2021

1]\orgdivDepartment of Mathematics and Statistics, \orgnameUniversity of Nevada, Reno, \orgaddress1664 \streetN. Virginia Street, \cityReno, \postcode89557, \stateNevada, \countryUSA

Withdrawal Success Estimation

Abstract

Given a geometric Lévy alpha-stable wealth process, a log-Lévy alpha-stable lower bound is constructed for the terminal wealth of a regular investing schedule. Using a transformation, the lower bound is applied to a schedule of withdrawals occurring after an initial investment. As a result, an upper bound is described on the probability to complete a given schedule of withdrawals. For withdrawals of a constant amount at equidistant times, necessary conditions are given on the initial investment and parameters of the wealth process such that withdrawals can be made with 95% confidence. When the initial investment is in the S&P Composite Index and , then the initial investment must be at least times the amount of each withdrawal.

keywords:

Dollar cost averaging, Terminal wealth, Standard and Poor, Lévy alpha-stable, Withdrawalspacs:

[pacs:

[JEL Classification]C22, E27, G11

MSC Classification]60E15, 60J70, 91B70

1 Introduction

A regular investing schedule involves predetermined investment amounts and times. In Brown (2021), a log-Normal lower bound is given for the returns of a regular investing schedule, provided the asset wealth process is a geometric Brownian motion. Here, the lower bound is generalized to geometric Lévy alpha-stable asset wealth processes. The main advantage of this generalization is that now, a lower bound can be produced when the asset wealth process has heavy tails and skewness. The generalized lower bound presented here has a log-Lévy alpha-stable distribution, and it is given as a lower bound for terminal wealth, instead of returns. Note that return indicates terminal wealth divided by the total invested.

An interesting application of the lower bound on terminal wealth addresses the probability to make a sequence of withdrawals. A transformation of the recursion indicating how much money is left after each withdrawal allows the withdrawals process to be considered in the framework of a regular investing schedule. Section 2.1 describes the transformation in detail. Since the transformed withdrawals process is a regular investing schedule, the lower bound on terminal wealth can be applied. As a result, it is possible to establish a relationship between given parameters and the probability to make a sequence of withdrawals.

The generalized lower bound is applied to dollar cost averaging (DCA). DCA is a particular regular investing schedule, where a constant amount is invested at equidistant time steps. When a constant amount is withdrawn at equidistant time steps, the transformed withdrawals process is DCA. Thus application of the generalized lower bound to DCA addresses withdrawals as well. Some applications use historic price data from the S&P Composite Index. Figure 1 illustrates a regular investing schedule vs a scedule of withdrawals.

1.1 Literature Review

Practical justification for using a geometric Lévy alpha-stable asset wealth process comes in several stages. First, values of the asset wealth process are collected at equidistant times. Then log-returns between successive values are computed. Last, log-returns are fit to a Lévy alpha-stable distribution and checked for independence. Note that independence of log-returns follows from the random walk hypothesis. For this reason, many of the works mentioned in the next paragraph do not address independence explicitly.

Lévy alpha-stable log-returns have been justified in several cases. To give an idea of what ranges of the shape parameter are practical, values of are also recorded. In Nolan (2003), the log difference of successive exchange rates is shown to fit a Lévy alpha-stable random variable. In particular, daily British Pound vs. German Mark exchange rates are fitted over 1980 to 1996, and monthly US Dollar vs Tanzanian Shilling exchange rates are fitted over 1975 to 1997. The former estimates , and the latter estimates . US stock log-returns are shown to follow a Lévy alpha-stable distribution in Fama (1965); Leitch and Paulson (1975). Chinese stock daily log-returns are shown to follow a Lévy alpha-stable distribution in Xu et al (2011). For US stocks, is generally estimated in the range 1.6 to 2. For Chinese stocks, is estimated around 1.4. In Cornew et al (1984), daily log-returns from commodity futures are well-fit to a Lévy alpha-stable distribution, and is typically estimated to be in the range 1.5 to 2. Overall, is practical.

Given a regular investing schedule and a random asset wealth process, terminal wealth is a sum of products of random variables. Since elements of the sum are dependent, the distribution of terminal wealth is complicated. As a result, it is desirable to find a bound on terminal wealth that has a simple distribution. Then it is possible to make interesting statements about terminal wealth using the simple distribution.

When the asset wealth process is a geometric Brownian motion, terminal wealth of a regular investing schedule is a sum of dependent log-Normal random variables. The sum can be estimated as a log-Normal random variable, as in Mehta et al (2007); Schwartz and Yeh (1982), but these estimates are not necessarily lower bounds. A lower bound for the sum is given in Dhaene et al (2002a, b), but it is a lower bound in the convex order sense. A lower bound in probability is given in Brown (2021), and that lower bound is generalized here to geometric Lévy alpha-stable wealth processes.

Terminal wealth of a continuous investment schedule has been considered Milevsky and Posner (2003). In particular, the investment schedule is the continuous version of DCA, and the asset wealth process is assumed to be a geometric Brownian motion w.r.t. time. As a result, the terminal wealth is integrated geometric Brownian motion.

Much of the recent research considering a schedule of withdrawals focuses on variable annuities. In a simple example of a variable annuity, an individual first pays a premium to an insurance company, and the insurance company invests the premium into a mutual fund. Then, the insurance company makes payouts to the individual at standard intervals (e.g. monthly, quarterly, semiannually or annually). The size of each payout depends on the options and benefits specific to the variable annuity contract. Furthermore, each set of options and benefits has associated fees and penalties written into the contract. One benefit that has recieved substantial attention is the guaranteed minimum withdrawal benefit, where an individual is guaranteed to at least withdraw the fee- and penatly-adjusted premium. Pricing of variable annuities with a guaranteed minimum withdrawal benefit has been addressed in several cases (e.g. Milevsky and Salisbury (2006); Dai et al (2008)). Here, results considering withdrawls use a single initial investment, or premium, and then a sequence of withdrawls.

Empirical research addresses the sustainability of a constant withdrawal amount at equidistant times, given the initial investment. In Cooley et al (1998), annual withdrawals are made from portfolios consisting of US stocks and bonds, using data from 1926 to 1995. The withdrawals are made over the periods 15, 20, 25 and 30 years. Portfolios having only stocks are better able to sustain higher withdrawal amounts, like 12% of the initial investment. Portfolios having 50% stocks and 50% bonds are better able to withstain withdrawal amounts that are 7% of the initial investment. In Cooley et al (2003), the effect of international diversification on sustainability of withrawals from a stock and bond portfolio is shown to be minor when the portfolio has at least 50% stocks; the time period considered is 1970 to 2001. Here, applications consider the probability to make a sequence of withdrawals, given an initial investment in just US stocks.

1.2 Main Results

Investment in exactly one asset is considered. All results require the assumption that the logarithm of the asset wealth process is a Lévy alpha-stable process.

For a regular investment schedule, a lower bound is given on the terminal wealth such that the logarithm of the lower bound has a Lévy alpha-stable distribution (see Theorems 1, 2 and 3). Theorem 1 provides recursive expression of the lower bound for the general investing schedule. Theorems 2 and 3 provide closed form expression of the lower bound for DCA and continuous DCA, respectively.

For a regular withdrawal schedule, an upper bound is given on the probability of being able to successfully execute all planned withdrawals. For the general case, where withdrawal amounts and times are unconstrained, the upper bound is a result of Theorems 4 and 6. For the case where withdrawal amounts and time intervals are equal, the upper bound is a result of Theorems 5 and 6. Remark 6 describes the upper bound for the case when withdrawals are continuous.

1.3 Applications

Applications are split into general applications and applications with data. General applications consider a range of parameters for the Lévy alpha-stable asset wealth process. Applications with data focus only on parameters that provide a good fit to the data. Data is from the S&P Composite Index, specifically the annual data from 1871 to 2020, including reinvested dividends and adjustment for inflation. This S&P index tracks the weighted average of stock prices for the largest US companies, where each company’s weight is equal to its market capitalization. Funds tracking this index, like the S&P 500, are very popular among investors. Data is taken from Robert Shiller’s online data library, and further details on this data can be found in Section 4.1.

General applications address the lump sum discount, discrete withdrawals and continuous withdrawals. The lump sum discount was introduced in Brown (2021). It indicates a lump sum investment that has a terminal wealth distribution that is no better than a given regular investing schedule. Note that a lump sum investment is a single investment at time 0. Here, the lump sum discount is described for continuous DCA using Theorem 3. The lump sum discount is invariant to the skewness and scale parameters of the asset wealth process, so it is illustrated for various location and shape parameters. In general, investing a similar amount in lump sum for less than half the time is no better than using continuous DCA.

The application addressing discrete withdrawals considers equal withdrawals at equidistant times. Suppose an investor wishes to make withdrawals with a given level of confidence, shape parameter and skewness parameter. Using Theorems 5 and 6, a procedure is outlined to give conditions on the location and scale parameters that force the initial investment to be at least the total intended to be withdrawn. The procedure is demonstrated for 95% confidence and particular shape and skewness parameters.

The application addressing continuous withdrawals suppose an investor wishes to continuously withdraw a specified amount, at a constant rate, with a given level of confidence. For 95% confidence with various shape, skewness and location parameters, conditions are given on the scale parameter that force the initial investment to be at least the total intended to be withdrawn.

Applications with S&P data first address the fit of log-returns to a Lévy alpha-stable process. In Brown (2021), log-returns are fit to a Brownian motion, which is a particular Lévy alpha-stable process. Main results allow log-returns to be fit to Lévy alpha-stable processes that are not Brownian motions. Consequently, a Lévy alpha-stable process is found that fits log-returns better than the Brownian motion of Brown (2021). The lower bound on returns from Theorem 2 is compared using the new Lévy alpha-stable process fit vs the Brownian motion fit. Quantiles are practically identical, except the quantiles less than .05. The quantiles under .05 are less with the Lévy alpha-stable process, implying there is additional downside risk that the Brownian motion fit misses. However, if a decision is made based on quantiles no less than .05, then the decision will likely be invariant to the Lévy alpha-stable process fit vs the Brownian motion fit.

Next, applications with S&P data consider discrete withdrawals. In order to make equal, annual withdrawals from the S&P Composite Index, with 95% confidence, it is necessary for the initial investment to be at least times the amount of each withdrawal.

Last, continuous withdrawals are considered. Given various levels of confidence, necessary initial investments are given to continuously withdraw a particular amount from the S&P Composite Index over years. To continuously withdraw with a high level of confidence, like 99%, the initial investment needs to be at least , when continuous withdrawals are made over years. For lower confidence, like 60%, the initial investment needs to be at least .

1.4 Organization

Section 2 provides the problem setup and main results. Main results are split into section 2.2 for regular investment and section 2.3 for withdrawals. Sections 3 and 4 provide application of the main results given in section 2. Applications are split into section 3 for general applications and section 4 for applications using data. Section 5 provides closing remarks, including a discussion of related future research ideas. Appendix A provides proofs of the theorems stated in Section 2.

2 Definitions & Main Results

2.1 Notation

Let be a Lévy alpha-stable process defined on the probability space . When using as a function of only, write in place of . For each , the characteristic function of , , is given by

where , , and .

For arbitrary , use to indicate that is a Lévy alpha-stable random variable with shape , skewness , scale and location . Moreover, has characteristic function

Say that is the Sharpe ratio of .

Let be a sequence in with . Suppose that is invested at each time step . Let for . The returns at time step are given by for , where the are computed recursively via

| (1) |

Note that is the terminal wealth at time .

Next consider the analogue to (1), but for withdrawals. In particular, suppose is invested at time , and is withdrawn at each time step , where . Then the amount remaining at time after withdrawal is computed recursively via

| (2) |

Note that can be withdrawn at times if and only if . Observe that

| (3) |

The following abbreviations will be used to shorten descriptions: dollar cost averaging (DCA), lump sum (LS), upper bound (UB) and lower bound (LB). In all expressions, indicates the natural logarithm. When convenient, expressions like w.p.1 will be abbreviated with . Equality in distribution will be denoted with .

2.2 Main Results for Regular Investment

Definition 1 recursively constructs the lower bound of terminal wealth. Theorem 1 describes the lower bound of terminal wealth recursively. Under the conditions and for , Theorem 2 describes the lower bound of DCA terminal wealth in closed form. Theorem 3 provides an upper bound on the cumulative distribution function of terminal wealth when and for , and the limit is taken as . This is the continuous version of DCA.

Note that a lower bound given for terminal wealth is easily transformed into a lower bound for returns. In particular, if w.p.1 and , then w.p.1 and

Definition 1.

Set and

where and .

Remark 1.

and are invariant to a rescaling of the investment amounts. In particular, if the substitution is made for each , then and do not change.

Theorem 1.

For every , w.p.1 and , where parameters are given recursively via

Remark 2.

In general can be any positive real number. A good choice for that leads to nice simplification is . Then the term in Theorem 1 disappears. Moreover, maximizes over .

Theorem 2.

Let and . Suppose , and for . Then for every , w.p.1 and , where

Remark 3.

In the construction of Theorem 2, . Furthermore, is increasing with . If , then is increasing with . If , then is decreasing with .

Theorem 3.

Let and . Let denote the returns at given , and for . Then for all , where and

Remark 4.

In the construction of Theorem 3, is the terminal wealth and return at time 1, since the total invested is 1. Furthermore, the integral needed to compute can be bounded, and it is well-approximated when is close to 0. Observe that for ,

| (4) |

Proof of the upper bound in (4) is given in Appendix A. It follows that

where if and otherwise.

2.3 Main Results for Withdrawls

For the remainder of this subsection, fix . In (3), is deterministic and is random. Alternatively, consider the recursion

| (5) |

where is random. Then for each , . Note that the if and only if holds because is a strictly increasing function of . Theorem 4 provides a lower bound for , where parameters are given recursively. Theorem 5 provides a lower bound for when every withdrawal is the same amount, and withdrawals are made at equidistant times. Furthermore, Theorem 5 expresses parameters of the lower bound in closed form. Theorem 6 uses the lower bound of to construct an upper bound for . Recall that if and only if withdrawals can be made. Remark 6 discusses continuous withdrawals.

Definition 2.

Set and

where and .

Theorem 4.

w.p.1 and , where parameters are given recursively via

Remark 5.

Like in Section 2.2, can be any positive real number, and a good choice for is .

Theorem 5.

Let and . Suppose for , and , for . Then w.p.1 and , where

Theorem 6.

The probability of being able to make withdrawals is no greater than the probability that , i.e. .

Remark 6.

Let and . Suppose one wishes to make continuous withdrawals at a constant rate from time 0 to time 1, such that a total of exactly 1 unit has been withdrawn by time 1. Given the initial investment of at time 0, the probability of success is no greater than , where and are computed as in Theorem 3, except with the substitution . This result is just a combination of Theorems 3 and 6, using (5).

3 General Applications

3.1 Lump sum discount

The lump sum discount, introduced in Brown (2021), can be evaluated using Theorems 1, 2 or 3. Here, it is evaluated for Theorem 3. The idea behind the lump sum discount is to identify a lump sum investment having a terminal wealth that is no better (in distribution) than the terminal wealth of continuous DCA.

The goal is to find a lump sum investment that, after time units, matches the terminal wealth distribution of the lower bound for continuous DCA. In particular, require

where and are as in Theorem 3. It follows that

| (6) |

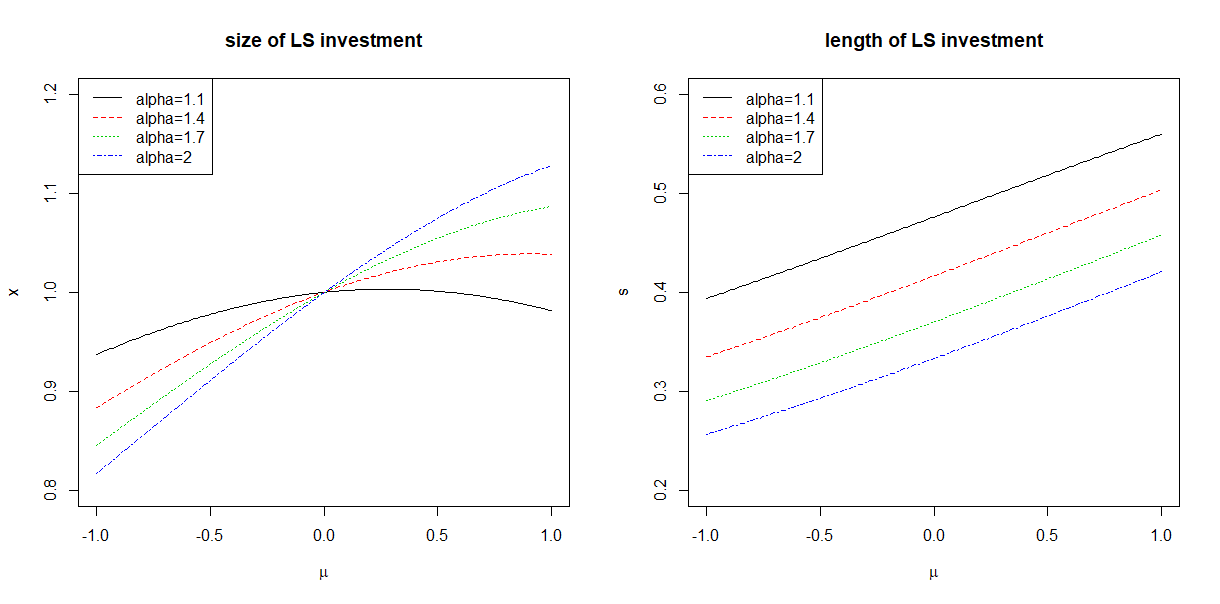

Since the continuous DCA of Theorem 3 invests a total of 1 currency unit over 1 unit of time, the lump sum discount is , indicating a lump sum investment of currency units for time units has no better terminal wealth than the continuous DCA. The result is also scalable, meaning if is invested over time units using continuous DCA, then a lump sum investment of for time units has a terminal wealth that is no better than the continuous DCA. Figure 2 shows and for various and . In general, investing a similar amount in lump sum for less than half the time is no better than using continuous DCA.

3.2 Discrete Withdrawls

Suppose an investor wishes to make equal withdrawals at equidistant time steps, with a given level of confidence. Theorems 5 and 6 make it possible to specify a necessary initial investment , meaning the investor must invest at least at time 0 in order to achieve the given level of confidence. For the remainder of this subsection, use to denote that necessary initial investment.

The procedure is as follows. Let denote the given level of confidence. Set , and solve for , where is as in Theorem 5. By Theorem 6, the probability of being able to make the withdrawals is no greater than . If an initial investment is made instead of , and , then . It follows from Theorem 6 that the probability of being able to make the withdrawals is less than . Therefore, is not a sufficient initial investment.

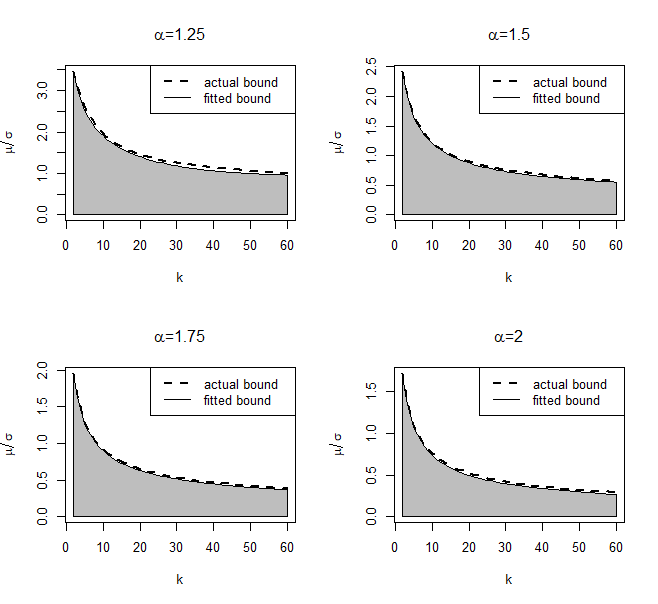

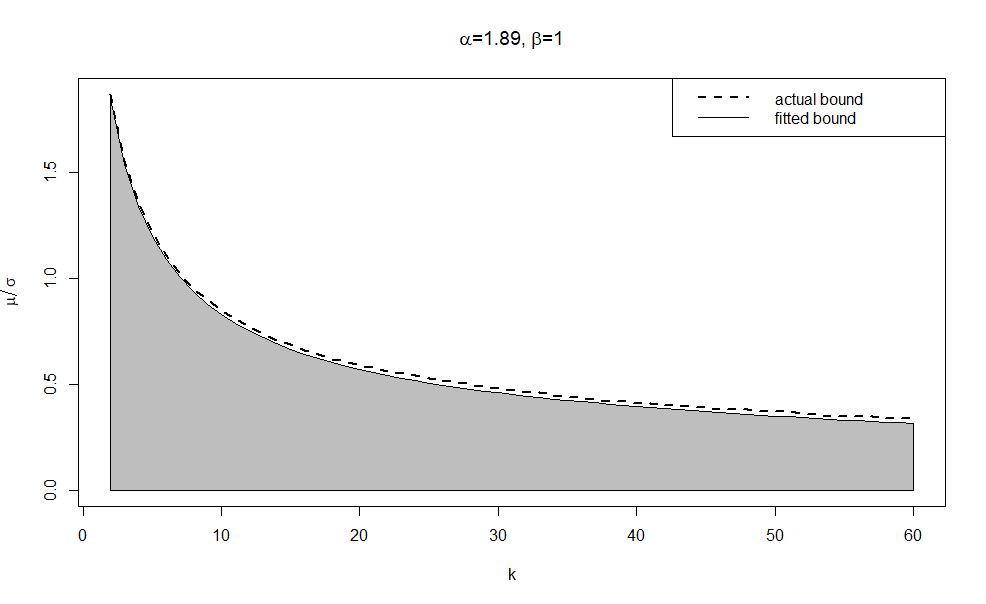

Without loss of generality, suppose the investor makes withdrawals as in Theorem 5. Then 1 unit is withdrawn at each time . An interesting result to pursue is: Given , , and , provide sufficient and such that , meaning the initial investment must be at least the total amount intended to be withdrawn. This result is achieved for , , and . Since and are fixed, sufficient ratios are given as a function of and in (7). Note that is required for the result to hold. The are provided in (8), where the matrix stores in its th row and th column. The interpretation of the result is as follows: If , , , and (7) holds, then in order to make equal withdrawals at each time , with 95% confidence, it is necessary for the initial investment to be at least times the amount of each withdrawal.

| (7) |

| (8) |

The bound (7) was constructed via computer using Algorithm 1. First, and were fixed at and . Then, for each , the returned were fit to the polynomial

Last, each was fit to the polynomial

so that (7) implies . Figure 3 illustrates the upper bound (7) for different . This procedure can also be executed for different and .

3.3 Continuous Withdrawls

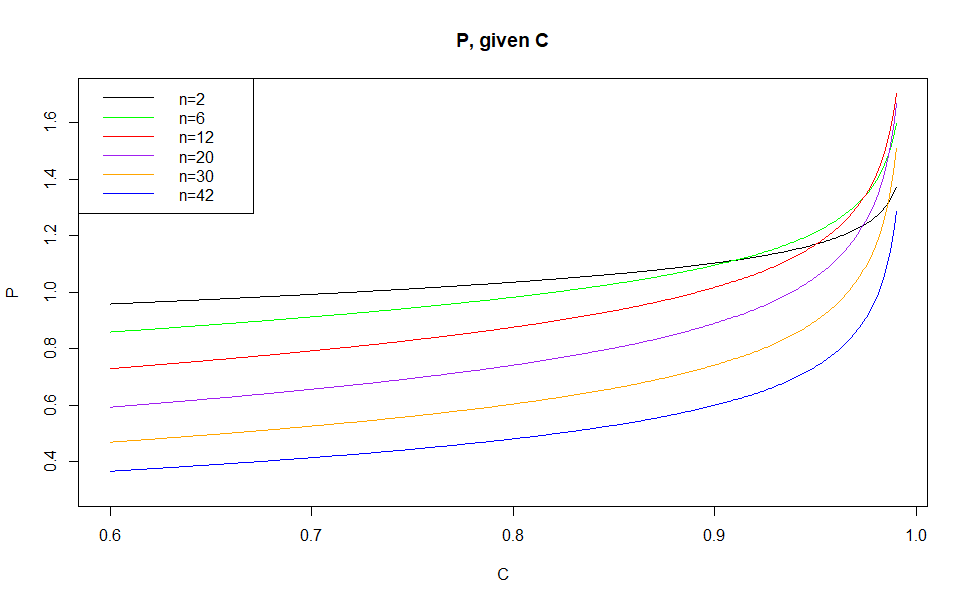

Suppose an investor wishes to continuously withdraw a total of 1 currency unit from time 0 to time 1, at a constant rate, with a given level of confidence. Remark 6 makes it possible to specify a necessary initial investment , meaning the investor must invest at least to achieve the given level of confidence. For the remainder of this subsection, use to denote that necessary initial investment.

The procedure is as follows. Let denote the given level of confidence. Set , and solve for , where is as in Remark 6. The probability of being able to withdraw the 1 unit is no greater than . Any initial investment less than results in a confidence level less than .

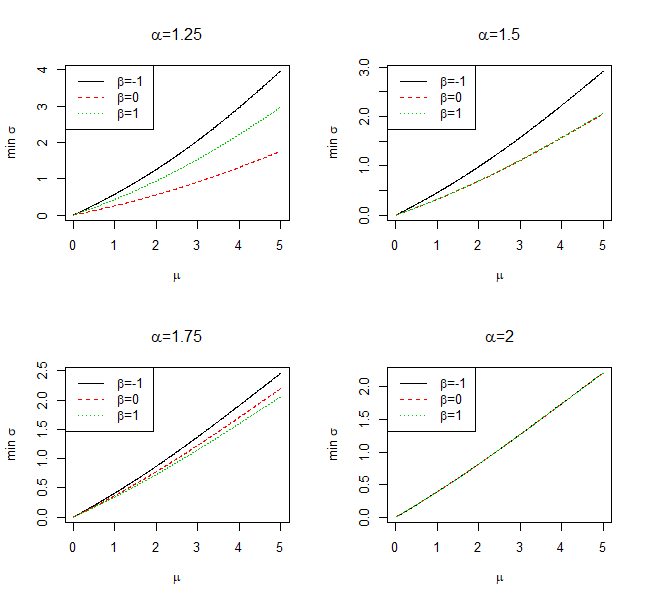

An interesting result to pursue is: Given , , and , provide sufficient such that , meaning the initial investment must be at least the total amount intended to be withdrawn. Algorithm 2 computes for each , which is an upper bound on . It follows that is a lower bound on . Figure 4 illustrates the lower bound on for and various and .

4 Applications with Data

4.1 Data

As in Brown (2021), main results are applied to annual data from the S&P Composite Index from 1871 to 2020. The index consists of large US companies, and each company’s weight is proportional to its market capitalization. The data was taken from http://www.econ.yale.edu/~shiller/data.htm and is collected for easy access at https://github.com/HaydenBrown/Investing.

The number of companies in the US stock market has increased significantly from 1871 to 2020. In order to account for this increase, the data is split into three indexes, each covering a different time interval. The indexes are Cowles and Associates from 1871 to 1926, Standard & Poor 90 from 1926 to 1957 and Standard & Poor 500 from 1957 to 2020. Cowles and Associates index is a backward extension of the S&P 90. The S&P 90 consists of 90 companies, and the S&P 500 consists of 500 companies.

| Notation | Description |

|---|---|

| I | average monthly close of the S&P composite index |

| D | dividend per share of the S&P composite index |

| C | January consumer price index |

As in Brown (2021), the data is transformed so that annual returns incorporate dividends and are adjusted for inflation. In particular, returns are computed using the consumer price index, the S&P Composite Index price and the S&P Composite Index dividend. Use the subscript to denote the th year of , and from Table 1. The return for year is computed as .

4.2 Set-up

In order to apply main results, the assumption that S&P annual log-returns arise from a Lévy alpha-stable process needs to be justified. This is done in two parts: first by establishing independence of annual log-returns, and second by establishing that annual log-returns follow a Lévy alpha-stable distribution.

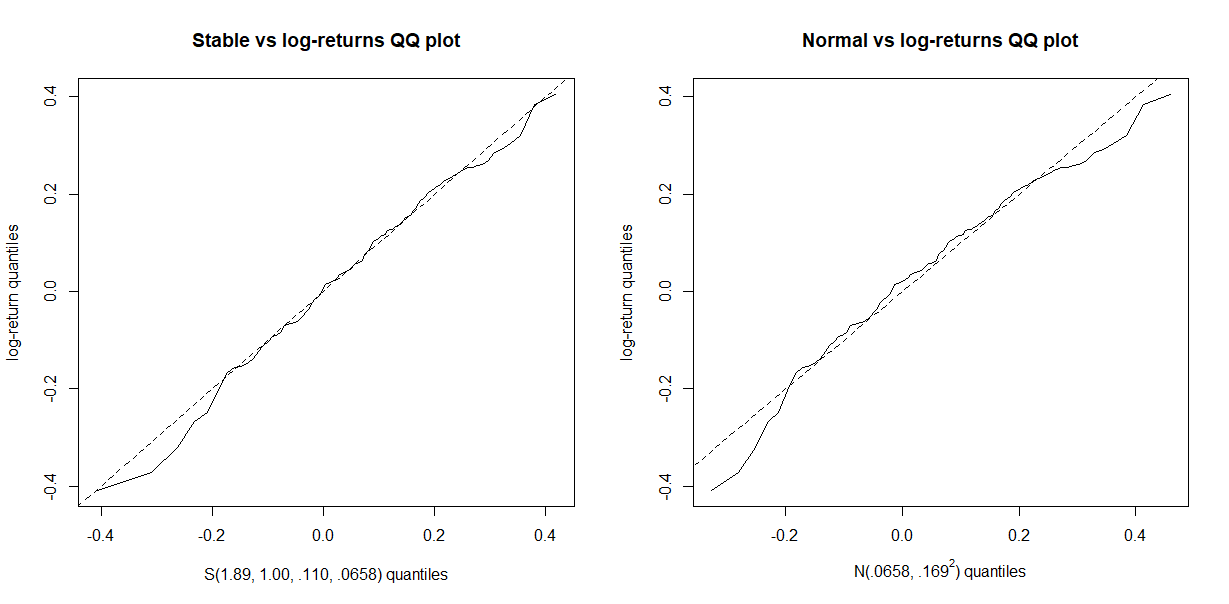

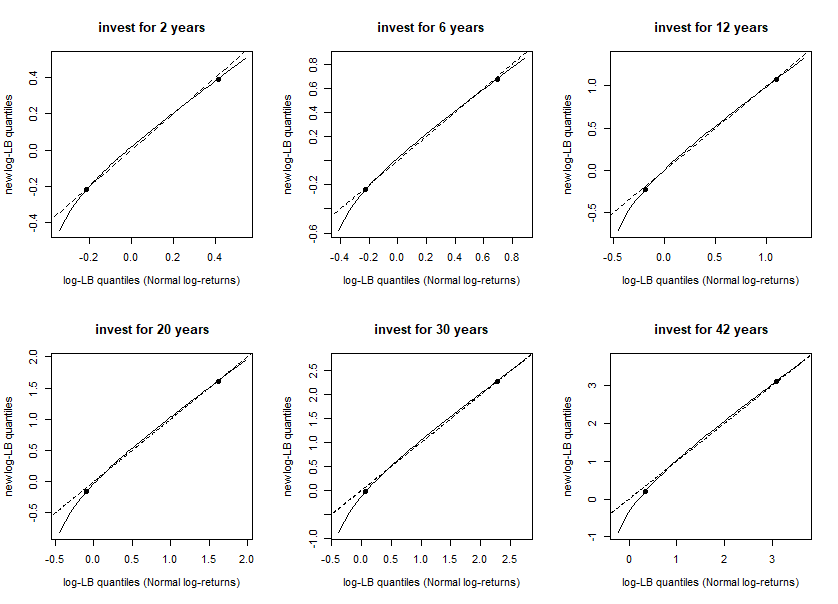

Independence of S&P annual returns is established in Brown (2021). The Lévy alpha-stable distribution of log-returns is established by visual inspection of quantile-quantile plots. Parameters are estimated using the iterative Koutrouvelis regression method with initial estimate Koutrouvelis (1980, 1981). The resulting estimate for parameters is . Figure 5 shows the quantiles of the estimated distribution vs the empirical quantiles of the log-returns. For comparison, Figure 5 also shows the quantiles of the Normal distribution with mean and standard deviation (used in Brown (2021)) vs the empirical quantiles of the log-returns.

The distribution offers a tighter quantile fit compared to the Normal distribution considered in Brown (2021). Note that the unit on the time domain is years, and applications using S&P log-returns use only annual investment and withdrawals (i.e. for ).

4.3 DCA quantiles

In Brown (2021), provided the best fit for annual log-returns. Section 2.2 generalizes the results of Brown (2021), allowing . In section 4.2, is given as a better fit for log-returns compared to . The goal here is to compare the lower bound of Theorem 2 when log-returns follow versus . Figure 6 shows the quantiles of the log lower bound when log-returns follow versus .

In Figure 6, observe that quantiles are nearly identical except the quantiles under .05. When log-returns follow , the quantiles under .05 are less than when log-returns follow . Thus, taking into account the skewness and wider shape () of log-returns leads to more significant downside risk compared to Normal log-returns. However, if a decision is based on quantiles .05 or greater, then the decision will likely be invariant to the choice of whether log-returns follow versus .

4.4 Discrete Withdrawls

Algorithm 1 is executed for , and . If , and (9) holds, then in order to make equal withdrawals at each time , with 95% confidence, it is necessary for the initial investment to be at least times the amount of each withdrawal.

| (9) |

Figure 9 shows that the bound (9) is very close to the returned by Algorithm 1. It has been verified that satisfies (9) for . Thus, in order to make equal, annual withdrawals from the S&P Composite Index, with 95% confidence, it is necessary for the initial investment to be at least times the amount of each withdrawal.

4.5 Continuous Withdrawls

This application is similar to what was done in section 3.3. Suppose an investor wishes to continuously withdraw a total of 1 currency unit from the S&P Composite Index over years, at a constant rate, with a given level of confidence. The same general procedure outlined in section 3.3 is used here. Let denote the given level of confidence. Set , and solve for , where is as in Remark 6. Any initial investment less than results in a confidence level less than . Set , , and . The goal here is to compute the necessary initial investment for . Algorithm 3 describes the procedure, and Figure 8 illustrates as a function of , for various . To continuously withdraw with a high level of confidence, like 99%, the initial investment needs to be at least , when continuous withdraws are made over years. For lower confidence, like 60%, the initial investment needs to be at least .

5 Conclusions & Further Research

As in Brown (2021), expected error between the lower bound of terminal wealth and the actual terminal wealth can be computed, but only in the case . When , the mean of a Lévy alpha-stable random variable is undefined, causing the expected error to be undefined. An upper bound for the log-error between the lower bound of terminal wealth and the actual terminal wealth is also presented in Brown (2021). However, the Lévy alpha-stable random variable has undefined 2nd or higher moments for . Consequently, the upper bound for log-error is less meaningful when because higher moments cannot be used to tighten the upper bound.

The lower bound for terminal wealth of a regular investment schedule has interesting application for withdrawals, since a schedule of withdrawals can be transformed into a regular investment schedule. The result is an upper bound on the probability to complete a given schedule of withdrawals. Analogously, an upper bound for terminal wealth of a regular investment schedule would produce a lower bound on the probability to complete a given schedule of withdrawals. With a lower bound on the probability to complete a given schedule of withdrawals, it would be possible to specify a sufficient initial investment to complete a given schedule of withdrawals with a particular level of confidence.

Appendix A Proofs

Lemma 1.

For all ,

Moreover, there is equality at .

Proof: See the Appendix of Brown (2021).

Lemma 2.

Let , and for . In addition, let and be independent. Then

and

Proof: The results are taken from Nolan (2020).

Theorem 1

Proof: The result is established via induction. By Definition 1 . Since , it follows from Lemma 2 that

Theorem 2

Proof: By Theorem 1, the result holds when and are as in Theorem 1. It remains to be verified is that the expressions of and given in Theorems 1 and 2 are equal. This is clearly the case for . Suppose the expressions of and given in Theorems 1 and 2 are equal for all where . Then by Theorem 1 and the induction assumption,

Using Theorem 1, the recursion with implies that , where

Observe that for all ,

It follows that

Thus, for all ,

| (13) |

Theorem 3

Proof: By Theorem 2, for each , there exists such that w.p.1 and , using the substitutions and to evaluate and . To be more clear, the mean and scale parameters are

It follows that for each and .

Note that is the integral of a geometric Lévy alpha-stable process w.r.t. time (see Milevsky and Posner (2003) for the derivation using and ), so exists. Existence of the limit follows because sample paths of a geometric Lévy alpha-stable process are càdlàg, which implies each sample path is integrable. Thus, converges pointwise on . Since each is -measurable, it follows from closure under pointwise limits that is -measurable.

By Lévy’s convergence theorem, existence of will follow if the characteristic functions of converge. Thus, it suffices to show that and converge.

Proof of the upper bound in (4)

Let and . Recall that . The goal is to show on . The result clearly holds for , so require . Observe that is differentiable on , where

| (14) |

From (14), it follows that iff , where . Set . Observe that and is continuous and strictly convex on . Thus, either on , on , or there exists such that on and on . Accounting for the fact that , all three cases imply that the global minimum of occurs at or . Last, observe that at and .

Theorems 4, 5 and 6

References

- \bibcommenthead

- Brown (2021) Brown H (2021) Dollar cost averaging returns estimation. arXiv preprint arXiv:211209807

- Cooley et al (1998) Cooley PL, Hubbard CM, Walz DT (1998) Retirement savings: Choosing a withdrawal rate that is sustainable. AAII Journal 20(2):16–21

- Cooley et al (2003) Cooley PL, Hubbard CM, Walz DT (2003) Does international diversification increase the sustainable withdrawal rates from retirement portfolios? JOURNAL OF FINANCIAL PLANNING-DENVER- 16(1):74–81

- Cornew et al (1984) Cornew RW, Town DE, Crowson LD (1984) Stable distributions, futures prices, and the measurement of trading performance. The Journal of Futures Markets (pre-1986) 4(4):531

- Dai et al (2008) Dai M, Kuen Kwok Y, Zong J (2008) Guaranteed minimum withdrawal benefit in variable annuities. Mathematical Finance: An International Journal of Mathematics, Statistics and Financial Economics 18(4):595–611

- Dhaene et al (2002a) Dhaene J, Denuit M, Goovaerts MJ, et al (2002a) The concept of comonotonicity in actuarial science and finance: applications. Insurance: Mathematics and Economics 31(2):133–161

- Dhaene et al (2002b) Dhaene J, Denuit M, Goovaerts MJ, et al (2002b) The concept of comonotonicity in actuarial science and finance: theory. Insurance: Mathematics and Economics 31(1):3–33

- Fama (1965) Fama EF (1965) The behavior of stock-market prices. The journal of Business 38(1):34–105

- Koutrouvelis (1980) Koutrouvelis IA (1980) Regression-type estimation of the parameters of stable laws. Journal of the American statistical association 75(372):918–928

- Koutrouvelis (1981) Koutrouvelis IA (1981) An iterative procedure for the estimation of the parameters of stable laws: An iterative procedure for the estimation. Communications in Statistics-Simulation and Computation 10(1):17–28

- Leitch and Paulson (1975) Leitch RA, Paulson AS (1975) Estimation of stable law parameters: stock price behavior application. Journal of the American Statistical Association 70(351a):690–697

- Mehta et al (2007) Mehta NB, Wu J, Molisch AF, et al (2007) Approximating a sum of random variables with a lognormal. IEEE Transactions on Wireless Communications 6(7):2690–2699

- Milevsky and Posner (2003) Milevsky MA, Posner SE (2003) A continuous-time reexamination of dollar-cost averaging. International Journal of Theoretical and Applied Finance 6(02):173–194

- Milevsky and Salisbury (2006) Milevsky MA, Salisbury TS (2006) Financial valuation of guaranteed minimum withdrawal benefits. Insurance: Mathematics and Economics 38(1):21–38

- Nolan (2003) Nolan JP (2003) Modeling financial data with stable distributions. In: Handbook of heavy tailed distributions in finance. Elsevier, p 105–130

- Nolan (2020) Nolan JP (2020) Univariate stable distributions. Springer

- Schwartz and Yeh (1982) Schwartz SC, Yeh YS (1982) On the distribution function and moments of power sums with log-normal components. Bell System Technical Journal 61(7):1441–1462

- Xu et al (2011) Xu W, Wu C, Dong Y, et al (2011) Modeling chinese stock returns with stable distribution. Mathematical and computer modelling 54(1-2):610–617