Pattern recovery and signal denoising by SLOPE when the design matrix is orthogonal 111The authors want to thank Małgorzata Bogdan, Patrick Tardivel, Wojciech Rejchel and Tomasz Żak for references, comments and discussion. The authors are thankful to anonymous referee for simplifying the proof of Lemma 3.1. First Author was supported by a French Government Scholarship. Research of the first and the second author was supported by Centre Henri Lebesgue, program ANR-11-LABX-0020-0.

Streszczenie

Sorted Penalized Estimator (SLOPE) is a relatively new convex regularization method for fitting high-dimensional regression models. SLOPE allows to reduce the model dimension by shrinking some estimates of the regression coefficients completely to zero or by equating the absolute values of some nonzero estimates of these coefficients. This allows to identify situations where some of true regression coefficients are equal. In this article we will introduce the SLOPE pattern, i.e., the set of relations between the true regression coefficients, which can be identified by SLOPE. We will also present new results on the strong consistency of SLOPE estimators and on the strong consistency of pattern recovery by SLOPE when the design matrix is orthogonal and illustrate advantages of the SLOPE clustering in the context of high frequency signal denoising.

1 Introduction

1.1 Introduction and motivations

The Linear Multiple Regression concerns the model , where is an output vector, is a fixed design matrix, is an unknown vector of predictors and is a noise vector. The primary goal is to estimate . In the low-dimensional setting, i.e., when the number of predictors is not larger than the number of explanatory variables and is of full rank, the ordinary least squares estimator has an exact formula . For practical reasons there is an urge to avoid the high-dimensionality curse, therefore we want the estimate to be sparse, i.e., to be descriptible by a smaller number of parameters. Several solutions were proposed to deal with such problem. One of them, the Least Absolute Shrinkage and Selection Operator (LASSO [7, 24]) involves penalizing the residual sum of squares with an norm of multiplied by a tuning parameter :

The LASSO estimator is not unbiased, but is a shrinkage estimator which shrinks some completely to zero, resulting in a sparser estimate. In the case of being an orthogonal matrix, i.e. , the exact formula for introduced by Tibshirani [24] is based on :

Another approach to reduce the dimensionality is the Sorted Penalized Estimator

(SLOPE [3, 2, 25]), which not only generalizes the LASSO method, but also allows to clusterize the similar coefficients of . In SLOPE, -norm is replaced by its sorted version , which depends on the tuning vector , where :

where is a decreasing permutation of absolute values of :

The case of being an arithmetic sequence was studied by Bondell and Reich [5] and called the Octagonal Shrinkage and Clustering Algorithm for Regression (OSCAR). The special case of SLOPE with is LASSO. For we obtain the OLS estimator.

Clustering the predictors allows for additional dimension reduction by identifying variables with the same absolute values of regression coefficients.

One may recently observe the rise of interest in methods, which cluster highly correlated predictors [6, 12, 14, 17, 18, 23]. SLOPE is ideal for this task, since it is capable to identify the low-dimensional structure, which is called the SLOPE pattern, defined by Schneider and Tardivel with the subdifferential of the SLOPE norm [20]. For the convention of this article we let .

As we will denote the number of clusters of i.e., the number of nonzero components of .

Definition 1.0.1 (SLOPE pattern [4]).

The SLOPE pattern is a function

such that

where is a rank of in a vector of distinct nonzero values among . We adopt the convention that .

As we denote the set of all possible SLOPE patterns of .

Fact 1.0.1 (Basic properties of SLOPE pattern [20]).

-

(a)

for every there exists such that ,

-

(b)

(sign preservation),

-

(c)

(cluster preservation),

-

(d)

(hierarchy preservation).

Example 1.0.1.

.

Remark 1.0.1 (Subdifferential description of the SLOPE pattern [20]).

Let satisfy . Then

where is a subdifferential of the function at , i.e.:

The subdifferential approach may be applied to a wider class of penalizers being polyhedral gauges, cf. [22].

Definition 1.0.2 (Pattern recovery by SLOPE).

We say that the SLOPE estimator recovers the pattern of when

The clustering properties of SLOPE have been studied before, cf. [5, 11], but the researchers consider strongly correlated predictors, which are being used in financial mathematics to group the assets with respect to their partial correlation with the hedge fund return times series [13]. In our article we decided to suppose the orthogonal design

| (1) |

This is a classical and natural assumption in the case where n and p are fixed, cf. [24]. Moreover, in the asymptotic case, where and is fixed, it is usually supposed that , cf. [26, 27]. In (1) the design matrix is orthogonal.

Then, the Euclidean norm of each -dimensional column of equals . If it was , the terms of would vanish to zero for large , which is not natural.

Such class of matrices is being widely used in signal analysis, [19, 8]. For general the problem is considered in our parallel article [4].

To study the properties of SLOPE we often use the closed unit ball in the dual norm of , which was studied e.g. by Zeng and Figueiredo [25]. This dual ball is described explicitely as a signed permutahedron, see e.g. [16, 20].

| (2) |

In this article we prove novel results on the strong consistency of SLOPE both in estimation and in pattern recovery. We also introduce a new, based on minimaxity, approach to relations between and .

1.2 Outline of the paper

In Section 2 we derive the connections between and in the orthogonal design. We use the minimax theorem of Sion, cf. [1]. In Section 3 we focus on the properties of . We use the geometric interpretation of SLOPE to explain its ability to identify the SLOPE pattern and provide new theoretical results on the support recovery and clustering properties using a representation of SLOPE as a function of the ordinary least squares (OLS) estimator. Similar approach for LASSO was used by Ewald and Schneider, cf. [10].

To analyze the asymptotic properties of the SLOPE estimator, e.g. its consistency, we have to assume that the sample size tends to infinity. Therefore, in Section 4 we define a sequence of linear regression models

In this sequence, the response vector , the design matrix and the error term vary with .

The error term has the normal distribution . We make no assumptions about the relations between and for .

In this paper we consider the specific, but statistically important model in which and columns of are orthogonal. The orthogonality assumption allows us to derive, by simple techniques, relatively precise results on the SLOPE estimator (e.g. Theorem 3.1 theorem), which seems unavailable when columns of are not orthogonal.

Substantially more difficult techniques based on subdifferential calculus are developed in [4]. These techniques are used in [4] to establish the properties of the SLOPE estimator in the general case, where the columns of are not orthogonal and may be much larger than . In the asymptotic theorem proved in [4] under different assumptions on stronger restrictions on tuning are considered.

We provide the conditions under which the SLOPE estimator is strongly consistent. Additionally, in case when for each the design matrix is orthogonal, we provide the conditions on the sequence of tuning parameters such that SLOPE is strongly consistent in the pattern recovery.

In Section 5 we show the applications of the SLOPE clustering in terms of high frequency signal denoising and illustrate them with simulations.

The Appendix covers the proofs of technical results.

2 Approach by minimax theorem

2.1 Technical results

Let denote the minimum value of the SLOPE criterion, attained by , i.e.

Since

it follows that

We immediately get the following result.

Corollary 2.0.1.

, where .

From this corollary it is seen that we can clearly limit our search to vectors from the compact set defined by . Therefore, we can equivalently define a SLOPE solution by

| (3) |

Proposition 2.0.1.

Let be the unit ball in the dual SLOPE norm. Then, for each ,

| (4) |

The proof is a simple application of the definition of the dual norm and the reflexivity of . Thus

2.2 Saddle point

Let the function be defined by

As an immediate consequence of ((3)) and Proposition 2.0.1 we obtain

It turns out that the order of the maximization over and the minimization over can be switched without affecting the result. To see this, note that both and are convex and compact. Moreover, for each fixed , is a convex continuous function with respect to and, for each fixed , is concave with respect to (in fact, it is linear). Therefore, all assumptions of the Sion’s minimax theorem are fulfilled (see [1, p. 218]) and thus there exists a saddle point such that

In the next section we shall see that the first coordinate of any saddle point is the SLOPE estimator.

2.3 SLOPE solution for the orthogonal design

Since for each fixed , the function is convex with respect to , any point , at which the gradient is zero, is a global minimum. If we rewrite as

and differentiate with respect to , we obtain

Equating this gradient to gives the following equation for the optimum point :

| (5) |

Substituting this into the equation for , we find that

Let be the number of elements of the cluster of , and .

Lemma 2.1.

Let be any solution of

and let be the corresponding point from given by

Then, , for all and hence

-

(a)

, ,

-

(b)

and are similarly sorted, i.e.

if , then , -

(c)

for any permutation satisfying , if there is a such that ,

then .

The proof is given in the Appendix. An immediate consequence of the Lemma is the following result.

Lemma 2.2.

The point defined as in Lemma 2.1 is the saddle point of the function .

The proof is given in the Appendix. We use the last lemma to prove the main result of this section.

Theorem 2.3.

Let the point be defined as in Lemma 2.1. Then is the SLOPE estimator of .

Dowód.

Using the fact that (see previous lemma) we have

Corollary 2.3.1.

In the linear model satisfying we have

is the proximal projection of onto .

Projections onto are widely used in [15] in the study of the notion of degrees of freedom. However, the Corollary 2.3.1 is not stated there explicitely.

Remark 2.3.1.

3 Properties of SLOPE in the orthogonal design

3.1 SLOPE vs. OLS

By the Theorem 2.3 and Corollary 2.3.1, when

, the orthogonal projection of the ordinary least squares estimator

onto the unit ball is equal to .

For and this property is illustrated on Figure 1.

The figure represents (black arrows) depending on the localization of in the orthogonal design. For being the blue point located on the area labelled by the first component of is positive and the second is null.

For being the yellow point located on the area labelled by both components of have equal absolute value (clusterization), but their signs are opposite. For being the red point located on the area labelled by both components of are positive and the first component is smaller than the second one. The blue polytope is the dual SLOPE unit ball and labels

associated to the areas of this figure correspond to all SLOPE patterns for

and .

In the orthogonal design, one may also explicitly compute the SLOPE estimator. Indeed, by the Corollary 2.3.1, is the image of by the proximal operator of the SLOPE norm. Therefore, this operator has a closed form formula [2, 21, 9]. This explicit expression gives an analytical way to learn that SLOPE solution is sparse and built of clusters.

Lemma 3.1.

In the linear model satisfying we have

| (6) |

As (6) is not proven in [3, Equation (1.14)], we give the proof in the Appendix. The next theorem gives a sufficient condition for the clustering effect of the SLOPE estimator in the orthogonal design.

Theorem 3.2.

Consider a linear model with orthogonal design

. Let be a permutation of such that

For ,

if , then .

Dowód.

In the following theorem we derive necessary and sufficient conditions under which SLOPE in the orthogonal design recovers the support of the vector , i.e.

Theorem 3.3.

Under orthogonal design , let be a permutation of satisfying . Without loss of generality suppose that with . The necessary and sufficient condition for SLOPE to identify the set of relevant covariables is:

-

(a) ,

-

(b) ,

-

(c)

4 Asymptotic properties of SLOPE

In this section we discuss several asymptotic properties of SLOPE estimators in the low-dimensional regression model in which is fixed and the sample size tends to infinity. For each we consider a linear model

| (7) |

where is a vector of observations, is a deterministic design matrix with , is a vector of unknown regression coefficients and is a noise term, which has the normal distribution . We make no assumptions about the dependence between and for . In particular, does not need to be a subsequence of .

When defining the sequence of SLOPE estimators, we assume that the tuning vector varies with . More precisely, for each its coefficients are fixed and .

By we denote the SLOPE estimator corresponding to the tuning vector :

| (8) |

4.1 Strong consistency of the SLOPE estimator

Let us recall the definition of a strongly consistent estimator of , i.e. we have almost surely.

Below we discuss consistency of the sequence of SLOPE estimators, defined by (8).

Theorem 4.1.

Consider the linear regression model (7) and assume that

where is a positive definite matrix. Let , , be the SLOPE estimator corresponding to the tuning vector .

-

(a)

If , then .

-

(b)

If , then is not strongly consistent for .

Before proving the above theorems we start with stating a simple technical lemma. It follows quickly from the Borel-Cantelli Lemma and the tail inequality:

If , then , .

Lemma 4.2.

Assume that is a sequence of Gaussian random variables, defined on the same probability space, which converges in distribution to for some . Then, for any ,

Our proof of the strong consistency of SLOPE is based on the strong consistency of the OLS estimator. The latter result is a folklore and we prove it in our setting.

Proposition 4.2.1.

Consider the linear regression model (7).

If , where is positive definite, then .

Dowód.

Proof of Theorem 4.1.

(a) It follows from Theorem 2.1 that there exists a vector such that

Since takes values in , it follows that . Hence,

| (9) |

because . The assumption that implies that the matrix is invertible and hence the least squares estimator of is unique and has the form . Combining with ((9)) the fact that , we conclude that

(b) Since minimizes over the function

and since , it follows that

The last equality follows from the fact that .

Suppose to the contrary that . Then, using the facts that

and that , we have

For this provides a contradiction since the inequality does not hold when the value of is sufficiently close to . ∎

Remark 4.2.1.

The proof of Theorem 4.1 (b) does not exclude that for large enough.

However, the definition of strong consistency requires the convergence for any value of the parameter . We prove that if true parameter satisfies and , then is not convergent for .

4.2 Asymptotic pattern recovery in the orthogonal design

We again consider a sequence of linear models ((7)) but this time we assume that for each the deterministic design matrix of size satisfies

| (10) |

As usual, we assume Gaussian errors, .

Let be the SLOPE estimator defined by (8). With the above notation we present the main result of this section.

Theorem 4.3.

Assume that

and that there exists such that

| (11) |

Then we have

Note that above conditions are satisfied e.g. by .

Dowód.

Without loss of generality we may assume that and . Indeed, we can always achieve such condition by permuting the columns of and changing their signs.

Since the space of models is discrete, we have to show that for large ,

a.s. We divide the proof into the following four parts:

-

(a)

a.s. for large ,

-

(b)

a.s. for large ,

-

(c)

a.s. for large ,

-

(d)

a.s. for large .

The points (b) and (d) follow quickly by the strong consistency of . To prove (a) and (c) we reduce the problem to the orthogonal design case. We have

where , and . Clearly, (10) implies that , which allows to use results from the orthogonal design. However, we note that the OLS estimators are the same in the original model and its scaled version .

Let be a permutation of satisfying

By the strong consistency of the OLS estimator, taking sufficiently large, we may ensure that the clusters of do not interlace in in the sense that if , then a.s. for sufficiently large.

Let us now consider point (a). Let denote the cluster containing , that is, the set . In view of the ordering of , there exists such that

We will show that if , then for large

| (12) |

thus for , which finishes the proof of (a).

Now assume that . Then, by Theorem 3.2, the condition (12) is satisfied if

| (13) |

holds for large and both and have the same sign. The latter is ensured by the strong consistency of the OLS estimator and the fact that .

If , then we have the following bound

| (14) |

Take any . Since both and have the normal distribution with the same mean, by Lemma 4.2, we have

In view of (14) and (11), this implies that (13) holds true for large . Hence, (a) follows.

It remains to establish (c). Assume that . Clearly, condition (a) from Theorem 3.3 is satisfied thanks to the strong consistency of the OLS estimator. For (b),

we have for ,

which converges to . On the other hand, the left-hand side of (b) converges a.s. to , which is positive. Thus, condition (b) from Theorem 3.3 holds for large . Condition (c) from Theorem 3.3 follows from Lemma 4.2. Indeed, we have for and ,

while

Thus, all assumptions of Theorem 3.3 are verified and the proof is complete. ∎

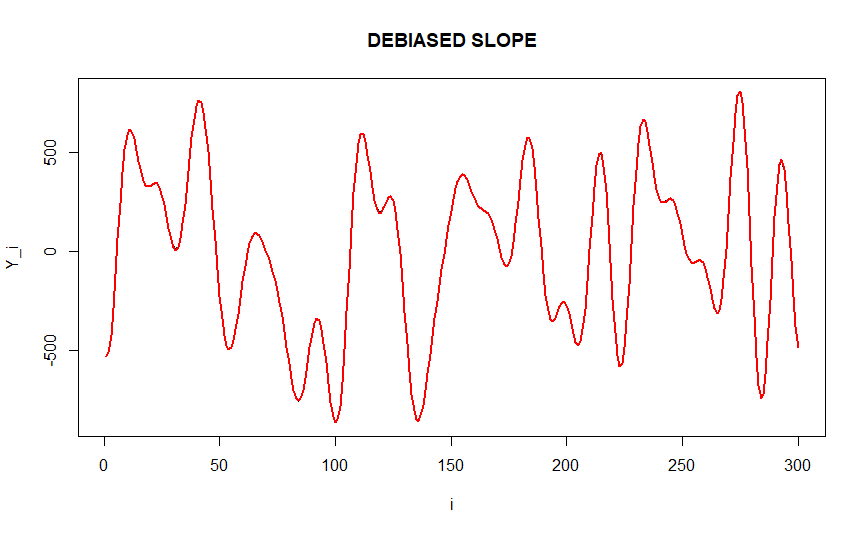

5 Applications and simulations

Below we present an application of SLOPE in signal denoising. In our example is an orthogonal system of trigonometric functions, i.e.

and for

and . Here is a vector consisting of two clusters: coordinates with absolute value and coordinates with absolute value . The absolute values of coordinates of are sorted in a decreasing way. The signs of the nonzero coordinates are chosen independently with random uniform distribution. To avoid large bias caused by the shrinkage nature of LASSO and SLOPE, we debias them by combining with the OLS method. For that reason we use the following definition of the pattern matrix and the clustered design matrix , which is based on the SLOPE pattern:

Definition 5.0.1.

Let be a pattern in with nonzero clusters. The pattern matrix is defined as follows

Definition 5.0.2.

Let be a pattern in and . For we define the clustered design matrix by .

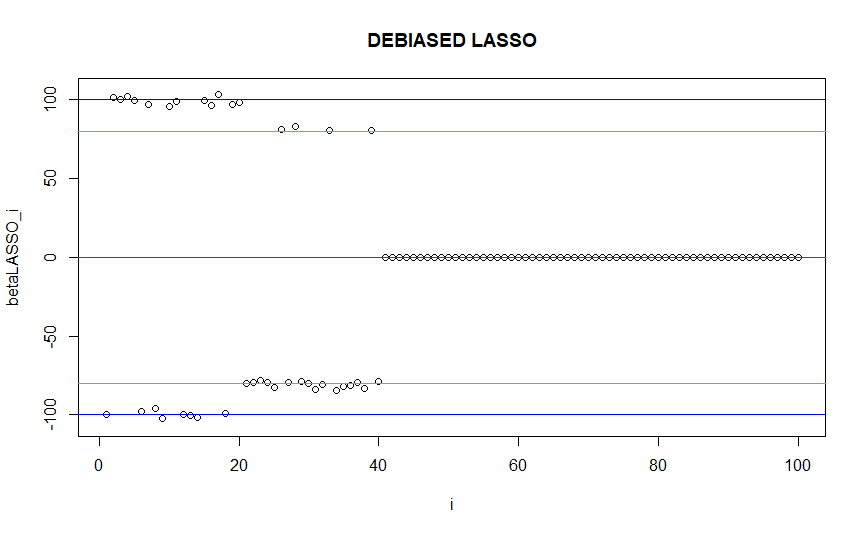

To perform the debiased SLOPE, we begin with recovering the support and clusters of a true vector with SLOPE. Then, using the obtained SLOPE pattern , we replace the design matrix with its clustered version . Then we perform the Ordinary Least Squares regression for the model , where consists only of distinct absolute values of .

Analogously we proceed with the debiased LASSO. However, in this method we use the LASSO pattern matrix defined in a following way:

For LASSO we have the LASSO pattern being a sign vector, cf. [22]. For , denotes the number of nonzero coordinates. If , then we define the corresponding pattern matrix by

i.e. the submatrix of obtained by keeping columns corresponding to indices in . Then we define the reduced matrix by

Equivalently, we have . The notion of pattern matrix also appears in [4]. In our example and .

We compare the Mean Square Error and the signal denoising of the classical OLS estimation, the LASSO with the tuning parameter minimizing the cross-validated error, the denoised version of LASSO with and the denoised version of SLOPE with the tuning vector chosen with respect to the scaled arithmetic sequence ().

![[Uncaptioned image]](/html/2202.08573/assets/ols1.png)

![[Uncaptioned image]](/html/2202.08573/assets/lasso1.png)

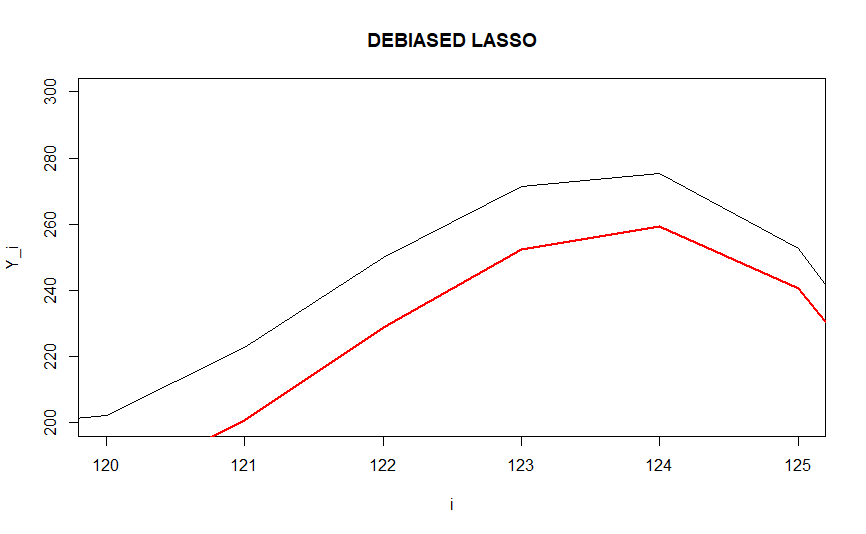

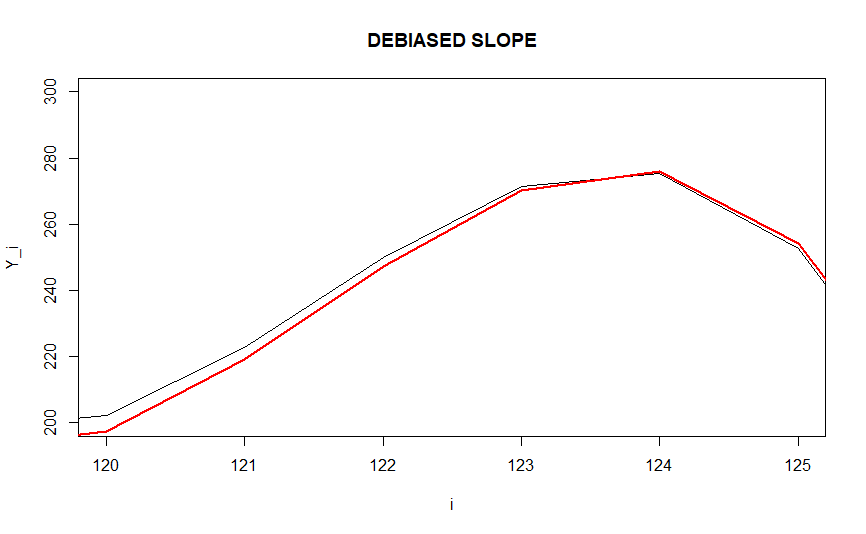

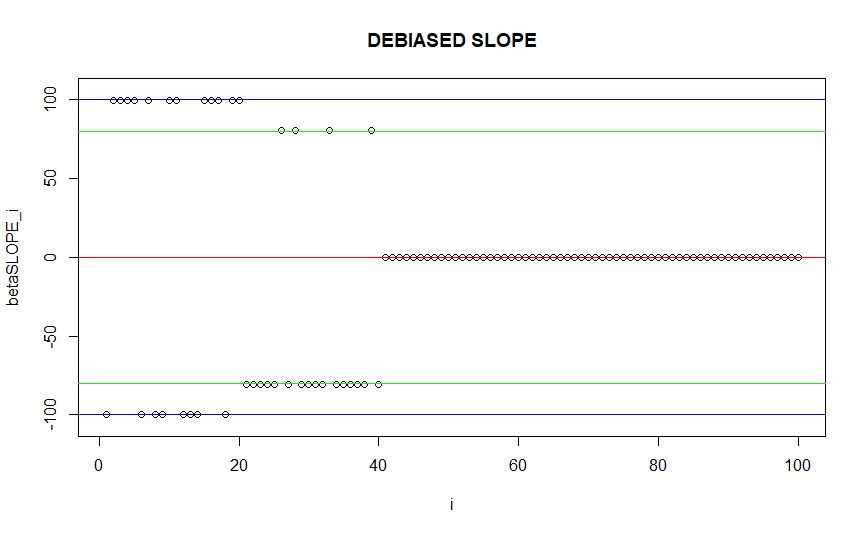

We also compare debiased SLOPE with debiased LASSO, as shown in Figure 4. The horizontal lines correspond to the true values of . As one may observe, in the presented setting LASSO does not recover the true support, while debiased SLOPE perfectly recovers support, sign and clusters.

| OLS | LASSO-CV | LASSO-LS | SLOPE-LS | |

| 613.6797 | 426.3705 | 171.7957 | 20.74967 |

Dodatek A Appendix

Proof of Lemma 2.1.

Since the matrix is nonnegative definite, it follows that the function defined by

is convex in . Therefore, at the point , where attains its global minimum over , the gradient of satisfies

This implies , for all , because

In the proof of parts (a), (b) and (c) we use the fact that maximizes over .

To prove part (a) suppose that for some and define

Then we have ,

which is impossible since .

To prove part (b), consider a permutation of such that

and are similarly sorted. Define the point

, where , for . If , then, by the Hardy-Littlewood-Pólya rearrangement inequality,

which is impossible since .

Finally, to prove part (c), suppose that , and that . In this case there is a sufficiently small , such that

If then

which is impossible. ∎

Proof of Lemma 2.2.

At first we note that for all

where the last inequality follows from the fact that , for all , see the proof of 2.1. Therefore, . Moreover, from the definition of the point it is seen that . These two facts imply that

Since (by the max-min inequality), we have the equality throughout. This completes the proof. ∎

Proof of Lemma 3.1.

Observe that

Therefore both optimization problems differ by , which does not depend on , which implies their equivalence. ∎

Literatura

- [1] J. P. Aubin, Mathematical Methods of Game and Economic Theory. North-Holland Publishing Company, 1980.

- [2] M. Bogdan, E. van den Berg, C. Sabatti, W. Su and E. J. Candès, SLOPE – Adaptive Variable Selection Via Convex Optimization, Ann. Appl. Stat. 9 (2015), 1103-1140.

- [3] M. Bogdan, E. van den Berg, W. Su and E. J. Candès, Statistical estimation and testing via the sorted L1 norm, arXiv:1310.1969 (2013).

- [4] M. Bogdan, X. Dupuis, P. Graczyk, B. Kołodziejek, T. Skalski, P. Tardivel and M. Wilczyński, Pattern recovery by SLOPE, arXiv:2203.12086 (2022).

- [5] H. D. Bondell and B. J. Reich, Simultaneous regression shrinkage, variable selection, and supervised clustering of predictors with OSCAR, Biometrics, 64 (2008), no. 1, 115-123.

- [6] H. D. Bondell, B. J. Reich. Simultaneous factor selection and collapsing levels in ANOVA. Biometrics 65.1 (2009), no. 1, 169–177.

- [7] S. Sh. Chen and D. L. Donoho, Basis pursuit, Proceedings of 1994 28th Asilomar Conference on Signals, Systems and Computers, IEEE 1 (1994), 41-44.

- [8] S. Sh. Chen, D. L. Donoho and M. A. Saunders, Atomic decomposition by basis pursuit, SIAM J. Sci. Comput. 20 (1998), no. 1, 33–61.

- [9] X. Dupuis and P. Tardivel, Proximal operator for the sorted norm: Application to testing procedures based on SLOPE, hal-03177108v2 (2021).

- [10] K. Ewald and U. Schneider, Uniformly Valid Confidence Sets Based on the Lasso, Electron. J. Stat. 12 (2018), no. 12, 1358–1387.

- [11] M. AT Figueiredo and R. Nowak, Ordered weighted l1 regularized regression with strongly correlated covariates: Theoretical aspects, Artificial Intelligence and Statistics, PMLR (2016), 930-938.

- [12] J. Gertheiss and G. Tutz, Sparse modeling of categorial explanatory variables, Ann. Appl. Stat. 4 (2010), no. 4, 2150–2180.

- [13] P. Kremer, D. Brzyski, M. Bogdan and S. Paterlini, Sparse index clones via the sorted -norm, SSRN 3412061 (2019).

- [14] A. Maj-Kańska, P. Pokarowski and A. Prochenka, Delete or merge regressors for linear model selection, Electron. J. Stat. 9 (2015), no. 2, 1749–1778.

- [15] K. Minami, Degrees of freedom in submodular regularization: a computational perspective of Stein’s unbiased risk estimate, J. Multivariate Anal. 175 (2020), 104546.

- [16] R. Negrinho and A. D. Martins, Orbit Regularization, NIPS (2014).

- [17] Sz. Nowakowski, P. Pokarowski and W. Rejchel, Group Lasso merger for sparse prediction with high-dimensional categorical data, arXiv:2112.11114 (2021).

- [18] M.-R. Oelker, J. Gertheiss and G. Tutz, Regularization and model selection with categorical predictors and effect modifiers in generalized linear models, Stat. Model. 14 (2014), no. 2, 157–177.

- [19] K. R. Rao, N. Ahmed, M. A. Narasimhan, Orthogonal transforms for digital signal processing, Proceedings of the Eighteenth Midwest Symposium on Circuits and Systems (1975), 1–6.

- [20] U. Schneider and P. Tardivel, The geometry of uniqueness, sparsity and clustering in penalized estimation, arXiv:2004.09106 (2020).

- [21] P. Tardivel, R. Servien and D. Concordet, Simple expression of the LASSO and SLOPE estimators in low-dimension, Statistics 54 (2020), 340-352.

- [22] P. Tardivel, T. Skalski, P. Graczyk and U. Schneider, The Geometry of Model Recovery by Penalized and Thresholded Estimators, hal-03262087 (2021).

- [23] B. G. Stokell, R. D. Shah and R. J. Tibshirani, Modelling High-Dimensional Categorical Data Using Nonconvex Fusion Penalties, arXiv:2002.12606 (2021).

- [24] R. Tibshirani, Regression shrinkage and selection via the lasso. J. R. Stat. Soc. Ser. B. Stat. Methodol 101 (1996), no. 1, 167-188.

- [25] X. Zeng and M. AT Figueiredo, Decreasing Weighted Sorted Regularization, IEEE Signal Processing Letters 21 (2014), no. 10, 1240-1244.

- [26] P. Zhao and B. Yu, On model selection consistency of Lasso, J. Mach. Learn. Res. 7 (2006), 2541-2563.

- [27] H. Zou, The adaptive lasso and its oracle properties, J. Amer. Statist. Assoc. 101 (2006), no. 476, 1418-1429.