Detecting data-driven robust statistical arbitrage strategies with deep neural networks

Abstract.

We present an approach, based on deep neural networks, that allows identifying robust statistical arbitrage strategies in financial markets. Robust statistical arbitrage strategies refer to trading strategies that enable profitable trading under model ambiguity. The presented novel methodology allows to consider a large amount of underlying securities simultaneously and does not depend on the identification of cointegrated pairs of assets, hence it is applicable on high-dimensional financial markets or in markets where classical pairs trading approaches fail. Moreover, we provide a method to build an ambiguity set of admissible probability measures that can be derived from observed market data. Thus, the approach can be considered as being model-free and entirely data-driven. We showcase the applicability of our method by providing empirical investigations with highly profitable trading performances even in dimensions, during financial crises, and when the cointegration relationship between asset pairs stops to persist.

Keywords: Robust Statistical Arbitrage, Model Uncertainty, Deep Learning, Trading Strategies

1. Introduction

In this paper we present an empirically tractable method using neural networks that allows identifying robust statistical arbitrage strategies in financial markets.

The term statistical arbitrage is commonly used in finance to describe trading strategies which are profitable on average, but, in contrast to pure arbitrage strategies (see e.g., [16, 18, 48] for their detection), not necessarily in every market scenario that is deemed to be possible. This generalized notion therefore forms the foundation for a systematic approach enabling to trade profitably even in markets in which it is difficult or impossible to detect pure arbitrage strategies.

A popular class of trading strategies that are often referred to as statistical arbitrage strategies are pairs trading strategies, which all rely on the fundamental idea that, given two financial assets are strongly related, e.g., through a cointegration property (compare e.g. [14]) or through a low level of the variance of the spread between the two assets (compare e.g. [33]), then deviations of the spread are assumed to last only for a short period of time and, thus, eventually the spread of the asset pair will return to its long-term equilibrium. This mean-reversion property is exploited by trading in the opposite direction of the deviation after the deviation has exceeded a certain threshold and by clearing the position when the spread has reached again a level close to its long-term equilibrium, see also [5, 25, 30, 33, 43, 44, 52, 58].

The apparent drawback of applying pairs trading strategies is the strong dependence on the underlying mean-reversion property of the spread process. Indeed, if the mean-reversion relation breaks down and thus the spread does not converge to its equilibrium, then the pairs trading approach will in general not be profitable. Moreover, in an empirical study, [24] provide evidence that the profitability of pairs trading strategies has declined over the recent years, mainly as it has become increasingly difficult to identify profitable asset pairs.

In contrast, our contribution builds on another class of statistical arbitrage strategies that do not rely on a mean-reversion property. We will show that these strategies are profitable even in periods where the pairs trading approach fails. Our approach relies on the idea of Bondarenko ([10]), who introduced and characterized statistical arbitrage strategies as strategies which are profitable on average given any terminal value of the underlying securities at a fixed maturity , i.e., if denotes the profit of a trading strategy investing in underlying securities , then statistical arbitrage strategies fulfil as well as . Based on this idea, [41] generalized the notion of statistical arbitrage from [10] by introducing -arbitrage defined through zero-cost payoffs (which are not necessarily the payoffs of trading strategies) fulfilling

| (1.1) |

for being a -algebra , which allows, in particular, to take into account more flexible choices of trading strategies, possibly adjusted to available information.

Building on the definition of -arbitrage, the results from [10, Proposition 1], [41, Proposition 6], and [53, Theorem 3.3] characterize the existence of -arbitrage strategies by relating the absence of strategies fulfilling (1.1) to the existence of -measurable Radon-Nikodym densities, a result which can be considered as an extension of the fundamental theorem of asset-pricing (compare [2, 11, 13, 21, 37, 56] for several versions of the fundamental theorem of asset-pricing in different underlying settings) which connects the absence of arbitrage with the existence of pricing measures. The authors from [53] further propose and validate empirically an embedding-methodology to exploit statistical arbitrage on financial markets. All these mentioned contributions assume that the underlying securities behave according to a previously fixed underlying probability measure . To account for ambiguity with respect to the choice of an underlying probability measure [47] recently introduced the notion of -robust -arbitrage referring to trading strategies that allow for -arbitrage independent which measure from the considered ambiguity set of measures is the ”correct” underlying probability measure, as the strategy is required to be profitable for all measures from the ambiguity set. Hence, this notion allows, in particular, to take into account probability measures that would incur losses for conventional pairs trading strategies, and thus to determine trading strategies that are profitable even in scenarios where pairs trading fails.

To compute -robust statistical arbitrage strategies, i.e., -robust -arbitrage strategies for the choice , where denotes the terminal values of the underlying securities, a methodology in [47] is provided that relies on a linear programming approach. This routine cannot be applied in high-dimensional settings since it relies on linear programming. To overcome this limitation, we establish a numerical method involving deep neural networks to determine -robust statistical arbitrage strategies. To this end, we introduce a functional which penalizes trading strategies that are not statistical arbitrage strategies for each of the considered measures from the ambiguity set . We show as a main result in Theorem 2.14 that minimizing this functional among trading strategies that can be represented as the outputs of deep neural networks is, for a sufficiently large penalization parameter, equivalent to the determination of -robust statistical arbitrage strategies. In particular, through the representation of trading strategies by neural networks, our approach is applicable even in high dimensions, in contrast to approaches relying on linear programming, and is hence tractable even when the trading strategy depends on a large amount of underlying assets. We provide empirical evidence in Section 4.4 of the applicability of our approach in a high-dimensional setting, where we consider strategies investing in underlying assets from the S&P universe.

As a choice of the ambiguity set , we propose a purely data-driven approach as follows. First, relying on a historical time-series of stock returns, a probability measure is constructed that considers each sequence of observed historical returns as equally likely to occur again in the future. Second, since this measure allows no deviation of future returns from historical returns, we consider a ball around this measure (where the ball is taken with respect to the Wasserstein-distance). Finally, we provide a methodology to explicitly generate measures from this ball.

In contrast to the determination of statistical arbitrage strategies with respect to a fixed underlying probability measure, taking into account the ambiguity set allows, particularly, that the future developments of the underlying process differ to a certain degree (this degree can be specified by the applicant and is expressed in terms of the Wasserstein-distance) from the historical evolution. Indeed, by using this data-driven ambiguity set of measures we provide empirical evidence for the profitability of our approach in overall bad market scenarios (Section 4.3), in high-dimensional financial markets (Section 4.4), and in scenarios where classical pairs trading approaches fail (Section 4.5).

The remainder of this paper is as follows. In Section 2 we introduce the underlying setting and present our main theoretical results. Section 3 presents an approach to first derive an ambiguity set of measures from financial data and then use a numerical method to compute -robust statistical arbitrage strategies when considering the data-implied set as the ambiguity set of physical measures. In Section 4 we then provide empirical evidence for the applicability of our approach by studying several relevant examples involving real-world data. Section 5 concludes and provides an outlook to future research. The proofs of all mathematical statements are provided in Section 6.

2. Setting and main results

We consider a financial market on which we examine the evolution of underlying securities at future times . The future values of all securities are assumed to be bounded from below and from above by some (possibly very large) constants111Compare also Figure 3 where we illustrate that if the width of the interval , , spanned by the bounds of the securities, exceeds a certain threshold, then the performance of our approach does not further improve. Thus, assuming a setting considering large bounds for the underlying securities turns out to be no restriction in practice when applying our approach.. More precisely, for each there exist security-specific bounds satisfying . We then define

which refers to the bounds for the evolution of the underlying assets until time . Then, we model the evolution of the values of the underlying securities until time through the canonical process on and we denote this process by , which is for ; defined by

Moreover, we introduce for the values of the securities at each time the notation and denote for the observed, and therefore deterministic, spot prices at initial time . Then we define the gross profit of a trading strategy , consisting of Borel measurable functions , (where is a constant) via

Additionally, we assume that trading in a strategy induces transaction costs. If a trader adjusts at time his trading position and changes it to a new position , then this adjustment causes transactions costs for some measurable non-negative function . Thus, given some trading strategy , the overall transaction costs until time are measured by

with the convention for all . Therefore, the net overall profit of a trading strategy is given by

Assumption 2.1.

We assume for all , , and that the map

is continuous.

Remark 2.2.

Typical forms of transaction costs which satisfy Assumption 2.1 are given by the following two specifications.

-

(i)

Per share transaction costs, where for some for all .

-

(ii)

Proportional transaction costs, where for some for all .

Compare also [12, Section 2.2] and [15, Section 3.1], where additional examples are discussed.

2.1. -robust -arbitrage strategies

The notion of (statistical) arbitrage depends crucially on the choice of an underlying probability measure. To take into account uncertainty with respect to the choice of the correct underlying model - and the associated probability measure - we consider a set , where denotes the set of Borel probability measures on . The set can thus be considered as an ambiguity set of admissible physical probability measures. Our approach relies on the notion of -robust -arbitrage, which is borrowed from [47] and adjusted to the present multi-asset setting with transaction costs.

Definition 2.3 (-robust -arbitrage).

Let , and let be a sigma-algebra on . Then, a self-financing strategy is called a -robust -arbitrage strategy if the following conditions are fulfilled.

-

(i)

-

(ii)

.

Let , and consider the following set of strategies which are bounded by and which are -Lipschitz.222Let . Then, we say a function is -Lipschitz if for all , with denoting the Euclidean norm on . Note that for any and we denote by the supremum-norm restricted to the set . Moreover, to simplify notations, we write for if the dimension is clear.

| (2.1) | ||||

The constant , which restricts the amount an investor is able to invest, possesses therefore a natural interpretation as a given budget constraint. Moreover, we obtain from the following lemma that is compact.

Lemma 2.4.

Let Assumption 2.1 hold true. Then, for all and all the space is compact in the uniform topology on .

Given some measurable function and some -algebra , we are interested in solving the following conditional super-replication problem

Solutions of are interesting for two reasons. For a financial derivative with payoff function , the value describes the upper bound of prices for which do not allow for -robust -arbitrage, given the market admits no -robust -arbitrage opportunities, see also the discussion in [47, Section 4.2]. On the other hand, if the market admits -robust -arbitrage, the definition of allows to determine -robust -arbitrage strategies. Indeed, when considering , then leads, according to Definition 2.3, directly to a -robust -arbitrage strategy, since implies the existence of some strategy with negative price which has, conditional on , a non-negative payoff.

2.2. An approximation of via penalization

In the following we establish a numerical method to compute as well as associated -robust -arbitrage strategies relying on a penalization approach, similar to the approaches pursued in [8, 17, 19, 27, 28, 29, 39] . To facilitate a numerical implementation, we impose the standing assumption that contains a finite amount of measures.

Assumption 2.5.

The set contains a finite amount of measures.

Let , let be some Borel measurable function, and let be some -algebra on , then to approximate numerically, we introduce for each the following functional

where is some penalization function which penalizes trading strategies for which the conditional super-replication constraint

is violated. To ensure that penalizes as intended, we impose additionally the following assumption on the geometry of .

Assumption 2.6.

Let be a continuous function with the property that , and that .

A natural choice for the function is therefore given by

for some , . As we will show below, the compactness of , stated in Lemma 2.4, induces the existence of some strategy attaining the value of .

Lemma 2.7.

2.3. An approximation of through neural networks

Next, we show how the functional can be approximated with trading strategies whose positions are represented by an appropriate class of neural networks.

To this end, we present a problem-tailored class of fully-connected feed-forward neural networks which we will use to approximate the class of bounded and Lipschitz-continuous trading strategies .

We refer to [9], [23] [35], or [38], which are excellent monographs on neural networks, for a general introduction to networks, as well as to [7], [12], [19], [27], [28], [29], [46], [49], [54] for applications in financial mathematics.

More specifically, for any we consider fully-connected neural networks which have input dimension , output dimension , and number of layers defined as functions of the form

| (2.2) | ||||

where are affine functions of the form

| (2.3) |

where for we have with being a non-constant function which is referred to as activation function. The vector contains the number of neurons of the hidden layers. We call also the hidden dimension of the neural network.

Remark 2.9.

Frequent choices of activation functions that have turned out to perform well in practice include the sigmoid function

and the ReLU function

For an extensive overview on different activation functions we refer the reader to [35].

Assumption 2.10.

We assume that the activation function is either one time continuously differentiable and not polynomial, or that is the ReLU.

For a fixed activation function, we consider the set of all neural networks with input dimension , hidden layers, hidden dimension , and output dimension and we call this set . Next, we introduce an additional degree of freedom by considering all neural networks where the hidden dimension is arbitrary and the number of hidden layers is not specified, i.e.,

We further restrict to those neural networks with outputs that are componentwise bounded by a constant and -Lipschitz, when restricted to , .

| (2.4) | ||||

where denotes the canonical projection onto the -th component, i.e., we have for every function the representation , . One reason for the importance and popularity of deep neural networks is their universal approximation property (compare e.g., for the classical result [40, Theorem 2], [42, Theorem 3.2] for arbitrary input and output dimensions, and [26, Theorem 1] for neural networks which are Lipschitz continuous with respect to some pre-specified constant). We establish the following form of a universal approximation theorem tailored to our setting which is useful to approximate trading positions from .

Lemma 2.11.

Let Assumption 2.10 hold true. Then, for all , for all and for all the set is dense in

| (2.5) |

with respect to the uniform topology on .

We remark that the requirement on the activation function formulated in Lemma 2.11 is in particular fulfilled by those activation functions mentioned in Remark 2.9. The reduction of to those strategies that can be represented by neural networks leads to the set

The associated functional is then defined accordingly by

which relies on the same penalization as expressed through the function . The following result employing Lemma 2.11 establishes that can indeed be approximated arbitrarily well by appropriate neural networks.

2.4. Computation of -robust statistical arbitrage strategies with neural networks

We now focus on the computation of -robust statistical arbitrage strategies. These are -robust -arbitrage strategies with the specific choice . These strategies have a particular importance as they can be interpreted as profitable trading strategies on average given any terminal value, compare also [10], [41], [47], and [53]. As contains an infinite number of sets, it is a priori unclear how to compute numerically a conditional expectation with respect to . However, recall that conditional expectations with respect to any -algebra generated by a finite partition can be computed efficiently.333Recall that if is generated by a finite partition , for some with for all , then for all -integrable random variables .

Thus, with Pseudo-Algorithm 1 we establish a routine enabling the generation of random sets from the -algebra . To this end, we consider for every the finite partition of generated according to (2.7) in Pseudo-Algorithm 1.

| (2.6) |

| (2.7) |

For any realization of the Pseudo-Algorithm 1, we set

| (2.8) |

One possible choice of distribution according to which the random sets from (2.6) are generated is the following: For each and for all , let

| (2.9) |

with being independent of for . Moreover, we denote by the distribution of .

The following proposition then shows that for - almost all realizations of Pseudo-Algorithm 1, conditional expectations with respect to the sigma-algebra can be approximated arbitrarily well by conditional expectations with respect to , defined in (2.8), for large enough . Since each is generated by a finite partition, this allows to compute the corresponding conditional expectation efficiently.

Proposition 2.13.

Let , , let be Borel measurable with , and let . Moreover, consider Pseudo-Algorithm 1, where are distributed for , according to . Then we have

We build on Proposition 2.8, Proposition 2.12, and Proposition 2.13 to establish the following main theorem.

Theorem 2.14.

In particular, in view of Equation (2.10) we have for large enough and that where is an optimization problem involving neural networks which can be solved efficiently. We will apply this approximation on real-world data in the next section.

Remark 2.15.

-

(i)

Proposition 2.13 and Theorem 2.14 rely on the construction from Pseudo-Algorithm 1 that allows to generate random partitions . Note that while (2.6) and (2.9) are numerically tractable, the creation of sets involving complements as in (2.7) grows exponentially with the dimension and is therefore not tractable in higher dimensions. For this reason, we call this methodology a pseudo-algorithm and provide with Algorithm 3 a numerical feasible methodology to generate indicator functions of sets of the corresponding partition avoiding the explicit creation of complements. As it turns out in Algorithm 4, considering indicator functions instead of computing explicit sets is sufficient to compute expressions of the form

Hence, we consider Pseudo-Algorithm 1 as a theoretical routine, while Algorithm 3 and Algorithm 4 can be used in practice to compute -robust statistical arbitrage strategies.

-

(ii)

Proposition 2.13 and Theorem 2.14 remain still valid if we replace by any family , for which each forms a partition of such that for each and . This is satisfied, e.g., by the (deterministic) dyadic partition of . For our numerical experiments we decided however to use the partition from Pseudo-Algorithm 1, mainly because Algorithm 3 admits a computationally efficient algorithm to construct indicators of sets in .

-

(iii)

If the sigma-algebra is countably generated, i.e., , then a similar procedure as in Proposition 2.13 and Theorem 2.14, where the case is considered, can be obtained, by generating for each a finite partition such that for all . However, note that for it is not guaranteed that one can efficiently generate elements as in (2.6) of Pseudo-Algorithm 1. However, if it is possible to do so, one can apply the same Algorithm 3 to efficiently compute indicators of the partition obtained via (2.7).

3. Determination of the ambiguity set and the numerical algorithm

We next use the approximation for large justified by Theorem 2.14 and introduce an approach enabling to detect -robust statistical arbitrage strategies on financial markets. First, in Section 3.1, we propose an approach to determine an entirely data-driven ambiguity set , then, in Section 3.2, we provide a neural network-based numerical algorithm.

3.1. Determination of an ambiguity set of physical measures

We assume that we are able to observe a time series

consisting of observed past prices of each of the underlying securities on which we rely our trading strategy on. The past observation dates are denoted by with , compare also Figure 1.

Based on the time series , our aim is to construct an entirely data-driven ambiguity set such that we are able to detect -robust statistical arbitrage strategies which turn out to be profitable. Recall that we aim to determine a trading strategy which trades at future dates . Assume for sake of simplicity that

and that . Further, assume that at time we observe the spot values

This allows us to determine the empirical measure , relying on the observations from and on the current spot values , through

| (3.1) |

where denotes the Dirac measure with unit mass at , and where the multiplication with as well as division with respect to is meant component-wise. This means, according to (3.1), the measure assigns equal probability to all scaled paths of length that were observed at times to occur in the future, compare also the left and middle panel of Figure 2. Note that the construction in (3.1) ensures particularly that the future paths evolve according to observed paths while the scaling ensures that the spot value of all considered future paths coincides with .

Left: An exemplary observed path is displayed. Centre: In the case the future paths with positive probability under are shown. To each of the paths equal probability is assigned. Right: A possible realization of is depicted, the paths from are deviated according to a normally distributed realization of .

The empirical measure relies entirely on past data and on the spot value , whereas for the future development of the securities we want to take into account uncertainty with respect to the choice of the underlying probability measure, but still consider only such measures which are in a certain sense close to the observed data. To measure the distance between two probability measures , we therefore introduce the -Wasserstein-distance555Alternatively, one could have used, e.g., the Kullback-Leibler divergence ([45]) to measure the distance between two measures. However, the Kullback-Leibler divergence requires absolute continuity of the considered measures, which means in our case that considered measures would have been restricted to the support determined by the observed prices . The -Wasserstein distance does not suffer from this restriction. which is defined as

with denoting the set of all joint distributions of and , compare e.g. [3, 55, 59] for more details on the Wasserstein distance and the related topic of optimal transport. Let , then we consider some ambiguity set such that the therein contained measures lie within the Wasserstein ball around with radius , i.e.,

In that way each can be considered to be close to the empirical measure . Next, we introduce for some the perturbed measure

| (3.2) |

compare also the right panel of Figure 2. The following lemma asserts that choosing appropriately ensures that the measure is indeed contained in .

Lemma 3.1.

Then, based on Lemma 3.1, we are able to determine a set which contains a finite number of . We summarize this procedure in Algorithm 2.

Remark 3.2.

Given a time series with for all and spot prices , we can construct the following way. Consider for

| (3.4) |

Based on the above bounds and , we define, for some , the underlying space by setting

| (3.5) |

Then, we see that and for each and satisfying (3.3) we have .

| (3.6) | ||||

| (3.7) |

3.2. The numerical algorithm to compute statistical arbitrage strategies

We rely on Theorem 2.14, which ensures that for sufficiently large values , i.e., we choose as discussed below Lemma 2.4. We remark that Pseudo-Algorithm 1 allows to generate finite partitions of contained in the -algebra . Based on this methodology, we propose a method specified in Algorithm 3 that allows to compute efficiently indicator functions of the form for , . Note that this method provides an extremely efficient method that reduces the exponential complexity of the brute force approach to indicator computation to a linear time complexity. Moreover, according to the considerations from Section 3.1, we propose the following Algorithm 4 to detect -robust statistical arbitrage strategies, where is an ambiguity set defined as in (3.7); see also Algorithm 2.

| (3.8) | ||||

4. Real-world examples

In this section we show that the presented approach can be applied successfully to real-world-data. In particular, the experiments provide empirical evidence for the applicability of the determined set of physical measures in Section 3.1 even in a multi-asset environment. Moreover, we highlight the extraordinary performance of our robust trading approach in crisis-periods.

4.1. Implementation

To apply Algorithm 4, we use the framework provided by PyTorch ([50]) and train neural networks with a Batch-normalization layer for the input and fully-connected layers with neurons in the first layer, neurons in the second layer, and neurons in the third layer, where is the number of considered assets (the coefficient varies across the provided examples). We consider future times999We chose since this number provides a numerically tractable quantity of trading days that can be taken into account while still allowing to consider a large number of stocks. This leads to a trading period of days (recall that there is no trading on the last day of the period) and indeed, empirical findings indicate that most of the autocorrelation of daily stock returns is contained in the most recent stock returns (compare [22, Table 3.1]). and hence the network architecture consists of independent fully-connected subnetworks for , whereas are constants which are trained, too. Each neural network , takes the past realizations of the assets of the trading days after as inputs and outputs the trading positions of all assets at day . The activation functions of all hidden layers are ReLU functions. To only consider neural networks from the set for and, in particular, to bound the output of the neural network by the constant , we use in the notation of (2.2) for a -activation function (which is bounded by the absolute value 1) and matrices with biases which are randomly initialized for (using standard initialization in PyTorch), whereas and . A predetermined Lipschitz constant could be enforced through per-layer Batch-normalization ([36]), weight restrictions ([4]), or through regularization ([51]), however we decided to not use any of these methods specifically for this purpose and to allow, a priori, to be arbitrarily large. However, note that a posteriori , since the parameters of the neural networks in practice remain bounded over the training period (see e.g., [7, Fig. 4]). Moreover, a large Lipschitz constant is preferred to not exclude (too many) tradings trategies, and in order to keep our approach as simple as possible it is sufficient to know about the existence of some constant which can be arbitrarily large but finite.

We apply Algorithm 4 with training iterations and choose a penalization parameter101010Note that a small penalization parameter such as turns out to be sufficient in practice. In contrast, choosing too large may result in numerical instabilities as observed in [39, Section 4.1] regarding a similar penalization approach. Compare also the relatively small penalization parameters chosen in [28, Section 4]. of , a radius of the Wasserstein Ball around the empirical measure, , per share transaction costs111111These numbers represent conservative upper estimates of transaction costs that apply in practice. Typically, transaction costs are even smaller. Compare, e.g., [1] where the fees for trading in different markets are indicated. These fees do not exceed of the trade value in all listed cases. with , proportional transaction costs with , a penalization function for all the examples below, and we report a value of leading to sets that are considered when applying Algorithm 3 in all of the following examples. Moreover, we use the bounds as elaborated in Remark 3.2, where we set . Further, we adopt a learning rate of for low dimensional cases (1 or 2 assets) and a learning rate of for high dimensional cases (10 assets and more), as empirical tests have shown that choosing different learning rates for low and high dimensional cases, respectively, significantly improves the training speed. In the sequel (Table 15, 2, 3, 4, 5, 6, 7), we report the numerical results by taking the average of independent experiments to balance off the effect of random weight initialization. In each of these experiments we partition the testing period into consecutive sub-periods of length to which we apply our trained strategy.

For the reader’s convenience the applied Python-codes are provided and can be found under https://github.com/YINDAIYING/Deep-Robust-Statistical-Arbitrage.

Remark 4.1.

As neural networks turn out to be extremely sensitive with respect to the scale of the input (compare e.g. [6, 57]), we decided in the implementation to normalize the inputs by scaling the stock prices of each asset separately such that the spot values of each asset equals to , i.e. and therefore to consider a Wasserstein-ball around that takes these normalized spot values into account.

4.2. Comparison with the linear programming approach from [47]

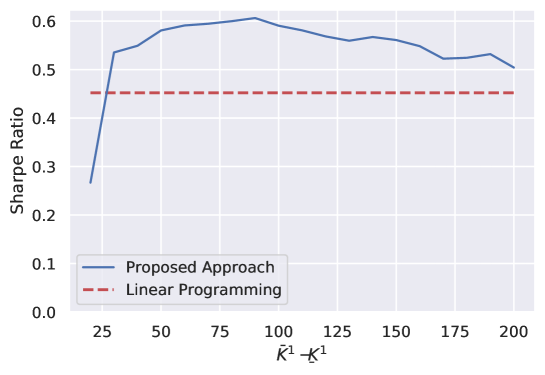

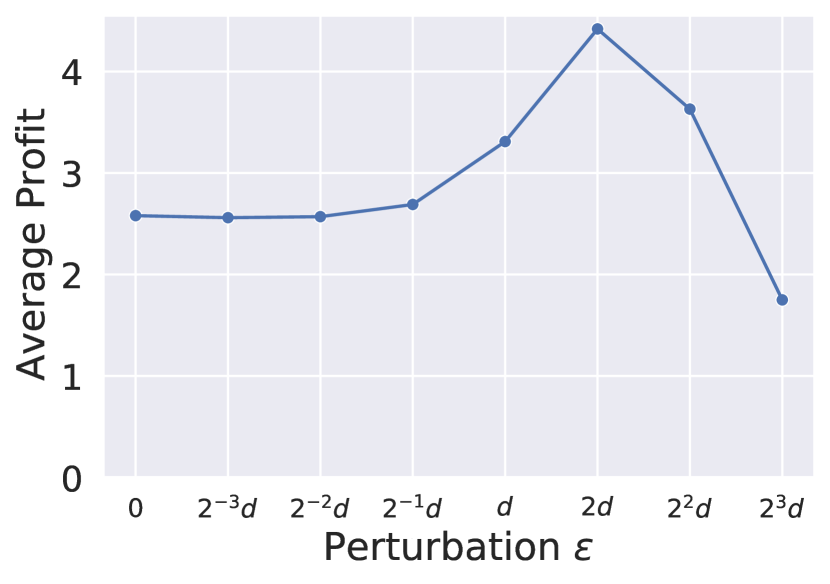

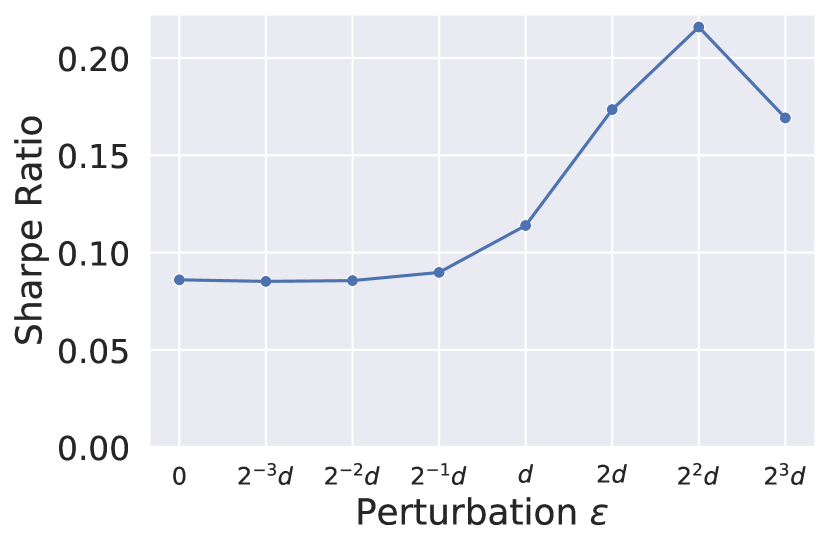

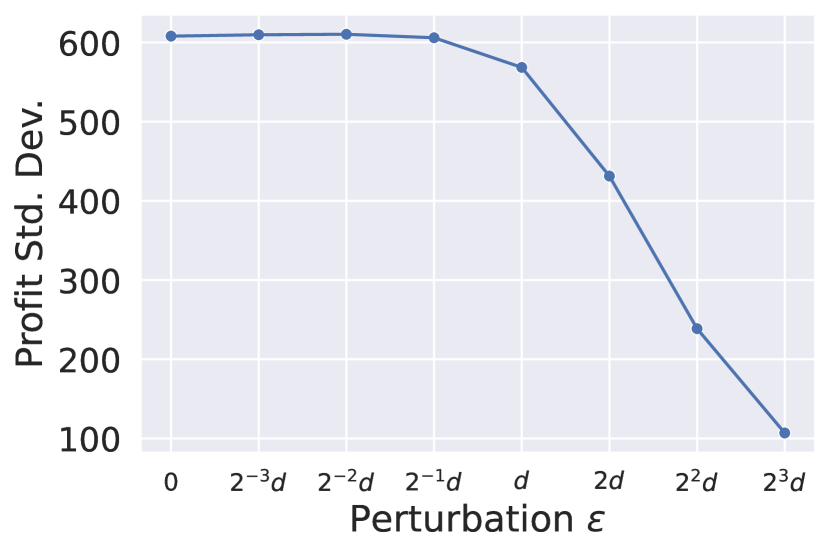

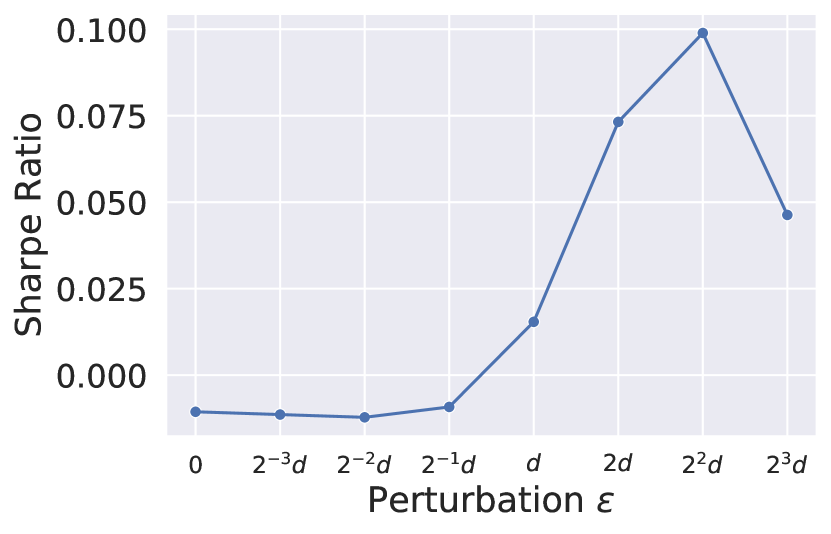

In this example, we compare our approach, relying on Algorithm 4, with the linear programming (LP) approach proposed in [47, Section 5.2]. Note that the LP-approach in [47] is computationally tractable only in low dimensions, typically . To this end, we borrow the setting from [47, Section 5.2] and also consider the price evolution of the EUROSTOXX 50 in a training period from January until August , and in a testing period ranging from September until July , while assuming that , , i.e., we face a trading period of approximately one month with one intermediate trade. We train strategies according to Algorithm 4 while using different bounds and and then test the performance of the trained strategies for various values of and . The performance measure is defined by the Sharpe ratio of the strategies applied to the testing period in dependence of , averaged over all independent experiments. In Figure 3, the Sharpe ratio of the calculated strategy is plotted against the difference between the upper bound and the lower bound centered at the price of . One can observe that the Sharpe ratio of the proposed approach is slightly higher than the Sharpe ratio of the LP-approach from [47] once the bounds width exceeds a certain value (around in this example), reaches its highest value when the width equals a value of about , and declines slightly when increasing the width of the bounds further.

As the best trading performance, i.e., the highest Sharpe ratio, can be observed when the asset values are assumed to be restricted by relatively small bounds, this provides strong evidence that the underlying setting, which assumes (large) bounds for stock prices, imposes no constraint for the detection of optimal trading strategies.

In this example, the bounds (3.4) mentioned in Remark 3.2 take the values and , respectively. We set and hence have . Figure 3 supports that the choice of these bounds is reasonable, since increasing the interval width further does not significantly improve the performance of our trading approach.

Note that Figure 3 also illustrates that both LP-approach and the neural network approach from Algorithm 4 perform remarkably well in the considered setting, while the neural network approach even marginally outperforms the LP-approach from [47] which we here used as benchmark to compare. The drawback of the LP-approach however is that it is no more applicable in higher dimensions. We provide with the examples from Section 4.4 empirical evidence that our approach (Algorithm 4) can still be applied successfully in higher dimensions in contrast to the LP-approach.

4.3. Outperformance of the market

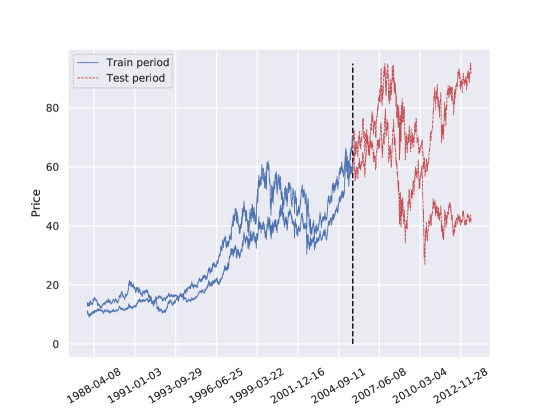

We consider underlying securities. These are the American stock market index and the European market index EUROSTOXX , respectively. To estimate the ambiguity set according to the methodology proposed in Section 3.1 we consider historic daily data of both underlying indices from to . This results in observation dates. We set the number of future trading days to and consider daily trading. We train a trading strategy according to Algorithm 4 and test it on the period from to , in which the considered indices perform remarkably bad121212We refer to [31, 34, 43] for detailed discussions of different trading periods over the last years., compare Figure 4 which depicts both the evolution in the train period and the test period. In practice, to account for recent changes in the underlying time series, it might be important to train the model with streamed data, that is, to fine-tune the model with the most recent incoming data, which is known as online-learning in the literature, see also [20]. We adjust our framework to online-learning by performing another iterations of fine-tuning with the augmented data during the test period every time the trading window is shifted forward. Given that there are non-overlapping trading windows in the test period, the total number of iterations in the setting will be , compared to merely iterations without incorporating online-learning. Due to the increased computational costs, we only demonstrate online-learning in this and EUROSTOXX scenario, see also Table 15.

The results in Table 15 showcase that our trained strategy clearly outperforms the market and therefore provide empirical evidence that the robust strategies determined by our approach are able to cut losses even in extremely difficult market scenarios.

| Transaction Costs | 0 | B&H | Prop. | Prop. | P.S. | P.S. O.L. | P.S. |

|---|---|---|---|---|---|---|---|

| Overall Profit | 9881.76 | -9932.61 | 9185.23 | -11203.11 | 10473.57 | 12555.82 | -9992.61 |

| Average Profit131313Here, and in all other tables Average Profit refers to overall profit divided by the number of periods with trading days on the testing data. | 65.88 | -66.22 | 61.24 | -74.69 | 69.82 | 83.7 | -66.62 |

| Profit Std. Dev. | 331.04 | 1588.11 | 329.81 | 1588.22 | 338.82 | 416.32 | 1588.11 |

| % of Profitable Trades | 57.09 | 53.33 | 55.68 | 52.67 | 57.75 | 59.2 | 53.33 |

| Max. Profit | 2858.41 | 3375.2 | 2841.78 | 3367.87 | 2999.97 | 3010.74 | 3374.8 |

| Min. Profit | -835.69 | -5430.9 | -843.13 | -5438.59 | -823.28 | -1363.3 | -5431.3 |

| Sharpe Ratio | 1.0604 | -0.221 | 0.9882 | -0.249 | 1.1115 | 1.0931 | -0.2220 |

| Sortino Ratio | 2.7023 | -0.285 | 2.5075 | -0.321 | 2.9117 | 2.0721 | -0.2860 |

4.4. Trading in a large number of stocks

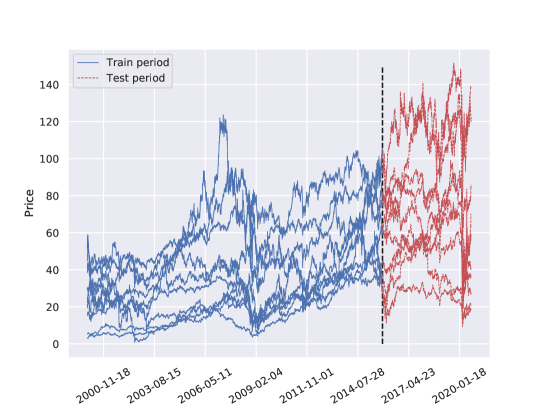

In this example we consider , and securities, respectively, which correspond to some of the largest constituents of the 161616In the case we consider the companies with ticker symbols: OKE, PG, RCL, SBUX, UNM, USB, VMC, WELL, WMB, XOM. The considered companies in higher dimensions can be found in the provided github-repository under https://github.com/YINDAIYING/Deep-Robust-Statistical-Arbitrage.. The training period ranges from to and the testing period from to , compare Figure 6, where we illustrate securities. In Table 2, Table 3, Table 4, Table 5, and Table 6, we depict the results of the trained strategy evaluated on the testing period.

| Transaction Costs | 0 | B&H | Prop. | Prop. | P.S. | P.S. |

|---|---|---|---|---|---|---|

| Overall Profit | 147.01 | -281.30 | 138.21 | -446.66 | 116.41 | -521.30 |

| Average Profit | 1.23 | -2.34 | 1.15 | -3.72 | 0.97 | -4.34 |

| Profit Std. Dev. | 39.09 | 292.96 | 41.4 | 292.95 | 41.31 | 292.96 |

| % of Profitable Trades | 58.17 | 60.0 | 57.82 | 60.0 | 57.17 | 60.0 |

| Max. Profit | 222.59 | 1006.6 | 238.49 | 1005.4 | 237.51 | 1004.6 |

| Min. Profit | -287.12 | -2027.2 | -316.25 | -2028.35 | -316.24 | -2029.2 |

| Sharpe Ratio | 0.1513 | -0.042 | 0.1311 | -0.067 | 0.1030 | -0.078 |

| Sortino Ratio | 0.1978 | -0.036 | 0.1761 | -0.058 | 0.1454 | -0.067 |

| Transaction Costs | 0 | B&H | Prop. | Prop. | P.S. | P.S. |

|---|---|---|---|---|---|---|

| Overall Profit | 415.37 | -381.65 | 423.05 | -811.11 | 397.55 | -861.65 |

| Average Profit | 3.46 | -3.18 | 3.53 | -6.76 | 3.31 | -7.18 |

| Profit Std. Dev. | 137.6 | 662.9 | 154.21 | 662.9 | 154.13 | 662.9 |

| % of Profitable Trades | 63.27 | 61.67 | 64.72 | 61.67 | 64.50 | 61.67 |

| Max. Profit | 592.85 | 2313.9 | 659.84 | 2310.7 | 657.89 | 2309.9 |

| Min. Profit | -1122.15 | -3968.0 | -1271.88 | -3971.03 | -1272.54 | -3972.0 |

| Sharpe Ratio | 0.1129 | -0.025 | 0.1211 | -0.054 | 0.1139 | -0.057 |

| Sortino Ratio | 0.1166 | -0.024 | 0.0959 | -0.051 | 0.0903 | -0.054 |

| Transaction Costs | 0 | B&H | Prop. | Prop. | P.S. | P.S. |

|---|---|---|---|---|---|---|

| Overall Profit | 968.91 | -239.36 | 946.17 | -817.62 | 873.44 | -959.36 |

| Average Profit | 8.07 | -1.99 | 7.88 | -6.81 | 7.28 | -7.99 |

| Profit Std. Dev. | 217.52 | 858.26 | 282.87 | 858.26 | 282.75 | 858.26 |

| % of Profitable Trades | 63.08 | 60.83 | 64.52 | 60.0 | 64.23 | 60.0 |

| Max. Profit | 947.24 | 3049.4 | 1142.82 | 3045.0 | 1138.95 | 3043.4 |

| Min. Profit | -1716.77 | -5102.98 | -2296.56 | -5107.17 | -2298.22 | -5108.98 |

| Sharpe Ratio | 0.1805 | -0.012 | 0.148 | -0.042 | 0.1367 | -0.049 |

| Sortino Ratio | 0.2012 | -0.012 | 0.1174 | -0.04 | 0.1087 | -0.046 |

| Transaction Costs | 0 | B&H | Prop. | Prop. | P.S. | P.S. |

|---|---|---|---|---|---|---|

| Overall Profit | 1566.16 | -481.26 | 1216.11 | -1211.09 | 1074.3 | -1441.26 |

| Average Profit | 13.05 | -4.01 | 10.13 | -10.09 | 8.95 | -12.01 |

| Profit Std. Dev. | 381.43 | 1042.09 | 413.06 | 1042.08 | 412.91 | 1042.09 |

| % of Profitable Trades | 66.08 | 63.33 | 65.68 | 62.5 | 65.4 | 62.5 |

| Max. Profit | 1459.80 | 3655.6 | 1518.15 | 3650.08 | 1513.39 | 3647.6 |

| Min. Profit | -3036.73 | -6138.28 | -3336.13 | -6143.52 | -3339.02 | -6146.28 |

| Sharpe Ratio | 0.1837 | -0.02 | 0.1304 | -0.051 | 0.1154 | -0.061 |

| Sortino Ratio | 0.1448 | -0.019 | 0.1007 | -0.047 | 0.0894 | -0.056 |

| Transaction Costs | 0 | B&H | Prop. | Prop. | P.S. | P.S. |

|---|---|---|---|---|---|---|

| Overall Profit | 1039.23 | -595.20 | 445.82 | -1460.74 | 193.16 | -1795.20 |

| Average Profit | 8.66 | -4.96 | 3.72 | -12.17 | 1.61 | -14.96 |

| Profit Std. Dev. | 497.81 | 1214.28 | 568.63 | 1214.28 | 568.52 | 1214.28 |

| % of Profitable Trades | 64.6 | 62.5 | 64.18 | 62.5 | 63.6 | 62.5 |

| Max. Profit | 1743.07 | 3994.96 | 1866.62 | 3988.3 | 1859.4 | 3984.96 |

| Min. Profit | -3996.79 | -7134.54 | -4646.44 | -7140.77 | -4651.58 | -7144.54 |

| Sharpe Ratio | 0.092 | -0.022 | 0.0351 | -0.053 | 0.0154 | -0.065 |

| Sortino Ratio | 0.0738 | -0.02 | 0.0272 | -0.048 | 0.0122 | -0.06 |

In particular, our results show that the approach can indeed be applied to high-dimensional data in contrast to conventional approaches such as linear programming. Moreover, our approach clearly beats the market in all considered cases.

4.5. Outperformance of pairs trading strategies

In a third example we show that with our approach using Algorithm 4 it is possible to trade profitably in a market environment where classical pairs trading approaches fail. To this end, we consider securities which show a high degree of mutual dependence. More specifically, we study the stocks of ExxonMobil (Ticker symbol: XOM) and of BP p.l.c (Ticker symbol: BP). The training period ranges from to and indeed, an augmented Dickey-Fuller test (compare e.g. [32]) indicates with a -value of that the spread XOM-BP is stationary and thus XOM and BP are indeed cointegrated. However, as depicted in Figure 8, in the testing period that ranges from to , the cointegration relationship breaks down, i.e., the spread diverges, and thus conventional pairs trading approaches fail. However, as the results in Table 7 indicate, a trading strategy that was trained according to Algorithm 4 performs even in this environment remarkably well. This provides further evidence for the robustness of our presented approach.

| Transaction Costs | 0 | B&H | Prop. | Prop. | P.S. | P.S. |

|---|---|---|---|---|---|---|

| Overall Profit | 106.89 | -149.40 | 90.17 | -201.46 | 85.14 | -229.40 |

| Average Profit | 0.54 | -0.75 | 0.45 | -1.01 | 0.43 | -1.15 |

| Profit Std. Dev. | 5.05 | 54.3 | 5.01 | 54.3 | 4.87 | 54.3 |

| % of Profitable Trades | 56.6 | 53.5 | 54.95 | 53.0 | 55.45 | 53.0 |

| Max. Profit | 44.23 | 121.0 | 43.08 | 120.67 | 42.36 | 120.6 |

| Min. Profit | -17.3 | -221.7 | -17.5 | -221.94 | -17.7 | -222.1 |

| Sharpe Ratio | 0.5421 | -0.073 | 0.4538 | -0.098 | 0.4396 | -0.112 |

| Sortino Ratio | 1.1163 | -0.095 | 0.9506 | -0.128 | 0.9317 | -0.146 |

5. Conclusion and Future Research

In this paper we have presented a deep-learning based approach to the computation of profitable trading strategies. In the main result in Theorem 2.14 we prove, in particular, the convergence of a penalized functional involving strategies that can be represented by neural networks towards the minimal conditional super-replication price of profitable trading strategies. This allows theoretically to determine profitable trading strategies by optimizing neural networks. To ensure also the practical applicability of our approach, we have introduced an algorithm in Section 3 for the determination of a data-driven ambiguity set of underlying probability measures as well as an algorithm for the computation of -robust statistical arbitrage strategies. In Section 4 we then have shown in several empirical examples that our approach indeed leads to profitable trading outcomes, even in scenarios where it is naturally difficult for trading strategies to perform well.

Analogue to the setting from [47], the presented approach can be extended in a natural way by trading in liquid options and by considering more general -algebras , leading to the notion of -robust -arbitrage strategies instead of -robust statistical arbitrage strategies. In this case, the -algebra may require a different approximation as the case , which was considered in Proposition 2.13. Moreover, the determination of the ambiguity set in Section 3.1, even though entirely data-driven and straightforward, could also be replaced by approaches that include, for example, a more subtle weighting of past returns or even by a Bayesian approach in which one updates sequentially an assumed prior distribution contingent on observed returns. Eventually we remark that all of our results, and in particular Theorem 2.14, not only enable the approximation of -robust -arbitrage strategies, but also allow to detect strategies that conditionally super-replicate some payoff and thus allow to involve mispriced derivatives (with payoff ) into trading. We leave these extensions and its effects on the outcomes of the resultant trading strategies for future research.

6. Proofs

Proof of Lemma 2.4.

Let , and pick a sequence . Note that, by definition of , for all , it holds as well as for all . Thus, according to the Bolzano–Weierstrass theorem, there exists a convergent subsequence of as well as for for each . Moreover, for all , and for all , we have and that is -Lipschitz. Hence, by the Arzelà–-Ascoli theorem, for all , there exists a subsequence of converging uniformly on . Inductively we obtain therefore a subsequence such that converges against some , such that for each the subsequence converges to some , and such that converges uniformly for each , against some -Lipschitz function . Due to the assumed continuity of the transaction costs , for all , this implies the uniform convergence

Moreover, it holds , since

∎

Proof of Lemma 2.7.

Let be some -algebra. We define the map

The map is continuous with respect to the uniform topology induced by due to the dominated convergence theorem and by the assumed continuity of . Let be a sequence with . Then, by the compactness of , as stated in Lemma 2.4, there exists a subsequence and some such that

where the last equality is a consequence of the continuity of . ∎

Proof of Proposition 2.8.

Let be some -algebra. First, we note that the condition ensures the existence of some strategy such that

Thus, due to Assumption 2.6, we have for all

By the assumption that and by the above inequality we obtain for each

This means in particular that exists and

| (6.1) |

Moreover, by Lemma 2.7, for each there exists which minimizes , i.e., we have that

| (6.2) |

According to Lemma 2.4, is compact, thus there exists a uniformly convergent subsequence with limit . Hence, by (6.2) we have

| (6.3) |

Since is continuous and nonnegative the dominated convergence theorem and the boundedness of the expression in (6.3) imply that

| (6.4) |

By Assumption 2.6, this in turn can only hold if

| (6.5) |

By the validity of (6.5), we see that

| (6.6) |

Further, since , we have with (6.2) that for all

| (6.7) |

We consider in (6.7) the limit and obtain with (6.4) that

| (6.8) |

Thus, combining (6.1), (6.8), and (6.6) yields the following inequalities

which implies that . ∎

Proof of Lemma 2.11.

Let , , , , and let be some function such that is -Lipschitz with for all . We define for all the truncated function by

which is -Lipschitz, since for all we have by construction

Then, according to a version of the universal approximation theorem for Lipschitz functions in the form of [26, Theorem 1], there exists for all some neural network , , which is -Lipschitz continuous, and which fulfils

| (6.9) |

Thus, by (6.9), and since by construction , we have for all that

Moreover, we observe for all that

Then by defining we obtain

Finally, note that , as the set also contains neural networks which are not fully connected, which can be seen by setting the weights of connections from a neural network in , which do not appear in partially connected networks, to be . ∎

Proof of Proposition 2.12.

Let be some -algebra, and let . First note that as we have . Hence it remains to prove that . To that end, according to Lemma 2.7 there exists some such that

By Lemma 2.11 there exists a sequence such that for all we have for all and such that

This implies particularly for all , that uniformly on for . By the dominated convergence theorem, with the continuity of and the continuity of the transaction costs for all , we have that

Thus, as for all , we obtain

∎

Proof of Proposition 2.13.

We first show that the following equality holds -almost surely:171717More precisely, we show that the following holds for -almost all realizations of following (2.7) and (2.9).

| (6.10) |

Note that for all it holds

| (6.11) |

Hence, it follows by (6.11) that and in particular

This proves one inclusion of (6.10). Next, for the other inclusion, pick for some arbitrary numbers . Then we aim to show that -almost surely

| (6.12) |

Let , for , be the random variables which are -distributed, i.e,

where is independent of for . Choose so large such that for all and for all . Then, we define events

It follows now from under that the following equality holds for all

for each . Thus, by using the independence of , we have for all

This implies that . By the Borel–Cantelli lemma and by the fact that the events are independent, we have . Thus, -almost surely we have

| (6.13) |

for infinitely many . Therefore, -a.s., there exists a subsequence which fulfils (6.13) for every . Hence, -a.s., according to the Bolzano–Weierstrass theorem, there exists a subsequence which converges, and due to (6.13) we have for for all . We hence get

Next, note that is generated by

Therefore, by using (6.12) we obtain -a.s. that

Thus, the claim (6.10) is proved.

Next, we show (ii). To this end, let be Borel measurable with , let , and . Since and are both bounded, it holds . Moreover, by definition, is an increasing sequence of -algebras. Given , it follows from Lévy’s zero-one law that,

where, by Lévy’s zero-one law, the convergence holds both -almost surely and in .

∎

Proof of Theorem 2.14.

Let , . Moreover, let , which holds true -a.s. according to Proposition 2.13. By Lemma 2.7, for all and all there exists some strategy such that

and some s.t.

According to Lemma 2.4, is compact, thus there exists a subsequence of (labelled identically) such that converges uniformly for against some . Then, it follows with the dominated convergence theorem, the continuity of the transaction costs, the continuity of , and with Proposition 2.13 that

| (6.14) |

By the tower property of the conditional expectation and by Jensen’s inequality, as is convex, it holds for every , by using , that

| (6.15) |

Thus, we obtain by (6.14) that

This means we have shown that for each

Therefore we conclude with Proposition 2.12, and Proposition 2.8 that

∎

Proof of Lemma 3.1.

We set for and define

Then it holds by construction that

This shows . ∎

Acknowledgments

Financial support by the MOE AcRF Tier 1 Grant RG74/21 and by the Nanyang Assistant Professorship Grant (NAP Grant) Machine Learning based Algorithms in Finance and Insurance is gratefully acknowledged.

References

- [1] InteractiveBrokers. https://www.interactivebrokers.com/en/index.php?f=1590&p=stocks2, 2022 (accessed February 7, 2022).

- [2] Beatrice Acciaio, Mathias Beiglböck, Friedrich Penkner, and Walter Schachermayer. A model-free version of the fundamental theorem of asset pricing and the super-replication theorem. Mathematical Finance, 26(2):233–251, 2016.

- [3] Luigi Ambrosio. Lecture notes on optimal transport problems. In Mathematical aspects of evolving interfaces (Funchal, 2000), volume 1812 of Lecture Notes in Math., pages 1–52. Springer, Berlin, 2003.

- [4] Cem Anil, James Lucas, and Roger Grosse. Sorting out Lipschitz function approximation. In International Conference on Machine Learning, pages 291–301. PMLR, 2019.

- [5] Marco Avellaneda and Jeong-Hyun Lee. Statistical arbitrage in the US equities market. Quant. Finance, 10(7):761–782, 2010.

- [6] Jimmy Lei Ba, Jamie Ryan Kiros, and Geoffrey E Hinton. Layer normalization. arXiv:1607.06450, 2016.

- [7] Michel Baes, Calypso Herrera, Ariel Neufeld, and Pierre Ruyssen. Low-rank plus sparse decomposition of covariance matrices using neural network parametrization. IEEE Transactions on Neural Networks and Learning Systems, 34(1):171–185, 2023.

- [8] Jean-David Benamou, Guillaume Carlier, Marco Cuturi, Luca Nenna, and Gabriel Peyré. Iterative Bregman projections for regularized transportation problems. SIAM J. Sci. Comput., 37(2):A1111–A1138, 2015.

- [9] Yoshua Bengio. Learning deep architectures for AI. Now Publishers Inc, 2009.

- [10] Oleg Bondarenko. Statistical arbitrage and securities prices. The Review of Financial Studies, 16(3):875–919, 2003.

- [11] Bruno Bouchard and Marcel Nutz. Arbitrage and duality in nondominated discrete-time models. The Annals of Applied Probability, 25(2):823–859, 2015.

- [12] H. Buehler, L. Gonon, J. Teichmann, and B. Wood. Deep hedging. Quant. Finance, 19(8):1271–1291, 2019.

- [13] Matteo Burzoni, Frank Riedel, and H. Mete Soner. Viability and arbitrage under Knightian uncertainty. Econometrica, 89(3):1207–1234, 2021.

- [14] João Caldeira and Guilherme V Moura. Selection of a portfolio of pairs based on cointegration: A statistical arbitrage strategy. Available at SSRN 2196391, 2013.

- [15] Patrick Cheridito, Michael Kupper, and Ludovic Tangpi. Duality formulas for robust pricing and hedging in discrete time. SIAM J. Financial Math., 8(1):738–765, 2017.

- [16] Samuel N. Cohen, Christoph Reisinger, and Sheng Wang. Detecting and repairing arbitrage in traded option prices. Appl. Math. Finance, 27(5):345–373, 2020.

- [17] R. Cominetti and J. San Martín. Asymptotic analysis of the exponential penalty trajectory in linear programming. Math. Programming, 67(2, Ser. A):169–187, 1994.

- [18] Zhenyu Cui, Wenhan Qian, Stephen Taylor, and Lingjiong Zhu. Detecting and identifying arbitrage in the spot foreign exchange market. Quant. Finance, 20(1):119–132, 2020.

- [19] Luca De Gennaro Aquino and Carole Bernard. Bounds on multi-asset derivatives via neural networks. Int. J. Theor. Appl. Finance, 23(8):2050050, 31, 2020.

- [20] Marcos Lopez De Prado. Advances in financial machine learning. John Wiley & Sons, 2018.

- [21] Freddy Delbaen and Walter Schachermayer. A general version of the fundamental theorem of asset pricing. Math. Ann., 300(3):463–520, 1994.

- [22] Zhuanxin Ding, Clive WJ Granger, and Robert F Engle. A long memory property of stock market returns and a new model. Journal of empirical finance, 1(1):83–106, 1993.

- [23] Matthew F Dixon, Igor Halperin, and Paul Bilokon. Machine Learning in Finance. Springer, 2020.

- [24] Binh Do and Robert Faff. Does simple pairs trading still work? Financial Analysts Journal, 66(4):83–95, 2010.

- [25] Binh Do, Robert Faff, and Kais Hamza. A new approach to modeling and estimation for pairs trading. In Proceedings of 2006 financial management association European conference, volume 1, pages 87–99. Citeseer, 2006.

- [26] Stephan Eckstein. Lipschitz neural networks are dense in the set of all Lipschitz functions. arXiv:2009.13881, 2020.

- [27] Stephan Eckstein, Gaoyue Guo, Tongseok Lim, and Jan Obłój. Robust pricing and hedging of options on multiple assets and its numerics. SIAM J. Financial Math., 12(1):158–188, 2021.

- [28] Stephan Eckstein and Michael Kupper. Computation of optimal transport and related hedging problems via penalization and neural networks. Appl. Math. Optim., 83(2):639–667, 2021.

- [29] Stephan Eckstein, Michael Kupper, and Mathias Pohl. Robust risk aggregation with neural networks. Math. Finance, 30(4):1229–1272, 2020.

- [30] Robert J. Elliott, John van der Hoek, and William P. Malcolm. Pairs trading. Quant. Finance, 5(3):271–276, 2005.

- [31] Thomas Fischer and Christopher Krauss. Deep learning with long short-term memory networks for financial market predictions. European Journal of Operational Research, 270(2):654–669, 2018.

- [32] Wayne A Fuller. Introduction to statistical time series, volume 428. John Wiley & Sons, 2009.

- [33] Evan Gatev, William N Goetzmann, and K Geert Rouwenhorst. Pairs trading: Performance of a relative-value arbitrage rule. The Review of Financial Studies, 19(3):797–827, 2006.

- [34] Pushpendu Ghosh, Ariel Neufeld, and Jajati Keshari Sahoo. Forecasting directional movements of stock prices for intraday trading using LSTM and random forests. Finance Research Letters, page 102280, 2021.

- [35] Ian Goodfellow, Yoshua Bengio, Aaron Courville, and Yoshua Bengio. Deep learning, volume 1. MIT press Cambridge, 2016.

- [36] Henry Gouk, Eibe Frank, Bernhard Pfahringer, and Michael J Cree. Regularisation of neural networks by enforcing lipschitz continuity. Machine Learning, 110(2):393–416, 2021.

- [37] J. Michael Harrison and Stanley R. Pliska. Martingales and stochastic integrals in the theory of continuous trading. Stochastic Process. Appl., 11(3):215–260, 1981.

- [38] Mohamad H Hassoun. Fundamentals of artificial neural networks. MIT press, 1995.

- [39] Pierre Henry-Labordere. (martingale) optimal transport and anomaly detection with neural networks: A primal-dual algorithm. Available at SSRN 3370910, 2019.

- [40] Kurt Hornik. Approximation capabilities of multilayer feedforward networks. Neural networks, 4(2):251–257, 1991.

- [41] Stefan Kassberger and Thomas Liebmann. Additive portfolio improvement and utility-efficient payoffs. Math. Financ. Econ., 11(2):241–262, 2017.

- [42] Patrick Kidger and Terry Lyons. Universal approximation with deep narrow networks. In Conference on Learning Theory, pages 2306–2327. PMLR, 2020.

- [43] Christopher Krauss. Statistical arbitrage pairs trading strategies: Review and outlook. Journal of Economic Surveys, 31(2):513–545, 2017.

- [44] Christopher Krauss, Xuan Anh Do, and Nicolas Huck. Deep neural networks, gradient-boosted trees, random forests: Statistical arbitrage on the S&P 500. European Journal of Operational Research, 259(2):689–702, 2017.

- [45] S. Kullback and R. A. Leibler. On information and sufficiency. Ann. Math. Statistics, 22:79–86, 1951.

- [46] Eva Lütkebohmert, Thorsten Schmidt, and Julian Sester. Robust deep hedging. Quant. Finance, 22(8):1465–1480, 2022.

- [47] Eva Lütkebohmert and Julian Sester. Robust statistical arbitrage strategies. Quant. Finance, 21(3):379–402, 2021.

- [48] Ariel Neufeld, Antonis Papapantoleon, and Qikun Xiang. Model-free bounds for multi-asset options using option-implied information and their exact computation. Management Science, 2022.

- [49] Ariel Neufeld and Julian Sester. A deep learning approach to data-driven model-free pricing and to martingale optimal transport. IEEE Transactions on Information Theory, 2022.

- [50] Adam Paszke, Sam Gross, Francisco Massa, Adam Lerer, James Bradbury, Gregory Chanan, Trevor Killeen, Zeming Lin, Natalia Gimelshein, Luca Antiga, Alban Desmaison, Andreas Kopf, Edward Yang, Zachary DeVito, Martin Raison, Alykhan Tejani, Sasank Chilamkurthy, Benoit Steiner, Lu Fang, Junjie Bai, and Soumith Chintala. Pytorch: An imperative style, high-performance deep learning library. In H. Wallach, H. Larochelle, A. Beygelzimer, F. d'Alché-Buc, E. Fox, and R. Garnett, editors, Advances in Neural Information Processing Systems 32, pages 8024–8035. Curran Associates, Inc., 2019.

- [51] Henning Petzka, Asja Fischer, and Denis Lukovnikov. On the regularization of Wasserstein GANs. In International Conference on Learning Representations, 2017.

- [52] Hossein Rad, Rand Kwong Yew Low, and Robert Faff. The profitability of pairs trading strategies: distance, cointegration and copula methods. Quant. Finance, 16(10):1541–1558, 2016.

- [53] Christian Rein, Ludger Rüschendorf, and Thorsten Schmidt. Generalized statistical arbitrage concepts and related gain strategies. Math. Finance, 31(2):563–594, 2021.

- [54] Johannes Ruf and Weiguan Wang. Hedging with linear regressions and neural networks. Journal of Business & Economic Statistics, 40(4):1442–1454, 2022.

- [55] Ludger Rüschendorf. Monge-Kantorovich transportation problem and optimal couplings. Jahresber. Deutsch. Math.-Verein., 109(3):113–137, 2007.

- [56] Walter Schachermayer. The fundamental theorem of asset pricing under proportional transaction costs in finite discrete time. Mathematical Finance: An International Journal of Mathematics, Statistics and Financial Economics, 14(1):19–48, 2004.

- [57] Jorge Sola and Joaquin Sevilla. Importance of input data normalization for the application of neural networks to complex industrial problems. IEEE Transactions on nuclear science, 44(3):1464–1468, 1997.

- [58] Ganapathy Vidyamurthy. Pairs Trading: quantitative methods and analysis, volume 217. John Wiley & Sons, 2004.

- [59] Cédric Villani. Optimal transport: old and new, volume 338. Springer Science & Business Media, 2008.