tactis: Transformer-Attentional Copulas for Time Series

Abstract

The estimation of time-varying quantities is a fundamental component of decision making in fields such as healthcare and finance. However, the practical utility of such estimates is limited by how accurately they quantify predictive uncertainty. In this work, we address the problem of estimating the joint predictive distribution of high-dimensional multivariate time series. We propose a versatile method, based on the transformer architecture, that estimates joint distributions using an attention-based decoder that provably learns to mimic the properties of non-parametric copulas. The resulting model has several desirable properties: it can scale to hundreds of time series, supports both forecasting and interpolation, can handle unaligned and non-uniformly sampled data, and can seamlessly adapt to missing data during training. We demonstrate these properties empirically and show that our model produces state-of-the-art predictions on multiple real-world datasets.

1 Introduction

In numerous time series forecasting contexts, data presents itself in a raw form that rarely matches the standard assumptions of classical forecasting methods. For instance, in healthcare settings and economic forecasting, groups of related time series can have different sampling frequencies, be sampled irregularly, and exhibit missing values (Shukla & Marlin, 2021b; Sun et al., 2020). Covariates that are predictive of future behavior may not be available for all historical data, or may be available in a different form, e.g., due to changes in measurement methodology. Moreover, optimal decision-making in downstream tasks generally requires the full joint predictive distribution over arbitrary future time horizons (Peterson, 2017), not just marginal quantiles thereof at a fixed horizon. We seek to develop general forecasting methods that are both suitable for a wide range of downstream tasks and that can handle all stylized facts about real-world time series—as they are, not as they ought to be—namely:

-

•

Joint characterization of a multivariate stochastic process, forecasting trajectories at arbitrary time horizons;

-

•

Presence of non-stochastic covariates, either static or time-varying, used as conditioning variables;

-

•

Variables within the process that are measured at different sampling frequencies or irregularly sampled;

-

•

Missing values for arbitrary time points and variables;

-

•

Variables with different domains——with skewed and fat-tailed marginal behavior.

Classical times series models, such as arima (Box et al., 2015) and exponential smoothing methods (Hyndman et al., 2008), are very restricted in their handling of the above stylized facts. Although extensions have been proposed that deal with individual issues, they cannot easily deal with all and require considerable domain knowledge to be effective. Machine learning models have recently gained in popularity (Benidis et al., 2020). Nevertheless, methods introduced in recent years all suffer from limitations when dealing with one or more of the above listed stylized facts, or neglect in their handling of the full predictive distribution.

Separately, multivariate forecasting models based on copulas have been popular in econometrics for more than a decade (Patton, 2012; Rémillard et al., 2012; Krupskii & Joe, 2020; Mayer & Wied, 2021). These models enable the separate characterization of the joint behavior of a group of random variables from their marginal behavior. This has been found to be especially valuable in areas such as finance and insurance where marginals are known to exhibit particular patterns of skewness and kurtosis. Recently in machine learning, low-rank Gaussian copula processes with LSTMs (Hochreiter & Schmidhuber, 1997) have been proposed for high-dimensional forecasting (Salinas et al., 2019).

Building on the recent successes of transformers as general-purpose sequence models (Vaswani et al., 2017) and their success in time series forecasting (Rasul et al., 2021b; Tashiro et al., 2021; Tang & Matteson, 2021), we propose a transformer architecture that can tackle all the above stylized facts about real-world time series. Notably, we show how to represent an implicit copula when sampling from the transformer decoder model. Moreover, by representing each observation as a distinct token with its own timestamp, we can naturally handle irregularly sampled times series as well as series with missing values and unequal sampling frequencies. We also show that an efficient two-dimensional attention scheme lets us scale to hundreds of time steps and series using vanilla attention (Bahdanau et al., 2015).

Contributions:

-

1.

We present Transformer-Attentional Copulas for Time Series (tactis), a highly flexible transformer-based model for large-scale multivariate probabilistic time series prediction (§ 4).

-

2.

We introduce attentional copulas, an attention-based architecture that estimates non-parametric copulas for an arbitrary number of random variables (§ 4.2).

-

3.

We theoretically prove the convergence of attentional copulas to valid copulas (§ 4.3).

-

4.

We conduct an empirical study showing tactis’ state-of-the-art probabilistic prediction accuracy on several real-world datasets, along with notable flexibility (§ 5).

2 Background

2.1 Problem Setting

We are interested in the general problem of estimating the joint distribution of values missing at arbitrary time points in multivariate time series. This general task encompasses classical problems, such as probabilistic forecasting, backcasting, and interpolation.

Formally, we consider a set of multivariate time series , where each is a collection of possibly-related univariate time series. For simplicity, we elaborate the notation for a single element of . Let , where the are univariate time series with arbitrary lengths . Each is associated with (i) a Boolean mask , such that if is observed and otherwise, (ii) a matrix of time-varying covariates , where each represents arbitrary additional information about the observations, and (iii) a vector of time stamps s.t. , indicating the times at which the data were measured. Note that this setting naturally supports unaligned time series with arbitrary sampling frequencies.

Our goal is to infer the joint distribution of missing time series values given all known information:111We slightly abuse the notation and omit random variables.

| (1) |

where and are the observed () and missing () elements of , respectively.

From this problem formulation, one can recover standard time series problems via specific masking patterns. For instance, a -step probabilistic forecasting task can be defined by setting the last elements of each to zero.

2.2 Transformers

The model that we propose builds on the transformer architecture for sequence-to-sequence transduction (Vaswani et al., 2017). Transformer models have an encoder-decoder structure, where the encoder learns a representation of the tokens of an input sequence, and the decoder generates the tokens of an output sequence autoregressively, based on the input sequence. The main feature of such models is that they can capture non-sequential dependencies between tokens via attention mechanisms (Bahdanau et al., 2015). This is in sharp contrast with recurrent neural networks (Goodfellow et al., 2016), such as LSTMs (Hochreiter & Schmidhuber, 1997), which are inherently sequential. Transformers have been widely discussed in the literature and we thus refer the reader to the seminal work of Vaswani et al. (2017) for additional details. As we later describe, transformers allow tactis to view time series as sets of tokens, among which non-local dependencies can be learned regardless of considerations like alignment and sampling frequency.

2.3 Copulas

Copulas are mathematical constructs that allow separating the joint dependency structure of a set of random variables from their marginal distributions (Nelsen, 2007). Such a separation can be used to learn reusable models that can be applied to seemingly different distributions, where variables have different marginals but share the dependency structure.

Formally, a copula is the joint cumulative distribution function (CDF) of a -dimensional random vector on the unit cube with uniform marginal distributions, i.e.,

| (2) |

where . According to Sklar (1959)’s theorem, the joint CDF of any random vector can be expressed as a combination of a copula and the marginal CDF of each random variable ,

| (3) |

and the corresponding probability density222Assuming that the distribution is continuous. is given by:

| (4) |

where is the copula’s density function and is the marginal density function of . It is thus possible to estimate seemingly complex joint distributions by learning the parameters of a simple internal joint distribution (the copula) and marginal distributions, which can even be estimated empirically. One classical approach, which has been abundantly used in time series applications, is the Gaussian copula (Nelsen, 2007), where is constructed from a Gaussian distribution.

In this work, we avoid making such parametric assumptions and propose a new attention-based architecture trained to mimic a non-parametric copula, which we term attentional copula. tactis learns to produce the parameters of the copula, on-the-fly, based on learned variable representations. It can thus reuse a learned dependency structure across multiple sets of variables, by mapping them to similar representations.

3 Related Work

Neural Networks for Time Series Forecasting Although studied in the 1990’s (Zhang et al., 1998), neural networks and other machine learning (ML) techniques had long been taken with caution in the forecasting community due to a perceived propensity to overfit (Makridakis et al., 2018). In recent years, however, the field has seen a number of demonstrations of successful ML-based forecasting, in particular winning the prestigious M5 competition (Makridakis et al., 2021, 2022). For neural networks, work has mostly centered around so-called global models (Montero-Manso & Hyndman, 2021), which in contrast to classical statistical methods such as arima (Box et al., 2015) or exponential smoothing (Hyndman et al., 2008), learn a single set of parameters to forecast many series. A first wave of approaches in the recent resurgence was primarily based on recurrent or convolutional neural network encoders (Shih et al., 2019; Chen et al., 2020). Oreshkin et al. (2020) introduce a recursive decomposition based on a residual signal projection on a set of learned basis functions. Le Guen & Thome (2020) introduce an approach for univariate probabilistic forecasting based on determinantal point processes to capture structured shape and temporal diversity. Extensions of classical state-space models have also been proposed (Yanchenko & Mukherjee, 2020; de Bézenac et al., 2020). Comprehensive surveys of deep learning methods for forecasting appear in Lim & Zohren (2021) and Benidis et al. (2020), restricting coverage to regularly-sampled data. Of relevance to the present work are studies of probabilistic multivariate methods, transformer-based approaches, copulas, and techniques enabling irregular sampling.

Probabilistic Multivariate Methods Narrowing attention to methods carrying out probabilistic forecasting of the joint distribution of a multivariate stochastic process, DeepAR (Salinas et al., 2020) computes an iterated one-step-ahead Monte Carlo approximation of the predictive distribution by sampling from a fixed functional form whose parameters are the result of a recurrent neural network (RNN). Likewise, Rasul et al. (2021a) propose instead to model the predictive joint one-step-ahead distribution using a denoising diffusion process (Ho et al., 2020; Sohl-Dickstein et al., 2015); however, with the diffusion dynamics conditioned on an RNN, the model cannot easily deal with missing values or irregularly sampled time series. Rasul et al. (2021b) propose to model the predictive joint one-step-ahead distribution by a multivariate normalizing flow (Papamakarios et al., 2021), parametrized by either a RNN or a transformer. For general density estimation, Uria et al. (2014) propose an order-agnostic autoregressive density estimator based on neural networks, with Hoogeboom et al. (2022) extending the approach to diffusion models; both are related to the autoregressive copula decomposition that we propose herein.

Transformer-based approaches have come to the fore more recently, on the strength of their successes in other sequence modeling tasks. Lim et al. (2021) introduce the temporal fusion transformer, combining recurrent layers for local processing and self-attention layers for characterizing long-term dependencies, evaluating performance on quantile loss measures; notably, the architecture makes use of a gating mechanism to suppress unnecessary covariates. Li et al. (2019) introduce a transformer with subquadratic memory complexity along with convolutional self-attention to better handle local context. Spadon et al. (2021) propose a recurrent graph evolution neural networks, which embeds transformers, to carry out point multivariate forecasting. Wu et al. (2020) propose an adversarial sparse transformer to estimate conditional quantiles of the predictive distribution. Tashiro et al. (2021) use a conditional score-based diffusion model explicitly trained for interpolation and report substantial improvements over existing probabilistic imputation models, as well as competitive performance on some forecasting tasks against recently-proposed deep learning models. Tang & Matteson (2021) introduce a variational non-Markovian state space model where the latent dynamics are given by an attention mechanism over all previous latents and observed tokens. They report good multivariate probabilistic forecasting results on five standard datasets, as well as on the task of human motion prediction. Wu et al. (2021) introduce an auto-correlation mechanism in place of self attention and report good accuracy on long-horizon point forecasting benchmarks. Recently, outside of time series forecasting, Müller et al. (2022) show how to train a transformer-based model to approximate the Bayesian posterior predictive distribution in regression tasks; these results are in the spirit of the forecasting and interpolation results that we present in this paper.

Copulas-Based Forecasting There exists an abundant literature on uses of copulas (Größer & Okhrin, 2021) for economic and financial forecasting, although most published models have focused on fixed functional forms (Patton, 2012; Rémillard et al., 2012). Aas et al. (2009) introduce vine copulas that provide increased pairwise flexibility, and Krupskii & Joe (2020); Mayer & Wied (2021) suggest more flexible forms for forecasting applications. In ML, Lopez-Paz et al. (2012) propose to carry out domain adaptation using a form of non-parametric copulas based on kernel estimators. For forecasting, Salinas et al. (2019) introduce GPVar, an LSTM-based method that dynamically parametrizes a Gaussian copula. To the best of our knowledge, none of the published methods show how to sample from a non-parametric copula resulting from an autoregressive decomposition of a time-varying conditional copula distribution, as we introduce in this work.

Irregular Sampling Gaussian processes have been widely used to handle irregularly-sampled series (Williams & Rasmussen, 2006; Chapados & Bengio, 2007), but these approaches are limited in other ways, notably in computational tractability. More recently, Shukla & Marlin (2021a) have proposed a transformer-like attention mechanism to re-represent an irregularly sampled time series at a fixed set of reference points, and evaluate on interpolation and classification tasks.

4 The tactis Model

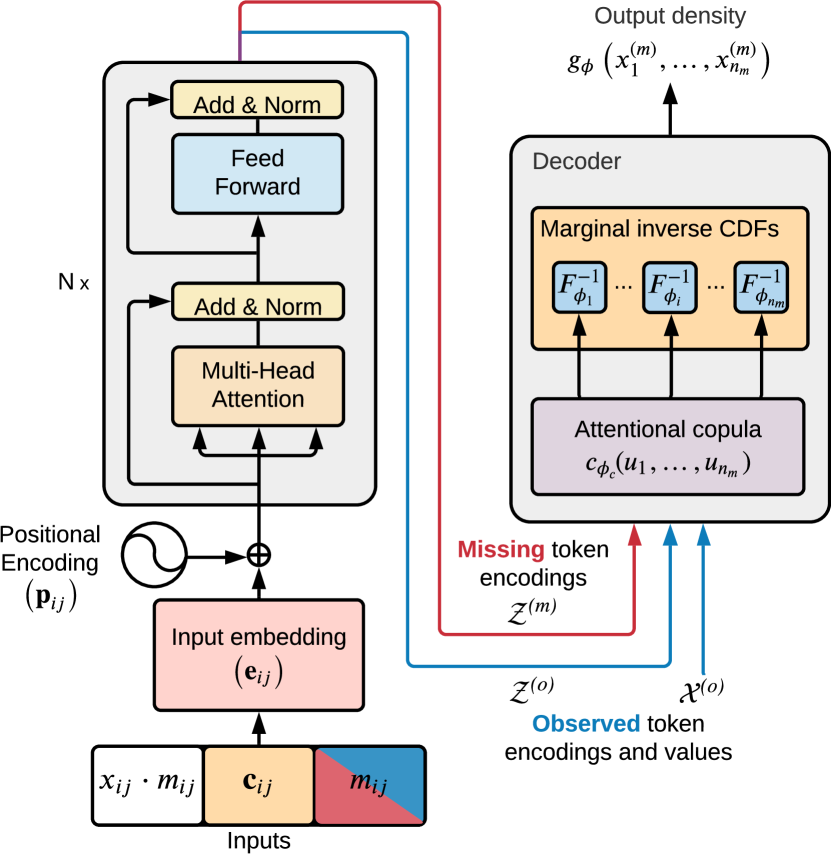

Our contribution is a flexible model for multivariate probabilistic time series prediction composed of a transformer encoder (Vaswani et al., 2017) and an attention-based decoder trained to mimic a non-parametric copula; hence the name Transformer-Attentional Copulas for Time Series (tactis). Fig. 1 shows an overview of the model architecture.333Code available at https://github.com/servicenow/tactis.

Akin to classical Transformers (Vaswani et al., 2017), tactis views the elements of a multivariate time series () as an arbitrary set of tokens, where some tokens are observed and some are missing (based on ). The encoder is tasked with learning a meaningful representation of each token, such as to enable the decoder to infer a multivariate joint distribution over the values of the missing tokens. Due to the use of attention in both the encoder and the decoder, tactis can adapt to an arbitrary number of tokens, without retraining.

tactis learns the conditional predictive distribution of arbitrary missing values in multivariate time series. At inference time, it is the pattern of missing values themselves—namely, where they are located with respect to measured values—that determines whether it performs forecasting, interpolation, or another similar task. Consequently, tactis naturally supports changes in its inputs, such as the unavailability of some time series, and in its outputs, such as changes in forecast horizon. Moreover, it inherently supports misalignment and differences in sampling frequencies, since each token is encoded separately. This is in sharp contrast with classical vector autoregressive models (Wei, 2018) and most recurrent neural networks, which jointly consider the values of each time series at a given time step () as a vector . We now detail the encoder, decoder, training procedure, and provide some theoretical guarantees.

4.1 Encoder

As shown in Fig. 1, the encoder used in tactis is identical to that of standard Transformers (Vaswani et al., 2017), except that all tokens (observed and missing) are jointly encoded.

Input embedding The encoder starts by producing a vector embedding () for each element in each time series (i.e., tokens), which accounts for its value , the associated covariates444Optionally, we include a learned, per series, embedding in . , and whether it is observed or missing . Such embeddings are given by a neural network with parameters , with masking the values of missing tokens:

Positional encoding We add information about a token’s time stamp to the input embedding via a positional encoding . For simplicity, we use the positional encodings of Vaswani et al. (2017), based on sine and cosine functions of various frequencies, and obtain the final embeddings as . Note that other choices, such as positional encodings tailored to time series (e.g., accounting for holidays, day of week, etc.), would be viable, but we keep such explorations for future work.

Then, following Vaswani et al. (2017), the embeddings are passed through a stack of residual layers that combine multi-head self-attention and layer normalization to obtain an encoding () for each token. Such encodings contain a complex mixture of information from other tokens that were deemed relevant by the attention mechanism, such as the value of their covariates, their time stamp, and the values of observed tokens.

Scalability One well-known limitation of transformers is the large time and memory complexity of self-attention, scaling quadratically with the number of tokens. However, improving the efficiency of transformers is an active field of research (Tay et al., 2020; Lin et al., 2021) and any progress in this direction is poised to be directly applicable to tactis. In this work, when applying tactis to large datasets, such as those in § 5, we take advantage of the fact that each token is indexed by two independent indices: for the variables, and for the time steps. We do so by employing the temporal transformer layers of Tashiro et al. (2021), which first compute self-attention between the tokens of each variable () and then between the tokens at a given time step (). Hence, instead of scaling in , the time and memory complexity scale in , where is the number of time series and is the length of the longest time series. One downside of this approach is that, for attention within a given time step () to make sense, the time series must be aligned. When using temporal transformer layers, we will refer to our model as tactis-tt.

4.2 Decoder

As stated in Eq. 1, we aim to learn the joint distribution of the values () of missing tokens (), given the values of observed tokens (), the covariates (), and the time stamps (). We achieve this via an attention-based decoder trained to mimic a non-parametric copula (see § 2.3), which we now describe.

Since the data consists of an arbitrary set of observed and missing tokens, we introduce the following notation: , , , and , which respectively denote the encoded representations and values of observed and missing tokens. We also use and to denote the set of all covariates and timestamps, respectively (see § 2.1).

Our goal is to accurately estimate the joint density of missing token values, using a model such that:

where the distributional parameters555We use subscripted versions of and to denote distributional parameters and neural network parameters, respectively. are produced by a neural network parametrized by :

Crucially, note that using encoded token representations (; see § 4.1) as inputs into the decoder ensures that the resulting density is conditioned on observations. We consider the following copula-based structure for :

| (5) |

where , is the density of a copula, and and respectively represent the marginal (univariate) cumulative distribution and density functions of .

The structure of allows for a wealth of different copula parametrizations (e.g., the Gaussian copula of Salinas et al. (2019)). The crux of tactis resides in how each of the components is parametrized. Notably, we propose to use normalizing flows (Tabak & Turner, 2013) to model the marginals, and we develop a flexible non-parametric copula that can automatically adapt to a changing number of missing tokens (). We now outline these constructs, for which an overview appears in Fig. 2.

Marginal distributions To model the marginal CDFs (), we seek a univariate function that (i) maps values to , (ii) is monotonically increasing, (iii) is both continuous and differentiable. We achieve this using a modified version of the Deep Sigmoidal Flows (DSF) of Huang et al. (2018), where we simply remove the logit function of the last flow layer to obtain values in . The parameters of each flow are produced by a neural network with parameters , which are shared across all ,

| (6) |

The marginal densities are obtained by differentiating w.r.t. , an efficient operation for DSF. In addition to satisfying our desiderata, DSFs have been shown to be universal density approximators, thereby not constraining the modeling ability of tactis.

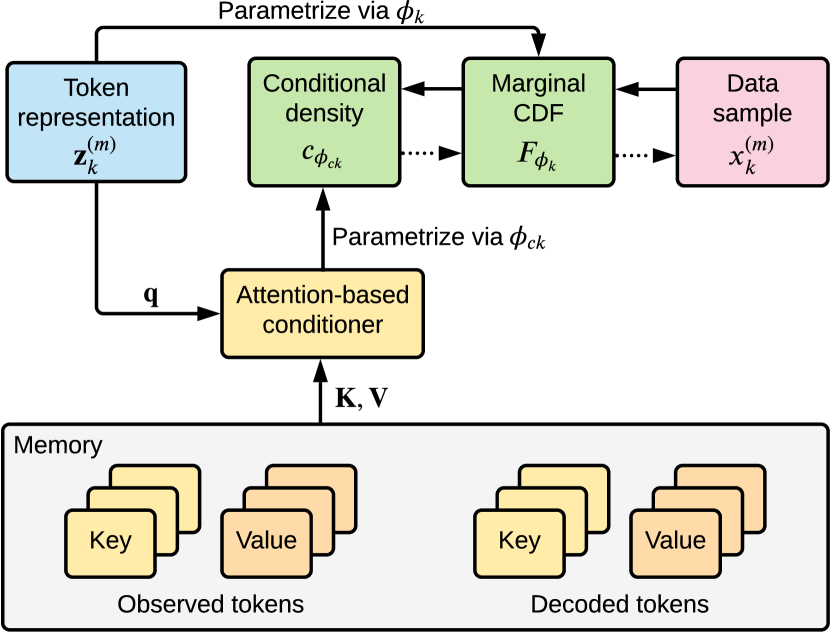

Copula density According to the definition of a copula (§ 2.3), we must parametrize a distribution on the unit cube with uniform marginals. We consider an autoregressive factorization of the copula density according to an arbitrary permutation of the indices . We denote the copula density and its parameters by :

| (7) |

where is conditional density in the factorization and . Importantly, we let be the density of a uniform distribution , and we use an attention-based conditioner to obtain the parameters of the remaining conditional distributions , for . We call the resulting construct an attentional copula.

Attention-based conditioner This component of the decoder produces the parameters for the conditional density by performing attention over a memory composed of the representations of observed tokens and missing tokens that are predecessors in the permutation: , as well as their CDF-transformed666For observed tokens, transformation via the normalizing flow does not necessarily correspond to a CDF transform, but it ensures that all values are on a similar scale. values . The conditioner is composed of several layers, which are as follows. First, we calculate keys and values for each element in the memory using two modules parameterized by and , respectively: 777For simplicity, we use a single attention head in the presentation, but in practice, we use multiple (see Vaswani et al. (2017)).

| (8) |

We then calculate a query for our token of interest using a module with parameters :

Let and be the matrices of all keys and values for tokens in the memory, respectively. Following Vaswani et al. (2017), we obtain an attention-based representation :

where is a module with parameters . We repeat this process from Eq. 8 for each layer, with different parameters, and replacing by the output of the previous layer. Finally, we obtain the parameters of the conditional distribution using a module parameterized by applied to the of the last layer:

Choice of distribution Any distribution with support on can be used to model the conditional distributions . We choose to use a piecewise constant distribution, i.e., we divide the support into a number of bins, each parametrized by a probability density that applies to all the points it contains. Such a distribution can approximate complex multimodal distributions on without making parametric assumptions, similarly to van den Oord et al. (2016). The number of bins is a hyperparameter and controls approximation quality. Other valid choices include the Beta distribution and mixtures thereof.

Sampling We first draw a sample from the copula, autoregressively, following an arbitrary permutation . As per the definition of attentional copulas, the first element of the permutation is always sampled from a . Then, we transform each of the sampled values using their corresponding inverse marginal CDF, i.e., . This is possible since DSFs are invertible functions (see § B.2 for details).

This concludes the presentation of the decoder. However, one question remains: what guarantees that will converge to a valid copula? The key is in the training procedure.

4.3 Training Procedure

Let be the density estimator described in Eq. 5, where the copula is factorized according to permutation . Let be the set containing the parameters of all the components of the encoder and the decoder, respectively. We obtain by minimizing the expected negative log-likelihood of our model over permutations drawn uniformly at random888Note that we do not differentiate through the sampling of permutations. We simply consider a random permutation at each forward propagation. from the set of all permutations and samples drawn from the set of all time series :

| (9) |

Theorem 1.

Proof.

Hence, tactis provably learns to disentangle the joint dependency structure of random variables from their marginal distributions via flexible non-parametric attentional copulas.

5 Experiments

We start by presenting an experiment that supports the validity of attentional copulas (§ 5.1). Then, we demonstrate the state-of-the-art performance of tactis using a forecasting benchmark composed of several real-world datasets (§ 5.2). Finally, we present a series of experiments that emphasize the flexibility of the tactis model (§ 5.3).

5.1 Empirical Validation of Attentional Copulas

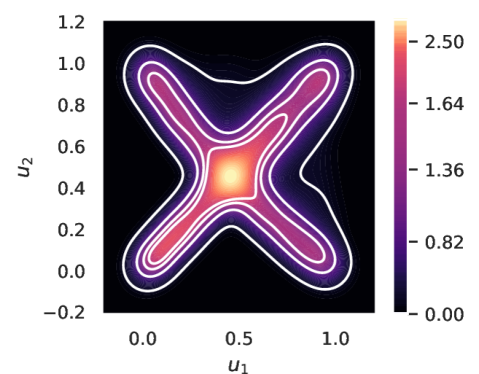

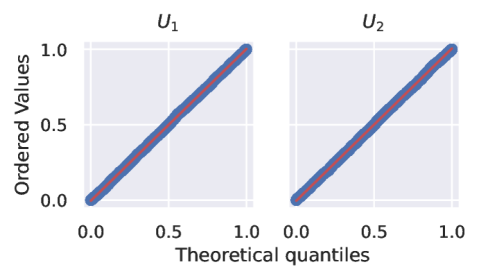

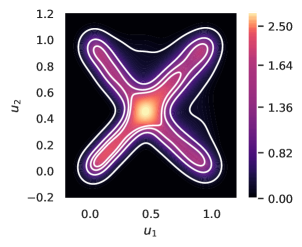

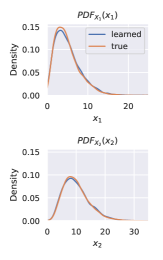

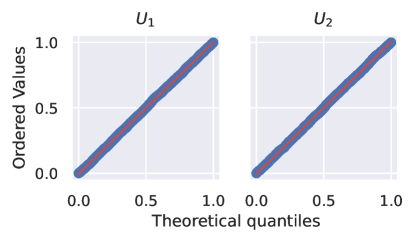

Theorem 1 guarantees that, at convergence to a minimum of Eq. 9, attentional copulas will be valid copulas. However, it does not tell us if this setting is reachable with finite amounts of data, model capacity, and training time. Hence, we conduct a simple experiment, where we generate data from a distribution with a known copula structure and verify if the tactis decoder correctly recovers the ground truth. For simplicity and ease of visualization, we use a bivariate distribution, where the underlying copula is an x-shaped mixture of two Clayton copulas. The details are given in § D.1.

The results are shown in Fig. 3. We observe that the learned copula density closely matches the ground truth (Fig. 3a). Furthermore, its marginal distributions are indistinguishable from the distribution (Fig. 3b), making it a valid copula. This experiment, albeit simple, provides empirical evidence that learned attentional copulas can be valid, even in practical settings. See § D.1 for additional results and discussion.

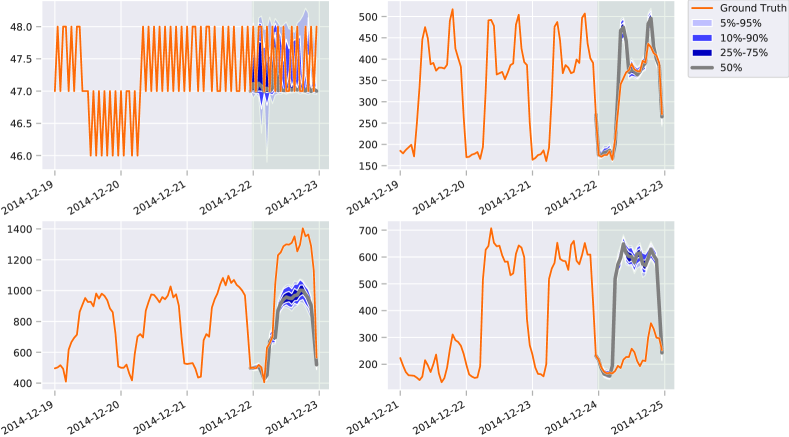

5.2 Forecasting: Comparison to the State of the Art

| Model | electricity | fred-md | kdd-cup | solar-10min | traffic | Avg. Rank |

|---|---|---|---|---|---|---|

| Auto-arima | ||||||

| ETS | ||||||

| TempFlow | ||||||

| TimeGrad | ||||||

| GPVar | ||||||

| tactis-tt |

We now assess the performance of tactis in comparison with state-of-the-art forecasting methods. Of particular interest is whether the model’s great flexibility is detrimental to the quality of its predictions.

Baselines We benchmark against multiple deep-learning-based methods that generate multivariate probabilistic forecasts, namely: GPVar (Salinas et al., 2019), an LSTM-based method that parametrizes a Gaussian copula; TempFlow (Rasul et al., 2021b), a transformer-based method that models the predictive distribution using normalizing flows; and TimeGrad (Rasul et al., 2021a), an autoregressive method based on diffusion models. We also compare to classical methods: arima (Box et al., 2015) and ETS exponential smoothing (Hyndman et al., 2008). The comparison is based on tactis-tt, a variant of tactis that uses temporal transformer layers in the encoder (see § 4.1). In addition to these comparisons, we provide a detailed ablation study in § D.4.

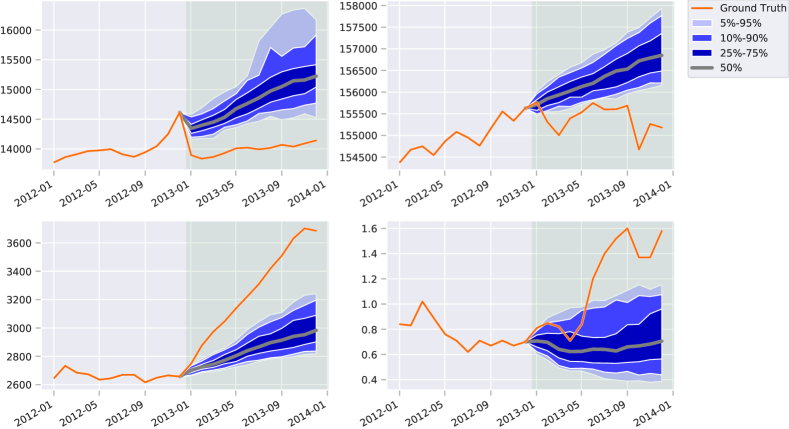

Datasets We consider five real-world datasets from the Monash Time Series Forecasting Repository (Godahewa et al., 2021): electricity, fred-md, kdd-cup, solar-10min, and traffic (see § C.1 for details). These were selected for being high-dimensional (107–862 variables), exempt of missing values, and sampled at diverse frequencies (10 min., hourly, monthly).

Evaluation procedure Model accuracy is assessed via a backtesting procedure, which mimics the use of forecasting models in real-world settings. A detailed presentation can be found in § C.5. In short, we define a series of retraining timestamps for each dataset. At each timestamp, the models are trained with all of the preceding data, and their accuracy is assessed using subsequent data. We then report metrics aggregated over all timestamps. The hyperparameters of each method are selected based on the protocol and grids described in § C.3 and § C.4, respectively.

Metrics We use the CRPS-Sum (Salinas et al., 2019), a multivariate extension of the univariate Continuous Ranked Probability Score (CRPS) (Matheson & Winkler, 1976), as our main evaluation metric (see § C.6 for a detailed presentation). In short, this metric corresponds to the CRPS of the univariate series obtained by summing forecasts along the variable axis. For completeness, we also report results for two additional metrics in § C.6: the CRPS and the energy score (Gneiting & Raftery, 2007). Finally, we assess how well each method does as a general forecasting algorithm, rather than a dataset-specific one, by measuring the average rank of each method, w.r.t. all others, over all datasets and retraining timestamps.

Benchmark results The CRPS-Sum results are reported in Tab. 1. From these, it is clear that tactis-tt compares favourably to the state of the art. It achieves the lowest CRPS-Sum for out of datasets and outperforms most baselines on the remaining ones. In fact, tactis-tt outperforms all deep-learning-based methods on fred-md and outperforms all but GPVar on solar-10min. Furthermore, it achieves the lowest average rank (), suggesting that, if one had to choose a method to use without prior knowledge of the data, tactis-tt would be the better option. Hence, these results suggest that the great flexibility of tactis, which we highlight in the next section, does not seem to undermine its performance.

5.3 Model Flexibility

We now present a series of experiments that emphasize the flexibility of the tactis model, namely its support for interpolation, unaligned and non-uniformly sampled data, and its ability to scale to hundreds of time series.

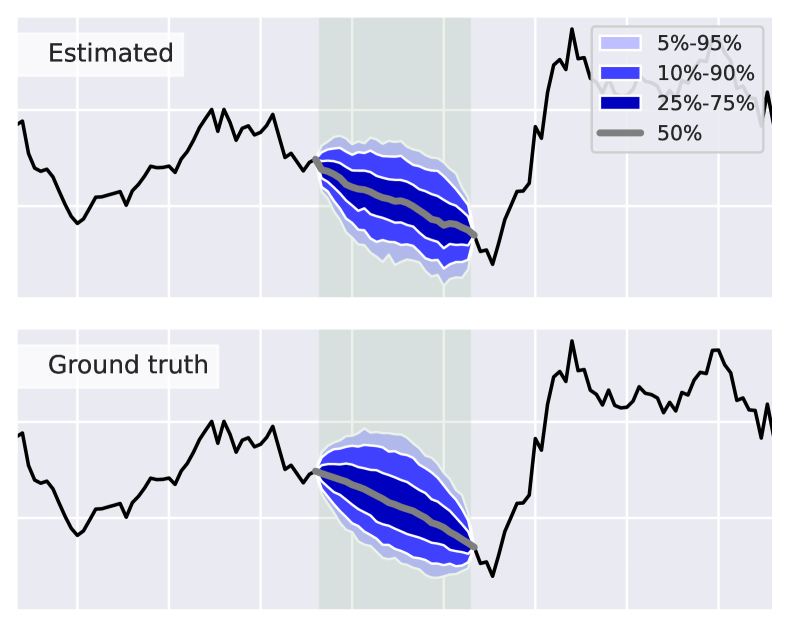

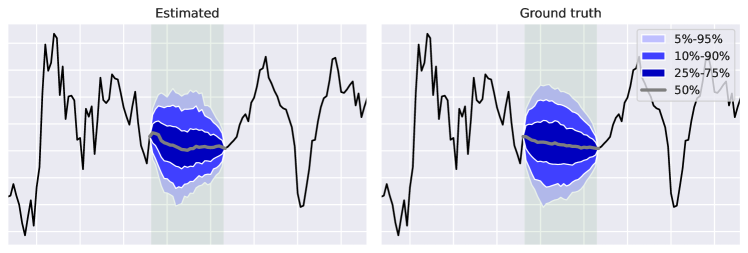

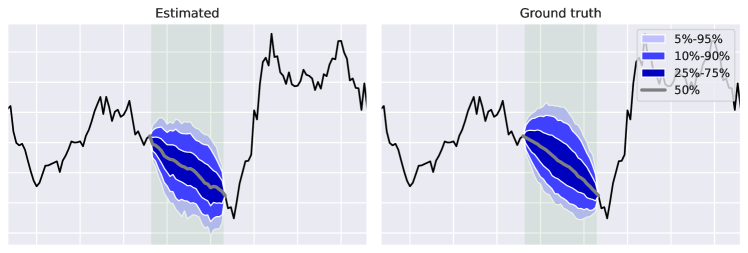

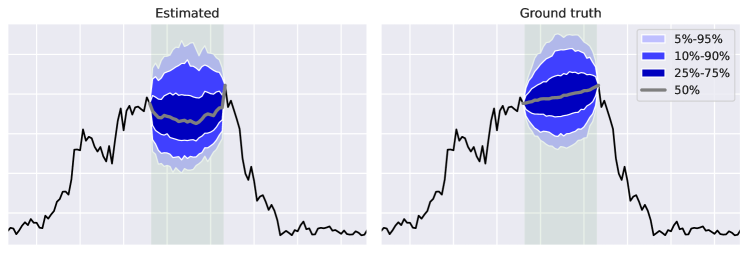

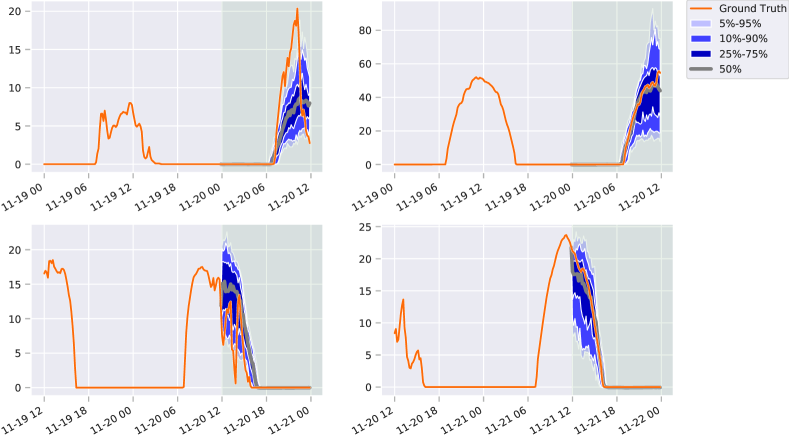

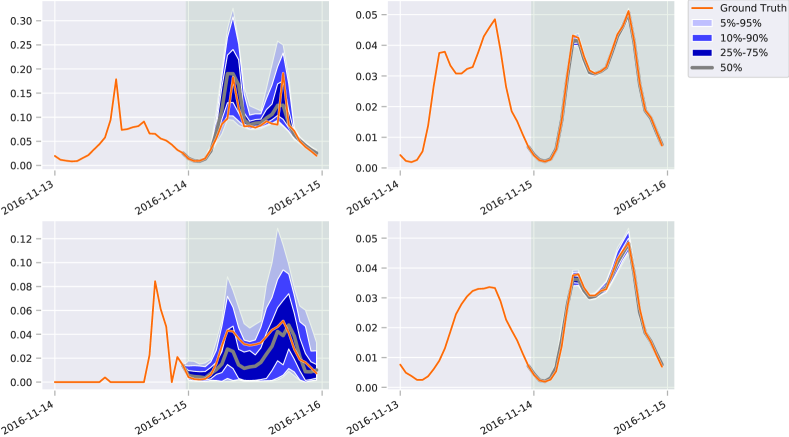

Prediction Beyond Forecasting tactis relies on a Boolean-valued mask to determine which values of a multivariate time series must be predicted (see § 2.1). This enables it to support arbitrary prediction tasks, such as forecasting, interpolation, and even combinations thereof. Here, we demonstrate support for interpolation by showing that tactis can correctly estimate the distribution of a gap in observed values within a stochastic volatility process (Kim et al., 1998). Specifically, we train tactis to estimate the distribution of missing values centered within a univariate time series sampled from such a process. We then compare the estimated joint conditional distribution to the ground truth posterior distribution of missing values. A typical result, where tactis closely approximates the ground truth, is shown in Fig. 4. Additional results, as well as a full description of the data generation and experimental protocols are available in § D.2.

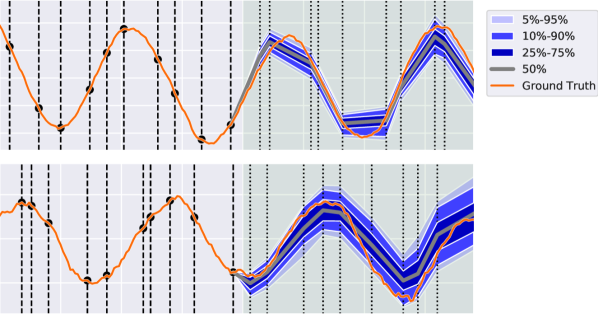

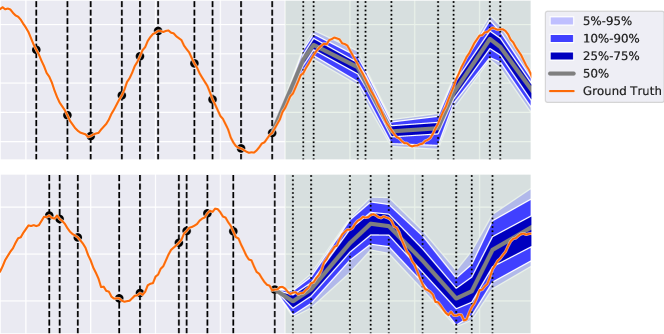

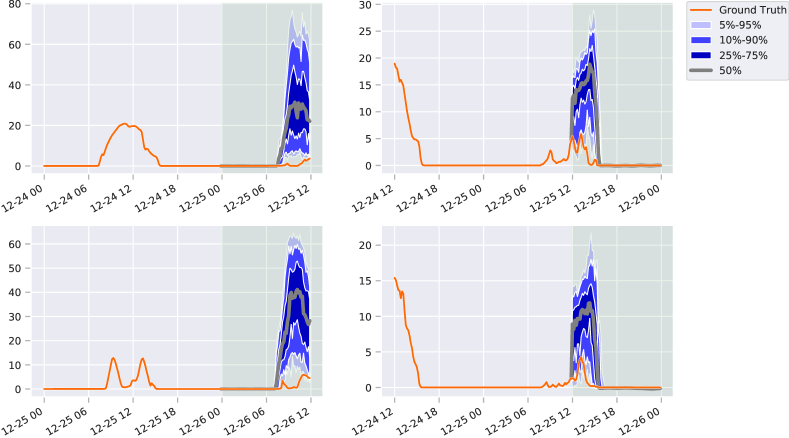

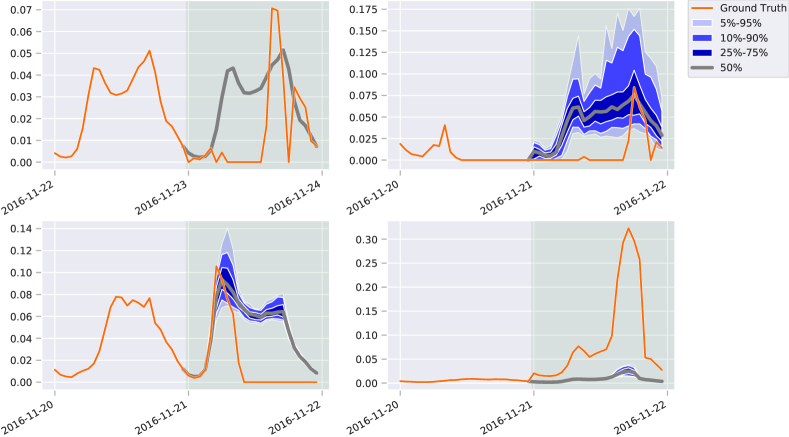

Unaligned and non-uniformly sampled series One particularity of tactis is that it considers each observed data point, in each time series, as a distinct token over which to perform self-attention. The model operates on the set of input tokens, irrespective of their alignment and sampling frequencies, enabling native support for unaligned and non-uniformly sampled time series.999The tactis-tt variant does not support this setting (see § 4.1). Here, we conduct a simple experiment to demonstrate that tactis operates well in this setting. We sample data from a bivariate noisy sine process with observations spaced randomly in each series (see § D.3 for details). We then train tactis to forecast the distribution of missing values at the end of each series. As shown in Fig. 5, tactis produces accurate forecasts for this data, illustrating its support for unaligned and non-uniformly sampled time series.

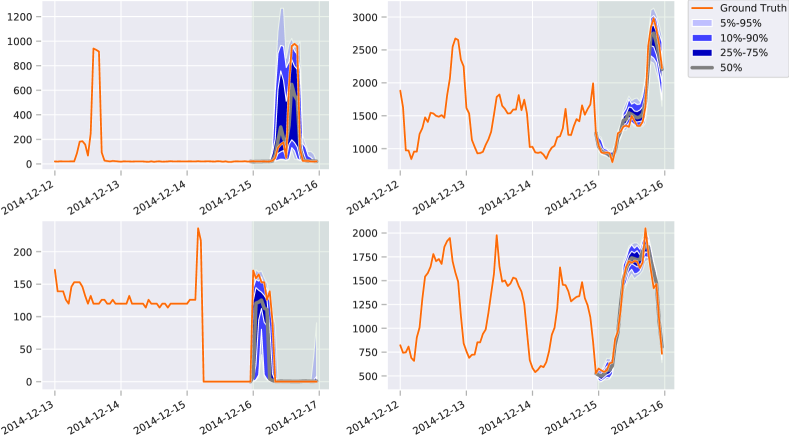

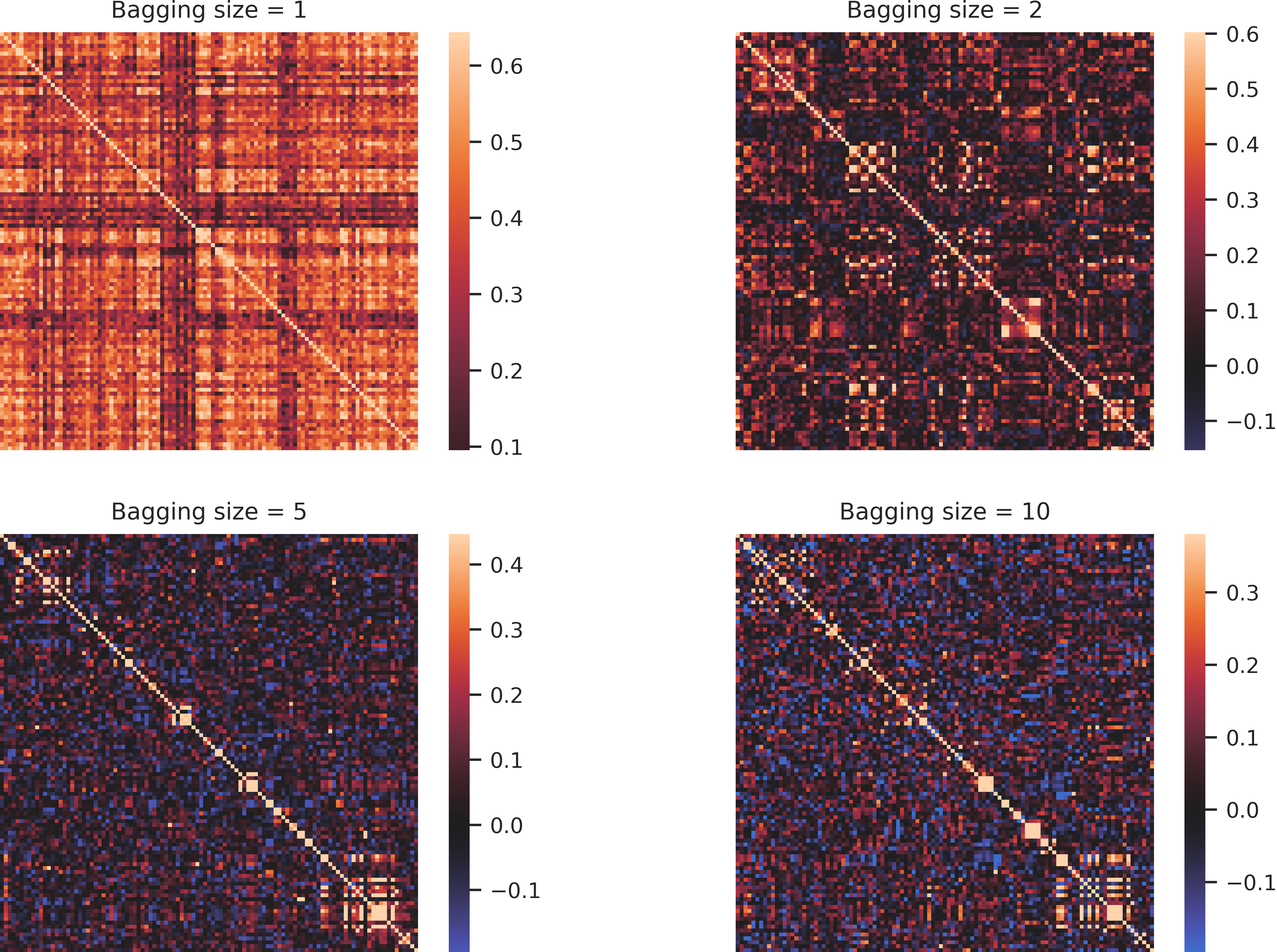

Scaling to hundreds of time series One key properties of attention-based models, such as tactis, is that they can seamlessly be applied to data of varying dimensionality, without retraining. We make use of this property to devise a scalable training procedure for tactis, which we detail in § B.3. In short, we train the model using batches composed of a random subset of time series, called a bag ( in the forecasting benchmark). This significantly limits the running time and memory usage of the model. Then, at inference time only, we apply the model to all series. In Tab. 2, we explore the effect of on the predictive performance of tactis-tt. The results indicate that this parameter has very little impact on the accuracy of the model. However, as we show in § E.3.1, small values of , such as , can negatively affect the learned inter-series correlations. Hence, the model can be trained efficiently without incurring a significant penalty in terms of predictive performance as long as the bag size is not unreasonably small.

| Bagging size | CRPS | CRPS-Sum | Energy |

|---|---|---|---|

| — | — | ||

| 2 | |||

| 5 | |||

| 10 | |||

| 15 | |||

| 20 | |||

| 25 | |||

| 30 |

6 Discussion

This work proposes tactis, a method for probabilistic time series inference that combines the flexibility of attention-based models with the density estimation capabilities of a new type of non-parametric copula, termed attentional copula. In addition to achieving state-of-the-art performance on tasks such as probabilistic forecasting and interpolation, we showed that tactis reaches an unprecedented level of flexibility: it can infer missing values at arbitrary time points in multivariate time series (via masking) can learn from unaligned/non-uniformly sampled data, can be trained when subsets of the data are missing at random, can handle the presence of observed non-stochastic covariates, and can estimate complex distributions beyond the reach of classical copula models, such as the Gaussian copula.

That said, there are several interesting directions in which tactis could be extended. First, the model’s ability to learn multivariate dependencies may benefit from using positional encodings specifically designed for temporal data, rather than those of Vaswani et al. (2017). Second, the applications of recent advances in large-scale transformers (e.g., Choromanski et al. (2021)) to tactis could significantly reduce the amount of resources required by the model, especially in the sampling phase, where bagging is not applied. The elaboration of more efficient sampling procedures (e.g., based on learning conditional independences) also constitutes a promising prospect. Third, a thorough study of the training dynamics of tactis may reveal architecture changes or auxiliary tasks that could significantly accelerate learning. Fourth, tactis could be extended to series measured in discrete domains by adapting the estimation of marginal distributions in the decoder.

Finally, we believe that this work could serve as a basis for models that address the cold-start problem, making sensible predictions in contexts where very few historical observations of the process are available. In fact, tactis could be trained on time series from a wealth of domains, reusing the same attentional copula, but fine-tuning its encoder to new, unforeseen domains. Such extensions towards foundation models (Bommasani et al., 2021) for probabilistic time series constitute exciting prospects.

Acknowledgements

The authors are grateful to G. Abuhamad, P. Beaudoin, D. Berger, I. Laradji, C.-W. Huang, A. Lacoste, P.-A. Noël, S. Paquet, and P. Rodriguez-Lopez for thoughtful suggestions.

References

- Aas et al. (2009) Aas, K., Czado, C., Frigessi, A., and Bakken, H. Pair-copula constructions of multiple dependence. Insurance: Mathematics and Economics, 44(2):182–198, 2009. URL https://EconPapers.repec.org/RePEc:eee:insuma:v:44:y:2009:i:2:p:182-198.

- Alexandrov et al. (2020) Alexandrov, A., Benidis, K., Bohlke-Schneider, M., Flunkert, V., Gasthaus, J., Januschowski, T., Maddix, D. C., Rangapuram, S., Salinas, D., Schulz, J., Stella, L., Türkmen, A. C., and Wang, Y. GluonTS: Probabilistic and Neural Time Series Modeling in Python. Journal of Machine Learning Research, 21(116):1–6, 2020. URL http://jmlr.org/papers/v21/19-820.html.

- Bahdanau et al. (2015) Bahdanau, D., Cho, K., and Bengio, Y. Neural machine translation by jointly learning to align and translate. In Bengio, Y. and LeCun, Y. (eds.), 3rd International Conference on Learning Representations, ICLR 2015, San Diego, CA, USA, May 7-9, 2015, Conference Track Proceedings, 2015. URL http://arxiv.org/abs/1409.0473.

- Benidis et al. (2020) Benidis, K., Rangapuram, S. S., Flunkert, V., Wang, B., Maddix, D., Turkmen, C., Gasthaus, J., Bohlke-Schneider, M., Salinas, D., Stella, L., Callot, L., and Januschowski, T. Neural forecasting: Introduction and literature overview. arXiv.org, 2020. URL http://arxiv.org/abs/2004.10240.

- Bohlke-Schneider & Salinas (2021) Bohlke-Schneider, M. and Salinas, D. personal communication, 2021.

- Bommasani et al. (2021) Bommasani, R., Hudson, D. A., Adeli, E., Altman, R., Arora, S., von Arx, S., Bernstein, M. S., Bohg, J., Bosselut, A., Brunskill, E., et al. On the opportunities and risks of foundation models. arXiv preprint arXiv:2108.07258, 2021.

- Box et al. (2015) Box, G. E. P., Jenkins, G. M., Reinsel, G. C., and Ljung, G. M. Time series analysis: forecasting and control. John Wiley & Sons, fifth edition, 2015.

- Chapados & Bengio (2007) Chapados, N. and Bengio, Y. Augmented functional time series representation and forecasting with gaussian processes. In Platt, J., Koller, D., Singer, Y., and Roweis, S. (eds.), Advances in Neural Information Processing Systems, volume 20. Curran Associates, Inc., 2007. URL https://proceedings.neurips.cc/paper/2007/file/81e74d678581a3bb7a720b019f4f1a93-Paper.pdf.

- Chen et al. (2020) Chen, Y., Kang, Y., Chen, Y., and Wang, Z. Probabilistic forecasting with temporal convolutional neural network. Neurocomputing, 399:491–501, 2020.

- Choromanski et al. (2021) Choromanski, K. M., Likhosherstov, V., Dohan, D., Song, X., Gane, A., Sarlos, T., Hawkins, P., Davis, J. Q., Mohiuddin, A., Kaiser, L., Belanger, D. B., Colwell, L. J., and Weller, A. Rethinking attention with performers. In International Conference on Learning Representations, 2021. URL https://openreview.net/forum?id=Ua6zuk0WRH.

- de Bézenac et al. (2020) de Bézenac, E., Rangapuram, S. S., Benidis, K., Bohlke-Schneider, M., Kurle, R., Stella, L., Hasson, H., Gallinari, P., and Januschowski, T. Normalizing kalman filters for multivariate time series analysis. In Larochelle, H., Ranzato, M., Hadsell, R., Balcan, M. F., and Lin, H. (eds.), Advances in Neural Information Processing Systems, volume 33, pp. 2995–3007. Curran Associates, Inc., 2020. URL https://proceedings.neurips.cc/paper/2020/file/1f47cef5e38c952f94c5d61726027439-Paper.pdf.

- Gneiting & Raftery (2007) Gneiting, T. and Raftery, A. E. Strictly proper scoring rules, prediction, and estimation. Journal of the American statistical Association, 102(477):359–378, 2007.

- Godahewa et al. (2021) Godahewa, R., Bergmeir, C., Webb, G. I., Hyndman, R. J., and Montero-Manso, P. Monash time series forecasting archive. In Neural Information Processing Systems Track on Datasets and Benchmarks, 2021. forthcoming.

- Goodfellow et al. (2016) Goodfellow, I., Bengio, Y., and Courville, A. Deep Learning. MIT Press, 2016. http://www.deeplearningbook.org.

- Größer & Okhrin (2021) Größer, J. and Okhrin, O. Copulae: An overview and recent developments. WIREs Computational Statistics, n/a(n/a):e1557, 2021. doi: https://doi.org/10.1002/wics.1557. URL https://wires.onlinelibrary.wiley.com/doi/abs/10.1002/wics.1557. A good initial read to give a higher level of understanding of what copulas are and what kinds of copulas have been studied.

- Ho et al. (2020) Ho, J., Jain, A., and Abbeel, P. Denoising diffusion probabilistic models. In Larochelle, H., Ranzato, M., Hadsell, R., Balcan, M. F., and Lin, H. (eds.), Advances in Neural Information Processing Systems, volume 33, pp. 6840–6851. Curran Associates, Inc., 2020. URL https://proceedings.neurips.cc/paper/2020/file/4c5bcfec8584af0d967f1ab10179ca4b-Paper.pdf.

- Hochreiter & Schmidhuber (1997) Hochreiter, S. and Schmidhuber, J. Long short-term memory. Neural computation, 9(8):1735–1780, 1997.

- Hoogeboom et al. (2022) Hoogeboom, E., Gritsenko, A. A., Bastings, J., Poole, B., van den Berg, R., and Salimans, T. Autoregressive diffusion models. In International Conference on Learning Representations, 2022. URL https://openreview.net/forum?id=Lm8T39vLDTE.

- Huang et al. (2018) Huang, C.-W., Krueger, D., Lacoste, A., and Courville, A. Neural autoregressive flows. In Dy, J. and Krause, A. (eds.), Proceedings of the 35th International Conference on Machine Learning, volume 80 of Proceedings of Machine Learning Research, pp. 2078–2087. PMLR, 10–15 Jul 2018. URL https://proceedings.mlr.press/v80/huang18d.html.

- Hyndman et al. (2008) Hyndman, R., Koehler, A. B., Ord, J. K., and Snyder, R. D. Forecasting with exponential smoothing: the state space approach. Springer Science & Business Media, 2008.

- Hyndman et al. (2022) Hyndman, R., Athanasopoulos, G., Bergmeir, C., Caceres, G., Chhay, L., O’Hara-Wild, M., Petropoulos, F., Razbash, S., Wang, E., and Yasmeen, F. forecast: Forecasting functions for time series and linear models, 2022. URL https://pkg.robjhyndman.com/forecast/. R package version 8.16.

- Hyndman & Khandakar (2008) Hyndman, R. J. and Khandakar, Y. Automatic time series forecasting: the forecast package for R. Journal of Statistical Software, 26(3):1–22, 2008. doi: 10.18637/jss.v027.i03.

- Kim et al. (1998) Kim, S., Shephard, N., and Chib, S. Stochastic volatility: Likelihood inference and comparison with ARCH models. The Review of Economic Studies, 65(3):361–393, 07 1998. ISSN 0034-6527. URL https://doi.org/10.1111/1467-937X.00050.

- Koochali et al. (2022) Koochali, A., Schichtel, P., Dengel, A., and Ahmed, S. Random noise vs state-of-the-art probabilistic forecasting methods: A case study on crps-sum discrimination ability. arXiv preprint arXiv:2201.08671, 2022.

- Krupskii & Joe (2020) Krupskii, P. and Joe, H. Flexible copula models with dynamic dependence and application to financial data. Econometrics and Statistics, 16:148–167, 2020. ISSN 2452-3062. doi: https://doi.org/10.1016/j.ecosta.2020.01.005. URL https://www.sciencedirect.com/science/article/pii/S2452306220300216.

- Le Guen & Thome (2020) Le Guen, V. and Thome, N. Probabilistic time series forecasting with shape and temporal diversity. In Larochelle, H., Ranzato, M., Hadsell, R., Balcan, M. F., and Lin, H. (eds.), Advances in Neural Information Processing Systems, volume 33, pp. 4427–4440. Curran Associates, Inc., 2020. URL https://proceedings.neurips.cc/paper/2020/file/2f2b265625d76a6704b08093c652fd79-Paper.pdf.

- Li et al. (2019) Li, S., Jin, X., Xuan, Y., Zhou, X., Chen, W., Wang, Y.-X., and Yan, X. Enhancing the locality and breaking the memory bottleneck of transformer on time series forecasting. In Wallach, H., Larochelle, H., Beygelzimer, A., d'Alché-Buc, F., Fox, E., and Garnett, R. (eds.), Advances in Neural Information Processing Systems, volume 32. Curran Associates, Inc., 2019. URL https://proceedings.neurips.cc/paper/2019/file/6775a0635c302542da2c32aa19d86be0-Paper.pdf.

- Lim & Zohren (2021) Lim, B. and Zohren, S. Time-series forecasting with deep learning: a survey. Philosophical Transactions of the Royal Society A: Mathematical, Physical and Engineering Sciences, 379(2194):20200209, 2021. doi: 10.1098/rsta.2020.0209. URL https://royalsocietypublishing.org/doi/abs/10.1098/rsta.2020.0209.

- Lim et al. (2021) Lim, B., Arık, S. Ö., Loeff, N., and Pfister, T. Temporal Fusion Transformers for interpretable multi-horizon time series forecasting. International Journal of Forecasting, 37(4):1748–1764, 2021. ISSN 0169-2070. doi: https://doi.org/10.1016/j.ijforecast.2021.03.012. URL https://www.sciencedirect.com/science/article/pii/S0169207021000637.

- Lin et al. (2021) Lin, T., Wang, Y., Liu, X., and Qiu, X. A survey of transformers, 2021. URL https://arxiv.org/abs/2106.04554.

- Lopez-Paz et al. (2012) Lopez-Paz, D., Hernández-lobato, J., and Schölkopf, B. Semi-supervised domain adaptation with non-parametric copulas. In Pereira, F., Burges, C. J. C., Bottou, L., and Weinberger, K. Q. (eds.), Advances in Neural Information Processing Systems, volume 25. Curran Associates, Inc., 2012. URL https://proceedings.neurips.cc/paper/2012/file/8e98d81f8217304975ccb23337bb5761-Paper.pdf.

- Makridakis et al. (2018) Makridakis, S., Spiliotis, E., and Assimakopoulos, V. Statistical and machine learning forecasting methods: Concerns and ways forward. PLoS ONE, 13(3):e0194889–26, 2018.

- Makridakis et al. (2021) Makridakis, S., Spiliotis, E., Assimakopoulos, V., Chen, Z., Gaba, A., Tsetlin, I., and Winkler, R. L. The M5 uncertainty competition: Results, findings and conclusions. International Journal of Forecasting, 2021. ISSN 0169-2070. doi: https://doi.org/10.1016/j.ijforecast.2021.10.009. URL https://www.sciencedirect.com/science/article/pii/S0169207021001722.

- Makridakis et al. (2022) Makridakis, S., Spiliotis, E., and Assimakopoulos, V. M5 accuracy competition: Results, findings, and conclusions. International Journal of Forecasting, 2022. ISSN 0169-2070. doi: https://doi.org/10.1016/j.ijforecast.2021.11.013. URL https://www.sciencedirect.com/science/article/pii/S0169207021001874.

- Matheson & Winkler (1976) Matheson, J. E. and Winkler, R. L. Scoring rules for continuous probability distributions. Management science, 22(10):1087–1096, 1976.

- Mayer & Wied (2021) Mayer, A. and Wied, D. Estimation and inference in factor copula models with exogenous covariates, 2021. URL https://arxiv.org/abs/2107.03366.

- Montero-Manso & Hyndman (2021) Montero-Manso, P. and Hyndman, R. J. Principles and algorithms for forecasting groups of time series: Locality and globality. International Journal of Forecasting, 37(4):1632–1653, 2021. ISSN 0169-2070. doi: https://doi.org/10.1016/j.ijforecast.2021.03.004. URL https://www.sciencedirect.com/science/article/pii/S0169207021000558.

- Müller et al. (2022) Müller, S., Hollmann, N., Arango, S. P., Grabocka, J., and Hutter, F. Transformers can do Bayesian inference. In International Conference on Learning Representations, 2022. URL https://openreview.net/forum?id=KSugKcbNf9.

- Nelsen (2007) Nelsen, R. B. An introduction to copulas. Springer Science & Business Media, second edition, 2007.

- Newey & West (1987) Newey, W. K. and West, K. D. A simple, positive semi-definite, heteroskedasticity and autocorrelation consistent covariance matrix. Econometrica, 55(3):703–708, 1987. ISSN 00129682, 14680262. URL http://www.jstor.org/stable/1913610.

- Newey & West (1994) Newey, W. K. and West, K. D. Automatic Lag Selection in Covariance Matrix Estimation. The Review of Economic Studies, 61(4):631–653, 10 1994. ISSN 0034-6527. doi: 10.2307/2297912. URL https://doi.org/10.2307/2297912.

- Oreshkin et al. (2020) Oreshkin, B. N., Carpov, D., Chapados, N., and Bengio, Y. N-BEATS: Neural basis expansion analysis for interpretable time series forecasting. In International Conference on Learning Representations, 2020. URL https://openreview.net/forum?id=r1ecqn4YwB.

- Papamakarios et al. (2021) Papamakarios, G., Nalisnick, E., Rezende, D. J., Mohamed, S., and Lakshminarayanan, B. Normalizing flows for probabilistic modeling and inference. Journal of Machine Learning Research, 22(57):1–64, 2021. URL http://jmlr.org/papers/v22/19-1028.html.

- Paszke et al. (2019) Paszke, A., Gross, S., Massa, F., Lerer, A., Bradbury, J., Chanan, G., Killeen, T., Lin, Z., Gimelshein, N., Antiga, L., Desmaison, A., Kopf, A., Yang, E., DeVito, Z., Raison, M., Tejani, A., Chilamkurthy, S., Steiner, B., Fang, L., Bai, J., and Chintala, S. Pytorch: An imperative style, high-performance deep learning library. In Wallach, H., Larochelle, H., Beygelzimer, A., d’Alché Buc, F., Fox, E., and Garnett, R. (eds.), Advances in Neural Information Processing Systems 32, pp. 8024–8035. Curran Associates, Inc., 2019. URL http://papers.neurips.cc/paper/9015-pytorch-an-imperative-style-high-performance-deep-learning-library.pdf.

- Patton (2012) Patton, A. J. A review of copula models for economic time series. Journal of Multivariate Analysis, 110:4–18, 2012.

- Peterson (2017) Peterson, M. An Introduction to Decision Theory. Cambridge Introductions to Philosophy. Cambridge University Press, second edition, 2017. doi: 10.1017/9781316585061.

- Pinson & Tastu (2013) Pinson, P. and Tastu, J. Discrimination ability of the energy score. DTU Informatics, 2013.

- R Core Team (2020) R Core Team. R: A Language and Environment for Statistical Computing. R Foundation for Statistical Computing, Vienna, Austria, 2020. URL https://www.R-project.org/.

- Rasul (2021a) Rasul, K. PyTorchTS, 2021a. URL https://github.com/zalandoresearch/pytorch-ts.

- Rasul (2021b) Rasul, K. personal communication, 2021b.

- Rasul et al. (2021a) Rasul, K., Seward, C., Schuster, I., and Vollgraf, R. Autoregressive denoising diffusion models for multivariate probabilistic time series forecasting. In Meila, M. and Zhang, T. (eds.), Proceedings of the 38th International Conference on Machine Learning, volume 139 of Proceedings of Machine Learning Research, pp. 8857–8868. PMLR, 18–24 Jul 2021a. URL https://proceedings.mlr.press/v139/rasul21a.html.

- Rasul et al. (2021b) Rasul, K., Sheikh, A.-S., Schuster, I., Bergmann, U. M., and Vollgraf, R. Multivariate probabilistic time series forecasting via conditioned normalizing flows. In International Conference on Learning Representations, 2021b. URL https://openreview.net/forum?id=WiGQBFuVRv.

- Rémillard et al. (2012) Rémillard, B., Papageorgiou, N., and Soustra, F. Copula-based semiparametric models for multivariate time series. Journal of Multivariate Analysis, 110:30–42, 2012. ISSN 0047-259X. doi: https://doi.org/10.1016/j.jmva.2012.03.001. URL https://www.sciencedirect.com/science/article/pii/S0047259X1200070X. Special Issue on Copula Modeling and Dependence.

- Salinas et al. (2019) Salinas, D., Bohlke-Schneider, M., Callot, L., Medico, R., and Gasthaus, J. High-dimensional multivariate forecasting with low-rank Gaussian copula processes. Advances in Neural Information Processing Systems, 32:6827–6837, 2019.

- Salinas et al. (2020) Salinas, D., Flunkert, V., Gasthaus, J., and Januschowski, T. DeepAR: Probabilistic forecasting with autoregressive recurrent networks. International Journal of Forecasting, 36(3):1181–1191, 2020.

- Seabold & Perktold (2010) Seabold, S. and Perktold, J. statsmodels: Econometric and statistical modeling with Python. In 9th Python in Science Conference, 2010.

- Shih et al. (2019) Shih, S.-Y., Sun, F.-K., and Lee, H.-y. Temporal pattern attention for multivariate time series forecasting. Machine Learning, 108(8-9):1421–1441, 2019.

- Shukla & Marlin (2021a) Shukla, S. N. and Marlin, B. Multi-time attention networks for irregularly sampled time series. In International Conference on Learning Representations, 2021a. URL https://openreview.net/forum?id=4c0J6lwQ4_.

- Shukla & Marlin (2021b) Shukla, S. N. and Marlin, B. M. A survey on principles, models and methods for learning from irregularly sampled time series, 2021b. URL https://arxiv.org/abs/2012.00168.

- Sklar (1959) Sklar, A. Fonctions de répartition à dimensions et leurs marges. Publications de l’Institut Statistique de l’Université de Paris, 8:229–231, 1959.

- Sohl-Dickstein et al. (2015) Sohl-Dickstein, J., Weiss, E., Maheswaranathan, N., and Ganguli, S. Deep unsupervised learning using nonequilibrium thermodynamics. In Bach, F. and Blei, D. (eds.), Proceedings of the 32nd International Conference on Machine Learning, volume 37 of Proceedings of Machine Learning Research, pp. 2256–2265, Lille, France, 07–09 Jul 2015. PMLR. URL https://proceedings.mlr.press/v37/sohl-dickstein15.html.

- Spadon et al. (2021) Spadon, G., Hong, S., Brandoli, B., Matwin, S., Rodrigues-Jr, J. F., and Sun, J. Pay attention to evolution: Time series forecasting with deep graph-evolution learning. IEEE Transactions on Pattern Analysis & Machine Intelligence, 2021. ISSN 1939-3539. doi: 10.1109/TPAMI.2021.3076155.

- Stan Development Team (2022) Stan Development Team. Stan modeling language users guide and reference manual, 2022. URL https://mc-stan.org.

- Sun et al. (2020) Sun, C., Hong, S., Song, M., and Li, H. A review of deep learning methods for irregularly sampled medical time series data, 2020. URL https://arxiv.org/abs/2010.12493.

- Tabak & Turner (2013) Tabak, E. G. and Turner, C. V. A family of nonparametric density estimation algorithms. Communications on Pure and Applied Mathematics, 66(2):145–164, 2013.

- Tang & Matteson (2021) Tang, B. and Matteson, D. Probabilistic transformer for time series analysis. Advances in Neural Information Processing Systems, 34, 2021.

- Tashiro et al. (2021) Tashiro, Y., Song, J., Song, Y., and Ermon, S. CSDI: Conditional score-based diffusion models for probabilistic time series imputation. In Advances in Neural Information Processing Systems, volume 34, 2021.

- Tay et al. (2020) Tay, Y., Dehghani, M., Bahri, D., and Metzler, D. Efficient transformers: A survey, 2020. URL https://arxiv.org/abs/2009.06732.

- Uria et al. (2014) Uria, B., Murray, I., and Larochelle, H. A deep and tractable density estimator. In International Conference on Machine Learning, volume 32, pp. 467–475. PMLR, 2014.

- van den Oord et al. (2016) van den Oord, A., Dieleman, S., Zen, H., Simonyan, K., Vinyals, O., Graves, A., Kalchbrenner, N., Senior, A., and Kavukcuoglu, K. Wavenet: A generative model for raw audio. In Arxiv, 2016. URL https://arxiv.org/abs/1609.03499.

- Vaswani et al. (2017) Vaswani, A., Shazeer, N., Parmar, N., Uszkoreit, J., Jones, L., Gomez, A. N., Kaiser, Ł., and Polosukhin, I. Attention is all you need. In Advances in neural information processing systems, pp. 5998–6008, 2017.

- Wei (2018) Wei, W. W. Multivariate time series analysis and applications. John Wiley & Sons, 2018.

- Wiese et al. (2019) Wiese, M., Knobloch, R., and Korn, R. Copula & marginal flows: Disentangling the marginal from its joint. arXiv preprint arXiv:1907.03361, 2019.

- Williams & Rasmussen (2006) Williams, C. K. and Rasmussen, C. E. Gaussian processes for machine learning, volume 2. MIT press Cambridge, MA, 2006.

- Wu et al. (2021) Wu, H., Xu, J., Wang, J., and Long, M. Autoformer: Decomposition transformers with auto-correlation for long-term series forecasting. In Ranzato, M., Beygelzimer, A., Dauphin, Y., Liang, P., and Vaughan, J. W. (eds.), Advances in Neural Information Processing Systems, volume 34, pp. 22419–22430. Curran Associates, Inc., 2021. URL https://proceedings.neurips.cc/paper/2021/file/bcc0d400288793e8bdcd7c19a8ac0c2b-Paper.pdf.

- Wu et al. (2020) Wu, S., Xiao, X., Ding, Q., Zhao, P., Wei, Y., and Huang, J. Adversarial sparse transformer for time series forecasting. In Larochelle, H., Ranzato, M., Hadsell, R., Balcan, M., and Lin, H. (eds.), Advances in Neural Information Processing Systems, volume 33, pp. 17105–17115. Curran Associates, Inc., 2020. URL https://proceedings.neurips.cc/paper/2020/file/c6b8c8d762da15fa8dbbdfb6baf9e260-Paper.pdf.

- Yanchenko & Mukherjee (2020) Yanchenko, A. K. and Mukherjee, S. Stanza: A nonlinear state space model for probabilistic inference in non-stationary time series. arXiv, pp. 2006.06553v1, 2020.

- Zhang et al. (1998) Zhang, G., Eddy Patuwo, B., and Y. Hu, M. Forecasting with artificial neural networks:: The state of the art. International Journal of Forecasting, 14(1):35–62, 1998. ISSN 0169-2070. doi: https://doi.org/10.1016/S0169-2070(97)00044-7. URL https://www.sciencedirect.com/science/article/pii/S0169207097000447.

Appendix – Table of Contents

appendix.Aappendix.Bsubsection.B.1subsection.B.2subsection.B.3subsection.B.4appendix.Csubsection.C.1subsection.C.2subsection.C.3subsection.C.4subsection.C.5subsection.C.6appendix.Dsubsection.D.1subsection.D.2subsection.D.3subsection.D.4appendix.Esubsection.E.1subsection.E.2subsection.E.3

Appendix A Theory: Proof of Theorem 1

Theorem 1.

Proof.

To show that is the density of a valid copula, we need to show two properties: 1) it is a distribution on the unit cube , 2) the marginal distribution of each random variable is uniform.

Property (1) is trivially satisfied since, by construction, the support of each conditional distribution is limited to the interval (see § 4.2, paragraph Choice of distribution).

Property (2) is a consequence of minimizing the problem in Eq. 9. Recall that the parameters of the decoder, , are obtained by minimizing the following expression:

| (10) |

Notice that the term inside the logarithm in Eq. 10 corresponds to a geometric mean. This quantity is always smaller or equal to the arithmetic mean, and equality is reached i.i.f. all elements over which the mean is calculated are equal. Hence, we can rewrite the expression in Eq. 10 as:

where is exactly zero i.i.f. the density estimated by the model is permutation invariant, i.e., .

Based on this expression, we conclude that the parameters that minimize the problem in Eq. 9 lead a density estimator that (i) is invariant to permutations and (ii) that minimizes the negative log-likelihood of the data . It naturally follows from Eq. 5 that the embedded copula density is also permutation invariant.

Now, recall that, by construction, the marginal density of the first element in a permutation , is taken to be that of a (see § 4.2, paragraph Copula density). Given that the copula density is invariant to permutations, the marginal distribution of all variables must necessarily be . Thus, Property (2) is satisfied.

Since Properties (1) and (2) are both satisfied, we conclude that the attentional copula , with parameters obtained from a decoder with parameters is a valid copula.

∎

Appendix B Implementation Details

B.1 Libraries Used

The version of tactis used in this work is implemented in PyTorch (Paszke et al., 2019). It relies on the PyTorchTS library (Rasul, 2021a), which allows the integration of PyTorch models with the GluonTS library (Alexandrov et al., 2020), on which we rely heavily in our experiments for data processing, model training, and evaluation. The implementation is available at https://github.com/servicenow/tactis.

B.2 Inverting the Marginal Flows

When sampling from the learned joint distribution, it is needed to compute the inverse of the marginal CDF for each variable, i.e., to invert the marginal flows: . Since is strictly monotonic by construction, many search algorithms can be applied. We choose to rely on binary search due to its numerical stability and ease of implementation. While such searches are relatively slow, the overhead in compute time is negligible compared to other computations in the decoder, which are dominated by the transformer layers in the copula.

One weakness of using flows as marginal distributions is that there is very little pressure toward having well-regularized tails ( or ). When sampling from these flows, they will rarely produce values that are much smaller or larger than those in the observed data due to these tails not having the correct shape. Given the difficulty of training the flows to avoid this issue entirely, we opted to consider only a portion of the marginals when sampling. That is, instead of sampling from the full range in the attentional copula, we rescale sampled values to be in the range: . This issue and alternative solutions have also been explored in Wiese et al. (2019).

B.3 Bagging: Efficient Training in High Dimensions

Two of the models in our benchmarks: GPVar and tactis-tt, can be trained with arbitrary subsets of the time series in the data without having to adjust their parameters.101010Note that all variants of tactis that we consider also support such bagging during training. Hence, the memory footprint of the model during the training phase can be significantly reduced by considering bags of randomly selected time series. In our experiments, each training batch for these models is a bag of time series. At sampling time, the models are applied to the full set of time series.

B.4 Data Normalization

It is often desirable for a model to be scale and translation invariant. For tactis, we thus transform the data according to what we call the ”Standardization” procedure. For each sample, we compute the means and variances for each series using only the values of the observed tokens . The values of both the observed and missing tokens is then transformed using

| (11) |

After sampling, we can undo this transformation using

| (12) |

Note that we consider a lower bound of for the variance to avoid division by zero in cases where all values are (nearly) identical. The precise value of this lower bound has no impact on the training when all values are identical. Yet, it has a massive one when sampling since the sampled values are unlikely to all be zero when the marginal flows are not perfectly fitted. Choosing a very small lower bound thus minimizes this issue.

Appendix C Forecasting Benchmark

C.1 Datasets

| Short name | Monash name | Frequency | Number of series | Prediction length |

|---|---|---|---|---|

| electricity | Electricity Hourly Dataset | 1 hour | 321 | 24 |

| fred-md | FRED-MD Dataset | 1 month | 107 | 12 |

| kdd-cup | KDD Cup Dataset (without Missing Values) | 1 hour | 270 | 48 |

| solar-10min | Solar Dataset (10 Minutes Observations) | 10 minutes | 137 | 72 |

| traffic | Traffic Hourly Dataset | 1 hour | 862 | 24 |

Tab. 3 describes the five datasets that are included in our benchmark. These datasets were selected due to being publicly available in the Monash Time Series Forecasting Repository (Godahewa et al., 2021), not containing missing values, having a large (but reasonable) number of dimensions, and being sampled at diverse frequencies. A modified version of the electricity dataset is often used for benchmarking in the literature, allowing a rough comparison of our results with those of other authors and reinforcing our belief that they are correct. A variant of the solar-10min dataset, with hourly frequency, is also often used in the literature. We opted for the 10 minutes version to include such a high-frequency dataset in the benchmark. The prediction length for this dataset was limited to 72 (12 hours) due to a prediction length of 144 (24 hours) being too taxing for the transformer-based models. The fred-md dataset was selected due to the nature of its series: various economic indicators, which exhibit a wide variety of behaviours. For the kdd-cup dataset, a prediction length of 48 (2 days) was used to challenge the models at producing longer forecasts than for the other hourly-frequency datasets. Finally, the traffic dataset was selected for being very high-dimensional (862 series).

C.2 Training Procedure

C.2.1 Deep Learning Models

All deep learning models in our benchmarks: TempFlow, TimeGrad, GPVar, and tactis-tt, are trained using the same procedure, except for a few exceptions for GPVar, which we detail below. Each training is done in a Docker container giving access to an nvidia Tesla P100 GPU with 12 GB of GPU RAM, 2 CPU cores, and 32 GB of CPU RAM.

Batch size

These models are fairly memory-intensive and the amount of resources required varies considerably based on the hyperparameters and the dataset considered. Hence, it was necessary to devise a batch-size selection procedure that would ensure that the model did not outgrow the available resources. To select the batch sizes for a given set of hyperparameters, we ran a small number of training iterations with various batch sizes (powers of two from 1 to 256) and kept the largest one which did not result in an out-of-memory error. While this method is crude, it allows hyperparameters that require less memory to take advantage of the available memory to train faster due to higher parallelization.

Training loop

In each training epoch, the models are presented with 1600 random samples from the training set. Since the batch size is variable, we consider batches per epoch. As is explained in § B.3, the GPVar, and tactis-tt models use bagging during training and thus only see a random subset of all series at each iteration. To compensate for this, the number of batches per epoch for these models is increased to . The batches are built by randomly sampling (uniformly) windows of length equal to the sum of the prediction and history lengths from the training dataset. Only complete windows are considered.

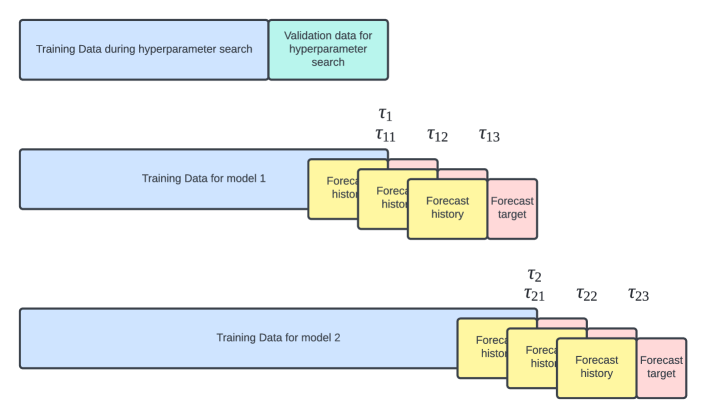

After each epoch, we compute a validation score on a subset of the training set used only for validation (see Fig. 6). The training ends when the first of the following condition is reached:

-

•

The model has trained for 200 epochs,

-

•

The model has trained for more than 3 days, or

-

•

It has been 20 epochs since the best validation score (early stopping).

The resulting model, which is used to compute the final metrics, is the one with minimal validation score. Since we compute the validation score at each epoch, the final model can be from an earlier epoch than the last one performed.

Exceptions for GPVar

Following communication with GPVar authors (Bohlke-Schneider & Salinas, 2021), we trained that model on CPU instead of GPU, due to performance concerns. To compensate for not having a GPU, we allocate 8 CPU cores and 64 GB of CPU RAM instead of the 2 CPU cores and 32 GB of CPU RAM allocated to models trained on GPU (see above). Furthermore, we used the GluonTS Trainer for GPVar, which implemented its own stopping conditions for training. Following what was done for other models, we added a condition which stopped training after a maximum of 3 days.

C.2.2 Classical Models

Our Auto-arima results are obtained by running the auto.arima function (Hyndman & Khandakar, 2008) of the forecast package (Hyndman et al., 2022) in the R programming language (R Core Team, 2020). This automatically searches the model specification on a per-time series basis. Since the function supports univariate time series only, we run the function independently for each time series (i.e., we treat a -dimensional multivariate problem as independent univariate problems), with the hyperparameters and parameters being specific to each time series. We restrict the search to sarima models with maximum order , and the default values for the other function parameters. We carry out an automatic Box-Cox transformation for positive-valued time series. For each time series, we limit fitting time to a maximum of 30 minutes, reverting to a simpler arma model with no seasonality or Box-Cox transformation if the original fitting fails. A fit is considered to have failed if the following conditions are encountered:

-

•

Maximum time limit is exceeded;

-

•

The in-sample fitted values contain non-finite values;

-

•

Fewer than 20% of the simulated predictive trajectories contain finite values (e.g. the predictive simulations diverge) or contain values that are not within a factor of 1,000 (in absolute value) of the training observations.

Our ETS (error, trend, seasonality) exponential smoothing (Hyndman et al., 2008) results are obtained through the ETSModel implementation within Python’s statsmodels package (Seabold & Perktold, 2010). This implementation replicates the R implementation within the forecast package discussed above. An automatic hyperparameter search is carried out to select, on a per-dataset basis, the following hyperparameters:

-

•

Trend: either none or additive;

-

•

Seasonality: either none or additive.

For robustness across a wide variety of datasets, the error term is always considered additive. As with the arima results, since ETS is univariate, independent fitting and predictive simulations of the model are carried out for each time series.

C.3 Hyperparameter Search Protocol

For each model and each dataset under consideration, we ran a hyperparameter search to find the best hyperparameters, which were then used when comparing the forecasting quality of the models. We opted to perform such a search ourselves instead of selecting previously published hyperparameter combinations for two reasons: 1) some datasets that we consider had not been considered when evaluating some methods we compare to, and 2) to maximize the fairness of the comparison by performing an equally extensive search for each model.

In each dataset, the final subset of the time steps is reserved for the backtesting procedure, which will be described in § C.5. From the remaining time steps, a window at the end of length equals to 7 times the prediction length is reserved to serve as the validation set, which is used to compute the metrics used to select the best hyperparameters. All the remaining data, i.e., what comes before the validation set, is used as the training set. See Fig. 6 for a visual representation of this split.

For each model, we considered 50 hyperparameter combinations, randomly selected amongst a range of values defined for each hyperparameter of the model. The models are trained 5 times for each combination of hyperparameters, using random initializations and data sampling orders. For each of these training runs, we compute forecasts using 100 samples for each prediction window in the validation set and average their CRPS-Sum.

We then selected the best hyperparameter combination as being the one where none of the 5 training runs failed due to numerical or memory errors and for which the worst CRPS-Sum value amongst the 5 training runs was the lowest. We considered the worst of the 5 runs instead of the mean or median since we observed that, for some architectures, some hyperparameters led to unstable training, which resulted in significant variability in the quality of the results. The rationale for avoiding such hyperparameter combinations is that such instability would be undesirable in real-world applications.

C.4 Hyperparameter Ranges

In this section, we list the values considered for each hyperparameter of each method. The ranges considered for the baselines are inspired by those published in their respective papers and implementations.

Tab. 4 shows the hyperparameters for the tactis-tt model.

| Hyperparameter | Possible values | |

|---|---|---|

| Model | Encoder transformer embedding size (per head) and feed forward network size | k, f, est |

| Encoder transformer number of heads | fks, et, | |

| Encoder number of transformer layers pairs | s, ef, kt | |

| Encoder time series embedding dimensions | efkst | |

| Decoder MLP number of layers | ekst, f, | |

| Decoder MLP hidden dimensions* | eft, , ks | |

| Decoder transformer number of heads | , , efkst | |

| Decoder transformer embedding size (per head) | efst, k, | |

| Decoder number transformer layers | ef, s, kt | |

| Decoder number of bins in conditional distribution | efst, k, | |

| Decoder DSF number of layers | fks, et | |

| Decoder DSF hidden dimensions | ft, eks | |

| Dropout | fkst, , e | |

| Data | Normalization | Standardizationefkst |

| History length to prediction length ratio | ft, ks, e | |

| Training | Optimizer | RMSpropefkst |

| Learning rate | s, efkt, | |

| Weight decay | et, ks, f, | |

| Gradient clipping | efks, t |

Tab. 5 shows the hyperparameters for the TempFlow model. Parameters in teletype font refer to parameters in the authors implementation in PyTorchTS (Rasul, 2021a), with all other parameters left at their default value. The choice of possible hyperparameters for the TempFlow model has been discussed with its authors (Rasul, 2021b).

| Hyperparameter | Possible values | |

|---|---|---|

| Model | d_model | , k, es, t, f |

| dim_feedforward_scale | e, , fkst | |

| num_heads | f, s, t, ek | |

| num_encoder_layers | t, k, efs | |

| num_decoder_layers | et, f, ks | |

| dropout_rate | est, k, f | |

| flow_type | "RealNVP"ekst, "MAF"f | |

| n_blocks | f, , ekst | |

| hidden_size | t, f, s, k, e | |

| n_hidden | , fk, est | |

| conditioning_length | , fs, t, k, e | |

| dequantize | Falseekst, Truef | |

| Data | History length to prediction length ratio | efk, s, t |

| Training | Optimizer | Adamefkst |

| Learning rate | fs, et, k | |

| Gradient clipping | kst, ef, |

Tab. 6 shows the hyperparameters for the TimeGrad model. Parameters in teletype font refer to parameters in the authors implementation in PyTorchTS (Rasul, 2021a), with all other parameters left at their default value.

| Hyperparameter | Possible values | |

|---|---|---|

| Model | num_layers | , , efkst |

| num_cells | fkt, s, e | |

| dropout_rate | fs, e, kt | |

| diff_steps | , , efkst | |

| beta_schedule | "linear"fk, "quad"est | |

| residual_layers | e, t, fks | |

| residual_channels | fks, , et | |

| scaling | Falset, Trueefks | |

| Data | History length to prediction length ratio | ft, ks, e |

| Training | Optimizer | Adamefkst |

| Learning rate | ft, e, ks | |

| Gradient clipping | , fks, et |

Tab. 7 shows the hyperparameters for the GPVar model. Parameters in teletype font refer to parameters in the authors implementation in GluonTS (Alexandrov et al., 2020), with all other parameters left at their default value.

| Hyperparameter | Possible values | |

|---|---|---|

| Model | num_layers | e, k, fst |

| num_cells | t, fs, k, , e | |

| cell_type | "lstm"fks, "gru"et | |

| use_marginal_transformation | Trueefkst, False | |

| rank | f, ek, st | |

| dropout_rate | ft, e, ks | |

| Data | History length to prediction length ratio | , st, efk |

| Training | Optimizer | Adamefkst |

| Learning rate | eft, ks, | |

| Weight decay | k, ft, , , es | |

| Gradient clipping | efkst |

C.5 Backtesting Protocol

We evaluate the performance of all models using a backtesting procedure that mimics how they would be applied to real-world problems. In practice, due to the high cost of hyperparameter search, it would be done seldomly. Model training with fixed hyperparameters is less expensive and would be done periodically. Finally, forecasting using a pre-trained model is cheap and would be done as needed. Therefore, in our framework, we conduct a single hyperparameter search, retrain the model multiple times (periodically), and calculate forecasts at multiple time stamps between retrainings.

For each dataset, we define backtesting timestamps , , …, . For each backtesting timestamps , we further define multiple forecasting timestamps , , …, . The hyperparameter search described in § C.3 is done using only data before , while the -th model is trained using only the data before . A visual representation of the split between the data used for model training, the historical data used for the forecast, and the target data to which forecasts are compared is shown in Fig. 6.

We use for all datasets. For electricity, we select Mondays at midnight as training time , with one week between each, and estimate forecasts every 24 hours between them. For fred-md, we select Januaries for the , with one year between each, and estimate only a single forecast at the same time. For kdd-cup, we also select Mondays at midnight for the , with two weeks between each, and estimate forecasts every 48 hours between them. For solar-10min, we also select Mondays at midnight for the , with one week between each, and estimate forecasts every 12 hours between them. For traffic, we also select Mondays at midnight for the , with one week between each, and estimate forecasts every 24 hours between them. The last backtesting timestamp for each dataset is selected as the last possible timestamp that follows the respective criterion while still having enough data after it for the full prediction range.