When do you Stop Supporting your Bankrupt Subsidiary? A Systemic Risk Perspective

Abstract

We consider a network of bank holdings, where every holding has two subsidiaries of different types. A subsidiary can trade with another holding’s subsidiary of the same type. Holdings support their subsidiaries up to a certain level when they would otherwise fail to honor their financial obligations. We investigate the spread of contagion in this banking network when the number of bank holdings is large, and find the final number of defaulted subsidiaries under different rules for the holding support. We also consider resilience of this multilayered network to small shocks. Our work sheds light onto the role that holding structures can play in the amplification of financial stress. We find that depending on the capitalization of the network, a holding structure can be beneficial as compared to smaller separated entities. In other instances it can be harmful and actually increase contagion. We illustrate our results in a numerical case study and also determine the optimal level of holding support from a regulator perspective.

Keywords: systemic risk, financial contagion, holdings, multilayered networks

1 Introduction

At first, financial risk was managed at an individual firm level, and has been considered on a bilateral basis. However, after the financial crisis of 2007-2009, we have gained the understanding that this risk can spread akin to a virus through the entire banking system. And similar to a virus, the risk increases the more nodes succumb to the shock. This phenomenon is known as systemic risk – the risk that a (small) shock that hits the system spreads throughout the system to a degree that it endangers the entire system. This spread is also referred to as financial contagion. There are two distinct ways for this risk to spread – through local connections (for example when one bank cannot honor its obligations to another), and through global connection (for example when asset prices are impacted, as a result of liquidations). This paper will focus on the contagion spread through local connections.

One of the first papers on the spread of contagion through local connections is Eisenberg and Noe, (2001); which finds a clearing equilibrium payment in a network of banks connected by liabilities. Numerous generalizations and follow up studies include e.g., Anand et al., (2015); Halaj and Kok, (2015); Boss et al., (2004); Elsinger et al., (2013); Upper, (2011); Gai et al., (2011); Bardoscia et al., (2017). Generalizations such as fire sales and bankruptcy costs have been considered in Elsinger, (2009); Rogers and Veraart, (2013); Elliott et al., (2014); Glasserman and Young, (2015); Weber and Weske, (2017); Capponi et al., (2016); Elsinger, (2009); Elliott et al., (2014); Weber and Weske, (2017); Gouriéroux et al., (2012); Cifuentes et al., (2005); Nier et al., (2007); Arinaminpathy et al., (2012); Amini et al., (2013); Chen et al., (2016); Weber and Weske, (2017); Amini et al., 2016b ; Bichuch and Feinstein, (2019, 2022)). We also refer to, e.g., Weber and Weske, (2017); Staum, (2013); Hüser, (2015) for additional review of this literature.

Another stream of literature considers contagion effects in random networks (Gai and Kapadia, (2010); Amini et al., 2016a ; Detering et al., (2019, 2020), and Detering et al., (2021) for an extension incorporating fire sales). In these papers, asymptotic methods (as the number of banks increases to infinity) are facilitated to determine the final damage to the system after some initial shock hits some banks. From the perspective of random graph theory, the results on contagion in random networks link to a process called bootstrap percolation. This is a process which models the spread of some activity or infection within a graph via its edges. It has been analysed for Erdos-Rényi random graphs Janson et al., (2012) and random regular graphs Balogh and Pittel, (2007), and these results have later been extended to inhomogeneous graph in Amini and Fountoulakis, (2014); Amini et al., (2014); Detering et al., (2019).

Notably, in all these models the banks in the network have always been thought as an indivisible atom. In other words, the entire bank must be in one state only (e.g. bankrupt or solvent). In reality this is not the case. First, big international banks are usually big holding companies, with dozens if not hundreds of subsidiaries, that are divided by business lines and locations (e.g. JPMorgan Chase111https://www.sec.gov/Archives/edgar/data/19617/000119312508043536/dex211.htm and AIG222https://www.sec.gov/Archives/edgar/data/5272/000110465920023889/exhibit21.htm). Second, a financial loss—possibly amplified through contagion—does not necessarily affect the entire bank (at least not immediately), but often starts with one (or more) of its subsidiaries (see e.g. the classical example of AIG in Lewis, (2010)). The contagion then can spread both between subsidiaries of different banks (e.g. through local connections), and between different subsidiaries of the same bank (e.g. through the holding).

For corporations, becoming a holding with subsidiaries has several advantages: It allows corporations to defer taxable business income and use these earnings for other business opportunities or, by channeling income to low tax countries, reduce taxes altogether. In other instances, it allows them to limit the spillover risk if one business line is in trouble. In this case, the holding acts as a pure shareholder and enjoys limited liability. Often bank holdings naturally divide into subsidiaries based on location (i.e. Europe, US) and/or business lines (i.e. broker-dealers, commercial bank, insurance, asset management). The precise judicial setup differs across different countries but two main types of subsidiaries are prevalent:

-

•

Type A: The holding acts as an asset holder with full liability for the business activity of its subsidiary. This setup is usually accompanied by a profit transfer agreement ensuring fiscal unity. It is common in Europe; and is becoming more common in the US333https://www.fdic.gov/regulations/reform/resplans/plans/boa-165-2107.pdf,444https://www.federalreserve.gov/econres/notes/feds-notes/foreign-banks-asset-reallocation-intermediate-holding-company-rule-of-2016-20210512.htm. For the holding this structure has the advantage that profits from the subsidiary are often collected on a pretax basis and can be netted with losses from other subsidiaries or the holding. For creditors of the subsidiary, an obvious advantage is that holdings support their subsidiaries, and cover some of their losses.

-

•

Type B: The holding acts as a shareholder of its subsidiaries with limited liability. This is the standard holding structure in the US555https://www.wsj.com/articles/paul-kupiec-and-peter-wallison-the-fdics-bank-holding-company-heist-1419292997. From a risk perspective this holding structure is beneficial for the holdings, as the default of a subsidiary does not directly impact other business lines of the same holding. It might promote greater risk taking, because losses not covered by equity are immediately beared by other market participants, and not by the holding first.

While for the corporations themselves, the advantages are imminent, whether holdings are beneficial from a society perspective is less clear. In particular it is not well understood how shocks propagate in a network of bank holdings and what influence the holding structure has on the contagion process.

In this paper we address this important research question and try to understand the influence of the holding structures on the propagation of shocks through the financial system. We are particularly interested in the effect that support of the holding for its stressed subsidiary has on contagion. Holdings might support their subsidiaries beyond their financial liability for several reasons. For example they might fear the reputation cost of a bankrupt subsidiary, or the threat of a possible change in credit rating if a subsidiary defaults. In other cases, the holding might support its subsidiary because it still believes in its business model, and considers the solvency problems to be of temporary nature. We assume that all holdings will support their subsidiaries up to the same fixed capital , and we also allow for full support (). We consider two holding types which mimic the situation and described above. Depending on the holding type, the financial support of the holding for one subsidiary has different implications for the holdings other subsidiary.

We pursue our analysis in a random network setup which raises also some interesting new theoretical challenges. From a technical perspective our model setup provides a first instance of a multilayered random network in which contagion spreads through different channels and where interactions between layers is through the nodes. This complicates the analysis compared to a one layer network as the state of the nodes is not determined by a one dimensional quantity, but rather lies in a multidimensional domain. Our analysis includes a multi-layer analog to the classical bootstrap percolation process mentioned above.

We perform our analysis in a simple toy model. For this we consider a network of banks. Every bank has two subsidiaries, which we refer to as subsidiary and . We assume that subsidiaries only trade with subsidiaries of the same kind, i.e. subsidiary of one bank might trade with subsidiary of another bank but not with its subsidiary . The capital of the holding is the sum of the capitals of the subsidiaries, because the holding itself is not involved in any business activity. We then consider a contagion process that is triggered by a financial shock and then propagates throughout the network according to the following rules:

-

1.

If a subsidiary has exposure to a newly defaulted subsidiary of another holding, then its capital is reduced by this exposure.

-

2.

A subsidiary defaults as soon as:

-

•

Its capital has reached the maximal holding support level or,

-

•

Its capital is greater than , but the holding has not enough capital to support it. For holding structure of type this means that the subsidiary’s capital is non-positive. Whereas, for holding structure of type this means that the capital of the entire holding is non-positive, and both subsidiaries will default.

-

•

-

3.

For holding structure of type any support for a stressed subsidiary negatively affects the holding’s other subsidiary. For holdings of type , the support does not affect its other subsidiary.

All holdings will support their subsidiaries up to the same fixed level , when possible. For type holdings, the support for a subsidiary in distress has to come directly from the other subsidiary of the same holding. It can be thought of the holding reallocating capital from the healthy subsidiary to the other distressed subsidiary. For holding structures of type , the support for a troubled subsidiary does not change the capital of the other subsidiary. Instead, this support can be thought of as coming from a borrowing transaction of the holding against the capital of the healthy subsidiary. In any case, the holding supports its subsidiaries up to the level if possible and gives up on them when faced with substantial losses larger than . For holdings of type , limiting the loss from a stressed subsidiary at is only possible by either selling this subsidiary or by offloading the assets of this subsidiary into a bad bank construction. As mentioned already, our results also cover the case of full liability.

We investigate the above described contagion mechanism in a banking network where the number of banks is large and, under both holding types and , we find the final number of defaulted type and type subsidiaries at the end of the cascade. We further investigate resilience of this multilayered network to small shocks. We find that depending on the capitalization of the network the holding structure can be beneficial as compared to smaller separated entities. This is because the holding is able to support a distressed subsidiary with capital from a subsidiary that is better off, therefore reducing the probability of default of the distressed subsidiary. However, if this support goes too far, it can actually amplify the spread of contagion because healthy parts of the network get weakened and trigger new rounds of feedback effects. In a numerical case study we determine the optimal support level from a regulator perspective.

The paper is structured as follows: In Section 2 we state our model and our main result regarding the final number of defaulted subsidiaries of different types. In Section 3 we derive results that allow us to classify networks according to their resilience to small shocks. We give an example of a system in which the default of one subsidiary immediately triggers the default of the holding’s second subsidiary. Still this system is more resilient than its fully separated counterpart due to the fact that the default of both subsidiaries can be slightly deferred with some holding support. Section 4 contains our numerical case study in which we also determine the optimal holding support. We summarize our results in Section 5. All proofs are in Section 6.

2 Model and main result

We consider a network of banks and label each bank by an index . Each bank is structured as a holding with two subsidiaries of different type and . We denote the type subsidiary of bank by and the type subsidiary of bank by . We denote the set of type subsidiaries by and the set of type subsidiaries by . We assume that subsidiaries only trade with subsidiaries of the same type, i.e. subsidiary of type 1 of bank might trade with subsidiary of type of another bank but not with subsidiary of type . The type can for example originate from a business line (e.g. fixed income or equities), or from a location (e.g. US and Europe). The assumption then implies that there is no cross trading between subsidiaries of different types, and linkage is only through the holdings. We consider a network that describes these trading activities. In this toy model we assume that every loan is of equal unit size . For this let denote the exposure of subsidiary of bank towards subsidiary of bank . We then build a network by drawing a directed link from subsidiary of bank to subsidiary of bank if . We do not allow for self loops and multiple edges.

We denote by and the capital of subsidiary and of bank . The total capital of the bank is then equal to . This is the initial capital structure of each bank holding. As mentioned in the introduction already, in this paper we consider two types of holding structure. Type A that mimics the situation where the holding acts as an asset holder of the assets of its subsidiary and type B where the holding acts as a shareholder of its subsidiary. We assume in the following that all holdings are of the same type, either all of type or all of type . Our results could however easily be extended to networks that consist of type and type holdings. In what follows, several quantities that are introduced depend on , but in order to lighten the notation we make this dependency only specific when necessary.

We assume that some subsidiaries are in default, i.e. the set is not empty, where

Let be a global support level. A subsidiary of bank is in default if either its capital is less than or, despite being larger then , the capital structure of the holding, expressed by , is such that subsidiary defaults. For holding structure this is the case if the subsidiary has defaulted () and the holding has no capital to support it (). For holding structure due to the joint liability this can even be the case if the subsidiary would be solvent by itself () but due to distress of the other subsidiary the total holding capital is negative (). However, if , then even for type , subsidiary can only default if , because we assume that a holding gives up on its subsidiary if the subsidiary reaches a capital of which in turn limits the negative impact on the supporting subsidiary.

The initial defaults in now trigger a cascade that then evolves in generations or rounds. In each round, the contagion expands, because a defaulted subsidiary causes a loss of to every subsidiary it traded with and therefore reduces their capital by . We denote by and the capital of subsidiary and of bank in round , and set . In round , the total capital of the bank is then equal to .

Following above considerations, for bank with capital structure , subsidiary is in default in round if one of the following conditions hold:

-

•

.

-

•

For a holding structure of type : and .

For a holding structure of type : and .

If subsidiary of bank defaults in round , then for all unless subsidiary had already defaulted. Updating the capitals of all subsidiaries ends the round and the next round then starts.

In round , the set of banks with defaulted type subsidiary is denoted by

| (1) |

and denotes the set of all defaulted subsidiaries at step . This then leads to the two cascades

where both cascade processes are strongly coupled through the holdings. The cascade of all subsidiaries is given by

This cascade stops after at most iterations and we denote by the final sets of defaulted subsidiaries for . Such a process is exemplified for a small network with and support level in Figure 1.

In the following we want to determine in a random network setting. For this let us first stress that when a holding supports a subsidiary that has a non-positive capital, we formalize this support not by actually increasing the capital of the supported subsidiary in order to lift it above , but by reducing the threshold at which it defaults by . Similarly in case of the holding type , the support for one subsidiary does not reduce the other subsidiary’s capital but instead increases the level at which the other subsidiary defaults to above zero. While both descriptions are equivalent and lead to the same defaulted subsidiaries, actually changing the capital to formalize the holding support is less convenient for the mathematical analysis. In fact, our approach of changing the default level has the advantage that in order to determine whether a subsidiary of a holding with capital structure has defaulted, one simply needs to check whether is in some subset of . This subset is the default region and it differs for types and . We shall specify the default regions now.

For simplicity we assume that all capitals are bounded by , and because a subsidiary defaults always when the capital is less or equal than , we do not need to consider any capitals less than . We therefore define as the domain for the holding capital. Above consideration then leads us to the default regions ( respectively) for subsidiary and subsidiary and for holding of type , respectively . They are explicitely given by

| (2) | |||

| (3) | |||

| (4) | |||

| (5) |

With the help of these regions we may then rewrite

for . Recall that to simplify the notation the dependency on of is implicit. In Figure 2 we display the default regions for both holding structures of type and . By the definition of the contagion process for type it follows trivially that smaller leads to less infections. However, we will see in the following that the situation for type is more complicated and interesting phenomena arise.

In order to determine we need to specify our random network setting. We fix and and assume that is present with probability for and that all edges are mutually independent. Instead of a fixed network we analyse a sequence of networks of increasing size. For , let as before and be the initial capital of subsidiary , respectively of bank . Let then and be the capitals of the subsidiaries for a network of size . We will often drop the dependency on in the notation when it does not lead to confusion. Let be the indicator that a directed edge from subsidiary of bank to subsidiary of bank is present. Let and the in- respectively out-degree of subsidiary of bank . Clearly then and as , where denotes convergence in probability.

In order to ensure that our asymptotic statements are relevant also for networks of finite size we shall need some regularity. In particular we require that the proportion of banks with a certain capital structure stabilizes as the network size increases. This is ensured by the following standing assumption for the rest of this paper:

Assumption 2.1.

For each , denote the joint empirical distribution function of and by

We assume that there exists a distribution on such that it holds for all . Denote by a random vector distributed according to .

Considering a network of holding types , we note that for fixed the contagion process only starts if there exists at least one bank such that . Under Assumption 2.1, this will be the case for large if .

We further define boundaries of the default regions by:

| (6) | |||

| (7) | |||

| (8) | |||

| (9) |

For example for a holding to be in means that its subsidiary is at risk of default. This is the case either because the subsidiary defaults as soon as it has a new defaulted neighbor ( or ) itself or because it defaults as soon as the other subsidiary has a new defaulted neighbor (). We refer again to Figure 2 for an illustration of these sets.

Moreover, we define the following subsets to be the sets of all points such that a link to subsidiary results in a default of subsidiary , for . The points on the boundary from which transition to the default region is possible through links from subsidiary are given by:

| (10) | |||

| (11) | |||

| (12) | |||

| (13) |

and for those through links from subsidiary :

| (14) | |||

| (15) | |||

| (16) | |||

| (17) |

It clearly holds that and for . These boundary regions turn out to be important as they allow us to derive criteria for the contagion process to stop. Heuristically, bank holdings with capital on the boundary have very vulnerable subsidiaries and if there are too many of them, the contagion process can quickly regain momentum even after it had slowed down.

Our first result, Theorem 2.3, describes the size of the final fraction of defaulted type and type subsidiaries. Its proof is based on a sequential reformulation of the process. This formulation leads to the same final outcome, but instead of exploring the effect of all defaulted subsidiaries at once, in each step only the effect of one defaulted subsidiary is considered. It turns out that in this reformulated process, the entire state of the system can be described in the limit () by a system of continuous functions. In the following we introduce these functions and provide some heuristic explanation for the results whose rigorous proof is given in Section 6.

Let for be the probability that a Poisson distributed random variable with parameter takes value . Let further for , the probability that a Poisson distributed random variable with parameter is greater or equal . We also define for the probability that two independent Poisson distributed random variables and with parameter and respectively, take the values and , i.e. .

Now define the functions for by

| (18) |

where the inequality is meant component-wise. In the continuous approximation mentioned above, the two arguments and describe the number of defaulted type respectively type subsidiaries whose effect on the system has already been taken into account, divided by . For a holding with original subsidiary capitals , the probability that due to links from these defaulted institutions, the capital has been reduced to , is approximately given by and thus heuristically describes the fraction of holdings that have the capital , after a fraction (respectively ) of type (respectively type ) subsidiaries have defaulted.

With the functions defined, we may sum over all those that are in the default region of subsidiary in order to get the total fraction of defaulted type subsidiaries . The effect of the fraction on the system has already been considered and it remains to explore the impact of the rest, i.e.

| (19) |

for . Recall that to simplify the notation the dependency on of is implicit.

A calculation based on Figure 2 concludes that

and

The corresponding expressions and for subsidiary can be derived similarly.

It will turn out that the first joint zero of the functions and allows us to determine the final number of defaulted type and type subsidiaries. Note that for we get that and similarly for and thus the systems decouple.

Let us also calculate the partial derivatives of as they appear in the statement of the following theorem. With , for one obtains that

| (20) |

where . For a vector we obtain the directional derivatives

| (21) |

In the following proposition we collect some more properties of the function that will be important for the statement and proof of our first main Theorem 2.3.

Proposition 2.2.

Let . The functions are continuous and:

-

1.

and thus is a joint zero of the functions if and only if .

-

2.

is increasing in its second argument and is increasing in its first argument.

We are now ready to state the first result that allows us to determine the final number of defaulted type and type subsidiaries. We provide several applications of this result in Section 4.

Theorem 2.3.

Let . Consider a sequence of financial systems satisfying Assumption 2.1 and let . Then there exists a unique smallest (component-wise) positive joint root of the functions . Moreover, the following holds for :

-

1.

For all , with high probability

-

2.

If in addition there exists a vector such that , then

Here denotes convergence in probability.

3 Resilience

In this section we consider how small infections can propagate through a financial network and amplify to lead to significant damage. For this we start with an a-priory uninfected network, parametrized by with and then apply ex-post infections. The ex-post infections will lead to , a network with lower capitalized banks, and we determine the spread of contagion in this new network based on the characteristics of . This provides a measure of resilience of the system to shocks.

Since our results hold for both, type and type holdings, and the proofs are generic, we drop the holding type in the notation, and since we will work with different financial systems we now include the random variable in the notation of the functionals defined in (19) and write . Before we move on let us first collect some additional properties of these functions which we need in what follows.

Proposition 3.1.

Let a configuration for the financial system and let its functional. Let further with and mutually independent Poisson distributed random variables with parameter and respectively. Then,

| (22) |

Moreover, by the law of total probability

| (23) |

with and mutually independent and independent of Poisson distributed random variables with parameter and .

With the help of the previous proposition it becomes clear from the representation of that a larger default region leads to a larger number of defaulted subsidiaries. In particular in the case of type subsidiaries, a decrease of leads to fewer infections. Of course this observation can also be made directly from the specification of the process in Section 2, but in order to derive our results in this section the representations provided in Proposition 3.1 will turn out useful.

As a direct consequence of the last proposition we obtain the following two corollaries:

Corollary 3.2.

Let be a sequence of random variables on that converges weakly to . Then and converge to and for all , uniformly on compacts.

Corollary 3.3.

Let and be configurations for the financial system and let respective be their functional. Then:

-

1.

If for all , that is stochastically dominates , then

for all .

-

2.

Moreover, denote by the set of entrance points to the default region , that is

(24) (25) (26) (27) If in addition there exists such that , then

for all .

We now move on to the statement of our main result in this section Theorem 3.4 and first specify what is exactly meant by a shock to the system.

Specification of financial shock: Following previous literature on contagion in financial networks Amini et al., 2016a ; Detering et al., (2019, 2021, 2022) we now consider a network that has a-priory no defaults, meaning . We then apply a small shock to the system. This shock has the effect that the capital of some subsidiaries (and therefore their holdings) is reduced and we assume this reduction to be such that some subsidiaries actually default.

For a shock that affects a fraction this leads to a new financial system which is such that:

-

1.

(no one is better off after the shock),

-

2.

(an fraction of holdings is affected by the shock),

-

3.

(some defaults occur due to the shock).

Resilience: We now call a financial system described by resilient if for every given , there exists such that for all shocked systems of with , the number of defaulted subsidiaries at the end of the default processes is less then w.h.p..

If on the contrary, there exists a lower bound , such that for every shocked system with and , it holds that w.h.p., then we call the system non-resilient.

The following theorem gives criteria for resilience and non-resilience based on the derivative in of the functional of the uninfected network, parametrized by .

Theorem 3.4.

We have the following statement regarding resilience:

-

1.

If there exists a vector such that , then the network is resilient.

-

2.

If there exists a vector such that , then the network is non-resilient.

In particular the conditions 1. and 2. are mutually exclusive.

Let us provide some rough sketch of the proof of Theorem 3.4, which is fully worked out in the Appendix: We know by Proposition 2.2 that for the network without defaults it holds that . If condition holds and there exists a vector such that the directional derivative of both functions and is negative, then this implies that in the direction both functions become negative. As long as the shock is small, i.e. small, we obtain by Corollary 3.2 that is close to and is close to for and in some compact set. Despite this will imply that for small there exists a small such that for . The following Lemma 3.5 then shows that serves as an upper bound for the first joint zero of and which then leads to the conclusion of resilience.

Lemma 3.5.

Let be such that , then it holds that .

In order to show non-resilience we first observe that condition 2. implies that in the direction the functions and are both becoming positive. By continuity of the derivative this in particular implies that for all for some . We can then use Corollary 3.3 to show that also for all . Then one can use the properties of derived in Proposition 2.2 to conclude that the smallest fixed-point of and is bounded by . Because the choice of only depends on the specification of and not on the precise specification of , this allows us to conclude non-resilience.

In the following we provide some examples that demonstrate the effect that the holding support can have on the resilience/non-resilience of the network.

Example 3.6.

Consider a financial network with and for . We assume that the holdings are of type . We first consider the decoupled system . For this we obtain

and therefore for , which is positive for any and the system is therefore non-resilient. This is as expected as for because the systems are decoupled and the propagation of distress in one system is not influenced by the other system. It is well known then (see for example Hofstad, (2016)) that each system separately forms a giant component for . We have , the capital of each subsidiary equals and it defaults as soon as one of their debtors default. This implies that as soon as one subsidiary in the giant component defaults, then the entire giant component defaults.

We now look at the coupled case and note that because of the capital structure of the uninfected network, the area of the default region that can actually be reached does not depend on for . It is therefore sufficient to consider . We observe that

with

| (28) | |||||

| (29) |

and thus . It follows that for any . The system is therefore resilient. The fact that the system is resilient for might be surprising at first for the following reason. If a subsidiary defaults, then the default of the holding’s other subsidiary is triggered immediately as well. This is because when the default happens the holdings capital is . From this perspective the coupling can lead to many additional defaults as a result of a defaulted subsidiary. On the other hand however, it allows to contain second order effects as healthy holdings with both subsidiaries still having capital equal to require a total of 2 links to defaulted subsidiaries in order to trigger the default of one and then automatically both subsidiaries. This example shows also that it can be beneficial from a regulator perspective if entities form little support groups. Although the distress of one member of the group can then pull down all the others in that group, the formation of support groups can in some instances still lead to a more resilient system.

Example 3.7.

We consider now a network with , which means that for all banks their type subsidiary would be in default if it was not supported by the holding through the other subsidiary. We assume that the holdings are of type . Again, we only need to consider the case . Then

with

Then, we obtain that

which is for and for . It follows that the system is resilient for and non-resilient for . Note that in this example it is clear from the discussion above about the giant component that for the system must be non-resilient because one link from a defaulted subsidiary leads automatically to the default of both subsidiaries of the same holding. Because for each subsidiary network has its own giant component, it is clear that this network is more prone to large cascades than two separated networks with the same connection probability. For and the coupling than has actually a negative effect for the type subsidiary network. The effect of connecting to the under-capitalized type network is the same as adding additional second edges between the type subsidiaries with probability . Subsidiary inherits the exposures of subsidiary . Due to these additional edges, the network gets non-resilient. It is not surprising that the additional edges have the same effect as increasing the connection probability, because for two nodes and , the probability of having neither an edge between the type subsidiaries nor between the type subsidiaries is given by where the term becomes negligible for large .

4 Case Study

We now study the contagion process for a number of different system configurations and illustrate a few intuitive findings. For different system configurations we determine the optimal support level. We wish to highlight that the optimal support level is viewed from the point of a (benevolent) regulator, who wishes to stabilize the financial system (by some measure), by imposing rules on the financial entities to support their own subsidiaries. These support actions may not be optimal from the point of view of an individual agent, and may not be a Nash equilibrium.

We assume that all subsidiaries of type have capital except for an share which has capital and thus defaults. Similarly, all type subsidiaries have capital equal to except for an share that has capital and thus defaults. Assuming that the defaulted subsidiaries of type are chosen independently of those of type , this of course implies that is such that for and and independent. Then we obtain that

and

The functions and are simply derived by exchanging the role of and . Observe that for respectively our specification implies that the default of type , respectively type , subsidiaries triggers immediately the default of the type , respectively type , subsidiary of the same holding.

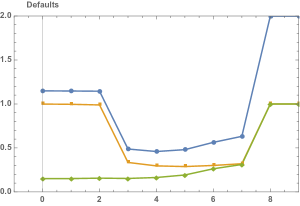

In our first example we choose the parameters and and , so that both layers in the networks are equally connected. We assume that in both subnetworks 15% of the subsidiaries are defaulted, i.e. . We consider a holding type . The only difference between the type network and the type network is then the capitalization. The type network is better capitalized. Also note that for , each default of a type subsidiary immediately triggers the default of its corresponding type subsidiary, which implies that in this case the actual fraction of initially defaulted type subsidiaries is equal to . The same holds for the type subsidiaries if .

For ranging from to we determine the first joint zero of the functions and which gives us the final number of defaulted type and type subsidiaries according to Theorem 2.3. The results are displayed in Figure 3. This is a typical example where the number of defaults in both subsidiaries first decreases, reaches a minimum and then increases as increases. While at first, this may seem counterintuitive, as more support, should mean less defaults, we remind that if a holding supports its distressed subsidiary (in case of type ) then the holdings other subsidiary takes a hit of up to . With this in mind it is not surprising that large may cause the second subsidiary to default.

For the systems are decoupled. We observe that in this case, as a results of strong contagion, almost all type subsidiaries default. This is due to the relatively low capital in this network and the relatively strong connectivity. The contagion is very much driven by higher order effects. This can be seen by calculating the probability that a subsidiary that is not initially defaulted defaults as a result of edges to initially defaulted subsidiaries. This probability is equal to the probability that a Poisson distributed random variable with parameter is at least , and calculates as which thus accounts only for a very low share of the final defaults. Subsidiary network is different. Due to the larger capital almost no contagion takes place. This is not surprising because the probability that an initially not defaulted subsidiary defaults as the result of edges from initially defaulted subsidiaries is very low. It is equal to the probability that a Poisson distributed random variable with parameter is larger than . This probability is less than .

With support for the subsidiaries , the contagion in the type network can be significantly contained. In fact we see that with a support level of , the fraction of defaulted type subsidiaries is reduced to without significantly increasing the number of defaulted type subsidiaries. As a result also the total number of defaulted subsidiaries (type together with type ) is reduced. In fact the lowest fraction of all the defaults is obtained for . With larger support, however, the subsidiaries in the type network get weakened substantially up to the point where more of them default. These defaults then channel back into the type network and so forth. For this leads to almost all subsidiaries defaulting.

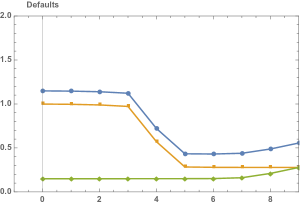

In comparison we now consider a network in which we change the connection probability to while keeping all other parameters unchanged. The results are shown in Figure 4. Due to the lower overall connectivity in the type network, the weakening of the type subsidiaries, as a result of their support for the type counterparts, has much less effect because defaults do not amplify. In particular we do not see the feedback effects in between the two layers that we saw in the previous example. While for strong support ( and ), the fraction of defaulted type subsidiaries has increased from to and , this increase does not trigger new default rounds in the type network. Observe that for both examples for , the number of defaulted type and type subsidiaries equal. In fact, because a subsidiary supports the holdings other subsidiary up to the point where it defaults itself, for , the subsidiaries always default together.

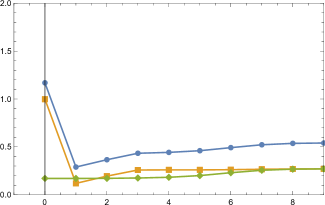

Clearly a decrease in the initial shock decreases the number of subsidiaries that default (Figure 5). It also should be noted that at a low level of support, and with a low degree of connectivity there is very little influence on the defaults in the more capitalized subnetwork as the holding support increases.

We also illustrate that this holding structure can be a stabilizing force ensuring resilience in the sense of Section 3. We consider the case from Example 3.7, with a holding with two (identical) subsidiaries and with a small initial shock: Without the holding with the two networks of subsidiaries separated, there is a cluster of defaults (approximately ), as a result of the propagation of the initial (small) shock. Whereas, once the holding is added, and the support is non-zero (), the defaults decrease to .

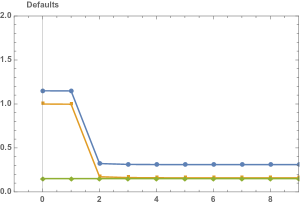

As a last example we consider again our original setting with , , and , but now with a holding structure . For this holding structure the support for one subsidiary has no negative effect on the other subsidiary of the same holding. As we mentioned previously, the support can be thought of as a loan that is taken against the positive capital of the holdings solvent subsidiary. The external lender is thus faced with the risk of both subsidiaries defaulting at the end. This external lender is not part of the network. As expected, we therefore see a significant reduction of the number of defaulted subsidiaries with stronger holding support and the maximal holding support leads to the fewest defaults. This is illustrated in Figure 6.

5 Conclusion

We proposed a simple model for a financial network of bank holdings with subsidiaries. This model allows us to study the role that the holding structure and the holding’s support for troubled subsidiaries has on the propagation of the contagion in a financial system. We observe that when (financial) firms are grouped into holdings this can have both, positive and negative effects. The support of a holding for a subsidiary in distress can mitigate or defer defaults and thus increase financial stability. However, in low capitalized systems, it can also amplify contagion as distress can reach previously healthy parts of the system. We show this phenomena in two ways: with a numerical case study that uses our theoretical results about the final default fraction, and analytically, based on a notion of resilience which allows us to investigate the spread of small initial shocks. We also determine the optimal support level from a regulator perspective. We stress that this is a simple model, which allows for many interesting generalizations, including more subsidiaries, more heterogeneous degrees, or holding that have additional capital.

6 Proofs

All the proofs in this section are generic for therefore we continue to omit from the notation.

Proof of Proposition 2.2.

Continuity follows by continuity of the functions and and dominated convergence.

For part 1. recall that with . Since if or is larger than , it follows that and thus .

Part 2. follows from (20), and the fact that . ∎

Proof of Theorem 2.3.

First observe that by Proposition 2.2 the function is increasing in its second argument while is increasing in its first argument. Moreover, for and for since . These properties allow to apply the proof of Lemma 3.2. in Detering et al., (2020) without any changes and we can conclude that a component-wise smallest joint root exists.

As mentioned above, instead of directly considering the contagion process based on rounds as described in (1), we explore the set by sequentially quantifying the effect of a defaulted subsidiary on the rest of the system. So, in each step we only expose the effect of one (yet unexposed) defaulted subsidiary. Such a sequential reformulation is standard in the literature and was first used for exploration of the giant component (see Hofstad, (2016) for instance) and later used for bootstrap percolation and financial contagion (see Janson et al., (2012); Amini et al., 2016a ; Detering et al., (2019)). The situation here, however, is conceptually more complicated because of the complexity of the contagion process and we therefore describe it in some detail. First note that whenever a subsidiary reaches the capital we know for sure that it has defaulted, independent of the second subsidiary’s financial situation. Therefore, there is no need to reduce the capital of such a subsidiary further in case it receives additional links from defaulted subsidiaries. This implies that each holding only takes on a finite number of relevant states.

During the exploration process we keep track of several quantities:

-

•

The sets for consisting of those holdings with capital of subsidiary being equal to and capital of subsidiary being equal to at step . At the beginning of the process () we set for all .

-

•

The sets of unexplored, defaulted type subsidiaries. At the beginning of the process we have defined by: if and only if . So, contains those subsidiaries of type which are in default at the beginning of the process.

-

•

The number and of already explored type and type subsidiaries. We set .

We now describe one step of this exploration process: At the very beginning of the step we choose uniformly a defaulted subsidiary from . We denote this subsidiary by . We then draw the links from to all the holdings in the sets . We then update these sets as follows. If in step we selected a type subsidiary and the subsidiary of holding receives a link from , then will be moved into unless in which case it will just remain in its current set (). During this exploration, some subsidiaries might move into their default region. If this happens and a type or type subsidiary goes bankrupt, we generate a copy of it and place it into the set , respectively . At the end of the step, if the selected subsidiary was in we set and , and we remove the subsidiary from the set of defaulted unexplored subsidiaries (i.e. we set . If the selected subsidiary was from , then we set and and remove the subsidiary (). Note that elements in and are distinguishable. The process ends at and corresponds to the total number of defaulted subsidiaries. Moreover, , because in each step we have exactly explored one subsidiary. Note that the procedure is such that the capital of some subsidiaries is still being updated although they have already defaulted (and possibly have been explored) but this updating has no effect. This happens if a subsidiary defaults with more capital than .

We start with proving the first statement of the theorem, the lower bound for based on this sequential exploration. Let and and and let describe the entire system, i.e.

We would like to stress that the the vector is a random vector and that we have chosen the lower case letters in order to distinguish from the random sets , and the for .

With probability in step a type subsidiary is selected that leads to a reduction of the number of vertices in by . On the other hand, each subsidiary in receives an edge from the selected subsidiary with probability and thus defaults and is added to . Similar, if a subsidiary of type is selected, which happens with probability , then each subsidiary in receives an edge from this subsidiary with probability , defaults and is added to . These considerations lead to

| (30) | |||||

| (31) | |||||

| (32) |

for with

| (33) |

and similarly for . Moreover, a similar combinatorial argument yields that

with

for . And finally

| (34) |

with for .

While the above calculated differences are random and very much depend on the degree of the chosen subsidiary in each step, it turns out that the sum of a few successive steps becomes concentrated at the mean and can be described by a vector valued continuous function. For this consider therefore the vector valued function defined by the system of differential equations:

| (35) |

| (36) |

| (37) |

Now note that the functions fulfill a Lipchitz condition on the domain

| (38) | |||||

for any as can easily be seen by calculating the partial derivatives and observing that they are bounded. This implies existence of a solution to the system (35) and (36). Since the solution exists on for any positive , we can of course extend the solution to .

The next step of the proof is to solve the system described by (35) and (36). In order to do so, define the following implicitly given functions

| (39) | |||

| (40) |

defined on . Note that and thus . The equation for is a simple linear equation solved by

| (41) |

Note that is a constant term multiplied by the probability that two independent Poisson distributed random variables with parameters and are zero. This allows to guess that for ,

| (42) |

To see that above expression does in fact satisfy (36), first note that

and

Then for we get from (42) that

| (43) | ||||

| (44) |

which verifies (36). The case where or is in can be verified similarly and is left to the reader.

In order to derive and , recall that

We then make the following Ansatz for the solution:

| (45) |

Note that the are well defined on as the sum is only over finitely many terms. A tedious, but straightforward calculation of taking derivatives of (45), verifies that satisfies (35) as most of the terms in the sum cancel out and only the terms on the boundaries remain.

For we now want to approximate the quantities with , and for the quantities with respectively. We use Wormald, (1995)[Theorem 2] to show that in fact

| (46) | |||||

| (47) | |||||

| (48) |

with high probability. By above considerations, assumptions (ii) and (iii) of Wormald, (1995)[Theorem 2] are satisfied. To see that also assumption (i) is satisfied, note that in each step of the exploration, the number of vertices receiving an edge from the currently explored defaulted subsidiary is bounded by the degree of this subsidiary. Let be the largest out-degree in the graph. A simple probabilistic bound for is given by

By Stirling’s formula, it follows that for any and thus

We may choose and for condition (i) in Wormald’s Theorem. This implies that the approximation (46)-(48) holds uniformly for

with high probability.

Let now . By the definition of the system it is clear that all quantities are in between and and thus by (46)-(48) and the definition of it follows that .

Let us now set , where the limit clearly exists as is increasing in and bounded by . Moreover, and we shall thus define .

Note that for . Moreover, since is the smallest (component-wise) joint zero of and , and due to the monotonicity and continuity of and , and of as derived in Proposition 2.2, it follows that . Let . By the previous considerations it follows that w.h.p. for every and thus by (46) w.h.p. for any and by it follows that

with high probability. This proves the first part of the theorem.

Now we will show that under the additional assumption that there exists such that , it holds in fact that

We know that and by continuity of the derivative and because of

it follows that also for small enough. Since it follows by (20) that

| (49) | |||

| (50) |

for some sufficiently close to . We shall track the process until the step by making use of (46) - (48), and then we explore the remaining subsidiaries in the sets in rounds. We place the holdings with capital in four sets which we define now and where a holding might be placed in more than one set. For this, let us call a subsidiary weak if it can default by either receiving one edge from a defaulted subsidiary itself or because the other subsidiary of the same holding receives a link from a defaulted subsidiary. We call a subsidiary strong if it can only default if this subsidiary and the other subsidiary of the same holding, receive in total at least two links from defaulted subsidiaries. For let be the set that includes those holdings with weak type subsidiary and those with strong type subsidiary. Note that for but the other four possible intersections of these sets are not necessary empty. Further for each we define the subsets of holdings whose weak type subsidiary defaults in round of the exploration process and the subsets of holdings whose strong type subsidiary defaults in round of the exploration process.

| (51) | |||

| (52) |

w.h.p.. This allows us now to bound the expected number of weak subsidiaries of type that default in the first round through a combinatorial counting argument by

and in particular

| (53) |

for any provided that and , which we can ensure by possibly decreasing further. We further choose and obtain that

Similarly we find for the very rough bound

with such that , provided that is chosen small enough. In particular it then follows that

| (55) |

Our plan is now to show that for it holds for every that

| (56) | |||

| (57) |

This implies

| (58) |

and from this it follows that

| (59) |

and therefore

| (60) |

The quantity on the right hand side of (60) can be made arbitrarily small by decreasing . So in order to conclude, it remains to show (56) and (57).

For this is done above. Suppose that (56) and (57) holds for . Then it follows for by (51) and (52) that

| (61) | |||||

| (64) |

and in particular

For a subsidiary to be in it must receive a link from the set and one from . It follows from a very rough bound that

| (65) | |||||

for sufficiently small. This finishes the proof. ∎

Proof of Proposition 3.1.

First note that the graph that describes the bound of the default region for subsidiary is a non-decreasing function of the capital of subsidiary . Similarly the graph that describes the bound of the default region of subsidiary is a non-decreasing function of the capital of subsidiary (see Figure 2). We rewrite (19):

| (66) | |||||

For fixed because of , it follows that

The shape of the default region is such that if and , then also . This implies that in the inner sum in (66) for we can actually drop the condition . Thus we can rewrite the double sum in (66) as

| (67) |

Now observe that is the conditional expectation of the random variable , given that and

the conditional expectation of the random variable

| (68) |

given that . By the definition of , this is just the probability that is in the default region where and being independent Poisson distributed random variables with parameter and respectively. Summing over , as we do in (67), now gives us by the law of total expectation the unconditional probability of which shows (22). By the law of total probability it follows that

with and being mutually independent Poisson distributed random variables with parameter and independent of . ∎

Proof of Corollary 3.2.

We prove the result for , the proof for is very similar. For fixed , point-wise convergence follows directly from Proposition 3.1 since for every , the integrand in (22) is bounded by . By weak convergence of it then follows that converges to . Let now compact. For simplicity we assume that is an interval of the form with but the proof for general compact sets does not pose any further complications. For a given , choose now and points such that for every there exists , such that . Now choose large enough such that for all . By (20), the partial derivatives of are bounded by . Therefore, for arbitrary , choose such that . By the triangular inequality

which shows uniform convergence. ∎

Proof of Corollary 3.3.

Proof Theorem 3.4.

We start with the proof for 1. Let be given. We know by Corollary 3.2 that if and are close (in distribution), then the functionals and their derivatives are close. Now, if there exists a direction such that , then for small enough, we know that also for . In fact, it follows by continuity that for in some neighborhood of . By possibly decreasing even further to the point that and ensuring that , we get that for . By Lemma 3.5 below, it follows that the first joint zero of and is bounded by . By (21) we may assume that is such that where . It then follows by Theorem 2.3 that .

To show part 2. about non-resilience: Again we start with an uninfected network , which implies that . By assumption,

and by continuity on the directional derivative in the direction , there exists some neighborhood of such that

for . This implies that for

We show that this in fact implies that for any . Let now and assume without loss of generality that is to the right of the line in . Let the unique point on the line with the same first coordinate as the point , i.e. where . We then know that . However, by monotonicity of with respect to , it follows that . If instead was on the left of the line the same argument applied to the second coordinate and the function would show that . Because was chosen arbitrary, we conclude that for any .

Now consider the infected network parameterized by with and . It follows by Corollary 3.3 item 2. that

for all and . By above consideration we know that no point exists such that both and are . This implies that there exists also no point such that both and are . In particular because of , there can not be any joint zero of and in . Again, by Theorem 2.3 part 1. it follows that , independent of the specification of . ∎

Proof Lemma 3.5.

First note that for any and for any . We now construct a decreasing sequence of points with and such that exists and is a joint zero of and .

For this, set , and then for every odd we define by and

| (69) |

and for even we define by and

| (70) |

We first need to show that the above sets are not empty and that is actually a well defined point in for every . By assumption, we have that . For the set defined in (69) as long as , it follows by continuity of and by that the set is not empty and . Moreover, by definition of , it holds that and by monotonicity of in its first argument it holds that as long as . The same argument applies to (70).

Clearly, the sequence is decreasing and bounded from below by . This implies that the sequence converges to some point . Moreover, because whenever is odd and whenever is even, it follows by continuity of that and thus is a joint zero. Note that the sequence is defined to approximate the joint zero from a region where both function values are . ∎

References

- (1) Amini, H., Cont, R., and Minca, A. (2016a). Resilience to Contagion in Financial Networks. Mathematical Finance, 26(2):329–365.

- Amini et al., (2013) Amini, H., Filipović, D., and Minca, A. (2013). Systemic risk with central counterparty clearing. Swiss Finance Institute Research Paper No. 13-34, Swiss Finance Institute.

- (3) Amini, H., Filipović, D., and Minca, A. (2016b). Uniqueness of equilibrium in a payment system with liquidation costs. Operations Research Letters, 44(1):1–5.

- Amini and Fountoulakis, (2014) Amini, H. and Fountoulakis, N. (2014). Bootstrap Percolation in Power-Law Random Graphs. Journal of Statistical Physics, 155(1):72–92.

- Amini et al., (2014) Amini, H., Fountoulakis, N., and Panagiotou, K. (2014). Bootstrap percolation in Inhomogeneous random graphs. arXiv:1402.2815.

- Anand et al., (2015) Anand, K., Craig, B., and Von Peter, G. (2015). Filling in the blanks: Network structure and interbank contagion. Quantitative Finance, 15(4):625–636.

- Arinaminpathy et al., (2012) Arinaminpathy, N., Kapadia, S., and May, R. M. (2012). Size and complexity in model financial systems. Proceedings of the National Academy of Sciences, 109(45):18338–18343.

- Balogh and Pittel, (2007) Balogh, J. and Pittel, B. G. (2007). Bootstrap percolation on the random regular graph. Random Structures Algorithms, 30(1-2):257–286.

- Bardoscia et al., (2017) Bardoscia, M., Barucca, P., Brinley Codd, A., and Hill, J. (2017). The decline of solvency contagion risk. Bank of England Staff Working Paper, 662.

- Bichuch and Feinstein, (2019) Bichuch, M. and Feinstein, Z. (2019). Optimization of fire sales and borrowing in systemic risk. SIAM Journal on Financial Mathematics, 10(1):68–88.

- Bichuch and Feinstein, (2022) Bichuch, M. and Feinstein, Z. (2022). A repo model of fire sales with vwap and lob pricing mechanisms. European Journal of Operational Research, 296(1):353–367.

- Boss et al., (2004) Boss, M., Elsinger, H., Summer, M., and Thurner, S. (2004). Network topology of the interbank market. Quantitative Finance, 4(6):677–684.

- Capponi et al., (2016) Capponi, A., Chen, P.-C., and Yao, D. D. (2016). Liability concentration and systemic losses in financial networks. Operations Research, 64(5):1121–1134.

- Chen et al., (2016) Chen, N., Liu, X., and Yao, D. D. (2016). An optimization view of financial systemic risk modeling: The network effect and the market liquidity effect. Operations Research, 64(5).

- Cifuentes et al., (2005) Cifuentes, R., Shin, H. S., and Ferrucci, G. (2005). Liquidity risk and contagion. Journal of the European Economic Association, 3(2-3):556–566.

- Detering et al., (2019) Detering, N., Meyer-Brandis, T., and Panagiotou, K. (2019). Bootstrap Percolation in Directed Inhomogeneous Random Graphs. The Electronic Journal of Combinatorics, 26(3).

- Detering et al., (2019) Detering, N., Meyer-Brandis, T., Panagiotou, K., and Ritter, D. (2019). Managing default contagion in inhomogeneous financial networks. SIAM Journal on Financial Mathematics, 10(2):578–614.

- Detering et al., (2021) Detering, N., Meyer-Brandis, T., Panagiotou, K., and Ritter, D. (2021). An integrated model for fire sales and default contagion. Mathematics and Financial Economics, 15(1):59–101.

- Detering et al., (2022) Detering, N., Meyer-Brandis, T., Panagiotou, K., and Ritter, D. (2022). Suffocating fire sales. SIAM Journal on Financial Mathematics, 13(1):70–108.

- Detering et al., (2020) Detering, N., Meyer-Brandis, T., Panagiotou, K., Ritter, D., et al. (2020). Financial contagion in a stochastic block model. International Journal of Theoretical and Applied Finance, 23(08):1–53.

- Eisenberg and Noe, (2001) Eisenberg, L. and Noe, T. H. (2001). Systemic risk in financial systems. Management Science, 47(2):236–249.

- Elliott et al., (2014) Elliott, M., Golub, B., and Jackson, M. O. (2014). Financial networks and contagion. American Economic Review, 104(10):3115–3153.

- Elsinger, (2009) Elsinger, H. (2009). Financial networks, cross holdings, and limited liability. Österreichische Nationalbank (Austrian Central Bank), 156.

- Elsinger et al., (2013) Elsinger, H., Lehar, A., and Summer, M. (2013). Network models and systemic risk assessment. In Handbook on Systemic Risk, pages 287–305. Cambridge University Press.

- Gai et al., (2011) Gai, P., Haldane, A., and Kapadia, S. (2011). Complexity, concentration and contagion. Journal of Monetary Economics, 58(5):453–470.

- Gai and Kapadia, (2010) Gai, P. and Kapadia, S. (2010). Contagion in Financial Networks. Proc. R. Soc. A, page 2401–2423.

- Glasserman and Young, (2015) Glasserman, P. and Young, H. P. (2015). How likely is contagion in financial networks? Journal of Banking and Finance, 50:383–399.

- Gouriéroux et al., (2012) Gouriéroux, C., Héam, J.-C., and Monfort, A. (2012). Bilateral exposures and systemic solvency risk. Canadian Journal of Economics, 45(4):1273–1309.

- Halaj and Kok, (2015) Halaj, G. and Kok, C. (2015). Modelling the emergence of the interbank networks. Quantitative Finance, 15(4):653–671.

- Hofstad, (2016) Hofstad, R. v. d. (2016). Random Graphs and Complex Networks, volume 1 of Cambridge Series in Statistical and Probabilistic Mathematics. Cambridge University Press.

- Hüser, (2015) Hüser, A.-C. (2015). Too interconnected to fail: A survey of the interbank networks literature. Journal of Network Theory in Finance, 1(3):1–50.

- Janson et al., (2012) Janson, S., Łuczak, T., Turova, T., and Vallier, T. (2012). Bootstrap percolation on the random graph . Ann. Appl. Probab., 22(5):1989–2047.

- Lewis, (2010) Lewis, M. (2010). The Big Short : Inside the Doomsday Machine. New York :Simon & Schuster.

- Nier et al., (2007) Nier, E., Yang, J., Yorulmazer, T., and Alentorn, A. (2007). Network models and financial stability. Journal of Economic Dynamics and Control, 31(6):2033–2060.

- Rogers and Veraart, (2013) Rogers, L. C. and Veraart, L. A. (2013). Failure and rescue in an interbank network. Management Science, 59(4):882–898.

- Staum, (2013) Staum, J. (2013). Counterparty contagion in context: Contributions to systemic risk. In Handbook on Systemic Risk, pages 512–548. Cambridge University Press.

- Upper, (2011) Upper, C. (2011). Simulation methods to assess the danger of contagion in interbank markets. Journal of Financial Stability, 7(3):111–125.

- Weber and Weske, (2017) Weber, S. and Weske, K. (2017). The joint impact of bankruptcy costs, fire sales and cross-holdings on systemic risk in financial networks. Probability, Uncertainty and Quantitative Risk, 2(1):9.

- Wormald, (1995) Wormald, N. C. (1995). Differential Equations for Random Processes and Random Graphs. The Annals of Applied Probability, 5(4):1217 – 1235.