Individual Fairness in Feature-Based Pricing for Monopoly Markets

Abstract

We study fairness in the context of feature-based price discrimination in monopoly markets. We propose a new notion of individual fairness, namely, -fairness , which guarantees that individuals with similar features face similar prices. First, we study discrete valuation space and give an analytical solution for optimal fair feature-based pricing. We show that the cost of fair pricing is defined as the ratio of expected revenue in an optimal feature-based pricing to the expected revenue in an optimal fair feature-based pricing (CoF) can be arbitrarily large in general. When the revenue function is continuous and concave with respect to the prices, we show that one can achieve CoF strictly less than , irrespective of the model parameters. Finally, we provide an algorithm to compute fair feature-based pricing strategy that achieves this CoF.

1 Introduction

The Internet has transformed the way markets function. Today’s Internet-based ecosystems such as entertainment and e-commerce marketplaces are more consumer-centric and information-driven than ever before. Data and AI systems are primarily used to power advertising, consumer retention, and personalized experience. These AI systems are deployed to aggregate individual choices and preferences to make personalized experiences possible. It is a common practice to use aggregated information about consumers to offer different prices to different consumers or segments of the market; this practice is commonly termed price discrimination Varian (1992).

Price discrimination has come under ethical scrutiny on multiple instances in the recent past. For example, it was found that Orbitz, an online travel agency, charges Mac users more than Windows users Mattioli (2012). Uber’s strategy to charge personalized prices came under heavy consumer backlash Dholakia (2015); Mahadawi (2018), and thanks to the fine-grained data analysis of consumer behavior, several such instances were reported in e-commerce and retail industry Hinz et al. (2011). More recently, Pandey and Caliskan (2021) showed that neighborhoods with high non-white populations, higher poverty, younger residents, and high education levels faced higher cab trip fares in Chicago. Not surprisingly, the regulatory bodies and research community has taken notice. Economists have raised concerns on fairness issues of personalized pricing Michel (2016). Price discrimination based on nationality or residence is made illegal in the EU (2020). In the USA, a white house report provides guidelines for enforcing existing anti-discrimination, privacy, and consumer protection laws while practicing discriminatory pricing White House (2015). Given the overwhelming evidence and rising concerns, there is an urgent need to study price discrimination and fairness formally.

Sellers or firms use price discrimination for multiple reasons, including increasing revenue, covering transportation and storage costs, increasing market reach, rewarding loyal consumers, promoting a social cause, and so on Cassady (1946). In general, price discrimination does not always raise ethical and fairness issues and hence requires a careful inspection to categorize situations where this practice may lead to treatment disparity and invite regulatory intervention Alan (2020). In this work, we focus on designing the pricing strategies for a seller (monopolist) who wants to maximize the revenue via price discrimination while ensuring fairness amongst the consumers.

A revenue-maximizing seller with complete knowledge of consumer valuations without fairness consideration would charge each consumer her valuation for the product. This pricing strategy, otherwise called first-degree price discrimination, may result in wild fluctuations in prices and is considered unfair in general Moriarty (2021). Also, in practice, sellers do not have full access to individual consumer valuations but may have a distribution over valuations through features. In such feature-based pricing (FP), the seller segregates the market into segments through the consumer features. The seller’s problem then reduces to finding optimal pricing for each segment Bergemann et al. (2015); Cummings et al. (2020). Such FP is referred to as third-degree price discrimination in the literature. In this paper, our goal is to ensure fairness issues in feature-based personalized pricing.

Our Contributions

We introduce the notion of -fairness in price discrimination which ensures that similar individuals face similar prices. We emphasize that if individuals with similar features are charged differently by segregating them into different segments, the interpersonal price comparison based on their features renders fairness issues. With this, we introduce a model for optimal fair feature-based pricing (FFP) as the problem of maximizing revenue while ensuring -fairness . We begin with two segments in the market and discrete valuations and propose an optimal FFP scheme (Section 4.2). To quantify the loss in the revenue due to fairness, we then introduce cost of fairness (CoF) – the ratio of expected revenue in an optimal FFP to the expected revenue in an optimal FP. We prove that a constant lower bound on CoF is impossible to achieve in general.

Next, in Section 5.1, under the assumption that the revenue function is concave in offered prices Bergemann et al. (2021)111this assumption is standard in economics as a large number of probability distributions follow this, we show that one can achieve a constant upper bound on CoF. Here, first, we show that the seller can compute optimal FFP using a convex program if it has access to distributional information (knows all consumers’ valuation distribution functions). We then identify a class of FFP strategies, namely LinP-FFP that satisfy -fairness . With the help of these pricing strategies, we then show that the CoF is strictly less than irrespective of model parameters. Finally, we propose OPT-LinP-FFP, an time algorithm where is the number of segments that does not need access to complete distributional information and computes -fair pricing that achieves the aforementioned CoF (Algorithm 1 and Theorem 7).

2 Related Work

The impact of discriminatory pricing on consumer and seller surplus was first considered by Bergemann et al. (2015) when the consumer characteristics are known to the seller. The authors proposed a method to provide the optimal market segmentation. The generalized problem was then considered by Cummings et al. (2020) which extended the work of Bergemann et al. (2015) to the case where only partial information about the consumer’s valuation was known to the seller.

When the valuations of the consumers are not known, Elmachtoub et al. (2019, 2021) propose feature-based pricing and provides bounds on the value generated using idealized personalized pricing and Feature-based pricing over Uniform pricing. The value of feature-based pricing depends on the correlation of valuations and consumer features. Huang et al. (2019) consider the first-degree price discrimination over the social network where the centrality measures in social networks determine the features of the consumers. They provide bounds on the value of network-based personalized pricing in large random social networks with varying edge densities. Our work follows a similar approach because we derive personalized pricing from the features. However, naive feature-based pricing can be very unfair to the consumers, as we show in Proposition 2. Our focus is to design feature-based pricing that is fair at the same time.

Recently, many questions have been raised on the ethical side of price discrimination methods. Moriarty (2021) strongly criticizes online personalized pricing and suggests that personalized prices compete unfairly for social surplus created by transactions. Gerlick and Liozu (2020) points out the need to design personalized pricing with ethical considerations, which can provide win-win outcomes for both organizations and consumers. Richards et al. (2016) discusses that discriminatory pricing leads to the perception of unfairness amongst the consumers, which undermines the stability of retail platforms. They discuss that when consumers are involved in forming the prices, this leads to improved fairness perception, thus leading to better retentivity. Levy and Barocas (2017) discusses that web-based platforms typically use many private features of user profiles to connect buyers and sellers. When users interact on such platforms, it leads to discrimination regarding race, gender, and possibly other protected characteristics. All these studies lead to understanding the optimal price discriminatory strategies under the fairness constraint, which is the focus of our work.

Finally, Kallus and Zhou (2021) presents a list of metrics like price disparity, equal access, allocative efficiency fairness to measure and analyze fairness in feature-based pricing and study its interplay with welfare. The metrics discussed are mainly the group fairness notions which are entirely different from -fairness discussed in this paper. We emphasize that though the above papers discuss the ethical issues in price discrimination, none of them provides a systematic approach to design the pricing strategy that maximizes the revenue and ensures the fairness guarantee.

3 Preliminaries

We consider a market with a monopolist seller seeking to price a single product available in infinite supply. The market is divided into finite number of segments , where represents the segment. The seller, given access to , can choose to price discriminate across segments to extract maximum revenue.

| Notation | Description |

|---|---|

| FP | Feature-based Pricing |

| FFP | Fair Feature-based Pricing |

| , | Valuations CDF, PDF for consumer segment respectively |

| Set of all consumer features/types | |

| Support set of consumers’ valuations | |

| Consumer feature of the segment | |

| The fraction of consumers in the segment | |

| Feature-based price vector | |

| Revenue generated per consumer in the segment | |

| Revenue generated by across all consumer segments | |

| Price function in optimal price discrimination | |

| A real-valued metric on the consumer feature space | |

| Fairness parameter | |

| Optimal fair feature-based price function | |

| Price vector for OPT-LinP-FFP | |

| CoF | Cost of Fairness |

| Linear approximation of concave revenue curve with as parameter |

Consumers’ valuations for the single product are non-negative random variables drawn from the set (same across all segments). Let be the cumulative distribution function for the valuation of the consumers in segment, and be corresponding probability density function (probability mass function when is discrete). In this paper, we consider the following two cases separately, (a) is discrete and finite, and (b) is continuous. Next, we present feature-based pricing model.

3.1 Feature-based Pricing Model

In feature-based pricing (FP), one can consider, without loss of generality, that the consumer feature is a representative of the market segment to which she belongs. Note that multiple consumers may have the same feature vector, and all the consumers having identical features belong to the same market segment. For simplicity, we will write price offered to the consumer in the segment. A consumer makes the purchase only if her valuation is equal to or more than the offered price. The expected revenue per consumer generated from the segment with a price is given by

| (1) |

Whenever it is clear from the context we refer to expected revenue per consumer from a segment to be expected revenue from that segment. Let be the fraction of consumers in the segment, then the expected revenue per consumer generated across all segments is given as . We assume that s are known to the seller. We call the sellers problem of revenue maximization as OPT where and .

In the absence of fairness constraints, OPT reduces to charging each segment separately and optimal FP strategy consisting for segment is given by

Fairness in Feature-based Pricing

Let be a distance function over . We assume that such a function exists and is well defined in , i.e., is a metric space. The distance function quantifies the dissimilarity between feature vectors of individuals belonging to market segments. For simplicity we write . Individual fairness in FP strategy is defined as:

Definition 1 (-fairness ).

A price function is -fair with respect to iff for all , we have

| (2) |

We call a pricing strategy Fair Feature-based Pricing (-FFP) that satisfies Eq. 2 with a given value of . It is easy to see from the definition that any -FFP is also -FFP for any . We will drop the quantifier and call it FFP when it is clear from the context.

Cost of Fairness (CoF)

Next, we define CoF as the deviation from optimality due to fairness constraints given in Eq. 2. It is defined as the ratio of expected revenue generated by optimal feature-based pricing and fair feature-based pricing.

Definition 2 (Cost of Fairness (CoF)).

Cost of fairness for an FFP strategy is defined as

| (3) |

4 FFP for Discrete Valuations

We want to ensure -fairness in the pricing strategy given the optimal FP. -fairness is achieved by maximizing revenue while satisfying the fairness constraints. In this section, we derive optimal FP (Section 4.1), propose how to achieve -fairness (Section 4.2), and provide an upper bound on CoF (Section 4.3) for discrete valuation setting.

We consider the simplest setting described as follows: Let the consumer segments be given by and their valuations are drawn from a discrete set , we assume without loss of generality. Let and . Further, let () denote the probability that a consumer has valuation in segment 1 (segment 2). The expected revenue generated by is given by:

| (4) |

4.1 Optimal Feature-based Pricing

As discussed earlier, can be maximized by maximizing for each market segment independently if there are no fairness constraints. This problem is an integer program with price for each consumer type being a discrete variable. The revenue generated depends on and (, , in the current simplest case). The optimal FP is then given as

| (5) |

Proof.

For a market segment , and . So, if

otherwise, .

∎

Next, we analyze the fairness aspects of the above pricing strategy.

4.2 Optimal Fair Feature-based Pricing

Let be a metric space. We model the Optimal fair feature-based pricing (FFP) problem as integer program which maximizes with -fairness constraints described in Eq.(2). We denote this problem as OPT and the corresponding optimal FFP strategy is denoted as . First we make an interesting and very useful claim for binary valuations.

Lemma 1.

When , and if is not -fair, OPT reduces to OPT where .

Proof.

Let be the tuple of offered prices. Note that if or , then the optimal with support and will be trivially fair. We consider a more interesting case when and . In this case, the only candidate support sets for optimal fair pricing strategy are: , , , . The optimal FFP does not take values from the set as the consumers with valuation would not make any purchase. Hence, the expected revenue with support will be less than or equal to the expected revenue with support . ∎

We now relax the constraint of binary valuation and analyze the optimal fair pricing scheme for valuations. The consumer segments are with and , the valuations are drawn from the set , and and . This is a simple extension of the pricing problem, OPT modelled as an integer program where the prices are drawn from the set . If is not -fair then, the corresponding OPT can be solved by reducing it to OPT with given by:

Given the set , the pricing problem OPT can be solved in constant time. It is easy to see that computing takes time for valuations and consumer types. Therefore, the fair pricing problem OPT can be solved in time.

4.3 CoF Analysis

For , based on the values of we have the following cases:

-

1.

-

2.

-

3.

,

-

4.

,

In cases 1 and 2, optimal fair pricing is equivalent to uniform pricing and therefore are ‘trivially’ fair with CoF = 1, i.e., . For case 3, and are given as:

Then the cost of fairness for case 3 is given as:

| CoF | ||||

| (6) |

Replacing with and with in the above expression, we get a similar approximation of CoF for case 4.

Proposition 2.

Cost of fairness with discrete valuations can go arbitrarily bad.

Proof.

From Eq. 6 when , we have . The CoF (in Case 3 and/or Case 4) is arbitrarily bad if when there is a large difference between and . Note that is uninteresting as the seller is unable to distinguish between two segments. ∎

Note that being arbitrarily large need not be a commonly occurring setting. Hence, we work with bounded support valuations in the backdrop of the above negative results. In the next section, we make assumptions based on standard economic literature about the revenue functions , i.e., concave revenue functions and common support Bergemann et al. (2021). As argued in Section 3 of Dhangwatnotai et al. (2015), valuation distributions satisfying Monotone Hazard Rate (MHR) satisfy the assumptions as mentioned above regarding revenue functions. It is also observed that the revenue functions are concave for another commonly analyzed family of distributions in literature called the regular distributions in which the virtual valuation is non-decreasing (Section 4.3 of Bergemann et al. (2021)). MHR is a common assumption in Econ-CS Hartline and Roughgarden (2009). Therefore, in the following section, we analyze the cost of fairness for such valuation distributions and the associated concave revenue functions.

5 FFP for Continuous Valuations

In this section, we consider feature-based pricing with continuous valuations. We impose a standard restriction on the revenue functions such that they are concave on the common support Bergemann et al. (2021). The consumer segments are identified by the associated feature vectors . is the marginal cost defined as a minimum feasible valuation for which a seller is willing to sell the product. The marginal cost may include the cost of production, transportation, etc. On the other hand, is the maximum consumer valuation. Without loss of generality, we consider that maximum consumer valuation is greater than marginal cost; i.e., trade occurs.

We begin with a tight upper bound on the CoF under conditions as mentioned above (Section 5.1) followed by two pricing schemes based on the available information about the revenue functions (Section 5.2), and finally, we present an algorithm that achieves the CoF bound in Section 5.3.

5.1 Optimal FFP for Continuous Valuations

The problem of determining optimal FFP can be modeled as a convex program with -fairness as linear constraints. The convex program below describes OPT model with complete knowledge of revenue functions .

Let be a solution to the above problem.

5.2 LinP-FFP and CoF Analysis

Let . With the following proposition, we propose a class of -fair pricing strategies.

Proposition 3.

For a given , if the price function satisfies for all then it satisfies -fairness .

Proof.

From triangle inequality, we have . The last inequality results from the fact that and . ∎

In other words, for ensuring that the prices for different segments are not too different, it is enough to ensure that the pricing for each segment is not too different from some common point . The pricing for all the segments would hence be around this point and could be determined with respect to this point. We term this point as pivot. We now present the second FFP model, an -fair pricing strategy that is pivot-based and satisfies the condition in Proposition 3, with access to only for a given .

| (8) |

We call this pricing scheme LinP-FFP. It is easy to see that the above pricing strategy is -fair. We now present the CoF bound for LinP-FFP.

Theorem 4.

The Cost of Fairness for optimal fair price discrimination with concave revenue functions satisfies

Proof.

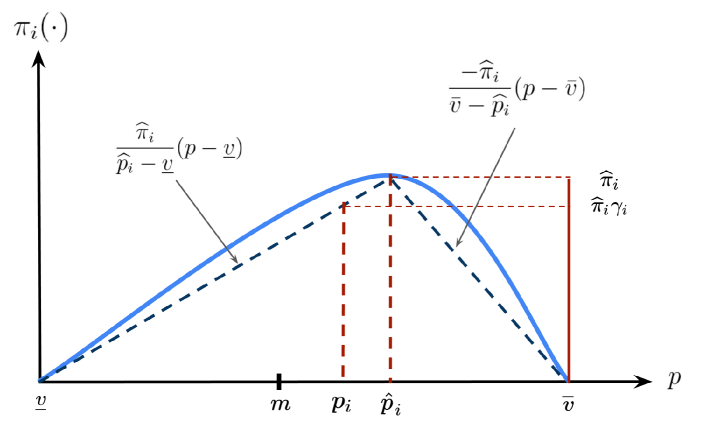

We prove that the above CoF is satisfied by LinP-FFP and hence the theorem. Let be a pivot point (See Figure 1). Let

| (9) |

Let be the expected revenue generated from the segment under . We now show the following supporting lemma.

Lemma 5.

The pricing strategy given in Eq. 8 guarantees at-least fraction of optimal revenue from segment , i.e., .

Proof.

A lower bound to the concave revenue functions for any segment is the piecewise linear approximation , given by (see Figure 1):

| (10) |

So, for each consumer segment we have,

Expected revenues generated per consumer in segment by pricing rule in Eq. (8) for , , and remaining cases are given below in the respective order

This proves the lemma. ∎

Let denote the expected revenue generated from the segment by . So, CoF for optimal FPP is given by:

| CoF | (Optimality of ) | |||

| (Lemma 5) | ||||

It is worth noting here that the cost of fairness does not depend on the number of the segments and the distribution of the population among these segments. So, if the segments are well separated in terms of the distance between features of consumers across segments the number of segments as well as the distribution of consumer population in these segments do not affect revenue guarantee. Also, if the admissible prices are supported over a large interval, the fairness guarantee becomes weaker. This insight discourages pricing schemes with wildly varying prices across segments. Finally, if , i.e., without any fairness constraints, we recover the bound of 2 proved in Bergemann et al. (2021).

We emphasize that the bound is strictly less than because, under fairness constraints, and typically the consumer types are well separated in the feature space according to the metric else, the consumer types are indistinguishable for the seller hence, for all . This is an improvement of the CoF bound given in Bergemann et al. (2021).

Tightness of CoF bound:

We claim that the CoF bound presented above is tight. In the following example, equality holds and proves the tightness of the bound.

Example 1 (Tightness of the CoF bound).

Consider where . Consider be such that with where , and . It can be seen that if is such that , any FP satisfying and is an optimal FFP (fair FP), and the corresponding . If , the optimal FP is -fair and so, . Hence, for this example, . This shows the tightness of the CoF bound derived in Theorem 4.

We now present an algorithm, OPT-LinP-FFP, to find the optimal pivot in the above LinP-FFP strategy when only and s are known.

5.3 Proposed Algorithm

As LinP-FFP satisfies -fairness (Proposition 3), and also achieves CoF bounds in Theorem 4, we look for a pricing strategy optimal within class of LinP-FFP. It reduces to finding an optimal pivot that maximizes revenue. In this section, we propose a binary-search-based algorithm for the same. For pricing , the expected revenue generated per consumer is given by . Let . Observe from Lemma 5 that is lower bounded as:

| (13) | ||||

Determining Optimal Pivot

As we can see, the revenue generated by LinP-FFP is lower bounded by a piecewise linear function in . With the aim of achieving a better lower bound, we now address the problem of determining an optimal pivot .

Pricing Algorithm

In what follows, we call the candidate points for optimal pivot, i.e., for maximizing , as critical points. We denote the set of these critical points as .

Lemma 6.

as a function of is concave and piecewise linear with the set of critical points .

Proof.

It is easy to see that for a segment , as a function of is continuous and piecewise linear with breakpoints (i.e., points at which piecewise linear function changes slope): and provided they are in the range . The set of breakpoints is hence . Also, the slope monotonically decreases at the breakpoints, i.e., is a concave function of .

From Eq. 13, we can see that is a weighted sum over all segments, of ’s with constant weights . So, as a function of is concave and piecewise linear with breakpoints belonging to the following set: . Hence, a point that maximizes belongs to either the aforementioned set of breakpoints, or the set of its boundary points . Thus, the set of critical points . ∎

Our algorithm OPT-LinP-FFP (Optimal Linearized Pivot-based Fair Feature-based Pricing) which determines an optimal pivot and provides an -fair pricing strategy () is presented in Algorithm 1.

Theorem 7.

The OPT-LinP-FFP algorithm (a) returns optimal pivot point and runs in time, and (b) achieves the CoF bound given in Theorem 4.

Proof.

(a) The first module is the creation and sorting of the set of critical points , which takes time. Owing to Lemma 6, we can find an optimal pivot using binary search over . Here, the number of critical points are at most , i.e., . So, in the second module that finds an optimal pivot, the binary search in the outer (while) loop runs for iterations, and the inner (for) loops run for iterations overall. Thus, the running time of the second module is . The third module that computes pricing for the different segments runs in time. So, the total running time of Algorithm 1 is .

(b) From Theorem 4, for , the CoF bound holds. Also, for all . We have:

This completes the proof of the theorem. ∎

6 Discussion

This paper built a foundation for the design of fair feature-based pricing by proposing a new fairness notion called -fairness . Our impossibility result on the discrete valuation setting restricted us from attaining a finite cost of fairness (CoF) in general settings. Interestingly, in the continuous valuation setting with concave revenue functions, we showed that a family of pricing schemes, LinP-FFP, provided a CoF strictly less than . Finally, we proposed an algorithm, OPT-LinP-FFP, which gave us an optimal pricing strategy within this family. It is worth noting that the algorithm does not require a complete distribution function; peaks of revenue distributions are sufficient statistics for computing optimal fair feature-based pricing.

We leave the problem of finding an optimal segmentation (optimal value of and corresponding -partition of the market) as interesting future work. We assumed a monopoly market. It will be interesting to study optimal fair pricing in the face of competition and other constraints such as finite supply, non-linear production cost, and variable demand.

References

- (1)

- Alan (2020) Kaplan Alan. 2020. Hospital Price Discrimination Is Deepening Racial Health Inequity. https://catalyst.nejm.org/doi/full/10.1056/CAT.20.0593.

- Bergemann et al. (2015) Dirk Bergemann, Benjamin Brooks, and Stephen Morris. 2015. The limits of price discrimination. American Economic Review 105, 3 (2015), 921–57.

- Bergemann et al. (2021) Dirk Bergemann, Francisco Castro, and Gabriel Weintraub. 2021. Third-Degree Price Discrimination Versus Uniform Pricing. arXiv:1912.05164 [econ.GN]

- Cassady (1946) Ralph Cassady. 1946. Techniques and Purposes of Price Discrimination. Journal of Marketing (pre-1986) 11, 000002 (10 1946), 135. https://www.proquest.com/scholarly-journals/techniques-purposes-price-discrimination/docview/209297864/se-2?accountid=27233 Copyright - Copyright American Marketing Association Oct 1946; Last updated - 2021-09-09; CODEN - JMKTAK.

- Cummings et al. (2020) Rachel Cummings, Nikhil R. Devanur, Zhiyi Huang, and Xiangning Wang. 2020. Algorithmic Price Discrimination. In Proceedings of the 2020 ACM-SIAM Symposium on Discrete Algorithms (SODA). SIAM, 2432–2451. https://doi.org/10.1137/1.9781611975994.149 arXiv:https://epubs.siam.org/doi/pdf/10.1137/1.9781611975994.149

- Dhangwatnotai et al. (2015) Peerapong Dhangwatnotai, Tim Roughgarden, and Qiqi Yan. 2015. Revenue maximization with a single sample. Games and Economic Behavior 91 (2015), 318–333.

- Dholakia (2015) Utpal Dholakia. 2015. Everyone Hates Uber’s Surge Pricing – Here’s How to Fix It. https://hbr.org/2015/12/everyone-hates-ubers-surge-pricing-heres-how-to-fix-it.

- Elmachtoub et al. (2019) Adam N. Elmachtoub, V. Gupta, and Michael L. Hamilton. 2019. The Value of Personalized Pricing. Revenue & Yield Management eJournal (2019).

- Elmachtoub et al. (2021) Adam N Elmachtoub, Vishal Gupta, and Michael L Hamilton. 2021. The value of personalized pricing. Management Science (2021). https://doi.org/10.1287/mnsc.2020.3821

- EU (2020) Communications Authority EU. 2020. Pricing and payments. https://europa.eu/youreurope/citizens/consumers/shopping/pricing-payments/index_en.htm.

- Gerlick and Liozu (2020) Joshua A. Gerlick and Stephan M. Liozu. 2020. Ethical and Legal Considerations of Artificial Intelligence and Algorithmic Decision-making in Personalized Pricing. Journal of Revenue and Pricing Management 19, 2 (2020), 85–98. https://doi.org/10.1057/s41272-019-00225-2

- Hartline and Roughgarden (2009) Jason D Hartline and Tim Roughgarden. 2009. Simple versus optimal mechanisms. In Proceedings of the 10th ACM conference on Electronic commerce. 225–234.

- Hinz et al. (2011) Oliver Hinz, II-Horn Hann, and Martin Spann. 2011. Price Discrimination in E-Commerce? An Examination of Dynamic Pricing in Name-Your-Own Price Markets. MIS Quarterly 35, 1 (2011), 81–98. http://www.jstor.org/stable/23043490

- Huang et al. (2019) Jiali Huang, Ankur Mani, and Zizhuo Wang. 2019. The Value of Price Discrimination in Large Random Networks. In Proceedings of the 2019 ACM Conference on Economics and Computation (Phoenix, AZ, USA) (EC ’19). Association for Computing Machinery, New York, NY, USA. https://doi.org/10.1145/3328526.3329617

- Kallus and Zhou (2021) Nathan Kallus and Angela Zhou. 2021. Fairness, Welfare, and Equity in Personalized Pricing. In Proceedings of the 2021 ACM Conference on Fairness, Accountability, and Transparency (Virtual Event, Canada) (FAccT ’21). Association for Computing Machinery, New York, NY, USA, 19. https://doi.org/10.1145/3442188.3445895

- Levy and Barocas (2017) Karen Levy and Solon Barocas. 2017. Designing Against Discrimination in Online Markets. Berkeley Technology Law Journal 32, 3 (2017), 1183–1238. https://www.jstor.org/stable/26488980

- Mahadawi (2018) Arwa Mahadawi. 2018. Is your friend getting a cheaper Uber fare than you are? https://www.theguardian.com/commentisfree/2018/apr/13/uber-lyft-prices-personalized-data.

- Mattioli (2012) Dana Mattioli. 2012. On Orbitz, Mac Users Steered to Pricier Hotels. https://www.wsj.com/articles/SB10001424052702304458604577488822667325882.

- Michel (2016) Stefan Michel. 2016. Is personalized pricing fair? https://www.imd.org/research-knowledge/articles/is-personalized-pricing-fair/.

- Moriarty (2021) Jeffrey Moriarty. 2021. Why online personalized pricing is unfair. Ethics and Information Technology 23 (09 2021), 1–9. https://doi.org/10.1007/s10676-021-09592-0

- Pandey and Caliskan (2021) Akshat Pandey and Aylin Caliskan. 2021. Disparate Impact of Artificial Intelligence Bias in Ridehailing Economy’s Price Discrimination Algorithms. Association for Computing Machinery, New York, NY, USA, 822–833.

- Richards et al. (2016) Timothy J. Richards, Jura Liaukonyte, and Nadia A. Streletskaya. 2016. Personalized Pricing and Price Fairness. International Journal of Industrial Organization 44 (2016), 138–153. https://doi.org/doi.org/10.1016/j.ijindorg.2015.11.004

- Varian (1992) Hal R. Varian. 1992. Microeconomic Analysis (third ed.). Norton, New York.

- White House (2015) Obama White House. 2015. Big data and differential pricing. https://obamawhitehouse.archives.gov/sites/default/files/whitehouse_files/docs/Big_Data_Report_Nonembargo_v2.pdf.