Single-Leg Revenue Management with Advice

Abstract

Single-leg revenue management is a foundational problem of revenue management that has been particularly impactful in the airline and hotel industry: Given units of a resource, e.g. flight seats, and a stream of sequentially-arriving customers segmented by fares, what is the optimal online policy for allocating the resource. Previous work focused on designing algorithms when forecasts are available, which are not robust to inaccuracies in the forecast, or online algorithms with worst-case performance guarantees, which can be too conservative in practice. In this work, we look at the single-leg revenue management problem through the lens of the algorithms-with-advice framework, which attempts to harness the increasing prediction accuracy of machine learning methods by optimally incorporating advice about the future into online algorithms. In particular, we provide an online algorithm that attains every point in the Pareto frontier between consistency (performance when advice is accurate) and competitiveness (performance when advice is inaccurate) for every advice. We also study the class of protection level policies, which is the most widely-deployed technique for single-leg revenue management: we provide an algorithm to incorporate advice into protection levels that optimally trades off consistency and competitiveness. Moreover, we numerically evaluate the performance of these algorithms on synthetic data. We find that our algorithm for protection level policies performs remarkably well on most instances, even if it is not guaranteed to be on the Pareto frontier in theory. Our results extend to other unit-cost online allocations problems such as the display advertising and the multiple secretary problem together with more general variable-cost problems such as the online knapsack problem.

1 Introduction

The field of revenue management, one of the pillars of operations research, got its start with the airline industry in the twentieth century (Talluri and Van Ryzin, 2004). Since then, it has found use in a variety of industries, covering the entire gamut from retail to hospitality. The goal of revenue management is to design price and quantity control policies that optimize the revenue of a firm. In this work, we will focus on quantity control. In particular, we consider a single-resource unit-cost resource allocation problem in which the decision maker wants to optimally allocate a limited inventory of a single resource to sequentially arriving requests. Each request consumes one unit of inventory, and generates a reward. For historical reasons, the terminology of revenue management is tailored to the airlines industry, and we continue with this convention in this work, but it is worth noting that the model and results apply more generally. For example, our results apply to the so-called display ad problem, in which impressions need to be assigned to advertisers to maximize clicks (Feldman et al., 2010), or the multiple secretary problem, in which applicants arrive sequentially and the best candidates need to be hired (Kleinberg, 2005). Moreover, we can also cover variable-cost problems such as the online knapsack problem (Zhou et al., 2008) or budget-constrained bidding in repeated auctions (Balseiro and Gur, 2019).

Consider an airline that operates a flight with economy seats. The seats in the economy cabin are demanded by a variety of customer types, which motivates airlines to offer different fare classes, each of which is designed to cater to a different market segment. For example, airlines often offer Basic Economy fares for leisure travelers who are price-sensitive. These low-fare tickets do not afford the holder any perks like seat selection, luggage check-in, upgrade eligibility, extra miles, priority boarding etc. On the other end of the spectrum are Full Fare Economy tickets that come with all of the aforementioned perks and are designed to be frequently available for late bookings for business travelers who have to travel at short notice. Given this collection of fare classes (which we assume to be fixed), how should an airline control the number of seats sold to customers from different fare classes in order to maximize revenue? This is referred to as the single-leg revenue management problem.

The crux of the single-leg revenue management is captured by the following trade-off: If the airline sells too many seats to customers from lower fare classes, then it will not be able to sell to higher-fare-class customers that might arrive later, and if the airline protects too many seats for higher fare-class customers, it will lose revenue from the lower fare classes if the demand for higher-fare classes never materializes. In the absence of any information about the fare classes of customers that will arrive, this problem falls under the paradigm of online algorithms and competitive analysis. This is the approach taken by Ball and Queyranne (2009), who characterized the optimal performance (in terms of competitive ratio) that any policy can achieve. In contrast, the vast majority of past work on single-leg revenue management assumes that accurate distributional forecasts are available about the customers that will arrive, and then proceeds to characterize the optimal policy in terms of the forecasts (see Gallego and Topaloglu 2019 for a recent overview). Often, additional assumptions like low-before-high (customers belonging to lower-fare classes arrive first) are also required for these results.

It would come as no surprise that policies which leverage the forecast perform much better than the policy of Ball and Queyranne (2009) when the sequence of customers is consistent with the forecast, but lose all performance guarantees when this is not the case. This work aims to achieve the best of both worlds by marrying the robustness of competitive analysis with the superior performance that can be achieved with forecasts. Robustly incorporating forecasts into algorithms is of fundamental importance in today’s data-driven economy, with the rising adoption of machine-learning-based prediction algorithms. To do so, we assume that we have access to advice about the sequence of customers that will arrive, but we do not make any assumptions about the accuracy of this advice. We develop algorithms that perform well when the advice is accurate, while maintaining worst-case guarantees for all sequences of customers. Because our algorithms take the advice as a black box, they can harness the increasing prediction power of machine learning methods. Our approach falls under the framework of Algorithms with Advice, which has found wide application of late (see Mitzenmacher and Vassilvitskii 2020 for a recent survey).

Before moving onto our contributions, we briefly discuss the centerpiece of single-leg revenue management theory and practice: protection level policies (also called booking limit policies), which play a vital role in our results. It is a class of policies parameterized by protection levels, one for each fare class. A protection level for a fare class is a limit on the number of customers that are accepted with fares lying below that fare class. A protection level policy accepts a customer if doing so does not violate any of the protection levels and rejects her otherwise. The motivation behind these limits (and the inspiration for the name ‘protection level policies’) is the need to protect enough capacity for higher fare classes and prevent lower fare classes from consuming all of the capacity. These policies have desirable theoretical properties in a variety of models and are widely deployed in practice (see Talluri and Van Ryzin 2004 for a detailed discussion).

1.1 Main Contributions

As is often the case for the Algorithms with Advice framework, we assume that the advice contains the minimum amount of information necessary to achieve optimal performance when the advice is accurate. For the single-leg revenue management problem, this translates to the top fares that will arrive, specified as a frequency table of fare classes (e.g. 60 Basic Economy customers and 40 Full Fare customers) without any information about the order. Our choice of advice has the advantage of being easy to estimate because of its low sample complexity. Given an advice, we consider the following competing goals: (i) Consistency: The competitive ratio of the algorithm when the advice is accurate, i.e., the instance conforms with the advice; (ii) Competitiveness: The worst-case competitive ratio over all sequences of customers, regardless of conformity to the advice.

Since different firms might have differing levels of confidence in the advice they receive (from machine-learning systems or humans), we are motivated to study the frontier that captures the trade-off between consistency and competitiveness. In particular, we allow the required level of competitiveness to be specified as an input alongside with the advice, and then attempt to maximize the level of consistency that can be attained while maintaining this level of competitiveness. We note that the choice of competitiveness as input is arbitrary and all of our algorithms can be modified to take the required level of consistency as input instead. Before stating our results, we describe an example that illustrates their flavor.

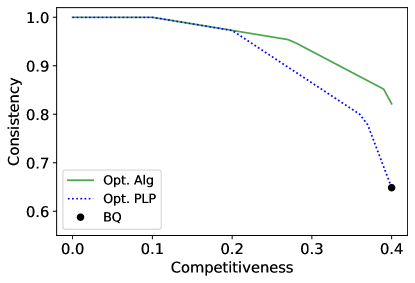

Example 1.

Consider a plane with economy seats and fare classes given by . The airline is advised that, of the customers predicted to arrive, 20 customers would want the $200 fare class, 60 customers would want the $400 fare class and 10 customers would want the $800 fare class, while the remaining customers (assumed to be at least 10 in number) would want the $100 fare class. Suppose the airline is not completely confident about this advice and would like to optimally tradeoff consistency and competitiveness. In this work, we show that the consistency-competitiveness Pareto frontier that captures the optimal way to perform this tradeoff for every advice can be computed efficiently using a Linear Program ( ‣ 3.2), and give an algorithm (Algorithm 1) that achieves this optimal performance. We depict the Pareto frontier for the advice above with a solid line in Figure 1. If we are restricted to using protection level policies, then we describe another algorithm (Algorithm 2) that yields the optimal tradeoff. We depict the performance of Algorithm 2 with a dotted line in Figure 2. Our results show that consistency can be significantly increased by sacrificing only a small amount of competitiveness.

The Consistency-Competitiveness Pareto Frontier. We construct an LP, and develop an optimal algorithm based on it, that completely characterizes the Pareto frontier of consistency and competitiveness. More precisely, we give an efficient LP-based optimal algorithm (Algorithm 1) which, given an advice and a required level of competitiveness, achieves the highest level of consistency on that advice among all online algorithms that satisfy the required level of competitiveness. We remark that most algorithms in the literature do not attain the best level of consistency for every advice, but instead, are only shown to be optimal for the worst-case advice. In contrast, our LP-based optimal algorithm attains the best possible level of competitiveness for all advice and levels of competitiveness. In other words, for every advice, we construct an LP to efficiently compute the consistency-competitiveness Pareto frontier, and also develop an online algorithm whose performance lies on this Pareto frontier. We achieve this through the following steps: (i) First, we assemble a collection of hard customer sequences for the given advice; (ii) Then, we construct an LP that aims to maximize consistency while maintaining the required level of competitiveness on these hard instances; (iii) Finally, we use the solution of the LP to construct a collection of protection levels, and optimally switch between these protection levels, to attain the highest possible level of consistency, while attaining the required level of competitiveness on all customers sequences. The crux of the proof lies in guessing the right collection of sequences to distill the fundamental tradeoffs of the problem, and then proving that these are in fact the hardest sequences, i.e., our online algorithm which is designed to do well on these hard sequences performs well on all sequences.

Optimal Protection Level Policy. In recognition of the central role of protection level policies in single-leg revenue management theory and practice, we also characterize the optimal way to incorporate advice into protection level policies. We emphasize that, even though our optimal algorithm makes use of protection levels to make decisions, it is not a protection level policy because it may switch between protection levels. This switch between protection levels comes at the cost of some desirable practical properties of protection level policies like monotonicity (never rejecting a customer from a certain fare class and then accepting a customer from the same fare class that arrives later) and being oblivious to the fare class of the customer before making the accept/reject decision. However, we show that this switch is necessary for optimality: protection level policies can be sub-optimal in their consistency-competitiveness trade-off. Nonetheless, the significance of protection level policies to the theory and practice of revenue management warrants our investigative efforts. We develop an algorithm (Algorithm 2) that takes as input an advice and required level of competitiveness, and outputs protection levels which correspond to the protection level policy that maximizes consistency in the set of all protection level policies that satisfy the required level of competitiveness. To rephrase, regardless of the advice, no protection level policy can achieve higher consistency and competitiveness than the one based on Algorithm 2.

Robustness. Since no prediction algorithm can be completely accurate, it is also important for any algorithm to achieve good performance when the sequence of fares is “close” to the advice. We use an appropriately modified norm to define a distance between the realized fare sequences and the advice, and show that the performance of our algorithms degrades gracefully as a function of this distance. In particular, we show that the performance of protection level policies degrades linearly as a function of the distance. Moreover, we describe a relaxed version of our optimal algorithm (Algorithm 3) whose performance also degrades linearly with the distance in a neighborhood of the advice.

Numerical Experiments. Finally, we also run numerical experiments on synthetic data with the aim of (i) comparing the performance of our optimal LP-based algorithm (Algorithm 1) and our optimal protection level policy (Algorithm 2); and (ii) comparing the average performance of our algorithms when the sequence of customers is drawn from a distribution centered on the advice. We find that protection level policies are optimal for most types of advice, and that the essence of its sub-optimality is captured by our bad example (Example 3). Moreover, we find a graceful degradation in the performance of our algorithms as a function of the noise in the distribution that generates the sequences. We also find that our algorithms continue to perform better than that of Ball and Queyranne (2009) even under high levels of noise.

1.2 Additional Related Work

Single-Leg Revenue Management. The single-leg revenue management problem has a long history in revenue management. Littlewood (2005) characterized the optimal policy for the two-fare class setting under known-stochastic customer arrival with the LBH (low before high, i.e., customers arrive in increasing order of fares) assumption. Brumelle and McGill (1993) extended the results to multiple fare classes, under the additional assumption of independence across fare classes, via a dynamic programming formulation resulting in a protection level policy that is optimal. Lee and Hersh (1993), Robinson (1995) and Lautenbacher and Stidham Jr (1999) dispense with the LBH assumption and characterize the optimal policy in this dynamic setting. All of the aforementioned works assume that the stochastic process governing customer arrival is completely known. Van Ryzin and McGill (2000), Kunnumkal and Topaloglu (2009) and Huh and Rusmevichientong (2006) relax this assumption by considering a setting in which LBH demand is drawn from some stationary unknown distribution repeatedly. They give an adaptive procedure for updating the protection levels using samples from this distribution that converges to the optimal protection levels. The stationarity assumption allows them to learn the optimal protection levels perfectly for future demand. As discussed earlier, Ball and Queyranne (2009) broke from the tradition of stochastic assumptions and looked at the problem through the lens of competitive analysis. Lan et al. (2008) extended their work by allowing for known upper and lower bounds on the number customers from each fare class. Under the assumption that these bounds always hold, they develop algorithms which achieve the optimal competitive ratio. Importantly, their algorithm loses its guarantees when the bounds are violated. Like Lan et al. (2008), we also develop a factor-revealing LP. But, unlike their LP, which is simple enough to be solved in closed form, our LP solves a complex optimization problem based on more intricate hard instances and does not admit a closed-form solution. Ma et al. (2021) generalize the single-leg model by allowing the firm to price the fare classes, and show that this can be done without any loss in the competitive ratio. We refer the reader to the comprehensive books by Talluri and Van Ryzin (2004) and Gallego and Topaloglu (2019) for a detailed discussion on single-leg revenue management. Recent work has also studied the single-leg revenue management problem under other models which go beyond the classical adversarial and stochastic analysis. Hwang et al. (2021) develop online learning algorithms for a model with two fare classes in which the sequence of fares is selected by an adversary, but a randomly selected subset of that sequence arrives in random order. Each customer joins the random-order subset independently with the same probability and this random component of the input sequence allows their algorithm to partially learn the sequence. Aouad and Ma (2022) study the more general stochastic matching problem in which the number of customers of each type are drawn from some distribution, and then these customers arrive in an adversarial or random order. Golrezaei et al. (2022) also study a setting with two types of fare classes in which the decision maker does not know the reward of each fare class. They posit the existence of a test period in which each customer is sampled independently with the same probability and reveals her reward to the user. Their algorithm uses this sample information to obtain asymptotically optimal performance.

Algorithms with Advice. Motivated by the ubiquity of machine-learning systems in practice, a recent line of work looks at improving algorithmic performance by incorporating predictions. Here, the goal is to avoid making assumptions about the quality of the predictions and instead design algorithms that perform better when the prediction is accurate while maintaining reasonable worst-case guarantees. This framework has predominantly been applied to online optimization problems like caching (Lykouris and Vassilvtiskii, 2018; Rohatgi, 2020), ski-rental and online scheduling (Purohit et al., 2018), the secretary problem (Antoniadis et al., 2020; Dütting et al., 2021), online ad allocation (Mahdian et al., 2012) and queueing (Mitzenmacher, 2021). While our problem can be thought of as an online allocation problem, the results of (Mahdian et al., 2012) are not directly applicable because they assume that rewards are proportional to resource consumption, which does not hold for the revenue management problem. The classical secretary problem (and its multi-secretary generalizations) share the basic setup with the single-leg revenue management problem—they are both single-resource unit-cost resource allocation problems. The difference being that, unlike the stochastic assumptions made in the secretary literature, the single-leg revenue management model considered here only requires the rewards to belong to some known finite set and allows for them to be adversarially chosen. This makes the existing results on the secretary problem with advice (Antoniadis et al., 2020; Dütting et al., 2021) incomparable to ours. Advice has also been used to improve data structures (Mitzenmacher, 2019) and run-times of algorithms (Dinitz et al., 2021). We refer the reader to Mitzenmacher and Vassilvitskii (2020) for a more detailed discussion.

Other Work. The single-leg revenue management problem is a special type of online packing problem with one resource, unit costs and varying rewards coming from a known set. Under adversarial input, a constant competitive ratio cannot be obtained for online packing in general, but a long line of work shows that it can be achieved for important special cases like online matching (Karp et al., 1990), the Adwords problem (Mehta et al., 2007) and the Display Ads problem with free disposal (Feldman et al., 2009). On the other hand, near optimal performance can be obtained for stochastic or random order input under mild assumptions (Devanur and Hayes, 2009; Feldman et al., 2010; Agrawal et al., 2014; Alaei et al., 2012). See Mehta et al. (2013) for a survey on online allocation. The Adwords problem, which is particular important for the online advertising industry, has also been studied in a variety of models that interpolate between the adversarial and stochastic settings (Mirrokni et al., 2012; Esfandiari et al., 2015).

2 Model

We consider a single-resource unit-cost resource allocation problem: a firm (airline) has units of a resource (seats on a plane) it wants to allocate to sequentially arriving requests (customers). Each request consumes one unit of the resource and generates a reward. We assume that the reward can take possible values (fare classes), which we denote by . To simplify notation, we include a special zero request with . At each time step , a request arrives, whereupon its reward is revealed to the firm and an irrevocable accept/reject decision is made. We only assume that the firm knows the set of possible rewards , and do not require the firm to know the total number of requests that will arrive.

2.1 Applications

Before proceeding further with the model, we discuss its applicability to internet advertising markets, the online knapsack problem, the multi-secretary problem, and the airline industry. In the display ad problem, which has received considerable attention due to its prominence in internet advertising, advertisers enter into contracts with websites to display a certain number of ads (Feldman et al., 2010). Here the capacity is the number of impressions guaranteed by the contract and when a visitor arrives the website needs to decide whether to display an ad to the visitor, which counts against the advertiser’s contract and consumes one unit of this resource. The rewards are the appropriately discretized click-through-rate (CTR) estimates for showing an ad to the visitor. The goal of the website is to maximize the total CTR while satisfying the contractual obligations.111Even though reservation contracts have requirements, in practice they are treated as packing problems (see, e.g., Mehta et al. 2013). A common approach is for publishers to penalize shortfalls by adding penalties to the objectives, which can be incorporated to our model by adjusting fares down.

Our framework can also be used to model the online knapsack problem (Zhou et al., 2008) when the possible number of item types is finite. Without loss of generality, we can assume that the weight of each item is a non-negative integer because such an assumption can always be satisfied with rescaling. Given an instance of the online knapsack problem, we can construct an instance of the single-leg revenue management problem as follows: If an item has weight and reward , replace it with items, each with weight 1 and reward . Thusm if the possible weights are and the possible item rewards are , then the corresponding single-leg revenue management problem with fares has the same worst-case competitive ratio. With this reduction, the guarantees for our algorithms which incorporate advice also continue to hold for the online knapsack problem (see Appendix A for details). Moreover, Zhou et al. (2008) show that the online knapsack problem captures budget-constrained bidding in repeated auctions, thereby also bringing the latter under the purview of our framework.

The multi-secretary problem (Kleinberg, 2005) captures the setting in which a company wishes to hire employees, each of whom takes up one position and generates varying amounts of productivity (reward). It is assumed that the employee is interviewed and the associated reward is revealed to the company before making the accept/reject decision. Our model captures the adversarial-version of the multi-secretary problem where no assumption is made about the rewards other than membership in some known set .

Finally, as discussed earlier, the origin of our model lies in the airline industry, where the fare classes are decided in advance, customers arrive online, and accept/reject decisions need to be made to maximize revenues. Moreover, it is a standard assumption in the single-leg revenue management literature that the different fare classes are designed to perfectly segment the market through their perks (Talluri and Van Ryzin, 2004): customers belong to a fare class and do not substitute between them. In the rest of the paper, we continue with tradition and use the terminology of the airline industry and the single-leg revenue management problem to describe our model. Henceforth, requests will be referred to as customers and the possible rewards as fare classes or fares.

2.2 Advice, Online Algorithms, and Performance Metrics

We next present some definitions that will be used in our analysis.

Definition 1.

An instance of the single-leg revenue management problem is a variable-length sequence of customer fares , where and for all . We denote the set of all instances by .

As is customary in competitive-ratio analysis, we will measure the performance of an online algorithm by comparing it to the performance of the clairvoyant optimal.

Definition 2.

For an instance of the single-leg revenue management problem, represents the maximum revenue one can obtain if one knew the entire sequence in advance, i.e., is the sum of the highest fares in if and the sum of all fares if .

The classical work of Ball and Queyranne (2009) assumes that, at time , the firm has no information about the future sequence of fares , and then goes on to characterize the worst-case competitive ratio (the ratio of the revenue of the firm to that of a clairvoyant entity that knows the entire instance) over all instances. In today’s data-driven world, their assumption about the complete lack of information about future fares can be too pessimistic. We relax it and assume that the firm has access to an oracle that provides the firm with predictions about the fares that will arrive. In practice, this oracle is often a machine-learning model trained on past data about fares. We capture this through the notion of advice as used in the algorithms-with-advice framework (see Mitzenmacher and Vassilvitskii 2020 for a survey).

Definition 3.

An advice is an element of the set which represents the top highest fares that are predicted to arrive. In particular, an advice is interpreted to mean that we will receive an instance for which it would be possible to pick customers with fare for all , and doing so would yield the optimal revenue of . In light of this, we will use to denote for all .

Before proceeding further, we note some important properties of the advice:

-

•

It does not take into account the order of the fares and is limited to the frequency of each fare type. Moreover, it only requires information about the top highest fares.

-

•

Each element contains just enough information to compute the optimal solution for any instance that conforms with the advice: pick customers with fare for all .

Our choice of advice drastically reduces the size of the space of possible predictions, allowing for efficient learning from past data. For example, firms could train machine learning models that map contexts (season, flight information, economic trends, etc.) to a prediction on the number of customers, which translates to a regression problem for each fare class. Moreover, compared to other choices of advice such as the arrival order of customers, our advice is permutation invariant, which leads to more robust algorithms that are less sensitive to perturbations in the data.

In this work, we consider online algorithms that take as input an advice, and then make accept/reject decisions for sequentially arriving customers in a non-clairvoyant fashion. The goal is to perform well when the arriving customers conform to the advice (consistency), while maintaining worst-case guarantees for the case when the advice is not a good prediction of customer fares (competitiveness). Like Ball and Queyranne (2009), we allow the online algorithm to accept fractional customers.

Definition 4.

An online algorithm (possibly randomized) that incorporates advice takes as input an advice , an instance as history and a fare from as the fare type of the current customer; and outputs a fractional accept quantity that satisfies the capacity constraint, i.e., almost surely it satisfies

Remark 1.

Since all of the algorithms discussed in this work incorporate advice, we will refer to online algorithms that incorporate advice simply as online algorithms.

Remark 2.

Even though we allow online algorithms to fractionally accept customers, all of the online algorithms we propose in this work satisfy the following property: If we run the algorithms with the modified capacity of and completely accept the fractionally accepted customers then the number of acceptances does not exceed and degradation in the performance of the online algorithm is . Since most applications (including the airline industry) satisfy , our algorithms have negligible rounding error. See Appendix B for details.

Next, we rigorously define the performance metrics needed to evaluate online algorithms that incorporate advice, beginning with the definition of consistency, which captures the performance of an online algorithm when the instance conforms to the advice.

Definition 5.

For advice , let be the smallest index such that . Define to be the set of all instances that conform to the advice . An online algorithm is -consistent on advice if, for any instance , it satisfies

The following definition captures the performance of online algorithms on all instances, regardless of their conformity to the advice.

Definition 6.

An online algorithm is -competitive if for any advice and instance ; we have

Ball and Queyranne (2009) showed that no online algorithm can be -competitive for any strictly greater than . Hence, every online algorithm is -competitive for some .

The central goal of this work is to study the multi-objective optimization problem over the space of online algorithms which entails maximizing both consistency and competitiveness. In particular, for every advice, we characterize the Pareto frontier of consistency and competitiveness, thereby capturing the tradeoff between these two incongruent objectives. We conclude this section with the definition of protection level policies, which are a class of online algorithms that play a critical role in our results (and single-leg revenue management in general).

2.3 Protection Level Policies

Protection level policies are the method-of-choice for single-leg revenue management in the airline industry, and have garnered extensive attention in the revenue management literature (Talluri and Van Ryzin, 2004; Ball and Queyranne, 2009). It is a form of quantity control parameterized by protection levels : the firm accepts at most customers with fares or lower. The idea stems from the need to preserve capacity for higher paying customers that might arrive in the future. More precisely, on an instance where for some , the fraction of accepted by the protection level policy with protection levels can be iteratively defined as

Our algorithm (Algorithm 1) will use protection level policies as subroutines to attain the optimal level of consistency for a given level of competitiveness. We note, however, that this does not make Algorithm 1 a protection level policy, since it may switch between different protection levels. Moreover, in reverence to their role in revenue management theory and practice, we will also characterize the protection level policy that attains the optimal level of consistency for a given level of competitiveness among all protection level policies (Algorithm 2). We conclude this section with an example to build some intuition.

Example 2.

Let , and . Consider the execution of the protection level policy parameterized by on the sequence . Then, since , we accept the first two customers with fare . At the third step, we reject the customer with fare because we have already accepted two customers with fare or below, and thus accepting it would violate the second protection level . Note that we reject this customer despite the fact that we have not accepted any customer with fare and . Finally, we accept the customer with fare in the fourth time step. Now, contrast this with the sequence . In this case, we would accept the first customer with fare like before. We would also accept the second customer with fare because it does not violate either or . In the third step, we would reject the customer with fare because we have already accepted two customers with fare or below. Finally, we accept the fourth customer with fare .

3 The Consistency-Competitiveness Pareto Frontier

The goals of consistency and competitiveness can be at odds with each other. Therefore, depending on the level of confidence in its prediction model, different firms will want to target different levels of consistency and competitiveness. Nonetheless, it would always be desirable to use an online algorithm that optimally trades off consistency and competitiveness. In other words, we would like online algorithms whose performance lies on the consistency-competitiveness Pareto frontier.

To achieve this, we will describe an online algorithm that, given an advice and a desired level of competitiveness, achieves the optimal level of consistency on advice while maintaining -competitiveness.

Definition 7.

Fix an advice and a level of competitiveness . Let denote the set of all online algorithms that are -competitive. Then, the optimal level of consistency for advice under the -competitiveness requirement is defined as follows:

In subsection 3.1, we discuss a collection of instances that capture the core difficulty that every non-clairvoyant online algorithm faces in maximizing consistency. Using this collection of hard instances, in subsection 3.2 we establish an LP-based upper bound on . Then, in subsection 3.3, we define an algorithm that achieves a level of consistency that matches this LP-based upper bound, thereby completely characterizing . For the rest of this section, fix an advice and a level of competitiveness . Moreover, let be the lowest fare that forms a part of .

3.1 Hard Instances

In our optimal algorithm, which we discuss in the next subsection, we will use protection level policies as subroutines to make accept/reject decisions. It is not too difficult to see that, given a collection of customers, every protection level policy earns the least amount of revenue when the customers arrive in increasing order of fares (see Lemma 1 in Appendix C.1 for a formal proof). Looking ahead, we will define hard instances in which the customers arrive in two phases, with the fares satisfying an increasing order in each phase.

First, observe that any -consistent algorithm must obtain a revenue of on any instance that conforms with the advice. To capture this, we define to be the “largest” instance that conforms to the advice , i.e., is the instance that consists of customers of fare type for and customers of fare type for arriving in increasing order of fares (see Figure 2). More precisely, set and define the instance as

-

•

if for some and

-

•

if for some .

Note that and , i.e., picking customers of fare type is optimal.

Next, define to be the instance truncated at the fare , including fare . More precisely, , where for and for . These instances represent prefixes of and aim to exploit the non-clairvoyance of online algorithms: If an online algorithm receives the partial instance , the complete instance can be for any .

To define the hard instances, we will also need the instances in which fares arrive in increasing order of fares, in blocks of customers of each fare type. Let be the instance in which customers from each fare type arrive in increasing order, i.e., if for some (see Figure 3). Furthermore, let denote the instance obtained by pruning to contain fares or lower.

Given two instances , we use to denote the instance in which the sequence of fares in is followed by the sequence of fares in . With these definitions in place, we are now ready to define the set of hard instances:

Before proceeding to our LP-based upper bound that makes use of these hard instances , we pause to provide some intuition. Any online algorithm that is -consistent needs to attain a revenue greater than or equal to when presented with the instance . But, given a prefix of , a non-clairvoyant algorithm has no way of knowing whether the full instance will be or not. Therefore, it has to have the same accept/reject decisions on and every prefix. Furthermore, to be -competitive, the online algorithm has to achieve -competitiveness on every instance. This places a constraint on the amount of capacity that an algorithm can commit in its pursuit of -consistency because the instance can be any prefix of (including itself) followed by .

3.2 LP-based Upper Bound

Next, we define a Linear Program (LP) that uses the hard instances to bound from above. We use the variables to capture the number of customers of type accepted in or any of its prefixes . Moreover, we use to denote the number of customers of type accepted from the part of . Finally, we use to denote the number of customers of fare type in the instance , i.e., if and otherwise. The following LP maximizes the level of consistency of any online algorithm that is -competitive against prefixes of and all the hard instances. First, for feasibility, (0a) enforces the capacity constraint for all hard instances . (0b) ensures -competitiveness on prefixes of , given by . (0c) guarantees -consistency on the advice instance . (0d) ensures -competitiveness on the hard instances .

| s.t. | (0a) | |||||

| (0b) | ||||||

| (0c) | ||||||

| (0d) | ||||||

| (0e) | ||||||

| (0f) | ||||||

Consider an online algorithm that is -competitive and -consistent on advice . Let be the random variable that denotes the number of customers of fare type that accepts when presented with instance . Since is a prefix of for all , also denotes the number of customers of fare type that accepts when presented with the instance for all . Furthermore, for , let be the random variable that denotes the number of customers of fare type accepted by after time step in the instance . Since the instance is a prefix of , for , the random variable also denotes the number of customers with fare accepted by after time when presented with the instance .

Now, set for all and for all . Then, by virtue of linearity of expectation, we get that the feasibility, -consistency and -competitiveness of implies the feasibility of as a solution of ‣ 3.2, thereby implying , where denotes the optimal value of ‣ 3.2. Hence, we get the following upper bound:

Theorem 1.

For a given advice and a required level of competitiveness , let be the optimal value of ‣ 3.2. Then, .

In the next subsection, we use ‣ 3.2 to describe an online algorithm that is -competitive, and -competitive on advice . As a consequence, we will get that . We conclude by noting that ‣ 3.2 has some redundancies in the constraints and the variables, e.g., (0b) for implies (0d) for , and for in every optimal solution. While the linear programming formulation can be tightened by removing the additional constraints and variables, we kept these to simplify the exposition.

3.3 LP-based Optimal Algorithm

-

•

For , set . Moreover, set .

-

•

For , set if and if . Moreover, set for all .

-

1.

Let be the fare class of customer , i.e., . Calculate the fraction of customer that would be accepted under : set and let be the largest index such that (set if no such index exists). If , update to reflect the anticipated rejection of a fraction of .

-

2.

Check Trigger Condition. If and for some , i.e., the total rejections among fares exceeds the rejections among fares in under LP solution :

-

•

Set trigger and (set if no such index exists).

-

•

While such that : Set .

-

•

Set , i.e., is the value with which the ‘While’ loop terminates.

-

•

Switch Protection Levels. Set for all .

-

•

-

3.

Make decision according to . Accept fraction of customer and update , for all , to reflect the increase in number of customers of fare or lower accepted by the algorithm.

In this subsection, we describe an algorithm (Algorithm 1) that is -consistent for advice while also being -competitive. This allows us to establish the main result of this section:

Theorem 2.

Note that, in particular, Theorem 2 implies that ‣ 3.2 is an efficient method of computing the consistency-competitiveness Pareto frontier. Furthermore, for every advice , Algorithm 1 provides a way to achieve levels of consistency and competitiveness that lie on this Pareto frontier, thereby characterizing the tradeoff between consistency and competitiveness for every advice. In the rest of this subsection, we motivate Algorithm 1 and sketch the proof of Theorem 2. The full proof is relegated to Appendix C.1.

Algorithm 1 is based on protection level policies and operates in two phases. Throughout its run, it maintains active protection levels , and makes accept/reject decisions based on them. Importantly, these active protection levels are not fixed and take on different values in the two phases. The transition between the two phases in captured by the trigger . Since the protection levels change with time, Algorithm 1 is not a protection level policy. The protection levels of both phases are determined using an optimal solution of ‣ 3.2. In particular, we use the solution to construct protection levels, denoted by for phase and candidate protection levels for phase , defined as follows:

These protection levels are motivated by the hard instances. In particular, is devised to achieve a reward of on instance and is devised to achieve a revenue of on instance .

Initially, the active protection levels are set equal to with the goal of achieving good performance on , or more generally for any instance that conforms to the advice. If the advice is accurate, we show that the algorithm accrues a reward larger than , which in turn is larger than because of (0c). But this is not enough as the algorithm also needs to be -competitive. If the algorithm keeps using to make decisions even when the advice is inaccurate, it risks rejecting too many customers and violating the -competitiveness requirement. Therefore, it keeps track of the loss from rejecting customers in the form of , and uses this information to trigger the phase transition.

Intuitively, the phase transition should be triggered if continuing with protection levels would result in a violation of the -competitiveness requirement. To that end, in Step 1 we calculate the additional rejection that would result from the continued use of and update the rejections . In order to ensure that these rejections do not violate -competitiveness, the algorithm compares them to rejections made by ‣ 3.2 on the instance : it allocates a rejection-capacity of to fare for all . Here, fare classes are ignored because we do not require the advice to be good on fare classes which are not predicted to form a part of the optimal solution. To generate even greater leeway for the instance to deviate from the advice, the algorithm enforces these capacities in an upward-closed manner, i.e., we allow rejections of lower fares to cannibalize the rejection-capacity of higher fares (up to fare ). In particular, the trigger condition checks whether for some . The summation is limited to because the algorithm has filled the protection levels till fare , i.e., , and we can charge the rejections against these acceptances to ensure -competitiveness. The definition of implies that the algorithm accepts every customer with fare larger than , however the number of such customers can potentially be zero and we cannot charge the rejections against them.

Once the trigger is invoked, the algorithm needs to select new protection levels which satisfy the following crucial properties: (i) the number of customers accepted till the trigger pull should not violate these new protection levels; and (ii) ensure -competitiveness. Algorithm 1 achieves this by carefully choosing a set of protection levels from the collection . It sets to be the new active protection levels and uses them to make decisions on the remaining customers.

The proof of Theorem 2 involves a fine-grained analysis of the performance of Algorithm 1. We begin by showing that Algorithm 1 achieves a fraction of for any instance that conforms to the advice. Note that no assumptions are made about the order in which the fares arrive. Since the order of the fares can effect when the phase transition occurs, we cannot directly leverage the proof techniques developed for analyzing protection level policies. Consequently, we first carefully analyze the phase transition rule to ensure that it is not triggered on any instances which conforms to the advice and then bound the performance of the protection level policy based on by leveraging ‣ 3.2.

Consistency is not the only requirement and we also need to ensure -competitiveness of Algorithm 1. As mentioned earlier, Algorithm 1 is not a protection level policy, and consequently cannot be analyzed as one. In light of the lack of structure imposed on the instance and the novel phase transition that is part of Algorithm 1, apriori it is not even clear what the hard instances for Algorithm 1 look like, and even though we referred to the instances defined in Subsection 3.1 as ‘hard’, it is not clear that -competitiveness on hard instances of Subsection 3.1 ensures -competitiveness on all instances. The design of the hard instances goes hand-in-hand with the proof of Theorem 2, with the latter guiding the former. Establishing -competitiveness is rife with technical challenges: (i) the trigger condition for the phase transition relies on rejections, compelling us to keep track of rejections, which is not required for analyzing protection level policies; (ii) ensuring that using (which is designed to perform well when the advice is true) to make decisions before the phase transition does not cause Algorithm 1 to make irrevocable decisions that preclude -competitiveness. We tackle (i) by developing finer bounds on which take rejections into account and connecting them to the reward accumulated by Algorithm 1, and establish (ii) by performing an intricate case-analysis of the procedure used by Algorithm 1 to select the post-transition protection levels. Our analysis has to continually contend with the lack of order in the instance and its effect on the phase transition, making (i) and (ii) even more challenging.

4 Optimal Protection Level Policy

By carefully constructing and switching between protection levels, Algorithm 1 employs protection level policies with different protection levels as sub-routines to achieve performance that lies on the consistency-competitiveness Pareto frontier. In particular, it runs the protection level policy based on when the trigger is and runs the protection level policy based on once . This switch between protection levels can lead to non-monotonicity: Algorithm 1 may accept a customer of a particular fare type having rejected another customer of that same fare type at an earlier time step (see Example 3). Non-monotonicity “can lead to the emergence of strategic consumers or third parties that specialize in exploiting inter-temporal fare arbitrage opportunities, where one waits for a lower fare class to be available. To avoid such strategic behavior, the capacity provider may commit to a policy of never opening fares once they are closed” (Gallego and Topaloglu, 2019). Additionally, in order to switch between protection levels, Algorithm 1 also requires information about the fare types of customers that were rejected, which may not be available depending on the context.

In contrast, using a single protection level policy on the entire instance (i.e., using the same protection levels at all time steps) avoids these issues, in addition to satisfying a multitude of other practically-relevant properties which make protection level policies the bedrock of single-leg revenue management (see Talluri and Van Ryzin 2004 for a detailed discussion). As we will show later in this section, this insistence on using a single set of protection levels at all time steps comes with a loss of optimality. Nonetheless, the practical importance of protection level policies warrants an investigation into the optimal way to incorporate advice for protection level policies. To that end, in this section, we characterize the protection level policy that attains the optimal level of consistency for a given advice among all protection level policies that are -competitive.

Definition 8.

Fix an advice instance and a level of competitiveness . Let denote the set of all protection level policies that are -competitive. Then, the optimal level of consistency for advice that can be attained by protection level policies under the -competitiveness requirement is defined as follows:

4.1 Computing the Optimal Protection Levels

-

1.

Set for .

-

2.

For to :

-

(a)

Define

(1) and set for all .

-

(b)

If : Define

(2) then set for all .

-

(a)

-

3.

Return protection levels .

-

1.

Set .

-

2.

CoreSubroutine.

-

3.

If , set . Else if , set .

The goal of this subsection is to describe an algorithm (Algorithm 2) which, given advice and a required level of competitiveness , outputs protection levels such that the protection level policy based on is (nearly) -consistent on advice . Before proceeding to the algorithm, we define a few terms necessary for its description. For the remainder of this subsection, fix an advice and a required level of competitiveness . Recall that protection levels are simply vectors such that . If a vector satisfies but then we call it infeasible. Given an instance and protection levels , we use to denote the revenue obtained by the protection level policy with protection levels when acting on the instance . Furthermore, recall that denotes the number of customers of fare type in the instance , i.e., if and otherwise. Finally, our description of Algorithm 2 also makes use of the instances defined in subsection 3.1.

The core subroutine in Algorithm 2 takes as input a desired level of consistency and decides whether any protection level policy can achieve -consistency on advice while also being -competitive. It does so by iterating through the fares in increasing order to and setting to be smallest level that satisfies the following properties:

-

•

The (possibly infeasible) protection levels ensure a revenue greater than or equal to on instance . We define in (1) to be such that , and then set to ensure -competitiveness on :

-

•

The (possibly infeasible) protection levels preserve the potential to attain a revenue greater or equal to on instance , i.e., if we were to accept all of the customers in with fare strictly greater than (leading to a revenue of ), in addition to the fares accepted according to the protection level policy till fare (which yield a revenue of ), then we can guarantee a revenue greater than or equal to . We define in (2) to be such that , and increase by to preserve the potential to attain -consistency:

In the proof of Theorem 3, we show that these protection levels are feasible () if and only if some feasible protection level policy can attain -consistency on advice while being -competitive. To do so, we prove that the core subroutine minimizes the total capacity needed to achieve the required level of consistency and competitiveness, thereby implying that if any feasible protection level policy can achieve it, then the protection levels are feasible. Algorithm 2 simply uses this core subroutine to perform a binary search over the space of all consistency levels to find the largest one which can be attained for advice while being -competitive. The ‘Return’ step ensures that Algorithm 2 returns feasible protection levels: It sets and computes the corresponding protection levels , which are guaranteed to satisfy because of the binary search procedure.

Theorem 3.

If are the protection levels returned by Algorithm 2, upon receiving required level of competitiveness , advice , and approximation parameter as input, then the protection level policy based on is -consistent on advice and -competitive. Moreover, the runtime of Algorithm 2 grows polynomially with the input size and .

The proof of Theorem 3 can be found in Appendix D.1. The technical challenge lies in establishing the following fact: If any protection level policy can achieve -consistency and -competitiveness, then the core subroutine with returns protection levels which are feasible (i.e., ). To achieve this, we iteratively define linear programs, each of which builds on the solution of previous programs, in order to connect the consistency and competitiveness of an arbitrary protection level policy to that of Algorithm 2.

4.2 Sub-optimality of Protection Level Policies

As we alluded to at the beginning of this section, protection levels policies do not always yield performance that lies on the consistency-competitiveness Pareto frontier. In fact, as we show in this subsection, in some cases it can be quite far from the Pareto frontier. We do so by exhibiting an example that illustrates the sub-optimality of protection level policies.

Example 3.

Assume that the capacity satisfies . Set , where is a large number. Moreover, set , and . Consider . Then, using the notation of Algorithm 2, we get that , , , , and

Therefore, . Hence, using Lemma 9 in Appendix D, we get that . Next, note that the following values form a feasible solution of ‣ 3.2: and

Hence, we get that , thereby showing that, in the worst case, protection level policies may be far from the optimal. This example also demonstrates the lack of monotonicity in Algorithm 1. The solution described above is an optimal integral solution of the LP and very close to the optimal solution of the LP. If Algorithm 1 receives the instance , it will initially reject some customers with fare because and , and then accept customers with fare when they arrive as part of because .

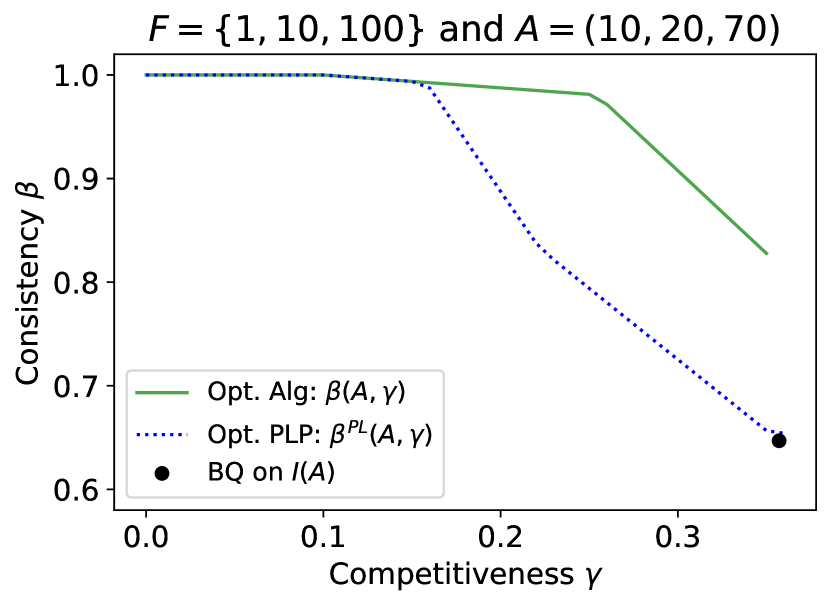

We conclude this section by providing some intuition behind the sub-optimality of protection level policies that motivated the above example. The central difference between the LP-based optimal algorithm (Algorithm 1) and the optimal protection level policy (Algorithm 2) is that the former changes the protection levels it uses if the instance deviates from the advice. Hence, if the advice is turning out to be true then the optimal LP-based algorithm can use the minimum amount of capacity needed to maintain -competitiveness on the prefix of the instance seen so far, in an attempt to conserve capacity and deploy it on customers with higher fares that will arrive later, thereby attaining high consistency. To do so, it uses the protection levels , as defined in Algorithm 1, while the advice is true. Crucially, need not be -competitive on instances that cannot go on to conform with the advice, and is optimized for consistency. This does not violate the competitiveness requirement because if the instance deviates from the advice, the LP-based optimal algorithm stops using and switches to protection levels that allow it to attain -competitiveness. On the other hand, the optimal protection level policy lacks this adaptivity and uses the same protection levels throughout. This forces it to use more capacity on lower fares because it needs to maintain -competitiveness on instances in which a large number of such customers arrive, even though the advice predicts a low number and the instance is consistent with the advice. This “overcommitment” to lower fares prevents it from attaining the optimal level of consistency. In our empirical evaluation of the two algorithms (see Section 6), we found this overcommitment to be the main driver of the sub-optimality of protection level policies: In settings that are not geared to exploit this overcommitment, the optimal protection level policy (Algorithm 2) attains performance on the consistency-competitiveness Pareto frontier.

5 Robustness

Till now, the performance of an algorithm has been evaluated along two dimensions: (i) consistency considers the performance of an online algorithm when the instance conforms to the advice (); and (ii) competitiveness considers the performance of an online algorithm on all instances. In practice, we would also like our online algorithm to perform well in the vicinity of the advice . To that end, in this section, we show that the performance of protection level policies degrades gracefully as the instance deviates from the advice; and a natural modification of Algorithm 1 also exhibits graceful performance degradation when the instance is close to conforming with the advice. We begin by defining a notion of dissimilarity (or distance) between the instance and the advice, which will allow us to quantify the robustness to deviations. The distance between an advice and an instance is given by

| (3) |

where represents the number of customers of fare type in instance , and, as before, is the lowest fare that forms a part of . The definition of is motivated by the following equivalence: if and only if , i.e., conforms to advice . Recall that we use to denote the total revenue collected by the protection level policy with protection levels . The following result shows that the performance of protection level policies degrades smoothly as a function of the distance between the instance and the advice.

Theorem 4.

For every advice , instance and protection levels , we have

We can leverage Theorem 4 to show that the optimal protection levels returned by Algorithm 2 are robust to deviations in the advice.

Corollary 1.

Let be the protection levels returned by Algorithm 2 when given required level of competitiveness , advice and approximation parameter as input. Then, for every instance , we have .

Next, for , we define a variation of Algorithm 1 called the -relaxed LP-based Optimal Algorithm through the following changes:

-

•

Set instead of .

-

•

Replace the trigger condition ‘If and for some ’ in Step 2 with ‘If and for some ’.

The rest of the algorithm is identical to Algorithm 1 (The precise algorithm can be found in Appendix E). Recall that Algorithm 1 keeps track of the rejections, and changes the trigger from to when the rejection-capacity is exceeded. The intuition behind it being that if the deviation of the instance from the advice large enough to exceed the rejection capacity, then the advice is not accurate and we no longer need to focus on ensuring consistency. But, in the worst-case, this does not give the machine-learning algorithm which generates the advice much room for error.

The -relaxed Algorithm 1 resolves this issue by increasing the rejection capacity by . As long as the advice was good enough for the instance to satisfy , the -relaxed Algorithm 1 would continue to aim for consistency. The next theorem establishes that this makes the -relaxed Algorithm 1 robust to deviations from the advice.

6 Numerical Experiments

In this section, we numerically evaluate the performance of the LP-based optimal algorithm (Algorithm 1) and the optimal protection level policy (Algorithm 2) on a variety of advice and problem parameters. We do so with two central goals in mind: (i) comparing the performance of the two algorithms; (ii) evaluating the robustness of both algorithms, by computing the expected performance of both algorithms when the instance is drawn from a distribution centered on the advice. In this section, we will use the consistency of the -competitive protection level policy of Ball and Queyranne (2009) as a benchmark, which is equal to , where are the protection levels used by the policy of Ball and Queyranne (2009). Note that the consistency-competitiveness frontier of the policy of Ball and Queyranne (2009) is always a point because the algorithm has a fixed competitiveness. However, in general we do have that its consistency satisfies because the algorithm of Ball and Queyranne (2009) performs better on instances that are well behaved. Moreover, consistency of their algorithm always lies entirely below the lowest point of the consistency-competitiveness frontier of the optimal protection level policy (Algorithm 2) by virtue of our algorithm being optimal. In other words, for every advice , the consistency of the policy of Ball and Queyranne (2009) is always less than . Based on this observation, it comes as no surprise that the LP-based optimal algorithm (Algorithm 1) and the optimal protection level policy (Algorithm 2) have much higher consistency than the policy of Ball and Queyranne (2009), which is oblivious to the advice. Throughout this section, we fix the capacity to be .

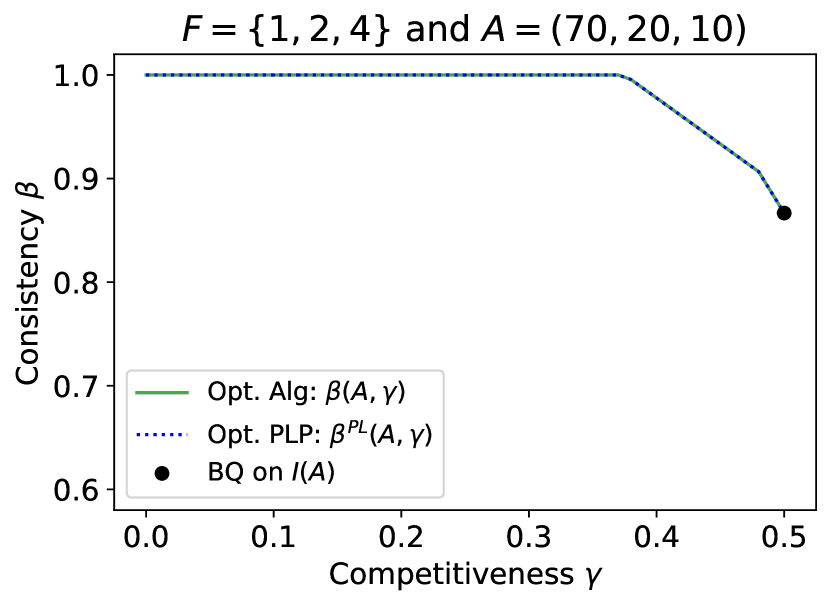

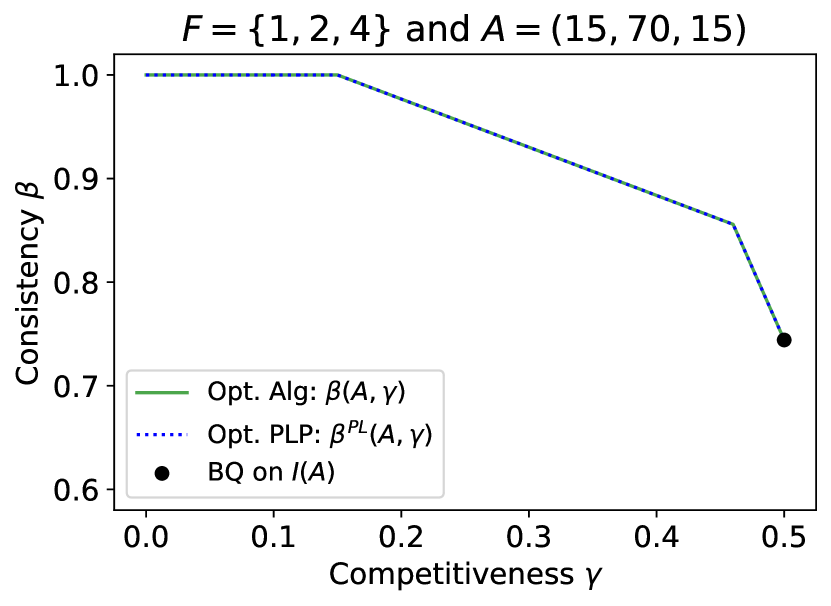

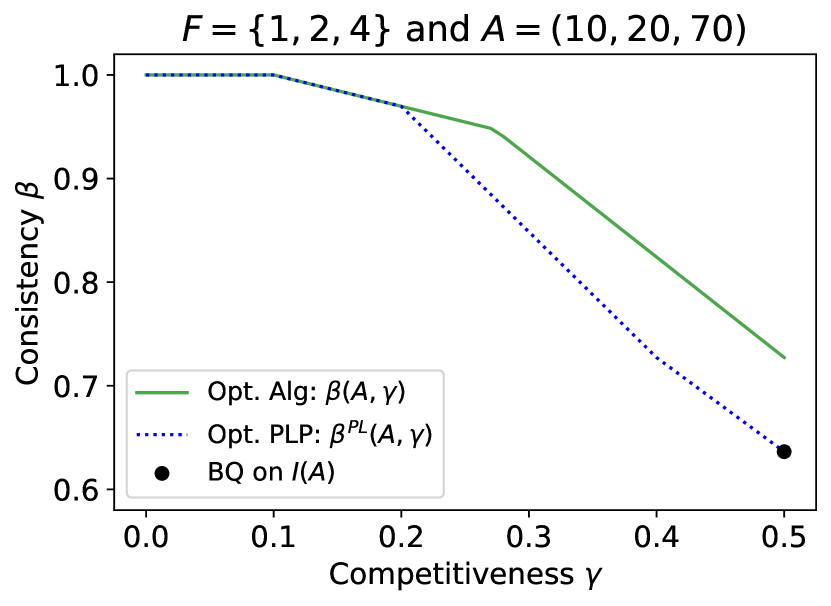

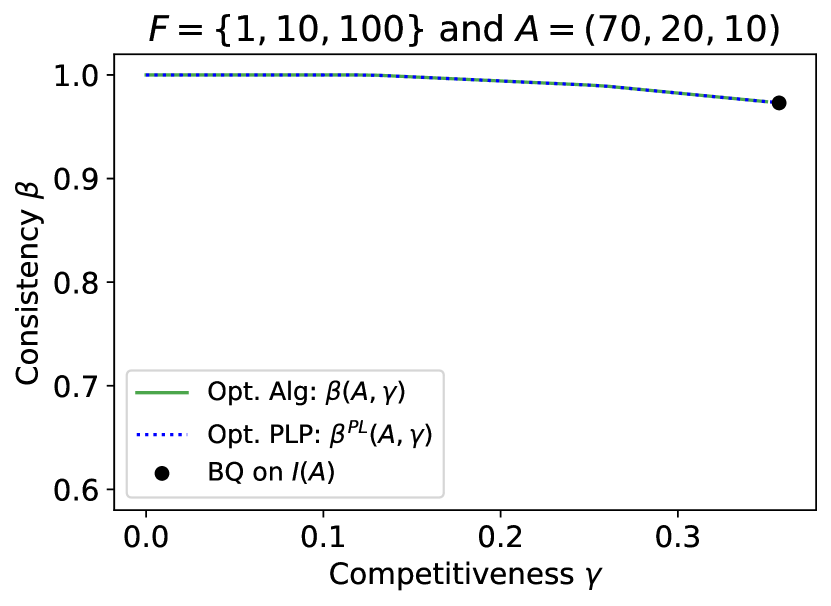

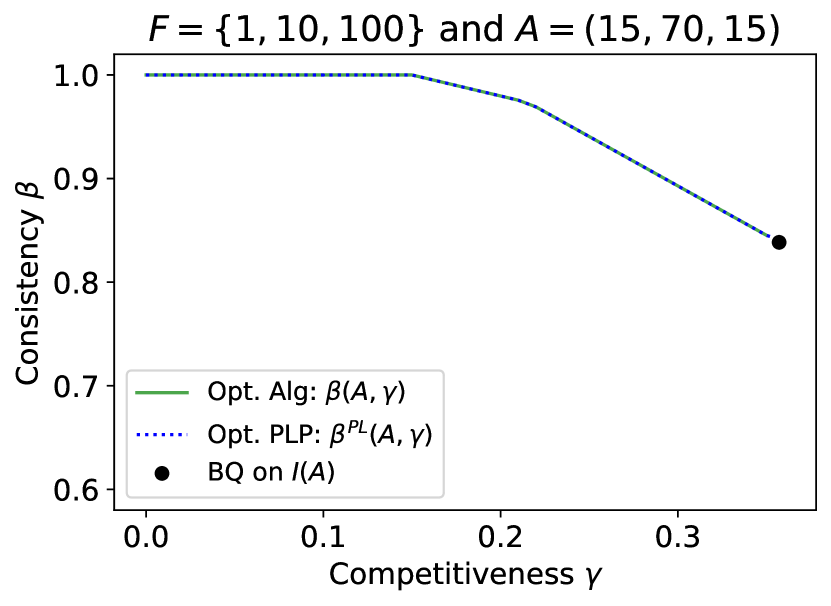

6.1 Comparing the Policies

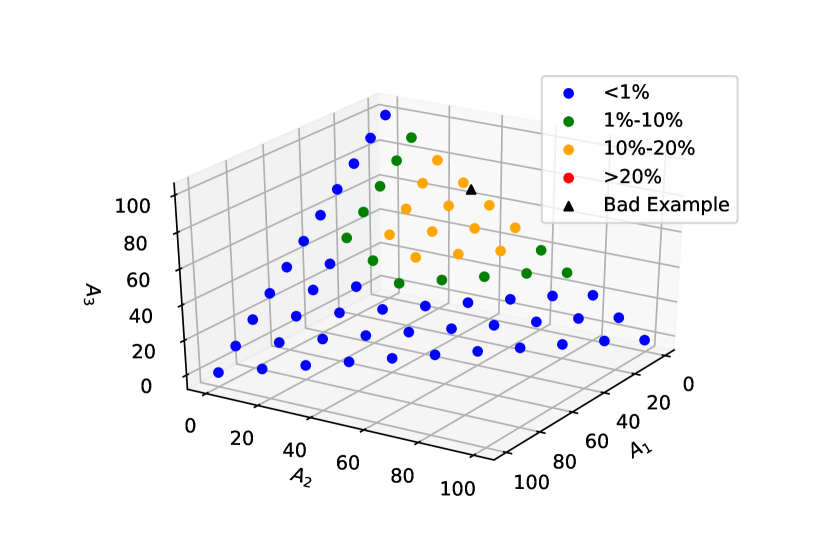

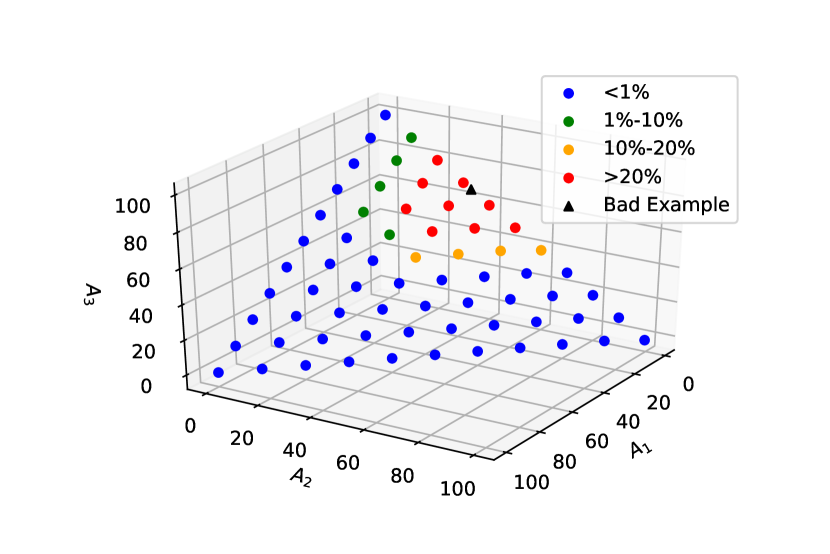

In Figure 4, we plot the consistency-competitiveness performance frontiers of the LP-based optimal algorithm (Algorithm 1), represented by , and that of the optimal protection level policy, represented by and computed using Algorithm 2. We do so for two sets of fares: (i) fares that are close to each other, as represented by with ; (ii) fares that are well-separated, represented by with . Moreover, we also vary the advice by how much weight it puts on the different fare classes. These plots indicate that protection level policies are only sub-optimal when the advice is similar to the bad example discussed in Subsection 4.2. To explore this trend further, we define the notion of relative sub-optimality of protection level policies for every advice as

We evaluated for the grid of advice composed of all advice that satisfy 222With the following modification: whenever , we we set and reduce by 1. This change is introduced to make the advice more similar to the bad example of Subsection 4.2. We classified this grid of advice based on relative sub-optimality, represented by the different colors in Figure 5. We found that the relative sub-optimality is less than for a large majority of the advice. Moreover, we also found that the relative sub-optimality is high for advice that makes the optimal protection level policy overcommit (see Subsection 4.2). To demonstrate this, we also plot the bad example (Example 3) of Subsection 4.2 which is designed to make the optimal protection level policy overcommit. We found that the relative sub-optimality increases with the proximity to this example. Moreover, we performed this evaluation of the relative sub-optimality for two sets of fares: (i) Fares that are close to each other, as represented by ; (ii) Fares that are well-separated, represented by with . We found that the sub-optimality increases with the separation of the fares, but not too greatly. Finally, we also found that, across all the values of advice and fares we considered, the maximum value of the relative sub-optimality was always less than . Our experiments suggest that the optimal protection level policy performs remarkably well on most advice, only exhibiting sub-optimality when the advice compels it to overcommit. In the next section, we continue with the comparison between the two policies with the added dimension of robustness.

6.2 Robustness

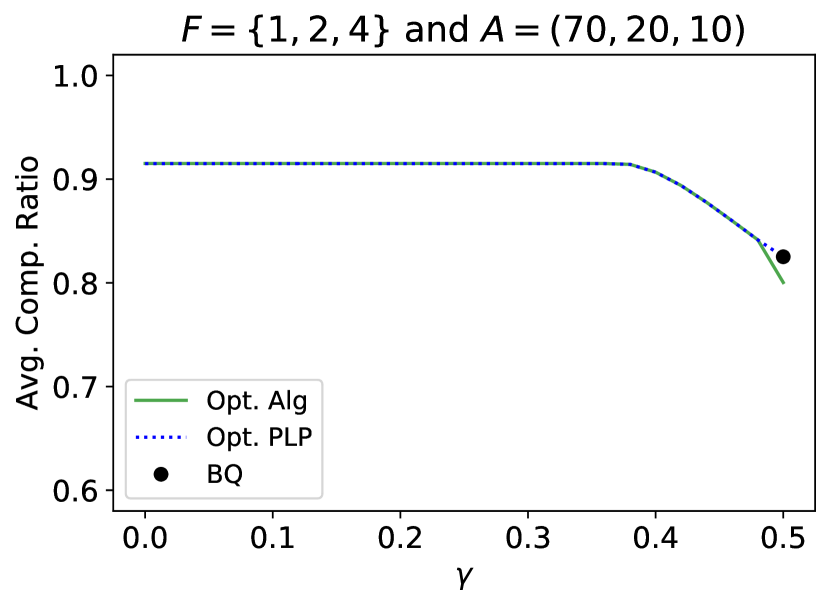

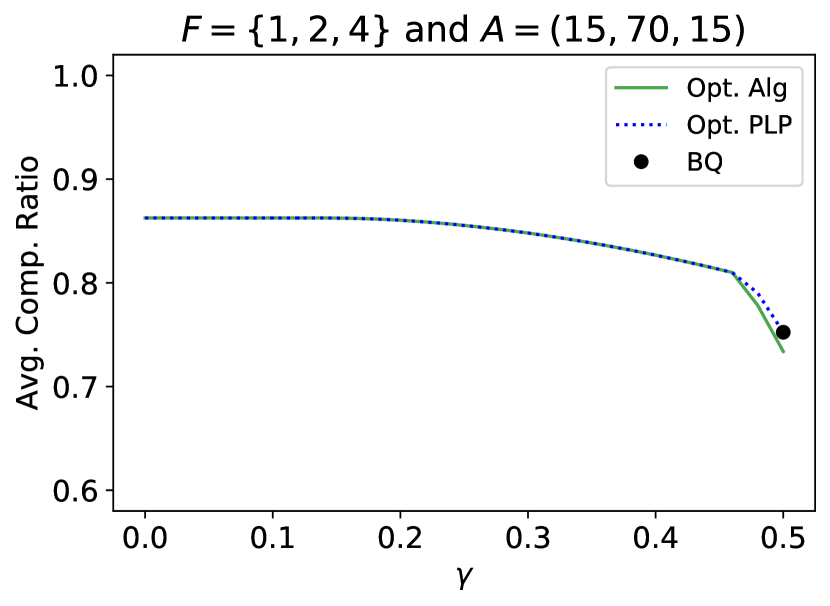

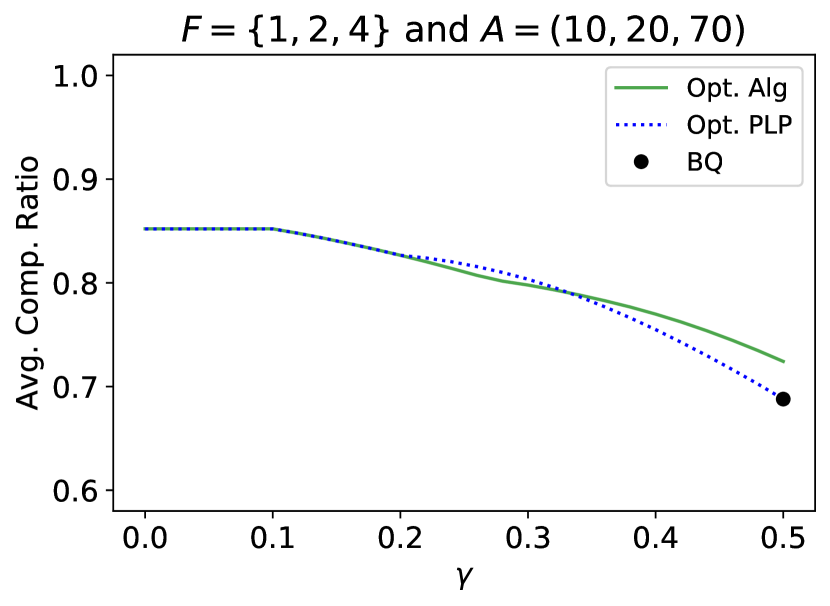

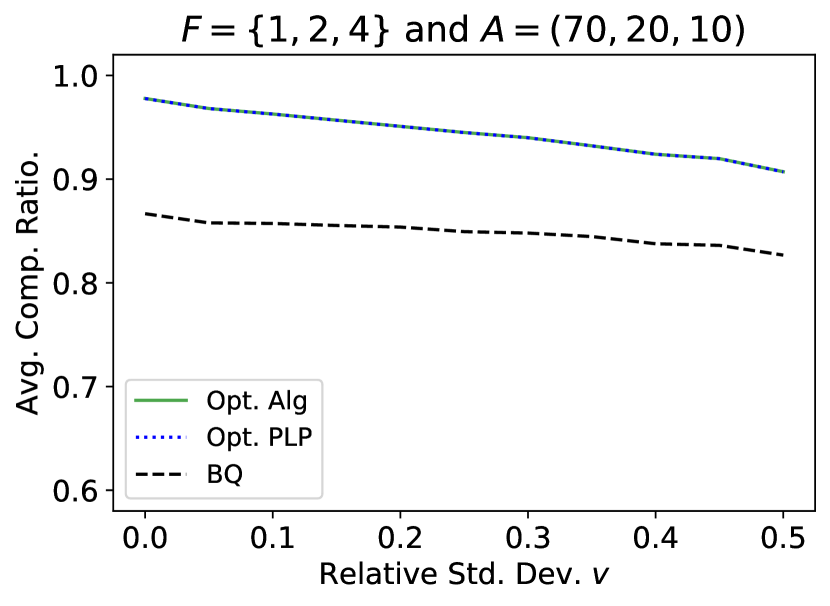

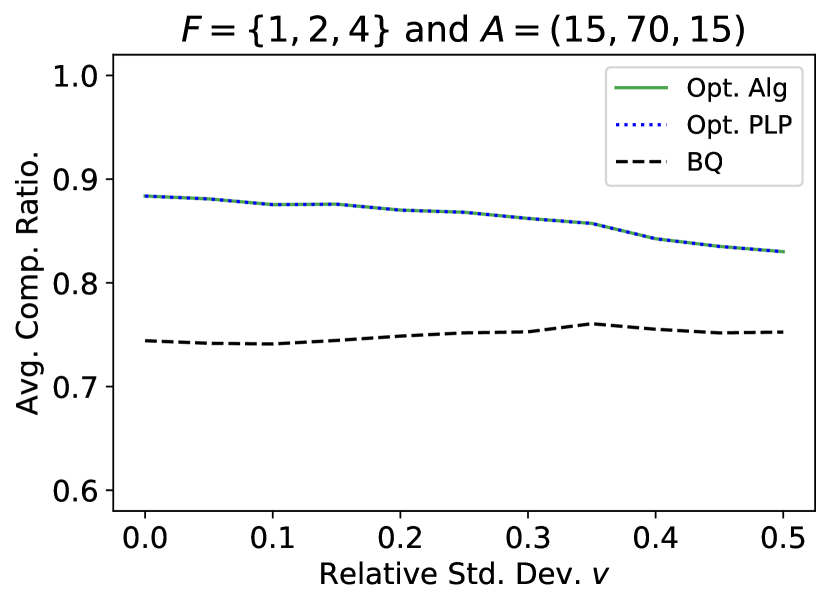

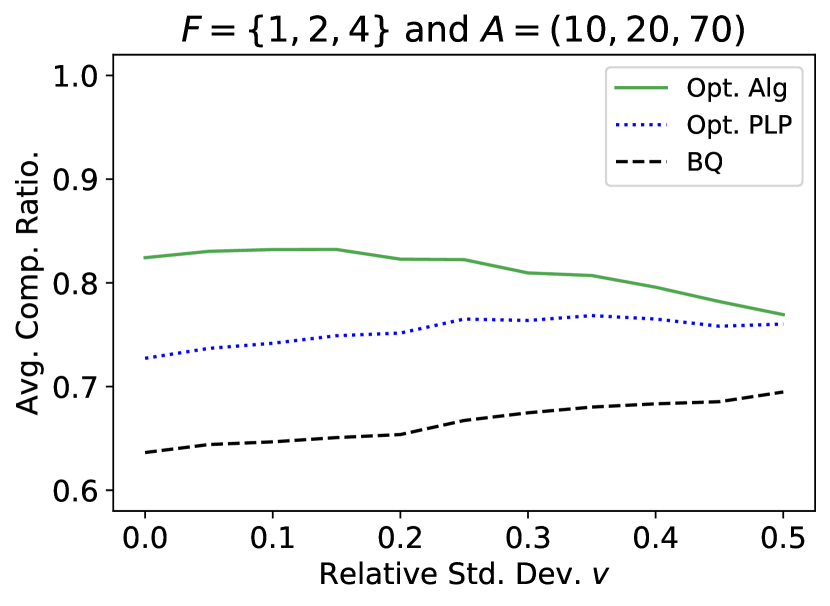

In this subsection, we evaluate the robustness of the LP-based optimal algorithm (Algorithm 1) and the optimal protection level policy (Algorithm 2) in a variety of settings. To do so, given advice , we generated random instances centered on the advice as follows: (i) For each fare class with , we draw , where and for some coefficient of variation (also called relative standard deviation); (ii) To get a non-negative integer value, we set for , and set to make sure that the capacity can be filled; (iv) We string together fares of type in increasing order to construct an instance . We fix the fares to be (which implies ) and the capacity to be . Moreover, we consider three different advice given by . In our first experiment on robustness, we set the coefficient of variation and drew 1000 instances for each advice. We computed the average competitive ratio of the algorithms on these instances as a function of (Algorithm 1 and Algorithm 2 were given the advice as the input). The results are shown in Figure 6. As the figure shows, even when the instances have relative noise compared to the advice, our algorithms continue to perform better than the policy of Ball and Queyranne (2009). Moreover, we find the difference in performance between the LP-based optimal policy and the optimal protection level policy reduces in the presence of noise even for advice that makes the optimal protection level policy overcommit in the absence of noise. We note that, for advice and , the performance of the LP-based optimal algorithm is identical to that of the optimal protection level policy because the optimal protection level policy is optimal in the absence of noise (see Figure 4), which leads ‣ 3.2 to return a solution that mimics the optimal protection levels. In our second experiment on robustness, we fixed and changed the noise in the instances by altering the coefficient of variation. In Figure 7, we plot the average competitive ratio (averaged over 1000 instances sampled using the aforementioned procedure) as a function of the coefficient of variation. The results indicate that the performance of our algorithms degrades gracefully with the noise in the instance generating process. It is important to note that we did not use the robust version of our LP-based optimal algorithm described in Section 5, which boasts stronger theoretical robustness guarantees.

7 Conclusion and Future Work

In this work, we look at the single-leg revenue management problem through the lens of Algorithms with Advice. We describe an optimal procedure for incorporating advice using an LP-based algorithm (Algorithm 1). Moreover, we also provide an efficient method for optimally incorporating advice into protection level policies, which is the most widely-used class of algorithms in practice. Our algorithms are simple, efficient and easy to implement. We believe that our optimal protection level policy should be relatively straightforward to implement on top of the existing infrastructure of airlines and hotels, which heavily rely on protection level policies. We hope that the algorithmic insights developed in this work can make these systems more robust to prediction errors.

We leave open the question of incorporating advice that dynamically changes with time. In practice, our algorithms can be repeatedly used with the updated advice on the remaining capacity, but our results do not capture their performance under arbitrary dynamic advice. Like many of the previous works on algorithms with advice, we also consider deterministic advice. This is motivated by the fact that most machine-learning models make point predictions. Our robustness guarantees allow us to bound the performance for distributions centered on the advice, but it would be interesting to analyze distributional advice, especially one which is updated in a Bayesian manner across time. Furthermore, we leave extensions of our results to network revenue management problems with multiple resources for future work.

References

- Agrawal et al. (2014) Shipra Agrawal, Zizhuo Wang, and Yinyu Ye. A dynamic near-optimal algorithm for online linear programming. Operations Research, 62(4):876–890, 2014.

- Alaei et al. (2012) Saeed Alaei, MohammadTaghi Hajiaghayi, and Vahid Liaghat. Online prophet-inequality matching with applications to ad allocation. In Proceedings of the 13th ACM Conference on Electronic Commerce, pages 18–35, 2012.

- Antoniadis et al. (2020) Antonios Antoniadis, Themis Gouleakis, Pieter Kleer, and Pavel Kolev. Secretary and online matching problems with machine learned advice. Advances in Neural Information Processing Systems, 33:7933–7944, 2020.

- Aouad and Ma (2022) Ali Aouad and Will Ma. A nonparametric framework for online stochastic matching with correlated arrivals. arXiv preprint arXiv:2208.02229, 2022.

- Ball and Queyranne (2009) Michael O Ball and Maurice Queyranne. Toward robust revenue management: Competitive analysis of online booking. Operations Research, 57(4):950–963, 2009.

- Balseiro and Gur (2019) Santiago R Balseiro and Yonatan Gur. Learning in repeated auctions with budgets: Regret minimization and equilibrium. Management Science, 65(9):3952–3968, 2019.

- Brumelle and McGill (1993) Shelby L Brumelle and Jeffrey I McGill. Airline seat allocation with multiple nested fare classes. Operations research, 41(1):127–137, 1993.

- Devanur and Hayes (2009) Nikhil R Devanur and Thomas P Hayes. The adwords problem: online keyword matching with budgeted bidders under random permutations. In Proceedings of the 10th ACM conference on Electronic commerce, pages 71–78, 2009.

- Dinitz et al. (2021) Michael Dinitz, Sungjin Im, Thomas Lavastida, Benjamin Moseley, and Sergei Vassilvitskii. Faster matchings via learned duals. Advances in Neural Information Processing Systems, 34, 2021.

- Dütting et al. (2021) Paul Dütting, Silvio Lattanzi, Renato Paes Leme, and Sergei Vassilvitskii. Secretaries with advice. In Proceedings of the 22nd ACM Conference on Economics and Computation, pages 409–429, 2021.

- Esfandiari et al. (2015) Hossein Esfandiari, Nitish Korula, and Vahab Mirrokni. Online allocation with traffic spikes: Mixing adversarial and stochastic models. In Proceedings of the Sixteenth ACM Conference on Economics and Computation, pages 169–186, 2015.

- Feldman et al. (2009) Jon Feldman, Nitish Korula, Vahab Mirrokni, Shanmugavelayutham Muthukrishnan, and Martin Pál. Online ad assignment with free disposal. In International workshop on internet and network economics, pages 374–385. Springer, 2009.

- Feldman et al. (2010) Jon Feldman, Monika Henzinger, Nitish Korula, Vahab S Mirrokni, and Cliff Stein. Online stochastic packing applied to display ad allocation. In European Symposium on Algorithms, pages 182–194. Springer, 2010.

- Gallego and Topaloglu (2019) Guillermo Gallego and Huseyin Topaloglu. Revenue management and pricing analytics, volume 209. Springer, 2019.

- Golrezaei et al. (2022) Negin Golrezaei, Patrick Jaillet, and Zijie Zhou. Online resource allocation with samples. arXiv preprint arXiv:2210.04774, 2022.

- Huh and Rusmevichientong (2006) Woonghee Tim Huh and Paat Rusmevichientong. Adaptive capacity allocation with censored demand data: Application of concave umbrella functions. Technical report, Technical report, Cornell University, School of Operations Research and …, 2006.

- Hwang et al. (2021) Dawsen Hwang, Patrick Jaillet, and Vahideh Manshadi. Online resource allocation under partially predictable demand. Operations Research, 69(3):895–915, 2021.

- Karp et al. (1990) Richard M Karp, Umesh V Vazirani, and Vijay V Vazirani. An optimal algorithm for on-line bipartite matching. In Proceedings of the twenty-second annual ACM symposium on Theory of computing, pages 352–358, 1990.

- Kleinberg (2005) Robert Kleinberg. A multiple-choice secretary algorithm with applications to online auctions. In Proceedings of the sixteenth annual ACM-SIAM symposium on Discrete algorithms, pages 630–631. Citeseer, 2005.

- Kunnumkal and Topaloglu (2009) Sumit Kunnumkal and Huseyin Topaloglu. A stochastic approximation method for the single-leg revenue management problem with discrete demand distributions. Mathematical Methods of Operations Research, 70(3):477, 2009.

- Lan et al. (2008) Yingjie Lan, Huina Gao, Michael O Ball, and Itir Karaesmen. Revenue management with limited demand information. Management Science, 54(9):1594–1609, 2008.

- Lautenbacher and Stidham Jr (1999) Conrad J Lautenbacher and Shaler Stidham Jr. The underlying markov decision process in the single-leg airline yield-management problem. Transportation science, 33(2):136–146, 1999.

- Lee and Hersh (1993) Tak C Lee and Marvin Hersh. A model for dynamic airline seat inventory control with multiple seat bookings. Transportation science, 27(3):252–265, 1993.

- Littlewood (2005) Ken Littlewood. Special issue papers: Forecasting and control of passenger bookings. Journal of Revenue and Pricing Management, 4(2):111–123, 2005.

- Lykouris and Vassilvtiskii (2018) Thodoris Lykouris and Sergei Vassilvtiskii. Competitive caching with machine learned advice. In International Conference on Machine Learning, pages 3296–3305. PMLR, 2018.

- Ma et al. (2021) Will Ma, David Simchi-Levi, and Chung-Piaw Teo. On policies for single-leg revenue management with limited demand information. Operations Research, 69(1):207–226, 2021.

- Mahdian et al. (2012) Mohammad Mahdian, Hamid Nazerzadeh, and Amin Saberi. Online optimization with uncertain information. ACM Transactions on Algorithms (TALG), 8(1):1–29, 2012.

- Mehta et al. (2007) Aranyak Mehta, Amin Saberi, Umesh Vazirani, and Vijay Vazirani. Adwords and generalized online matching. Journal of the ACM (JACM), 54(5):22–es, 2007.

- Mehta et al. (2013) Aranyak Mehta et al. Online matching and ad allocation. Foundations and Trends® in Theoretical Computer Science, 8(4):265–368, 2013.

- Mirrokni et al. (2012) Vahab S Mirrokni, Shayan Oveis Gharan, and Morteza Zadimoghaddam. Simultaneous approximations for adversarial and stochastic online budgeted allocation. In Proceedings of the twenty-third annual ACM-SIAM symposium on Discrete Algorithms, pages 1690–1701. SIAM, 2012.

- Mitzenmacher (2019) Michael Mitzenmacher. A model for learned bloom filters, and optimizing by sandwiching. arXiv preprint arXiv:1901.00902, 2019.

- Mitzenmacher (2021) Michael Mitzenmacher. Queues with small advice. In SIAM Conference on Applied and Computational Discrete Algorithms (ACDA21), pages 1–12. SIAM, 2021.

- Mitzenmacher and Vassilvitskii (2020) Michael Mitzenmacher and Sergei Vassilvitskii. Algorithms with predictions, 2020.

- Purohit et al. (2018) Manish Purohit, Zoya Svitkina, and Ravi Kumar. Improving online algorithms via ml predictions. Advances in Neural Information Processing Systems, 31:9661–9670, 2018.

- Robinson (1995) Lawrence W Robinson. Optimal and approximate control policies for airline booking with sequential nonmonotonic fare classes. Operations Research, 43(2):252–263, 1995.

- Rohatgi (2020) Dhruv Rohatgi. Near-optimal bounds for online caching with machine learned advice. In Proceedings of the Fourteenth Annual ACM-SIAM Symposium on Discrete Algorithms, pages 1834–1845. SIAM, 2020.

- Talluri and Van Ryzin (2004) Kalyan T Talluri and Garrett Van Ryzin. The theory and practice of revenue management, volume 1. Springer, 2004.

- Van Ryzin and McGill (2000) Garrett Van Ryzin and Jeff McGill. Revenue management without forecasting or optimization: An adaptive algorithm for determining airline seat protection levels. Management Science, 46(6):760–775, 2000.

- Zhou et al. (2008) Yunhong Zhou, Deeparnab Chakrabarty, and Rajan Lukose. Budget constrained bidding in keyword auctions and online knapsack problems. In International Workshop on Internet and Network Economics, pages 566–576. Springer, 2008.

Appendix A Application to the Online Knapsack Problem

Consider an online knapsack problem where the possible weights are with and the possible item rewards are . Define the corresponding set of possible fares . Extending our definition of advice for the single-leg revenue management problem, we will assume that the advice for the online knapsack problem specifies the total number of the different types of items that are predicted to form the optimal solution. Construct the corresponding advice for single-leg revenue management problem as follows: If units of item are predicted to be a part of the optimal solution in , then customers with fare are predicted to be in . Moreover, given an instance for the online knapsack problem, construct an instance for the single-leg revenue management problem as follows: Iterate over and for each item in the instance , add customers with fare to . These constructions ensure that and . Therefore, it is easy to see that when we run our algorithm on with advice and translate the decisions to online knapsack by accepting the corresponding fraction of each item, we achieve the same revenue bounds for the online knapsack problem.

Appendix B Rounding Error