Meta-Learners for Estimation of Causal Effects:

Finite Sample Cross-Fit Performance

Abstract

Estimation of causal effects using machine learning methods has become

an active research field in econometrics. In this paper,

we study the finite sample performance of meta-learners for

estimation of heterogeneous treatment effects under the usage of

sample-splitting and cross-fitting to reduce the overfitting bias.

In both synthetic and semi-synthetic simulations we find that the

performance of the meta-learners in finite samples greatly depends on

the estimation procedure. The results imply that sample-splitting and

cross-fitting are beneficial in large samples for bias reduction and

efficiency of the meta-learners, respectively, whereas full-sample

estimation is preferable in small samples. Furthermore, we derive

practical recommendations for application of specific meta-learners in

empirical studies depending on particular data characteristics such

as treatment shares and sample size.

Keywords: Meta-learners, causal machine learning, heterogeneous treatment effects, Monte Carlo simulation, sample-splitting, cross-fitting.

JEL classification: C15, C18, C31.

1 Introduction

In recent years there has been a growing interest in the estimation of causal effects using machine learning algorithms, particularly in the field of economics [4]. The newly emerging synthesis of machine learning methods with causal inference has a large potential for a more comprehensive estimation of causal effects [87]. On the one hand, it enables a more flexible estimation of average effects which are of main interest in microeconometrics [66]. On the other hand, it advances the estimation beyond the average effects and allows for a systematic analysis of effect heterogeneity [7]. Both of these aspects contribute to a better description of the causal mechanisms and thus to a possibly more efficient treatment allocation \parencitesZhao2012Kitagawa2018Athey2021Nie2021. Hence, applied empirical researchers can greatly benefit from the usage of machine learning methods ranging from evaluation of public policies and business decisions to designing personalized interventions \parencitesAndini2018Bansak2018.

Machine learning estimators as such are, however, primarily designed for prediction problems and thus cannot be used directly for causal inference. Therefore, new approaches for the estimation of causal parameters using machine learning emerged [[, see]for an overview]Athey2019a. In particular, the development of the so-called meta-learners have received considerable attention \parencites(see e.g.)()Kunzel2019Kennedy2020[or][]Nie2021a. Meta-learners decompose the causal problem into separate prediction problems that can be solved by standard machine learning algorithms and subsequently combined to estimate the causal parameters of interest [34]. Such an approach is advantageous for several reasons. First, the meta-learners do not modify the objective function of the machine learning methods but rather combine their predictions in order to estimate the causal effect. This enables to directly leverage the superior prediction power of machine learning estimators. Second, the meta-learners are generic algorithms refraining from a specific usage of any particular machine learning method. This allows to apply any suitable supervised learning method for the particular prediction problem at hand. Third, the meta-learners are attractive due to the ease of implementation using standard statistical software. This permits researchers to apply the meta-learners without any potential restrictions due to limited availability in software packages and enables tailored implementation for particular types of data. Despite the attractive features of the meta-learners, there is little guidance for applied empirical researchers on how to choose from a variety of the meta-learners proposed in the literature, with lack of unifying simulation evidence for an assessment of the performance of the meta-learners in applied empirical settings.

The complexity of the meta-learners for the estimation of the causal parameters varies widely and often hinges on a prior estimation of the conditional means of the outcome and the treatment, also referred to as the nuisance functions, that are not of primary interest [29]. Due to the machine learning, or in general flexible estimation of such nuisance functions the meta-learners are prone to the overfitting bias, i.e. own observation bias, which stems from fitting the data too well such that the prediction performance gets compromised [56]. This bias then pollutes the estimation of the causal parameters, when the machine learning estimators of the nuisance functions are directly plugged into the estimation of the causal effect using the same data [100]. Therefore, sample-splitting has been proposed in the literature to reduce the overfitting bias by using one part of the sample for estimation of the nuisance functions and the other part of the sample for estimation of the causal effect. In order to regain the full sample size efficiency of the estimator cross-fitting repeats the estimation by swapping the samples and averaging the estimated causal effects [29]. However, the usage of sample-splitting and cross-fitting is not well understood in practice and the specific definitions of meta-learners differ substantially in their implementation of these procedures. Despite the ambiguous definitions, there is a lack of simulation evidence concerned with the usage of sample-splitting and cross-fitting within the meta-learning framework and thus limited guidance for or against specific implementations. Moreover, there appears to be limited knowledge about how the asymptotic arguments translate into finite sample properties of the meta-learners.

In this paper, we address both of the above issues and study the finite sample properties of the machine learning based meta-learners for the estimation of causal effects based on the specific implementations using the full-sample, sample-splitting and cross-fitting procedures for varying sample sizes. We focus on evaluating the estimation of heterogeneous treatment effects as these provide the most detailed description of the underlying causal mechanisms and thus allow for a better assessment of the individualized impacts of an intervention. For this purpose, we review the most widely used meta-learning algorithms together with their assumptions with respect to sample-splitting and cross-fitting and identify their strengths and weaknesses. We conduct both synthetic and empirically grounded semi-synthetic simulations comparing the performance of the meta-learners in various settings featuring unequal treatment shares, non-linear functional forms and large-dimensional feature sets. Importantly, within the simulations we explicitly study the convergence performance of the meta-learners based on growing sample sizes up to observations. Furthermore, we derive practical recommendations on the choice of specific meta-learners and the respective estimation procedures for applied empirical work.

The results of our simulation experiments reveal that the choice of the estimation procedure has a large impact on the performance of the machine learning based meta-learners in finite samples. For sufficiently large samples we provide evidence for the theoretical arguments of bias reduction via sample-splitting and cross-fitting, while for smaller samples we observe adverse effects of these procedures when using machine learning. The results show that, if computation time is not a constraint, cross-fitting is always preferable to sample-splitting as it keeps the bias low, while successfully reducing the variance of the estimators even in small samples. However, the results imply heterogeneous impacts of the estimation procedures on the performance of the different meta-learners. We detect meta-learners for which the performance is stable regardless of the estimation procedure and for which the performance is more sensitive to the choice thereof. This holds not only with regard to bias and variance, but also with regard to convergence rates. Beyond the impacts of the estimation procedures, the results reveal clear patterns for the performance of particular meta-learners based on data characteristics. As such, we identify meta-learners suitable for empirical settings with highly unbalanced treatment shares, irrespective of the sample size, as well as meta-learners that are unstable in small samples but have superior performance once larger samples become available. Finally, we set apart meta-learners with undesirable statistical properties that should be avoided for estimation of causal effects.

This paper contributes to the causal machine learning literature in several ways. First, we provide unifying simulation evidence of meta-learning algorithms for the estimation of heterogeneous causal effects in large-dimensional and highly non-linear settings based on synthetic and semi-synthetic simulations. Second, we explicitly study the meta-learners under the full-sample, sample-splitting and cross-fitting implementations, respectively and thereby provide evidence on the contrast between the asymptotic arguments and finite sample properties. Third, we empirically investigate the convergence performance of the meta-learners by repeating the simulation experiments with growing sample sizes. Finally, we derive relevant practical recommendations for applied empirical work which are based on the particular observable data characteristics.

The rest of this paper is organized as follows. We briefly discuss the related literature in Section 1.1. Section 2 introduces the notation, the parameters of interest and their identification. Section 3 reviews the considered meta-learners and the estimation procedures. Section 4 describes the synthetic as well as semi-synthetic simulations and presents the corresponding results. The main findings of the study are discussed in Section 5. Section 6 concludes. Further details including descriptive statistics, an exhaustive summary of the main and supplementary results as well as a computation time analysis are provided in Appendices A, B and C, respectively.

1.1 Related Work

Within the fast developing causal machine learning literature, many different meta-learning algorithms of different complexities have been proposed. Following the naming convention of meta-learners based on the capital letters, the less complex meta-learners include the S-learner and the T-learner \parencites[see][and]Lo2002[][for early ideas of these approaches]Hansotia2002[and][for applications in the marketing domain]Kane2014222In the marketing literature the so-called uplift modelling is concerned with the same target of estimating causal effects and developed in parallel to the classical econometric and causal machine learning literature. For a comprehensive overview of the literature on uplift modelling see [36]. [52] and [145] provide unified surveys of uplift modelling harmonized with the econometric and causal machine learning literature, respectively. which besides the treatment effect function do not require estimation of any additional nuisance functions. However, the most prominent and widely used meta-learners in the literature consist of the more complex X-learner [86], the DR-learner [75], and the R-learner [101], which all require prior estimation and combination of several nuisance functions, such as the conditional means of the outcome and the treatment, to estimate the causal effect. We define the meta-learners formally and discuss them in more detail in Section 3.2. In this paper, we focus on the above-listed meta-learners in order to provide a contrast between less and more complex algorithms for the estimation of causal effects. Moreover, these particular meta-learners have been extensively studied theoretically as well as applied in various empirical settings, including economics \parencitesKnaus2020bJacob2021Sallin2021Valente2022, public policy \parencitesKristjanpoller2021Shah2021, marketing \parencitesGubela2020Gubela2021, medicine \parencitesLu2018Duan2019 or sports [46]. Some further examples of meta-learners proposed in the literature consist of the U-learner and Y-learner [129], or more recently the IF-learner [33] and RA-learner [34], which are, however, beyond the scope of this paper.

Besides the meta-learning framework, there has been also a substantial development of specific causal estimators based on direct modifications of particular machine learning algorithms. Especially, the tree-based estimators have been studied extensively in this respect. These include Causal Trees [6] as well as Causal Boosting [105] and Causal Forests [140] with the extensions of the Modified Causal Forests [87] and the Generalized Random Forests [9]. These methods are based on the underlying predictive algorithms of Regression Trees [25], Boosted Trees [44] and Random Forests [24], respectively. Furthemore, Bayesian versions of Regression Trees, the so-called BART [30] have been adapted for estimation of causal effects as well \parencitesHill2011Taddy2016Hahn2020. Besides the estimators based on recursive partitioning, important causal adjustments have been applied in respect to regularization based estimators such as the Lasso \parencitesQian2011Belloni2013aTian2014 or Lasso-augmented Support Vector Machines [64]. Additionally, further machine learning algorithms such as the Nearest Neighbours [41] or Neural Networks \parencitesJohansson2016Shalit2017Schwab2018Shi2019 have been transformed towards causal inference as well. For a comprehensive overview of many of these estimators, we refer the interested reader to [8], [82] and [69], or to [12] for numerous empirical examples. While many of these methods have well-established theoretical properties, they restrict the researcher in the choice of the machine learning method. In this paper, although we focus on the machine learning estimation of causal effects, we refrain from an analysis of these methods due to major conceptual differences to the meta-learning framework and the lack of comparability in terms of the usage of sample-splitting and cross-fitting procedures.

In general, the literature on the finite sample properties of causal machine learning estimators under unified framework seems to be rather scarce. One of the exceptions in the econometric literature333[142] conduct similar empirically grounded simulation study in medical context, while [94] use synthetic data. is [81] who study a wide range of estimators for heterogeneous as well as (group) average treatment effects, including direct estimators as well as some meta-learners in an Empirical Monte Carlo Study as developed in [62] and [89]. [81] find no estimator to perform uniformly best, but notice that estimators which model both the outcome as well as the treatment process are substantially more robust throughout all data generating processes considered, which can be observed in our simulations as well. Among the meta-learners considered, the DR-learner and the R-learner perform especially well in terms of the root mean squared error. Moreover, using the Random Forest as a base learner turns out to be more stable with better statistical properties in contrast to using the Lasso, particularly in smaller samples, which also motivates the usage of the Random Forest in our simulations. However, although both meta-learners are implemented with cross-fitting, an explicit consideration of different sample-splitting or cross-fitting schemes is missing. A recent work by [98] also focuses on a variety of causal machine learning estimators, inclusive of selected meta-learning algorithms, in an empirically grounded simulation design. [98] find Bayesian estimators, including the DR-learner with BART as a base learner, to perform best in estimating the heterogeneous treatment effects. In addition to [81], the simulations of [98] provide results on statistical inference in terms of coverage rates and length of the confidence intervals for the estimated causal effects. Nevertheless, albeit [98], similarly as [81], implement the relevant estimators using cross-fitting, a devoted assessment of this procedure is omitted. [34] focus directly on meta-learning algorithms for estimation of heterogeneous treatment effects, but refrain from studying sample-splitting and cross-fitting procedures and rely fully on the full-sample estimation. In this regard, [150] study the performance of treatment effect estimators based on cross-fitting, including some meta-learners as well. Similarly to [81] they find the DR-learner with an ensemble machine learning base learners together with cross-fitting to perform the best among all considered estimators, both in comparison to cases without cross-fitting and to parametric base learners. However, [150] study exclusively the estimation of average effects without examining convergence performance of the estimators, considering only a single sample size of observations.444Numerous other recent studies in the epidemiology literature focus on the estimation of average effects using the DR-learner based on cross-fitting, typically in small samples. For details see [13], [96], [99], [147] and [32]. Recently, [68] focuses on the estimation of heterogeneous treatment effects under various cross-fitting schemes for selected meta-learning algorithms. Also, in this simulation study the DR-learner together with the R-learner achieve consistently the best results. [68] stresses the heterogeneous impacts of the particular sample-splitting and cross-fitting procedures on each meta-learner, which is documented in our simulations as well. Nevertheless, even though considering varying sample sizes within the simulation experiments, the considered sample sizes are limited to observations. Overall, none of the above studies focuses directly on the convergence performance of the meta-learners under various estimation procedures which still remains an open question. To the best of our knowledge, this is the first paper that empirically studies the convergence properties of the meta-learners under full-sample, sample-splitting and cross-fitting implementations with growing sample sizes up to several thousands of observations, reaching in our simulations.

2 Framework and Identification

In order to describe the effects of interest and their corresponding identification assumptions we rely on the potential outcome framework [114]. We assume a population from which a realization of i.i.d. random variables is given consisting of a random sample . Here, we consider a binary treatment variable that is equal to for the treated group and equal to for the control group, respectively. According to the treatment status we define the potential outcome under treatment for the case when and correspondingly the potential outcome under control for . Additionally, we define a -dimensional vector of exogenous pre-treatment covariates such that . Given this definition we can characterize the Individual Treatment Effect (ITE) as follows:

However, the fundamental problem of causal inference is that we never observe both potential outcomes at the same time [60]. Hence, the observed outcomes are defined according to the observational rule as . The observed data then consists of the triple . Nevertheless, it is still possible to identify the expectation of under additional assumptions \parencites(compare)()Rubin1974[or][]Imbens2015. Thus, we shift the effect of interest towards the Conditional Average Treatment Effect (CATE) which takes the expectation of , conditional on covariates and is given as:

where and are the response functions for potential outcomes under treatment and under control, respectively. In this paper we always refer to the CATE with conditioning on all observed exogeneous covariates and thus focusing on the finest level of heterogeneity [[, see e.g.]]Knaus2021.555In general, the term CATE describes conditional average treatment effects on various aggregation levels [87]. In our case, the CATE corresponds to the Individualized Average Treatment Effect (IATE). Additionally, researchers and especially policy makers might be interested in a low-dimensional heterogeneity level based on some pre-specified heterogeneity covariates of interest, which are referred to as the Group Average Treatment Effects (GATEs). Such effects are, however, beyond the scope of our study and the interested reader is referred to [149], [67] and [124] for a theoretical analysis and to [81] for simulation based results or to [31], [80], [58] and [47] for empirical applications estimating policy relevant GATEs. [86] point out that the best estimator for is also the best estimator for in terms of the mean squared error (MSE).

In order to identify the effects of interest, we need a set of identification assumptions. We operate under the selection-on-observables strategy666For estimation of heterogeneous treatment effects under different identification strategies see e.g. [9], [15] and [23] for the case of instrumental variables and [148], [116] and [103] for the case of difference-in-differences. [[, see e.g.]]Imbens2015 and assume that we observe all relevant confounders, i.e. all covariates that jointly influence both the treatment and the potential outcomes, and . We state the following identification assumptions:

Assumption 1 (Conditional Independence)

.

Assumption 2 (Common Support)

.

Assumption 3 (SUTVA)

.

Assumption 4 (Exogeneity)

.

According to Assumption 1, also referred to as the conditional ignorability or unconfoudedness assumption, we assume that the potential outcomes are independent of the treatment assignment once conditioned on the covariates, i.e. we assume that there are no hidden confounders. Assumption 2, also known as the overlap assumption, states that the conditional treatment probability is bounded away from and and thus it is possible to observe treated as well as control units for each realization of . Assumption 3 is known as the stable unit treatment value assumption and indicates that the observed treatment value for a unit is independent of the treatment exposure for other units, which rules out any general equilibrium or spillover effects between treated and controls. Lastly, Assumption 4 specifies that the covariates are not influenced by the treatment.777Analogously to the definition of potential outcomes, we denote potential covariates under control and under treatment as and , respectively. Under these assumptions it follows that

| (2.1) | ||||

| (2.2) | ||||

| (2.3) | ||||

| (2.4) |

and thus the CATE can be nonparametrically identified from observable data [63].

3 Meta-Learning Algorithms and Estimation Procedures

In the machine learning literature meta-learning represents algorithms that exploit knowledge about learning to improve the algorithm’s performance, as generally defined by [138]. These include various algorithms that learn to solve new task from prior learning experience, i.e. learning to learn \parencitesSchmidhuber1987Thrun1998, algorithms that learn from multiple related tasks, i.e. multi-task learning [27], or algorithms that learn from multiple models solving identical task, i.e. ensemble learning [37].888For a recent survey on meta-learning, see [137]. Recently, the meta-learning framework has been adopted within the causal machine learning literature for learning causal effects from multiple prediction models [[, see for example]]Kunzel2019, which could be termed accordingly as causal learning.

At a high level the meta-learners for estimation of heterogeneous causal effects are two-step algorithms. In the first step they define regression functions, in the causal machine learning literature often denoted as the nuisance functions \parencitesChernozhukov2018cKennedy2020, which can be estimated by any supervised learning method fulfilling suitable regularity conditions, i.e. the base learner.999The base learners can be in general any set of black-box methods as long as they are consistent estimators of the nuisance functions and sufficiently minimize the prediction error in terms of the MSE \parencitesKunzel2019Kennedy2020Nie2021a. However, in order to provide explicit error bounds and achieve specific convergence rates on the estimation of the causal effect, the base-learners must fulfill a set of regularity conditions such as smoothness or sparsity [1]. We discuss the particular conditions required for each meta-learner in Section 3.2. In the second step they use the estimated nuisance functions to construct an estimator for the causal effect, i.e. the meta-learner. Various meta-learners then differ in the definitions of the nuisance functions and their subsequent usage to obtain the final estimator for the causal effects. Depending on the algorithm complexity, some meta-learners require estimation of only one single model whereas others require estimation of multiple models. This raises the question of data usage within the estimation procedure and thus the possible need for sample-splitting and cross-fitting, respectively.101010Recently, related issue of data usage of the meta-learning algorithms with respect to splitting into training and validation set for the learning to learn domain has been discussed by [11] and [117].

In general, the nuisance functions are defined as conditional expectations of various types. The most common types are the propensity score function and the response function. First, the propensity score is defined as the conditional probability of a binary treatment given the covariates as follows:

In the causal inference literature the propensity score plays a central role [113] in many matching and reweighting methods to balance the distributions of treated and controls \parencites(see)()Hahn1998[and][among others]Huber2013. Second, the response function is broadly defined as the conditional expectation of an outcome variable given a conditioning set of explanatory variables. The particular definitions of the response function then differ in the specification of the conditioning set and the subset of the data used. For the meta-learners studied in this paper, the following definitions of the response function are of interest:

| (3.1) | ||||

| (3.2) |

where Equation 3.1 defines the response function with conditioning on both the covariates as well as the treatment indicator , while and describe the response functions with conditioning on the covariates in the subpopulation under treatment and under control , accordingly. Similarly, Equation 3.2 defines the response function with conditioning only on covariates. The meta-learners then use selected nuisance functions together with the available data as inputs for the estimation of the CATE function which can be generally denoted as follows:

where is a function of the respective inputs, which is detailed for each particular meta-learning algorithm in Section 3.2. The problem arises when estimating the nuisance functions using flexible machine learning methods as these are prone to the overfitting bias, i.e. the ‘own observation bias’. The overfitting bias emerges when the in-sample data is fitted too well such that the out-of-sample performance is compromised [[, see e.g.]for a general discussion of the overfitting issue in machine learning]Hastie2009. Hence, a single observation can have a large influence on the predictions for covariates as pointed out by [8]. [29] and [100] thus propose sample-splitting procedures that allow for elimination of such overfitting biases.111111Original ideas of using sample-splitting procedures to eliminate own observation bias stem from the literature on density estimation going back to [22], [21] and [104] among others.

3.1 Sample-Splitting and Cross-Fitting

Theoretical arguments express the need for sample-splitting when the causal estimator involves several estimation steps such as the estimation of nuisance functions. Within the meta-learning framework the nuisance functions are typically highly complex and potentially high-dimensional functions estimated by supervised machine learning methods such as penalized regression, tree-based methods, neural networks, etc. Using the same data sample for machine learning estimation of the nuisance function as well as for estimation of the causal effect leads to overfitting which induces a bias in the CATE estimator. On a high level, the bias of the CATE estimator can generally be decomposed into an estimation error of learning the CATE function itself, and the estimation error in learning the nuisance functions, encompassing the overfitting bias [[, see e.g.]]Kennedy2020.121212The machine learning estimation of the nuisance functions might additionally induce so-called regularization bias. This is due to the effective MSE minimization that restricts the variance of the estimator, but introduces a bias, which might not decay fast enough. For a discussion of the regularization bias in treatment effect estimation, see [29]. [29] show that for the ATE estimation the overfitting bias can be controlled by using sample-splitting, while [75] and [101] extend this concept for the CATE estimation. In that case one part of the sample is used to estimate the nuisance functions and the other part is used to estimate the causal effect.131313Sample-splitting procedures are frequently used in causal machine learning literature including Double Machine Learning [29], Causal Forests \parencitesWager2018Lechner2019 or the here-discussed meta-learners \parencitesKennedy2020Nie2021a. As a result, the bias term stemming from overfitting can be shown to be bounded and to converge to zero sufficiently fast. Building upon this result, [100] propose an advanced sample-splitting scheme called double sample-splitting. In this case, not only the nuisance functions are estimated together on a separate part of the sample but each single nuisance function is estimated on an own separate part of the sample. In practice, the training data is split into equally sized parts, with being the number of nuisance functions to estimate and the remaining part of the data serves for estimation of the causal effect. [100] show that under the double sample-splitting the bias term converges to zero at a faster rate compared to standard sample-splitting where all nuisances are estimated on the same sample.141414The intuition for this result comes from the observation that for estimators using multiple nuisance functions, such as the doubly robust estimators as e.g. the herein discussed DR-learner, the estimation error involves a product of the biases from the estimation of the nuisance functions. This induces additional nonlinearity bias if all nuisance functions are estimated using the same data, which gets effectively removed by using separate samples for estimation of each of the functions. For more details see [100] and [75]. The double sample-splitting procedure has also been recently implemented by [75] in the context of the DR-learner.

In general, the overfitting bias could also be controlled for by restricting the complexity of the nuisance functions which would, however, prevent high-dimensional settings as well as usage of a variety of machine learning estimators or ensembles of those.151515For results in the context of the Lasso estimation under sparsity see [16]. Hence, the advantage of using sample-splitting is to allow for a high degree of complexity of the nuisance functions estimated by a wide class of machine learning estimators [75].

It follows that, theoretically, sample-splitting prevents overfitting and thus reduces the bias in the final causal estimator \parencitesChernozhukov2018cWager2018. At the same time, however, the variance of the estimator increases as less data is effectively used for estimation. Cross-fitting [29] and respectively double cross-fitting [100] have been proposed in the literature in order to reduce the variance loss induced by sample-splitting. In this procedure, the roles of the data parts get switched such that each part has been used for both the estimation of nuisances as well as the causal effect estimation. The final CATE estimator is then an average of the separate effect estimators produced. This method can be further extended to use more than splits denoted as -fold cross-fitting [29] with the final CATE estimator given as:

where is the CATE estimator based on the -th fold.161616Increasing the efficiency of a sample-splitting based estimator by swapping the roles of the data samples and averaging the resulting estimates goes back to [118] in the context of estimation of semi-parametric models.

The above theoretical arguments have a direct impact on the implementation of various meta-learning algorithms. Under the double sample-splitting the more models have to be estimated within the meta-learning algorithm, the more data splits are being implicitly induced, while the impact thereof in finite samples is not clear a priori as pointed out by [100]. As such, the researcher faces a typical bias-variance trade-off with respect to sample-splitting. In order to illustrate the issue it is instructive to decompose the MSE of a CATE estimator :

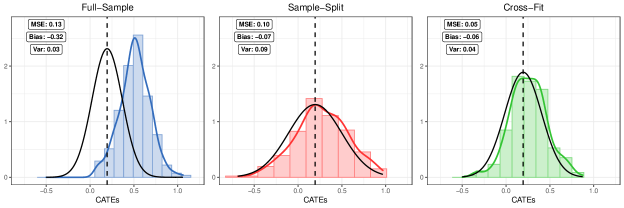

Naively using the full data sample for estimation of both the nuisance functions as well as the CATE function leads to a higher bias due to overfitting but at the same time to lower variance as all available data is used for estimation. Using sample-splitting eliminates the overfitting bias but results in higher variance due to less data being used for estimation. In contrast, cross-fitting both removes the overfitting bias and reduces the variance by effectively using all the available information from the data for estimation. Figure 1 illustrates this theoretical argument by contrasting the distributions of the CATE parameter under full-sample estimation, double sample-splitting and double cross-fitting, resulting from a Monte Carlo simulation based on a large training sample of observations (further details on the meta-learner and the simulation design are provided in Sections 3.2 and 4, respectively). We observe that the theoretical arguments can be documented in finite samples too. As such, the full sample version exhibits substantial bias due to overfitting as its distribution is shifted away from the true value of the CATE parameter, but with a rather low variance. On the contrary, the double sample-splitting version successfully eliminates the overfitting bias as the simulated distribution is centered around the true value of the CATE, however with much larger variance. Finally, the double cross-fitting version keeps the reduction in bias whilst having a much lower variance in comparison to the double sample-splitting version as the spread of the CATE distribution comes close to the full sample version, indicating the gain in efficiency of this procedure.

Apart from the illustrative example above, the empirical question remains the precise quantification of this bias-variance trade-off for various meta-learners and to what degree this might vary with different sample sizes. Different meta-learners use different nuisance functions in different ways which might have an influence on the performance under the particular estimation procedures. Even though sample-splitting and cross-fitting help to eliminate the overfitting bias, in finite samples less data available for estimation might even lead to higher bias due to errors in learning the CATE function itself, especially for small sample sizes. In this paper we address this open question via Monte Carlo simulations and compare the performance of various meta-learners under full-sample, double sample-splitting and double cross-fitting procedure for several different sample sizes to shed more light onto the finite sample properties. We follow [100] and choose the double sample-splitting, respectively double cross-fitting procedure due to its theoretically faster convergence rates. Furthermore, we opt for the setting with equally sized folds as suggested by [75]. Additionally, we always distinguish between the training and validation data. We use the training data for learning the nuisance function and the CATE function, including the double sample-splitting and double cross-fitting procedure, while we evaluate the CATEs on a set of new validation data. An illustration of the data usage under full-sample estimation, double sample-splitting and double cross-fitting procedure is provided in Figure 2.

Further motivation for the usage of sample-splitting and cross-fitting stems from the theoretical arguments for conducting statistical inference about the causal parameters of interest. As such, sample-splitting plays a crucial role in obtaining estimators that are not only approximately unbiased but also normally distributed which in turn allows for a valid construction of confidence intervals. In this vein, [29] provide results for the estimators of average treatment effect (ATE) that rely on sample-splitting and cross-fitting procedures. [124] and [149] extend this analysis for parametric and nonparametric estimators of group average treatment effects (GATEs), respectively. In the context of Causal Forests, [140], [87], and [9] also rely on sample-splitting procedures termed ‘honesty’ to provide inference for causal effects on various levels of aggregation. Nonetheless, in the context of meta-learning estimation of causal effects, there appears to be lack of unifying model-free theory for conducting statistical inference so far. One exception is the study by [86] that analyses various versions of bootstrapping for estimation of standard errors for the CATEs. Recently, [69] makes use of such bootstrapping procedures to construct confidence intervals in an empirical application. Besides the computational burden, however, none of the bootstrapping procedures studied by [86] seems to reliably provide accurate coverage rates. However, the meta-learners analyzed in [86] do not make use of sample-splitting, which could potentially improve the performance of the bootstrapping for estimation of standard errors, given the insights from the related literature. While we do study the properties of the distribution of the CATEs within the simulation experiments in Section 4, we do not further analyse the estimation of standard errors mainly due to computational reasons and focus primarily on the point estimators. However, apart from the computational aspects, we note that combining sample-splitting and cross-fitting with bootstrapping for statistical inference about causal effects within the meta-learning framework might be a promising avenue for future research.

3.2 Meta-Learners

In the following, we review the meta-learning algorithms for estimation of heterogeneous treatment effects and discuss their advantages and disadvantages in particular empirical settings.

3.2.1 S-learner

The first meta-learning algorithm we investigate is the S-learner as denoted by [86]. The early ideas of the S-learner stem from the marketing

literature on uplift modelling [92] and the epidemiology

literature, where the S-learner is also being referred to as

g-computation \parencitesRobins1986Snowden2011. More recently,

the S-learner has been proposed for the estimation of heterogeneous treatment

effects based on the Regression Trees [5] and Random

Forests [93] as well as their

Bayesian versions, i.e. BART \parencitesHill2011Green2012. According to the naming

convention of [86], S- stands for Single as this

meta-learner involves only one single model, namely the response

function, , that needs to be estimated. The final causal

effect is, in this case, obtained as a difference between predictions of the

response function with setting the treatment indicator to and

, respectively.171717Similar notion of predicted difference in the scope of model interpretation has been proposed by [77]. The algorithm can be described as follows:181818As a matter of notation, we refer to the training data used for

model estimation with superscript T as

and the validation data used for effect prediction with superscript

V as .

As can be seen from Algorithm 1, the S-learner does not assign any special role to the treatment indicator within the estimation procedure and uses it only post hoc in the computation of the causal effect. Thus, if the treatment indicator is not strongly predictive for the outcome the S-learner will tend to estimate a zero treatment effect.191919[86] argue that the S-learner is actually biased towards zero. Nevertheless, the S-learner will perform particularly well if the true CATE function is indeed zero, i.e. if , which has also been documented in the simulation experiments of [86]. For the forest based S-learner, [84] proposes a modification of the algorithm such that it shrinks towards the ATE instead of zero by performing a Ridge regression in the final leaves of the trees within the forest.202020For a detailed explanation of this procedure see [84]. In our simulations, we study a simpler modification of the forest based S-learner by always including the treatment indicator in the random subset of covariates when determining the splits. By doing so, we always give the S-learner the chance to split on the treatment indicator which might potentially alleviate the zero-bias issue. We will henceforth denote such learner as the SW-learner, where the W reflects the enforcement of the treatment indicator into the splitting set of covariates. We discuss the behaviour of the SW-learner more closely throughout the simulation results in Section 4.3. Furthermore, notice that the Algorithm 1 consists of only one nuisance function that needs to be estimated and thus does not require any sample-splitting or cross-fitting within the training sample induced by multiple nuisance functions, hence it always has access to the full sample of the training data.212121Nevertheless, an optional additional sample-splitting or cross-fitting could potentially improve the performance of the S-learner by reducing the possible overfitting of the base learner as such. This is, however, beyond the scope of our analysis and is left for future research. However, from a theoretical perspective, [1] show that modelling the CATE as a single response function as in the S-learner is not optimal in terms of achieving the fastest convergence rate as this depends on the complexity, defined as sparsity-to-smoothness ratio, of the response functions in the treated, , and the control sample, , and pooling these into a single response function enforces the complexity for treated and controls to be the same.

3.2.2 T-learner

The T-learner is another common and widely used meta-learner that we

investigate in our study. Similarly to the S-learner, its early applications

emerged in the marketing literature on the uplift modelling \parencitesHansotia2002Radcliffe2007, while more recently it has been suggested for estimating

heterogeneous treatment effects in the fields of medicine [42]

and econometrics [5].

In the econometric literature it is sometimes also called

as the basic [87], plug-in [75] or naive [101] CATE estimator.

According to [86], T- stands for Two as

this meta-learner involves two models that need to be estimated,

defined by the treatment indicator . These are namely the

response function in the treated sample, , and the response

function in the control sample, . This is in contrast to the

above S-learner which pools the two response functions into a single

one. However, similarly to the S-learner the causal effect is computed

as a difference in predictions of the two response functions, which

is motivated by the identification result as in Equation (2.4).

The algorithm can be summarized as follows:222222Notationwise, we refer

to a subset of the data defined by a specific value of the variable as

for example by a subscript as .

Hence the T-learner uses the treatment indicator to split the estimation of the response function into two parts. This procedure is expected to work particularly well if the CATE function is complicated and there are no common trends in the response functions. This phenomenon finds supportive evidence in several simulation studies \parencites(see for example)()Kunzel2019Jacob2020Curth2021[or][]Nie2021a. Nonetheless, it is expected to work rather poorly if the CATE function is simple, as the response functions are not trained jointly and thus their difference might be unstable \parencitesLechner2019Kennedy2020Nie2021a. In terms of the estimation of the nuisance functions, the T-learner behaves similarly to the S-learner, as only the response functions need to be estimated to compute the CATE. As such no additional sample-splitting induced by multiple nuisance functions is required as the response functions are themselves estimated on separate samples defined by treated and control.232323Again, this does not preclude that an optional sample-splitting or cross-fitting might be beneficial for the same reason as in the case of the S-learner [[]provides some results on this issue for the T-learner]Jacob2020. Using an honest forest as a base learner would also add an implicit sample-splitting procedure, however, this is not analysed herein. Theoretically, the convergence rate of the base learners for estimating the response functions directly translates into the rate for estimating the CATE \parencitesKunzel2019Kennedy2020 and thus depends on the complexity, i.e. the dimension and the smoothness, of the response functions [1].242424For a detailed analysis of the optimal minimax rates for the T-learner, we refer to [1] and [86].

3.2.3 X-learner

The above mentioned problems of the T-learner are aggravated if

the treatment assignment is highly unbalanced, meaning that the vast majority

of observations in the sample belongs to only one treatment status.

[86] therefore propose the X-learner which

addresses this issue. The X-learner builds on the T-learner and, as such,

first estimates the two response functions and

. It then uses these estimates to impute the unobserved

individual treatment effects for the treated, , and

the control, .

The imputed effects are in turn used as pseudo-outcomes to

estimate the treatment effects in the treated sample, , and

the control sample, , respectively. The final CATE estimate

is then a weighted average of these treatment effect

estimates weighted by the propensity score, .252525In the

original definition of the X-learner, the estimation of the propensity

score is not exactly specified as it could be any weighting function

in general. However, in practice the estimation of the propensity

score is recommended [86]. Thus the X-learner

additionally uses the information from the treated to learn about the

controls and vice-versa in a Cross regression style, hence the

X term in its naming label. The learning algorithm can be

detailed as follows:

According to Algorithm 3, the X-learner, in contrast to the T-learner, firstly uses the response functions for imputing the unobserved individual treatment effects instead of directly estimating the CATE. Secondly, these imputed individual treatment effects are used for estimating the CATE and reweighted by the propensity scores. The reweighting helps to put more weight on the treatment effects which have been estimated more precisely, i.e. the ones coming from the larger treated or control sample, respectively. For this reason, the X-learner is expected to work particularly well in unbalanced settings, which is often the case in practice as the share of treated might be restricted financially or otherwise \parencites(see)()Arceneaux2006Gerber2008Broockman2016[or][for such unbalanced empirical settings]Goller2020. Furthermore, by directly estimating the treatment effects in the second step it enables the estimator to learn structural properties of the CATE function from the data and is thus expected to work well if the CATE function is approximately linear or sparse [86]. Theoretically, [86] indeed prove that the X-learner achieves a faster convergence rate than the T-learner in cases where the treatment assignment is highly unbalanced or when the CATE function is linear. Even if no assumptions about the CATE function are imposed, the X-learner can be proven to achieve the same rate as the T-learner. This hinges on regularity conditions such as the Lipschitz continuity of the response functions.262626More specifically, [86] prove that the X-learner can indeed achieve the parametric rate if the CATE function is estimated by OLS, while the nuisance functions can be estimated at any nonparametric rate. Furthermore, they prove that the X-learner achieves the minimax optimal rate if both the nuisance functions and the CATE function are estimated via -NN regression. In simulations of [86] the X-learner performs reasonably well even in other non-favourable settings. Notice further that Algorithm 3 requires more estimation steps than the previous two meta-learners. Additionally to the estimation of the response functions, the X-learner requires the estimation of the treatment effect functions as well as the propensity score function. This raises the question of possible overfitting and hence the need for sample-splitting and cross-fitting, respectively. However, there is theoretically no explicit requirement for sample-splitting in the case of the X-learner when estimating the nuisance functions, apart from training and validation data split [86]. Yet, it might well be that the sample-splitting and further cross-fitting have a non-negligible influence on the performance of the learner in finite samples. We address this issue by implementing the double sample-splitting and double cross-fitting version of the X-learner in the simulation study. For the case of the full-sample estimation we use the out-of-bag predictions of the underlying forest as estimates of the nuisance functions as recommended by [93] and [8]. The out-of-bag predictions are based on the observations that have been left ‘out of the bag’ when drawing bootstrap samples to estimate the trees of the forest [56]. Such observations, however, randomly appear both as training as well as validation observations across the trees of the forest and thus such out-of-bag predictions are neither the classical in-sample fitted values nor proper out-of-sample predictions and should not be confused with the ‘honest’ predictions. We use the out-of-bag predictions for all meta-learners within our analysis.

3.2.4 DR-learner

Although the X-learner makes use of the estimation of multiple nuisance

functions, it does not provide the double robustness property which

exploits the fact that the estimator remains consistent if either the

response function or the propensity score function is misspecified

\parencitesKennedy2017Lee2017. Recently, [75] proposed the

DR-learner where DR symbolizes the

Double Robustness property of the learner. The DR-learner

constructs a doubly robust score in the first estimation stage and

estimates the CATE in the second stage. There have been many other

versions of the DR-learner proposed in the literature, but these were

restricted to a particular estimator used in the second stage and are

thus not part of the meta-learning framework. For example,

[124] propose a linear estimation of the CATE function,

whereas a local-constant estimation is proposed by [149]

and [40], which works well for the estimation of GATEs,

i.e. for low-dimensional conditioning set. The main advantage of the

DR-learner in comparison to the other versions lies in the general

model-free second stage estimation of the CATE function. However,

common to all versions in the literature is the estimation of the doubly

robust score272727Also called efficient score or efficient

influence function in the literature \parencitesRobins1995Hahn1998. by

machine learning methods in the first stage also known as Double

Machine Learning [29]. For a comprehensive overview

of the CATE estimators building on the doubly robust score see

[79]. The specific algorithm for the DR-learner is then

defined as follows:

As can be seen in Algorithm 4 above, the DR-learner estimates the very same nuisance functions, and , as the X-learner but uses them in a completely different manner. It combines the nuisance functions as well as the outcome and treatment data in a doubly robust way to construct the pseudo-outcome , i.e. the doubly robust score. The score is then regressed on the covariates to estimate the final CATE function. Therefore, the DR-learner can also adapt to structural properties of the CATE such as smoothness or sparsity. For this reason the DR-learner is expected to work well in similar situations as the X-learner with a more balanced treatment assignment, as too extreme propensity scores might possibly yield the estimator unstable \parencitesHuber2013Powers2018, especially in high dimensions [35]. Moreover, it should have an additional advantage over the X-learner thanks to its double robustness property. The theoretical analysis of [75] uses the double sample-splitting procedure in order to derive a sharp error bound that rests only on stability conditions for the estimation of the CATE function. The theoretical results then exploit the rate double robustness which allows for faster error rates for the second-stage CATE estimation under weaker rate conditions for the first-stage estimation of the nuisance functions. The simulations of [75] also suggest a faster convergence rate of the DR-learner in comparison to the X- and T-learner. In order to achieve the optimal rates282828[75] shows that the DR-learner achieves the minimax optimal rate under smoothness or sparsity conditions for the nuisance and the CATE functions. the DR-learner explicitly requires the double sample-splitting as defined by [100], while the double cross-fitting procedure remains optional. Theoretically it is not clear how important the role of the optional cross-fitting is for the DR-learner in finite samples and how much of the efficiency loss due to sample-splitting can be thereby regained. In order to shed light on this issue we investigate the implementations of the DR-learner with double sample-splitting, double cross-fitting, as well as a version with full-sample estimation.

3.2.5 R-learner

Yet another approach of first estimating nuisance functions and then

using them to learn the treatment effects stems from the literature on

partially linear model originally developed by [112].

[101] build on these ideas to flexibly estimate heterogeneous

treatment effects and develop the R-learner, where the

R stands for the recognition of the contribution of [112]

as well as for the Residualization approach. In the first step,

the R-learner estimates the response function, ,

similarly to the S-learner but without conditioning on the treatment

indicator, as well as the propensity score function . It then

residualizes the outcome and the treatment by the predictions of the

response and the propensity score function, respectively, to construct a

modified outcome. In the second step, the R-learner regresses the

modified outcome on the covariates, weighted by the squared residualized

treatment292929An estimation procedure without the weighting step

is in literature referred to as the U-learner

\parencitesStadie2018Kunzel2019Nie2021a. However, such estimator

turned out to be quite unstable in the simulation experiments in

[101] as well as in those of [86] and will

thus not be considered further in our analysis., i.e.

, to estimate the CATE function

[120]. Analogous transformation of the outcome is also

used by the Causal Forest of [9] termed local

centering, or in the G-estimation for sequential trials by

[110]. The full estimation procedure of the R-learner can

be summarized as follows:

As follows from Algorithm 5, the R-learner separates the estimation into two steps. First, it eliminates the spurious correlations between the response function and the propensity score function and second, it optimizes the CATE function . From this standpoint the R-learner follows a related estimation scheme as the DR-learner and is expected to work well in similar settings where the nuisance functions as well as the CATE function might have a high degree of complexity. A possible advantage of the R-learner over the DR-learner might stem from the additional weighting which reduces the impact of extreme propensity scores as pointed out by [69]. In their simulation experiments, [101] show good performance of the R-learner in settings with complicated nuisance functions and rather simple CATE function. The theoretical analysis of [101] shows that the convergence rate of the R-learner depends on the complexity of the CATE function and is not affected by the complexity of the nuisance functions as long as they are estimated at sufficiently fast rates.303030For the case of estimating the CATE function via penalized kernel regression, [101] prove that the R-learner achieves the minimax optimal rate and additionally show that the X-learner does not achieve the optimal rate in general unless the treatment assignment is not highly unbalanced. Furthermore, for these theoretical results [101] explicitly require sample-splitting and cross-fitting, respectively. In particular, they advocate for a 5- or 10-fold cross-fitting procedure as defined by [29]. In order to examine the importance of the cross-fitting in finite samples we compare the performance of the R-learner as in the above cases with full-sample estimation, double sample-splitting and double cross-fitting, respectively.

4 Simulation Study

We study the finite sample performance of meta-learners for estimation of heterogeneous treatment effects based on Random Forests \parencites()()Breiman2001[see also][for a comprehensive introduction]Biau2016. The focus of the Monte Carlo study lies in an assessment of the influence of sample-splitting and cross-fitting in the causal effect estimation. For this purpose we compare the above discussed meta-learners estimated with full-sample, double sample-splitting, and double cross-fitting.

We rely on the Random Forest as the base learner for all meta-learners for several reasons. First, different meta-learners require estimation of different nuisance functions which involve different types of outcome variables. As such, the response functions mostly involve a continuous outcome variable whereas the propensity score function includes a binary outcome. Hence, when using Random Forests no additional adjustments need to be done in terms of estimation as it automatically estimates probabilities in case of binary outcome and expected values in case of continuous outcomes, respectively. This is in contrast to linear learners such as the Lasso [135], Ridge [59] or Elastic Net [151] where the estimator needs to be modified using appropriate link function for proper probability estimation [[, see for example]for the Logit-Lasso]Hastie2009. Second, Random Forest is a local nonparametric method which does not need any data pre-processing to flexibly learn the underlying functional form from the data [56]. Thus, Random Forest is able to approximate any function with different degrees of complexity which is often the case in treatment effect estimation where the nuisance functions tend to be rather difficult complex functions while the CATE function itself is often argued to be simple and sparse \parencitesKunzel2019Kennedy2020Sekhon2021. This is again an advantage in comparison to the linear learners mentioned above which become more flexible once an augmented covariate set consisting of polynomials and interactions is created and thus can be regarded as global nonparametric methods [56]. Third, in contrast to other flexible state-of-the-art machine learners such as Neural Networks the theoretical properties of Random Forests are better understood which makes it less of a black-box method [[, see] for a discussion of statistical properties of Random Forests]Meinshausen2006, Biau2012, Wager2014, Wager2014a, Scornet2015, Mentch2016, Wager2018, Athey2019. In particular, [122] prove the consistency of the original Random Forest algorithm as developed by [24] that we employ in our simulations, without relying on the ‘honesty’ condition.313131The consistency (in MSE) result holds under the condition that the number of leaves is smaller than the number of observations. In our simulations, we ensure this by growing trees with minimum leaf size bigger than 1 (see Table 1). We refrain from the honesty feature to avoid additional sample-splitting that would further reduce the effective sample size. This is important as the consistency of the base learner is a fundamental condition shared across all considered meta-learners. [122] also show that Random Forests can effectively adapt to sparsity of the underlying model, which we explicitly make use of within our simulation design. Additionally, another reason why we do not use the Lasso and linear learners as such is due to a substantial increase in variance as they are prone to outliers as documented in the simulation studies of [68] as well as [81]. Furthermore, Random Forests are a popular choice as a base-learner in empirical studies using meta-learners too \parencitesDuan2019Knaus2020b. Lastly, from the practical standpoint there is a vast variety of fast and reliable software implementations of Random Forests which makes it easy to use for practitioners.323232In our simulations we use the R-package ranger which provides a fast C++ implementation of Random Forests, particularly suited for high-dimensional data [143]. Further options in the R language [107] include the grf package written by [134], the forestry package by [85] or the randomForest package by [91].

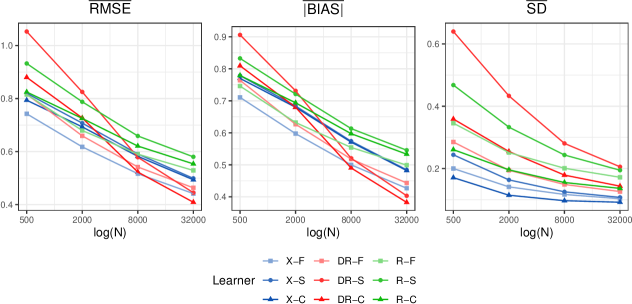

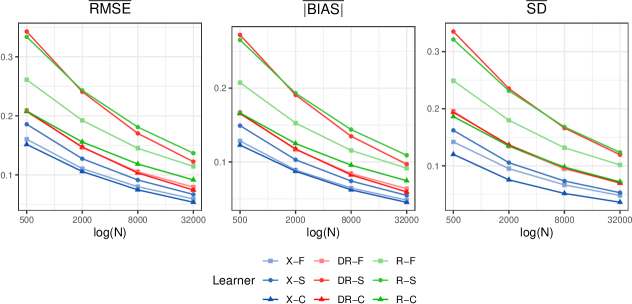

In order to objectively evaluate the performance and the robustness of different meta-learners in estimating heterogeneous treatment effects with regard to the double sample-splitting and double cross-fitting, we design several simulation scenarios. On the one hand, for each meta-learner we construct such a data generating process (DGP) that suits the particular advantages of the respective meta-learner, i.e. we design a simulation scenario where each meta-learner is expected to work best. Hence, we are able to check if the particular meta-learner outperforms the others and how big the performance discrepancies are for the other meta-learners in comparison to the expected best performing meta-learner. On the other hand, we design a simulation scenario with a complex DGP where none of the meta-learners has a priori an explicit advantage, which serves as our main simulation design of interest. Thus we can compare the performance of the meta-learners in an objective manner and quantify the deviations to their respective best performance cases. Furthermore, common to all DGPs is the observational study design, i.e. there is always selection into treatment and thus all considered meta-learners have to deal with confounding and not only with modelling the treatment effect itself. Moreover, in contrast to many simulation studies where the nuisances are simple low-dimensional functions \parencitesWager2018Kunzel2019Kennedy2020, we model all nuisance functions as highly non-linear but sparse functions with large-dimensional covariate space to test the potential of the machine learning methods, though still largely obeying the theory induced limitations. For other complex simulation designs see also [68] or [150] as well as [87] and [81] for the Empirical Monte Carlo Studies. Importantly, in order to study the approximate convergence rates of the meta-learners we repeat each simulation scenario several times with increasing training sample sizes using . We emphasize that the considered sample sizes substantially exceed the ones from previous simulation studies devoted to the analysis of sample-splitting methods, which were limited to [68] and [150] observations, respectively. Furthermore, the large samples enable us to study the performance of the meta-learners in settings in which the application of machine learning methods is arguably more relevant. We choose to always quadruple the sample size, which allows us to easily benchmark the results with the parametric rate, in which case the estimation error is expected to halve with each increase of the sample size. We then evaluate the performance measures on a validation set with sample size of to reduce the prediction noise as is usual in many Monte Carlo studies \parencitesJanitza2016Hornung2017Okasa2019Jacob2020Knaus2021. Lastly, in terms of the tuning parameters for the Random Forest base-learner we stick to the default, in the literature commonly used settings, corresponding to trees, the number of randomly chosen split variables set to the square root of number of features, and the minimum leaf size equal to .333333We refrain from cross-validation or other tuning parameter optimization procedures due to computational constraints. We recommend such optimization in the applied work as it might considerably improve the performance of the estimator [[, see]for an evidence based on Neural Networks]Curth2021, however, for the purposes of the simulation study it would not change the relative ranking of the meta-learners as each of them uses the very same base learner. Finally, for each DGP we simulate the training data times in total, where we use replications for the smallest sample size and decrease the number of replications down to for the largest sample size, due to computational reasons.343434Notice, however, that we only halve the number of replications while quadrupling the sample size and as such we may limit a possible deterioration of the performance in terms of the simulation error. A similar strategy for balancing the precision and the computational burden has been used in the simulations by [87], [93] or [81]. Detailed results on the simulation error are provided in Appendix B.2.

4.1 Performance Measures

For the evaluation of the performance of the considered meta-learners with regard to the sample-splitting and cross-fitting in detail, we employ several evaluation measures. First, to assess the overall estimator performance we compute the root mean squared error for each observation from the validation sample over the simulation replications:353535We take the square root of the MSE to have the same scale as for the other performance measures, i.e. the absolute bias and the standard deviation.

Next, we decompose the root mean squared error and evaluate the bias and variance component separately to contrast the theoretically expected asymptotic behaviour of sample-splitting and cross-fitting with the finite sample properties. Hence, we additionally compute the mean absolute bias:

as well as the standard deviation of the treatment effects:

Furthermore, inspired by the simulation study of [81] we also compute the Jarque-Bera statistic \parencitesJarque1980Bera1981 to test for the normality of the treatment effect predictions:363636See [131] for a discussion of the Jarque-Bera test and its comparison to other tests for normality.

where and is the skewness and the kurtosis of the treatment effect predictions for observation , respectively. As a matter of presentation for CATEs, we report the mean values of the RMSE, absolute bias, standard deviation and the Jarque-Bera statistic over validation observations.373737As such, we define the average RMSE as and analogously for the remaining performance measures. Additionally, for the Jarque-Bera statistic we report also the share of CATEs from the validation sample for which the normality gets rejected at the 5% confidence level. For details, see Appendix B.2. Additionally, we provide evaluation of further performance measures in Appendix B.2.

4.2 Simulation Design

In the general simulation design we follow [86] and specify the response functions for potential outcomes under treatment, , and control, , the propensity score, , and the treatment effect function, , respectively. First, we simulate a -dimensional matrix of covariates drawing from the uniform distribution, as previously used in simulations of [140], [86] or [101] among others, such that:

and defining the correlation structure according to [39] using a random correlation matrix generated by the method of [72].383838For a detailed correlation heat map of the covariates and descriptive statistics of the simulated datasets see Appendix A. Second, we specify the response functions and simulate the potential outcomes as:

with errors that are independent of the covariates . Third, we define the propensity score function and simulate the treatment assignment according to:

and use the observational rule to set the observed outcomes such that:

to complete the observable triple . The subsequent simulation designs then differ only with respect to how the corresponding functions, namely and are specified. For all of our simulations we define the response function under non-treatment according to the well-known Friedman function ([*]Friedman1991) to create a difficult yet standardized setting, which has been used also in the simulations of [19] and [101], as follows:

| (4.1) |

hence effectively creating a highly non-linear but sparse response function which is difficult to estimate on its own.393939Note that refers to the mathematical constant, i.e. . The response function under treatment is then defined simply as:

while we vary the specification of the treatment effect function throughout our simulation designs. Lastly, we model the propensity score function similarly to [140] and [86] using the distribution with parameters and such that:

| (4.2) |

while the scale parameter controls the share of treated in the sample and at the same time helps to bound the resulting probabilities away from and and thus to avoid extreme propensity scores which might yield some meta-learners using such propensities for reweighting unstable \parencitesHuber2013Powers2018. We additionally make the propensity score dependent on features of dimension in a non-linear fashion using the functional form specification of [101] and set:

which creates a non-linear setting that is hard to model as opposed to, e.g. polynomial transformations alone. Similarly, such non-linear transformations for the propensity scores using the sine function have been used also in simulations by [87] and [81].

| General Settings | |

|---|---|

| Number of DGPs | 6 |

| Number of Replications | |

| Training Sample | |

| Validation Sample | |

| DGP Settings | |

| Covariate Space Dimension | |

| Signal Covariates in Response Function | |

| Signal Covariates in Propensity Score Function | |

| Signal Covariates in Treatment Function | |

| Forest Settings | |

| Number of Trees | |

| Random Subset of Split Covariates | |

| Minimum Leaf Size | |

As a matter of notation we refer to as the dimension of the covariate space, , and as the dimension of the signal covariates in the response function, the propensity score function, and the CATE function, respectively. We set the aforementioned dimensions as follows: , , and varies with forthcoming simulation designs. We note that such large-dimensional covariate set is quite unique as the majority of simulation studies relies on low-dimensional covariate sets \parencites(see e.g.)()Kunzel2019Jacob2020[or][]Nie2021a.404040An exception is the simulation study of [105] who explicitly study the estimation of heterogeneous treatment effects in high-dimensions. We further define the sets of covariates such that . By doing so we make it difficult for the meta-learners to accurately fit the functions and eliminate the spurious correlations between the response and propensity score functions. Moreover, it also becomes a non-trivial task to disentangle the confounding effects from the actual treatment effect heterogeneity which the herein discussed meta-learners are specifically designed for. Finally, a general overview of the simulation study is provided in Table 1.

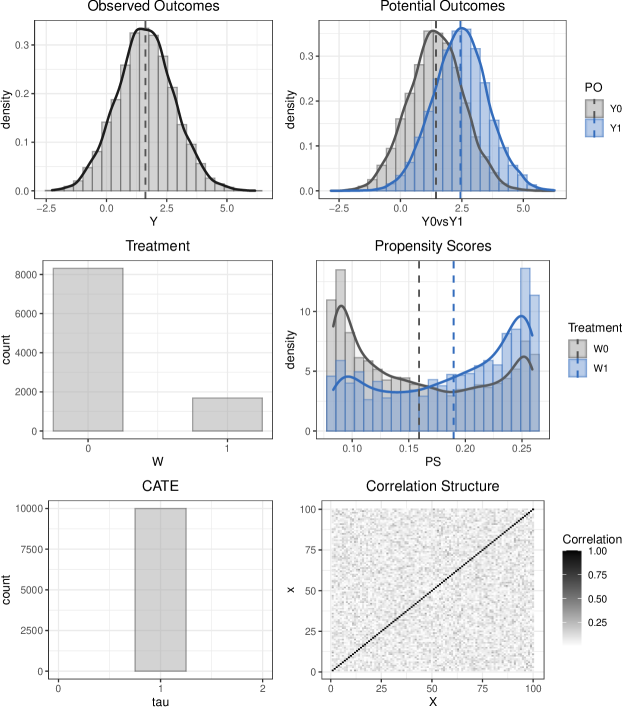

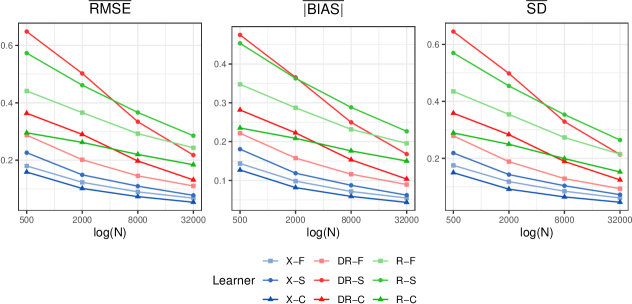

4.2.1 Simulation 1: balanced treatment and constant zero CATE

The first simulation design features our complicated sparse non-linear nuisance functions as defined above in Equations (4.1) and (4.2) in contrast to a very simple CATE function. In fact, the treatment effect here is defined as being constant and equal to zero:

with a balanced treatment assignment with the scaling factor which results in approximately 50% treated and 50% of control units. Such DGP with zero CATE serves as a benchmark and should implicitly suit the S-learner as the treatment indicator is not predictive for the outcome. Nevertheless the other meta-learners with the exception of the T-learner should be also capable of capturing the true zero effect as this is often a showcase example when motivating the particular meta-learners as well as simulating their performance \parencites(see)()Kunzel2019Kennedy2020[and][for details]Nie2021a.

4.2.2 Simulation 2: balanced treatment and complex nonlinear CATE

In the second simulation design we keep the balanced treatment allocation but feature a highly complex and non-linear CATE function resulting from a completely disjoint DGPs for the response function under treatment and under control. As such the response function under control is defined according to Equation (4.1), while the response function under treatment is defined as a non-zero constant, i.e. . The CATE is then defined as:

Such simulation setups have been previously used also in [86] or in [101]. In this case the response functions, and , are uncorrelated and thus there is no advantage in pooling those two together. Rather, estimating these two functions separately is the best strategy as there is nothing additional to learn from the other treatment group. For this reason, the T-learner should perform best here, however the meta-learners which also estimate the response functions separately such as the X- and DR-learner are expected to perform well too. Clearly, other meta-learners such as the S- and R-learner which estimate the pooled response function have a disadvantage as they first need to learn the disjoint structure.

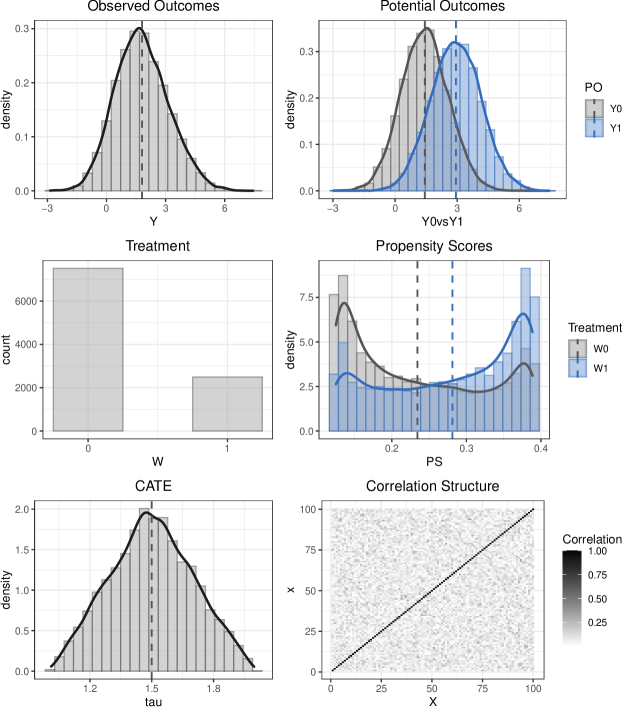

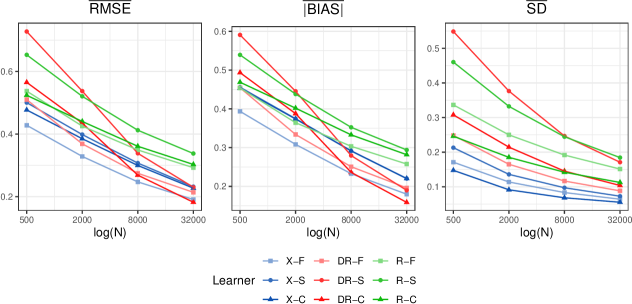

4.2.3 Simulation 3: highly unbalanced treatment and constant non-zero CATE

In our third simulation design we change the scaling factor in the propensity score function to such that we generate approximately 15% treated units.414141In contrast to [86] we do not specify the treatment imbalance as extreme as 1% treated mostly for computational reasons. Due to our smallest sample size of used in the simulations and the double sample-splitting procedure, it might occasionally happen that the estimated propensity scores would be exactly zero which would prevent estimation of the DR-learner as well as the R-learner due to the division by zero when constructing the pseudo-outcomes. In our specification, even with the share of the treated being in expectation, the aforementioned issue with zero propensity scores still might occur. In such cases, we redraw the sample to ensure at least of treated. However, this occurs only a handful of times out of 2000 draws in total and only for the smallest sample size considered. [101] also use similar restrictions on the propensity scores in their simulations due to the very same issue. We then model the treatment effect as a constant as for example in [75] or [101] and thus create a scenario with highly complicated nuisance functions and very simple CATE function given as:

Accordingly, the X-learner should perform best in this scenario given the high imbalance in the treatment assignment and the sparse CATE function at the same time. In contrast, other meta-learners using the propensity score for reweighting such as the DR- and R-learner might perform worse due to potentially extreme propensity scores close to the bounds. Furthermore, the T-learner is clearly disadvantaged in this scenario due to the high treatment imbalance as well as due to the simple CATE function, whereas the S-learner is not expected to work particularly well either due to the relatively bigger effect size bounded away from zero.

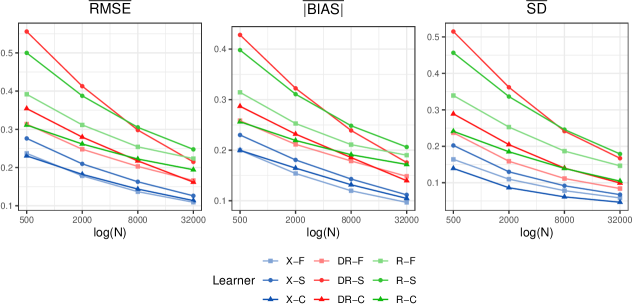

4.2.4 Simulation 4: unbalanced treatment and simple CATE

In our fourth simulation design we model the CATE function similarly to the above design as a simple non-zero constant and combine it with an indicator function as also used by [86] to add more structure to the CATE. As such we define the treatment effect as:

and otherwise keep the DGP same as in the third design while only increasing the share of treated to roughly 25% as is the case in the simulations of [101] by setting . By doing so we should theoretically shift the advantage from the X-learner more onto the DR-learner as both meta-learners are motivated by complex nuisance functions and a simple CATE function with the difference of the X-learner being designed particularly for highly unbalanced treatment allocation. Also the R-learner is expected to perform relatively well in this scenario due to the less unbalanced treatment shares, whereas the S- and T-learner are not expected to perform well for the same reasons as in the above situations.

4.2.5 Simulation 5: unbalanced treatment and linear CATE

The fifth simulation design features the same nuisance functions and treatment share as the fourth design, however, here instead of the indicator function we model the treatment effect as a low-dimensional linear function as:

as used in one of the simulation designs of [101] where the R-learner performed best and as such it is also expected to have an advantage here. Yet again the X- and DR-learner should perform comparatively well in this setting while the S- and T-learner not so much for the very same reasons as stated above.

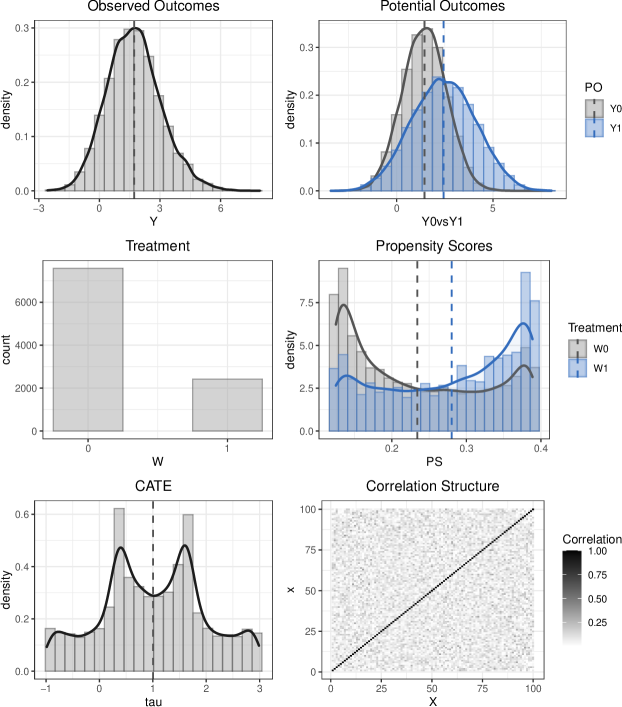

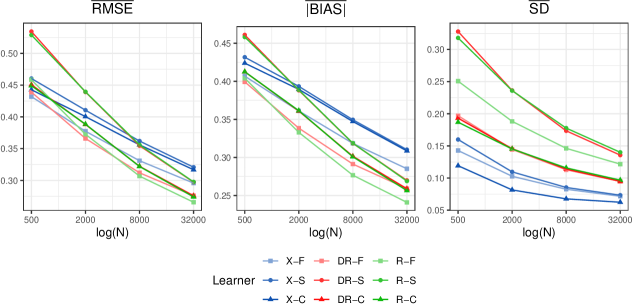

4.2.6 Main Simulation: unbalanced treatment and nonlinear CATE

In the last simulation design we create the most complex scenario in which none of the meta-learners has an a priori advantage and thus presents our main simulation design of interest. In this case not only the nuisances but also the CATE itself is modelled as a smooth non-linear function of a slightly larger dimension than in the previous settings, i.e. . Following [140] we specify the CATE function as follows: