Computational methods for adapted optimal transport

Abstract

Adapted optimal transport (AOT) problems are optimal transport problems for distributions of a time series where couplings are constrained to have a temporal causal structure. In this paper, we develop computational tools for solving AOT problems numerically. First, we show that AOT problems are stable with respect to perturbations in the marginals and thus arbitrary AOT problems can be approximated by sequences of linear programs. We further study entropic methods to solve AOT problems. We show that any entropically regularized AOT problem converges to the corresponding unregularized problem if the regularization parameter goes to zero. The proof is based on a novel method—even in the non-adapted case—to easily obtain smooth approximations of a given coupling with fixed marginals. Finally, we show tractability of the adapted version of Sinkhorn’s algorithm. We give explicit solutions for the occurring projections and prove that the procedure converges to the optimizer of the entropic AOT problem.

keywords:

[class=MSC]keywords:

and

1 Introduction

For distributions of a time series, the usual Wasserstein distance does not account for the underlying information structure dictated by the flow of time. This can be inadequate in certain situations: indeed, problems like optimal stopping, stochastic control or pricing and hedging in mathematical finance, as well as operations such as the Doob decomposition or the Snell envelop, are discontinuous with respect to the Wasserstein topology, and Wasserstein barycenters of martingale measures do not retain the martingale property, see [5, 9]. The adapted Wasserstein distance remedies these problems [6, 9]. More generally, adapted optimal transport (AOT) problems are becoming increasingly popular as an alternative to classical optimal transport (OT) whenever a temporal component is included in the setting. These problems range from the study of dynamic Cournot–Nash equilibria in games of mean field kind (see, e.g., [1, 8]), generative models where temporal data is used (see, e.g., [45, 46]), quantifying approximation quality in multistage stochastic programs (see, e.g., [39]), derivation of concentration inequalities on the Wiener space (see, e.g., [34]), robust pricing and hedging in mathematical finance (see, e.g., [5]), and sensitivity analysis in multiperiod optimization problems (see, e.g., [10]).

1.1 Adapted optimal transport problems

For two marginal distributions and , the classical optimal transport problem is of the form

| (OT) |

where is a cost function and is the set of couplings between and . We are interested in settings where and are distributions of a time series, say on ,

The basic concept of AOT is most natural in its Monge formulation. Recall that the Monge formulation for classical OT is given by

| (Monge-OT) |

where the infimum is taken over all measurable maps satisfying the pushforward condition that equals . The basic premise of AOT is that these transport maps should be adapted. While general maps can be written as , adapted maps are of the form

| (adapted Monge maps) |

i.e., only depends on . Adapted transport maps encode the intuition that the decision of where to transport mass at time can only depend on the realizations of the values of that are known up to time . Using adapted transport maps, we can define the adapted analogue to (Monge-OT) as

| (Monge-AOT) |

Going towards a Kantorovich formulation over couplings, consider the coupling which is induced by , i.e., . Adaptedness of means that under , the first components of are independent of given . This is a condition which can be transferred to arbitrary couplings, and we accordingly define

which we call the set of causal couplings between and (cf. Definition 2.1 and Remark 2.2). This leads to the first AOT problem, called causal OT, which is studied in this paper,

| (Causal-OT) |

Notably, (Causal-OT) is the correct relaxation of (Monge-AOT) in the sense that adapted Monge maps are dense in for suitable non-atomic measures , see [11]. While the problems (Monge-AOT) and (Causal-OT) respect the temporal component, both problems lack symmetry. In many situations, and particularly when going towards a concept of adapted Wasserstein distance, symmetry is desirable or even necessary. To alleviate asymmetry, one may symmetrize the causality constraint and define the set of bicausal couplings

and the corresponding problem

| (Bicausal-OT) |

In the same spirit as (Monge-AOT) and (Causal-OT), one can also consider a Monge version of (Bicausal-OT), c.f. [12]. We call both (Causal-OT) and (Bicausal-OT) AOT problems and, if we can use both interchangeably, we simply write

| (AOT) |

where is a placeholder for either symbol, or .

1.2 Discretization and stability

With increasing theoretical interest in AOT problems, building a solid computational foundation is important to enable the utilization of AOT in applications. As a starting point, like classical OT, AOT reduces to a linear program whenever the marginal distributions are finitely supported, see Lemma 3.11. Discrete bicausal problems even allow for a backward induction, reducing the optimization to iteratively solving families of classical OT problems, see [4].

To solve general AOT problems with marginals and , the baseline strategy is to approximate the marginals by a sequence of discrete (i.e. finitely supported) marginals and . Controlling the resulting approximation error requires a suitable stability of AOT problems with respect to perturbations in the marginals, which means the mapping

has to be continuous in a suitable sense. We provide both qualitative and quantitative continuity results for this mapping in Theorems 3.6 and 3.9. The results extend to entropically regularized AOT problems (cf. Section 1.3 below), and in this case we even obtain stability results for the respective optimizing couplings. Our main technique is based on an adapted version of the concept of the shadow – a coupling which shadows the dependence structure of another coupling between differing marginals (see Definition 3.3) – which builds on the recent work in [23]. A necessary component of our stability results is that marginals are compared with respect to an adapted Wasserstein distance, and not just a Wasserstein distance. This entails an important practical implication: when approximating an AOT problem with marginals and by a sequence of discrete problems, the marginals have to be approximated with respect to an adapted distance, and not just the Wasserstein distance. Such approximations are studied for instance in [3, 9, 11].

Our results show that AOT is surprisingly well behaved for an OT problem with additional constraints. This is not always the case, for instance, the related martingale OT problem is not stable in dimension (at least for the weak topology on the marginals) as shown in [15], while the corresponding question in dimension received considerable attention [7, 28, 44]. We further mention that computational methods for AOT problems have so far mostly been focused on backward induction, see [39, 40, 41]. A notable exception is [46], where the authors utilize an approximate numerical scheme for causal OT based on duality.

1.3 Entropic regularization

Many of the recent applications of OT build on fast approximate solutions which are based on regularization (e.g., [20, 27, 38]). Particularly entropic regularization is widely used, as it allows for a computationally efficient solution of the regularized problem using Sinkhorn’s algorithm [19]. We study entropic regularization for general AOT problems in this paper. Entropic AOT problems are of the form

| (Entropic-AOT) |

where , denotes the Kullback-Leibler divergence (or relative entropy) and is the product measure between and . Utilization of entropic regularization for discrete bicausal problems was recently initiated by [41], where the authors used Sinkhorn’s algorithm to speed up the computation of the backward induction, see also Remark 6.12 for a short discussion of the approach in [41] compared with the adapted version of Sinkhorn’s algorithm (cf. Section 1.4) studied in this paper. We showcase in Theorem 4.2 that for general AOT problems, similar to classical OT, the approximation error introduced by entropic regularization vanishes for a small enough regularization parameter, i.e.,

The proof is again based on the adapted version of the shadow, which is used in Lemma 4.1 to obtain smoothed versions of a given coupling. Even for classical OT, this approach may be a fruitful alternative to other methods studied for instance in [13, 17, 22, 35]. For our purposes, this method has the benefit that the smoothed coupling inherits the adaptedness properties of the initial coupling.

1.4 Sinkhorn’s algorithm

We introduce and study an adapted version of Sinkhorn’s algorithm to solve (Entropic-AOT). In this algorithm, one defines the initial measure via , and iteratively

for . Hereby, the sets and are chosen such that and the respective projection steps should be easy to compute. For instance for the causal problem (Causal-OT), we choose , the set of couplings with fixed first and arbitrary second marginal, and , the set of couplings with arbitrary first and fixed second marginal. We show computational tractability of the resulting projection steps, both in the primal and dual form, see Lemmas 6.2 and 6.4, respectively. We further show that the values corresponding to converge, even linearly, to the optimal value of (Entropic-AOT), see Theorem 6.11. The method of proof is based on the recent work [16] proving convergence of Sinkhorn’s algorithm for multimarginal OT. We give another short proof of convergence of Sinkhorn’s algorithm in Proposition 6.5 based on stability, which is however only applicable to the causal problem. In contrast to Theorem 6.11, Proposition 6.5 does not give a rate of convergence, but it applies even to unbounded cost functions under suitable moment assumptions on the marginals.

1.5 Duality

Duality is a key concept to fully understand and work with optimal transport problems, which has been studied in the context of AOT by, e.g., [1, 4]. However, particularly the dual formulations for entropic AOT, which are necessary tools to study the adapted version of Sinkhorn’s algorithm, are not included in the current literature. In Proposition 5.2, we show that for bounded and continuous cost functions and suitably defined sets of functions , we have the dual formulations:

The proof builds on known duality results and Sion’s minimax theorem. For entropic AOT, we show in Lemma 6.8 that the dual supremum is attained and that optimizers can be characterized by adapted versions of the Schrödinger equations. This result is a key component in the proof of Theorem 6.11 showing the linear convergence of Sinkhorn’s algorithm.

1.6 Structure of the paper

The remainder of this paper is structured as follows: in Section 2 we introduce necessary notation and define the AOT problems. In Section 3, results related to the shadow and stability of AOT problems are derived. Section 4 is concerned with the convergence of the entropically regularized AOT problem for vanishing regularization parameter. Section 5 states and proves the dual formulations for AOT. And finally, Section 6 gives the results related to the adapted version of Sinkhorn’s algorithm.

2 Setting, notation and preliminary results

2.1 Notational conventions

Let denote the number of time steps and write , for Polish path spaces with metrics , respectively. We denote by (resp. ) the continuous (resp. and bounded) functions mapping to . Further, we say that a function has growth of order at most whenever is bounded for some . Moreover, let be the set of bounded and measurable functions mapping to , and let be the set of Borel probability measures on , and the measures with finite -th moment (integrating ). For all definitions stated above, one can replace with any other Polish space. We denote by the set of couplings between and , that is the set of probability measures on with first marginal and second marginal , and we will always use the notation .

Since adapted transport problems involve disintegrations and taking marginals, we will take some time to introduce a proper notation:

First, for measures on or (we give the notation for , while the corresponding versions for are analogous): Let and . Define and as the projection of onto . Define , where ∗ denotes the pushforward operator. That means, is the marginal of on the coordinates included in . If we will write and if we will write , and similarly with , , etc. For the disintegration, we use the notation , where is a stochastic kernel. For we will abuse notation slightly and write . Finally for , we define (which is a stochastic kernel mapping ), where the same notation applies. The standard disintegration thus reads

| (1) |

Now, for joint distributions. Let and . With slight abuse of notation, we regard and also as projections mapping from onto the respective coordinates in and . Then, we define and as previously for and for . For the disintegration, we write and for and we define (which is a stochastic kernel mapping onto . The same convention as previously applies when plugging values into the kernels. The special case (and similarly when the roles of and are reversed) is treated as follows: instead of writing the empty set we will use and set . For example, then denotes the law of and denotes the -marginal of . Similarly, we write for the disintegration of w.r.t. . With these conventions in mind, the standard disintegration reads

| (2) |

Another disintegration which is perhaps more intuitive when considering as a randomized transport from to would be

| (3) |

Let and let be a measurable kernel. Then we write for the measures that satisfies, for all ,

| (4) |

In order to reduce the number of brackets we will frequently write instead of .

2.2 Adapted optimal transport and its entropic versions

Definition 2.1.

A measure is called causal if, for all , we have -almost surely

| (5) |

or equivalently, we have under the following conditional independence

| (6) |

The set of all causal probability measures is denoted by . Analogously, the set of anticausal measures is defined as the set of measures such that holds almost surely for all . The set of bicausal measures is defined as .

Note that when is the -marginal of , the right-hand side of (5) coincides in fact -a.s. with . In particular, the kernel does not depend on .

Remark 2.2.

By the chain rule of conditional independence [30, Proposition 5.8], we have

Thus, this reasoning yields that if and only if, for ,

| (7) |

or equivalently, we have -almost surely

| (8) |

Let be continuous. Define the set of causal, anticausal and bicausal couplings between two measures and as , and , respectively. Whenever is specified, is assumed to have growth of order at most and .

Whenever a statement is the same for the regular, causal, anticausal or bicausal version, we will use an index as a placeholder. For example, can mean either of , , , . We define the (adapted) optimal transport problem as

We denote by the relative entropy between given by if (i.e., if is absolutely continuous w.r.t. ) and , else. For , we define the entropic versions of the (adapted) optimal transport problem by

If , we will simply write .

Remark 2.3 (Existence).

We remark that, when the cost is lower semicontinuous and lower-bounded, existence of optimizers to the problems and follows by standard arguments due to weak compactness of , c.f. Lemma A.3. Moreover, by strict convexity of the relative entropy the optimizer of is unique.

3 Stability

For and we define the (adapted) versions of the Wasserstein distance by

and similarly on . For , the (adapted) Wasserstein distance is defined by

For the definition of causality for , we regard the spaces as a single space, and the usual definition, that is Definition 2.1, applies. For disintegrations of we use the notation for marginals, for disintegrations, etc. For instance, being causal means that

for all .

3.1 Adapted version of the shadow

The convolution of two stochastic kernels and is given by the (unique) kernel satisfying

for and .

Concatenation of different couplings will be a recurrent tool throughout this paper. The following Lemma establishes the key property that concatenation of causal couplings remains causal.

Lemma 3.1.

Let . Let where we write and . Then

| (9) |

Proof.

Let . Let and note that by Fubini’s theorem

Similarly to the above calculation, it is straightforward to see that .

It remains to show that . We write . Since , the causality of is equivalent to the following: For , we have

| (10) |

By definition of , we have -almost surely that , thus,

| (11) |

Let . Since we have, by causality of the latter,

| (12) |

Using (11) and (12) we find by the chain rule [30, Proposition 5.8] that

| (13) |

Similarly, we have due to and that

| (14) |

Finally, we find that (13) and (14) imply (10) by the chain rule [30, Proposition 5.8], which concludes the proof. ∎

Using the previous Lemma together with Minkowski’s inequality immediately yields the following:

Corollary 3.2 (To Lemma 3.1).

Let . Then .

Definition 3.3 (Shadow).

Lemma 3.4 (Properties of the shadow).

Let . Let , , and where we write and . Let be the -shadow of and denote by the transport cost between and associated with the coupling , and similarly .

-

(i)

It holds

-

(ii)

For any other coupling and its -shadow it holds

In particular, since is the -shadow of , it holds

-

(iii)

If is causal, is anticausal and is causal, then is causal. If and are - and -optimal, then

-

(iv)

If is anticausal, is causal and is anticausal, then is anticausal. If and are - and -optimal, then

-

(v)

Let . If and are causal, then . If and are - and -optimal, then

Proof.

The first property (i) is clear by definition of . Property (ii) follows immediately from the data processing inequality (cf. [23, Lemma 4.1]).

(iii), (iv) are obviously equivalent and we show only (iii). Write for the disintegration kernel of w.r.t. the second coordinate. Since is anticausal, we find that is causal. Write . Then, we find that

That is, can be defined as a concatenation of causal kernels in such an order that is the joint first and last marginal. I.e., and by Lemma 3.1 it thus follows that . The second claim in (iii) follows from (i).

(v): We have to show that for all . Let us denote by , where and note that by causality , c.f. Remark 2.2, and the same for . Thus can be disintegrated as

where the terms in (…) are irrelevant for and thus

which implies , which shows the claim. ∎

3.2 Stability of adapted optimal transport and its entropic versions

For stability of the entropic problems (in particular, for the convergence of the causal Sinkhorn algorithm later), it will be necessary to control adapted distances through relative entropy. We will even show that adapted distances can – for bounded settings – be controlled in a quantitative fashion via the total variation distance. For two measures , we recall the lattice minimum for Borel sets , or equivalently one can define via its density

For reference, we recall that the following equality holds

| (TV) | ||||

see, e.g., [36, Definition 2.15] and [36, Lemma 2.20]. Further, we define

| (AV) |

which we call the adapted variation. The following results establishes that total variation and adapted variations are equivalent up to a constant.

Lemma 3.5.

Let . Then we have

| (15) |

Proof.

The assertion is trivially satisfied when , since then adapted variation and total variation coincide. We show the statement by induction: Assume that (15) holds for . Let be a path space with -time steps and , then

where the last inequality holds by the data processing inequality for the total variation, see for example [23, Lemma 4.1] and note that the proof therein also works for the total variation distance. Let and write for . We can define a bicausal coupling by

This allows us to estimate the adapted variation: Consider the diagonal in that is the set of pairs with and write , where is the measure which has density w.r.t. . Note that essentially corresponds to the part of that is supported on the diagonal. We find

| (16) |

which can be seen as follows: the inequality is due to and the definition (AV). The first equality follows from decomposing into two measures and , and then using the definition of the kernel . The second inequality stems from (TV) and the definition of the kernel . Finally, the last equality is a straight-forward application of Fubini’s Theorem.

Recall that by Remark 2.3 there exist optimizers of the problems and as long as the cost is lower semicontinuous and lower-bounded. We can state the first main result:

Theorem 3.6 (Qualitative stability).

Let and be continuous and have growth of order at most . Let and , , be a sequences converging to resp. in . Then

and accumulation points of optimizers of are optimizers of . Further,

and the associated optimizers converge in .

Proof.

In this proof, subsequences will be relabeled by the initial index. Since we will require shadows in this proof, we fix the notation as an optimizer of and similarly as an optimizer of .

We first show the statement for . Let be optimizers of and be an optimizer of .

We show that any limit point of satisfies . To this end, let be the -shadow of . By Lemma 3.4 (i), (iii) and (iv), and (in ) as well. Since is closed by Lemma A.3, follows.

Since by weak compactness, any subsequence of has a further subsequence converging to an accumulation point , which by the above satisfies , we get

On the other hand, let be the -shadow of . Then, by Lemma 3.4 (i), (iii) and (iv), and . Thus

where the inequality follows from and the equality is due -convergence of to .

Concerning the proof for : The inequality can be shown analogously as above, while using lower-semicontinuity of the relative entropy. On the other hand, the reverse inequality again can be derived analogously by using the properties of the shadow, see Lemma 3.4 (ii). ∎

To quantify the respective stability results, we require some assumptions on both marginal distributions and the cost function:

Definition 3.7.

Let , , and . We say that the cost function satisfies , if

Further, we say that satisfy , resp , for , if

| () | |||||

| () |

Note that is clearly a weaker assumption than Lipschitz continuity of , and also satisfied in more general and relevant cases, see, e.g., [23, Example 3.4 and Lemma 3.5]. Criteria for are given in [23, Lemma 3.10]. The following establishes that is satisfied in bounded spaces.

Theorem 3.9 (Quantitative stability).

Let , , and satisfy for . Let .

-

(i)

We have

-

(ii)

Let . Let be the optimizer of and be the optimizer of . If satisfy , then

If and even satisfy , then

Proof.

We fix the notation as an optimizer of and as an optimizer of .

(i): As the statements for and follow by similar reasoning, we only show them for : Let be an optimizer of and be the -shadow of . Then, since (cf. Lemma 3.4(iii) and (iv)), and using Lemma 3.4(i) and (ii), as well as the assumption on , we get

The reverse inequality follows by symmetry, and thus the proof of (i) is completed.

(ii): We introduce additional notation for the values

where . First, we treat the case where satisfy .

Let be the -shadow of . The basic method of proof is the following:

While the second inequality is just assumption for and , it remains to justify steps (1) and (2). Step (1) follows by the Pythagorean theorem for relative entropy [18, Theorem 2.2], combined with the standard reformulation for entropic optimal transport (cf. [23, Lemma 4.4], which works entirely analogously for the adapted optimal transport). Step (2) follows by noting that the proof for actually shows and thus .

Next, we assume that satisfy . Then, the basic method of proof works as above, where we additionally use that by Lemma 3.4(v), it holds , since the coupling induced by the shadow is causal. Thus, we get

The anticausal direction works analogously by using assumption for . This completes the proof. ∎

Remark 3.10.

We shortly mention that in the above Theorems 3.6 and 3.9, some results are stated in less generality than possible to avoid overly lengthy statements.

For instance in Theorem 3.6, holds already if only and , by Lemma 3.4 (iii). Parts of the conclusions can also be strengthened in Theorem 3.6. For instance, we can conclude that optimal couplings converge with respect to .

In Theorem 3.9, similar specifications can apply. For instance, in part (ii), if only satisfy (but not ), we can still obtain the given bound for (but no longer for ).

3.3 Discretization and LP formulation

The baseline approach for solving infinite-dimensional optimization problems like optimal transport is via approximation by a discrete setting, thereby making the optimization problem finite-dimensional. In optimal transport, this translates to discretizing the marginal distributions. The stability results obtained in Section 3.2 show that the deviation of both optimal values and optimizers can be controlled when discretizing the marginals suitably, i.e., in a sense that they approximate the initial marginals well in . This section states the resulting linear program for discrete AOT. Because the structure for the causal, bicausal, and anticausal problems are similar, we only treat the causal case in this section.

Let have finite support, and let and for brevity, denote by , . We further write . Let for . For , denote by the first entries and by its -th entry, and similarly for . For all , let for some be an enumeration of the set , and for some be an enumeration of . We similarly define for and for for some .

The following states the LP formulation for causal optimal transport.

Lemma 3.11.

The optimization problem

is a linear program of the form {mini}—l— π_x, y:x ∈S_μ, y ∈S_ν∑_x ∈S_μ, y ∈S_ν c(x, y) π_x, y \addConstraintπ_x, y∈[0, 1],x ∈S_μ, y ∈S_ν, \addConstraint∑_x ∈S_μ π_x, y=ν(y),y ∈S_ν, \addConstraint∑_y ∈S_ν π_x, y=μ(x),x ∈S_μ, \addConstraint(∑_~x∈S_μ:~x_1:t = x_1:t^(i) μ(~x)) (∑_~x∈S_μ:~x_1:t = x_1:t^(i)~x_t+1 = x_t+1^(k) ∑_~y∈S_ν:~y_1:t = y_1:t^(j) π_~x, ~y) \addConstraint=(∑_~x∈S_μ:~x_1:t = x_1:t^(i)~x_t+1 = x_t+1^(k) μ(~x)) (∑_~x∈S_μ:~x_1:t = x_1:t^(i) ∑_~y∈S_ν:~y_1:t = y_1:t^(j) π_~x, ~y), \addConstraintk ∈[n_t+1], j ∈[m_1:t], i ∈[n_1:t], t ∈[N-1].

Proof.

Objective function and marginal constraints are clear. It is left to show that the final set of equality constraints encodes the marginal constraint for and causality. In other words, the last constraint has to encode

for all . Since all measures are discrete, this simply means that they put the same weight on each relevant atom , i.e.

Noting

and

this shows (after multiplying by the denominator) how the terms involving occur in the given equality constraint. The terms involving work analogously: Defining , as an enumeration of , we have

Writing each summand as a fraction (analogously to above), we find that the denominator reads

which is independent of and we can thus multiply by this term (leading to the right hand side term involving in the constraint). Finally, the sum of numerators reads

which yields the final term involving on the left hand side of the constraint. ∎

3.4 Numerical example: approximation of adapted Wasserstein distance

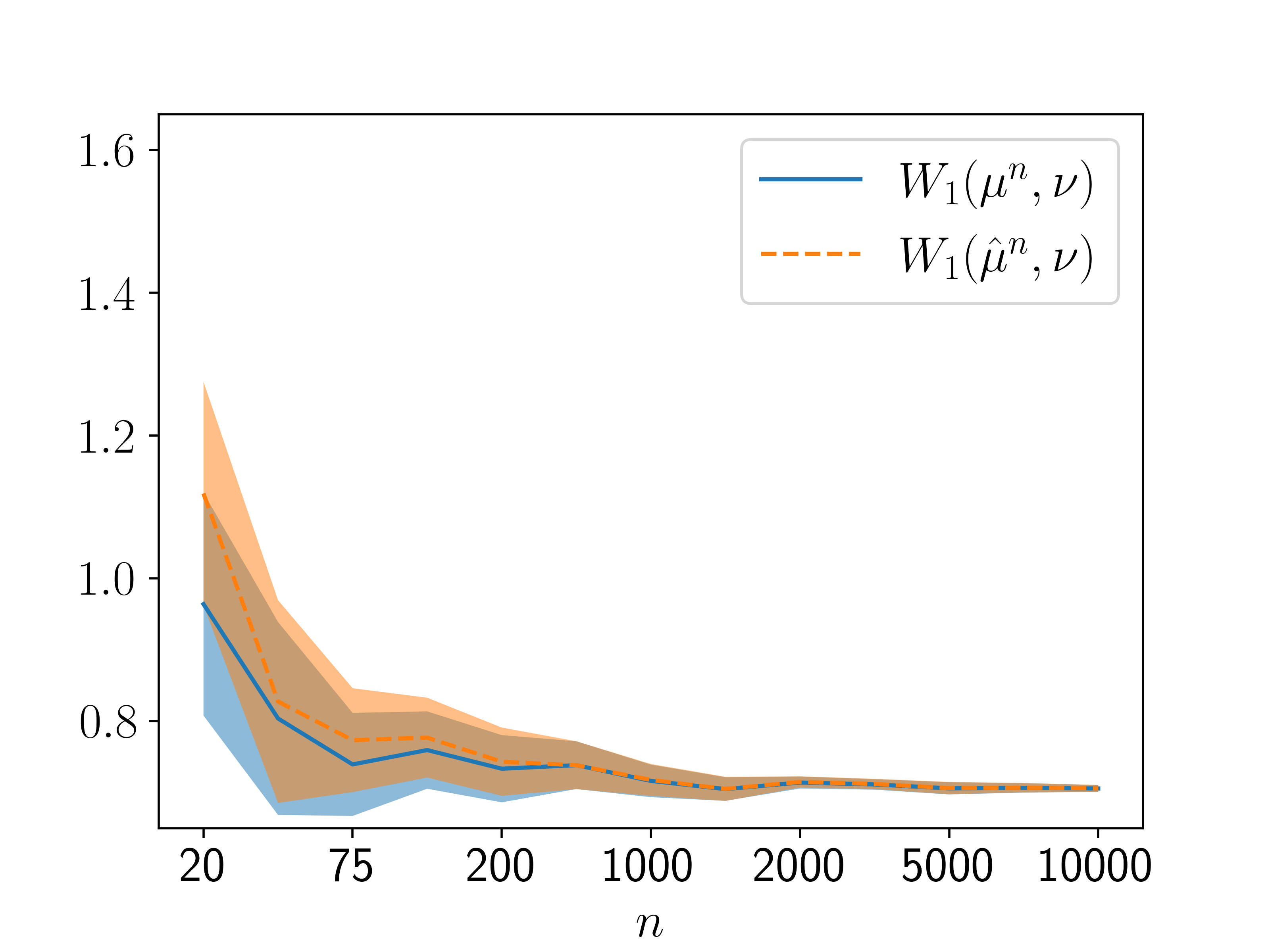

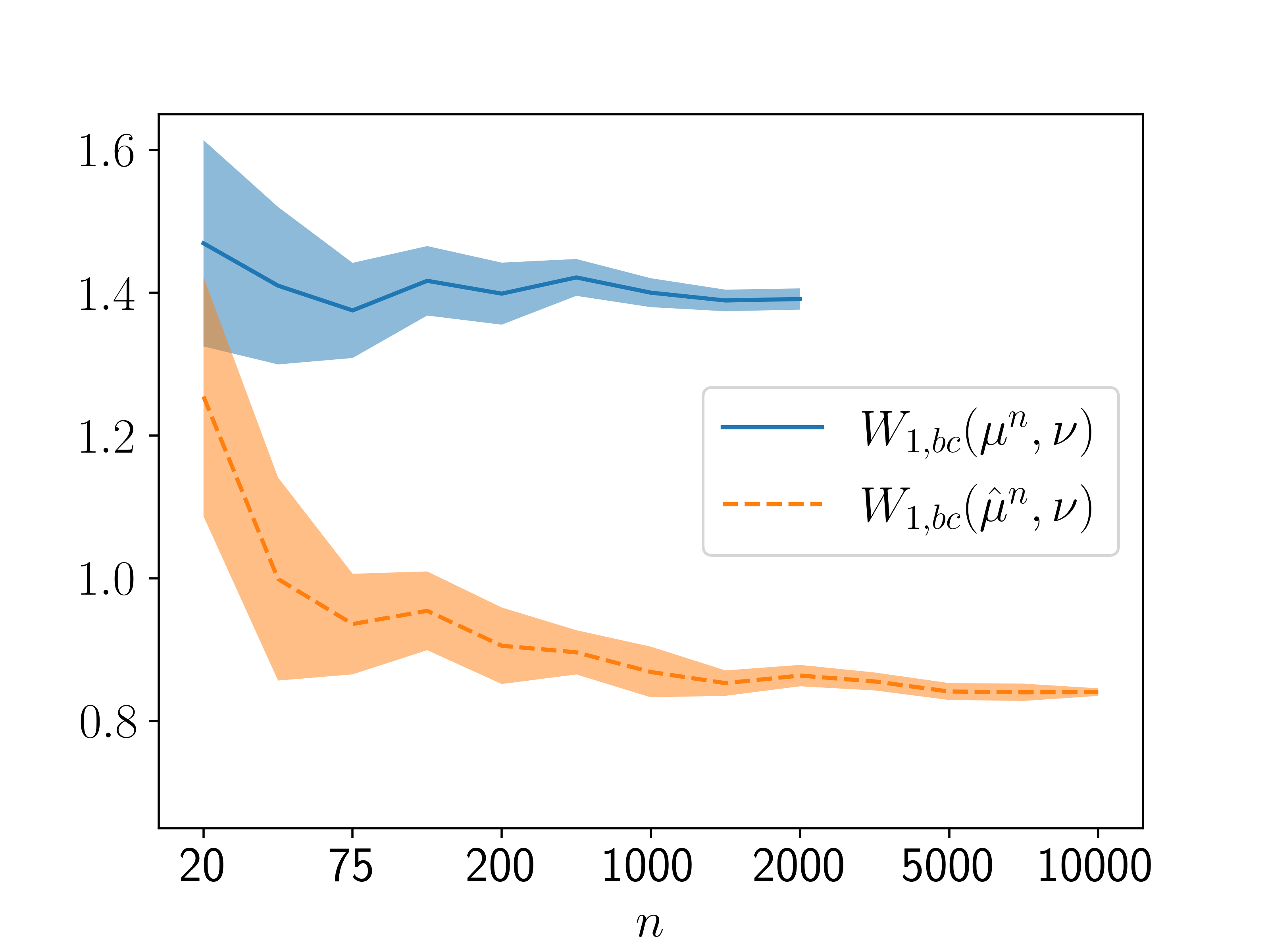

This section aims to illustrate both the LP formulation for bicausal optimal transport problems given by Lemma 3.11 and the qualitative stability result Theorem 3.6, which justifies the approximation of continuous problems via discretization. The code to reproduce the experiments is available at https://github.com/stephaneckstein/aotnumerics.

Consider two marginals , where is the discrete time restriction of a Brownian motion starting at , and is the distribution of a trinomial model starting at . That is, the transition kernels are a normal distribution with mean and variance , while . The goal is to numerically calculate and to compare it with .

To calculate these distances, we assume that we know the precise form of , but only i.i.d. sample paths , . We denote by the empirical measure of . We emphasize that does not converge to zero (cf. [3]), and thus to apply Theorem 3.6, cannot be used. Indeed, due to the continuous nature of , all disintegrations of are almost surely deterministic. Thus under , the transition kernel going forward from is simply the Dirac measure at , i.e., , which is far from the normal distribution given by . We thus use an adapted empirical measure , where approximately points at each time step are clustered together to allow for an empirical approximation which has non-deterministic transition kernels (cf. [3, Definition 1.2] for a precise construction).

All computations are performed via a direct implementation of the resulting linear program as in Lemma 3.11 (adjusted to the standard and bicausal case) using Gurobi [29]. The results are illustrated in Figure 1. We see that for the calculation of , it does not matter whether one uses or , as the approximation using both these empirical measures converges to the same value for large . However, when calculating , it is crucial to use so that Theorem 3.6 guarantees convergence for . While in this particular case, the conclusion could already be reached with the triangle inequality, Theorem 3.6 of course applies to general bicausal optimal transport problems, and not just to . Regarding computational times, we note that the most relevant cases, calculation of and , incurred runtimes within the same order of magnitude, e.g., for the average runtimes to calculate were 2.55, 3.90 and 5.25 seconds, while for they were 5.63, 10.22 and 14.38 seconds, all using a single GHz CPU.

4 Approximation of adapted transport by its entropic version

In this section, we first show how the results for the shadow give a very simple methodology for smoothing a given coupling, while the smoothed version keeps the same marginal distributions. Smoothness is understood with respect to the product measure of the marginals in this case. While to the best of the authors’ knowledge, the presented method is novel even for non-adapted transport problems, the method extends readily to adapted problems, yielding smoothed versions of couplings with the same marginals and that are adapted (causal, bicausal, or anticausal) in the same sense as the non-smoothed coupling.

The following results are stated under the assumption that the marginals can be discretely approximated in , which is satisfied in many cases (see, e.g., [3, Theorem 1.3], [9, Theorem 5.5], [11, Lemma 4.6]). We suspect it holds unconditionally in Polish spaces, which is however not a focus of this work, and thus left as an assumption.

Lemma 4.1.

Let and . Assume that there exist discrete measures such that

Let . Then there exist such that and there are constants such that holds -almost surely.

Proof.

Fix , and consider -optimal couplings denoted by

First, we write for the -shadow of . Next, we define as the -shadow of . Then, by Corollary 3.2 we have

which, together with Lemma 3.4, yields the first claim.

To see the second claim, note that, since and are discrete (and so is the product measure ), there is with

Write , then we get

Since and are the second marginals of and , respectively, is a marginal density of and thus almost surely bounded by as well. ∎

While the following theorem is only stated for entropically regularized optimal transport, the strategy of proof extends readily to regularization by other divergences.

Theorem 4.2.

Let , and . Let be continuous and have growth of order at most . Assume that there exist discrete measures such that

Then

and accumulation points of -optimizers (for ) are optimizers of .

Proof.

Clearly, , thus

To see the reverse direction, pick an optimizer of . We choose , as the sequence given by Lemma 4.1 applied w.r.t. , then

where we recall that for some constants that are also provided by Lemma 4.1. Note that the second last equality is due to -convergence of to . The final statement of the theorem is a simple consequence of convergence of the values (that was shown above) and the fact that is closed by Lemma A.3. ∎

5 Duality

In this section we derive the duality results which will be used to study Sinkhorn’s algorithm. To state the dual formulations of both and we introduce functional spaces: First, we define the classical functional spaces

that determine the marginal constraints in optimal transport. We denote by and the sets where resp. can be even bounded and measurable. Next, we define functional spaces of continuous functions that characterize causality. For this reason, we have to refine the topologies on : For , and , we fix measurable kernels and given by

| (18) | |||

| (19) |

Write and for the topology on and , that is obtained by Lemma A.1 and makes the kernels (18) and (19) for all respectively, continuous. Again, by Lemma A.1 we have, for ,

is a subset of , and

is a subset of . We write

and let and be defined analogously as above when is allowed to be bounded and measurable. We define the functional spaces

and write again and for the corresponding spaces when and are replaced by and respectively. We finally define

Remark 5.1.

We remark that : Indeed, let . We set iteratively , for ,

and , and . Then,

Similarly, we see that .

The following states the duality results which will used in Section 6.

Proposition 5.2.

Let , and . Then

| (20) | ||||

| (21) |

Proof.

For classical OT, (20) is of course well known (see, e.g., [43]). We first show (20) in full generality, where we reason similarly as in [1, Theorem 4.3]: By Lemma A.2 a probability with first marginal is causal if and only if, for all ,

Hence, if and only if

Note that we may replace by in the display above, which yields weak duality: the left-hand side in (20) and (21) dominates the respective right-hand side.

In order to show the reverse inequalities, we abbreviate

First, note that is linear in both arguments. As, for all , we have (lower semi-)continuity w.r.t. weak convergence of measures of on . Since and have the same Borel sets as and respectively, we find that and are Borel measures on the Polish spaces and . Thus, we have that is a compact subset of . For any we have that . We may apply [2, Theorem 2.4.1] and the classical optimal transport duality in order to get

where the first equality follows directly from the characterization of given in Lemma A.2 and we used for the final equality that is a linear space containing and .

To show (21), we only treat the case for notational convenience, while the general case follows by considering the transformed cost function . Note that

see, e.g., [36, Proposition 2.12] (even though arbitrary measurable functions with are used in [36], the version with follows by standard approximation arguments and the observation that the left-hand side dominates the right-hand side as a consequence of the elementary inequality for all and ). Moreover, the term

(where we substituted in the second line) is, for fixed , convex and lower semicontinuous in the variable and, for fixed , concave in the variable . Thus by again applying [2, Theorem 2.4.1], we find

Note that the integral simplifies in all cases, for instance if , then , where and the functions and correspond to and , respectively as in the definition of and .

6 Sinkhorn’s algorithm

Within this section, we continue working with , while the general case may be recovered by scaling the cost function . We start the section by defining Sinkhorn’s algorithm and showing how the respective iterations can be computed both in the primal and the dual formulation. Observe that

where is defined via

| (22) |

since the value of differs from only by the constant . Recall that the unique optimizer exists by Remark 2.3. In other words, computing the optimizer of the problem is the same as computing the projection of onto the set with respect to relative entropy.

The basic premise of Sinkhorn’s algorithm is to regard the set of measures we optimize over, , as an intersection of simpler sets. Instead of computing the projection of onto directly, the algorithm consists of iteratively projecting onto the simpler sets. For , define

These sets will serve as the simple building blocks of the sets we project onto. We focus on the causal and bicausal problem in the following. We are thus interested in computing

Definition 6.1 (Sinkhorn steps).

Let and . Let be as defined in (22) and for ,

We refer to a step in the algorithm as causal step if we project on , normal step if we project on and anticausal step if we project on .

The choice of determines which problem, either causal or bicausal OT, is solved. If , then the causal problem is solved, and if , then the bicausal problem is solved. This choice remains fixed throughout the whole algorithm. We note that the existence of the minimizers is shown in Lemma 6.2 for causal and anticausal steps, respectively well known and tractable (see, e.g., [37]) for the normal step. While tractability of projecting onto the set is well known, the following results establish the analogue for . The symmetric result for can directly be inferred, but is not stated explicitly.

Lemma 6.2 (Causal projection: primal version).

Let be such that

Recursively, we define functions and a measure through its disintegrations: Set and, for ,

and

Then, we have

Proof.

First note that by plugging in the recursion for , we can rewrite for

| (23) |

Let and we show that . Using the chain rule of the relative entropy, see [21, Theorem C.3.1], we find

| (24) |

where, again by the chain rule and as is causal,

| (25) |

Let and set , , and . We show

| (26) |

Since and , this will yield the claim. Combining (23) and (24) imply

| (27) |

To shorten notation, we define the kernels

Note that the definition of in the statement of the present lemma implies

which is understood point-wise (for each ), and can easily deduced by changing the reference measure and using the chain rule as in (25). Hence, using (27) and the definition of , we get

where the inequality uses that and optimality of . This shows (26) and thus the claim. ∎

Corollary 6.3.

Let be equivalent, i.e. and , such that

and for , assume -a.s.

| (28) | |||

| (29) |

for measurable functions and

for measurable. Then, given as in Lemma 6.2 satisfies

Proof.

Recall that is defined as the dual space to the constraint , cf. Section 5.

Lemma 6.4 (Causal projection: dual version).

Let , , and have density for some measurable and bounded function . Let and be such that

| (32) |

Then, is the unique minimizer of .

Moreover, can be decomposed as a sum, , where are explicitly given by the following recursion: Set and, for ,

and .

Proof.

First we show optimality of when its density takes the form as in (32). Obviously, . Thus, for with we get

| (33) | ||||

which implies that . Further, if was another minimizer, then (33) yields that , thus, .

Concerning the second assertion, let and rewrite the left-hand side in (32) as

| (34) | ||||

| (35) |

where the second equality holds if and only if , since then, for ,

Let and be given as in the statement of the lemma. Moreover, set which is by construction in , then we have

| (36) |

Note that is a density w.r.t. , whereas for , are densities w.r.t. . Thus, by defining as in (32) with , we obtain from comparing (34), (35), and (36) that

and . Finally, by uniqueness that was shown in the first part, we derive that any satisfying (32) has to coincide with , hence, . ∎

6.1 The causal case via stability

In this section, we give a quick argument, following the lines of [23, Section 3.4], to prove the convergence of Sinkhorn’s algorithm via the stability results obtained in Section 3.2. This is based on the argument that iterations of the algorithm are each optimal - albeit for their own marginals instead of the true ones. As it is, this line of argument only works in the causal case but not the bicausal one. The reason is that for causal OT, the causality constraint is satisfied every second step during Sinkhorn’s algorithm. For bicausal OT on the other hand, each iteration may fail to satisfy a bicausality constraint, and hence the respective stability results cannot be applied directly. In the following proposition, notice that for a bounded metric (and thus bounded cost function), no assumptions on the marginals are required at all.

Proposition 6.5.

Let and assume is continuous and has growth of order at most . Denote by the optimizer of and let be the causal iterations of Sinkhorn’s algorithm as defined in Definition 6.1. If has finite exponential moments of order ,111Which is defined as for some . then converges in to as , . If further has finite exponential moments of order as well, then also converges in to as .

Proof.

Write for . To ease notation, we write and . By the Pythagorean theorem for the relative entropy, see [18, Equation (3.1) and Corollary 3.1], we find for any which has finite entropy w.r.t. (and therefore also w.r.t. ) that

| (37) |

where . A quick calculation (cf. [42, Proposition 2.1]) reveals

By the tail assumptions on and and by [14, Corollary 2.3], this implies convergence of the marginals (and thus in particular convergence of the -th moments). Further, by Pinsker’s inequality and Lemma 3.5, this convergence also holds in . Convergence in (which directly implies convergence for a bounded metric) together with convergence of the -th moments implies convergence in , and thus

Notably, for , this convergence holds without the tail assumption on (since for these iterations the first marginal of equals ).

We turn towards applying our stability result for for some . We set

and obtain , which we abbreviate as . We remark that as a consequence of (37). Further, the respective densities are given by Lemma 6.2. We obtain for some constants

| (38) | ||||

where follows by Corollary 6.3, where we note that the problem on the left hand side of the equality is finite by plugging in the optimizer , and the right hand side is finite by plugging in , while the form of coming from Lemma 6.2 satisfies the assumptions of Corollary 6.3. To continue, we denote by the measure on that satisfies , and find

by the integrability condition on . Following up on (38), we obtain

where the last equality holds as the value of does not depend on .

Thus, by Theorem 3.6, we obtain that converges in to for , . Since, as consequence of (37), converges to zero, converges weakly to as well for . Finally, since the -th moments of converge (by convergence of the moments of the marginals as shown above), also converges in to , which completes the proof.∎

6.2 Linear convergence for bounded cost functions

For the main result of this section, we require attainment of dual optimizers and adapted versions of Schrödinger equations. We first define the adapted Schrödinger equations, (39) and (40), and illustrate their relation to the dual Sinkhorn step from Lemma 6.4. We recall that the supremum norm of a function is given by .

Lemma 6.6 (Dual Sinkhorn steps).

Let and we write , . We define the causal Sinkhorn step recursively by setting ,

| (39) | ||||||

and . Then, satisfies

The converse anticausal step is defined analogously by inverting the roles of the coordinates and and of the functions and , and satisfies the same bounds. Finally, given , the converse normal step is given by defining via

| (40) |

which satisfies, with decomposition as in Remark 5.1,

Proof.

First, we show the maximizing property of . By weak duality (i.e., Fenchel-Young inequality applied to the function , for ) we have that

Further, one quickly sees that duality is attained whenever there exists a such that for some , since then, for any

where a construction for such a function is given in Lemma 6.4. This construction coincides with the definition of here, and thus is a maximizer.222Note the simplification that since for does not depend on , it does not influence and can thus be disregarded in the definition of . Further, note that the assumption in Lemma 6.4 such that is a density can be made without loss of generality by normalization.

Regarding the bounds for , we introduce some notation: for some function , we denote by

its maximum variation in the -th variable of (and similarly we define ). Then one finds by the triangle inequality and since is constant in . Since for , is a centered version (in the variable , given all other variables) of , it thus holds

| (41) |

Further, a straightforward calculation reveals , which recursively and combined with (41) leads to the stated bound for for . The case works analogously by noting that takes values in the range .

Regarding , the maximizing property in this case is the usual Schrödinger equation, and thus clear. The bounds follow completely analogously to the case for , noting that . ∎

Lemma 6.7 (Dual optimizers are attained).

Let be measurable and bounded, then

Proof.

Take a maximizing sequence . Define by applying to the Sinkhorn step (alternating causal and anticausal, respectively causal and normal) -times, as defined in Lemma 6.6. Then, is still a maximizing sequence since Lemma 6.6 shows that the value of can only increase by applying the Sinkhorn steps, and further is uniformly bounded by a constant only depending on and . In fact, each component of is uniformly bounded, since we can assume without loss of generality (for example by translating by a constant and by ) that , which are both bounded above and below by . We can apply Komlós’ Lemma [33, Theorem 1a] which yields a subsequence (which we relabel by the initial sequence) such that

converge -almost surely to some element , respectively, and the limits clearly satisfy the same uniform bounds as the sequence. Write . By uniform boundedness, this convergence also holds in and thus and thus . The next computation reveals optimality of :

where we used Fatou’s lemma and the concavity of for an arbitrary , which is uniformly upper bounded when . ∎

Lemma 6.8 (Schrödinger equations).

Let be bounded, then any dual maximizer

with satisfies the adapted versions of the Schrödinger equations, i.e., satisfies (39) and, in case of bicausal OT, satisfies the respective anticausal analogue of (39), and in case of causal OT, satisfies (40). Further, using the normalization , there exists a constant only depending on such that

Proof.

Let , be given as in (39).

We have to show that satisfies, for ,

| (42) |

Note that if (42) holds for and , then -almost surely

| (43) |

Next, we differentiate under the integral sign, which is justified by standard results, e.g., [26, Theorem 2.27]), in order to obtain first order optimality conditions that has to satisfy: for consider the first order conditions for the mapping

| (44) |

and the test function given by

where and are continuous and bounded. Differentiation of (44) at gives

where the first equality is due to optimality of . As was arbitrary, this yields -almost surely

from which we derive, as was arbitrary, that -almost surely

is a measurable function of and ; in other words, is constant in .

Let , or such that for . In both cases, we find thanks to (43) that -almost surely

The next computation yields (42) for , since

Assume now that for , then (43) yields that

This is the same objective function as for normal entropic OT with cost function , and thus the case of (42) is just the non-adapted Schrödinger equation. This completes the proof of (42). In the bicausal case, the respective analogue for follows by symmetry. And for the causal case, (40) for is quickly derived similar to the non-adapted Schrödinger equation, and thus omitted.

The uniform bounds are satisfied by noting that the same bounds as given by Lemma 6.6 are given for and and thus by working backwards in time, the claim follows. ∎

The next lemma is insightful in order to understand Sinkhorn iterations in their dual form. Though the lemma is stated for causal projections, there are obvious analogues for classical and anticausal projections.

Lemma 6.9.

Let and , and with densities

Then

Proof.

It suffices to show that is constant for any with or . Since , we have that is constant for all . Assume w.l.o.g. that the entropy of w.r.t. is finite, then we conclude with

In the following, we introduce notation for the dual steps for Sinkhorn’s algorithm and a suitable normalization. Let be the Sinkhorn iterations from Definition 6.1. Further, denote by and the corresponding dual sets (cf. Section 5) to the building blocks from Definition 6.1. We know by Lemma 6.4, or equivalently Lemma 6.6, and its analogues that for

for some . Further, by Lemma 6.9, the respective function only depends on the prior function , but not on , and similarly only depends on , but not on . Thus, with this notation we have

We further denote by and the respective dual optimizers for , and introduce the normalized versions

Lemma 6.10.

The normalized Sinkhorn potentials satisfy the following.

-

(i)

There exists a constant only depending on such that

-

(ii)

For any , is orthogonal to in , i.e.,

Proof.

Part (i) follows from Lemma 6.6 since one can inductively show that, the following bounds for ,

imply the same bounds for . We may argue mutatis mutandis for . Note that

where the first inequality follows by the maximizing property in Lemma 6.6 and the last by weak duality. Finally, we have

which easily yields the claim.

Regarding (ii), we have to show that

This can again be shown via backward induction. Indeed, let

where we use the same notation as in Lemma 6.8. Note that, for , does not depend on and similarly does not depend on , hence,

Then, for , we get

Therefore, we conclude with

which vanishes by definition of and . ∎

To state the following theorem, denote by the objective value of Sinkhorn after the -th step, i.e.,

which obviously satisfies . The following result is based on the idea of Carlier [16] for the classical Sinkhorn’s algorithm.

Theorem 6.11 (Linear convergence of Sinkhorn’s algorithm).

There exist constants and only depending on and such that

Proof.

We will use strong convexity of the exponential function, i.e., we have for , and

| (45) |

In our case, as all functions are bounded (cf. Lemma 6.10 (i)), we will apply this inequality with , and denote by .

To ease notation, write . Using (45), we obtain

| (46) | ||||

where the equality uses Lemma 6.10 (ii). First, note that

| (47) |

since is chosen in a way so that is the density of a measure contained in (respectively ) w.r.t. .

Next, we treat the term in the above. Let

Again, as is up to a normalizing factor the density of w.r.t. , we find that

vanishes, because both terms on the right-hand side are zero by definition of and . Hence, we can apply Young’s inequality in order to derive

| (48) | ||||

By combining (46), (47) and (48), we obtain

where the last inequality holds due to the Lipschitz property of the exponential restricted to with constant . Finally, completely analogously to (46) we get (where we adopt the notation )

hence, the value is increasing in and

Then choosing yields

from where we easily conclude the first claim. The second claim follows by

which can be shown analogously to (46) and the subsequent line of arguments. ∎

Remark 6.12 (Sinkhorn’s algorithm in backward induction).

We shortly discuss the use of Sinkhorn’s algorithm to (approximately) solve the optimal transport problems in the backward induction of bicausal transport, as done in [41]. There are interesting connections of this utilization of Sinkhorn’s algorithm compared to the adapted version of Sinkhorn’s algorithm studied in this paper. First, both are (part of) algorithms to solve the entropic transport problem .

Concerning the algorithm proposed in the present paper, one may regard the Sinkhorn steps as the “outer algorithm”, which operate on joint couplings for the whole path space. Each step within the Sinkhorn algorithm, that is the projection onto or , respectively, are calculated using a backward induction, see Lemma 6.4. Thus, the backward induction can be seen as the “inner algorithm”.

In contrast, concerning the algorithm proposed in [41], one may regard the backward induction therein as the “outer algorithm”, whereas Sinkhorn’s algorithm is used to solve the respective steps of the backward induction. Thus, Sinkhorn’s algorithm takes the role of the “inner algorithm”.

There are theoretical arguments for both utilizations of Sinkhorn’s algorithm. First, we showed that the adapted version of Sinkhorn’s algorithm converges, even linearly, while the backward induction steps (the “inner algorithm”) can – at least for discrete spaces – be calculated precisely. Thus, the only errors resulting from the adapted version of Sinkhorn’s algorithm are happening in the outer loop. If convergence has not been reached yet, with this structure the algorithm can simply continue iterating in order to achieve convergence.

On the other hand, using Sinkhorn’s algorithm to calculate the steps of the backward induction as in [41] introduces an error in each step. Since the value of each time step is used as an input to the next step , this error propagates. Even though this error can be controlled, because entropic optimal transport is stable with respect to perturbations in the cost function, see, e.g., [23, 32], one may intuitively wish to avoid such propagating errors.

It is however also plausible that using Sinkhorn’s algorithm to calculate the steps of the backward induction as in [41] improves the speed of convergence compared to the adapted version of Sinkhorn’s algorithm. Indeed, with the adapted version of Sinkhorn’s algorithm, to calculate the transition kernels for time , one utilizes the current sub-optimal solution of the later time steps , since these are taken from the same iteration step. However, using backward induction as the outer algorithm, the later time steps have already reached their convergence criteria and can thus be regarded as more accurate inputs to the current step .

6.3 Numerical example: comparison of algorithms

To give a basic idea of the practical applicability of the introduced version of Sinkhorn’s algorithm, this section reports numerical results, where the focus is on both runtime and accuracy. The code to reproduce the experiments is available at https://github.com/stephaneckstein/aotnumerics.

The marginals and will be randomly generated Markovian trees on , , with width and number of branches (cf. [41, Chapter 5]), meaning that the transition kernels will be supported on at most integer points in the range . We choose two cost functions and given by

where the normalization by is used so that the supremum norm of the cost function on the support of the considered measures is around one, and thus the regularization parameter can be reasonably chosen within the same range for both cost functions.

| LP |

|

|

|

|

||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| cost function | ||||||||||||||

| 10 | 0.97 | - | - | 0.08 (12.7%) | 0.74 (0.48%) | |||||||||

| 25 | 107.10 | - | - | 0.47 (14.43%) | 4.31 (1.13%) | |||||||||

| 50 | - | - | - | 2.34 (-) | 19.37 (-) | |||||||||

| 10 | 1.61 | 0.60 | 1.08 (0.81%) | 0.08 (13.82%) | 0.97 (0.46%) | |||||||||

| 25 | 205.10 | 24.09 | 11.55 (1.51%) | 0.50 (16.25%) | 4.78 (1.24%) | |||||||||

| 50 | - | 308.55 | 79.72 (1.73%) | 2.21 (16.10%) | 18.60 (1.56%) | |||||||||

| cost function | ||||||||||||||

| 10 | 1.08 | - | - | 0.22 (0.99%) | 3.02 (0.07%) | |||||||||

| 25 | 106.86 | - | - | 1.49 (1.70%) | 18.13 (0.08%) | |||||||||

| 50 | - | - | - | 9.12 (-) | 105.01 (-) | |||||||||

| 10 | 1.55 | 0.60 | 2.44 (0.06%) | 0.27 (0.96%) | 4.59 (0.10%) | |||||||||

| 25 | 197.23 | 21.61 | 23.86 (0.03%) | 1.47 (1.87%) | 22.09 (0.06%) | |||||||||

| 50 | - | 315.70 | 108.97 (0.02%) | 8.74 (2.37%) | 105.86 (0.08%) | |||||||||

| 10 | 25 | 50 | 75 | 100 | |

|---|---|---|---|---|---|

| DPP (LP) | 0.62 | 21.61 | 315.70 | 1285.48 | 3784.37 |

| Sinkhorn () | 4.59 (0.10%) | 22.09 (0.06%) | 105.86 (0.08%) | 230.40 (0.07%) | 500.14 (0.04%) |

The results are reported in Table 1. Therein, we compare different algorithms, both exact (LP as in Lemma 3.11, and backward induction for the bicausal problem) and approximate (causal and bicausal version of Sinkhorn’s algorithm, and backward induction using Sinkhorn’s algorithm as the inner solver). Linear programs were implemented using Gurobi [29]. Sinkhorn’s algorithm for the backward induction was implemented using the PythonOT package [25]. Causal and bicausal versions of Sinkhorn’s algorithm as presented in this section were implemented from scratch in Python.

Table 1 shows that the runtime of the direct LP implementation using Lemma 3.11 increases quickly for increasing , but we emphasize that it is the only method to produce exact values for the causal problem. Causal and bicausal version of Sinkhorn’s algorithm give accurate results (for ) in comparable times to methods based on backward induction for bicausal problems, and noticably also much faster times than the direct LP implementation for the causal problem. Further, using yields quick approximate solutions, even for large values of .

Comparing the columns DPP () and Sinkhorn (), we note that the same theoretical problems are implemented, and the differences in relative error results purely from numerical inaccuracies and differing stopping criteria, cf. Remark 6.12. We emphasize that both methods start to be significantly faster than the exact DPP implementation for . We give additional values showing the extrapolation of this trend in Table 2. Therein, we see that for even larger values of , the Sinkhorn algorithm yields increasingly larger benefits in runtime compared to the exact backward induction method. Thus, Sinkhorn’s algorithm has particular benefits if the actual optimal transport problems occurring in the backward induction are large (). If however all transition kernels are supported on a small number of points (), there are no benefits in runtime compared to an exact backward induction using linear programming.

To conclude, numerically the introduced versions of Sinkhorn’s algorithm give comparable results to state of the art methods based on backward induction for the considered bicausal problems, while having the benefit of also being applicable to causal problems. In both cases (causal and bicausal), the runtime of Sinkhorn’s algorithm is drastically faster than a direct LP implementation even for moderately sized problems.

[Acknowledgments] The authors are grateful to two anonymous referees for their insightful remarks and constructive feedback. SE thanks the Erwin Schrödinger Institute for Mathematics and Physics, University of Vienna, where major parts of this project were completed.

Appendix A Topological aspects of AOT

Lemma A.1.

Let be a Polish space with topology , be a sequence of Polish spaces, and be a family of measurable kernels . Then there exists a Polish topology on such that the Borel--algebras generated by and coincide, and, for ,

| (49) | ||||

is continuous. In particular, we have that

Proof.

The map where is measurable and is Polish as a countable product. Hence, by [31, Theorem 13.11] there exists a Polish topology on such that

is continuous, , and the Borel sets of and coincide. Clearly, this is equivalent to (49). Finally, note that, for fixed , the map is continuous on . Consequently, is continuous on . Write for the continuous map . We can decompose

into , which shows . ∎

Lemma A.2.

Let , , and . Then if and only if we have, for all ,

Proof.

Since we have by Definition 2.1 that is causal if and only if, for all ,

As continuous functions are point-separating on , see for example [24, Chapter 3, Theorem 4.5], we find by the previous that is causal if and only if, for all and ,

Rearranging the terms in the displayed equation above yields the assertion. ∎

Lemma A.3.

Let and . Then is compact w.r.t. weak convergence in .

Proof.

As the Borel sets of and resp. and coincide, we have that and are Borel measures on and respectively. Thus, is a compact subset of . By Lemma A.2 we get

Since the identity above yields compactness of as a subset of , hence, it is compact in . ∎

References

- [1] {barticle}[author] \bauthor\bsnmAcciaio, \bfnmBeatrice\binitsB., \bauthor\bsnmBackhoff, \bfnmJulio\binitsJ. and \bauthor\bsnmJia, \bfnmJunchao\binitsJ. (\byear2021). \btitleCournot–Nash Equilibrium and Optimal Transport in a Dynamic Setting. \bjournalSIAM Journal on Control and Optimization \bvolume59 \bpages2273–2300. \endbibitem

- [2] {bbook}[author] \bauthor\bsnmAdams, \bfnmDavid R\binitsD. R. and \bauthor\bsnmHedberg, \bfnmLars I\binitsL. I. (\byear1999). \btitleFunction spaces and potential theory \bvolume314. \bpublisherSpringer Science & Business Media. \endbibitem

- [3] {barticle}[author] \bauthor\bsnmBackhoff, \bfnmJulio\binitsJ., \bauthor\bsnmBartl, \bfnmDaniel\binitsD., \bauthor\bsnmBeiglböck, \bfnmMathias\binitsM. and \bauthor\bsnmWiesel, \bfnmJohannes\binitsJ. (\byear2022). \btitleEstimating processes in adapted Wasserstein distance. \bjournalThe Annals of Applied Probability \bvolume32 \bpages529–550. \endbibitem

- [4] {barticle}[author] \bauthor\bsnmBackhoff, \bfnmJulio\binitsJ., \bauthor\bsnmBeiglbock, \bfnmMathias\binitsM., \bauthor\bsnmLin, \bfnmYiqing\binitsY. and \bauthor\bsnmZalashko, \bfnmAnastasiia\binitsA. (\byear2017). \btitleCausal transport in discrete time and applications. \bjournalSIAM Journal on Optimization \bvolume27 \bpages2528–2562. \endbibitem

- [5] {barticle}[author] \bauthor\bsnmBackhoff-Veraguas, \bfnmJulio\binitsJ., \bauthor\bsnmBartl, \bfnmDaniel\binitsD., \bauthor\bsnmBeiglböck, \bfnmMathias\binitsM. and \bauthor\bsnmEder, \bfnmManu\binitsM. (\byear2020). \btitleAdapted Wasserstein distances and stability in mathematical finance. \bjournalFinance and Stochastics \bvolume24 \bpages601–632. \endbibitem

- [6] {barticle}[author] \bauthor\bsnmBackhoff-Veraguas, \bfnmJulio\binitsJ., \bauthor\bsnmBartl, \bfnmDaniel\binitsD., \bauthor\bsnmBeiglböck, \bfnmMathias\binitsM. and \bauthor\bsnmEder, \bfnmManu\binitsM. (\byear2020). \btitleAll adapted topologies are equal. \bjournalProbability Theory and Related Fields \bvolume178 \bpages1125–1172. \endbibitem

- [7] {barticle}[author] \bauthor\bsnmBackhoff-Veraguas, \bfnmJulio\binitsJ. and \bauthor\bsnmPammer, \bfnmGudmund\binitsG. (\byear2022). \btitleStability of martingale optimal transport and weak optimal transport. \bjournalThe Annals of Applied Probability \bvolume32 \bpages721–752. \endbibitem

- [8] {barticle}[author] \bauthor\bsnmBackhoff-Veraguas, \bfnmJulio\binitsJ. and \bauthor\bsnmZhang, \bfnmXin\binitsX. (\byear2022). \btitleDynamic Cournot-Nash Equilibrium: The Non-Potential Case. \bjournalarXiv preprint arXiv:2202.13813. \endbibitem

- [9] {barticle}[author] \bauthor\bsnmBartl, \bfnmDaniel\binitsD., \bauthor\bsnmBeiglböck, \bfnmMathias\binitsM. and \bauthor\bsnmPammer, \bfnmGudmund\binitsG. (\byear2021). \btitleThe Wasserstein space of stochastic processes. \bjournalarXiv preprint arXiv:2104.14245. \endbibitem

- [10] {barticle}[author] \bauthor\bsnmBartl, \bfnmDaniel\binitsD. and \bauthor\bsnmWiesel, \bfnmJohannes\binitsJ. (\byear2022). \btitleSensitivity of multi-period optimization problems in adapted Wasserstein distance. \bjournalarXiv preprint arXiv:2208.05656. \endbibitem

- [11] {barticle}[author] \bauthor\bsnmBeiglböck, \bfnmMathias\binitsM. and \bauthor\bsnmLacker, \bfnmDaniel\binitsD. (\byear2018). \btitleDenseness of adapted processes among causal couplings. \bjournalarXiv preprint arXiv:1805.03185. \endbibitem

- [12] {barticle}[author] \bauthor\bsnmBeiglböck, \bfnmMathias\binitsM., \bauthor\bsnmPammer, \bfnmGudmund\binitsG. and \bauthor\bsnmSchrott, \bfnmStefan\binitsS. (\byear2022). \btitleDenseness of biadapted Monge mappings. \bdoi10.48550/ARXIV.2210.15554 \endbibitem

- [13] {barticle}[author] \bauthor\bsnmBindini, \bfnmUgo\binitsU. (\byear2020). \btitleSmoothing operators in multi-marginal optimal transport. \bjournalMathematical Physics, Analysis and Geometry \bvolume23 \bpages1–27. \endbibitem

- [14] {binproceedings}[author] \bauthor\bsnmBolley, \bfnmFrançois\binitsF. and \bauthor\bsnmVillani, \bfnmCédric\binitsC. (\byear2005). \btitleWeighted Csiszár-Kullback-Pinsker inequalities and applications to transportation inequalities. In \bbooktitleAnnales de la Faculté des sciences de Toulouse: Mathématiques \bvolume14 \bpages331–352. \endbibitem

- [15] {barticle}[author] \bauthor\bsnmBrückerhoff, \bfnmMartin\binitsM. and \bauthor\bsnmJuillet, \bfnmNicolas\binitsN. (\byear2021). \btitleInstability of Martingale optimal transport in dimension . \bjournalarXiv preprint arXiv:2101.06964. \endbibitem

- [16] {bunpublished}[author] \bauthor\bsnmCarlier, \bfnmGuillaume\binitsG. (\byear2021). \btitleOn the linear convergence of the multi-marginal Sinkhorn algorithm. \bnoteworking paper or preprint. \endbibitem

- [17] {barticle}[author] \bauthor\bsnmCarlier, \bfnmGuillaume\binitsG., \bauthor\bsnmDuval, \bfnmVincent\binitsV., \bauthor\bsnmPeyré, \bfnmGabriel\binitsG. and \bauthor\bsnmSchmitzer, \bfnmBernhard\binitsB. (\byear2017). \btitleConvergence of entropic schemes for optimal transport and gradient flows. \bjournalSIAM Journal on Mathematical Analysis \bvolume49 \bpages1385–1418. \endbibitem

- [18] {barticle}[author] \bauthor\bsnmCsiszár, \bfnmImre\binitsI. (\byear1975). \btitleI-divergence geometry of probability distributions and minimization problems. \bjournalThe annals of probability \bpages146–158. \endbibitem

- [19] {barticle}[author] \bauthor\bsnmCuturi, \bfnmMarco\binitsM. (\byear2013). \btitleSinkhorn distances: Lightspeed computation of optimal transport. \bjournalAdvances in neural information processing systems \bvolume26 \bpages2292–2300. \endbibitem

- [20] {binproceedings}[author] \bauthor\bsnmCuturi, \bfnmMarco\binitsM. and \bauthor\bsnmDoucet, \bfnmArnaud\binitsA. (\byear2014). \btitleFast computation of Wasserstein barycenters. In \bbooktitleInternational conference on machine learning \bpages685–693. \bpublisherPMLR. \endbibitem

- [21] {bbook}[author] \bauthor\bsnmDupuis, \bfnmPaul\binitsP. and \bauthor\bsnmEllis, \bfnmRichard S\binitsR. S. (\byear2011). \btitleA weak convergence approach to the theory of large deviations. \bpublisherJohn Wiley & Sons. \endbibitem

- [22] {barticle}[author] \bauthor\bsnmEckstein, \bfnmStephan\binitsS., \bauthor\bsnmKupper, \bfnmMichael\binitsM. and \bauthor\bsnmPohl, \bfnmMathias\binitsM. (\byear2020). \btitleRobust risk aggregation with neural networks. \bjournalMathematical finance \bvolume30 \bpages1229–1272. \endbibitem

- [23] {barticle}[author] \bauthor\bsnmEckstein, \bfnmStephan\binitsS. and \bauthor\bsnmNutz, \bfnmMarcel\binitsM. (\byear2021). \btitleQuantitative stability of regularized optimal transport and convergence of Sinkhorn’s algorithm. \bjournalarXiv preprint arXiv:2110.06798. \endbibitem

- [24] {bbook}[author] \bauthor\bsnmEthier, \bfnmStewart N\binitsS. N. and \bauthor\bsnmKurtz, \bfnmThomas G\binitsT. G. (\byear2009). \btitleMarkov processes: characterization and convergence. \bpublisherJohn Wiley & Sons. \endbibitem

- [25] {barticle}[author] \bauthor\bsnmFlamary, \bfnmRémi\binitsR., \bauthor\bsnmCourty, \bfnmNicolas\binitsN., \bauthor\bsnmGramfort, \bfnmAlexandre\binitsA., \bauthor\bsnmAlaya, \bfnmMokhtar Z.\binitsM. Z., \bauthor\bsnmBoisbunon, \bfnmAurélie\binitsA., \bauthor\bsnmChambon, \bfnmStanislas\binitsS., \bauthor\bsnmChapel, \bfnmLaetitia\binitsL., \bauthor\bsnmCorenflos, \bfnmAdrien\binitsA., \bauthor\bsnmFatras, \bfnmKilian\binitsK., \bauthor\bsnmFournier, \bfnmNemo\binitsN., \bauthor\bsnmGautheron, \bfnmLéo\binitsL., \bauthor\bsnmGayraud, \bfnmNathalie T. H.\binitsN. T. H., \bauthor\bsnmJanati, \bfnmHicham\binitsH., \bauthor\bsnmRakotomamonjy, \bfnmAlain\binitsA., \bauthor\bsnmRedko, \bfnmIevgen\binitsI., \bauthor\bsnmRolet, \bfnmAntoine\binitsA., \bauthor\bsnmSchutz, \bfnmAntony\binitsA., \bauthor\bsnmSeguy, \bfnmVivien\binitsV., \bauthor\bsnmSutherland, \bfnmDanica J.\binitsD. J., \bauthor\bsnmTavenard, \bfnmRomain\binitsR., \bauthor\bsnmTong, \bfnmAlexander\binitsA. and \bauthor\bsnmVayer, \bfnmTitouan\binitsT. (\byear2021). \btitlePOT: Python Optimal Transport. \bjournalJournal of Machine Learning Research \bvolume22 \bpages1-8. \endbibitem

- [26] {bbook}[author] \bauthor\bsnmFolland, \bfnmGerald B\binitsG. B. (\byear1999). \btitleReal analysis: modern techniques and their applications \bvolume40. \bpublisherJohn Wiley & Sons. \endbibitem

- [27] {barticle}[author] \bauthor\bsnmGulrajani, \bfnmIshaan\binitsI., \bauthor\bsnmAhmed, \bfnmFaruk\binitsF., \bauthor\bsnmArjovsky, \bfnmMartin\binitsM., \bauthor\bsnmDumoulin, \bfnmVincent\binitsV. and \bauthor\bsnmCourville, \bfnmAaron C\binitsA. C. (\byear2017). \btitleImproved training of wasserstein gans. \bjournalAdvances in neural information processing systems \bvolume30. \endbibitem

- [28] {barticle}[author] \bauthor\bsnmGuo, \bfnmGaoyue\binitsG. and \bauthor\bsnmObłój, \bfnmJan\binitsJ. (\byear2019). \btitleComputational methods for martingale optimal transport problems. \bjournalThe Annals of Applied Probability \bvolume29 \bpages3311–3347. \endbibitem

- [29] {bmisc}[author] \bauthor\bsnmGurobi Optimization, LLC (\byear2022). \btitleGurobi Optimizer Reference Manual. \endbibitem

- [30] {bbook}[author] \bauthor\bsnmKallenberg, \bfnmOlav\binitsO. (\byear1997). \btitleFoundations of modern probability \bvolume2. \bpublisherSpringer. \endbibitem

- [31] {bbook}[author] \bauthor\bsnmKechris, \bfnmAlexander\binitsA. (\byear2012). \btitleClassical descriptive set theory \bvolume156. \bpublisherSpringer Science & Business Media. \endbibitem

- [32] {barticle}[author] \bauthor\bsnmKeriven, \bfnmNicolas\binitsN. (\byear2022). \btitleEntropic Optimal Transport in Random Graphs. \bjournalarXiv preprint arXiv:2201.03949. \endbibitem

- [33] {barticle}[author] \bauthor\bsnmKomlós, \bfnmJanos\binitsJ. (\byear1967). \btitleA generalization of a problem of Steinhaus. \bjournalActa Mathematica Academiae Scientiarum Hungaricae \bvolume18 \bpages217–229. \endbibitem

- [34] {barticle}[author] \bauthor\bsnmLassalle, \bfnmRémi\binitsR. (\byear2018). \btitleCausal transport plans and their Monge–Kantorovich problems. \bjournalStochastic Analysis and Applications \bvolume36 \bpages452–484. \endbibitem

- [35] {barticle}[author] \bauthor\bsnmLéonard, \bfnmChristian\binitsC. (\byear2012). \btitleFrom the Schrödinger problem to the Monge–Kantorovich problem. \bjournalJournal of Functional Analysis \bvolume262 \bpages1879–1920. \endbibitem

- [36] {bbook}[author] \bauthor\bsnmMassart, \bfnmP.\binitsP. (\byear2007). \btitleConcentration inequalities and model selection. \bseriesLecture Notes in Mathematics \bvolume1896. \bpublisherSpringer, Berlin \bnoteLectures from the 33rd Summer School on Probability Theory held in Saint-Flour, July 6–23, 2003. \bmrnumber2319879 \endbibitem

- [37] {bmisc}[author] \bauthor\bsnmNutz, \bfnmMarcel\binitsM. (\byear2021). \btitleIntroduction to Entropic Optimal Transport. \endbibitem

- [38] {barticle}[author] \bauthor\bsnmPeyré, \bfnmGabriel\binitsG. and \bauthor\bsnmCuturi, \bfnmMarco\binitsM. (\byear2019). \btitleComputational optimal transport: With applications to data science. \bjournalFoundations and Trends® in Machine Learning \bvolume11 \bpages355–607. \endbibitem

- [39] {barticle}[author] \bauthor\bsnmPflug, \bfnmG Ch\binitsG. C. (\byear2010). \btitleVersion-independence and nested distributions in multistage stochastic optimization. \bjournalSIAM Journal on Optimization \bvolume20 \bpages1406–1420. \endbibitem

- [40] {barticle}[author] \bauthor\bsnmPflug, \bfnmGeorg Ch\binitsG. C. and \bauthor\bsnmPichler, \bfnmAlois\binitsA. (\byear2012). \btitleA distance for multistage stochastic optimization models. \bjournalSIAM Journal on Optimization \bvolume22 \bpages1–23. \endbibitem

- [41] {barticle}[author] \bauthor\bsnmPichler, \bfnmAlois\binitsA. and \bauthor\bsnmWeinhardt, \bfnmMichael\binitsM. (\byear2021). \btitleThe nested Sinkhorn divergence to learn the nested distance. \bjournalComputational Management Science \bpages1–25. \endbibitem

- [42] {barticle}[author] \bauthor\bsnmRüschendorf, \bfnmLudger\binitsL. (\byear1995). \btitleConvergence of the iterative proportional fitting procedure. \bjournalThe Annals of Statistics \bpages1160–1174. \endbibitem

- [43] {bbook}[author] \bauthor\bsnmVillani, \bfnmCédric\binitsC. (\byear2009). \btitleOptimal transport: old and new \bvolume338. \bpublisherSpringer. \endbibitem

- [44] {barticle}[author] \bauthor\bsnmWiesel, \bfnmJohannes\binitsJ. (\byear2019). \btitleContinuity of the martingale optimal transport problem on the real line. \bjournalarXiv preprint arXiv:1905.04574. \endbibitem

- [45] {barticle}[author] \bauthor\bsnmXu, \bfnmTianlin\binitsT. and \bauthor\bsnmAcciaio, \bfnmBeatrice\binitsB. (\byear2021). \btitleQuantized Conditional COT-GAN for Video Prediction. \bjournalarXiv preprint arXiv:2106.05658. \endbibitem

- [46] {barticle}[author] \bauthor\bsnmXu, \bfnmTianlin\binitsT., \bauthor\bsnmWenliang, \bfnmLi Kevin\binitsL. K., \bauthor\bsnmMunn, \bfnmMichael\binitsM. and \bauthor\bsnmAcciaio, \bfnmBeatrice\binitsB. (\byear2020). \btitleCot-gan: Generating sequential data via causal optimal transport. \bjournalAdvances in Neural Information Processing Systems \bvolume33 \bpages8798–8809. \endbibitem