Learning Stationary Nash Equilibrium Policies in -Player Stochastic Games with Independent Chains

Abstract

We consider a subclass of -player stochastic games, in which players have their own internal state/action spaces while they are coupled through their payoff functions. It is assumed that players’ internal chains are driven by independent transition probabilities. Moreover, players can receive only realizations of their payoffs, not the actual functions, and cannot observe each other’s states/actions. For this class of games, we first show that finding a stationary Nash equilibrium (NE) policy without any assumption on the reward functions is interactable. However, for general reward functions, we develop polynomial-time learning algorithms based on dual averaging and dual mirror descent, which converge in terms of the averaged Nikaido-Isoda distance to the set of -NE policies almost surely or in expectation. In particular, under extra assumptions on the reward functions such as social concavity, we derive polynomial upper bounds on the number of iterates to achieve an -NE policy with high probability. Finally, we evaluate the effectiveness of the proposed algorithms in learning -NE policies using numerical experiments for energy management in smart grids.

Index Terms:

Stochastic games, stationary Nash equilibrium, dual averaging, dual mirror descent, Nikaido-Isoda function, learning in games, smart grids.I Introduction

Since the early work on the existence of a mixed-strategy Nash equilibrium in static noncooperative games [1], and its extension on the existence of stationary Nash equilibrium policies in dynamic stochastic games [2], substantial research has been done to develop scalable algorithms for computing Nash equilibrium (NE) points in static and dynamic environments. NE provides a stable solution concept for strategic multiagent decision-making systems, which is a desirable property in many applications, such as socioeconomic systems [3], network security [4], and routing and scheduling [5], among many others [6, 7].

In general, computing NE is PPAD-hard [8], and it is unlikely to admit a polynomial-time algorithm. Thus, to overcome this fundamental barrier, two main approaches have been adapted in the past literature: i) searching for relaxed notions of stable solutions, such as correlated equilibrium [9], which includes the set of NE; and ii) searching for NE points in special structured games, such as potential games [10] or concave games [11]. Thanks to recent advances in the field of learning theory, it is known that some tailored algorithms for finding relaxed notions of equilibrium in case (i) can also be used to compute NE points of structured games in case (ii). For instance, it is known that the so-called no-regret algorithms always converge to the set of coarse correlated equilibria [7], and they can also be used to compute NE in the class of socially concave games [12]. However, such results have mainly been developed for static games, in which players repeatedly play the same game and gradually learn the underlying stationary environment. Unfortunately, extension of such results to dynamic stochastic games [2, 13], in which the state of the game evolves as a result of players’ past decisions and the realizations of a stochastic nature, imposes major challenges.

One major challenge that makes the learning task harder as one moves from static games to dynamic stochastic games is the level of uncertainty and nonstationarity introduced on players’ decision-making trajectories due to state dynamics. The reason is that players’ payoffs depend not only on the actions of others but also on the state of the game, which evolves stochastically as a function of players’ actions. Therefore, not only do the players need to learn about each other’s actions, but they also need to learn about the state trajectory to respond properly. In this work, we expand over the past literature and extend the existing results for learning stationary NE policies to a subclass of dynamic -player stochastic games with independent chains. Such games provide natural modeling for many applications, such as multiagent wireless communication [14, 15, 16], robotic navigation [17], and energy management in smart grids [18], among others [19, 20]. In this class of games, there are players, where each player has its own finite state space and finite action set . Moreover, the state-action transition matrices are assumed to be independent across players. However, the players are coupled through their reward functions such that the reward of player , denoted by , depends on the states and actions of all players.

I-A Related Work

While learning NE for two-player zero-sum static games has been long known in the literature with a variety of learning algorithms such as fictitious play or regret minimization dynamics, only recently these results have been extended to two-player zero-sum stochastic games [21, 22]. Moreover, learning NE in -player repeated static games under various assumptions on the payoff functions has been extensively studied in the past literature [12, 23]. However, these results mainly work for the static setting and cannot be applied directly to dynamic games with stochastic state-action transitions.

Recent advances in the field of reinforcement learning (RL) [17] have raised substantial interest in developing efficient learning algorithms for computing optimal stationary policies in single-agent Markov decision processes (MDP) [24, 25, 26]. MDPs are general frameworks that can model many real-world decision-making problems in the face of uncertainties [27, 17, 28]. Multiagent extensions of MDPs, in which multiple agents (players) want to maximize their payoffs while interacting under a random environment, have been studied using the framework of stochastic games (a.k.a. Markov games) [2]. However, the results for equilibrium computation in stochastic games are often much weaker than those for single-agent MDPs, mainly because of the nonstationary environment that is induced by players’ decisions [17]. In general, there are strong lower bounds for computing stationary NE in stochastic games that grow exponentially in terms of the number of players [29]. Therefore, prior work has largely focused on the special case of two-player zero-sum stochastic games [30, 19, 17, 31, 32, 22]. For instance, [21] provided finite-sample NE convergence result for independent policy gradient methods in two-player zero-sum stochastic games without coordination. More recently, [22] adapted the classical fictitious play dynamics with Q-learning for stochastic games and analyzed its convergence properties in two-player zero-sum stochastic games. However, their convergence results are asymptotic and do not provide any explicit convergence rate.

While two-player zero-sum stochastic games constitute an important basic setting, there are many problems with a large number of players, a situation that hinders the applicability of the existing algorithms for computing a stationary NE. To address this issue, researchers have recently developed learning algorithms for finding NE in special structured stochastic games. For instance, [33] shows that policy gradient methods can find a NE in -player general-sum linear-quadratic games. An application of RL for finding NE in linear-quadratic mean-field games has been studied in [34]. Moreover, [35, 36] show that -player Markov potential games, an extension of static potential games to dynamic stochastic games, admit polynomial-time algorithms for computing their NE policies. Unfortunately, the class of Markov potential games is very restrictive because it requires strong assumptions on the existence of a general potential function. In fact, even establishing the existence of such a potential function could be a challenging task [37, 38]. Motivated by numerous applications of large-scale stochastic games, in this work, we develop polynomial-time learning algorithms for computing NE policies for a natural class of payoff-coupled stochastic games with independent chains [16, 19].

This work is also related to a large body of literature on the mirror descent (MD) algorithm [39, 40], and its variant dual averaging (DA), also known as lazy mirror descent [41, 42]. Both MD and DA have been extensively used in online convex optimization [43, 41], online learning for MDPs with changing rewards [26], regret minimization [7], and learning of NE in continuous games [44, 45, 23, 46]. Although MD and DA algorithms share similarities in their analysis, DA algorithms are believed to be more robust in the presence of noise, while MD algorithms often provide better convergence rates [42]. For that reason, we will study both of these variants.

I-B Contributions

We consider the class of payoff-coupled stochastic games with independent chains and develop efficient decentralized learning dynamics toward computing their stationary -NE policies. Moreover, under certain assumptions on the reward functions, we show that the proposed learning dynamics converge almost surely or in expectation to a stationary -NE policy with nonasymptotic polynomial-time convergence rates. Our main contributions can be summarized as follows:

-

•

Using a reduction of such stochastic games to a static virtual game in terms of occupation measures, we show that for general reward functions, computing a stationary -NE policy is PPAD-hard, despite the independency of chains.

-

•

Leveraging the virtual game formulation for general reward functions, we devise novel polynomial-time learning algorithms, which converge in a weaker distance (namely, the averaged Nikaido-Isoda gap) to the set of -NE policies almost surely. In particular, we show that if the sequence of iterates converges with positive probability, it must be an -NE policy.

-

•

For reward functions that satisfy social concavity property, we show that for any , after at most episodes, their time-average policies will form an -NE policy with probability at least , where is a constant and the expected length of each episode is bounded above by , where is the worst mixing time of players’ internal chains across all stationary policies. Moreover, we improve this bound to for convergence in expectation to an -NE policy.

-

•

We extend our convergence results when the game admits a stable equilibrium and evaluate the effectiveness of the proposed algorithms in learning -NE policies using numerical experiments.

Our proposed algorithms are simple, easy to implement, and work in a fully decentralized manner. The players take action in the original stochastic game and observe their realized payoffs. They then use this information in the static virtual game, which is a compact representation of the original static game, to update their policies in the space of occupation measures. However, the virtual game can be played only once, and thus the existing learning algorithms for repeated static games such as [12] cannot be applied directly to compute a NE. Nevertheless, using a sampling method, we show how to repeatedly play over the original stochastic game and use the collected information in the virtual game to guide the learning dynamics to a NE. In addition to Markov potential games and linear-quadratic stochastic games, this work provides another subclass of -player stochastic games that, under some assumption on players’ reward functions, provably admit polynomial-time learning algorithms for finding their stationary -NE policies.

I-C Organization

In Section II, we introduce payoff-coupled stochastic games with independent chains. In Section III, we provide a dual formulation for such games and establish several preliminary results. In Section IV, we develop an algorithm for learning -NE policies. In Section V, we present our convergence results in terms of the averaged Nikaido-Isoda gap function to the set of -NE policies and without any assumptions on the reward functions and establish polynomial-time convergence rates in high probability or in expectation. In Section VI, we consider structured reward functions when they are socially concave or allow the existence of a stable equilibrium and obtain stronger polynomial-time convergence rates in terms of the Euclidean distance to the set of -NE policies. In Section VII, we provide simulations to evaluate the effectiveness of our proposed algorithm. Conclusions are given in Section VIII, and omitted proofs and auxiliary lemmas can be found in Appendix I.

II Problem Formulation

We consider a stochastic game with players, where each player has its own finite set of states and finite set of actions . We denote the joint state and action set of players by and , respectively. At any discrete time , we use and , respectively, to denote the (random) state and action of player . Similarly, we use and , respectively, to denote the joint state and action vectors for all players at time . Moreover, we let be the (random) reward received by player at time , where, without loss of generality, we assume that the rewards are normalized such that . At any time , the information available to player is given by the history of its realized states, actions, and rewards, i.e., . In particular, we note that player is not able to observe other players’ states and actions, nor can it access the structure of its reward function . At any time , player takes an action based on its information set and receives a reward , which also depends on other players’ states and actions. After that, the state of player changes from to a new state with probability , where the transition probability matrix is known only to player and is independent of other transition matrices.

A general policy for player is a sequence of probability measures over that at each time selects an action based on past observations with probability . Use of general policies is often computationally expensive, and in practical applications, players are interested in easily implementable policies. In that regard, the class of stationary policies constitutes the most well-known class of simple policies, as defined next.

Definition 1

A policy for player is called stationary if the probability of choosing action at time depends only on the current state , and is independent of the time . In the case of the stationary policy, we use to denote this time-independent probability.

Assumption 1

We assume that the joint transition probability can be factored into independent components , where is the transition model for player . Moreover, we assume that players’ policies belong to the class of stationary policies.111In fact, for single-agent MDPs, restriction to the class of stationary policies is without loss of generality, and the optimal policy can be chosen from stationary policies [47].

Given some initial state , the objective for each player is to choose a stationary policy that maximizes its long-term expected average payoff given by

| (1) |

where ,222More generally, given a vector , we let be the vector of all coordinates in other than the th one. and the expectation is with respect to the randomness introduced by players’ internal chains and their policies . As is shown in the next section, under the ergodicity Assumption 2, for any stationary policy profile , the limit in (1) indeed exists and equals (12). This fully characterizes an -player stochastic game with initial state , in which each player wants to choose a stationary policy to maximize its expected aggregate payoff . In the remainder of the paper, we shall refer to the above payoff-coupled stochastic game with independent chains as .

Definition 2

A policy profile is called a Nash equilibrium (NE) for the game if for any and any policy . It is called an -NE if for any and any policy .

III A Dual Formulation and Preliminaries

Here, we provide an alternative formulation for the stochastic game based on occupation measures. Intuitively, from player ’s point of view, its long-term expected average payoff depends on the proportion of time that player spends in state and takes action , denoted by its occupancy measure . Thus, the policy optimization for player can be viewed as an optimization problem in the space of occupancy measures, where players want to force their chains to spend most of their time in high-reward states. An advantage of optimization in terms of occupancy measures is that due to the independency of players’ internal chains, the payoff functions admit a simple decomposable form, which is easier to analyze than the original policy variables. We shall use this dual formulation to develop learning algorithms for finding a stationary -NE.

To provide the dual formulation, let us use to denote players’ stationary policies, where is the probability simplex over . We can write

| (2) | ||||

| (3) | ||||

| (4) |

where the third equality results from because players are using stationary policies that depend only on their own state. Moreover, the last equality holds because, by Assumption 1, one can show that (see Lemma 4).

On the other hand, following of a stationary policy by player induces a Markov chain over with transition probability

| (5) |

Thus, assuming that the Markov chain is ergodic, if we let be the stationary distribution of , we have . For any player , let us define to be the occupancy probability measure that is induced over its state-action set by following the stationary policy , that is

| (6) | ||||

| (7) | ||||

| (8) | ||||

| (9) |

In other words, is the proportion of time that the policy spends over state-action . Now, we can write the payoff function (1) as

| (10) | ||||

| (11) |

Combining (6) with the above relation shows that the payoff (1) can be written using occupation measures as

| (12) |

where is defined to be a vector of dimension whose -th coordinate is given by

Moreover, for fixed policies of other players with induced occupations , using (6) and (12), the optimal stationary policy for player is obtained by solving the MDP:

| (13) |

Lemma 1 ([47], Theorem 4.1)

Given any MDP and any feasible occupation measure over its set of state-action, one can define a corresponding stationary policy

| (14) |

such that following policy in that MDP induces the same occupation measure as over the state-action set , i.e., .

Therefore, using Lemma (1), the problem of finding the optimal stationary policies for the players reduces to one of finding the optimal occupation measures for them. To characterize the set of feasible occupation measures, from (6) we have , such that . Since is the stationary distribution of , we must have , which can be written in terms of occupation variables as . This fully characterizes the set of feasible occupation measures for player as the feasible points of the following polytope:

where is the indicator function. It is worth noting that since player knows the transition matrix , it can compute its occupation polytope a priori using at most linear constraints. Thus, the stochastic game can be equivalently formulated in a dual (virtual) form as defined next.

Definition 3

The virtual game associated with the stochastic game is an -player continuous-action static game, where the payoff function and the action set for player are given by and , respectively.

Proposition 1

The -player stochastic game admits a stationary NE policy. Moreover, finding a stationary NE for without any assumption on the reward functions is PPAD-hard.

Proof:

To find a stationary NE policy for , it is sufficient to find a pure-strategy NE in the static virtual game, in which case one can use Lemma 1 to obtain a stationary NE policy from . Thus, it is enough to show that the virtual game admits a pure-NE. This statement is also true by Rosen’s theorem [11] for concave games.333A continuous-action game is called concave if for each player and any fixed actions of the other players, the payoff function of player is concave and continuous with respect to its own action. Note that from (12), the payoff function of each player in the virtual game is concave with respect to its own action , and the action set is convex and compact.

Finally, in the special case where each player has only one state, i.e., , the virtual game reduces to a static -player noncooperative matrix game, in which the action set for player is given by , and the entries of the payoff matrix for player are given by . Then, an occupation measure for player can be viewed as a mixed strategy over its action set with the expected payoff function . Therefore, if we can find a stationary NE for in this special case, we can find a mixed-strategy NE in the virtual game. Since the latter is PPAD-hard [48], finding a stationary NE for without any assumption on the reward functions is also PPAD-hard. Q.E.D.

Using Proposition 1, it is unlikely that scalable learning algorithms can obtain a stationary NE in without imposing extra assumptions on the players’ reward functions . That is why in the remainder of this paper, we restrict our attention to the cases where players’ reward functions allow the existence of scalable learning algorithms. In fact, using the equivalence between the stochastic game and the virtual game, we shall focus only on developing learning algorithms to find an -NE for the virtual game. This, in view of Lemma 1 and continuity of the payoff functions, immediately translates to learning algorithms for finding a stationary -NE for the original game . However, we should note that for developing a learning algorithm, we cannot solely rely on the virtual game, which is a compact representation of . In other words, unlike , which can be played iteratively, the virtual game can be played only once, as it encodes the information of the entire horizon into a single-shot static game. Nevertheless, using a sampling method as in [25] that was given for single-agent MDPs, we show how to repeatedly play over and use the collected information in the virtual game to guide the learning dynamics to a NE.

IV A Learning Algorithm for -NE Policies

In this section, we develop our main learning algorithm for the stochastic game . We first consider the following assumption on the mixing time of players’ internal chains, which we shall impose in the remainder of this paper.

Assumption 2

For any player and any stationary policy chosen by that player, the induced Markov chain that is given in (5) is ergodic, and its mixing time is uniformly bounded above by some parameter ; that is, , for all .

In fact, Assumption 2 is a standard assumption used in the MDP literature [49, 50, 26], and is much needed to establish meaningful convergence results. Otherwise, if the transition probability matrix of a player is such that for some policy the induced chain takes an arbitrarily large time to mix, then there is no hope that player can evaluate the performance of policy in a reasonably short time.

Definition 4

Given a positive constant , we define to be the shrunk occupation polytope for player , where is the column vector of all ones of dimension . Similarly, for a vector of positive constants , we define .

The shrunk occupation polytope contains all feasible occupation measures for player with coordinates of at least . In fact, by restricting player ’s occupations to be in , we can assure that player uses stationary policies that choose any action with probability at least , hence encouraging exploration during the learning process. Thanks to continuity of the payoff functions, working with shrunk polytope with a sufficiently small threshold can only result in a negligible loss in players’ payoff functions.

Lemma 2

For any , there exist , such that any -NE for the virtual game with shrunk action sets is a -NE for the virtual game with action sets . In particular, can be determined by player independently of others and based only on its internal transition probability matrix .

Now we are ready to describe our main learning algorithm (Algorithm 1). The algorithm proceeds in different episodes (batches), where each batch contains a random number of time instances. Given any ,444Here, is an input parameter that can be set freely, and controls the accuracy of the final policies to form a stationary NE policy. each player first uses Lemma 2 to determine a threshold , and chooses an initial occupation measure . The occupation measure of player at the beginning of batch is denoted by ; during batch , player chooses actions according to the stationary policy that is obtained, using (14), from the occupation measure . A batch continues for a random number of time instances until each player has visited all its states at least once. Using Assumptions 2 and 1, a simple coupling argument shows that the expected number of time instances in batch can be upper-bounded by . The reason is that the length of batch equals the maximum cover time among Markov chains , whose expected value can be bounded, using Matthews method [51], by the number of states and the mixing time of those chains. Using the collected samples during batch , one can construct an (almost) unbiased estimator for the gradient of the payoff function . The estimator is then used in a DA oracle with an appropriately chosen step-size/regularizer to obtain a new occupation measure .

Input: Initial occupation measure , step-size sequence , a fixed threshold , initial dual score , and a strongly convex regularizer .

For , do the following:

-

At the end of batch , denoted by , compute

and keep playing according to this stationary policy during the next batch . Let be the first (random) time such that all states in are visited during . Batch terminates at time .

-

Let , and be a random vector (initially set to zero), which is constructed sequentially during the sampling interval as follows:

-

–

For and while , player picks an action according to , and observes the payoff and its next state . If , then update , and compute

(15) where is the basis vector with all entries being zero except that the -th entry is 1.

-

End For

-

–

-

In the end of batch , compute the dual score , and update the occupation measure:

(16)

End For

It is worth noting that the information structure of the game does not allow for centralized computations, as players cannot observe each others’ states and actions because of competition or privacy concerns (see Section VII for an example). Moreover, selfish players indeed have incentives to follow Algorithm 1. The reason is that each player is greedily and independently improving its aggregate payoff by observing its past rewards and using a regularized gradient ascent in the space of occupation measures.

Remark 1

The only point in Algorithm 1 that requires a small amount of coordination among players is the computation of . While this can be performed using a simple signaling mechanism, it can be further relaxed if players take to be a (logarithmic) factor of the maximum expected cover time , which, because of independency of chains, introduces a small biased term in the definition of -NE.

V Convergence Results Using Nikaido-Isoda Gap Function

In this section, we analyze the convergence and convergence rate of Algorithm 1 to a stationary -NE policy measured in terms of the Nikaido-Isoda gap function. The results of this section are general and hold without any assumption on the players’ reward functions. In the next section we specialize these results to specific types of reward functions to establish stronger convergence results. To that end, let us consider the following definition which allows us to measure the distance of the iterates of Algorithm 1 from a NE.

Definition 5

The Nikaido-Isoda function is given by

Remark 2

If ,555This maximum value is also known as the total gap function and has been used in the prior literature to measure the distance of an action profile to a NE [52]. then must be an -NE. This is because for any player and any we must have , which means that the maximum utility that any player can obtain by unilaterally deviating from to can be at most . Thus is an -NE for the virtual game with shrunk action set and by Lemma 2 it must be an -NE for the virtual game.

To analyze Algorithm 1, we first show that the estimator constructed at the end of batch is nearly an unbiased estimator for the gradient of player ’s payoff function. To that end, let us consider the increasing filtration sequence , which is adapted to the history of random variables . More precisely, we let contain all measurable events that can be realized up to the end of batch (i.e., until time ), such that is -measurable but is not. We have the following lemma.

Lemma 3

Let Assumption 2 hold and assume that each player follows Algorithm 1. Conditioned on , the expected reward vector that player computes at the end of batch satisfies

where the above inequality is coordinatewise, and the expectation is with respect to the randomness of players’ policies and their internal chains.

V-A Almost Sure Convergence with Dual Averaging Updates

Using the previous lemma, we are now ready to prove the following main theorem.

Theorem 2

Assume that the players’ regularizer functions are -strongly convex for some . Moreover, assume that the sequence of step-sizes satisfy ,666For simplicity, we are assuming that all players have the same sequence of step-sizes . Otherwise, all the results remain valid by writing the equations separately for each player . In fact, any sequence , where , satisfies the step-size condition of Theorem 2. and let . Given , if all players follow Algorithm 1 with , then as , almost surely

Proof:

If we define , due to the quasilinear structure of the payoff functions , for any we have

Therefore, we have

| (17) |

To upper-bound the right-hand side in (17), we use the Fenchel coupling as a Lyapunov function, where and is the convex conjugate of . By choosing and in Lemma 5, for any and fixed , we can write

By summing this inequality over , and rearranging the terms, and because , we obtain

| (18) |

Next, let us consider martingale difference sequences and , and use and to denote their corresponding zero-mean martingales, respectively. Then, we have

| (19) |

where the last inequality holds because . Similarly,

| (20) | |||

| (21) |

where the second inequality uses the Cauchy-Schwartz inequality, and the third inequality holds because . Thus, using the -bounded martingale convergence theorem [53] (Theorem 2.18), almost surely, we have

| (22) | ||||

| (23) |

Now, using the linearity of expectation and since is -measurable, we can write

| (24) | |||

| (25) | |||

| (26) | |||

| (27) |

where the last inequality uses (18). Moreover, using Lemma 3 and the Cauchy-Schwartz inequality, we have

| (28) |

where the last inequality follows from , , and the choice of . Thus, using (17), for any , we obtain

| (29) | ||||

| (30) | ||||

| (31) |

where the last inequality uses the Cauchy-Schwartz inequality and .

If we define a martingale difference , and its corresponding zero-mean martingale , we have

| (32) |

where the first inequality is obtained by using the triangle inequality, and the last inequality holds by the step-size assumption. Therefore, using the -bounded martingale convergence theorem [53] (Theorem 2.18), almost surely we have . Thus, we can write

Substituting the above relation into (29) and taking a maximum from both sides over , we obtain

| (33) | ||||

| (34) |

where the last inequality uses . Using (22) and since and , as , almost surely we have . Q.E.D.

One immediate corollary of the above theorem is that if with positive probability the sequence of occupation measures generated by Algorithm 1 converges to some limit point , then the stationary policy corresponding to is almost surely a stationary -NE for the game . The reason is that by continuity of with respect to its arguments and by conditioning on the event that , almost surely we have This in view of Remark 2 shows that must be an -NE for the virtual game. However, in the following theorem, we provide an alternative proof for this statement that requires weaker conditions on the choice of players’ stepsizes and the tuning parameter . The proof of this result is deferred to Appendix I.

Theorem 3

Given , let , and suppose that each player follows Algorithm 1 using a sequence of step-sizes that satisfy and , where . If with positive probability the sequence of occupation measures generated by Algorithm 1 converges to some point , then the stationary policy corresponding to the limit point is a stationary -NE for the stochastic game .

In fact, with extra effort, one can leverage the almost-sure convergence result of Theorem 2 to derive high-probability convergence rates for Algorithm 1 in terms of the averaged Nikaido-Isoda gap. This has been shown in the following theorem.

Theorem 4

Proof:

Let us consider the last expression (33) in the proof of Theorem 2, i.e.,

| (35) |

To establish high probability convergence rates, we can bound the terms in the above expression as follows. For , define the events , , and . Since , and are martingale sequences, and are nonnegative submartingales. Using Doob’s maximal inequality for submartingales [53] (Theorem 2.1), we have

| (36) | ||||

| (37) | ||||

| (38) | ||||

| (39) |

where the second equality holds because by conditioning on , it is easy to see that the expectation of the cross terms of a martingale different sequence equals zero. Similarly, we can write

| (40) | ||||

| (41) | ||||

| (42) |

where we note that for bounding , we have used the -norm version of Doob’s maximal inequality together with the triangle inequality. Finally, to upper-bound , we can write

| (43) | ||||

| (44) | ||||

| (45) | ||||

| (46) | ||||

| (47) | ||||

| (48) | ||||

| (49) | ||||

| (50) |

where in the above derivations is the first (random) time at which , and the fourth inequality uses the definition of and the fact that . Moreover, the last inequality holds because . Since , , and , we have

| (51) | |||

| (52) |

Now, given any , if we take , with probability at least , none of the events , and will occur, i.e., . Therefore, using (35), with probability at least , for every , we have

Thus, with probability , for any such that . Q.E.D.

V-B Expected Convergence Using Mirror Descent Updates

The results of Theorems 2 and 4 hold in an almost sure sense with a high-probability convergence rate. In particular, players can use any -strongly convex functions as the regularizer. For instance, if regularizers are taken to be quadratic functions , the policy update step in (16) reduces to a simple -norm projection on the shrunk polytope , which can be done quite efficiently in polynomial time. In particular, the use of a DA oracle in the structure of Algorithm 1 can potentially improve the performance of the learning algorithm in the presence of noise due to averaging of the dual scores. However, in this section we show that if players are allowed to choose specific regularizers (e.g., an entropic function), one can obtain improved convergence rates in expectation and independent of the parameters . Motivated by the natural policy gradient that achieves a fast convergence rate for solving MDPs [24], in the following theorem, we show that one can obtain a faster expected convergence rate by replacing the policy update rule (16) in Algorithm 1 with an MD oracle with Kullback-Leibler (KL) divergence as the regularizer. Of course, this speedup comes at the cost of a more complex projection in the final step (16) of Algorithm 1.

Theorem 5

Proof:

First, we note that, without loss of generality, we can normalize the rewards to be in by simply replacing each with . Such normalization only shifts players’ payoff functions by the same constant , and all the equilibrium analysis remains as before. In this way, we may assume . Now, if we use , , , and in the statement of Lemma 6 (see Appendix I), for any , we have

Taking a conditional expectation from this expression with respect to , we get

| (55) | ||||

| (56) | ||||

| (57) | ||||

| (58) | ||||

| (59) | ||||

| (60) |

Therefore, for any player , any , and any time index , we have

By taking an unconditional expectation from (17), we can write

| (61) | ||||

| (62) | ||||

| (63) | ||||

| (64) | ||||

| (65) | ||||

| (66) |

As the above relation holds for any , we get for any such that . Q.E.D.

VI Convergence Results for Games with Structured Reward

As we showed in Proposition 1, finding a stationary NE for the stochastic game without any assumption on the reward functions is at least as hard as finding a mixed-strategy NE in normal-form games and is unlikely to admit an efficient learning algorithm. Although the results of the previous section hold generally, the convergence guarantees were in terms of the averaged Nikaido-Isoda gap function. However, one can obtain stronger convergence results by imposing extra assumptions on the reward functions. Therefore, in this section, we consider the stochastic game when the virtual game satisfies a certain social concavity or monotonicity property, which allows us to establish stronger convergence results.

VI-A Socially Concave Games

We begin by considering the following socially concave property [12], which has been shown to exist in many static games, such as linear Cournot games, linear resource allocation games, and TCP congestion control games.

Definition 6

A virtual game is called socially concave if i) there are positive constants such that is a concave function of , and ii) for any player and any fixed , the payoff function is a convex function of .

Although the social concavity is a condition that is imposed on the virtual game, it can be used to derive conditions on the original game . Here are two examples.

Example 1

The virtual game associated with any two-player zero-sum stochastic game is socially concave. That is because by taking , due to the zero-sum property of the payoffs, we have , which is constant, and hence a concave function. Moreover, as , for any fixed , a linear (and hence convex) function of . Similarly, for any fixed , is a linear function of .

Example 2

Consider the original stochastic game for which a positive linear combination of reward functions is constant, i.e., . Such a situation frequently arises in stochastic resource allocation games in which a constant amount of resources must be shared among the players at each time instance. Using (12) we can write , which shows that is a constant (and hence concave) function. Now by change of variables if we let for some , we can express each using the new decision variables as . Since is the sum of multinomials with nonnegative coefficients , it is known that such a change of variable makes the function jointly convex with respect to the new variables [54]. Therefore, for any fixed , is a convex function of , and the resulting virtual game is socially concave in the space of new decision variables . Of course, one also needs to slightly modify the structure of Algorithm 1 to cope with this change of variables, such as updating the dual scores using and updating the policy using , which resembles the soft-max policy update rule frequently used in reinforcement learning literature [24].

Theorem 6

Assume that the virtual game is socially concave, and let and for some . Given any , we have:

-

(a)

If players follow Algorithm 1 with -strongly convex regularizers, then almost surely is an -NE as . In particular, given , with probability at least , is an -NE for any .

- (b)

Proof:

(a) Let us consider an arbitrary and fix it. We can write777Here, we have used the scaled version of the payoffs instead of in the definition of .

| (67) | ||||

| (68) | ||||

| (69) | ||||

| (70) |

where the first inequality is valid because is a concave function of , and the second inequality holds because is a convex function of . By talking maximum from both sides of the above inequality with respect to and using Theorem 2, we obtain

Thus, as , almost surely we have , which in view of Remark 2 shows that forms an -NE. Moreover, due to the choice of stepsize , we have and . Thus, using Theorem 4, with probability at least , is an -NE for any . As , this gives an asymptotic convergence rate that scales only quadratically in the number of players and the size of their state/action spaces.

(b) As is shown in (67), because of the social concavity assumption, the Nikaido-Isoda function is a convex function with respect to its second argument. Thus, using Jensen’s inequality, we have

where the last inequality follows from Theorem 5 for any time instance such that . Substituting and into this relation shows that is an -NE for any such that . As , this gives an asymptotic convergence rate that scales only logarithmically in terms of the size of players’ state spaces. Q.E.D.

For players, Theorem 6 provides improved convergence rates compared to those given in [19] (Theorems 3.1 and 3.2). However, this speedup comes at a cost as the convergence result of [19] holds under weaker assumptions on the ergodicity and mixing time of the players’ Markov chains. In fact, unlike the learning algorithm in [19] that uses a combination of UCB and fictitious play, Algorithm 1 is arguably simpler to implement and works for any number of players assuming social concavity.

VI-B Games with Stable Equilibrium

In this section, we consider another special case of reward functions and show that if the virtual game admits a stable NE as defined next, almost surely a subsequence of occupation measures generated by Algorithm 1 will converge to an -NE.

Definition 7

An occupation profile is called a stable NE for the virtual game if , with equality if and only if , where is the vector of players’ payoff gradients with respect to their own strategies. If, in addition, , for some constant , then is called an -strongly stable NE.

Since the virtual game with payoff functions is a concave game, if we use NE characterization for concave games [11, 23], an occupation profile is a NE if and only if . This, in view of Definition 7, shows that a stable NE can be viewed as a NE that is globally attractive. To measure the convergence speed of Algorithm 1 to a stable NE , we again consider the averaged Nikaido-Isoda function with respect to an stable equilibrium , i.e.,

where is the sequence of iterates generated by Algorithm 1.888In fact, if , almost surely there must be a subsequence such that , which justifies the choice of for measuring the distance of the iterates to . The following theorem shows that the in the presence of stable NE, the accumulation points of the sequence can be considered as good estimates for the -NE policies.

Theorem 7

Assume that the virtual game admits a stable NE . If each player follows Algorithm 1 with , a -strongly convex regularizer, and a sequence of step-sizes that satisfy and , then almost surely . If, in addition, is -strongly stable, almost surely there are infinitely many such that . Moreover, with probability at least , we have for any such that .

Proof:

By choosing in relation (33), we have

| (71) |

where we note that by the martingale convergence theorem and the choice of step-size, as , all the terms on the right-hand side of the above expression (except the term ) almost surely converge to zero. Therefore, almost surely we have . Moreover, using the multilinear structure of the payoff functions , we have . Since is a stable NE, each of the summands , is nonnegative, which together with implies that almost surely there exists a subsequence , such that . In particular, if is strongly stable, almost surely , which completes the first part.

To prove the high probability convergence rate, we can again define the events , and as before and conclude that for any , if we take , with probability at least , we have , , and . Substituting these relations into (71), we conclude that with probability at least ,

Thus, for every such that , with probability at least we have . Q.E.D.

VII Numerical Results

In this section, we provide several numerical results to illustrate the effectiveness of the proposed Algorithm 1 in learning -NE policies, even in the absence of social concavity or the existence of a stable equilibrium. Motivated by applications such as energy management in smart grids, we first consider the following stochastic game model.

VII-A Game Model

Consider an energy market with one utility company and players, which can both produce and consume energy. Each player generates energy using its solar panel or wind turbine and is equipped with a storage device that can store the remaining energy at the end of each day . Let denote the (quantized) amount of stored energy of player at the beginning of day with maximum storage capacity . Moreover, let be a random variable denoting the amount of harvested energy for player at the end of day , whose distribution is determined by the weather conditions on that day. Now if we denote the total amount of energy consumed by player during day by , then the stored energy at the end of day (or the beginning of day ) is given by , where . In particular, player needs to purchase units of energy from the utility company on day to satisfy its demand on that day. On the other hand, the utility company sets the energy price as a function of total demands , which is given by . If denotes the utility that player derives by consuming units of energy, then the reward of player at time is given by . In particular, if players are at distant locations, they likely experience independent weather conditions, so their transition probability models that are governed by stochasticity of will be independent. In this game, players want to adopt consumption policies to maximize their aggregate rewards despite not being able to observe others’ states/actions.

VII-B Parameters Setup

In order to simulate the performance of Algorithm 1 for the above game setup, we consider the following choice of parameters.

-

•

Each player has a storage capacity size of , and .

-

•

Each player has its own i.i.d. random harvested energy that is uniformly distributed over , where is a player-specific constant.

-

•

The price function is given by the players’ aggregate demand, i.e., , where is a parameter set by the utility company. We will consider two cases of (i.e., free energy) and .

-

•

We set , and the reward functions are normalized by (which is the maximum reward a player can obtain) to ensure .

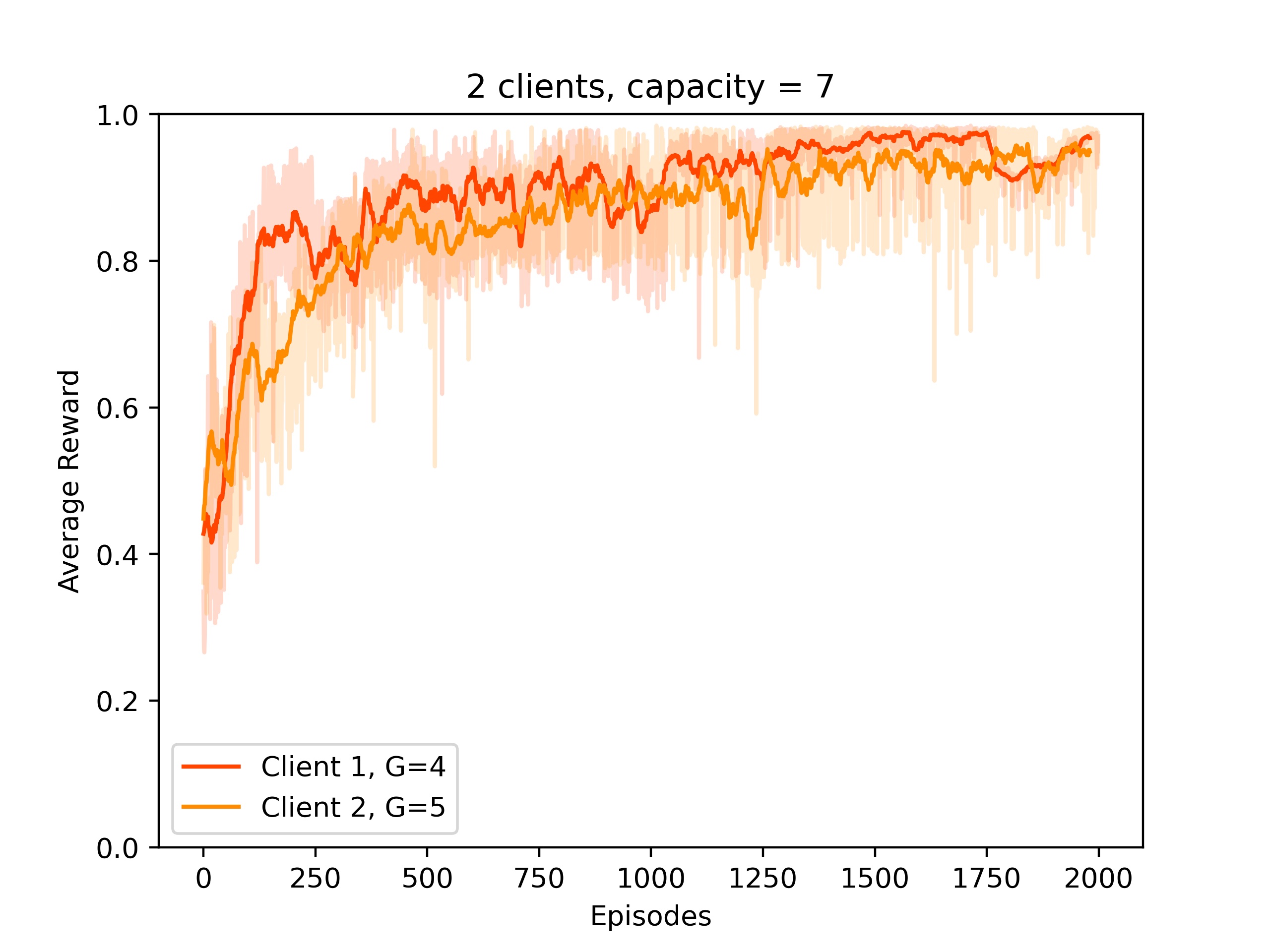

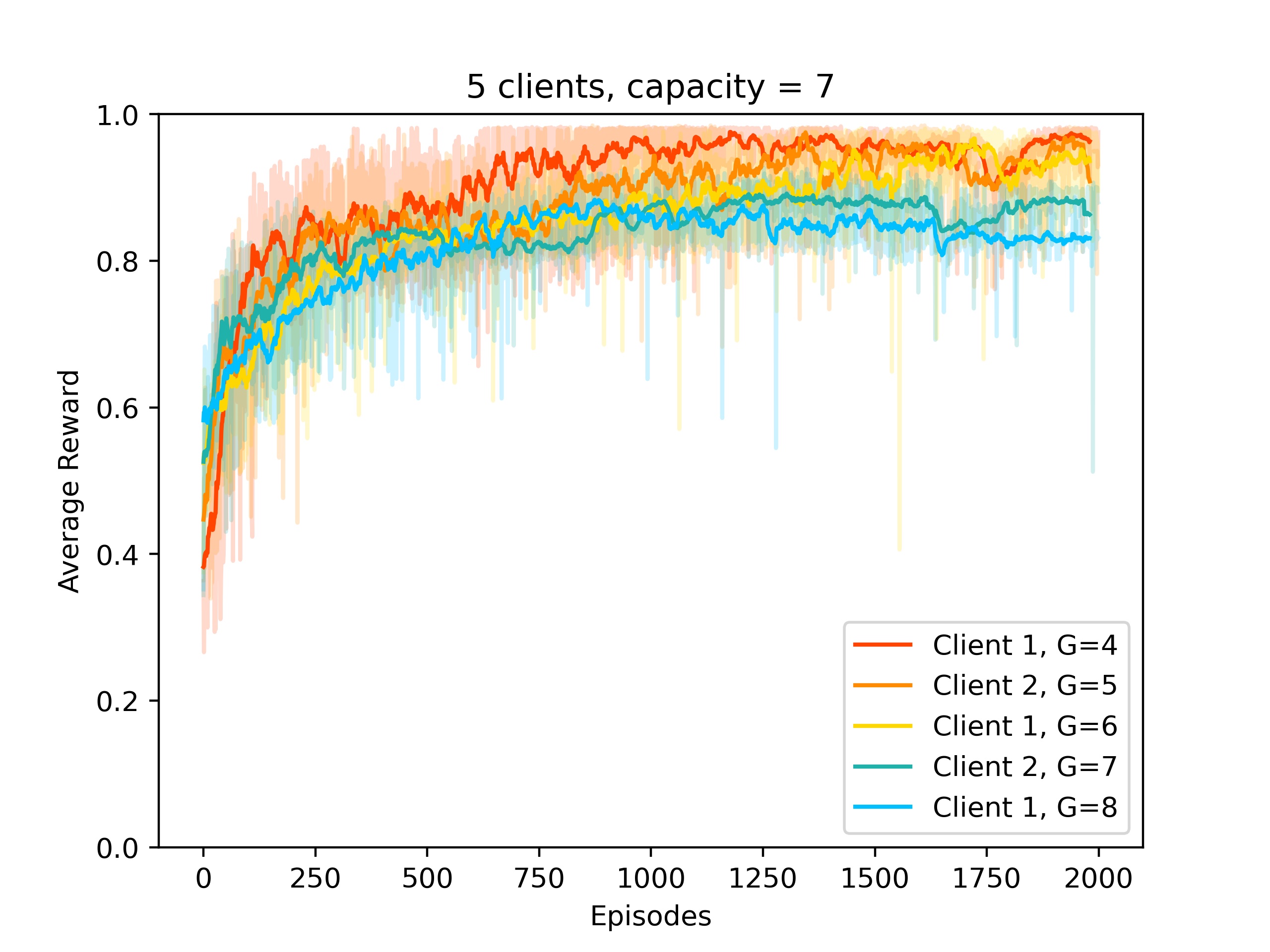

We run Algorithm 1 with the choice of , regularizers , shrunk parameter , and . For the price parameter , i.e., when the energy is free, the players aggressively consume energy because they can always get access to free energy. Thus, it is not surprising that the equilibrium payoffs will approach 1 as depicted in Figure 1 for both cases of players and players.

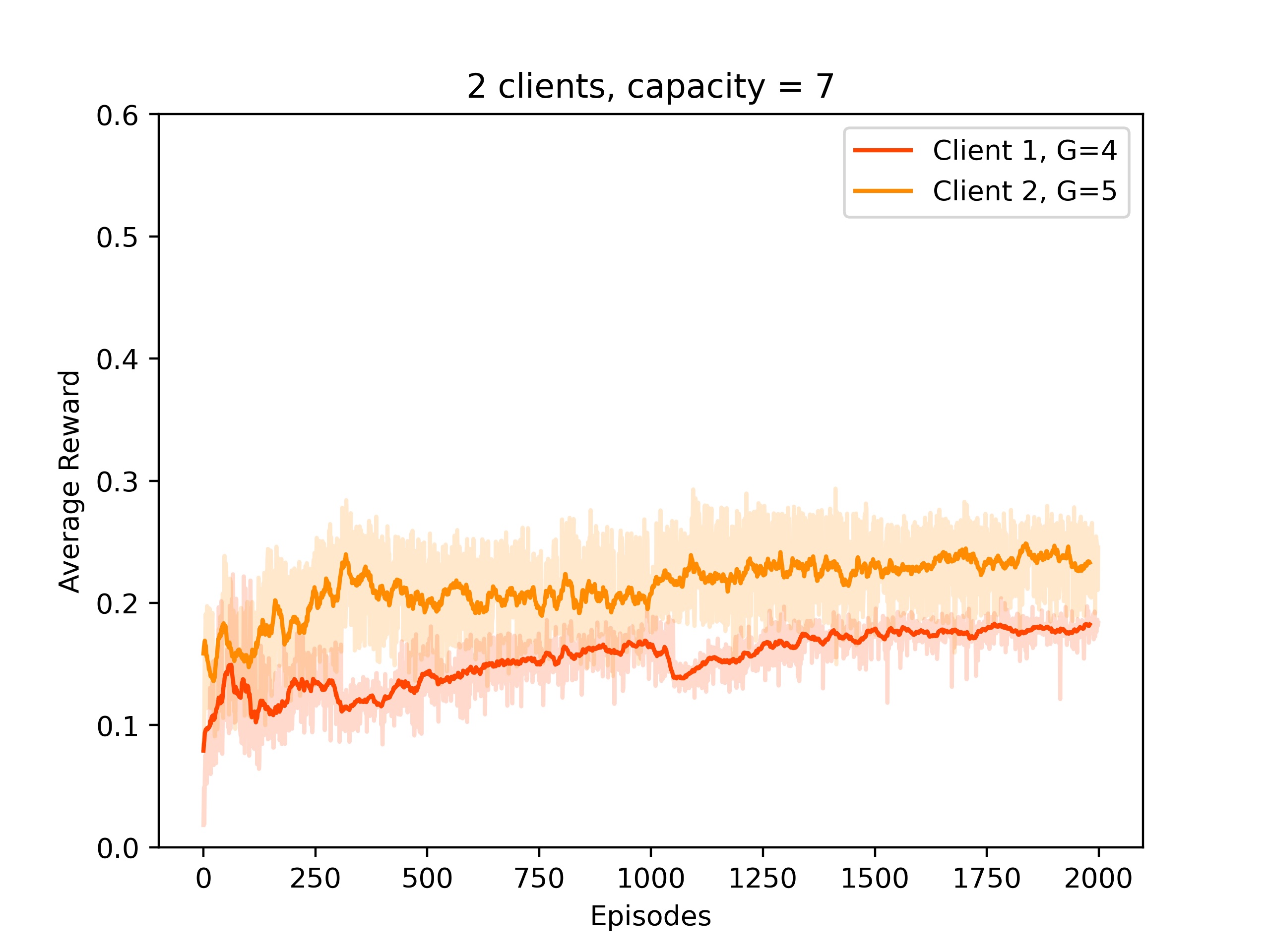

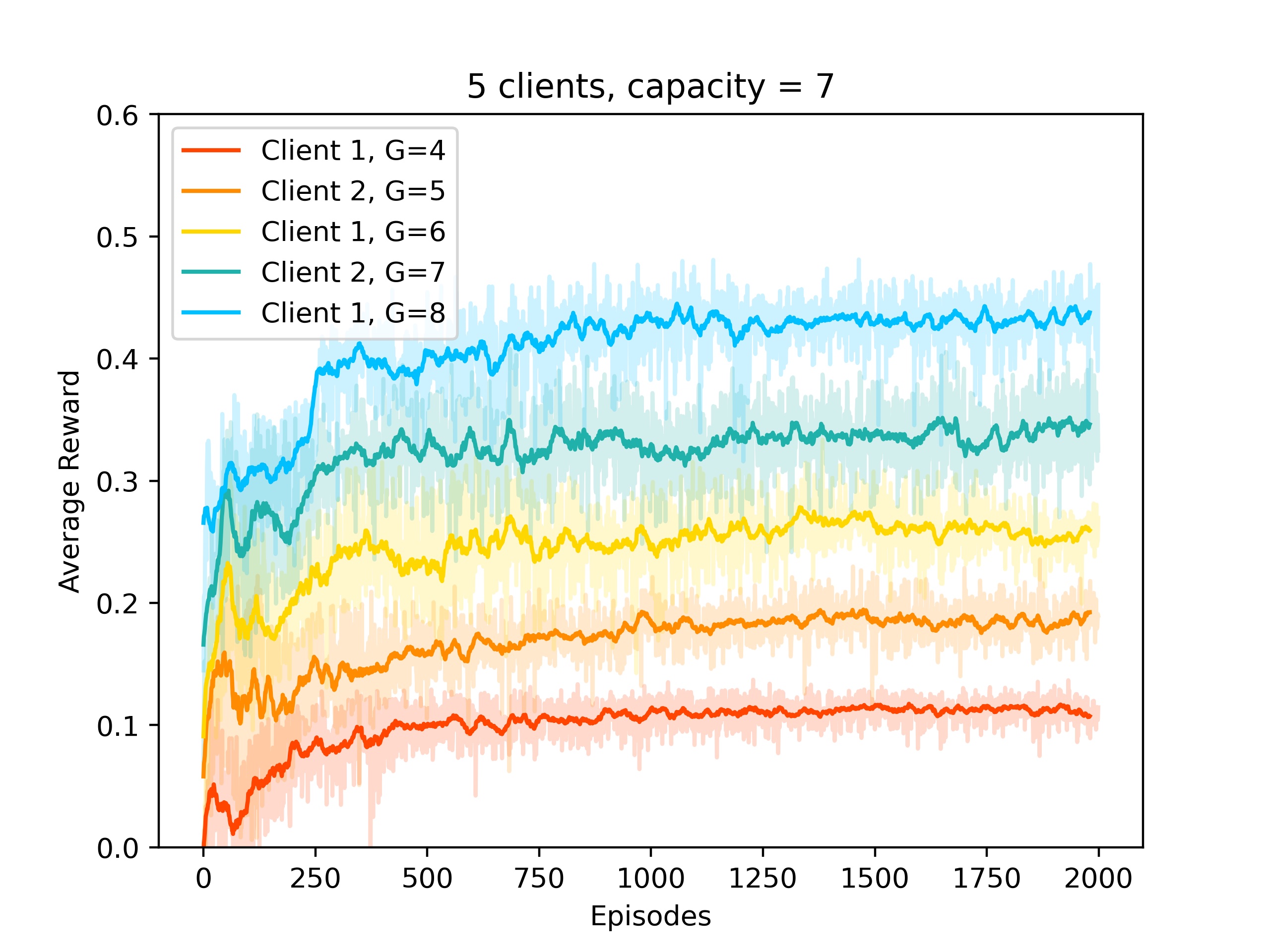

For the price parameter , the players’ averaged reward trajectories versus the number of episodes during the run of the algorithm are illustrated in Figure 2-(a) when there are players, and in Figure 2-(b) when there are players. As can be seen, the trajectories in both cases converge fast to equilibrium trajectories with less oscillation as the number of episodes increases. It can be seen from the figures that in both cases, the equilibrium averaged rewards are obtained nearly after episodes, which scales polynomially in terms of the game parameters and the numbers of players.

VIII Conclusions

In this work, we studied a subclass of stochastic games in which players have their own independent internal chains while they are coupled through their payoff functions. By establishing an equivalence between stationary NE in such games and NE points in a virtual continuous-action concave game, we developed scalable learning algorithms that converge to the set of -NE policies in terms of the averaged Nikaido-Isoda gap function (for general rewards) and in terms of the Euclidean distance (for structured rewards). We also derived high probability or expected convergence rates that scale quadratically or logarithmically in terms of the game parameters in both cases. Beyond Markov potential games and linear-quadratic stochastic games, this work provides another interesting class of stochastic games that admit scalable learning algorithms under some assumptions.

In general, there are strong computational lower bounds for developing scalable learning algorithms in -player stochastic games. On the other hand, stochastic games provide natural paradigms for modeling competition under uncertainty. One approach to overcoming the computational barrier of learning NE in large-scale stochastic games is to rely on mean-field approximations or to study stochastic aggregative games [17, 34, 55]. The main underlying assumption in mean-field games and aggregative games is that the individual actions of the players do not play a major role in the evolution of the state dynamics, but rather the mean/aggregate of their actions is the deriving force of the dynamics. Such an approach may simplify the learning task by allowing the players to focus on learning the mean-field trajectory of the actions/states rather than individual actions/states. However, the main difference between our work and those lines of work is that we target a more ambitious goal, i.e., learning in the space of all (exponentially many) action profiles. Interestingly, we showed that under certain assumptions, such as the independence of players’ chains with structured rewards, one could avoid an exponential running time to learn the stationary NE policies, even for players, and without any mean-field approximation. In particular, our convergence rate results are not asymptotic, as is often the case for mean-field games. Therefore, studying other classes of stochastic games on the middle ground between mean-field/aggregative stochastic games and two-player stochastic games whose special structure allows scalable learning algorithms for computing NE policies is an interesting future research direction.

References

- [1] J. F. Nash, “Equilibrium points in -person games,” Proceedings of the National Academy of Sciences, vol. 36, no. 1, pp. 48–49, 1950.

- [2] L. S. Shapley, “Stochastic games,” Proceedings of the National Academy of Sciences, vol. 39, no. 10, pp. 1095–1100, 1953.

- [3] M. O. Jackson, Social and Economic Networks. Princeton University Press, 2010.

- [4] T. Alpcan and T. Başar, Network Security: A Decision and Game-theoretic Approach. Cambridge University Press, 2010.

- [5] T. Roughgarden, Twenty Lectures on Algorithmic Game Theory. Cambridge University Press, 2016.

- [6] T. Başar and G. Zaccour, Handbook of Dynamic Game Theory. Springer, 2018.

- [7] N. Cesa-Bianchi and G. Lugosi, Prediction, Learning, and Games. Cambridge University Press, 2006.

- [8] C. Daskalakis, P. W. Goldberg, and C. H. Papadimitriou, “The complexity of computing a Nash equilibrium,” SIAM Journal on Computing, vol. 39, no. 1, pp. 195–259, 2009.

- [9] R. J. Aumann, “Correlated equilibrium as an expression of Bayesian rationality,” Econometrica: Journal of the Econometric Society, pp. 1–18, 1987.

- [10] D. Monderer and L. S. Shapley, “Potential games,” Games and Economic Behavior, vol. 14, no. 1, pp. 124–143, 1996.

- [11] J. B. Rosen, “Existence and uniqueness of equilibrium points for concave -person games,” Econometrica: Journal of the Econometric Society, pp. 520–534, 1965.

- [12] E. Even-Dar, Y. Mansour, and U. Nadav, “On the convergence of regret minimization dynamics in concave games,” in Proceedings of the Forty-First Annual ACM Symposium on Theory of Computing, 2009, pp. 523–532.

- [13] T. Başar and G. J. Olsder, Dynamic Noncooperative Game Theory. 2nd Ed, SIAM, 1999.

- [14] E. Altman, K. Avratchenkov, N. Bonneau, M. Debbah, R. El-Azouzi, and D. S. Menasché, “Constrained stochastic games in wireless networks,” in IEEE GLOBECOM 2007-IEEE Global Telecommunications Conference. IEEE, 2007, pp. 315–320.

- [15] P. Narayanan and L. N. Theagarajan, “Large player games on wireless networks,” arXiv preprint arXiv:1710.08800, 2017.

- [16] E. Altman, K. Avrachenkov, N. Bonneau, M. Debbah, R. El-Azouzi, and D. S. Menasche, “Constrained cost-coupled stochastic games with independent state processes,” Operations Research Letters, vol. 36, no. 2, pp. 160–164, 2008.

- [17] K. Zhang, Z. Yang, and T. Başar, “Multi-agent reinforcement learning: A selective overview of theories and algorithms,” Handbook of Reinforcement Learning and Control, Springer, pp. 321–384, 2021.

- [18] S. R. Etesami, W. Saad, N. B. Mandayam, and H. V. Poor, “Stochastic games for the smart grid energy management with prospect prosumers,” IEEE Transactions on Automatic Control, vol. 63, no. 8, pp. 2327–2342, 2018.

- [19] S. Qiu, X. Wei, J. Ye, Z. Wang, and Z. Yang, “Provably efficient fictitious play policy optimization for zero-sum Markov games with structured transitions,” in International Conference on Machine Learning. PMLR, 2021, pp. 8715–8725.

- [20] E. Altman, K. Avrachenkov, R. Marquez, and G. Miller, “Zero-sum constrained stochastic games with independent state processes,” Mathematical Methods of Operations Research, vol. 62, no. 3, pp. 375–386, 2005.

- [21] C. Daskalakis, D. J. Foster, and N. Golowich, “Independent policy gradient methods for competitive reinforcement learning,” Advances in Neural Information Processing Systems, vol. 33, pp. 5527–5540, 2020.

- [22] M. O. Sayin, F. Parise, and A. Ozdaglar, “Fictitious play in zero-sum stochastic games,” SIAM Journal on Control and Optimization, vol. 60, no. 4, pp. 2095–2114, 2022.

- [23] P. Mertikopoulos and Z. Zhou, “Learning in games with continuous action sets and unknown payoff functions,” Mathematical Programming, vol. 173, no. 1, pp. 465–507, 2019.

- [24] A. Agarwal, S. M. Kakade, J. D. Lee, and G. Mahajan, “On the theory of policy gradient methods: Optimality, approximation, and distribution shift,” Journal of Machine Learning Research, vol. 22, no. 98, pp. 1–76, 2021.

- [25] M. Wang, “Primal-dual learning: Sample complexity and sublinear run time for ergodic Markov decision problems,” arXiv preprint arXiv:1710.06100, 2017.

- [26] A. R. Cardoso, H. Wang, and H. Xu, “Large scale Markov decision processes with changing rewards,” in 33rd Conference on Neural Information Processing Systems 32 (NIPS), 2019, pp. 1–11.

- [27] Y. Chen, J. Dong, and Z. Wang, “A primal-dual approach to constrained Markov decision processes,” arXiv preprint arXiv:2101.10895, 2021.

- [28] Y. Jin and A. Sidford, “Efficiently solving MDPs with stochastic mirror descent,” in International Conference on Machine Learning. PMLR, 2020, pp. 4890–4900.

- [29] Z. Song, S. Mei, and Y. Bai, “When can we learn general-sum Markov games with a large number of players sample-efficiently?” arXiv preprint arXiv:2110.04184, 2021.

- [30] Y. Zhao, Y. Tian, J. D. Lee, and S. S. Du, “Provably efficient policy gradient methods for two-player zero-sum Markov games,” arXiv preprint arXiv:2102.08903, 2021.

- [31] Y. Tian, Y. Wang, T. Yu, and S. Sra, “Online learning in unknown Markov games,” in International Conference on Machine Learning. PMLR, 2021, pp. 10 279–10 288.

- [32] M. Sayin, K. Zhang, D. Leslie, T. Başar, and A. Ozdaglar, “Decentralized Q-learning in zero-sum Markov games,” Advances in Neural Information Processing Systems, vol. 34, pp. 18 320–18 334, 2021.

- [33] B. M. Hambly, R. Xu, and H. Yang, “Policy gradient methods find the Nash equilibrium in N-player general-sum linear-quadratic games,” Preprint, submitted August 2, https://dx.doi.org/10.2139/ssrn.3894471, 2021.

- [34] M. A. uz Zaman, K. Zhang, E. Miehling, and T. Bașar, “Reinforcement learning in non-stationary discrete-time linear-quadratic mean-field games,” in 2020 59th IEEE Conference on Decision and Control (CDC). IEEE, 2020, pp. 2278–2284.

- [35] R. Zhang, Z. Ren, and N. Li, “Gradient play in multi-agent Markov stochastic games: Stationary points and convergence,” arXiv preprint arXiv:2106.00198, 2021.

- [36] S. Leonardos, W. Overman, I. Panageas, and G. Piliouras, “Global convergence of multi-agent policy gradient in Markov potential games,” arXiv preprint arXiv:2106.01969, 2021.

- [37] S. V. Macua, J. Zazo, and S. Zazo, “Learning parametric closed-loop policies for Markov potential games,” arXiv preprint arXiv:1802.00899, 2018.

- [38] D. Mguni, Y. Wu, Y. Du, Y. Yang, Z. Wang, M. Li, Y. Wen, J. Jennings, and J. Wang, “Learning in nonzero-sum stochastic games with potentials,” arXiv preprint arXiv:2103.09284, 2021.

- [39] A. S. Nemirovski and D. B. Yudin, Problem Complexity and Method Efficiency in Optimization. Wiley-Interscience Series in Discrete Mathematics, Wiley, New York, 1983.

- [40] A. Beck and M. Teboulle, “Mirror descent and nonlinear projected subgradient methods for convex optimization,” Operations Research Letters, vol. 31, no. 3, pp. 167–175, 2003.

- [41] S. Bubeck, “Convex optimization: Algorithms and complexity,” arXiv preprint arXiv:1405.4980, 2014.

- [42] A. Juditsky, J. Kwon, and É. Moulines, “Unifying mirror descent and dual averaging,” arXiv preprint arXiv:1910.13742, 2019.

- [43] E. Hazan, “Introduction to online convex optimization,” arXiv preprint arXiv:1909.05207, 2019.

- [44] B. Gao and L. Pavel, “Continuous-time discounted mirror descent dynamics in monotone concave games,” IEEE Transactions on Automatic Control, vol. 66, no. 11, pp. 5451–5458, 2020.

- [45] M. Bravo, D. S. Leslie, and P. Mertikopoulos, “Bandit learning in concave -person games,” arXiv preprint arXiv:1810.01925, 2018.

- [46] Z. Zhou, P. Mertikopoulos, A. L. Moustakas, N. Bambos, and P. Glynn, “Mirror descent learning in continuous games,” in 2017 IEEE 56th Annual Conference on Decision and Control (CDC). IEEE, 2017, pp. 5776–5783.

- [47] E. Altman, Constrained Markov Decision Processes. CRC Press, 1999.

- [48] C. Daskalakis, “On the complexity of approximating a Nash equilibrium,” ACM Transactions on Algorithms (TALG), vol. 9, no. 3, pp. 1–35, 2013.

- [49] E. Even-Dar, S. M. Kakade, and Y. Mansour, “Online Markov decision processes,” Mathematics of Operations Research, vol. 34, no. 3, pp. 726–736, 2009.

- [50] G. Neu, A. György, C. Szepesvari, and A. Antos, “Online Markov decision processes under bandit feedback,” IEEE Transactions on Automatic Control, vol. 59, no. 3, pp. 676–691, 2013.

- [51] D. A. Levin and Y. Peres, Markov Chains and Mixing Times. American Mathematical Soc., 2017.

- [52] N. Golowich, S. Pattathil, and C. Daskalakis, “Tight last-iterate convergence rates for no-regret learning in multi-player games,” Advances in Neural Information Processing Systems, vol. 33, pp. 20 766–20 778, 2020.

- [53] P. Hall and C. C. Heyde, Martingale Limit Theory and its Application. Academic Press, 1980.

- [54] S. Boyd, S. P. Boyd, and L. Vandenberghe, Convex Optimization. Cambridge University Press, 2004.

- [55] E. Meigs, F. Parise, and A. Ozdaglar, “Learning in repeated stochastic network aggregative games,” in 2019 IEEE 58th Conference on Decision and Control (CDC). IEEE, 2019, pp. 6918–6923.

Appendix I: Omitted Proofs and Auxiliary Lemmas

Proof of Lemma 2: Since each polytope is a compact set and characterized by finitely many (continuous) linear constraints, for any , there exist , such that by replacing the constraint in the description of by , the shrunk polytope has a maximum distance of at most from . In other words, for any point , there exists such that . Thus, by choosing , for any , there exists such that .

Now, let be an -NE for the virtual game with shrunk action polytope , and note that also belongs to . Consider any arbitrary , and let be the corresponding closest point to as described above. Then, for any player , we have

| (72) | ||||

| (73) |

where the first inequality uses the fact that is an -NE with respect to the shrunk polytope . Since was chosen arbitrarily, the above inequality shows that is a -NE with respect to the original polytope .

Proof of Lemma 3: Given and an arbitrary state-action , let be the first (random) time that the state is visited during the sampling interval , i.e., is the first time for which . Since each state is sampled once, the expected value of the -th coordinate of equals

| (74) |

where is the indicator function, and the second equality holds because at time the played action equals with probability . Given , let be the stationary distribution induced over states by using policies . We can write

| (75) | ||||

| (76) | ||||

| (77) | ||||

| (78) | ||||

| (79) |

Given , let be the probability distribution of being at different states at time should players follow policies . Since , using triangle inequality, we can write

| (80) | ||||

| (81) | ||||

| (82) | ||||

| (83) | ||||

| (84) | ||||

| (85) |

where the third equality holds by the independency Assumption 1,999Conditioned on , the event is determined by player ’s internal state transition matrix and a given policy , which is independent from the event , as the latter is determined by other players’ state transition matrices and their given fixed policies . and the last inequality holds by the ergodicity Assumption 2. Since with probability 1, we have .

Proof of Theorem 3: Suppose by contradiction that is not an -NE for the virtual game, and let . Since the virtual game is a concave game, using the NE characterization for concave games, there exists a player and deviation strategy such that . Thus, if we let , for any and such that and , we have . To show that, we note that each coordinate of lies in because

Thus , and we can write

| (86) | ||||

| (87) | ||||

| (88) |

where the second inequality uses the Cauchy-Schwartz inequality, and the last inequality holds by the choice of parameter .

Let us define the (coordinatewise) martingale difference sequence , and the corresponding zero-mean martingale . Consider the nondecreasing sequence of positive numbers . Then, we can write

| (89) | ||||

| (90) | ||||

| (91) | ||||

| (92) |

where the last equality is obtained using an argument similar to that used to derive (74), and the final inequality holds because and . Since by the step-size assumption and , using the martingale convergence theorem, almost surely we have

| (93) |

Let be the event that converges to . Conditioned on , almost surely we get

| (94) | ||||

| (95) | ||||

| (96) | ||||

| (97) | ||||

| (98) |

where the last equality holds by Lemma 3, by relation (93), and because due to continuity of . Using (94) and since , we obtain , which, together with , implies that almost surely

| (99) |

Moreover, because , we have . Therefore, for all sufficiently large , almost surely we have

Since by the assumption and within we have , with positive probability we must have as . This contradiction shows that must be an -NE.

Auxiliary Lemmas

Lemma 4

Let Assumption 1 hold. Then, .

Proof:

We use an induction on . For the initial step , the statement trivially holds. We can write

| (100) | |||

| (101) | |||

| (102) | |||

| (103) |

where the second and third equalities use Assumption 1 and the hypothesis. Q.E.D.

Lemma 5 ([23], Proposition 4.3)

Let be a -strongly convex function over a convex compact set , and be its convex conjugate defined by . Let be the Fenchel coupling function. Then, , and we have

where .

Lemma 6 ([25], Lemma 4)

Let be an -dimensional probability simplex and be a compact and convex subset of . Moreover, let be an arbitrary nonpositive vector and assume . Consider the following two-step MD update rule:

| (104) |

Then, for any , we have , where .