sec0em2.75em \cftsetindentssubsec2.75em3.5em

Holdout sets for safe predictive model updating

Abstract

In complex settings, such as healthcare, predictive risk scores play an increasingly crucial role in guiding interventions. However, directly updating risk scores used to guide intervention can lead to biased risk estimates. To address this, we propose updating using a ‘holdout set’ — a subset of the population that does not receive interventions guided by the risk score. Striking a balance in the size of the holdout set is essential, to ensure good performance of the updated risk score whilst minimising the number of held out samples. We prove that this approach enables total costs to grow at a rate for a population of size , and argue that in general circumstances there is no competitive alternative. By defining an appropriate loss function, we describe conditions under which an optimal holdout size (OHS) can be readily identified, and introduce parametric and semi-parametric algorithms for OHS estimation, demonstrating their use on a recent risk score for pre-eclampsia. Based on these results, we make the case that a holdout set is a safe, viable and easily implemented means to safely update predictive risk scores.

1 Introduction

Risk scores estimate the probability of an event given predictors . Their use has become routine in medical practice (topol2019), where is typically a binary random variable representing an adverse event incidence and various clinical observations. Once calculated, risk scores may be used to guide interventions, perhaps modifying , with the aim of decreasing the probability of an adverse event. For example, the QRISK3 score predicts thromboembolic risk given predictors including age and hypertension (hippisley17), and a high score may prompt prescription of antihypertensives or more frequent follow-up.

Risk scores are typically developed by regressing observations of on . Should the joint distribution of subsequently change, or ‘drift’, then risk estimates may become biased (tsymbal04). This can happen naturally over time, meaning that risk scores typically need to be updated periodically to maintain accuracy.

Updating of the risk score will involve obtaining new observations of , but crucially the distribution of may also have changed due to the effect of the risk score itself: that is, high predicted risk of an adverse event may trigger intervention to reduce that risk. The effect of such interventions may be impractical to infer or measure, and indeed the fact that intervention took place may be unrecorded. In the example above, this means individuals prescribed antihypertensives in response to higher QRISK3 scores should have lower thromboembolic risk than they would have if QRISK3 was not used. Should a new risk score be fitted to observed , the effect of hypertension on risk would be underestimated. This bias is worsened by heavier intervention resulting in risk scores becoming ‘victims of their own success’ (lenert19). This framework of directly updating a risk score on an ‘intervened’ population has been termed ‘repeated risk minimisation’ (perdomo20) in the context when such bias is accounted for, or ‘naïve updating’ (liley21updating) when it is not.

In liley21updating we briefly noted that this bias could be avoided by splitting the population on which the score can be used into an ‘intervention’ set and a ‘holdout’ set, with an updated model trained on the latter. In this work, we formally develop this proposal for practical use in real-world predictive risk score updating and prove its suitability. In particular, we address a vital tension in the choice of an optimal holdout size (OHS) for the holdout set: for the risk score to be accurate, the holdout set should not be too small; but any samples in the holdout set will not benefit from risk scores, so nor should it be too large. The holdout set must be actively generated; it is not sufficient to simply update a model using samples who received a risk score but were untreated.

Use of a holdout set appears ethically tenuous. However, we argue that in many circumstances it is unethical to not use a holdout set, in that other options lead to worse outcomes. Essentially, use of a holdout set limits costs incurred from inaccuracies in prediction to individuals in that set, whereas all alternatives lead to risk score inaccuracy across the entire population. We formalise these arguments in Section 3, in particular showing that the updating paradox described above is inevitable for risk scores on complex systems intended to guide interventions.

Contributions in this area are important due to rapidly evolving legislation. Currently, the European Union treat each update of a risk model as a separate risk score requiring re-approval, but in the United States a proactive approach is taken with a ‘total-life cycle’ paradigm which allows practitioners to update risk models as necessary without requesting approval (fda19). This approach could allow updating-induced biases to go undetected, and highlights the need for safe updating methods in risk score deployment. The use of holdout sets as examined in this work offers one potential solution.

We begin by reviewing relevant literature in Section 1.1, and introduce a motivating example in Section 1.2, with which we will work throughout. Our first question is whether a hold-out set is worth the cost, as opposed to simply continuing to use the existing score with degraded performance, or updating naïvely. We set out the problem and notation precisely in Section 2. In Section 3, we then develop theory which proves that under certain simplifying assumptions, as long as drift and intervention effects occur, the cost of holding out samples is generally justified and that the holdout set approach outperforms common alternatives. We then turn attention to the problem of selecting holdout set size in Section 4, constructing an optimisation problem to find an OHS. Therein we also set out why several apparent alternatives are not competitive. In Section 5, we describe two algorithms for OHS estimation, using a parametric model, and using Bayesian emulation. In Section 6, we support our findings with numerical demonstrations and resolve our motivating example by applying our methods to a risk score for pre-eclampsia (pre) to estimate an OHS for updating it.

1.1 Review of related work

Widespread collection of electronic health records has spurred development of new diagnostic and prognostic risk scores (cook15; liley21medRxiv), which can allow detection of patterns too complex for humans to discover. Examples of such scores in widespread use include: EuroSCORE II, which predicts mortality risk at hospital discharge following cardiac surgery (nashef12); and the STS risk score from the United States, predicting risk of postoperative mortality (shahian18). Many such scores have demonstrable efficacy in clinical trials and in-vivo (chalmers13; wallace14; hippisley17).

An important general concern with these scores is continued accuracy of predictions. A 2011 review found that risk scores for hospital readmission perform poorly and highlighted issues with design of their trials (kansagara11). More recently, an analysis of a sepsis response score used during the COVID pandemic found increasing risk overestimation over time (finlayson20). Various efforts have been made to standardise procedures in risk score estimation to address these issues (collins15).

Several algorithms have been developed to update models with new data in the presence of drift (lu18), which ideally leads to the best possible model performance after every update. However, adaptation of model updating to avoid naïve updating-induced bias requires explicit causal reasoning (sperrin19) and often further data collection (liley21stacked). In a seminal paper, perdomo20 analyse asymptotic behaviour of repeated naïve updating, giving necessary and sufficient conditions under which successive predictions end up converging to a stable setting where they essentially predict their own effect. Other approaches to optimise a general loss function by modulating parameters of the risk score are developed in mendler20; drusvyatskiy20; li21 and izzo21. These approaches seek to minimise a ‘performative’ loss to the population in the presence of an arbitrary risk score, whilst our approach seeks to target risk scores which reliably estimate the same quantity, namely in a ‘native’ system prior to risk score deployment. Our approach is well-suited to settings where the performative loss is essentially intractable, requiring cost estimates of risk scores only in limited settings.

We note that ‘stability’ is not necessarily desirable in terms of the distribution of interventions: in the QRISK3 setting, if an individual is at untreated risk of 50% and treated risk of 10%, with treatment distributed proportionally to assessed risk, a ‘stable’ risk score would assess risk as e.g. 30%, prompting a milder intervention than actual untreated risk would suggest, after which true risk remains at 30%, regardless of treatment cost.

We found no literature directly addressing the focus in this paper: determining how large a holdout set should be. Similar problems do arise in clinical trial design: stallard17 estimate the optimal size of clinical trial groups for a rare disease in which individuals not in the trial stand to gain more than those in it, using a Bayesian decision-theoretic approach accounting for benefit to future patients in the population. Our problem is related to computation of a minimal training size for a clinical prediction model riley20, but rather than being limited by financial cost of obtaining training samples, we are limited by a cost to all individuals in the holdout set, allowing specification of an explicit tradeoff for larger sample sizes.

OHS estimation requires quantification of expected material costs when using risk scores trained to holdout data sets of various sizes: that is, the cost of reduced accuracy from limiting the OHS, as well as the cost due to individuals in the holdout set not benefiting from a risk score. Such costs depend on the error in risk predictions. The relation of predictive error to training set size is well studied and known as the ‘learning curve’, which can sometimes be accurately parameterised (amari93). A recent review paper suggests a power-law is accurate for simple models (viering21).

1.2 Motivating example

In this example, we consider the ASPRE score (akolekar13) for evaluating risk of pre-eclampsia (pre), a hypertensive complication of pregnancy, on the basis of predictors derived from ultrasound scans in early pregnancy. Although treatable, pre confers a serious risk to both the fetus and the mother. The risk of pre is lowered by treatment with aspirin through the second and third trimesters (rolnik17), but aspirin therapy itself confers a slight risk, contraindicating universal treatment, and suggesting prescription of aspirin only if the risk of pre is sufficiently high or other indications are present (acog16). The ASPRE score was developed to aid clinicians in estimating pre risk and has been shown to be useful in prioritising patients for aspirin therapy (rolnik17b). We will not differentiate early- and late-stage pre.

Due to changing population demographics, the influence of risk factors is likely to change over time, and the ASPRE score will need to be periodically updated. As discussed, a naïve re-fitting of a risk score on the basis of () maternal assessment in early pregnancy and () eventual pre incidence could lead to dangerous underestimation of pre risk, due to individuals previously assessed as high risk being treated in response to the assessment.111It is possible that the existing ASPRE score is already affected by the very problem we describe, in that some individuals in the ASPRE training set potentially were treated with aspirin due to concerns about PRE risk and so had a lower pre risk than they would have had otherwise. This could be managed as per e.g. vangeloven20, but we do assume this effect is minimal and do not do so here.

This could be avoided by maintaining a holdout set. For patients in this set, no ASPRE score would be calculated at first scan, and treatment would be according to best practice in the absence of a risk score. An updated ASPRE score can then be fitted to data from these patients. Patients in this holdout set go without the benefit of the ASPRE score, leading to a less accurate allocation of prophylactic treatment (aspirin) and consequently a higher risk of pre (rolnik17b). However, an inappropriately small holdout set would lead to an inaccurate updated model, reducing the benefit of future use of the score.

2 Problem description

2.1 General setup

We presume a random process , , representing the covariates of a single sample at time . We let have distribution where has constant support .

To demonstrate why we opt to use a holdout set approach, we define two functions dependent on . We define as the probability of an event if no risk score is in place, and as the probability of an event when a risk score is used to guide decisions. We will not explicitly consider events as random variables (for the moment); rather we will simply consider and as functions. We will generally omit the argument from , as it will usually be clear. We will use to informally denote the sets of functions , respectively.

We wish to estimate rather than , since it gives a risk of the event in question under standard practice: that is, without already using a risk score. An agent may opt to intervene in addition to standard practice if is high.

We thus aim to generate risk scores which estimate for on some interval. Risk scores will be fitted to samples observed over a time period for . Denote by

| (1) |

a risk score fitted to samples of with , , and where is a uniform distribution, a Bernoulli distribution, and is a function possibly depending on . We will measure deviation of a risk score from a function using (essentially) mean-square generalisation error:

| (2) |

We will consider four options for how best to decide on a series of risk scores to be used over a time period . We will use the term ‘epoch’ to mean periods of time , , , with during which a particular risk score is used and a new risk score is (potentially) fitted. From Section 4 onwards, we will generally take which we will be able to do without loss of generality.

-

Holdout:

Amongst samples encountered while , , we withhold randomly chosen samples from attaining risk scores, and fit a risk score to them. We thus obtain a risk score for use on the epoch . We call this approach the holdout strategy.

-

No-update:

We use a risk score , fitted to a number of samples at time 0, and continue using this score throughout the period. We call this the no-update strategy.

-

Naïve update:

Whenever , , we fit a risk score to as many samples as possible (say ) on whom a risk score is already used. We thus attain a risk score for use on the epoch . We call this approach the naïve update strategy.

We also consider the performance of an unspecified alternative which is ‘less than asymptotically perfect’, in that for some period of time the risk score is (on average) a slightly biased estimator of .

-

Alternative:

We consider an arbitrary alternative giving rise to a risk score at time for which for some value :

(3) where denotes any information used to fit risk scores , and does not depend on any parameters of the strategy (e.g., update frequency ), though may depend on 222We will make assumptions under which the no-update strategy is of the alternative-strategy type. We differentiate them here to illustrate examples of such alternative strategies..

We will finally consider an ‘oracle’ option. Rather than perfect information (e.g. perfect knowledge of for all ), our oracle can observe acting on a number of samples:

-

Oracle:

We presume that whenever , , we fit a risk score to samples of , for which , , and use the risk score on the epoch . We call this approach the oracle strategy.

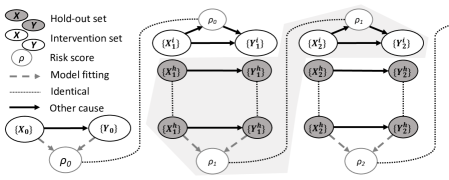

Our strategy for ‘holdout’ updating is illustrated with as a causal graph in Figure 1. The ellipses , correspond to sets of observations of with and in epoch 0, representing initial training data, to which a risk score is fitted, where .

We use the shorthand (‘’ for intervention) to mean a set of samples from with , representing the set of samples on which the risk score is used, and (‘’ for holdout) to mean sets of samples from with as close to as possible, representing the set of ‘holdout’ samples on which the next risk score is fitted. We define corresponding sets and representing observations: for , we have the corresponding in distributed as and for , we have the corresponding in distributed as .

Under a ‘native’ setting prior to deployment of a risk score, and have a single causal link, modelled by risk score (leftmost epoch of Figure 1). Once is in use in the intervention set in epoch 1 (ellipses , ), a second causal pathway through is established from to , but there remains only one causal pathway from to in the holdout set (middle epoch of Figure 1). The quantities in the shaded area do not causally depend on any quantities outside the shaded area; we will consider them together in section 4. The updating process can be continued rightwards (, , ).

3 Motivation for use of a holdout set

We argue that use of a holdout set approach is generally necessary for tolerable total population costs when updating a risk score. In this sense, we argue that it is an ethical imperative to consider use of a holdout set in this context. We will now make and justify a series of assumptions (which will only be used directly in this section). We will discuss robustness to these assumptions in Section 3.1.

The motivation for updating a risk score is generally that the true risk changes continuously with time in a random way. If did not change with (or changed only in a known way) there would be no need to update a well-fitted risk score. Lipschitz-continuous change in the distribution of covariates and the risk function underlies the assumption that, for a risk score to be useful, it must remain reasonably accurate for a period of time after it is fitted.

Assumption A1 (Non-negligible drift).

We have

Assumption A2 (Continuous drift in population distribution).

is -Lipschitz continuous in with respect to total variation distance.

Assumption A3 (Continuous drift in target function).

For all , is -Lipschitz continuous in (where does not depend on )

We presume that adding more samples to a training set for a risk score improves its error at an rate (typical of, for instance, linear models). In subsequent sections, we will consider instead an arbitrary ‘learning curve’.

Assumption A4 (Expected prediction error).

For , denoting

we have

for any time , where the expectation is over the data used to fit .

Since we assume prediction of an adverse event, we want to lower the chance of this event as much as possible. We define a cost per sample in terms of the reduction in the probability of an adverse event which can be achieved by intervention: that is, how much lower is (probability of an adverse event when using a risk score to guide decisions) than (probability of adverse event). For the moment, we are unconcerned with the scale of this cost, so we assume a unit coefficient for this difference. We shift this cost so that it is zero when we are doing ‘as well as possible’; that is, when is exactly .

Assumption A5 (Costs).

For a sample encountered at time , when a risk score is in use, we define the expected total cost, , as:

where

| (4) |

that is, so that if .

If no risk score is used, the risk goes unmodified, so we may take . Under our specification of cost, we then have

so we may take to represent the cost per sample when no risk score is used.

We now make a key assumption in presuming that the risk score is ‘useful’, in that our propensity to make smaller than depends directly on the accuracy of the score. Taken together, A5 and A6 constrain the relationship between and , helping to simplify the statement of our initial results, but we will show that we can substantially weaken this assumption in Section 3.1, and discuss our reasons for making this type of assumption in Section 5.1.

Assumption A6 (Usefulness of risk score).

If a risk score is in use at time , we have,

for some constant .

We note that it immediately follows that cost is minimised at if and only if holds -almost everywhere (our cost may, therefore, be considered an ‘excess cost’ over a super-oracle with essentially perfect knowledge of ), and we allow that a sufficiently inaccurate risk score may incur a higher cost than no risk score, which could potentially occur in real settings. Finally, we make simplifying assumptions of independence of samples at different times and a constant population size.

Assumption A7 (Population size and holdout number).

The times at which samples are observed occur uniformly randomly over time (that is, from a Poisson process) with a mean of samples per unit of time. When using the holdout strategy, we use a constant number of samples in each epoch (if there are fewer than samples available in , we use no risk score for the subsequent epoch , but this will be rare). Samples of are independent.

We define the ‘cost of a strategy’ as the cost accrued over time interval using a given strategy ‘strat’ (which may be: : holdout; : no-update; : naïve update; : alternative or : oracle). We now state three results, the first of which establishes the growth rate of the holdout strategy over time.

Theorem 1.

We note the immediate corollary that, for a fixed , the asymptotic cost of the oracle strategy above:

| (5) |

is the same as that obtained with a holdout set size , and if we choose then

| (6) |

and we achieve an optimal sublinear asymptotic growth rate of if , . We now consider the costs of the no-update and naïve-update strategies. We will show that for either strategy, costs must grow at least linearly in population size (thereby also showing that the updating paradox arises inevitably from assumptions A5, A6):

Theorem 2.

We note that Theorem 2 immediately implies a dominance of the holdout-set strategy, since we cannot attain sublinear cost growth with the no-update, naïve-update, or alternative strategies.

Finally, we show that for fixed , the holdout strategy is essentially optimal in that its cost is asymptotically similar to that of the oracle strategy. This is not true for the no-update, alternative or naïve-update strategies, for which total cost arbitrarily exceeds that of the oracle.

Theorem 3.

We prove Theorems 1, 2 and 3 in supplementary section S2. Restrictions on in Theorems 2, 3 are required because for large (relative to Lipschitz constants , ) too much drift occurs between updates to guarantee sustained performance for the time a risk score is in use.

In general, our results show that any strategy for which alternative strategy condition (3) holds leads to higher costs than the holdout set approach. We claim that it is essentially impossible for a strategy to evade condition (3) (that is, be able to arbitrarily closely approximate at almost all ) without the use of a holdout set, and hence have costs competitive to the holdout-set strategy.

In our setting, without a holdout set, the only information available when we wish to update the model is a set of samples of and for some , where and (if , the risk score is prompting no change in behaviour, which generally contradicts its usefulness). With only this information, we cannot hope to infer without error. To see this, suppose we have some risk score in place over an epoch and observe the function . All we know about comes from assumptions A5 and A6, that is:

| (8) |

from which is not identifiable (see supplement S3.1 for an explicit example).

We may alternatively try to estimate using our knowledge of with (we will say ). If , there is no drift, and the risk score need not be updated. To accurately infer from , we would need to know exactly how changes with , whereas typically drift in is random.

It is more conceivable that could be inferred from using additional information (for instance, records of interventions). However, risk scores are usually used in complex settings (e.g. medicine, finance or law), and decisions are nuanced, so the extent to which a decision is due to a risk score is hard to quantify, even if decisions are explicitly recorded. In the most general setting where we have no additional information, we claim a holdout set provides the most principled statistical approach.

3.1 Robustness

We briefly discuss the robustness of the findings in Theorems 1, 2 and 3 to Assumptions A1-A7. We first note that we can weaken Assumption A6 to

| (9) |

where , for some constants and , whilst retaining the correctness of Theorem 2, requiring only minor modifications to Theorems 1, 3, and Equation 6 (Supplement S2.4).

If Assumption A1 does not hold, then the risk score need not be updated at all, since this implies that for large enough , and are similar. If a risk score must be updated in order to use new data types or methodology, then use of a holdout set may still be necessary.

We do not explicitly mention the possibility of ‘latent’ covariates which influence the risk of outcome . Rather, we may simply assume that risk scores are considered as marginals over latent covariates, which we discuss in greater detail as part of Supplement S3.2. Additionally, we do not assume that drift is independent of our actions: that is, the choice of who to intervene on may affect in the future. However, we do not explicitly model any long-term effects of intervention.

If or are not Lipschitz continuous for some (Assumptions A3, A2 respectively), then a risk score approximating will not necessarily approximate , even for small . Practically, this means that performance of a risk score fitted prior to cannot be guaranteed after . In practice, this could readily occur (for instance, a financial risk score fitted prior to an unexpected disaster), but such an event would nonetheless be better-managed using the holdout-set strategy than others, since a holdout set could be used to ‘reset’ the risk score after .

Heuristically, when using a naïve update strategy, a less-biased risk score (that is, for which is more similar to ) will initially result in lower costs during the first deployment epoch (by a mechanism analogous to Assumption A6), but then suffer higher costs after updating (since lower bias induces a larger difference between and by assumption A5, worsening the consequences of using to approximate ). Under assumption A1, a non-updated model will accrue greater costs over time. We make the case that holdout sets enable good estimation of for most of the sample population at all .

These heuristics generally remain true when using a metric of similarity between and other than , or when assumptions A4, A6, A5 and A7 only roughly hold. In such cases, the holdout set approach will still tend to be lower-cost than other approaches for sufficiently large , although the precise statements of the Theorems may not hold. For example, if Assumption A4 fails perhaps due to model mis-specification so that accuracy decreases to a positive minimum, then costs will grow linearly with the holdout set strategy. However, it will be closer to the oracle strategy than no-update, naïve-update or alternative strategies.

Nonetheless, we do acknowledge that our formulation is quite prescriptive. We roughly model a medical setting in which a physician sees a patient, assesses them, then intervenes and sends them away, only observing some outcome later. There are of course related settings for which this formulation is inappropriate, and we once again must defer to heuristic arguments in such situations.

3.2 Note on ethics

In medical settings (such as our motivating example) the use of holdout sets appears ethically tenuous, due to differential treatment of samples in and out of the holdout set. We argue, however, that the use of holdout sets in these settings should still be considered. Our main reason is the absence of a viable alternative: as above, in many settings it is not possible to attain costs comparable to an idealised oracle strategy without a holdout set. We recapitulate that, even in the event that risk-score guided interventions are recorded, it is not sufficient to use a ‘natural’ holdout set by simply considering individuals who received a risk score, but were untreated, and it is not necessarily possible to infer (Supplement S3.2).

We do note an important subtle assumption is that is finite (Assumption A5). Settings in which it is unacceptable for even one sample to not have a risk score correspond to an infinite , and in such settings we must make do with a risk score for which performance is not close to optimal. By contrast, there are settings for which the absence of a risk score is less serious: for instance, if the outcome in question is not life-threatening and for which existing best practice is often adequate for identifying cases (e.g., tooth decay (zukanovic13) or minor sexually transmitted infections (kranzer21)). In such settings the use of a holdout set is more ethically acceptable, since the cost to any given individual (even in the holdout set) is low.

Lastly, we underscore the importance of considering the adoption of a holdout set, when other ethical concerns do not take precedence. In situations where a holdout set is not feasible, and withholding any treatment is deemed unacceptable, the ability to effectively respond to a drifting ground truth is compromised. Consequently, updates would ultimately yield sub-optimal risk scores for the entire population.

4 Choosing the size of a holdout set

For the remainder of this paper, we will be concerned with choosing an optimal size for the holdout set. We begin by somewhat simplifying our formulation, with a focus on total cost, and no longer using Assumptions A1-A7. We will retain and as having roughly their existing meanings.

Returning to Figure 1, we consider the aggregate set of all samples , and denote the total number of samples by . Note that costs arising from a decision about holdout set size in epoch are realised across an epoch boundary: that is, costs accrued from a larger holdout set are incurred by the holdout set in , whilst cost savings from the same larger holdout set are gained by the intervention set in .

We denote the samples in the ‘holdout’ set as (where ‘’ indicates ‘data’). Since we choose to be as close in time to as possible, we will presume that

A risk score is fitted to which approximates and is used in the intervention set . We will presume that samples in are pairwise independent, as are samples in , although samples in the latter depend on through the fitted risk score.

We define and as random variables associated with the total ‘cost’ of an observation with covariates in the holdout set in epoch and intervention set in epoch respectively. As opposed to the previous section, the meaning of this cost is left unspecified, but is taken to include both the cost of potentially managing the event and any costs of intervention. Function depends on only through the risk score fitted to . We define the expected cost per observation in the holdout and intervention sets, respectively:

| (10) |

Subscripted values and indicate variance in , independent of . We now express total cost across all samples as function of holdout set size

| (11) |

We may take , , to be scaled such that has the same meaning as in assumption A5, but for this and remaining sections, this assumption of scaling is no longer needed. In this sense, we may take the meaning of as contextual dependent on the application; for instance, in QRISK3 it may mean total number of deaths for a fixed healthcare budget.

4.1 Sufficient conditions for existence of an OHS

In this Section, we consider conditions under which the cost can be readily optimised. We discuss estimation of , and in Section 5. We begin with the following assumptions:

Assumption B1.

does not depend on : in a medical context, this means for example that treatment plans and outcomes for patients without risk scores do not depend on the number of such patients.

Assumption B2.

is monotonically decreasing in : the more data available to train the risk score, the greater its clinical utility.

Assumption B3.

There exists such that : a good enough risk score will lead to better patient outcomes than baseline treatment, and a poor enough risk score fitted to small amounts of data leads to worse expected outcomes than baseline treatment.

Assumption B4.

for , with expectations over training data: the ‘learning curve’ for our risk score is convex; there are diminishing returns in the cost per patient from adding more samples to the training data.

We may extend the domain of , to the real interval such that both functions are smooth; and , given assumption B2, , given assumption B4. This leads to the result that there exists an optimal size for the holdout set minimizing the expected total cost. The proof is given in Supplement S4.

As an immediate consequence, we note that the OHS always exceeds the minimal training sample size required to match baseline treatment.

Corollary 1.

The value of always exceeds the value of in assumption B3, since if we have

Consequently assumption B4 may be relaxed for ; we need only be concerned with the behaviour of at realistically large values of , rather than . We also have

and since for large , we have that expected total costs are increasing, but bounded by the per observation expected cost of baseline treatment .

4.2 Robustness to Assumptions B1-B4

The applicability of Assumptions B1-B4 in real world settings requires careful consideration. We address violations of Assumptions B2 and B4 in Section 5.3 and Assumptions B1 and B3 here.

Assumption B1 is fundamental to the success of the holdout set concept. It may be violated if, for instance, agents who can make interventions learn the behaviour of a risk score and apply this to samples with no score. However, such violations are not of serious concern: if we presume that such changes in agents endure over time, then they can be considered as simply contributing to drift, which need not be independent of holdout set size.

If ethically appropriate, Assumption B1 could be assured by partitioning agents to manage only samples in holdout sets or only in intervention sets (e.g., cluster randomisation). This requires assuming that changes in agent behaviour as above do not endure until the following epoch.

If Assumption B3 fails because , we may show a weaker result (the presence of a non-trivial but potentially non-unique minimum loss) by replacing Assumptions B2, B3 and B4 with:

Assumption B5.

There exists an such that

This assumption is essentially stating that at some point the risk score will greatly outperform a risk score built with no data. This leads to the result that:

Theorem 6.

Suppose Assumption B1 holds, and there exists such that . Then there exists an such that: and .

Both results are proved in Supplement S4. In the setting where and Assumption B1 does not hold, it may be reasonable in some settings to assign samples in the holdout set risk scores based on no data (for example risk scores generated entirely from expert opinion) and blind agents to holdout/intervention status. Under this setting we may have greater assurance in Assumption B1.

5 Estimation of OHS

5.1 Estimation of

We are aiming to find a holdout set size which minimises costs during an epoch , (noting that the holdout set will be used late in the epoch when ). This choice must be made during epoch (when ). We have the following:

-

1.

An approximate number of samples on which the model will be used or refitted;

-

2.

A cohort of samples with , , with small.

In 2 the samples are from a holdout set if , or from initial training data if . We aim to estimate the cost function at . Our approach is to estimate for and assume that the OHS is approximately conserved from to , though in reality drift may occur in .

At time , we need to estimate constants , , and the function . The constants and are straightforward: , the total number of samples on which a predictive score can be fitted or used, will usually be known or specified (item 1); and , the average cost per sample under baseline behaviour without a score, can be estimated from observed costs in the cohort in item 2. The function (Equation 10) is more difficult to estimate, as it involves quantifying costs of hypothetical risk scores. We may tractably estimate by assuming that

| (12) |

where is a risk score fitted to , is a measure of error, and is some nondecreasing function. We claim that in general circumstances we may take to be linear and to be expected mean-squared error (MSE) or a similar general loss. We derive this heuristically in Supplement S5 and derive expressions for directly in a specific case in Section 6.3. Once is known, this allows to be estimated readily by establishing the ‘learning curve’ of the risk score using item 2.

Some direct estimates of are necessary to determine . One option is to designate subcohorts of the intervention set in epoch to receive risk scores fitted to smaller subsamples of available training data, allowing direct observation of the costs of such risk scores. While simple, this approach may be ethically tenuous and expensive. Other options include estimating the function through expert opinion or other outside information.

In summary, we recommend that is estimated by jointly making a small number of estimates during epoch , either directly or indirectly, to establish , and thereafter estimated by evaluating the error of a risk score fitted to samples using the set in item 2 and transforming it according to the estimated .

5.2 Parametric estimation of OHS

A natural algorithm for estimating the OHS is immediately suggested by Theorem 4: assume is known up to parameters , and estimate , and to estimate the OHS. Parameters of may be estimated from observations of pairs , potentially with error in . To minimize the number of estimates of we iteratively add observations to an existing set of observations so as to greedily reduce expected error in the resultant OHS estimate.

We suggest a routine parametric algorithm (Algorithm 1) with estimation of asymptotic confidence intervals. Full details of theory, proofs and algorithms are given in Supplement S6.

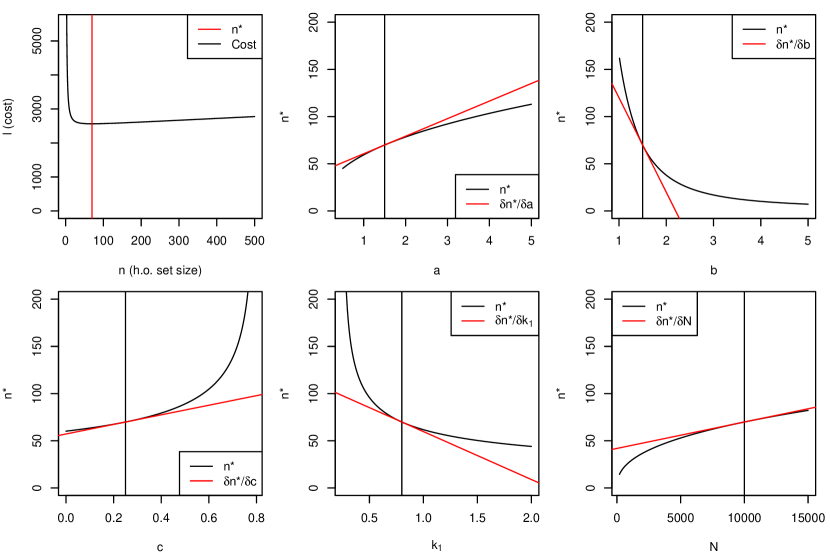

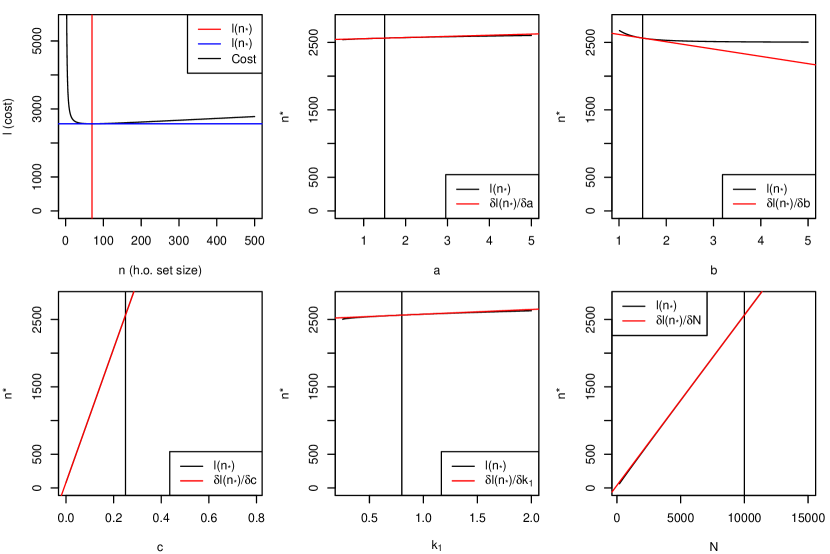

We use the shorthands and . Consistency of Algorithm 1 depends on whether eventually contains enough elements of sufficient multiplicity to estimate consistently. Sampling some positive proportion of values of randomly from guarantees that the multiplicity of all almost surely eventually exceeds any finite value, readily ensuring consistency. Finite-sample bias of depends on and the variance of . See Supplementary Figure 8 for typical forms of .

5.3 Semi-parametric (emulation) estimation of OHS

Parametrization of may be inappropriate if the learning curve of the risk score or the relation between the learning curve and (from Section 5.1) are complex (viering21). We propose a second algorithm which is less reliant on assuming a parametric form for , using Bayesian optimisation (brochu2010tutorial). We quantify the uncertainty in through the construction of a Gaussian process emulator of . The prior mean function for this emulator takes a particular parametric form, but crucially can deviate from this prior function with the addition of data.

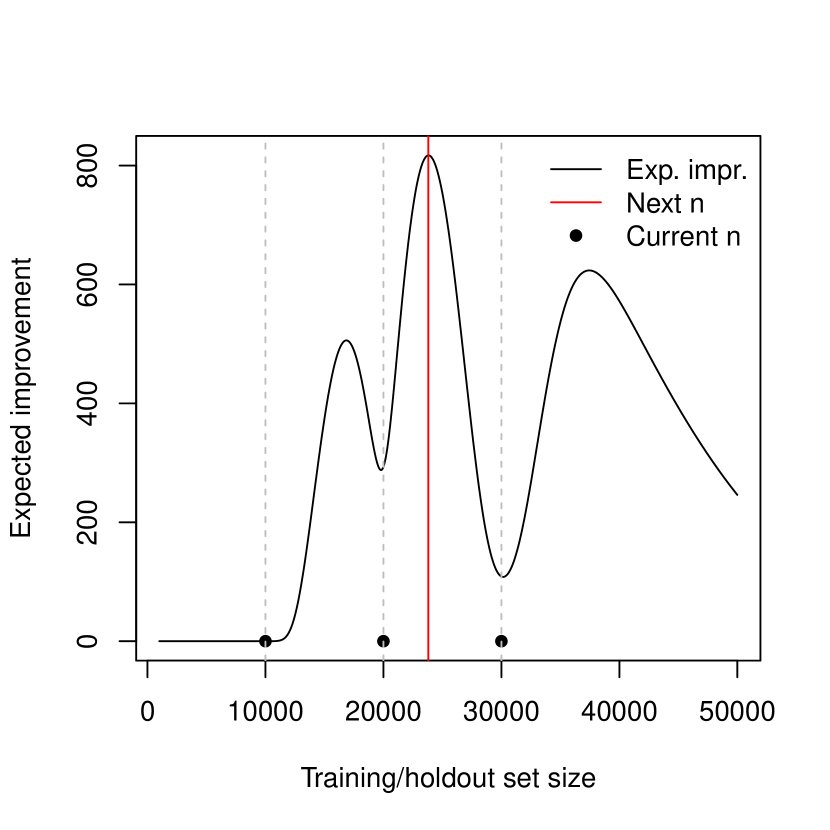

We take the corresponding to the minimum cost function value (for the evaluated points) to be our OHS estimate. Values of at which to estimate are selected using an ‘expected improvement’ function , whereby if we roughly expect the minimum cost to decrease by at least from adding another estimate of to our data. This also provides a natural stopping criterion. Our approximate procedure is given in Algorithm 2. Further algorithm details and proofs of consistency are in Supplement S7.

6 Simulations

6.1 Simulation showing dominance of holdout set approach

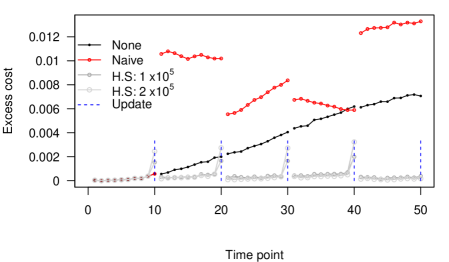

We briefly illustrate the theory described in Section 2.1 using simulated data, similar to our motivating example, which satisfiess Assumptions A1-A5, A7 and the weaker form of Assumption A6 (Equation 9) with , , , , , , and (details in Supplement S8.1). Figure 2 shows total costs accrued per sample during unit time periods of no-update (‘none’), naïve-update (‘naive’) and holdout-update (‘H.S’) at two holdout sizes over time. As drift occurs in , the costs associated with the no-update strategy increase due to increasingly poor approximation of , and the costs of the naïve-update strategy increase dramatically due to intervention effects. The total costs of the holdout-set approaches remain low. Choice of holdout set size aims to balance increased costs due to non-intervention in the holdout set (the ‘spikes’) against inaccuracy in fitted scores after drift. We demonstrate the natural emergence of an OHS in a simulated context in Supplement S8.2.

6.2 Comparison of parametric and emulation algorithms

In this section, we give circumstances in which one of Algorithms 1 or 2 may be preferable to the other. We consider two versions of the function :

where: ‘p’/‘np’ denote ‘parametric assumptions satisfied/not satisfied’, and . We assume and are known to be and respectively. For emulation, we use a kernel width and variance of .

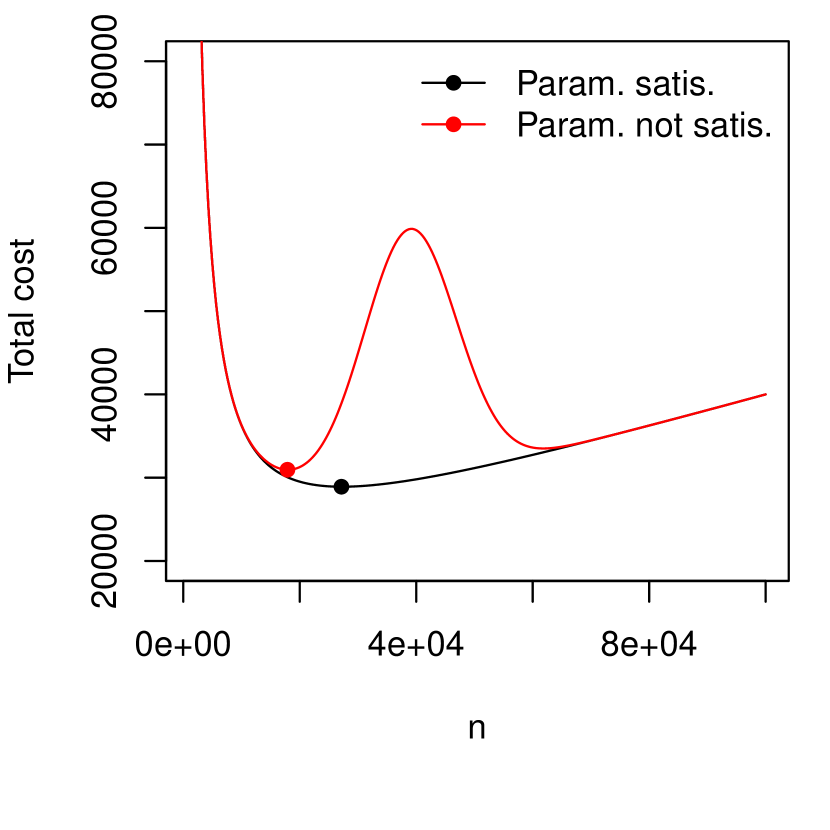

The function exhibits ‘double-descent’ behaviour (Supplementary Figures 11(a), 11(b)), which is possible for learning curves (viering21) but violates assumptions B2, B4.

We firstly show the distribution of estimates of OHS using both algorithms when takes either form above. To fit , we use 200 randomly chosen values from for , with values independently sampled as , where . Supplementary Figure 11(c) shows the distributions and medians of OHS estimates using the parametric and emulation algorithms in settings with parametric assumptions either satisfied or not.

The results confirm expectations that the parametric OHS estimate is empirically unbiased and has less variance than the emulation estimate when parametric assumptions are satisfied, but is biased when they are not. Variance of OHS estimates using the emulation method is lower when parametric assumptions are not satisfied, because the true cost function has a sharper minimum in that case (see Supplementary Figure 11(b)). Since the cost function is ‘flat’ around the minimum in the setting where parametric assumptions are satisfied (Supplementary Figure 11(b)), the consequences of the high variance of the semi-parametric (emulation) estimator are minimal, as the cost is similar across a range of values near the OHS.

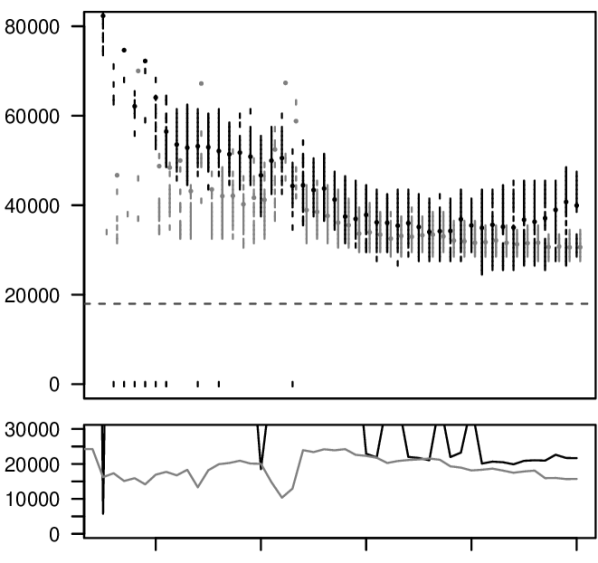

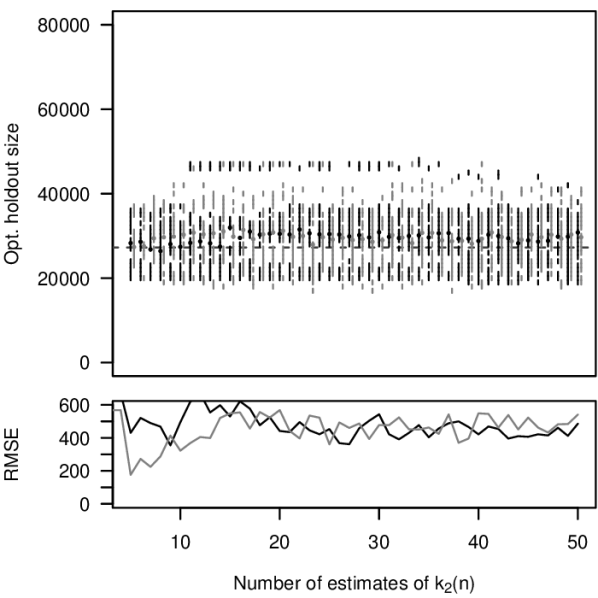

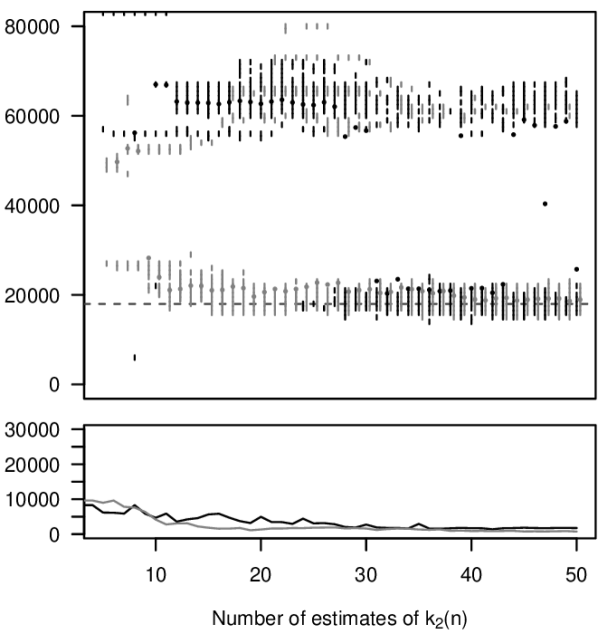

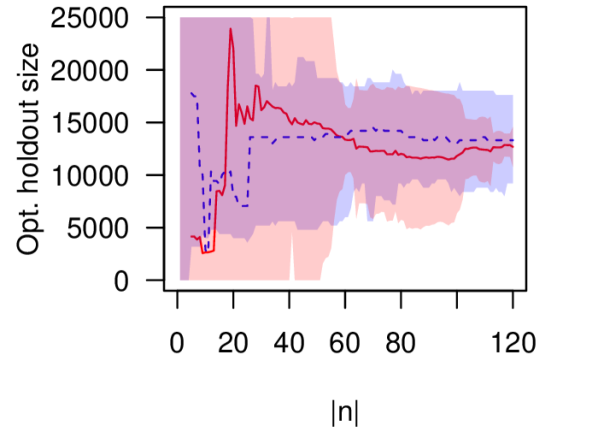

We next examine the convergence rates of OHS estimates when sampling the ‘next’ value of , , greedily, using Equation 68 for Algorithm 3 or for Algorithm 4, versus simply randomly selecting uniformly in . This is shown in Figure 4, which depicts medians and OHS estimates at various sizes of under the different methods for selecting .

Convergence is faster when next points are picked greedily rather than randomly and when using parametric estimates (though these are biased and inconsistent for ). This is highlighted by the smaller panels which show the root mean-square error between the total cost at the estimated optimal sizes and the total cost at the true OHS. In particular, observe that the non-parametric method shows bifurcation, detecting both local minima in the double descent setting, whilst the parametric method converges to a mid-point which is far from optimal in terms of total costs.

6.3 Illustration in realistic setting

We now return to the initial motivating example of Section 1.2. Supposing ASPRE is to be refitted every five years, the intervention set should include all individuals in the subsequent years before the model is refitted, and all individuals not used in the next refitting procedure. Suppose we refit ASPRE for use in a population of 5 million individuals, from which we have approximately 80,000 new pregnancies per year. The incidence of pregnancy per year is now so we have (SE ). We must now estimate and from published data. Although this method is not especially generalisable, and will generally be more easily estimable given raw data, which is not publicly available.

We presume a simple clinical action in which a fixed proportion of individuals at the highest assessed pre risk are treated with aspirin. We assume , the proportion of individuals assigned to the treatment group in rolnik17b due to having an estimated risk of pre . We assume that if untreated with aspirin, a proportion of individuals designated to be ‘low-risk’ (lowest 90%) will develop pre, as will a proportion of individuals designated high-risk.

To estimate , and ultimately , we considered the study reported in ogorman17 assessing sensitivity and specificity of NICE and ACOG guidelines in assessing pre risk. In this study, 8775 indivduals were assessed, amongst which 239 developed pre, for an overall incidence of . We estimated the performance of a ‘baseline’ estimator of pre risk (that is, in the absence of any ASPRE score) by linearly interpolating the points corresponding to ‘ACOG aspirin’, ‘NICE’ and ‘ACOG’ on ROC curves in Figure 1 of that paper. On this basis, a baseline estimator identifying the 10% of individuals at highest pre risk (approximately 800) would correspond to the point on the interpolated ROC curve with which occurs at roughly a 20% detection (true positive) rate and a 10% false positive rate, close to that of the NICE guidelines.

Since few women in the study were treated with aspirin, we assume that pre rates in the highest-10% and lowest-10% risk groups assessed by baseline risk (NICE) are untreated risk (that is, if not treated with aspirin). At the inferred true and false positive rates, we would expect a pre rate amongst the 10% of women designated highest-risk by the NICE guidelines and amongst the 90% designated lower risk, where

with standard errors and . We denote by the relative reduction in pre risk with aspirin treatment. Aspirin reduces pre risk to approximately (SE 0.09) of untreated risk (rolnik17) so we take . Now, treating errors in , and as pairwise independent, we have

| (13) |

with . We estimate the population prevalence of untreated pre as the frequency observed in the original ASPRE data: . Note that, although this is approximately equal to , they are different quantities: is the population frequency of pre amongst individuals at the lowest 90% risk by NICE guidelines.

Denoting as the untreated risk of pre in the top 10% of individuals according to an ASPRE score trained on individuals (and correspondingly), we note that it is equal to the sensitivity (or TPR) of the risk score at the level where proportion of individuals are designated high-risk. Thus for any training set size , we have so the average cost to an individual in the intervention set may be expressed in terms of :

We denote ‘cost’ as simply the number of cases of pre in a population, so total expected cost per individual under ‘baseline’ treatment (clinical actions without the aid of a risk model) is

| (14) |

with standard error approximately 0.001. Note that this is not equal to the untreated pre risk in the population, since some proportion of individuals are treated pre-emptively.

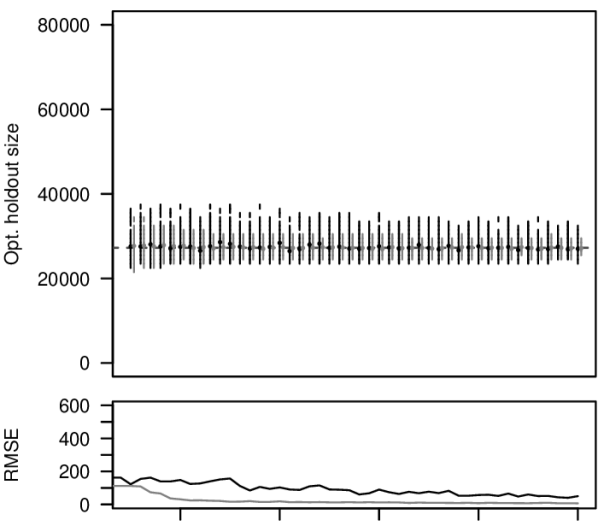

The data used to fit the initial ASPRE model could be used to estimate and hence for potential model updates. We do not have access to this dataset, but demonstrate estimation of a learning curve on synthetic data designed to resemble it. In this case, is easy and fast to estimate, and is well-approximated by a power law, so we would favour use of algorithm 3. In order to mimic a real example where such estimation is time consuming or costly we use both algorithms and restrict ourselves to use only values of , determined using either algorithm 3 or 4. For both algorithms, we assumed a power-law form .

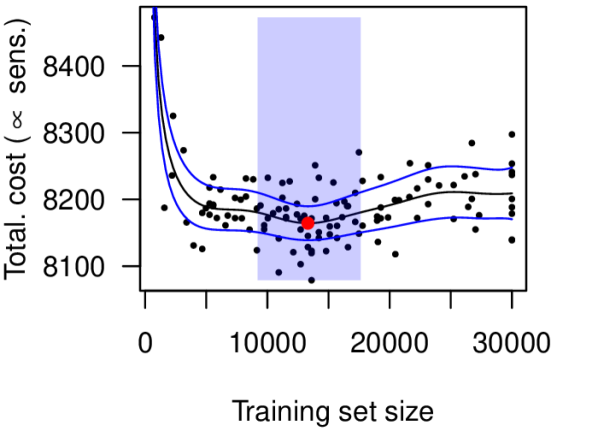

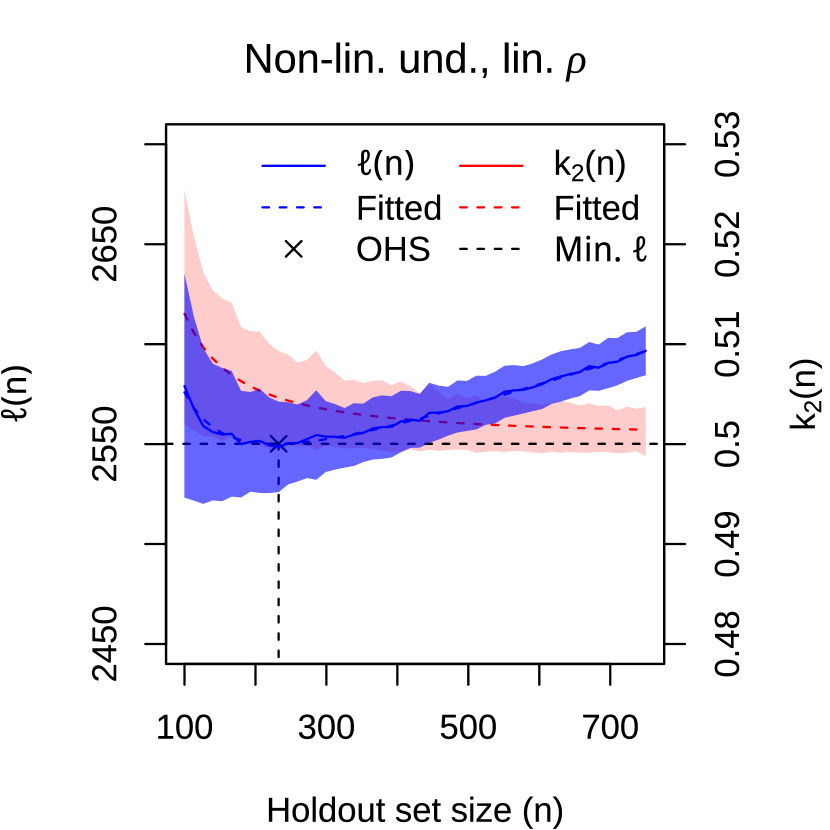

Using the parametric algorithm, we found an OHS of 10271 (90% CI 8103-12438), with minimum cost (expected cases over five years) of 8172. Using the emulation algorithm, we found an OHS of 13313 with an expected cost of 8164, with holdout sizes of 9210-17619 having a probability of cost . Figure 5 shows estimated cost functions, OHSs, and error using the two algorithms.

7 Concluding remarks

In this work we propose the use of a holdout set to safely update predictive models, and describe considerations in determining the optimal size of such a set. We establish theoretical properties of this optimal size under common conditions, and develop two algorithms for estimating it, evaluating their use in both a toy simulation and a real-life motivated simulation. The holdout set approach comprises a practical and simple approach to an important problem in practical applied statistical modelling and machine learning, which will be increasingly important as risk scores start to be used ever more routinely to prompt intervention in real-world applications.

An appealing alternative for managing the effects of intervention without holdout sets is to attempt to explicitly infer parameters of an underlying causal structure (alaa18; sperrin19). However, this approach cannot evade the difficulties we describe in Section 3: either we must be able to observe more detail (for instance, values of covariates after interventions which is often impractical) or make simplifying assumptions (such as absence of drift). In such relaxed settings, non-holdout-set options may allow a lower asymptotic and finite-sample cost than holdout set use. However, they will have higher asymptotic costs than holdout-set use in the more general setting considered here. A second potential non-holdout set option is to explicitly specify interventions which are to be made in response to risk scores, rather than leave them up to end-users (ochs19; liley21stacked), but in typical complex settings in which we wish to use risk scores, we may wish to retain the autonomy of end users in decision-making. Indeed, prescriptive risk score based interventions would cause a model to fall under medical device regulation in the United Kingdom, so many risk scores there are developed for information only.

Our methods may be extended in several ways. We do not consider the possibility of combining information over training iterations, which could reduce the number of training samples needed for a given prediction error. It is also possible that information from the intervention set could be used alongside the holdout set to partially infer the effect of interventions. We presume a setting in which a risk score is periodically updated, but continual or ‘online’ updating is also used (delange21) and is also susceptible to intervention effects. A holdout set approach may also be usable in this setting.

Our simulations and theoretical findings show several non-obvious properties of the optimal holdout set size. We note that if the mean square error of the risk score decreases as (Assumption A4), then the OHS increases as , with the immediate consequence that the OHS is a vanishing proportion of for large enough . Moreover, in practical settings, the true OHS is fairly small, with rapidly diminishing returns to increasing risk score accuracy (Section 6.3). Interestingly, as demonstrated in Supplement S8.2, a more accurate risk score does not necessarily lead to lower OHS size. Given Corollary 1 (and as seen in Figure 5(c)), it is generally better to err on a higher side of the optimal holdout set size, since cost increases at most linearly, whereas it can increase faster for smaller holdout sets.

We propose two algorithms for estimating an optimal size for a holdout set. The parametric method is simple and converges rapidly, but the use of a Gaussian process emulator requires fewer assumptions. We advise use of the emulator method if the risk score is fitted using complex methods which may not lead to readily parametrisable . A reasonable option if parametrisability of is uncertain is to use both estimation algorithms, and favour the emulation method if results disagree.

We strongly suggest planning an updating strategy for a risk model before it is deployed. This work illustrates one strategy in this direction and we hope stimulates both use of and extensions of such methods for safe predictive score updating.

Acknowledgements

The authors would like to thank the anonymous referees, an Associate Editor and the Editor for their constructive comments that improved the quality of this paper.

SH’s contributions arose from an MSc dissertation for the MISCADA programme at Durham University. We thank Catalina Vallejos, Sebastian Vollmer and Bilal Mateen for helpful discussion.

LJMA was partially supported by a Health Programme Fellowship at the Alan Turing Institute. JL and LJMA were partially supported by Wave 1 of The UKRI Strategic Priorities Fund under the EPSRC Grant EP/T001569/1, particularly the ‘Health’ theme within that grant and The Alan Turing Institute; and by Health Data Research UK, an initiative funded by UKRI, Department of Health and Social Care (England), the devolved administrations, and leading medical research charities; SRE is funded by the EPSRC doctoral training partnership at Durham University, grant reference EP/R513039/1.

References

Holdout sets for predictive model updating

Supplementary materials

Part I

S1 General notation

This supplement requires several sets of notation, which will be introduced as needed. However, we note some commonalities. Throughout this document we will take to generically mean ‘covariates’ and to mean ‘outcomes’. The subscript will be taken to mean ‘time’ in a continuous sense, and the subscript to mean ‘epoch’, referring to consecutive episodes of time. The superscript will correspond to the holdout set, and to the intervention set. The number will refer to the total number of samples on which a risk score may be trained or used during an epoch, and to denote a holdout set size, usually taken to be variable. We denote the standard normal PDF and CDF by , respectively, the Bernoulli distribution with parameter as , and the Poisson distribution with parameter as .

S2 Proofs of Theorems 1, 2 and 3

S2.1 Theorem 1

Theorem 1.

Proof.

We begin by establishing an inequality on the quantity

| (15) |

where and the expectation is over the data used to fit .

As in assumption A4, denote and note that, by assumption A3, we have

| (16) |

To establish an upper bound, we use (in order) assumptions A3, A2, inequality 16, and assumption A4. Taking these, along with noting that for any , we have:

| (17) |

In any period , the probability of at least samples being encountered in , given and , satisfies the (weak) condition:

| (18) |

Consider costs accrued in the period with , under the holdout strategy. We encounter some total number of samples . We assign at most samples to the holdout set, with a total cost of at most (as a consequence of Assumption A5). The remaining samples each accrue a cost proportional to 17, as long as at least samples were observed in . We thus have

| (19) | ||||

| (20) |

The total cost per unit time accrued over the total epochs is thus

| (21) |

∎

S2.2 Theorem 2

Theorem 2.

Proof.

We will begin with a simple lemma which we will use repeatedly:

Lemma S1.

If, for all , we have , then

Proof.

We secondly prove a short lemma to show that we need not consider the no-update strategy separately from the alternative strategy:

Proof.

We note that from assumption A1 we have

| (25) |

As , since , we have from assumption A4:

| (26) |

so for sufficiently large fixed we have (using Lemma S1)

| (27) |

where the expectation is also over data used to fit . Hence the no-update strategy is in the ‘alternative’ class of strategies, with for all .

∎

Recalling our definition of as

we simply choose any with , so for large enough , we have

| (28) | ||||

| (29) |

as required, establishing the theorem for and .

We now establish the rate of growth of the costs of the naive update strategy. The essential idea is

-

1.

We consider two consecutive time periods and , with .

-

2.

We introduce an ‘index’ value which is the similarity of the risk score used during period to the function governing risk at the start of that period.

-

3.

Given assumption A3, we establish that is not very different from with , so is similar to the difference between the risk score and the function throughout the period . We conclude that governs the total cost accrued during time period , in that the larger , the larger the total cost.

-

4.

We then consider the similarity between and during the period during which the risk score is fitted for use during period . Since the ‘cost’ (the difference between and ) and ‘inaccuracy’ (the difference between the risk score and ) are related by assumptions A5, A6, the difference between and is also governed by , with a larger corresponding to a smaller difference.

-

5.

Since (the risk score for use in time period is fitted to with , the similarity between and in this period is also the similarity between and the new risk score. We establish that is similar in time period and in time period , so the difference between and , and hence the difference between and the risk score is largely conserved. Since a small means a large difference between and for , it means a large difference between the risk score and for .

-

6.

Thus a small means a large cost in time period and a large means a large cost in . We show that there is a non-negligible cost accrued overall. When summed across all such time periods, this results in a contribution to overall cost.

When using the naive update strategy, the costs during the time period depend on the similarity between and during the time period . The risk score used during the time period under the naive update strategy is . We define

Note that this is not an expectation; we will show a bound on the accrued costs which does not depend on . Given assumption A3, we have, for (using a tighter bound than Lemma S1):

| (30) |

By similar arguments we have

For any in the time period , we have, by assumptions A6 and A5:

| (31) |

We now consider two cases.

Case 1.

for some

Conceptually, in this case, use of the risk score in fact makes the risk worse than would the use of no risk score at all at time . In this case, we have, by assumption:

so for any :

and the total expected cost accrued over the time period (during which we encounter samples) is:

| (32) | ||||

and for any we may choose dependent only on sufficiently small that

| (33) |

Case 2.

for all .

The risk score used during the period is . Denote . We now have:

| (34) |

We consider the expectation over the data used to fit to note that for , using Lemma S1:

For brevity, denote

| (35) |

Note that by choosing a large enough (and hence sufficiently small ) and a sufficiently small we may ensure is arbitrarily small.

The expected total cost accrued during the period (during which we encounter samples) is thus, from expression 30:

| (36) | ||||

where both expectations are over only the number of samples encountered. The total cost accrued during the period is, from expression 34

| (37) | ||||

and hence the total cost over both periods is

For any we may choose (dependent only on , , , ) sufficiently small that for large enough :

Recalling expression 33 for the earlier case, we denote

| (38) |

so, in either case:

We now finally consider the cost accrued over the entire time period , where . We have

as required.

∎

S2.3 Theorem 3

Theorem 3.

Proof.

We begin with the following lemma:

Lemma S3.

For sufficiently large :

| (39) |

Proof.

We employ assumptions A1 and A3. Firstly, we choose a (with existence guaranteed by assumption A1) for which . There must be some with such that

Let be a number satisfying

| (40) |

so and . We now have

∎

We firstly consider . We have, selecting a large enough that by Lemma S3, and recalling expressions 18 and 19:

| (41) |

We next consider and , recalling from Lemma S2 that we need only consider the latter. We note that

| (42) |

Recalling our definition of as

we choose any with , so for large enough , we have for small enough :

We next consider . We recall from expression 38 in the proof of Theorem 2 that for any we may choose (dependent only on , , , ) sufficiently small that for large enough we have:

where does not depend on . Thus, for sufficiently small :

| (43) | |||

as required.

∎

S2.4 Relaxation of assumption A6

Our assumption A6 is prescriptive, necessitating a strict relationship between a particular conception of ‘accuracy’ of the risk score (as measured by ) and the amount by which we can reduce in expectation (assumption A5).

We may substantially weaken assumption A6 and maintain our results, although the statement of Theorem 1 becomes a little more complex. We consider the alternative assumption (using the conventions for ‘upper’ and ‘lower’):

Assumption A6-alt.

Suppose a risk score is in use at time , and denote . We have

for some constants , and constants , satisfying .

along with a slight strengthening we will need for Theorem 3 (stating that cost must be determined by a function of , not merely bounded)

Assumption A6-add.

With , as per assumption Assumption A6-alt and as per assumption A5, we have , where is a continuous function.

and note the following:

Remark 1.

Suppose we replace A6 with Assumption A6-alt in the statement of theorems 1, 2 and 3. Then, replacing the statement of Theorem 1 with

then theorems 1 and 2 still hold. If we additionally make assumption Assumption A6-add, then the statement of Theorem 3 still holds, with an asymptotic growth rate of rather than for strategies , , .

Before proceeding to the proof, we note that in analogy to the main manuscript, we may specify an asymptotic optimal holdout size and corresponding cost in terms of , although this time we must allow dependency on .

For a fixed , a holdout set size of (regardless of ) will give an optimal asymptotic cost of

and if we choose

| (44) |

we may achieve an optimal growth rate (for sufficiently small ) of:

Proof.

Theorem 1. For Theorem 1 we proceed in the same way until expression 19, where we instead have (employing the observations that and for , since )

| (45) |

with a total cost per unit time accrued over the total epochs is thus

Theorem 2. To establish Theorem 2 for we pick up at equation 28 to instead note

For we begin by rephrasing equation 31 as

We must rework case 1; we now have, by assumption:

so for any :

and the total expected cost accrued over the time period (during which we encounter samples) is:

hence we may choose dependent only on sufficiently small that

| (46) |

for some positive constant .

For case 2, we again appeal to expression 30 to rewrite expression 36 (using the fact that since )

We may recalculate the final three lines of derivation 34 as:

| (47) |

and hence rewrite expression 37 as

and hence the total cost over both periods is

Analogous to the proof of Theorem 2, given , we may choose (dependent only on , , , ) sufficiently small that for large enough :

Recalling expression 46 for the earlier case, we denote

| (48) |

so, in either case:

and the proof proceeds as above.

Theorem 3. For Theorem 3, we must additionally make assumption Assumption A6-add, since without it there is no guarantee that costs of various strategies will be similar even if the associated risk scores are equally similar to .

We require a slightly modified form of Lemma S3; namely that for sufficiently large we have

which can proved in essentially the same way as the original lemma by first noting that since , we have

With this, we may trudge back to derivation 41, delete any occurrences of the constant , replace with , and replace any instances of with , and see that the derivation holds.

S3 Notes on ethics and alternative options

S3.1 Non-identifiability of from and

As in the main paper, suppose that we are a researcher at time , at which a risk score is in place, and we have at hand only a set of sample covariate values and values (or rather, samples from ). It is immediate that we cannot infer from this: we do not directly observe or values , and without further assumptions on the relationship between and , we cannot judge what is.

Intuitively, however, we may expect that will be similar to if we have little confidence in the risk score (and hence take little risk-score guided action) and will be different from if we are more confident that the risk score resembles . These intuitions are quantified by assumptions A5 and A6, in that we have:

| (50) |

We show in this section that this is (unsurprisingly) not enough to uniquely identify . Our construction is elementary, but somewhat laborious. Let be a function and consider the function as follows:

| (51) |

where

and all expectations are over . We note that

| (52) |

If we choose close to , we can ensure is small enough that

| (53) |

and hence and equation 51 has a root (call it ). Thus, for arbitrary close to , we can find an such that also satisfies

| (54) |

so is not distinguishable from , even with knowledge of , , and hence is not identifiable from alone.

S3.2 Use of natural hold-out sets and recorded interventions

Ethical objections to the use of holdout sets are in a sense due to the need to actively with-hold some samples from access to a risk score. A brief discussion is merited on potential use of ‘natural’ hold-out sets, in which some proportion of a population may be assumed to behave like a holdout set without actively requiring withholding of scores. We will use our motivating example (section 1.2) to illustrate this idea.

An obvious setting in which a natural holdout set would be appropriate is in the case where an effectively random subset of samples already do not have access to a risk score. In our example, this may comprise a set of individuals under the care of a medical practitioner who chose not to use the ASPRE score. As long as the distribution of covariates of such individuals is typical of the population distribution (that is, is conserved) and the behaviour of such practitioners is typical of the general behaviour of practitioners in the absence of a risk score (that is, is conserved) then such a subset of individuals can be used as a holdout set.

Other options may not be appropriate. In particular, we consider options for a setting in which the intervention is recorded (that is, whether an individual was given aspirin). The set of individuals for whom no intervention was recorded (that is, did not get prescribed aspirin) do not constitute a holdout set in our sense: the function measures the probability of an event under normal care without a risk score, and patients without a risk score may still get prescribed aspirin.

A more sophisticated option, which at first appears to be a panacea, involves explicitly considering probabilities of outcomes when aspiring is prescribed or not, and attempting to estimate directly. However, by careful analysis in a causal sense, and by introducing the idea of a ‘latent’ covariate (discussed in our previous paper, liley21updating) which contributes to risk but is not included in the risk model, we may show that this is generally impractical, or at least more difficult than it seems. For a more detailed analysis of this setting we refer the reader to sperrin19.

We presume we are working at a fixed time (that is, disregard dependence on ) and denote by a set of covariates included in a risk score, an indicator for whether aspirin was prescribed or not, a ‘latent’ covariate (taking values in for simplicity) which is not amongst covariates but influences the probability of an outcome, the event in question (in this case, the incidence of pre-eclampsia) and the event of whether the practitioner had access to a risk score ( for yes, for no). The random variables have the following left causal structure if and the right causal structure if :

in which are partly dependent on , the decision to prescribe aspirin is made based on and with the decision rule modulated by , and is dependent on , and . To reconcile with our earlier notation we have

assuming conditional independence of and given .

Changing from 0 to 1 perturbs the joint distribution of . If we begin by disregarding and assuming that depends deterministically only on and only on , we may expand as follows:

| (55) |

where conditional independence of and given arises because we may assume can affect only through the decision of whether to prescribe aspirin.

Expansion 55 suggests a straightforward procedure to estimate : although we do not directly observe the quantity , it could be readily estimated without with-holding any risk scores by (for exaple) surveying clinicians on their likely course of action should they see a patient with . The remaining quantity, , appears estimable from observations of

Unfortunately this is more difficult than it appears. Because is used exclusively to make a decision on , only one of the pairs will ever be observed, so one of the terms in expansion 55 will be inestimable from the data. If we were observing data in a setting with , this would not be a problem because the points which are never observed coincide exactly with those points for which . However, because the decision rule changes when changes from 0 to 1, when we will fail to observe some values of for which , and hence we cannot consistently estimate . This problem is alleviated if is chosen with some degree of randomness across all values of , although as our ability to estimate depends on this randomness, it must be substantial to be a workable solution.

If we do allow the presence of latent covariates , then we induce a dependence of on . To see this, we expand as follows:

| (56) |

and note that the second term varies with , since affects the distribution (conceptually, a risk score may increase the degree to which influences ). Unless we observe along with , we cannot infer this second quantity, and hence we cannot directly estimate .

S4 Proofs of Theorems 4, 5, and 6

Theorem 4.

Proof.

As discussed in the main manuscript, we may impose that

| (57) |

Since both and are positive and monotonically decreasing in , so is . Now

| (58) | ||||

| (59) | ||||

| (60) |

By assumption B3 in the main manuscript, , and, from equation 57, , so both terms in equation 60 are negative when and . When , the second term vanishes while the first one is positive, as by assumption B3 in the main manuscript. We thus have . By assumption, is smooth, so by Bolzano’s Theorem, there must exist at least one point for which , which is an extremum of .

We now prove that this extremum is unique and a minimum. First, by assumption B4 in the main manuscript, we may impose that

| (61) |

Taking the second derivative of

| (62) | ||||

| (63) |

and using equations 57 and 61, we see that is strictly positive, and, as a consequence, is monotonically increasing. Therefore, the extremum of at we found earlier is unique and, as , it is a minimum.

If , let . If , let be the closest natural number to either side of . From assumption B3 in the main manuscript, cannot be or . In both scenarios, this completes the proof.

∎

Lemma S4.

Suppose assumption 1 holds and there exists such that . Then .

Proof.

∎

We now have

Proof.

All that is needed to show that there exists a holdout set size where and . This will be the in assumption B5.

Theorem 6.

Suppose assumption B1 holds, and there exists such that . Then there exists an such that: and .

Proof.

S5 Estimation of

We argue in this section that can generally be a modelled as a linear function of expected mean squared error of the risk score. Suppose that we are interested in making predictions at a time . We consider a risk score which is an inexact approximation of (recalling the definition of from section 3 as the probability of given at time when no risk score is used). We will write , where indicates expectation over randomness in actual cost for a given sample with a given risk score, and a risk score fitted to samples .

If it is reasonable to assume that has a straightforward form in terms of , , then a corresponding form for may be immediate. For instance, if one of

holds, for some constants , , then will be linear in

| (64) |

respectively. As discussed in the main manuscript, this reduces the estimation of to estimating the ‘learning curve’ of a risk score, and expectations of risk score accuracy measures such as those above over and can be readily estimated for small given training samples .

In more general cases where simple forms of cannot be assumed, we claim that if is smooth in , we should generally expect to be approximately linear in the expected mean-square error of the risk score.

We work from the following heuristic:

For any given sample and a range of possible risk scores for that sample, the intervention taken will minimise the expected cost for the risk score which is unbiased.

This is equivalent to

| (65) |

for all in the domain of . We suppose firstly that is smooth in , and write

noting that by assumption.

The value represents the curvature with respect to of the function about . Practically, this corresponds to the tolerance or robustness of the intervention: the amount of cost incurred due to a given deviation of the risk score from . We claim that this quantity will thus have relatively low variation across values of , as the degree of robustness should be roughly constant.

Given this, we have

where , are independent of and , and is the standard mean-square error of . Hence

so is approximately linear in .

Suppose that we have a simple setting where we have a single intervention which we may use, which has a proportional effect on the risk of (that is, , with ). We intervene on a sample if their risk score exceeds a particular threshold . The cost function is now discontinuous, but we may simply derive the form of in terms of risk score performance.

We assume that the intervention has a fixed cost , and that an event has a fixed cost . Then

| (66) |

disregarding potential baseline costs common to all samples. We may now apply the heuristic above more directly, by presuming that the threshold is chosen so as to minimise the expectation of over under the assumption that . In other words, we choose the threshold that gives us the best outcome assuming the risk score is correct.

This implies that for , we have (if true risk is below the threshold, it is cheaper not to intervene) and for , we have (if true risk is above the threshold, it is cheaper to intervene).

We now have:

and, denoting and presuming exists and is finite, we have

where , , are constant, and readily estimated from several observations of . This form is unsurprising: if a risk score is such that the sign of agrees with the sign of , it will have identical cost to a risk score which agrees with everywhere.

S6 Parametric OHS estimation

In this section, we describe estimation of optimal holdout set sizes by explicit parametrisation of the function . As in section 5.2 in the main paper, we take . We will take , , to mean partial derivatives with respect to , and the shorthand and . We will also write , , and for brevity. We presume that is an unbiased estimate of , so corresponds to ‘true’ parameter values.

We firstly develop asymptotic confidence intervals for parametric OHS estimates to link error in parameter estimates to error in optimal size. The sample-size used in the following denotes a proxy for effort expended in estimating .

Theorem S7.

Assume that , and are continuous in and in some neighbourhood of , and that parametrizes a setting satisfying assumptions B1-B4. Suppose that behaves as a mean of of appropriately-distributed samples in satisfying in distribution where does not depend on , that an estimate of is available which is independent of and satisfies in distribution, and that is finite and unique as above. Then denoting

we may uniquely define and we have

in distribution, and denoting , the confidence intervals

satisfy and as .

The proof is given in Supplement S6.2 below. A consequence is that for sufficiently accurately estimated costs, the OHS will be a non-trivial size:

In light of the proportionality assumption in Section 5.1, and the tendency of the accuracy of a risk score with number of training samples (‘learning curve’) to follow a power-law form (viering21), we recommend considering such a parametric form for (i.e. with ), and provide explicit asymptotic confidence intervals for this setting in Supplement S6.1. Examples of variation in and with a power-law form for , are shown in Supplementary Figures 8, 9.