appAppendix Bibliography

Minimum Wages and Optimal Redistribution††thanks: Email: damianvergara@berkeley.edu. First version: September, 2021. This version: . I am especially grateful to Danny Yagan, Pat Kline, and Emmanuel Saez, for continuous guidance and encouragement throghout this project. I also thank Alan Auerbach, Nano Barahona, Sydnee Caldwell, David Card, Patricio Domínguez, Cecile Gaubert, Andrés González, Attila Lindner, Cristóbal Otero, Pablo Muñoz, Michael Reich, Marco Rojas, Jesse Rothstein, Harry Wheeler, Gabriel Zucman, my discussants Benjamin Glass and Thomas Winberry, and seminar participants at the Online Public Finance Workshop for Graduate Students, the NTA 114th Annual Conference on Taxation, the XIII RIDGE Forum Workshop on Public Economics, UC Berkeley, and Universidad Adolfo Ibáñez for very helpful discussions and suggestions. Early versions of this project benefited from discussions with Jakob Brounstein, Sree Kancherla, Maximiliano Lauletta, Michael Love, Billy Morrison, and Mónica Saucedo. I acknowledge financial support from the Center of Equitable Growth at UC Berkeley. This paper previously circulated under the title “When do Minimum Wages Increase Social Welfare? A Sufficient Statistics Analysis with Taxes and Transfers”. Usual disclaimers apply.

Abstract

This paper analyzes whether a minimum wage should be used for redistribution on top of taxes and transfers. I characterize optimal redistribution for a government with three policy instruments – labor income taxes and transfers, corporate income taxes, and a minimum wage – using an empirically grounded model of the labor market with positive firm profits. A minimum wage can increase social welfare when it increases the average post-tax wages of low-skill labor market participants and when corporate profit incidence is large. When chosen together with taxes, the minimum wage can help the government redistribute efficiently to low-skill workers by preventing firms from capturing low-wage income subsidies such as the EITC and from enjoying high profits that cannot be redistributed via corporate taxes due to capital mobility in unaffected industries. Event studies show that the average US state-level minimum wage reform over the last two decades increased average post-tax wages of low-skilled labor market participants and reduced corporate profits in affected industries, namely low-skill labor-intensive services. A sufficient statistics analysis implies that US minimum wages typically remain below their optimum under the current tax and transfer system.

1 Introduction

Governments use income taxes and transfers to redistribute to low-income individuals. However, those taxes and transfers can be distortionary, yielding an equity-efficiency tradeoff (Mirrlees, 1971; Piketty and Saez, 2013). This paper asks whether a minimum wage can relax that tradeoff and enable more efficient redistribution than income taxes and transfers alone.

Economists have long debated this question. Mill (1884) suggested that a minimum wage was the simplest way to redistribute profits to raise the incomes of low earners but Stigler (1946) articulated the argument that a minimum wage is inefficient relative to income-based taxes and transfers given its effects on employment. More recently, attempts to formally address this question have provided mixed answers by using frameworks that fail to incorporate empirically relevant channels through which minimum wages can perform redistribution (Hungerbühler and Lehmann, 2009; Lee and Saez, 2012; Cahuc and Laroque, 2014; Lavecchia, 2020). Empirically, a growing literature has found that minimum wages increase incomes of low earners with limited reductions in employment (Lee, 1999; Autor et al., 2016; Cengiz et al., 2019; Dube, 2019; Fortin et al., 2021; Manning, 2021), possibly accompanied by reduced corporate profits (Draca et al., 2011; Harasztosi and Lindner, 2019; Drucker et al., 2021). Yet, even if minimum wages redistribute from high-earning capitalists to low-earning workers, it remains unsettled whether such redistribution is preferred over analogous redistribution via corporate income taxes and income-based transfers alone, or to what extent there exist interactions between the minimum wage and the tax system that help governments to redistribute more efficiently when using all instruments together.

This paper proposes a novel theoretical framework to analyze the redistributive role of the minimum wage when taxes and transfers are also available to the policymaker. I characterize optimal redistribution for a government with three policy instruments: labor income taxes and transfers, corporate income taxes, and a minimum wage. The analysis illustrates the channels through which the minimum wage affects the income distribution, explicitly describing its tradeoffs and interactions with the tax system. Results are expressed as a function of reduced-form “sufficient statistics” that can be estimated from appropriate data. The sufficient statistics feature, which is illustrated in an empirical exercise using publicly available US data, provides a direct connection between theory and evidence in the optimal policy analysis.

The model of the labor market uses directed search and two-sided heterogeneity to allow for three potentially relevant features regarding the use of a minimum wage: the possibility of limited employment effects, wage and employment spillovers to non-minimum wage jobs, and positive firm profits. A population of workers with heterogeneous skills and costs of participating in the labor market decides whether to enter the labor market and which sort of job to seek. A corresponding population of capitalists with heterogeneous productivity decides whether to create firms, how many vacancies to post, and attaches a wage to those vacancies. In the model, minimum wage changes affect workers’ application strategies which, in turn, affect the posting behavior of firms. These behavioral responses can lead to limited employment effects and spillovers to non-minimum wage jobs. The model features positive profits in equilibrium and reproduces other empirically relevant characteristics of labor markets such as wage dispersion for similar workers (Card et al., 2018) and finite firm-specific labor supply elasticities (Sokolova and Sorensen, 2021). Importantly, allocations are constrained efficient in directed search models (Moen, 1997; Wright et al., 2021) so the analysis restricts the attention to the redistributive role of the minimum wage rather than its efficiency rationales usually discussed in the related literature.

I use this model of the labor market to characterize optimal policy when a utilitarian social planner chooses the minimum wage, the labor income tax system, and the corporate tax rate to maximize social welfare taking as given social preferences for redistribution. Considering first a case with no taxes and transfers, the minimum wage affects the welfare of active low- and high-skill workers through its effects on equilibrium wages and employment probabilities, and the welfare of capitalists through its effects on profits. This implies that the minimum wage can affect both the relative welfare within labor income earners and between labor and capital income earners. When income taxes and transfers are present, the optimal minimum wage depends additionally on fiscal externalities from both sides of the market. On the workers’ side, changes in wages and employment induce a change in income tax collection and transfer spending. On the firms’ side, the change in profits affects corporate tax revenue. The optimal minimum wage increases when the corporate tax rate is low, both because the revenue loss is smaller and the welfare gains from redistributing from capitalists to workers are higher.

When the planner simultaneously chooses the tax system and the minimum wage, binding minimum wages can be desirable because they can make tax-based redistribution more efficient. To illustrate why, suppose that the optimal tax schedule with no minimum wage resembles an EITC to redistribute to low-wage workers. If firms internalize the effects of the EITC, they will react by lowering pre-tax wages (Rothstein, 2010). However, the minimum wage prevents firms from decreasing wages, thereby increasing the efficacy of the EITC. In other words, the minimum wage allows the transfer to low-wage workers to be partially paid by firm profits. When corporate taxes distort pre-tax profits, they cannot fully correct this incidence distortion, suggesting that combining minimum wages and corporate taxes is possibly optimal for taxing profits. The fiscal benefit of the minimum wage is accompanied by a vacancy posting distortion that can generate disemployment effects. This distortion is possibly small at low levels but growing as the minimum wage departs from the market wage, generating a tradeoff for the planner.

Given this intuition, I show that if the effect on vacancies is negligible when the minimum wage is set at the market level, then having a binding minimum wage is desirable if the planner still wants to redistribute profits from the affected firms to other individuals in the economy after having used the corporate tax rate. This condition is met when the corporate tax is distorting enough not to distribute profits to workers at the socially desired level. I also show that, under the optimal minimum wage, the marginal tax rate on employed low-skill workers is negative if the social planner values redistribution toward them. This conclusion extends Lee and Saez (2012) result on the complementarity between the EITC and the minimum wage using a framework with imperfect labor markets and positive firms profits.

I then study in greater depth the interaction of the minimum wage and the corporate tax rate under international tax competition. Corporate taxes may optimally be low because capital in manufacturing can flow to lower-tax countries (Devereux et al., 2008; Devereux et al., 2021). A minimum wage with incidence on manufacturing could similarly cause capital to flow to lower-tax countries. However, if the minimum wage predominantly affects non-tradable services industries, then changes in the minimum wage generate little capital distortions. I show that the minimum wage can be desirable as a kind of industry-specific corporate tax if it affects profits in immobile service firms while leaving corporate taxes low for unaffected mobile firms. Formally, the welfare benefits of increasing the minimum wage are larger when the capital in non-affected firms is more mobile because the optimal corporate tax decreases, making a stronger case for a binding minimum wage that does not encourage undesirable capital flows.

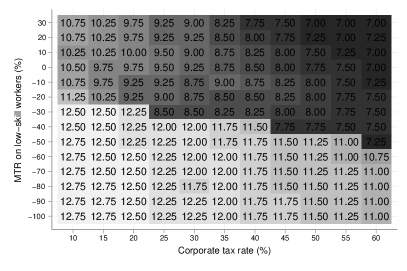

To close the theoretical discussion, I present a suggestive numerical exercise to illustrate the intuitions developed throughout the policy analysis. I calibrate a restricted version of the model to study how the optimal minimum wage changes under different tax systems. Optimal minimum wages are higher when the EITC is larger and when the corporate tax rate is lower, but social welfare is larger when all instruments are used together. Then, a general finding of the analysis is that social planners should not make the tax system and the minimum wage compete for who is the most efficient redistributive policy. Instead, social planners can benefit from using all instruments together. Optimal redistribution possibly consists of a binding minimum wage, a non-trivial corporate tax rate, and a targeted EITC.

One feature of the policy analysis is that some results can be written as a function of sufficient statistics, meaning that reduced-form causal effects can be used to assess whether minimum wages are too high or too low under a given tax and transfer system. Changes in capitalists’ welfare after minimum wage changes coincide with profit effects. Changes in workers’ welfare after minimum wage changes are summarized by the change in the expected utility of participating in the labor market which, under the assumptions of the model, equals the change in the average post-tax wage of labor market participants including the unemployed. This sufficient statistic, whose sign is theoretically ambiguous, aggregates all wage, employment, and participation responses that can affect workers’ utility in a single elasticity.

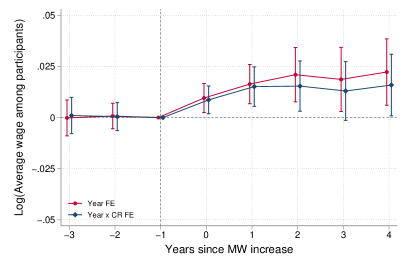

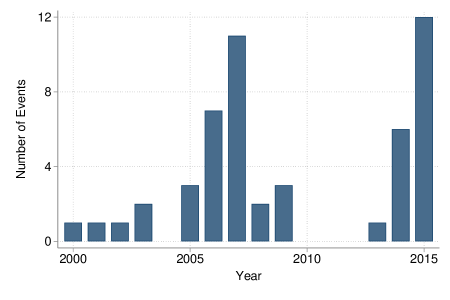

Given this attribute, the final part of the paper provides empirical estimates of these sufficient statistics by exploiting US state-level variation in minimum wages. I follow Cengiz et al. (2019); Cengiz et al. (2022) and estimate stacked event studies, where events are defined as state-level hourly minimum wage increases of at least $0.25 (in 2016 dollars) in states where at least 2% of the pre-event year working population earned less than the new minimum wage and where treated states did not experience other relevant minimum wage increases in the pre-event window. I identify 50 events in the period 1997-2019 for which the outcomes of interest are observed through an eight-year balanced window.

The data consists of yearly state-level aggregates of different outcomes of interest. To measure workers’ outcomes, I follow Cengiz et al. (2019); Cengiz et al. (2022) and use the individual-level NBER Merged Outgoing Rotation Group of the CPS to compute average pre-tax hourly wages and the Basic CPS monthly files to compute employment and participation rates. I combine these data sources to compute pre-tax versions of the worker-level sufficient statistics at the skill-by-state-by-year level, where low- and high-skill workers are defined by their college attainment. To estimate workers’ side fiscal externalities, I use data on income maintenance benefits, medical benefits, and gross federal income taxes taken from the BEA regional accounts. State-level average profits are proxied by the gross operating surplus estimates from the BEA regional accounts and normalized by the average number of private establishments reported in the QCEW data files. Combining both data sources I compute average pre-tax profits per establishment at the industry-by-state-by-year level.

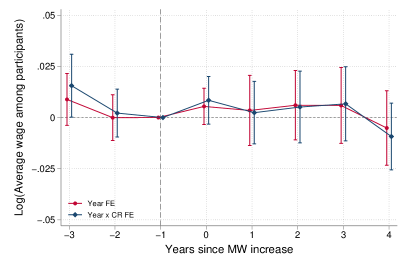

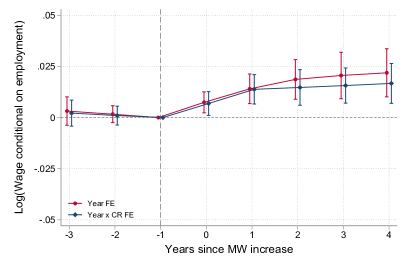

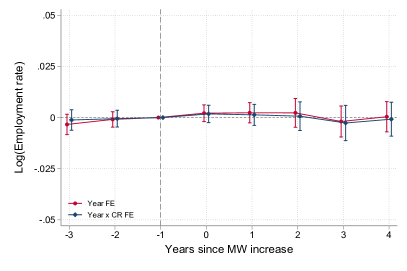

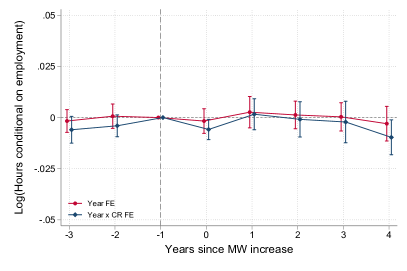

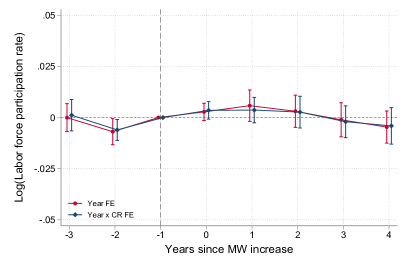

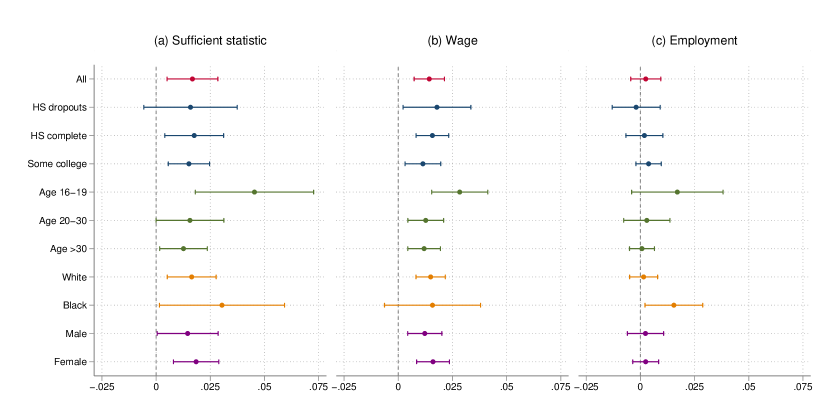

The empirical results imply that minimum wages have increased low-skill workers’ welfare with an estimated elasticity of around 0.1. Conversely, all specifications estimate a precise zero elasticity for the high-skill workers’ analog. Results for low-skill workers are stable across demographic groups, suggesting that the welfare gains are not concentrated on particular groups of “winners”. If anything, teens (aged 16-19) and black low-skill workers seem to experience larger welfare gains from minimum wage increases, but no group experiences welfare losses. Consistent with Cengiz et al. (2019); Cengiz et al. (2022), decomposing the sufficient statistic of low-skill workers across different margins shows that the entire effect is driven by an increase in the wage conditional on employment. No effect is found on hours, employment, or participation.

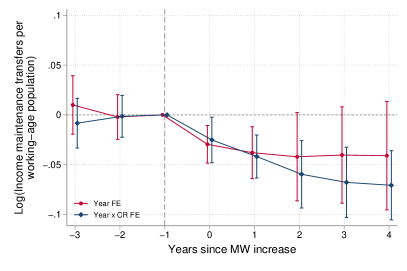

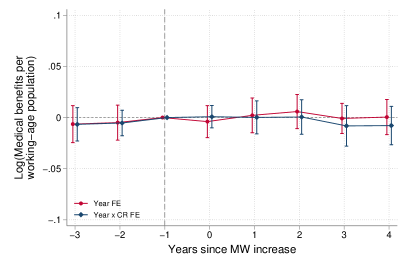

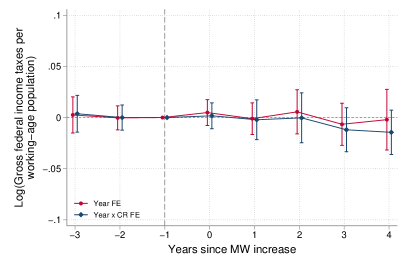

The estimated elasticity of income maintenance benefits to minimum wage changes ranges between -0.31 and -0.39, suggesting sizable fiscal externalities on the workers’ side of the market. This result is consistent with Reich and West (2015), who find elasticities of around -0.2 for SNAP expenditures, and Dube (2019), who finds that after-tax income elasticities are one-third smaller than their pre-tax analogs. These fiscal externalities attenuate the welfare gains for low-skill workers. I find no effects on medical transfers and gross federal income tax liabilities, suggesting that most of the worker-level fiscal effects are mediated by targeted transfers based on pre-tax income levels.

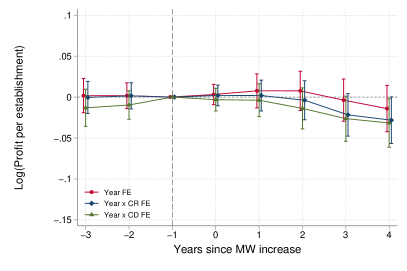

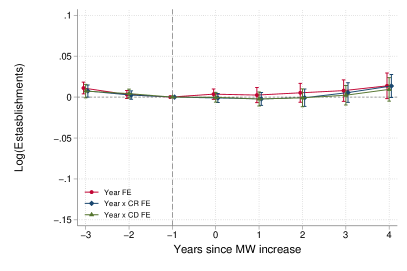

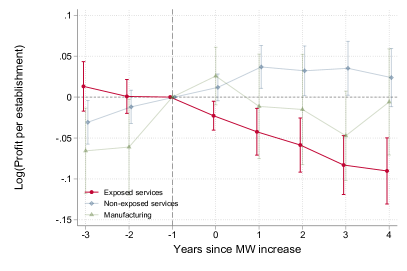

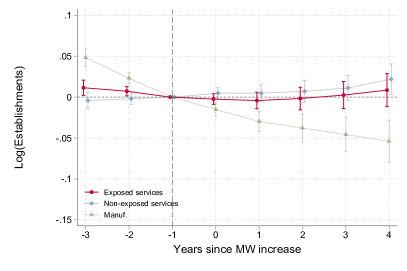

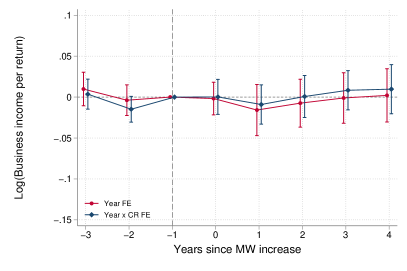

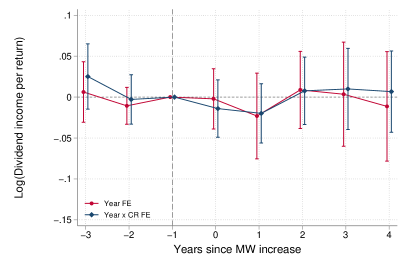

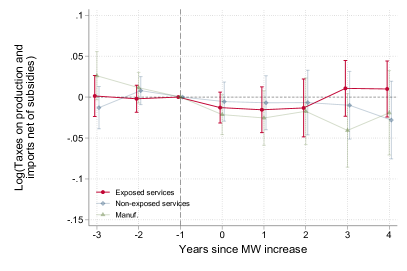

When looking at pre-tax profits per establishment, the estimated elasticity is zero when pooling all industries. However, I find a clear negative effect in “exposed industries” with large numbers of minimum wage workers (retail trade, low-skill health services, food, accommodation, and social services) with an estimated elasticity of -0.36. No association is found between profits and minimum wage events in manufacturing and non-exposed service industries. The effect on the number of establishments in the exposed services is negligible, suggesting that changes in average pre-tax profits are driven by the intensive margin. The estimated effect of pre-tax profits generates a fiscal externality in terms of corporate tax revenue that is not significantly present in other sources of capital income revenue such as business and dividend income reported in the SOI state-level tables.

To interpret the estimates through the lens of the optimal policy analysis, I plug the empirical estimates into the theoretical results to assess the desirability of small minimum wage increases under different calibration choices. In the absence of preferences for redistribution, increasing the minimum wage is close to being welfare-neutral. However, increasing the minimum wage generates substantial welfare gains when distributional concerns between workers and capitalists are incorporated. Intuitively, results show that minimum wages help low-skill workers, hurt firm owners in exposed industries, and generate fiscal savings in income transfers but fiscal costs in terms of corporate tax revenue. Total gains for low-skill workers are comparable to total losses for capitalists, and the net fiscal effect is approximately zero. However, average post-tax profits per capitalist are between five and six times larger than average per capita post-tax wages of active low-skill workers. As a result, when including social preferences for redistribution, the gains for workers substantially outweigh the losses for capitalists. Hence, results suggest that, under existing tax and transfer systems, the average past increase in state-level minimum wages has increased social welfare, and increasing the minimum wage today would do so as well.

Related literature and contributions

The main contribution of this paper is to provide a normative analysis of the minimum wage in a framework with taxes and transfers. Previous literature abstracts from firm profits, firm-level heterogeneity, and corporate taxation, and bases the analysis on labor market models that do not explicitly accommodate empirically relevant general equilibrium effects of the minimum wage that can dampen employment impacts. Lee and Saez (2012) use a competitive supply-demand framework and show that the case for binding minimum wages under optimal taxes depends on labor rationing assumptions. Cahuc and Laroque (2014) contest Lee and Saez (2012)’s result by arguing that the minimum wage cannot improve welfare on top of an optimal non-linear tax schedule even if the labor demand is modeled as a standard monopsonist. Both analyses abstract from search frictions and firm-level heterogeneity, and do not give a central role to firm profits. Hungerbühler and Lehmann (2009) and Lavecchia (2020) consider random search models but also abstract from firm profits, restricting the role of the minimum wage under optimal taxes to solving search and matching inefficiencies.

A complementary literature studies the welfare consequences of the minimum wage using structural models that abstract from tax-design questions. Some papers also abstract from the distributional dimension and focus on efficiency rationales motivated by labor market imperfections (Flinn, 2006; Wu, 2021; Ahlfeldt et al., 2022; Drechsel-Grau, 2022). Two recent papers give an important role to redistribution within the analysis. Berger et al. (2022) propose a general equilibrium model of oligopsonistic labor markets and find that welfare improvements from minimum wage increases stem mainly from redistribution because reductions in labor market power can simultaneously generate misallocation as large-productive firms increase their market shares. Consistent with my analysis, they find that the main distributional benefits come from redistributing from capitalists to low-skill workers. Hurst et al. (2022) develop a general equilibrium model to compare the short- and long-run impacts of the minimum wage, finding that the minimum wage encourages capital-labor substitution in the long-run. They argue this generates unintended distributional consequences on low-skill workers that are displaced by capital. Their results favor the tax system but also suggest that a moderate minimum wage can improve the efficacy of the EITC by setting a wage floor for firms. My analysis differs from theirs since I focus on the optimal policy design and its short- and medium-run – rather than long-run – consequences. I also explicitly discuss the interactions between the minimum wage and the corporate tax policy.111Dworczak et al. (2021) indirectly analyzes the redistributive consequences of the minimum wage by studying redistribution through markets and price controls using mechanism design techniques. Loertscher and Muir (2022) also use mechanism design methods to explore whether minimum wages can reduce involuntary unemployment caused by market power.

In terms of optimal redistribution, this paper adds to the literature that explores whether the combination of different instruments can improve the efficiency of the tax system. Seminal examples include Diamond and Mirrlees (1971), who study the interaction between production and consumption taxes, and Atkinson and Stiglitz (1976) and Saez (2002), who study the interaction between income and commodity taxation. Recent papers that study the interaction between a standard income tax system and other policy instruments include Gaubert et al. (2020), Ferey (2022), and Ferey et al. (2022). This paper also adds to the analysis of redistributive policies in labor markets with frictions (Hungerbühler et al., 2006; Stantcheva, 2014; Sleet and Yazici, 2017; Kroft et al., 2020; Bagger et al., 2021; Hummel, 2021b; Mousavi, 2021; Craig, 2022; Doligalski et al., 2022), and to the analysis of redistribution between capital and labor income (Atesagaoglu and Yazici, 2021; Eeckhout et al., 2021; Hummel, 2021a).

Finally, the empirical results add to a large literature that studies the effects of minimum wages on different outcomes. The workers’ side results at the skill-level complement the vast literature that studies effects on wages and employment (Manning, 2021). Results on income maintenance transfers and other fiscal outcomes complement the evidence presented in Reich and West (2015) and Dube (2019). Finally, the empirical results on profits are in line with the findings of Draca et al. (2011), Harasztosi and Lindner (2019), and Drucker et al. (2021) and are, to my knowledge, the first such findings derived using US data.

Structure of the paper

2 Model of the Labor Market

This section develops a model of the labor market with positive firm profits that can accommodate limited employment effects and spillovers to non-minimum wage jobs after minimum wage increases.

2.1 Setup: workers and capitalists

Overview

The model is static and uses directed search and two-sided heterogeneity. On one side, there is a population of workers that is heterogeneous in two dimensions: skills and costs of participating in the labor market. For simplicity, I assume workers are either low-skill or high-skill. On the other side, there is a population of capitalists with heterogeneous productivities. Labor market interactions are modeled following a directed search approach (Moen, 1997). Capitalists decide whether to create firms based on expected profits. Conditional on creating a firm, they post wages and vacancies, with all vacancies posted at a given wage forming a sub-market.222The notion of sub-market should not be confounded with the notion of local labor market. Sub-markets only vary with wages and, in principle, all workers are equally able to apply to them. Both concepts could be closer in a more general model with multidimensional firm heterogeneity and heterogeneous application costs. Labor markets are segmented, meaning that wages and vacancies are skill-specific. Workers observe wages and vacancies and make their labor market participation and application decisions. In equilibrium, there is a continuum of sub-markets indexed by , characterized by skill-specific wages, , vacancies, , and applicants, , with indexing skill.

Matching technology

There are standard matching frictions within each sub-market. The number of matches within a sub-market is given by the matching function , with continuously differentiable, increasing and concave, and possessing constant returns to scale. The matching technology is allowed to be different for low- and high-skill workers (Berman, 1997; Hall and Schulhofer-Wohl, 2018).

Under these assumptions, the sub-market skill-specific job-finding rate can be written as

| (1) |

with , where is the sub-market skill-specific vacancies to applicants ratio, also denoted as sub-market tightness. Intuitively, the higher the ratio of vacancies to applicants, the more likely that an applicant will be matched with one of those vacancies. Likewise, the sub-market skill-specific job-filling rate can be written as

| (2) |

with . Intuitively, the lower the ratio of vacancies to applicants, the more likely that the firm will be able to fill the vacancy with a worker. Neither workers or firms internalize that their behavior affects equilibrium tightness, so they take and as given when making their decisions.

Workers

The population of workers is normalized to 1. The exogenous shares of low- and high-skill workers are given by and , respectively. Conditional on skill, each worker draws a parameter that represents the cost of participating in the labor market, which admits different interpretations such as search costs, disutility of (extensive margin) labor supply, or other opportunity costs of working such as home production. Let and be the skill-specific density and cumulative distributions of , respectively, both of which are assumed to be smooth.

Workers derive utility from the after-tax wage net of labor market participation costs. Since the model abstracts from intensive margin decisions, I refer to wages, incomes, or earnings indistinctly. The utility of not entering the labor market is , where is a lump-sum transfer paid by the government to non-employed individuals. is the same for all workers, regardless of their type. When entering the labor market, workers apply to jobs. Following Moen (1997), I assume that workers can apply to jobs in only one sub-market.333See Kircher (2009) and Wolthoff (2018) for models where workers can simultaneously apply to several sub-markets. Conditional on employment, after-tax wages in sub-market are given by , where is the (possibly non-linear) income tax-schedule, with . Then, the expected utility of entering the labor market for a worker of type is given by

| (3) |

since workers apply to the sub-market that gives them the highest expected after-tax wage internalizing that the application ends in employment with probability and unemployment with probability .

Recall that depends on the mass of workers of skill that apply to jobs in sub-market : given a stock of vacancies, the more workers apply, the smaller the likelihood of being employed. Then, individuals take as given but it is endogenously determined by the aggregate application behavior. This implies that, in equilibrium, all markets have the same expected after-tax wage, i.e., , for all ; if not, workers have incentives to change their applications toward markets with higher expected values, pushing downward the job-filling probabilities and restoring the equilibrium. This means that workers face a trade-off between wages and employment probabilities because it is more difficult to get a job in sub-markets that pay higher wages.444I assume risk neutrality. Incorporating risk aversion does not affect the high-level analysis but affects the empirical approximations of the relevant objects of the optimal policy analysis. I come back to this discussion in the next section.

In what follows, I define so . The labor market participation decision is given by . This implies that if , otherwise. Let denote the mass of active workers of skill , that is, the mass of workers of skill that enter the labor market. Then, . Inactive workers are given by . Denote by the mass of individuals of skill applying to jobs in sub-market , so . I assume away sorting patterns based on , that is, application decisions conditional on participating in the labor market are independent from .

Note that the expression implies that can be written as a function of and , for all (Moen, 1997). Formally, , with and .555Since , then . Recalling that and asssuming yields the result. This result simplifies the analysis below since it implies that, conditional on wages, equilibrium behavior can be summarized by the scalars without needing to characterize the continuous sequence of .

Capitalists

The population of capitalists is normalized to . Each capitalist draws a parameter that represents firm productivity. Let and be the density and cumulative distributions of , respectively, both of which are assumed to be smooth.

Capitalists observe and choose whether to create a firm. Firms are price-takers in the output market (with the price normalized to 1). Technology is assumed to depend on , low- and high-skill workers, and the (flat) corporate tax rate, , so a firm of productivity that hires workers generates revenue equal to , with twice differentiable, , and , , and , for . Allowing the revenue function to depend on accomodates, in a reduced-form fashion, the fact that corporate tax rates can distort pre-tax profits (Kennedy et al., 2022).666In Appendix A, I propose two different microfoundations of that generate dependence on : a capital allocation problem, where capitalists have a fixed stock of capital that have to allocate between the domestic firm and an international outside option, and an effort allocation problem, where revenue also depends on the owners’ effort. The same arguments may lead to also depend on the minimum wage. I use the capital allocation problem in a policy application in Section 4.

Firms choose skill-specific wages, , and vacancies, , internalizing that is the result of the matching process. While firms take the job-filling probabilities as given, they internalize that paying higher wages increases the job-filling probabilities. In other words, the wage choice is equivalent to the sub-market choice. I rewrite job-filling probabilities as , with (since firms take as given), so . Posting vacancies has a cost , with and . Then, pre-tax profits are given by revenue net of labor costs:

| (4) | |||||

Denote the value function by . Then, after-tax profits are given by .

Conditional on , firms are homogeneous. Then, the solution to the profit maximizing problem can be characterized by functions and . Appendix A derives the first-order conditions and shows that dispersion in productivities leads to dispersion in wages, with wages marked down relative to the marginal productivities.777The effective wage markdown is governed by the wage-dependent job-filling probabilities – which emulate firm-specific labor supply elasticities – and the vacancy creation costs. indexes sub-markets as well as the productivity levels of capitalists that create firms, so , , and .

Capitalists pay a fixed cost, , to create firms, and receive the lump-sum transfer, , when remaining inactive, so they create firms when . Since profits are increasing in productivity, the entry rule defines a productivity threshold, , implicitly determined by such that capitalists create firms only if . Then, the mass of active capitalists is given by . The mass of inactive capitalists, , is given by , with .

2.2 Discussion

Before introducing a minimum wage to the model, I discuss some features and limitations of the proposed framework. This is a non-exhaustive discussion which is continued in Appendix A.

Directed search

Directed search models generate efficient outcomes in terms of search and posting behavior (Moen, 1997; Wright et al., 2021). That is, these models don’t exhibit inefficient mixes of applicants and vacancies as can happen in random search models (Hosios, 1990; Mangin and Julien, 2021). In Appendix A, I show that the proposed model maintains this property, which I interpret a feature rather than a design flaw as it fosters a focus on the redistributive role of the minimum wage rather than on its efficiency rationales (e.g., Burdett and Mortensen, 1998; Acemoglu, 2001).888This result can be thought of as an extension of Moen (1997) result to a setting with ex-ante firm-level heterogeneity and positive profits. I show that not only posting is efficient, but also the entry thresholds at the worker- and firm-levels.

Monopsony power

While search and posting behavior is efficient, the model admits monopsony power through wage-dependent job-filling probabilities that have a similar flavor to the standard monopsony intuition of upward-slopping firm-specific labor supply curves (Robinson, 1933; Card et al., 2018) supported by recent empirical evidence (Staiger et al., 2010; Azar et al., 2019; Dube et al., 2020; Sokolova and Sorensen, 2021; Bassier et al., 2022). Firms internalize that paying higher wages lead to more applicants, so wages are marked down relative to marginal productivities.999Appendix A shows that the standard markdown equation can be derived from the firm’s first order conditions.

Low-wage labor markets

The equilibrium of the model is consistent with other stylized facts of low-wage labor markets. The model features wage dispersion for similar workers (Card et al., 2018), wage posting rather than bargaining, which has been found to be more relevant for low-wage jobs (Hall and Krueger, 2012; Caldwell and Harmon, 2019; Lachowska et al., 2022), and can rationalize bunching in the wage distribution at the minimum wage (Cengiz et al., 2019).

Restricted heterogeneity

One limitation of the model is that the dimensions of worker- and firm-level heterogeneity are limited. On the workers’ side, the model assumes that all workers of the same skill type get the same expected utility. Hurst et al. (2022) suggest within-skill heterogeneity can mask important distributional effects if there are winners and losers within skill-type after minimum wage changes. Extending the model in this direction would imply that – which will play an important role in the optimal policy analysis – can be different for different groups of low- and high-skill workers.101010Formally, consider an additional variable, such that . This could be the case if, for example, workers of type can apply to a different pool of firms than workers of type . I come back to this discussion in Section 5 where I empirically explore for heterogeneities in the estimated welfare changes within skill groups.

On the firm side, one-dimensional heterogeneity is a convenient simplification. Extending the model to multidimensional heterogeneity, , is straightforward so long as workers do not have preferences for these attributes. This could accommodate, for example, variation in factor shares. In this setting, the problem’s solution would be given by wage and vacancy functions and , and by a set of conditional productivity thresholds, . Such an extension adds little intuition to the general policy analysis while introducing more complicated notation. The above argument requires workers to not have preferences over beyond its effect on wages and vacancies. Hence, the simple extension to multidimensional heterogeneity does not apply to non-wage amenities.111111For evidence on their importance, see Bonhomme and Jolivet (2009), Mas and Pallais (2017), Maestas et al. (2018), Sorkin (2018), Taber and Vejlin (2020), Jäger et al. (2021), Le Barbanchon et al. (2021), Lindenlaub and Postel-Vinay (2021), Sockin (2021), Lamadon et al. (2022), and Roussille and Scuderi (2022). Amenities can affect the policy analysis for two reasons. First, if workers rank firms using a composite index of expected wages and amenities and the latter are not taxed, then the tax system can distort workers’ preferences (Lamadon et al., 2022). Second, if amenities are endogenous, minimum wage increases may induce firms to worsen the non-wage attributes of the job (Clemens et al., 2018; Clemens, 2021). Such effects could attenuate potential welfare gains to workers after minimum wage hikes.

2.3 Introducing a minimum wage

I introduce a minimum wage, , to explore how the predictions of the model speak to the related empirical literature. I separately explore the effects on workers and capitalists decisions.

Low-skill workers

In equilibrium, , for all sub-markets . Let be the sub-market constrained by the minimum wage, so . Differentiating yields

| (5) |

Since , and assuming , is not a feasible solution to equation (5). This implies that changes in necessarily affect the equilibrium values of , , or both.

Intuitively, an increase in the minimum wage mechanically makes minimum wage jobs more attractive for low-skill workers. This effect is captured by : the increase in the attractiveness of this sub-market is the net-of-tax gain conditional on working, , times the employment probability, . This attracts new applicants toward minimum-wage sub-markets (from other sub-markets and/or from outside the labor force), thus pushing downwards until the across sub-market equilibrium is restored. This decreases the employment probability in sub-market , whose effect is captured by the change in the employment probability, , times after-tax income conditional on employment, . These two effects capture the standard effects on wages and employment debated in the minimum wage literature. How these effects balance determine the overall impact on expected utility.

This tradeoff captures the essence of the general equilibrium effects of the model: the initial change in applications toward minimum-wage jobs triggers a sequence of reactions that reconfigure labor market outcomes. Changes in also affect the equilibrium of unconstrained low-skill sub-markets. To see this, let be a sub-market that is not constrained by the minimum wage, so . Differentiating yields

| (6) |

Equation (5) suggests that the left-hand-side of equation (6) is unlikely to be zero, implying that or or both are possibly affected by changes in the minimum wage. There are two forces that mediate this spillover. First, the change in applicant flows between sub-markets and from in and out of the labor force affects the employment probabilities of all sub-markets until the equilibrium condition of equal expected utilities is restored. This effect is captured by the first term of equation (6). Second, firms can also respond to changes in applicants. The potential wage response is captured in the second term of equation (6) and changes in vacancy posting implicitly enter the terms of equations (5) and (6).

Changes in also induce changes in labor market participation, since , so . Then, whenever , minimum wage hikes increase labor market participation. The behavioral response is scaled by , which may be negligible. This effect may result in positive impacts on expected utilities with little participation effects at the aggregate level.

High-skill workers

If , equilibrium effects for high-skill workers take the form of equation (6). Then, the question is whether there are equilibrium forces that rule out solutions of the form . In this model, effects in high-skill sub-markets are mediated by the production function, since demand for high-skill workers depends on low-skill workers through . Then, this model may induce within-firm spillovers explained by a technological force. Changes in low-skill markets affect high-skill posting, thus affecting high-skill workers application decisions.

Firms

Workers react to changes in the minimum wage by changing their application strategies and extensive margin decisions, thus affecting sub-markets’ tightness and the profit maximization problem of the firms. Appendix A provides expressions for the effects of minimum wage changes on firms’ outcomes, which are analytically complex given the potential non-linearities of the matching, production, and vacancy cost functions. In what follows, I describe the main intuitions behind the analysis.

Firms for which the minimum wage binds optimize low-skill vacancies and high-skill wages and vacancies taking low-skill wages as given. The effect of the minimum wage on low-skill vacancy posting is ambiguous. On one hand, an increase in the minimum wage induces a mechanical increase in labor costs, decreasing the expected value of posting a low-skill vacancy. However, if sub-market tightness decreases given the increase in applicants, job-filling probabilities increase. This effect increases the expected value of posting a low-skill vacancy. Within the minimum wage sub-market, the net effect on vacancies is more likely to be negative the lower the productivity.121212In the model, it is possible to have productivity dispersion across firms that pay the minimum wage. Concretely, all firms whose market low-skill wage is lower than bunch at conditional on entry. That is, the least productive firms among the constrained group reduce their size after increases in the minimum wage while the most productive firms within this group could have null or positive firm-specific employment effects.

Firms for which the minimum wage does not bind also react by adapting their posted wages and vacancies to changes in their relevant sub-market tightness. The analytical expression for the wage spillover is difficult to sign and interpret but directly depends on the change in sub-market tightness (see equation (A.XXI) of Appendix A). Since wages and vacancies are positively correlated at the firm and skill level, if wage spillovers are positive, then unconstrained firms also post more vacancies and, therefore, increase their size. Therefore, the model has potential to generate reallocation effects.

Profits are also affected by minimum wage changes. Firms for which the minimum wage binds face a reduction in profits regardless of the employment effect. This in turn leads marginal firms to exit the market after increases in the minimum wage. Firms for which the minimum wage does not bind may also have their profits affected given the change in the equilibrium job-filling probabilities.

Relation to empirical literature

The purposely imposed tractability needed for the optimal policy analysis puts limits on the ability of the model to fully rationalize observed labor market reactions to minimum wage changes.131313For structural models with richer levels of heterogeneity and flexibility, see Haanwinckel (2020), Ahlfeldt et al. (2022), Berger et al. (2022), Drechsel-Grau (2022), Engbom and Moser (2022), and Hurst et al. (2022). However, the proposed framework generates predictions consistent with the empirical literature that favor its suitability for the policy analysis.

One systematic finding of the empirical literature is that minimum wage hikes generate positive wage effects with limited – or elusive – disemployment effects (see Manning, 2021 for a recent review). This empirical fact is inconsistent with a perfectly competitive model of the labor market, and is difficult to rationalize with a random search framework since it requires an implausibly large labor force participation response that is at odds with the empirical literature (Cengiz et al., 2022). The proposed framework can rationalize positive wage effects with limited employment and participation effects through the equilibrium changes in applications. When the minimum wage increases, constrained firms face a mechanical increase in their labor costs. However, job applicants reallocate applications toward these jobs, increasing the expected value of posting vacancies. This effect attenuates the negative shock in labor costs. The reorganization of applications within the mass of active workers can mediate this result when the size of the density at the margin of indifference is low enough to prevent important participation responses.

The empirical literature also finds that minimum wages generate spillovers to non-minimum wage jobs in terms of wages and employment both within and between firms (Cengiz et al., 2019; Derenoncourt et al., 2021; Dustmann et al., 2022; Forsythe, 2022; Giupponi and Machin, 2022), and have negative effects on firm profits (Draca et al., 2011; Harasztosi and Lindner, 2019; Drucker et al., 2021). The model incorporates both sets of predictions. The same responses in applications that dampen the employment effects generate spillovers to firms that pay higher wages through changes in their sub-markets’ tightness, and to high-skill workers through technological restrictions embedded in the production function.141414The model fails to accommodate other relevant effects of the minimum wage documented in the empirical literature, namely the passthrough of minimum wages to output prices (MaCurdy, 2015; Allegretto and Reich, 2018; Harasztosi and Lindner, 2019; Leung, 2021; Ashenfelter and Jurajda, 2022; Renkin et al., 2022) and their effects on worker- and firm-level productivity (Riley and Bondibene, 2017; Mayneris et al., 2018; Coviello et al., 2021; Ruffini, 2021; Emanuel and Harrington, 2022; Ku, 2022). Appendix A argues that these pieces are unlikely to play a central role in the optimal policy analysis.

3 Optimal Policy Analysis

This section uses the model of the labor market to characterize optimal redistribution for a social planner with three policy instruments: labor income taxes, a corporate tax rate, and a minimum wage.

3.1 Social planner’s problem

The notion of optimal policy refers to policy parameters that maximize a social welfare function. Following related literature (Kroft et al., 2020; Lavecchia, 2020), the social planner is assumed to be utilitarian and maximize the sum of expected utilities. I assume the social planner does not observe and and, therefore, constrains the policy choice to second-best incentive-compatible policy schemes.

The social welfare function is given by

| (7) | |||||

where are the policy parameters – the minimum wage, the (possibly non-linear) income tax schedule, and the flat corporate tax rate – and is an increasing and concave function that accounts for preferences for redistribution. induces curvature to the individual money-metric utilities, thus allowing social gains from redistributing from high- to low-utility individuals. The incentive compatibility constraints are included in the limits of integration since the planner internalizes that the policy parameters affect the participation decisions through , , and . The first term of equation (7) accounts for the utility of inactive workers and inactive capitalists who get income equal to . The second and third terms account for the expected utility of low- and high-skill workers that enter the labor market, also referred to as active workers. Finally, the last term accounts for the utility of active capitalists.151515The average expected utility of active workers of skill is , where . Then, total expected utility is given by , which yields the expressions above noting that . The average utility of capitalists is , with . Their total utility is therefore , which yields the expression above noting that .

Assuming no exogenous spending requirement, the planner’s budget constraint is given by

| (8) | |||||

where is the mass of employed workers of skill in sub-market and is the skill-specific unemployment rate given by . The budget constraint establishes that the transfer paid to individuals with no market income must be funded by the tax collection on employed workers and active capitalists.

Understanding

To better understand the role of , define the average social marginal welfare weights (SMWWs) of inactive workers, active workers of skill type , and active capitalists of type as

| (9) |

where is the budget constraint multiplier. Average SMWWs represent the social value of the marginal utility of consumption normalized by the social cost of raising funds, thus measuring the social value of redistributing one dollar uniformly across a group of individuals. When the SMWWs are above one, the planner benefits from redistribution since the gains outweight the distortions induced by the increase in revenues. A given value of indicates that the government is indifferent between more dollars of public funds and 1 dollar of additional consumption of individuals of group (Saez, 2001).

The utilitarian assumption used in equation (7) implies that the SMWWs are endogenous to final allocations (and, therefore, to the policy parameters) since social welfare only depends on the concave transformation of individual money-metric utilities. Alternative formulations of the problem can generate different microfoundations for the SMWWs, for example, through exogenous Pareto weights or generalized SMWWs (Saez and Stantcheva, 2016). More generally, SMWWs are sufficient statistics for preferences for redistribution since their values inform the willingness to transfer incomes between different groups of individuals. I return to this when discussing the results of the optimal policy analysis.

Rationing assumptions

Since the social planner cares about expected utilities, rationing assumptions conditional on entering the labor market do not affect the welfare analysis: all workers have equal ex-ante expected utilities, so the allocation to jobs and unemployment after policy changes does not condition the planner’s problem. By contrast, rationing assumptions are central in optimal policy analyses based on competitive labor markets (Lee and Saez, 2012). Rationing matters if sorting to firms conditional on participation depends on , and would play a role if adding additional layers of worker-level heterogeneity imply that some groups are more likely to work at low-wage firms or to be unemployed. This would affect the analysis since the presence of winners and losers within skill-group may distort the assessment of the distributional effects of minimum wage increases (Hurst et al., 2022). I return to this question in Section 5 when testing for heterogeneities in the empirical estimation of the worker-level sufficient statistics.

3.2 Case with no taxes

I now proceed to analyze the redistributive properties of the minimum wage using the framework described above. I start abstracting from the tax system to isolate the effects on the relative tradeoff between low-skill workers, high-skill workers, and capitalists. Taxes and transfers are introduced in the next subsection.

Proposition I: In the absence of taxes, increasing the minimum wage is welfare improving if

| (10) |

Proof: See Appendix B.

Proposition I shows that a small increase of the minimum wage can affect the welfare of active low-skill workers (first term), active high-skill workers (second term), and active capitalists (third term). Depending on the change in utility for the different groups ( and ), the social value of those changes ( and ), and the size of the groups ( and ), increasing the minimum wage may be desirable or not for the social planner.161616While changes in and also affect extensive margin decisions, those margins do not induce first-order welfare effects because marginal workers and capitalists are initially indifferent between states. This implies that the minimum wage can affect both the relative welfare within labor income earners and between labor and capital income earners.

Welfare weights

To understand why the analysis emphasizes the distributional effects of the minimum wage, consider a situation where , for all . Then, the planner’s problem is reduced to assessing changes in total output. The analysis changes when SMWWs are unrestricted. Total output could decrease after minimum wage increases, but if the gains for winners are more socially valuable than the losses for losers, then increasing the minimum wage can be welfare-improving. For example, if the social planner does not care about the utility of capitalists and high-skill workers, there could be scope to increase the minimum wage if the utility of low-skill workers increases after the policy change. The utilitarian assumption implies that SMWWs are endogenous to final allocations, so they are inversely proportional to after-tax incomes. The steepness of the relationship depends on the concavity of .

Sufficient statistics

Given values for the SMWWs, if the sizes of the groups are observed, taking equation (10) to the data requires values for and . Reduced-form estimates of these elasticities facilitate the quantitative assessment of Proposition I without needing to impose structural restrictions on the primitives of the model of the labor market. That is, empirical counterparts of and work as sufficient statistics (Chetty, 2009; Kleven, 2021) for assessing the welfare implications of minimum wage changes.

Profits are, in principle observable, so it is feasible to have reduced-form estimates of . Regarding , recall that, in the absence of taxes, . Multiplying both sides by the sub-market mass of applicants, , and integrating over , yields

| (11) |

where is the skill-specific unemployment rate and , with , is the average wage of employed workers. This implies that is equal to the average wage of active workers including the unemployed. In the case with taxes, is equal to the average pre-tax wage of active workers including the unemployed net of the their average tax liabilities.171717Recall that, in the case with taxes, . Multiplying both sides by the sub-market mass of applicants, , and integrating over , gives (12) where . If the tax schedule is constant, then (13) The first term represents the change in the average pre-tax wage among active workers (see equation (11)). The second term represents the change in average tax liabilities net of transfers among active workers. In both cases, can be computed using data on wages, tax liabilities, employment and participation rates. Then, can be estimated to quantitatively assess equation (10). Section 5 illustrates this exercise.

Two things are worth discussing about the sufficient statistic for workers, . First, captures all general equilibrium effects that affect workers’ utility, including effects on wages, employment, and participation. There is an unsettled discussion in the public debate about the appropriate way of weighting these different effects. The proposed framework offers an avenue for aggregating them into a single elasticity.181818While the sign of is in principle ambiguous, it is not determined by the sign of the employment effects. Appendix A shows the disemployment effects that can be tolerated for the minimum wage to increase average workers’ welfare given positive wage effects. If employment and wage effects are positive, welfare effects on workers are unambiguously positive. Second, equation (11) relies on the risk-neutrality assumption made in Section 2. If workers are risk-averse, then Proposition I remains valid but no longer equals the average wage among active workers including the unemployed, so it cannot be estimated without further assumptions. One way to assess the concerns of using the risk-neutral sufficient statistic is to decompose the empirical estimate across the different margins. If changes in employment are negligible relative to changes in wages, then the risk-neutrality assumption should not have first-order effects on the interpretation of the estimated elasticities. I come back to this discussion in Section 5.

3.3 Case with taxes

The case without taxes informs about the direct welfare effects of the minimum wage. However, in the presence of taxes, changes in labor market outcomes and profits affect tax collection and transfer spending. These fiscal externalities matter for assessing whether increasing the minimum wage is desirable.

Fixed taxes

I first consider a case where the social planner takes the tax system as given and chooses to maximize equation (7). This extension characterizes the mechanical interactions between the minimum wage and the tax system. When unmodeled constraints restrict the scope for simultaneous tax reforms, this case may be the policy-relevant scenario for assessing the desirability of minimum wage reforms.

Proposition II: If taxes are fixed, increasing the minimum wage is welfare improving if

| (14) |

Proof: See Appendix B.

The first line of Proposition II reproduces the welfare tradeoff described in Proposition I. The second to fourth lines summarize the fiscal externalities on both sides of the market. These fiscal externalities matter for the analysis since they either relax or restrict the planner’s budget constraint, consequently relaxing or restricting the redistribution already done by the existing tax system.

The second line describes the fiscal externalities on low-skill labor markets. The first term shows that, if low-skill employment increases, there is an increase in tax collection (or expenditure if there are transfers to workers), , and a decrease in transfers paid to unemployed individuals, . The opposite happens when employment decreases. The second term shows that if the wages of employed workers change, income tax collection changes according to the shape of the income tax schedule, . The third line represents the same effects but for high-skill labor markets.

The fourth line describes the fiscal externalities on the capitalists’ side. The first term shows that changes in profits affect the corporate tax revenue. If profits decrease, the social planner collects less revenue. The second term shows that firms that exit the market generate a negative fiscal externality since they switch from paying taxes to receiving a transfer. Both effects are increasing in the corporate tax rate: the larger , the larger the revenue loss produced by smaller profits and extensive margin responses.

Firm-level fiscal externalities seem particularly relevant in the current state of international tax competition (Devereux et al., 2008; Devereux et al., 2021). Under international capital mobility, it may be difficult to enforce large corporate tax rates because capital can fly to low-tax countries. If corporate taxes are low, then the rationale for using the minimum wage becomes stronger. One concern with this argument is that the same reasons that limit corporate tax rates could apply to the minimum wage: international capital could also react to minimum wage changes. In Section 5 I document that the profit effects are concentrated in labor-intensive industries whose capital is presumably less mobile relative to other industries. By contrast, the effects of corporate tax changes on pre-tax profits seem to be concentrated in capital-intensive industries (Kennedy et al., 2022). This suggests that the economic reasons that push corporate tax rates down are not extendable to minimum wages. I formalize this intuition in Section 4.

Optimal taxes

The previous analysis illustrates the mechanical interaction between the minimum wage and the tax schedule but does not answer if both policies are desirable at an hypothetical joint optimum. The following proposition explores the desirability of the minimum wage when the social planner jointly optimizes the tax system and the minimum wage. For analytical simplicity, I assume that either , or that the social planner can implement skill-specific income tax schedules.191919This allows me to solve the planner’s problem doing pointwise maximization. These assumptions increase the attractiveness of the tax system, making more restrictive the case for a binding minimum wage.

Proposition III: If taxes are optimal, increasing the minimum wage is welfare improving if

| . | (15) |

Furthermore, at the joint optimum: (i) the SMMWs of inactive individuals, active low-skill workers, and active high-skill workers average to 1, and (ii) the average SMMW among active capitalists is below 1.

Proof: See Appendix B.

At a high-level, Proposition III reproduces the same intuition as Proposition II: the desirability of the minimum wage depends on both the effects on the relative welfare of active low-skill workers, active high-skill workers, and active capitalists, and on the fiscal externalities generated on labor markets and profits. However, when taxes are optimized together with the minimum wage, how the minimum wage affects welfare and generates fiscal effects changes. This is reflected in two important differences between equations (14) and (15) that illustrate the forces that play a role in the joint optimum.

First, all relevant elasticities are micro rather than macro elasticities (Landais et al., 2018b, a; Kroft et al., 2020; Lavecchia, 2020), which I denote by partial derivatives. Macro elasticities (Propositions I and II) internalize all general equilibrium effects of the minimum wage, while micro elasticities (Proposition III) mute some of these effects because, at the joint optimum, the minimum wage moves in tandem with taxes. Recall that , with . When taxes are fixed, both and can react to minimum wage changes. However, at the joint optimum, an increase in the minimum wage is accompanied by a change in tax-based subsidies to low-skill workers, possibly leading consumption fixed. Then, the minimum wage directly affects workers’ welfare mainly through potential changes in the employment probabilities driven by changes in vacancy posting. This logic also applies to the effects on employment and profits.202020The direct welfare effects on workers are proportional to the (presumably negative) employment effects. If , multiplying by and integrating over yields . Then, if is fixed, (16)

The fiscal externalities are also affected by optimal taxes. Changes in the minimum wage paired with reductions in low-wage subsidies affect within-firm redistribution. This effect is captured by the term which, for the minimum wage sub-market, is equal to low-skill employment given that . Intuitively, there are fiscal gains from minimum wage increases because they switch the burden of redistribution from the government to firms and, therefore, relax the social planner’s budget constraint by transferring profits to the social planner. To develop intuition, consider a marginal increase in the subsidy to low-skill workers. This reform increases labor supply, so firms optimally react by lowering pre-tax wages (Rothstein, 2010). The minimum wage mutes this behavioral response, making the transfer to low-skill workers less costly. This reform cannot be exactly mimicked by the corporate tax since it distorts pre-tax profits. Possibly, both instruments are used to redistribute profits to workers.212121Firm-level heterogeneity, revenue distortions, and entry distortions impede to fully redistribute from capitalists to workers. That is why the average SMWW of active capitalists is less than 1 at the joint optimum.

The desirability of the minimum wage at the joint optimum depends on how these two forces balance; the assessment of equation (15) is ultimately a quantitative question. Distortions in vacancies are likely to be negligible when the minimum wage is just above the market level. Consequently, the fiscal benefit likely dominates the employment costs when being close to the market level. As the minimum wage departs from the market level, the employment costs increase and become more likely to outweigh the fiscal benefits, hinting at the existence of an interior solution for the optimal minimum wage policy. The next section considers a restricted version of the model to provide concrete analytical conditions to justify binding minimum wages under optimal taxes.222222The proposition also states that, in the joint optimum, the SMMWs of inactive individuals, active low-skill workers, and active high-skill workers average to 1, which is a standard result of optimal tax analyses with quasi-linear utility functions.

Caveats

I briefly discuss two elements that may affect the optimal policy analysis whose formal treatment is beyond the scope of this paper.

First, the theoretical attractiveness of the income tax system relies on its flexibility. In the real world, income tax schedules are not fully non-linear, are not perfectly enforced, and are costly to administrate because, for example, tax evasion, tax avoidance, and imperfect benefit take up.232323See, for example, Andreoni et al. (1998), Slemrod and Yitzhaki (2002), Kleven et al. (2011), Currie (2006), Kopczuk and Pop-Eleches (2007), Chetty et al. (2013), Bhargava and Manoli (2015), Guyton et al. (2017), Goldin (2018), Cranor et al. (2019), Finkelstein and Notowidigdo (2019), Guyton et al. (2021), and Linos et al. (2021). These frictions generate additional efficiency costs to the tax system.242424Abstracting from tax evasion also rules out additional complementarities between the minimum wage and the tax system. For example, if workers under report their incomes, then the minimum wage can increase tax collection by setting a floor on reported labor income (Bíró et al., 2022; Feinmann et al., 2022). Minimum wages can also be difficult to enforce (Stansbury, 2021; Clemens and Strain, 2022), so a more general analysis should consider the relative enforcement costs of the two instruments. On the other hand, tax and transfer systems can tag on additional variables such as family size. That type of flexibility is unlikely to apply to the minimum wage policy (Stigler, 1946). This benefit from using the tax system is not present in the proposed analysis.

Second, the minimum wage affects the distribution before taxes and transfers while taxes and transfers alter pre-tax values to generate the after-tax distribution.252525This claim is true only to a first-approximation since changes in taxes can also affect the pre-tax income distribution (Roine et al., 2009; Alvaredo et al., 2013; Piketty et al., 2014; Vergara, 2022). The optimal policy analysis assumes that the social value of after-tax allocations does not depend on the composition between pre-tax incomes and taxes and transfers. However, recent evidence suggests that affecting the pre- and the post-tax and transfer distribution has different implications for long-run trends in inequality (Bozio et al., 2020; Blanchet et al., 2022). Also, social preferences may put different weights on the two types of interventions. For example, McCall (2013) provides survey evidence that suggests that the US public cares about inequality and redistribution, but prefers policies that address inequality within the firm rather than with taxes and transfers. This is consistent with the results of state-level ballot initiatives that have favored minimum wage changes relative to reforms to top marginal income tax rates (Saez, 2021). Such social preferences could be incorporated by generalizing the SMWWs (Saez and Stantcheva, 2016).

4 Policy Applications

The policy analysis developed in the previous section uses an equilibrium framework to study, at a high-level, the desirability of the minimum wage. When taxes are fixed, the desirability of the minimum wage depends on the relative weight of the direct effects on workers and capitalists – net of fiscal externalities – which can be empirically measured by sufficient statistics. However, when the social planner optimizes both the minimum wage and the tax system, the generality of the model puts limits to the analytical insights that can be obtained in terms of concrete policy recommendations.

In this section, I consider a restricted version of the model to get additional analytical results on the minimum wage desirability under optimal taxes. I consider three policy applications. First, I explore conditions under which it is optimal to have a binding minimum wage that complements a tax-based subsidy to low-skill workers. Second, I focus on the interaction between the minimum wage and the corporate tax rate when the corporate tax distortions differ between firms. Finally, I develop a suggestive numerical exercise to further explore the interactions between the policy instruments at the joint optimum.

4.1 When is it optimal to have a binding minimum wage complemented by a tax-based subsidy to low-skill workers?

Proposition III above gives conditions under which increasing the minimum wage when the tax system is optimal is welfare improving. Equation (15), however, is difficult to assess both in empirical and analytical terms.262626To identify micro elasticities, it is needed variation in minimum wages while holding after-tax allocations fixed. In what follows, I restrict the model to gain analytical tractability and derive additional results that inform the optimal policy at the joint optimum. As noted below, some of these restrictions are supported by the empirical evidence presented in the next section.

The findings presented in the next section suggest that the profit incidence of the minimum wage is concentrated in low-skill labor-intensive services industries, while no effect on profits is found in other industries. This finding is consistent with the idea that minimum wage workers are concentrated in industries such as food and accommodation, low-skill health services, and retail. The empirical results also show no effect of minimum wage reforms on the number of establishments – even in affected industries – and on high-skill workers’ outcomes. Given these facts, the first assumption restricts firm-level heterogeneity to represent a two-industry economy with inframarginal firms and no within-industry heterogeneity, where firms in one sector only hire low-skill workers and firms in the other sector only hire high-skill workers. To fix ideas, one sector will represent “services” and the other “manufacturing”. This simplification puts restrictions on the wage distribution but accommodates the fact that the firms and workers that are affected by the minimum wage may be different from the non-affected ones.272727Under this assumption, the wage distribution consists on two mass points, a low-skill wage (the minimum wage) and a high-skill wage. The results presented in the next section suggest no heterogeneous effects of minimum wage reforms on low-skill workers, suggesting that wage dispersion within skill types is unlikely to play an important role in these applications.

Assumption 1 (A1): There are two fixed populations of inframarginal capitalists indexed by with sizes , where capitalists of type – “services” – only employ low-skill workers, and capitalists of type – “manufacturing” – only employ high-skill workers. Their respective production functions are given by and , and their respective SMWWs are denoted by and .

I also assume that the technological second-order effects captured by are negligible. This is done for analytical tractability. Abstracting from these second-order effects works against the minimum wage desirability. Intuitively, if a minimum wage shock pushes firm size downwards, there is an unintended benefit to firms because the marginal product of labor increases if technology features decreasing returns to scale. This effect attenuates the potential employment effects of the minimum wage.

Assumption 2 (A2): , for .

Given these assumptions, the following proposition shows that when the social planner jointly optimizes the minimum wage and the income tax system, the minimum wage must bind if both the vacancy distortions and the social value of profits are small. The proposition also provides sufficient conditions on the SMWW of active low-skill workers under which the optimal binding minimum wage is complemented by a negative marginal tax rate on employed low-skill workers. The proposition extends existing results on the complementarity of the minimum wage and policies such as the EITC to a more general labor market framework with search and matching frictions and firm profits (Lee and

Saez, 2012).

Proposition IV: Assume A1 and A2 hold. Consider the allocation induced by the optimal tax system with no minimum wage. Let denote the elasticity of low-skill labor market tightness with respect to changes in the minimum wage when after-tax allocations are fixed.

(i) If when is set at the market-level, having a binding minimum wage is optimal if .

(ii) Under the optimal binding minimum wage, the optimal marginal tax rate on employed low-skill workers is negative if

| (17) |

where , , and is (the absolute value of) the elasticity of low-skill labor market tightness with respect to changes in low-skill net-of-tax wage when the minimum wage is fixed.

Proof: See Appendix B.

The first part of the proposition provides conditions under which having a binding minimum wage on top of the optimal tax system is desirable. A binding minimum wage under optimal taxes generates three effects that are illustrated by the following hypothetical reform. Suppose the planner increases the minimum wage and simultaneously increases the net-tax on employed low-skill workers (possibly, by reducing a subsidy), to hold after-tax incomes fixed. This generates a positive fiscal gain for the planner proportional to low-skill employment. This fiscal externality is paid by employers through higher wages, so there is a mechanical decrease in profits also proportional to low-skill employment. Finally, while wages are fixed and labor supply is invariant to the change in the wage given the decrease in the subsidy, firms may have incentives to decrease vacancies. The distortion in posted vacancies generates a congestion externality that, most likely, has a negative effect on social welfare.282828On one hand, the smaller employment probabilities affect the expected utility of inframarginal low-skill workers. On the other hand, the decrease in posted vacancies generates a marginal increase in profits and a potential positive fiscal externality, since the planner has to pay the subsidy to employed low-skill workers to a small mass of individuals. If the former effect dominates, then the congestion externality decreases social welfare.

Whether the social planner wants to have a binding minimum wage depends on how these three forces balance. When the minimum wage is set at the market wage and, therefore, the policy respects the first order conditions of the firm, a marginal increase in the minimum wage is likely to have negligible effects on vacancy posting. In those cases, the marginal increase in the minimum wage mimics a one-to-one transfer from profits to the social planner. This transfer increases social welfare only if the SMWW on affected profits, , is smaller than 1. When vacancy distortions are not negligible, the fiscal externality has to compensate for both the decrease in profits and the overall effects of the congestion externality, implicitly requiring an even smaller SMWW on affected capitalists.292929Lee and Saez (2012) find that, under efficient rationing and optimal taxes, a binding minimum wage is always desirable if the SMWW on active low-skill workers is greater than 1. It is tempting to think that firms setting wages work as an analog of efficient rationing. However, firms can also adjust vacancy posting which generates the congestion externality. Formally, my model cannot be written as a particular case of Diamond and Mirrlees (1971), so I cannot apply the results on quantity controls in second-best economies proposed by Guesnerie (1981) and Guesnerie and Roberts (1984).

The condition above requires that the SMWW on affected capitalists is smaller than 1 under the optimal tax allocation. That is, incorporates the effect of the optimal corporate tax rate. If the corporate tax rate is non-distortionary, its optimal value is possibly large, making approach 1. On the contrary, if the corporate tax rate is very distortionary, its optimal value is possibly small, making approach 0 when pre-tax profits are large. Then, the corporate tax rate matters for the desirability of the minimum wage. If the distortion of the corporate tax increases with the square of the tax rate, the optimum possibly involves both a corporate tax rate and a binding minimum wage.

The second part of the proposition provides conditions under which the optimal minimum wage is complemented by tax-based transfers to employed low-skill workers such as the EITC. The condition specifies a threshold on the SMWW of active low-skill workers that depends on the effects of the EITC on labor market tightness.303030With no matching frictions, , so equation (17) is reduced to , which is the standard result on the EITC desirability in frictionless labor markets with extensive margin responses (Lee and Saez, 2012; Piketty and Saez, 2013). Since the EITC generates an increase in labor supply and wages are fixed, firms react by decreasing vacancies, thus generating a congestion externality. This effect is captured by which, as captured in the denominator, generates a market-level inefficiency that makes the critical SMWW higher: the transfer to active low-skill workers needs to be socially valuable beyond the generated distortion. Also, the congestion effect generates an increase in profits that may slack the critical SMWW because of two reasons. First, if the planner values redistribution toward firms, the increase in after-tax profits is socially valuable. Second, even if , the transfer to firms allows the social planner to enforce larger corporate tax rates by reducing its distortions on pre-tax profits.

4.2 Minimum wages and corporate tax rates under international capital mobility

The second policy application focus on the interaction between the minimum wage and the corporate tax rate. The two-sector model specified in A1 allows to tractably incorporate additional differences between affected and non-affected firms. In particular, services and manufacturing not only differ in their exposure to minimum wage workers but also their capital intensity and capital mobility. Manufacturing is more capital intensive, and its capital is presumably more internationally mobile than the one employed in services industries. This observation suggests that the behavioral response of profits to changes in corporate taxes is also likely to differ between industries.