22email: ykcheng@amss.ac.cn 33institutetext: Department of Computer Science, Shanghai Jiao Tong Univerisity, Shanghai, China

33email: rowdark@sjtu.edu.cn 44institutetext: Washington University in St. Louis, St. Louis, MO, the U.S.

44email: l.rong@wustl.edu

ABSNFT: Securitization and Repurchase Scheme for Non-Fungible Tokens Based on Game Theoretical Analysis

Abstract

The Non-Fungible Token (NFT) is viewed as one of the important applications of blockchain technology. Currently NFT has a large market scale and multiple practical standards, however several limitations of the existing mechanism in NFT markets still exist. This work proposes a novel securitization and repurchase scheme for NFT to overcome these limitations. We first provide an Asset-Backed Securities (ABS) solution to settle the limitations of non-fungibility of NFT. Our securitization design aims to enhance the liquidity of NFTs and enable Oracles and Automatic Market Makers (AMMs) for NFTs. Then we propose a novel repurchase protocol for a participant owing a portion of NFT to repurchase other shares to obtain the complete ownership. As the participants may strategically bid during the acquisition process, we formulate the repurchase process as a Stackelberg game to explore the equilibrium prices. We also provide solutions to handle difficulties at market such as budget constraints and lazy bidders.

Keywords:

Non-Fungible Token Asset-Backed Securities Blockchain Stackelberg Game1 Introduction

Ever since the birth of the first piece of Non-Fungible Token (NFT) [10] [22], the world has witnessed an extraordinarily fast growth of its popularity. NFT markets, especially Opensea111Opensea Platform. https://opensea.io/, have prospered with glamorous statistics of a total of over 80 million pieces of NFTs on the platform and a total transaction volume of over 10 billion US dollars.222Data source from Opensea https://opensea.io/about

NFT is a type of cryptocurrency that each token is non-fungible. The first standard of NFT, ERC-721 [9], gives support to a type of tokens that each has a unique identifier. The feature of uniqueness makes NFTs usually be tied to specific assets, such as digital artwork and electronic pets. Some researches also explore the application of NFT in patent, copyright and physical assets [5] [19].

The technology of NFT has also advanced rapidly. Besides ERC-721, ERC-1155 [8] is also a popular standard of NFT. ERC-1155 is a flexible standard that supports multiple series of tokens, each series is a type of NFT or Fungible Token (FT). NFT protocols are usually derived by smart contracts in a permissionless blockchain, but there are now some NFT designs for permissioned blockchains [11].

Although NFT has a large market scale and multiple practical standards, there still exist several limitations in NFT market, one of which is the poor liquidity.

The issue of liquidity is crucial in both De-fi and traditional finance. Usually, if assets have higher liquidity, they would have higher trading volume, and further have higher prices [2]. Particularly, in blockchain, the liquidity of Fungible Tokens, such as wBTC and ETH, has been enhanced by Oracles [16] and Automated Market Makers (AMMs) [3] like Uniswap and Sushiswap. However, the non-fungibility property of NFT leads to poor liquidity. For this reason, the existing NFT marketplace usually uses the English Auction or Dutch Auction to trade NFTs [13].

-

•

Firstly, Non-Fungibility means indivisible.

As the NFT series with the highest market value, CryptoPunks has an average trading price of 189 Eth33390-day average before November 22, 2021. Data source from https://opensea.io/activity/cryptopunks, which is worth more than 790, 000 U.S. dollars444The price of Eth here refers to the data on November 22, 2021. https://etherscan.io/chart/etherprice. If bitcoins are expensive, we can trade 0.01 bitcoins, but we can’t trade 0.01 CryptoPunks. As a result, the liquidity of CryptoPunks is significantly lower than other NFT series. Therefore, the liquidity for NFTs with high values is limited.

-

•

Secondly, shared ownership is not allowed because of Non-Fungibility. Therefore, it’s difficult to reduce risk and enhance the liquidity of NFTs through portfolios. What’s more, Some NFT assets such as patents need financial support to foster the process of development. They would require a means to attract finance. The above two limitations also exist in traditional settings.

- •

1.1 Main Contributions

We present ABSNFT, a securitization and repurchase scheme for NFT, which overcomes the above-mentioned limitations from the following three aspects.

-

•

Firstly, we propose an Asset-Backed Securities (ABS) [4] solution to settle the limitations of non-fungibility of NFT. We design a smart contract including three parts: NFT Securitization Process, NFT Repurchase Process, and NFT Restruction Process. In our smart contract, a complete NFT can be securitized into fungible securities, and fungible securities can be reconstructed into a complete NFT.

The securitization process manages to resolve the majority of issues the current NFT application is confronted with: the securities of NFT have lower values compared to the complete one before securitization, which increases market liquidity; securities could act as fungible tokens that can be applied in Oracles and AMMs; the investment risk is being reduced dramatically; financing is possible since securities can belong to different owners.

-

•

Secondly, we design a novel repurchase process based on Stackelberg game [20], which provides a mechanism to repurchase NFT securities at a fair price. The NFT Repurchase Process can be triggered by the participant who owns more than half of the securities of the NFT. We analyze the Stackelberg Equilibrium (SE) in three different settings and get good theoretical results.

-

•

Thirdly, we propose solutions to the budget constraints and lazy bidders, which make good use of the decentralization of blockchain. We propose a protocol that allows participants to accept financial support in the repurchase game to reduce the influence of budget constraints. We also propose two solutions for players that might not bid in the game, which prevent the game process from being blocked and protect the utility of lazy bidders.

1.2 Related Works

In financial research, there are two well-studied repurchase scenarios, repurchase agreement and stock repurchase.

Repurchase agreement is a short-term transaction between two parties in which one party borrows cash from the other by pledging a financial security as collateral [1]. The former party is called the security issuer, and the latter party is called the investors. To avoid the failure of liquidation, the security issuer needs to mortgage assets or credit. An instance of such work from the Federal Reserve Bank of New York Quarterly Review introduces and analyzes a repurchase agreement for federal funds [15]. The Quarterly Review describes the repurchase agreement as “involving little risk”, as either parties’ interests are been safeguarded.

Studies of repurchase agreement cannot be directly applied to our topic. The key point is that the problem we are studying is not to mortgage NFTs to obtain cash flow, but to securitize NFTs to overcome the restrictions of non-fungibility. What’s more, the repurchase prices are usually derived from the market model. But the NFT market is not as mature as the financial market, which makes it hard to calculate a fair price through the market model.

Stock repurchase refers to the behavior that listed companies repurchase stocks from the stockholders at a certain price [7]. Usually, stock repurchase is adopted to release positive signals to the stock market and doesn’t aim to repurchase all stocks. However, NFTs usually need to be complete without securities in cross-chain scenarios.

Oxygen [17] is a decentralized platform that supports repurchase agreement based on digital assets. In Oxygen, users can borrow cash flow or assets with good liquidity by pledging assets with poor liquidity. The repurchase prices and the evaluations of assets are provided by a decentralized exchange, Serum [18]. However, such pricing method is dangerous because decentralized exchanges are very vulnerable to attacks like flash loans [21].

ABSNFT is distinguished among all these works because it adapts well to the particularities of NFT market and blockchain.

-

•

First, the securities in ABSNFT represent property rights rather than creditor’s rights. Investors do not need to worry that the cash flow or the mortgaged assets of the securities issuer may not cover the liquidation, which may be risky in a repurchase agreement. What’s more, any investor can trigger a repurchase process as long as he owns more than half of the shares.

-

•

Second, the repurchase process of ABSNFT doesn’t depend on market models or exchanges. The repurchase price is decided by the bids given by participants, and every participant won’t get negative utility if he bids truthfully.

-

•

Third, ABSNFT has well utilized the benefits of blockchain technology. The tradings of securities are driven by the smart contract. The operations of ABSNFT don’t rely on centralized third-party and are available for participants.

The rest of the paper is arranged as follows. Section 2 introduces the NFT securitization process. In Section 3 and Section 4, we study the two-player repurchase game in a single round and the repeated setting. In Section 5, we analyze the repurchase game with multiple leaders and one follower. In section 6, we discuss the solution to the issues with budget constraints and lazy bidders in the blockchain setting. In the last section, we give a summary of ABSNFT and propose some future works.

2 NFT Securitization and Repurchase Scheme

In this section, we would like to introduce the general framework of the smart contract, denoted by , which includes the securitization process, the trading process, repurchase process and restruction process for a given NFT.

=

2.1 Basic Setting of NFT Smart Contract

There are two kinds of NFTs discussed in this paper.

-

•

Complete NFT. Complete NFTs are conventional non-fungible tokens, which appear in blockchain systems as a whole. Each complete NFT has a unique token ID. We use to denote one complete NFT with token ID of .

-

•

Securitized NFT. Securitized NFTs are the of complete NFTs. A complete NFT may be securitized into an amount of securitized units. All units of securitized NFTs from a complete NFT have the same ID, associated with the ID of . Thus we denote the securitized NFT by . In our smart contract, all securitized NFTs can be freely traded.

In our setting, all complete NFTs and securitized NFTs belong to one smart contract, denoted by . Although the securitized NFTs are similar to the fungible tokens in ERC-1155 standard [8], our smart contract is actually quite different from ERC-1155 standard. That is because all securitized NFTs in , associated to one complete NFT, have the same ID, while different NFTs and different fungible tokens generally have different token IDs in ERC-1155 standard. Therefore, our is based on ERC-721 standard [9], and the complete NFTs are just the NFTs defined in ERC-721. Table 1 lists all functions in .

| Function Name | Function Utility |

|---|---|

| Return the address of the owner of . | |

| Transfer the ownership of from address to address . Only the owner of has the right to trigger this function. | |

| Return the total amount of in contract . | |

| Return the amount of owned by address . | |

| addr1,addr2 | Transfer the ownership of unit of from address to address . |

| Freeze , and then transfer units of to address . Only the owner of can trigger this function. | |

| Burn all , unfreeze , and then transfer the ownership of to address . Only the one who owns all amounts of can trigger this function. | |

| Start the repurchase process of . Only the one who owns more than half amounts of can trigger this function. |

The task of smart contract includes securitizing complete NFTs, trading the securitized NFTs among participants, and restructing complete NFT after repurchasing all securitized NFTs with the same ID. Bescause the transactions of securitized NFTs are similar to those of fungible tokens, we omit the trading process here and introduce NFT securitization process, NFT repurchse process and NFT restruction process in the subsequent three subsections respectively.

2.2 NFT Securitization Process

This subsection focuses on the issue of Asset-Backed Securities for Complete NFTs. We propose Algorithm 1 to demonstrate the NFT securitization process. To be specific, once is triggered by the owner of , the units of securitized NFTs are generated and transferred to address in Line 2-4; then the ownership of would be transferred to a fixed address in Line 5.

It is worth to note that if has not been triggered, securitized NFTs can be freely traded in blockchain system.

2.3 NFT Repurchase Process

After the securitization process, a complete NFT is securitized into units of . Suppose that there are participants, , each owning units of . Thus . If there is one participant, denoted by , owing more than half of (i.e. ), then he can trigger the repurchase process by trading with each , . Majority is a natural requirement for a participant to trigger a repurchase mechanism, and thus our repurchase mechanism sets the threshold as . In addition, if the trigger condition is satisfied (i.e., someone holds more than half of shares), then there must be exactly one participant who can trigger the repurchase mechanism. This makes our mechanism easy to implement. Our mechanism also works well if the threshold is larger than .

Let be ’s value estimate for one unit of and be the bid provided by , , in a deal. Specially, our smart contract requires each value and bid to discretize our analysis. We assume that the estimation of is private information of , not known to others. The main reason is that most of NFT objects, such as digital art pieces, would be appreciated differently in different eyes.

Participants may have different opinions about a same NFT, which makes each of them has a private value . Without loss of generality, we assume that ’s private value on the complete NFT is .

Mechanism 1

(Repurchase Mechanism) Suppose participant owes more than half of and triggers the repurchase mechanism. For the repurchase between and , ,

-

•

if , then successfully repurchases units of from at the unit price of ;

-

•

if , then fails to repurchase, and then he shall sell units of to . The unit price that pays is , and obtains a discounted revenue for each unit of .

Mechanism 1 requires that the repurchase process only happens between and , . If , then successfully repurchases units of from , and the utilities of and are

| (1) |

If , then fails to repurchase from , and the utilities of and are

| (2) |

All participants must propose their bids rationally under Mechanism 1. If the bid is too low, would face the risk of repurchase failure. Thus, the securities of would be purchased by other participants at a low price, and ’s utility may be negative. Similarly, if bid of , , is too high, would purchase securities with an extra high price and get negative utility. However, if a participant bids truthfully, he always obtains non-negative utility.

During the repurchase process, the key issue for each participant is how to bid , , based on its own value estimation. To solve this issue, we would model the repurchase process as a stackelberg game to explore the equilibrium pricing solution in the following Section 3 to 5.

2.4 NFT Restruction Process

Once one participant successfully repurchases all securitized NFTs, he has the right to trigger , shown in Algorithm 2, to burn these securitized NFTs in Line 3 to 4 and unfreeze , such that the ownership of would be transferred from address to this participant’s address in Line 5.

After NFT restruction, all are burnt, and is unfrozen. The owner of has the right to securitize it or trade it as a whole.

3 Two-Player Repurchase Stackelberg Game

This section discusses the repurchase process for a two-player scenario. To be specific, in the two-player scenario, when a player owns more than half of , denoted by , he will trigger the repurchase process with another player . To explore the optimal bidding strategy for both players, we model the repurchase process as a two-stage Stackelberg game, in which acts as the leader to set its bid in Stage I, and , as the follower, decides its bid in Stage II. Recall that all bids and all values are in .

-

(1)

’s bidding strategy in Stage II: Given the bid of , set by in Stage I, decides its bid to maximize its utility, which is given as:

(3) -

(2)

’s bidding strategy in Stage I: Once obtain the optimal bid of in Stage II, which is dependent on , goes to compute the optimal bid by maximizing his utility function , where

(4)

3.1 Analysis under Complete Information

(1) Best response of in Stage II. Given the bid provided by , in Stage II, shall determine the best response to maximize his utility.

Lemma 1

In the two-stage Stackelberg game for repurchase process, if the bid is given in Stage I, the best response of in Stage II is

| (5) |

Proof

According to (3), is monotonically increasing when and monotonically decreasing when . So . In addition, when , we have

It implies that the best response of is if . When , we have

So under the situation of , the best response of is . ∎

(2) The optimal strategy of in Stage I. The leader would like to optimize his bidding strategy to maximize his utility shown in (4).

Lemma 2

In the two-stage Stackelberg game for repurchase process, the optimal bidding strategy for the leader is

| (6) |

Proof

Based on Lemma 1, we have

Thus is monotonically increasing when and monotonically decreasing when , indicating the optimal bidding strategy . In addition, for the case of , if , then by Lemma 1 and On the other hand, if , then by Lemma 1 and Therefore, , showing the optimal bidding strategy of is when . Similarly, for the case of , we can conclude that . This lemma holds. ∎

Theorem 3.1

When , there is exactly one Stackelberg equilibrium where . And when , there is exactly one Stackelberg equilibrium where .

Furthermore, the following theorem demonstrates the relation between Stackelberg equilibrium and Nash equilibrium.

Theorem 3.2

Each Stackelberg equilibrium in Theorem 3.1 is also a Nash equilibrium.

The proof of Theorem 3.2 is provided in Appendix A.

3.2 Analysis of Bayesian Stackelberg Equilibrium

In the previous subsection, the Stackelberg equilibrium is deduced based on the complete information about the value estimate and . However, the value estimates may be private in practice, which motivates us to study the Bayesian Stackelberg game with incomplete information. In this proposed game, although the value estimate is not known to others, except for itself , , the probability distribution of each is public to all. Here we use to denote the random variable of value estimate. Based on the assumption that all are integers, we continue to assume that each ’s value estimate has finite integer states, denoted by , and its discrete probability distribution is , , and , .

(1) Best response of in Stage II. Because is deterministic to , and is given by in Stage I, Lemma 1 still holds, so

(2) Optimal bidding strategy of in Stage I. By Lemma 1, we have

Based on the probability distribution of , the expected utility of is:

| (7) |

To be specific, if , then , and obtains his maximal expected utility at . If , then , and obtains his maximal expected utility at . If there exists an index , such that , , then

Therefore, can obtain his maximal expected utility at , when . Otherwise, ’s maximal expected utility is achieved at . Hence, the optimal bid .

Theorem 3.3

There is a Stackelberg equilibrium in the Bayesian Stackelberg game.

-

(1)

If , then and is a Stackelberg equilibrium.

-

(2)

If , then and is a Stackelberg equilibrium.

4 Repeated Two-Player Stackelberg Game

This section would extend the study of the one-round Stackelberg game in the previous section to the repeated Stackelberg game. Before our discussion, we construct the basic model of a repeated two-player Stackelberg game by introducing the necessary notations.

Definition 1

Repeated two-player Stackelberg repurchase game is given by a tuple , where:

-

•

is the set of two participants. The role of being a leader or a follower may change in the whole repeated process.

-

•

is the total amount of . W.l.o.g., we assume that is odd, such that one of must have more than half of .

-

•

is the set of participants’ value estimates. Let be an integer.

-

•

is the set of sequential states. , in which are integers, , and because is odd. represents the terminal state, where . If the sequential states are infinity, then . Let us denote .

-

•

is the set of sequential leaders, where is the leader in the -th round. To be specific, , if ; otherwise, . It shows the participant who triggers the repurchase process in each round should be the follower.

-

•

is the set of sequential prices bidded by , .

-

•

is the utility function of player in a single round. The detailed expressions of will be proposed later.

In practice, , , may not be common information. However, we can extract them from the historical interaction data of the repeated game by online learning [23] or reinforcement learning [14] methods. Therefore, we mainly discuss the case with complete information in this section.

Repeated Stackelberg Game Procedure Repeated game consists of several rounds, and each round contains two stages. In the -th round,

-

•

In Stage I, the leader provides a bid .

-

•

In Stage II, the follower provides a bid .

-

•

If , successfully purchased units of from at the unit price of .

-

•

If , purchases units of from at the unit price of . And only obtains a discounted revenue .

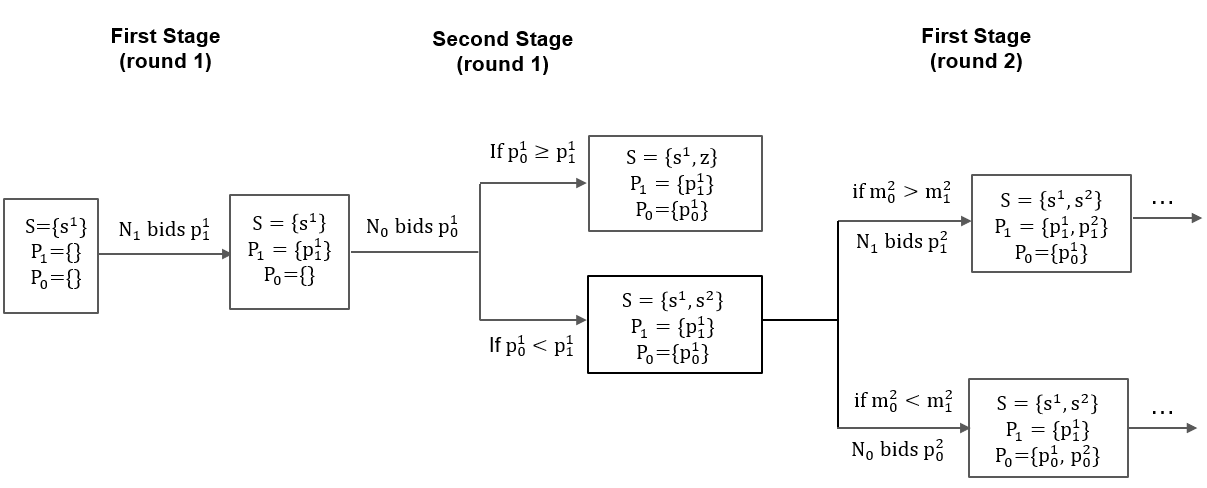

The whole game process is shown in Figure 1. Based on the description for the -th round of repeated game, the utilities of and are

| (8) |

| (9) |

Both participants are interested in their total utilities in the whole process

Lemma 3

For each participant , , if his bid is set as in the -th round, , then .

Lemma 4

If the repeated game goes through indefinitely, that is , then .

Proof

For the -th round, let be the leader and thus is the follower. Since there are only two players, all will belong to one player, if the follower can successfully repurchase from the leader, and then the repeated game stops. It means that in the -th round, units of is bought by from and the game stops at the terminal state . So if the repeated game goes through indefinitely, it must be that in each , , and buys from . Thus in the -th round, .

| (10) |

and

This result holds. ∎

Lemma 5

If there is a Stackelberg equilibrium in the two-player repeated Stackelberg game, then in this Stackelberg equilibrium.

Proof

Suppose to the contrary that in this Stackelberg equilibrium, then there must exist , such that . However, by Lemma 3, we know that if each player sets its price as , then its utility . Hence can obtain more utility by setting , which is a contradiction that doesn’t give the best response in this Stackelberg equilibrium. ∎

Lemma 6

If there is a Stackelberg equilibrium in the two-player repeated Stackelberg game, then the repeated game stops in a finite number of steps, meaning , in this Stackelberg equilibrium.

The following theorem states that once a Stackelberg equilibrium exists and , then this player must buy all at last.

Theorem 4.1

If , , and a Stackelberg equilibrium exists, then , in all Stackelberg equilibria.

Proof

Based on Theorem 4.1, we go to prove the existence of the Stackelberg equilibrium by proposing an equilibrium strategy in the following theorem.

Theorem 4.2

If , , the following strategy is a Stackelberg equilibrium:

| (11) |

The proof of Theorem 4.2 is provided in Appendix B.

5 Multi-Player Repurchase Stackelberg Game

This section goes to extend the discussion for the multi-player scenario, in which has more than half of , and are repurchased participants. triggers the repurchase process, and asks all other repurchased participants to report their bids at first, and decides his bid later. We also model the repurchase process of the multi-player scenario as a two-stage Stackelberg game, where are the leaders to determine their bids in Stage I, and acts as the followers to decide his bid in Stage II. Different from the two-player scenario, shall trade with each , . Then each , , has his utility as (1) and (2). But the utility of is the total utility from the trading with all . That is

5.1 Analysis of Stackelberg Equilibrium

In the Stackelberg repurchase game for multi-player scenario, shall trade with each , . Inspired by the Stackelberg equilibrium in the two-player Stackelberg game, we first discuss the best response of , if each reports his bid as

| (12) |

Then we study the collusion from a group of repurchased players. Our task is to prove that once a group of repurchased participants deviate from the bidding strategy (12), then their total utility must be decreased. This guarantees that each participant would like to follow the bidding strategy (12).

Lemma 7

In the Stackelberg repurchase game for the multi-player scenario, if all leaders set their bids as (12) in Stage I, then the best response of the follower in Stage II is .

Proof

To study the collusion of repurchased participants, we partition the set of into two disjoint subsets and , such that each follows the bidding strategy (12), while each does not. Thus given all bids provided by players, the bid profile can be equivalently expressed as . Here we are interested in the total utility of all players in , and thus define

Following Lemma shows that once a group of participants deviate from the bidding strategy (12), then their total utility decreases.

Lemma 8

Let and . Then

The proof of Theorem 8 is provided in Appendix C.

Theorem 5.1

In the multi-player Stackelberg repurchase game, the bid profile is a Stackelberg equilibrium, where is set as (12).

Proof

To simplify our discussion, we define the price profile , and denotes the profile without the price of . So . From Lemma 7, we have the best response of in Stage II is . However, Lemma 8 indicates that no one would like to deviate from the pricing strategy (12), as Thus given the price profile , nobody would like to change its strategy unilaterally. Therefore, is a Stackelberg equilibrium. ∎

From the perspective of cooperation, we can observe that no group of repurchased participants would like to collude to deviate from the bidding strategy (12) by Lemma 8. Thus we have the following corollary.

Corollary 1

Given the Stackelberg equilibrium of , no group of repurchased participants would like to deviate this equilibrium.

In the case of incomplete information, the analysis of the Bayesian Stackelberg equilibrium becomes extremely complicated. As discussed in Section 3.2, in the case of the two-player Stackelberg game, the leader only needs to optimize the utility based on incomplete information. However, when there are multiple leaders, the strategies of leaders should reach a Bayesian Nash equilibrium, which is much more difficult to calculate. So we regard it as our future work to analyze the Bayesian Stackelberg equilibrium of the multi-player repurchase Stackelberg game.

6 Discussion

6.1 A Blockchain Solution to Budget Constraints

In the previous settings, we do not consider the budget constraints. However, this is a common problem for many newly proposed mechanisms. Therefore, we propose a solution scheme by blockchain for the setting with budget constraints.

Suppose owes more than half of and triggers the repurchase process. Our mechanism consists of two stages. All participants except for report their bids in Stage I, and gives his bid in Stage II. We assume ’s budget is larger than , so that he can repurchase all other shares at his bid . For , , if , should pay . However, the payment of may exceed his budget, such that has not enough money to buy units of . Under this situation, we provide a blockchain solution for to solve the problem of budget shortage. That is, we allow to sell his option of buying units of to anyone in the blockchain system. If nobody would like to buy ’s repurchase option, then can repurchase ’s shares at a lower price. Therefore, after reporting bids, additional four steps are needed to finish the payment procedure.

-

•

Step 1. pays . After the payment, gets pieces of . For each with , , he gets the revenue of and loses units of .

-

•

Step 2. For all that , shall pay to buy units of from . Once units of of is sold to , obtains a discounted revenue .

If would not like to repurchase , then he can sell his repurchase option to others at a price of . The price of repurchase option could be negative, meaning that shall pay to another who accepts his chance. If does nothing, we regard that proposes . -

•

Step 3. If a participant in the blockchain system accepts the price of , then he would propose a transaction to buy units of from . The total cost of this participant is , in which is paid to and obtains a discounted revenue of . And units of are transferred from to the participant who buys the repurchase option.

At the end of this step, let be the participant set, in which each participant’s repurchase option hasn’t been sold yet. -

•

Step 4. For each participant , repurchases units of from at a lower price of . At the end of this step, obtains units of , and obtains a revenue of .

6.2 A Blockchain Solution to Lazy Bidders

Under some circumstances, an holder might not bid in the repurchase process, who is named as a lazy bidder. This lazy behavior may block the repurchase process. To solve the problem caused by lazy bidders, we propose the following two schemes.

-

•

Custody Bidding. NFT’s smart contract supports the feature for the holders to assign administrators to report a bid when the holder is idle or fails to make a bid.

-

•

Value Predetermination. Whenever a participant obtains any units of , this participant is required to predetermine the value at which he is willing to bid, and this information is stored in the smart contract. At the beginning of the repurchase process, if a participant fails to make a bid within a certain amount of time, the smart contract automatically reports this participant’s predetermined bid. This does not mean, however, that the participant has to bid at the predetermined price if he decides to make an active bid.

7 Conclusion

In this paper, we propose a novel securitization and repurchase scheme for NFT to overcome the restrictions in existing NFT markets. We model the NFT repurchase process as a Stackelberg game and analyze the Stackelberg equilibria under several scenarios. To be specific, in the setting of the two-player one-round game, we prove that in a Stackelberg equilibrium, , the participant who triggers the repurchase process, shall give the bid equally to his own value estimate. In the two-player repeated game, all securities shall be finally owned by the participant who has a higher value estimate. In the setting of multiple players, cooperation among participants cannot bring higher utilities to them. What’s more, each participant can get non-negative utility if he bids truthfully in our repurchase process.

How to securitize and repurchase NFT efficiently is a popular topic in the field of blockchain. Our work proposes a sound solution for this problem. In the future, we continue to refine our theoretical analysis. First, for the multi-player repurchase Stackelberg game, we will consider the case with incomplete information and explore the Bayesian Stackelberg equilibrium. Second, a model of blockchain economics will be constructed to analyze the payment procedure in Section 6.1. Furthermore, there exist some other interesting problems, including how to securitize and repurchase a common-valued NFT [12], how to host Complete NFTs or Securitized NFTs in decentralized custody protocols [6], whether ABSNFT can serve as a price Oracle, and so on.

Acknowledgment

This research was partially supported by the National Major Science and Technology Projects of China-“New Generation Artificial Intelligence” (No. 2018AAA

0100901), the National Natural Science Foundation of China (No. 11871366), and Qing Lan Project of Jiangsu Province.

References

- [1] Acharya, V.V., Oncu, S.: The repurchase agreement (repo) market. Regulating Wall Street pp. 319–350 (2011)

- [2] Amihud, Y., Mendelson, H.: Liquidity, asset prices and financial policy. Financial Analysts Journal 47(6), 56–66 (1991)

- [3] Angeris, G., Chitra, T.: Improved price oracles: Constant function market makers. In: Proceedings of the 2nd ACM Conference on Advances in Financial Technologies. pp. 80–91 (2020)

- [4] Bhattacharya, A.K., Fabozzi, F.J.: Asset-backed securities, vol. 13. John Wiley & Sons (1996)

- [5] Çağlayan Aksoy, P., Özkan Üner, Z.: Nfts and copyright: challenges and opportunities. Journal of Intellectual Property Law & Practice (2021)

- [6] Chen, Z., Yang, G.: Decentralized custody scheme with game-theoretic security. arXiv preprint arXiv:2008.10895 (2020)

- [7] Constantinides, G.M., Grundy, B.D.: Optimal investment with stock repurchase and financing as signals. The Review of Financial Studies 2(4), 445–465 (1989)

- [8] ERC-1155: https://erc1155.org/

- [9] ERC-721: https://erc721.org/

- [10] Fairfield, J.: Tokenized: The law of non-fungible tokens and unique digital property. Indiana Law Journal, Forthcoming (2021)

- [11] Hong, S., Noh, Y., Park, C.: Design of extensible non-fungible token model in hyperledger fabric. In: Proceedings of the 3rd Workshop on Scalable and Resilient Infrastructures for Distributed Ledgers. pp. 1–2 (2019)

- [12] Kagel, J.H., Levin, D.: Common value auctions and the winner’s curse. Princeton University Press (2009)

- [13] Kong, D.R., Lin, T.C.: Alternative investments in the fintech era: The risk and return of non-fungible token (nft). Available at SSRN 3914085 (2021)

- [14] Li, C., Yan, X., Deng, X., Qi, Y., Chu, W., Song, L., Qiao, J., He, J., Xiong, J.: Latent dirichlet allocation for internet price war. In: Proceedings of the AAAI Conference on Artificial Intelligence. vol. 33, pp. 639–646 (2019)

- [15] Lucas, C.M., Jones, M.T., Thurston, T.B.: Federal funds and repurchase agreements. Federal Reserve Bank of New York Quarterly Review 2(2), 33–48 (1977)

- [16] Mammadzada, K., Iqbal, M., Milani, F., García-Bañuelos, L., Matulevičius, R.: Blockchain oracles: A framework for blockchain-based applications. In: International Conference on Business Process Management. pp. 19–34. Springer (2020)

- [17] Oxygen: Breathing new life into crypto assets. https://oxygen.trade/OXYGEN_White_paper_February.pdf

- [18] Serum: https://www.projectserum.com/

- [19] Valeonti, F., Bikakis, A., Terras, M., Speed, C., Hudson-Smith, A., Chalkias, K.: Crypto collectibles, museum funding and openglam: Challenges, opportunities and the potential of non-fungible tokens (nfts). Applied Sciences 11(21), 9931 (2021)

- [20] Von Stackelberg, H.: Market structure and equilibrium. Springer Science & Business Media (2010)

- [21] Wang, D., Wu, S., Lin, Z., Wu, L., Yuan, X., Zhou, Y., Wang, H., Ren, K.: Towards a first step to understand flash loan and its applications in defi ecosystem. In: Proceedings of the Ninth International Workshop on Security in Blockchain and Cloud Computing. pp. 23–28 (2021)

- [22] Wang, Q., Li, R., Wang, Q., Chen, S.: Non-fungible token (nft): Overview, evaluation, opportunities and challenges. arXiv preprint arXiv:2105.07447 (2021)

- [23] Weed, J., Perchet, V., Rigollet, P.: Online learning in repeated auctions. In: Conference on Learning Theory. pp. 1562–1583. PMLR (2016)

Appendix

A. Proof of Theorem 3.2

Proof

From Theorem 3.1 we know that the best response of is always . Next, we shall discuss the best response of under the condition that ’s bidding strategy is . By (4), we have

So monotonically increases when and monotonically decreases when , implying . Particularly, when , we have

showing the best response of is . On the other hand, when ,

showing the best response of is . This result holds. ∎

B. Proof of Theorem 4.2

Proof

Let us denote the above strategy (11) as and . We have

| (13) |

Denote to be the best responses of with respect to strategy , and is similar. Then

Obviously, . If , from (13) we have So

Now let us consider the case that , for any .

Denote , and we have .

(1) If , then .

If , then . And we have when . Combined with , we have .

If , then

So .

(2) When , we have .

For , we define . Similarly, we define .

If , so we have when . Then

If , . If , , then . So

Above all, we have

| (14) |

∎

C. Proof of Lemma 8

Proof

By Lemma 2, if follower sets its price as in Stage II, then the optimal price is by leader is Stage I. It means that , implying

| (15) |

Let us simplify the best response of as . From Lemma 1 we have

| (16) |

From the utility function (1) and (2), we have

| (17) |

Then

| (18) |

Denote , then

| (19) |

and

| (20) |

Because is the best response of in Stage II given other players’ prices ,

In addition, we have

where the inequality is from (16). So

| (21) | |||||