remarkRemark \newsiamremarkhypothesisHypothesis \newsiamthmclaimClaim \headersA Lifted Framework for Sparse RecoveryY. Rahimi, S. H. Kang, and Y. Lou

A Lifted Framework for Sparse Recovery††thanks: Submitted to the editors DATE. \fundingThis work was partially funded by NSF CAREER 1846690 and Simons Foundation grant 584960.

Abstract

Motivated by re-weighted approaches for sparse recovery, we propose a lifted (LL1) regularization which is a generalized form of several popular regularizations in the literature. By exploring such connections, we discover there are two types of lifting functions which can guarantee that the proposed approach is equivalent to the minimization. Computationally, we design an efficient algorithm via the alternating direction method of multiplier (ADMM) and establish the convergence for an unconstrained formulation. Experimental results are presented to demonstrate how this generalization improves sparse recovery over the state-of-the-art.

keywords:

Compressed sensing, sparse recovery, reweighted L1, nonconvex minimization, alternating direction method of multipliers,65K10, 49N45, 65F50, 90C90, 49M20

1 Introduction

Compressed sensing [10] plays an important role in many applications including signal processing, medical imaging, matrix completion, feature selection, and machine learning [13, 15, 25]. One important assumption in compressed sensing is that a signal of interest is sparse or compressible. This allows for an efficient representation of high-dimensional data only by a few meaningful subsets. Compressed sensing often involves sparse recovery from an (under-determined) linear system that can be formulated mathematically by minimizing the “pseudo-norm,” i.e.,

| (1) |

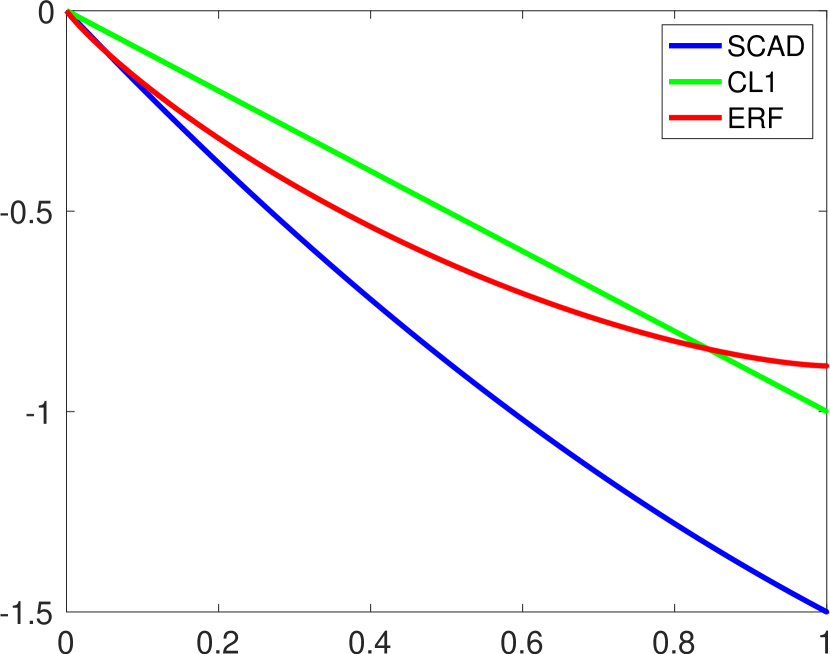

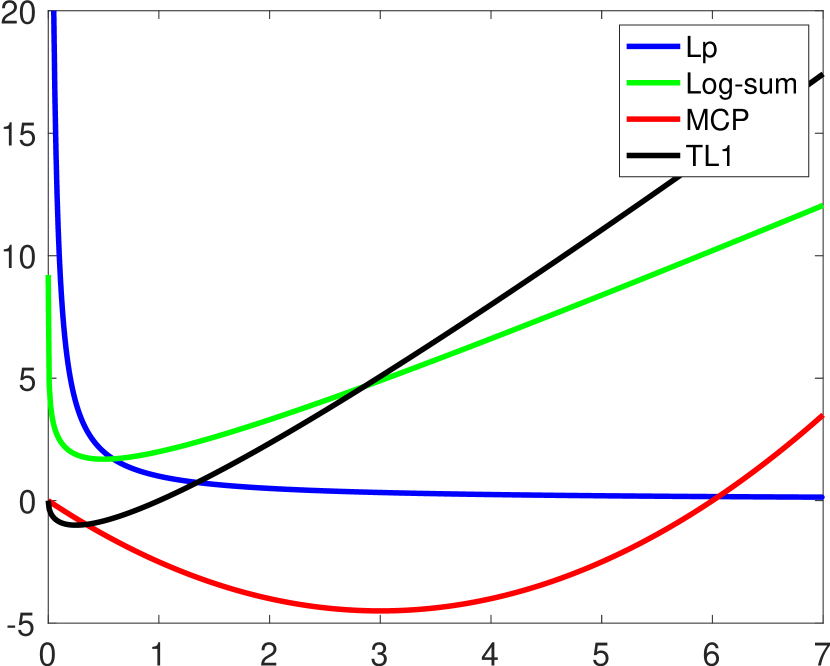

where is called a sensing matrix and is a measurement vector. Since the minimization problem (1) is NP-hard [26], various regularization functionals are proposed to approximate the penalty. The norm is widely used as a convex relaxation of which is called LASSO [33] in statistics or basis pursuit [9] in signal processing. Due to its convex nature, the norm is computationally traceable to optimize with exact recovery guarantees based on restricted isometry property (RIP) and/or null space property (NSP) [4, 11, 34]. Alternatively, there are non-convex models, i.e. concave with respect to the positive cone, that outperform the convex approach in practice. For example, [6, 39, 40], smoothly clipped absolute deviation (SCAD) [14], minimax concave penalty (MCP) [44], capped (CL1) [23, 32, 47], and transformed (TL1) [24, 45, 46] are separable and concave penalties. Some non-separable non-convex penalties include sorted [20], [21, 22, 41, 42], and [31, 36].

In this paper, we generalize a type of re-weighted approaches [5, 17, 38] for sparse recovery based on the fact that a convex function can be smoothly approximated by subtracting a strongly convex function from the objective [27]. In particular, we propose a lifted regularization, which we referred to as lifted (LL1),

| (2) |

where we denote and is the standard Euclidean inner product. In (2), the variable plays the role of weights with as a set of restrictions on , e.g., or . The function is decreasing near zero (please refer to Definition 2.1 for multi-variable decreasing function) to ensure a non-trivial solution of (2), and is a parameter. We also consider a more general function , instead of when making a connection of the proposed model to several existing sparse-promoting regularizations in Section 2.2. Note that “” is used instead of “” in (2), since we assume that the infimum is attained by at least one point.

To find a sparse signal from a set of linear measurements, we propose the following constrained minimization problem:

| (3) |

We lift the dimension of a single vector in the original problem (1) into a joint optimization over and in the proposed model (3). We can establish the equivalence between the two, if the function and the set satisfy certain conditions. For the measurements with noise, we also consider an unconstrained formulation, i.e.,

| (4) |

where is a balancing parameter.

From an algorithmic point of view, the lifted form enables us to minimize two variables each with fast implementation, and can lead to a better local minima in higher dimension than the original formulation [27, 43]. To minimize (3) and (4), we apply the alternating direction method of multipliers (ADMM) [3, 16], and conduct convergence analysis of ADMM for solving the unconstrained problem (4). We demonstrate in experiments that the proposed approach outperforms the state-of-the-art. Our contributions are threefold,

-

•

We propose a unified model that generalizes many existing regularizations and re-weighted algorithms for sparse recovery problems;

- •

-

•

We present an efficient algorithm which is supported by a convergence analysis.

The rest of the paper is organized as follows. In Section 2, we present details of the proposed model, including its properties with an exact sparse recovery guarantee. Section 3 describes the ADMM implementation and its convergence. Section 4 presents experimental results to demonstrate how this lifted model improves the sparse recovery over the state-of-the-art. Finally, concluding remarks are given in Section 5.

2 The Proposed Lifted Framework

We first introduce definitions and notations that are used throughout the paper. The connection to well-known sparsity promoting regularizations is presented in Section 2.2. We present useful properties of LL1 in Section 2.3, and establish its equivalence to the original problem in Section 2.4.

2.1 Definitions and Notations

We mark any vector in bold, specifically denotes the all-ones vector and denotes the zero vector. For a vector we define as the -th largest component of . We say that a vector majorizes with the notation if we have and . For two vectors the notation means each element of is smaller than or equal to the corresponding element in similarly for , and . The positive cone refers to the set . A rectangular subset of is a product of intervals. We define two elementwise operators, and both returning a vector form by taking maximum and multiplication respectively for every component. The proposed regularization (2) can be rewritten using the -functon as

| (5) |

We use (2) and (5) interchangeably throughout the paper. The constrained LL1 problem (3) is equivalent to

| (6) |

where . We denote as the set , as the symmetric group of elements, and a permutation of a vector is defined as We summarize relevant properties of a function as follows,

Definition 2.1.

Let be a function, we say that

-

•

the function is separable if there exists a set of functions for s.t.

-

•

The function is strongly convex with parameter if

(7) -

•

The function is symmetric if and .

-

•

The function is coercive if

-

•

The function is decreasing on if and .

2.2 Connections to Sparsity Promoting Models

Many existing models can be understood as a special case of the proposed LL1 model (3). We start by two recent works. One is a joint minimization model [48] between the weights and the vector,

| (8) |

where is a fixed number. With the assumption that the weights are binary, the authors [48] established the equivalence between (1) and (8) for a small enough . Another related work is the trimmed LASSO [1, 2],

which is equivalent to the LL1 form on the right with . In the middle, the sum is over the smallest components of the vector for a given sparsity .

In what follows, we consider a more general form of as opposed to i.e.,

| (9) |

As a consequence of Fenchel–Moreau’s theorem, regularizations that are concave on the positive cone are of the form Eq. 9. In other words, we have the following theorem:

Theorem 2.2.

Any proper and lower semi-continuous function that is concave on the positive cone can be lifted by a convex function and a set such that as in (9). Here and .

Please refer to Supplement for detailed computations and proof of Theorem 2.2. Using this idea, we relate (9) to the following functionals that are widely used to promote sparsity.

(i) The model [7] is defined as As , approaches to , while it reduces to for . Much research focuses on due to a closed-form solution [39, 40] in the optimization process. By choosing and , we can express the regularization as

(ii) The log-sum penalty [5] is given by for a small positive parameter to make the logarithmic function well-defined. The re-weighted algorithm [5] (IRL1) minimizes , which is equivalent to (9) in that

(iii) Smoothly clipped absolute deviation (SCAD) [14] is defined by

| (10) |

This penalty is designed to reduce the bias of the model. For and , we have is equivalent to

(iv) Mini-max concave penalty (MCP) [44] is defined by

| (11) |

Same purpose of reducing bias as SCAD, MCP consists of two piece-wise defined functions, which is simpler than SCAD. For and , we can rewrite as

(v) Capped (CL1) [47] is defined as with a positive parameter As the function approaches to The CL1 penalty is unbiased, and has less internal parameters than SCAD/MCP. For and , the CL1 regularization can be expressed as

It is similar to the model in [48], except for a binary restriction on as in (8).

(vi) Transformed (TL1) [24] is defined as It reduces to for and converges to as The TL1 regularization is Lipschitz continuous, unbiased, and equivalent to

(vii) Error function penalty (ERF) [17] is defined by

| (12) |

This model is less biased than and gives a good approximation to for a small value of . Let , then for and , the ERF function is equivalent to

| Model | Regularization | Function | Set |

|---|---|---|---|

| log-sum | |||

| SCAD | (10) | ||

| MCP | (11) | ||

| CL1 | |||

| TL1 | |||

| ERF | Eq. 12 |

We summarize these existing regularizations with their corresponding function and set in Table 1. All these functions are separable, and hence we can plot as a univariate function. As illustrated in Fig. 1, each function is decreasing on a small interval near origin, thus motivating the conditions on the function presented in Definition 2.10 as well as Theorems 2.11 and 2.13 for exact recovery guarantees.

2.3 Properties of the Proposed Regularization

There is a wide range of analysis related to concave and symmetric regularization functions based on RIP and NSP conditions [4, 11, 34, 35] regarding the sensing matrix . Our general model satisfies all the NSP-related conditions discussed in [35] so that the exact sparse recovery can be guaranteed. Theorem 2.3 summarizes some important properties of the proposed regularization.

Theorem 2.3.

For any and a feasible set on the weights defined in (2) has the following properties,

-

(i)

The function where denotes the convex conjugate of a function , thus is concave in the positive cone.

-

(ii)

If is symmetric on , then is symmetric on .

-

(iii)

If is separable on , then is separable on .

-

(iv)

If is separable and symmetric on , satisfies the increasing property on , i.e., for any , and reverses the order of majorization, i.e., if .

-

(v)

If is separable and is rectangular, then satisfies the sub-additive property on , i.e.,

The equality holds if and have disjoint support, and each coordinate of has the same minimum.

-

(vi)

Let be compact and continuous. Then is continuous and the set of sub-differentials of at the point is given by

where Conv is the convex hall of the points. In addition, the function is differentaible at the points where the minimizer is unique. Consequently, if is strongly convex, is continuously differentiable on the positive cone.

-

(vii)

If and takes its minimum value at some point in , then we have for that

Proof 2.4.

(i) Recall the convex conjugate of a function is defined as Comparing it to the definition in (2), we have . As convex conjugate is always convex, is concave on the positive cone.

(ii) If is symmetric, it is straightforward that is also symmetric.

(iii) Since is a separable function, breaks down into scalar problems, and hence is separable.

(iv) The increasing property follows from the fact that we have for every

Taking the minimum of both sides with respect to proves the increasing property. The reverse order of majorization can be proved in the same way as in [35, Proposition 2.10].

(v) The sub-additive property can be proved in the same way as in [35, Lemma 2.7].

(vi) It is straightforward that

| (13) |

for each . We set . As is continuous, the map is continuous for every , and for each , the function is continuous. For , it follows from Ioffe-Tikhomirov’s Theorem [18, Proposition 6.3] that

| (14) |

where .

(vii) Given with , we denote which implies and It further follows from that . For , we have and hence

Using proprieties (i)-(v), we can prove that every -sparse vector is the unique solution to (3) if and only if satisfies the generalized null space property (gNSP) of order . Please refer to [35, Theorem 4.3] for more details on gNSP. As for the property (vii), it has algorithmic benefits, as many optimization algorithms are designed for continuously differentiable functions. We show in Theorem 2.5 that is related to and if is separable (without the assumption of strong convexity on ). The relationship of to iteratively re-weighted algorithms, e.g., [5, 17] is characterized in Theorem 2.8.

Theorem 2.5.

Suppose and is separable, i.e., with each being a strictly decreasing function on with a bounded derivative. If and for , we have that for all ,

-

(i)

, as .

-

(ii)

, as .

Proof 2.6.

(i) For any fixed , we consider the derivative of with respect to each of its component, i.e., . If then is negative due to decreasing and hence the minimum is attained at . If , is positive for a small enough due to the assumption that is bounded. Then positive derivative implies that the function is increasing, and hence the minimum is attained at . In summary, if is sufficiently small, then we obtain that if and if . For this choice of we get that and

which implies that for a small enough that depends on the choice of . By letting , we have for all

(ii) Since there exists a value of with and so for large enough , the derivative is always negative. It further follows from the decreasing function that the minimizer is always attained at to reach to the desired result. Similarly to (i), by letting the analysis holds for all

Theorem 2.5 implies that the function approximates the norm from below. We can define a function of as a transformation between and for a fixed . As characterized in Corollary 2.7, this relationship motivates to consider a type of homotopic algorithm (discussed in Section 3) to better approximate the desired norm, although is not homotopy itself (it is not continuous with respect to ).

Corollary 2.7.

If is a decreasing sequence converging to zero and satisfies the conditions in Theorem 2.5, then a sequence of functions and are increasing, i.e.,

If we do not restrict all the functions attain the same value at as in Theorem 2.5, but rather can take different values, then the proposed regularization is equivalent to a weighted model with a certain shift of ; see Theorem 2.8.

Theorem 2.8.

Suppose and is separable, i.e., with each being a strictly decreasing function on with a bounded derivative. If and for , we have for all ,

| (15) |

In another words, for a sufficiently large , is approaching to a weighted model.

Proof 2.9.

Since each derivative is bounded, then there exists a positive number (depending on ) such that is negative for . As a result, the minimizer of is attained at . For a sufficiently large the minimizer . By letting Eq. 15 holds for all

2.4 Exact Recovery Analysis

There are many models approximating the minimization problem (1), and yet only a few of them have exact recovery guarantees. Motivated by the equivalence [48] between the model (1) and (8) with a sufficiently small parameter , we give conditions on the function to establish the equivalence between our proposed model (3) and (1). Note that the weight vector in our formulation is not binary, but takes continuous values. By taking Table 1 and Fig. 1 into account, we consider two types of functions defined as follows:

Definition 2.10.

Let be a separable function with for . We define

-

•

Type B: All functions have bounded derivatives on and are strictly decreasing on with the same value at and , i.e. there exist two constants such that

-

•

Type C: All functions are convex on with the same value at and with the same minimum at a point other than zero, i.e. there exist two constants such that and .

An important characteristic both types of functions share is that they are decreasing near zero. Type B functions are defined on a bounded interval, and we enforce a box constraint on for strictly decreasing . Type C refers to convex functions defined on an unbounded interval due to Note that Theorems 2.5 and 2.8 hold when is a Type B or Type C function. We establish the equivalent between (3) and (1) for Type B and Type C functions in Theorem 2.11 and Theorem 2.13, respectively.

Theorem 2.11.

Proof 2.12.

Since is a Type B function, we represent with each strictly decreasing and having bounded derivatives on Without loss of generality, we assume that and Denote and Here otherwise there exists a solution to (1) with sparsity less than . Since has bounded derivatives, there exists a scalar such that and .

Let be a solution of (3). If we obtain Therefore, is an increasing function on thus attaining its minimum at . As a result, we have ; otherwise is not a minimizer of (3). In addition, we have and , as is strictly decreasing. By combining two cases of and we estimate a lower bound of

where we use the assumptions of and together with by the definitions of and On the other hand, the lower bound for can be achieved by any solution of with sparsity , by choosing for and otherwise. Therefore, we have .

Next we show that must have sparsity . If for some , then we have Note that the inequality is strict, forcing to be strictly greater than the lower bound , which is a contradiction. Therefore, if we must have . Based on the definition of we have , which implies is a minimizer of (1).

Theorem 2.13.

Suppose and is a Type C function in Definition 2.10. Then there exists a constant such that the model (3) is equivalent to (1).

Proof 2.14.

We define , , and in the same way as in the proof of Theorem 2.11. Since is convex, is increasing and hence and . Then there exists a scalar such that . Without loss of generality, we assume . In this setting, we get

which implies that The rest of the proof follows exactly from the one of Theorem 2.11, thus omitted.

Remark 2.15.

In Theorems 2.11 and 2.13, we consider a linear constraint set All the analysis can be extended to a feasible set of inequality constraints, e.g., for . In this case, we can show that our model Eq. 6 with a given is equivalent to the following formulation,

| (16) |

3 Numerical Algorithms and Convergence Analysis

We describe in Section 3.1 the alternating direction method of multipliers (ADMM) [3, 16] for solving the general model, with convergence analysis presented in Section 3.2. In Section 3.3, we discuss closed-form solutions of the -subproblem for two specific choices of .

3.1 The Proposed Algorithm

We define a function to unify the constrained and the unconstrained formulations, i.e., for (3) and for (4). We introduce a new variable in order to apply ADMM to minimize

| (17) |

The corresponding augmented Lagrangian becomes

| (18) |

where is the Lagrangian dual variable and is a positive parameter. The ADMM scheme involves the following iterations,

| (19) |

The original problem (3) jointly minimizes and which are updated separately in (19). In particular, the -subproblem can be expressed as

| (20) |

In general, one may not find a closed-form solution to (20). For a separable function and a rectangular set , the -update simplifies into one-dimensional minimization problems; refer to Section 3.3 for the -update with two specific functions that are used in experiments. For the -update, it has a closed-form solution given by

where

For the constrained formulation, i.e., , the -subproblem becomes

It is equivalent to a projection into the affine solution of , which has a closed-form solution,

For the unconstrained formulation, , the -subproblem also has a closed-form solution by solving a linear system,

| (21) |

The ADMM iterations (19) minimize the general model (6) for a fixed value of . Following Theorem 2.5 and Corollary 2.7, we consider a type of homotopy optimization (also known as continuation approach) [12, 37] to update in order to better approximate the norm. In particular, we gradually decrease to while optimizing (17) for each . Algorithm 1 summarizes the overall iteration for the proposed approach.

Remark 3.1.

We remark that letting approach to is not exactly a homotopy algorithm, as the transformation between and is not continuous. We observe empirically the rate that decays to zero plays a critical role in the performance of sparse recovery. On the other hand, we should minimize to approximate the norm. This formulation requires the inversion of for different in the -update, which is computationally expensive, as opposed to pre-computing the inverse of with a fixed value

3.2 Convergence Analysis for ADMM

We prove the convergence for the ADMM method (19) for the unconstrained case, i.e., . In addition, we assume that is a Type B or Type C function that is continuously differentiable on . Note that we apply an adaptive update in Algorithm 1, but the convergence analysis is restricted to a fixed value.

In this case of Type C functions , and it follows from optimality conditions for each sub-problem in (19) that there exists and such that

| (22) |

with .

Note that for the Type B functions, and the optimality condition for sub-problem is that there exists such that and and .

Lemma 3.2.

Proof 3.3.

Theorem 3.4 (Sufficient decrease condition).

Proof 3.5.

The -update in (19) and Lemma 3.2 lead to

Using the -update in (19) and the last optimality condition in (22), we have

As for the -update, we get

where the last inequality comes from the definition of subgradient. For the -update, we use the fact that is a minimizer, hence

Adding all these inequalities yields the desired inequality (23) with . If , then leading to the sufficient decreasing of

Theorem 3.6 (Residue convergent).

Suppose the sequence is generated by (19). If is a Type B or Type C function with, , the following hold as

Proof 3.7.

Theorem 3.8 (Stationary points).

Proof 3.9.

Using from Lemma 3.2, i.e., we have

Consequently, we obtain that

| (24) |

If then , showing is lower bounded. On the other hand, Theorem 3.4 gives an upper bound of i.e., .

The boundedness of and together with (24) implies that is bounded, and hence is bounded due to Then the Bolzano-Weierstrass Theorem guarantees that there exists a subsequence, denoted by , that converges to a limit point, i.e.

Let be the corresponding variables in the optimality condition (22). As we know is bounded by Therefore, there exists a limit point of the sequence Without loss of generality, we assume it is the sequence itself, i.e., and hence we have .

Type C: If is a type C function then and hence the optimality condition for the update is with . We define

and so and (since is continuously differentiable). The optimality condition implies that . Since all the equations in (22) are continuous, we can replace by and take the limit as to get

where with , and . Hence, is a stationary point of . Furthermore, we have from the proof of Lemma 3.2, leading to . Together with we get

which means that is a stationary point of (4) for .

Type B: If is a type B function then and hence the optimality condition for the update is with and with and .

Note that we have . Since and is continuously differentiable hence the sequence is bounded and converges to the limit . Combining the boundedness of together with the optimality conditions, the sequences and must be bounded. Therefore, each sequence has a convergent sub-sequence and without loss of generality, we may assume it is the sequence itself, i.e., and . We must have

and and with the conditions and . The rest of the analysis is similar to the Type C functions and we get

which means is a stationary point of and

which means that is a stationary point of (4) for .

3.3 Algorithm updates for different functions

Here we consider two examples of functions, with which the -subproblem has a closed-form solution. We define one function as , a Type B function, with , and a Type C function with . For these combinations the update for (20) simplifies to

Note that for this choice of , the proposed model simplifies to

which can be solved by a quadratic programming with linear constraints and positive semi-definite matrix.

4 Numerical Experiments

We demonstrate the performance of Algorithm 1 with and two specific functions discussed in Section 3.3. We compare with the following sparsity promoting regularizations: [9], [8, 39], transformed (TL1) [45], [42], and ERF [17]. For each model, we consider both constrained and unconstrained formulations. Specifically for the model, we adopt the iteratively reweighted least-squares (IRLS) algorithm [8] in the constrained case, and use the half thresholding [39] as a proximal operator for minimizing the unconstrained formulation. Both and TL1 are minimized by the difference of convex algorithm (DCA) for the best performance as reported in [42, 45]. We use the online code provided by the authors of [17] to solve for the ERF model. We use the default values of model parameters suggested in respective papers; note that and do not involve any parameters. All the experiments are conducted on a Windows desktop with CPU (Intel i7-6700, 3.19GHz) and MATLAB (R2021a).

4.1 Constrained Models

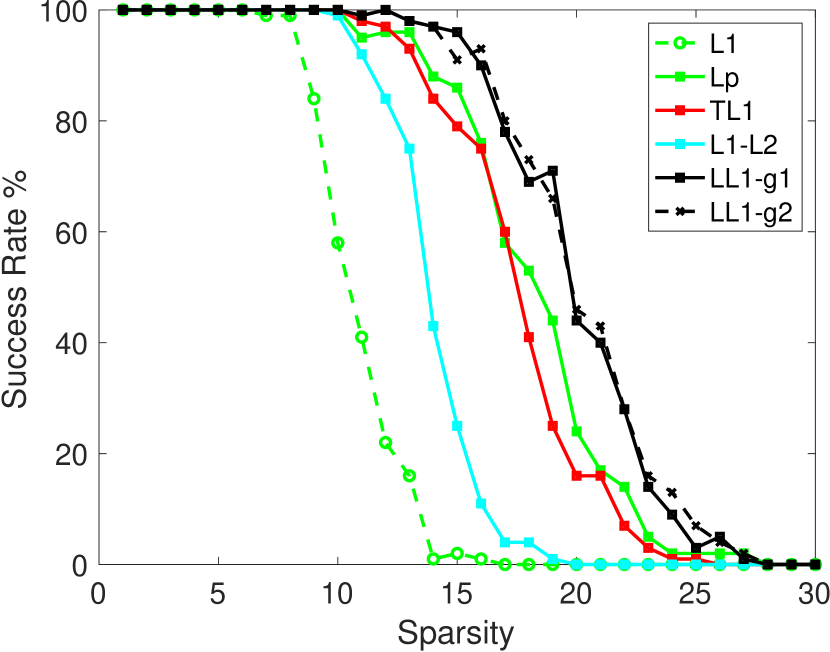

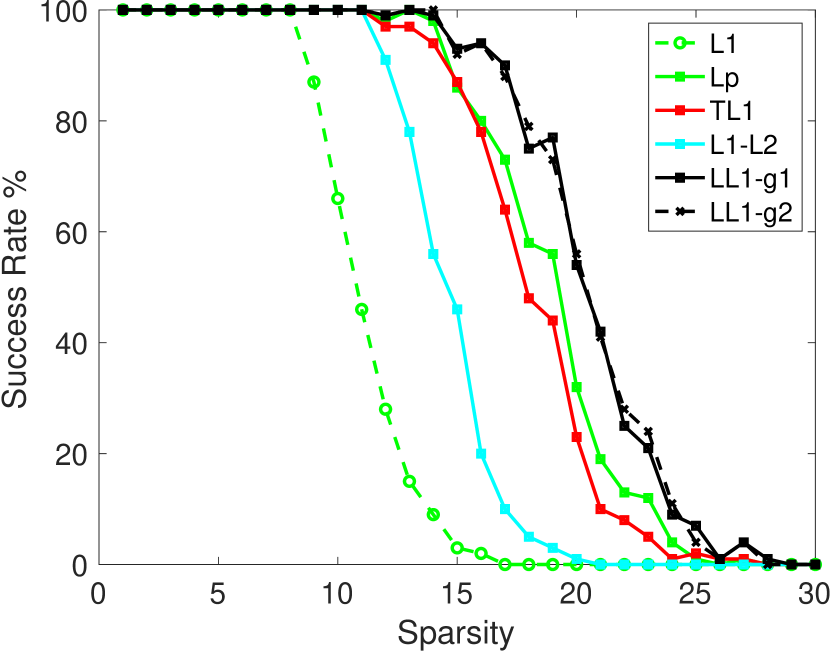

We examine the performance of finding a sparse solution that satisfies the constraint . We consider two types of sensing matrices, Gaussian and over-sampled discrete cosine transform (DCT). The Gaussian matrix is generated based on the multivariate normal distribution , where for a parameter The over-sampled DCT matrix is defined by with each column defined as

where is a uniformly random vector and is a scalar. The larger is, the larger the coherence of the matrix is, thus more challenging to find a sparse solution.

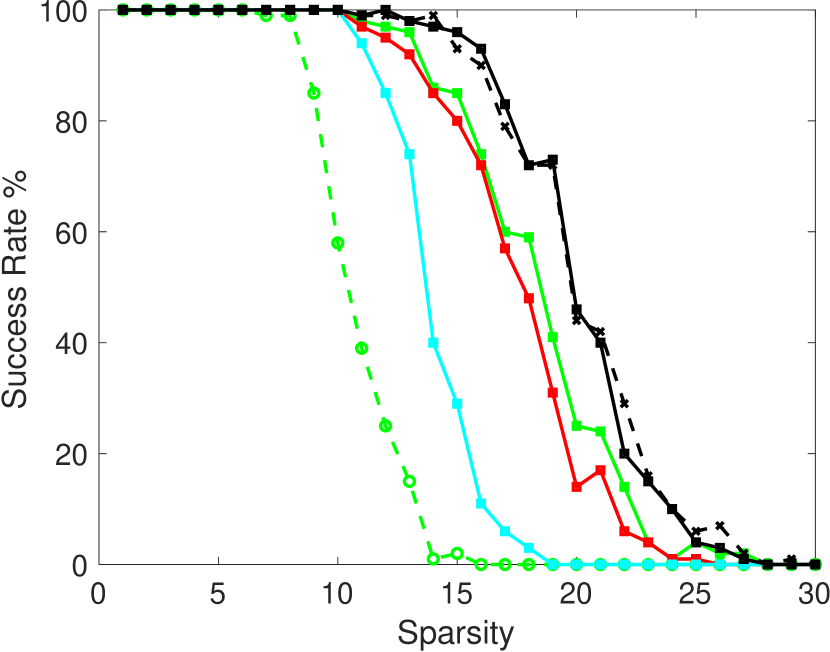

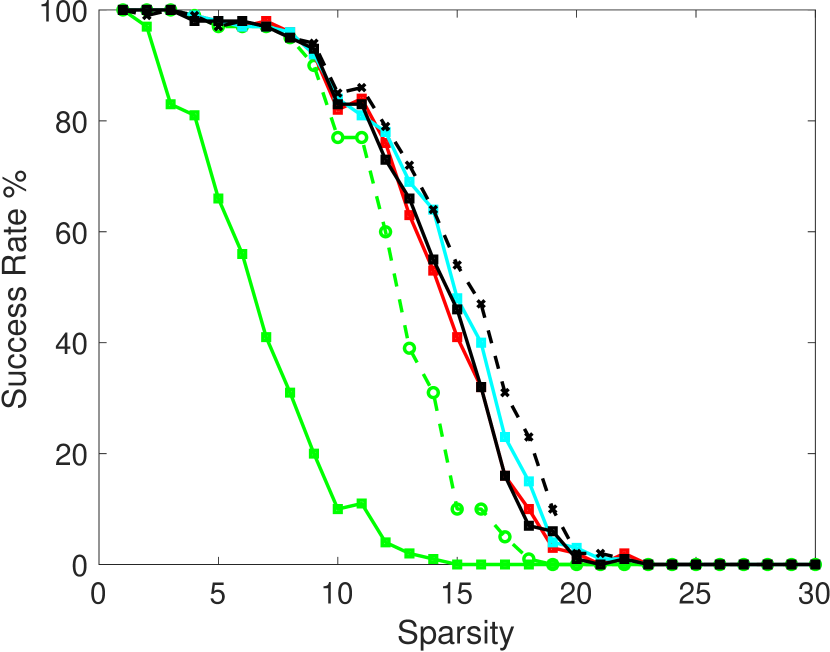

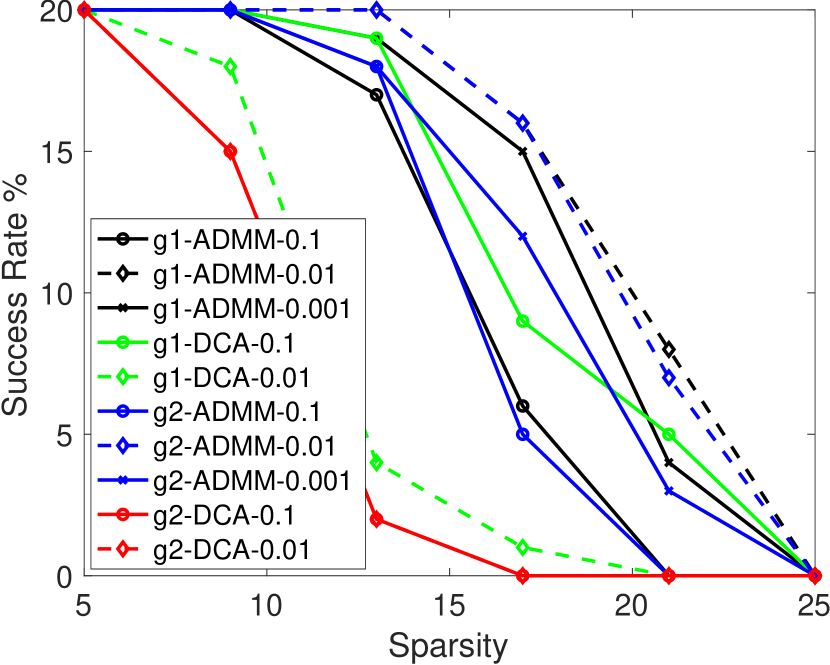

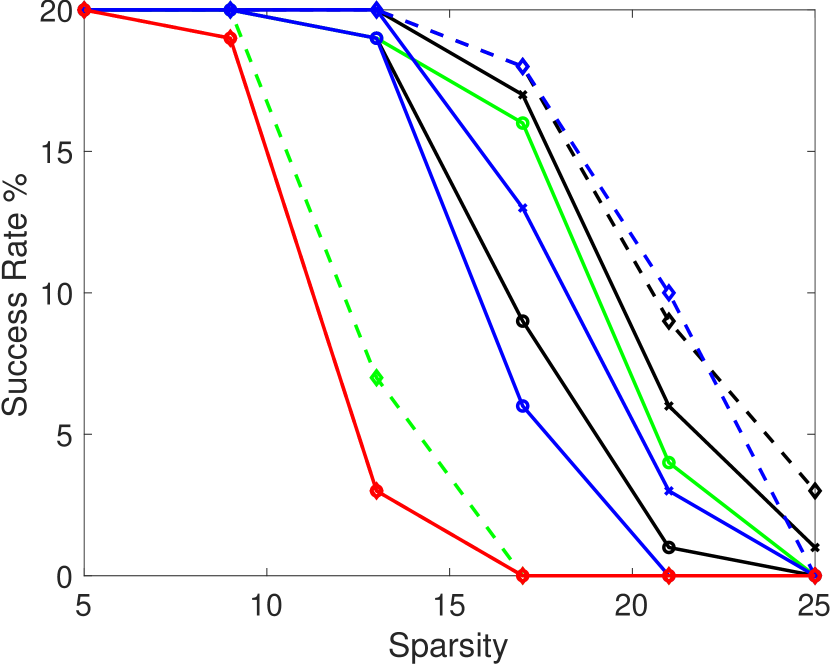

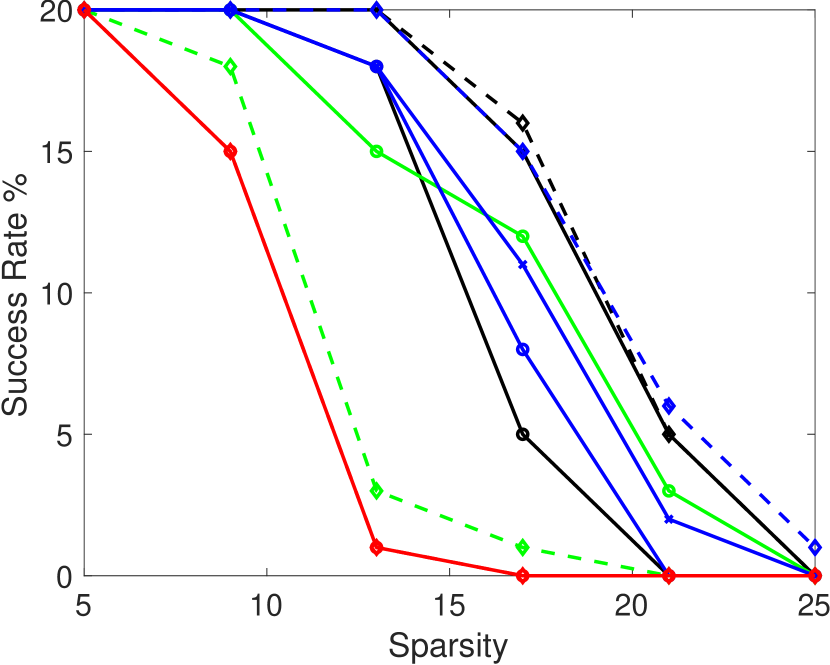

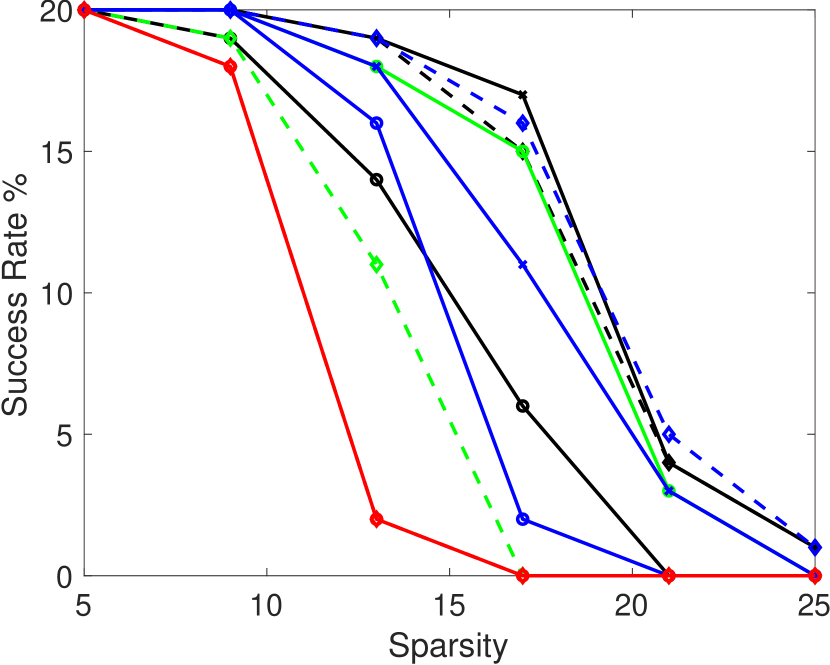

We fix the dimension as for Gaussian and DCT matrix, while generating Gaussian matrices with and DCT matrices with . The ground truth vector is simulated as -sparse signal, where is the total number of nonzero entries each drawn from normal distribution and the support index set is also drawn randomly. We evaluate the performance by success rates where a “successful” reconstruction refers to the case when the distance of the output vector and the ground truth is less than , i.e.

Fig. 2 presents success rates for both Gaussian and DCT matrices, and demonstrates that the proposed LL1 outperforms the state of the art in all the testing cases. For the Gaussian matrices, the parameter has little affect on the performance, as we observe the same ranking of these models under various values. As for the DCT matrices, the parameter influences the coherence of the resulting matrix. For smaller value, is the second best, while TL1 and perform well for coherent matrices (for ). With a well-chosen function, the proposed LL1 framework always achieves the best results among the competing methods. The results of LL1 using with and with are similar. This phenomenon illustrates that our model works best as it is equivalent to the model for small enough .

4.2 Unconstrained Models

We consider the unconstrained model for comparison on noisy data:

| (25) |

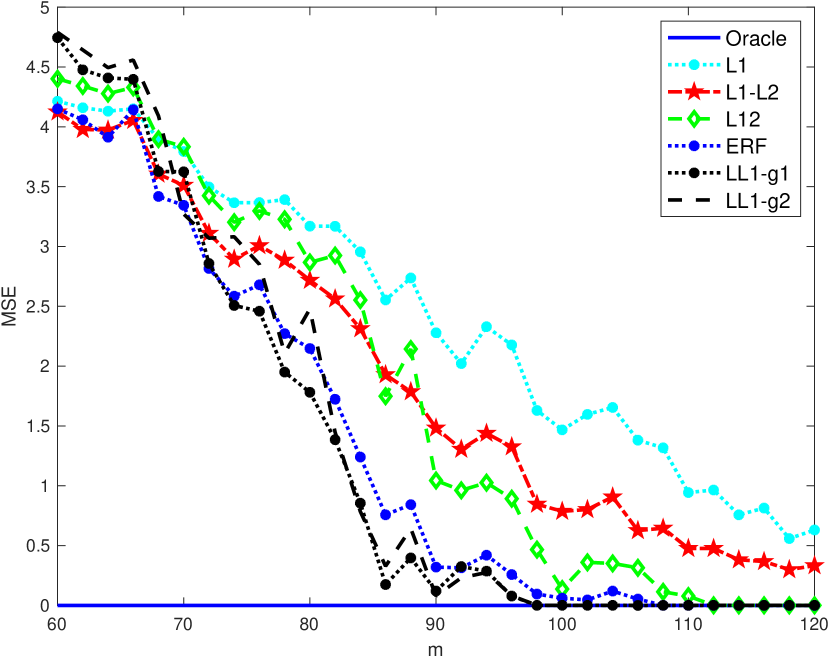

where is a regularization parameter. We consider signals of length with sparsity , and measurements , determined by a Gaussian sensing matrix . The columns of are normalized with mean zero and unit norm. A Gaussian noise with means zero and standard deviation is also added to the measurements. To evaluate the success rate of algorithms, we consider the mean-square-error (MSE) of the output signal with the ground-truth solution using the formula

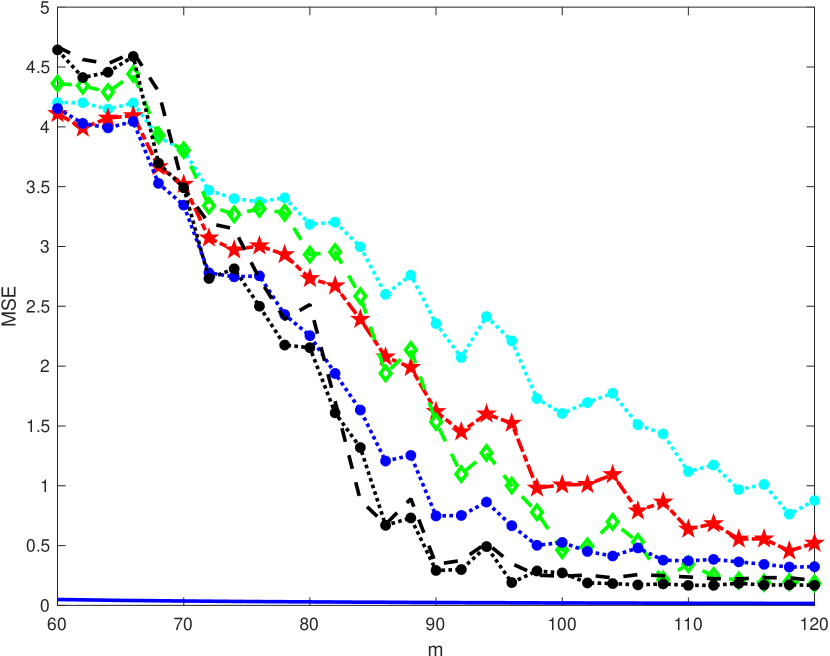

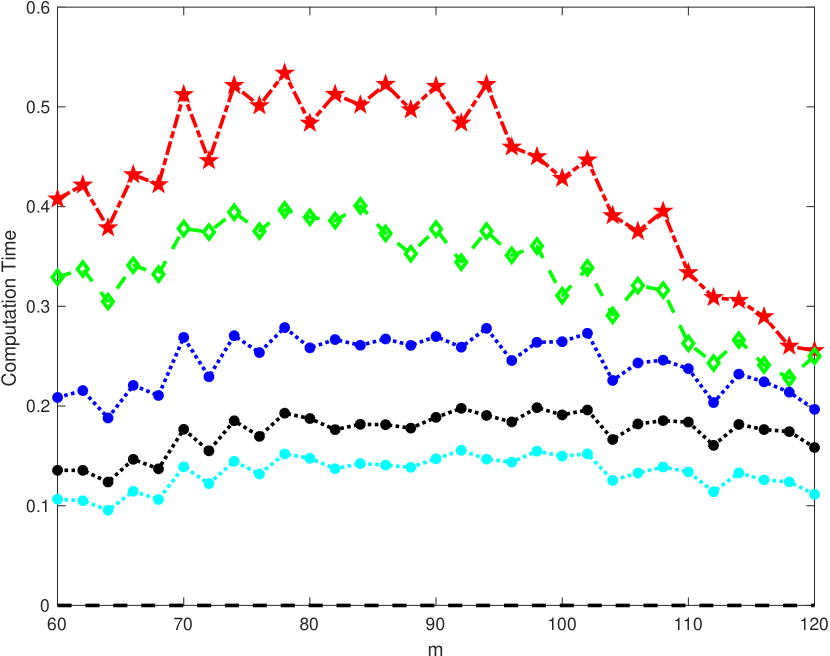

For each algorithm, we compute the average of MSE for 100 realizations by ranging the number of measurements between . Fig. 3 present the comparison results for two noise levels . All the algorithms perform badly with a few measurements, and as the number of measurements increases, their MSE error decreases. For the smaller amount of the noise (), our approach almost works perfectly in around measurements, while other algorithms either require more measurements to achieve the nearly perfect MSE or are unable to do so. Fig. 3(c) presents the computational times, which suggests that LL1 performs as fast as the model and at the same time it has the lowest recovery error.

When the noise level is high, for instance , then it is almost impossible to reconstruct the ground-truth signal using any number of measurements. In such cases, our algorithm finds a signal that is sparser and has smaller objective for any choice of the regularization parameter .

4.3 Comparing the ADMM and DCA based algorithms

Alternatively to ADMM, one can minimize the proposed model (3) and (4) by the difference of convex algorithm (DCA) [19, 29, 30]. More specifically, since our function is convex on the positive cone, then we use the algorithm introduced in [28], where we only need to find the sub-differential of the function on . We used the function to unify the constrained and the unconstrained formulations and we have the model

| (26) |

Since the function is concave on , it can be written as a difference of two convex functions, i.e., where and for An interesting fact about using a DCA form is that if is a Type B or Type C then for we have sub-differentials of the form

For , take then the DCA iterations become

| (27) |

We implement the DCA iterations of (27) for for its simplicity and efficiency as opposed to . In addition, we can consider an adaptive scheme to update which is adopted in Algorithm 2.

We compare ADMM (Algorithm 1) and DCA (Algorithm 2) for minimizing the same constrained formulation (3) with and discussed in Section 3.3. We are particularly interested in the algorithmic behaviors when dynamically updating . As mentioned in Theorem 2.11, is supposed to be small enough to approximate the solution. A common way involves an exponential decay in the form of for . If the parameter is close to then converges to zero too quickly and hence the algorithm cannot converge to a good local minimum as it is equivalent to having in the very beginning. On the other hand, if is close to then slowly decreases to zero; and as a result, Algorithm 1 may terminate before is small enough for to approximate the norm.

The comparison between ADMM and DCA on Gaussian and DCT matrices is presented in Fig. 4. By fixing we select the optimal for ADMM with that achieves the smallest relative error to the ground-truth. Then using the optimal parameters and Fig. 4 presents the ADMM results for and the DCA ones for . For all the cases, ADMM is superior to DCA in that it is less sensitive to . In addition, DCA consists of two loops and hence it is generally slower than ADMM. Our experiment shows that a suitable choice for our experiments is .

5 Concluding Remarks

In this paper, we proposed a lifted model for sparse recovery, which describes a class of regularizations. Specifically we established the connections of this framework to various existing methods that aim to promote sparsity of the model solution. Furthermore, we proved that our method can exactly recover the sparsest solution under a constrained formulation. We promoted the use of ADMM to solve for the proposed model with convergence analysis. An alternative approach of using DCA was discussed in Section 4.3, showing the efficiency of ADMM over DCA. Experimental results on both noise-free and noisy cases illustrate that the proposed framework outperforms the state-of-the-art methods in terms of accuracy and is comparable to the convex approach in terms of computational time.

One future work involves the convergence analysis of ADMM for solving the constrained model. One diffciculty lies in the fact that the corresponding function is a -function, which is not differentiable nor coercive, and as a result, the proof presented in Section 3.2 for the unconstrained minimization is not applicable for the constrained case. We observe that the ADMM algorithm for the constrained case does converge and the augmented Lagrangian is decreasing. This empirical evidence suggests the potential to prove the convergence or sufficiently decreasing of the augmented Lagrangian, which will be left as a future work.

References

- [1] T. Amir, R. Basri, and B. Nadler, The trimmed lasso: Sparse recovery guarantees and practical optimization by the generalized soft-min penalty, SIAM Journal on Mathematics of Data Science, 3 (2021), pp. 900–929.

- [2] D. Bertsimas, M. S. Copenhaver, and R. Mazumder, The trimmed lasso: Sparsity and robustness, arXiv preprint arXiv:1708.04527, (2017).

- [3] S. Boyd, N. Parikh, and E. Chu, Distributed optimization and statistical learning via the alternating direction method of multipliers, Now Publishers Inc, 2011.

- [4] E. J. Candès, J. Romberg, and T. Tao, Stable signal recovery from incomplete and inaccurate measurements, Comm. Pure Appl. Math., 59 (2006), pp. 1207–1223.

- [5] E. J. Candes, M. B. Wakin, and S. P. Boyd, Enhancing sparsity by reweighted l1 minimization, Journal of Fourier analysis and applications, 14 (2008), pp. 877–905.

- [6] R. Chartrand, Exact reconstruction of sparse signals via nonconvex minimization, IEEE Signal Processing Letters, 14 (2007), pp. 707–710.

- [7] R. Chartrand and W. Yin, Iteratively reweighted algorithms for compressive sensing, in International Conference on Acoustics, Speech, and Signal Processing, 2008, pp. 3869–3872.

- [8] R. Chartrand and W. Yin, Iteratively reweighted algorithms for compressive sensing, in 2008 IEEE international conference on acoustics, speech and signal processing, IEEE, 2008, pp. 3869–3872.

- [9] S. S. Chen, D. L. Donoho, and M. A. Saunders, Atomic decomposition by basis pursuit, SIAM review, 43 (2001), pp. 129–159.

- [10] D. L. Donoho, Compressed sensing, IEEE Trans. on Inf. Theory, 52 (2006).

- [11] D. L. Donoho and X. Huo, Uncertainty principles and ideal atomic decomposition, IEEE Trans. Inf. Theory, 47 (2001), pp. 2845–2862.

- [12] D. M. Dunlavy and D. P. O’Leary, Homotopy optimization methods for global optimization, Report SAND2005-7495, Sandia National Laboratories, (2005).

- [13] Y. C. Eldar and G. Kutyniok, Compressed sensing: theory and applications, Cambridge university press, 2012.

- [14] J. Fan and R. Li, Variable selection via nonconcave penalized likelihood and its oracle properties, Journal of the American statistical Association, 96 (2001), pp. 1348–1360.

- [15] S. Foucart and H. Rauhut, A mathematical introduction to compressive sensing, Bull. Am. Math, 54 (2017), pp. 151–165.

- [16] D. Gabay and B. Mercier, A dual algorithm for the solution of nonlinear variational problems via finite element approximation, Computers & mathematics with applications, 2 (1976), pp. 17–40.

- [17] W. Guo, Y. Lou, J. Qin, and M. Yan, A novel regularization based on the error function for sparse recovery, Journal of Scientific Computing, 87 (2021), pp. 1–22.

- [18] A. Hantoute and M. López, Characterizations of the subdifferential of the supremum of convex functions, Journal of Convex Analysis, 15 (2008), pp. 831–858.

- [19] R. Horst and N. V. Thoai, Dc programming: overview, Journal of Optimization Theory and Applications, 103 (1999), pp. 1–43.

- [20] X.-L. Huang, L. Shi, and M. Yan, Nonconvex sorted minimization for sparse approximation, Journal of the Operations Research Society of China, 3 (2015), pp. 207–229.

- [21] Y. Lou and M. Yan, Fast l1-l2 minimization via a proximal operator, J. Sci. Comput., 74 (2018), pp. 767–785.

- [22] Y. Lou, P. Yin, Q. He, and J. Xin, Computing sparse representation in a highly coherent dictionary based on difference of and , J. Sci. Comput., 64 (2015), pp. 178–196.

- [23] Y. Lou, P. Yin, and J. Xin, Point source super-resolution via non-convex l1 based methods, J. Sci. Comput., 68 (2016), pp. 1082–1100.

- [24] J. Lv, Y. Fan, et al., A unified approach to model selection and sparse recovery using regularized least squares, Annals of Stat., 37 (2009), pp. 3498–3528.

- [25] E. C. Marques, N. Maciel, L. Naviner, H. Cai, and J. Yang, A review of sparse recovery algorithms, IEEE access, 7 (2018), pp. 1300–1322.

- [26] B. K. Natarajan, Sparse approximate solutions to linear systems, SIAM journal on computing, 24 (1995), pp. 227–234.

- [27] Y. Nesterov, Smooth minimization of non-smooth functions, Mathematical programming, 103 (2005), pp. 127–152.

- [28] P. Ochs, A. Dosovitskiy, T. Brox, and T. Pock, On iteratively reweighted algorithms for nonsmooth nonconvex optimization in computer vision, SIAM Journal on Imaging Sciences, 8 (2015), pp. 331–372.

- [29] T. Pham-Dinh and L.-T. Hoai-An, Convex analysis approach to d.c. programming: Theory, algorithms and applications, Acta Mathematica Vietnamica, 22 (1997), pp. 289–355.

- [30] T. Pham-Dinh and L.-T. Hoai-An, A d.c. optimization algorithm for solving the trust-region subproblem, SIAM J. Optim., 8 (1998), pp. 476–505.

- [31] Y. Rahimi, C. Wang, H. Dong, and Y. Lou, A scale-invariant approach for sparse signal recovery, SIAM Journal on Scientific Computing, 41 (2019), pp. A3649–A3672.

- [32] X. Shen, W. Pan, and Y. Zhu, Likelihood-based selection and sharp parameter estimation, Journal of the American Statistical Association, 107 (2012), pp. 223–232.

- [33] R. Tibshirani, Regression shrinkage and selection via the lasso, Journal of the Royal Statistical Society: Series B (Methodological), 58 (1996), pp. 267–288.

- [34] A. M. Tillmann and M. E. Pfetsch, The computational complexity of the restricted isometry property, the nullspace property, and related concepts in compressed sensing, IEEE Trans. Inform. Theory, 60 (2014), pp. 1248–1259.

- [35] H. Tran and C. Webster, A class of null space conditions for sparse recovery via nonconvex, non-separable minimizations, Results in Applied Mathematics, 3 (2019), p. 100011.

- [36] C. Wang, M. Yan, Y. Rahimi, and Y. Lou, Accelerated schemes for the minimization, IEEE Transactions on Signal Processing, 68 (2020), pp. 2660–2669.

- [37] L. T. Watson, Theory of globally convergent probability-one homotopies for nonlinear programming, SIAM Journal on Optimization, 11 (2001), pp. 761–780.

- [38] D. Wipf and S. Nagarajan, Iterative reweighted and methods for finding sparse solutions, IEEE Journal of Selected Topics in Signal Processing, 4 (2010), pp. 317–329.

- [39] Z. Xu, X. Chang, F. Xu, and H. Zhang, regularization: A thresholding representation theory and a fast solver, IEEE Trans. Neural Netw. Learn. Syst., 23 (2012), pp. 1013–1027.

- [40] Z. Xu, G. H., W. Yao, and H. Zhang, Representative of regularization among regularizations: an experimental study based on phase diagram, Acta Automatica Sinica, 38 (2012), pp. 1225–1228.

- [41] P. Yin, E. Esser, and J. Xin, Ratio and difference of and norms and sparse representation with coherent dictionaries, Communications in Information and Systems, 14 (2014), pp. 87–109.

- [42] P. Yin, Y. Lou, Q. He, and J. Xin, Minimization of for compressed sensing, SIAM J. Sci. Comput., 37 (2015), pp. A536–A563.

- [43] C. Zach and G. Bourmaud, Iterated lifting for robust cost optimization, in BMVC, 2017.

- [44] C.-H. Zhang et al., Nearly unbiased variable selection under minimax concave penalty, The Annals of statistics, 38 (2010), pp. 894–942.

- [45] S. Zhang and J. Xin, Minimization of transformed penalty: Closed form representation and iterative thresholding algorithms, arXiv preprint arXiv:1412.5240, (2014).

- [46] S. Zhang and J. Xin, Minimization of transformed penalty: theory, difference of convex function algorithm, and robust application in compressed sensing, Mathematical Programming, 169 (2018), pp. 307–336.

- [47] T. Zhang, Multi-stage convex relaxation for learning with sparse regularization, in Advances in neural information processing systems, 2008, pp. 1929–1936.

- [48] W. Zhu, Z. Huang, J. Chen, and Z. Peng, Iteratively weighted thresholding homotopy method for the sparse solution of underdetermined linear equations, Science China Mathematics, (2020), pp. 1–26.

Supplement

This section includes the proof of Theorem 2.2 and the computations to find a lift of sparsity promoting models mentioned in section 2.2 into our generalized model.

Proof 5.1 (Proof of Theorem 2.2).

Set

The function is proper, lower semi-continuous and convex, hence by Fenchel-Moreau’s theorem we have that . Also we have

using . In addition,

Therefore,

where

Given a regularization function we want to find a proper function and a set such that up to a constant. Using Theorem 2.2, we can directly find , however sometimes it might be easier to use the following observation which leads to simpler computations. Suppose has a unique minimizer and hence satisfies By assuming that the minimum of (9) is finite, the optimality condition gives for where denotes the interior of the set (Note that can have non-zero coordinates on the boundary of .) Thus, we only need to solve the following two equations for a function with respect to on the feasible set :

| (28) |

-

1.

model: Consider , and note that . For and , the (28) simplifies into

for all . From the first equation we get that and then from the second equation we get . A solution for is for . Finally taking and , one can check that .

-

2.

log-sum penalty: Consider , and note that . For and , the (28) simplifies into

for all . From the first equation we get that and then from the second equation we get . A solution for is for . Finally taking and , one can check that .

-

3.

Smoothly clipped lasso model: Consider , and note that

(29) For and , the first equation in (28) simplifies into

for all . In the case of we get that which means we should have and . By taking and , one can check that .

- 4.

-

5.

Capped model: Consider , and note that

(31) For and , the first equation in (28) simplifies into

for all . Note that the second equation in (28) only happens if the minimizer is in the interior of the set . Consider , therefore for this case since the minimizer is on the boundary, therefore we need a function which is nonzero in the interior of and for we have and for we have . Therefore and a solution for this is . Finally taking and , one can check that .

-

6.

Transformed model: Consider , and note that . For and , the (28) simplifies into

for all . From the first equation we get that and then from the second equation we get . A solution for is for . Finally taking and , one can check that .

-

7.

Error function penalty: Consider , and note that and . For and , the (28) simplifies into

for all . From the first equation we get that and then from the second equation we get . A solution for is for . Finally taking and , one can check that .