Optimal Spend Rate Estimation and Pacing

for Ad Campaigns with Budgets

Abstract

Online ad platforms offer budget management tools for advertisers that aim to maximize the number of conversions given a budget constraint. As the volume of impressions, conversion rates and prices vary over time, these budget management systems learn a spend plan (to find the optimal distribution of budget over time) and run a pacing algorithm which follows the spend plan.

This paper considers two models for impressions and competition that varies with time: a) an episodic model which exhibits stationarity in each episode, but each episode can be arbitrarily different from the next, and b) a model where the distributions of prices and values change slowly over time. We present the first learning theoretic guarantees on both the accuracy of spend plans and the resulting end-to-end budget management system. We present four main results: 1) for the episodic setting we give sample complexity bounds for the spend rate prediction problem: given samples from each episode, with high probability we have where is the optimal spend rate for the episode, is the estimate from our algorithm, 2) we extend the algorithm of Balseiro and Gur [12] to operate on varying, approximate spend rates and show that the resulting combined system of optimal spend rate estimation and online pacing algorithm for episodic settings has regret that vanishes in number of historic samples and the number of rounds , 3) for non-episodic but slowly-changing distributions we show that the same approach approximates the optimal bidding strategy up to a factor dependent on the rate-of-change of the distributions and 4) we provide experiments showing that our algorithm outperforms both static spend plans and non-pacing across a wide variety of settings.

1 Introduction

Online advertising is a massive industry worth around billion dollars in 2020 in the United States alone [37]. Advertisers bidding within large online platforms are usually constrained by budget, and must decide how to distribute this budget over time as the supply and demand of impressions change. For example, there are more users online during the day than at night, leading to a variable density of impressions opportunities (see e.g. Figure 1 in Liu and Hill [29]). Furthermore, users may be more likely to interact with an ad outside of working hours, leading to those impressions generating more value for advertisers (e.g. Table 2 in Liu and Hill [29]). Finally, competition for impressions may vary over the course of the day, as other advertisers may allocate more budget to high-value periods (e.g. Figures 2 and 3 in Agarwal et al. [3]).

The temporal effects have led to a variety of work on constructing spend plans for a campaign which learn how to distribute a budget over time [30, 2, 3, 28]. Generally, the approach taken in these works is twofold: first, they use some model (e.g. a high dimensional time series model) to forecast the number of impression opportunities over the course of a day. This is taken as the spend plan. Secondly, they use a pacing algorithm, which tries to match the empirical spend rate to the spend plan. Lee et al. [28] modify the bid to control spend, while Agarwal et al. [3] modify their participation probability to control spend.

There are several limitations to the above approaches. First, they model the density of impression opportunities assuming that value per user and price per user is roughly constant. Considerable evidence [29, 3] refutes this assumption, suggesting that conversion rates and prices change over time. Second, their work focuses on empirical rather than theoretical results, limiting our understanding about which settings we can predict the resulting algorithms to have good performance. This motivates the problem that we study in this paper: Can we identify non-stationary settings for which we can provably learn a spend plan that approximates the optimal distribution of budget, and where the end-to-end system provably performs well?

More formally: We study the problem of computing optimal spend plans from a learning-theoretic perspective in two settings: an episodic model, and a model in which price and value distributions change smoothly over time. For the first, we consider an advertiser with budget that participates in a sequence of single-item second-price auctions, called rounds. These auctions are divided into episodes of rounds111We assume equal sized episodes to simplify the presentation of the paper. Our results can be generalized to different sized episodes where the size of episodes can also be estimated.. Each episode has a fixed product distribution , with values for and independently prices in . Prices and values within an episode are i.i.d., while prices and values across episodes are independently, but not identically, distributed. Let be the average spend per round of a strategy spending budget over rounds. For all , and denote the probability density functions (pdf) of distributions and respectively. Second, we consider a non-episodic setting, where all distributions are guaranteed to change smoothly: each round has a product distribution with the property that , and for all .

For both settings, we ask: First, can we accurately estimate an optimal spend allocation? Second, given an (approximately) optimal spend plan, can we implement a pacing algorithm that satisfies the budget constraint and achieves vanishing regret compared to the ex-post optimal?

1.1 Main Contributions

Our main contributions are as follows.

-

•

Episodic Setting. We propose a pair of algorithms 1) ApproxSpendRate, an offline algorithm that estimates the optimal spend plan on samples, and 2) EpisodicAdaptivePacing, an online algorithm that adaptively follows the spend plan over new auctions, that jointly have regret vanishing in and , compared to the best bidding strategy in hindsight. The formal statement appears as Theorem 25 in Section 4 and relies on the following additional results:

-

–

Estimating Optimal Spend Plan. In Section 3 we bound the accuracy of constructing of an optimal spend plan. We give an algorithm ApproxSpendRate, that given samples from each episode, with probability at least , produces a spend plan that satisfies where is the optimal spend rate for the episode, is the estimate from our algorithm and is the number of episodes.

-

–

Online Pacing Algorithm on Spend Plan. In Section 4 we then give an adaptive pacing algorithm EpisodicAdaptivePacing that takes an (approximately accurate) spend plan, and implements a bidding strategy that follows this spend plan over new auctions. The regret of this algorithm vanishes in and with respect to the best bidding strategy in hindsight.

-

–

-

•

Slow-moving Distributions. In Section 5, for slow-moving distributions we learn a spend plan as if the data came from an episodic model with number of episodes . The end-to-end performance achieves a constant factor approximation of the to the best bidding strategy in hindsight, where the constant factor depends on the rate at which the distributions change.

-

•

Experimental Evidence. Finally, in Section 6 we present experiments where we compare the performance of our method to the Balseiro and Gur [11] algorithm (which neither estimates nor uses a spend plan as it was designed for adversarial and stationary settings). Our method compares favorably to the ex-post optimal strategy and outperforms other methods in a wide variety of settings.

1.2 Related Work

Optimal Spend Rate Estimation.

There are number of works that aim to estimate optimal spend rates for budget pacing [30, 2, 3, 28]. Ma et al. [30] and Agarwal et al. [2] primarily focus on the on the spend plan estimation. Both of these papers aim to forecast user visits, which correlates strongly with the number of impression opportunities. They do this using time series modeling techniques for users within the targeting criteria of a campaign. These works do not attempt to estimate how conversion rates or prices for ad opportunities change over time. Lee et al. [28] and Agarwal et al. [3] combine user visit estimates with an online pacing algorithm to match the spend rate to the user visit rate. Similar to the approaches below, Lee et al. [28] uses a multiplicative shading strategy (i.e. bidding instead of ) to control spend, while Agarwal et al. [3] participate in each auction with a parameterized probability to control spend. None of these papers give formal guarantees on the performance of the end-to-end budget management system.

Online Algorithms for Pacing. Work on pacing algorithms has only focused on guarantees for pacing algorithms in absence of a spend plan. In many cases, for repeated second-price auctions, the optimal pacing strategy in hindsight is a multiplicative shading strategy (i.e. bidding for the auction at time for a fixed that does not vary over time) [36, 20, 24, 12, 16]. Balseiro and Gur [12] were the first to give online learning algorithms that approximate this best response. For i.i.d. value and price distributions, they give an online algorithm with regret . Similar guarantees are also shown by Balseiro et al. [10] who achieve regret for stationary value and price distributions setting without assuming independence between values and prices. There are few works that give provable guarantees for non-stationary competition and values. Balseiro and Gur [12] consider the case of adversarial values and prices and show that no algorithm can achieve sub-linear regret with respect to any benchmark that obtains more than fraction of the utility obtained by using the optimal strategy with the power of hindsight (where is an upper bound on the value). They also give an algorithm which obtains the upper bound on the regret with respect to fraction of the optimal. Balseiro et al. [10] considers both an ergodic setting and a periodic setting where regret grows as . Their algorithms do not construct a spend plan and instead rely on the fact that at a macro-level the expected optimal spend rate is constant. By contrast, in our setting obtaining no-regret may depend on saving enough budget for the end of the campaign (for example to reach users on the weekend for a week-long campaign). Only by explicitly constructing an approximately optimal spend plan can one give guarantees for such campaigns.

Conitzer et al. [17] show that for individual first-price single-item auctions, multiplicative shading yields the Eisenberg-Gale outcome of the corresponding Fisher market (though generally multiplicative shading is not a best response in this setting). Gao et al. [22] give an online learning algorithm for this setting that results in this equilibrium and can be run in a decentralized way by each advertiser individually.

While bid modification yields the an optimal strategy for a bidder, an alternative way to respect a budget constraint is to limit the number of auctions a bidder participates in. Mehta et al. [32] give revenue guarantees for the online matching problem where users (in this case, impressions for sale) arrive one at a time and the auction selects a winner who pays their bid; once a bidder has exhausted their budget they will no longer be selected as a winner. Subsequently bidder selection has been applied to more general settings [1, 6, 23, 27]. Since truthful bidding is not a best response for advertisers in bidder selection mechanisms, this line of work is less directly relevant to our work.

In the previous two lines of work, advertisers know the value they have for an impression when they bid. A separate line of work considers a bandit setting, where the value is only revealed to advertisers after they win an auction. Amin et al. [4] and Tran-Thanh et al. [38] give theoretical guarantees for discrete value distributions. Flajolet and Jaillet [21] extend these results to continuous distributions. Finally, Nuara et al. [33] and Avadhanula et al. [5] consider the problem of allocating budget across different channels. The different channels have different distributions and as such bear some similarity to the setting we consider. However, since all channels are simultaneous available and each channel is i.i.d., the spend rate remains constant over time (cf. our setting where spend rates change).

Equilibrium Analysis

In addition to the work on online algorithms, there’s a growing body of work that analyzes the equilibria of pacing systems under the assumption that all advertisers use the same bid-shading approach, e.g. [14, 13, 8, 16, 17, 7, 15]. The framework of Balseiro et al. [9] studies stationary equilibria and characterize Bayesian optimal mechanisms that satisfy budget constraints.

2 Setting and Preliminaries

We study the problem of designing a bidding algorithm for budget-constrained advertisers in non-stationary settings. This bidding algorithm aims to maximize utility subject to a given budget constraint . The algorithm participates in a sequence of single-item second-price auctions222Our model captures additional settings, including posted prices and second-price auctions with reserve prices, but for ease of exposition we consider second-price auctions throughout.. We refer to each auction as a round. In the following we present the notation for the episodic setting that we study, the non-episodic setting is formally introduced in Section 5.

In every round , the bidder observes a value for the impression opportunity333 could capture the value that the advertiser has for a conversion times the probability of a conversion of the impression opportunity. The latter may depend on context like the user or a search query and is estimated by the platform. and submits a bid to the auctioneer. Let be the highest competing bid for the impression opportunity. When the bidder wins, spends , and gains utility . Otherwise she loses, pays , and gains utility . The bidder’s goal is to maximize their utility subject to the sum of expenditures across rounds being at most .

A strategy of the bidder is a sequence of deterministic444While all of our algorithms are deterministic, the lower bound in Lemma 8 can be extended to randomized mappings as well. For ease of exposition, our algorithms use only deterministic strategies. mappings where uses the information that is available to bidder in round to produce bid . We focus attention on strategies that respect the budget constraint.

Definition 1 (Budget-feasibly Strategy).

is budget feasible if for any realized values and prices .

A strategy’s utility is simply its total utility over rounds.

Definition 2 (Performance of a Strategy).

For a given budget feasible strategy , it’s performance on a realized sequence of values and prices is given by

| (1) |

As benchmark, we consider the best (fractional) allocation in hindsight on the realized values and prices . While the benchmark may appear to be strong, it is commonly used in the budget pacing literature.

Definition 3 (Hindsight Strategy Benchmark).

The performance of the hindsight strategy on a realized sequence of values and prices is given by

Here represents a fractional allocation of impression opportunities. We measure the regret of a strategy compared to the benchmark in expectation over the values and prices. We use the notion of -regret proposed by [26], a multiplicative notion:

Definition 4 (-regret).

For strategy and , the -regret with respect to the hindsight strategy is:

Where the expectation is over sampled from , that is, in episode is sampled from .Our algorithm first constructs a spend plan prior to the auctions, using historical data. The accuracy of the spend plan will be a function of the sample size our algorithm is given.

Definition 5 (Sample Complexity).

The sample complexity of achieving a given approximation factor is the minimum number of samples such that there exists an (offline) learning algorithm with the desired approximation.

Of particular interest are algorithms where both the -regret is sublinear in , and additionally, approaches using a polynomial number of samples. We overload the term “vanishing regret” for such situations.

Definition 6 (Vanishing Regret).

A strategy (which has access to samples from ) has vanishing regret if and .

2.1 Outline of the Solution

As mentioned previously, our algorithm first produces a spend plan from data, then uses a pacing algorithm to meet that spend plan. The former is an offline learning problem that happens before the campaign starts. The latter is an online algorithm that operates on the spend plan and realized expenditures. Before going into these components, it is informative to understand why this decomposition in a spend plan and pacing algorithm makes sense.

Why Historical Data is Needed.

Balseiro et al. [9] have studied pacing for non-stationary distributions without using historical data. Could the episodic setting that we’re studying be amenable to positive results without historical data too? Unfortunately this is not the case. The following is an example with two episodes for deterministic algorithms. We generalize the example in the lemma that follows.

Example 7.

Consider two instances of the episodic setting characterized by the episodic distributions, and (where ). All the distributions consist of a single atom: prices distributions and yield with probability . The value generated by is , by is and by is .

Consider a buyer with budget , thus they can buy precisely half the impression opportunities. In both instances, the first episode yields utility per round that is won, but the second episode differs for the two instances. For , the per-round utility when the bidder wins is , while for it is .

So if the bidder faces the first instance, she needs to win all but a sublinear (in ) number of rounds in episode 1 for vanishing regret, but if she faces the second instance she may win at most a sublinear number of rounds in the first episode. Since she doesn’t know which instance she faces until she enters episode 2, any strategy must incur regret on at least one of , .

The example above can be generalized to a stronger result for instances with more episodes and that includes randomized algorithms.

Lemma 8.

Any strategy that only depends on the history in round , for a large enough , and budget such that , for any number of episodes , for any such that , there exists an instance of the episodic setting with distributions such that

Proof.

In an adversarial setting where the values and prices are arbitrary, in each round , Balseiro and Gur [12, Theorem 1] show that for any strategy such that depends only on the history , for a large enough , for any budget satisfying where is the upper bound on the values, for any such that , there exists adversarial values and such that .

Note that if then truthful bidding is feasible and achieves the optimal utility. When , then the above result says that there exists a barrier of such that for any strategy that only depends on the history, there always exists an instance where cannot obtain better than fraction of the optimal utility. In other words, if the budget constraint is active, the lower the budget, the smaller the fraction of the optimal budget constrained utility the advertiser can hope to attain.

Since we don’t make any assumptions about how distributions are related across the episodes, we can extend the analysis and the adversarial case example of Balseiro and Gur [12, Theorem 1] to work in the episodic setting and show that similar lower bounds can be shown for such strategies in our setting as well. Specifically, in the proof of Balseiro and Gur [12, Theorem 1], the adversarial example has the value fixed as for all rounds, and the price profile is samples from a distribution such that the round auction is divided into episodes. When , then by setting in the proof for Balseiro and Gur [12, Theorem 1], we can recover the guarantee that there exists an instance such that for . If , then the complete example is scaled down by replacing with . Note that since , we have that , thus the example is valid. We also get that . Thus, we obtain that for . ∎

Since algorithms in the episodic setting that only operate on the immediate history fail to have vanishing regret, we use access to historical data in the form of samples from the distribution.

Why Spend Plans are Needed.

With access to samples from the distribution, one could still attempt to design an algorithm that does not involve a spend plan. Recall from the related work that ex-post the optimal bidding strategy is to bid for some constant . So what if we used samples to estimate this and used this directly? The following lemma shows that this yields linear regret with constant probability.

Lemma 9.

There exists an instance of the episodic setting with distributions such that the ex-ante optimal pacing multiplier incurs regret with probability at least .

Proof.

Let and such that the prices drawn from in episode 1 are equal to some positive constant and the prices drawn from in episode is equal to such . The values drawn from are with probability and are equal to with the remaining probability for some constant . The values drawn from in the second episode is always equal to such that .

Consider the episodic setting defined by distribution and budget . In episode , most of the impressions have no value but with a small probability, we might observe high value and expensive impressions. In the episode , every impression is cheap and high value.

The corresponding ex-ante optimal pacing multiplier in this case is . The pacing strategy derived from always bids . In expectation, wins all impressions in episode each with utility , and wins impression of utility resulting in expected utility of .

Although the expected utility is high, but in the realized case, if more than one impression of value and price is present in episode , then the fixed pacing strategy wins both these impressions with depletes the complete budget, leaving no budget for episode 2 and a total utility . When compared to the Hindsight strategy , the hindsight strategy always ends up buying all the impressions in second episode and thus gets utility .

Thus, if at least two impressions with positive utility appear in episode , the regret is equal to which is . The probability that at least two positive utility impressions appear in episode is which is greater than for .

This implies that with probability at least , ∎

Instead we construct an intermediate spend plan and combine this with an adaptive pacing algorithm; an approach we outline next.

Outline of the Solution using Spend Plans.

To understand the optimal spend plan, we first introduce the notation of spend functions which represent the expected expenditure of strategies that shade by a fixed shading multiplier.

Definition 10 (Spend Function).

Consider a fixed pacing strategy that always bids and is not restricted by any budget constraints. The expected expenditure of in a single round in episode is

| (2) | ||||

| (3) |

Definition 11 (Optimal Spend Rates).

Given an episodic setting where the ex-post optimal bidding strategy is to bid , we define as optimal spend rates if for all , , where .

In simpler words, the optimal spend plan is characterized by the optimal spend rates , such that the is equal to expected expenditure of the ex post optimal bidding strategy in a single round in episode . We define the dual of the expectation of the optimization problem in Definition 3 as

| (4) |

The ex-post optimal bidding strategy bids where is the dual minimizer (), which spends the complete budget in expectation:

| (5) |

where are the optimal spend rates. Refer to Appendix A for a detailed exposition about the characterization of the optimal spend rates through the dual of the problem. Knowing the optimal spend rates can help decompose the entire campaign into smaller budget constrained campaigns for each episode where the distributions of values and prices remain stationary. The exact formulation of optimal spend rates requires complete knowledge of the distributions which is not available, instead we have access to historic samples from the distribution . This is reasonable to assume as we are designing this framework for large online ad exchanges which usually have access to a lot of historical data. Our solution is is a two step pipeline:

-

1.

1. Approximate optimal spend rates: Use historical samples from to approximate optimal spend rates as .

-

2.

2. Adaptive pacing with spend rates: Use the approximate spend rates to construct an online pacing algorithm that runs on realized impressions.

2.2 Preliminaries

We will use some results on uniform convergence and pacing for i.i.d. settings in this paper.

2.2.1 Dvoretzky-Kiefer-Wolfowitz (DKW) Inequality

The Dvoretzky-Kiefer-Wolfowitz (DKW) inequality [19, 31] gives a uniform convergence bound on the empirical cumulative distribution function.

Lemma 12 (DKW Inequality).

Given samples from a distribution . The empirical cdf on the samples is given by . With probability at least

2.2.2 Kernel Density Estimation

While the DKW inequality 12 gives strong uniform convergence bounds on the cdf of a distribution, bounding the probability density function (pdf) of a distribution is more challenging. A common approach to do this is to use Kernel Density Estimation (KDE) [18, 35]. Let be the distribution with pdf that we want to estimate as . Formally the Kernel Density Estimation is defined below for scalar distributions which we use in our setting.

Definition 13 (Kernel Density Estimation).

Given a kernel , scalar , and samples from the distribution , the KDE is given by

While most results on KDE are for bounding the mean squared error (), recent work by Jiang [25] gives a uniform convergence guarantee for KDE. We present a simplified version of their result below.

Lemma 14 ([25]).

If is Lipschitz and bounded i.e. there exists a constant such that for and for some constant , then there exists a constant (that depends on , , , and some other constants), such that with probability at least and by setting , the kernel density estimate satisfies that

provided that is spherically symmetric, non-increasing, and has exponential decay (i.e. where is a non decreasing function s.t. for all , for some fixed , , and )

A number of popular kernel choices such that Gaussian, exponential, uniform, and many more satisfy the requirements of lemma 14. While the Lipschitz requirement appears strong, a large number of common distributions such as the normal distribution, Cauchy distribution, exponential distributions and lognormal distributions have Lipschitz and bounded pdfs.

2.2.3 Balseiro-Gur Pacing Algorithm

Consider a setting with just one episode such that the values and prices in every round are sampled from fixed stationary distributions and . Balseiro and Gur [12] give an adaptive pacing algorithm based on minimizing the dual . In every round , the algorithm bids and the pacing parameter is updated using a projected gradient decent style update in the direction that minimizes the dual.

3 Approximating Optimal Spend Rates

We first turn our attention to estimating optimal spend plans in the episodic setting. Given samples from , we will divide our budget across episodes by estimating target spend rates that approximate the optimal spend rates additively. The main theorem we’ll prove in this section is the following.

Theorem 16.

Given , , , sample oracles and , where is Lipschitz and bounded, sampling budget , , setting , w.p. , for each episode , ApproxSpendRate returns s.t.

ApproxSpendRate (Algorithm 1) is based on the fact that the ex-post optimal bidding strategy spends the complete budget in expectation. The resulting algorithm consists of three main steps: i) use historical samples to approximate spend functions for each episode as , ii) use eq. 5 to approximate as , and iii) estimate the expected spend per round for each episode using the approximate spend functions and .

Before we discuss how to approximate the spend functions , in Lemma 17 we show that a good approximation of allows for a good approximation of the optimal spend rates .

Lemma 17.

In Algorithm 1, for each episode if the estimated episodic spend function obtained the end of Line 15 satisfies , then for each , the algorithm returns spend rate such that .

Proof.

The proof progresses in two steps: First, we show that the episodic guarantee in the premise of the lemma yields a bound for the overall spend function. Next, we show that the approximate spend functions when evaluated on yield provable bounds on the resulting episodic spend rates, where is the optimal pacing parameter learned using the estimated overall spend function.

First note that the episodic bounds yield a bound on the overall spend function ).

| (6) | ||||

| (7) | ||||

| (8) | ||||

| (9) |

Where eq. 6 follows from the definition of and eq. 30, eq. 7 follow from the triangle inequality, and eq. 8 follows from the fact that . Since this holds for arbitrary , this implies that .

Using eq. 31, and the formulation of the algorithm, we know that , and eq. 9 implies . Combining the two, we get

It can easily be shown that for any episode , is a monotonically decreasing function in . Consider , since all values and prices are non-negative, for any and , .

So there are two possible case, 1) or .

Consider Case 1) i.e. , then

| (10) | ||||

| (11) |

Where eq. 10 and eq. 11 follow from the monotonicity of and . Similarly, using the other direction for the case , we get that for every ,

Now consider for some ,

Thus, for all , it holds that . ∎

3.1 Approximating spend functions

Recall from Definition 10 that for an episode with value distribution and price distribution , \useshortskip

This implies that if we can approximate and , we can use eq. 3 to approximate . In algorithm 2, we use the empirical estimate of , and use Kernel Density Estimation to approximate as .

The estimate of the spend function satisfies the following uniform convergence bound.

Lemma 18.

Given samples from and (where is Lipschitz and bounded), setting ApproxSpendSP (Algorithm 2) returns the approximate episodic spend function such that with probability at least it holds that

Proof.

Consider any , with probability at least ,

where the first and second inequality follow from triangle inequality. For the third step, we use the PDF and CDF concentration bounds, and the fact for any , .

Here notation hides the terms along with constants like , from lemma 14 and . ∎

Combining the results of results of Lemma 17 and Lemma 18 completes the proof of Theorem 16. theorem 16 implies that using historical samples, we can approximate the optimal spend rates up to an additive factor that goes down at the rate of . In section 3.2, we show that in a simpler setting with constant prices, we can obtain a tighter error bound that goes down at the rate of .

3.2 Tighter results for Constant Prices

We consider a simpler setting where within an episode the price per impression is fixed as and only the value is sampled from distribution . For the setting where all prices in episode are , the spend function (Definition 10) simplifies to:

To estimate we only need to estimate ; we give the procedure ApproxSpendFP in Algorithm 3. The concentration guarantees for follow from a straightforward application of the DKW inequality (Lemma 12).

Lemma 19.

Given value samples from and price , ApproxSpendFP (Algorithm 3) returns the approximate episodic spend function such that with probability at least it holds that

Proof.

Combining the results of results of lemma 19 and Lemma 17, we can show a tighter analogue of theorem 16 for the constant price setting.

Theorem 20.

Given an episodic setting with fixed prices and parameters , , , sampling oracles , sampling budget , , with probability at least , for each episode , by replacing ApproxSpendSP (algorithm 2) with ApproxSpendFP (algorithm 3) (at Line 7), ApproxSpendRate (algorithm 1) returns spend rate such that:

4 Pacing using Approximate Spend Rates

Now that we have learned the spend rates, in this section we show how we can adapt the Adaptive Pacing Algorithm of [12] to work with changing spend rates which approximate the optimal spend rates.

The main idea is that using our learned spend rates, we can efficiently divide the budget across the episodes and then within each episode, we work with the budget assigned to us, and use the adaptive pacing algorithm of Balseiro and Gur [12] as subroutine. We present this algorithm as EpisodicAdaptivePacing (Algorithm 4), a detailed version of which appears as Algorithm 7 in Appendix B.

At the beginning of the campaign, we instantiate an overall budget Budget as the total budget of the campaign and an episodic budget for the first episode. The budget for each episode is limited ahead of time and if algorithm runs out of the episodic budget , then it cannot buy more item in this episode, even though it may have leftover budget for the whole campaign. The intuition behind this is that the budget assigned to each episode is based on the (approximation of) the optimal spend rate. If there is left over budget after an episode ends, then the budget is simply carried forward to the next episode.

In each episode, the adaptive pacing algorithm tries to match the spend in each round to target spend rate of that round. Intuitively the algorithm works by taking the equivalent of a Stochastic Gradient Descent step in the direction of the negative of the gradient of the Lagrangian of that episode. Note that here the Lagrangian dual /average Lagrangian dual for each episode is different as is characterised by the budget for that episode. We can now show that if the spend rate estimates are good, then the resulting strategy has vanishing regret.

Definition 21 (Admissible Distributions).

Joint distribution such that the dual function is thrice differentiable in for all and with bounded gradients and is strongly convex, where price distribution is atomic with all mass on , or is Lipschitz and bounded.

Lemma 22.

To prove the lemma, we need the following additional result:

Lemma 23.

If , it holds that

where .

Proof.

Let the optimizer of be . We know that the optimizer of is . Note that since , using monotonicity of the spend functions, Consider

∎

Proof of Lemma 22.

Let’s assume we divide the budget into budgets for all episodes . This results in an online budget constraint bid pacing problem for each individual episode. Let denote the episodic dual function for episode when the budget for episode is . Similar to spend functions, if the budget allocation is optimal, that is , we can decompose the dual across episodes by using episodic dual functions .

| (12) | ||||

| (13) | ||||

| (14) | ||||

| (15) | ||||

| (16) |

Equation 13 follows from Equation 31; and Equation 16 follows from the definition of . Thus is the dual for the episode when the budget for the episode is .

Let . Using KKT conditions, similar to Equation 5, we can show that if for all , then for all

Thus satisfies the KKT conditions for as well. This furthermore implies that is an optimizer for . This results in the following conclusion:

| (17) |

This implies that if the budget allocation across each episode is , i.e optimal, then the optimal value of the dual can be obtained by optimizing the dual of each of the episode.

Let the strategy obtained by using our techniques be called . uses spend rates in each episode and assigns budget according to these rates. Once the budget has been divided, the behaviour of in each episodes is independent of the other episodes. Hence we can divide the utility obtained by across the episodes, i.e. .

Where and is the strategy induced by on episode by limiting the budget for as .

Thus is just the adaptive pacing strategy given in Balseiro and Gur [12], being run for episode with spend rate . Since things are i.i.d within the episode, we can directly use the results of [12]. The corresponding dual induced by the episodic sub-problem with budget is

The expected utility of in episode is given by . We use a corollary of Lemma 15 which implies that by fixing the budget for episode as , using , we have

We know show that if the estimates are good, the optimal of the episodic dual with budget is not too less compared to optimal episodic dual when the budget of the episode is . Using Lemma 23, for an episode

Summing over all rounds and using Equation 17 we get,

Using weak duality (Equation 27), we have

∎

Putting Everything Together.

The final missing component is that the spend rate estimator yields an additive guarantee, while the pacing algorithm expects a multiplicative guarantee. We give a transformation for the the spend plan in Algorithm 5. Lemma 24 shows that this yields the multiplicative guarantee.

Lemma 24.

Given spend rates such that for all , then for all .

Proof.

We can now restate our main result formally, which follows from Lemma 19, Lemma 18, Lemma 22, and Lemma 24.

Theorem 25 (Main Theorem).

5 Slow-moving Distributions

In this section, we consider a setting where the value and price distributions changes at every time step. In this setting, we still consider an advertiser with budget who participates in auctions. Each round has a product distribution , where is the distribution over impression value and over the highest competing bid . Thus, the round setting is characterized by distribution . We consider settings where this distribution changes slowly over time.

Definition 26 (slow-moving distribution).

A round campaign distribution is called slow moving if for all , we have \useshortskip

| (20) |

Even though the value and price distributions change in every round, since is slow moving, we can generate approximately accurate spend plans by treating ranges of auctions as episodes. While the distribution in these episodes aren’t stationary, the learned spend plan is approximately accurate as the distribution is slow-moving.

Definition 27 (Admissible Moving Distributions).

Joint distribution s.t. it satisfies definition 21 and for any rounds and that fall in the same episode, the spend function is strongly monotone, i.e. for some constant .

As per definition 10, the average spend function for rounds in episode can be given as and for the ex-post optimal bidding strategy of bidding , we have

| (21) |

where are the optimal spend rates. The accuracy of the spend plan now depends on the choice for and parameters and that capture how fast the distribution is changing.

Lemma 28.

Given , , sampling oracles and such that is slow moving, number of episodes to break into , , , then with probability at least , using algorithm 6, in Line 4, ApproxSpendRate (algorithm 1) returns spend rates such that for every episode ,

provided is Lipschitz and bounded by setting .

Proof.

Consider . For any round belonging to episode , we have

| (22) |

Similarly, for any round belonging to episode we have

| (23) |

Let be the empirical cdf obtained using samples from . Using the DKW inequality (Lemma 12), with probability at least , we have . Similarly, let be the kernel density estimate of obtained using samples. Using Lemma 14, with probability at least , we have . Combining the concentration results with eq. 22 and eq. 23, we that that with probability at least , for all episodes

| (24) |

Consider the episodic spend function induced by and as . For all episodes , with probability at least , we have

where the first, second, and third inequality follow from triangle inequality. For the fourth step, we use eq. 24 and the fact for any , . Using Lemma 17, we get that for all , with probability at least , we have .

∎

Now that we have approximate spend rates, we can use the estimates to divide the budget across the smaller episodes and use EpisodicAdaptivePacing (Algorithm 4) to perform online pacing. Combining all the guarantees, we can show the following main result for this setting.

Theorem 29.

Theorem 29 is implied by combining lemma 28, lemma 24, and lemma 22. Theorem 29 implies our results for the episodic setting can be extended to obtain results for more general settings. We can also observe that in this case, the in doesn’t converge to as grows, since the nonstationarity within an episode does not decrease with more samples.

6 Experiments

In this section we give empirical evidence that our end-to-end pipeline of optimal spend rate estimation and online pacing provides noticeable benefits over episode-blind pacing schedules and truthful bidding in a variety of synthetic environments.

Datasets.

We create synthetic datasets to test the performance of the algorithms under consideration. For the values, we consider three distributions: uniform, normal, and lognormal. For the prices, we consider three settings: fixed prices (our analysis focuses on this setting before generalizing), normally distributed prices, and the max of multiple draws from a lognormal distribution.555Prior work, e.g. [34], suggest that bids in ad auctions typically follow a lognormal distribution. The combination of lognormal values with max-of-lognormal-draws as prices is a realistic simulation of auction environment which is captured in the lognorn_v_maxlognorm_p dataset. We combine these into synthetic datasets, see Table 1. We divide the time horizon into 10 episodes, i.e. with differing parameters of distributions for each episode and use .

| Data set | Value distributions | Price distributions |

|---|---|---|

| uniform_v_fix_p | Uniform dist over | Fixed price |

| normal_v_fix_p | Fixed price | |

| lognorm_v_fix_p | Fixed price | |

| uniform_v_normal_p | Uniform dist over | |

| normal_v_normal_p | ||

| lognorn_v_maxlognorm_p |

6.1 Learning Accurate Spend Plans

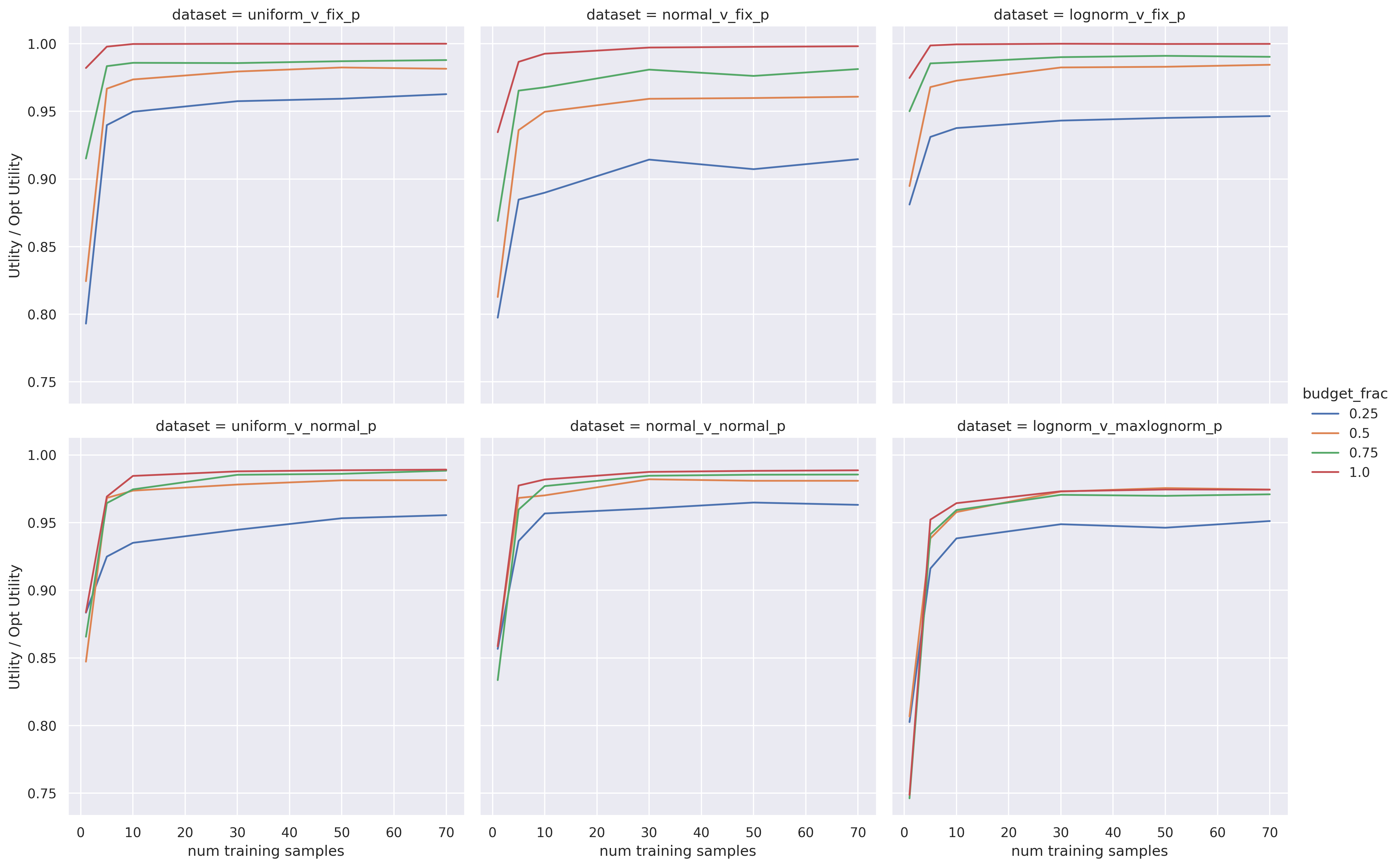

To understand how the performance of our end-to-end pacing is dependent on the numbers of samples available in the spend plan estimation phase, we plot the ratio of the optimal utility that the pacing system is able to obtain as a function of the number of training samples in Figure 1. We consider 4 different budget levels: let be the expenditure of the campaign that bids their value in each auction, we consider budgets for .

Figure 1 shows the effect of varying the training set size, where a sample in the training set corresponds to a value and price draw from each episode. Two things are clear from the results: 1) with increasing samples, the performance improves quickly, and 2) the budget level is important for the overall performance as the optimal budget allocation problem gets harder for smaller budgets. This is in agreement with the theoretical results of the pacing system obtained in Theorem theorem 25. Finally, it does appear that the performance hits a plateau. This is likely due to the online part of the algorithm which does not scale with increased offline learning sample size.

6.2 End-to-end Performance

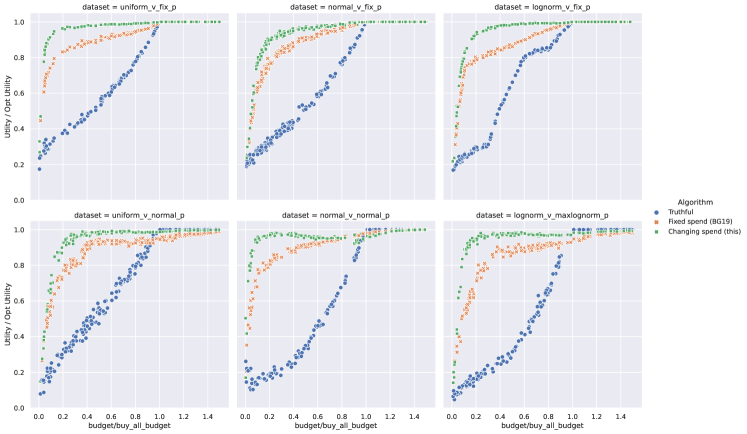

Algorithms. We compare the performance of 1) our algorithm, 2) constant spend rate [12] (which uses a linear cumulative expenditure over the duration of the campaign, and gives us an understanding of the benefit of estimating spend rates when competition is time-varying), and 3) no pacing (which enters the advertiser’s value in each auction until they run out of budget).

Results. The values and prices were generated in the same way as above. For each dataset, we run simulations where we a budget for the campaign is drawn uniformly from , where is the expenditure of the campaign that bids truthfully in each auction. Then we run all the pacing algorithms for this dataset sample and budget level. We repeat this process 150 times to get 150 data points per dataset for each algorithm. We plot the ratio of the optimal utility that the pacing system is able to obtain as a function of the budget level in Figure 2. Our algorithm outperforms both benchmarks almost everywhere. The only time where the “Truthful” benchmark performs better are in situations where the advertiser has enough budget to buy (almost) all impressions. There is one area where “Fixed spend (BG19)” outperforms our algorithm. It happens for the “normal_v_normal_p” dataset when ; we do not have an explanation why this particular range performs poorly.

References

- Abrams et al. [2008] Zoö Abrams, S Sathiya Keerthi, Ofer Mendelevitch, and John A Tomlin. Ad delivery with budgeted advertisers: A comprehensive lp approach. Journal of Electronic Commerce Research, 9(1), 2008.

- Agarwal et al. [2010] Deepak Agarwal, Datong Chen, Long-ji Lin, Jayavel Shanmugasundaram, and Erik Vee. Forecasting high-dimensional data. In Proceedings of the 2010 ACM SIGMOD International Conference on Management of data, pages 1003–1012, 2010.

- Agarwal et al. [2014] Deepak Agarwal, Souvik Ghosh, Kai Wei, and Siyu You. Budget pacing for targeted online advertisements at linkedin. In Proceedings of the 20th ACM SIGKDD international conference on Knowledge discovery and data mining, pages 1613–1619, 2014.

- Amin et al. [2012] Kareem Amin, Michael Kearns, Peter Key, and Anton Schwaighofer. Budget optimization for sponsored search: Censored learning in mdps. arXiv preprint arXiv:1210.4847, 2012.

- Avadhanula et al. [2020] Vashist Avadhanula, Riccardo Colini-Baldeschi, Stefano Leonardi, Karthik Abinav Sankararaman, and Okke Schrijvers. Stochastic bandits for multi-platform budget optimization in online advertising. In The World Wide Web Conference, 2020.

- Azar et al. [2009] Yossi Azar, Benjamin Birnbaum, Anna R. Karlin, and C. Thach Nguyen. On revenue maximization in second-price ad auctions. In Amos Fiat and Peter Sanders, editors, Algorithms - ESA 2009, pages 155–166, Berlin, Heidelberg, 2009. Springer Berlin Heidelberg. ISBN 978-3-642-04128-0.

- Babaioff et al. [2020] Moshe Babaioff, Richard Cole, Jason Hartline, Nicole Immorlica, and Brendan Lucier. Non-quasi-linear agents in quasi-linear mechanisms. arXiv preprint arXiv:2012.02893, 2020.

- Balseiro et al. [2017] Santiago Balseiro, Anthony Kim, Mohammad Mahdian, and Vahab Mirrokni. Budget management strategies in repeated auctions. In Proceedings of the 26th International World Wide Web Conference, Perth, Australia, 2017.

- Balseiro et al. [2020a] Santiago Balseiro, Anthony Kim, Mohammad Mahdian, and Vahab Mirrokni. Budget-constrained incentive compatibility for stationary mechanisms. In Proceedings of the 21st ACM Conference on Economics and Computation, pages 607–608, 2020a.

- Balseiro et al. [2020b] Santiago Balseiro, Haihao Lu, and Vahab Mirrokni. Dual mirror descent for online allocation problems. In International Conference on Machine Learning, pages 613–628. PMLR, 2020b.

- Balseiro and Gur [2017] Santiago R. Balseiro and Yonatan Gur. Learning in repeated auctions with budgets: Regret minimization and equilibrium. In Proceedings of the 2017 ACM Conference on Economics and Computation, EC ’17, pages 609–609, New York, NY, USA, 2017. ACM. ISBN 978-1-4503-4527-9. doi: 10.1145/3033274.3084088. URL http://doi.acm.org/10.1145/3033274.3084088.

- Balseiro and Gur [2019] Santiago R Balseiro and Yonatan Gur. Learning in repeated auctions with budgets: Regret minimization and equilibrium. Management Science, 65(9):3952–3968, 2019.

- Borgs et al. [2007] Christian Borgs, Jennifer Chayes, Nicole Immorlica, Kamal Jain, Omid Etesami, and Mohammad Mahdian. Dynamics of bid optimization in online advertisement auctions. In Proceedings of the 16th international conference on World Wide Web, 2007.

- Cary et al. [2007] Matthew Cary, Aparna Das, Benjamin Edelman, Ioannis Giotis, Kurtis Heimerl, Anna R. Karlin, Claire Mathieu, and Michael Schwarz. Greedy bidding strategies for keyword auctions. In Jeffrey K. MacKie-Mason, David C. Parkes, and Paul Resnick, editors, EC, pages 262–271. ACM, 2007. ISBN 978-1-59593-653-0. URL http://dblp.uni-trier.de/db/conf/sigecom/sigecom2007.html#CaryDEGHKMS07.

- Chen et al. [2021] Xi Chen, Christian Kroer, and Rachitesh Kumar. The complexity of pacing for second-price auctions, 2021.

- Conitzer et al. [2018] Vincent Conitzer, Christian Kroer, Eric Sodomka, and Nicolas E. Stier-Moses. Multiplicative pacing equilibria in auction markets. In Conference on Web and Internet Economics (WINE’18), Oxford, UK, 2018.

- Conitzer et al. [2019] Vincent Conitzer, Christian Kroer, Debmalya Panigrahi, Okke Schrijvers, Eric Sodomka, Nicolas E. Stier-Moses, and Chris Wilkens. Pacing equilibrium in first-price auction markets. In Proceedings of the 2019 ACM Conference on Economics and Computation, EC ’19, pages 587–587, New York, NY, USA, 2019. ACM. ISBN 978-1-4503-6792-9. doi: 10.1145/3328526.3329600. URL http://doi.acm.org/10.1145/3328526.3329600.

- Davis et al. [2011] Richard A Davis, Keh-Shin Lii, and Dimitris N Politis. Remarks on some nonparametric estimates of a density function. In Selected Works of Murray Rosenblatt, pages 95–100. Springer, 2011.

- Dvoretzky et al. [1956] Aryeh Dvoretzky, Jack Kiefer, and Jacob Wolfowitz. Asymptotic minimax character of the sample distribution function and of the classical multinomial estimator. The Annals of Mathematical Statistics, pages 642–669, 1956.

- Feldman et al. [2007] Jon Feldman, S Muthukrishnan, Martin Pal, and Cliff Stein. Budget optimization in search-based advertising auctions. In Proceedings of the 8th ACM conference on Electronic commerce, 2007.

- Flajolet and Jaillet [2017] Arthur Flajolet and Patrick Jaillet. Real-time bidding with side information. In Proceedings of the 31st International Conference on Neural Information Processing Systems, pages 5168–5178. Curran Associates Inc., 2017.

- Gao et al. [2021] Yuan Gao, Christian Kroer, and Alex Peysakhovich. Online market equilibrium with application to fair division, 2021.

- Goel et al. [2010] Ashish Goel, Mohammad Mahdian, Hamid Nazerzadeh, and Amin Saberi. Advertisement allocation for generalized second-pricing schemes. Oper. Res. Lett., 38(6):571–576, November 2010. ISSN 0167-6377. doi: 10.1016/j.orl.2010.09.002. URL http://dx.doi.org/10.1016/j.orl.2010.09.002.

- Hosanagar and Cherepanov [2008] Kartik Hosanagar and Vadim Cherepanov. Optimal bidding in stochastic budget constrained slot auctions. In Proceedings 9th ACM Conference on Electronic Commerce (EC-2008), Chicago, IL, USA, June 8-12, 2008, page 20, 2008. doi: 10.1145/1386790.1386794. URL http://doi.acm.org/10.1145/1386790.1386794.

- Jiang [2017] Heinrich Jiang. Uniform convergence rates for kernel density estimation. In International Conference on Machine Learning, pages 1694–1703. PMLR, 2017.

- Kakade et al. [2009] Sham M Kakade, Adam Tauman Kalai, and Katrina Ligett. Playing games with approximation algorithms. SIAM Journal on Computing, 39(3):1088–1106, 2009.

- Karande et al. [2013] Chinmay Karande, Aranyak Mehta, and Ramakrishnan Srikant. Optimizing budget constrained spend in search advertising. In Proceedings of the Sixth ACM International Conference on Web Search and Data Mining, WSDM ’13, pages 697–706, New York, NY, USA, 2013. ACM. ISBN 978-1-4503-1869-3. doi: 10.1145/2433396.2433483. URL http://doi.acm.org/10.1145/2433396.2433483.

- Lee et al. [2013] Kuang-Chih Lee, Ali Jalali, and Ali Dasdan. Real time bid optimization with smooth budget delivery in online advertising. In Proceedings of the Seventh International Workshop on Data Mining for Online Advertising, pages 1–9, 2013.

- Liu and Hill [2020] Jia Liu and Shawndra Hill. Moment marketing: Measuring dynamics in cross-channel ad effectiveness. Available at SSRN 3670024, 2020.

- Ma et al. [2019] Xiaoyang Ma, Lan Zhang, Lan Xu, Zhicheng Liu, Ge Chen, Zhili Xiao, Yang Wang, and Zhengtao Wu. Large-scale user visits understanding and forecasting with deep spatial-temporal tensor factorization framework. In Proceedings of the 25th ACM SIGKDD International Conference on Knowledge Discovery & Data Mining, pages 2403–2411, 2019.

- Massart [1990] Pascal Massart. The tight constant in the dvoretzky-kiefer-wolfowitz inequality. The annals of Probability, pages 1269–1283, 1990.

- Mehta et al. [2007] Aranyak Mehta, Amin Saberi, Umesh Vazirani, and Vijay Vazirani. Adwords and generalized online matching. Journal of the ACM (JACM), 54(5), 2007.

- Nuara et al. [2020] Alessandro Nuara, Francesco Trovò, Nicola Gatti, and Marcello Restelli. Online joint bid/daily budget optimization of internet advertising campaigns, 2020.

- Ostrovsky and Schwarz [2011] Michael Ostrovsky and Michael Schwarz. Reserve prices in internet advertising auctions: A field experiment. In Proceedings of the 12th ACM conference on Electronic commerce, pages 59–60, 2011.

- Parzen [1962] Emanuel Parzen. On estimation of a probability density function and mode. The annals of mathematical statistics, 33(3):1065–1076, 1962.

- Rusmevichientong and Williamson [2006] Paat Rusmevichientong and David P. Williamson. An adaptive algorithm for selecting profitable keywords for search-based advertising services. In Proceedings 7th ACM Conference on Electronic Commerce (EC-2006), Ann Arbor, Michigan, USA, June 11-15, 2006, pages 260–269, 2006. doi: 10.1145/1134707.1134736. URL http://doi.acm.org/10.1145/1134707.1134736.

- Statista [2020] Statista. Online advertising revenue in the united states from 2000 to 2020, 2020. https://www.statista.com/statistics/183816/us-online-advertising-revenue-since-2000/.

- Tran-Thanh et al. [2012] Long Tran-Thanh, Archie Chapman, Alex Rogers, and Nicholas R Jennings. Knapsack based optimal policies for budget–limited multi–armed bandits. In Twenty-Sixth AAAI Conference on Artificial Intelligence, 2012.

Appendix A Characterizing the optimal pacing strategy and budget allocation in expectation

Recalling that the optimal strategy on the realized values and prices is obtained by the hindsight strategy (definition 3). The Lagrangian dual of the optimization problem in definition 3 is given by:

| (L(KP)) | (25) | ||||

Where we define to be . The dual is obtained from the Lagrangian by setting for all such that , i.e. winning all impressions with value greater than times the price which can be done by bidding .

By weak duality, we have

| (26) |

Since and are being sampled from the fixed distribution defined by , taking expectation over equation 26 and using Jensen’s inequality, we get

| (27) |

Let and be the minimizer of . Assuming to be differentiable, using Karush-Kuhn-Tucker conditions, we have , , and . If , it implies that we are effectively not constrained by the budget and truthful bidding achieves the optimal utility in expectation as it wins all items with positive utility.

The gradient of can be written as

where

We call the overall spend function. By definition, is the expected expenditure over all the rounds when buying all items such that , obtained by bidding . The KKT complementary slackness condition implies that if , then i.e.

| (28) |

This implies that the strategy with a fixed pacing multiplier that bids achieves better expected utility than the expected utility of the hindsight strategy . If truthful bidding is not optimal (i.e ), then the expected expenditure of this strategy is . Not that the expenditure guarantee for the optimal fixed shading strategy is only satisfied in expectation, i.e. it spends budget in expectation.

For the rest of the theoretical claims, we restrict ourselves to the case that . The case implies that the budget constraint is not binding, so truthful bidding is the optimal strategy. Our algorithm will naturally adapt to this setting as well.

Let be the average spend in each round (over the whole campaign) if we buy all items such that . Equation 28 implies that for the optimal dual variable

| (29) |

Using Definition 10, . is the expected spend per round in an episode if the dual variable is , corresponding to the strategy which bids by multiplicatively shading the value by a factor of and ends up buying all the impressions in the episode with value per unit spent at least . In our framework, the spend function can be decomposed across the episodes by introducing episodic spend functions. We show this decomposition below:

| (30) | ||||

where is the episodic spend function. This definition helps us to define the optimal budget allocation as where is the optimal spend rate for episode given by . Note that if , using Equation 5, we have

| (31) |

Appendix B Detailed Algorithms

B.1 EpisodicAdaptivePacing: Adaptive pacing using a spend plan

We present ApproxSpendRate (Algorithm 1) which uses historical data to compute approximately optimal spend rates from samples.

For each episode , the subroutine ApproxSpendSP (Algorithm 2) estimates the episodic spend function as a function of using the historic samples and . For fixed prices, we use a simpler episodic spend prediction function estimate ApproxSpendFP (Algorithm 3). Both functions try to estimate and return an empirical approximate of we denote as .

Then using the structure of overall average spend function , (Equation 30), we can construct an approximation of the overall average spend function as . Based on our discussion about the optimal structure of the problem, for optimal dual variable , we know that (Equation 5). Using our empirical estimate , we compute , an empirical estimate of . We can compose our approximations to form , an approximation to .