period illiquid savings (analogous to end of period ). is the pooled value of total liquid and illiquid savings. is labor income. The post-decision value function is:

| (79) | |||||

| (80) | |||||

| (81) | s.t. | ||||

| (82) | |||||

| (83) | |||||

| (84) | |||||

| (85) |

Here labor income comes from a distribution . Likewise are all parameters. The keep value function is:

| (86) | |||||

| (87) | s.t. | ||||

| (88) | |||||

| (89) |

The keep value function is the value function at a point if the agent chooses to consume and not withdraw or deposit funds into the illiquid asset, . The adjust value function is:

| (90) | |||||

| (91) | s.t. | ||||

| (92) | |||||

| (93) |

The adjust value function is the value of adjusting the illiquid asset. Notice the agent is unable to consume this period. This model with it’s nonlinear and kinked decision rule cannot be effectively modeled with a method like perturbation. Even so, I use my estimation technique to get a Bayesian posterior distribution. This model matches the liquid asset, illiquid asset and consumption to synthetic data generated by a model.

Appendix B Background on Simulation Neural Ratio Estimators

BA. General Approach of simulation-based Inference

The differences between the two simulation-based inference approaches roughly centers around what conditional density estimator to use. Sequential Neural Ration Estimators (SNRE) uses a GAN and Sequential Neural Posterior Estimators (SNPE) use a normalizing flow. While one can sample a lot of points from the joint, an iterative approach where one fits the density estimator on sampled data then re-samples leads to lower variance. I will start discussing SNRE, by introducing the GAN

BB. Generative Adversarial Networks

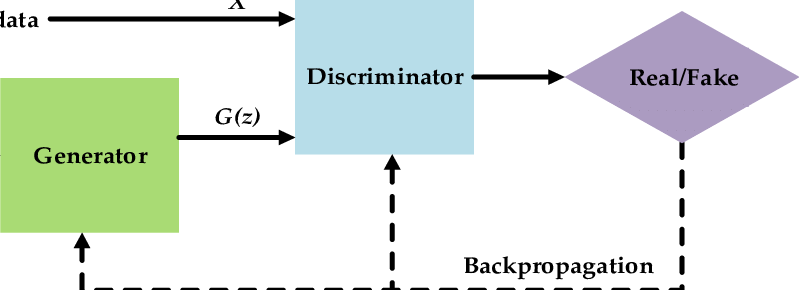

The GAN is an algorithm that uses two competing models moving in tandem to generate data that matches data generated from the real world (Goodfellow et al., 2014). Below is a diagram describing the structure of a basic GAN:

The generator is a neural network (or any differentiable model like a dynamic macro model) which attempts to produce data (unconditionally or conditionally via some inputs ) that resembles data in the real world. The discriminator is another neural network (or any trainable model that can produce a logistic output), which outputs the probability a given input data comes from the underlying data generating process and not from the generator. The two networks play a game where the objective of the generator is to convince the discriminator to assign high likelihood to its output and the objective of the discriminator is to assign the correct probabilistic label, a number between 0 or 1, to input that is either generated data or real data. One way to think about a GAN as a simulated method of moments algorithm where the moment conditions automatically evolve over many rounds to pick the most mismatched moments between the true data and the model. When thought in this way, it’s intuitive to recognize that the GAN is nearly a full information and efficient estimation procedure. For more thorough proofs see Kaji, Manresa and Pouliot (2020).

More mathematically, the objective of the discriminator is to minimize a logit loss of input that comes either from real data , or the generator where the are shocks that generate stochasticity in the GANs generation. Mathematically the discriminator loss is:

| (94) |

This is just a logit loss applied to data either coming from the data generating process or the generator. Likewise the generator’s loss is to fool the discriminator:

| (95) |

These two loss functions can be compactly represented as:

| (96) |

Equation 96 makes it clear the GAN objective is a minimax game with a solution that is a Nash equlibrium. However what is important for simulation-based estimation is to recover likelihoods/probabilities. The next proposition following Goodfellow et al. (2014) will show how to do that:

Proposition 1.: For a fixed generator, the optimal discriminator will produce a logistic output:

| (97) |

Proof: Using equation 94, for the loss of the generator:

| (98) | ||||

| (99) |

Any discriminator that maximizes the integral: , maximizes the integral pointwise over all . Thus the optimal discriminator will set the first order condition of the intergrand to zero:

| (101) |

Rearranging equation 101 gets the result of the proposition.

Then one can use this proposition along with the discriminator output to estimate a likelihood ratio.

BC. Sequential Neural Ratio Estimation

In SNRE, Durkan, Murray and Papamakarios (2020) use a GAN, not to match a underlying data like in proposition 1, but to contrast between two different distributions to estimate a density. In macro, the dataset is typically a single data point with correlated timesteps. Using a GAN to discriminate between real data and fake data would not work because the GAN would learn a delta function for the real data. In order to ameliorate this, the authors use contrastive learning where they differentiate between the generated distribution and the independent distribution, , where x is sampled uniformly from the empirical distribution of simulated data. Then they contrast the independent distribution, with the true joint: . Furthermore, knowing the optimal discriminator gives the ratio discussed in 97. The authors then recover the ratio: , using the fact that equals . Thus, the density of the posterior , where is the prior. This extends Kaji, Manresa and Pouliot (2020) GAN approach in allowing estimation of models with a latent time dimension. One can extend this to multi-round inference where one uses the GAN as a better proposal distribution than the prior, by sampling from the GAN using MCMC. Then one uses importance sampling to deal with the mismatch in proposal distribution and prior. See Durkan, Murray and Papamakarios (2020), Hermans, Begy and Louppe (2020) and the SNRE theoretical sections of the appendix for more information.

Appendix C Proofs

CA. Outline

There are two main parts of this section: 1.) How the Bayesian estimation procedure works, 2.) The estimation procedure with the normalizing flow density estimator.

CB. Bayesian Estimation

The Bayesian estimation procedure assumes the existence of a suitable density estimator that has all the properties of the normalizing flow. It will be convenient to assume the properties of the normalizing flow as stated which will be proved in the normalizing flow section (following Huang et al. (2018)).

The first step is to draw samples from the joint distribution and I will show this is possible. Since , the best procedure is to draw from the prior, then draw from the likelihood . This draws one sample from the joint distribution. Since the posterior is defined as , if one can fit a conditional density estimator on on the joint samples one can get the posterior distribution of by conditioning with the true data, .

This procedure is enough to generate samples from the posterior distributions. However, this procedure has high variance if the prior is far away from the posterior as you are sampling in places where the posterior has little mass. A more computationally efficient way is to sample in multiple rounds. In the first round one uses the prior distribution, however in later rounds one samples from a proposal distribution which should be the most updated guess on the posterior (denoted with a hat) , then one adjusts via importance sampling for the fact that is not the same as .

Theorem 5 In multi-round simulation-based inference, estimating from a proposal distribution rather than a prior requires adding an adjustment factor to the density estimation of samples produced. Assuming the flow, , can converge to any probability distribution in distribution (Theorem 9), then when one fits to the data sampled from the proposal distribution , one will converge to the true posterior

Proof: In order to perform the adjustments note that . Call the incorrect proposal distribution and define which is the conditional distribution that would be obtained by naively training a conditional estimator on the joint that contains the incorrect proposal distribution. Then

| (102) |

Since the joint distribution with the differing proposal distribution has a pdf of so the conditional distribution which one is drawing samples from has pdf . If one is fitting a density estimator on the differing proposal joint data via maximum likelihood as one does with a normalizing flow, one will recover estimates the distribution . However, if one fits the density estimator (ie adjusting the likelihood by the importance weights), then converges to by the dominated convergence theorem. by eq 102.

In multi-round simulation-based inference, the prior is the first proposal distribution and the normalizing flow is the resulting first round estimate of the posterior: . Then for the second round , where the proposal is now the estimated posterior recovered in the first round evaluated at the real data. Later rounds iteratively replace the proposal with the estimated posterior recovered from the previous round (and importance sample). Because importance sampling requires the ratio: (), f needs to be both easily sampled from as well as having easily calculable pdf. A normalizing flow can do this, as illustrated in the below section.

CC. Normalizing Flows in Depth