ifaamas \acmConference[AAMAS ’22]Proc. of the 21st International Conference on Autonomous Agents and Multiagent Systems (AAMAS 2022)May 9–13, 2022 OnlineP. Faliszewski, V. Mascardi, C. Pelachaud, M.E. Taylor (eds.) \copyrightyear2022 \acmYear2022 \acmDOI \acmPrice \acmISBN \acmSubmissionID??? \affiliation \institutionKAIST \cityDaejeon \countrySouth Korea \affiliation \institutionKAIST \cityDaejeon \countrySouth Korea \affiliation \institutionKAIST \cityDaejeon \countrySouth Korea \affiliation \institutionKorea University of Technology and Education \cityCheonan \countrySouth Korea

Automatic Calibration Framework of Agent-Based Models for Dynamic and Heterogeneous Parameters

Abstract.

Agent-based models (ABMs) highlight the importance of simulation validation, such as qualitative face validation and quantitative empirical validation. In particular, we focused on quantitative validation by adjusting simulation input parameters of the ABM. This study introduces an automatic calibration framework that combines the suggested dynamic and heterogeneous calibration methods. Specifically, the dynamic calibration fits the simulation results to the real-world data by automatically capturing suitable simulation time to adjust the simulation parameters. Meanwhile, the heterogeneous calibration reduces the distributional discrepancy between individuals in the simulation and the real world by adjusting agent related parameters cluster-wisely.

Key words and phrases:

Agent-Based Model; Simulation Validation; Likelihood-Free Inference; Parameter Calibration1. Introduction

Recently, enhanced computing power has motivated the construction of Agent-Based Models (ABMs) in a highly complex manner, and their efficacy has been expanded to various domains, such as market modeling Bonabeau (2002), traffic management Naiem et al. (2010), and urban planning Hosseinali et al. (2013). According to this extended applicability, the accuracy of the ABM compared to the target real-world is also in demand. Therefore, validation of the ABM becomes essential Beisbart and Saam (2018).

ABM naturally diverges from the real-world because of temporal discrepancies and agent heterogeneity. To fit the simulation to the real-world, we introduce two distinctive calibration methods regulating each diverging source: one is the dynamic calibration that adjusts the input parameters to vary over the simulation time to improve the temporal fitness. However, it could be computationally prohibitive to optimize dynamically varying parameters if we tune dynamic parameters at every time tick; therefore, we consider the regime as the smallest unit in parameter diversification. The regime is an object to be optimized via the Hidden Markov Model (HMM) Bishop (2006) for every iteration. The other is the heterogeneous calibration that fits the simulation to the real-world by diversifying parameters and optimizing these diversified parameters, which are likely to differ by agents. In this case, the agent cluster becomes the smallest unit of parameter diversification in heterogeneous calibration to limit the computational bottleneck. We obtain agent clusters by applying a Gaussian Mixture Model (GMM) Bishop (2006) to the latent embeddings extracted by the Variational Auto-Encoder (VAE) Kingma and Welling (2013).

As a generalization of two methods, we introduce a calibration framework of the ABM (Algorithm 1) by interchangeably adjusting dynamic parameters with consecutive iterations and heterogeneous parameters with consecutive iterations. Notably, the calibration framework reduces to the dynamic (or heterogeneous) calibration if (or ). In experiments, we established that each calibration method and their joint calibration framework significantly improve the simulation fitness to the real-world.

2. Details in Two Calibration Methods

Dynamic Calibration The dynamic calibration is a particle-based approach Sisson et al. (2007) that iteratively updates the proposal distribution, which is parametrized by , where is the single-shot real-world observation and is the calibration target parameters. The next candidate particles are sampled from this proposal distribution, and the calibration at the end estimates the optimal set of parameters that best fits the simulation to the real-world after calibration iterations. Based on the Bayes rule, the proposal distribution satisfies , where and are the building blocks to model the proposal distribution. According to Wood (2010), we estimate as an empirical Gaussian distribution estimated from 10 simulation replications. Additionally, we model as a product of Beta distributions , where is the parameter value of the -th regime, and is the shape coefficients of the Beta distribution of the -th regime. We update the proposal distribution by maximizing with respect to each iteration.

Heterogeneous Calibration The heterogeneous calibration works by Bayesian optimization. The Bayesian optimization Frazier (2018) is applied to a surrogate model of the fitness function estimated by the Gaussian process Tresidder et al. (2012). The approach using a surrogate model has been introduced previously in many disciplines. One distinctive point from previous research is that we separate agents by clusters and assign diverse parameter values to the divided clusters. Notably, the response curve of the ABM is sometimes non-differentiable at branch points, where the emergent behavior does not arise unless the parameter value reaches to such points. Because the most prominent Expected Improvement (EI) acquisition function sometimes fails to converge to the global minimum when the response curve is non-differentiable Bodin et al. (2019), our strategy involves mixing various acquisition functions Hoffman et al. (2011) to optimize the heterogeneous parameters. We propose the next set of candidate parameters randomly selected from 1) random sample, 2) max argument of predictive variance (exploration), 3) min argument of predictive mean (exploitation), and 4) max argument of weighted Expected Improvement Sóbester et al. (2005).

3. Experiments

We tested our calibration methods with the real estate market ABM of South Korea Yun and Moon (2020). The real-world housing market consists of various types of agents and is significantly affected by economic trends; therefore, the market is a favorable scenario for testing our calibration methods. There are three dynamic parameters: Market-Participation-Rate, Market-Price-Increase-Rate, and Market-Price-Decrease-Rate, as well as two heterogeneous parameters: Willing-to-Pay and Purchase-Rate. These are unobservable parameters that determine the underlying demand and supply curve of the model, so these are the representative parameters to calibrate.

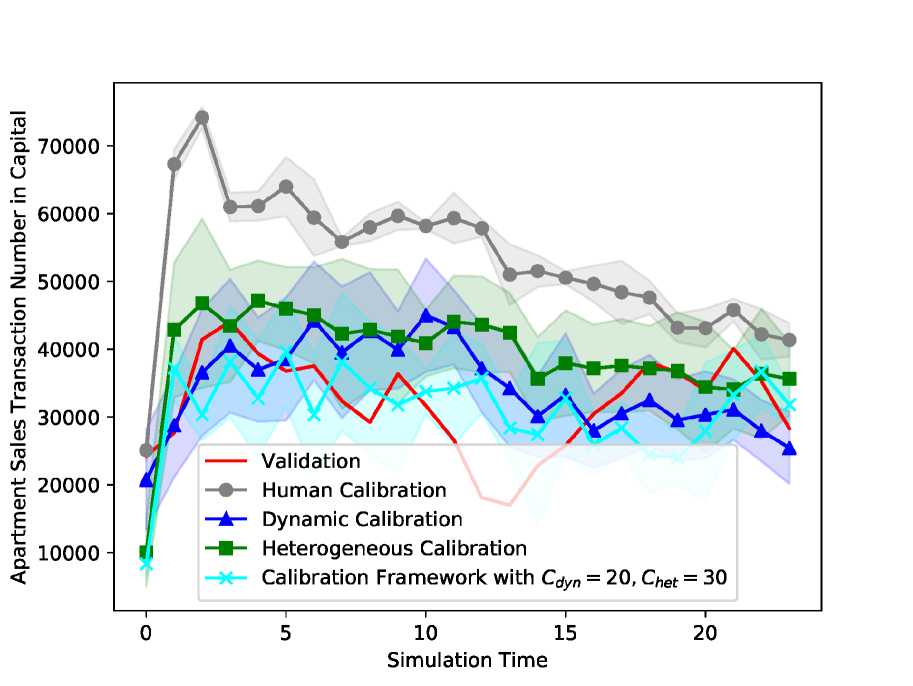

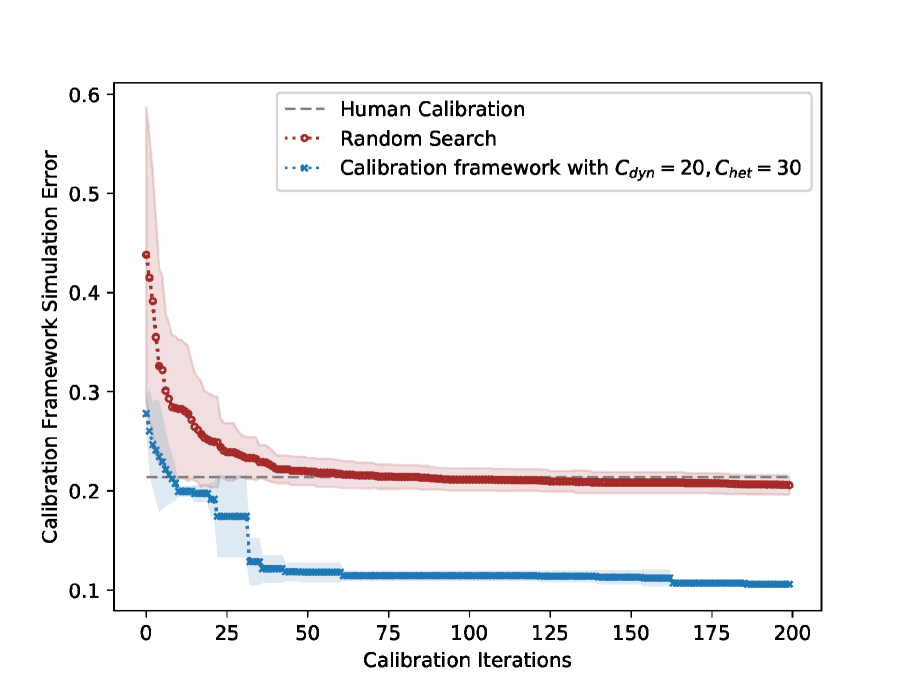

Figure 1-(a) compares the observation with 1) manual human calibration, 2) dynamic calibration, 3) heterogeneous calibration, and 4) combined calibration. Both of the suggested calibration methods significantly improve the human manual calibration. For Mean Absolute Percentage Error (MAPE), the human calibration is 0.765, whereas the MAPE is reduced to 0.281 in the dynamic calibration, and 0.232 in the heterogeneous calibration. In addition, we obtain a simulation that is best suited to the observation by combining two calibration methods with a MAPE of 0.219. Figure 1-(b) demonstrates that the suggested calibration framework outperforms to random search and human calibration.

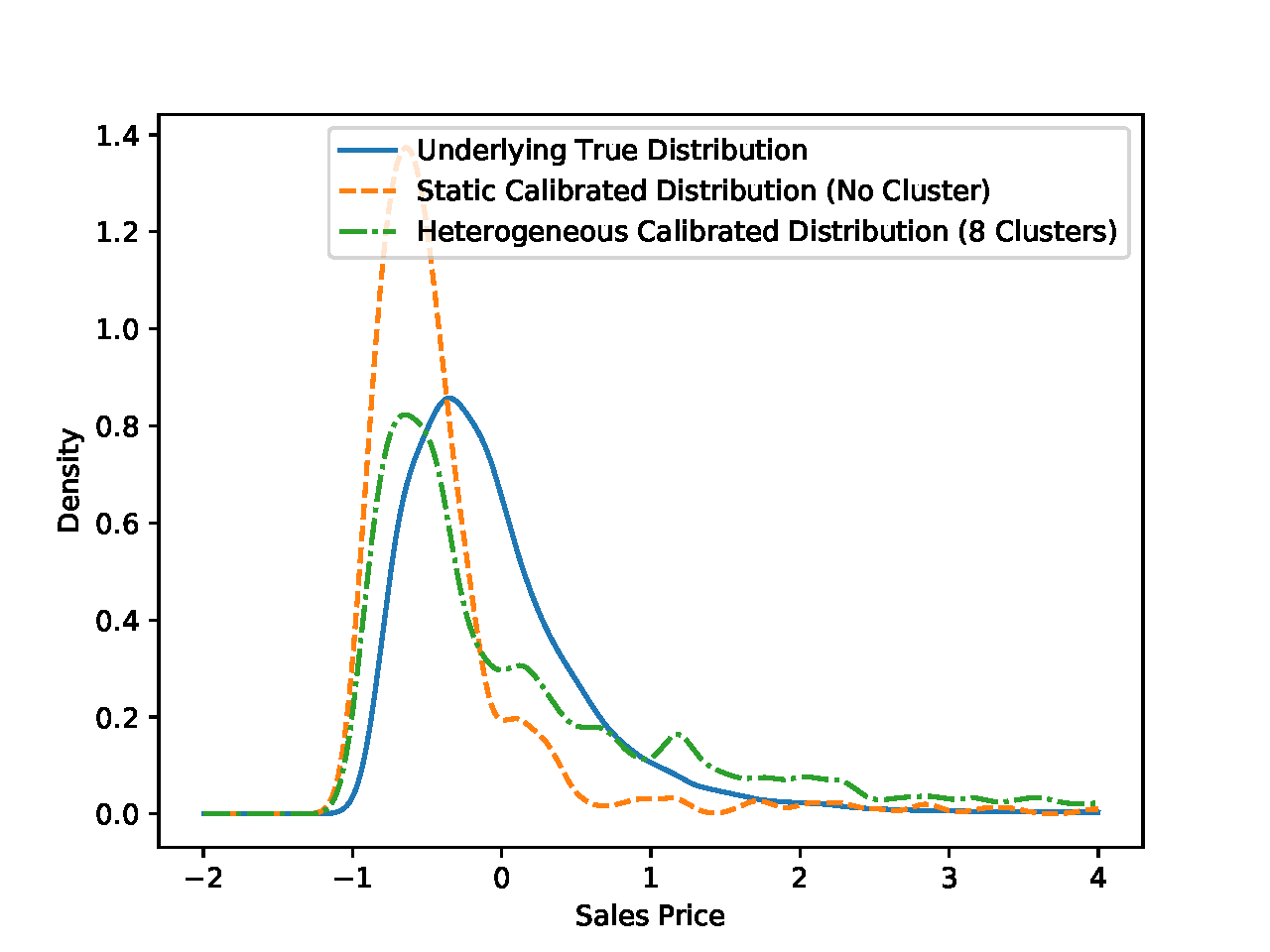

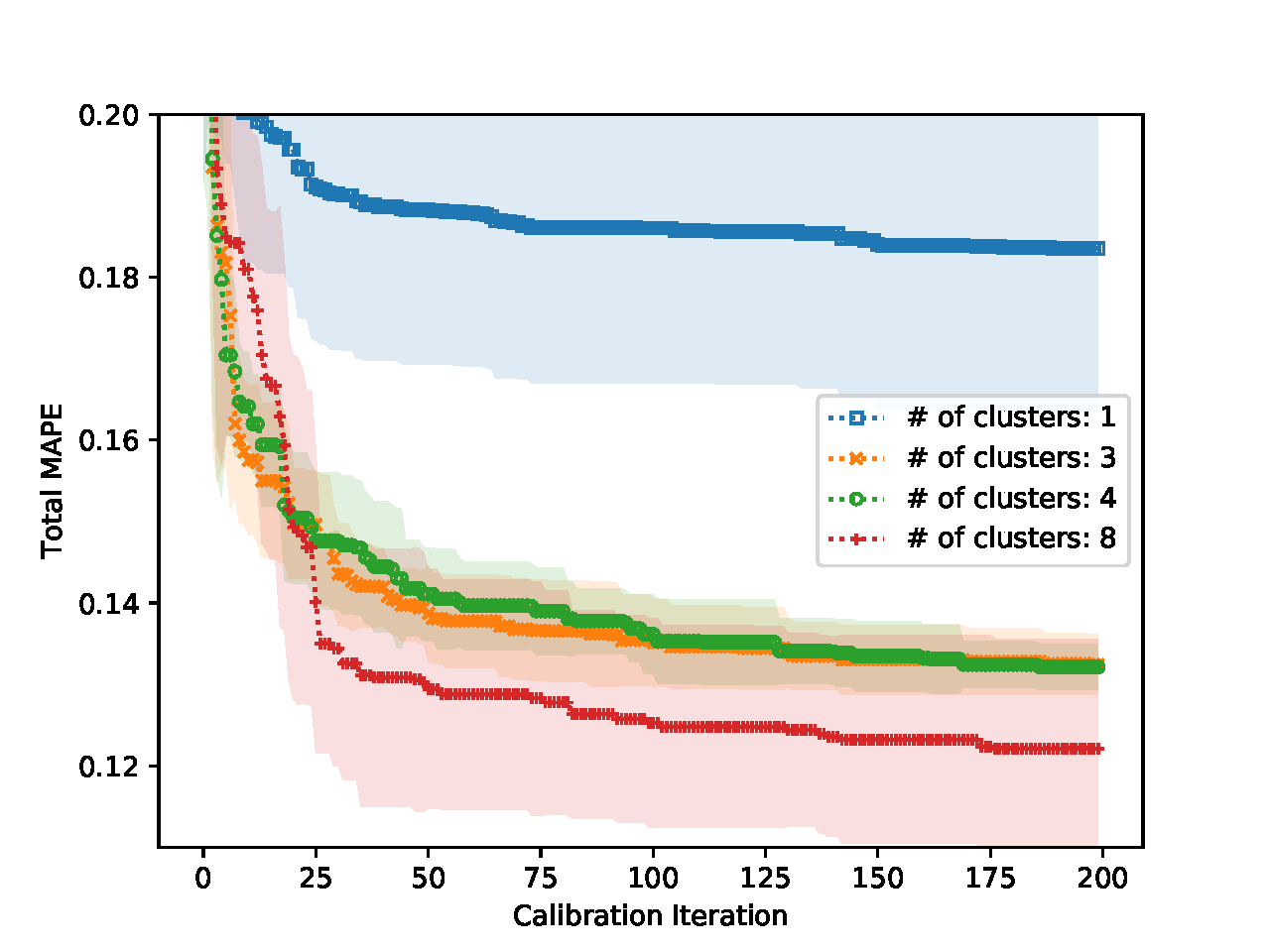

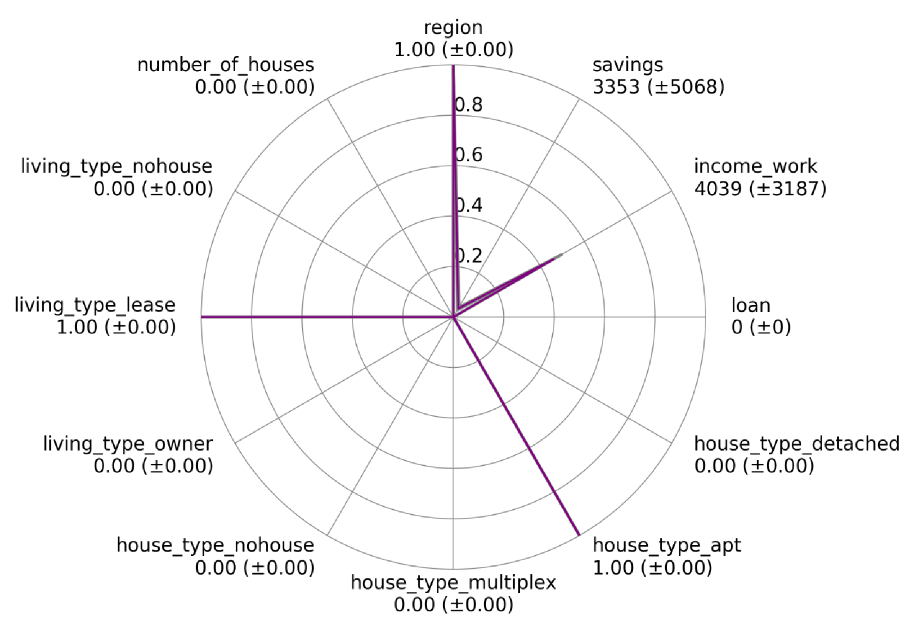

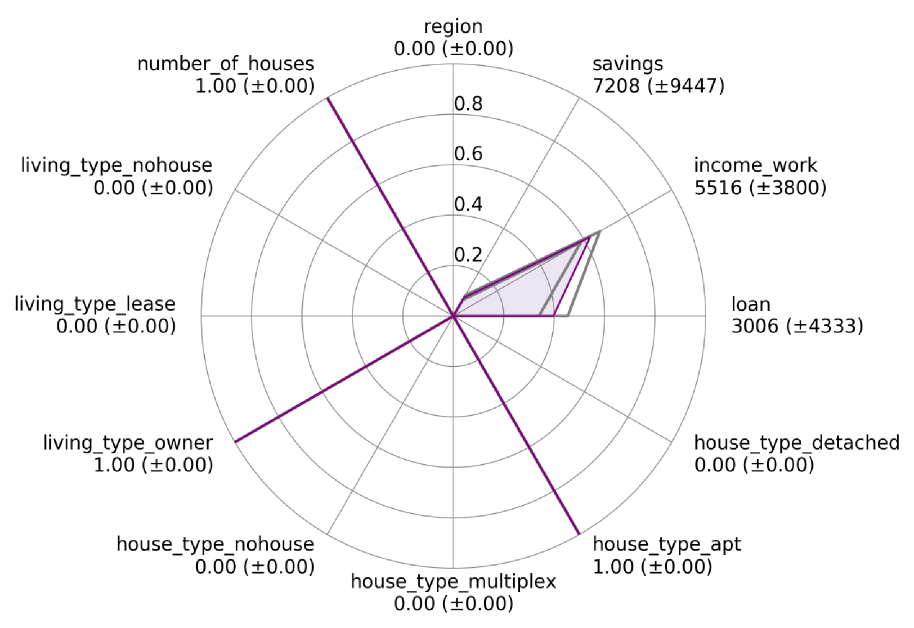

Figure 2-(a) presents the validity of heterogeneous calibration by showing that undifferentiated parameter is too rigid to fit the true distribution. Conversely, owing to the expanded degree of freedom, the heterogenous calibration not only improves the targeted summary statistics, but also fits the overall distribution as in Figure 2-(b). In Figure 3, agents in the left/right clusters live in rental/own houses, and this difference leads the optimal Willing-to-Pay to be 0.9/0.3 for left/right clusters, respectively. This indicates that agents in the left cluster without their own house are more willing to buy a new house in the near future.

4. Conclusion

This study proposes an automatic calibration framework of the ABM that generalizes both dynamic and heterogeneous calibrations, which discovered a well-calibrated parameter sets in experiments.

This research was supported by Development of City Interior Digital Twin Technology to establish Scientific Policy through the Institute for Information communication Technology Planning evaluation(IITP) funded by the Ministry of Science and ICT(2018-0-00225).

References

- (1)

- Beisbart and Saam (2018) Claus Beisbart and Nicole J Saam. 2018. Computer Simulation Validation: Fundamental Concepts, Methodological Frameworks, and Philosophical Perspectives. Springer.

- Bishop (2006) Christopher M Bishop. 2006. Pattern recognition and machine learning. springer.

- Bodin et al. (2019) Erik Bodin, Markus Kaiser, Ieva Kazlauskaite, Neill DF Campbell, and Carl Henrik Ek. 2019. Modulated Bayesian Optimization using Latent Gaussian Process Models. stat 1050 (2019), 26.

- Bonabeau (2002) Eric Bonabeau. 2002. Agent-based modeling: Methods and techniques for simulating human systems. Proceedings of the national academy of sciences 99, suppl 3 (2002), 7280–7287.

- Frazier (2018) Peter I Frazier. 2018. A Tutorial on Bayesian Optimization. stat 1050 (2018), 8.

- Hoffman et al. (2011) Matthew Hoffman, Eric Brochu, and Nando de Freitas. 2011. Portfolio allocation for Bayesian optimization. In Proceedings of the Twenty-Seventh Conference on Uncertainty in Artificial Intelligence. AUAI Press, 327–336.

- Hosseinali et al. (2013) Farhad Hosseinali, Ali A Alesheikh, and Farshad Nourian. 2013. Agent-based modeling of urban land-use development, case study: Simulating future scenarios of Qazvin city. Cities 31 (2013), 105–113.

- Kingma and Welling (2013) Diederik P Kingma and Max Welling. 2013. Auto-encoding variational bayes. arXiv preprint arXiv:1312.6114 (2013).

- Naiem et al. (2010) Amgad Naiem, Mohammed Reda, Mohammed El-Beltagy, and Ihab El-Khodary. 2010. An agent based approach for modeling traffic flow. In 2010 The 7th International Conference on Informatics and Systems (INFOS). IEEE, 1–6.

- Sisson et al. (2007) Scott A Sisson, Yanan Fan, and Mark M Tanaka. 2007. Sequential monte carlo without likelihoods. Proceedings of the National Academy of Sciences 104, 6 (2007), 1760–1765.

- Sóbester et al. (2005) András Sóbester, Stephen J Leary, and Andy J Keane. 2005. On the design of optimization strategies based on global response surface approximation models. Journal of Global Optimization 33, 1 (2005), 31–59.

- Tresidder et al. (2012) Es Tresidder, Yi Zhang, and AI Forrester. 2012. Acceleration of building design optimisation through the use of kriging surrogate models. Proceedings of building simulation and optimization (2012), 1–8.

- Wood (2010) Simon N Wood. 2010. Statistical Inference for Noisy Nonlinear Ecological Dynamic Systems. Nature 466, 7310 (2010), 1102.

- Yun and Moon (2020) Tae-Sub Yun and Il-Chul Moon. 2020. Housing market agent-based simulation with loan-to-value and debt-to-income. Journal of Artificial Societies and Social Simulation 23, 4 (2020).