Asymptotics of cointegration tests for high-dimensional VAR()

Abstract.

The paper studies nonstationary high-dimensional vector autoregressions of order , VAR(). Additional deterministic terms such as trend or seasonality are allowed. The number of time periods, , and the number of coordinates, , are assumed to be large and of the same order. Under this regime the first-order asymptotics of the Johansen likelihood ratio (LR), Pillai–Bartlett, and Hotelling–Lawley tests for cointegration are derived: the test statistics converge to nonrandom integrals. For more refined analysis, the paper proposes and analyzes a modification of the Johansen test. The new test for the absence of cointegration converges to the partial sum of the Airy1 point process. Supporting Monte Carlo simulations indicate that the same behavior persists universally in many situations beyond those considered in our theorems.

The paper presents empirical implementations of the approach for the analysis of SP stocks and of cryptocurrencies. The latter example has a strong presence of multiple cointegrating relationships, while the results for the former are consistent with the null of no cointegration.

1. Introduction

Starting with the pioneering work of Sims (1980), vector autoregressions (VARs) became a workhorse model in macroeconomics and other fields. Many key time series in macroeconomics and finance (e.g., consumption and output) are nonstationary, and the properties of VARs can be very different depending on whether one is dealing with a stationary or nonstationary series. Moreover, there is a further subdivision to be accounted for in the case of nonstationary series: it is important to understand whether the data are cointegrated—that is, whether there exists a stationary nontrivial linear combination within the considered series (e.g., the log of consumption minus the log of output is stationary while the series themselves have unit roots).

Classical tools for testing cointegration (see, e.g., Johansen (1995), Maddala and Kim (1998), and Juselius (2006)) fail to achieve the desired finite sample performance when the number of time series, , is large. Thus, they are not commonly used in such settings, and the design of proper tools to handle cointegration under a large remained an open problem for years (see, e.g., Choi (2015, Sections 2.3.3, 2.4)). Recently Onatski and Wang (2018, 2019) and Bykhovskaya and Gorin (2022) have opened a new avenue based on the “ converging to a constant” asymptotic regime. However, the testing procedures of these texts cover only VAR(), while, in practice, researchers rarely confine themselves to VARs of order , instead usually considering at least two lags. Indeed, as noted already in Pagan (1987), “most applications of Sims’ methodology have put the number of lags between four and ten.” Since Pagan (1987) the lengths of available time series and computing power have only increased, thus allowing researchers to work with even more complex models. Hence, it is important to generalize and extend the above papers to a VAR() setting, which is the main topic of our text.

Our paper analyses a family of tests for the absence of cointegration for nonstationary VAR(), such as the Johansen likelihood ratio (LR) test (Johansen (1988, 1991)) and related Hotelling–Lawley and Pillai–Bartlett tests (see, e.g., Gonzalo and Pitarakis (1995) and references therein) as and jointly and proportionally go to infinity. The shared feature of these tests is that their statistics are based on the squared sample canonical correlations between certain transformations of current changes and past levels of the data. The main contribution of our paper is in the asymptotic analysis of these canonical correlations. First, we show that for VAR() with general , under the null of no cointegration (and some additional technical conditions) the empirical distribution of the squared sample canonical correlations converges to the Wachter distribution. As a corollary, we deduce the first-order deterministic limits of the above test statistics. Second, we introduce a modification of the testing procedure and prove much more refined results in the modified setting. By computing the exact asymptotic behavior of the probability distributions of individual canonical correlations after proper recentering and rescaling, we are able to compute the critical values for the test of no cointegration with correct asymptotic size as and jointly and proportionally go to infinity.

We remark that there is a wide scope of literature devoted to the corrections of Johansen’s LR test and its relatives (originally developed based on fixed , large asymptotics) for large values of (see, e.g., Reinsel and Ahn (1992), Johansen (2002), Swensen (2006), Cavaliere et al. (2012), and Onatski and Wang (2019)). The distinguishing feature of our work is that we are not trying to correct the finite asymptotic statements, which stop working for large , by introducing various empirical adjustments. Instead, we develop a theoretical framework for working with the large case directly. One advantage is that our approach explains the general phenomenology and predicts the asymptotic behavior. As a result, the empirical or simulational adjustments for particular values of the parameters of the model are no longer needed.

To achieve the above, in our proofs we use the VAR() results of Bykhovskaya and Gorin (2022) as a cornerstone. The main technical work is devoted to producing recursive arguments, which reduce the VAR( behavior to that of VAR() and eventually to VAR(). The central role is played by highly nontrivial projections from the group of orthogonal matrices to the smaller subgroup of orthogonal matrices. While such projections have previously been used in asymptotic representation theory, to the authors’ knowledge, this is their first appearance in the econometrics or statistics context. Thus, many new properties of those projections need to be developed in our framework.

The rest of the paper is organized as follows. Section 2 describes our setting and provides the first asymptotic results. Section 3 constructs our modified test and computes its asymptotics, while Section 4 presents supporting Monte Carlo simulations. Section 5 illustrates our theoretical findings on S&P100 data and on the prices of cryptocurrencies. Finally, Section 6 concludes. All proofs are in Sections 7.1–7.4. The accompanying R package is available at the Github https://github.com/eszter-kiss/Largevars.

2. First-order asymptotics of sample canonical correlations

We consider an -dimensional vector autoregressive process of order , VAR(), based on a sequence of i.i.d. mean zero Gaussian111We expect that all our results continue to hold for non-normally distributed errors as long as they have enough moments (cf. such distribution-independence results in other high-dimensional models, as in Erdos and Yau (2012), Tao and Vu (2012), Han et al. (2018), and Yang (2022a)). errors with nondegenerate covariance matrix . That is, written in the error correction form,

| (1) |

where , is a -dimensional vector of deterministic terms, such as a constant, a trend or seasonality (extra explanatory variables are also allowed as long as they are observed), and are unknown parameters. The process is initialized at fixed . We do not impose any restrictions on ; thus, we allow for arbitrary correlations across coordinates of . In contrast, many previous approaches rely on specific properties of the covariance matrix ; see, e.g., Breitung and Pesaran (2008), Bai and Ng (2008, Section 7) and Zhang et al. (2018).

Remark 1.

Alternatively, the error correction form can be written as

so that . Whether we use the former (Eq. (1)) or the latter form does not affect our results. The testing procedures of our interest are based on the residuals from regressing on , which are the same as the residuals from regressing on .

We are interested in the behavior of the squared sample canonical correlations between transformed past levels (lags) and changes (first differences) of the data . As shown in (Johansen, 1988, 1991) (see also Anderson (1951)), the correlations are related to whether the process is cointegrated. To be more specific, they appear in the likelihood ratio test for the presence and rank of the cointegration. Let us formally define these correlations. Here and below ∗ denotes matrix transposition.

Procedure 1 (Johansen (1991)).

Let , , and . We regress lags and changes on regressors (lagged changes and deterministic terms) and define the residuals

| (2) |

Define further matrices and finally set

The eigenvalues of are squared sample canonical correlations of and , where is matrix composed of columns .

Johansen’s LR statistic for testing the hypothesis (at most cointegrating relationships) versus the alternative (between and cointegrating relationships) with has the form222We omit a usual scaling factor of for the statistics (3), (4), and (5).

| (3) |

the Pillai–Bartlett statistic is

| (4) |

and Hotelling–Lawley statistic is

| (5) |

See Gonzalo and Pitarakis (1995) for a discussion and many references about these statistics.

In Theorem 3 we show that the empirical measure of eigenvalues of converges (weakly in probability) to the Wachter distribution. The theorem generalizes the results of Onatski and Wang (2018) from the VAR() to the VAR() setting.333While Onatski and Wang (2018, Theorem 1) allows the data to be VAR() under restriction (9), they construct the matrix involved in the statistical testing procedures as if the data were VAR(). That is, the formal procedure is based on a misspecified VAR() setting, while we use the true VAR() procedure. As illustrated in Section 4.3, using an underspecified VAR can lead to severe size distortions.

Definition 2.

The Wachter distribution is a probability distribution on that depends on two parameters and and has density

| (6) |

where the support of the measure is defined via

| (7) |

Theorem 3.

Let follow Eq. (1). Suppose that is fixed and, as ,

| (8) |

| (9) |

Then, for each continuous function on , we have

| (10) |

Equivalently, the empirical measure of eigenvalues of converges (weakly in probability) to the Wachter distribution of density .

Imposing assumption (9) can be viewed as a dimension reduction (cf. sparsity assumption). Approximating data with low-rank matrices is a widely used and powerful technique in data science, in machine learning applications such as recommender systems (e.g., movie preference recognition), and in computational mathematics. We refer the reader to Udell and Townsend (2019) for theoretical explanations of the suitability of low-rank models and many references to situations in which they are very efficient. In our particular context, the number of unknown parameters in the VAR model (1) is proportional to , and we have access to observations. Since and are of the same order in the asymptotic regime (8), the model (1) can overfit the data. We view the rank restriction (9) as a natural way to avoid overfitting444An alternative way to introduce a low-rank assumption into the VAR model is, instead of using the error correction form in (1), to rewrite the evolution as . Then, in the spirit of factor models, one can impose the low-rank assumption on . Notice that for , so that low-rank assumptions on higher-order lags in this and our setting are related. This alternative low-rank restriction complements ours via the rank of : in our setting, the number of cointegrating relationships grows sublinearly in , while in the alternative setting, this number is close to . While none of our theorems directly cover the factor setting, numeric simulations in Section 4.5 indicate that the tests that we develop remain useful. (cf. the discussion in Wang et al. (2022) and Wang and Tsay (2022)). Section 5 illustrates that the results obtained under this assumption are consistent with the behavior of large-dimensional financial datasets. Another setting in which we can expect (9) to be satisfied is when there are a few special coordinates in , e.g., some macroeconomic indicators, that mostly drive the behavior of the entire vector . This would correspond to the case where the columns of corresponding to those indicators are nonzero while the other columns are zero.

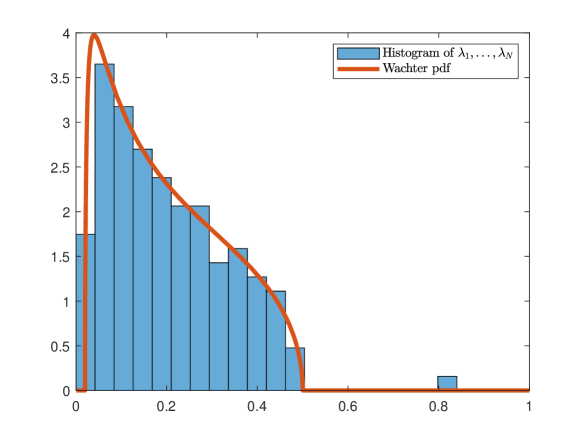

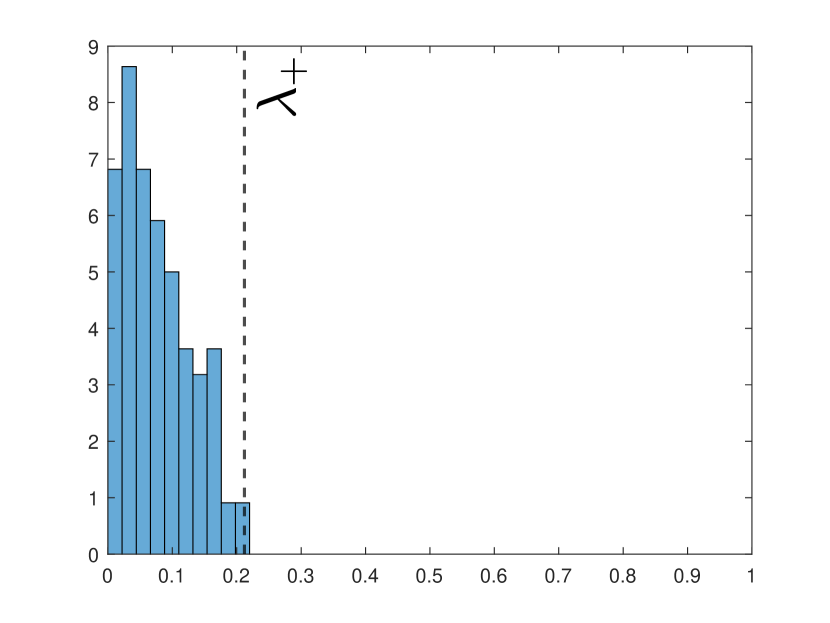

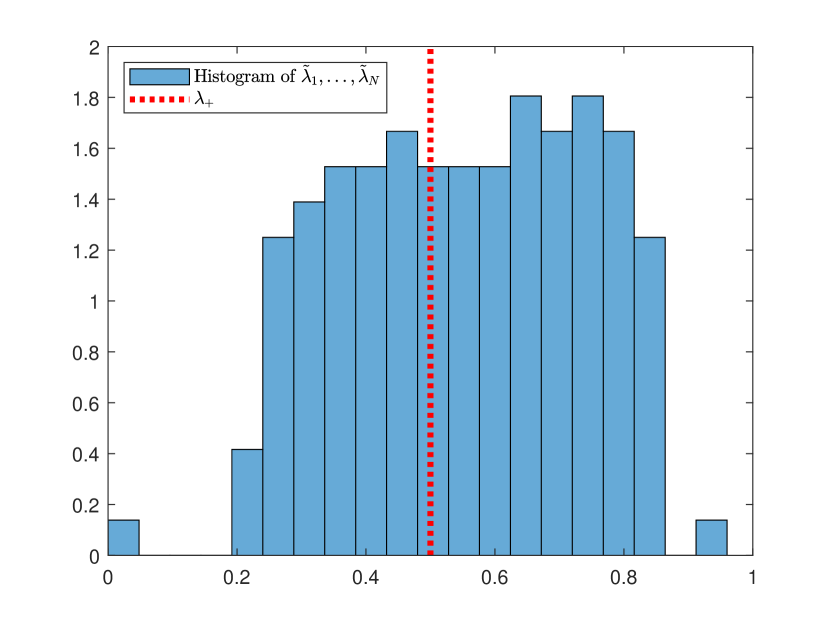

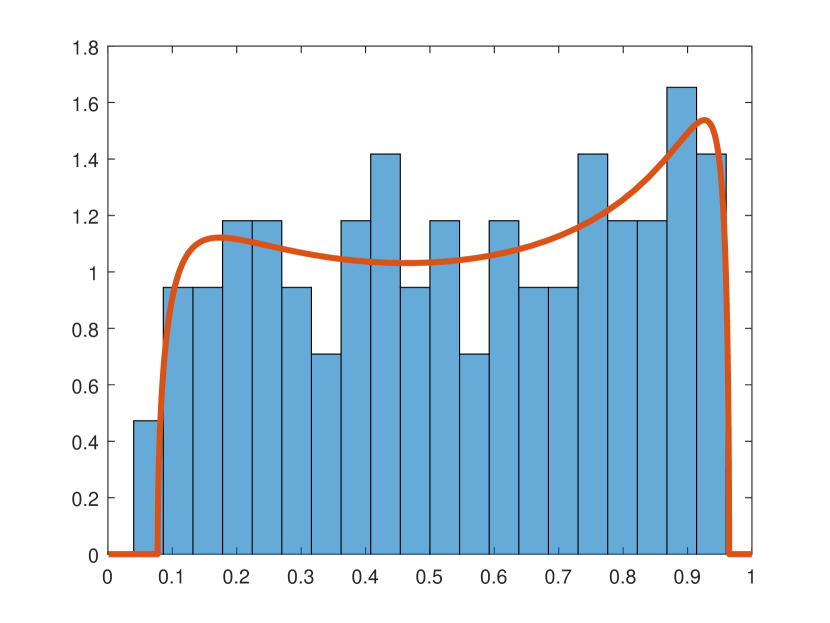

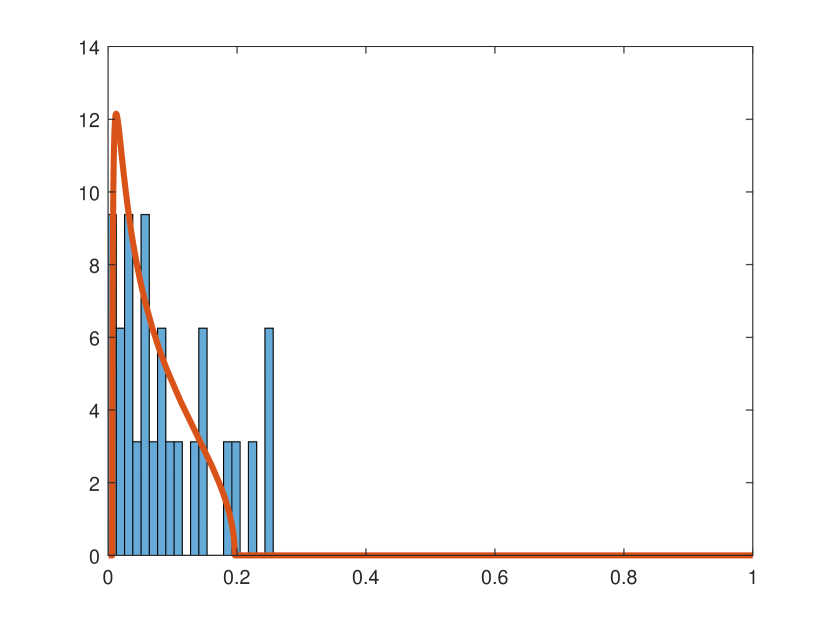

Figure 1 illustrates Theorem 3 for independent standard normal errors and . The parameters are , , , where is an -column matrix of ones, is an matrix with one at the intersection of the 1st row and the 2nd column and zeros everywhere else, and is an matrix with ones in the first column and zeros everywhere else. Thus, all the matrices have rank one. The parameters of the Wachter distribution are . The single separated (rightmost) eigenvalue corresponds to , i.e., one cointegrating relationship. Generally, we expect that if there are separated eigenvalues and the value of in Procedure 1 is correctly specified, then there are at least cointegrating relationships.

The proof of Theorem 3 is based on treating the setting of (1) as a small-rank perturbation of a more restrictive setting analyzed in Section 3. The small-rank assumption in (9) is crucial for the validity of the theorem, and we expect that the asymptotic behavior changes in situations when (9) fails. This expectation is supported by the Monte Carlo experiment in Section 4.4. In contrast, the assumption that can potentially be relaxed. When , the matrix has deterministic eigenvalues equal to , which should be taken into account in asymptotics. This case can be also addressed by our methods, but we do not continue in this direction.

An important corollary of Theorem 3 is that it provides the asymptotic behavior of various tests constructed from eigenvalues of .

Corollary 4.

Under the assumptions of Theorem 3, suppose that the ranks and are such that

Let . Then we have convergence in probability for the test statistics:

and asymptotic inequalities: for each ,

Note that, when , for the Johansen LR and Hotelling–Lawley (HW) statistics, we obtain inequalities rather than equalities. This is because of the singularity of and at : while Eq. (10) controls average behavior, it does not control individual eigenvalues. Hence, the largest eigenvalue can be arbitrarily close to , so that the LR and HW statistics reach large negative and positive values, respectively. However, for similar statistics in the modified setting of the next section the inequalities turn into equalities (as can be proven by combining Theorem 4 and Proposition 1).

For commonly used tests, one often takes (i.e., ), in which case . We also remark that the integrals in Corollary 4 can be explicitly computed in many situations. For instance, the one appearing in the asymptotic of the Pillai–Bartlett statistic for , is

There are several applications of Theorem 3 and Corollary 4:

-

•

They can be used for validation of the applicability of model (1) to a given dataset. Namely, if a VAR() model with low-rank matrices and agrees with data, then irrespective of the true values of these parameters, we expect to see the Wachter distribution in the histogram of , . In Section 5 we perform such a validation on SP and cryptocurrency data sets for VAR() with and observe a remarkable match. (VAR() for SP is also reported in (Bykhovskaya and Gorin, 2022, Figure 7).)

-

•

They can be used as a screening device for preliminary conclusions about the rank of : If the rank is finite, then for any and we should be in the -neighborhood of the limits in Corollary 4.

-

•

As explained in Onatski and Wang (2018), such results can be used to explain overrejection in some of the widely used tests for the rank of .

To draw further economical and statistical conclusions and to develop precise statistical tests and their critical values, one needs to go beyond the first-order asymptotic results of Theorem 3 and Corollary 4. In the next section we introduce relevant modifications and develop appropriate second-order asymptotics.

3. Cointegration test: Second-order asymptotics

In the regime of and growing simultaneously and proportionally, the first-order asymptotics of tests based on the squared sample canonical correlations are given in Corollary 4. To perform testing and be able to reject at a given significance level, we need to be more precise and find a centered limit, which would be a random variable rather than a constant. To do this, we need to impose additional conditions on , , and in Eq. (1). Let us first describe the modified procedure and then state the asymptotic results.

3.1. Test

We restrict our attention to the case , i.e.,

| (11) |

The null hypothesis of no cointegration is or . The complement to is . However, to design our test we use an alternative hypothesis:

As in Bykhovskaya and Gorin (2022), our test is based on a modification of the Johansen LR test. The Johansen LR test for the original (i.e., ) versus is

| (12) |

where are defined in Procedure 1. Let us describe how our modified test proceeds.

Procedure 2.

Step 1. De-trend the data and define

| (13) |

Note that we do a time shift in line with the notation in Bykhovskaya and Gorin (2022).

Step 2. Define regressors and dependent variables: For any , set

Define

The main difference between and from Procedure 1 is the usage of cyclic indices: values at are replaced by values at .

Step 3. Calculate the residuals from regressions on and on :

| (14) |

Step 4. Calculate the squared sample canonical correlations between and , where is an matrix composed of columns . That is, define

| (15) |

| (16) |

Then, calculate eigenvalues of the matrix . The eigenvalues solve the equation

| (17) |

Step 5. Form the test statistic

| (18) |

The subscript in (18) indicates that we modify the Johansen LR test to develop the large asymptotics. This statistic after centering and rescaling will be compared with appropriate critical values to decide whether one can reject (see Theorem 5). Visually, rejections correspond to the case when the largest eigenvalues are separated from the rest (as in Figure 1).

An alternative way to write residuals is via an orthogonal projector: Let be a linear subspace of dimension in -dimensional vector space, spanned by vector and all rows of matrices , , where is a cyclic version of the conventional lag operator and is its th power, that is, the cyclic lag applied times. The cyclic lag operator maps a vector to . Let denote the projector on orthogonal complement to . Then,

| (19) |

3.2. Second-order asymptotics

In this section we show that, under additional restrictions, the eigenvalues are very close (up to for arbitrary ) to a known random matrix distribution. From this result we deduce our main theorem (Theorem 5), which gives the large limit of the test statistic in Eq. (18). Before we formally state the results, let us define the relevant random matrix distributions.

3.2.1. Definitions

Definition 1.

The (real) Jacobi ensemble is a distribution on real symmetric matrices of density proportional to

| (20) |

with respect to the Lebesgue measure, where are two parameters, is the identity matrix, and means that both and are positive definite.

The Jacobi ensemble is a generalization of the Beta distribution to the space of square matrices (when , we obtain the Beta distribution). It plays a prominent role in statistics; e.g., it appears in canonical correlation analysis for independent data sets and in multivariate analysis of variance (see, e.g., Muirhead (2009)).

Definition 2.

The Airy1 point process is a random infinite sequence of reals

that can be defined through the following proposition.

The marginals of the Airy1 point process can be calculated via various methods (see, e.g., Forrester (2010) for more details).

3.2.2. Theorems

The null for (11) is not a point hypothesis, as it does not specify . A simplifying procedure when we are faced with such a composite space of the maintained hypothesis is to assume some fixed values of the parameters as a proxy for the null hypothesis. Along these lines, for the next theorems we are going to introduce additional restrictions and specify the values of . Thus, our model is going to be fully specified (up to a constant , which will disappear in the testing procedure). We proceed to implement this approach in testing the hypothesis of no cointegration and introduce the restricted 555We discuss the consequences of using for testing the null after Theorem 5.:

| (22) |

In other words, under the data generating process turns into

| (23) |

where is an (unknown) -dimensional vector.

Theorem 4.

Fix , and suppose that in such a way that . For the data generating process (11) with restrictions given by (22), one can couple (i.e., define on the same probability space) the eigenvalues of the matrix and eigenvalues of the Jacobi ensemble in such a way that, for each , we have666One can show that the probability in (24) is exponentially close to : there exists a constant , which depends on , , and , such that, for all and satisfying , the probability under the limit in Eq. (24) is larger than . Analyzing the proof of Theorem 4, we can obtain this inequality by combining (66) with large deviations bounds for the smallest and largest eigenvalues of the Jacobi ensemble (see e.g., Anderson et al. (2010, Section 2.6.2) for the latter).

| (24) |

The proof of Theorem 4 relies on two steps. First, we modify our matrix a bit, which leads to a surprising appearance of the Jacobi ensemble, as shown in Section 7.2. Second, in Section 7.3 we show that the distance between the original model and the modified one becomes small as .

Combining Theorem 4 with known asymptotic results for the Jacobi ensemble, which we recall in Proposition 1 in Section 7.1, we derive the asymptotics of (18) in the following theorem.

Theorem 5.

Remark 6.

The condition is another way to require that and grow to infinity proportionally. For example, it is guaranteed by the joint limit (8). The role of is only to make sure that does not get too close to (if approaches , then approaches and explodes) or (if becomes large, then and tend to at the same speed and vanishes).

Theorem 5 gives us the basis of cointegration testing in the large setting. Treating as a proxy for , we can use our asymptotic results to test high-dimensional VARs for the presence of cointegration. Formally, to perform testing, one first needs to calculate the statistic following Procedure 2. We recommend using small777In Theorem 5 is kept fixed as and grow. The role of this choice and the motivations for sticking to it are discussed in detail in (Bykhovskaya and Gorin, 2022, Section 3.2). values of , such as , or . Then, one needs to calculate , as in Theorem 5, and compare the result with quantiles of the sum of Airy1, . If the rescaled statistic is larger than the quantile, we reject the null of no cointegration at the level. We report the quantiles for in Table 1. See also Bykhovskaya et al. (2023) for more detailed tables for .

| 1 | 0.44 | 0.97 | 1.45 | 2.01 |

|---|---|---|---|---|

| 2 | -1.88 | -1.09 | -0.40 | 0.41 |

| 3 | -5.91 | -4.91 | -4.03 | -2.99 |

Note that, although the asymptotic result (25) is shown under the restrictions , we believe that it extends well beyond : the same asymptotic results and testing procedures continue to hold in many situations with nonzero in Eq. (11). While we do not have a full rigorous proof, we expect the following to be true:

For the data generating process (11), assume that the ranks of all are bounded, as are the norms of all the matrices and vectors involved in the specification of the process (see Section 8 for more details). Then conclusion (25) of Theorem 5 should continue to hold.

We collect extensive evidence supporting this statement. In Section 4 we report results from Monte Carlo simulations consistent with it. Further, in Section 8.1 we present a precise mathematical conjecture in this direction and give a heuristic argument for its validity. The intuition is that generic small-rank matrices are negligible relative to the scale of the rest of the process and, thus, their addition does not change the asymptotics. For this intuition to hold, it is important to correctly specify the parameter in the procedure to be equal to (or greater than) its true value. Otherwise (i.e., if we do not regress on the relevant in the procedure), the presence of can have an effect similar to that of the presence of nonzero : it leads to the appearance of special highly correlated linear combinations of rows of and , which changes the behavior of the largest canonical correlations ; see also the simulations in Section 4.3.

Theorem 5 means that under the largest eigenvalues are close to , which is the right point of the support of the Wachter distribution in Eq. (6). The relevance of this theorem for cointegration testing stems from the fact that we expect some of the eigenvalues to be much larger than when cointegrating relationships are present. As an illustration, see Figure 1, where of rank leads to the largest eigenvalue being to the right of and separated from the other eigenvalues. The separation is due to the small rank of . However, even if the rank of is large, we expect the largest eigenvalue to be significantly larger than , and, thus, the test remains relevant (see Section 4.5). Providing rigorous results on the consistency of the test is an important task for future research. We present the first result in this direction in Corollary 5 in Section 8.2, where we produce a lower bound on the power of the test against a particular “one cointegrating relationship” alternative and show that the power tends to as tends to infinity.

4. Monte Carlo simulations

4.1. Size

We refer to Bykhovskaya and Gorin (2022, Section 5) for the finite sample size performance of our test for . The results for VAR() are similar, and we do not show them in much detail here. For illustration purposes and to represent the comparative statics, Table 2 reports the empirical size for (those numbers correspond to our empirical example in Section 5.1) for tests based on VAR(), procedures.888Depending on the assumed order of autoregression, we have different numbers of regressors in Procedure 2. We can see that the numbers are close to the desired and, for the same and , a lower order of VAR leads to slightly better results.

| VAR() | VAR() | VAR() | VAR() |

|---|---|---|---|

4.2. vs.

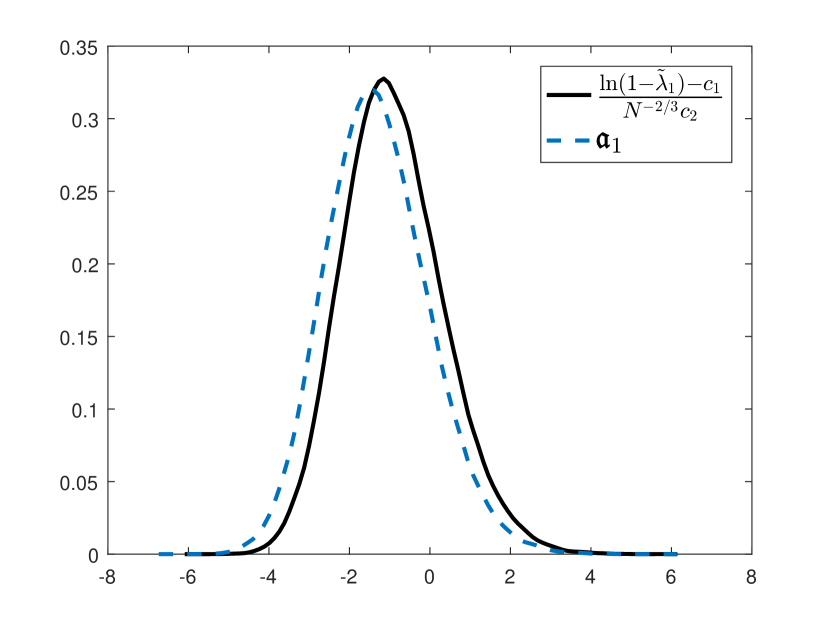

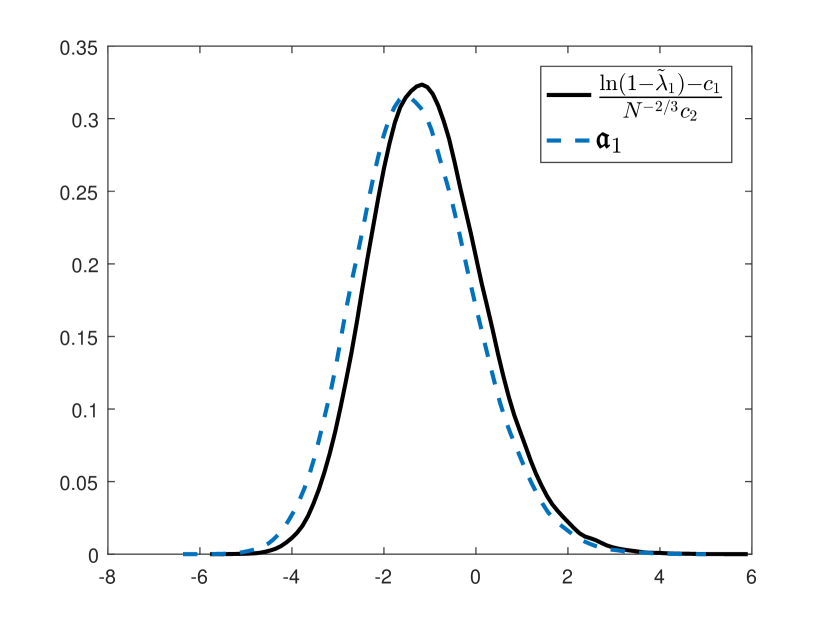

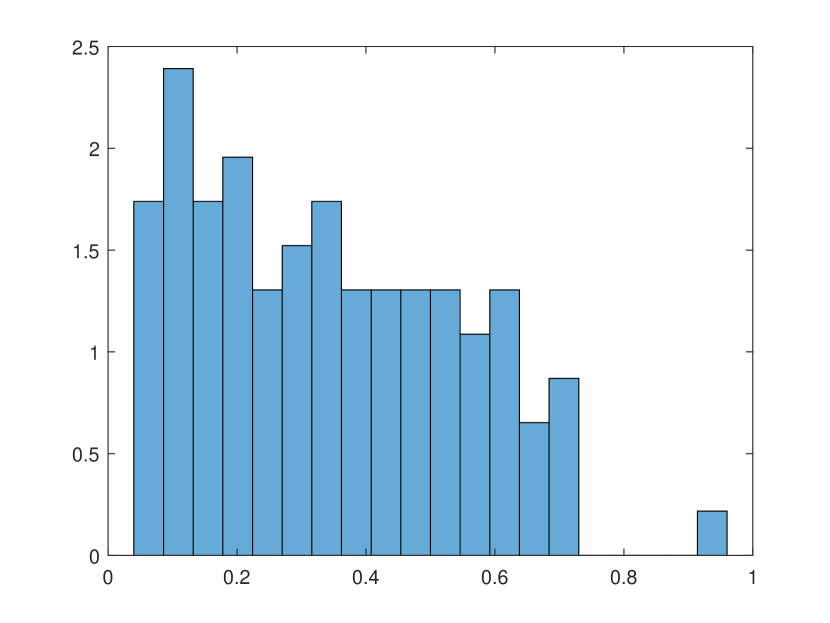

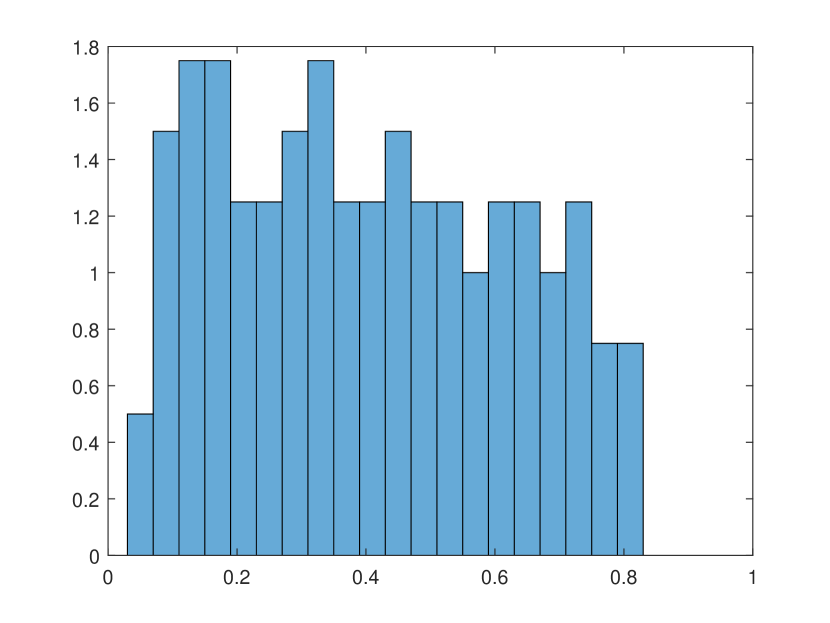

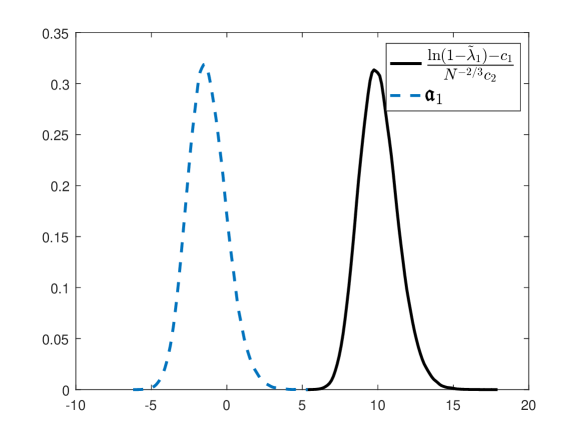

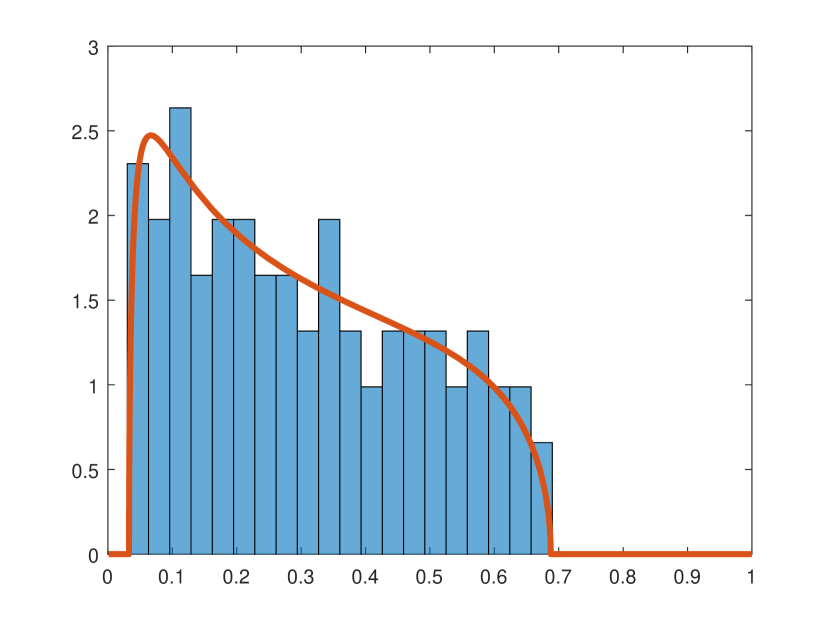

An important aspect of our analysis for is the introduction of the additional restrictions maintained under the null. We would like to check whether Theorem 5 can hold under the less restrictive instead of . Some theoretical results in this direction are provided in Section 8.1. Here we complement them with Monte Carlo simulations. For , we simulate the data based on i.i.d. errors , zero , and nonzero (i.e., this corresponds to but not ). We then compare the density of the test based on the largest eigenvalue ( case of Theorem 5 with statistic ), with the density of the first coordinate of the Airy1 point process, . If the densities coincide, then it means that we can still use the asymptotics from Theorem 5 to test the null of no cointegration.

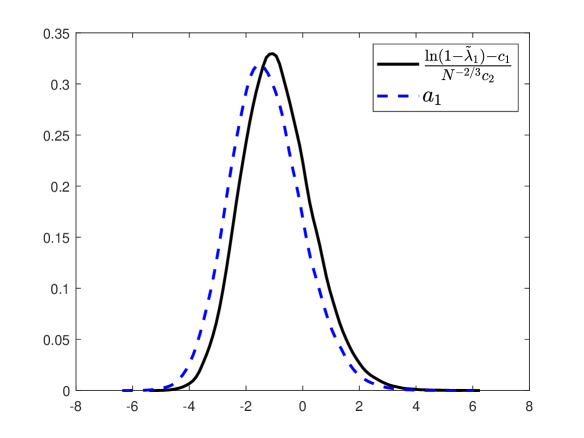

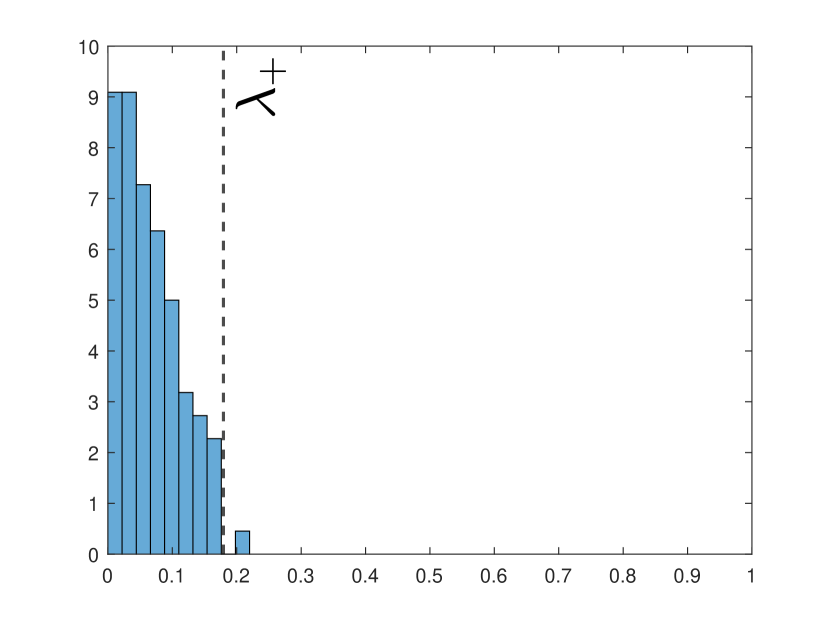

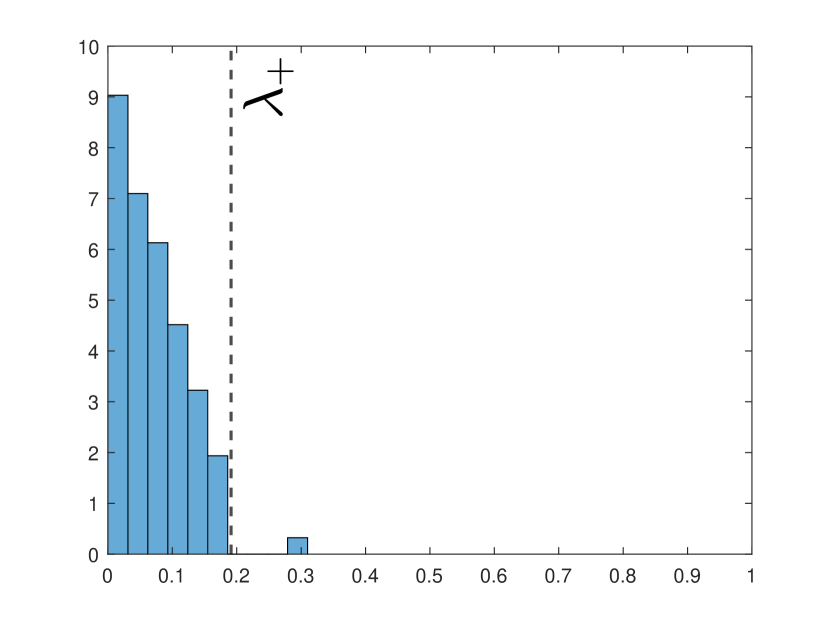

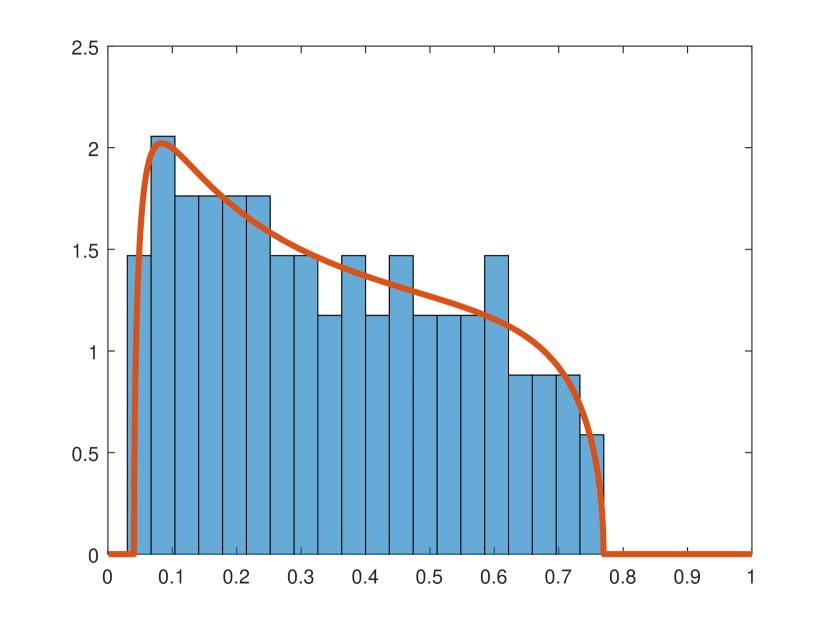

Let be a matrix with at the cell and s everywhere else and let be a matrix with s filling the entire column and s everywhere else. In the first two experiments we take . We set in the first one, which guarantees stationarity of but allows for strong time correlations in the first coordinate via the factor. In this case the rank of is . In the second experiment we consider an asymmetric matrix , which has a close to singular value because of the factor; the rank of is in this case. The results are illustrated in Figure 2. In the third experiment, we take , , and , so that both matrices are of rank . The value guarantees stationarity of , since . The result is shown in Figure 3. We interpret the outcomes of these three experiments as a strong argument toward the validity of an analogue of Theorem 5 well beyond the setting.999The minor mismatches between densities as in Figures 2 and 3 should be expected even under . Theorem 4 (after multiplication of the result by , as in Eq. (25)) predicts errors of at least in the approximations under .

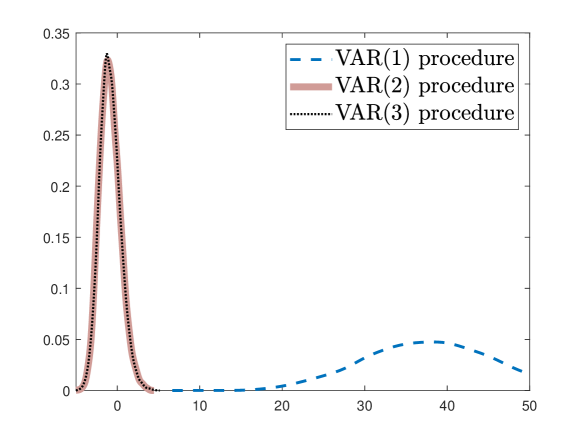

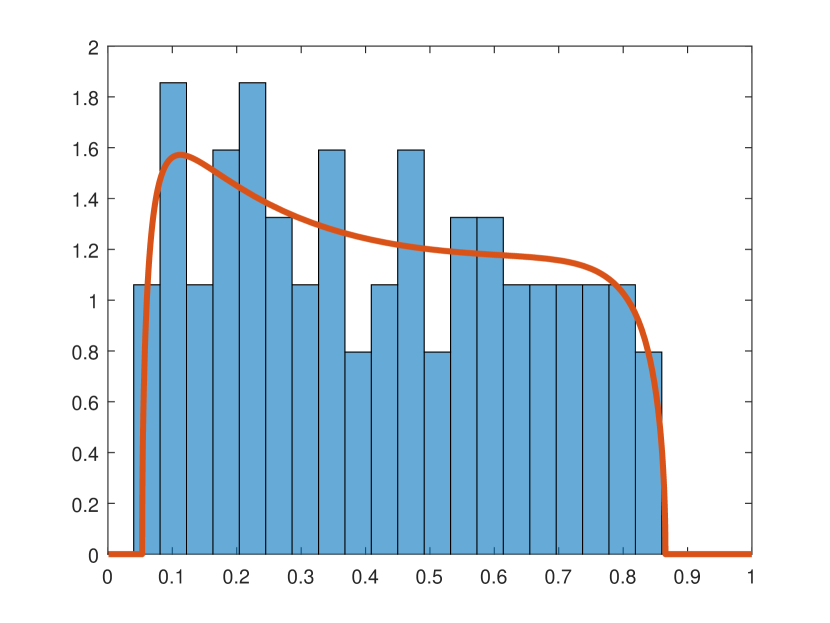

4.3. Order of VAR

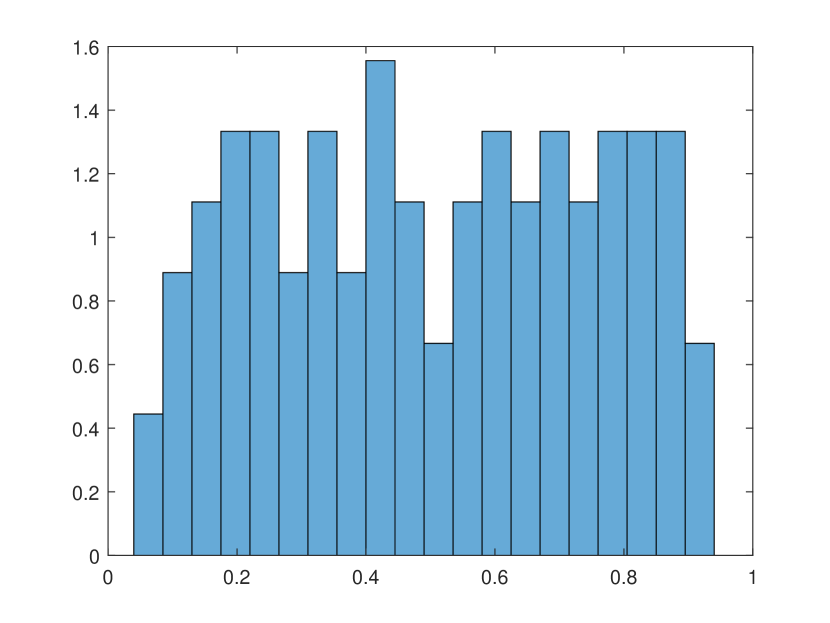

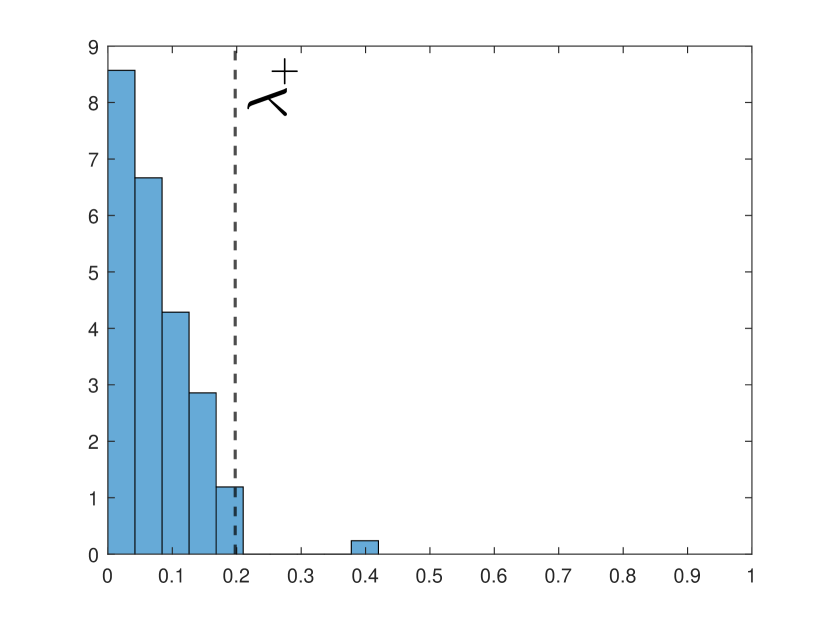

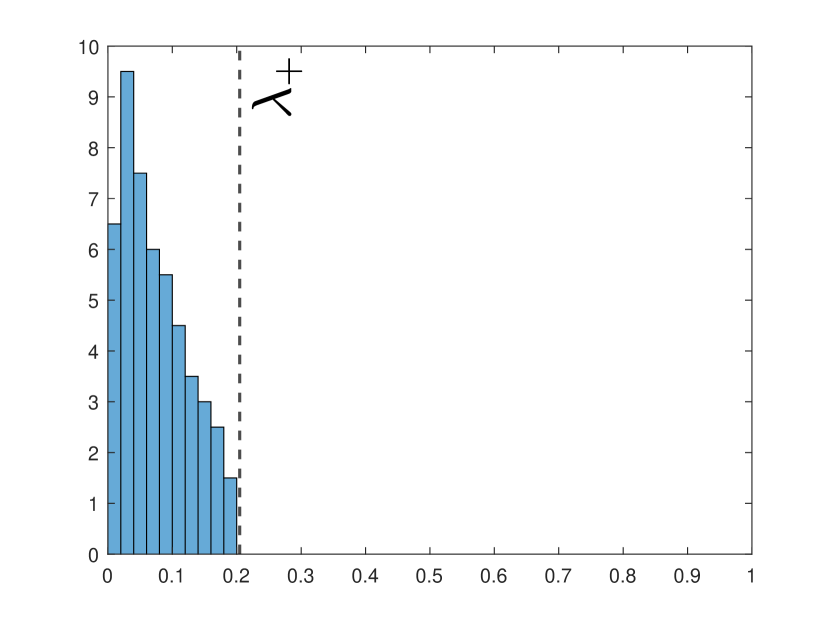

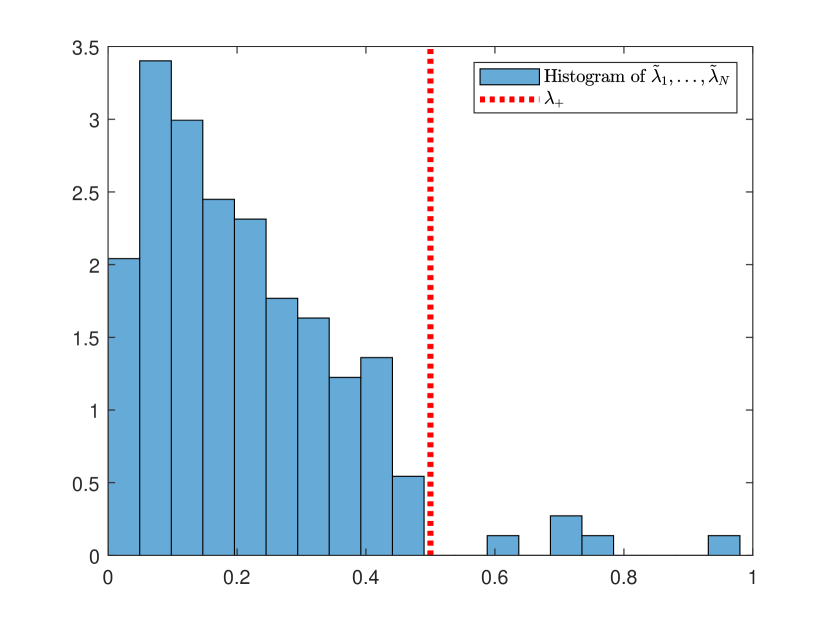

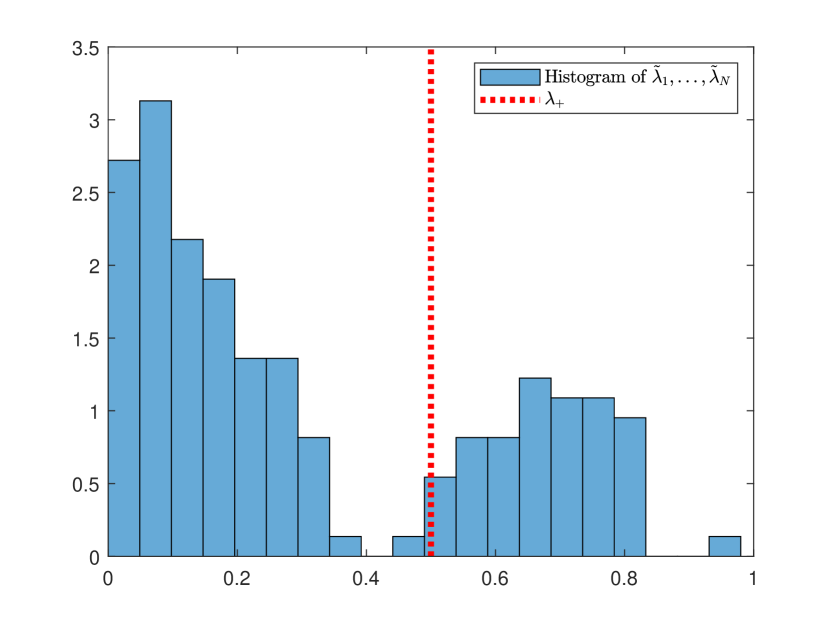

It is essential for the experiments in the last paragraph that the data generating process is VAR(2) and that the procedure we use also corresponds to VAR(2), i.e., in the notations of Sections 2 and 3. As illustrated in Figure 4, using a larger would lead to similar results, while incorrectly using a VAR(1) procedure when the data generating process is VAR(2) would imply wrong centering and scaling. Moreover, one can spot in Figure 5 that underestimation of the order of the VAR can be misinterpreted as a presence of cointegration101010Related simulations for are also reported in (Bykhovskaya and Gorin, 2022, Section 7.3): For small , such as , the VAR(1) procedure still performs well. However, as grows to , the performance quickly deteriorates ( in Figure 4). (largest eigenvalue separated from the rest leading to the large value of the test statistic). However, as we increase the order, the largest eigenvalue becomes inseparable from the rest, and no sign of false cointegration remains present. Thus, practitioners are encouraged to experiment with the order of the VAR to make sure that they are detecting cointegration and not simply using the wrong model.

Note that one should be careful if using classical information criteria for estimating the order of a VAR in our situation. They are known to be unreliable in high-dimensional settings and may underestimate (see, e.g., the simulations in Gonzalo and Pitarakis (2002)). A possible approach to choosing is to look sequentially at histograms of eigenvalues at . If the outlier eigenvalues larger than exist for the procedures with all and perhaps move closer to as grows (corresponding to a decrease in the power of the test), then this is a strong indication of the presence of cointegration. On the other hand, if there is a sharp transition—i.e., outlier eigenvalues are present when we use the VAR() procedure for and abruptly disappear at —then this is an indication that the true model is VAR() without cointegration (see Figure 6).

All of the above reinforces the importance of using the VAR() rather than the VAR() procedure.

4.4. Small ranks

To illustrate the importance of small ranks (e.g., (9) in Theorem 3), we also redo the same procedure for a matrix of full rank and set to be , where is an identity matrix. The result is shown in Figure 7. While the shape and the scale (corresponding to rescaling in Theorem 5) of the distribution remain similar, the location changes. Thus, the small-rank restriction of Eq. (9) is important not only in the context of Theorem 3 but also for correct centering in possible generalizations of Theorem 5.

4.5. Power

Finally, we simulate the process based on to assess the power of our cointegration testing procedure. We refer the reader to Bykhovskaya and Gorin (2022, Section 5.2) for many simulations in the case and do not repeat similar experiments here.

For the first experiment, we use , , and . Figure 8 shows the results of the simulation. Two curves are separated; moreover, the black straight line (test distribution) is flatter than the blue dashed curve (). First, the separation of the curves is in line with the usefulness of Theorem 5 in cointegration hypothesis testing, since the test statistic was designed to distinguish between and . Second, the distinct variances are due to the fact that (as we expect from a comparison with results on spiked random matrices in the literature; see, e.g., Baik et al. (2005)) under the alternative () the test needs to be scaled differently: Instead of rescaling one should use . This result is in line with the power analysis of our test in Section 8.2.

For the second experiment, we use , , , , and , where is a matrix with ones on the first diagonal elements and zeros elsewhere. The histograms of eigenvalues for are shown in Figure 9. As becomes large, we are no longer in the framework of Theorem 3, and the result about the convergence to the Wachter distribution does not apply. Nevertheless, we observe that the largest eigenvalues are significantly larger than of Theorem 5. Recall that our testing procedure is based on comparing the largest eigenvalues111111More precisely, logarithms of 1 minus eigenvalues vs. . with . Thus, this leads to the conclusion that our test is useful for all values of : the test rejects of no cointegration (i.e., the hypothesis) at a very high statistical significance level.

5. Empirical illustrations

5.1. SP

We illustrate our asymptotic theorems on the SP100 data. We use logarithms of weekly prices of assets in the SP100 over ten years (January 1, 2010, to January 1, 2020), which gives us observations across time. More detailed description of the variables can be found in Bykhovskaya and Gorin (2022, Section 6).

For the SP100 data set we use Procedure 2 to calculate . We do this for various choices of . The case (VAR(1)) corresponds to Bykhovskaya and Gorin (2022). The results are shown in Figure 10.

We see a striking match between the histograms and Wachter densities for all , which is an indication that the setting of Theorem 3 is a proper modeling for the SP data. We do not see any outliers in the largest eigenvalues, which would appear if there were cointegration. Indeed, our test statistics based on Theorem 5 are for , respectively, while the and critical values are and . Because the former numbers are smaller than the latter numbers, we do not reject the “no cointegration” hypothesis.

5.2. Cryptocurrencies

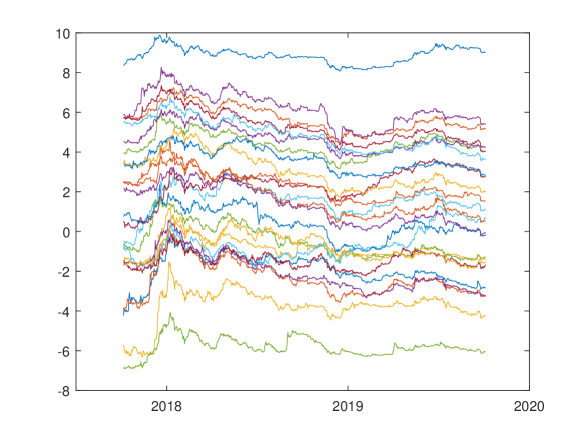

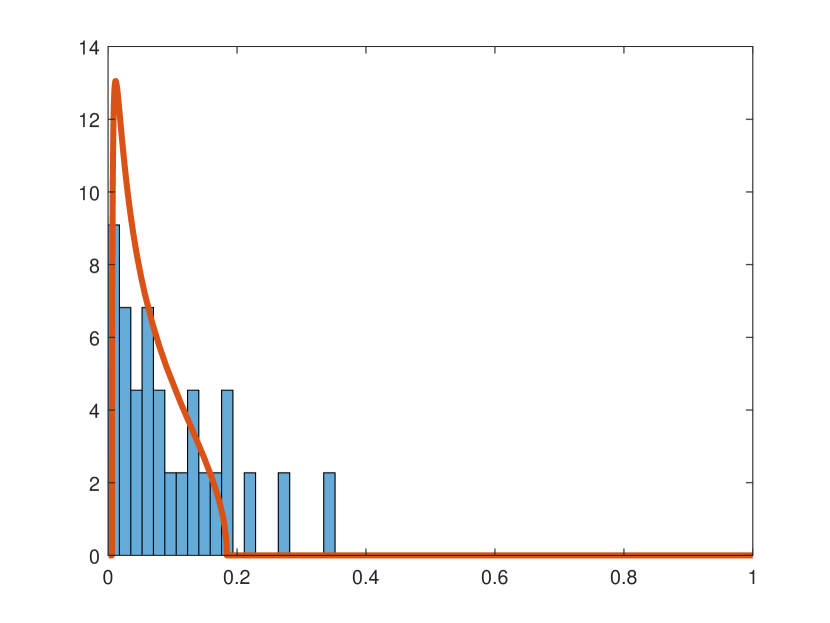

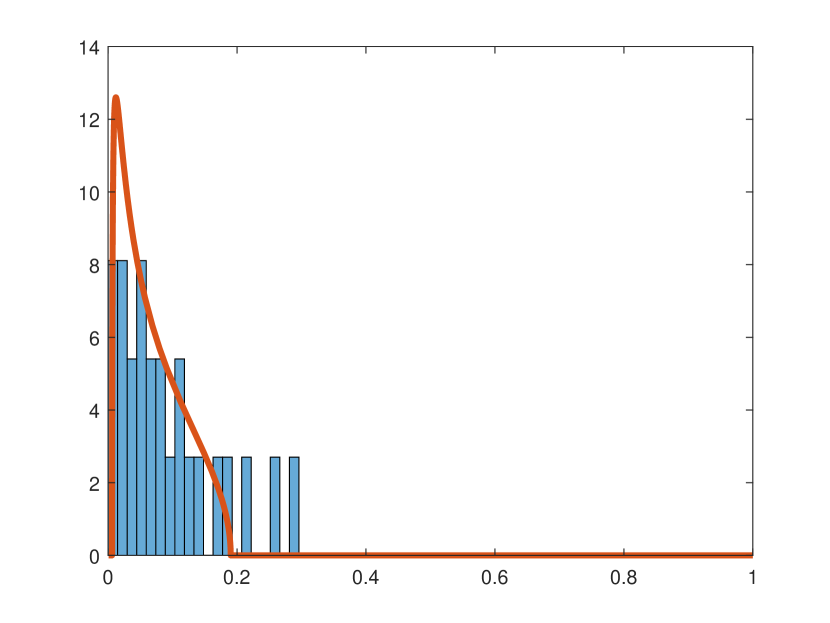

In this subsection we redo the calculations for cryptocurrencies instead of SP stocks. We use the data from Keilbar and Zhang (2021) (25 series from the Github repository). Logarithms of daily prices for two years (from October , , to October , ) are shown in Figure 11. The results of Procedure 2 used to calculate are shown in Figure 12.

Similarly to the SP example in the previous subsection, we see a match between the eigenvalues and the Wachter distribution.121212The Wachter distribution depends on the order of the VAR, , and on the ratio . Thus, the orange curves in Figures 10 and 12 have different shapes and supports. However, there is a major difference between Figures 10 and 12: The latter has around 3 eigenvalues to the right of the support of the orange curve (Wachter distribution). This is an indication of the presence of approximately cointegrating relationships. This is reinforced by our test, which has p-values below for all four choices of the order of VAR() ().

The difference in results for traditional stocks and cryptocurrencies can be explained by the fact that the cryptocurrency market is still very inefficient and, thus, has numerous trading possibilities. The presence of cointegration can be one such inefficiency.

6. Conclusion

High-dimensional data are becoming increasingly widespread in economics and other sciences. Thus, appropriate machinery for handling such data is needed. We believe that the use of random matrix theory is inevitable for the development of the area: As soon as dimensions are high, random matrices start to contribute. Along these lines, in our paper the central role is played by random matrix objects: the Wachter distribution, Airy1 point process, and Jacobi ensemble.

The present paper focused on nonstationary high-dimensional VARs and presented the asymptotic limit of the Johansen LR test for cointegration and its modifications. Because the limit is nonrandom, the appropriate second-order statistic was derived, and a new test for the presence of cointegration was proposed. The new test builds upon the Johansen LR, while having some extra modifications. This new test is suitable for a vector autoregression of order with an intercept.

The main focus of the present paper is the null of no cointegration. The next essential step is to be able to test whether the cointegration rank is for , i.e., to find the true rank of cointegration. Heuristics for finding the correct value of can already be seen in our simulations and data sets (cf. Figures 1, 10, and 12): When there are no cointegrations, all eigenvalues (squared canonical correlations) are to the left of the end-point of the support of the Wachter distribution. In contrast, we expect each cointegrating relationship to lead to an eigenvalue between the right end-point of the support of the Wachter distribution and . Identifying the exact conditions under which this heuristic is correct represents an important problem for future research.

7. Appendix 1: Proofs

First, in Section 7.1 we collect known statements about the asymptotics of the Jacobi ensemble of Definition 1, which will be used in our subsequent proofs.

Second, in Theorem 2 of Section 7.2 we introduce a novel random matrix model for the Jacobi ensemble. Our proof of Theorem 2 proceeds through certain intricate inductive computations of large-dimensional matrix integrals.

Third, in Section 7.3 we connect the matrix model of Section 7.2 to the cointegration setting: for that we use the rotational symmetry of the Gaussian law to express the squared sample canonical correlations solving (17) under the hypothesis in terms of a certain deterministic orthogonal matrix. Replacing this deterministic matrix by a uniformly random one, we arrive at the Jacobi ensemble of Theorem 2. We proceed by bounding the error in this replacement, which relies on the rigidity estimate for orthogonal matrices (66), but needs special care due to various matrix inversions involved in our procedures. Eventually, we arrive at Theorem 4. This theorem is our main technical result. Combining Theorem 4 with Proposition 1 from Section 7.1, we finish the proof of Theorem 5 from the main text.

Finally, in Section 7.4 we prove Theorem 3 by combining Theorem 4 with Proposition 1 of Section 7.1 and general statements about small rank perturbations.

7.1. Asymptotic of Jacobi ensemble

In this section we review the asymptotic results for the Jacobi ensemble introduced in the Definition 1 as .

We assume that as , also , in such a way that

| (28) |

where and are two parameters, which stay bounded away from and from as .131313Johnstone (2008, Theorem 1) suggests to use and instead of and , respectively, in order to improve the speed of convergence. However, we found in Bykhovskaya and Gorin (2022) that for the tests in VAR() case the usefulness of this correction depends on the exact value of the ratio and we are not going to pursue this direction here. We further define the equilibrium measure of the Jacobi ensemble through:

| (29) |

where the support of the measure is defined via

| (30) |

One can check that for every . Further, define

| (31) |

and note that

where the normalization was chosen to match the behavior of the Wigner semicircle law near edges .

Proposition 1 (See Johnstone (2008), Forrester (2010), and Han et al. (2016)).

Suppose that in such a way that and in (28) stay bounded. For the second conclusions we additionally assume that is bounded away from and for the third conclusion we additionally require to be bounded away from . Let be random eigenvalues of Jacobi ensemble . Then

-

(1)

weakly in probability.

This means that for any continuous function we have convergence in probability:

(32) -

(2)

For as in Proposition 3, we have convergence in finite-dimensional distributions for the largest eigenvalues:

(33) In particular, converges to the Tracy-Widom distribution .

-

(3)

We also have convergence in distribution for the smallest eigenvalues141414The limiting processes arising for the largest and smallest eigenvalues are independent.

(34)

7.2. A new model for the Jacobi ensemble

The Jacobi ensemble appearing in Theorem 4 originates in the following computation of exact distribution. In addition to real symmetric matrices ( in the usual random matrix notations) it also covers the case of complex Hermitian matrices ().

Theorem 2.

Fix and assume . Let be an –dimensional subspace in the –dimensional space and let be uniformly random orthogonal matrix with determinant if ( is a uniformly random unitary matrix if ). Let be an orthogonal projector on the space orthogonal to , ,…, . Let be a projector on the subspace and be a projector on the subspace . Then non-zero eigenvalues of coincide with those of the Jacobi ensemble of real symmetric if (complex Hermitian if ) matrices of density proportional to

| (35) |

Remark 3.

We can replace in the definition of with . Indeed, if , then . If , then disappears (one can say that it becomes an identical operator) and the random operators and has the same law, since the uniform measure on the orthogonal group is invariant under the inversion .

By a similar argument applied inductively we can replace with . Note, however, that for we can not replace it with .

The case of Theorem 2 is established in (Bykhovskaya and Gorin, 2022, Theorem 6 in Appendix). The proof of Theorem 2 uses the following three auxiliary ingredients.

Lemma 4 (Block matrix inversion formula).

For matrices , , , , we have:

| (36) |

Proof.

Direct computation. ∎

Lemma 5 (Cayley transform).

Suppose that all eigenvalues of matrix are different from . Then is an orthogonal matrix with determinant , if and only if the matrix defined through

| (37) |

is skew-symmetric, i.e., it satisfies .

Proof.

The formulas (37) imply that if and only if . On the other hand, for a skew-symmetric , we have . Hence, . ∎

Lemma 6.

Choose two positive integers , and set . Let be a uniformly random orthogonal matrix with determinant . Write in the block form according to splitting:

Then is a orthogonal matrix of determinant uniformly distributed among all such matrices. In addition, the random matrices and are independent.

Remark 7.

The law of is explicit. The computation (44) below implies that the density of is proportional to

Remark 8.

Proof of Lemma 6.

First, note that the distribution of eigenvalues of is absolutely continuous and, hence, is almost surely invertible and the matrix is well-defined. Our next task is to show that is an orthogonal matrix with determinant . We use Cayley transform for that. Combining (37) with (36) we have

| (38) |

Since is skew-symmetric, so is its top–left corner . We claim that is the Cayley transform of , which would imply that is orthogonal of determinant . Indeed,

| (39) |

It remains to compute the distributions of and and show their independence. In terms of the distribution of (as a uniformly random orthogonal matrix of determinant ) is given by the density proportional to

| (40) |

see, e.g., Forrester (2010, (2.55)) and notice that for the two equalities. We rewrite the block form (38) of as

where is skew-symmetric and is an arbitrary matrix. We further introduce the notation . Recalling that , we transform

| (41) |

We also define

Note that is an alternative parameterization of , in which is an arbitrary matrix and is an arbitrary skew-symmetric matrix. Using the formula for the determinant of a block matrix

| (42) |

we rewrite (40) as

| (43) |

Further, notice that

Hence, the last line of (43) is transformed into

| (44) |

where in the last line we use and change variables and using the general Jacobian computations:

-

•

The map on matrices has the Jacobian

(45) -

•

The map from the space of skew-symmetric matrices to itself has the Jacobian

(46)

The first identity (45) follows from the observation that each column of is transformed by linear map and there are such columns. The second is similar and we refer to Forrester (2010, (1.35)) for details.

The key important feature of the last line of (44) is that it has a product form, which implies the joint independence of , , and . Hence, the density of is proportional to . Comparing with (40) and noting that the dimension changed from to , we conclude that is a uniformly random orthogonal matrix of determinant .

Proof of Theorem 2.

We only give a proof for the real case ; the complex case can be proven by the same argument. The proof is induction in with base case being (Bykhovskaya and Gorin, 2022, Theorem 6 in Appendix) and the induction step being based on Lemma 6.

Step 1. We first note that the particular choice of deterministic space in the statement of the theorem is not important: any other deterministic choice of can be achieved by a change of basis of the –dimensional space, which keeps the probability distribution of and, hence, entire construction invariant. In particular, the probability distribution of is unchanged. However, we need to be more careful, if we would like to make random, as correlations with might cause issues.

Step 2. Take any . We claim that replacement of with everywhere in the statement of Theorem 2 does not change the eigenvalues of . Indeed, the only important feature of here is that it is an orthogonal operator commuting with . Hence, the change leads to the image of the projector being multiplied by ; in more details, the transformation takes the form . Further, gets transformed to and undergoes a similar transformation: . The same is true for : it undergoes the transformation . We conclude that the product is transformed into . Since conjugations do not change eigenvalues, we are done.

The arguments of Steps 1 and 2 might give a feeling that we can actually replace by any random space. However, this is not the case. Repeating the same arguments, we see that replacement leads to the same eigenvalues of the projector as if we replaced . In both Steps 1 and 2 had the same distribution as , hence, the eigenvalues were unchanged. But in general, if is correlated with in a non-trivial way, then the distribution might change.151515For instance, if is spanned by eigenvectors of , then the spaces , ,…, all coincide, which is a very different behavior from the case of deterministic .

Step 3. We now transform the statement of Theorem 2 by replacing with and further replacing by everywhere. Since the uniform (Haar) measure on the orthogonal matrices is invariant under inversion, the law of eigenvalues of is unchanged and the ingredients of Theorem 2 are now as follows:

-

•

is a uniformly random orthogonal matrix with determinant and is an arbitrary (deterministic) –dimensional subspace of the –dimensional space, whose choice is irrelevant for the statement.

-

•

is the projector on the orthogonal complement of , , …, , .

-

•

is the projector on the subspace and is the projector on the subspace . (The latter can be replaced by without changing the outcome. Indeed, for that we need start from instead of , which is possible by Remark 3).

-

•

The claim is that the eigenvalues of are distributed as (35).

We are going to prove this last statement by induction in . For that we choose to be the span of the last coordinate vectors, split with and project everything on the first coordinate vectors (which are orthogonal complement to ). We rely on Lemma 6 and use and notation from that lemma.

Step 4. We claim that the subspace in –dimensional space spanned by the first coordinates of , , …, (since has zero projection on the first coordinates, we do not need it here) is the same as the subspace spanned by , , …, , where is –dimensional space spanned by columns of the matrix .

Indeed, the first coordinates of are by definition of the block structure in Lemma 6. Further, to go from powers of to powers of we make the following observation: take a vector in –dimensional space and write it as , where is -dimensional vector (one can think of being in ) and is –dimensional vector (one can think of being in the orthogonal complement of ) and write

Then the –dimensional vector takes the form

Since we only care about the linear span of columns and already belongs to the desired linear span, the last term can be ignored and we arrive at , which then implies the claim.

Step 5. Next, consider the projection of on the orthogonal complement to , , …, , . This is the same as the the projection of the first coordinates of on the orthogonal complement (in –dimensional space) to first coordinates of , , …, . Hence, combining with the argument of Step 4, this is the same as the projection of on the orthogonal complement of , , …, . It is convenient to note that .

Step 6. Finally, consider the projection of on the orthogonal complement of , , …, , . By Steps 4 and 5 this is the same as the projection of the first coordinates of on the orthogonal complement of , , …, . Representing in the block form, the first coordinates of are the span of the columns of the sum of the top–left corner of multiplied by plus the top-right corner of multiplied by . Using Lemma 4, we get the span of the columns of

which is the same as .

Step 7. Combining the results of Steps 6 and 7 with Lemma 6, we identify the eigenvalues of with the eigenvalues of obtained by the following procedure:

-

•

is a uniformly random orthogonal matrix with determinant , where .

-

•

is the projector on orthogonal complement of , , …, .

-

•

is the projector on the subspace and is the projector on the subspace .

Since is independent from by Lemma 6, this is the same form as the one at the end of Step 3, but with decreased by , decreased by , and replaced by . Decreasing by and by leaves the formula (35) unchanged, hence, we can invoke the induction assumption, thus, finishing the proof. ∎

7.3. A perturbation of the Jacobi ensemble.

Recall the cyclic shift161616Note that in Bykhovskaya and Gorin (2022) we expressed all the operators in terms of rather than . operator acting in –dimensional space. Let be the –dimensional space orthogonal to the vector , i.e., . Note that is an invariant space for and let denote the restriction of on the subspace .

Take a uniformly-random orthogonal (or unitary if ) operator acting in –dimensional space and define an operator acting in :

Proposition 9.

Assume and let be as above. Take an arbitrary –dimensional subspace in –dimensional space . Let be the orthogonal projector on the space orthogonal to , ,…, . Let be the projector on the subspace and be the projector on the subspace . Then the distributions of non-zero eigenvalues of coincides with that of the squared sample canonical correlations solving (17) under the hypothesis .

Comparing Proposition 9 with Theorem 2 and Remark 3 one notices that the differences are in restricting on the subspace (hence, decreasing the dimension by ) and in replacement .

Proof of Proposition 9.

Step 1. We start by transforming the Gaussian noise . Let be matrix, whose -th column is . Take any non-degenerate matrix and transform . Thus, we leave unchanged and recalculate , . We claim that the canonical correlations solving Eq. (17) are unchanged. Indeed, the linear subspace stays the same and so does the projector . For each , the vector is transformed by and is transformed by Recall that the space includes vector , which leads to the projector canceling the additional terms and in the last two formulas. Hence, the matrices and are transformed by and . Therefore,

We conclude that Eq. (17) is multiplied by and, hence, its roots are preserved.

By choosing an the covariance matrix becomes identical. Hence, for the rest of the proof we assume without loss of generality that is identical, which means that the matrix elements of are i.i.d. standard Gaussians.

Step 2. Let us now reduce the canonical correlations solving Eq. (17) to eigenvalues for a product of projectors. By definition the canonical correlations are eigenvalues of matrix

Note that for any two rectangular matrices and of the same sizes the non-zero eigenvalues of and of coincide. Hence, the desired canonical correlations are also eigenvalues of matrix

The last matrix is a product of two projectors:171717For a closer match to the proposition that we are proving, note also that if and are projectors, then eigenvalues of and are the same. the first one projects on the space spanned by columns of and the second one projects on columns of .

Step 3. The next step is to express via various matrices involved in constructing and . Let be the orthogonal projector on the subspace . Under we have . Also

Further, we define the summation matrix . It has ’s below the diagonal and ’s on the diagonal and everywhere above the diagonal:

We set

By a straightforward linear algebra (see (Bykhovskaya and Gorin, 2022, Section 9.2) for some details) one shows that the linear operator preserves the space (orthogonal to ). In addition, its restriction on the subspace coincides with , where is the identical operator acting in .

We can write

| (47) |

We claim that . Indeed, coincides with , where

Since is the summation operator, we have and the claim is proven because .

Step 4. Previous steps yield the following expressions for and . Take the –dimensional space (belonging to -dimensional space ) spanned by the columns of . Let be the orthogonal projector on the space orthogonal to , , …, . (Note that can be replaced by in the last definition without changing ). Then the space spanned by columns of is . On the other hand, the space spanned by columns of is . At this point, we see strong similarities with objects in the statement of Proposition 9 with main difference being in the assignment of randomness: is deterministic and is random, but is random and is deterministic. Thus, it remains to relocate the random part.

For that we notice that due to the rotational invariance of the Gaussian law (here it is important that we made the covariance matrix identical on the first step), the space spanned by the columns of has the same law as . The reason is that both laws give uniformly random –dimensional subspace of –dimensional space .

Since everything was previously expressed through the span of columns of , denote , we now simply replace those by the columns of . Then the space orthogonal to , , …, becomes the space orthogonal to , , …, . Equivalently, this is the space orthogonal to , , …, . is the projector on this space. We conclude that the law of canonical correlations (17) is the same as the law of non-zero eigenvalues of the product of two projectors: the first one projects on the subspace and the second one projects on the subspace . Up to a change of basis (by matrix ), which does not change the eigenvalues, we have arrived precisely at the expression from the statement of the proposition. ∎

The next proposition explains the effect of the replacement on the eigenvalues of the product of projectors in Theorem 2 and Proposition 9. We need to introduce some additional notations.

Choose positive integers , , and , such that and an arbitrary –dimensional subspace in –dimensional space. Let

be a map from the group of orthogonal matrices of determinant to –tuples of reals on interval, defined by the following procedure: Take . Let be the orthogonal projector on the space orthogonal to , ,…, . Let be the projector on the subspace and be the projector on the subspace . Then maps to largest eigenvalues of .

We also need three norms:

-

(1)

is the norm of a vector , defined as .

-

(2)

is the supremum norm of a vector , defined as .

-

(3)

is the spectral norm of a matrix , defined as the square root of the largest eigenvalue of . Equivalently, .

Proposition 10.

Suppose that is fixed, while is growing and depends on in such a way that for some . Let and be two random matrices, such that:

-

•

is a uniformly random orthogonal matrix with determinant .

-

•

The eigenvalues of are almost surely different from .

-

•

For each we have

(48)

Then for each we have

| (49) |

Proposition 10 claims a continuity of map . The proof needs care because of the inversions in the definition of the map .

Remark 11.

Proposition 10 has a version for complex numbers, in which all orthogonal matrices are replaced by unitary matrices. The proof of the complex version is the same.

The proof of Proposition 10 relies on three lemmas which we prove later in this section. For these lemmas we write matrices and of Proposition 10 in the block forms according to the splitting :

| (50) |

Lemma 12.

Let be a orthogonal matrix of determinant written in the block form according to the splitting . If all eigenvalues of are different from , then so are the eigenvalues of and of .

Lemma 13.

Under the assumptions of Proposition 10 we have

| (51) |

Lemma 14.

Under the assumptions of Proposition 10, let be the –dimensional subspace of –dimensional space spanned by the last coordinate vectors. There exists an orthogonal matrix , depending only on and an orthogonal matrix, , depending both on and on , such that , and

| (52) |

Proof of Proposition 10.

The proof is induction in with the base case proven in Bykhovskaya and Gorin (2022), see the continuity of in the proof of Proposition 13 there. For the induction step we recycle the ideas in the proof of Theorem 2.

First, recall a property of function , which we established in Steps 1 and 2 of Theorem 2: if is a orthogonal matrix, then

| (53) |

Note that conjugations (by the same orthogonal matrix for and ) leave the three conditions of Proposition 10 unchanged, hence, the (53) implies that statement of proposition remains the same for any choice .

Second, we make the replacements of Steps 2 and 3 of Theorem 2 individually for and . The replacement does not change the eigenvalues of , while inversion of and keeps the conditions of Proposition 10 unchanged. Summing up, we replace the map in Proposition 10 by a new map defined through: Let be the subspace spanned by the last coordinate vectors in –dimensional space. Let be the orthogonal projector on the space orthogonal to , ,…, . Let be the projector on the subspace and be the projector on the subspace (or, equivalently, on ). Then is largest eigenvalues of .

Using the block notations (50), steps 4-7 in the proof of Theorem 2 imply the following almost sure identities:

| (54) |

| (55) |

We would like to check that the right-hand sides of (54) and (55) are close by using the induction assumption.

Using (53) and Lemma 14, we rewrite the right-hand sides of (54) and (55) as:

| (56) |

Let us check that we can apply the induction assumption to deduce that the expressions of (56) are close to each other:

- •

-

•

By Lemma 12, is well-defined and no eigenvalues of are equal to . Hence, the eigenvalues of are almost surely different from .

- •

Hence, using the statement, the expressions in (56) are close to each other as and, therefore, (54) is close to (55). ∎

Proof of Lemma 12.

Let us show that has no eigenvalues . We argue by contradiction and assume that there exists an –dimensional vector of length such that . Note that by orthogonality of . Hence, using the notation for the scalar product, we have

Therefore, , which readily implies that the –dimensional vector is an eigenvector of with eigenvalue . Contradiction.

Next, for the matrix , let us use its representation as a Cayley transform developed in (39):

where is a skew-symmetric matrix. If was an eigenvector of with eigenvalue , then we would have

which is impossible for non-zero . ∎

Proof of Lemma 13.

Note that whenever is a submatrix of , we have . Hence, the spectral norms of the differences , , , are all small with probability tending to as . Addition, multiplication, and inversion of matrices are all Lipschitz operations as long as factors are bounded for the multiplication and singular values are bounded away from for the inversion. Therefore, it remains to show that the norms of the factors , , and are uniformly bounded (since , , and are close to , , and , respectively, the norms of the latter are then going to be bounded as well). For and the bound on the norm is straightforward, as they are submatrices of , whose norm is . Hence, and .

In order to deal with we rely on the fact that the distribution of the symmetric matrix is explicit. It has density (see, e.g., (Forrester, 2010, (3.113) and the formula immediately after)) proportional to:

| (57) |

This is a particular case of the Jacobi ensemble of Definition 1 and we can use the large asymptotic of the latter recorded in Proposition 1. Therefore, there exists a constant , such that all the eigenvalues of are smaller than with probability tending to as . Hence, by the triangular inequality

with probability tending to as . We conclude that

Proof of Lemma 14.

We will be proving a slightly different statement, in which is the span of the first (rather than last) coordinate vectors. The desired statement of the theorem is then obtained by replacing , and , where is the (orthogonal matrix) which swaps th and th basis vectors for .

We know that the matrices and are close to each other and our aim is to show that the orthonormal bases of and its orthogonal complement, and and its orthogonal complement can be chosen to also be close to each other. For that we need to produce some formulas for these bases, which is what we do in the rest of the proof. The delicacy of this argument stems from the fact that given a space, in general, there might be no continuous way to produce an orthogonal matrix, such that the space is spanned by its first columns. (For instance, by the hairy ball theorem one can not continuously complement a unit vector in –dimensional space to an orthonormal basis.) Hence, we need to be more careful.

We start by replacing with

and replacing with

Clearly, and . The advantage of and is that their columns are orthonormal. Indeed,

and similarly for .

Claim. and are asymptotically close to each other:

| (58) |

Note that and are built out of and with operations of addition, multiplication, inversion, and square root. The first one is Lipschitz in spectral norm, the second one is Lipschitz as long as the factors are uniformly bounded, and for the last two we additionally need the singular values of the factors to be uniformly bounded away from uniformly181818For the square root operation on positive-definite matrices we can first rescale so that its spectrum belongs to segment for some and then use Taylor series expansion of the square root: to deduce the Lipschitz property. . We already explained in the proof of Lemma 13 that has spectral norm at most and that (and hence also its inverse and its transpose) has singular values bounded away from and . Hence, it remains only to deal with in the definition of . Since is a submatrix of uniformly random matrix, the law of is explicit. It has density (see, e.g., (Forrester, 2010, (3.113) and the formula immediately after)) proportional to:

| (59) |

This is a particular case of the Jacobi ensemble of Definition 1 and we can use the large asymptotic of the latter recorded in Proposition 1, which implies that the eigenvalues of are bounded away from as . The claim is proven.

Next, we produce the desired orthogonal matrix by the Gramm-Schmidt orthogonalization procedure: letting be the –th coordinate vector in –dimensional space, and be the –th column of , we start from vectors

and orthogonalize them. This is a valid procedure, since the Gramm matrix of the above vectors is almost surely non-degenerate (this is equivalent to the non-degeneracy of the top corner of , which is true due to absolute continuity of the distribution of this corner with respect to the Lebesgue measure on matrices that can be deduced from Remark 7).

We set the columns of to be the vectors from the orthogonalization procedure. Since the vectors are orthonormal, is orthogonal. Note that since the columns of are orthonormal, the first steps of the orthogonalization procedure are trivial and the first columns of are . In particular, these columns span , as desired.

We proceed to the construction of . It is tempting to do exactly the same procedure (with all indices replaced by indices ), but that is not going to work: the problem is that while the top corner of was almost surely non-degenerate, but it can have singular values arbitrary close to . Eventually, this leads to unstability of the orthogonalization procedure and, hence, there is no way to guarantee that the results of orthogonalization for and are close to each other.

Therefore, we proceed in a different way. Set . Because the first columns of are , we have

where stays for the filled with matrix elements. Hence, since and were close, we have

| (60) |

Let , , denote the columns of and consider vectors

We are going to orthogonalize these vectors. The advantage over the procedure we used for is that now the top submatrix of is close to identity, which is going to make the orthogonalization procedure well-behaved. In order to make the orthogonalization procedure explicit, we are going to use a block version of the Cholesky decomposition.

For that set and write in the block form according to the splitting :

Let denote the matrix written in the block form as

We would like to perform orthogonalization of the columns of . For that we first compute

| (61) |

We further would like to represent as

| (62) |

Comparing with (61) we conclude that

| (63) |

Since the spectral norm of a submartix is at most the spectral norm of the matrix, (60) implies that

| (64) |

Therefore, is close to , is close to , is close to , is close to .

Note that and are positive-definite symmetric matrices, hence, they have well-defined square roots. In addition,

The goal of all these manipulations with matrices is to define

| (65) |

The two key properties of are:

-

•

The span of the first columns of coincides with .

-

•

is orthogonal. Indeed, using (62) we have

Hence, we can finally set

We have

as desired. It remains to show that the matrix is very close to identity, as this would imply that is close to . For that we consider each factor in (65) and see that they are close to identical matrices by (64). Hence,

as desired. ∎

Proof of Theorem 4.

We start by explicitly constructing the desired coupling. For the Jacobi ensemble we use the realization of Theorem 2 and for the matrix of the Johansen test we use the realization of Proposition 9. We set to match the notations and it remains to couple of Theorem 2 with of Proposition 9.

The eigenvalues of are all roots of unity of order different from . In the complex case we can diagonalize to turn it into diagonal matrix with the roots of unity on the diagonal. In the real case , the matrix should be block-diagonalized (with blocks of size and one additional block of size corresponding to eigenvalue if is even): the pair of complex conjugate roots of unity and gives rise to the matrix of rotation by the angle . Let us denote by the resulting (block) diagonal matrix multiplied by . In order to avoid ambiguity about the order of eigenvalues, we assume that the blocks correspond to the increasing order of , i.e., the top-left corner of corresponds to the pair of the closest to eigenvalues of .

The eigenvalues of also lie on the unit circle and if , then they come in complex-conjugate pairs. Hence, can be similarly block-diagonalized (we do not need to multiply by this time) and we denote through the result. The distinction with is that the eigenvalues are random and so is . The law of the eigenvalues of is explicitly known in the random-matrix literature. Both for and they form a determinantal point process on the unit circle with explicit kernel. The repulsion between the eigenvalues leads to them being very close to evenly spaced as . We summarize this property in the following statement (which is a manifestation of a more general rigidity of eigenvalues, see, e.g., Erdos and Yau (2012)), whose proof can be found in Meckes and Meckes (2013, Lemma 10, , case, and Section 5).

Claim. There exist constants , such that for , every , there exists and for every we have 191919All the constants can be made explicit, following Meckes and Meckes (2013).

| (66) |

We remark that since and are block-diagonal, the bound on the maximum matrix element of their difference is equivalent to a similar bound for any other norm, e.g., for the spectral norm, which we used in Proposition 10.

We now choose another uniformly-random orthogonal (or unitary if ) matrix (independent from the rest), replace with and replace with . The invariance of the uniform measure on the orthogonal group (or on the unitary group if ) with respect to right/left multiplications, implies the distributional identities:

The right-hand sides of the identities provide the desired coupling and (66) implies that these two random matrices are close to each other as .

7.4. Small rank perturbations

In this section we prove Theorem 3 by combining Theorem 4 with Proposition 1 and general statements about small rank perturbations. The key step of the proof is the following observation:

Theorem 15.

Proof.

Throughout the proof we assume that the matrices and are invertible. In principle, invertibility might fail for some : in such situation we can still use Moore–Penrose inverse in order for the statements to make sense, and we are not going to detail this.

In the following argument we use various properties of ranks:

-

•

If a matrix differs from a matrix only in columns, then ;

-

•

;

-

•

;

-

•

If matrices and are invertible, then .

We refer to the time series defined by (1) as and to the time series defined by (23) as . We form two matrix and with columns and , , respectively. Our first task is to show that as .

For that we subtract (23) from (1) to get:

| (69) |

In the matrix form, (69) represents the matrix with columns as a sum of low rank matrices, with the total rank (coming from the right-hand side of (69)) at most

| (70) |

The matrix is obtained from by multiplication by the summation matrix

Hence, the rank of is at most (70) and by assumption (9) of Theorem 3.

Next, we should take into account that the procedures for constructing , from and , from are slightly different. Namely, the latter involves cyclic shifts of indices, rather than usual shifts, involves regressing over only constants, rather than deterministic terms , and finally involves detrending (13). However, cyclic shifts only affect the first indices and, hence, lead to bounded difference in ranks, and similarly for detrending. Regressing on terms leads to another difference in ranks, which is negligible after division by in the limit by (9). The conclusion is that , from one side and , on the the other side are constructed from two finite sets of matrices, which differ by small rank perturbations, by finitely many of operations of addition, multiplication, and inversion. Each of these operations preserves the smallness of the rank of perturbations and, hence,

| (71) |

Since and are obtained from , and , , respectively, by the same algebraic operations, (68) follows from (71). ∎

Proof of Theorem 3.

Let denote the eigenvalues of and let denote the eigenvalues of . Combining Theorem 4 with Proposition 1 we conclude that the empirical measure of converges:

| (72) |

We would like to show that can be replaced by in (72). Note that although the spectra of matrices and are real, but these matrices are not symmetric. Similarly to (68), , however, in general, for non-symmetric matrices even rank perturbations can lead to significant changes in the spectrum. Hence, we need to be more careful and symmetrize and by using projectors as in (68).

Note that for any two matrices and , the non-zero eigenvalues of and of coincide. Recalling that and using the notations (67), we conclude that the eigenvalues of are the same as largest eigenvalues of . Since , they are also the same as largest eigenvalues of and the same as those of . Similarly, the eigenvalues of are the same as largest eigenvalues of .

Denote . All the involved matrices are symmetric and we can use classical inequalities between eigenvalues of a Hermitian matrix and Hermitian matrix , where has rank , see, e.g., Horn and Johnson (2013, Corollary 4.3.5). In our situation the inequalities read

| (73) |

Therefore, for any points ,

Hence, (72) implies

| (74) |

8. Appendix 2. Discussion of asymptotics under and

The goal of this section is to discuss the asymptotics of the test statistic of (18) under various data generating processes (11) generalizing of (22) and Theorem 5.

8.1. Beyond

We start by working under a slightly more restrictive assumption than (9) of Theorem 3. Let be the spectral norm of a matrix .

Conjecture 1.

Fix some . Suppose that the data generating process is

| (75) |

-

(1)

and the covariance matrix satisfies and ;

-

(2)

and for all ;

-

(3)

All roots of the following characteristic equation (76) satisfy202020This guarantees that is process, which is a standard assumption in the cointegration literature. :

(76) -

(4)

and for all .

Then as in such a way that , the conclusion of Theorem 5 continues to hold with the same and :

| (77) |

We do not expect the conditions in Conjecture 1 to be optimal. For instance, the Gaussianity assumption can likely be relaxed, as the simulations of Bykhovskaya and Gorin (2022, Section 7.1) indicate, and it is plausible that condition can be replaced with slow growth of , as in Theorem 3. Nevertheless, we wanted to record Conjecture 1 in the present form, as a precise statement to be addressed in the future work. We are not giving a proof of Conjecture 1 here: the required mathematical apparatus does not exist so far. Instead, we are going to provide a heuristic argument for its validity based on our recent results in Bykhovskaya and Gorin (2023) in a related, yet different setting.

Bykhovskaya and Gorin (2023) studied the following general setting: let and be two random linear subspaces in –dimensional space with , and all three numbers assumed to be growing to infinity. In addition, suppose that there are special vectors inside and other special vectors inside , where is assumed to stay finite as other parameters grow. We directly observe and , but not or . Can we reconstruct , , or at least identify their presence by looking at the squared sample canonical correlations between and and corresponding vectors?

The connection to our cointegration tests comes from taking as the space spanned by the rows of , as defined after (14), and as the space spanned by the rows of . The value corresponds to the cointegration rank and correspond to the cointegrating relationships.

While any finite can be analyzed in a similar fashion, let us stick to case for simplicity, so that we have a single vector and another vector . The most important quantity is the sample squared correlation coefficient between vectors and . It turns out that if is large (i.e., close to , because ), then the largest canonical correlation between and is clearly separated from the rest (reminiscent of Figure 1) and the corresponding eigenvectors can be used to extract information on and . On the other hand, if is small, then the histogram of the canonical correlations does not have such a spiked eigenvalue and all the information about and is washed out. Bykhovskaya and Gorin (2023, Theorem 2.5, Theorem 3.2, Theorem 3.3, Theorem 3.4) proved the existence of separating the above two regimes for a variety of settings for the data generating process for , , , and , see also Bao et al. (2019); Yang (2022b). However, the results of Bykhovskaya and Gorin (2023) do not address the setting relevant to cointegration and further new ideas would be necessary to find the value of for cointegration or rigorously prove its existence. Nevertheless, because the cointegration testing is also based on canonical correlations, one expects that the same phenomenology is true for it and, therefore, there should be the following dichotomy:

-

(1)

If the linear subspace (in –dimensional space) spanned by the rows of (as defined after (14)) has a special vector and the linear subspace spanned by rows of has a special vector , such that the sample squared correlation coefficient between and is atypically large compared to correlation coefficients of other vectors (e.g., if it is close to ), then the histogram of all squared canonical correlations would have a spike as in Figure 1 and we should be able to reject the null of no cointegration.

- (2)

We now present heuristics in favor of Conjecture 1 based on this dichotomy. Some of the technical details are omitted as we try to express the key ideas instead.

Heuristics for Conjecture 1.

For simplicity of the presentation we stick to the case , take the covariance matrix to be identical, set , and let to be a matrix, which has in the upper-left corner and everywhere else. Clearly, and the only root of (76) is , hence, the third condition in the statement of Conjecture 1 turns into .

Note that if we look only at the last out of coordinates of , then we are in the setting of Theorem 5 and asymptotics (25) holds. In particular, the largest canonical correlation is not separated from the rest. Hence, we only need to investigate how the addition of the special first row changes the situation. We will rely on the above dichotomy for our assessment. There are two ways how the addition of the first coordinate changes the setting compared to the situation when it did not exist (and was smaller by ):

-

(1)