Differentially Private Top-k Selection via Canonical Lipschitz Mechanism

Abstract

Selecting the top- highest scoring items under differential privacy (DP) is a fundamental task with many applications. This work presents three new results. First, the exponential mechanism, permute-and-flip and report-noisy-max, as well as their oneshot variants, are unified into the Lipschitz mechanism, an additive noise mechanism with a single DP-proof via a mandated Lipschitz property for the noise distribution. Second, this new generalized mechanism is paired with a canonical loss function to obtain the canonical Lipschitz mechanism, which can directly select k-subsets out of items in time. The canonical loss function assesses subsets by how many users must change for the subset to become top-. Third, this composition-free approach to subset selection improves utility guarantees by an factor compared to one-by-one selection via sequential composition, and our experiments on synthetic and real-world data indicate substantial utility improvements.

1 Introduction

Let be a set of items and be a data vector comprised of numerical scores for these items. Depending on the application domain the items can be thought of as features, policies, models, or in some cases physical objects as the term suggests. The top- selection problem seeks to select highest scoring items, i.e., . It is a fundamental problem with myriads of applications (see (Ilyas et al., 2008) for a survey) and also a building block in analytic tasks including classification, summarization, and content extraction (Wu et al., 2007; Fujiwara et al., 2013). The applications of top- selection are typically fueled by user data and thus have raised privacy concerns (Narayanan & Shmatikov, 2009). To address such concerns, it is crucial that top- selection preserves privacy. This is possible by enforcing differential privacy (DP) (Dwork et al., 2014) which, informally speaking, ensures that the selected items do not depend heavily on any single user’s private information.

A data vector is derived from some object and is influenced through the private information of a set of users . This influence is a central concept in DP, which deploys random processes (mechanisms) whose behavior is relatively similar with or without the input of a particular user. To achieve this, functions which determine the behavior of the process must have a limited sensitivity to individual users:

Definition 1.1 (sensitivity).

Let be some arbitrary domain. A function has sensitivity , if , for any and any pair of objects with Hamming distance 1 between and .

The methods proposed in this work are oblivious111While the underlying object can often be thought of as a database of user records, it may also lack a natural division into user-specific parts. For example, can contain numerical features of some video in which the individuals appear in. In this case, there are no “user records”, but one can still model each individual as a “user” who influences the numerical features . to or even . The notation conveys that, given a fixed , the function behaves like a regular function .

In practice the sensitivity of functions may be asymmetric (). Yet, for shift-invariant mechanisms (McKenna & Sheldon, 2020) one can apply a shifting trick to reduce it to a sensitivity (cf. Theorem A.15 in Appendix A.8) generalizing methods for monotonic functions (Dwork & Roth, 2013; McKenna & Sheldon, 2020) without having to resort to generalized sensitivity notions like bounded range (Durfee & Rogers, 2019).

The -DP methods translate the bounded sensitivity over the function values into a bounded sensitivity over the log-probabilities of selection options:

Definition 1.2 (-DP selection).

Let be a random variable supported over a set of possible outputs and . Reporting the value is -DP, for a given , if has sensitivity .

This ensures that if two objects and differ in the participation of at most one user, then observing provides little insight into the participation status of a user due to the bounded log-likelihood ratio of participation scenarios vs. , i.e., . Consider the well-known example of the Netflix prize dataset (Bennett & Lanning, 2007) and queries asking for top- movies/patterns, based on movie ratings and other user information. Then -DP modifies query answers to limit inferences on user data.

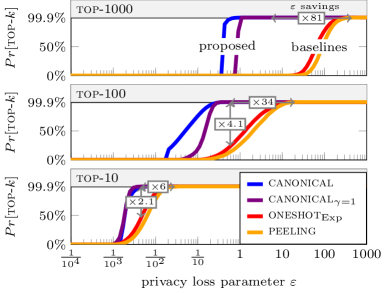

Our work considers the top- selection problem under -DP, proposing novel methods that reduce utility loss both in theory (cf. Section 5) and in practice (cf. Figure 1 for results on the Netflix prize dataset) and are amenable to simple, efficient implementations. Our main contributions are:

I. Lipschitz Mechanism.

Inspired by the report-noisy-max mechanism (Dwork & Roth, 2013), equivalences of the exponential mechanism (McSherry & Talwar, 2007) and permute-and-flip mechanism (McKenna & Sheldon, 2020) to their additive noise formulations (Durfee & Rogers, 2019; Ding et al., 2021), we sought a property that unifies them and guarantees -DP. We discovered that adding noise to each score and reporting the index of the maximal noisy score is -DP if is -Lipschitz (cf. Theorem 4.1). Hence, we call this additive noise method the Lipschitz mechanism. This mechanism instantiates many popular mechanisms and novel variants via different choices for noise distributions and parameter :

| Noise Distr. | top- with | top- with |

|---|---|---|

| Gumbel | Exp. Mechanism | peeling |

| Laplace | Report-Noisy-Max | |

| (Half-)Logistic | (new) | (new) |

| Exponential | Permute-And-Flip | (new) |

Reporting the indices of the largest utility values is also -DP ( reduces the internally) and instantiates the faster oneshot mechanisms, such as the mechanism (Qiao et al., 2021). The Lipschitz mechanism yields the first -DP proof of a oneshot variant of permute-and-flip (). Due to the versatility of the Lipschitz mechanism, we use it both to instantiate existing work, as well as new top- methods that apply the mechanism directly on the set of -subsets as the selection domain (with ).

II. Canonical Lipschitz Mechanism for top-.

Applying general selection mechanisms, such as the Lipschitz mechanism, over an exponentially large selection domain is prohibitive in cost. Thus, specialized mechanisms for suitable loss functions are needed. A natural loss function is inspired by the well-known trick that a single user can change the number of user changes needed (for a solution to become optimal) at most by one. We investigated how to deploy such a canonical loss function over the domain of -subsets, as recent works indicate strong utility guarantees for canonical functions in general (Asi & Duchi, 2020b, a; Medina & Gillenwater, 2020). Prior work on related loss functions for top- over items (Joseph et al., 2021) specialized the exponential mechanism to improve the sampling time from to . As this is still too costly for large , we develop faster methods. By plugging the canonical loss function into the Lipschitz mechanism with , we obtain the Canonical Lipschitz mechanism (canonical) and its faster variant ():

| Runtime | Prior Mechanisms | Contribution |

|---|---|---|

| naively applied mechanisms | - | |

| joint (Joseph et al., 2021) | - | |

| peeling (Durfee & Rogers, 2019) | canonical | |

| (Qiao et al., 2021) |

canonical can be sampled in and in time, both storing only a handful auxiliary values (cf., Appendix A.1). Their subset probabilities (when instantiating the exponential mechanism) can be obtained in time and space matching their sampling time complexities.

III. Composition-Free vs Sequential Composition.

Traditionally, top- has been approached by repeated -DP selections without-replacement (peeling), which is -DP via sequential composition (McSherry, 2009). We show222We consider two different forms of analysis. One is based on investigating noise terms exploiting the additive noise formulation of the Lipschitz mechanism (cf. Theorem 5.5) and the other is based on classical utility loss bounds (cf. Theorem 5.6). In both analyses, we obtain the result of an improvement by a factor for . that composition-free methods like canonical improve utility guarantees by a factor compared to peeling and our experiments on synthetic and real-world data show similarly conclusive results.

Notational conventions can be found below.

| is the natural logarithm, i.e., |

| and for |

| and for |

| for |

| for |

| for |

| are the last ’s sorted by |

| (sorting ties are broken arbitrarily) |

| mechanisms select from with privacy loss |

| hides log terms and hides normalization terms |

2 Lipschitz Mechanism for Discrete Selection

Definition 2.1 (Lipschitz Mechanism).

Let be a pair of a cumulative and an inverse distribution function for which is -Lipschitz, i.e., for any :

Let , be a data object, be the selection domain of the mechanism, and be independent for each possible output . Let for have sensitivity . Then the output of the Lipschitz mechanism is:

Each loss value is negated/rescaled and then distorted by adding noise terms generated via inverse transform sampling. Then the items with the largest noisy values are reported. The -DP proof (cf. Theorem 4.1) follows from the Lipschitz condition. This condition is for instance satisfied by the standard Laplace, Gumbel, Exponential Distribution and (Half-)Logistic distribution functions (cf. Appendix A.3).

The standard exponential distribution and satisfies the Lipschitz condition tightly (), has the smallest variance amongst the considered distributions, and consistently performed best in our experiments (cf. Figure 4 in Appendix A.2). The Laplace distribution matches the exponential distribution except that it selects a random sign i.e., absolute values are still exponentially distributed. Laplace noise tends to distort the loss values more than exponential noise due to opposing signs. The Gumbel distribution with is often used as the default to simplify the analysis and because it allows to easily derive probabilities as it instantiates the exponential mechanism and probabilities are therefore proportional to simple exponential terms. These benefits come at the price of slightly higher loss value distortion.

2.1 Lipschitz mechanism for Discrete Selection over exponentially large selection domains

Naively sampling the Lipschitz mechanism over a selection domain takes time. This is problematic if is exponentially large as is the domain of top- selection. Yet, it can be evaded if loss-values can be grouped into few classes with distinct loss-values. For large groups with the same loss value, only the group members with the largest noise values can ever be selected and each group member has the same probability to receive those noise values. Hence, it suffices to generate the largest noise values per group. This can be done efficiently using order statistics for uniform random variables, because is strictly increasing and each needed order statistic can be generated sequentially in arithmetic operations (Lurie & Hartley, 1972). In the special case of , only one noise term per group needs to be generated. Let be i.i.d. standard uniform random variables used to generate the noise terms of a group of size via inverse transform sampling. From order statistics of standard uniform variables, it follows that is distributed equally to . Thus, directly generates the maximal noise term of the group and its elements have a uniform probability of receiving this maximal noise term.

3 Canonical Lipschitz Mechanism for Top-

3.1 Canonical Loss Function

Let be some scoring function over a set of items with sensitivity . Let be all -subsets of . Let for any the utility loss be a shorthand for , where each component for .

A common loss function for many problems is to quantify how much the data object would need to change in terms of participants for a potential output to become optimal. This has been shown to offer strong utility guarantees for a large class of problems (Asi & Duchi, 2020b, a; Medina & Gillenwater, 2020). The optimality zone of a potential output is the vector space of all -dimensional vectors whose largest values are in the indices . The canonical loss function is then the distance to the nearest data vector in :

This definition of canonical loss is real-valued unlike in (Asi & Duchi, 2020b, a; Medina & Gillenwater, 2020). However, after rounding up the value can be interpreted as the number of users needed to transform into s.t. :

Lemma 3.1.

The function has sensitivity .

Proof.

The canonical loss function and has sensitivity . Thus, if is replaced with a value in , then is replaced by an integer between and . ∎

3.2 Top-

Definition 3.2 (score vector).

Let be a scoring function with sensitivity . Items are assigned scores with for . The (descending) order statistics of the components of are:

Let be indices such that:

The top- of a score vector are its -largest components:

Definition 3.3 (top-).

Let and . Then:

As releasing the top- under DP is not always possible, it is useful to identify groups of subsets that are good approximations. For this purpose, all -subsets are partitioned into disjoint utility classes based on an integer and an integer , where is only allowed if . The integer relates to the highest missing rank from the subset and is the lowest present rank in the subset:

Definition 3.4 (utility class).

The utility class is comprised of all subsets of the form with and .

Thus, each subset fully contains the top-, while the remaining items are contained in the top-. The subset can be thought of as the “head”, as the “body” and as the “tail” of a subset.

Intuitively, is the best item missing from and even the worst item in needs to overtake . The factor is due to the fact that users can both increase by and decrease by such that overtaking takes half as much effort. This can be generalized by a parameter (matching the previous definition for ):

Theorem 3.5 (top- canonical loss function).

Let .

has sensitivity for any .

Proof.

If all values of a set change at most by , then their extrema can also change at most by (see Lemma A.22 in Appendix A.8). As the values of for and the values for for change at most by , the values of and also change at most by , since and .

The term can therefore change at most by and the term can change by at most . Thus, the difference can change by at most . ∎

By plugging the function in Theorem 3.5 into the Lipschitz mechanism with and using the techniques in Section 2.1 to deal with exponentially large selection domains, we obtain the Canonical Lipschitz mechanism, which can be sampled in (cf. Theorem A.1 in Appendix A.1).

Numerical precision can be either achieved by taking computations into the log-space333 One can use from the Gumbel distribution where it simplifies to . As are binomial coefficients that can be computed via multiplications, it is trivial to take the computations into the log-space. or via special libraries.

While Theorem A.1 applies to any , the mechanism can be sampled in time for , as only each has a distinct loss value. In this case there are subsets for each loss value .

4 Differential Privacy Guarantees

All approaches considered in this work are instantiated through the Lipschitz mechanism, which only requires a distribution choice s.t. is -Lipschitz for any and the loss function to have some known sensitivity . Thus, it suffices to prove:

Theorem 4.1.

The Lipschitz mechanism from Definition 2.1 is -DP for any loss function with finite sensitivity .

Proof.

We use here the same variables as in Definition 2.1. Let be a shorthand for . Let be an arbitrary -subset of and be the items missing from . Let the loss and . Let the noisy normalized loss and .

Let . Then based on minimal and maximal component values of and the probability is equal to:

The integration variable is the -largest noisy value overall. Thus, it covers all possible events where are the -largest noisy values and all events are disjoint, differing at least in the -largest noisy value.

Let . Then replacing with maximizes a user’s impact on , due to the following properties that follow from the additive noise framework:

-

(i.)

Monotonicity: Replacing with and with maximizes a user’s impact on .

-

(ii.)

Shift-Invariance: Replacing both and with and has no effect on .

It is easy to see that (ii.) can be used to cancel out changes to in (i.) by doubling down on changes to . For , this corresponds to the claims about regular mechanisms in (McKenna & Sheldon, 2020).

As is independent of , it is only left to show that changes by at most a multiplicative factor due to a single user.

From inverse transform sampling with follows is for any equal to:

Replacing the normalized loss with replaces with . This means the noisy normalized loss is replaced with and the probability is equal to:

The -Lipschitz condition on implies for any . Thus, with the value of fluctuates at most by a multiplicative factor and fluctuates at most by a multiplicative factor due to . ∎

5 Theoretical Comparison

5.1 Comparison of Canonical for different

The subset classes have better utility for larger and smaller . The parameter governs how much canonical prioritizes against . Inversely, for small values of the mechanism improves , but neglects . By trading privacy loss for utility canonical with smaller can become as good as canonical with larger at minimizing :

Lemma 5.1 (internal superiority).

For and , -DP has superior utility to -DP , i.e., for any

Proof.

Let and (cf. Definition 3.4). Then the following holds:

Since , then and just needs to be large enough to scale to . This is achieved due to , which is implied by . ∎

Corollary 5.2.

-DP has superior utility to -DP as shown in Lemma 5.1.

5.2 Noise Analysis of Canonical vs Peeling

Let without loss of generality. For the Lipschitz mechanism with Gumbel noise, the maximum of i.i.d. standard Gumbel random variables (RVs) is distributed and the difference of two standard Gumbel RVs follows a standard Logistic RV. We seek a a specific difference that instructs how far non-top- options leap forward compared to top- ones, hence called Logistic Leap.

To obtain simpler formulas we add for canonical an additional subset with the same loss value as the previously worst one to the selection domain , which can only disadvantage canonical.

Lemma 5.3 (Canonical Logistic Leap).

Let be the selection domain with an additional (dummy) subset s.t. . Let be the subset selected by canonical with parameter . Let:

with . Then:

Proof.

Let be a matrix whose entries are independent noise terms:

Without loss of generality we can fix and then replace by as according to Corollary 5.2 this incurs no utility loss. Replacing with is equivalent to multiplying all noise terms by .

is the noise-term received by the top-, while the sub-matrix of with where are the noise-terms received by the non-top- subsets.

Let . For , we can define . The non-top- subset that receives the noise term leaps ahead of the top- subset if , but fails to overtake the top- subset if . Due to these implications, the probability inequalities in the statement hold.

With non-top- subset noise terms we get and we can then write as with . ∎

As peeling removes in each round an item and we want to simplify it, we charitably remove the item with utility , which results in the elimination of more noise terms assigned to non-top- items (helping peeling) as would occur due to the item selection:

Lemma 5.4 (Peeling Logistic Leap).

Let be subset selected by peeling from items . Let:

Then:

Proof.

Let be a matrix whose entries are independent noise terms:

For peeling, is the noise term received by the item with score in round , while is the submatrix of (depicted as right half) with where and with the bottom noise terms, i.e., noise terms of items in the bottom partition “after” the top-k. Let . For peeling, we can define . The bottom item that receives the noise term leaps ahead of top item in round if , but fails to overtake if . Similarly, if then is displaced and if the top-item is not displaced by any bottom item. The probability inequalities in the statement follow from these implications.

With bottom noise terms we get . ∎

Proof.

Since , . Then, for , we rewrite via as and . As , the claim then follows due to and . ∎

5.3 Utility Loss Bounds for Canonical vs Peeling

Based on standard utility guarantees for the exponential mechanism one can derive:

Theorem 5.6.

Let be the selected set by canonical with supposing . Let be the outputted set by peeling. Let and .

Let be the failure rate. Then with at least probability it holds that and with utility loss terms:

Also, for , it holds that .

Proof.

The proof follows from several Theorems and Lemmas in Appendix A.8. For canonical:

-

•

Lemma A.19 adopts standard theorems for the exponential mechanism to obtain general utility guarantees (instantiated by Lipschitz mechanism with from the Gumbel distribution).

- •

For peeling, Lemma A.21 plugs the score function over the items into Lemma A.19, but uses a reduced failure rate s.t. selections have a joint success rate .

Due to independence one can here use the Šidák correction for family wise error rates of hypothesis tests . As this leads to terms that complicate comparisons, is rewritten via the Bonferroni correction and a ratio between both corrections is used to restore the Šidák correction. We derive in Lemma A.18 that the Bonferroni correction is as expected a very good approximation and that which even for is smaller than such that . From that then follows the inequality for in the claim. For , and . Thus, . ∎

6 Related Work

The report-noisy-max mechanism (Dwork & Roth, 2013) adds Laplace noise to utility values and then selects the item with the maximal noisy value. Other popular mechanisms can be formulated in a similar way, i.e., by adding instead Gumbel noise (Durfee & Rogers, 2019) one gets the exponential mechanism (EM) and by adding Exponential noise (Ding et al., 2021) one gets the permute-and-flip (P&F) mechanism. In this work, we extend these results and unification efforts via the proposed Lipschitz mechanism. We model it as a single mechanism rather than a framework or family of mechanisms as the DP proof is independent of instantiations. We show that in the context of the Lipschitz mechanism asymmetric sensitivities (Dong et al., 2020) can be reduced to ordinary sensitivities, generalizing results on monotonic functions (Dwork & Roth, 2013; McKenna & Sheldon, 2020) that are treated to have sensitivity . Due to its generality, the Lipschitz mechanism also instantiates oneshot variants that select the largest noisy values (Qiao et al., 2021), e.g., the oneshot variant of P&F (McKenna & Sheldon, 2020) did not have a DP proof although it promises the best utility amongst oneshot mechanisms.

The joint EM (Joseph et al., 2021) is a mechanism that directly selects -subsets based on a loss function akin to canonical loss. Aside from the problem definition, the joint EM paper employs a loss function that counts how many users are needed to change the utility values of the subset to match the utility values of the top-. Catching up with the top- may not displace all items of the top- and instead yields a mix of top- and subset items. In contrast, the canonical loss function requires all missing top- items to be displaced by subset items, which is desirable as it requires more users (cf. Lemma A.24 in Appendix A.8). The joint EM can be sampled in time, whereas all proposed methods with the canonical loss function require only time. The authors of (Joseph et al., 2021) mention as a caveat of joint EM that it may be difficult to avoid exponentially large values in the matrix multiplications that are needed to compute loss value multiplicities. In contrast, the canonical loss value multiplicities ( from Definition 3.4) are binomial coefficients which can be computed with simple methods in the log-space to avoid large values.

Previous works did not theoretically compare direct subset selection with composition methods, but have shown that canonical loss functions offer general utility guarantees (Asi & Duchi, 2020b, a; Medina & Gillenwater, 2020) if they are plugged into the EM (Asi & Duchi, 2020a). Our motivation to generalize beyond the EM are results for P&F which show it consistently improves upon the EM (McKenna & Sheldon, 2020). Our experiments also indicate for the Lipschitz mechanism that using from the Exponential distribution leads to best utility (cf. Figure 4 in Appendix A.2). Last, there are several works (Chaudhuri et al., 2014; Carvalho et al., 2020; Cesar & Rogers, 2021) that focus on approximate DP (Dwork et al., 2014; Beimel et al., 2016), i.e, -DP with . This work focuses on pure -DP, leaving the related question open.

7 Empirical Comparison

We compared four top- mechanisms:

-

•

peeling (Durfee & Rogers, 2019) is one-by-one -DP selection without replacement via Exp. Mechanism

- •

- •

-

•

as canonical except with .

We did not compare to the Joint Exponential Mechanism (Joseph et al., 2021), due to its prohibitive cost for large . Apart from its runtime, it is in any case very similar to canonical (see Section 6). We implemented all methods in Python. More details in Section A.2 of the Appendix and on \urlhttps://github.com/shekelyan/dptopk.

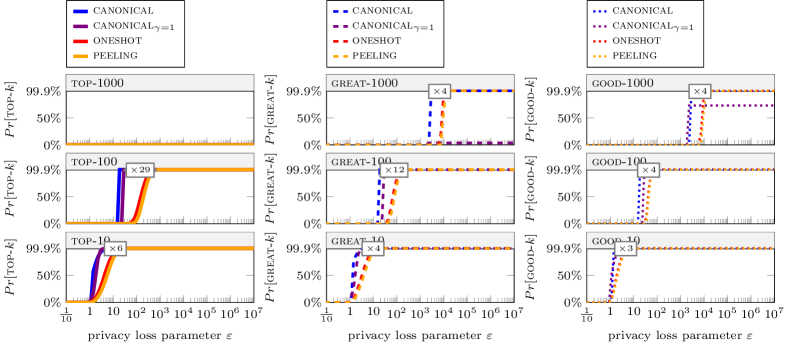

7.1 Top-: Real-World data

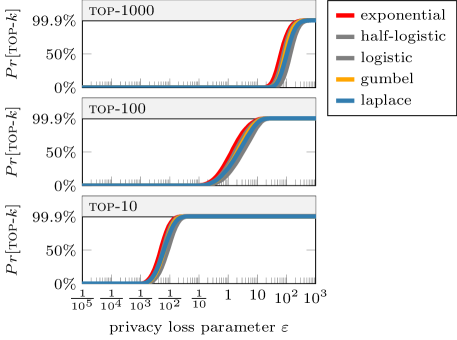

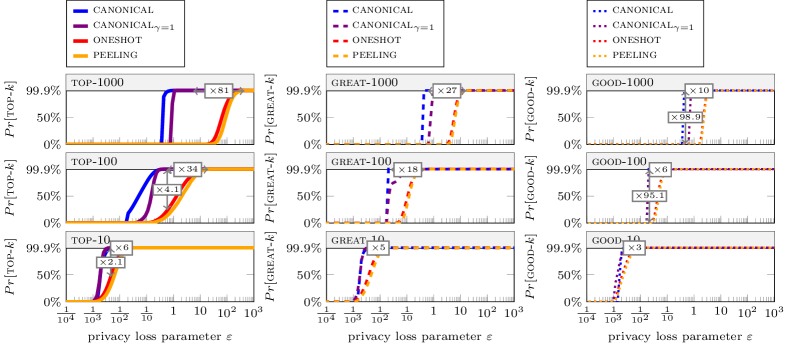

In this experiment, is based on half a million users who rated movies in the Netflix prize dataset (see Introduction) between and . Each component is equal to the number of users that gave the movie a 5/5 rating such that the sensitivity is (cf. Theorem A.15 in Appendix). As can be seen in Figure 1 the new methods canonical / almost certainly return the correct top- with a privacy budget of , whereas classical methods require an up to larger privacy budget to achieve the same feat. For , the privacy budget of our methods is smaller and for it is smaller. In the Appendix, we report similar results for five additional real-world datasets (cf. Table 1 and Figures 6,7,8,9,10). In conclusion, the new methods show vast improvements.

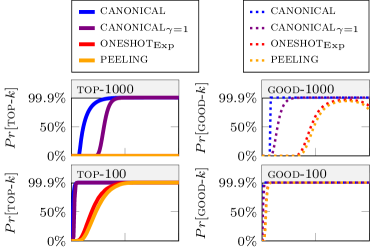

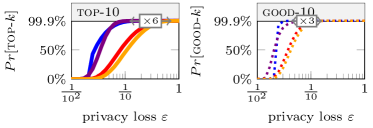

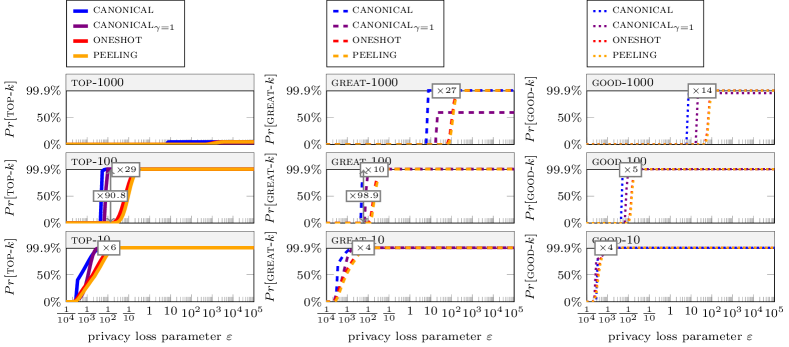

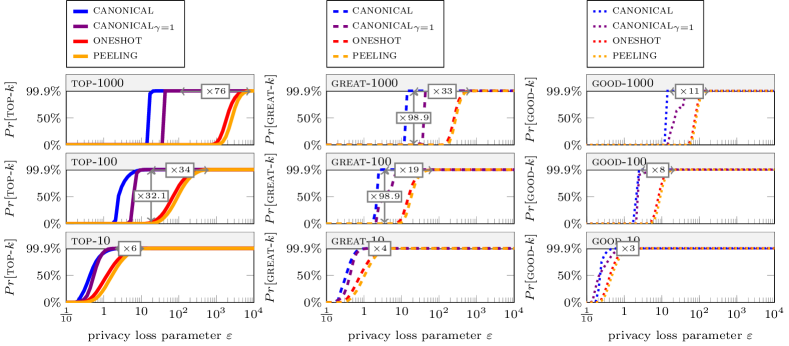

7.2 Top-: Synthetic Data

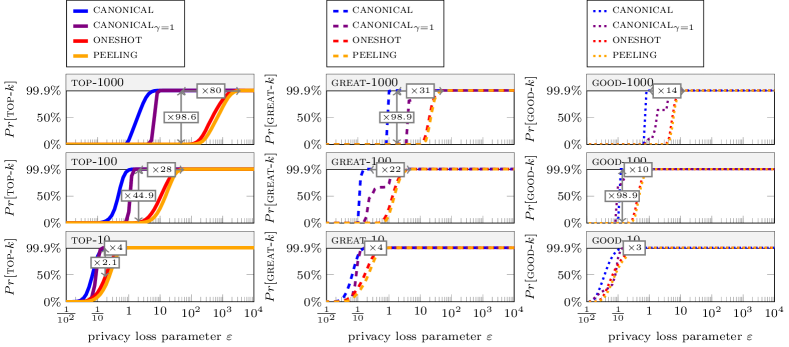

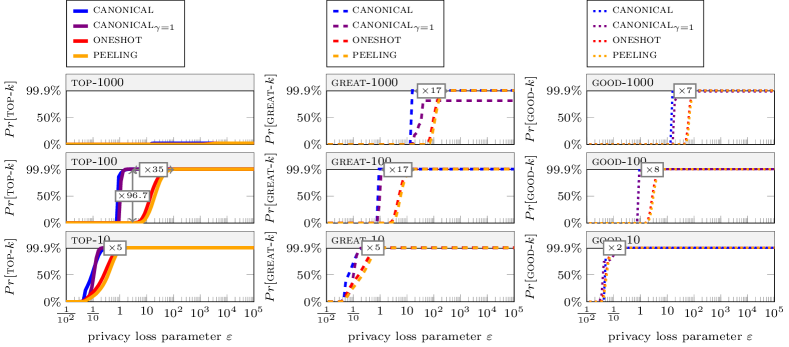

We generated with directly by Zipf’s law, i.e., and . Figure 3 shows the results for varying parameter of Zipfian distribution, which controls how challenging the distribution is; scores are uniform when . canonical and appear clearly superior to the existing mechanisms, being able to sample the top- or top- with a probability many times larger. For top-, the difference is not obvious for , but it becomes much larger for smaller (see Figure 3). Besides top-, we considered a “good”- subset as one that replaces at most half of the top- elements with elements from the top- without touching the top-, i.e., with and (cf. Definition 3.4). The new mechanisms again outperform classical ones, particularly for large and small which is more demanding, but with a smaller margin than for top-.

7.3 Runtimes

In our experiments with runtime measurements444Running on a laptop with 3.2Ghz Apple M1 processor and Python 3.99 interpreter using one single thread/core. The reported runtimes do not include sorting the data vector , which in our experiments took less than ( secs)., canonical was as fast as peeling (average s) and was as fast as oneshot (average ms). As all methods are simple, the recorded runtimes can be predicted with relative error by for methods peeling / canonical and by for methods oneshot / .

8 Discussion

We investigated three questions in this work. If it is possible to unify existing discrete selection mechanisms with an additive noise framework, if it is possible to operate selection mechanisms efficiently over subsets as an immediate selection domain, and if there are theoretical differences between approaches that select a -subset directly or independently in steps (Peeling). The Lipschitz mechanism conclusively answers the first question, the Canonical Lipschitz mechanism (canonical) is itself an affirmative answer to the second question, and our analysis shows an factor improvement of canonical (our direct approach) over Peeling when , i.e., when does not grow faster than . Experimental results also indicate clear practical benefits, i.e., being able to quickly and reliably obtain high utility subsets with a far smaller privacy budget.

Open questions include if the Lipschitz mechanism could be generalized to non-finite selection domains, if other loss functions over subsets could yield similar efficiency and utility results, and if the theoretical analysis could be extended beyond Gumbel noise, which is used to instantiate the exponential mechanism. Specifically, it appears all noise distributions perform fairly similarly. Also, it would be interesting to see if unification, efficiency, and theoretical results in the same spirit could be achieved for other differential privacy (DP) notions such as approximate DP.

References

- Asi & Duchi (2020a) Asi, H. and Duchi, J. C. Instance-optimality in differential privacy via approximate inverse sensitivity mechanisms. Advances in Neural Information Processing Systems, 33, 2020a.

- Asi & Duchi (2020b) Asi, H. and Duchi, J. C. Near instance-optimality in differential privacy. arXiv preprint arXiv:2005.10630, 2020b.

- Balog et al. (2017) Balog, M., Tripuraneni, N., Ghahramani, Z., and Weller, A. Lost relatives of the gumbel trick. In ICML, pp. 371–379, 2017.

- Beimel et al. (2016) Beimel, A., Nissim, K., and Stemmer, U. Private learning and sanitization: Pure vs. approximate differential privacy. Theory Comput., 12(1):1–61, 2016. doi: 10.4086/toc.2016.v012a001. URL \urlhttps://doi.org/10.4086/toc.2016.v012a001.

- Bennett & Lanning (2007) Bennett, J. and Lanning, S. The netflix prize. In In KDD Cup and Workshop in conjunction with KDD, 2007.

- Carvalho et al. (2020) Carvalho, R. S., Wang, K., Gondara, L., and Miao, C. Differentially private top-k selection via stability on unknown domain. In UAI, volume 124, pp. 1109–1118, 2020.

- Cesar & Rogers (2021) Cesar, M. and Rogers, R. Bounding, concentrating, and truncating: Unifying privacy loss composition for data analytics. In Algorithmic Learning Theory, pp. 421–457. PMLR, 2021.

- Chaudhuri et al. (2014) Chaudhuri, K., Hsu, D., and Song, S. The large margin mechanism for differentially private maximization. In NIPS, pp. 1287–1295, 2014.

- Ding et al. (2021) Ding, Z., Kifer, D., Steinke, T., Wang, Y., Xiao, Y., Zhang, D., et al. The permute-and-flip mechanism is identical to report-noisy-max with exponential noise. arXiv preprint arXiv:2105.07260, 2021. \urlhttps://arxiv.org/pdf/2105.07260.pdf.

- Dong et al. (2020) Dong, J., Durfee, D., and Rogers, R. Optimal differential privacy composition for exponential mechanisms. In International Conference on Machine Learning, pp. 2597–2606. PMLR, 2020.

- Durfee & Rogers (2019) Durfee, D. and Rogers, R. Practical differentially private top-k selection with pay-what-you-get composition. In Proceedings of the 33rd International Conference on Neural Information Processing Systems, pp. 3532–3542, 2019.

- Dwork & Roth (2013) Dwork, C. and Roth, A. The algorithmic foundations of differential privacy. Theoretical Computer Science, 9(3-4):1–277, 2013. \urlhttps://projects.iq.harvard.edu/files/privacytools/files/the_algorithmic_foundations_of_differential_privacy_1.pdf.

- Dwork et al. (2014) Dwork, C., Roth, A., et al. The algorithmic foundations of differential privacy. Found. Trends Theor. Comput. Sci., 9(3-4):211–407, 2014.

- Fujiwara et al. (2013) Fujiwara, Y., Nakatsuji, M., Shiokawa, H., Mishima, T., and Onizuka, M. Fast and exact top-k algorithm for pagerank. In AAAI, 2013.

- Ilyas et al. (2008) Ilyas, I. F., Beskales, G., and Soliman, M. A. A survey of top-k query processing techniques in relational database systems. ACM Comput. Surv., 40(4), October 2008. ISSN 0360-0300. doi: 10.1145/1391729.1391730. URL \urlhttps://doi.org/10.1145/1391729.1391730.

- Joseph et al. (2021) Joseph, M., Gillenwater, J., Ribero, M., et al. A joint exponential mechanism for differentially private top-k set. In NeurIPS 2021 Workshop Privacy in Machine Learning, 2021.

- Lurie & Hartley (1972) Lurie, D. and Hartley, H. Machine-generation of order statistics for monte carlo computations. The American Statistician, 26(1):26–27, 1972.

- McKenna & Sheldon (2020) McKenna, R. and Sheldon, D. R. Permute-and-flip: A new mechanism for differentially private selection. NeurIPS, 33, 2020.

- McSherry & Talwar (2007) McSherry, F. and Talwar, K. Mechanism design via differential privacy. In FOCS, pp. 94–103, 2007.

- McSherry (2009) McSherry, F. D. Privacy integrated queries: an extensible platform for privacy-preserving data analysis. In Proceedings of the 2009 ACM SIGMOD International Conference on Management of data, pp. 19–30, 2009.

- Medina & Gillenwater (2020) Medina, A. M. and Gillenwater, J. Duff: A dataset-distance-based utility function family for the exponential mechanism. arXiv preprint arXiv:2010.04235, 2020.

- Narayanan & Shmatikov (2009) Narayanan, A. and Shmatikov, V. De-anonymizing social networks. In S&P 2009, pp. 173–187, 2009.

- Qiao et al. (2021) Qiao, G., Su, W., and Zhang, L. Oneshot differentially private top-k selection. In Meila, M. and Zhang, T. (eds.), Proceedings of the 38th International Conference on Machine Learning, volume 139 of Proceedings of Machine Learning Research, pp. 8672–8681. PMLR, 18–24 Jul 2021. URL \urlhttps://proceedings.mlr.press/v139/qiao21b.html.

- Wu et al. (2007) Wu, X., Kumar, V., Ross Quinlan, J., Ghosh, J., Yang, Q., Motoda, H., McLachlan, G. J., Ng, A., Liu, B., Yu, P. S., Zhou, Z.-H., Steinbach, M., Hand, D. J., and Steinberg, D. Top 10 algorithms in data mining. Knowl. Inf. Syst., 14(1):1–37, December 2007. ISSN 0219-1377. doi: 10.1007/s10115-007-0114-2. URL \urlhttps://doi.org/10.1007/s10115-007-0114-2.

Appendix A Appendix

A.1 Implementation

Theorem A.1.

The Canonical Lipschitz Mechanism for top- can be sampled in time for pre-sorted scores.

Proof.

The mechanism releases a subset from class (cf. Definition 3.4) with equal to:

with and for .

The binomial coefficients for each can be computed in by starting with and and decreasing until . In each step, decreases by and can be used to update the binomial coefficient. The number of subsets in each class is equal to the distinct number of possibilities for the body , which is equal to the number of -subsets out of items (counted as if ). All subsets in the class from Definition 3.4 have the same loss value. As the time complexity of implementations hinges upon the distinct number of loss values, one can see that there is the class with the top- and otherwise and . Thus, the total number of classes is

. ∎

The time can be reduced to for as only each has a distinct loss value. In this case which can be also computed via time updates by considering that for :

When instantiating the exponential mechanism, subset probabilities . For sampling large numbers can be avoided by taking into the logspace:

Lemma A.2.

Let , then

Proof.

∎

A.2 Replicability and Additional Experimental Results

Datasets are described in Table 1. The sensitivities of all featured (count-based) datasets are presumed to be via the shifting trick (cf. Theorem A.15).

We aggregate classes from Definition 3.4 into high utility predicates:

The predicate mandates to be the exact top-. The predicate mandates for the inclusion of the top- and exclusion of of items outside of top-. For this means inclusion of all top- items and the remaining items must come from top-. The predicate mandates for the inclusion of the top- and exclusion of items outside of top-.

Workflow of how each plot (with in -axis) is generated:

-

•

The vector is fixed for one of the datasets and given as input to all mechanisms.

-

•

The subset size is fixed

-

•

The privacy loss is then varied with sufficient precision for plotting purposes

-

•

For each data point either the probability distribution over is computed (canonical, or probabilities are estimated via Monte Carlo methods (using ideas from Section 2.1) with generated subset classes (). Additionally, a subset is sampled for runtime measurements and validation purposes.

- •

Implementation details:

The inverse distribution function used in the approaches (always standard distribution parameters):

| Approach | Distribution | |

|---|---|---|

| Exponential | ||

| peeling | Gumbel | |

| canonical | Gumbel | |

| Gumbel |

Additional plots:

-

•

Figure 4 compares the Lipschitz mechanism with for different choices of .

- •

-

•

Figures 6, 7, 8, 9, 10 replicate results from the paper for five additional datasets. Some datasets lack a sufficient number of users to reach good utility with any -DP methods with . In some rare instances the top- can be one out of many arbitrary subsets (we break ties arbitrarily for top-), because we do not modify to break ties between uniform values.

| Dataset | Size | Description (of data from which is extracted) |

|---|---|---|

| netflix | 17770 | Netflix movie ratings (we count how many users gave each movie a 5/5 rating) |

| patent | 4096 | Citation network among a subset of US patents |

| searchlogs | 4096 | Query logs for query “Obama” issued from Jan. 1, 2004 to Aug. 9, 2009. |

| medcost | 4096 | Personal medical expenses based on a national home and hospice care survey |

| income | 4096 | “Personal Income” attribute of the IPUMS American community survey data |

| hepth | 4096 | Citation network among high energy physics pre-prints on arXiv |

| Top- selection with | Top- oneshot selection with |

|---|---|

|

|

A.3 The Lipschitz Mechanism: Overview

The standard Exponential, Gumbel, Laplace, Logistic and Half-Logistic distribution are examples of distributions that satisfy the Lipschitz property mandated in the Lipschitz mechanism:

-

•

Theorem A.3: The standard Exponential distribution with for , for and for satisfies the Lipschitz condition from the Lipschitz mechanism.

-

•

Theorem A.6: The standard Gumbel distribution with for and for satisfies the Lipschitz condition from the Lipschitz mechanism.

-

•

Theorem A.11: The standard Laplace distribution with for and for and for satisfies the Lipschitz condition from the Lipschitz mechanism.

-

•

Theorem A.12: The standard Half-Logistic distribution with for and for and for satisfies the Lipschitz condition from the Lipschitz mechanism.

-

•

Theorem A.13: The standard Logistic distribution with for and for satisfies the Lipschitz condition from the Lipschitz mechanism.

For some of these distributions the Lipschitz instantiates popular mechanisms from the literature:

- •

- •

- •

A.4 Exponential Lipschitz Mechanism: Permute-And-Flip Mechanism

The Lipschitz mechanism is -DP when adding exponentially distributed noise:

Theorem A.3 (Lipschitz condition: Exponential distribution).

Let and .

Then .

Proof.

From the last equality we obtain:

∎

The Lipschitz condition follows for if it is met for :

Lemma A.4.

Let be a strictly increasing function.

If for , then for follows:

Proof.

case : As is strictly increasing it follows that . Also, from the statement we know that for . Thus, , which implies

case : Let and .

from which we obtain

and

∎

The Lipschitz mechanism with instantiates the Permute-And-Flip mechanism (McKenna & Sheldon, 2020) when adding exponentially distributed noise (confirming the results of (Ding et al., 2021)):

Theorem A.5 (Permute-and-Flip via Exponential Noise).

If then matches the Permute-and-Flip mechanism.

Proof.

Let for a loss function with sensitivity .

This means for each a (uniform) random number between and is drawn and the smallest is selected. Let . Then any will be certainly rejected and all non-rejected ones have the same probability of being the smallest. Let be the number of accepted elements, such that is a Poisson Binomial random variable where each summation term is a Bernoulli random variable with success probability . Then . The rejection probability is then:

Selecting a random non-rejected item is equivalent to selecting the first non-rejected item if items are in a random order. This matches Permute-and-Flip, which goes through items in random order, rejects each item with probability and then selects the first item that does not get rejected.

∎

A.5 Gumbel Lipschitz Mechanism: Exponential Mechanism

The Lipschitz mechanism is -DP when adding Gumbel distributed noise terms :

Theorem A.6 (Lipschitz condition: Gumbel distribution).

Let and . Then:

Proof.

Due to Lemma A.4 one can presume without loss of generality that .

Let and , then from Lemma A.18 follows that:

The claim follows due to Lemma A.4.

∎

The Lipschitz mechanism with instantiates the Exponential Mechanism (McSherry & Talwar, 2007) when adding the Gumbel distributed noise terms (for it matches the Peeling technique using the Exponential Mechanism (Durfee & Rogers, 2019)):

Theorem A.7 (Exponential Mechanism via Gumbel trick).

If for the Lipschitz mechanism with , then .

Proof.

Let be the selection domain and for any . Then:

Each term is then an exponential random variable with rate and . A proof for this property can be found in the following Lemma A.8.

∎

For independent events with exponentially distributed time delays, each event’s probability of preceding the others is proportional to their rate. This well-known property has for instance been used to prove the Gumbel Trick (Balog et al., 2017):

Lemma A.8 (Exponential clocks).

Let be i.i.d. and be a finite set. Let supported over . Then .

Proof.

Let .

As this is how one would generate an exponential random variable with rate , it follows that the density , cumulative and complementary cumulative . The probability from the claim can then be written as:

The last equality follows from for any with . Let and . Then . Hence, .

∎

A.6 Laplace Lipschitz Mechanism: Report Noisy Max Mechanism

Theorem A.9.

As the Lipschitz condition limits how fast a distribution function can change, satisfying the Lipschitz condition is inherited by doubled/mirrored distribution:

Lemma A.10.

Let be a strictly increasing function that satisfies the Lipschitz condition .

Let .

Then also satisfies the Lipschitz condition

.

Proof.

Due to Lemma A.4 one can presume without loss of generality that .

Case (which implies ) where :

The latter implies

Furthermore, for , is strictly increasing. Thus, and satisfies the Lipschitz condition.

Case and where .

In the second step it is exploited that adding the same positive value to numerator and denominator can only move the ratio closer to (see Lemma A.16).

Case and :

In this case is strictly increasing, whereas is strictly decreasing with . Thus, the ratio cannot be larger than for the cases or that have already been covered. ∎

The Lipschitz mechanism is -DP when adding Laplace distributed noise:

Theorem A.11 (Lipschitz condition: Laplace distribution).

Let and .

Let .

Then .

A.7 Logistic Lipschitz Mechanism

The Lipschitz mechanism is -DP when adding Halflogistic distributed noise:

Theorem A.12 (Lipschitz condition: Halflogistic distribution).

Let and . Then .

Proof.

The additive term in numerator and denominator only moves the ratio closer to (see Lemma A.16). As is the distribution function of the exponential distribution, the claim then follows via Theorem A.3.

∎

Theorem A.13 (Lipschitz condition: Logistic distribution).

Let and . Then .

A.8 Additional Theorems and Proofs

Lemma A.14 (canonical loss function).

Let be some discrete-valued output domain, and comprise any score vectors s.t. , where is the optimal -subset. Let have sensitivity .

Then the function loss defined in the following has sensitivity :

Proof.

Let . In the following, is used as a shorthand for the subspace with .

As for , a single user can change each component of by at most . If is replaced by then each term is replaced by . Based on the definition of the norm, it then follows that .

Then the values for different form a set over which a minimum is taken. If all values of a set change by at most , then their extrema also change at most by (see Lemma A.22 in supplementary material). Hence the sensitivity of is equal to .

∎

In the context of shift-invariant selection mechanisms, one can apply the following shifting trick to obtain a reduced sensitivity analysis for counting-based functions and alike:

Theorem A.15 (asymmetric sensitivity).

Let with and .

Let , and and for any . Then the function has sensitivity .

Proof.

By definition . Thus, for any it holds that and . ∎

For positive reals the ratio of is smaller than , because and are closer to each other than and :

Lemma A.16.

Let be positive reals with . Then:

Proof.

Assume that . Thus, we get , , and which contradicts in the statement. Thus, . From , we get and thus . Therefore, we obtain

. ∎

Lemma A.17.

Let with and . Then:

Proof.

A variant of Bernoulli’s inequality is for any reals and . Due to , one can pick to obtain .

Then for any is a well-known inequality due to the following. The derivative of with respect to is and as for . Thus, for the function is increasing and base case . The rest follows from which is a well-known identity that offers one way to define the exponential function. It follows a simple proof using L’Hôpital’s rule:

∎

Lemma A.18.

Let . Then:

which follows that for (and for ).

Proof.

This relates to Bonferroni and Šidák corrections for family-wise error rates (FWER) in hypothesis testing. The Šidák correction is exact in case of independence, i.e., , whereas the Bonferroni correction is in that case conservative, i.e., (the success rate is unnecessarily large). This also means and their ratio . According to Lemma A.17 for with it holds that . Thus, we can set to obtain:

Clearly, . And we know . Therefore by inserting we get . Thus, we can continue with:

The rest follows from being strictly decreasing. ∎

Lemma A.19 (EM utility guarantees).

Let be the selection domain, and be the sensitivity of the loss function .

Then iff is a random variable supported over with , then with probability it holds that with:

where opt are all selection options with minimal loss.

Proof.

Let . Theorem 3.11 in (Dwork & Roth, 2013)):

With probability :

Let , then with probability :

∎

Lemma A.20 (canonical utility loss bounds).

Let be the selected set by canonical with and from the Gumbel distribution with tail item . With at least probability :

Proof.

For it follows directly that the loss value of each subset is , that the optimal loss is and the logarithm of the domain size is with . Due to Corollary 5.2 for the privacy loss must simply be replaced with . ∎

Lemma A.21 (peeling utility loss bounds).

Let be the selected set by peeling with . Let . Then with probability :

Proof.

Each selection has and . Let . If each of the selections satisfies with probability , then all items satisfy with probability , which includes the tail item . By replacing in with one then obtains the claim. ∎

Lemma A.22.

Let and be a shorthand for the interval . Let . Then if , it holds that:

Proof.

Follows from and analogously .

∎

Lemma A.23 (top- canonical loss function).

Let be a -subset of .

Proof.

If , then and .

If , then from follows that , but the top- item . In order for to become optimal all of its items need to catch up with the missing top- item . The tail item has the largest gap to . Let be the gap between and ’s tail that must become for to become an optimal solution.

Let with .

Let , which increases any with by and decreases all others by . Through algebraic reformulations one gets .

Then for .

Due to the definition of the norm , because and . Hence one gets:

∎

Lemma A.24.

Let with . Let and . Let and for . Let be indices sorted by and be indices sorted by such that :

Let for any and for any . Let for any and be defined as in Definition 3.4, which implies and . Let:

Let be a -dimensional vector space where the indices have the largest values of each vector (allowing for ties), then:

(i) :

(ii) :

Proof.

Claim (i) follows directly from Lemma A.23 where canonical is matches the subset loss function . Claim (ii) follows from the following example.

Let and . As the index is missing from , each vector cannot have a larger value for the component with index than for the component with index , i.e., . Then:

Intuitively, is the maximal change to the scores to make them as good as , i.e., is not worse than . It does not match , because raising in all components of by and decreasing all others by will not produce a vector in , because is still larger than and that index is not featured in . In contrast, is not larger than . ∎

The function joint matches the right-hand-side of the equation in Lemma 5 of (Joseph et al., 2021). The factors in the proof are due to the norm, i.e., cannot only have larger values than for indices contained in , but also smaller values for indices missing from . This corresponds to users being able to both raise and lower all scores by the sensitivity value (cf. Definition 1.1), which for count-based functions can be halved in the context of selection mechanisms (cf. Theorem A.15).