Forecasting Stock Options Prices via the Solution of an Ill-Posed Problem for the Black-Scholes Equation

Abstract

In the previous paper (Inverse Problems, 32, 015010, 2016), a new heuristic mathematical model was proposed for accurate forecasting of prices of stock options for 1-2 trading days ahead of the present one. This new technique uses the Black-Scholes equation supplied by new intervals for the underlying stock and new initial and boundary conditions for option prices. The Black-Scholes equation was solved in the positive direction of the time variable, This ill-posed initial boundary value problem was solved by the so-called Quasi-Reversibility Method (QRM). This approach with an added trading strategy was tested on the market data for 368 stock options and good forecasting results were demonstrated. In the current paper, we use the geometric Brownian motion to provide an explanation of that effectivity using computationally simulated data for European call options. We also provide a convergence analysis for QRM. The key tool of that analysis is a Carleman estimate.

Key words: Black-Scholes equation, European call options, geometric Brownian motion, probability theory, ill-posed problem, quasi-reversibility method, Carleman estimate, trading strategy.

1 Introduction

A new heuristic mathematical algorithm designed to forecast prices of stock options was proposed in [10]. This algorithm is based on the so-called Quasi-Reversibility Method (QRM). QRM is a regularization method for an ill-posed problem for the Black-Scholes equation. The goal of this paper is to address both analytically and numerically the following question: Why this algorithm has worked well for real market data in [10, 13]? Our explanations are based on our new analytical results in the probability theory and are supported by our numerical results for the computationally simulated data generated by the geometrical Brownian motion.

A significant advantage of the technique of [10] is that it uses historical data about stock and option prices only over short time intervals. This assumption is a practically valuable one since formations of those prices are random processes. This indicates that the information used in the algorithm possesses stable probabilistic characteristics.

The mathematical model of [10] was supplied by a trading strategy. Results of [10, Table 4] for real market data of [3] indicate that a combination of that mathematical model with that trading strategy has resulted in 72.83% profitable options out of 368 options for real market data. More recently, the model of [10] was used in [13] to forecast stock option prices in the case when results of QRM are enhanced by the machine learning approach, which was applied on the second stage of the price forecasting procedure. Market data of [3] for total 169,862 European call stock options were used in [13]. Following the machine learning approach, these data were divided in three sets [13, Table 1]: training (132,912 options), validation (13,401 options) and testing (23,549 options). Total 23,549 options were tested by QRM, and good results on predictions of options with profits were obtained in [13, first lines in Tables 2,3]. Later the authors of [13] have tested the performance of QRM for all those 169,862 options, and results were almost the same as ones of [13, first lines in Tables 2,3]. However, since the latter results are not yet published, then we do not discuss them here.

Remark 1.1: Without further specifications, we consider in this paper only European call options. The mathematical model of [10] does not use neither the payment function at the expiry time nor the strike price.

We now present in Tables 1,2 the most recent results of [13], which were obtained using the method of [10] for the data consisting of 23,549 historical trades collected in 2018. The same market data of [3] were used in Tables 1,2. Option prices for one trading day ahead of the present day were forecasted. Definitions of accuracy, precision and recall are well known, see, e.g. [8].

In Table 1, “Error” means the average relative error of predictions of option prices, i.e.

where is the total number of tested options, and are correct and forecasted prices respectively of the option number

Table 2. The percentage of options with correct predictions of profits via the Quasi-Reversibility Method for the market data of [3] for 23,549 options [13, Table 3]

| Method | Correctly Predicted Profitable Options |

|---|---|

| QRM | 55.77% |

A perfect financial market does not allow a winning strategy [7]. This means that to address the above question, we need to assume that the market is imperfect. The present article considers a model situation, in which there is a difference between the volatility of the underlying stock and traders’ opinion of the volatility of an European call option generated by this stock. We prove analytically that, theoretically, this allows one to design a winning strategy. First, we back up this theory numerically for the ideal case when both volatilities are known. In practice, however, only is approximately known from [3], where implied volatility of option prices is posted. It is reasonable to conjecture that

Second, to address the question posed in the first paragraph of this section for the non ideal case, we consider a mathematical model, in which the dynamics of the stock prices is generated by the stochastic differential equation of the geometric Brownian motion. This allows us to computationally generate the time series of stock prices. At the same time, we assume that the price of the corresponding stock option is governed by the Black-Scholes equation, in which the volatility coefficient is . Hence, using that time series of stock prices, we apply the Black-Scholes formula to get the time series for prices of the corresponding options. Next, we apply the QRM to predict the prices of these options for one trading day ahead of the current one. Next, we formulate the winning strategy for the non ideal case.

Both the theory and the numerical studies of this paper support our two hyphotheses formulated in subsection 6.3. Our first hypothesis that the heuristic algorithm of [10] actually figures out in many cases the sign of the difference . Our second hypothesis is also based on our results below as well as on the “Precision” column of Table 1 and the second column of Table 2. More precisely, the second hypothesis is that probably about 56% of tested 23,549 options of [13] with the real market data had

This algorithm of [10] is based on the solution of a new initial boundary value problem (IBVP) for the Black-Scholes equation, see, e.g. [2, 24] for this equation. Since the Black-Scholes equation is actually a 1-D parabolic Partial Differential Equation (PDE) with the reversed time, then that IBVP is ill-posed, see, e.g. [10] for an example of a high instability of a similar problem. The ill-posedness of that IBVP is the main mathematical obstacle of that algorithm. Therefore, we solve that IBVP both here and in [10] by a specially designed version of QRM. QRM stably solves this problem forwards in time for two consecutive trading days after the current one. QRM is a version of the Tikhonov regularization method [23] being adapted to ill-posed problems for Partial Differential Equations (PDEs). We refer to [16] for the first publication on QRM as well as to [4, 5, 9, 11, 12] for some more recent ones.

We provide a convergence analysis for QRM being applied to the above problem. The main new element of this analysis is that we lift a restrictive assumption of [10] of a sufficiently small time interval. We note that the smallness assumption imposed on the time interval is a traditional one for initial boundary value problems for parabolic PDEs with the reversed time, see [9], [17, Theorem 1 of section 2 in Chapter 4], where a certain Carleman estimate was used. However, a new Carleman estimate was derived in [11] for a general parabolic operator of the second order with variable coefficients in the D case. This estimate enables one to lift that smallness assumption. We simplify here the Carleman estimate of [11] as well as some other results of [11] via adapting them to our simpler 1D case, as compared with the D case of [11].

The Black-Scholes equation describes the dependence of the price of a stock option from the price of the underlying stock and time [1, 2, 24]. In fact, this is a parabolic Partial Differential Equation with the reversed time. Let be the maturity time and is the present time [24]. Traditionally, initial boundary value problems for the Black-Scholes equation are solved backwards with respect to time with the initial condition at . The latter is a well posed problem, for which the classic theory of parabolic PDEs works, see, e.g. the book [15] for this theory.

However, the maturity time is usually a few months away from the present time. It is obviously impossible to accurately predict the future behavior of the volatility coefficient of the Black-Scholes equation on such a large time interval. Since the formations of both stock and option prices are stochastic processes, then it is intuitively clear a good accuracy of forecasting of stock option prices for long time periods is unlikely.

Thus, we focus in this paper on forecasting of option prices for a short time period of just one trading day ahead of the current one. Let the time variable counts trading days. Since there are 255 trading days annually, then we introduce the dimensionless time as

| (1.1) |

Hence,

| (1.2) |

Remark 1.2. To simplify notations, we still use everywhere below the notation for the dimensionless time of (1.1).

Remark 1.3. There are many important questions about the technique of [10], which are not addressed in this paper, such as, e.g. the performance of this technique for some “stress” tests, its performance for significantly larger sets of market data, its performance for the case when the transaction cost is taken into account, and many others. However, addressing any of those questions would require a significant additional effort. Therefore, those questions are outside of the scope of this publication. Still, the question of the transaction cost might probably be addressed using a threshold number in our trading strategy for the non-ideal case, see subsection 6.3.

This paper is organized as follows. In section 2 we show that a winning strategy on an infinitesimal time interval might be possible if In section 3 we present the heuristic mathematical model of [10]. In section 4 we present a convergence analysis for our version of QRM. In section 5 we use arguments of the probability theory to justify our trading strategy in the ideal case when both volatilities and are known. In section 6 we describe our numerical studies and end up with a trading strategy for the non ideal case when only the volatility is known. In addition, we formulate in section 6 our two hyphotheses mentioned above. Concluding remarks are given in section 7.

Disclaimer. This paper is written for academic purposes only. The authors do not provide any assurance that the technique of this paper would result in a successful trading on a real financial market.

2 A Possible Winning Strategy

Let be the volatility of a certain stock and be the price of this stock. Consider an option corresponding to this stock. Let be an idea of the volatility of that option, which has been developed among the agents, who trade this option on the market. If , then the financial market is imperfect, and an opportunity for designing a winning strategy exists.

At a given time , the time until the maturity will occur is

| (2.1) |

Let be the stock price and be the payoff function of that option at the maturity time We assume that the risk-free interest rate is zero. Let be the price of that option and the variable is the one defined in (2.1). We assume that the function satisfies the Black-Scholes equation with the volatility coefficient [1, Chapter 7, Theorem 7.7]:

| (2.2) |

The specific formula for the payoff function is , where is the strike price [1]. Then the price function of the option is given by the Black-Scholes formula [1]:

| (2.3) |

where and

| (2.4) |

Let The stochastic equation of the geometric Brownian motion for the stock price with the volatility has the form where is the Wiener process. The Itô formula implies

| (2.5) |

where is the option price change on an infinitesimal time interval and is the Wiener process.

| (2.6) |

The mathematical expectation of is zero [1, Chapter 4]. Therefore, we find that the expected value of the increment of the option price on an infinitesimal time interval is

| (2.7) |

In the mathematical finance, the second derivative

| (2.8) |

is called Greek For an European call option [1, Chapter 9]

| (2.9) |

Therefore, it follows from (2.7)-(2.9) that the sign of the mathematical expectation of the increment of the option price on an infinitesimal time interval is determined by the sign of the difference Thus, if then a possible winning strategy involves buying an option at the present time and selling it in the next trading period. If then the winning strategy is to take the short position at the present time and to close the short position in the next trading period.

3 The Mathematical Model

3.1 The model

We now describe the mathematical model of [10]. We use this model here for computationally simulated data. Also, it was used in [13] for real market data to obtain the above Tables 1,2. We do not differentiate in this model between volatilities and and just use the time dependent volatility

Everywhere below, as the dimensionless time, we still use the notation for in (1.1) for brevity. Let be the volatility of the option at the moment of time . When working with the market data in [10, 13], we have used the historical implied volatility listed on the market data of [3]. Let and be respectively the bid and ask prices of the option and and be the bid and ask prices of the stock. It is known that

For brevity, we simplify notations as , . We impose a natural assumption that

It was observed on the market data in [10, formulas (2.3)-(2.6)] that the relative differences are usually small,

| (3.1) |

Hence, we define the initial condition at of the function as the linear interpolation on the interval between and

| (3.2) |

Define the domain We assume that the volatility of the option depends only on , i.e. Let be the partial differential operator of the Black-Scholes equation,

| (3.3) |

We impose the following initial and boundary conditions on the function

| (3.4) |

| (3.5) |

Conditions (3.3)-(3.5) represent the heuristic mathematical model of [10, formulas (2.3)-(2.6)]. Also, (3.3)-(3.5) is our IBVP for the Black-Scholes equation. We now formulate this as Problem 1:

Problem 1 is ill-posed since we need to solve equation (3.3) forwards in time.

Remarks 3.1:

- 1.

-

2.

As it is a conventional way in the theory of Ill-Posed problems, we increase here the required smoothness of the solution from to

3.2 Three steps

In order to solve Problem 1, we need first to define the time dependent option’s volatility and boundary conditions , Then the initial condition in (3.4) would be found via (3.4). We explain these in Steps 1,2 of this subsection 3.2.

In our computations of [10, 13] we have used the Implied Volatility of the options in the Last Trade Price (IVOL) of the day for [3]. As to and we have used the End of the Day Underlying Price Ask and the End of Day Underlying Price Bid of [3]. Similarly for and in which case the End of the Day Option Price Ask and the End of Day Option Price Bid of [3] were used. The moment of time is the End of the Present Day Time, and similarly for the following two trading days of and for the preceding two trading days Naturally, the question can be raised here on how did we find future values of boundary conditions and for in (3.5), and the same for This question is addressed in Step 2 below. Our method for the solution of Problem 1 consists of three steps:

Step 1 (introducing dimensionless variables). First, we make equation (3.3) dimensionless. Recall that Introduce the dimensionless variable for as:

Let denotes one dimensionless trading day. By (1.2)

| (3.6) |

By (3.2) the function is transformed in the function

| (3.7) |

And the operator in (3.3) is transformed in the operator ,

| (3.8) |

| (3.9) |

| (3.10) |

Problem is transformed in Problem 2:

Problem 2. Assume that functions

| (3.11) |

Find the solution of the following initial boundary value problem:

| (3.12) |

| (3.13) |

| (3.14) |

where the partial differential operator is defined in (3.8), the function is defined in (3.9), the initial condition is defined in (3.7), and the domain is defined in (3.10).

Step 2 (interpolation and extrapolation). Having the historical market data for an option up to “today”, we forecast the option price for “tomorrow” and “the day after tomorrow”, with 255 trading days annually. “One day” corresponds to “Today” means “Tomorrow” means “The day after tomorrow” means We forecast these prices for the interval as via the solution of problem (3.12)-(3.13). To do this, however, we need to know functions and in the “future”, i.e. for We obtain approximate values of these functions via interpolation and extrapolation procedures described in the next paragraph.

Let be “the day before yesterday”, be “yesterday” and be “today”. Let be any of three functions . First, we interpolate the function by the quadratic polynomial for using the values We obtain

| (3.15) |

Next, we extrapolate (3.15) on the interval via setting

The so defined functions were used to numerically solve problem (3.12)-(3.13) for both the computationally simulated data below and for real market data of Tables 1,2 above as well as in [10].

Step 3 (Numerical solution of Problem 2. Regularization). Since problem (3.3)-(3.5) is ill-posed, then we apply a regularization method to obtain an approximate solution of this problem. More precisely, we solve the following problem:

Minimization Problem 1. Let be the regularization Tikhonov functional defined as:

| (3.16) |

where is the regularization parameter. Minimize functional (3.16) on the set where

| (3.17) |

Minimization Problem 1 is a version of QRM for Problem 2. This version is an adaptation of the QRM for problem (3.12)-(3.13). In section 4 we present the theory of this specific version of the QRM. In particular, Theorem 4.2 of section 4 implies uniqueness of the solution of Problem 2 and provides an estimate of the stability of this solution with respect to the noise in the data. Theorem 4.3 of section 4 implies existence and uniqueness of the minimizer of the functional on the set defined in (3.17). Following the theory of Ill-Posed problems, we call such a minimizer “regularized solution” [23]. Theorem 4.4 estimates convergence rate of regularized solutions to the exact solution of Problem 2 with the noiseless data. These estimates depend on the noise level in the data.

4 Convergence Analysis

In this section, we provide convergence analysis for Problem 2 of subsection 3.2. This problem is the IBVP for parabolic equation (3.12) with the reversed time, see (3.8). The QRM for this problem for a more general parabolic operator in with arbitrary variable coefficients was proposed in [9] and convergence analysis was also carried out there. Then corresponding theorems were reformulated in [10]. Although a stability estimate was not a part of [10], such an estimate was proven in [9]. It was pointed out in Introduction, however, that traditional stability estimates for this problem were proven, using a certain Carleman estimate, only under the assumption that the time interval is sufficiently small. The same is true for the convergence theorems of QRM in [9, 10]. Unlike this, the smallness assumption was lifted in [11] via a new Carleman estimate. In this section, we significantly modify results of [11] for a simpler 1-D case. Recall (see Introduction) that this modification allows us to obtain more accurate estimates in the 1-D case, as compared with the D case of [11]. We note that even though we work in our computations below on a small time interval (see (3.6) and (3.10)), the smallness assumption of [9, 10], [17, Theorem 1 of section 2 in Chapter 4] might result in the requirement of even a smaller length of that interval.

4.1 Problem statement

Consider a number and denote

Let two numbers and Let the function satisfies:

| (4.1) |

Let functions In the above case of subsection 3.2,

We now formulate Problem 3, which is a slight generalization of Problem 2.

Problem 3. Find a solution of the following initial boundary value problem (IBVP):

| (4.2) |

| (4.3) |

| (4.4) |

Remark 4.1. Since Problem 3 is a more general one than Problem 2, then our convergence analysis for Problem 3, which we provide below, is also valid for Problem 2.

The reason why we use the linear function for in (4.4) is our desire to simplify the presentation by using the fact that, in the case of Problem 2, the initial condition in (3.14) is the linear function defined in (3.7). Problem 3 is an IBVP for the parabolic equation (4.2) with the reversed time. Therefore, this problem is ill-posed. Just as it is always the case in the theory of Ill-Posed problems [23], we assume that the boundary in (4.3) are given with a noise of the level where is a sufficiently small number, i.e.

| (4.5) |

where functions are “ideal” noiseless data. Following to one of postulates of the theory of Ill-Posed problems, we assume that there exists an exact solution of problem (4.2)-(4.4) with these noiseless data. We will estimate below how this noise affects the accuracy of the solution of Problem 3 (if this solution exists) and also will establish the convergence rate of numerical solutions obtained by QRM to the exact one as

Consider the following analog of functional (3.16):

| (4.6) |

Introduce the set

| (4.7) |

We construct an approximate solution of Problem 3 via solving the following problem:

Minimization Problem 2. Minimize the functional on the set given in (4.7).

Similarly with the Minimization Problem1, Minimization Problem 2 means QRM for Problem 3.

4.2 Theorems

In this subsection, we formulate four theorems for Problem 3. Let be a parameter. Introduce the Carleman Weight Function for the operator as:

| (4.8) |

Hence, the function is decreasing on ,

| (4.9) |

Denote

| (4.10) |

| (4.11) |

Theorem 4.1 (Carleman estimate). Let the coefficient of the operator satisfies conditions (4.1). Then there exist a sufficiently large number and a constant both depending only on listed parameters, such that the following Carleman estimate holds for the operator

| (4.12) |

Carleman estimate (4.12) is the key to proofs of Theorems 4.2, 4.4.

Theorem 4.2 (Hölder stability estimate for Problem 3 and uniqueness). Let the coefficient of the operator satisfies conditions (4.1). Assume that the functions and are solutions of Problem 3 with the vectors of data and respectively, where Also, assume that error estimates (4.5) of the boundary data hold. Choose an arbitrary number . Denote

| (4.13) |

Then there exists a sufficiently small number and a constant both depending only on listed parameters, such that the following stability estimate holds for all

| (4.14) |

Below and denote different constants depending only on listed parameters.

Corollary 4.1 (uniqueness). Let the coefficient of the operator satisfies conditions (4.1). Then Problem 3 has at most one solution (uniqueness).

Proof. If then (4.14) implies that in Since is an arbitrary number, then in

Theorem 4.3 (existence and uniqueness of the minimizer). Let functions Let be the set defined in (4.7). Then there exists unique minimizer of functional (4.6) and

| (4.15) |

In the theory of Ill-Posed Problems, this minimizer is called “regularized solution” of Problem 3 [23]. According to the theory of Ill-Posed problems, it is important to establish convergence rate of regularized solutions to the exact one In doing so, one should always choose a dependence of the regularization parameter on the noise level i.e. [23].

Theorem 4.4 (convergence rate of regularized solutions). Let be the solution of Problem 3 with the noiseless data Let functions Let be the unique minimizer of functional (4.6) on the set . Assume that error estimates (4.5) hold. Choose an arbitrary number . Let be the number defined in (4.13) and let

| (4.16) |

Then there exists a sufficiently small number depending only on listed parameters such that the following convergence rate of regularized solutions holds for all

| (4.17) |

4.3 Proof of Theorem 4.1

We assume in this proof that The case can be obtained via density arguments. It is assumed in this proof that and is sufficiently large. We remind that denotes different constants depending only on listed parameters. Change variables as

| (4.18) |

Hence,

Hence,

| (4.19) |

We have used here We now estimate from the below terms in the second line of (4.19).

Step 1. Estimate from the below We have:

Thus,

| (4.20) |

Step 2. Estimate from the below We have:

| (4.21) |

Step 3. Estimate from the below the entire second line of (4.19). Using (4.20), (4.21) and Cauchy-Schwarz inequality “with

| (4.22) |

we obtain

Thus, we have obtained that

| (4.23) |

Using (4.19) and (4.23) as well as dropping the non-negative term in the right hand side of (4.23), we obtain

| (4.24) |

4.4 Proof of Theorem 4.2

Introduce the following functions:

| (4.31) |

| (4.32) |

| (4.33) |

| (4.34) |

| (4.35) |

It follows from (4.4), (4.5) and (4.31)-(4.35) that:

| (4.36) |

| (4.37) |

| (4.38) |

Square both sides of equation (4.39), multiply by the function and integrate over the domain Using (4.9) and (4.38), we obtain

| (4.43) |

Hence, applying Carleman estimate (4.12) to the left hand side of (4.43) and taking into account (4.9)-(4.11), we obtain

| (4.44) |

Since and also since by (4.8) in then (4.44) implies

| (4.45) |

4.5 Proof of Theorem 4.3

Denote the scalar product in the space Let be the function defined in (4.34). Then, using (4.6) and (4.37), consider the functional

| (4.54) |

Suppose that the function is a minimizer of the functional on the space i.e.

| (4.55) |

Consider the function Then it follows from (4.11) and (4.32) that where the set is defined in (4.7). Also, Hence, (4.55) implies that the function is a minimizer of the functional on the set .

We now prove the reverse. Suppose that a function is a minimizer of the functional on the set , i.e.

| (4.56) |

Consider the function And for every function consider the function Then by (4.56)

Hence, is a minimizer of functional (4.54) on the space Therefore, it is sufficient to find a minimizer of the functional on the space

By the variational principle the function is a minimizer of the functional if and only if the following integral identity is satisfied:

| (4.57) |

Consider a new scalar product in defined as

Recall that Obviously,

Hence, norms and are equivalent. Hence, one can consider the scalar product as the scalar product in

Hence, we can rewrite (4.57) as

| (4.58) |

The right hand side of (4.58) can be estimated as

Hence, the right hand side of (4.58) can be considered as a bounded linear functional of Hence, by Riesz theorem there exists unique function such that

Comparing this with (4.58), we obtain

Therefore, Thus, we have proven existence and uniqueness of the minimizer of the functional on the space Therefore, it follows from the discussion in the beginning of this proof that there exists unique minimizer of the functional on the set and this minimizer is

4.6 Proof of Theorem 4.4

We still use notations (4.31)-(4.35). By Corollary 4.1 Problem 3 has at most one solution. Hence, there exists unique exact solution of Problem 3 with the data in (4.3) and (4.4). Hence, we have the following analog of integral identity (4.57)

| (4.59) |

Subtract (4.59) from (4.57). Then, using (4.33), (4.35) and (LABEL:7.52), we obtain

| (4.60) |

Set in (4.60) Then, using (4.38) and Cauchy-Schwarz inequality, we obtain

| (4.61) |

| (4.62) |

Inequality (4.61) is equivalent with

Since by (4.9) in then (4.61) implies

| (4.63) |

Hence, applying Carleman estimate (4.12) to the left hand side of (4.63) and recalling again that , we obtain

Hence, we obtain similarly with (4.45)

Combining this with (4.62), we obtain

| (4.64) |

Suppose now that as stated in (4.16). Choose as in (4.46) and as in (4.48). Then (4.47), (4.49), (4.52) and (4.64) imply

| (4.65) |

The target estimate (4.17) of this theorem follows immediately from the triangle inequality, (4.5), (4.31)-(4.35) and (4.65).

5 Probabilistic Arguments for a Trading Strategy

A heuristic algorithm of section 3 can be used as the basis for a trading strategy of options. The algorithm predicts the option price change relatively to the current price. The fact that this algorithm uses the information about stock and option prices only over a small time period makes realistic the assumptions of the model of Section 2 about the volatilities being independent on time. Formulas (2.6) and (2.9) indicate that the sign of the mathematical expectation of the option price increment should likely define the trading strategy. In addition to the mathematical expectation of the option price increment, it is necessary to take into account indicators that reflect the risk of using that trading strategy. This is because the option price dynamics is described by a random process. Based on the model of Section 2, we construct in this section such indicators for a ”perfect” trading strategy, which always correctly predicts the sign of the mathematical expectation of the option price increment.

We assume in this section that both the volatility of the stock and the idea of the volatility of the call option, which has been developed among the participants involved in trading of this option, are known. Recall that we have assumed in Section 2 that the dynamics of the stock price is described by a stochastic differential equation of the geometric Brownian motion with the initial condition , and also that the corresponding option price is , where and the function can be found by the Black-Scholes formula (2.5). The option price expected by option market participants is described by a stochastic process , where the expected stock price satisfies the stochastic differential equation of the geometric Brownian motion with the initial condition

| (5.1) |

Here is a Wiener process, and the processes and are independent.

Let be a certain moment of time and be a sufficiently small number. The true option price at the moment of time is On the other hand, at the same moment of time the price of this option expected by the participants of the market is . It follows from (2.6) that, on the small time interval a winning trading strategy of the options trading should be based on an estimate of the probability that . This probability is given in Theorem 5.1.

Theorem 5.1. Let be a sufficiently small number and be the function defined in (2.4). The probability that at the time the true option price is greater than the price expected by the participants of the options market is

| (5.2) |

Proof. The derivative

is called the Greek delta. This parameter for a call option is

| (5.3) |

Since by (5.3) then the inequality is equivalent to the inequality . It follows from (5.1) that the latter inequality is equivalent with

It follows from the properties of the geometric Brownian motion, see, e.g. [19, Chapter 5, section 5.1] that the random variables

are normally distributed. Hence, the difference of these two random variables is also a normally distributed random variable, see, e.g. [14, Chapter 9, section 9.3], i.e.

Therefore, the value given by formula (5.2) is indeed the probability that the true option price is greater than the expected option price

Theorem 5.1 implies that the operation of buying an option at the time moment and selling it at the time moment will be profitable with the probability given in (5.2), and this operation will be non-profitable with the probability

Hence, if , then it is reasonable to buy an option at the moment of time and sell it at the moment of time Otherwise, it is reasonable to go in the short position on the option at . Suppose that . A winning strategy, which takes into account risks, should involve the repetition operation multiple times with the same independent probabilities of outcomes. Consider non-overlapping small time intervals of the same duration on which the option purchase operations are carried out at the moment of time with the subsequent sale at the moment of time .

Consider random variables

| (5.4) |

If then the operation of buying that option at the moment of time and selling it at the moment of time was profitable. If then that operation was non profitable. The random variables are independent identically distributed random variables [14, Chapter 18, section 18.1]. The frequency of profitable trading operations is characterized by the random variable

| (5.5) |

It follows from [14, Chapter 9, section 9.3] that the variable has a binomial distribution with the mathematical expectation given in (5.2) and with the dispersion , where

| (5.6) |

By the Central Limit Theorem of de Moivre-Laplace, the probability that more than half of trades are profitable is estimated as [14, Chapter 2, section 2.2]:

| (5.7) |

| (5.8) |

In our trading strategy, we decide to make transactions if and only if the probability of the profitable trading is not less than a given value Hence, by (5.7) and (5.8)

| (5.9) |

where is the inverse function of the function of (2.4). By (5.9)

Thus, we should have

| (5.10) |

To fulfill inequality (5.10), the imperfection of the stock market must be significant. More precisely, it follows from (5.2) and (5.10) that the difference between the volatilities and must satisfy the following inequality:

| (5.11) |

Based on this estimate of the difference , we design a trading strategy in the ideal case. “Ideal” means that we know both volatilities and

Trading Strategy for the Ideal Case:

Let and be two threshold numbers. Our trading strategy considers three possible scenarios:

-

1.

If , then it is recommended to buy a call option at the current moment of time with the subsequent sale at the next moment of time .

-

2.

If , then then it is recommended to go short at the current moment of time , followed by closing the short position at time .

-

3.

If , then it is recommended to refrain from trading.

The threshold values and might probably estimated via numerical simulations using the method of section 3, combined with formula (5.11).

6 Numerical Studies

6.1 Some numerical details for the algorithm of section 3

We have computationally simulated the market data as described in subsection 6.2. These data gave us initial and boundary conditions (3.2), (3.4) and (3.5), which, in turn, led us to (3.14), (3.13), see Steps 1,2 of subsection 3.2. Next, we have solved Minimization Problem (3.16), (3.17). To minimize functional (3.16), we wrote and in finite differences and, using the conjugate gradient method, have minimized the resulting discrete functional with respect to the values of the function at grid points. The starting point of the minimization procedure was . The regularization parameter was the same as in [10], and it was chosen by trial and error. The step sizes and of the finite difference scheme with respect to and were and respectively. Since by (3.6) and (3.10) then we had 100 grid points with respect to each variable and

6.2 The data

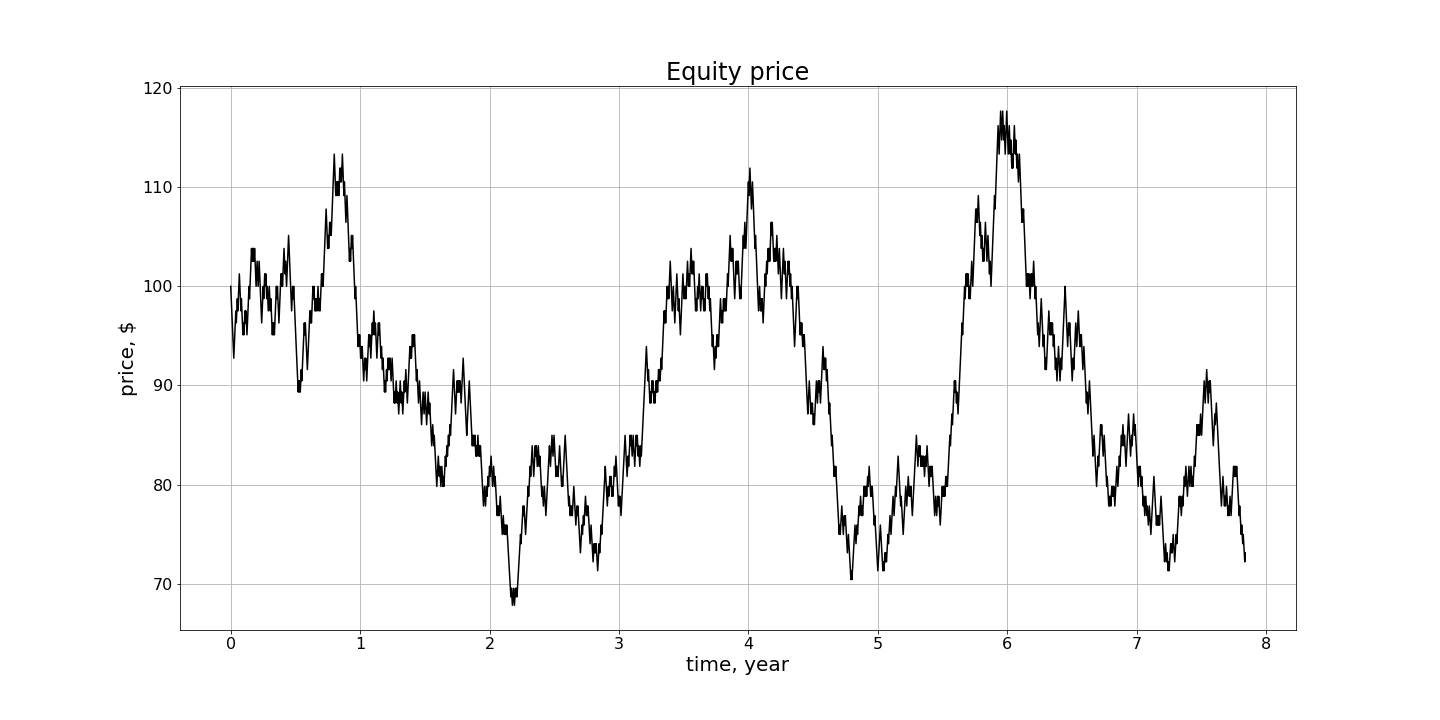

We construct the stock price trajectory as a solution to the stochastic differential equation with the initial condition where We model the stock prices and then the prices of 90-days European call options of this stock during the life of the stock, assuming that the options are reissued many times with the same maturity date of 90 days. Thus, we obtain a time series We set the payoff function for each option The generated stock price trajectory is shown on Figure 1.

The probabilistic analysis of section 5 of the random variable characterizes the effectiveness of an “ideal” trading strategy. Thus, we consider the ideal case first. Recall that “ideal” means here that this strategy is based on the knowledge of the information about the imperfection of the financial market, i.e. on the knowledge of both volatilities and . However, in the real market data only approximate values of are available [3].

We test total thirty three (33) values of More precisely, in our computational simulations, we took the discrete values of where

| (6.1) |

We now generate the function, which describes the dependence of the mathematical expectation of the random variable in (5.5) on . Keeping in mind that in all cases, we compute for each of the discrete values of in (6.1) the mathematical expectation of the random variable . We use formula (5.2) for also, see (2.4). This way we obtain the function which is the above dependence for the ideal case.

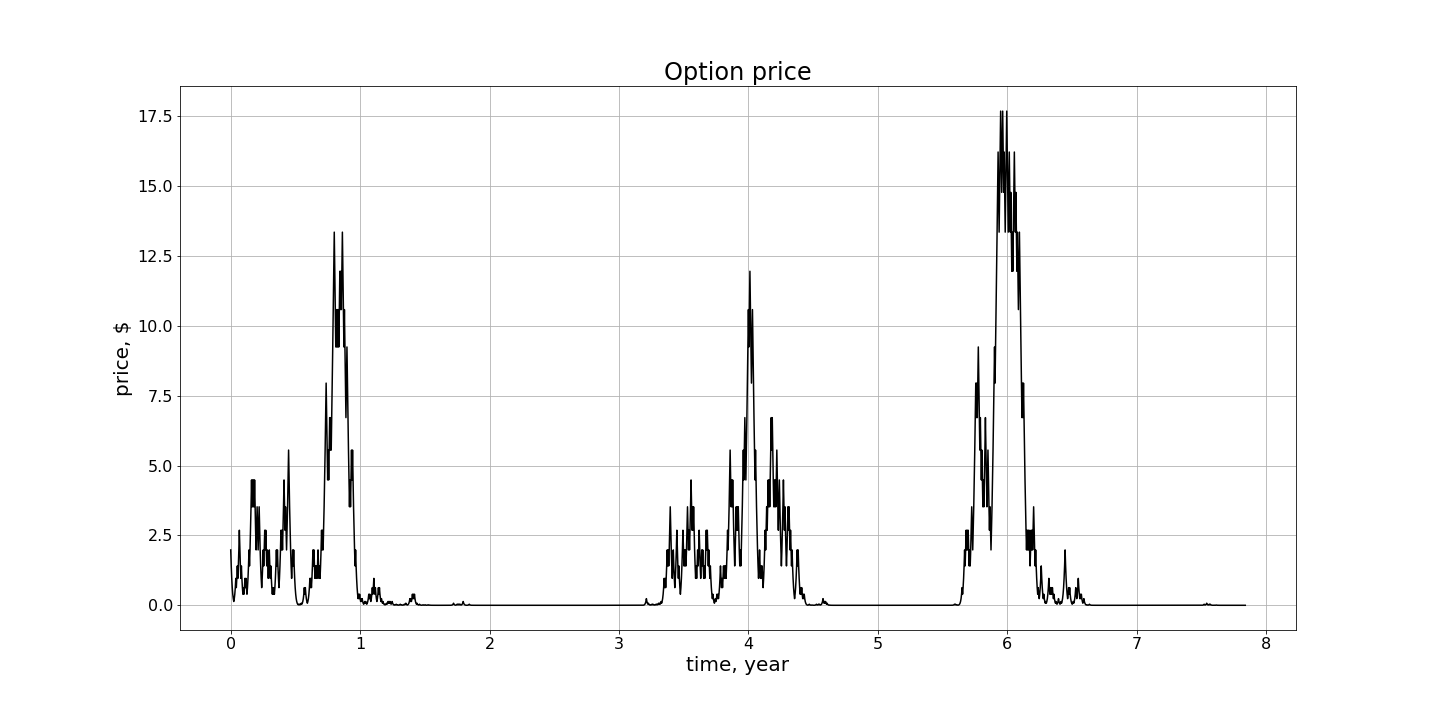

Second, we consider a non-ideal case. More precisely, we test how our heuristic algorithm works for the computationally simulated data described in this subsection. We choose non-overlapping time intervals where means one dimensionless trading day, see (1.2) and (3.6). We still use the dimensionless time as in (1.1), while keeping the same notation for brevity. For every fixed value of indicated in (6.1), we calculate the option price where the function is given by Black-Scholes formula (2.3). Thus, numbers form the option price trajectory. Figure 2 displays a sample of the trajectory of the option price for Based on (3.1), we set bid and ask stock prices as well as corresponding bid and ask option prices as:

Next, we solve Problem 2 of section 3 for each on the time interval by the algorithm of that section. When doing so, we take in (3.8) for for all In particular, this solution via QRM gives us the function We set the predicted price of the option at the moment of time as:

| (6.2) |

6.3 Results

For every discrete value of in (6.1), we introduce the sequence This sequence is similar with the sequence in (5.4). Recall that and are true prices of the option at the moments of time and respectively. We set

| (6.3) |

Next, we introduce the function of the discrete variable as:

| (6.4) |

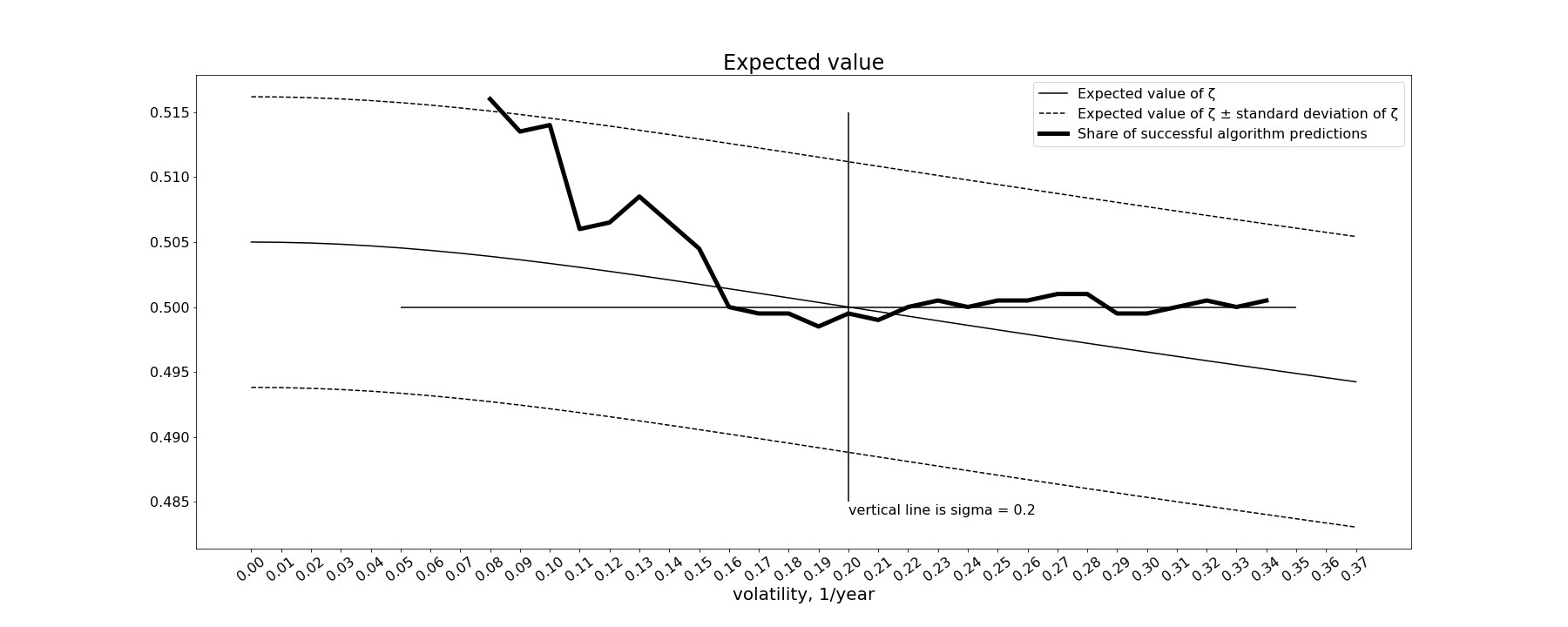

It follows from (6.3) and (6.4) that is the frequency of correctly predicted profitable cases for trading of this option with the market’s opinion of the volatility of the option. Predictions are performed by our algorithm of section 3. Comparison of (5.4) and (5.5) with (6.3) and (6.4) shows that is similar with the ideal case of the random variable The bold faced curve on Figure 3 depicts the graph of the function The middle non-horizontal curve on Figure 3 depicts the graph of the function which was constructed in subsection 6.2 for the ideal case. The upper and the lowest curves on Figure 3 display the shifts of the ideal curve up and down by where is the dispersion of and is given in (5.6). In other words, there is a high probability chance that the values of are contained in the trust corridor between these two curves. The vertical line indicates the “critical” value where is the volatility of the stock.

One can see from the bold faced curve of Figure 3 that as long as is either rather close to or the short position of this option represents a significant risk. However, when becomes less than the probability of the profit in the short position increases. This coincides with the prediction of our theory.

The bold faced curve is an analog of the middle curve of the mathematical expectation of the random variable in the ideal case. Since the bold faced curve on Figure 3 lies within the trust corridor of the ideal algorithm, then we conclude that our prediction accuracy of profitable cases is comparable with the ideal one.

Unlike the ideal case, in a realistic scenario of the financial market data of, e.g. [3] only the information about the approximate values of is available. It is this information, which was used in [10, 13] and, in particular, in Tables 1,2.

Thus, our results support the following trading strategy in the non-ideal case:

Trading Strategy for the Non-Ideal Case:

Let be a threshold number, which should be determined numerically by trial and error. For example, might probably be linked with the transaction cost. Let be the number defined in (6.2).

-

1.

If then it is recommended to buy the option at the current trading day and sell it on the next trading

-

2.

If then it is recommended to go short at the current trading day , and to follow by closing the short position at the trading day .

-

3.

If then it is recommended to refrain from trading.

We believe that our results support the following two hypotheses:

Hyphothesis 1: The reason why the heuristic algorithm of [10] and section 3 performs well is that it likely forecasts in many cases the signs of the differences for the next trading day ahead of the current one.

Hyphothesis 2: Since the maximal value of in the bold faced curve of Figure 3 is 0.515, which is rather close to the value of 0.5577 in the “Precision” column of Table 1 and in the second column of Table 2, then we probably had in those tested real market data about 56% of options, in which

7 Concluding Remarks

We have considered a mathematical model, in which two markets are in place: the stock market and the options market. We have assumed that the market is imperfect. More precisely, we have assumed that agents of the option market have their own idea about the volatility of the option, and this idea might be different from the volatility of the stock. We have proven that if that , then there is an opportunity for a winning strategy. A rigorous probabilistic analysis was carried out. This analysis has shown that the mathematical expectation of the correctly guessed option price movements can be obtained, and it depends on the difference between and .

We have considered both ideal and non-ideal cases. In the ideal case, both volatilities and are known. In the more realistic non-ideal case, however, only the volatility of the option is known from the market data, see, e.g. [3]. We have demonstrated in our numerical simulations that the accuracy of our prediction of profitable cases by the algorithm of [10] for the non-ideal case is comparable with that accuracy for the ideal case.

These results led us to two hypotheses. The first hypothesis is that our algorithm of [10] actually forecasts in many cases the signs of the differences for the next trading day ahead of the current one. Our second hypothesis is based on our above results as well as on the “Precision” column in Table 1 and the second column in Table 2. This second hyphothesis tells one that probably about 56% out of tested 23,549 options of [13] with the real market data had

A new convergence analysis of our algorithm was carried out. To do this, the technique of [11] was modified and simplified for our specific case of the 1-D parabolic equation with the reversed time. We have lifted here the assumption of [10] that the time interval is sufficiently small. Indeed, even though we actually work with a small number in our computations, that assumption might require even smaller values. In addition, we have derived a stability estimate for Problem 3 of subsection 4.1, which was not done in [10].

Acknowledgment

The work of A.A. Shananin was supported by the Russian Foundation for Basic Research, grant number 20-57-53002.

References

- [1] T. Bjork, Arbitrage Theory in Continuous Time, Oxford University Press, 1999.

- [2] F. Black and M. Scholes, The pricing of options and corporate liabilities, J. of Political Economy, 81, 637-654, 1973.

- [3] https://bloomberg.com.

- [4] L. Bourgeois, Convergence rates for the quasi-reversibility method to solve the Cauchy problem for Laplace’s equation, Inverse Problems, 22, 413–430, 2006.

- [5] L. Bourgeois and J. Darde, A duality-based method of quasi-reversibility to solve the Cauchy problem in the presence of noisy data, Inverse Problems, 26, 095016, 2010.

- [6] J.C. Cox, S.A. Ross and M. Rubinstein, Option pricing: a simplified approach, J. of Financial Economy, 7, 229-263, 1979.

- [7] E. F. Fama and K. R. French, The capital asset pricing model: theory and evidence, J. of Economic Perspectives, 18, No. 3, 25-46, Summer, 2004.

- [8] R. A. Irizarry, Introduction to Data Science: Data Analysis and Prediction Algorithms with R, Chapman & Hall/CRC Data Science Series, Taylor & Francis Group, 2020.

- [9] M.V. Klibanov, Carleman estimates for the regularization of ill-posed Cauchy problems, Appl. Numer. Math., 94, 46-74, 2015.

- [10] M.V. Klibanov, A.V. Kuzhuget and K.V. Golubnichiy, An ill-posed problem for the Black-Scholes equation for a profitable forecast of prices of stock options on real market data, Inverse Problems, 32, 015010, 2016.

- [11] M. V. Klibanov and A. G. Yagola,Convergent numerical methods for parabolic equations with reversed time via a new Carleman estimate, Inverse Problems, 35, 115012, 2019.

- [12] M. V. Klibanov and J. Li, Inverse Problems and Carleman Estimates: Global Uniqueness, Global Convergence and Experimental Data, De Gruyter, 2021.

- [13] M. V. Klibanov, K. V. Golubnichiy and A. V. Nikitin, Application of neural network machine learning to solution of Black-Scholes equation, arXiv: 2111.06642, 2021.

- [14] L. Koralov and Y.G. Sinai, Theory of Probability and Random Processes, Springer, 2007.

- [15] O.A. Ladyzhenskaya, V.A. Solonnikov and N.N. Uralceva, Linear and Quasilinear Equations of Parabolic Type, AMS, Providence, R.I., 1968.

- [16] R. Lattes and J.-L. Lions, The Method of Quasireversibility: Applications to Partial Differential Equations, Elsevier, New York, 1969.

- [17] M.M. Lavrentiev, V.G. Romanov and S.P. Shishatskii, Ill-Posed Problems of Mathematical Physics and Analysis, Providence, RI: American Mathematical Society, 1986.

- [18] R. Merton, Theory of rational option pricing, Bell J. of Economics and Management Science, 4, 141-183, 1973.

- [19] B. Oksendal, Stochastic Differential Equations, Springer, 2000.

- [20] https://money.cnn.com/data/markets/russell.

- [21] A. N. Shiryaev, Essentials of Stochastic Finance: Facts, Models, Theory, World Scientific Publishing, 1999.

- [22] S. E. Shreve, Stochastic Calculus for Finance II. Continuous - Time Models, Springer, 2003.

- [23] A. N. Tikhonov, A. V. Goncharsky, V. V. Stepanov and A. G. Yagola, Numerical Methods for the Solution of Ill-Posed Problems, Kluwer Academic Publishers Group, Dordrecht, 1995.

- [24] P. Wilmott, S. Howison and J. Dewyne, The Mathematics of Financial Derivatives, University Press, New York, 1997.