Solvability of Differential Riccati Equations and Applications to Algorithmic Trading with Signals

Abstract

We study a differential Riccati equation (DRE) with indefinite matrix coefficients, which arises in a wide class of practical problems. We show that the DRE solves an associated control problem, which is key to provide existence and uniqueness of a solution. As an application, we solve two algorithmic trading problems in which the agent adopts a constant absolute risk-aversion (CARA) utility function, and where the optimal strategies use signals and past observations of prices to improve their performance. First, we derive a multi-asset market making strategy in over-the-counter markets, where the market maker uses an external trading venue to hedge risk. Second, we derive an optimal trading strategy that uses prices and signals to learn the drift in the asset prices.

keywords:

Riccati equations, algorithmic trading, signals, adaptive strategies, statistical arbitrage, market making, optimal execution.The author is grateful to Álvaro Cartea, Patrick Chang, Olivier Guéant, Anthony Ledford, Leandro Sánchez-Betancourt, and the Oxford Victoria Seminar participants at Oxford for insightful comments. The author is grateful to the Oxford-Man Institute’s generosity and hospitality.

1 Introduction

Matrix differential Riccati equations (DREs) with indefinite matrix coefficients, i.e., matrices that are neither positive nor negative semi-definite, arise in a wide class of control problems such as linear-quadratic zero-sum games, control, linear-quadratic Gaussian (LQG) control problems with indefinite cost matrix, and linear-exponential-quadratic Gaussian (LEQG) control problems.

Most results on these equations provide a statement of equivalence between the existence of solutions to a DRE and the solvability of a control problem. In this paper, we provide an existence and uniqueness result for the solution to a type of DRE with indefinite matrix coefficients which arises in various control setups. Special cases of the DRE are relevant for algorithmic trading problems in LEQG setups, where the cost is an exponential of a quadratic functional of the state and the controls. In particular, the quadratic term matrix coefficient has both positive and negative eigenvalues, so classical existence results are not readily available.

We use the result to provide solutions to two algorithmic portfolio trading problems; one is market making with signals and hedging, the second is optimal trading with Bayesian learning of the drift. In both problems, the optimal strategies take the form of a linear feedback control whose feedback gain is obtained from the solution to a special case of the DRE that we study. Efficient numerical solving techniques for such equations have been extensively studied and provide computationally efficient methods to market participants, for whom speed and precision are key for better performance.

Market making

As a first application for liquidity providers, we introduce a comprehensive framework for multi-asset market making in OTC markets with three important features : portfolio dynamics that incorporate signals, external hedging and client tiering, and computationally efficient methods to obtain quotes for large portfolios.

OTC markets are off-exchange and quote-driven markets based on a network of market makers that allow clients to buy and sell securities. In these markets, quotes are either streamed to clients or clients request for quotes (RFQs).111For a better understanding of the RFQ system, we refer to Fermanian et al. (2016). In practice, OTC market makers provide liquidity for assets within a specific sector or asset class. Thus, the price dynamics of assets for which they make quotes usually share common stochastic trends and co-movements. For example, in OTC bond markets, a large number of bonds from different issuers are traded and one needs to account for the joint dynamics that they exhibit; appropriate dynamics are necessary to obtain quotes that balance risk at the portfolio level.

Furthermore, market makers often use price predictors to improve trading performance, and use instruments that offset their inventory risk to hedge their positions. Our framework uses multivariate Ornstein–Uhlenbeck (multi-OU) dynamics to model the joint dynamics of these variables. We use an approximation technique similar to that introduced in Bergault et al. (2018) and we solve the optimal quote and optimal hedging approximation problem using the DRE existence and uniqueness result. Finally, we study the quoting strategy with numerical examples for a market maker in charge of a single asset with mean reverting prices, and for a market maker in charge of a pair of cointegrated assets.

Optimal trading

As a second application for liquidity takers, we combine the tools of stochastic control and online learning to derive an optimal portfolio trading strategy. The agent uses observed prices and signals to continuously update her estimate of the drift in the prices. The strategy uses signals either to improve the performance of execution programmes or to execute statistical arbitrages. We show that the problem reduces to a DRE for which existence and uniqueness of a solution is a straightforward application of our result.

In most execution strategies in the literature, model parameters are estimated and fixed prior to the start of the trading window. There are two downsides to this approach. First, parameter misspecification makes the strategy non-optimal. Second, the strategy does not incorporate uncertainty about the parameters. This work builds on the work in Bismuth et al. (2019) and proposes a model where the agent uses a prior distribution over the drift parameter to encode her uncertainty, and continuously uses price and signal observations to update her estimate during the execution programme.

Literature review

Classical results on LQG problems and the associated DREs are in Abou-Kandil et al. (2012); Fleming and Rishel (2012). Jacobson (1973) uses optimal control to solve an LEQG control problem and obtains optimal controls that are equivalent to those obtained for quadratic differential games. Whittle (1990) and Lim and Zhou (2005) use the stochastic maximum principle to obtain similar results. Our existence and uniqueness result generalises that of Bergault et al. (2021); in particular, the matrix coefficients are deterministic time-dependent matrix functions and the quadratic term in the cost functional depends on the observed system. The existence and uniqueness of solutions in general remains an open problem for matrix DREs with indefinite matrix coefficients. This work relates to the literature that addresses the solvability of these equations in special cases; see Chen et al. (1998); Rami et al. (2001); Hu and Zhou (2003). Finally, matrix DREs arise in various algorithmic trading problems; see Cartea et al. (2019, 2022c); Barzykin et al. (2022),

In market making, the first approaches are in Ho and Stoll (1983); Glosten and Milgrom (1985); Avellaneda and Stoikov (2008). These frameworks have been extended in many directions; see Guéant et al. (2012, 2013); Cartea et al. (2014), and the books Cartea et al. (2015); Guéant (2016). Our work is related to the literature addressing the curse of dimensionality in multi-asset market making; see Guéant et al. (2013); Guéant (2017); Guéant and Manziuk (2019). A strand of the algorithmic trading literature uses market signals to improve the performance of strategies; see Cartea and Jaimungal (2016); Cartea and Wang (2020); Forde et al. (2022); Fouque et al. (2021); Cartea et al. (2022a, b).

In optimal execution, the first approaches are in Bertsimas and Lo (1998); Almgren and Chriss (1999), and model extensions are in Schied and Schöneborn (2009); Alfonsi and Schied (2010); Gatheral et al. (2012); Forsyth et al. (2012); Guéant (2015); Cartea et al. (2021); Cartea and Sánchez-Betancourt (2022b); see the comprehensive review Donnelly (2022). Several papers generalise the classical approaches of optimal execution to more complex price dynamics; see Cartea and Jaimungal (2016); Almgren (2012). In particular, similar to this work, Cartea et al. (2019) and Bergault et al. (2021) study optimal trading models where the joint dynamics of prices follow a multi-OU process. Our work also relates to the literature which incorporates uncertainty and learning in execution. Laruelle et al. (2013) derive a strategy where the agents learns the parameters of a jump process, Cartea et al. (2017) incorporate model uncertainty in execution, and Casgrain and Jaimungal (2019) derive strategies with learning of latent state distribution upon which prices depend. Similar to the problem addressed in this work, Bhudisaksang and Cartea (2021) introduce an adaptive control framework which is robust to model misspecification, where the agent learns the drift with jump-diffusion uncertainty. Recently, Cartea and Sánchez-Betancourt (2022a) derive closed-form strategies where a broker uses the toxic flow to extract alpha signals, and Cartea et al. (2023) use Gaussian processes to learn the mapping from signal values to trading performance.

The remainder of this paper proceeds as follows. Section 2 introduces a family of DREs with indefinite matrix coefficients and provides existence and uniqueness results based on a set of assumptions. Section 3 derives a portfolio market making strategy that uses signals to improve trading performance and uses a trading venue to hedge risk. The joint dynamics of the assets in the portfolio, the hedging instruments, and the signals follow multi-OU dynamics. We show that the approximation of the optimal quoting and hedging strategies reduces to a DRE that is a special case of that studied in Section 2. Finally, Section 4 solves optimal portfolio trading with Bayesian learning of the drift, using signals and past observations of the price to improve performance. We show that the problem reduces to a DRE that is also a special case of that studied in Section 2.

2 A general differential matrix Riccati equation

DREs with indefinite matrix coefficients arise in LQ games (Jacobson, 1973), control (Limebeer et al., 1992), LQG problems with indefinite cost (Chen et al., 1998), and LEQG problems (Whittle, 1990). Their solvability is also key in practical financial decision problems, such as portfolio optimisation (Zhou and Li, 2000), option pricing (Kohlmann and Zhou, 2000), and algorithmic trading (Bergault et al., 2021). The results in these works show that some control problem is well-posed if there are solutions to a DRE from which one obtains the optimal feedback control. In this section, we study a special type of DREs and provide conditions for the existence and uniqueness of a solution.

We motivate the DRE that we study by the type of DREs that arise in algorithmic trading problems where an agent adopts a CARA utility and where the dynamics of the asset prices are (linearly) driven by signals and past observations of prices. Section 3 and Section 4 give two examples of such problems.

In the remainder of this paper, the symbol denotes the first derivative of , the superscript ⊺ stands for the transpose operator, and is the set of positive integers. is the set of real matrices and is the set of real square matrices. We also denote the set of real symmetric matrices by . Finally, the subset of positive-definite and positive semi-definite matrices of are respectively denoted by and .

We study the matrix DRE

| (1) |

with terminal condition where and . Let , the matrix coefficients and are

| (2) |

and the terminal condition is

| (3) |

where and

We show that a solution to the DRE (1) with terminal condition (3) exists and is unique when the coefficients satisfy a set of assumptions. First, Subsection 2.1 shows that the solution to the DRE corresponds to the solution to an LEQG control problem. Next, Subsection 2.2 uses the control problem and our assumptions to provide a-priori bounds to the solution to the DRE, and subsequently obtains existence and uniqueness of a solution.

2.1 An equivalent exponential utility control problem

Here, we show that the DRE (1) corresponds to an LEQG control problem, which then becomes the key tool to prove the main result of existence and uniqueness of a solution in Subsection 2.2. Let be a filtered probability space that satisfies the usual conditions and which supports all the processes defined in this section. Consider the following deterministic matrix functions:

| (4) |

Note that and Furthermore, let be the rank of the matrix and consider a matrix such that for all The change of variables in (4) leads to the following matrix coefficients for the DRE (1):

| (5) |

Consider an observable system described by a -dimensional state processes with linear dynamics

| (6) |

where is known and is fixed. The matrix function encodes the linear dependence of the system to its previous state, scales the variance of the noise, and is a -dimensional standard Brownian motion with independent coordinates. Note that the SDE (6) admits a strong solution; see A.

An agent controls an -dimensional process that affects two measured outputs and The set of admissible controls is

| (7) |

where we define the linear growth condition on with respect to to be satisfied by an -valued, -adapted process if there exists a constant such that for all , almost surely.222Here, is a fixed norm on We write

The output is affected linearly and follows the dynamics

| (8) |

where is known. On the other hand, the output takes a quadratic form in the system and the controls and follows the dynamics

| (9) |

where is known. Note that the condition above guarantees that the dimension of the agent’s control is smaller than that of the system . In our problem, the output measures an objective that the agents targets at the terminal time , and the output measures an objective that the agent wishes to maximise or a cost that she wishes to minimise by the terminal time

The performance criterion of the agent associated with a control is

| (10) |

where measures risk aversion.

We introduce the following assumptions that are subsequently used in the remainder of this section:

Assumption 1

-

(i)

for all

-

(ii)

for all

-

(iii)

and commute for all

Assumption 2

.

In the optimisation problem (10), Assumption 1-(i) ensures that the term in the performance criterion that is quadratic in the state is a cost and not a gain. Assumptions 1-(ii) and 1-(iii) are technical conditions to obtain an upper bound for the value function which results in an upper bound for the solution to the DRE; see C. Finally, when , when the Assumptions 1 and 2 hold, and when the matrix coefficients in (1) are constant, the DRE (1) is similar to that in Bergault et al. (2021).

The agent maximises her performance (10) and her value function is

| (11) |

where the processes , and follow the dynamics

| (12) |

for and , with and . We state the following result for which a proof is given in A.

Proposition 1

The next theorem shows that the solution to the optimisation problem (10) is associated with that of the DRE (1); for a proof see B.

Theorem 1

Theorem 1 solves the control problem (11) when the DRE (1) with terminal condition (3) admits a unique solution on . The optimal control is a linear feedback with gains obtained from . Subsection 2.2 uses the equivalent control problem to find a-priori bounds and proves existence and uniqueness of a solution to the DRE (1).

2.2 Existence and uniqueness of a solution

The next theorem, for which a proof is given in C, provides conditions for the existence and uniqueness of a solution to the DRE (1) with terminal condition (3).

Theorem 2

The following results extend Theorem 2 and show that solutions to the DRE (1) provide solutions to larger families of DREs.

Corollary 1

Assume is the unique solution to (1), then the DRE

with terminal condition admits a unique solution, where and the coefficients are , and .

Corollary 2

Assume is the unique solution to (1) and let , then the DRE

with terminal condition admits a unique solution, where

In the next sections, we study two algorithmic portfolio trading problems which are solved using the result in Theorem 2. First, we extend multi-asset market making to dynamics that incorporate signals and hedging instruments. Next, we solve optimal portfolio trading with Bayesian learning of the drift.

3 Multi-asset optimal market making

We consider a market maker in charge of quoting multiple assets in an OTC market. She receives RFQs from different clients with variable sizes, and decides on the optimal quotes at any point in time. The market maker trades assets that she quotes and other hedging instruments in a dealer-to-dealer venue to hedge risk. The joint dynamics of the asset midprices, the hedging instruments prices, and a set of signals follow a multi-OU process. We use the approximation method introduced in Bergault et al. (2018) to obtain a quoting and hedging strategy that can efficiently be computed by solving the DRE (1).

3.1 The model

Let be a standard filtered probability space that supports all the processes we introduce and satisfies the usual conditions. A market maker operates in an OTC market and is in charge of a portfolio containing assets. She uses a set of signals and we model the joint dynamics of prices and signals by a -dimensional multi-OU process with dynamics:

| (18) |

where , the initial values are known, , , , and is a -dimensional standard Brownian motion with independent coordinates for some . Without loss of generality, we assume that the first elements of the vector correspond to the asset prices.

Multi-OU dynamics are effective when the market maker uses the predictive power of signals, or for hedging purposes when there exists a linear combination of assets that reduces the overall risk. In the dynamics (18), the parameter is the unconditional expectation of prices and signals in the long-run, and the matrix drives the joint deterministic part in the dynamics. We denote by the variance-covariance matrix associated with the process , and the variance-covariance matrix associated with the first elements of the process .

In practice, market makers hedge their positions with securities that they quote and with other liquid instruments for which they do not offer quotes, but which offset their risk. For example, a market maker in charge of corporate bonds hedges rates risk with bond futures, and further hedges credit risk with credit derivatives. Moreover, market makers use latent factor models and other market variables with predictive power to enhance performance. Our framework is designed for these cases.

To incorporate hedging instruments in our model, for which the market maker does not propose quotes, it is enough to consider zero RFQ arrival intensities for these assets. To incorporate signals, we consider joint dynamics of prices and signals, but only consider inventory in the assets; see Cartea et al. (2019) for a similar setup.

3.2 The dynamics

Throughout the trading window , the market maker interacts with clients and chooses the prices at which she is ready to buy or sell the quoted assets.

Bid and ask quotes

The market maker quotes depend on the client and the size of the request. We define the bid and ask prices of asset for client’s tier , as the -measurable maps , where is the -algebra of predictable subsets of , and are the Borelian sets of .

For and the maps and are the shifts from the reference price for, respectively, the bid and the ask quotes and we write

| (19) |

Number of transactions and RFQ sizes

We define the probability measures and that correspond to the distributions of the requested sizes at the bid and ask side, respectively, of client’s tier for asset , and which are used to integrate over the distribution of sizes.

For and we use two càdlàg -marked point processes and to model the number of transactions at the bid and ask side, for asset and tier . To construct the marked point processes, consider a new filtered probability space and two independent compound Poisson processes and with intensity one and with increments that follow the size distributions and . Let and be the associated random measures. For each and , let be a probability measure given by the Radon-Nikodym derivative

where is the stochastic exponential and and are the compensated processes associated with and , respectively. Thus, Brémaud and Jacod (1977) show that under , the marked point processes and have intensity kernels and , respectively, given by

Recall that the intensities corresponding to the hedging instruments are set to zero.

Moreover, for each asset and tier , we assume that the functions for the bid and the ask satisfy the following properties, where and are respectively the first and second derivative of : (i) is twice continuously differentiable, (ii) , (iii) , and (iv) .

Inventory and internalisation / externalisation

For , the inventory process of the market maker for asset is denoted by We denote by the vector process . The market maker uses another trading venue to trade the assets for which she proposes quotes, but also to trade other hedging instruments. After an RFQ is received and the trade is executed, the market maker can either internalise or externalise. To internalise, the market maker keeps the trade in her inventory (while waiting for an offsetting order). To externalise, the market maker hedges risk by instantaneously offsetting the trade fully or partly, at a cost, in a dealer-to-dealer trading venue. We use the process to model the trading speed of the market maker in the dealer-to-dealer market, and we consider that the execution costs from her trading activity are quadratic in the speed. Finally, the inventory of the market maker in asset has dynamics combining the results of her market making and hedging activity:

Cash process

We use the process to model the amount on the market maker’s cash account and which follows the dynamics

with given, quantifies the execution costs from externalisation, and is an matrix with The matrix maps the first elements of the -dimensional price to an -dimensional vector.

3.3 The optimisation problem

The market maker maximises the expected exponential utility of her final wealth by the end of the trading window :

| (20) |

where is the set of admissible strategies, and is defined as

The final wealth in the performance criterion (20) is the sum of the final cash amount and the remaining inventory valued at , where . The final penalty is a discount applied to the terminal mark-to-market value of the assets which penalises any non-zero final inventory. Note that in the case of hedging instruments with zero intensity, i.e., for which the market maker does not propose quotes, the performance (20) of the market maker does not depend on the quoting strategy. In particular, any admissible control for the hedging instruments yields the same performance.

The value function of the market maker is

where the controlled processes , , and start at with values for the state variables. The Hamilton–Jacobi–Bellman (HJB) equation associated with the market making problem is333The symbols for the value function and for the solution to the HJB are different unless one proves equality with a verification argument; see Barzykin et al. (2023) where the authors solve a similar problem. Below, we focus on an approximation problem for the optimal quotes.

| (21) |

where is the canonical basis of , with terminal condition

| (22) |

In the next proposition, for which a proof is straightforward, we use the ansatz

Proposition 2

To obtain the optimal trading (externalisation) speed in feedback form, we write the Legendre-Fenchel transform of the quadratic execution cost as

so the supremum of in (3.3) is reached at

Second, to obtain the optimal quotes in feedback form, similar arguments as in Guéant (2017) lead to the optimal bid and ask quotes and for an RFQ of size , where

| (27) |

and the functions and are

| (28) |

and denotes the derivative of with respect to . It is beyond the scope of this paper to provide a formal solution to the optimal quote problem and we focus on the approximation technique (see Barzykin et al., 2023, for a rigorous solution to a similar problem).

3.4 Quadratic approximation of the value function

One usually employs numerical methods to approximate the value function and hence the optimal quotes (3.3). These methods suffer from the curse of dimensionality and do not usually scale up to the multi-asset case, because the number of dimensions grows exponentially with the number of assets. In this subsection, we approximate the solution of the HJB (2) characterising the optimal quotes by the solution of another HJB for which computations are easier to carry out.

For small RFQ sizes, we use the approximation

Thus, the term we wish to approximate in (2) becomes a function of the form Moreover, the functions and in (2) are positive and decreasing in , so we use a quadratic approximation. Furthermore, a quadratic approximation simplifies the problem to finding the solution to a DRE of the form (1). More precisely, for all and , we approximate the Hamiltonian term

by the sum of the two quadratic functions

The values of the approximation coefficients for each request size are obtained using the Taylor expansion around :

Next, we denote the approximation of the function by , which verifies the HJB

| (29) |

with terminal condition

| (30) |

To further simplify the above HJB, use the ansatz

| (31) |

based on the next proposition whose proof is omitted.

Proposition 3

Assume that there exist matrix functions , , , , , satisfying the system of ODEs

| (32) |

with terminal conditions

| (33) |

where is the linear operator mapping a matrix onto the vector of its diagonal coefficients, and for , , , and :

Notice that the system of ODEs (32) can be solve sequentially. First, solve the subsystem in , then solve the linear subsystem in , and is obtained by an integration. Thus, obtaining the approximated reduces to solving the subsystem in . Define as

| (34) |

and observe that the ODE system in is equivalent to the DRE

| (35) |

with terminal condition

| (36) |

where

Assume that . Here, Assumptions 1 and 2 hold, thus the results of Section 2 apply to the DRE (35) with terminal condition (36). In particular, use Corollary 1 with and in the terminal condition (3) to obtain the DRE (35).

The approximation method of this section leads to the DRE (35) for which a solution exists and is unique, and which can be approximated rapidly using existent efficient solving techniques. Once the approximated value function is obtained, the approximated quotes are

| (37) |

where the functions and are in (3.3). Moreover, the externalisation strategy associated with the approximated value function is

| (38) |

The case of symmetric exponential intensity functions

If the intensity functions for the bid and ask sides are exponential, which is a commonplace assumption in the market making literature, then for all and , we write

| (39) |

where and are positive constants. Thus, the Hamiltonian functions are

and the approximated quotes are given by the shifts

| (40) | ||||

3.5 Numerical results

We study the optimal quotes (3.3) and the approximated quotes (3.4) for a market maker in charge of a single asset with mean reverting prices, and for a market maker in charge of two cointegrated assets. The market maker interacts with one client and we assume that a unique intensity function drives the trading flow at the bid and the ask and we write

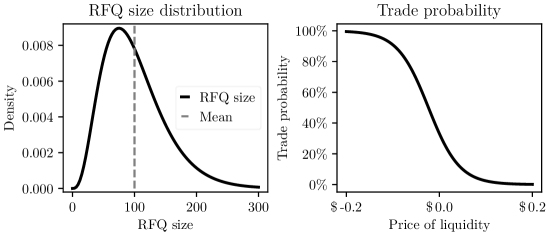

for all the assets that we consider, where is the base intensity, i.e., the intensity of order arrival when the price of liquidity is zero. Moreover, we assume that the RFQ sizes for all assets are distributed according to a Gamma distribution . Table 1 shows the parameter values for the intensity functions and the distribution of RFQ sizes, and Figure 1 shows the distribution of RFQ sizes and the probability to trade as a function of the price of liquidity implied by the parameter values of Table 1.

| Parameter | |||||

|---|---|---|---|---|---|

| Value |

To compute the optimal and approximated bid and ask quotes, we discretise the Gamma distribution (left panel of Figure 1) and we consider the sizes and the weights in Table 2. Finally, we assume that the market maker only trades if her inventory is within the range

| RFQ Size | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Weight |

3.5.1 Single-asset case

We consider a market maker in charge of a single asset. Table 3 shows the parameter values for the OU dynamics of the price in (18) and for the performance criterion in (20). In the single-asset case, the parameter drives the mean reversion speed of prices towards the long-term unconditional mean

| Parameter | |||||||

|---|---|---|---|---|---|---|---|

| Value | or |

To obtain the optimal shifts and , we employ an implicit Euler scheme to approximate the solution of the HJB (2).444The scheme is in dimension three; one for time, one for inventory, and one for the asset price. To obtain the approximated quotes (3.4), we use an implicit Euler scheme to approximate the solution to the DRE (35).555The code for the numerical examples is in https://github.com/FDR0903/Market_Making_Riccati.

Optimal quotes as a function of the RFQ size

Figure 2 shows the optimal quotes for the different RFQ sizes in Table 2, and shows that the price of liquidity at the bid and the ask increases with the RFQ size.

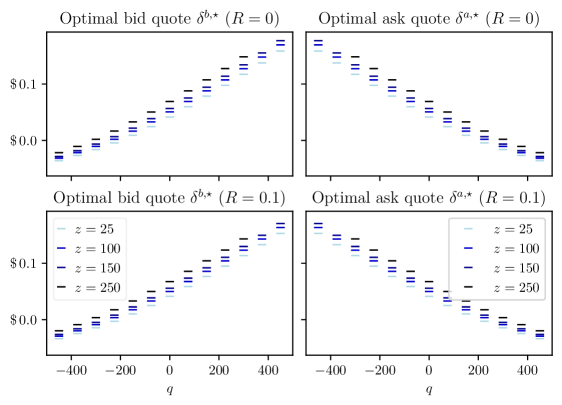

Optimal shifts as a function of the asset price

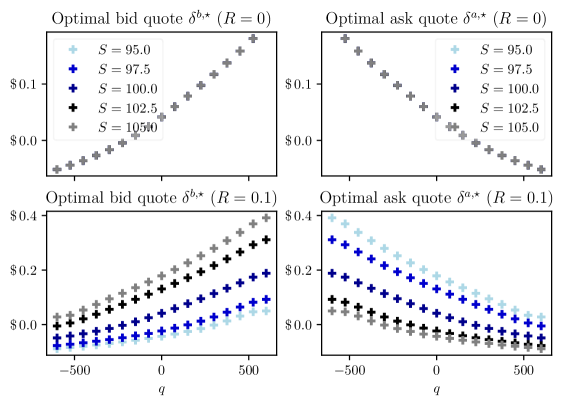

Figure 3 shows the optimal bid and ask quote shifts for different values of the price and the mean-reversion parameter . If then there is no deterministic part in the dynamics of the price, so the strategy is indifferent to the price level. If , then the strategy of the market maker has a speculative component; the market maker uses the difference between the price and its long-term mean to determine the price of liquidity at the bid and at the ask. More precisely, when the price is above , the market maker expects the prices to decrease and revert back to , so she increases the price of liquidity at the bid to maximise her profits from sellers, and she decreases the the price of liquidity at the ask to attract buyers. Similarly, when the price is below , the market maker expects the prices to increase, so she raises the price of liquidity at the ask and reduces it at the bid.

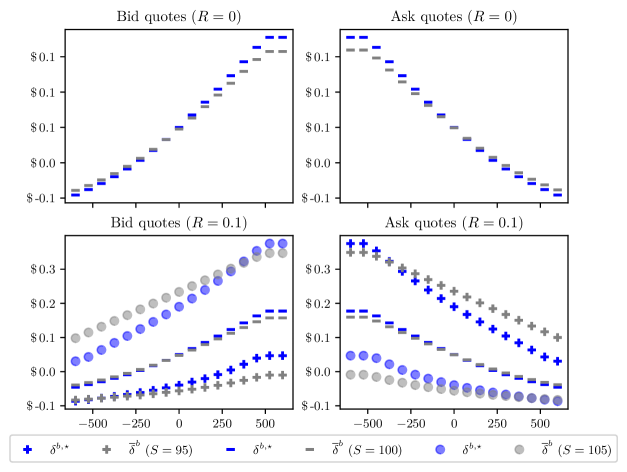

Quality of the approximation

Figure 4 shows the optimal shifts (3.3) and the approximated shifts (3.4) for different values of the price , the mean reversion parameter and the inventory . When the quality of the approximation is satisfactory for different levels of the inventory; recall that the quoting strategy does not depend on the price level. When the approximated bid quotes deviate from the optimal bid quotes when (i) the price is above and the inventory of the market maker is large and negative, and when (ii) the price is below and the inventory of the market maker is large and positive. Similarly, the approximated ask quotes deviate from the optimal ask quotes when (i) the price is below and the inventory of the market maker is large and positive, and when (ii) the price is above and the inventory of the market maker is large and negative. Most importantly, the approximated quotes capture all the relevant financial effects of the optimal quoting strategy: (i) the price of the liquidity increases with inventory at the bid and decreases with inventory at the ask, and (ii) the price of liquidity increases with the price level at the bid and decreases with the price level at the ask (when ).

3.5.2 Multi-asset case

We consider a market maker in charge of two cointegrated assets. Table 4 shows the parameter values for the multi-OU dynamics of the prices in (18) and for the performance criterion in (20). In the multi-asset case, the parameter is a matrix that drives the deterministic joint dynamics of the prices, and is the long-term unconditional mean. The matrix in Table 4 indicates that the prices are not correlated, however, the matrix implies that the space of cointegration vectors is spanned by i.e., the cointegration factor is stationary around

| Parameter | |||||||

|---|---|---|---|---|---|---|---|

| Value | days |

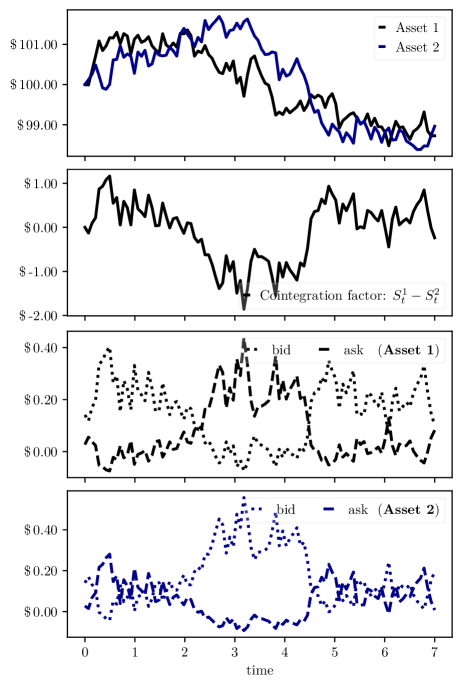

To obtain the optimal quote shifts and , one should employ a numerical scheme in dimension five; one for time, two for inventory in both assets, and two for the asset prices of both assets, which becomes rapidly intractable with fine grids. In contrast, the approximated shifts (3.4) are quickly computed with Riccati ODE solvers. Figure 5 shows the approximated bid and ask shifts for both assets for a simulation path of both prices.

The first two panels show that the prices are cointegrated and that the cointegration factor is mean reverting to The last two panels show the price of liquidity at the bid and the ask for both assets as a function of the price levels. In contrast to the single asset case, the speculative component of the quoting strategy uses the cointegration factor instead of the prices of the individual assets. In particular, when the cointegration factor is above the long-term mean , i.e., when , the market maker expects the price of asset to decrease and the price of asset to increase. Thus, she increases the price of liquidity at the bid for asset and at the ask for asset to maximise profits. Similarly, when , the market maker expects to increase and to decrease. Thus, the market maker increases the price of liquidity at the ask for asset and at the bid for asset to maximise profits.

4 Optimal execution and statistical arbitrage with Bayesian learning of the drift

In this section, we propose a second application of the existence result of Section 2. Consider an agent who is in charge of a portfolio. The agent is uncertain about the drifts in the prices of the assets in the portfolio, and has a prior Gaussian distribution. The model we introduce combines stochastic optimal control, to obtain an optimal trading schedule, with online learning of the drift from observed prices and signals, to update the estimate of the drift while trading. The strategy we derive uses information from prices and signals to enhance trading performance for execution programmes, or to execute statistical arbitrages based on price predictors.

In our model, the latest estimate at time of the true value of the drift is the expectation of the drift conditional on the filtration generated by the prices and signals up until time . The approach is powerful in two ways. First, it uses online learning to continuously adjust the drift to the information in recent observations of prices and predictive signals. Second, it incorporates the uncertainty on the future value of the drift.

First, we recall the Bayesian learning approach introduced in Bismuth et al. (2019). Next, we show that the optimal trading problem reduces to solving a DRE similar to that in (1).

4.1 Bayesian learning

We consider a market with assets, and an agent who uses signals, and let . We introduce the -dimensional Brownian motion adapted to the filtration . The joint dynamics of the prices and the signals are modelled by a -dimensional drifted Bachelier process with dynamics

| (41) |

where , , and we denote the variance-covariance matrix by .

The drifts are unknown to the agent but she has a Gaussian prior distribution that we denote by . The drift and the Brownian are not observed; however, the prices and the signals are continuously observed by the agent and they convey information about the true value of the drift. We use the Bayesian framework to update the estimation of the drift throughout the execution programme using the latest information available to the agent.

Let be the filtration generated by , which is the filtration that represents the information revealed to the agent. Notice that is not -adapted. We introduce the process defined as

The process is the latest estimated value of the drift given the information in the prices and the signals up to time . Now consider a non-degenerate multivariate Gaussian prior, i.e.,

| (42) |

where and . The authors in Bismuth et al. (2019) show that

| (43) |

where They also show that there exists a Brownian motion adapted to and that has the same correlation structure as that of , and that the dynamics of in (41) in the appropriate filtration are

| (44) |

where we define

| (45) |

4.2 Modelling framework and notations

An agent is in charge of a portfolio consisting of assets and she wishes to liquidate her initial inventory, or execute a statistical arbitrage if the initial inventory is zero, within a given period of time , where is fixed. She holds an -dimensional inventory described by the process with dynamics

where the initial inventory is known, and where is the trading speed process for each asset.

The joint dynamics of prices and signals are in (44), where is given and and are in (45).666We do not consider the permanent price; as justified in more detail in Bergault et al. (2021). We define the dynamics for the amount on the agent’s cash account as

| (46) |

where is given, is the positive-definite and symmetric price impact parameter which models execution costs incurred by the trader, and is an matrix with

As in the previous section, the agent maximises the performance criterion (20) and admissible strategies are in the set , where for ,

4.3 From HJB to DRE

The value function associated with the problem solves the HJB

for all with terminal condition

| (47) |

Similar to the previous section, one consider the two ansatzs

to obtain an ODE system in , , , , , and :

| (48) |

with terminal conditions and

The ODE system (48) can be solved sequentially. First, one solves the subsystem in , then the subsystem in becomes linear, and finally is obtained with an integration. Note that the subsystem of ODEs in can be written as the matrix DRE in

| (49) |

with terminal condition where

Assumptions 1 and 2 hold, in particular, the matrices and commute for all The DRE (49) is similar to the DRE (35), which is a special case of the family of problems introduced in Section 2. Thus, Theorems 1 and 2 solve the problem of optimal trading with Bayesian learning of the drift, in particular (49) admits a unique solution. In practice, efficient ODE solving techniques rapidly compute the solution to the DRE (49). Finally, we do not study the performance of the optimal strategy which has been thoroughly studied in Bismuth et al. (2019).

5 Conclusion

We obtained an existence and uniqueness result for a type of matrix DREs with indefinite matrix coefficients. The result is used to solve two algorithmic trading problems for liquidity providers and takers. The first problem is multi-asset market making, and we derived an approximation strategy which uses signals to enhance trading performance and a trading venue to hedge risk. The second problem is multi-asset optimal execution and statistical arbitrage, where the agent updates her estimation of the drift throughout the execution programme.

Appendix A Proof of Proposition 1

Take and consider the control The dynamics of the problem starting at become

and the performance criterion for the strategy becomes

In the remainder of the proof, the controlled process notation is dropped, i.e., we write and for all Next, write the solution of the SDE for the dynamics of for all as

| (50) |

where

To prove this point, consider the integrator and notice that

where Assumption 1-(iii) is used.777In particular, when the matrices and commute for all , so do the matrices and and so do the matrices and Next, integrate both sides to find the dynamics in (50). Notice that the solution is normal and write

where

for all

Use Fubini for and write

where

Appendix B Proof of Theorem 1

From HJB to Riccati

First, the HJB equation associated with the control problem (10) is

| (62) | ||||

| (63) |

for all with terminal condition

| (64) |

Consider the function defined in (14) and notice that it solves the HJB

| (65) | ||||

| (66) |

with terminal condition

| (67) |

The supremum in (65) is attained for the optimal control

| (68) |

Replace in (65) to obtain the new HJB

| (69) | ||||

| (70) |

Next, use the definition of in (14), replace in the HJB (69), and identify the terms of the polynomial to obtain the ODE system

| (71) |

with terminal conditions and Note that the ODE system in can be solved independently, that the ODE system in admits the solution and finally that is obtained with a simple integration in (13).

Theorem 1 assumes the DRE (1) with terminal condition (3) admits a unique solution. Let , , and be that solution. Consequently, the ODE system (71) admits a unique solution because and is in (13), and the candidate optimal control in feedback is

| (72) |

Define as in (14) and notice it solves the HJB equation (69) with terminal condition (67). Finally, define as in (15) and notice it solves the HJB equation (62) with terminal condition (64), which is the HJB associated to our control problem. Thus, is a candidate solution for the control problem (11).

Admissibility of the optimal control

To prove that in (72) is well-defined and admissible, consider the Cauchy initial value problem,

| (73) |

where , , and

Note from the affine form of in that satisfies a linear growth condition in and is therefore admissible.

Verification

Fix and . To prove that

use Ito’s lemma for and write

| (74) |

where the notation is used and

Next, use (14) and (15) to see that

where The equality in (74) thus becomes

| (75) |

By definition of , we know that and that equality holds for the control in (68) which corresponds to the optimal control (17). Thus, is a nonincreasing process, consequently

The next step is to prove that Note that is affine in and , and because satisfies a linear growth condition with respect to , there exists a constant such that, almost surely for all ,

Use the classical properties of the Brownian motion to write

and use the results in Karatzas and Shreve (2014) to obtain that is a martingale. Thus, because Finally, conclude that

Appendix C Proof of Theorem 2

Cauchy-Lipschitz theorem gives existence and uniqueness of a left-maximal solution on the set Theorem 1 ensures that the associated function defined in (14) is the value function of the problem on any interval where

The proof consists in establishing by contradiction that cannot be finite. This is achieved by providing a-priori bounds for a solution of (1) with terminal condition (3). This proves that the solution does not blow up in finite time.888Bounds are in the sense of the natural order on symmetric matrices: for , if and only if . The proof uses the original control problem to find bounds for the function in the form of polynomials of degree in which translate into bounds for the quadratic term of i.e.,

Lower bound

Fix take and consider the control The same arguments as in the proof A lead to the inequality in (52) which translates into

where

Note that exists in both cases of Theorem 2. The above order translates into the same order for the quadratic components of both polynomials of degree In particular, one obtains a lower bound for in the form

| (77) |

Upper bound

Fix take and notice that

| (78) | ||||

| (79) | ||||

| (80) |

because and are positive matrices. In the remainder of the proof for the upper bound, the controlled process notation is dropped for readability, i.e., we write and for all

Next, use integration by parts to obtain

and use (78) to write

| (81) | ||||

| (82) | ||||

| (83) | ||||

| (84) |

where , , the set is

| (85) |

the process has dynamics

and the last inequality holds because when then

Next, to solve the optimisation problem

| (86) |

define the associated value function as

| (87) |

The value function is the unique solution to the HJB equation

| (88) | ||||

| (89) |

with terminal condition . Next, use the ansatz

to obtain the HJB

| (90) | ||||

| (91) |

with terminal condition . So the HJB (90) becomes

| (92) |

where

where Assumption 1-(ii) ensures that is invertible. The optimal control in feedback form is

| (93) |

Next, use the ansatz to obtain the system of ODEs

| (94) |

with terminal condition . The system of ODEs (94) admits a unique solution because the equation in is a linear system. Moreover, and is obtained by a simple integration. The optimal control in feedback form in (95) becomes

| (95) |

Note that we obtain a classical solution to the optimisation problem (86) and a similar verification argument as in Theorem 1 ensures that the solution to the HJB corresponds to the value function . Thus, the inequality (81) becomes

thus

The above order translates into the same order for the quadratic components of both polynomials of degree In particular, one obtains an upper bound for in the form

| (96) |

Existence

As is considered finite, there exists with such that , stays in the compact set . This contradicts the maximality of the solution, hence , proving the result.

References

- Abou-Kandil et al. (2012) Abou-Kandil, H., Freiling, G., Ionescu, V., Jank, G., 2012. Matrix Riccati equations in control and systems theory. Birkhäuser.

- Alfonsi and Schied (2010) Alfonsi, A., Schied, A., 2010. Optimal trade execution and absence of price manipulations in limit order book models. SIAM Journal on Financial Mathematics 1, 490–522.

- Almgren (2012) Almgren, R., 2012. Optimal trading with stochastic liquidity and volatility. SIAM Journal on Financial Mathematics 3, 163–181.

- Almgren and Chriss (1999) Almgren, R., Chriss, N., 1999. Value under liquidation. Risk 12, 61–63.

- Avellaneda and Stoikov (2008) Avellaneda, M., Stoikov, S., 2008. High-frequency trading in a limit order book. Quantitative Finance 8, 217–224.

- Barzykin et al. (2022) Barzykin, A., Bergault, P., Guéant, O., 2022. Dealing with multi-currency inventory risk in fx cash markets. arXiv preprint arXiv:2207.04100 .

- Barzykin et al. (2023) Barzykin, A., Bergault, P., Guéant, O., 2023. Algorithmic market making in dealer markets with hedging and market impact. Mathematical Finance 33, 41–79.

- Bergault et al. (2021) Bergault, P., Drissi, F., Guéant, O., 2021. Multi-asset optimal execution and statistical arbitrage strategies under ornstein-uhlenbeck dynamics. arXiv preprint arXiv:2103.13773 .

- Bergault et al. (2018) Bergault, P., Evangelista, D., Guéant, O., Vieira, D., 2018. Closed-form approximations in multi-asset market making. arXiv preprint arXiv:1810.04383 .

- Bertsimas and Lo (1998) Bertsimas, D., Lo, A.W., 1998. Optimal control of execution costs. Journal of financial markets 1, 1–50.

- Bhudisaksang and Cartea (2021) Bhudisaksang, T., Cartea, A., 2021. Adaptive robust control in continuous time. SIAM Journal on Control and Optimization 59, 3912–3945.

- Bismuth et al. (2019) Bismuth, A., Guéant, O., Pu, J., 2019. Portfolio choice, portfolio liquidation, and portfolio transition under drift uncertainty. Mathematics and Financial Economics 13, 661–719.

- Brémaud and Jacod (1977) Brémaud, P., Jacod, J., 1977. Processus ponctuels et martingales: résultats récents sur la modélisation et le filtrage. Advances in Applied Probability 9, 362–416.

- Cartea et al. (2017) Cartea, Á., Donnelly, R., Jaimungal, S., 2017. Algorithmic trading with model uncertainty. SIAM Journal on Financial Mathematics 8, 635–671.

- Cartea et al. (2022a) Cartea, Á., Drissi, F., Monga, M., 2022a. Decentralised finance and automated market making: Execution and speculation. Available at SSRN .

- Cartea et al. (2022b) Cartea, Á., Drissi, F., Monga, M., 2022b. Decentralised finance and automated market making: Predictable loss and optimal liquidity provision. Available at SSRN .

- Cartea et al. (2023) Cartea, Á., Drissi, F., Osselin, P., 2023. Bandits for algorithmic trading with signals. Available at SSRN 4484004 .

- Cartea et al. (2022c) Cartea, Á., Flora, M., Vargiolu, T., Slavov, G., 2022c. Optimal cross-border electricity trading. SIAM Journal on Financial Mathematics 13, 262–294.

- Cartea et al. (2019) Cartea, Á., Gan, L., Jaimungal, S., 2019. Trading co-integrated assets with price impact. Mathematical Finance 29, 542–567.

- Cartea and Jaimungal (2016) Cartea, Á., Jaimungal, S., 2016. Incorporating order-flow into optimal execution. Mathematics and Financial Economics 10, 339–364.

- Cartea et al. (2015) Cartea, Á., Jaimungal, S., Penalva, J., 2015. Algorithmic and high-frequency trading. Cambridge University Press.

- Cartea et al. (2014) Cartea, Á., Jaimungal, S., Ricci, J., 2014. Buy low, sell high: A high frequency trading perspective. SIAM Journal on Financial Mathematics 5, 415–444.

- Cartea et al. (2021) Cartea, Á., Jaimungal, S., Sánchez-Betancourt, L., 2021. Latency and liquidity risk. International Journal of Theoretical and Applied Finance 24, 2150035.

- Cartea and Sánchez-Betancourt (2022a) Cartea, Á., Sánchez-Betancourt, L., 2022a. Brokers and informed traders: dealing with toxic flow and extracting trading signals. Available at SSRN .

- Cartea and Sánchez-Betancourt (2022b) Cartea, Á., Sánchez-Betancourt, L., 2022b. Optimal execution with stochastic delay. Finance and Stochastics , 1–47.

- Cartea and Wang (2020) Cartea, Á., Wang, Y., 2020. Market making with alpha signals. International Journal of Theoretical and Applied Finance 23, 2050016.

- Casgrain and Jaimungal (2019) Casgrain, P., Jaimungal, S., 2019. Trading algorithms with learning in latent alpha models. Mathematical Finance 29, 735–772.

- Chen et al. (1998) Chen, S., Li, X., Zhou, X.Y., 1998. Stochastic linear quadratic regulators with indefinite control weight costs. SIAM Journal on Control and Optimization 36, 1685–1702.

- Donnelly (2022) Donnelly, R., 2022. Optimal execution: A review. Available at SSRN .

- Fermanian et al. (2016) Fermanian, J.D., Guéant, O., Pu, J., 2016. The behavior of dealers and clients on the european corporate bond market: the case of multi-dealer-to-client platforms. Market microstructure and liquidity 2, 1750004.

- Fleming and Rishel (2012) Fleming, W.H., Rishel, R.W., 2012. Deterministic and stochastic optimal control. volume 1. Springer Science & Business Media.

- Forde et al. (2022) Forde, M., Sánchez-Betancourt, L., Smith, B., 2022. Optimal trade execution for Gaussian signals with power-law resilience. Quantitative Finance 22, 585–596.

- Forsyth et al. (2012) Forsyth, P., Kennedy, S., Tse, S.T., Windcliff, H., 2012. Optimal trade execution: a mean quadratic variation approach. Journal of Economic dynamics and Control 36, 1971–1991.

- Fouque et al. (2021) Fouque, J.P., Jaimungal, S., Saporito, Y.F., 2021. Optimal trading with signals and stochastic price impact. arXiv preprint arXiv:2101.10053 .

- Gatheral et al. (2012) Gatheral, J., Schied, A., Slynko, A., 2012. Transient linear price impact and fredholm integral equations. Mathematical Finance: An International Journal of Mathematics, Statistics and Financial Economics 22, 445–474.

- Glosten and Milgrom (1985) Glosten, L.R., Milgrom, P.R., 1985. Bid, ask and transaction prices in a specialist market with heterogeneously informed traders. Journal of financial economics 14, 71–100.

- Guéant (2015) Guéant, O., 2015. Optimal execution and block trade pricing: a general framework. Applied Mathematical Finance 22, 336–365.

- Guéant (2016) Guéant, O., 2016. The Financial Mathematics of Market Liquidity: From optimal execution to market making. volume 33. CRC Press.

- Guéant (2017) Guéant, O., 2017. Optimal market making. Applied Mathematical Finance 24, 112–154.

- Guéant et al. (2012) Guéant, O., Lehalle, C.A., Fernandez-Tapia, J., 2012. Optimal portfolio liquidation with limit orders. SIAM Journal on Financial Mathematics 3, 740–764.

- Guéant et al. (2013) Guéant, O., Lehalle, C.A., Fernandez-Tapia, J., 2013. Dealing with the inventory risk: a solution to the market making problem. Mathematics and financial economics 7, 477–507.

- Guéant and Manziuk (2019) Guéant, O., Manziuk, I., 2019. Deep reinforcement learning for market making in corporate bonds: beating the curse of dimensionality. Applied Mathematical Finance 26, 387–452.

- Ho and Stoll (1983) Ho, T.S., Stoll, H.R., 1983. The dynamics of dealer markets under competition. The Journal of finance 38, 1053–1074.

- Hu and Zhou (2003) Hu, Y., Zhou, X.Y., 2003. Indefinite stochastic riccati equations. SIAM Journal on Control and Optimization 42, 123–137.

- Jacobson (1973) Jacobson, D., 1973. Optimal stochastic linear systems with exponential performance criteria and their relation to deterministic differential games. IEEE Transactions on Automatic control 18, 124–131.

- Karatzas and Shreve (2014) Karatzas, I., Shreve, S., 2014. Brownian motion and stochastic calculus. volume 113. springer.

- Kohlmann and Zhou (2000) Kohlmann, M., Zhou, X.Y., 2000. Relationship between backward stochastic differential equations and stochastic controls: a linear-quadratic approach. SIAM Journal on Control and Optimization 38, 1392–1407.

- Laruelle et al. (2013) Laruelle, S., Lehalle, C.A., et al., 2013. Optimal posting price of limit orders: learning by trading. Mathematics and Financial Economics 7, 359–403.

- Lim and Zhou (2005) Lim, A.E., Zhou, X.Y., 2005. A new risk-sensitive maximum principle. IEEE transactions on automatic control 50, 958–966.

- Limebeer et al. (1992) Limebeer, D.J., Anderson, B.D., Khargonekar, P.P., Green, M., 1992. A game theoretic approach to H∞ control for time-varying systems. SIAM Journal on Control and Optimization 30, 262–283.

- Rami et al. (2001) Rami, M.A., Chen, X., Moore, J.B., Zhou, X.Y., 2001. Solvability and asymptotic behavior of generalized riccati equations arising in indefinite stochastic lq controls. IEEE Transactions on Automatic Control 46, 428–440.

- Schied and Schöneborn (2009) Schied, A., Schöneborn, T., 2009. Risk aversion and the dynamics of optimal liquidation strategies in illiquid markets. Finance and Stochastics 13, 181–204.

- Whittle (1990) Whittle, P., 1990. A risk-sensitive maximum principle. Systems & Control Letters 15, 183–192.

- Zhou and Li (2000) Zhou, X.Y., Li, D., 2000. Continuous-time mean-variance portfolio selection: A stochastic lq framework. Applied Mathematics and Optimization 42, 19–33.