Estimation of the tail index of Pareto-type distributions using regularisation 11footnotemark: 1

Abstract

In this paper, we introduce reduced-bias estimators for the estimation of the tail index of a Pareto-type distribution. This is achieved through the use of a regularised weighted least squares with an exponential regression model for log-spacings of top order statistics. The asymptotic properties of the proposed estimators are investigated analytically and found to be asymptotically unbiased, consistent and normally distributed. Also, the finite sample behaviour of the estimators are studied through a simulations theory. The proposed estimators were found to yield low bias and MSE. In addition, the proposed estimators are illustrated through the estimation of the tail index of the underlying distribution of claims from the insurance industry.

Keywords and Phrases: Statistics of extremes ; tail index; Pareto-type distribution; large deviations; Hill estimator; Strong law of large numbers; Limit theorem.

MSC 2010: 62G32, 60F10, 60F25.

1 Introduction

Pareto-type distributions are often encountered in applications in the area of Finance [1, 2, 3], re-insurance [4, 5, 6], risk management [7, 8, 9] and telecommunication [10, 11]. This distribution type has tail function,

| (1) |

or equivalently upper tail quantile function

| (2) |

The component and are slowly varying functions expressed as

| (3) |

The parameter , is strictly positive for Pareto-type distributions and is also known as the tail index.

Suppose denote independent and identically distributed (i.i.d) random variables drawn from a distribution belonging to the maximum domain of attraction of the Pareto family of distributions, then for some auxiliary sequences of constants and [12]

| (4) |

where The estimation of continues to receive considerable attention in statistics of extremes as all inferences in extreme value analysis depend on the tail index. In practice, we seek estimators with less variance and bias as possible. A parametric or semi-parametric approach can be employed to estimate the tail index,[13], [14], [15], [16]. However, in this paper we employ the semi-parametric approach to develop reduced-bias estimators since they result in bias reduction.

Under the semi-parametric framework, the tail index estimators are dependent on the largest observations, with these assumption about :

-

Assumption 1: as .

-

Assumption 2: as .

The most widely used semi-parametric tail index estimator is the Hill estimator [17]. [17] approximates the top order statistics with a Pareto distribution and estimates using a maximum likelihood estimator (MLE). The Hill estimator has the minimum asymptotic variance among the semi-parametric estimators but it is very sensitive to the choice of [18]. This drawback of the estimator makes its usage challenging in practice, especially in the selection of the tail fraction, . [17] defined the tail estimator as

| (5) |

The Hill estimator due to it popularity has received several generalisations: See for example the works of [19], [20], [21], [22], [23], [24, 25] and [26].

Another estimator which is also a refinement of the Hill estimator is the bias-corrected Hill estimator [27]. The authors proposed two approaches for reducing the bias of the Hill estimator while maintaining the asymptotic variance of the Hill estimator. Empirically, the bias-corrected Hill estimator yields stable tail index estimates compared to the Hill estimator, i.e., the bias-corrected Hill estimator is less sensitive to the choice of relative to the Hill estimator.

In this study, we seek to propose alternative tail index estimators which empirically yield much more stable tail index estimates and attain the minimum asymptotic variance of the Hill estimator under some conditions. Tail index estimators which yield stable estimates are highly sort after in practice since they alleviate the problem of selecting an optimal to some extent.

2 Estimation Methods

We let denote a sequence of i.i.d random variables drawn from a population with distribution function and the associated tail quantile function . Let be the order statistics associated with the sample. Using Eqn. (2), the order statistics can be jointly expressed as,

| (6) |

where , represent the order statistics of the standard uniform distribution. Using Eqn. (6), we [28] demonstrated that

| (7) |

and we also obtained a more refined expression of Eqn. (7) by imposing a second-order assumption on the rate of convergence to Eqn. (3). This is stated in as an assumption as follows:

Assumption 3: There exists a real constant and a rate function satisfying as such that for all ,

| (8) |

with [28].

Under assumption 3, [28] showed that the weighted log-spacings of order statistics,

| (9) |

are approximately exponentially distributed. They particularly obtained the expression

| (10) |

where as , and are i.i.d exponentially distributed with a unit mean and () is a second-order parameter. The authors employed MLE to the estimate the parameters in Eqn. (10).

Using Eqn. (10) and assumptions 1 and 2, [29], demonstrated that can be further approximated as a regression model,

| (11) |

where is the slope, is the covariate, is the intercept and are error terms with asymptotic mean, , and variance, .

[29] proposed the ordinary least squares estimator for the estimation of in Eqn. (11). Further, based on Eqn. (11), [13] have introduced the ridge regression estimator for estimating . In this paper, we propose the regularised weighted least squares estimators for estimating in Eqn. (11).

2.1 The proposed estimators

In order to estimate , the loss function of the regularised weighted least squares for Eqn. (11) is defined as

| (12) |

Here, is the weight function defined as

| (13) |

where . Thus, and decreases linearly with respect to . The exponent is chosen such that

| (14) |

In this study, we consider .

Thus, we would define such that . Note that, is random through , and when the exponent is , is deterministic. In particular, when , we obtain the weight function as introduced by [30]. Nevertheless, we can approximate the weight as a limit of the current result by allowing to approach .

We minimize the loss function with respect to and to obtain jointly estimates and

| (15) |

and

| (16) |

while,

| (17) |

| (18) |

and

| (19) |

We substitute Eqn. (13) into Eqn. (17) to obtain an explicit expression for Eqn. (17) as

| (20) |

The parameter is estimated using the minimum variance approach introduced in [13].

In addition, the parameter in Eqn. (12) is the penalty that regulates the bias coefficient . The loss function, , minimises the weighted sum of squared residuals and also regulates the size of the bias coefficient . The penalty term shrinks the bias term, to as the penalty parameter, , increases. Thus, the larger the value of , the higher the contribution of the penalty term to the loss function and the stronger the regularisation process. To obtain an estimator for the penalty term, , we minimise the mean squared error (MSE) of the proposed estimator, . See,example [13].

Note that, since the weight function depends on the ’s, the estimators in Eqn. (15) and Eqn. (16) also depend on the ’s through the weight function. Therefore, we would find the MSE by conditioning on the ’s. From Eqn. (15) and Eqn. (16), the MSE for is obtained as

| (21) |

| (22) |

| (23) |

| (24) |

and

| (25) |

We now derive an expression for the penalty term, . Minimising over , the optimal value of is obtained by solving the equation

| (26) |

we obtain,

| (27) |

In order to estimate , we assume the slowly varying function in (8) is constant.Thus, we have

| (28) |

for some . We estimate via the estimator proposed by [31] to obtain

| (29) |

The penalty term, is required to be non-negative; therefore we define . We the obtain a penalty term and the estimators which does not depend on ’s,by averaging over the ’s, as follows:

| (30) |

and we defined the proposed estiamtor of by

2.1.1 Asymptotic Properties of the Proposed estimators

Unbiasedness, consistency and normality are desirable properties of a good estimator. In this section, we investigate desirable properties of the proposed estimator possesses.

We shall summarise the asymptotic behaviour of the statistics used to build the MSE of the proposed estimator in Lemma 1. These properties will be required in the proof of the asymptotic consistency and sampling distribution of the proposed estimator. Henceforth, anytime we use the term it is with respect to the law of the i.i.d sequence .

Lemma 1.

Assume that is estimated by a consistent estimator and (14) holds, then as and ;

-

i.

-

ii.

-

iii.

-

iv.

.

Lemma 2.

Suppose and are estimated by their respective consistent estimators and , then as and ,

| (31) |

It follows from Lemma 2 that the regularised weighted least estimator, is asymptotically unbiased. That is, as , . The bias of the proposed estimator is given as,

where

Since the term in the bracket converges to as almost sure by Lemma 2, the expectation of the term will converge to as . Therefore,

which gives , .

Similarly, we may use Lemma 1 and Lemma 2,to show that the MSE of as . Now, observe that

and therefore, we have

This implies that the proposed estimator is asymptotically consistent under some conditions.

Theorem 3.

Corollary 4.

Suppose (3) and (8) holds and also . Assume is estimated by a consistent estimator with Then as and ,

Theorem 3 discusses the asymptotic normality of defined in Eqn.(16). To prove Theorem 3 we require the following properties in addition.

We write

| (32) |

Lemma 5.

Let and Then as ,

where .

Lemma 6.

Let be independent random variables from an exponential distribution with mean , for all . Then for any

| (33) |

where is defined by Eqn.(15).

Remark 7.

Lemma 6 shows the statistics as .

The next Lemma is about the satisfaction of the Lyapunov’s version of the central limit theorem. The Lyapunov’s variant of the central limit theorem assumes the existence of a finite moment of an order higher than two.

Lemma 8.

Suppose that are independent random variables such that and , then there exists such that

| (34) |

where

Remark 9.

Setting the penalty term to 0 reduces the regularised weighted least squares estimator to a weighted least squares estimator. The difference between this weighted least squares estimator and the one introduced by [30] is that, this weighted least squares estimator has smaller asymptotic variance and this is due to the introduction of randomness into the weight function. The resulting weighted least squares estimator is also asymptotically unbiased, consistent, and normally distributed with mean and variance .

For proofs of the above Lemmas we refer interested person to [30].

3 Simulation Study

In the previous section, we proposed the regularised weighted least squares estimators under the semi-parametric setting to estimate the tail index of the underlying distribution of a given data from the Pareto-type of distributions. In this section, we perform a simulation study to compare the performance of our proposed estimators to other existing semi-parametric tail index estimators. Particularly, the regularised weighted least squares, RWLS, the reduced-bias weighted least squares with modified weight function, WLS, the ridge regression, RR [13], the least squares, LS [29], the Hill estimator, HILL [17] and the bias-corrected Hill, BCHILL [27] in the case of Pareto-type distributions are compared.

3.1 Simulation design

We consider the Fréchet and Burr XII from the Pareto-type distributions as shown in Table 1. For each distribution , we generate 1000 repetitions of samples of size and . For the Fréchet distributions, we consider and ; and for the Burr XII we consider the mixtures

-

i.

,

-

ii.

and

-

iii.

to obtain the tail index values and , respectively. We consider the finite sample behaviour of the proposed estimators, RWLS and WLS, and also compared these estimators with RR, LS, BCHILL and HILL. The MSE and bias are plotted as a function of the number of top-order statistics, , to investigate the estimators’ sample path behaviour.

In the case of the weight function, the ’s will be replaced with their point estimate, in this case, the mean of a standard uniform distribution. In the case of , we select such that , as . This choice of is made because in practice we have observed that it yields much more stable estimates compared to when is selected such that in application.

| Distribution | |||

|---|---|---|---|

| Burr type XII | |||

| Fréchet |

3.2 Discussion of simulation results

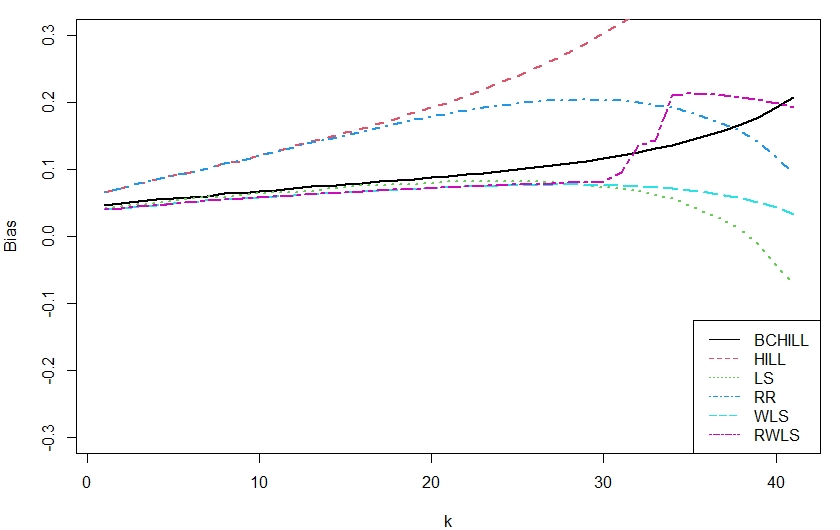

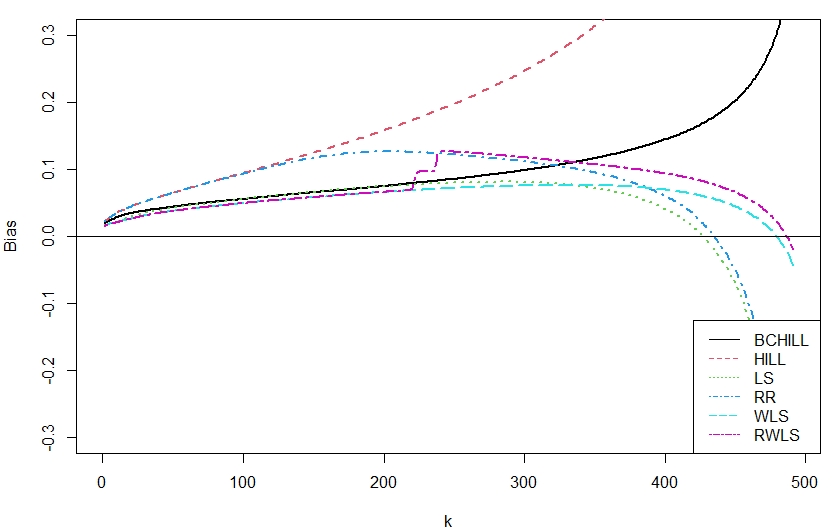

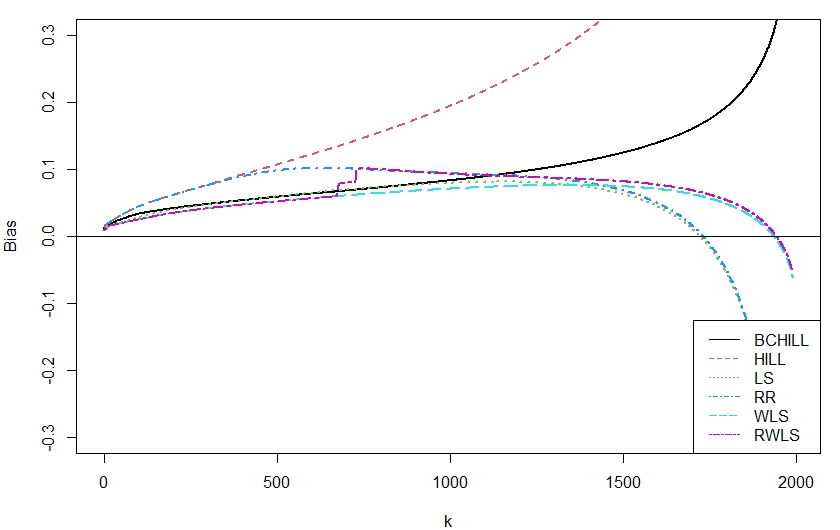

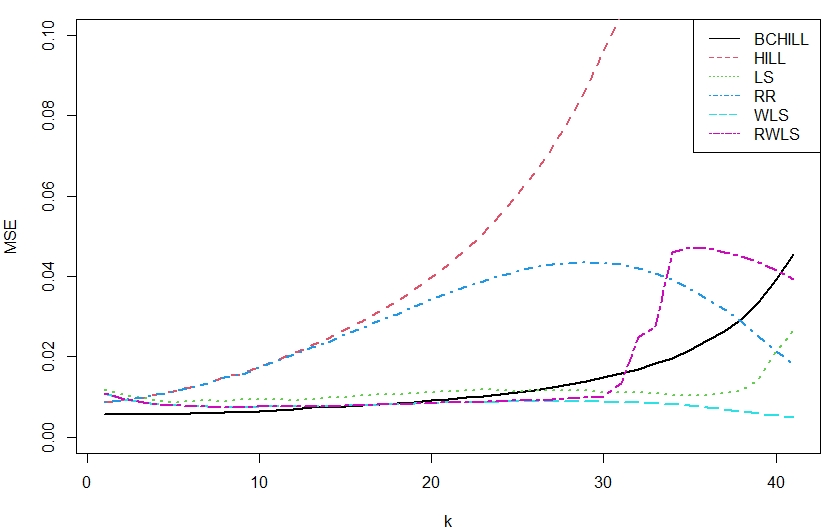

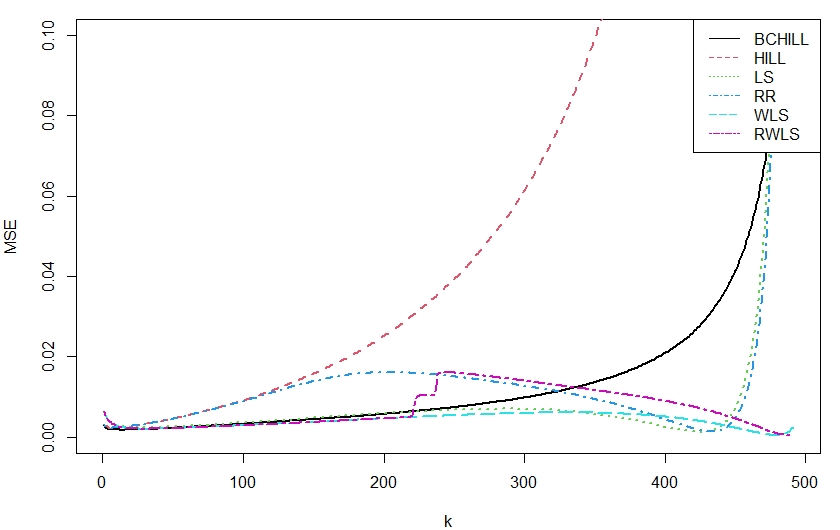

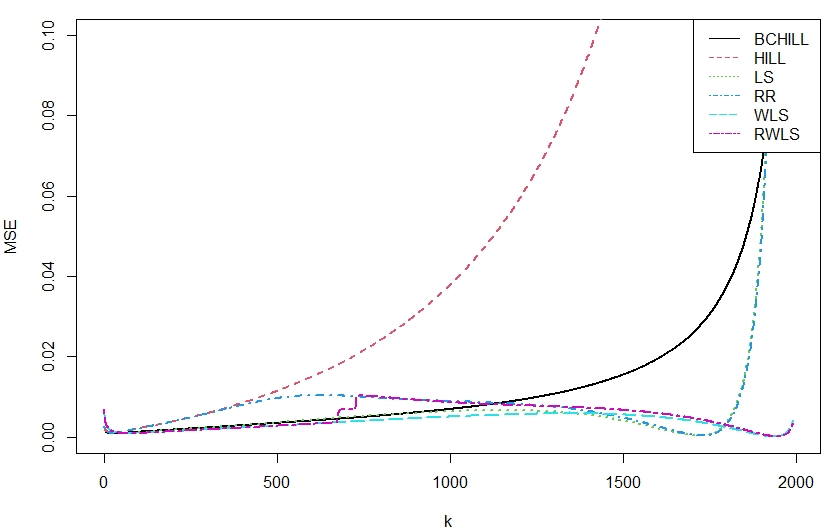

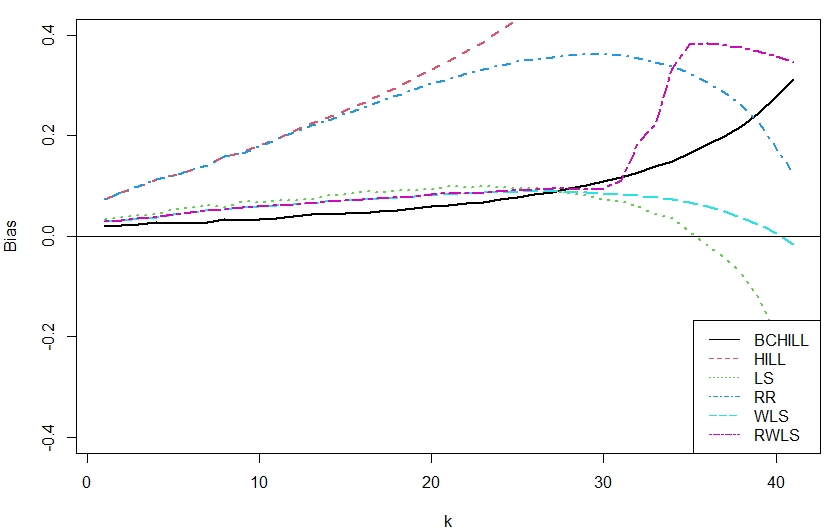

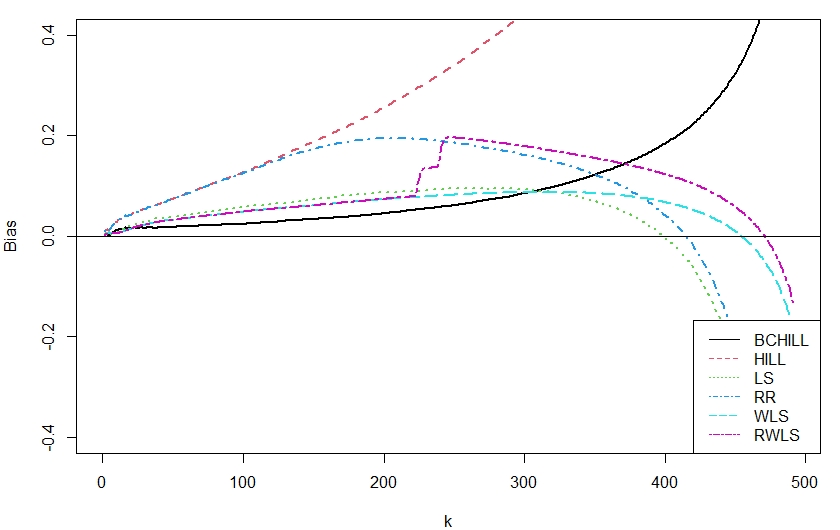

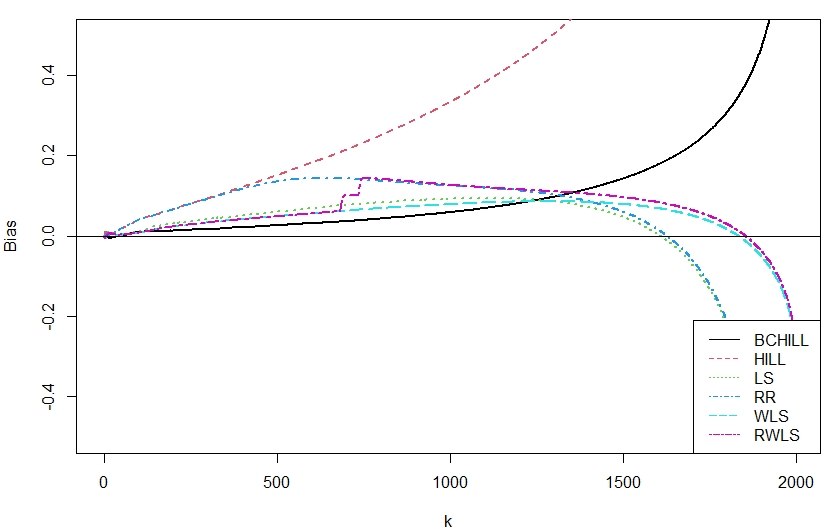

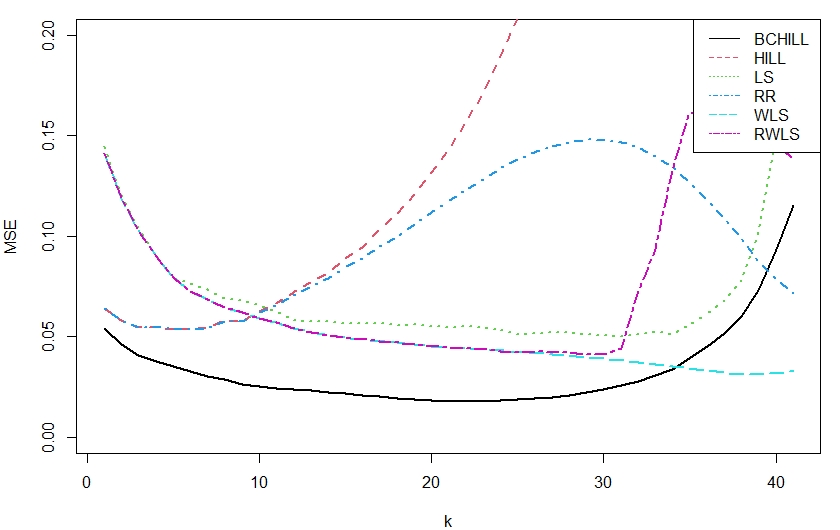

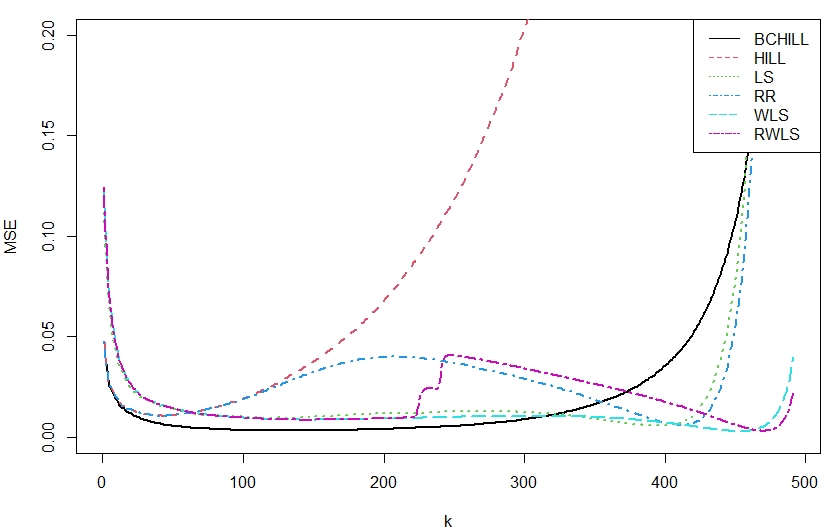

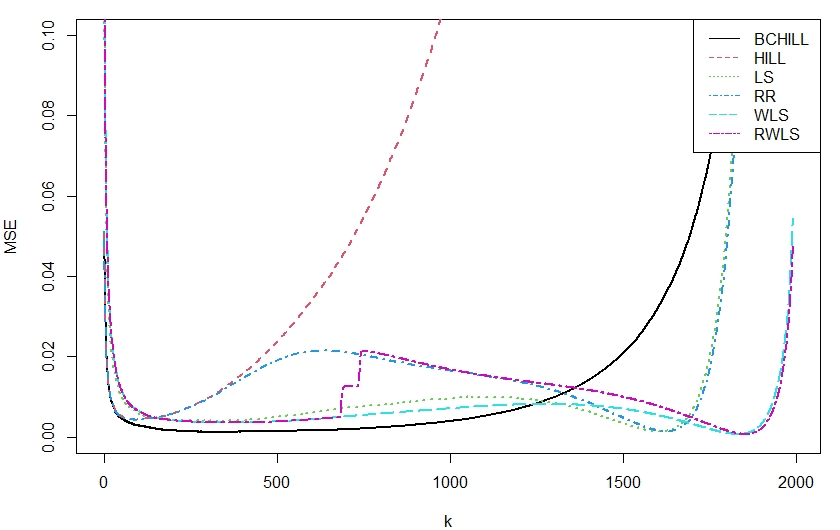

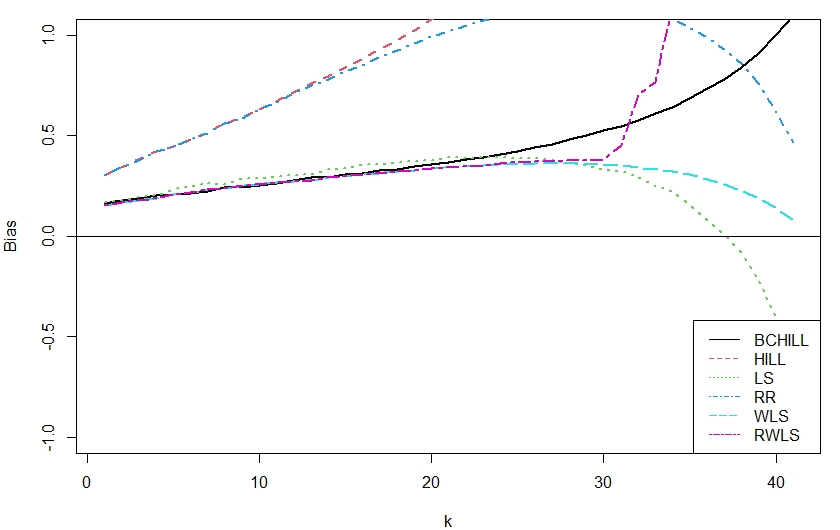

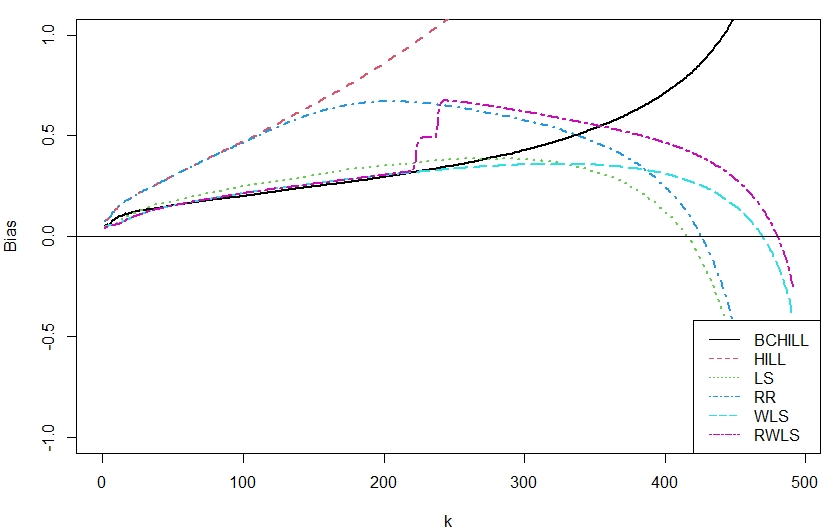

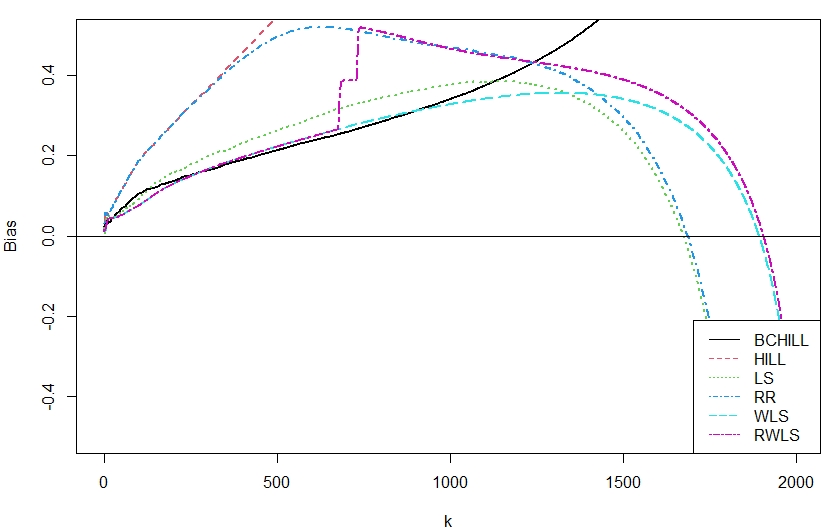

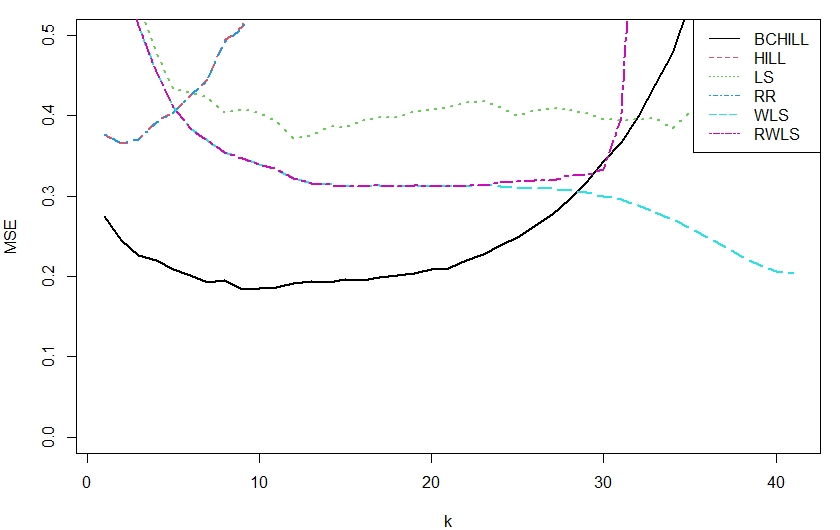

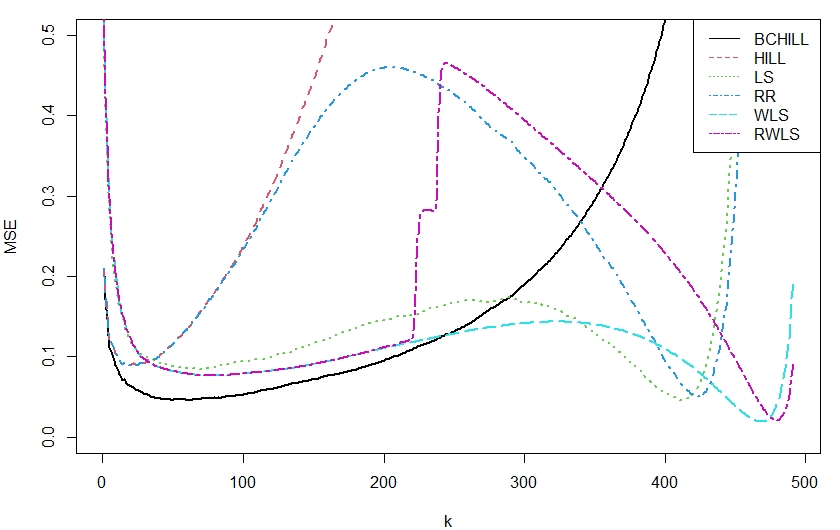

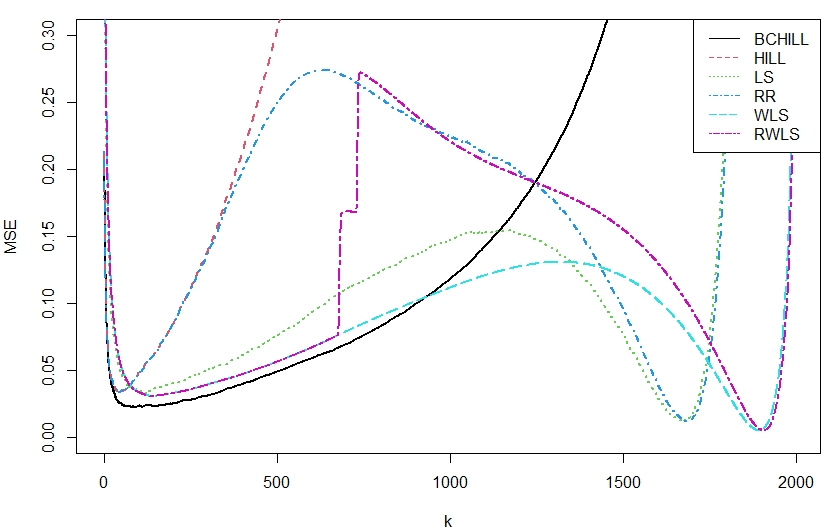

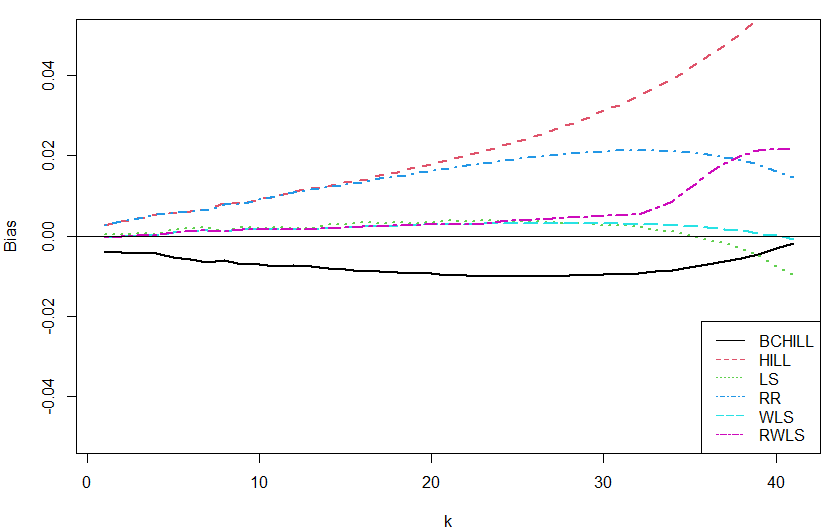

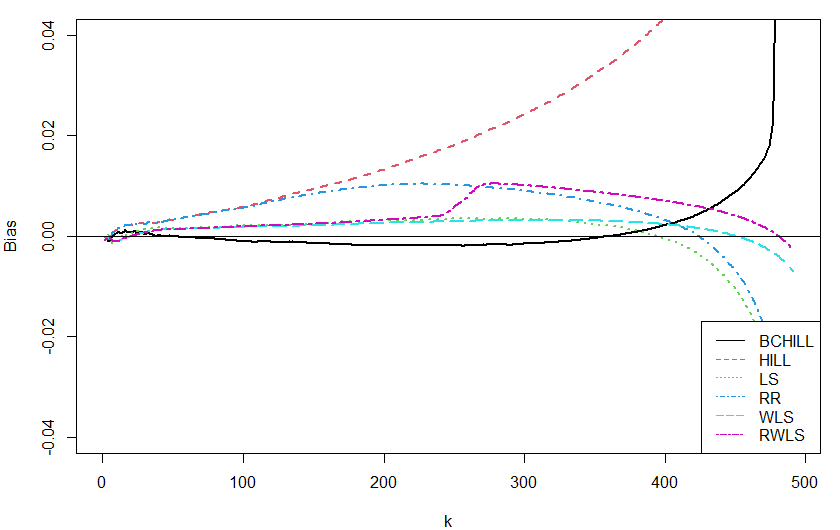

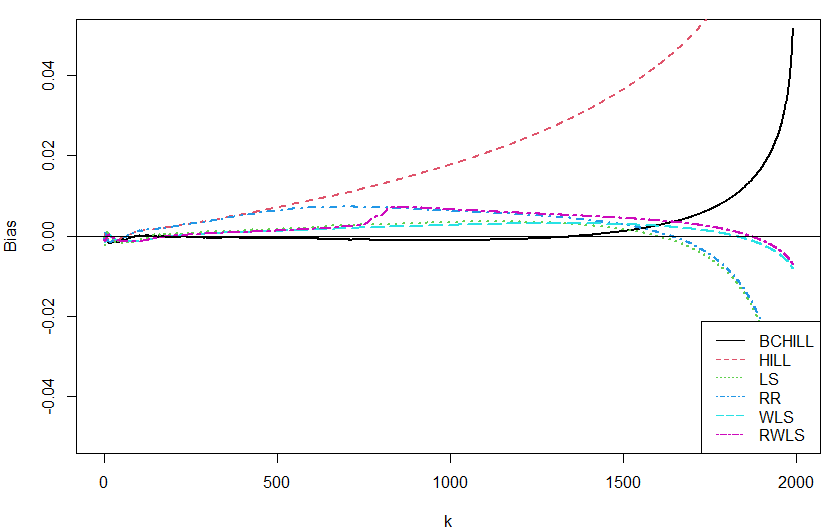

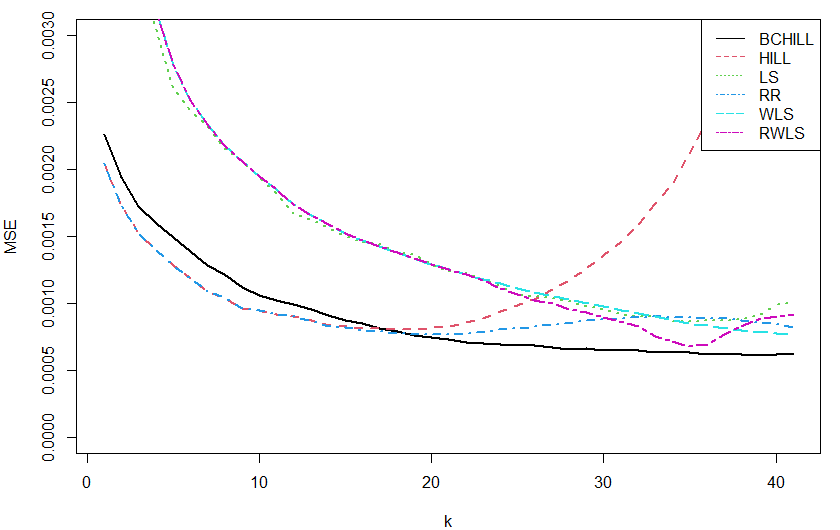

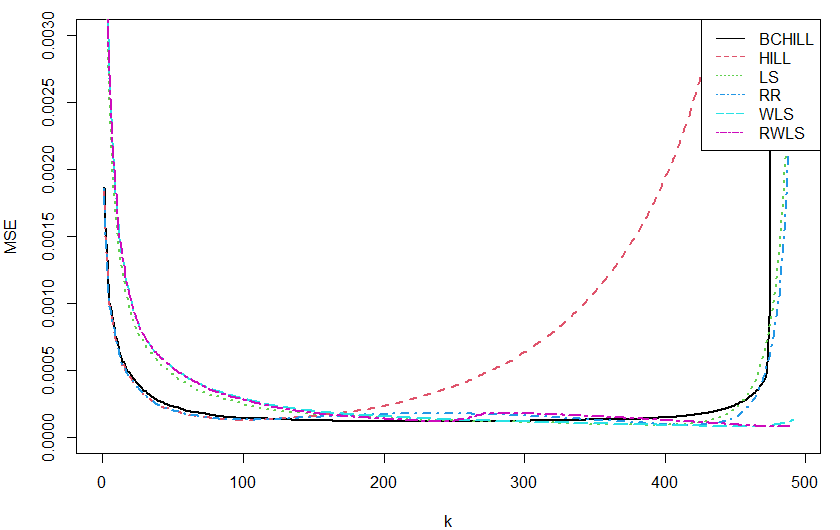

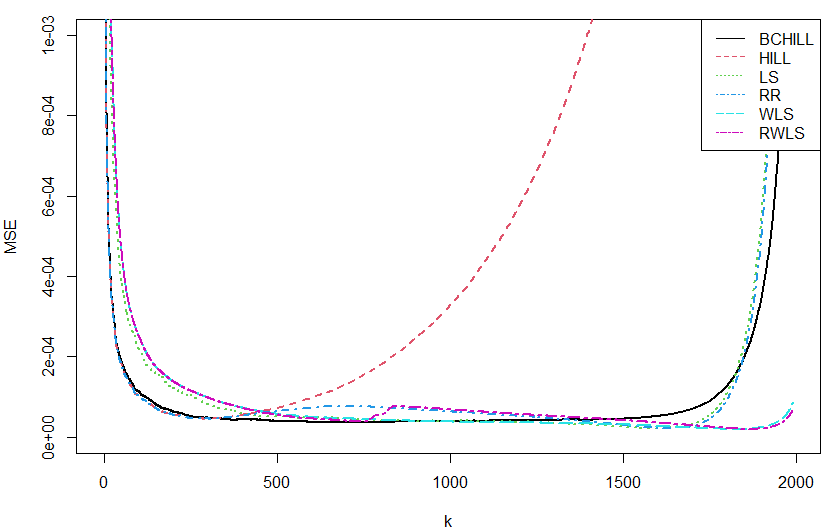

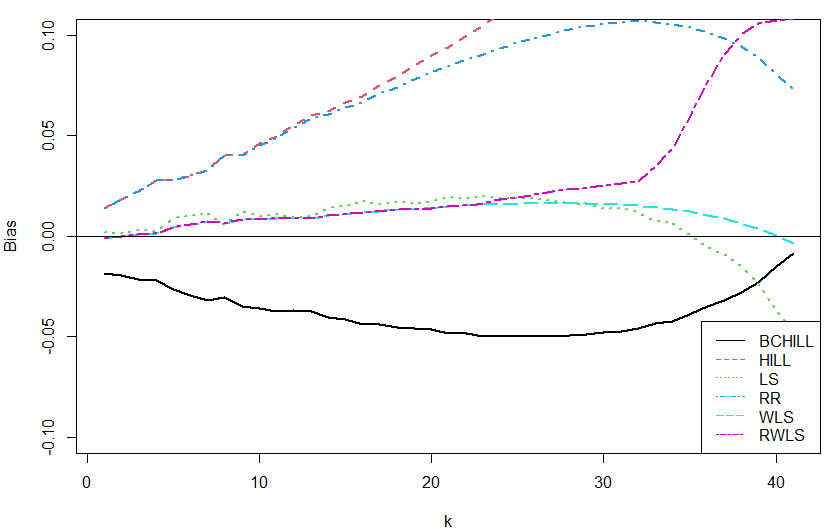

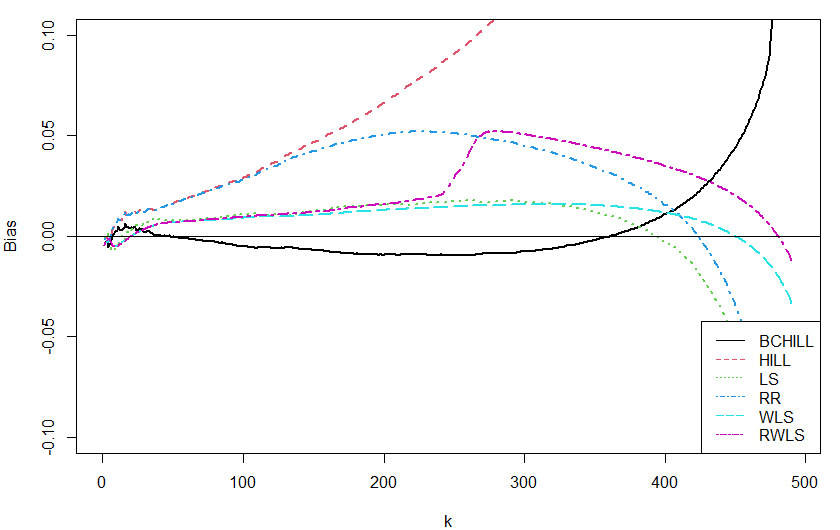

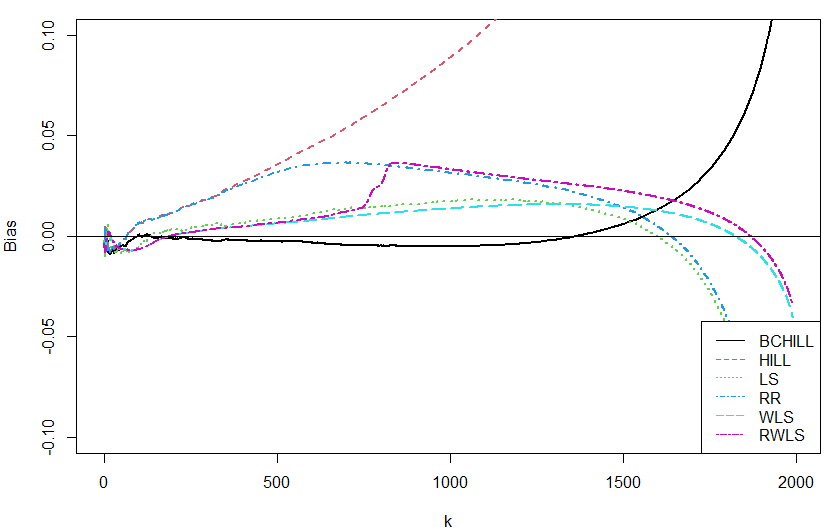

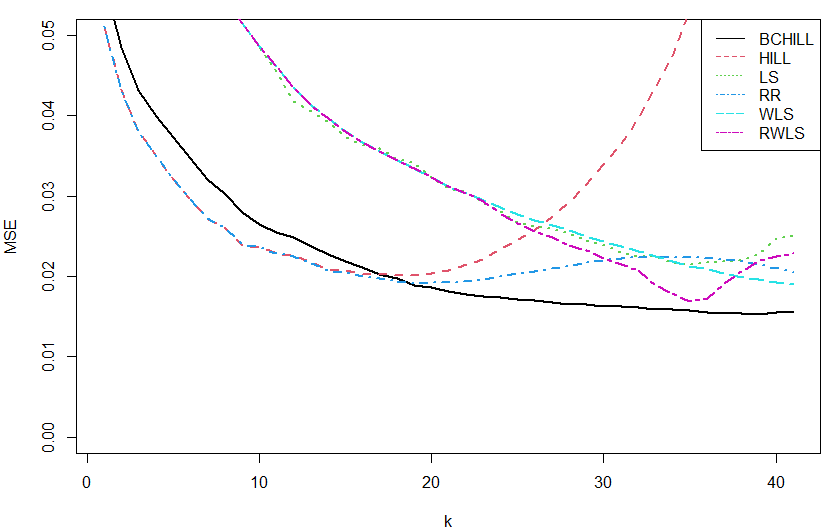

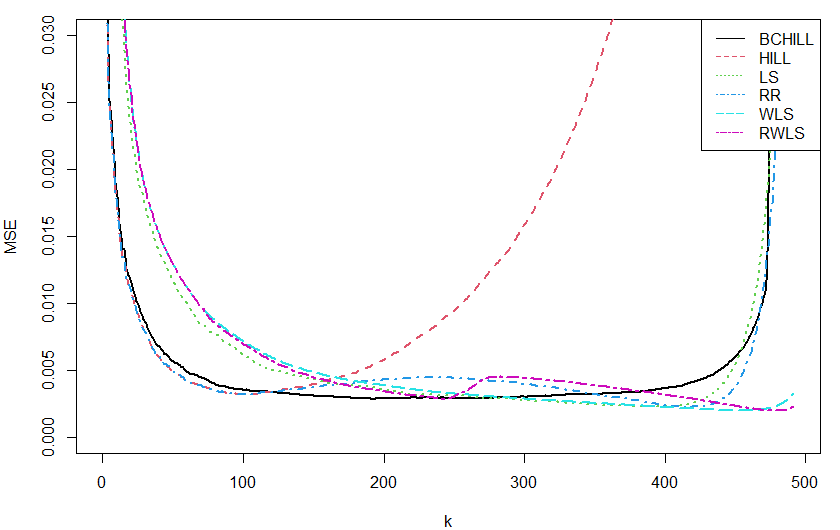

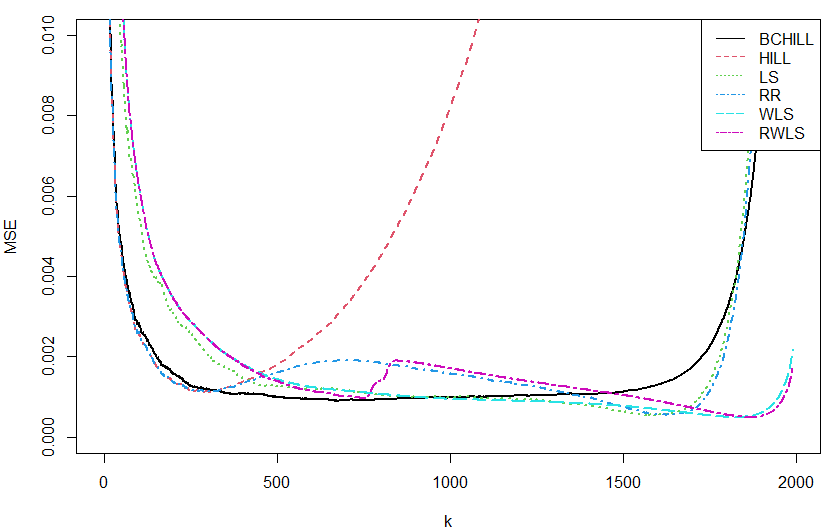

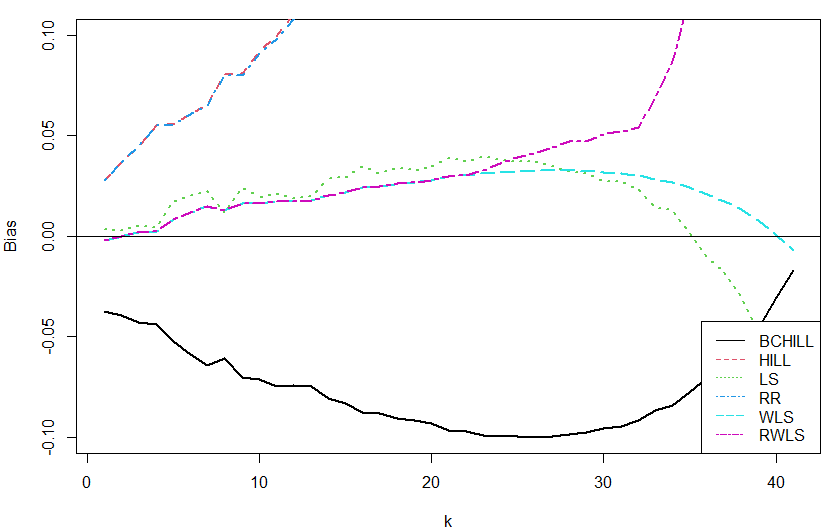

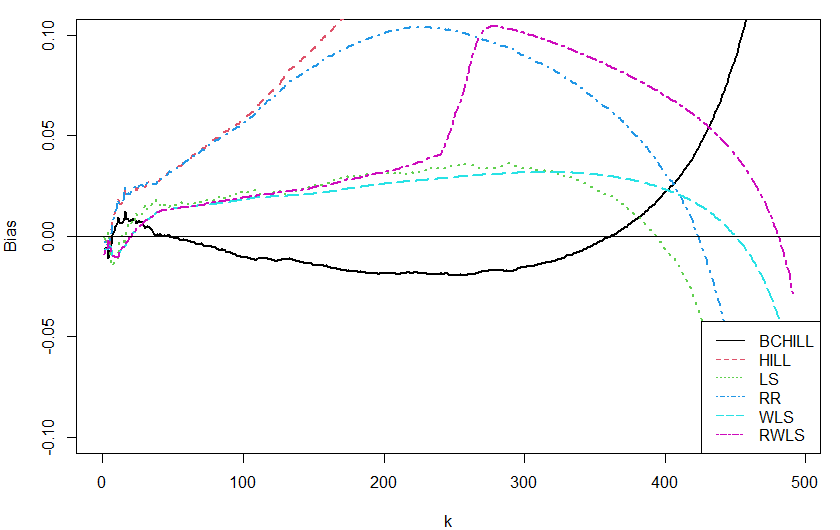

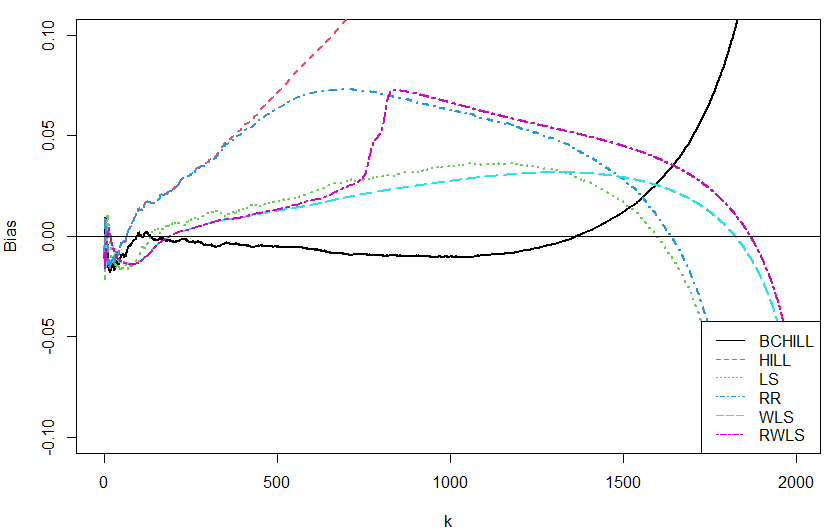

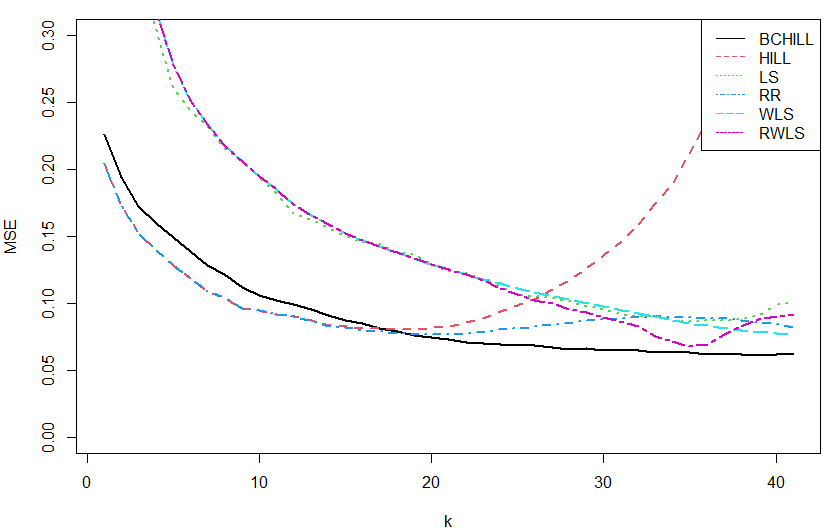

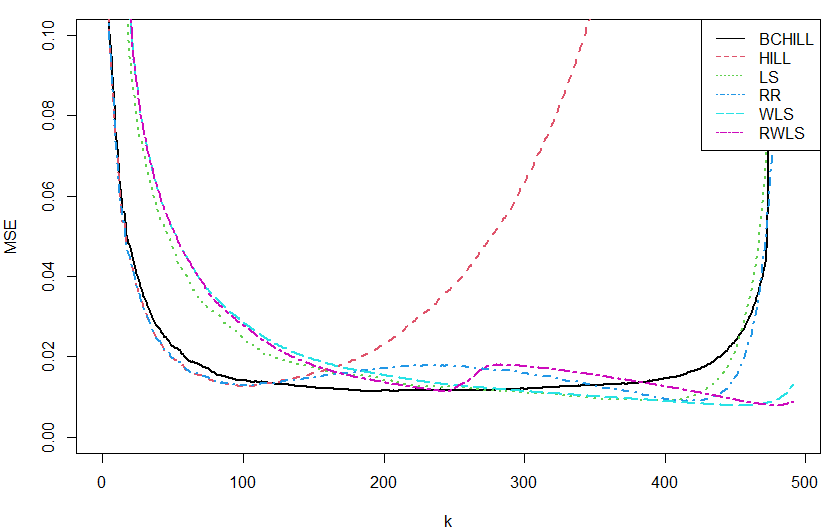

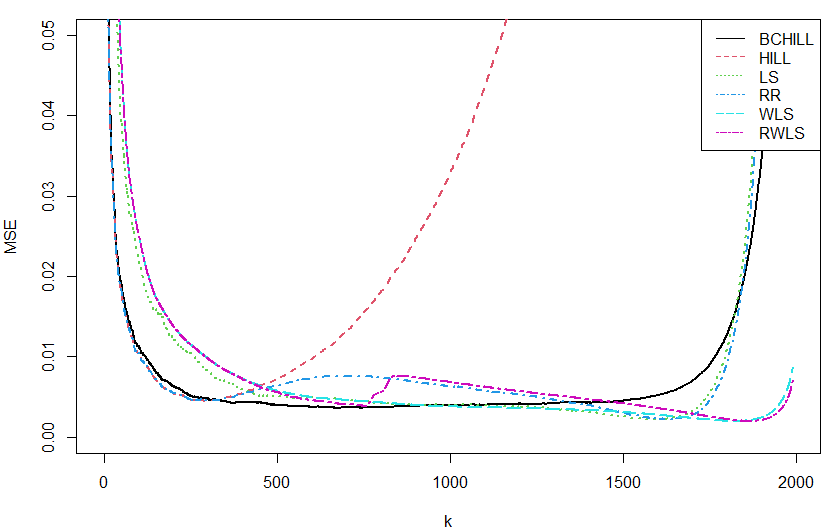

In this section, we discuss the behaviour of RWLS and WLS relative to RR, LS, HILL and BCHILL. The Mean Square Error (MSE) and bias are the performance measures in the simulation studies. The simulation results for the Burr distribution with different tail indexes are shown in Figures 1 - 3. Also, Figures 4 - 6 present the simulation results for the Fréchet distribution with varying tail indexes.

From these figures, the plots of WLS and RWLS follow the same sample path for , i.e., their performance are relatively the same on that interval. WLS and LS are very close to each other, though generally, WLS slightly outperforms LS in terms of MSE and bias. Thus, generally the WLS can be considered the most appropriate estimator of the tail index among the regression-based estimators (i.e., RR, LS, WLS and RWLS) since it mostly has smallest bias and MSE across all samples.

Additionally, the MSE plots of the proposed estimators are low and near constant over the central part of , except in the case of Burr XII with . With the exception of the HILL estimator (which globally has the highest MSE), the MSE curves of the estimators are mostly close to each other in the central region, especially in the case of the Fréchet distribution. This implies that the proposed estimators are competitive with the existing estimators. However, the proposed estimators, WLS and RWLS, generally attain the lowest bias for small samples, i.e., . Furthermore, for medium to large values of , the sample paths of RWLS in the MSE and bias plots are between HILL and RR. Even though the BCHILL estimator mostly has the smallest MSE and bias, the proposed estimators (RWLS and WLS) outperform it for large values of .

Hence, from the simulation results, WLS and RWLS are appropriate for the estimation of the tail index of the Pareto-type distributions in terms of MSE and bias.

4 Applications

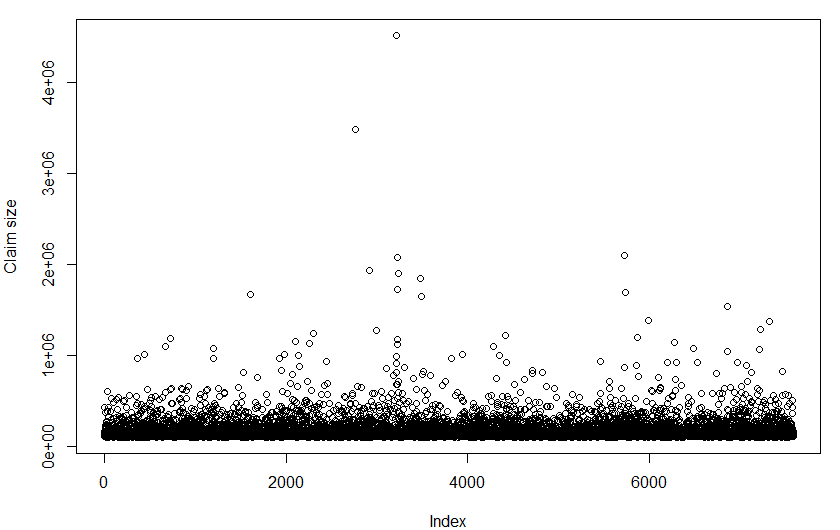

In this section, we consider the estimation of the tail index of the underlying distribution of two datasets from the insurance industry. First, the SOA Group Medical Insurance dataset consists of over 170,000 claims recorded from 1991 to 1992. In this study, we consider the 1991 dataset, which comprised 75,789 claims and have been studied widely in the extreme value context (see e.g [18],[4]). Considering the large size of this dataset, we focus on the extreme tail of the data and hence consider the top 10% data points, (i. e, ). The SOA dataset is available at https://lstat.kuleuven.be/Wiley/Data/soa.txt.

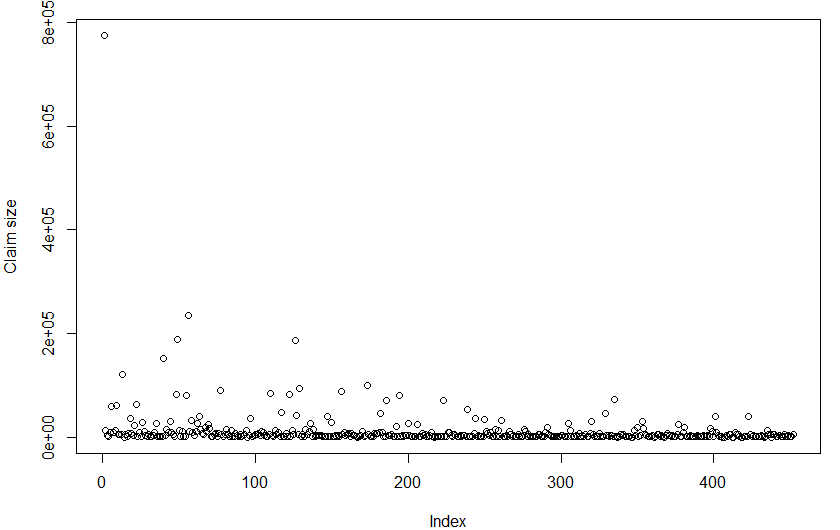

Second, the automobile insurance data from Ghana consists of 452 claims from July 7, 2020, to May 11, 2021 and can be found at https://github.com/kikiocran/TailEstimators We will refer to this dataset as the GH claims in this study. To the best of our knowledge this dataset has never been used in the extreme value theory literature.

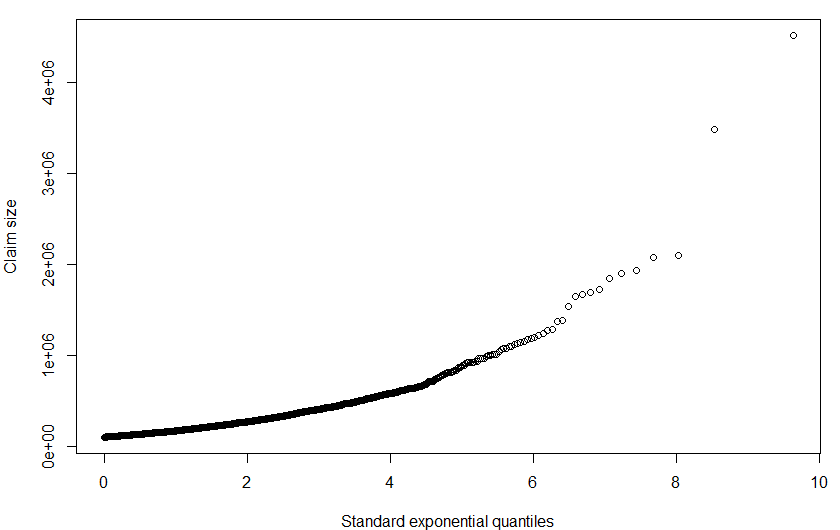

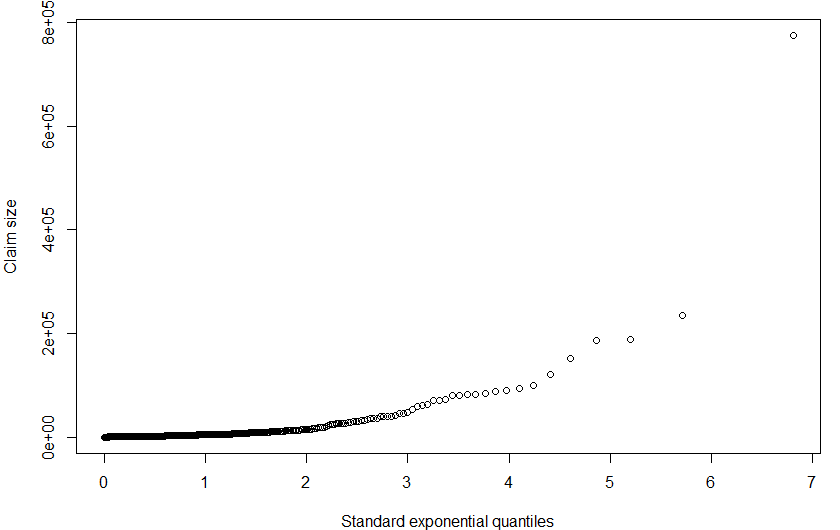

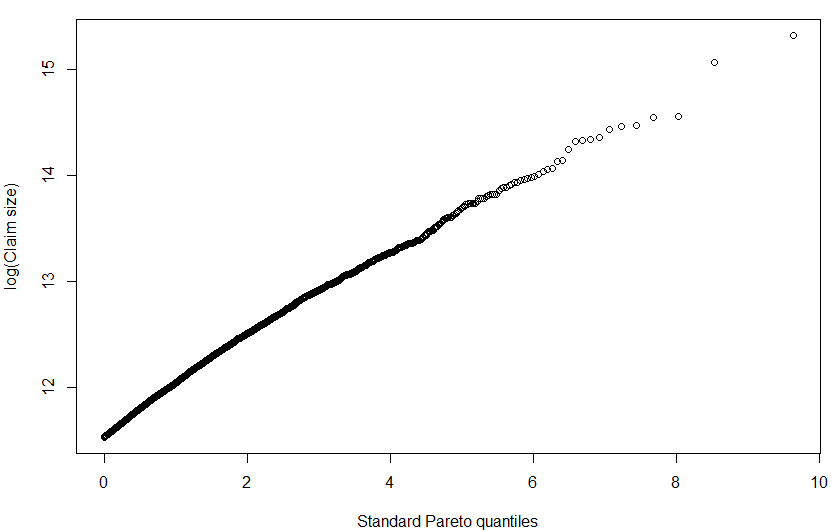

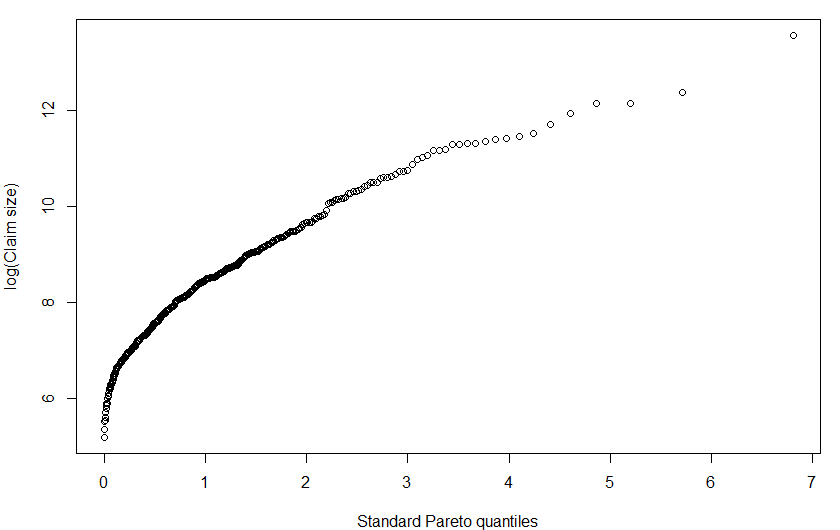

The scatter plots of the SOA, and the GH claims are shown in Figure 7. We observe that two claims and one claim in the SOA and GH claims, respectively, appear to be far detached from the bulk of the data. These observations can also be seen to deviate from linearity and far removed from the bulk of the points respectively in the Pareto and exponential Q-Q plots (Figure 8) of the two datasets. Such large observations are suspected outliers and may significantly influence the tail index estimates (see e.g [4]). The convex curvature of the exponential Q-Q plots and the near linearity of the Pareto Q-Q plots of the datasets indicate that the datasets suggest that they belong to the Pareto-type distributions.

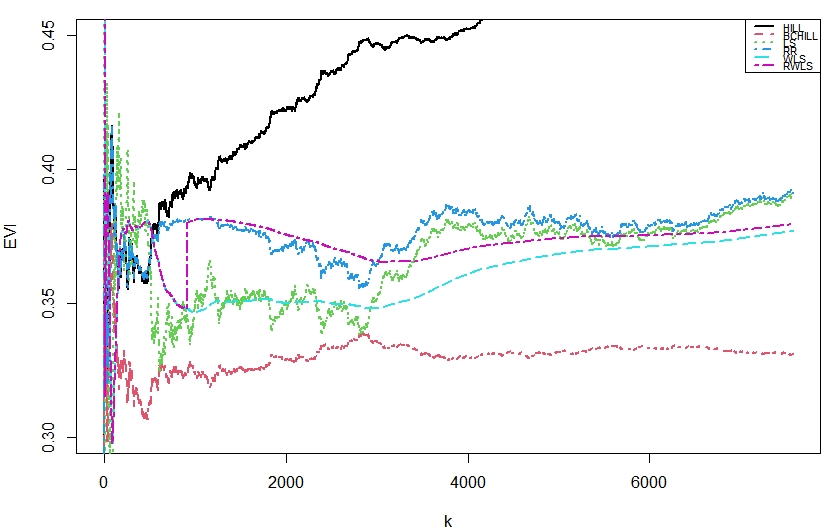

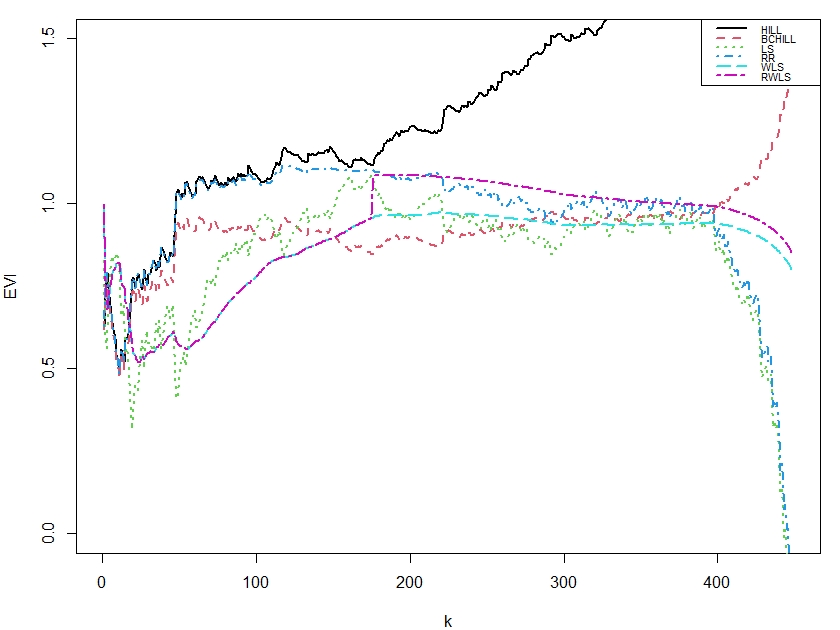

Figure 9 shows the sample paths of the tail index estimators for the underlying distributions of the two datasets. The plot of HILL diverges as increases, i.e., it is very sensitive to the changes in . Hence, it is not an appropriate estimator for estimating the tail index. The other estimators exhibit some form of stability, however, the sample paths of the proposed estimators (i.e., RWLS and WLS) are smooth, that is, these estimators are less sensitive to changes in . All the tail index estimators considered are very unstable for small values of due to the small number of exceedances. A specific tail index estimate can be obtained from the plots of WLS and RWLS for both datasets.

5 Conclusion

In this paper, we proposed tail index estimators for the Pareto-type of distributions using the regression model. In addition to the ordinary least squares and the ridge regression estimators, we proposed the regularised weighted least squares and the weighted least squares estimators as alternative reduced-bias estimators. The tail index estimates by the proposed estimators are generally stable and smooth across a broader path of . The characteristics of the proposed estimators are as follows;

-

they are asymptotically consistent, unbiased and normally distributed with mean and variance .

-

the MSE curves are low and flat over the central part of .

-

the plots of their tail index estimates are more stable, smooth and horizontal than the Hill, ordinary least squares and the bias-corrected Hill estimators.

In conclusion, comparatively, the proposed estimators are competitive to the existing estimators and can be considered as appropriate estimators of the tail index with MSE, bias and in real-life application.

6 Proofs

Proof of Lemma 1.

-

i.

It follows that,

where and hence, as , we have

-

ii.

It follows that,

where . Therefore,

as . That is, as .

-

iii.

The expression can also be written as

Therefore, as , .

-

iv.

can also be expressed as

It also follows that, as , .

∎

Proof of Lemma 6.

The proof requires the use of large deviation principles (LDP). From Eqn.(15) and Eqn.(32), Given , is exponentially distributed with mean

Therefore, we have

| (35) |

Using Lemma 6, Eqn.(35) and similar calculations as in [30], the moment generating function of given the law of is

It follows that

Now using the bound on , see Lemma 5 and the Squeeze Theorem, we obtain

Hence, by the Grtner Ellis Theorem, conditional on the statistics follows a Large Deviation Principle (LDP) with speed and a rate function defined as

where . This implies for every , we have

where . The atypical behaviour of the rate function is when , therefore

Thus, as and this ends the proof. ∎

Proof of Lemma 8.

We observe that are independent but not identical distributed random variables.

-

(i)

where and is the Hill estimator. Hence we have

-

(ii)

Let be the probability density function of given and observe that we

where for . Therefore we have that

Now define

and note that

Hence,

∎

Proof of Theorem 3.

Using Lemma 6 and Lemma 8, we can prove Theorem 3. It has been established in Lemma 6 that as . Lemma 8 also establishes that the Lyapunov’s condition holds for Central Limit Theorem; hence, by the Lyapunov’s Central Limit Theorem;

.

Therefore, all we need to complete the proof of Theorem 3, is to specify the parameters of the normal distribution.

Recall from (16) that

Also, from Lemma 6, asymptotically, the second term on the right hand side vanishes, so we would concentrate on the first term of the expression only.

Let

The expected value of is given as

Hence as . Recall that, , and by assumption and are independent, therefore, the variance of is given by

Using the assumption , as we have which completes the proof of Theorem 3. ∎

References

- [1] F. Longin, Extreme events in finance: A handbook of extreme value theory and its applications, John Wiley & Sons, 2016.

- [2] M. M. Kithinji, P. N. Mwita, A. O. Kube, Adjusted extreme conditional quantile autoregression with application to risk measurement, Journal of Probability and Statistics 2021 (2021).

- [3] K. Gkillas, P. Katsiampa, An application of extreme value theory to cryptocurrencies, Economics Letters 164 (2018) 109–111.

- [4] R. Minkah, T. de Wet, A. Ghosh, Robust estimation of pareto-type tail index through an exponential regression model, Communications in Statistics-Theory and Methods (2021) 1–19.

- [5] R. Minkah, Tail index estimation of the generalised pareto distribution using a pivot from a transformed pareto distribution, Science and Development Journal 4 (1) (2020) 1–19.

- [6] C. Rohrbeck, E. F. Eastoe, A. Frigessi, J. A. Tawn, Extreme value modelling of water-related insurance claims, The Annals of Applied Statistics 12 (1) (2018) 246–282.

- [7] A. J. McNeil, Estimating the tails of loss severity distributions using extreme value theory, ASTIN Bulletin: The Journal of the IAA 27 (1) (1997) 117–137.

- [8] G. Magnou, An application of extreme value theory for measuring financial risk in the uruguayan pension fund, Compendium: Cuadernos de Economía y Administración 4 (7) (2017) 1–19.

- [9] E. Afuecheta, C. Utazi, E. Ranganai, C. Nnanatu, An application of extreme value theory for measuring financial risk in brics economies, Annals of Data Science (2020) 1–40.

- [10] N. Mehrnia, S. Coleri, Wireless channel modeling based on extreme value theory for ultra-reliable communications, IEEE Transactions on Wireless Communications (2021).

- [11] B. Finkenstadt, H. Rootzén, Extreme values in finance, telecommunications, and the environment, CRC Press, 2003.

- [12] M. Ivette Gomes, L. De Haan, L. H. Rodrigues, Tail index estimation for heavy-tailed models: accommodation of bias in weighted log-excesses, Journal of the Royal Statistical Society: Series B (Statistical Methodology) 70 (1) (2008) 31–52.

- [13] S. Buitendag, J. Beirlant, T. de Wet, Ridge regression estimators for the extreme value index, Extremes 22 (2) (2018) 271–292. doi:10.1007/s10687-018-0338-4.

- [14] V. Brazauskas, R. Serfling, Robust and efficient estimation of the tail index of a single-parameter pareto distribution, North American Actuarial Journal 4 (4) (2000) 12–27.

- [15] C. Wang, G. Chen, A new hybrid estimation method for the generalized pareto distribution, Communications in Statistics-Theory and Methods 45 (14) (2016) 4285–4294.

- [16] Y. M. Tripathi, S. Kumar, C. Petropoulos, Improved estimators for parameters of a pareto distribution with a restricted scale, Statistical Methodology 18 (2014) 1–13.

- [17] M. B. Hill, A simple general approach to inference about the tail of a distribution, Annals of Statistics 3 (5) (1975) 1163 – 1174.

- [18] J. Beirlant, Y. Goegebeur, J. Teugels, J. Segers, Statistics of Extremes : Theory and Applications Statistics of Extremes, 2004.

- [19] S. Csorgo, P. Deheuvels, D. Mason, Kernel estimates of the tail index of a distribution, The Annals of Statistics (1985) 1050–1077.

- [20] J. Danielsson, D. W. Jansen, C. G. De vries, The method of moments ratio estimator for the tail shape parameter, Communications in Statistics-Theory and Methods 25 (4) (1996) 711–720.

- [21] J. Beirlant, P. Vynckier, J. L. Teugels, Excess functions and estimation of the extreme-value index, Bernoulli (1996) 293–318.

- [22] J. Beran, D. Schell, M. Stehlík, The harmonic moment tail index estimator: asymptotic distribution and robustness, Annals of the Institute of Statistical Mathematics 66 (1) (2014) 193–220.

- [23] M. F. Brilhante, M. I. Gomes, D. Pestana, A simple generalisation of the hill estimator, Computational Statistics & Data Analysis 57 (1) (2013) 518–535.

- [24] V. Paulauskas, M. Vaičiulis, A class of new tail index estimators, Annals of the Institute of Statistical Mathematics 69 (2) (2017) 461–487.

- [25] V. Paulauskas, M. Vaičiulis, On an improvement of hill and some other estimators, Lithuanian Mathematical Journal 53 (3) (2013) 336–355.

- [26] S. Resnick, C. Stărică, Smoothing the hill estimator, Advances in Applied Probability 29 (1) (1997) 271–293.

- [27] F. Caeiro, M. I. Gomes, D. Pestana, Direct Reduction of Bias of the Classical Hill Estimator, Statistical 3 (2) (2005) 113–136.

- [28] J. Beirlant, G. Dierckx, Y. Goegebeur, G. Matthys, Tail Index Estimation and an Exponential Regression Model, Extremes 2 (2) (1999) 177–200. doi:10.1023/A:1009975020370.

- [29] J. Beirlant, G. Dierckx, A. Guillou, C. Starica, On exponential representations of log-spacings of extreme order statistics, Extremes 5 (2002) 157–180.

- [30] E. Ocran, R. Minkah, K. Doku-Amponsah, A reduced-bias weighted least square estimation of the extreme value index, arXiv preprint arXiv:2110.08570 (2021).

- [31] M. I. Gomes, M. J. Martins, “asymptotically unbiased” estimators of the tail index based on external estimation of the second order parameter, Extremes 5 (1) (2002) 5–31.