A PDE-Based Analysis of the Symmetric Two-Armed Bernoulli Bandit

Abstract.

This work addresses a version of the two-armed Bernoulli bandit problem where the sum of the means of the arms is one (the symmetric two-armed Bernoulli bandit). In a regime where the gap between these means goes to zero as the number of prediction periods approaches infinity, i.e., the difficulty of detecting the gap increases as the sample size increases, we obtain the leading order terms of the minmax optimal regret and pseudoregret for this problem by associating each of them with a solution of a linear heat equation. Our results improve upon the previously known results; specifically, we explicitly compute these leading order terms in three different scaling regimes for the gap. Additionally, we obtain new non-asymptotic bounds for any given time horizon. Although optimal player strategies are not known for more general bandit problems, there is significant interest in considering how regret accumulates under specific player strategies, even when they are not known to be optimal. We expect that the methods of this paper should be useful in settings of that type.

1. Introduction

The multi-armed bandit is a classic sequential prediction problem. At each round, the predictor (player) selects a probability distribution from a finite collection of distributions (arms) with the goal of minimizing the difference (regret) between the player’s rewards sampled from the selected arms and the rewards of the best performing arm at the final round. The player’s choice of the arm and the reward sampled from that arm in that round are revealed to the player, and this prediction process is repeated until the final round.

Since the rewards of the arms that are not sampled are not revealed to the player, this is an incomplete information problem. This leads to a principal challenge in devising player strategies for multi-armed bandits: balancing exploration of different arms with the exploitation of the information gathered during the earlier periods. However, in the case of a two-armed Bernoulli bandit where the arms are distributed symmetrically, i.e., each arm is distributed independently according to a Bernoulli distribution and the sum of the means of the arms is one (symmetric two-armed Bernoulli bandit), this challenge is not present. In this case, sampling from one arm is statistically equivalent to sampling from the other arm.

The optimal player strategy in this setting is, perhaps, not difficult to guess; but we appear to be the first to give a proof of its optimality in the minimax setting. Also, even in this simplified setting, the incomplete information aspect of the problem is remains, and the optimal regret has not been determined previously. Accordingly, we develop a fresh PDE-based perspective on the symmetric two-armed Bernoulli bandit problem and apply it to determine the leading order term of optimal regret when the gap between these means of the arms goes to zero as the number of prediction periods approaches infinity, i.e., the difficulty of detecting the gap increases as the sample size increases.

Although optimal player strategies are not known for most other bandit problems, there is significant interest in considering how regret accumulates under specific player strategies, even when they are not known to be optimal. We expect that the methods of this paper should be useful in settings of that type. Accordingly our primary algorithmic contribution is a methodological advance, which augments the toolkit one can bring to bear on any bandit problem once the (potentially suboptimal) player’s strategy has been fixed.

Stochastic bandits can be viewed as an interaction between an “adversary” that sets the distributions of the arms at the start of the game and the player who plays according to a specific strategy. In the simplified setting of the symmetric two-armed bandit, our methods allow us to obtain a rather complete understanding of how the regret achieved by the optimal player strategy depends on (a) the number of time steps, and (b) the gap between the means of the two arms. Although the power of our “adversary” is restricted to setting the gap between the arms, there appears to be essentially no method in the literature that allows one to evaluate the regret corresponding to various gap regimes except for the fixed gap and the gap that scales as where is the number of prediction periods. Our methods allow for the first time to determine the leading order behavior of the regret in all other scaling regimes for the gap.

While the case of general bandits is more challenging, since the player needs to balance exploration and exploitation, there are more realistic settings than the symmetric two-armed bandit in which exploration is not needed.111One may ask if bandit-type problems that do not require exploration should be categorized as “bandits”. The incomplete information aspect of the problems described in the paragraph accompanying this footnote led to highly nontrivial algorithmic questions despite the lack of exploration. Accordingly, consistently with those references we shall also refer to the present simplified problem as a “bandit” problem. For example, reference [feldman] considered a Bayesian two-armed bandit where each arm is distributed according to an arbitrary probability distribution; the special feature of that problem is that both distributions are known to the player, although the player does not know which distribution is associated with each arm. This reference showed that the optimal player in that setting is myopic. Reference [rodman] further showed that the myopic player is optimal in the Bayesian -armed bandit setting where the player knows that one arm has distribution (but does not know which arm) and all the other arms have the same distribution (different from ).222See also reference [zaborskis] that showed the same result restricted to Bernoulli distributions. One important application of the problem described in the previous sentence is that it leads to lower bounds for the general -armed bandit, where the player has no special information about the arms.333See, e.g., Theorem 3.5 in reference [bubeck_book].

The minimax optimal regret and pseudoregret we determine in the symmetric two-armed bandit setting lead to new regret and pseudoregret lower bounds in the general two-armed bandit setting. Existing nonasymptotic lower bounds rely on information theory, in particular Pinsker’s inequality, to bound below the (pseudo)regret in certain symmetric bandit problems, which lead to lower bounds in the general bandit problems. (We further discuss these lower bounds later in this section.) Our results lead to new nonasymptotic lower bounds established without appealing to information theory in the two-armed setting. We hope that our methods will make progress towards better lower bounds in general -armed bandit problems.

Let refer to a pair of distributions (arms) where arm (the safe arm) is assigned with probability and with probability independently from the other arm and the history, and the other arm (the risky arm) is assigned with probability and with probability also independently. This work studies the following problem.

We denote the time by nonpositive integers such that the starting time is and the final time is zero. This convention is convenient because it will lead to the relevant value functions of the game being dependent on instead of had we set the starting time to 0 and the final time to .

Although the identities of the safe and risky arms are never revealed to the player, the player knows that the distribution of the arms is symmetric.444As the analysis below shows, an optimal player is the same for all feasible values of the gap . Therefore, the player would not get any additional advantage if the numerical value of the gap were revealed to her. We also denote the accumulated and instantaneous regret by

respectively. (These include rewards that have not been revealed to the player.) The associated final-time expected regret, or simply the regret, is given by the iterated expectation

| (1.7) |

which we denote succinctly as

The player strategy is specified for every prediction period where each is a discrete probability distribution over two arms. This distribution can in principle be a function of all information available to the player at time (the history), i.e., where

| (1.8) |

denotes the history, denotes the prior samples of the arms and denotes the previously revealed rewards.

Note that the accumulated regret and instantaneous regret are vectors while the final-time expected regret is a scalar. The player’s objective is to minimize the final-time expected regret for the choice of the safe and risky arms that maximizes this regret. Accordingly, a minimax optimal player is a minimizer of the minimax regret

| (1.9) |

where the set of feasible is given in the previous paragraph. (We will refer to this player as simply an optimal player when the context is clear.)

The suboptimality parameter or gap of the arms is given by where and are the means of the safe and the risky arms, respectively. We consider several scaling regimes where approaches zero as the number of prediction periods goes to infinity.

Reference [bather] considered the Bayesian version of our problem in the context of the following hypothesis test. Let the prior distribution be defined by assigning equal probabilities to

The expected number of times the inferior treatment (the risky arm ) is chosen is given by pseudoregret (also denoted as weak regret)

| (1.10) |

where the expectation is computed similarly to Eq. 1.7 and denotes the number of times the risky arm was sampled by the player. Accordingly, a sampling rule that minimizes the expected number of times the inferior treatment is chosen leads to the Bayesian symmetric two-armed Bernoulli bandit problem: it has the same definition as the symmetric two-armed Bernoulli bandit above, except that the index of the safe arm is sampled from a prior distribution over and the (Bayes) optimal player is a minimizer of the Bayesian pseudoregret (also called Bayes risk). In the case of the uniform prior, the Bayesian pseudoregret is given by

| (1.11) |

where the set of feasible is the same as in the setting of the minimax regret above.

For either choice of the safe arm, the distribution of arm 1 is the same as , where is the distribution of the second arm. Thus, the player will get the same information about the means of both distributions by sampling either arm. Accordingly a success observed in any trial with arm 1 is equivalent to a failure observed from arm 2, and the information derived from any sequence of trials does not depend on the sampling rule.

Let the revealed cumulative rewards of arm be given by

Reference [bather] determined that the following player that selects the arm with the highest posterior probability of being the safe one given the revealed rewards (myopic player) is Bayes optimal under the uniform prior.

Reference [bather] also determined the leading order term of the above-mentioned Bayesian pseudoregret (1.11) to be (which corresponds to in the centered version of the problem we consider below). Since an expectation is less or equal to the maximum, bounds below the minimax pseudoregret given by

| (1.12) |

Also, since (1.10) can be equivalently expressed as

| (1.13) |

we have for any and as a result of exchanging the maximum with the expectation. Therefore the Bayesian pseudoregret also bounds the minimax regret below. The Bayesian pseudoregret determined in [bather] corresponds to the regime in which the gap between the means of the arms is a constant multiple of (medium gap) where is the number of prediction periods.

Although it is well-known that one can achieve -regret and pseudoregret in this (and more general) bandit settings, the exact constant inside the was not previously known in the minimax setting; also regret and pseudoregret have not been previously determined across different scaling regimes of the gap. We obtain such results as well as eliminate several other conceptual barriers towards a more complete understanding of the regret under various scaling regimes of the gap by applying PDE-based methods to the symmetric two-armed bandit model. Our principal conceptual advances are the following:

-

(1)

We show that the optimal player in the symmetric two-armed bandit problem in the minimax setting is the same as in the Bayesian setting described above. We appear to be the first to give a proof of its optimality in the minimax setting, although its optimality in the Bayesian setting is known. This allows us to apply methods based on partial differential equations (PDE) to compute the regret and pseudoregret in the minimax setting. Thus, our methods make progress towards unifying the analysis of Bayesian and minimax regret on the one hand, and unifying the analysis of regret and pseudoregret, on the other hand.

-

(2)

Since the optimal player is discontinuous as a function of revealed gains, the spatial derivatives of the solutions of the relevant PDEs are also discontinuous. While this discontinuity does not affect the leading order term of the regret, it affects the discretization error. We are able to optimize this discontinuity to minimize this error.

-

(3)

We determine the minimax optimal regret and pseudoregret in the symmetric bandit setting, which leads to new regret and pseudoregret lower bounds in the general two-armed bandit setting. While existing nonasymptotic lower bounds rely on information theory, as further discussed below, our results lead to new lower bounds established by more elementary techniques.

These advances not only provide a fresh perspective on the symmetric two-armed bandit problem, but also allow us to improve on the existing bounds.

-

(1)

We show that the previously known leading order term of pseudoregret obtained in the Bayesian setting in [bather], corresponding to the medium gap regime, matches that in the minimax setting by associating the minimax pseudoregret with an explicit solution of a linear heat equation (Section 3.2). In the hypothesis testing framework described above, our results extend to the minimax setting the guarantee on the expected number of times the inferior treatment (risky arm) is chosen.

-

(2)

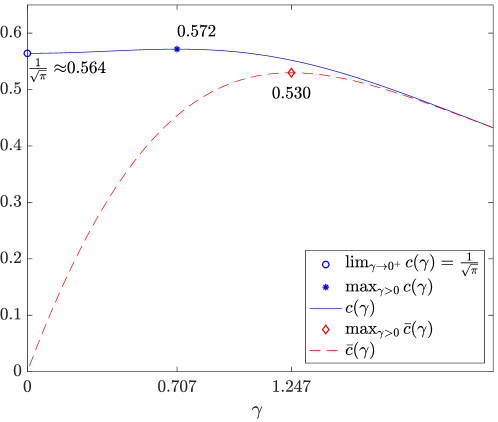

Although the optimal player is the same in the regret and pseudoregret settings, in the medium gap regime, the exact value of that inflicts the optimal regret is smaller than the one that inflicts the optimal pseudoregret, albeit still strictly larger than zero, which we believe has not been demonstrated previously. Specifically, the largest regret of (or in the equivalent centered problem described below) is achieved when the safe arm has mean (or in the centered problem) (Fig. 1).555These prefactors are rounded to 3 decimal places. In the hypothesis testing framework of [bather], the regret represents the expected difference between the outcomes of the better fixed treatment in hindsight and the outcomes of the sequence of treatments chosen by the player.

-

(3)

Our methods also obtain the leading terms of the regret and pseudoregret if the gap approaches zero (a) faster than a constant multiple of (small gap) or (b) slower than a constant multiple of (large gap) (Table 1).

-

(4)

In the small gap regime, the regret does not depend on the gap and in particular, it is the same as in the regime where the gap is zero. On the other hand, the optimal pseudoregret is (or in the centered version of the problem), which would be the same if the player naively sampled each arm an equal number of times. This establishes (again without appealing to information-theoretic tools) that the optimal player cannot detect the gap in this regime.

-

(5)

Our methods also provide new non-asymptotic guarantees in each of the three gap regimes (Section 3.2, Section 3.5 and Table 1).

PDE-based methods have been previously applied to other bandit problems. For example, references [Chernoff68, Chang87, Lai88] used free-boundary problems involving the heat equation to study bandit problems in the fixed gap regime. These bounds typically scale as and therefore do not guarantee regret whenever the gap approaches zero faster than a constant multiple of .666See also reference [Lai05] for a survey of these and related results. Reference [KW23] considered the diffusion limit of the Thompson sampling strategy in the general bandit setting, and among other results, upper bounded the pseudoreget associated with this strategy in the two-armed bandit setting in the large gap regime.777Since Thompson sampling is not necessarily an optimal strategy in the present setting, in Section 4 we confirm that the minimax regret we obtain for the symmetric two armed bandit in the large gap regime satisfies the upper bound in [KW23], and therefore our results are consistent with that reference. To our knowledge, the present paper is the first application of a PDE-based methods to guarantee minimax regret and pseudoregret in a bandit problem when the gap approaches zero at an arbitrary rate, i.e., the difficulty of detecting the gap increases arbitrarily as the sample size increases.

Our methods involve identifying a PDE whose solutions approximate the final time regret (asymptotically, in certain regimes as the number of time steps tends to infinity and the parameter tends to zero). It is easy to explain, at a conceptual level, why a PDE-based method is useful. Indeed, our symmetric two-armed bandit problem has the feature that the optimal player strategy is known, and it depends on the history in a very simple way. Therefore (as we shall explain), the evolution in time of the (optimal) player’s regret can be viewed as a random walk in a suitable state space. Since we are interested in the properties of this random walk over long times, one approach would be to consider a suitable scaling limit (in the same way that a simple random walk on a lattice can be studied by considering Brownian motion). For example, a Hamilton-Jacobi-Bellman PDE emerged in reference [zhu22] from applying a scaling argument in the context of considering optimal player strategies for -armed Bayesian bandits.888In that general setting, the optimal player is not known explicitly, and while the PDE-based model is supported by extensive numerical experiments, convergence of the value function of the discrete bandit problem to the PDE solution, as well as explicit regret bounds in different scaling regimes, have not yet been obtained analytically. Our PDE-based methods are aimed to make progress towards achieving those results.

In the present setting a more elementary alternative to the scaling argument is also available, namely: the backward Kolmogorov equation of the scaling limit is easy to guess; since the expected value of the random walk is like a discrete-time numerical scheme for this PDE, the fact that the PDE solution and this value function are close can be shown using little more than Taylor expansion. Our analysis uses this more elementary approach. Its execution is complicated by the fact that the solution of our PDE is not smooth – rather, it is piecewise smooth and at most in the spatial coordinates, with bounded second-order derivatives. But the execution is simplified by the fact that the solution can be found explicitly; therefore the error terms introduced by Taylor expansion have explicit estimates.

The symmetric two-armed Bernoulli bandit we examine is a restriction to of the -armed bandit distribution that provides essentially the only known lower bound for the general -armed stochastic bandit problem. In that setting there are probability distributions (arms) , and the safe arm is chosen uniformly at random at the start of the prediction process. In each period , the player determines which of the arms to follow by selecting a discrete probability distribution ; the arms’ rewards and the player’s choice of the arm are sampled independently from and , respectively; then this choice and the rewards of the chosen arm are revealed to the player. Theorem 3.5 in [bubeck_book] proved an lower bound using the probabilistic method. This proof is based on information theoretic tools, in particular Pinsker’s inequality, and entails averaging over random choices of the safe arm, which is distributed according to an i.i.d. Bernoulli distribution with mean . The remaining risky arms have the same mean for where is fixed.999The earlier reference [auer] originally proved a similar lower bound. In the foregoing reference, the authors noted that they are not aware of any other techniques to prove bandit lower bounds. The methods in our paper make progress towards developing new techniques to prove such bounds.101010By references [rodman, zaborskis] discussed earlier in this section, similarly to the optimal player in the symmetric two-armed Bernoulli bandit, the optimal player is myopic when it faces the -armed bandit distribution described in the paragraph accompanied by this footnote.

As noted previously the pseudoregret represents the expected number of times the inferior treatment (risky arm) is chosen while the regret represents the expected difference between the outcomes of the better arm in hindsight and the outcomes of the sequence of treatments chosen by the player. Nevertheless, the only known lower bounds for regret in general bandit problems are given by the pseudoregret associated with the stochastic Bernoulli distributions described in the previous paragraph. Our methods make progress towards developing new PDE-based techniques to prove lower bounds with respect to regret directly.

Another classic online learning problem is prediction with expert advice. This setting is rather different from the bandit problem: the rewards of all “arms” (referred to as experts in this setting) are revealed to the player in this problem, i.e., it is a complete information problem. References [Zhu, rokhlin, drenska2019prediction] connected this problem with a PDE, by considering a scaling limit as the number of time steps tends to infinity. A little later, [kobzar, kobzar_geom] obtained closely related results by more elementary Taylor-expansion-based methods. PDE-based analysis of regret has been used to determine asymptotically optimal strategies and regret in prediction with expert advice explicitly in certain cases [bayraktar2019b, bayraktar2019a], to analyze variations of this classic problem [bayraktar2020prediction, drenska2020c, drenska2020b, drenska2020a, harvey2020optimal], and to study drifting games [wang22] and unconstrained online linear optimization [zhang22]. In reference [bayraktar2022], PDE-based methods connected with the prediction with expert advice literature were used to guarantee regret in a bandit-like game where the adversary’s distribution in each round is revealed to the player in addition to the sampled gains. Notwithstanding the fundamental differences between stochastic bandits and complete information problems, like prediction with expert advice, the estimation of the value of the discrete game by a PDE solution using backwards induction (the“verification argument”) in this paper is similar to that in [kobzar].

2. Notation

If is a function of several variables, subscripts denote partial derivatives (so and are first derivatives, and , and are second derivatives). In other settings, the subscript is an index; in particular, the arms’ rewards and the player’s choice of the arm at time are and , and refers to the -th component of . When no confusion will result, we sometimes omit the index , writing for example rather than ; in such a setting, refers to the -th component of .

If is a function, is its Laplacian; however, the standalone symbol refers to the set of probability distributions on . and denote the sets and respectively for natural numbers and . is a vector in with all components equal to 1, but refers to the indicator function of the set . If and are functions, represents their convolution.

3. Main results

3.1. Optimality of the myopic player

In this section, we show that a myopic player is minimax optimal for the symmetric two-armed Bernoulli bandit.

In order to reduce the number of state variables, we center and normalize the range of rewards, such that each arm will have the reward with the probability of reward in the original problem, i.e., the rewards in the new game are given by

| (3.1) |

As shown in Appendix A, this centering eliminates the need to track and , the number of times each arm was pulled. In the remainder of this paper, we will only use the centered rewards but we will omit the superscript (hat). We may also omit the word centered when we refer the symmetric two-armed Bernoulli bandit with the centered rewards.

Let the difference between the cumulative revealed rewards be

| (3.2) |

Then the myopic player is given as follows.

This player chooses the safe arm such that the revealed rewards are most probable, i.e., it is the maximum likelihood estimator of the safe arm (as we explain in the opening paragraphs of Appendix A). We show in the same appendix that this strategy is also minimax optimal with respect to both regret and pseudoregret for the symmetric two-armed Bernoulli bandit.

3.2. Centered state variables

In this section, we define the state variables used in the remainder of this work. By Lemma 3.1, the minimax regret Eq. 1.9 is , i.e., the “adversary” achieves the maximum regret by making either arm safe.111111Note that the player of course does not need to know which arm is safe in order to implement . Therefore, we will assume that the safe and risky arms are secretly labeled as arms 1 and 2, respectively, and we will omit the parameter : the distribution of the symmetric two-armed Bernoulli bandit will be denoted where is the distribution of the safe arm and is the distribution of the risky arm.

We now define the centered difference between the cumulative revealed rewards as

| (3.4) |

As we will see below, this centering ensures that the increments of have mean zero as this state variable evolves in accordance with the rule of our bandit problem. Using the centered variables will simplify the calculations in the remainder of the paper. Accordingly, going forward we will only use the centered variable and omit the superscript (hat).

After centering , the myopic player is given as follows.

Let us also denote the centered difference between the cumulative hidden rewards by

and define

Finally, let us consider the difference between the reward of the arm not chosen by the player and the arm chosen, that is

We denote by , the cumulative sum of these differences at time :

We will omit the subscript from the state variables defined above for simplicity whenever this information is clear from context.

A brief calculation reveals that

It is therefore natural to define

3.3. Asymptotically optimal regret using a PDE solution

Let represent the final-time regret if the bandit game starts at time with specified values of and , and the player uses the strategy. Accordingly, for a symmetric two-armed Bernoulli bandit and an optimal player ,

| (3.12) |

where in accordance with the information flow of bandit problem, at time , is evaluated at ; at time , is evaluated at etc.. The increments of the state variables are and

Thus, the minimax optimal regret is

| (3.13) |

According to the rules of the Bernoulli bandit problem, the domain of is restricted to the values of , , , such that , , are integers, and . This function is characterized iteratively:

| (3.14a) | ||||

| (3.14b) | ||||

The foregoing characterization of resembles a numerical scheme for solving a PDE.121212Our use of an iterative scheme is similar to that in [kobzar]. The essence of our analysis is that we identify the PDE and use it to estimate the regret. We shall show that the leading order behavior of is given by a family of solutions of the following linear heat equation with a discontinuous source term:

| (3.15a) | |||

| (3.15b) | |||

where the spatial operator is just a Laplacian in

and the source term is

The form of the PDE (3.15) comes, roughly speaking, from the condition that the definition (3.14) of should be a consistent numerical scheme for the PDE. The argument that this leads to (3.15) is the essence of what we do in Appendix D (though we work harder in the Appendix than would have been needed to find the PDE, since the Appendix also provides error estimates).

The function can be determined explicitly. Let . Then the function of that solves the following ODE

| (3.16) |

where will be fixed later. We require to be smooth except at , continuous at , and to have at most linear growth at infinity. These conditions determine it up two constants: an additive constant, and the discontinuity (if any) of at . We eliminate the former by always taking , and we do not eliminate the latter since our best result will be obtained when has a small (-dependent) discontinuity at . Accordingly,

| (3.17) |

where the constant parametrizes the discontinuity of at . In this paper, we will assume that is positive (it will be in fact either or close to it since needs to be either or nearly so.)

If we take

then for ,

| (3.18a) | |||

| (3.18b) | |||

where . Therefore, the solution of Eq. 3.15 can be represented as

where

which we will refer to as the homogeneous solution,

which we will refer to as the non-homogeneous solution, and

where the convolutions are in the variables only and is the fundamental solution of Eq. 3.18a. In Appendix B, we show that after a suitable change of variables the above convolutions are one dimensional, and reduces to the fundamental solution of the 1D heat equation in Eq. 3.19.

Lemma 3.2.

Note that the discontinuity of and therefore at is

where the superscripts and denote the right and left derivatives, respectively, at that point. Also the discontinuity of at is

Therefore, if and , then is the unique solution of (3.15). For all , the discontinuity of and therefore at is

and is for all and .

In Appendix D, we prove, using induction backward in time, that the function approximates associated with the bandit problem up to a higher order “error” term , which can be estimated explicitly.131313While we use the asymptotic notation for conciseness and clarity of exposition, this and other error terms in this paper can be estimated by our methods with explicit constant prefactors. To obtain this estimate, we need certain bounds on derivatives of . The following bounds are proved in Appendix C.

Lemma 3.3.

We have , and for , . For integer ,

and

However, if , i.e., is , for ,

In all cases above, the bounds hold uniformly in and . At , the above mentioned bounds on apply to the right derivatives (the left second and higher order derivatives are zero).

Our proof that approximates must address the following technical issue: even if , so that is , the second derivative of with respect to is discontinuous at (due to the discontinuity of the source term ). Therefore, when we use a third order Taylor polynomial to estimate how changes when evolves, the conditions of the Taylor theorem are not satisfied on any interval containing the discontinuity. However, according to the rules of the Bernoulli bandit problem, the domain of is restricted to integer values of . Therefore, we only need to bound the evolution of over integer ’s. Near a point where we will estimate the evolution of by taking advantage of the explicit form of .

When is , the above-mentioned discontinuity of is a jump of size , but averaging leads to an “error term” at each time step. Accordingly, over the periods, these errors contribute an error to . Therefore, represents the leading order term of the regret only if dominates the error, i.e., where depends on . We shall show that this occurs in several regimes:

-

•

small gap when ;

-

•

medium gap when for constant ; and

-

•

large gap when slower than a constant multiple of .

These results follow from the following theorem, which is proved in Appendix D, combined with Theorem 3.6, which improves upon Theorem 3.4 in the large gap regime.

Theorem 3.4.

Let the functions and be as defined above, where is of (3.15), i.e., and . Then,

where the error term is and

When , the leading order terms of and are

Therefore, is .

By Eq. 3.13, we have determined the regret up to the discretization error:

To analyze the regret in different gap regimes, we examine the rescaled value of at the start of the game using the following result established in Appendix E.

Corollary 3.5.

For

| (3.21) |

if the leading order term of is as , we have

| (3.22) |

In the small gap regime , and therefore as . Since near , . This implies that the leading order regret is , which matches the standard bound obtained for this classic randomized adversary in the setting of prediction with expert advice.141414In this setting, the player strategy does not affect the leading order term of the regret. Therefore, the fact that the player does not have complete information in the bandit problem is irrelevant. See Example 2 in [kobzar] and note that the expectation of the maximum of two standard Gaussians is .

In the medium gap regime, for constant . Maximizing numerically for shows that for it has a unique maximizer . This yields the maximum leading order regret . The function is plotted in Fig. 1.

When dominates , i.e., , which is denoted as , the above theorem allows to determine the leading order term of the regret as long as . In this setting, as . Since at infinity, . Therefore, the leading order term of is , which dominates given above as long as .

If approaches zero as a constant multiple of or slower, and is a function, Theorem 3.4 does not recover the leading order term of the regret. In this regime, the leading order behavior of is still , but it no longer dominates the error. However, as shown in Appendix F by selecting the suitable constant and making discontinuous at , we can offset the error attributable to the discontinuity of at , and obtain the improved error term . We will also set the prefactor of the second order term in (3.16) to be different from the diffusion constant , which will reduce the error at .

3.4. Improved regret estimate in the large gap regime using a function

In this section, we will use a modified version of the function reduce the discretization error in the large gap regime. Specifically, by selecting the suitable constant and making discontinuous at , we can offset the error attributable to the discontinuity of at . Also by selecting a suitable prefactor of the second order term in we can eliminate the discretization error attributable to for .

Our function used to estimate the regret will still be represented as

where the smooth PDE solutions are given by

and

where is still the fundamental solution of the heat equation given in (3.19) and is given by (3.17). These properties will be sufficient to obtain the leading order regret estimates even though has now a small (-dependent) discontinuity at and, since ,

and are no longer solutions of linear heat equations. The bounds in Lemma 3.3 will still apply, and the foregoing modifications will lead to the improved error term , as shown in Appendix F.

Theorem 3.6.

The preceding theorem improves upon Theorem 3.4 and recovers the leading order term of the regret as long as approaches zero as any rate. The leading order term of the rescaled value of at the start of the game will be unchanged, as established in Appendix E.

The foregoing results are summarized in Table 1. If is fixed as , our methods do not extract the leading order term of the regret: the leading order term of will no longer dominate the error.

3.5. Asymptotically optimal pseudoregret

For a symmetric two-armed Bernoulli bandit , the pseudoregret Eq. 1.13 simplifies to

where is the gap between the arms and is the number of time arm 2 (the risky arm) is pulled.

Let represent the final-time pseudoregret if the bandit game starts at time with specified and , and the player uses the strategy . This function can be expressed similarly to Eq. 3.12 and is also characterized iteratively:

| (3.25a) | ||||

| (3.25b) | ||||

where and . The foregoing also resembles a numerical scheme for solving a PDE, similar to the one we considered in the previous section. Again, the domain of is restricted to integer values of , and , and we have

We identify the relevant PDE and use it to estimate the regret. Specifically, we will show that the leading order behavior of is given by a family of solutions of the following linear heat equation with a discontinuous source:

| (3.26a) | |||

| (3.26b) | |||

where the source term is

Again, the form of the PDE (3.26) comes, roughly speaking, from the condition that the definition (3.25) of should be a consistent numerical scheme for the PDE, and the argument that this leads to (3.26) parallels what we do in Appendix D to determine the PDE (3.15) in the context of regret (since the error estimates are somewhat different in the context of pseudoregret, they are determined in Theorem 3.9 and Theorem 3.11.)

Since the final value does not depend on , the homogeneous solution that satisfies Eq. 3.26 without the source term is just the final value. We let be a function of satisfying

| (3.27) |

The solution of this ODE with and at most linear growth at infinity is given by

| (3.28) |

and when , we obtain the following result.

Lemma 3.8.

If , then is the unique solution. For other choices of , is only at . For all , and therefore have a jump at . Note that

where is given by Eq. 3.17, and thus

where are given by Eq. 3.17 and Eq. 3.20 respectively. Therefore,

where is given by Eq. 3.20. Therefore, for , the bounds on and in Lemma 3.3 apply to and uniformly in and .

Since and therefore are smooth as , we don’t need to consider the final period separately for purposes of computing the discretization error. When is , the error accumulating in each time period attributable to in Eq. D.13 is

The first term in the preceding expression is estimated by Eq. D.17, which leads to the following theorem.

Theorem 3.9.

Let the functions and be as defined above, where is the solution, i.e., and . Then

where the error term is

When , the leading order terms of and are set forth in Theorem 3.4, and is

Since , we have determined the pseudoregret up to the discretization error

To analyze the pseudoregret in different gap regimes, we examine the prefactor of the leading order term of – it is determined by taking the terms attributable to in Appendix E (plus which corresponds to adding in Eq. 3.30 below).

Corollary 3.10.

In the medium gap regime, this function provides the constant prefactor of the leading order term of the regret, which is plotted in Fig. 1. Maximizing Eq. 3.30 numerically for shows that it has a unique maximizer at . This yields the leading order regret , which matches the result in [bather]. This and other references cited in this work use the 0/1 scaling of the rewards. Therefore, the constant prefactors of regret bounds in those references are smaller by a factor of than those in our paper.

In the small gap regime, since near , . This yields as the leading order term of the pseudoregret.

In the large gap regime, a computation similar to the corresponding computation in the previous section shows that the resulting leading order term of is . This term dominates as long as as ; so under this condition it reflects the leading order term of the pseudoregret. However, we can again reduce the first term of the error to by making discontinuous at .

When is given by (3.23) and , the cumulative error attributable to in Appendix F is

which leads to the following error estimate.

Theorem 3.11.

Let the functions and be as defined above, where is a function with given by (3.23) and . Then

where the error term is . When , is .

Using this improvement of Theorem 3.9 in the large gap regime, we recover the leading order term of the pseudoregret as long as at any rate as . The foregoing results are also summarized in Table 1.

| Small gap | Medium gap | Large gap: | |

If is fixed as , our methods do not extract the leading order term of the pseudoregret: the leading order term of will no longer dominate the error.

4. Relationship to existing results

As mentioned earlier, the symmetric two-armed Bernoulli bandit was previously considered in [bather]. That paper determined an asymptotically optimal Baysian pseudoregret , which matches our estimate. We are not aware of the leading order terms of the minimax optimal regret or pseudoregret having being determined previously (as opposed to Bayesian pseudoregret) in the symmetric version of the problem.

Since the regret and pseudoregret in the symmetric two-armed Bernoulli bandit bounds from below the minimax regret in the general two-armed stochastic and adversarial bandit problems, our results lead to an improved nonasymptotic lower bounds for the latter classes of problems.151515The existing asymptotic lower bound for the general (non-symmetric) two-armed Bernouilli bandit is still sharper however than the leading order term lower bound that follows from our results. In this setting, the minimax pseudoregret given by , where and are the means of the arms, is asymptotically bounded by where the lower and the upper bounds were determined in [bather] and [vogel1960] respectively. Previously, the best nonasymptotic lower bound known to us for the general two-armed bandit problem is obtained for our symmetric Bernoulli distribution using information-theoretic tools.161616See Theorem 3.5 in [bubeck_book]. For further reference, in the general two-armed bandit setting, the best nonasymptotic pseudoregret upper bound is achieved by information-directed sampling (Specifically, Proposition 3 in [russo14] established a pseudoregret bound for Bayesian bandits where in the context of two-armed bandits the number of player’s actions is . Subsequently, Corollary 10 in [lattimore21] extended this bound to oblivious adversaries in the minimax setting.) The best nonasymptotic regret upper bound known to us is achieved by an exponential weights-based algorithm (Theorem 3.4 in [bubeck_book]).

As noted in Section 1, reference [KW23] determined the upper bound on the pseudoregret of the diffusion limit of the Thompson sampling strategy in the general two-armed bandit setting in the large gap regime. Specifically, they showed that the rescaled pseudoregret () guaranteed by Thompson sampling with respect to the rescaled gap is upper bounded as follows

as the rescaled gap for any . Our result that the leading order term of is implies that . Therefore, for any , as above, . Therefore, the optimal regret in the two-armed symmetric bandit also satisfies the foregoing upper bound. This confirms that the optimal player performs in the two-armed symmetric setting no worse than (potentially suboptimal) Thompson sampling, and therefore our results are consistent with [KW23].

5. Conclusion

In this work, we determine the minimax optimal player and characterize the asymptotically optimal minimax regret and pseudoregret of the symmetric two-armed Bernoulli bandit by explicit solutions of linear heat equations when the gap between the means of the arms goes to zero as the number of prediction periods approaches infinity. We also provide new estimates of the non-asymptotic error. Our PDE-based proof works despite the fact that the solution of our PDE has discontinuous derivatives and is not a classical one on the entire domain. Although optimal player strategies are not known for more general bandit problems, we expect that the methods of this paper should be useful in considering how regret accumulates under specific player strategies, even when they are not known to be optimal. Separately, there are other bandit problems that do not require exploration, like the symmetric two-armed bandit in the fixed gap regime and the symmetric -armed Bernoulli bandit distributions (which are, as discussed above, used to bound the regret from below in general -armed bandit problems). We expect that the methods of our paper could be applied to such problems as well.

Acknowledgements

V.A.K. acknowledges helpful input from Chris Wiggins, and support from NSF grant DMS-1937254. R.V.K. acknowledges support from NSF grant DMS-2009746.

Appendix A Proof of Lemma 3.1

A minimax optimal player for the regret minimization problem is, by definition, a minimizer of Eq. 1.9, which can be expressed in the and coordinates as

| (A.1) |

Here, as discussed in Section 1, ranges over all possible player strategies; in particular, each depends only on the history that is available to the player at time . We shall show in this section that the strategy (defined by Eq. 3.3) is minimax optimal.

For purposes of this Appendix A, we will use centered gains but consistently with Section 3.1 we will not center to have zero mean, i.e., we will use the definition of given by Eq. 3.2. (Elsewhere in the paper we will use centered given by Eq. 3.4).

We start with an argument that makes this conclusion plausible (while also displaying transparently some key ideas). Recall that in terms of the centered gains , depends only on , where at any time the observed gains are . It chooses arm if , it chooses arm if , and it chooses the two arms with probability each if . This is a maximum likelihood estimator of the safe arm. Indeed, due to the symmetry of the two bandit arms, if is a trial from one arm then can be viewed as a trial from the other arm. Using this observation to convert observed trials of arm to trials of arm , we see that the sample mean of the resulting gains of arm is positive exactly when . Thus: based on the sample means available at time , arm is more likely to be safe if , arm is more likely to be safe if , and no distinction is possible if . Since the gains of the arms at distinct time steps are independent, the order in which the arms were chosen should be irrelevant; and since sampling either arm gives statistical information about both arms, the information gained at each step does not depend on the player’s choices. Thus, the sample means just discussed are the only information available to the player at time . In view of this, it is difficult to imagine how a different player strategy could do better than .

But the preceding argument is not a proof. The rest of this section provides a rigorous argument. Our argument is in a sense inductive. In fact, starting from any minimax optimal player strategy that differs from , we consider a new strategy obtained as follows:

-

(1)

If is the earliest time such that

we set

(This leaves unchanged relative to at times , and changes it to at time ).

-

(2)

At subsequent times we choose so that it is statistically equivalent to . Rather than give a formula for , it is more convenient to say how to sample it. For any given history of player choices and observed gains , the player samples as follows:

-

•

First, the player replaces by a choice sampled using (evaluated, of course, at the given history through time ).

-

•

If then has not been observed; however the statistically equivalent quantity has been observed. So the player samples by sampling evaluated at the modified history obtained by not only changing as indicated above but also replacing the time gain by

Using this procedure, the player’s choices (and therefore also her gains) at times are statistically identical to those obtained using .

-

•

We shall show that the strategy just defined does at least as well as . Iterating the preceding argument finitely many times, it follows that the strategy is optimal, as claimed.

A.1. Some simplifications and preliminary calculations

We begin by giving an alternative characterization of a minimax optimal player: it is one that maximizes the worst-case expected player gains:

| (A.2) |

To explain why, we observe that the player’s strategy and the adversary’s choice can only influence the value of in Eq. A.1. This is because does not depend on , and only the sign of , as a random variable, depends on – so that the expectation of does not depend on either. Thus, to solve (A.1) the player needs to find the optimal for

Since for all and , it suffices for the player to optimize

| (A.3) |

This confirms the alternative characterization (A.2).

Next, let us write the objective of (A.2) more explicitly. We have

| (A.4) |

where

| (A.5) |

can be written (remembering that depends on revealed history , as defined in Eq. 1.8) as

| (A.6) |

where we sum over all possible histories available at time . Moreover, in accordance with Eq. 1.7,

with the convention that if is the specific history under discussion,

and

Note that does not depend on ; this reflects the fact that the player’s strategy depends only on the history that was revealed to her (she does not know ).

We emphasize that is function of histories taking values in the space of probability distributions on the two arms. For example, given a strategy and history available after the first prediction round at time ,

is the probability that this player chooses arm at time if at time she chose arm and received the gain .

The probability of a particular sequence of gains is easily made explicit. The calculation is simplest when the gains are and . For any list of revealed gains at time , let be the number of times arm was chosen, and let be the sum of the revealed gains from arm . Then

| (A.7) |

and if and if .We will omit the subscript of when doing so is not expected to cause confusion. Since (A.7) is, by definition, the value of , a little algebra reveals that

| (A.8) |

Evidently, exactly the exponent on the right is positive. Since is the probability of the given sequence of gains if arm is safe, we have confirmed that chooses the arm that, by a maximum likelihood estimate, is more likely to be safe, given the observed sequence.

Since we prefer to work with centered gains (taking the values ), let us put the preceding calculation in those terms. To avoid confusion, for this paragraph (only) we denote the centered gains by (so ) and we write for the analogue of using centered gains. Then one easily checks that , so that the exponent on the right side of (A.8) is just . This agrees, of course, with our earlier argument that the sign of determines which arm is more likely to be safe, given the observed gains. For the remainder of this appendix, we will continue to work with the centered gains, but (as in the body of the paper) we shall write not to avoid notational clutter.

A.2. The optimality of

We are ready to explain the optimality of . Recall the plan indicated earlier: given an optimal strategy , we consider the first time when it differs from , and we consider the alternative strategy (discussed earlier) that uses at time and is statistically equivalent to for . Our goal is to show that the player’s worst case expected gains (A.2) are at least as large under the alternative strategy as under .

Since the alternative strategy is statistically identical to at times other than , we may focus exclusively on the situation at time .

The case is simple but instructive. At the initial time there is no history and , so is just a probability distribution on the two arms and . When we restrict our attention to time , the max-min (A.2) becomes

which reduces by simple algebra to

The optimal is easily seen to be – the value chosen by ; moreover, choosing this value makes the player indifferent to whether or (that is, the player is indifferent to the adversary’s choice which arm is safe).

For , the argument is similar in spirit though the details are more involved. We shall show that among strategies satisfying for , the choice is optimal for

| (A.9) |

where is defined by (A.5); moreover, the proof will reveal that this choice makes the player indifferent at time to whether or .

The argument relies on grouping the histories in a convenient way. Given any history , we say is its complement if lists the same gains but attributes them to the opposite arms; thus, for example, if , the complement of is . We will also omit the subscript when doing is not expected to cause confusion. Notice that every history has a complement, no history is its own complement, and if is the complement of then is the complement of . Given a complementary pair and , we introduce the notation

and we introduce the analogues for of and ,

Since and , it is convenient to group the terms in as follows:

| (A.10) |

Now, recall that the strategies under consideration here have for , and that is determined by the sign of . If we treat as a function of history, it is straightforward to see that when and are complementary,

(It is important here that if .) Thus, chooses arm whenever chooses arm , and vice versa. It follows that for the strategies under consideration,

for , and therefore

| (A.11) |

We now apply these observations to identification of the optimal for (A.9), which by (A.6) amounts to

Only the term with a factor of depends on , so it suffices to consider

Grouping the histories into complementary pairs and using (A.10) combined with (A.11), we see that this problem can be written in the form

where the summation is over all pairs of complementary strategies (chosen so that each strategy appears just once). Here the subscript indexes all possible histories through time but we omit the dependence of and on for simplicity. One easily sees that this optimization fits the conditions of Lemma A.1 below, if for a given pair of complementary histories through time we take , , , and .

Lemma A.1.

Let and be arbitrary vectors in . Then

is achieved when

Moreover, at any optimal the values of and are equal.

Proof.

Since for any real valued and , , we have

| (A.12) |

It suffices to consider such that for each . Indeed, for any admissible and , the vectors and are also admissible, and while , so the value of our objective at is at least as good as the value at . The assertion of the lemma is now clear, by optimizing the linear function . (We remark – though this will not be used – that the and identified above are in fact the only optimal choices, except that when then and can take any admissible value.) ∎

The lemma shows that an optimal strategy is obtained by taking and if , and if , and and if .171717Since , the ordering of , and is the same as ordering of , and when . When , the ordering of and does not matter. Essentially, this strategy chooses the arm for which is larger. Since

the optimal strategy just identified is in fact . The lemma also assures us that this strategy makes the player indifferent (through time ) to the choice of the safe arm .

As noted earlier, after repeating this argument finitely many times, we conclude that it is optimal to use the strategy at every time (through ), and that the final-time regret does not depend upon which arm is safe (in other words, .

The proof that is also optimal the context of pseudoregret is essentially the same, so we omit it.

Appendix B Proof of Lemma 3.2

Appendix C Proof of Lemma 3.3

C.1. Derivatives of

Since we can put one derivatives under the integral on the absolute value function and the remaining derivatives on the fundamental solution , for ,

| (C.1) |

Since , we have . Therefore, .

C.2. Derivatives of

It is elementary that , and for , . Similarly to (C.1), for , we can put one derivative on

| (C.2) |

However if , i.e. is , and we can put two derivatives on : for ,

and since , and ,

Therefore, for ,

| (C.3) |

Also since , we have

Appendix D Proof of Theorem 3.4

We will show that

where is given by Eq. D.15 in two steps. In the first step, we establish the upper bound:

| (D.1) |

uniformly in and where is given by Eq. D.13 and Eq. D.14. Since and therefore is not differentiable at and , in Section D.1 we consider the final prediction period separately from the earlier periods. Also Section D.2, we will treat separately the region where or where is smooth (D.2.1 and D.2.2) from the region where where and therefore are discontinuous (D.2.3). Since the lower bound

can be proved similarly to the upper bound, we omit the proof of lower bound to avoid repetition.

The second step connects and . Since is defined by the iterative scheme (3.14), in Section D.3, we show that by induction starting from the final time. The proof that is similar and therefore is omitted.

D.1. Final period

We consider the evolution of during the final prediction period ( changes from to ). Since ,

| (D.2) |

is bounded above uniformly in , and . Since the absolute values of and are uniformly bounded, then so is . Also since , we obtain

which is uniformly bounded from below. It is also bounded uniformly from above since . Therefore, Eq. D.2 is bounded above by a constant uniformly in , and .

Arguing as in the previous paragraph, we have

The first term vanishes since , while the second term is bounded uniformly in since

D.2. Periods before the final one

Now we consider the evolution of before the final prediction period, i.e., at . By the rules of the game only takes integer values. Since for any ,

where the last equality holds because the laws of and are the same. We consider

| (D.3a) | |||

| (D.3b) | |||

| (D.3c) | |||

By Taylor expansion Eq. D.3a is given by

where all the derivatives are evaluated at and

Since the expectation of the terms involving is zero and ,

Since the expectation of the third order term is also zero and , by Lemma 3.3

Finally, since , we have

| (D.4) |

Similarly Eq. D.3b is given by

where all the derivatives are evaluated at and

Since the expectation of the first order terms is again zero, and

Since the expectation of the third order term in is zero and , for , by Lemma 3.3,

| (D.5) |

Thus, using , we have

as well.

It remains to consider the evolution of . Since is at most at , we consider the following 3 cases.

D.2.1.

When , the above integrand is not defined at , i.e., when and . However, since this occurs at an endpoint of the integration interval, we can simply ignore it for the purpose of evaluating the integral. Therefore,

| (D.6) |

For we have , and therefore

where

| (D.7) |

and

For ,

As , the leading order term of is given by

and therefore,

| (D.8) |

D.2.2.

The function is linear for . Therefore,

where there is no error term () as a result of the linearity of .

D.2.3.

When , we must argue a little differently because is only piecewise smooth in . (Indeed is only at .) But our method still works using the explicit values of . Since ,

and we have

| (D.9) |

For ,

| (D.10) |

where

For ,

| (D.11) |

When , the leading order term of is . Using the definition of

where

| (D.12) |

Combining the foregoing, for all

where

| (D.13) |

When , the leading order term of is

| (D.14) |

D.3. Approximation of by by induction

Lastly, we show that (where the discretization error is defined below) by induction backwards from the final time. In doing so, we are proving the associated regret is approximately . If one accepts the use of our myopic player, then the bandit problem can be viewed as a Markov chain with as its state space; in this setting the PDE for is the backwards Kolmogorov equation associated with the scaling limit of this Markov chain.

This proof is similar in character to the proof of Theorem 3 in [kobzar]. Specifically, initialization of the induction follows from the fact that where the function is given by

| (D.15) |

for a constant . The inductive hypothesis is that

Since ,

We estimate by an integral. We first consider the term . Integrating from to such that , i.e., where , and also separately from to where (or from to if ) leads to the following cumulative error estimate

| (D.17) |

attributable to that term. Together with the other terms, we obtain

When , the leading order term of is

Appendix E Proof of Corollary 3.5

We will use the following function to analyze

| (E.1) |

As shown in Appendix J of [kobzar], solves with . Therefore, where solves the 1D linear heat equation on : with . Therefore, can be expressed as:

and

Also

where

| (E.2a) | |||

| (E.2b) | |||

Therefore,

Combining the foregoing results we obtain

| (E.3) |

When and , since and , the assertion of Corollary 3.7 follows if the leading order term of is .

When ,

| (E.4) |

When and , since , the assertion of Corollary 3.5 follows if the leading order term of is

Appendix F Proof of Theorem 3.6

We shall show that by making a slightly different choice of the constant in the definition of (so that and are no longer at ) and setting , the arguments we used in Appendix D give the same leading-order estimate for the final-time regret, with a better error term.

When is not at , the computation of

in Eq. D.4 is unchanged. However, instead of Eq. D.5, we have

and therefore

Next in Section D.2.1 we modify the calculation of after (D.6) as follows. To determine the value of that eliminates the discretization error, we set . This leads to

which is solved by

With this choice of ,

Therefore,

where

| (F.1) |

Also the analysis in Section D.2.2 is unchanged and we still have .

Next in Section D.2.3, we modify the calculation after (D.9) as follows. Since

(D.10) becomes

| (F.2) |

and for

| (F.3) |

Note that since the leading order behavior of as is unchanged (it is still ), this choice of does not affect the leading-order behavior of as , i.e. the value of is unchanged. But the errors for and at have been reduced as shown above from in Eq. D.8 and in Eq. D.12 to zero in Eq. F.1 and Eq. F.3. (The revised choice of does not affect our arguments for where is still zero.) This improves the overall error since the only error term is now . Bounding by an integral, we obtain

or, when ,