Large Sample Covariance Matrices of Gaussian Observations with Uniform Correlation Decay

Abstract.

We derive the Marchenko-Pastur (MP) law for sample covariance matrices of the form , where is a data matrix and as . We assume the data in stems from a correlated joint normal distribution. In particular, the correlation acts both across rows and across columns of , and we do not assume a specific correlation structure, such as separable dependencies. Instead, we assume that correlations converge uniformly to zero at a speed of , where may grow mildly to infinity. We employ the method of moments tightly: We identify the exact condition on the growth of which will guarantee that the moments of the empirical spectral distributions (ESDs) converge to the MP moments. If the condition is not met, we can construct an ensemble for which all but finitely many moments of the ESDs diverge. We also investigate the operator norm of under a uniform correlation bound of , where are fixed, and observe a phase transition at . In particular, convergence of the operator norm to the maximum of the support of the MP distribution can only be guaranteed if . The analysis leads to an example for which the MP law holds almost surely, but the operator norm remains stochastic in the limit, and we provide its exact limiting distribution.

Key words and phrases:

Sample covariance matrices, Marchenko-Pastur law, correlated Gaussian, operator norm2020 Mathematics Subject Classification:

Primary: 60B20. Secondary: 60F05, 60G551. Introduction

In contemporary statistical analyses, data sets are typically large both in the sample size and in the dimension of the observations. Since many test statistics are based on the eigenvalues of the sample covariance matrix, their asymptotic study has gained wide popularity and led to applications in many fields of modern sciences. In the classical setting of data matrices with independent and identically distributed (i.i.d.) entries, the famous Marchenko-Pastur law [12] describes the asymptotic distriution of these eigenvalues.

Ever since, the universality of the Marchenko-Pastur law is under close investigation: How far may we deviate from the classical i.i.d. assumption and still obtain the Marchenko-Pastur distribution as a limit? For example, in practical applications it is plausible to assume that data may be correlated or at least dependent. Even up to today, results for matrices with dependencies spreading over all entries are rather sparse: The recent paper [5], for example, establishes the Marchenko-Pastur law for data matrices with independent observations (columns), but where covariates within these columns may exhibit stochastic dependencies (but are assumed to be uncorrelated). They also provide an interesting review of previous literature in this direction.

Many previous analyses (cf. [5, 16, 3]) investigate the case where rows (resp. columns) of the data matrices are assumed to be independent and stochastic dependencies may only prevail within these rows (resp. columns). Studies which allow correlation to span both across rows and columns are sparse: In [14], separable sample covariance matrices were studied, which are of the form with , where is a deterministic Hermitian and positive semidefinite matrix, is an deterministic diagonal matrix with non-negative real-valued entries, and has i.i.d. entries with mean zero and unit variance. In this model the covariance structure of is given by the Kronecker product , which is a matrix. Since is determined by the entries of and , covariance structures determined by Kronecker products are somewhat limited in their variability. In other words, some covariance structures – such as the equicovariant structure (in Theorem 3 below) – cannot be expressed as a Kronecker product. Another study where correlations may span both across rows and columns is [8], where the authors derived the Marchenko-Pastur law for data matrices filled with jointly correlated random spins stemming from the Curie-Weiss model from statistical physics. There, even for the case of non-vanishing correlations, the Marchenko-Pastur law is recovered.

The present paper studies the case where data is jointly Gaussian distributed and where correlations may act both across rows and columns of the data matrix. In Theorem 1, we do not impose any conditions on the correlation structure except that we require all correlations to decay uniformly at a speed of , where for all . We employ the method of moments to derive our results and we show that if not , the Marchenko-Pastur law cannot be guaranteed by the method of moments. More precisely, there exist ensembles matching the condition, such that all sufficiently large moments of a subsequence of the ESDs diverge to infinity, allowing no conclusion about weak convergence. In Theorem 2, we investigate the convergence of the operator norms of our ensembles for which we assume that correlations decay uniformly at rates , where and are fixed in . We derive the following phase transition: For , the operator norm of the sample covariance matrices converges almost surely to the right endpoint of the support of the Marchenko-Pastur distribution. For , there exist ensembles matching the condition such that the operator norm converges to infinity. For , we provide an ensemble for which the operator norm remains stochastic in the limit, so in particular, it does not converge to a constant, nor to infinity. Finally, the case where all correlations are of the same size will be studied in depth in Theorem 3, where we provide precise limit results for the operator norm of the sample covariance matrices.

2. Setup and Results

We assume that observations are -dimensional random vectors, so that we obtain a data matrix with columns . Based on these data, we define the sample covariance matrix of dimension ,

and analyze the eigenvalues of as its dimensions tend to infinity. To be precise, we assume that the number of observations and the number of covariates grow asymptotically proportionally with each other, so that as . This assumption is typical in random matrix theory, see for instance the monographs [1, 15]. Throughout this paper, we assume that is a function of , i.e., , but for simplicity we suppress this dependence notationally. In the following, we write for any .

We impose the following assumptions about the sequence of data matrices :

-

(A1)

For all , , where is a positive semidefinite matrix, indexed by pairs , so that

and for all and .

-

(A2)

We assume that there exists a sequence in with for all such that the sequence satisfies:

(1) -

(A3)

There is a constant such that as .

Assumption (A1) states that all observations are jointly normal and have variance . Assumption (A2) can be considered the main assumption in our model: We do not require correlations to follow a specific structure, but we do require them to decay uniformly at a speed of .

For all , we define to be the empirical spectral distribution (ESD) of , i.e.

where are the eigenvalues of and denotes the Dirac measure at point . Note that the probability measures are random, as they depend on the random eigenvalues of .

Notationally, if is a probability measure on and is -integrable, we write , where when in doubt, is the variable of integration, for example, if , then . Now as is a random probability measure, its -th moment is a real-valued random variable.

Our first goal is to see converge weakly almost surely to the Marchenko-Pastur distribution with ratio index , where

, . The moments of are given by (see [1], for example)

| (2) |

Theorem 1.

The following statements hold:

-

i)

Let be an ensemble of jointly Gaussian observations satisfying assumptions (A1), (A2) and (A3), and let be the ESD of . Then the moments of converge almost surely to the moments of , that is

(3) In particular, (3) implies almost surely as .

-

ii)

The result in is tight in the following sense: For any sequence which does not satisfy for all , there exists an ensemble satisfying assumptions (A1), (A3), and also (1), such that all but finitely many moments of a subsequence of diverge to infinity.

Part of Theorem 1 shows that our conditions are methodically tight, i.e., if the uniform correlation bound in (A2) is relaxed, then the method of moments cannot be used to infer weak convergence.

Our second goal of this paper is to investigate the behavior of , the operator norm of . If the Marchenko-Pastur law holds, it is not unreasonable to expect to converge almost surely to the right endpoint of the Marchenko-Pastur distribution. Part in the following theorem shows that this is indeed the case for a large subclass of the models we investigated in Theorem 1 . However, in part of the following theorem we see that convergence of to need not take place, although Theorem 1 is applicable. Instead, the operator norm may remain stochastic in the limit.

Theorem 2.

Let be an ensemble of jointly Gaussian observations satisfying assumptions (A1), (A3), and

| (A2’) |

for some fixed . Then the following statements hold for .

-

i)

If , then almost surely as .

-

ii)

If , there exist ensembles satisfying the assumptions of the theorem such that almost surely as .

-

iii)

If , there exists an ensemble satisfying the assumptions of the theorem such that, as , converges almost surely to some non-degenerate random variable.

Statements and of Theorem 2 require the construction concrete examples. The leading example (a variant of which is also used for the proof of Theorem 1 ) is a setup we call equicovariant ensemble: An ensemble of centered jointly Gaussian observations will be called equicovariant with sequence , if for all and all we have . Statements and of Theorem 2 follow from the next result.

Theorem 3.

Let , where satisfies (A1), (A3) and is equicovariant with sequence for some fixed . Then as , the following statements hold:

-

i)

If , then converges almost surely to .

-

ii)

If , then

where is a standard normal random variable.

-

iii)

If , then

where is a standard normal random variable.

Further, the ensemble can be constructed so that the convergence in and holds almost surely.

3. Proof of Theorem 1: Analysis of moments.

In order to prove Theorem 1, we employ the method of moments. To apply this method, it is sufficient to carry out the following two steps. First, we show that

| (4) |

Second, if for all , is a finite decomposition such that for all , converges to a constant (this decomposition will become clear when showing (4)), then we show that

| (5) |

Indeed, by virtue of (4) we obtain weak convergence of to in expectation, and (5) yields almost sure convergence of the random moments which entails almost sure weak convergence of to . See e.g. [9] for details. This section is organized as follows: In Subsection 3.1 we introduce combinatorial concepts needed for our proof. in Subsection 3.2 we derive convergence of expected moments (4), and in Subsection 3.3 we show that the variances of the decomposed random moments decay summably fast (5).

3.1. Combinatorial Preparations

To show (4) and (5), we need the moments of and . The moments of are given above in (2), whereas we may calculate the moments of by

| (6) |

where for all and we define

| (7) |

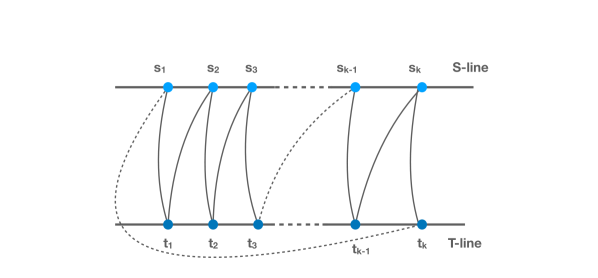

As we saw in (6), the random moments expand into elaborate sums. In order to be able to analyze these sums, we sort them with the language of graph theory. Each pair spans a Eulerian bipartite graph as in Figure 1.

Here, elements in the set resp. are called S-nodes resp. T-nodes. S- and T-nodes are considered different even if their value is the same and are thus placed on separate lines – called S-line and T-line – which are drawn horizontally beneath each other. Then we draw an undirected edge between and , , , whenever or appears in (7), where we allow for multi-edges. Here, if appears in (7), we will call the edge down edge, whereas if appears in (7), we call up edge (cf. Figure 1). This yields the graph , where

Each also denotes a Eulerian cycle of length through its graph by

| (8) |

Note that by construction, contains no loops, but may contain multi-edges. The language of graph theory allows us to express in a different way. Recall

| (9) |

with

| (10) |

For any pair of tuples , we define its profile

where for all

Here, an -fold edge in is any element for which there are exactly distinct other elements so that for .

We now find that for all , the Eulerian cycle traverses exactly -fold edges. As a result, the following trivial but useful equality holds:

| (11) |

Now for all we define the following set of profiles:

Using this notation, we may write

| (12) |

where

The transition from (9) to (12) allows us to keep track (in particular) of single and double edges since their contribution (or lack thereof) is a crucial point to analyze.

The next fundamental lemma will give an upper bound on the number of tuple pairs with at most vertices. Note that there are always at least two vertices present, since S-nodes and T-nodes are disjoint. Notationally, we set for any and if also , we set , even if we do not regard as a graph. In particular, .

Lemma 4.

Let , and be arbitrary. Then

Proof.

For i) we check how many possibilities we have to construct such an (). First, we determine the coloring for by picking a surjective function , determining which places in should contain equal or different entries. This admits at most choices. Now we pick a value for and have possibilities. Then if , we have no choice for since then must be equal to . Otherwise, if , we are left with at most choices for . Proceeding this way for , if for some then set , and otherwise we have at most choices for , and these non-trivial choices happen times after the initial choice of , thus admitting at most choices for . Likewise, we pick a color structure for for which we have at most choices and construct with at most choices. In total, we have at most

choices. This proves i), and for ii) we first decide on the number of different vertices in and the number of different vertices in such that . This choice of admits at most choices. Then with i), the statement follows. ∎

3.2. Convergence of expected moments

In this subsection we establish (4), which will prove the MP law in expectation. To this end, we proceed to analyze

| (13) |

The way we analyze (13) is to establish upper bounds on depending on its profile , and to bound by a function of , and . For the latter, we formulate the next lemma. It is a modification of corresponding lemmas obtained in [7] in the setting of random band matrices.

Lemma 5.

Proof.

Each is a -tuple in which for all the entry lies in the set , which follows directly from (11). Therefore,

where the fourth step is well-known fact about the central binomial coefficient. For the proof of statements and it suffices to establish the upper bounds for , since the bounds on then follow directly with Lemma 4 . Now to prove upper bounds for , the idea is to travel the Eulerian cycle generated by

| (14) |

by picking an initial node or and then traversing the edges in increasing cyclic order until reaching the starting point again. On the way, we count the number of different nodes that were discovered. Whenever we pass an -fold edge, only the first instance of that edge may discover a new vertex.

We start our tour at and observe this very vertex. Then, as we travel along the cycle, for each we will pass -fold edges out of which only the first instance can discover a new node, and there are of these first instances. Considering the initial node, we arrive at , which yields the desired inequality.

In presence of an odd edge, we can start the tour at a specific vertex such that the odd edge cannot contribute to the newly discovered vertices. To this end, fix an -fold edge in with odd. Let , , be the instances of the -fold edge in question in the cycle (14). Since is odd, we must find a such that and are both up edges or both down edges (where ), since we are on a cycle. W.l.o.g. and are a down edges. We start our tour at the T-node after . Since is a down-edge as well, its initial S-node must be discovered by an edge different from our -fold edge. In particular, none of the edges may discover a new vertex. Therefore, the roundtrip leads to the discovery of at most new nodes in addition to the first node.

∎

Having established bounds on the quantities in (13), we now proceed to make the expressions amenable for analysis. Note that by the generalized Hölder inequality, we can always apply the bound , which is the -th moment of a standard normal random variable. But we will have to bound in more sophisticated ways. Recall that is a -matrix of jointly Gaussian entries with covariance matrix

for all , . In particular, is a matrix, indexed by pairs.

To evaluate expectations of a product of correlated Gaussian random variables as in (6), (7), or (13), we use the “Theorem of Isserlis”, also know as “Wick’s theorem”, see e.g. [13] or [11].

Theorem 6.

Let and be a positive semidefinite, real symmetric matrix. If , then for all and , it holds

where denotes the set of all pair partitions on . In particular, we obtain for odd that

Using the formula of Isserlis, we can give a more detailed version of (13) as follows:

| (15) |

where for any , is the pair containing the nodes connected by the -th edge of .

Next, let us analyze for which we can expect an asymptotic contribution in (15).

Case 1: and for some .

We obtain

where the upper case is valid in presence of an odd edge (in which we then find at least a second odd edge), and the lower case is valid if no odd edges are present.

Therefore, by Lemma 5, and since each summand is uniformly bounded by some constant , we find a contribution of order , where means with a constant which depends only on .

Case 2: . In this case, admits only double edges, and we denote this specific profile by , so and for all . Then by Lemma 5, all have at most nodes, so we may subdivide this set further. We define

and note that by Lemma 4, , so that

Now we use the formula of Isserlis again to obtain

| (16) |

We observe in (16) that for each , there is exactly one pair partition which pairs all the double edges in , the subsequent product then assuming the value . For all finitely many other , we find at least two blocks in which pair two different edges, thus leading to at least two factors of off-diagonal entries in , thus at least to a decay of order . So for all ,

Therefore, (16) becomes

| (17) |

where means with constant .

Since by Lemma 5,

we obtain

| (18) |

It is well-known that (e.g. [9] or from the analysis in [1])

which is the -th moment of the MP distribution , cf. (2). Here, for any integers , , where an empty product equals .

We have now completely established the contribution in (15) stemming from those with . Their contribution is either vanishing or – in the case – yielding the moments of the Marchenko-Pastur distribution. Therefore, we will have shown (4) if we can show that those with have a vanishing contribution.

Case 3: .

Since , we obtain by Lemma 5 that

On the other hand, for every , each pair partition has at least blocks leading to off-diagonal entries of , thus yielding a decay of or faster in the product in (15). As a result,

Therefore, we see that under the condition that for all , all with will not contribute to the expected moments asymptotically. This proves the MP law in expectation, that is, (4), under assumptions (A1), (A2) and (A3).

3.3. Divergence of expected moments

In this subsection we prove the second statement of Theorem 1. We will show that if in the condition

| (19) |

we do not require that for all , that then there is an ensemble of correlated Gaussian data matrices the entries of which have covariance matrix satisfying this condition, but where all but finitely many moments diverge to infinity. To this end, let and such that . Then there is a and a subsequence such that for all . W.l.o.g. we may assume that and . Then define

Then surely, the sequence is a sequence of positive definite covariance matrices, and it satisfies (19). Inspecting the sum (15), we obtain with the same arguments as above, that the profiles with will yield the MP moments asymptotically (in the case ) or have a vanishing contribution (in the case for some ). We now observe that all summands in (15) are positive, so it suffices to identify a profile with and a contribution that diverges to infinity as for all large enough. To this end, let be the profile with and be the subset of all with . Then

On the other hand, for all , , and ,

Therefore, for ,

as soon as is chosen so large that . More precisely, for all , for .

3.4. Decay of the variances

When analyzing the expectation of the random moments, we used the finite decomposition of the random moment as in (12) and showed that for each , the -part of the random moment

| (20) |

converges in expectation to a constant; it converges to the -th moment of the Marchenko-Pastur distribution if , and to zero if . To establish that moments converge almost surely, it thus suffices to show that the variance of each -part (20) converges summably fast to zero. This variance is given by

| (21) |

Now by Isserlis’ formula,

| (22) |

where for any , is the pair containing the nodes connected by the -th edge of if or by the -th edge of if . Further, we obtain

| (23) |

We will call a partition contained, if any block is either a subset of or of . The key idea now is to associate any combination to the corresponding unique contained partition by defining the function , , and then

Denote by the set of non-contained pair partitions of . That is, each has at least one block (and thus at least two blocks) where and . Blocks with this property will be called traversing in what follows. Note that each has at least two traversing blocks. We observe

| (24) |

Thus, (21) becomes

| (25) |

It is our goal to show that (25) converges to zero summably fast. To this end, we define

and for all ,

In (25) we will now consider the partial sums over and then over for all .

Case 1: The edge-disjoint case.

Subcase 1: has only even edges.

Then by Lemma 5,

Since every non-contained will lead to at least 2 factors of decay in the product in (25), we obtain that the partial sum in (25) over is bounded by:

Subcase 2: has an odd edge.

Then by Lemma 5,

Also, we obtain at least factors of decay in the product in (25), since in the worst case, groups two single edges of each with a single edge of and all remaining single edges into pairs. Thus, the partial sum in (25) over is bounded by:

Case 2: The common-edge case.

In the edge-disjoint case, the fact that we considered only contained partitions helped in that the (at least) two traversing blocks led to two factors of decay in the product of covariances in (25). In the common-edge case, this advantage is diminished since it is possible the traversing blocks in group common (i.e. same) edges in and , leading to factors of in the product of covariances. To make up for this diminished decay, we need good bounds on the quantities , which is the content of the following lemma:

Lemma 7.

Proof.

For statement we assume w.l.o.g. that has an odd edge. Since the graphs spanned by and share common edges, we may take a tour around the joint Eulerian circle, starting before a common edge, traveling first all edges of and then all edges of . While walking the edges of , we can see at most different nodes by Lemma 5. Next, traveling all edges of , at most all the single edges and first instances of -fold edges with of may discover a new node, but only if they have not been traversed before during the walk along . Since we have common edges, we can see at most new nodes. We established the bounds on the number of vertices in . The second statement in follows immediately with Lemma 4 by concatenating and . For statement we proceed exactly in the same manner: Traveling we can see at most nodes by Lemma 5, then traveling we can see at most new nodes. Now apply Lemma 4 again. ∎

In the following subcases, we assume that the number of common edges is fixed and that we consider the subsum over in (25).

Subcase 1: has only even edges.

Then by Lemma 7,

Therefore, the partial sum in (25) over is bounded by

Subcase 2: has an odd edge.

Then by Lemma 7,

Now let be fixed. Then for each common edge, might pair a single edge in and the same single edge in , leading to a factor of in the product of covariances. This can happen at most times in the worst case. Also in the worst case, could then pair all the remaining single edges in with each other, and likewise the remaining single edges in with each other, leading to at least factors of decay in the product of covariances in (25). Therefore, the partial sum in (25) over is bounded by

This concludes the proof.

4. Proof of Theorems 2 and 3: Analysis of the Largest Eigenvalue.

In this section, we analyze the largest eigenvalue of where satisfies (A1), (A2’) and (A3), so that the correlations of the ensemble are uniformly bounded as follows:

for some fixed , where we assume for notational simplicity and w.l.o.g. that . We will show that if we can guarantee almost sure convergence to the operator norm of to , which is the maximum of the bounded support of the Marchenko-Pastur distribution , where . On the other hand, if , we can find an equicovariant ensemble matching above mentioned conditions and for which the operator norm of diverges to infinity almost surely. Lastly, if , we can find an ensemble matching (A1), (A2’), and (A3), for which the operator norm remains stochastic in the limit. The precise results for the cases and constitute Theorem 3, while qualitative versions of these results are mentioned in parts and of Theorem 2. This section is organized as follows: In Subsection 4.1, we show convergence of the operator norm for , thus proving Theorem 2 . A key lemma which is used here is proved in Subsection 4.2. Subsection 4.3 contains the proof of Theorem 3, where we construct the counterexamples for the cases and . From these counterexamples, statements and of Theorem 2 follow.

4.1. Convergence of the operator norm

To show convergence of the operator norm in the case , we follow the general strategy outlined in [10]. For , Theorem 1 implies that the Marchenko-Pastur law holds almost surely, from which it follows that almost surely, so it suffices to show almost surely. To this end, we fix and use

and show

for a suitable integer sequence . By the Borel–Cantelli lemma, this will imply . Writing and using

it suffices to find a sequence such that the terms

| (26) |

are summable over . To this end, as in [10] we will choose

| (27) |

Our analysis will greatly depend on the number of singles and doubles present in the paths in (26), and also on the number of distinct nodes that these paths visit. In this respect, the following lemma provides valuable information. For any given path we denote by the number of rows and by the number of columns that visits, and we set .

Lemma 8.

Let be arbitrary. Consider and the product as defined in (7). Then the following statements hold:

-

i)

has at least distinct entries.

-

ii)

has at most distinct entries.

-

iii)

If does not contain singles, then .

-

iv)

If , then contains at least singles.

-

v)

If has no singles, so , then has at least doubles.

-

vi)

If has singles, then it has at least doubles.

-

vii)

If has singles, then .

Proof.

For , note that after the first entry, there are row and column innovations left. For , we observe that a bipartite graph with nodes on the S-line and nodes on the T-line has at most edges. For , if were possible, then would have at least entries, which is impossible if each one is to occur at least twice. For , note that there are distinct variables. Delete from each a copy, then there are variables left, none of which were singles. Therefore, is an upper bound on the variables with multiplicity , so is a lower bound on the singles. It follows that is also a lower bound. Statements and are proven similarly to . For , the lower bound is elementary. For the other lower bound, note that has at most entries by , thus . The upper bound follows with the first statement in Lemma 5 b). ∎

Returning to (26), we denote by a valid bound for any , where the path visits nodes and has singles. Likewise, by we denote an upper bound on the number of paths with singles and different nodes. We point out that the constants and also depend on the length of the cycles and on , but we will suppress this dependence in what follows (except in the proof of Lemma 9). We can now bound (26) by

| (28) |

where we also used Lemma 8. The following lemma establishes bounds on the terms and in (28).

Lemma 9.

If has single edges, then for all large enough (independent of and ) we have the following valid bounds on and for , where is arbitrary but fixed.

-

a)

.

-

b)

.

-

c)

.

-

d)

.

-

e)

Whenever , we have

(29)

We defer the proof of the bounds in Lemma 9 to Subsection 4.2 and take them for granted for now. We would like to see that the r.h.s. of (28) is summable over . For the first term, this follows directly from the analysis in [10]. To see this, note that for , the bounds of Lemma 9 , , and coincide with the bounds of Lemma 1 and Lemma 2 in [10], the only difference being a prefactor of in our bound b), which does not affect the analysis. Therefore, it suffices to establish that

| (30) |

is summable over . Here, we distinguish between three regimes: The case where and are both small, the case where is small and is large, and the case where is large and is arbitrary. To clarify where we differentiate between “large” and “small”, we consult Lemma 9. We see that bound is only meaningful if

This is the small regime, the complement is the large regime. Further, if is small, then compatible with , is regarded small, and is regarded large. We will use the following basic lemma several times in what follows.

Lemma 10.

For any constants the term

is summable over .

Proof.

Taking the of the term and dividing by yields

which is smaller than for all large enough. Since is finite, the desired result follows. ∎

Case 1: is small and is large

In this case, we apply the bounds b) and e) of Lemma 9 and calculate

| (31) |

which is summable over , since the last sum remains bounded by some constant . Then, with , and (27), we find for any constants that for all large enough,

which shows summability of (31). Note that it was used that is small, since only for these small we may use the bound Lemma 9 for large .

Case 2: and are both small.

In this case, we employ the bounds and of Lemma 9 and calculate

| (32) |

To see that (32) is summable for any choice of , we distinguish two cases: First, if , the sum in (32) remains bounded as and summability of the entire term follows with Lemma 10. On the other hand, if but , the term in (32) is bounded by

which is also summable with Lemma 10.

Case 3: is large.

In this case, we apply the bounds and and calculate

which is summable by Lemma 10.

4.2. Proof of Lemma 9

We recall that

| (33) |

so a) follows immediately, since each factor in the product is bounded by . Statement c) is trivial and follows from (the proof of) Lemma 2 (a) in [10]. For d), we first allocate the non-single edges to places, for which we have at most possibilities. This also determines the places of the singles. Then we pick the nodes which may be chosen freely, for which we have at most possibilities. For the nodes that may be chosen freely, we have at most choices. For all other nodes we have at most choices. For , the statement is well-known for , see [10] Lemma 2 (b). If has singles, repeat each single twice after its first appearance, yielding a unique path of length without singles and with nodes. In formulas, we observe . Now the following statement holds: For all large enough we find that for all and , satisfies the bound in (29). This is readily seen by repeating the proof of Lemma 2 b) in [10] after replacing with at each step. The only place where heed must be taken is equation (13) in [10] where it must be argued that for all large enough, we find for all that whenever . But this follows since

and using that and , we find

for all large enough such that

Note that this choice of is independent of .

It remains to show b). For b), we fix a path with single edges and with . Denote by the number of distinct double edges in the path. By Lemma 8 we know that

| (34) |

To bound (33), we first consider the pair partitions in (33) which are contained in the sense that where is a pairing of the variables from the doubles and is a pairing of the remaining non-double variables, out of which are single.

For the non-double variables, we get possible pairings, each leading to a contribution of at most in the product over their blocks, since in the worst case, all singles are paired with each other, and the edges of multiplicity are also paired with each other.

For the doubles, we have exactly one partition which pairs all the doubles, leading to a contribution of exactly in the partial product over its blocks in (33). All other have void pairings (a void paring is a block which does not pair the two edges of a double edge) which then lead to a factor of at most in the partial product over its blocks in (33). Define for ,

Note that each with yields a contribution of at most in the sum (33).

To construct a , we first have choices for the doubles which shall not be paired. Then we choose a pair partition which only has void pairings, for which we have at most possibilities. For all other pairs there is only one pair partition in which pairs the pairs, so

As a result, for the sum in (33) over the contained pair partitions we obtain

| (35) |

for all large enough. This finishes the analysis of contained partitions .

It is left to analyze the contribution of the non-contained in (33), that is, those pair partitions which pair a double variable with a non-double variable. Each such has

-

•

at least traversings (i.e. blocks that pair a double variable with a non-double variable),

-

•

at most traversings,

-

•

always an even number of traversings.

Each traversing block yields a factor of decay of . Let , . Then to determine the traversing blocks, we first pick out of the double elements, and have for each at most choices for a partner among the variables, leading to at most choices for the traversing blocks. All other blocks contain either double variables only or non-double variables only. The non-double variables contain at least singles, so we get a decay of at least , for each of the possible pairings of these elements.

For the blocks over the remaining doubles we may have void pairings of the doubles, each leading to a decay of . To complete the pair partition, we need to determine the blocks for the remaining double elements in such a way that we get exactly void pairings. Due to the configuration of the traversing blocks, this might not be possible for a given ( possibilities), but we can always construct an upper bound: So we assume that it is possible to have exactly void pairings. This leaves double elements to be paired in a void way for which we have at most choices. Since the remaining double elements are paired, this leaves only one choice for these blocks. Combining everything we just argued, we obtain

4.3. Proof of Theorem 3

Let and let for all and all :

| (37) |

where is a matrix with i.i.d. distributed entries, is independent of and also distributed. Then , and for we have .

Let and denote by the matrix with entry at each place. Then

Since the entries in are i.i.d. Gaussian, it is well known that almost surely, which also implies that almost surely. Now we turn to and see that

has eigenvalues and , from which we deduce

so in particular almost surely. Next, we will show that is negligble. To this end, we calculate

the eigenvalues of which are and the sum of the entries in the first column. Therefore,

almost surely for any , which follows from the LLN of Marcinkiewicz-Zygmund (see e.g. [6]). Similarly it follows that almost surely, so that

| (38) |

almost surely. Since respectively , our findings immediately imply statements respectively (of course, statement also follows directly with part of Theorem 2).

Finally, we turn to the case where which is more involved because and are both of constant order. We have

where denotes the matrix with all entries one. In order to analyze the largest eigenvalue of , we note that for any orthogonal matrix it holds

| (39) |

For any real symmetric matrix , we denote its spectral decomposition by , where is the diagonal matrix whose -th diagonal element is the -th largest eigenvalue of , and is an orthogonal matrix. Choosing in (39), we get

where is the matrix with -entry equal to and all other entries zero. Since the matrix is orthogonally invariant, that is for any orthogonal matrix independent of , we conclude

| (40) |

In order to study the right-hand side in (40), we introduce for the diagonal matrices with and , . Further let be an matrix of i.i.d. standard Gaussian random variables. Then it holds that and have the same set of nonzero eigenvalues, and in particular . By either [4, Theorems 1.1-1.3] or [2, Theorems 4.1 and 4.2] (compare also with Theorem 11.3 in [15]), we have,

| (41) |

Writing for the columns of and using the notation , we get

where in the last step we used that by the law of large numbers. Utilizing the rotational invariance of the normal distribution and the fact that are independent from , we conclude that

Together with (41), this implies, as ,

| (42) |

Noting that , we now deduce from (40) and (42) that, since is independent of ,

| (43) |

Thus, we obtain

completing the proof.

References

- [1] Zhidong Bai and Jack W. Silverstein “Spectral Analysis of Large Dimensional Random Matrices” Springer, 2010

- [2] Zhidong Bai and Jianfeng Yao “On sample eigenvalues in a generalized spiked population model” In J. Multivariate Anal. 106, 2012, pp. 167–177 URL: https://doi.org/10.1016/j.jmva.2011.10.009

- [3] Zhidong Bai and Wang Zhou “Large sample covariance matrices without independence structures in columns” In Statist. Sinica 18.2, 2008, pp. 425–442

- [4] Jinho Baik and Jack W. Silverstein “Eigenvalues of large sample covariance matrices of spiked population models” In J. Multivariate Anal. 97.6, 2006, pp. 1382–1408 DOI: 10.1016/j.jmva.2005.08.003

- [5] Jennifer Bryson, Roman Vershynin and Hongkai Zhao “Marchenko-Pastur law with relaxed independence conditions” In Random Matrices: Theory and Applications, 2021 URL: https://doi.org/10.1142/S2010326321500404

- [6] Rick Durrett “Probability” Cambridge University Press, 2019

- [7] Michael Fleermann “Global and Local Semicircle Laws for Random Matrices with Correlated Entries”, 2019

- [8] Michael Fleermann and Johannes Heiny “High-dimensional sample covariance matrices with Curie-Weiss entries” In ALEA, Latin American Journal of Probability and Mathematical Statistics 17, 2020, pp. 857–876

- [9] Michael Fleermann and Werner Kirsch “Proof Methods in Random Matrix Theory”, 2022 URL: https://arxiv.org/abs/2203.02551

- [10] Stuart Geman “A limit theorem for the norm of random matrices” In Ann. Probab. 8.2, 1980, pp. 252–261 URL: http://links.jstor.org/sici?sici=0091-1798(198004)8:2<252:ALTFTN>2.0.CO;2-4&origin=MSN

- [11] Leon Isserlis “On a formula for the product-moment coefficient of each order of a normal frequency distribution in every number of variables” In Biometrika 12, 1918, pp. 134–139

- [12] V. A. Marčenko and L. A. Pastur “Distribution of eigenvalues in certain sets of random matrices” In Mat. Sb. (N.S.) 72 (114), 1967, pp. 507–536

- [13] Alexandru Nica and Roland Speicher “Lectures on the Combinatorics of Free Probability” Cambridge University Press, 2006

- [14] Debashis Paul and Jack W. Silverstein “No eigenvalues outside the support of the limiting empirical spectral distribution of a separable covariance matrix” In J. Multivariate Anal. 100.1, 2009, pp. 37–57 URL: https://doi.org/10.1016/j.jmva.2008.03.010

- [15] Jianfeng Yao, Shurong Zheng and Zhidong Bai “Large sample covariance matrices and high-dimensional data analysis”, Cambridge Series in Statistical and Probabilistic Mathematics Cambridge University Press, New York, 2015, pp. xiv+308 DOI: 10.1017/CBO9781107588080

- [16] Pavel Yaskov “A short proof of the Marchenko–Pastur theorem” In Comptes Rendus Mathematique 354.3 Elsevier, 2016, pp. 319–322

(Michael Fleermann)

FernUniversität in Hagen

Fakultät für Mathematik und Informatik

Universitätsstraße 1

58084 Hagen

E-mail address:

michael.fleermann@fernuni-hagen.de

(Johannes Heiny)

Ruhr-Universität Bochum

Fakultät für Mathematik

Universitätsstraße 150

44801 Bochum

E-mail address:

johannes.heiny@rub.de