A Large Confirmatory Dynamic Factor Model for Stock Market Returns in Different Time Zones††thanks: The Matlab code for this paper is available upon request.

Abstract

We propose a confirmatory dynamic factor model for a large number of daily returns across multiple time zones. The model has a global factor and three continental factors. We propose two estimators of the model: a quasi-maximum likelihood estimator (QML-just-identified), and an improved estimator (QML-all-res). Our estimators are consistent and asymptotically normal. In particular, the asymptotic distributions of QML-all-res are the same as those of the infeasible OLS estimators that treat factors as known and utilize all the restrictions of the parameters of the model. We apply the model to MSCI equity indices of 42 developed and emerging markets, and find that the market is more integrated when the US VIX is high.

- Keywords:

-

Daily Global Stock Market Returns; Time-Zone Differences; Confirmatory Dynamic Factor Model; Quasi Maximum Likelihood; Expectation Maximization Algorithm.

- JEL classification

-

C32; C55; C58; G15.

1 Introduction

Correlations among stock returns in different countries are an important ingredient of the strategic allocation decision to international stocks and for understanding the degree of segmentation of international capital markets. The last three decades have witnessed a heightening interest in measuring and modelling such correlations, whether under the rubric of stock market integration, country risk models, international stock co-movement, interdependence or otherwise. Gagnon and Karolyi (2006) and Sharma and Seth (2012) have carefully reviewed the early literature and categorized these studies according to methodologies, data sets, and findings.

The world’s stock markets are separated in time by substantial time-zone differences, to the extent that for example the American and main Asian markets do not overlap at all (although the European markets overlap a little with both the American and Asian markets). Table 1 lists the trading hours of the world’s top ten stock exchanges in terms of market capitalization on October 29th 2021. This shows the overlaps and lack of overlaps. Whenever using daily data to measure correlations, researchers have to address the issue of non-synchronous trading. This is because the closing prices of the American markets, say, contain a lot of news that could never have been in the closing prices of the Asian markets for the same calendar days (Schotman and Zalewska (2006)) and vice versa.

| Stock Exchanges | Market Cap | Trading Hours | Country | |

|---|---|---|---|---|

| (US trillions) | (Beijing Time) | |||

| 1 | New York S.E. | $26.91 | 21:30-04:00 ()† | US |

| 2 | NASDAQ S.E. | $23.46 | 21:30-04:00 ()† | US |

| 3 | Shanghai S.E. | $7.69 | 09:30-11:30, 13:00-15:00 | China |

| 4 | Tokyo S.E. | $6.79 | 08:00-10:30, 11:30-14:00 | Japan |

| 5 | Hong Kong S.E. | $6.02 | 10:00-12:30, 14:30-16:00 | China |

| 6 | Shenzhen S.E. | $5.74 | 09:30-11:30, 13:00-15:00 | China |

| 7 | London S.E. | $3.83 | 15:00-23:30† | UK |

| 8 | India National S.E. | $3.4 | 11:45-18:00 | India |

| 9 | Toronto S.E. | $3.18 | 21:30-04:00 ()† | Canada |

| 10 | Frankfurt S.E. | $2.63 | 15:00-23:30† | Germany |

The objective of this paper is to develop a framework to model correlations of daily stock returns in different markets across multiple time zones. This allows one to analyze international stock returns as if they were measured at the same time and location, and so allows empirical researchers to eliminate the substantial bias that would otherwise be manifested in whatever question they are addressing. The machinery will be a dynamic factor model, a special case of the generalized dynamic factor model first proposed by Forni et al. (2000). To make the model tractable, we make the following simplifying assumption: All the markets belong to one of three continents: Asia, Europe and America. We suppose that the logarithmic 24-hour close-to-close returns follow a dynamic factor model driven by both global and continental factors. This model reflects a situation in which international information represented by the global factor affects all the three continents simultaneously, but is only revealed in the returns of the three continents sequentially as their markets open in turn and trade on the new information (Koch and Koch (1991, p.235)). Local information represented by a continental factor accumulated since the last closure of that continent’s markets will also have an impact on the logarithmic 24-hour close-to-close returns of those markets in our framework. The dynamic factor structure can be consistent with a purely efficient market (if the dynamic parameter is exactly zero); it can also be consistent with market microstructure or sluggish response of prices introducing some short term autocorrelations that are presented through the dynamic evolution of the global factor.

We propose two estimators of the model: a quasi-maximum likelihood estimator (QML-just-identified), and an improved estimator (QML-all-res). A key issue here is identification and we show explicitly how to impose some of the restrictions implied by our model to guarantee identification. In particular, we impose a subset of restrictions, specifically of them. Because these restrictions cannot be written compactly in a matrix form, it took us a considerable amount of work to derive the large sample results of our estimator QML-just-identified. We next improve upon the QML-just-identified estimator and propose a QML-all-res estimator which takes all the restrictions implied by our model into account. The idea is that all these restrictions could be incorporated in an EM algorithm. Our estimators are consistent and asymptotically normal as the sample size increases. In particular, the asymptotic distributions of QML-all-res are the same as those of the infeasible OLS estimators that treat factors as known and utilize all the restrictions of the parameters of the model. We propose consistent standard errors and inference methods.

We apply our model to MSCI equity indices of 42 developed and emerging markets. Taking Asia-Pacific as an example, we find that the global factor has the largest loadings during the Asian sub-period. Mainland China and Hong Kong have large loadings on the continental factor, whereas Japan has minimal loadings on the continental factor. In addition, we adopt a methodology similar to Pukthuanthong and Roll (2009) to assess market integration. The US demonstrates the highest level of global integration but minimal regional integration. We also find evidence that the weak-form efficient market hypothesis does not hold across the globe and it takes more than a day for some international news to fully unfold or dissipate.

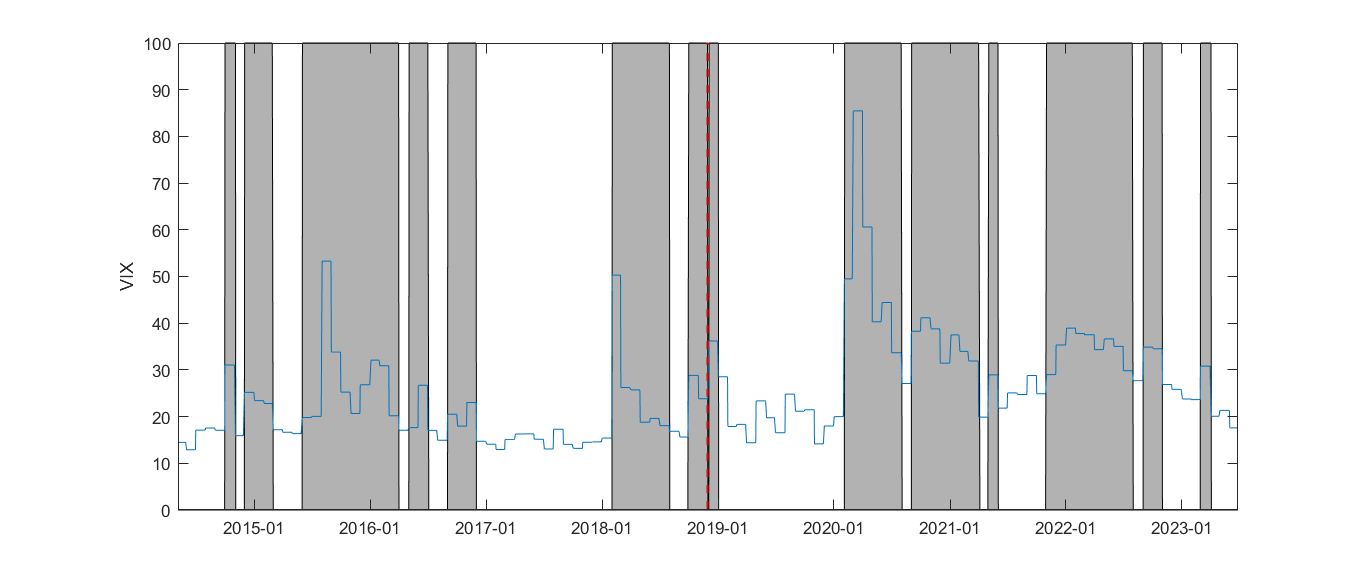

Furthermore, we investigate whether markets become more integrated during periods of high VIX. In particular, we divide the sample into four sub-samples: Before-HighVix, Before-LowVix, After-HighVix, and After-LowVix. Before-HighVix is the intersection of the before and high-VIX sub-samples, and so forth. By comparing the results between Before-HighVix and Before-LowVix (as well as between After-HighVix and After-LowVix), we find markets exhibit higher levels of integration during periods of higher VIX. This heightened integration is primarily driven by the increase of the magnitudes of loadings of the global factor during the Asian sub-period. This also means that, during periods of higher VIX, the returns of the Asian markets contain stronger trading signals for other markets.

1.1 Literature Review

There are several general approaches to address the issue of non-synchronous trading across international markets. The first approach is to use returns of relatively low frequencies: two-day returns (Forbes and Rigobon (2002), Corsetti et al. (2005), Dungey and Gajurel (2015)), weekly returns (Cappiello et al. (2006), Bekaert et al. (2009), Bekaert et al. (2014), Niţoi and Pochea (2019)), and monthly returns (Bekaert and Mehl (2019), Rapach et al. (2013)).

The second approach involves the use of intraday prices as the “pseudo” closing prices of one market to better match the closing prices of another market closing at an earlier time. For example, Schotman and Zalewska (2006) used an intraday price of the German market as its pseudo closing price when studying the German and Hungarian markets. The timing of the intraday price is chosen to match the closing time of the Hungarian market. Savva et al. (2009) and Gagnon and Karolyi (2009) also used this approach.

The third approach is attributed to Burns et al. (1998), who proposed a Vector Moving Average (VMA) structure for handling non-synchronous trading. This method has been widely utilized in various studies (Acharya et al. (2012), BenSaïda (2019), Opie and Riddiough (2020), Engle et al. (2015), Engle (2016) etc.).

The fourth approach involves using contemporaneous or lagged variables accordingly to reflect the time zone differences. For instance, Bekaert et al. (2023, p.11) wrote, “For the euro area, JP (Japanese) and EA (European) shocks that materialize before or during the European opening hours enter contemporaneously while the other shocks as well as the US shocks enter the information set on the next trading day.” Pukthuanthong and Roll (2009), Lehkonen (2015), Cai et al. (2009), He and Hamori (2021), and Marshall et al. (2021) all adopted this approach to account for non-synchronous trading.

We have a few remarks about these approaches. Using returns of relatively low frequencies as in the first approach prevents researchers from studying stock co-movement at higher frequencies. The second approach utilizes intraday data which might be unavailable or costly. The third approach is sensitive to the ordering of returns. For instance, using a vector of returns of Asia, Europe, and the US of the same calendar day might produce a different result from using a vector of returns of Europe and the US of the same calendar day, together with the return of Asia of the next day. The fourth approach is a very flexible way to address the non-synchronous trading issue, but does not allow one to identify the source of variation or its relative impacts as is possible in our framework.

The methodological approach of having global and continental factors, in some respects, is inspired by Lin et al. (1994) who investigated the correlation between the Nikkei 225 and S&P500 indices. They proposed a signal-extraction model containing a global factor and a local factor for the returns, but the model cannot generalize to a case of many stocks in multiple time zones easily. Our approach resembles that of Kose et al. (2003) who modeled 60 countries’ yearly macroeconomic aggregates (output, consumption and investment) using a dynamic factor model consisting of global, regional, and country-specific factors. The difference is that we work with daily stock returns and have the feature of sequential revelation of the international information, measured at 1/3-day frequency, in the returns of the three continents. Likewise, our approach is related to Hallin and Liška (2011) and Barigozzi et al. (2019), who considered generalized dynamic factor models in the presence of blocks,111Barigozzi et al. (2019) analyzed the US, European and Japanese stock returns. Their model allows for not only global or continental factors, but also factors affecting any two of the three markets. Nevertheless they found no global factors in their sample. and to nowcasting222In the nowcasting literature, researchers use factor models to extract the information contained in the data at higher frequencies than the target variable in order to forecast the target variable. (Giannone et al. (2008), Aruoba et al. (2009), Banbura et al. (2011), Banbura et al. (2013) etc.).

On the theoretical side, research about estimation of large factor models via the likelihood approach has matured over the last decade; Barigozzi (2023) provided the most recent and critical review on this topic. The likelihood approach enjoys several advantages compared to the principal components method (Banbura et al. (2013, p.204), Barigozzi (2023, p.37)). The most prominent advantage in our context (i.e., confirmatory factor models333See Jöreskog (1969) and Rubin and Thayer (1982) for early discussions of confirmatory factor models.) is its flexibility to incorporate (nonlinear) restrictions on the factor loading and covariance matrices, something cannot be easily achieved in the principal components method (Stock and Watson (2016, p.431)).

Doz et al. (2012) established an average rate of convergence of the estimated factors using a maximum likelihood estimator (MLE) via the Kalman smoother.444In fact, Doz et al. (2012) called their estimator the quasi-maximum likelihood estimator (QMLE) instead of the MLE. We re-label it as the MLE since we shall reserve the phrase QMLE for another purpose to be made specific shortly. Similarly for Bai and Li (2012)’s QMLE in the next paragraph. There is a rotation matrix attached to the estimated factors as the authors did not address identification of factor models. Moreover, they did not provide consistency or the limiting distributions of the loadings. In an important paper, Bai and Li (2012) took a different approach to study large exact factor models. Bai and Li (2012) obtained consistency, the rates of convergence, and the limiting distributions of the MLE of the factor loadings, idiosyncratic variances, and sample covariance matrix of factors. Factors are then estimated via a generalized least squares (GLS) method. Bai and Li (2016) generalized the results of Bai and Li (2012) to large approximate factor models.

Instead of maximizing a likelihood and finding the MLE, people usually use expectation maximization (EM) algorithms to estimate models in practice (Watson and Engle (1983), Quah and Sargent (1993), Doz et al. (2012), Rubin and Thayer (1982), Bai and Li (2012), Bai and Li (2016) etc.). Since an EM algorithm runs only for a finite number of iterations and converges to a local maximum, strictly speaking the estimate obtained by an EM algorithm is only an approximation to the MLE. However, in a breakthrough study, Barigozzi and Luciani (2022) showed that the estimate obtained by an EM algorithm, under the assumptions of their paper, converges to the MLE fast enough so that they are asymptotically equivalent.

The large sample results of the aforementioned studies are not applicable to our model because the proofs of these results are identification-scheme dependent. In particular, Bai and Li (2012), Bai and Li (2016) established their results under five popular identification schemes, none of which is consistent with our model.

1.2 Roadmap

The rest of the paper is structured as follows. Section 2 introduces the model. We explain our estimators and provide their large-sample theories in Sections 3 and 4, respectively. Section 5 conducts the Monte Carlo simulations to assess the performance of QML-all-res, and Section 6 presents empirical applications. Section 7 concludes. Additional materials and proofs are in the Online Supplement (OS in what follows).

1.3 Notation

Let denote the -dimensional Euclidean space. For , let and denote the Euclidean () and element-wise maximum () norms, respectively. Given a vector , creates a diagonal matrix whose diagonal elements are . We use to denote a conditional probability density function.

For an matrix , denotes the vector obtained by stacking columns of one underneath the other. The commutation matrix is an orthogonal matrix which translates to , i.e., . If is a symmetric matrix, its supradiagonal elements are redundant in the sense that they can be deduced from symmetry. If we eliminate these redundant elements from , we obtain a new vector, denoted . They are related by the full-column-rank, duplication matrix : . Conversely, , where is and the Moore-Penrose generalized inverse of . Let and denote the maximum and minimum eigenvalues of some real symmetric matrix, respectively. For any real matrix , let denote the Frobenius () norm.

Landau (order) notation in this paper, unless otherwise stated, should be interpreted in the sense that jointly, where and are the cross-sectional and temporal dimensions, respectively. We use to denote absolute positive constants (i.e., constants independent of anything which is a function of and/or ); identities of such s might change from one place to another.

2 Model

We begin by introducing our model in Section 2.1 and then provide its two-day representation in Section 2.2. As we shall demonstrate later, this two-day representation plays a crucial role in our QML estimation.

2.1 Setup

Our model is based on the closing prices of three stock markets in three continents, namely Asia, Europe and America; these closing prices are observed at their closing times. On a calendar day, the Asian market closes first, followed by the European market, and finally the American market closes. Let , and represent the logarithmic 24-hour close-to-close returns on day for stocks traded in the Asian, European, and American markets, respectively. Without loss of generality, we assume that each market has the same number of stocks: , and are all dimensional vectors. We formulate the following model for the logarithmic 24-hour close-to-close returns:

| (2.1) |

where and are the scalar unobserved global factors for the three sub-periods of day and s are the corresponding factor loadings. The three sub-periods are: the Asian sub-period (from the American close on day to the Asian close on day ), the European sub-period (from the Asian close on day to the European close on day ), and the American sub-period (from the European close on day to the American close on day ). and are the scalar unobserved 24-hour Asian, European, and American factors on day , respectively, and , and are the corresponding factor loadings. , and are the 24-hour Asian, European, and American idiosyncratic components, respectively. The global factor, along with and , is illustrated in Figure 1. We suppose for simplicity that the global factor follows an AR(1) process:

| (2.2) | ||||

where and for , .

Our model postulates that stock returns are driven by both a global factor and a continental factor. In particular, with the logarithmic 24-hour close-to-close returns of the three continents, we can identify the global factor within a sub-period (roughly a 1/3 day), since we observe the closing prices of some continent at the end of that sub-period. However, we are unable to identify the Asian continental factor, say, within the European sub-period since the closing prices of Europe do not provide any information about the Asian continental factor (see Assumption 1(iii)), but they do contain information about the global factor. The correlations of stock returns in different continents are solely due to the international news represented by the global factor.

Assumption 1.

-

(i)

The idiosyncratic components are independent across . For each , are identically and independently distributed (i.i.d.) across as .

-

(ii)

The innovations of the global factor are independent across . For each , are i.i.d. across as .

-

(iii)

The continental factors are independent across . For each , are i.i.d. across as . In addition, the continental factors are independent of the innovations of the global factor.

-

(iv)

The innovations of the global and continental factors are independent of the idiosyncratic components .

Assumption 1(i) assumes that the idiosyncratic components are independent across continents, which is reasonable. It also assumes that each of the three continental idiosyncratic components is i.i.d. across both the temporal and cross-sectional dimensions555The cross-sectional independence is implied by diagonality of the covariance matrix of normally distributed idiosyncratic components.. This is to simplify the large-sample theories but one could generalize this to weak temporal and cross-sectional dependence with more complicated notation and analysis.

Assumption 1(ii) says that the AR(1) process of the global factor is driven by Gaussian i.i.d. innovations. The variance is set to one for normalization. If the weak-form efficient market hypothesis (along with a time invariant risk premium) holds for stock markets across different time-zones, then one would expect . On the other hand, if certain international news takes more than a 1/3 day to fully unfold or dissipate, it is possible that .

Assumption 1(iii) assumes that the global and continental factors are independent so that a continental factor contains the information local to the continent itself. Again variances of the continental factors are set to one for normalization. In this way, the factors have clear economic interpretations – so the global and continental factors are indeed the “global” and “continental” factors, respectively. In fact, empiricists often orthogonalize global and regional factors (Bekaert et al. (2014)).

We have two reasons for modelling the continental factors being independent over days. First, since a continental factor measures the 24-hour continental information, orthogonal to the international news, we believe that investors can efficiently process such information at daily frequency, resulting in very weak auto-correlation of a continental factor. In contrast, the international news represented by the global factor, which measured at 1/3-day frequency, is more plausible to exhibit auto-correlation. Second, the focus of this paper is to study interdependence of stock markets across different time zones, so we abstain from putting unnecessary structures on the continental factors to complicate estimation or large-sample theories. Specifying an autoregressive structure for the continental factors may lead to less robust model estimates because of the possible convergence to local maxima when estimating the model.

Assumption 1(iv) assumes that and the innovations of the continental factors (i.e., standard normals) are independent of the idiosyncratic components . This is a standard assumption in the literature on dynamic factor models.

We have a few remarks about our model. First, it is not the same as a pure one-global-factor model. Although we only have one global factor, for each logarithmic 24-hour close-to-close return the global factor spans three sub-periods, with loadings on these sub-periods being different. On the contrary, a pure one-global-factor model would assume the same loadings on the three sub-periods, which is much more restrictive. In some sense, our model can be thought of as a constrained three-global-factors model. Nevertheless, this does not mean that our model is always suitable for any kind of data, so we conduct some misspecification analysis in our empirical application.

Second, our model has the potential to capture some international news affecting only two of the three continents. Suppose that some international news predominantly affects the European and American markets during the European sub-period. In this case, the Asian markets could have smaller loadings of the global factor during the European sub-period if this piece of international news is sufficiently important compared to other international news during the European sub-period in the sample. Nevertheless, some future work is needed in order to fully accommodate this modelling requirement.

2.2 The Two-Day Representation

We shall represent our model in a two-day form where every two calendar days is treated as a single time unit denoted by . Estimation and large sample theories are based on this two-day representation. Specifically, we have

| (2.3) |

for where

| (2.10) |

where is an abbreviation for , and so forth. We show in Section LABEL:sec_one_day_representation of the OS that a one-day representation is not identifiable under the case , when we ignore the auto-correlation between the stacked factors when setting up the likelihood.

The loading matrix has six row blocks of dimension . Let denote the th row of the th row block of , for and . In other words, is the factor loading for the th Asian stock in “day one”, while is the factor loading for the th European stock in “day two”. In the theoretical sections, we will use to denote factor loadings without referring to notation like or . Each contains ten zero elements and four non-zero elements.

The variances of the idiosyncratic components can be written compactly as

| (2.11) | |||

where is an abbreviation for , and so forth. The covariance matrix of is denoted by which is parametrized by :

| (2.12) |

The specific structures present in the loading matrix and the covariance matrix of factors distinguish our model from those considered by Bai and Li (2012).

3 Estimation

We propose two estimators of the parameters of the model: QML-just-identified and QML-all-res. In Section 3.1, we introduce the objective function for estimation. Sections 3.2 and 3.3 provide detailed expositions of these two estimators.

3.1 The QML Objective Function

Consider the two-day representation (2.3). Define and . Treating as i.i.d over , we can write down the quasi-log-likelihood of (scaled by ):

| (3.1) |

where . We call this the quasi-log-likelihood, and the estimator that maximizes (3.1) the QMLE, rather than the MLE, because are treated as i.i.d. over when setting up the likelihood. That is, we ignore the auto-correlation between and . This treatment is essential for setting up a simple likelihood function of the two-day representation and obtaining an analytic formula for the estimated factors. Treating as i.i.d. when setting up the likelihood, albeit incorrectly, will not destroy consistency or the asymptotic normality of the QMLE. This is the idea of working independence (Pan and Connett (2002)). Taking the auto-correlation between and into account when setting up the likelihood would result in the MLE. However, the large sample theories of the MLE are complicated because of the lack of an analytic formula for the estimated factors.

As mentioned by Bai and Li (2012), factors can be seen either as constant parameters or as a realization of a stochastic process. Treating factors as constant parameters allows for arbitrary dynamics in the factors. If one adopts this treatment, one might wonder whether the AR(1) assumption of the global factor, (2.2), is restrictive. Let us adopt this treatment for the moment for the two-day representation, which forms the basis of the QMLE. Under this treatment, the auto-correlation between and can be unspecified, but the covariance matrix of still needs to be specified. For example, Bai and Li (2012) set it to be an identity matrix in IC3, which means that the first 8 elements of , corresponding to the realizations of the global factor in 8 sub-periods, are orthonormal, which is more restrictive than in (2.12). Given that we already specify the auto-correlation of the first 8 elements of in (2.12), it seems innocuous to specify (2.2).

3.2 QML-Just-Identified

Utilizing the information that is symmetric, positive definite and that is diagonal, we showed in Section LABEL:sec_FOC of the OS that the resulting first-order conditions (FOCs) of (3.1), although guarantee the existence of a solution, could not be uniquely solved for or . We hence need to impose identification restrictions on the estimates of and to rule out the rotational indeterminacy. After imposing identification restrictions and a set of column-sign restrictions (Assumption 2), we obtain the QML-just-identified estimators and which are the unique solution of the following FOCs:666See Section LABEL:sec_FOC of the OS for details.

| (3.2) |

where . These FOCs are identical to (2.7) and (2.8) in Bai and Li (2012), which serve as the cornerstone for establishing the large sample theories. Although and imply more than restrictions on , imposing more than restrictions might result in no solution for (3.2).

How to select these restrictions from those implied by the model is crucial because we cannot impose a restriction that is not instrumental for identification of the two-day representation or establishment of the large-sample theories later. Let denote the loading of the th asset in the th row block of . Display (3.43) lists the rows of that have restrictions. Positions marked with ‘*’ have no restrictions; positions marked with ‘0’ are restricted to be 0; positions marked with ‘=’ are restricted to be equal to their counterparts while positions marked with ‘-’ mean these counterparts. Rows of without any restriction are not listed. In total, we impose 177 restrictions on (i.e., 156 zero and 21 equality restrictions).

| (3.43) |

The remaining 19 (=196-177) restrictions imposed on are:

| (3.44) | ||||

where is the th element of , and so forth. We now state the set of column-sign restrictions.

Assumption 2.

Suppose that the column signs of are known.

Note that Assumption 2 implies that all the column signs of are known. Bai and Li (2012) have made similar assumption as an implicit part of their identification schemes (IC2, IC3 and IC5) (see Bai and Li (2012, p.445, p.463)). Assumption 2 is justifiable in finance. If we use positive signs of the global and continental factors to represent positive sentiment conveyed by the news, then it is reasonable to assume that the factor loadings of the continental factors and the factor loadings of the global factor on a market in the sub-period most recent to the closure of that market, have more positive elements than negative ones. Thus in empirical applications we can choose the column signs of to be the ones resulting in most positive loadings so that Assumption 2 is satisfied. Such practice of fixing signs also exists in the literature of structural vector autoregressions (SVAR) ((Stock and Watson, 2016, p.451)).

Lemma 1.

Since the QML-just-identified estimator is unique, Lemma 1 is actually an implication of Proposition 1 in Section 4.1.

3.2.1 Computation and Initialization

Section LABEL:sec_compute_just of the OS explains how to compute QML-just-identified in practice. This is implemented by an EM algorithm, which is similar to the EM algorithm used for computing QML-all-res, to be explained in Section 3.3. It has been common practice to use the Principal Component (PC) estimator as the starting value of the EM algorithm (Doz et al. (2012), Bai and Li (2012), Barigozzi and Luciani (2022) etc.). We do not use this starting value because the PC estimator does not satisfy the restrictions implied by our model.

We now explain our choice of the starting value. It consists of two steps. First, let , , and represent the average returns on day of all the stocks in Asia, Europe, and America, respectively. We have

| (3.45) |

where for , and denotes the cross-sectional average of , and similarly for other loadings and . Note that in (3.45), and cannot be separately identified, so we only present their sum ; (2.2) still holds. We can use the classical maximum likelihood (ML) method to estimate (3.45) because the number of parameters of (3.45) is finite. In particular, we set up the log-likelihood function based on the Kalman filter and use the Quasi-Newton-Raphson algorithm to optimize the parameters. The large sample theory for the classical MLE ensures that the parameter estimates are -consistent. The estimated and are used as the starting values for and loadings of the global factor, respectively. In other words, all the elements of the starting value for are set to the estimated for and .

Second, consider (2.1) and replace and with their starting values in the first step. For each continent, assume all the elements of or are the same. Use ML to estimate this restricted version of the model, and use the estimated loadings of the continental factors and idiosyncratic variances as the starting values for and , respectively, for . To lessen the computational burden, one could use only a subset of the stocks, say, the first ten stocks in each continent. In our experience, this set of starting values work quite well.

3.3 QML-All-Res

We now improve upon the QML-just-identified estimator and propose a QML-all-res estimator that takes all the restrictions implied by , and into account. The idea is that all the restrictions could be incorporated in an EM algorithm. The complete quasi-log-likelihood of the two-day representation is

| (3.46) | |||

We emphasize again that we do not assume to be i.i.d. over in this paper, but we treat as i.i.d. when setting up the likelihood function. However, we do not rely on being i.i.d. in the derivation of the large sample theories.

Let denote the four non-zero elements in , which are the parameters of interest of loadings in the case of QML-all-res. The procedure of the EM algorithm is as follows:

-

(i)

Initialization. Let , where and are the QML-just-identified estimators for and , respectively, and is improved upon , the QML-just-identified estimator for (see Section LABEL:sec_def_of_minus of the OS for the definition of ).

-

(ii)

E-step. Let denote the estimate of in the th iteration. The E-step in the th iteration is to compute , where denotes the expectation with respect to the conditional density at .

- (iii)

- (iv)

We have some remarks about our EM algorithm. First, in the literature, there are two types of EM algorithms for estimation of factor models. The first type was used by Doz et al. (2012), and originally introduced in the 1980s-1990s, say, by Watson and Engle (1983) and Quah and Sargent (1993) (also see Barigozzi (2023, p.23) for a brief discussion on this). The second type was used by Bai and Li (2012) and originally proposed by Rubin and Thayer (1982). Both types of the EM algorithms use, in terms of our notation, in the E-step, where . The difference is that in the second type of EM algorithm because are independent – or treated as independent during estimation – over , is reduced to in the E-step, whereas in the first type of EM algorithm, are correlated over . Our EM algorithm is the second type.

Second, scholars usually consider the output of an EM algorithm as equivalent to the QML estimator (e.g., Doz et al. (2012), Bai and Li (2012)). This might not be true. Barigozzi (2023, p.24) wrote, “The EM algorithm defines a continuous path in the parameter space from the starting point to the stopping point along which the log-likelihood monotonically increases without leaping over valleys.” This implies that the EM algorithm only converges to a local maximum of the log-likelihood while the QMLE is the global maximum. Initialize the EM algorithm for QML-all-res with allows the local maximum to which the EM algorithm converges, to be close to the global maximum. This has some flavor of the one-step estimator (van der Vaart (1998, p.72)). Theory-wise, using as the starting value allows us to establish the large-sample theories of the QML-all-res estimator in Section 4.2 as the rates of convergence of the starting value serve as a stepping stone in the proof.

Third, we provide more details about step (iii) (i.e., the M-step). We derived in Section LABEL:sec_res_intro2 of the OS that

| (3.47) |

for and , where is the th element of , and is a selection matrix to pick out the non-zero elements in (i.e., , and ). Moreover, we have

| (3.48) |

for and . As for :

| (3.49) |

The analytic formula of the FOC of (3.49) is given by (LABEL:mle4_10) in the OS. Alternatively, one could obtain with numerical optimization, whose computational burden is almost negligible. We remark that alternative objective functions other than (3.49) could be used to compute in the th iteration. In fact, the QML-all-res estimator for could be set to any consistent estimator of in the step of initialization, and in the following iterations we do not update it. When evaluating (3.47), (3.48) and (3.49), one needs to compute and of the E-step. We derive in Section LABEL:sec_res_intro of the OS that

| (3.50) | ||||

4 Large Sample Theories

We make the following assumption. Let be a large constant.

Assumption 3.

-

(i)

The factor loadings satisfy for all and . All elements of are restricted to a compact set for all and .

-

(ii)

Assume for all and . Also is restricted to a compact set for all and .

-

(iii)

is restricted to be in a set consisting of all positive definite matrices with all the elements bounded in the interval .

-

(iv)

Suppose that is a positive definite matrix.

The first half of Assumption 3(i) is the same as Assumption (C.1) of Bai and Li (2012), whereas the second half of Assumption 3(i) requires that all the elements of the QML-just-identified estimator for loadings, , are estimated within a compact set. Assumption 3(ii) is the same as Assumption (C.2) and the first sentence of Assumption D of Bai and Li (2012). Assumption 3(ii) implies that the moment generating functions of are uniformly (in ) bounded. Assumption 3(iii) is part of Assumption D of Bai and Li (2012) and implies that and . Assumption 3(iv) is part of Assumption (C.3) of Bai and Li (2012).

4.1 QML-Just-Identified

We now present the large sample theories of the QML-just-identified estimator. The idea of the proof is based on that of Bai and Li (2012), but is considerably more involved because our identification scheme is non-standard.

Proposition 1.

Proposition 1(ii)-(iv) resemble Theorem 5.1 of Bai and Li (2012) and establish some average rates of convergence for and , and the rate of convergence for . Proposition 1(i) establishes the rate of convergence for the individual loading estimator . Theorem LABEL:thm5.2 in Section LABEL:sec_proof_of_just_clt of the OS establishes the asymptotic distributions of the QML-just-identified estimators. They are asymptotically normal, albeit inefficient. We feel that perhaps Proposition 1 is more important than Theorem LABEL:thm5.2 because the rates of convergence are the stepping stone for obtaining the large-sample theories for the QML-all-res estimator, which is the estimator we recommend in practice.

4.2 QML-All-Res

We will now present the large sample theories of the QML-all-res estimator. We first define the infeasible OLS estimators of , which not only treat as known, but also incorporate all the restrictions implied by and .

where is defined in (3.47) and . That is, these OLS estimators are the maximizers of the complete quasi-log-likelihood of the two-day representation , treating as known and taking into account of all the restrictions implied by , and . Corollary LABEL:coro_rate in Section LABEL:sec_coro of the OS establishes the uniform rates of convergence for the QML-all-res estimators. Such uniform rates of convergence are new to the literature.

Theorem 1.

Suppose that the assumptions of Proposition 1 hold. If and as , we have

-

(i)

where is the selection matrix to pick out the non-zero elements in for and .

-

(ii)

(4.2) for and .

-

(iii)

where

Theorem 1 presents the asymptotic distributions of the QML-all-res estimators. This is a consequence of the OLS estimators having these asymptotic distributions and the asymptotic equivalence of QML-all-res and the OLS estimators. Comparing Theorems 1 and LABEL:thm5.2 in the OS, we see that and are more efficient than the QML-just-identified counterparts because the asymptotic variances are smaller. This is expected as QML-all-res incorporates in more information than QML-just-identified does. Moreover, instead of having an estimate for matrix as QML-just-identified does, we now have an estimate for the only unknown parameter in : . Consistent estimates of the asymptotic variances could be obtained by replacing the unknown quantities with the QML-all-res estimates. In practice, we recommend to use the QML-all-res estimators.

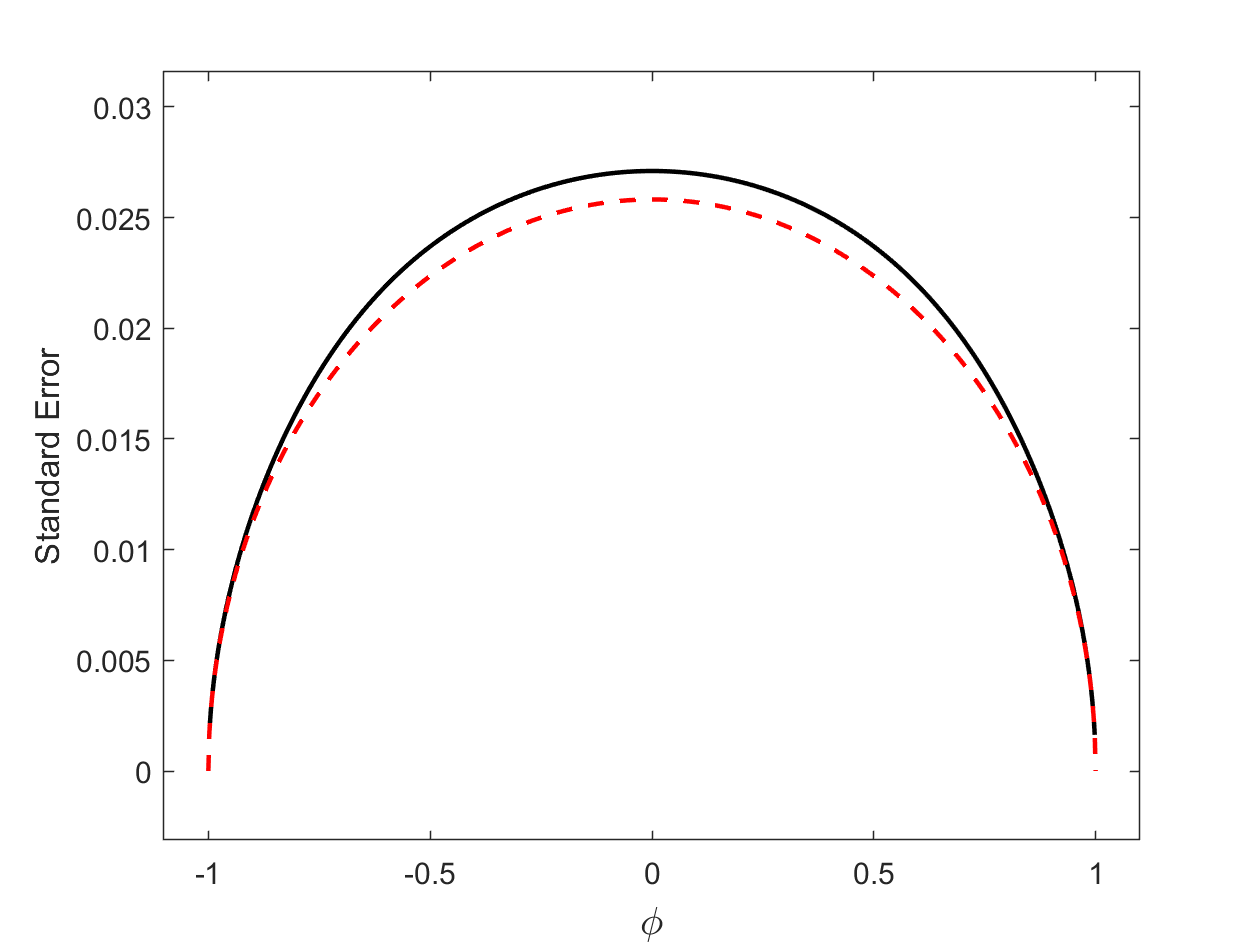

We also would like to discuss a bit about the complicated formula of . The standard error for (or ) is . Recall that both and ignore the auto-correlation between and when setting up the objective functions. If one could observe and takes the auto-correlation between and into account when setting up the objective function, the most efficient estimator of would be , where is a convenient way to denote the global factor in a sub-period of a day.777See (LABEL:res_r91) of the OS for the precise definition of . It is easy to show that the standard error for is . Figure 2 plots the standard errors of (or ) and against all the possible values of at . The black solid line denotes the standard error of (or ). The red dashed line denotes the standard error of . We see that is marginally more efficient than (or ). The gap between the black solid and red dashed lines is the cost of ignoring the auto-correlation between and . The gap is largest when is smallest. This is intuitive because when is large, the covariance matrix of , , already contains enough information for so ignoring the cross--period correlation of incurs minimal efficiency loss.

4.3 Estimated Factors

We now provide a large-sample result for estimated factors:

for .

Theorem 2.

Theorem 2 establishes the asymptotic distributions for the estimated factors. These asymptotic distributions are the same as Theorem 6.1(IC3) of Bai and Li (2012) and Proposition 5 of Barigozzi (2023) under the case of an exact factor model. As Barigozzi (2023) has pointed out, we need to consistently estimate , as is some sort of cross-sectional average, and at the same time we need to consistently estimate , as we use the QML-all-res estimators , which are consistent only if . For both Theorems 1 and 2 holding, we need for some , which is in line with the discussion following Theorem 2 of Barigozzi and Luciani (2022). The asymptotic covariance matrix could be consistently estimated by (see (LABEL:f_r15) of the OS).

5 Monte Carlo Simulations

5.1 Baseline Simulations

In this section, we conduct Monte Carlo simulations to evaluate performance of QML-all-res. We specify and , and a burn-in sample of 250 periods. Note that and correspond to two and six years’ daily data, respectively. Set . For , the idiosyncratic variance is drawn from uniform for , and

where are the th component of , , , , respectively, for , and , , , , , , and are all drawn from uniform. The econometrician observes those logarithmic 24-hour close-to-close returns. He is aware of the structure of the true model, but does not know the values of those parameters.

The number of the Monte Carlo samples is chosen to be 1000. From these 1000 Monte Carlo samples, we calculate the following three quantities for evaluation:

-

(i)

the root mean square error (RMSE) of the quantity of interest,

-

(ii)

the average of the standard errors (Ave.se) of the estimated elements of the quantity of interest.

-

(iii)

the average of the coverage probabilities (Cove) of the confidence intervals, formed by the point estimates 1.96the standard errors, of the elements of the quantity of interest.

Table 2 presents the RMSE, Ave.se, and Cove of the QML-all-res estimator. We see that the RMSE and Ave.se of the factor loadings are in general quite close to each other. However, in the case of , the RMSE is slightly larger than the Ave.se, indicating that the standard errors are slightly underestimated when . When increases to 200, the Ave.se gets closer to the RMSE. When increases from 100 to 200, the Cove improves considerably. We consider the size performance of QML-all-res pretty good as it is well known in the literature that size of large-dimensional factor models is difficult to control.

The performance of QML-all-res for is very good, with the Cove being very close to 0.95. Obtaining a good estimate of is relatively straightforward. In unreported Monte Carlo simulations, even the QML-just-identified estimator produces a reasonably accurate estimate of . When , or 750, the standard error of is under-estimated to some extent, resulting in a slightly lower Cove. However, the Cove improves as increases to 200.

| RMSE | Ave.se | Cove | RMSE | Ave.se | Cove | ||

|---|---|---|---|---|---|---|---|

| 0.0634 | 0.0528 | 0.8943 | 0.0363 | 0.0306 | 0.8998 | ||

| 0.0661 | 0.0555 | 0.8923 | 0.0376 | 0.0323 | 0.9002 | ||

| 0.0683 | 0.0557 | 0.8842 | 0.0385 | 0.0323 | 0.8953 | ||

| 0.0575 | 0.0520 | 0.9224 | 0.0332 | 0.0303 | 0.9243 | ||

| 0.0668 | 0.0520 | 0.8760 | 0.0381 | 0.0308 | 0.8830 | ||

| 0.0716 | 0.0549 | 0.8588 | 0.0398 | 0.0314 | 0.8760 | ||

| 0.0649 | 0.0530 | 0.8890 | 0.0372 | 0.0311 | 0.8949 | ||

| 0.0613 | 0.0538 | 0.9148 | 0.0349 | 0.0313 | 0.9230 | ||

| 0.0631 | 0.0536 | 0.9002 | 0.0364 | 0.0306 | 0.9042 | ||

| 0.0643 | 0.0544 | 0.8984 | 0.0370 | 0.0314 | 0.9017 | ||

| 0.0632 | 0.0525 | 0.8943 | 0.0363 | 0.0304 | 0.8989 | ||

| 0.0614 | 0.0559 | 0.9187 | 0.0352 | 0.0319 | 0.9236 | ||

| 0.0820 | 0.0792 | 0.9366 | 0.0471 | 0.0460 | 0.9418 | ||

| 0.0439 | 0.0276 | 0.8450 | 0.0213 | 0.0158 | 0.8750 | ||

| RMSE | Ave.se | Cove | RMSE | Ave.se | Cove | ||

| 0.0552 | 0.0515 | 0.9301 | 0.0319 | 0.0298 | 0.9309 | ||

| 0.0564 | 0.0537 | 0.9328 | 0.0323 | 0.0307 | 0.9353 | ||

| 0.0555 | 0.0522 | 0.9339 | 0.0320 | 0.0303 | 0.9359 | ||

| 0.0558 | 0.0538 | 0.9402 | 0.0322 | 0.0313 | 0.9424 | ||

| 0.0570 | 0.0505 | 0.9186 | 0.0327 | 0.0296 | 0.9222 | ||

| 0.0580 | 0.0526 | 0.9207 | 0.0334 | 0.0304 | 0.9225 | ||

| 0.0557 | 0.0510 | 0.9273 | 0.0321 | 0.0297 | 0.9303 | ||

| 0.0558 | 0.0531 | 0.9369 | 0.0321 | 0.0307 | 0.9396 | ||

| 0.0587 | 0.0520 | 0.9137 | 0.0337 | 0.0303 | 0.9167 | ||

| 0.0587 | 0.0529 | 0.9172 | 0.0339 | 0.0305 | 0.9177 | ||

| 0.0585 | 0.0510 | 0.9109 | 0.0336 | 0.0294 | 0.9137 | ||

| 0.0564 | 0.0530 | 0.9319 | 0.0325 | 0.0305 | 0.9344 | ||

| 0.0810 | 0.0791 | 0.9400 | 0.0466 | 0.0460 | 0.9445 | ||

| 0.0309 | 0.0272 | 0.9230 | 0.0176 | 0.0157 | 0.9200 | ||

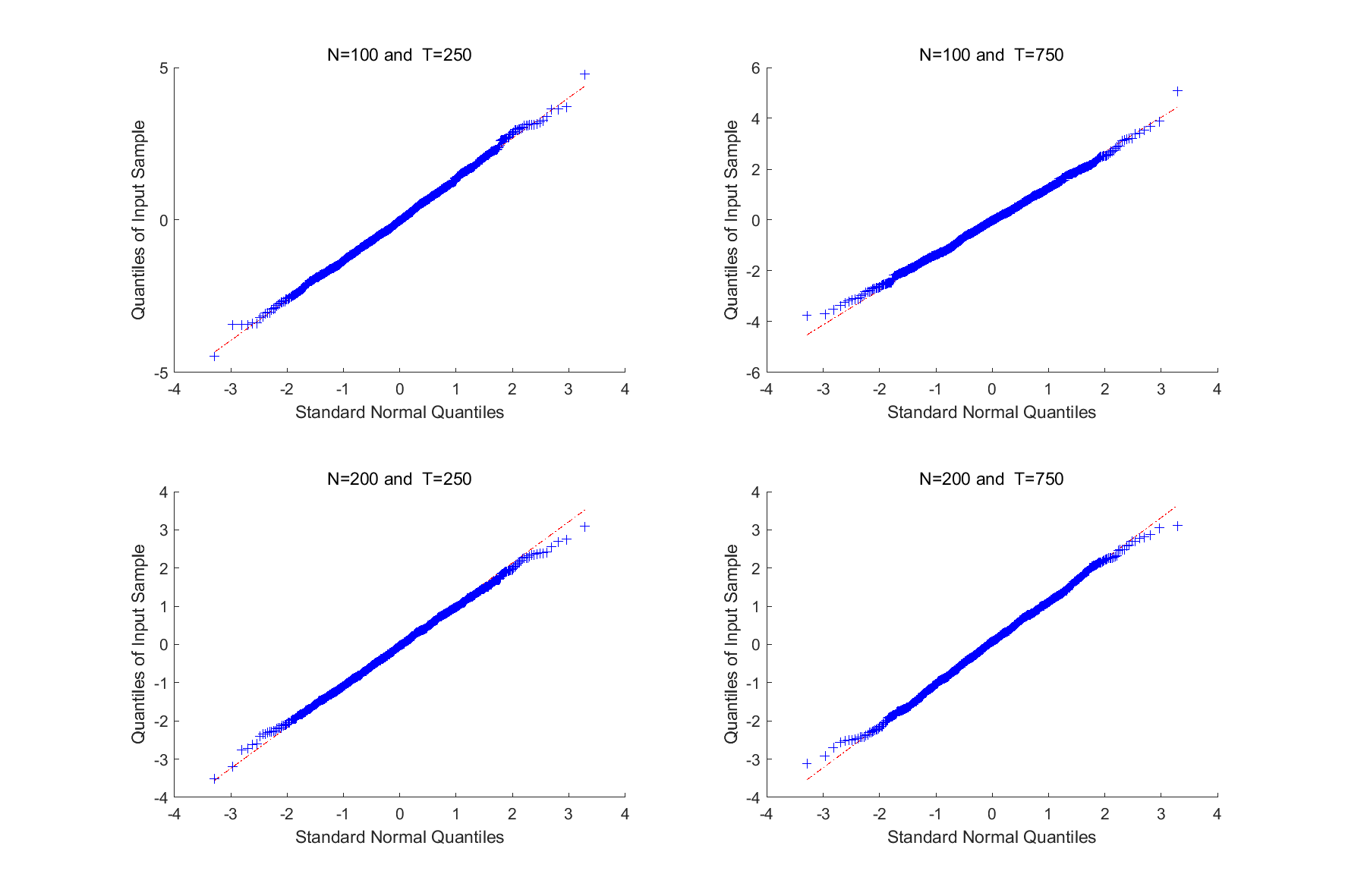

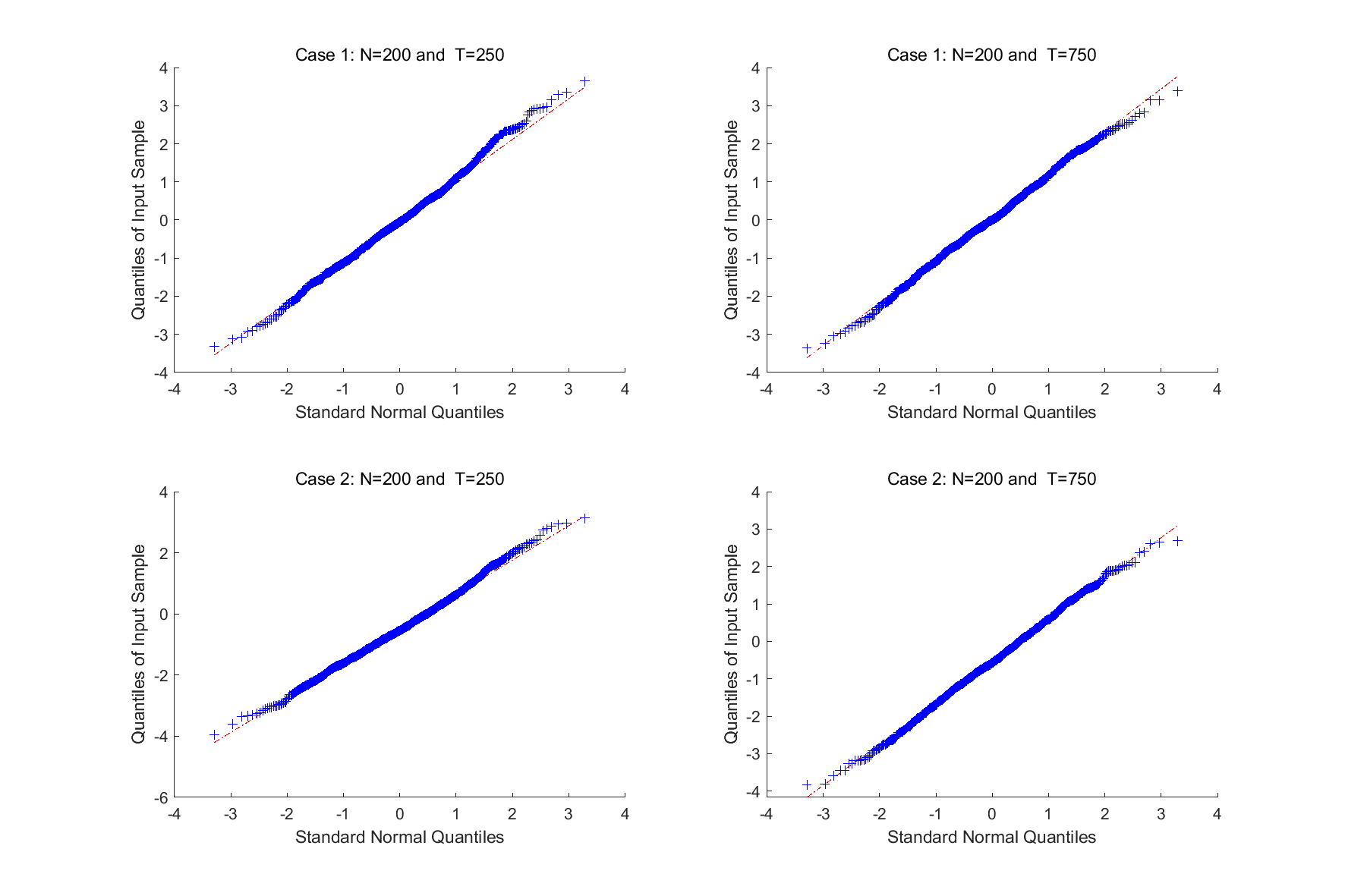

In Figures 3 and 4, we present the QQ plots of the 10th element of the standardized QML-all-res of and standardized , respectively, for illustrative purposes. The standardized estimator is calculated as the difference between the estimator and true value, divided by the standard error. These two plots demonstrate that our standardized estimators closely resemble the standard normal.

5.2 Simulations with Non-Gaussian Data

This section investigates simulations using data that deviate from the assumptions of the model. The parameters are generated in the same way as in Section 5.1. We draw each of , , , , , and independently across time from a distribution with 8 degrees of freedom and standardized to have variance 1. Furthermore, we include cross-correlation and auto-correlation in the idiosyncratic components. Specifically for , we generate in the following way:

where each of the elements in is independently across time drawn from a distribution with 8 degrees of freedom and standardized to have variance 1, and is an matrix which controls cross-correlation in the idiosyncratic components. We specify for , and 0 otherwise. We consider the following two cases:

-

Case 1: and . In this case, we only consider non-normal data but switch off cross-correlation and auto-correlation in the idiosyncratic components.

-

Case 2: and . In this case, we consider not only non-normal data but also cross-correlation and auto-correlation in the idiosyncratic components. We use a small because it is widely agreed that auto-correlation is quite small in finance.

The simulation results of these two cases are presented in Table 3. The performance of Case 1 or 2 is, as expected, worse than the baseline simulations, but still acceptable. The estimated standard errors become underestimated to some extent, a well known fact when fitting data generated from distributions using normal distributions. Take (i.e., ) as an example. The asymptotic variance of is a function of . Under Gaussianity, , so we can simplify the asymptotic variance to as in (4.2). Under non-Gaussianity, underestimates , so a straightforward solution is to use the sample 4th moment of to compute the standard error of . Doing so indeed improves Ave.se and Cove (see the rows of in Table 3). We leave the theories covering non-normal data for future research. However, in the empirical application in Section 6, we observe that most estimates of the parameters are highly significant with statistics much larger than 2. Therefore, slight underestimation of the standard errors has little impact on drawing inference in our application.

| Case 1 | |||||||

|---|---|---|---|---|---|---|---|

| RMSE | Ave.se | Cove | RMSE | Ave.se | Cove | ||

| 0.0563 | 0.0511 | 0.9244 | 0.0327 | 0.0297 | 0.9230 | ||

| 0.0567 | 0.0538 | 0.9313 | 0.0327 | 0.0310 | 0.9331 | ||

| 0.0561 | 0.0527 | 0.9307 | 0.0321 | 0.0304 | 0.9337 | ||

| 0.0565 | 0.0542 | 0.9367 | 0.0323 | 0.0313 | 0.9409 | ||

| 0.0587 | 0.0515 | 0.9093 | 0.0339 | 0.0294 | 0.9105 | ||

| 0.0581 | 0.0526 | 0.9197 | 0.0339 | 0.0303 | 0.9180 | ||

| 0.0567 | 0.0511 | 0.9227 | 0.0328 | 0.0299 | 0.9237 | ||

| 0.0564 | 0.0530 | 0.9337 | 0.0323 | 0.0308 | 0.9384 | ||

| 0.0603 | 0.0507 | 0.9041 | 0.0350 | 0.0302 | 0.9042 | ||

| 0.0603 | 0.0534 | 0.9088 | 0.0344 | 0.0303 | 0.9144 | ||

| 0.0595 | 0.0511 | 0.9050 | 0.0345 | 0.0296 | 0.9048 | ||

| 0.0575 | 0.0532 | 0.9256 | 0.0330 | 0.0307 | 0.9298 | ||

| 0.1058 | 0.0794 | 0.8547 | 0.0613 | 0.0461 | 0.8568 | ||

| 0.1058 | 0.1011 | 0.9206 | 0.0613 | 0.0592 | 0.9331 | ||

| 0.0306 | 0.0272 | 0.9070 | 0.0178 | 0.0157 | 0.9150 | ||

| Case 2 | |||||||

| RMSE | Ave.se | Cove | RMSE | Ave.se | Cove | ||

| 0.0572 | 0.0510 | 0.9184 | 0.0336 | 0.0297 | 0.9147 | ||

| 0.0581 | 0.0537 | 0.9233 | 0.0339 | 0.0309 | 0.9224 | ||

| 0.0580 | 0.0524 | 0.9205 | 0.0338 | 0.0303 | 0.9187 | ||

| 0.0606 | 0.0540 | 0.9160 | 0.0364 | 0.0312 | 0.9038 | ||

| 0.0599 | 0.0516 | 0.9030 | 0.0349 | 0.0294 | 0.8999 | ||

| 0.0593 | 0.0522 | 0.9119 | 0.0347 | 0.0302 | 0.9094 | ||

| 0.0581 | 0.0515 | 0.9150 | 0.0339 | 0.0299 | 0.9140 | ||

| 0.0600 | 0.0529 | 0.9145 | 0.0357 | 0.0308 | 0.9071 | ||

| 0.0620 | 0.0502 | 0.8944 | 0.0364 | 0.0302 | 0.8907 | ||

| 0.0615 | 0.0529 | 0.9014 | 0.0355 | 0.0302 | 0.9020 | ||

| 0.0606 | 0.0508 | 0.8986 | 0.0352 | 0.0295 | 0.8969 | ||

| 0.0604 | 0.0530 | 0.9104 | 0.0359 | 0.0306 | 0.9034 | ||

| 0.1049 | 0.0790 | 0.8551 | 0.0611 | 0.0460 | 0.8559 | ||

| 0.1049 | 0.0986 | 0.9154 | 0.0611 | 0.0577 | 0.9265 | ||

| 0.0347 | 0.0273 | 0.8830 | 0.0198 | 0.0157 | 0.8780 | ||

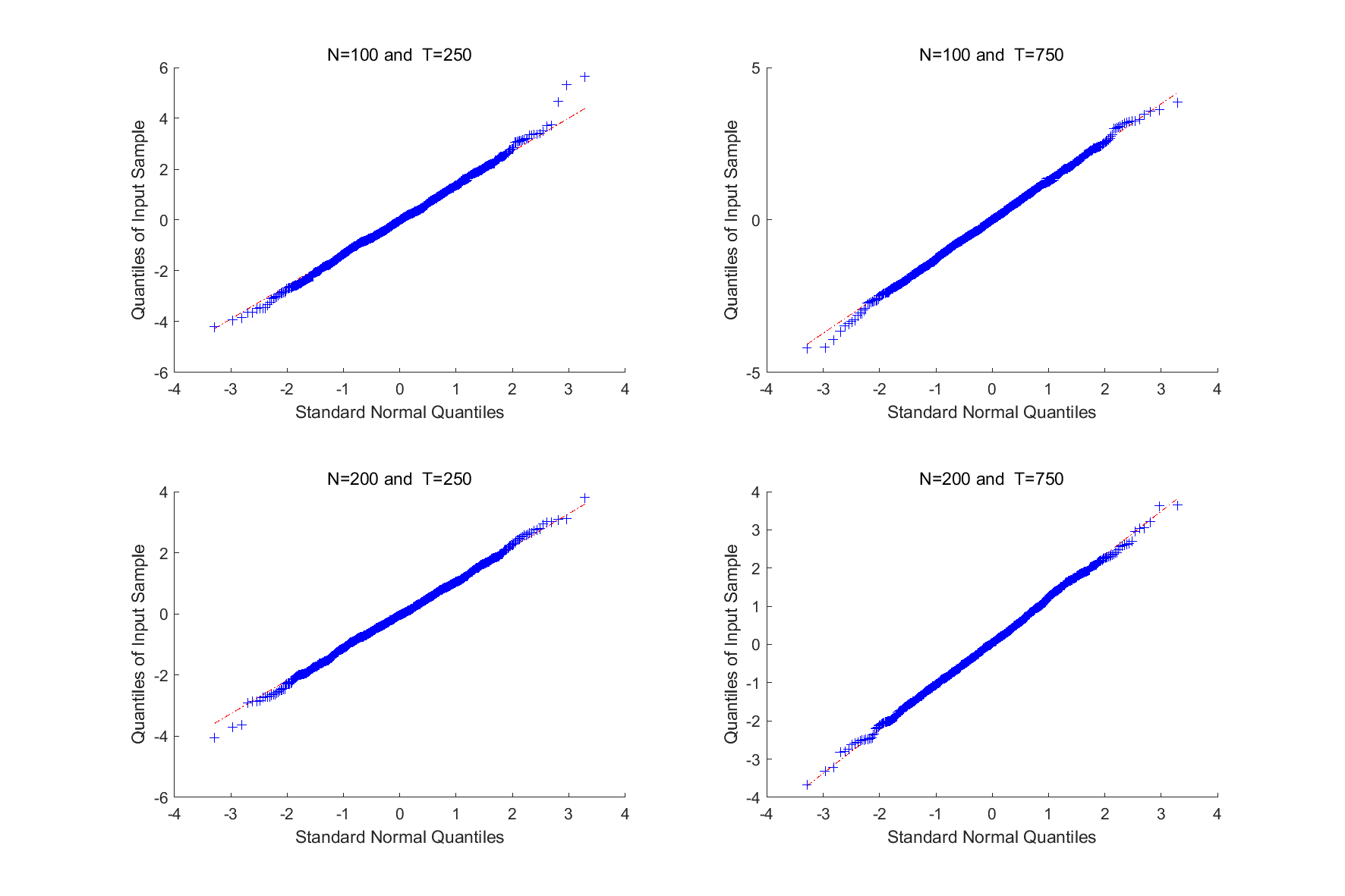

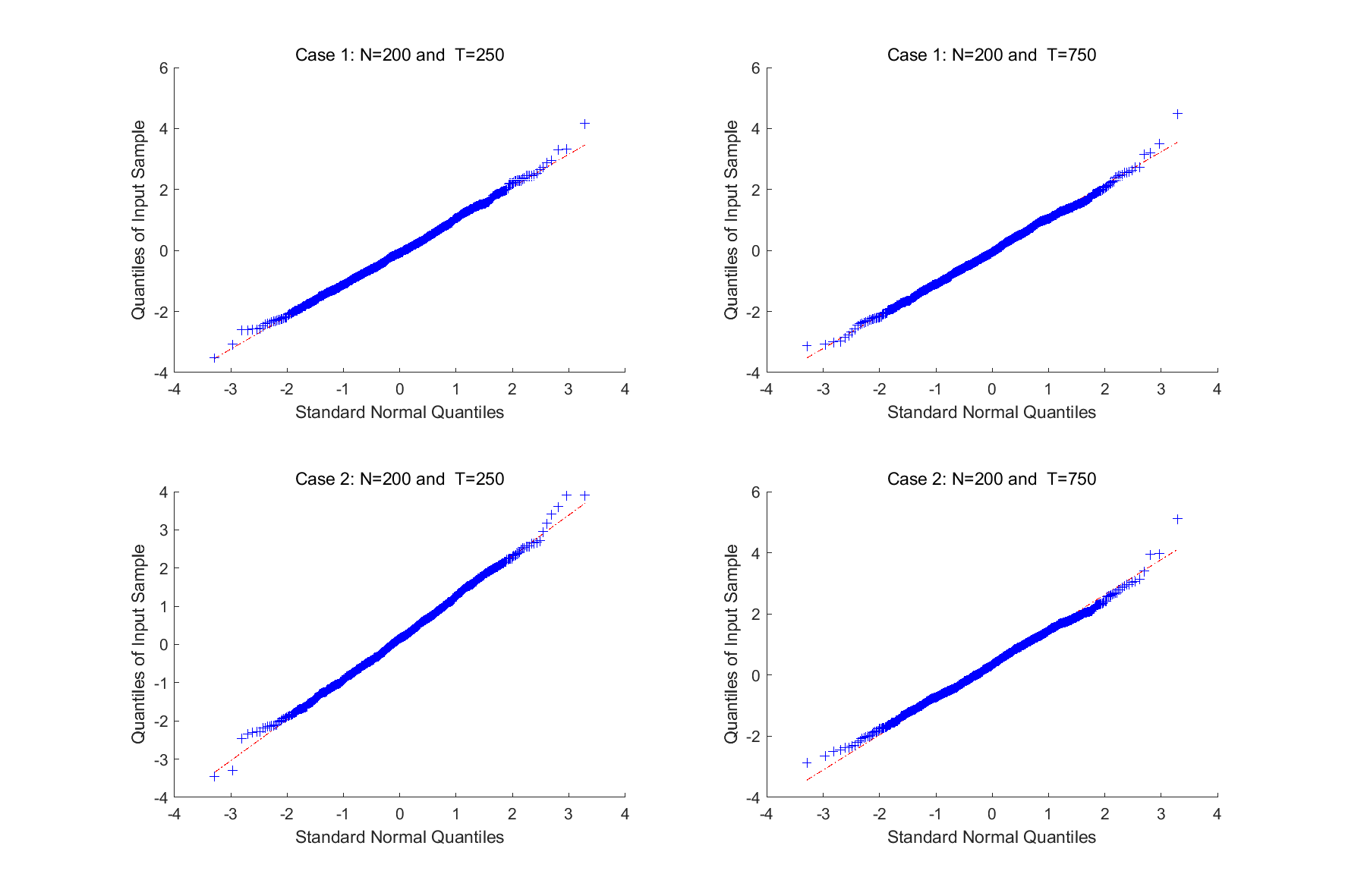

In Figures 5 and 6, we present the QQ plots of the 10th element of the standardized QML-all-res of and standardized , respectively, for illustrative purposes. The standardized estimator is calculated as the difference between the estimator and true value, divided by the standard error. These two plots demonstrate that our standardized estimators closely resemble the standard normal.

6 Empirical Application

We apply our model to MSCI equity indices of 42 developed and emerging markets. Daily indices were obtained from Eikon.888The markets include Australia, Austria, Belgium, Brazil, Canada, Chile, Colombia, Czech Republic, Denmark, Finland, France, Germany, Greece, Hong Kong, Hungary, India, Indonesia, Ireland, Italy, Japan, Mainland China, Malaysia, Mexico, Netherlands, New Zealand, Norway, Peru, Philippines, Poland, Portugal, Singapore, South Africa, South Korea, Spain, Sweden, Switzerland, Taiwan, Thailand, Turkey, United Kingdom, United States. The data are from May 5th, 2014 (the date when most indices are available) to June 23rd, 2023. For most markets, there are 6 indices (in USD currency): Large-Growth, Mid-Growth, Small-Growth, Large-Value, Mid-Value, and Small-Value. We have 212 indices in total. Dates with more than 50 missing indices are excluded.

We categorize these markets into three continents based on their closing times: Asia-Pacific, Europe, and Americas. We exclude the Israeli market from our sample because its closing time is far away from those of Asia-Pacific or Europe. All the returns have been demeaned. To better compare magnitudes of the loadings, we also standardize the returns so that they have unit variances (Stock and Watson (2016, p.422)). We shall use QML-all-res.

6.1 Basic Results

Table 4 displays the estimated factor loadings and idiosyncratic variances for Asia-Pacific. The indices for Mainland China, Hong Kong, and Japan are all presented, while only the Mid-Value and Mid-Growth indices are shown for other Asia-Pacific markets in the interest of space. Recall that represents the loading of the global factor during the Asian sub-period (from the American close on day to the Asian close on day ), and likewise for others. We have made two main observations. First, for the Asia-Pacific markets, the global factor has the largest loadings during the Asian sub-period, with Australia having the largest ones at approximately 0.7. Second, Mainland China and Hong Kong have large loadings of the continental factor, around 0.7, whereas Japan has minimal loadings of the continental factor.

| Mainland China LG | 0.385 (0.011) | 0.053 (0.011) | -0.144 (0.011) | 0.719 (0.011) | 0.295 (0.014) | |

|---|---|---|---|---|---|---|

| Mainland China LV | 0.429 (0.009) | 0.132 (0.009) | -0.031 (0.009) | 0.754 (0.010) | 0.211 (0.010) | |

| Mainland China MG | 0.371 (0.011) | 0.065 (0.011) | -0.142 (0.011) | 0.734 (0.011) | 0.284 (0.013) | |

| Mainland China MV | 0.386 (0.008) | 0.106 (0.008) | -0.086 (0.008) | 0.823 (0.008) | 0.142 (0.007) | |

| Mainland China SG | 0.338 (0.009) | 0.087 (0.009) | -0.159 (0.008) | 0.816 (0.009) | 0.173 (0.008) | |

| Mainland China SV | 0.364 (0.008) | 0.113 (0.008) | -0.089 (0.008) | 0.819 (0.008) | 0.162 (0.008) | |

| Hong Kong LG | 0.399 (0.012) | 0.136 (0.012) | 0.001 (0.012) | 0.673 (0.012) | 0.351 (0.017) | |

| Hong Kong LV | 0.433 (0.014) | 0.136 (0.014) | 0.140 (0.014) | 0.536 (0.014) | 0.457 (0.022) | |

| Hong Kong MG | 0.393 (0.015) | 0.078 (0.015) | -0.071 (0.015) | 0.518 (0.016) | 0.554 (0.026) | |

| Hong Kong MV | 0.432 (0.013) | 0.128 (0.013) | 0.079 (0.013) | 0.607 (0.013) | 0.400 (0.019) | |

| Hong Kong SG | 0.377 (0.009) | 0.150 (0.009) | -0.094 (0.009) | 0.780 (0.010) | 0.204 (0.010) | |

| Hong Kong SV | 0.402 (0.011) | 0.168 (0.011) | 0.013 (0.010) | 0.726 (0.011) | 0.260 (0.012) | |

| Japan LG | 0.343 (0.014) | 0.604 (0.014) | -0.155 (0.013) | 0.116 (0.014) | 0.429 (0.020) | |

| Japan LV | 0.328 (0.014) | 0.574 (0.014) | -0.072 (0.014) | 0.061 (0.015) | 0.483 (0.023) | |

| Japan MG | 0.340 (0.014) | 0.598 (0.014) | -0.162 (0.014) | 0.105 (0.014) | 0.443 (0.021) | |

| Japan MV | 0.339 (0.014) | 0.578 (0.014) | -0.064 (0.014) | 0.058 (0.014) | 0.467 (0.022) | |

| Japan SG | 0.334 (0.014) | 0.594 (0.014) | -0.162 (0.014) | 0.095 (0.014) | 0.456 (0.022) | |

| Japan SV | 0.326 (0.014) | 0.583 (0.014) | -0.085 (0.014) | 0.043 (0.015) | 0.476 (0.022) | |

| South Korea MV | 0.500 (0.014) | 0.239 (0.014) | 0.248 (0.013) | 0.344 (0.014) | 0.432 (0.020) | |

| Taiwan MV | 0.432 (0.014) | 0.263 (0.014) | 0.182 (0.014) | 0.388 (0.015) | 0.490 (0.023) | |

| Australia MV | 0.724 (0.012) | 0.275 (0.012) | -0.010 (0.012) | 0.037 (0.012) | 0.336 (0.016) | |

| India MV | 0.517 (0.016) | -0.038 (0.016) | 0.259 (0.016) | 0.207 (0.017) | 0.625 (0.029) | |

| Indonesia MV | 0.438 (0.016) | 0.017 (0.016) | 0.341 (0.016) | 0.199 (0.017) | 0.632 (0.030) | |

| Malaysia MV | 0.478 (0.016) | 0.068 (0.015) | 0.331 (0.015) | 0.241 (0.016) | 0.564 (0.027) | |

| New Zealand MV | 0.519 (0.017) | 0.192 (0.017) | -0.013 (0.017) | -0.019 (0.017) | 0.663 (0.031) | |

| Philippines MV | 0.341 (0.018) | 0.081 (0.018) | 0.277 (0.017) | 0.210 (0.018) | 0.724 (0.034) | |

| Singapore MV | 0.642 (0.014) | 0.138 (0.014) | 0.169 (0.014) | 0.239 (0.014) | 0.441 (0.021) | |

| Thailand MV | 0.521 (0.016) | -0.001 (0.016) | 0.247 (0.016) | 0.219 (0.016) | 0.613 (0.029) | |

| South Korea MG | 0.477 (0.014) | 0.251 (0.014) | 0.182 (0.014) | 0.362 (0.015) | 0.476 (0.022) | |

| Taiwan MG | 0.412 (0.015) | 0.263 (0.015) | 0.105 (0.015) | 0.375 (0.016) | 0.555 (0.026) | |

| Australia MG | 0.729 (0.011) | 0.318 (0.011) | -0.113 (0.011) | 0.063 (0.011) | 0.290 (0.014) | |

| India MG | 0.512 (0.016) | -0.004 (0.016) | 0.233 (0.016) | 0.221 (0.017) | 0.629 (0.030) | |

| Indonesia MG | 0.412 (0.017) | 0.001 (0.017) | 0.358 (0.016) | 0.187 (0.017) | 0.650 (0.031) | |

| Malaysia MG | 0.371 (0.017) | 0.094 (0.017) | 0.218 (0.017) | 0.270 (0.018) | 0.705 (0.033) | |

| New Zealand MG | 0.378 (0.018) | 0.213 (0.018) | -0.090 (0.018) | 0.023 (0.019) | 0.784 (0.037) | |

| Philippines MG | 0.299 (0.018) | 0.080 (0.018) | 0.275 (0.018) | 0.164 (0.018) | 0.770 (0.036) | |

| Singapore MG | 0.638 (0.014) | 0.132 (0.014) | 0.160 (0.013) | 0.272 (0.014) | 0.436 (0.021) | |

| Thailand MG | 0.482 (0.017) | -0.021 (0.017) | 0.219 (0.017) | 0.202 (0.017) | 0.678 (0.032) |

Table 5 displays the estimated factor loadings and idiosyncratic variances for the Europe. All the indices of the UK, France, and Germany are reported, while only the Mid-Value and Mid-Growth indices are reported for other European markets to save space. We have identified three key findings. First, all the European markets have substantial loadings of the global factor during the Asian sub-period, but small loadings of the global factor during the American sub-period. Second, all the Value indices exhibit non-negative loadings of the global factor during the European sub-period, particularly for the Large-Value ones. Conversely, most Growth indices have negative loadings of the global factor during the European sub-period. Third, most European markets have considerably large loadings of the continental factor, except for South Africa and Turkey.

| United Kingdom LG | -0.025 (0.016) | 0.605 (0.013) | 0.065 (0.012) | 0.512 (0.013) | 0.358 (0.017) | |

|---|---|---|---|---|---|---|

| United Kingdom LV | 0.402 (0.012) | 0.534 (0.010) | 0.057 (0.009) | 0.472 (0.010) | 0.209 (0.010) | |

| United Kingdom MG | -0.081 (0.012) | 0.688 (0.010) | 0.058 (0.009) | 0.577 (0.009) | 0.201 (0.009) | |

| United Kingdom MV | 0.131 (0.013) | 0.606 (0.011) | 0.092 (0.009) | 0.550 (0.010) | 0.233 (0.011) | |

| United Kingdom SG | -0.082 (0.013) | 0.672 (0.011) | 0.091 (0.010) | 0.553 (0.010) | 0.239 (0.011) | |

| United Kingdom SV | 0.157 (0.013) | 0.603 (0.011) | 0.111 (0.010) | 0.526 (0.010) | 0.242 (0.011) | |

| France LG | -0.076 (0.011) | 0.628 (0.009) | 0.021 (0.008) | 0.665 (0.009) | 0.175 (0.008) | |

| France LV | 0.382 (0.008) | 0.469 (0.007) | 0.065 (0.006) | 0.664 (0.006) | 0.094 (0.004) | |

| France MG | -0.085 (0.010) | 0.646 (0.008) | 0.059 (0.007) | 0.675 (0.008) | 0.134 (0.006) | |

| France MV | 0.263 (0.010) | 0.522 (0.009) | 0.079 (0.007) | 0.646 (0.008) | 0.145 (0.007) | |

| France SG | -0.200 (0.010) | 0.674 (0.009) | 0.041 (0.008) | 0.657 (0.008) | 0.153 (0.007) | |

| France SV | 0.177 (0.010) | 0.581 (0.008) | 0.089 (0.007) | 0.633 (0.008) | 0.141 (0.007) | |

| Germany LG | -0.148 (0.011) | 0.632 (0.009) | 0.017 (0.008) | 0.680 (0.009) | 0.169 (0.008) | |

| Germany LV | 0.211 (0.009) | 0.520 (0.008) | 0.053 (0.007) | 0.694 (0.007) | 0.124 (0.006) | |

| Germany MG | -0.326 (0.010) | 0.713 (0.009) | -0.008 (0.007) | 0.642 (0.008) | 0.143 (0.007) | |

| Germany MV | 0.085 (0.012) | 0.565 (0.010) | 0.030 (0.009) | 0.642 (0.010) | 0.217 (0.010) | |

| Germany SG | -0.297 (0.010) | 0.703 (0.008) | 0.022 (0.007) | 0.658 (0.008) | 0.129 (0.006) | |

| Germany SV | 0.024 (0.009) | 0.659 (0.008) | 0.047 (0.007) | 0.640 (0.007) | 0.123 (0.006) | |

| Austria MV | 0.376 (0.016) | 0.424 (0.013) | 0.043 (0.011) | 0.512 (0.012) | 0.335 (0.016) | |

| Belgium MV | 0.213 (0.016) | 0.428 (0.013) | 0.056 (0.011) | 0.608 (0.012) | 0.339 (0.016) | |

| Denmark MV | 0.148 (0.022) | 0.355 (0.018) | 0.102 (0.016) | 0.370 (0.017) | 0.664 (0.031) | |

| Finland MV | 0.047 (0.017) | 0.543 (0.014) | 0.024 (0.012) | 0.525 (0.013) | 0.398 (0.019) | |

| Greece MV | 0.164 (0.023) | 0.284 (0.020) | 0.074 (0.017) | 0.314 (0.018) | 0.758 (0.036) | |

| Italy MV | 0.318 (0.013) | 0.377 (0.011) | 0.019 (0.009) | 0.679 (0.010) | 0.234 (0.011) | |

| Netherlands MV | 0.328 (0.012) | 0.465 (0.010) | 0.067 (0.009) | 0.611 (0.010) | 0.212 (0.010) | |

| Norway MV | 0.121 (0.019) | 0.582 (0.016) | 0.014 (0.014) | 0.327 (0.015) | 0.483 (0.023) | |

| Poland MV | 0.136 (0.021) | 0.453 (0.018) | 0.072 (0.015) | 0.330 (0.016) | 0.613 (0.029) | |

| SouthAfrica MV | 0.173 (0.016) | 0.704 (0.014) | -0.060 (0.012) | 0.130 (0.013) | 0.363 (0.017) | |

| Spain MV | 0.396 (0.014) | 0.413 (0.012) | 0.064 (0.011) | 0.547 (0.011) | 0.289 (0.014) | |

| Sweden MV | -0.022 (0.013) | 0.653 (0.011) | 0.004 (0.010) | 0.563 (0.011) | 0.251 (0.012) | |

| Switzerland MV | 0.148 (0.013) | 0.585 (0.011) | 0.077 (0.009) | 0.581 (0.010) | 0.220 (0.010) | |

| Turkey MV | 0.123 (0.024) | 0.351 (0.020) | -0.053 (0.018) | 0.122 (0.019) | 0.815 (0.038) | |

| Belgium MG | -0.203 (0.018) | 0.564 (0.015) | 0.022 (0.013) | 0.531 (0.014) | 0.434 (0.020) | |

| Denmark MG | -0.412 (0.016) | 0.672 (0.013) | 0.029 (0.012) | 0.490 (0.012) | 0.350 (0.016) | |

| Finland MG | -0.114 (0.019) | 0.498 (0.016) | 0.007 (0.014) | 0.508 (0.015) | 0.513 (0.024) | |

| Ireland MG | -0.243 (0.021) | 0.470 (0.017) | 0.024 (0.015) | 0.455 (0.016) | 0.595 (0.028) | |

| Italy MG | 0.011 (0.014) | 0.480 (0.012) | -0.000 (0.010) | 0.694 (0.011) | 0.277 (0.013) | |

| Netherlands MG | -0.351 (0.017) | 0.601 (0.014) | 0.022 (0.012) | 0.540 (0.013) | 0.383 (0.018) | |

| Norway MG | -0.036 (0.020) | 0.583 (0.016) | 0.012 (0.014) | 0.354 (0.015) | 0.535 (0.025) | |

| Poland MG | -0.020 (0.019) | 0.562 (0.016) | 0.025 (0.014) | 0.388 (0.015) | 0.526 (0.025) | |

| Portugal MG | 0.072 (0.022) | 0.366 (0.018) | 0.041 (0.016) | 0.413 (0.017) | 0.666 (0.031) | |

| SouthAfrica MG | 0.042 (0.018) | 0.682 (0.016) | -0.063 (0.014) | 0.152 (0.014) | 0.475 (0.022) | |

| Spain MG | -0.116 (0.022) | 0.353 (0.019) | 0.028 (0.016) | 0.430 (0.018) | 0.702 (0.033) | |

| Sweden MG | -0.256 (0.012) | 0.731 (0.010) | -0.011 (0.009) | 0.562 (0.010) | 0.211 (0.010) | |

| Switzerland MG | -0.415 (0.012) | 0.735 (0.010) | 0.032 (0.009) | 0.545 (0.010) | 0.217 (0.010) | |

| Turkey MG | 0.089 (0.024) | 0.374 (0.020) | -0.053 (0.018) | 0.142 (0.019) | 0.805 (0.038) |

Table 6 presents the estimated factor loadings and idiosyncratic variances for Americas. We see that the United States and Canada have substantial loadings of the global factor during the American sub-period, whereas their loadings of the continental factor are negligible. On the other hand, the emerging American markets tend to have significantly large loadings of the global factor during the Asian sub-period. Brazil also has large loadings of the continental factor.

| United States LG | 1.013 (0.012) | -0.346 (0.012) | 0.332 (0.010) | 0.098 (0.009) | 0.188 (0.009) | |

|---|---|---|---|---|---|---|

| United States LV | 0.993 (0.010) | 0.093 (0.010) | 0.276 (0.008) | 0.060 (0.008) | 0.133 (0.006) | |

| United States MG | 1.069 (0.008) | -0.334 (0.008) | 0.354 (0.007) | 0.083 (0.006) | 0.095 (0.005) | |

| United States MV | 1.020 (0.007) | 0.090 (0.007) | 0.301 (0.006) | 0.064 (0.006) | 0.072 (0.003) | |

| United States SG | 1.089 (0.007) | -0.204 (0.008) | 0.320 (0.006) | 0.074 (0.006) | 0.078 (0.004) | |

| United States SV | 1.014 (0.008) | 0.130 (0.008) | 0.267 (0.007) | 0.055 (0.006) | 0.089 (0.004) | |

| Brazil LG | 0.271 (0.008) | 0.145 (0.008) | 0.413 (0.007) | 0.758 (0.007) | 0.097 (0.005) | |

| Brazil LV | 0.240 (0.011) | 0.281 (0.012) | 0.376 (0.010) | 0.672 (0.009) | 0.185 (0.009) | |

| Brazil MG | 0.264 (0.007) | 0.125 (0.007) | 0.423 (0.006) | 0.779 (0.006) | 0.069 (0.003) | |

| Brazil MV | 0.248 (0.009) | 0.200 (0.009) | 0.405 (0.007) | 0.741 (0.007) | 0.109 (0.005) | |

| Brazil SG | 0.269 (0.008) | 0.127 (0.008) | 0.413 (0.006) | 0.777 (0.006) | 0.080 (0.004) | |

| Brazil SV | 0.233 (0.006) | 0.172 (0.006) | 0.414 (0.005) | 0.788 (0.005) | 0.053 (0.003) | |

| Canada LG | 0.691 (0.015) | -0.128 (0.015) | 0.559 (0.012) | 0.068 (0.011) | 0.298 (0.014) | |

| Canada LV | 0.590 (0.013) | 0.228 (0.013) | 0.520 (0.011) | 0.054 (0.010) | 0.233 (0.011) | |

| Canada MG | 0.643 (0.014) | -0.104 (0.014) | 0.608 (0.012) | 0.072 (0.011) | 0.272 (0.013) | |

| Canada MV | 0.512 (0.015) | 0.123 (0.015) | 0.572 (0.013) | 0.057 (0.012) | 0.316 (0.015) | |

| Canada SG | 0.569 (0.016) | -0.115 (0.016) | 0.602 (0.013) | 0.066 (0.013) | 0.356 (0.017) | |

| Canada SV | 0.518 (0.015) | 0.091 (0.015) | 0.596 (0.012) | 0.057 (0.011) | 0.299 (0.014) | |

| Chile LG | 0.289 (0.021) | 0.041 (0.021) | 0.503 (0.017) | 0.143 (0.016) | 0.598 (0.028) | |

| Chile LV | 0.198 (0.021) | 0.160 (0.021) | 0.476 (0.018) | 0.147 (0.016) | 0.607 (0.029) | |

| Chile MG | 0.157 (0.022) | 0.073 (0.023) | 0.446 (0.019) | 0.115 (0.018) | 0.713 (0.034) | |

| Chile MV | 0.157 (0.022) | 0.148 (0.022) | 0.440 (0.019) | 0.133 (0.017) | 0.676 (0.032) | |

| Chile SG | 0.154 (0.022) | 0.109 (0.022) | 0.485 (0.018) | 0.101 (0.017) | 0.656 (0.031) | |

| Chile SV | 0.169 (0.021) | 0.104 (0.021) | 0.500 (0.018) | 0.104 (0.017) | 0.636 (0.030) | |

| Colombia LG | 0.321 (0.021) | 0.197 (0.021) | 0.393 (0.018) | 0.159 (0.016) | 0.606 (0.029) | |

| Colombia LV | 0.324 (0.019) | 0.228 (0.020) | 0.438 (0.016) | 0.173 (0.015) | 0.529 (0.025) | |

| Colombia SV | 0.190 (0.023) | 0.156 (0.023) | 0.373 (0.019) | 0.130 (0.018) | 0.726 (0.034) | |

| Mexico LG | 0.305 (0.019) | 0.154 (0.020) | 0.489 (0.016) | 0.180 (0.015) | 0.528 (0.025) | |

| Mexico LV | 0.299 (0.019) | 0.127 (0.019) | 0.533 (0.016) | 0.168 (0.015) | 0.499 (0.024) | |

| Mexico MG | 0.253 (0.020) | 0.017 (0.020) | 0.554 (0.017) | 0.136 (0.016) | 0.569 (0.027) | |

| Mexico MV | 0.260 (0.019) | 0.123 (0.019) | 0.555 (0.016) | 0.152 (0.015) | 0.501 (0.024) | |

| Mexico SG | 0.298 (0.019) | 0.087 (0.019) | 0.556 (0.016) | 0.164 (0.015) | 0.495 (0.023) | |

| Mexico SV | 0.293 (0.019) | 0.094 (0.019) | 0.546 (0.016) | 0.167 (0.015) | 0.507 (0.024) | |

| Peru LG | 0.522 (0.020) | 0.111 (0.020) | 0.372 (0.017) | 0.114 (0.016) | 0.549 (0.026) |

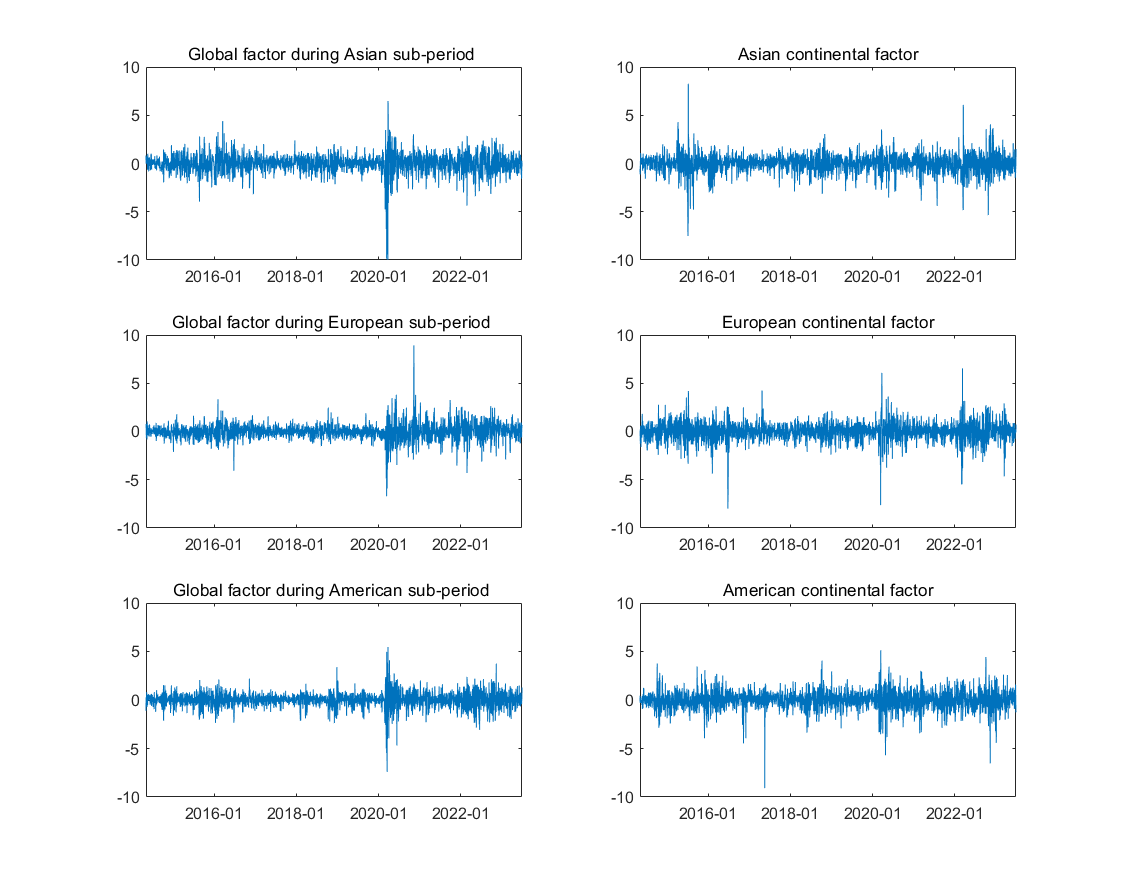

Overall, a large number of developing countries have large loadings of the global factor during the Asian sub-period. This means that the international news happened during the period between the American close on day and the Asian close on day has a substantial impact on the stock returns of these developing countries. Table 7 presents which is significantly different from 0. This implies that the weak-form efficient market hypothesis does not hold and it takes more than a day for some international news to fully unfold or dissipate. Figure 7 plots the estimated factors. We see that the global factor had a very large negative shock during the March of 2020, a period where the global stock markets crashed in the fear of Covid-19.

| Estimated value | Standard error | |

| 0.2491 | 0.0125 |

6.2 Integration

Financial market integration holds significant importance in the field of international finance. In our investigation, we adopt a methodology similar to Pukthuanthong and Roll (2009) to assess market integration. Pukthuanthong and Roll (2009) used the R-squared as a measure of integration, which is the proportion of variance explained by the explanatory variables. We define the proportion of variance explained by the global factor as the global integration index, while that explained by the continental factor as the regional integration index. The non-integration index is calculated as: .

Table 8 presents an analysis of integration of Asia-Pacific. We find that Mainland China and Hong Kong play a significant role in driving the Asia-Pacific regional integration. Specifically, most these markets demonstrate high regional integration, with approximately 50% of their variances explained by the continental factor. On the contrary, Japan shows high global integration, with over 50% of its variance explained by the global factor, but displays very low regional integration. In other words, Japanese indices are more globally integrated, while Chinese indices are more regionally integrated.

Table 9 presents an analysis of integration of Europe. The developed European markets, such as the UK, France, and Germany, exhibit higher levels of both the global and regional integration. On the other hand, the less developed European markets, such as Greece, Portugal, and Turkey, show lower levels of integration. For instance, the non-integration index of Turkish Mid-Growth index is as high as 81.19%, indicating that 81.19% of the variance of the Turkish Mid-Growth index is explained by neither the global nor continental factor.

Table 10 presents an analysis of integration of Americas. The US market demonstrates the highest level of global integration, with the global factor accounting for approximately 90% of its variance. However, the US market lacks regional integration, meaning it is not influenced by the American continental factor. Within Americas, Brazil holds the most prominent role in regional integration.

In summary, the US market is largely globally integrated, with approximately 90% of the variance of its returns being explained by the global factor. The Asia-Pacific regional integration is primarily driven by Mainland China and Hong Kong, while the American regional integration is mainly driven by Brazil. The developed and emerging markets exhibit different patterns.

| Global integration | Regional integration | Non-integration | |

|---|---|---|---|

| Mainland China LG | 0.1838 | 0.5192 | 0.2970 |

| Mainland China LV | 0.2365 | 0.5566 | 0.2069 |

| Mainland China MG | 0.1738 | 0.5408 | 0.2854 |

| Mainland China MV | 0.1892 | 0.6706 | 0.1402 |

| Mainland China SG | 0.1585 | 0.6685 | 0.1731 |

| Mainland China SV | 0.1738 | 0.6652 | 0.1609 |

| Hong Kong LG | 0.2134 | 0.4436 | 0.3430 |

| Hong Kong LV | 0.2798 | 0.2776 | 0.4426 |

| Hong Kong MG | 0.1840 | 0.2665 | 0.5495 |

| Hong Kong MV | 0.2543 | 0.3575 | 0.3883 |

| Hong Kong SG | 0.1990 | 0.5996 | 0.2013 |

| Hong Kong SV | 0.2336 | 0.5136 | 0.2527 |

| Japan LG | 0.5722 | 0.0131 | 0.4147 |

| Japan LV | 0.5277 | 0.0036 | 0.4686 |

| Japan MG | 0.5608 | 0.0106 | 0.4286 |

| Japan MV | 0.5453 | 0.0032 | 0.4514 |

| Japan SG | 0.5500 | 0.0087 | 0.4413 |

| Japan SV | 0.5362 | 0.0018 | 0.4620 |

| South Korea MV | 0.4773 | 0.1121 | 0.4106 |

| Taiwan MV | 0.3860 | 0.1443 | 0.4697 |

| Australia MV | 0.6874 | 0.0013 | 0.3113 |

| India MV | 0.3496 | 0.0417 | 0.6087 |

| Indonesia MV | 0.3456 | 0.0386 | 0.6157 |

| Malaysia MV | 0.3993 | 0.0559 | 0.5448 |

| NewZealand MV | 0.3616 | 0.0004 | 0.6381 |

| Philippines MV | 0.2460 | 0.0433 | 0.7106 |

| Singapore MV | 0.5302 | 0.0538 | 0.4159 |

| Thailand MV | 0.3592 | 0.0464 | 0.5945 |

| South Korea MG | 0.4220 | 0.1248 | 0.4532 |

| Taiwan MG | 0.3301 | 0.1355 | 0.5345 |

| Australia MG | 0.7256 | 0.0037 | 0.2706 |

| India MG | 0.3407 | 0.0476 | 0.6117 |

| Indonesia MG | 0.3289 | 0.0344 | 0.6367 |

| Malaysia MG | 0.2406 | 0.0710 | 0.6884 |

| NewZealand MG | 0.2324 | 0.0005 | 0.7670 |

| Philippines MG | 0.2141 | 0.0264 | 0.7595 |

| Singapore MG | 0.5177 | 0.0701 | 0.4122 |

| Thailand MG | 0.2981 | 0.0398 | 0.6621 |

| Global integration | Regional integration | Non-integration | |

|---|---|---|---|

| United Kingdom LG | 0.3965 | 0.2554 | 0.3481 |

| United Kingdom LV | 0.5856 | 0.2140 | 0.2004 |

| United Kingdom MG | 0.4868 | 0.3202 | 0.1931 |

| United Kingdom MV | 0.4777 | 0.2950 | 0.2272 |

| United Kingdom SG | 0.4778 | 0.2930 | 0.2292 |

| United Kingdom SV | 0.4972 | 0.2681 | 0.2347 |

| Germany LG | 0.3912 | 0.4457 | 0.1631 |

| Germany LV | 0.4049 | 0.4731 | 0.1220 |

| Germany MG | 0.4884 | 0.3798 | 0.1318 |

| Germany MV | 0.3781 | 0.4073 | 0.2146 |

| Germany SG | 0.4795 | 0.4009 | 0.1196 |

| Germany SV | 0.4798 | 0.4003 | 0.1199 |

| France LG | 0.3982 | 0.4316 | 0.1702 |

| France LV | 0.4864 | 0.4230 | 0.0906 |

| France MG | 0.4307 | 0.4399 | 0.1293 |

| France MV | 0.4535 | 0.4052 | 0.1413 |

| France SG | 0.4461 | 0.4088 | 0.1450 |

| France SV | 0.4718 | 0.3904 | 0.1378 |

| Austria MV | 0.4235 | 0.2528 | 0.3236 |

| Belgium MV | 0.3034 | 0.3630 | 0.3336 |

| Denmark MV | 0.2132 | 0.1344 | 0.6524 |

| Finland MV | 0.3340 | 0.2725 | 0.3935 |

| Greece MV | 0.1553 | 0.0974 | 0.7473 |

| Italy MV | 0.3199 | 0.4511 | 0.2290 |

| Netherlands MV | 0.4334 | 0.3612 | 0.2054 |

| Norway MV | 0.4145 | 0.1060 | 0.4795 |

| Poland MV | 0.2899 | 0.1070 | 0.6031 |

| SouthAfrica MV | 0.6138 | 0.0172 | 0.3690 |

| Spain MV | 0.4367 | 0.2867 | 0.2766 |

| Sweden MV | 0.4409 | 0.3121 | 0.2470 |

| Switzerland MV | 0.4541 | 0.3306 | 0.2153 |

| Turkey MV | 0.1638 | 0.0149 | 0.8213 |

| Belgium MG | 0.3150 | 0.2697 | 0.4153 |

| Denmark MG | 0.4716 | 0.2149 | 0.3135 |

| Finland MG | 0.2450 | 0.2526 | 0.5024 |

| Ireland MG | 0.2332 | 0.1976 | 0.5691 |

| Italy MG | 0.2466 | 0.4785 | 0.2748 |

| Netherlands MG | 0.3786 | 0.2686 | 0.3528 |

| Norway MG | 0.3508 | 0.1231 | 0.5262 |

| Poland MG | 0.3338 | 0.1482 | 0.5181 |

| Portugal MG | 0.1702 | 0.1692 | 0.6606 |

| SouthAfrica MG | 0.4976 | 0.0233 | 0.4791 |

| Spain MG | 0.1288 | 0.1815 | 0.6897 |

| Sweden MG | 0.5043 | 0.2969 | 0.1988 |

| Switzerland MG | 0.5430 | 0.2644 | 0.1927 |

| Turkey MG | 0.1677 | 0.0203 | 0.8119 |

| Global integration | Regional integration | Non-integration | |

|---|---|---|---|

| United States LG | 0.8522 | 0.0072 | 0.1407 |

| United States LV | 0.9004 | 0.0026 | 0.0970 |

| United States MG | 0.9253 | 0.0050 | 0.0697 |

| United States MV | 0.9454 | 0.0029 | 0.0517 |

| United States SG | 0.9400 | 0.0040 | 0.0561 |

| United States SV | 0.9340 | 0.0022 | 0.0638 |

| Brazil LG | 0.3418 | 0.5631 | 0.0951 |

| Brazil LV | 0.3851 | 0.4362 | 0.1788 |

| Brazil MG | 0.3353 | 0.5967 | 0.0680 |

| Brazil MV | 0.3569 | 0.5370 | 0.1061 |

| Brazil SG | 0.3297 | 0.5921 | 0.0782 |

| Brazil SV | 0.3373 | 0.6103 | 0.0525 |

| Canada LG | 0.7320 | 0.0041 | 0.2639 |

| Canada LV | 0.7897 | 0.0026 | 0.2077 |

| Canada MG | 0.7490 | 0.0047 | 0.2463 |

| Canada MV | 0.7018 | 0.0030 | 0.2952 |

| Canada SG | 0.6661 | 0.0041 | 0.3298 |

| Canada SV | 0.7169 | 0.0030 | 0.2801 |

| Chile LG | 0.3898 | 0.0203 | 0.5899 |

| Chile LV | 0.3763 | 0.0216 | 0.6021 |

| Chile MG | 0.2753 | 0.0132 | 0.7115 |

| Chile MV | 0.3094 | 0.0176 | 0.6730 |

| Chile SG | 0.3341 | 0.0103 | 0.6556 |

| Chile SV | 0.3547 | 0.0108 | 0.6344 |

| Colombia LG | 0.3912 | 0.0244 | 0.5844 |

| Colombia LV | 0.4621 | 0.0289 | 0.5090 |

| Colombia SV | 0.2653 | 0.0167 | 0.7180 |

| Mexico LG | 0.4519 | 0.0316 | 0.5164 |

| Mexico LV | 0.4825 | 0.0277 | 0.4898 |

| Mexico MG | 0.4170 | 0.0182 | 0.5648 |

| Mexico MV | 0.4817 | 0.0229 | 0.4954 |

| Mexico SG | 0.4854 | 0.0264 | 0.4882 |

| Mexico SV | 0.4729 | 0.0276 | 0.4995 |

| Peru LG | 0.4841 | 0.0119 | 0.5040 |

6.3 Misspecification

In this section, we explore the potential misspecification of our model: In other words, how effectively our model captures the information in ? One major concern regarding our model is the presence of only a single global factor –Could this be overly restrictive? The absence of factors affecting two of the three continents also raises a concern. Consequently, the sample correlation of the data might not be close to the QML-all-res estimate .

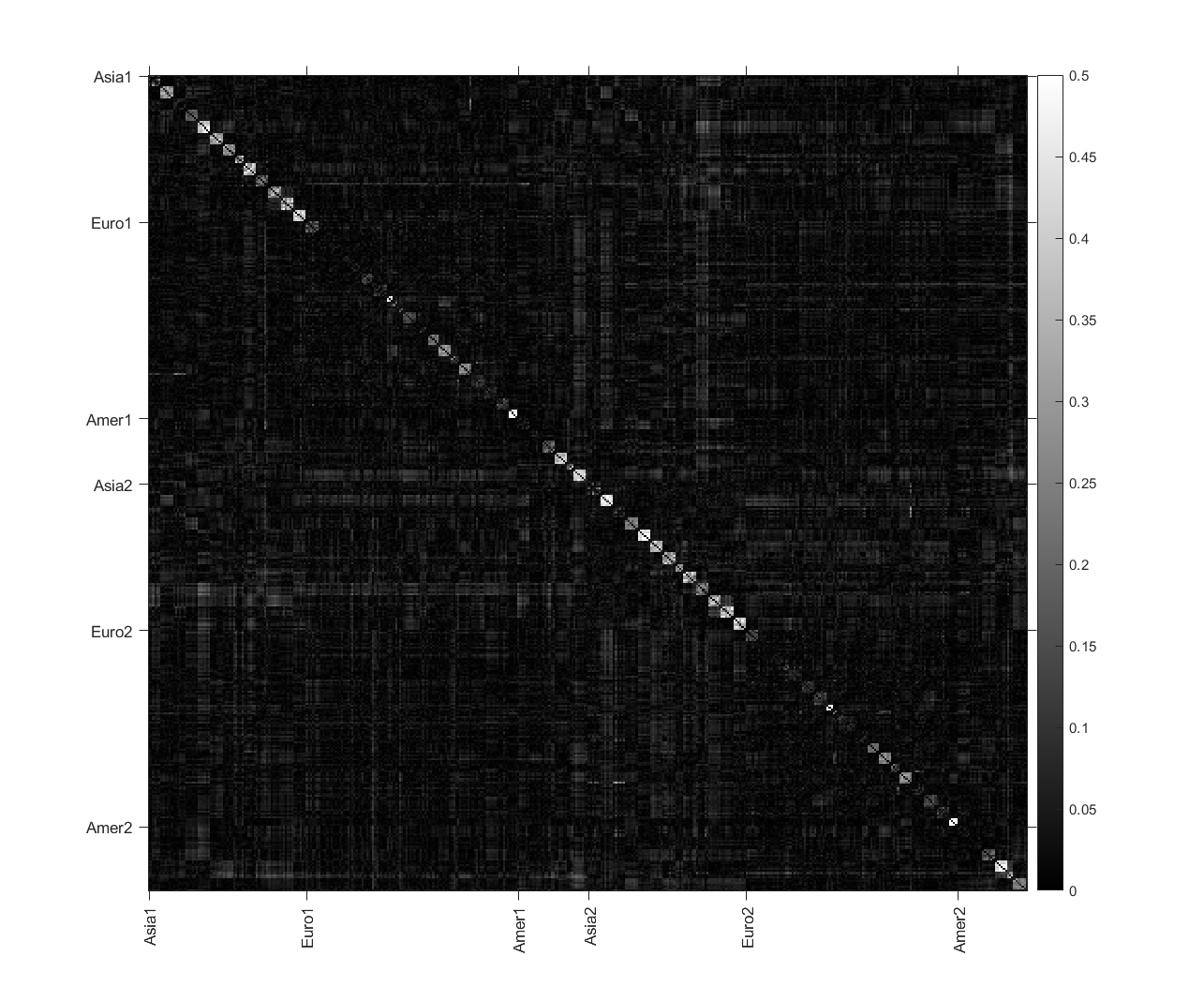

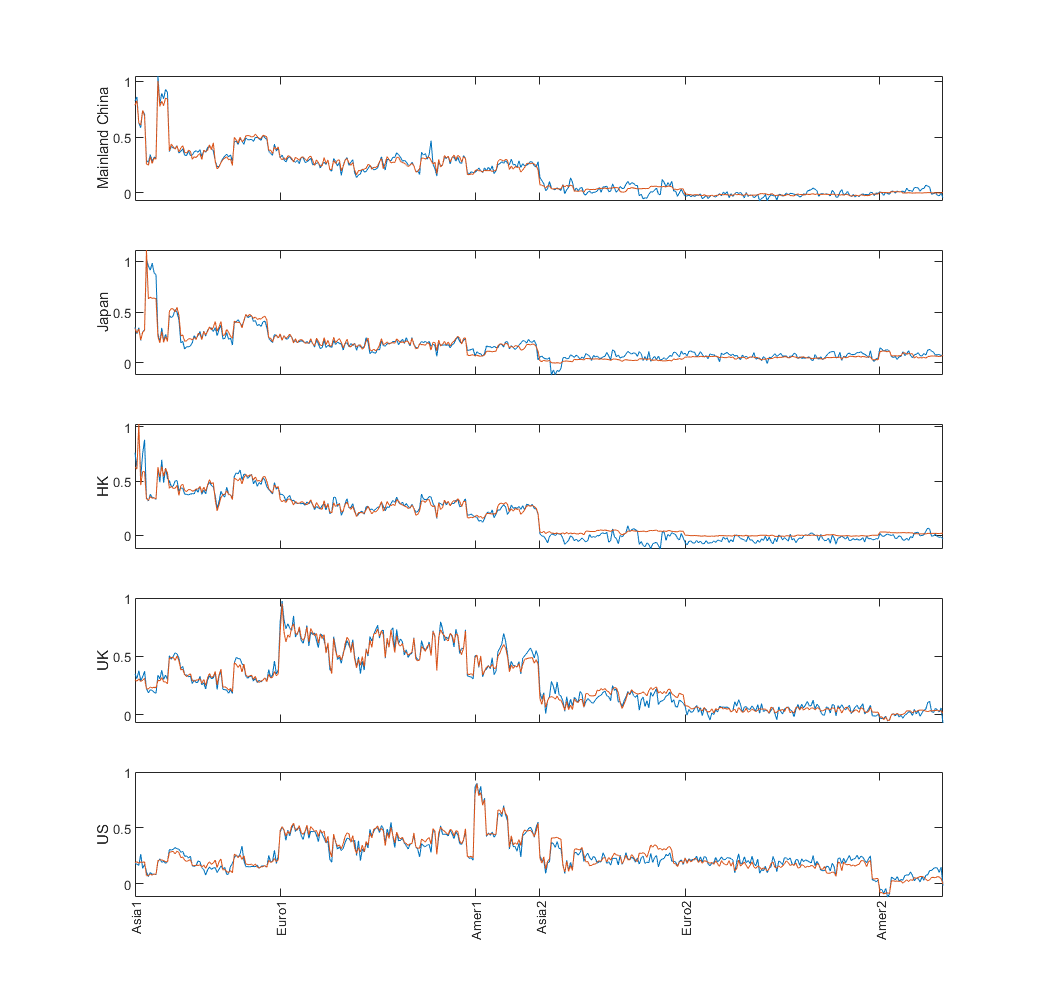

Figure 8 displays the absolute values of the elements of . “Asia1” denotes the first Asia-Pacific index in “day one”, while “Asia2” denotes the first Asia-Pacific index in “day two”, and so forth. We note that covariances among indices in the same market are not well captured by our model, as indicated by the white squares on the diagonal. This is because our model has global and continental factors, but lacks market-specific factors. However, introducing market-specific factors would lead to a substantial increase in the factor dimension. As one could see from the large black area in the figure, the elements of are quite small in magnitude for all but these intra-market pairs. Consequently, we assert that our model is designed to capture inter-market correlations rather than intra-market correlations.

Figure 9 displays the rows of or corresponding to the Large-Value indices of Mainland China, Japan, Hong Kong, UK, and US in “day one”. The red and blue lines in a sub-plot represent the corresponding row of and , respectively. The closeness of the two lines indicates that our model fits the data rather well for these main markets.