Confidence Intervals of Treatment Effects in Panel Data Models with Interactive Fixed Effects111The authors thank all seminar participants for their comments. We also thank Xinyi Wang for assistance in translating our original MATLAB codes into Python and R codes.

Abstract

We consider the construction of confidence intervals for treatment effects estimated using panel models with interactive fixed effects. We first use the factor-based matrix completion technique proposed by Bai and Ng, (2021) to estimate the treatment effects, and then use bootstrap method to construct confidence intervals of the treatment effects for treated units at each post-treatment period. Our construction of confidence intervals requires neither specific distributional assumptions on the error terms nor large number of post-treatment periods. We also establish the validity of the proposed bootstrap procedure that these confidence intervals have asymptotically correct coverage probabilities. Simulation studies show that these confidence intervals have satisfactory finite sample performances, and empirical applications using classical datasets yield treatment effect estimates of similar magnitudes and reliable confidence intervals.

Keywords: Bootstrap, Confidence interval, Treatment effects, Panel data analysis, Interactive effects, Matrix completion

JEL classification: C01, C21, C31, I18

Introduction

Treatment effects of certain policy interventions on economic entities are often of major interest in economic and econometric studies. In panel data models, estimation of and inference on treatment effects can be formulated as missing data problems. For instance, consider a sample of units with a policy intervention on units at time , so that the pre-treatment periods are , the post-treatment periods are , and the control units are . Let be the potential outcome in the absence of policy intervention for unit at time , and be the potential outcome under policy intervention for unit at time . We are interest in the treatment effect for , and it is easy to see that calculating requires knowing , which is actually unobservable (missing) for .

Many existing methods of estimating make efforts to construct “counterfactuals” for , (e.g., Abadie et al.,, 2010; Hsiao et al.,, 2012; Bai and Ng,, 2021; Athey et al.,, 2021; among others). The underlying models in counterfactual frameworks can be simplified as , where is the systematic part and is the idiosyncratic error. Then the predicted values serve the role as the counterfactuals for , and the treatment effects are estimated by for every . According to model specifications, assumptions, and estimation strategies, we can roughly classify the existing methods into the following 4 categories.

The first category is the synthetic control method proposed by Abadie and Gardeazabal, (2003) and Abadie et al., (2010). It approximates by a convex combination of , which can be obtained from a constrained regression. Generalisations of the synthetic control method can be found in, for example, Amjad et al., (2018), Abadie and L’Hour, (2021), Arkhangelsky et al., (2021), Ben-Michael et al., 2021a , Ben-Michael et al., 2021b , Kellogg et al., (2021), and Masini and Medeiros, (2021). One can see Abadie, (2021) for a comprehensive review. The second category is the the panel data approach proposed by Hsiao et al., (2012), which constructs the counterfactual by solving a linear regression of on . This approach is later extended by Ouyang and Peng, (2015), Li and Bell, (2017), and Hsiao et al., (2022). Methods in the third category use the factor model technique (e.g., Bai and Ng,, 2002; Bai,, 2003; Pesaran,, 2006; Bai,, 2009; Moon and Weidner,, 2015) to construct counterfactuals. Examples include Kim and Oka, (2014), Xu, (2017), and Bai and Ng, (2021). The last category starts from the statistical learning literature on matrix completion (e.g., Candès and Recht,, 2009; Candès and Plan,, 2010; Mazumder et al.,, 2010; Gamarnik and Misra,, 2016), and a recent example is Athey et al., (2021), which completes the potential outcome matrix via nuclear norm regularisation.

In practice, a mere point estimator of the treatment effect is not sufficient either theoretically or empirically, and a valid inference is needed, which usually requires the (asymptotic) distribution of . As , the idiosyncratic error term will dominate the distribution of as whenever the systematic part can be consistently approximated. Due to this issue, most studies make inferences on time series average treatment effects as the number of post-treatment periods (e.g., Hsiao et al.,, 2012; Li and Bell,, 2017; Li,, 2020, and Chernozhukov et al., 2021b, ), or make inferences on cross-sectional average treatment effects as the number of treated units (e.g., Xu,, 2017; Arkhangelsky et al.,, 2021; Ben-Michael et al., 2021b, ; Bai and Ng,, 2021), or assume the normality of error terms (e.g., Fujiki and Hsiao,, 2015; Bai and Ng,, 2021). However, these approaches can not simultaneously meet the following needs in empirical studies.

-

(1)

Inferences do not rely on any specific distributional assumptions (e.g., normality) on the error terms.

-

(2)

Inference are built on small number of post-treatment period, either because the observed post-treatment time span is short or in order to avoid confounding effects from other interventions in longer time span.

-

(3)

Inferences are performed not only for the (cross-sectional or time series) average treatment effect, but also for the treatment effect on every treated unit at each post-treatment period.

To the best of our knowledge, there are only few inferential studies simultaneously satisfy the three conditions above. Abadie et al., (2010) use a cross-sectional permutation strategy, where they apply the synthetic control method to every potential control unit to approximate the true distribution of treatment effect estimator under the null hypothesis of . Obviously, the validity of this permutation approach relies on the cross-sectional exchangeability of the units. Furthermore, if one wants to construct the confidence intervals of the treatment effects in this fashion, then the equality between distributions of outcomes in the absence of and under intervention up to a location shift is required. Chernozhukov et al., 2021a apply time series permutation test to the inference on treatment effects. For a given null hypothesis , they plug into the observed data matrix to compute the full outcome matrix in the absence of intervention, and then perform time series permutations of the residuals from the treated unit to obtain an approximation of the distribution of the test statistic under and the critical value. Confidence intervals can be obtained by grid searching on a set of different values of , which may lead to intensive computation. As the latest work, Cattaneo et al., (2021) build prediction intervals for synthetic control methods on conditional prediction intervals and non-asymptotic concentration. Since concentration inequalities only guarantee lower bounds of coverage probabilities, the proposed prediction intervals may suffer from conservativeness.

This paper aims to provide a theoretically non-conservative and computationally simple inferential procedure for the estimated treatment effects that simultaneously satisfy the above conditions, without imposing the cross-sectional exchangeability assumption. To be more specific, we apply bootstrap method to the treatment effect estimators proposed by Bai and Ng, (2021). Note that Bai and Ng, (2021)’s model keeps a simple factor structure but is quite general in the sense that it allows for multiple treated units and heterogeneous time of intervention. Bootstrapping is one of most commonly used tools to approximate an unknown distribution via resampling, and is shown to be asymptotically valid under mild conditions. We construct bootstrap-based confidence intervals of treatment effects in panel data models with interactive fixed effects. Specifically, we first apply the factor-based matrix completion technique proposed by Bai and Ng, (2021) to obtain point estimators of treatment effects. Then we follow Gonçalves et al., (2017) to approximate the distribution of by (block) wild bootstrap and bootstrap, and use the quantiles of bootstrapped distribution to construct confidence intervals of for every .

Our paper contributes to the literature in the following folds. First, we establish the validity of confidence intervals by proving that they have asymptotically correct coverage probabilities as , and our proposed confidence intervals do not require any specific distributional assumption on and are robust to small number of post-treatment periods. Thus, it is theoretically non-conservative and can meet the three needs for inferential purpose of treatment effects estimation in empirical studies. Second, we extend the bootstrap procedure in Gonçalves et al., (2017) to a more general case. Since Gonçalves et al., (2017) intend to make inference on factor-augmented regression models (Bai and Ng,, 2006) where the factors serves as intermediate variables, they only require valid bootstrap approximations of factors. In this paper, we intend to make inference on the factor model (with missing values) itself, and the estimators involve products of estimated factors, their associated loadings, and a rotation matrix. This implies that we need valid bootstrap approximations of factors, loadings, and the rotation matrix, which creates theoretical challenges. Nevertheless, we successfully establish the asymptotic validity of our proposed bootstrap for such a scenario.

The finite sample properties of proposed bootstrap construction of confidence intervals for estimated treatment effects are investigated through Monte Carlo simulation, using different data generating processes (DGPs) for models with or without exogenous covariates, and for models with heteroscedastic errors or serially correlated errors. The simulation results show that the proposed bootstrap procedure works remarkably well for constructing confidence intervals for estimated treatments. Namely, the empirical coverage ratios are quite close to nominal values in all cases we considered regardless of whether the number of unobserved factors are priorly given or estimated from data.

Finally, we revisit the benefits of political and economic integration of Hong Kong with Mainland China in Hsiao et al., (2012), as well as the effectiveness of the California Tobacco Control Program (CTCP) on per capita cigarettes consumption and personal health expenditures in Abadie et al., (2010). We note that the treatment effects estimated using our new method are of similar magnitudes to those in the literature, while our bootstrap procedure provides reliable confidence intervals showing that the impacts of CTCP were significant over time for both per capita cigarettes consumption and personal health expenditures, and that the impacts of political and economic integration of Hong Kong with Mainland China vanished over time, although significant in the first few years.

The rest of this article is organised as follows. Section 2 establishes the model and the assumptions. Section 3 focuses on the estimation and inference in a model without covariates, and Section 4 deals with a model with covariates. We conduct Monte Carlo simulations in Section 5, and apply our method to classical datasets in Section 6. Section 7 concludes. Mathematical proofs of main results are left to online appendices.

Notations: we introduce some notations that are frequently used throughout this paper. is the set of positive integers. is the identity matrix. denotes the transpose of matrix . For a vector , let be the Euclidean norm of . For a matrix , let be the Frobenius norm of . stands for a normal distribution with mean and variance . And , and denote almost sure convergence, convergence in probability and convergence in distribution, respectively. We let denote a generic finite positive constant, whose value does not depend on or and may vary case by case.

The Model

Suppose there are observations for and . Let the dummy variable indicate the -th unit’s treatment status at time with if under the treatment and if not. The observed data takes the form

| [1] |

where is the latent outcome of unit at time in the absence of treatment, and is the treatment effect on unit at time . For the ease of exposition, we assume for all and for all , where

with and . That is, we assume the last units are intervened by the treatment at time . Therefore, the observed matrix of outcomes is

Note that the above specification can be generated to allow for heterogeneous intervention time periods by letting be the time of the earliest intervention. This is consistent with the definition of in Bai and Ng, (2021) that corresponds to the “largest possible” missing block of the matrix.

We are interested in measuring the treatment effects of the policy intervention for the treated units after time , which are for . Note that measures the difference of the outcomes with and without the intervention of the treatment in the post-treatment periods. Unfortunately, the outcomes with and without the intervention of treatment cannot be simultaneously observed in reality for the same unit at a given time. This is because, once the policy intervention is in effect, then the researchers can only observe , not . Thus, in order to estimate , we need to generate the counterfactual of for , denoted as , and thus the treatment effect can be estimated as

| [2] |

Our goal in this paper is to estimate for when neither treated units nor the post treated periods is large, where the former can be formulated as average treatment effects across units (see Hsiao et al.,, 2022 for the aggregation of multiple treatment effects), and the latter can be formulated as the average treatment effects across post-treatment periods (see Fujiki and Hsiao,, 2015 and Li and Bell,, 2017).

Following the literature of treatment effects estimation using panels (e.g., Abadie et al.,, 2010; Hsiao et al.,, 2012; and Bai and Ng,, 2021), we assume that is generated by the following panel data model with interactive fixed effects:

| [3] |

where is a -dimensional vector of observed covariates of unit at time , is the idiosyncratic error term of unit at time , is an -dimensional time-variant unobserved factor at time , and is an -dimensional individual specific factor loading of unit , where is the number of unobserved factors and is usually unknown to researchers. 222 Even if is unknown in practice, it can be consistently estimated using the method described in Section 4 and 5 of Bai and Ng, (2002) or the method proposed by Alessi et al., (2010), and thus we can treat as known in the theoretical analyses below. This can be formally justified as follows. Let be a parameter in the model of interest and be the estimator of based on estimated number of factors . Note that takes values in , and then the consistency of its estimator implies that as . Therefore,

Let , , and for every . Define , , and . We make the assumptions below.

Assumption 2.1:

The factors and loadings satisfy the following conditions.

-

(1)

for all .

-

(2)

for all .

-

(3)

There exists an positive definite matrix , so that

as , .

-

(4)

There exists an positive definite matrix , so that

as , .

-

(5)

The eigenvalues of are distinct.

Assumption 2.2:

The distributions of the idiosyncratic errors have the following properties.

-

(1)

The idiosyncratic errors have no cross-sectional dependence, i.e., the sequences , , , are mutually independent.

-

(2)

For all , the process is strictly stationary and ergodic.

-

(3)

For all , the cumulative distribution function of is everywhere continuous.

-

(4)

The error terms are independent of the treatment status .

Assumption 2.3:

The moment conditions below hold for the full sample indexed by , the balanced subsample indexed by , the control subsample indexed by , the pre-treatment subsample indexed by , and the missing subsample indexed by .

-

(1)

and for all .

-

(2)

For all ,

-

(3)

-

(4)

For all ,

-

(5)

-

(6)

For all ,

-

(7)

Assumption 2.4:

The factors, loadings and errors satisfy central limit theorems.

-

(1)

For all , there exists an positive definite matrix , so that

as .

-

(2)

For all , there exists an positive definite matrix , so that

as .

Assumption 2.5:

The quantities , , , satisfy the conditions below.

-

(1)

and .

-

(2)

, , , are of the same order, i.e.,

Assumption 2.6:

The conditions below hold for the full sample indexed by , the control subsample indexed by , and the pre-treatment subsample indexed by .

-

(1)

for every .

-

(2)

, where

Assumption 2.7:

The conditions below hold for the full sample indexed by , the control subsample indexed by , and the pre-treatment subsample indexed by .

-

(1)

-

(2)

for all , where is the spectral norm of a matrix.

-

(3)

-

(4)

-

(5)

There exists a positive definite matrix , so that

Assumption 2.8:

is independent of and .

The moment and convergence conditions in Assumptions 2.1, 2.3, 2.4, 2.6, and 2.7 are used to establish probability bounds and asymptotic distributions. They are quite standard in the literature for panel models with interactive fixed effects, see, for example, Bai, (2003), Bai, (2009) and Bai and Ng, (2021), among others. The distribution and order conditions in Assumptions 2.2, 2.5, and 2.8 mainly work for the validity of our bootstrap procedure.

We make further remarks on some of the assumptions. Assumption 2.2(4) requires the strict exogeneity of treatment status, and one can find similar conditions in Assumption 5 of Hsiao et al., (2012) and Assumption 2 of Xu, (2017). Assumption 2.1(3) states that the factors in the pre-treatment subsample and post-treatment subsample have the same asymptotic second sample moment matrices as those in the full sample. Assumption 2.1(4) states that the factor loadings in the control subsample and treated subsample have the same asymptotic second sample moment matrices as those in the full sample. When either or is finite, Assumption 2.1(3) or 2.1(4) can be replaced with equality as in the identifying restriction PC1 on Page 19 of Bai and Ng, (2013) to fulfil the condition that either the factors or factor loadings possess the same properties in the full sample as well as in the post-treatment periods or for the treated units.

Estimation and Inference in a Model without Covariates

To highlight the essence of our approach for estimation and inference of treatment effects, in this section we focus on a special case of Model [3], where there is no covariate (i.e., ) and the model is reduced to a pure approximate factor model:

| [4] |

We will extend our suggested approach to the full model [3] in Section 4.

Estimation of Treatment Effects

Following Bai and Ng, (2021), we consider the factor-based approach to estimate for . Let , , and follow their definitions in Section 2. Since is unobserved for all , the south-east block of is missing in reality. Formally, we define two sub-matrices of :

| [5] |

That is, corresponds to the control subsample, and corresponds to the pre-treatment subsample. Let and be the factor and loading matrices associated with and , respectively. It is easy to see that , , is a sub-matrix formed by the first rows of , and is a sub-matrix formed by the first rows of .

In lieu of Bai and Ng, (2021), we can use the algorithm below to estimate the treatment effects for all .

Algorithm 3.1:

Treatment effect estimation via factor-based matrix completion (without covariates).

-

1.

Perform a singular value decomposition of , and let be an diagonal matrix with the largest singular values of on the diagonal in descending order. Then let and be and matrices containing the left and right singular vectors of respectively, corresponding to . Compute

[6] -

2.

Perform a singular value decomposition of , and let be an diagonal matrix with the largest singular values of on the diagonal in descending order. Then let and be and matrices containing the left and right singular vectors of respectively, corresponding to . Compute

[7] -

3.

Let be the first rows of . Compute

[8] and then let .

-

4.

Let denote the -th entry of , then compute the residuals for .

-

5.

For , the variance of is estimated by

[9] where

[10] with and as .

-

6.

For every , compute .

-

7.

For , the estimated treatment effect is , and the standard error of is .

Remark 3.1:

Since for every , it is asymptotically negligible in the standard error of . Here we include in the standard error of to improve finite sample performance.

Remark 3.2:

In the above algorithm, we discuss the estimation for individual treatment effects for each treated unit. If the interest is the average treatment effects (ATE) across treated units or across post-treatment periods, not individual treatment effects, see Hsiao et al., (2022) for discussion of the aggregation of multiple treatment effects across treated units, and see Fujiki and Hsiao, (2015) and Li and Bell, (2017) for discussion of the average treatment effects over post-treatment periods.

Construction of Confidence Intervals

When neither nor is large, the average treatment effects either across treated units or post-treatment periods may not be a good measure for inferential purpose since it is hard to establish the asymptotic properties of such effects. In order to provide inferential procedure for individual treatment effects especially when neither nor is large, motivated by Gonçalves et al., (2017), we adapt bootstrap method to construct the confidence intervals of for , without a specific distributional assumption on the error term or particular quantity on or .

Algorithm 3.2:

Confidence intervals of the treatment effects via bootstrap (without covariates).

-

1.

Apply Algorithm 3.1 to the sample and obtain , , , and .

-

2.

For :

-

(1)

For , let , where are i.i.d. or block i.i.d. from a standard normal distribution and are independent of the raw sample.

-

(2)

For , let be independently drawn from a discrete uniform distribution on the set , where .

-

(3)

For , let . Use to construct and in the same fashion as Equation [5].

-

(4)

Apply Algorithm 3.1 to the bootstrapped sample and , and obtain , , and .

-

(5)

For , compute

[11]

-

(1)

-

3.

In the previous step, we generate statistics denoted by for every . Let be the empirical quantile of , and let be the empirical quantile of .

-

4.

For , the equal tailed confidence interval of is

[12] and the symmetric confidence interval of is

[13]

Remark 3.3:

As is shown in the proof of Theorem 3.1, the distribution of is dominated by and the effect of is asymptotically negligible. However, the bootstrap procedure above takes into consideration in order to improve the finite sample performances.

Remark 3.4:

When the error terms are suspected of having serial correlation, a block wild bootstrap can be used to address this issue (e.g., Gonçalves et al.,, 2017). That is, a for block width , we let for every and such that in Step 2(1).

Under Assumptions 2.1–2.5 in this paper, the asymptotic properties of the bootstrapped confidence intervals [12] and [13] are summarized in the following theorem.

From Theorem 3.1, we can conclude that the bootstrap confidence intervals will provide a correct coverage for the estimated treatment effects in the post-treatment periods, and thus one could conduct statistical inference about the treatment effects based on the bootstrap confidence intervals. It also worths noting that even if our bootstrap procedure follows the idea of Gonçalves et al., (2017), the proof of bootstrap validity becomes quite complicated due to the differences in purposes and model specifications. Since Gonçalves et al., (2017) intend to make inference on factor-augmented regression models (Bai and Ng,, 2006) where the factors serves as intermediate variables, they only require valid bootstrap approximations of factors. In this paper, we intend to make inference on the factor model (with missing values) itself, and the estimators involve products of estimated factors, their associated loadings, and a rotation matrix. This implies that we need valid bootstrap approximations of factors, loadings, and the rotation matrix, which leads to laborious works.

Estimation and Inference in a Model with Covariates

In the above section, we discussed the estimation of the treatment effects and associated bootstrap confidence intervals for a pure factor model. Besides the unobserved factors, in practice, the outcome variable could also be affected by some exogenous regressors. To accommodate such a scenario, we extend the factor-based approach to a model with covariates, i.e., Model [3] in Section 2.

Estimation of Treatment Effects

For a factor model with covariates, i.e., a panel data model with interactive fixed effect, our estimation strategies involve an interactive fixed effect estimation (IFEE), which is described and studied in Bai, (2009). If were fully observed, we could directly use IFEE to estimate Model [3]. The general framework of IFEE is summarised in the algorithm to follow.

Algorithm 4.1:

Interactive fixed effect estimation.

-

1.

Input arguments. , a matrix. , a matrix, where is a matrix for every .

-

2.

Compute the starting value

[15] -

3.

Perform the following iteration until for some , where is a sufficiently small positive number.

-

(1)

Let

[16] -

(2)

Perform a singular value decomposition of the matrix , and let be an diagonal matrix with the largest singular values of on the diagonal in descending order. Then let and be and matrices containing the left and right singular vectors of corresponding to .

-

(3)

Let and .

-

(4)

Let

[17]

-

(1)

-

4.

Output arguments. , , and .

Now we turn to the estimation of treatment effect when are not observable. Let , , , , , , , , , and follow their definitions in Sections 2 and 3. Let , , and to be a sub-matrix formed by the first rows of .

Then we can use the algorithm below to estimate the treatment effects for all .

Algorithm 4.2:

Treatment effect estimation via factor-based matrix completion (with covariates).

-

1.

Apply Algorithm 4.1 to , and obtain , and .

-

2.

Apply Algorithm 4.1 to , and obtain and .

-

3.

Let be the first rows of . Compute

[18] and then let .

-

4.

Let denote the -th entry of , then compute the residuals for .

-

5.

For , the variance of is estimated by

[19] where

[20] with and as .

-

6.

For every , compute .

-

7.

For , the estimated treatment effect is , and the standard error of is .

Remark 4.1:

Because

| [21] |

for every , the variance of is comprised of , and . In spirit of Remark 3.1, we should include an estimate of in the standard error of to improve the finite sample performances. However, by Theorem 3 of Bai, (2009), , which is of higher order than for . Furthermore, a consistent estimation of is quite complicated. As a result of the cost-benefit trade-off, we do not include an estimate of in the standard error of .

Construction of Confidence Intervals

For the estimated for , we shall again use the bootstrap procedure discussed above to construct their confidence intervals.

Algorithm 4.3:

Confidence intervals of the treatment effects via bootstrap (with covariates).

-

1.

Apply Algorithm 4.2 to the sample and obtain , , , and .

-

2.

For :

-

(1)

For , let , where are i.i.d. or block i.i.d. from a standard normal distribution and are independent of the raw sample.

-

(2)

For , let be independently drawn from a discrete uniform distribution on the set , where .

-

(3)

For , let . Use to construct and in the same fashion as Equation [5].

-

(4)

Apply Algorithm 3.1 to the bootstrapped sample and , and obtain , , and .

-

(5)

For , compute

[22]

-

(1)

-

3.

In the previous step, we generate statistics denoted by for every . Let be the empirical quantile of , and let be the empirical quantile of .

-

4.

For , the equal tailed confidence interval of is

[23] and the symmetric confidence interval of is

[24]

Remark 4.2:

By Equation [21] and in spirit of Remark 3.3, a bootstrap procedure should take the distributions of all the 3 terms , and into consideration to ensure the finite sample performances. But in Algorithm 4.3, resampled observations are generated by a pure factor model and only the interactive fixed effects are estimated in every bootstrapped sample. Thus the bootstrap procedure only approximates the distribution of , ignoring the effect of . The underlying rationale is also a cost-benefit trade-off mentioned in Remark 4.1. On the one hand, by Bai, (2009) and Bai and Ng, (2021), we have and as for every . On the other hand, the computation of interactive fixed effect estimation is far more intensive than that of estimating a pure factor model. These two facts motivate us to ignore the effect of in the bootstrap procedure. Furthermore, evidence from Section 5 shows the current bootstrap procedure has already yielded satisfactory finite sample performances.

Remark 4.3:

If the error terms are suspected of having serial correlation, we suggest to use block wild bootstrap in Step 2(1). See Remark 3.4 for details.

As above, we can establish the validity of the proposed confidence intervals [23] and [24] in the sense that they have asymptotically correct coverage probabilities as .

Theorem 4.1 suggests that we can apply the proposed bootstrap procedure to conduct statistical inference for estimated treated effects from a panel with interactive fixed effects model.

Simulation Studies

In this section, we conduct several Monte Carlo experiments to investigate the finite sample properties of the proposed confidence intervals. 333MATLAB codes for simulation are available from the authors upon request.

In the data generating processes below, we assume that the common factors are i.i.d. as , and the factor loadings are also i.i.d. as . For the model with covariates, we assume that the covariates are i.i.d. as , where each entry of the matrix is drawn from . Let . We consider the following data generating processes. 444We also consider AR(1) factors, exponentially distributed errors, other variance structures, and dependence between factors and covariates. These results are available from the authors upon request.

-

•

DGP1: Model without covariates, .

-

•

DGP2: Model with covariates, .

The error term is defined as

| [26] |

where and are i.i.d. drawn from . We specify two variance structures of .

-

•

Case 1: and .

-

•

Case 2: are i.i.d. drawn from , and are i.i.d. drawn from .

Moreover, we consider the following marginal distributions of .

-

•

Margin 1: .

-

•

Margin 2: .

For demonstration, we assume there is only one treated unit and post-treatment periods. The treatment effects are assumed to be constants equal to 1, i.e., for . The number of control units and the number of pre-treatment periods . We construct the and , equal-tailed and symmetric confidence intervals for , . In Step 2(1) of Algorithms 3.2 and 4.3, we use ordinary wild bootstrap procedure for Case 1, and block wild bootstrap procedure with block width equal to 4 for Case 2. The number of factors is either treated as known or estimated using the method of Bai and Ng, (2002). For computational simplicity, a warp-speed method (Giacomini et al.,, 2013) is applied with 2000 replications for each scenario. We report the coverage rates (in percent) of confidence intervals in Tables 1–8. In these tables, EQ stands for equal-tailed confidence intervals and SY stands for symmetric confidence intervals.

Several interesting findings can be observed from the simulation results. On the first hand, the results in Table 1–4 clearly show that the empirical coverage ratio for treatment effects from a pure factor model is quite close to the nominal values (both 90% and 95% level) when the post-treatment period is short, regardless of whether the idiosyncratic errors are heteroscedastic or serially correlated, or whether the number of unobserved factors is known or estimated from the data. On the other hand, when exogenous covariates are included for treatment effects estimation, Tables 5–8 also show that our proposed bootstrapped confidence intervals are able to provide accurate coverage ratios for the estimated treatment effects in a panel model with exogenous regressors and with heteroscedastic or serially correlated errors. In general, the simulation results confirm the validity of our proposed bootstrap procedure in providing accurate and robust confidence intervals for estimated treatment effects using a panel with interactive fixed effects.

| Known number of factors, CI | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | |

| Known number of factors, CI | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | |

| Estimated number of factors, CI | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | |

| Estimated number of factors, CI | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | |

| Known number of factors, CI | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | |

| Known number of factors, CI | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | |

| Estimated number of factors, CI | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | |

| Estimated number of factors, CI | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | |

| Known number of factors, CI | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | |

| Known number of factors, CI | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | |

| Estimated number of factors, CI | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | |

| Estimated number of factors, CI | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | |

| Known number of factors, CI | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | |

| Known number of factors, CI | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | |

| Estimated number of factors, CI | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | |

| Estimated number of factors, CI | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | |

| Known number of factors, CI | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | |

| Known number of factors, CI | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | |

| Estimated number of factors, CI | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | |

| Estimated number of factors, CI | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | |

| Known number of factors, CI | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | |

| Known number of factors, CI | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | |

| Estimated number of factors, CI | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | |

| Estimated number of factors, CI | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | |

| Known number of factors, CI | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | |

| Known number of factors, CI | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | |

| Estimated number of factors, CI | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | |

| Estimated number of factors, CI | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | |

| Known number of factors, CI | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | |

| Known number of factors, CI | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | |

| Estimated number of factors, CI | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | |

| Estimated number of factors, CI | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | EQ | SY | |

Empirical Applications

In this section, we re-evaluate the impacts of Hong Kong’s Political and Economic Integration with Mainland China as well as the effects of California’s Tobacco Control Program using our proposed bootstrap procedure. 555MATLAB, Python and R codes for application are available from the authors upon request.

Hong Kong’s Political and Economic Integration with Mainland China Revisited

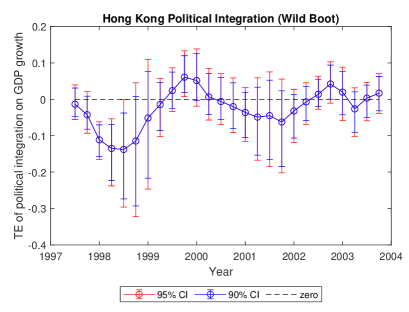

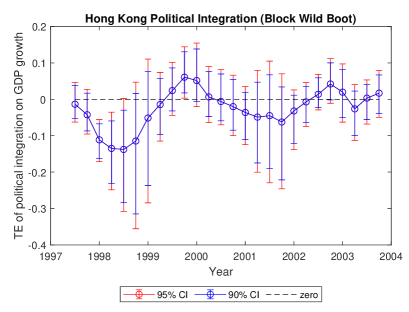

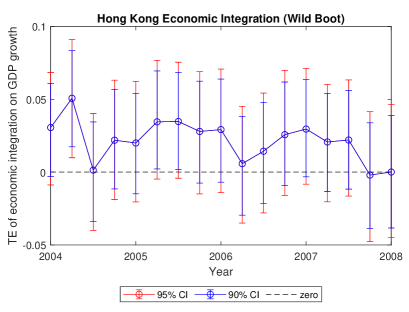

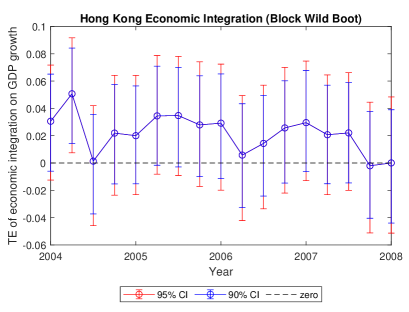

In this subsection, we revisit the impacts of political and economic integration of Hong Kong with Mainland China, which has been analysed in Hsiao et al., (2012). Since Hsiao et al., (2012) specify a pure factor model without covariates, we apply the methods in Section 3 of this paper to the dataset of Hsiao et al., (2012). For the results about political integration, quarterly real GDP growth rates from 1993Q1 to 1997Q2 of 10 countries and districts are used to form the counter-factual path of Hong Kong from 1997Q3 up to 2003Q4. The 10 countries and districts are Mainland China, Indonesia, Japan, Korea, Malaysia, Philippines, Singapore, Taiwan, Thailand and US. For the analysis of economic integration, quarterly real GDP growth rates of 24 countries and districts from 1993Q1 to 2003Q4 are used to form counter-factual path of Hong Kong from 2004Q1 to 2008Q1.

The results for the impact of political integration and economic integration with Mainland China on Hong Kong’s economic growth are provided in 1 and 2, respectively.

As is shown in Figure 1, the estimated treatment effects of Hong Kong political integration are of similar magnitudes and patterns as those in Hsiao et al., (2012). In Figure 2, the estimated treatment effects of Hong Kong economic integration are positive, as in Hsiao et al., (2012), and confidence intervals cover 0 in most of the periods. This suggests that the impact of political and economic integration of Hong Kong with Mainland China is significant in the first few years after integration, and vanishes afterward. This observation is in general consistent with the insignificant average treatment effects across post-treatment periods in Hsiao et al., (2012).

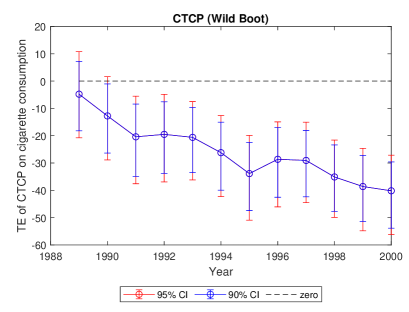

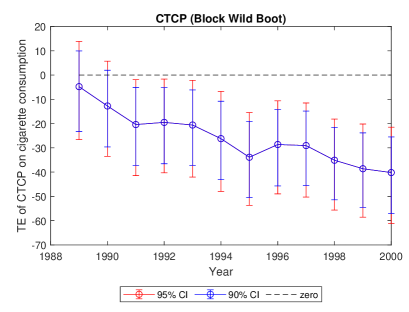

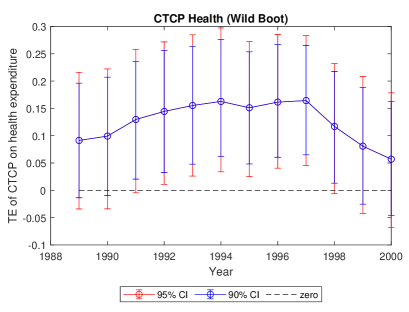

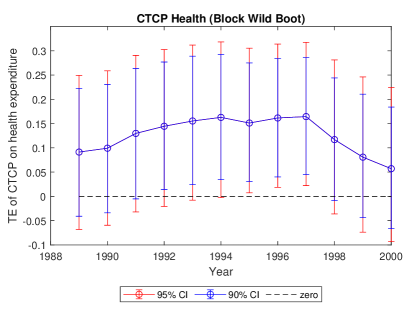

California’s Tobacco Control Program Revisited

Now we revisit the effectiveness of CTCP on per capita cigarettes consumption and personal healthcare expenditures using the methods discussed in Section 4 of this article. In November 1988, California passed the Proposition 99, which increased California’s cigarettes tax by 25 cents per pack and earmarked the tax revenue for health and anti-smoking measures. Proposition 99 triggered a wave of local clean-air ordinances in California. Abadie et al., (2010) used the synthetic control method for the period 1970-2000 to show that the California Tobacco Control Program had a significant impact on per capita cigarette consumption for the period 1989-2000, and that its impact continued to be enhanced over time.

Note that in the model and dataset of Abadie et al., (2010), covariates do not change over time, which violates Assumption 2.6(2) of this study. To accommodate time-variant covariates, we use the dataset of Hsiao and Zhou, (2019), who also revisit the impact of CTCP on per capita cigarettes consumption and personal healthcare expenditures but use a set of time-variant covariates: per capita GDP obtained from Abadie et al., (2010); poverty rates obtained from the National Census Bureau; educational attainment, defined as the percentage of obtaining college degree of population 25 years and over, obtained from the National Census Bureau.

In our analysis, the number of factors is estimated using the method proposed by Alessi et al., (2010), which shows better performance than Bai and Ng, (2002) in this and the next applications. Both ordinary wild bootstrap procedure and block wild bootstrap procedure with block width equal to 3 are considered, and equal tailed confidence intervals are reported. The results for the impact of CTCP on per capita cigarette consumption and personal healthcare expenditures are provided in 3 and 4, respectively.

Figure 3 shows that the estimated treatment effects are of similar magnitudes as those in Abadie et al., (2010); and that the confidence intervals indicate negative and significant impacts over time, consistent with their findings using permutation tests. Figure 4 shows that the estimated treatment effects of CTCP on health expenditure are of similar magnitudes as reported in Hsiao and Zhou, (2019). Consistent with their findings, confidence intervals indicate that the effects are short-lived. In both figures, we can see that the confidence intervals based on ordinary and block wild bootstrap procedures produce similar results.

Conclusion

In this paper, we consider the construction of confidence intervals for treatment effects estimated in panel models with interactive fixed effects, which serves as an alternative inferential approach. We first use the factor-based matrix completion technique proposed by Bai and Ng, (2021) for panel models to estimate the treatment effects, and then use bootstrap method to construct confidence intervals of the treatment effects for treated units at each post-treatment period. Our construction of confidence intervals requires neither specific distributional assumptions on the error terms nor large number of post-treatment periods. We also establish the validity of proposed bootstrap procedure that these confidence intervals have asymptotically correct coverage probabilities. Simulation studies show that these confidence intervals have satisfactory finite sample performances, and empirical applications using classical datasets yield treatment effect estimates of similar magnitude and reliable confidence intervals.

References

- Abadie, (2021) Abadie, A. (2021). Using synthetic controls: Feasibility, data requirements, and methodological aspects. Journal of Economic Literature, 59(2):391–425.

- Abadie et al., (2010) Abadie, A., Diamond, A., and Hainmueller, J. (2010). Synthetic control methods for comparative case studies: Estimating the effect of California’s tobacco control program. Journal of the American Statistical Association, 105(490):493–505.

- Abadie and Gardeazabal, (2003) Abadie, A. and Gardeazabal, J. (2003). The economic costs of conflict: A case study of the Basque Country. American Economic Review, 93(1):113–132.

- Abadie and L’Hour, (2021) Abadie, A. and L’Hour, J. (2021). A penalized synthetic control estimator for disaggregated data. Journal of the American Statistical Association, 116(536):1817–1834.

- Alessi et al., (2010) Alessi, L., Barigozzi, M., and Capasso, M. (2010). Improved penalization for determining the number of factors in approximate factor models. Statistics & Probability Letters, 80(23-24):1806–1813.

- Amjad et al., (2018) Amjad, M., Shah, D., and Shen, D. (2018). Robust synthetic control. The Journal of Machine Learning Research, 19(1):802–852.

- Arkhangelsky et al., (2021) Arkhangelsky, D., Athey, S., Hirshberg, D. A., Imbens, G. W., and Wager, S. (2021). Synthetic difference in differences. NBER working paper 25532.

- Athey et al., (2021) Athey, S., Bayati, M., Doudchenko, N., Imbens, G., and Khosravi, K. (2021). Matrix completion methods for causal panel data models. Journal of the American Statistical Association, 116(536):1716–1730.

- Bai, (2003) Bai, J. (2003). Inferential theory for factor models of large dimensions. Econometrica, 71(1):135–171.

- Bai, (2009) Bai, J. (2009). Panel data models with interactive fixed effects. Econometrica, 77(4):1229–1279.

- Bai and Ng, (2002) Bai, J. and Ng, S. (2002). Determining the number of factors in approximate factor models. Econometrica, 70(1):191–221.

- Bai and Ng, (2006) Bai, J. and Ng, S. (2006). Confidence intervals for diffusion index forecasts and inference for factor-augmented regressions. Econometrica, 74(4):1133–1150.

- Bai and Ng, (2013) Bai, J. and Ng, S. (2013). Principal components estimation and identification of static factors. Journal of Econometrics, 176(1):18–29.

- Bai and Ng, (2021) Bai, J. and Ng, S. (2021). Matrix completion, counterfactuals, and factor analysis of missing data. Journal of the American Statistical Association, 116(536):1746–1763.

- (15) Ben-Michael, E., Feller, A., and Rothstein, J. (2021a). The augmented synthetic control method. Journal of the American Statistical Association, 116(536):1789–1803.

- (16) Ben-Michael, E., Feller, A., and Rothstein, J. (2021b). Synthetic controls with staggered adoption. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 0(0):1–31.

- Bickel and Freedman, (1981) Bickel, P. J. and Freedman, D. A. (1981). Some asymptotic theory for the bootstrap. The Annals of Statistics, 9(6):1196–1217.

- Candès and Plan, (2010) Candès, E. J. and Plan, Y. (2010). Matrix completion with noise. Proceedings of the IEEE, 98(6):925–936.

- Candès and Recht, (2009) Candès, E. J. and Recht, B. (2009). Exact matrix completion via convex optimization. Foundations of Computational Mathematics, 9:717–772.

- Cattaneo et al., (2021) Cattaneo, M. D., Feng, Y., and Titiunik, R. (2021). Prediction intervals for synthetic control methods. Journal of the American Statistical Association, 116(536):1865–1880.

- Chang and Park, (2003) Chang, Y. and Park, J. Y. (2003). A sieve bootstrap for the test of a unit root. Journal of Time Series Analysis, 24(4):379–400.

- Cheng and Huang, (2010) Cheng, G. and Huang, J. Z. (2010). Bootstrap consistency for general semiparametric M-estimation. The Annals of Statistics, 38(5):2884–2915.

- (23) Chernozhukov, V., Wüthrich, K., and Zhu, Y. (2021a). An exact and robust conformal inference method for counterfactual and synthetic controls. Journal of the American Statistical Association, 116(536):1849–1864.

- (24) Chernozhukov, V., Wuthrich, K., and Zhu, Y. (2021b). A -test for synthetic controls. arXiv:1812.10820v6.

- Fujiki and Hsiao, (2015) Fujiki, H. and Hsiao, C. (2015). Disentangling the effects of multiple treatments—measuring the net economic impact of the 1995 great Hanshin-Awaji earthquake. Journal of Econometrics, 186(1):66–73.

- Gamarnik and Misra, (2016) Gamarnik, D. and Misra, S. (2016). A note on alternating minimization algorithm for the matrix completion problem. IEEE Signal Processing Letters, 23(10):1340–1343.

- Giacomini et al., (2013) Giacomini, R., Politis, D. N., and White, H. (2013). A warp-speed method for conducting Monte Carlo experiments involving bootstrap estimators. Econometric Theory, 29(3):567–589.

- Gonçalves and Perron, (2014) Gonçalves, S. and Perron, B. (2014). Bootstrapping factor-augmented regression models. Journal of Econometrics, 182(1):156–173.

- Gonçalves et al., (2017) Gonçalves, S., Perron, B., and Djogbenou, A. (2017). Bootstrap prediction intervals for factor models. Journal of Business & Economic Statistics, 35(1):53–69.

- Hsiao et al., (2012) Hsiao, C., Ching, H. S., and Wan, S. K. (2012). A panel data approach for program evaluation: Measuring the benefits of political and economic integration of Hong Kong with mainland China. Journal of Applied Econometrics, 27(5):705–740.

- Hsiao et al., (2022) Hsiao, C., Shen, Y., and Zhou, Q. (2022). Multiple treatment effects in panel-heterogeneity and aggregation. Advances in Econometrics , 43(B):81–101.

- Hsiao and Zhou, (2019) Hsiao, C. and Zhou, Q. (2019). Panel parametric, semiparametric, and nonparametric construction of counterfactuals. Journal of Applied Econometrics, 34(4):463–481.

- Kellogg et al., (2021) Kellogg, M., Mogstad, M., Pouliot, G. A., and Torgovitsky, A. (2021). Combining matching and synthetic control to tradeoff biases from extrapolation and interpolation. Journal of the American Statistical Association, 116(536):1804–1816.

- Kim and Oka, (2014) Kim, D. and Oka, T. (2014). Divorce law reforms and divorce rates in the usa: an interactive fixed-effects approach. Journal of Applied Econometrics, 29(2):231–245.

- Li, (2020) Li, K. T. (2020). Statistical inference for average treatment effects estimated by synthetic control methods. Journal of the American Statistical Association, 115(532):2068–2083.

- Li and Bell, (2017) Li, K. T. and Bell, D. R. (2017). Estimation of average treatment effects with panel data: Asymptotic theory and implementation. Journal of Econometrics, 197(1):65–75.

- Masini and Medeiros, (2021) Masini, R. and Medeiros, M. C. (2021). Counterfactual analysis with artificial controls: Inference, high dimensions, and nonstationarity. Journal of the American Statistical Association, 116(536):1773–1788.

- Mazumder et al., (2010) Mazumder, R., Hastie, T., and Tibshirani, R. (2010). Spectral regularization algorithms for learning large incomplete matrices. The Journal of Machine Learning Research, 11:2287–2322.

- Moon and Weidner, (2015) Moon, H. R. and Weidner, M. (2015). Linear regression for panel with unknown number of factors as interactive fixed effects. Econometrica, 83(4):1543–1579.

- Ouyang and Peng, (2015) Ouyang, M. and Peng, Y. (2015). The treatment-effect estimation: A case study of the 2008 economic stimulus package of China. Journal of Econometrics, 188(2):545–557.

- Park, (2003) Park, J. Y. (2003). Bootstrap unit root tests. Econometrica, 71(6):1845–1895.

- Pesaran, (2006) Pesaran, M. H. (2006). Estimation and inference in large heterogeneous panels with a multifactor error structure. Econometrica, 74(4):967–1012.

- van der Vaart, (1998) van der Vaart, A. W. (1998). Asymptotic Statistics. Cambridge University Press.

- Xu, (2017) Xu, Y. (2017). Generalized synthetic control method: Causal inference with interactive fixed effects models. Political Analysis, 25(1):57–76.

Confidence Intervals of Treatment Effects in Panel Data Models

with Interactive Fixed Effects

Online Supplementary Appendices

| Xingyu Li | Yan Shen |

| National School of Development | National School of Development |

| Peking University | Peking University |

| x.y@pku.edu.cn | yshen@nsd.pku.edu.cn |

Qiankun Zhou

Department of Economics

Louisiana State University

qzhou@lsu.edu

The online appendices include auxiliary lemmas, technical notes, and the proofs of Theorems 3.1 and 4.1. We first list some results for estimators and the associated residuals in panel models with interactive effects, and then provide the technical properties of bootstrap procedure. Finally, we use the above mentioned results to prove the theorems in the main paper.

Appendix A Properties of Estimators and Residuals

The lemmas in this section are cited or derived from some of the results in Bai, (2003), Bai, (2009), Gonçalves and Perron, (2014), and Bai and Ng, (2021). Note that Assumptions 2.1–2.8 of this paper are sufficient for Assumptions A–G of Bai, (2003), Assumptions A–E of Bai, (2009), panel factor model relevant conditions of Assumptions 1–5 of Gonçalves and Perron, (2014), and Assumptions A–D of Bai and Ng, (2021).

Estimators and Residuals in Section 3

We introduce some notations. Let and . Define rotation matrices

Lemma A.1:

-

(1)

and , where is the diagonal matrix consisting of the eigenvalues of , or equivalently, the eigenvalues of .

-

(2)

, , , and , where is the diagonal matrix consisting of the eigenvalues of , and is the corresponding eigenvector matrix such that .

-

(3)

for every .

-

(4)

for every .

-

(5)

, and .

-

(6)

Proof: Claim (1) is obtained by Lemma A.3(1) of Bai, (2003) (applied to the control subsample and pre-treatment subsample) and Assumption 2.1(3)(4) of this paper. Claim (2) follows from Proposition of Bai, (2003) (applied to the control subsample and pre-treatment subsample), Assumption 2.1(3)(4) of this paper, and the continuous mapping theorem. Note that Assumption 2.5(2) implies and as . Then applying Theorem 1(i) to the control subsample yields Claim (3), and applying Theorem 2(i) to the pre-treatment subsample yields Claim (4). The first part of Claim (5) is borrowed from Lemma A.1(i) of Bai and Ng, (2021), and the second part is by the first part and Claim (2). Claim (6) is obtained by applying Lemma A.1 of Bai, (2003) to the control subsample and pre-treatment subsample. ∎

For ease of citation, we state the inequality here. For and , we have

Proof: Let for every . By the proof of Theorem 2 of Bai, (2003) (applied to the pre-treatment subsample), for every , we have the following decomposition

where

By the triangle inequality and Cauchy-Schwartz inequality,

By Assumption 2.3(1),

Then Markov’s inequality implies that . By Lemma A.1(6) and Assumption 2.5(2),

From Assumption 2.3(5),

By the properties of matrix norms, the triangle inequality, Lemma A.1(2) and Markov’s inequality,

Applying Lemma B.3 of Bai, (2003) to the pre-treatment subsample yields

Then by the definition and property of Frobenius norm, Lemma A.1(2), Assumption 2.1(4) and 2.5(2),

Therefore, by the properties of matrix norms, the inequality and Lemma A.1(2),

Similarly we can show that

By the properties of matrix norms, the inequality, Lemma A.1(2) and Assumption 2.5(2),

which proves the conclusion. ∎

Lemma A.3:

-

(1)

-

(2)

-

(3)

-

(4)

-

(5)

-

(6)

-

(7)

-

(8)

-

(9)

-

(10)

Proof: Firstly, we prove Claims (1) and (2) with . By Assumptions 2.1(1)(2) and 2.3(1), we have , , and for every and every . Note that although Lemma C.1 of Gonçalves and Perron, (2014) requires their Assumptions 1–5, only the panel factor model relevant conditions of their Assumptions 1–5 are actually used, and these panel factor model relevant conditions automatically hold under Assumptions 2.1–2.5 of this paper. Then Claims (1) and (2) with are obtained by applying Lemma C.1 (i) and (ii) of Gonçalves and Perron, (2014) to the control subsample and pre-treatment subsample.

Claim (1) with follows from Lemma A.1(6) and the fact that is trivially . For , we use Lemma A.1(6) and Assumption 2.5(2) to conclude that

which in turn implies that

holds for any integer . Then Claim (1) with follows from the relationship between and . Claim (2) with can be proved analogously using some facts in the proof of Lemma A.2.

For every , Assumption 2.1(1) implies that

By the inequality, the properties of matrix norms, Markov’s inequality, Lemma A.1(2) and the first part of Claim (1),

which establishes the first part of Claim (3). The second part and Claim (4) can be proved analogously.

To prove Claims (5)–(10), we perform the following decomposition of for every .

| [27] |

By the inequality and properties of matrix norms,

Lemma A.1(5) implies that . By Assumptions 2.1(1)(2), 2.3(1) and Markov’s inequality,

Then Claims (5)–(10) follow from Claims (1)(2), Lemma A.1(2)(5), Assumption 2.5(2), and above facts. ∎

Proof: Firstly consider the case of By Equation [27], the inequality and the properties of matrix norms,

And the conclusion follows from Assumptions 2.1(1)(2), 2.5(2), Markov’s inequality, and Lemma A.1(2)(4)(5)(6).

For the case of , the result for the case of implies that

which in turn implies that

for every integer . ∎

Estimators and Residuals in Section 4

In this subsection, we show that adding covariates into the panel factor model does not alter the conclusions in Subsection A.1. Now , , and are estimated by Algorithm 4.1 (interactive fixed effect estimation), and

Other quantities follow their definitions in Subsection A.1.

Lemma A.5:

Proof: By Remark 5 of Bai, (2009), estimation of does not affect the rates of convergence and the limiting distributions of the estimated factors and loadings, so they are the same as those of a pure factor model. Since Lemmas A.1, A.2 and A.3(1)–(4) are asymptotic properties of the estimated factors and loadings in a pure factor model, they can be naturally extended to a factor model with covariates. ∎

Lemma A.6:

Proof: Applying Theorem 1 of Bai, (2009) to the control subsample yields

| [28] |

Now for every , admits a decomposition

For every , by the inequality and properties of matrix norms,

Furthermore,

Assumption 2.6(1) and Markov’s inequality imply that for every ,

Then the conclusions follow from above results, the arguments in the proofs of Lemmas A.3(5)–(10), A.4, and A.5. ∎

Appendix B Properties of Bootstrap

As is described in Step 2 of Algorithm 4.3 and explained in Remark 4.2, the bootstrap is conducted within a pure factor framework even for a factor model with covariates (i.e., the model in Section 4). By the construction of resampled observations and Lemma A.5, A.6, it follows that the properties of bootstrap quantities in Section 4 under Assumptions 2.1–2.8 are identical to those in Section 3 under Assumptions 2.1–2.5. Therefore, unless clarifying assumptions, we do not distinguishing between a pure factor model and a factor model with covariates in this section.

Moreover, since the proof of (ordinary) wild bootstrap can be straightforwardly extended to block wild bootstrap with extra notations, we provide the results for (ordinary) wild bootstrap procedure in what follows to save space.

Technical Notes

This subsection introduces some basic concepts and results of bootstrap asymptotic analysis. Let be the raw sample, i.e., for a pure factor model and for a factor model with covariates. For simplicity of notation, we omit the subscript and just write in stead of . Define and to be the conditional probability and expectation given , i.e., and . The conditional variance and conditional covariance are defined analogously.

For a bootstrap statistic , we say that is of an order in probability, denoted by , if and only if for any and ,

We say that is of an order in probability, denoted by , if and only if for any , there exists a such that

For a sequence of deterministic numbers ,

One can also see Pages 2891–2892 and Appendix A.1 of Cheng and Huang, (2010) for measure-theoretic definitions of bootstrap stochastic orders and relevant measurability issues.

The lemmas below list some properties of bootstrap stochastic orders that are frequently used in subsequent analyses.

Lemma B.1:

Let be a bootstrap statistic. If , then . If , then .

Proof: See the first paragraph on Page 387 of Chang and Park, (2003). ∎

Lemma B.2:

Suppose , , , , , and . Then

-

(1)

, and .

-

(2)

, and .

-

(3)

, and .

-

(4)

, and .

-

(5)

, , and .

-

(6)

, , and .

Proof: These results follow from the last a few lines on Page 1861 of Park, (2003), Lemma 1 of Chang and Park, (2003), and Lemma 3 of Cheng and Huang, (2010). ∎

Now we introduce the definition of conditional convergence in distribution. For a bootstrap statistic and a random element taking values in a metric space , we say that conditionally converges in distribution to (or equivalently, the conditional distribution of weakly converges to that of ) in probability, denoted by , if and only if for every bounded Lipschitz continuous function , we have as . The lemmas below list some properties of conditional convergence in distribution that are frequently used in subsequent analyses.

Lemma B.3:

If and , then and .

Proof: See Remark 2 of Chang and Park, (2003). ∎

Lemma B.4:

Suppose that the bootstrap statistic and random variable take their values in , and as . Let denote the conditional cumulative distribution function of , and denote the cumulative distribution function of , i.e., and for every . Then as for every , where is the set of all continuous points of . Moreover, if is everywhere continuous on , i.e., , then

Proof: For any and any , the distance between and is measured by

For any open set , construct a sequence of functions , so that for every . It is easy to see that is non-negative, bounded, and Lipschitz continuous with Lipschitz constant for every , and as . By the monotone convergence theorem,

Hence for any , there exists an , such that . Since , it follows that almost surely. By the boundedness and Lipschitz continuity of and the definition of conditional convergence in distribution, , which implies that

For any closed set , because is an open set, the above result implies that

Now consider any Borel set with , where and denote the closure and interior of a set, respectively. Then it follows that

which implies that as .

For any , let , then is Borel and satisfies . Therefore,

as .

If is everywhere continuous, i.e., , then for any , there exist , so that for every . Then for any ,

which implies that

For any , pick a such that . Since , we have

and the proof is complete. ∎

Ancillary Results about Bootstrap Samples

Let , and . Analogously to the population version, define , , to be a sub-matrix formed by the first rows of , and to be a sub-matrix formed by the first rows of . Then let be defined in Step 2(1)(2) of Algorithms 3.2 and 4.3.

Lemmas B.5–B.9 below verify (some of) the bootstrap high level conditions in Gonçalves and Perron, (2014) and Gonçalves et al., (2017). Lemma B.5 corresponds to Condition A*(b) of Gonçalves and Perron, (2014) and Condition A.1 of Gonçalves et al., (2017).

Lemma B.5:

If Assumptions 2.1–2.5 hold for a pure factor model or Assumptions 2.1–2.8 hold for a factor model with covariates, then as ,

-

(1)

For every ,

-

(2)

Proof: Since are i.i.d. from , it follows that . By the independence between and the raw sample, and Lemma A.3(8),

Moreover, by the inequality and Lemma A.3(9),

and the proof is complete. ∎

Lemma B.6 corresponds to Condition A*(c) of Gonçalves and Perron, (2014) and Condition A.2 of Gonçalves et al., (2017).

Lemma B.6:

If Assumptions 2.1–2.5 hold for a pure factor model or Assumptions 2.1–2.8 hold for a factor model with covariates, then as ,

-

(1)

For every ,

-

(2)

Proof: Because are i.i.d. as and independent of the raw sample, we have that and are conditionally independent given the sample whenever or , and . Then by Cauchy-Schwarz inequality, the inequality, and Lemma A.3(8)(9),

To prove the second claim, we use the inequality and Lemma A.3(9) to conclude that

and the proof is complete. ∎

Lemma B.7:

Proof: We still start from the i.i.d. nature of and consider . If , then and are independent of each other, and hence . If , then (1) and are independent of each other; (2) either is independent of , or is independent of . This implies that , , and hence . Now we have established that only if and . By this fact and Cauchy-Schwarz inequality,

By the inequality and Cauchy-Schwarz inequality,

The desired result follows from Lemma A.3(3)(8)(9). ∎

Lemma B.8:

Proof: From the definition of Frobenius norm and the properties of trace,

Because are i.i.d. as , we have . By the above facts, the properties of matrix norms, and Cauchy-Schwarz inequality,

By the inequality and Cauchy-Schwarz inequality,

The proof is completed by Lemmas A.1(5), A.3(3)(4)(9), and Assumption 2.5(2). ∎

Lemma B.9 corresponds to Condition B*(d) of Gonçalves and Perron, (2014) and Conditions A.5, A.6 of Gonçalves et al., (2017).

Lemma B.9:

If Assumptions 2.1–2.5 hold for a pure factor model or Assumptions 2.1–2.8 hold for a factor model with covariates, then as ,

-

(1)

For every ,

-

(2)

Proof: Note that by the i.i.d. nature of . By the properties of matrix norms and Cauchy-Schwarz inequality,

Then the first claim follows from Lemmas A.1(5), A.3(4)(8) and Assumption 2.5(2).

To show the second claim, we use the above results, Cauchy-Schwarz inequality and the inequality to conclude that

The proof is completed by Lemmas A.1(5), A.3(4)(9) and Assumption 2.5(2). ∎

In this paper, more bootstrap high level conditions are used in subsequent contents, and we list them as lemmas below.

Lemma B.10:

If Assumptions 2.1–2.5 hold for a pure factor model or Assumptions 2.1–2.8 hold for a factor model with covariates, then for every , as ,

-

(1)

-

(2)

-

(3)

Proof: Since are i.i.d. as , we have is finite for every . Hence . The desired results follow from Lemmas A.3(6)(8)(10) and B.1. ∎

Lemma B.11:

If Assumptions 2.1–2.5 hold for a pure factor model or Assumptions 2.1–2.8 hold for a factor model with covariates, then as ,

-

(1)

For every ,

-

(2)

Results about Bootstrap Statistics

Let , , , , , , , , , , , , , , , , , , and be the bootstrap analogues of , , , , , , , , , , , , , , , , , , and , respectively. These bootstrap analogues are obtained in Setp 2(4) of Algorithms 3.2 and 4.3. Let and . Moreover, define the bootstrap version of rotation matrices

Lemma B.12:

If Assumptions 2.1–2.5 hold for a pure factor model or Assumptions 2.1–2.8 for a factor model with covariates, then as ,

-

(1)

, and , where both and are diagonal matrices with on diagonals.

-

(2)

, and , where is defined in Lemma A.1.

Proof: By the definition and properties of Frobenius norm, Lemma A.3(4), and Assumption 2.5(2),

Moreover,

Let for every . Then by the definition and properties of Frobenius norm, and Lemma A.2,

By the triangle inequality, the properties of matrix norms, Cauchy-Schwarz inequality, and the above facts,

Combining these results with Lemma A.1(2)(5) yields

For the pre-treatment subsample, it follows immediately from Lemma A.1(5) that

And the desired results follow from the above facts and the proof of Lemma B.1 of Gonçalves and Perron, (2014). ∎

Lemma B.13:

If Assumptions 2.1–2.5 hold for a pure factor model or Assumptions 2.1–2.8 for a factor model with covariates, then for any integer , as ,

-

(1)

For the control subsample,

-

(2)

For the pre-treatment subsample,

Proof: For , the first claim follows by applying Lemma 3.1 of Gonçalves and Perron, (2014) to the control subsample. Note that Lemma 3.1 of Gonçalves and Perron, (2014) relies only on their Conditions A*(b), A*(c), and B*(d), which have been verified by Lemma B.5(2), B.6(2), and B.9(2) of this paper. One can easily see that conclusions of Lemma B.5(2), B.6(2), and B.9(2) also hold for the pre-treatment subsample, which implies that we can apply Lemma 3.1 of Gonçalves and Perron, (2014) to the pre-treatment subsample to prove Claim (2).

Now consider . The case for and Assumptions 2.5(2) implies that

which in turn implies that

holds for any integer . Then the proof is complete. ∎

Lemma B.14:

Proof: The proof is completed by applying Lemma 2 of Gonçalves et al., (2017) and the identity before that lemma to the control subsample. Note that Lemma 2 of Gonçalves et al., (2017) requires their Assumptions 1–2 and Condition A. Assumptions 1–2 of Gonçalves et al., (2017) are implied by Assumptions 2.1–2.5 of this paper, and Condition A of Gonçalves et al., (2017) has been verified by Lemmas B.5–B.9 of this paper.

The convergence rate differs from what is implied by Lemma 2 of Gonçalves et al., (2017), i.e., , because we use a looser bound for the term defined in the proof of Lemma 2 of Gonçalves et al., (2017). Specifically, by the triangle inequality and Cauchy-Schwarz inequality,

and this term turns out to be the dominant term of . ∎

For every , define .

Lemma B.15:

If Assumptions 2.1–2.5 hold for a pure factor model or Assumptions 2.1–2.8 for a factor model with covariates, then as ,

-

(1)

For every ,

-

(2)

Proof: By the triangle inequality, Cauchy-Schwarz inequality, and Lemmas B.10(1), B.13(2),

which proves the first claim. For the second claim, we use the above facts and Lemmas B.10(3), B.13(2) to conclude that,

and the proof is complete. ∎

Lemma B.16:

If Assumptions 2.1–2.5 hold for a pure factor model or Assumptions 2.1–2.8 for a factor model with covariates, then as ,

-

(1)

For every ,

-

(2)

Proof: Lemma B.11(1) implies that

and Claim (1) follows from Lemma B.12(1). Furthermore, Lemma B.11(2) implies that

and Claim (2) follows by the properties of matrix norms and Lemma B.12(1). ∎

Lemma B.17:

If Assumptions 2.1–2.5 hold for a pure factor model or Assumptions 2.1–2.8 for a factor model with covariates, then as ,

-

(1)

For every ,

-

(2)

Proof: By the triangle inequality, the properties of matrix norms, Cauchy-Schwarz inequality, Lemmas A.3(3), B.13(2), and Assumption 2.5(2),

Note that

where

By the above result and Lemma B.12(1), . By the triangle inequality, the properties of matrix norms, and Lemma B.13(2),

This completes the proof of Claim (1). Moreover, by the properties of matrix norms and Lemmas A.1(5), A.3(4),

which proves Claim (2). ∎

Lemma B.18:

Proof: The result follows immediately from the decomposition

| [29] |

Lemma B.19:

If Assumptions 2.1–2.5 hold for a pure factor model or Assumptions 2.1–2.8 for a factor model with covariates, then for every integer , as ,

-

(1)

For the pre-treatment subsample,

-

(2)

For the control subsample,

Proof: Firstly consider . Then Claim (1) can be easily established by the decomposition [29], the inequality, and Lemmas B.15(2), B.16(2), B.17(2). One can show that these conclusions also hold for the control subsample, and Claim (2) can be proved analogously.

Now we turn to the case of . By the results for the case of and Assumption 2.5(2),

which in turn implies that

for any integer . And the proof is completed by using Assumption 2.5(2) again. ∎

Lemma B.20:

Proof: The conclusion is established by the properties of matrix norms, the inequality, Lemmas B.12(1), B.19, and Assumption 2.5(2). ∎

Lemma B.21:

Proof: Let for every . By construction,

Moreover,

By the triangle inequality, the properties of matrix norms, Cauchy-Schwarz inequality, Lemmas B.22(2), B.20, and Assumption 2.5(2),

Similarly,

Above results imply that

One can also show that

Then the desired result follows from Lemma B.12. ∎

Lemma B.22:

If Assumptions 2.1–2.5 hold for a pure factor model or Assumptions 2.1–2.8 for a factor model with covariates, then for every , as ,

-

(1)

-

(2)

-

(3)

-

(4)

-

(5)

Proof: By the inequality, the properties of matrix norms, and Lemmas A.3(3), B.12(1), B.13,

The rest parts of Claims (1) and (2) can be proved analogously.

To verify Claims (3)–(5), we conduct the following decomposition

| [30] |

By the inequality,

and

Recall that . Claims (3) and (5) are established by Lemmas A.1(5), A.3(3), B.10(1), B.12, B.13(1), B.18, B.21 and Assumption 2.5(2). Claim (4) follows from Lemmas A.1(5), A.3(4), B.10(2), B.12, B.14 B.19(1), B.21 and Assumption 2.5(2). ∎

Lemma B.23:

Proof: For every , by the triangle inequality, the properties of matrix norms, Cauchy-Schwarz inequality, Lemma B.22(1)(3), and Assumption 2.5(2),

Then by construction and the triangle inequality,

By the triangle inequality, the properties of matrix norms, Cauchy-Schwarz inequality, Lemma B.22(2)(4), and Assumption 2.5(2),

Then the proof is complete. ∎

Lemma B.24:

Proof: By Assumptions 2.2(2), 2.3(1) and the fact that are i.i.d. as and independent of the raw sample, , , and . Then by Markov’s inequality, as ,

The decomposition [27], the triangle inequality, Cauchy-Schwarz inequality, and Lemmas A.4, A.6 imply that

By Cauchy-Schwarz inequality and Lemmas B.10(1), B.22(5),

Therefore,

And the proof is completed by Assumption 2.2(2) and the ergodic theorem. ∎

Appendix C Proof of Main Results

Proof of Theorem 3.1

For , define

Since is strictly stationary, we have for all .

By Cauchy-Schwarz inequality, Assumption 2.3(1), Markov’s inequality, and Lemma A.4,

Then admits a decomposition

By Assumption 2.2(2) and the ergodic theorem, as .

Proof: By the decomposition of in Equation [30] and Lemmas B.12, B.14, B.18, B.21, it follows that .

Let and be the cumulative distribution functions of and , respectively, i.e.,

Let and be the conditional cumulative distributions function of and given , respectively, so that and for every .

For two (unconditional or conditional) distribution functions and , we measure the distance between and by the Mallows metric that is defined as

where is the set of bivariate joint distribution functions with marginal distribution functions and . Let , and be the expectation with respect to for every . Then the Mallows metric can be equivalently expressed as

Moreover, let denote weak convergence of distribution functions. We say as if and only if for any bounded Lipschitz continuous function ,

One can see Lemma 2.2 (Portmanteau) of van der Vaart, (1998) for equivalent characterisations of weak convergence.

Proof: Let and be empirical distribution functions so that

We firstly show that given almost every realisation of , the quantity is uniformly integrable with respect to , i.e.,

Consider a fixed . By Assumption 2.2(2) and the ergodic theorem,

as . And by Assumption 2.3(1), as . Therefore, for any , there exists , such that . Given almost every realisation of , there exists , such that for all . Note that is decreasing in for any fixed , so holds for all and . Pick . Then

By construction, for every . The triangle inequality yields

The ergodic theorem implies that as for every . By Lemma 2.11 of van der Vaart, (1998) and the continuity of [which follows from Assumption 2.2(3)],

as . By Lemma 2.2 of van der Vaart, (1998), . We have shown that given almost every realisation of , the quantity is uniformly integrable with respect to . Applying Lemma 8.3 of Bickel and Freedman, (1981) yields that .

Let be drawn from a discrete uniform distribution on . Then conditional on , we have and for every . By the inequality and Lemma A.4,

Furthermore, by the inequality, Assumptions 2.2(2), 2.3(1), the ergodic theorem, and Lemma A.4,

and the proof is complete. ∎

Proof: By the proof of Lemma 8.3 of Bickel and Freedman, (1981), for every bounded Lipschitz continuous function with Lipschitz constant ,