Right large deviation principle for the top eigenvalue of the sum or product of invariant random matrices

Abstract

In this note we study the right large deviation of the top eigenvalue (or singular value) of the sum or product of two random matrices and as their dimensions goes to infinity. The matrices and are each assumed to be taken from an invariant (or bi-invariant) ensemble with a confining potential with a possible wall beyond which no eigenvalues/singular values are allowed. The introduction of this wall puts different models in a very generic framework. In particular, the case where the wall is exactly at the right edge of the limiting spectral density is equivalent, from the point of view of large deviations, to considering a fixed diagonal matrices, as studied previously in Ref. [1]. We show that that the tilting method introduced in Ref. [1] can be extended to our general setting and is equivalent to the study of a spherical spin glass model specific to the operation - sum of symmetric matrices / product of symmetric matrices / sum of rectangular matrices - we are considering.

1 Introduction

Since the pioneer work of Wishart [2] and Wigner [3] in the 60s, Random Matrix Theory (RMT) has found applications in many domains of research, ranging from the theory of disordered system [4, 5] to telecommunications [6] and finance [7] and even more recently to statistical learning theory [8, 9], to cite few examples. In particular the top eigenvalue/singular value of a random matrix plays a fundamental role in many fields: for example in statistics, Principal Component Analysis (PCA) [10] is often used to reduce the dimensions of a raw matrix based on the values of first top eigenvalues; in the study of the stability of a complex system [11, 12, 13, 14, 15] the top eigenvalue of the (opposite of the) stability matrix of a randomly linear system indicates whether the system is locally stable or not; in the theory of disordered system, the law of the top eigenvalue is related to the so-called complexity of the system, see Refs. [16, 17, 18].

Therefore, a natural question in RMT and related fields is the following: given a random symmetric (respectively rectangular) matrix , as the dimensions of this matrix grows, what is the typical value of the top eigenvalue (resp. singular value) and what is the probability to find it at a position, say , far from this typical value? When this probability is exponentially small, one says that the top eigenvalue satisfies a large deviation principle and the goal is to calculate both the speed of convergence (what is the power in in the exponential decay?) and the rate function (what is the leading prefactor and how does it depend on the position ?). The first natural case is to consider, as taken from an invariant ensemble, a family containing both the famous Gaussian orthogonal ensemble (GOE) and the Wishart ensemble of RMT. Based on a direct analogy between the ensemble of eigenvalues and a Coulomb gas of particles restricted on the real line, the large deviation can be computed explicitly, see Refs. [19, 20, 21, 22, 23, 24] and [25] for a review. In particular, both the speed of convergence and the rate functions depend on whether is above or below the typical value. The former is known as the right large deviation principle and the latter is known as the left large deviation principle. Several studies have gone beyond the invariant ensemble case by looking for example at generalized Wigner matrices, see Refs. [26, 27, 28, 29] or looking at small-rank deformation of an invariant ensemble, see Refs. [30, 31, 32]. Recently, there has been an interest in the so-called full-rank deformation:

-

1.

In Ref. [1], the authors studied the right large deviation for the sum , where is a random (uniform) orthogonal matrix, and and are two ’fixed diagonal’ matrices, based on a tilting method with the additive spherical integral.

-

2.

In Ref. [33], based on similar ideas, the author studied the (right) large deviation of the top eigenvalue of the sum where is a (slight generalization of a) GOE matrix.

-

3.

In Ref. [34] and based again on similar methods, the case of the large deviation of the top eigenvalue of the product , where is a diagonal matrix and is a Wishart matrix, was studied.

In this paper, we obtain explicitly the right large deviation principle for the top eigenvalue (or singular value if the matrices are rectangular) of the sum or the product of two arbitrary matrices; by which we mean that each matrix can be either taken from an invariant ensemble or can be a (randomly rotated) diagonal matrix. In particular, our results allows one to recover the three specific cases considered previously in Refs. [1, 33, 34] and to obtain new results for cases that have not been previously considered. To obtain our result, we first introduce an invariant ensemble with a wall, a natural generalization of the classical invariant ensemble. From the point of view of large deviations, we show that for a proper choice of the position of the wall (namely the wall is exactly at the edge of the spectrum), we recover the cases of deterministic matrices. Second, we extend the tilting method introduced in Ref. [1]. We argue that when one is considering respectively the product of two symmetric matrices or the sum of two rectangular matrices, one should replace the additive spherical integral with respectively the multiplicative spherical integral and the rectangular spherical integral. In each case, we give a natural interpretation of those spherical integrals as the partition function of a disordered system. Based on ideas develop in Ref. [35], we give the precise asymptotic behavior for the annealed free energies of any invariant random matrix, going beyond the case of GOE and Wishart matrices which can tackled by direct Gaussian integration. Combining this result with the asymptotic behavior of the quenched free energy of those three (additive, multiplicative, rectangular) spherical integrals derived in Refs. [36, 37, 38, 39, 40] allows us to get the rate function in each case.

The rest of the paper is organized as follows: in Sec. 2, we recall the main results concerning large deviations of the top eigenvalue of one random matrix from a (classical) invariant ensemble. This allows us to introduce the main concepts and notations used in this paper. In particular, we define the so-called invariant ensemble with a wall and also described the case of bi-invariant rectangular random matrices. In Sec. 3, we introduce the main tool to compute the rate function: the tilting method with spherical integrals. Our description of the tilting method has been made in a general framework in order to describe the idea of the computation for each of the three cases (sum of symmetric matrices, product of symmetric matrices, sum of rectangular matrices) simultaneously. We then go into detail for each case separately. We consider the case of the sum of two symmetric matrices in Sec. 4, the product of two symmetric matrices in Sec. 5 and the sum of rectangular matrices in Sec. 6. In each Section, we give explicitly the expression for the rate function together with concrete examples. This rate function admits up to three different regimes. Based on the similarity with the rate function of the simpler model of a rank-one deformation of one invariant random matrix, described in App. C and the rate function of the toy model of the sum of two rank-one matrix, described in App. D, we give a natural interpretation for each regime. In App. A, we recall classical properties of RMT and free probability that are used in the main text and App. B contains derivation of the quenched and annealed free energies.

2 Reminder on right large deviation for one random matrix: The pulled Coulomb gas approach

Before considering the addition or multiplication of two random matrices, let’s first briefly recall the simpler case of one random matrix in an invariant ensemble. We first start with symmetric random matrices.

2.1 Classical Rotationally Invariant Ensemble

For an analytic confining potential , we say that a matrix is drawn from a (classical rotationally) invariant ensemble if the probability to observe the matrix in a region in the space of symmetric matrices is defined as:

| (1) |

where is the Lebesgue measure over the space of symmetric matrices and is a constant ensuring that this probability is normalized to one. When considering positive semi-definite matrices, we will implicitly assume the potential to be defined on . For any orthogonal matrix we have which together with the cyclical property of the trace gives:

| (2) |

where is the group of orthogonal matrix; hence the name (rotationally) invariant ensemble.

Example (GOE matrices): If one considers the elements of the matrix to be independent (up to the symmetry) Gaussian random variables with mean zero and variance for the off-diagonal elements and for the diagonal elements, then this ensemble corresponds to the famous Gaussian Orthogonal Ensemble (GOE) for which the potential is equal to:

| (3) |

Example (Wishart matrices): Consider a rectangular matrix with , where the elements of are Gaussian independent random variables with mean zero and variance one, from which we construct the square matrix . The matrix is a (Gaussian White) Wishart matrix. It is rotationally invariant with potential:

| (4) |

where the asymptotic behavior in Eq. (4) corresponds to the double scaling limit and with . The invariant ensemble with the potential in Eq. (4) is sometimes known as the Laguerre Orthogonal Ensemble.

From there, it is a standard result of RMT that admits the following spectral decomposition , where the matrix of eigenvectors is taken uniformly over . To ease notation when it is needed, we write for the eigenvalues of the matrix . The joint density of the eigenvalues is given by:

| (5) |

The term is the Jacobian of the change of variable and is exactly the pairwise repulsive interaction of the -Coulomb gas. In the large limit, the empirical (random) spectral density converges to a non-random smooth density :

| (6) |

where is the solution of the Tricomi problem:

| (7) |

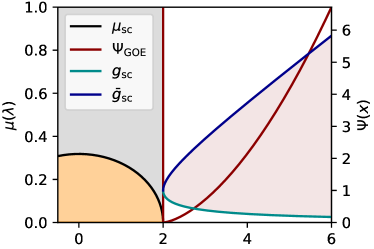

where stands for Principal Value. Example (GOE matrices and the semi-circle distribution): For GOE matrices with a quadratic potential given by Eq. (3), the solution of this Tricomi equation is given by the famous semi-circle distribution:

| (8) |

where is the indicator function, it is equal to if and zero otherwise. Example (Wishart matrices and the Marčenko-Pastur distribution): For Wishart matrices with potential given by Eq. (4), one obtains the Marčenko-Pastur distribution:

| (9) |

where the edges are given by .

2.2 Invariant Ensemble with a wall

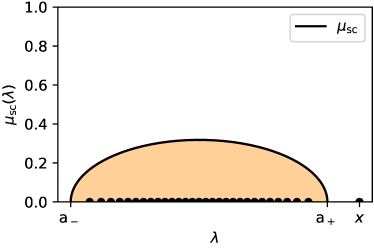

Importantly, Eq. (5) for the joint density of eigenvalues still makes sense if we introduce a wall at a position beyond which the potential is infinite. We say that a matrix is taken from an invariant ensemble with a wall at , which we denote by , if with uniform over and the follow the joint law of Eq. (5) with a confining potential such that . By construction, we still have the property (2) for random matrices taken from this ensemble. It is important to notice that the introduction of this wall does not change the limiting equilibrium density since and the solution of the Tricomi problem of Eq. (7) only depends on the values of the potential between the two edges . The introduction of these invariant ensembles with a wall might seem odd at first, but as we will see later on, this construction allows the study of the sum of two matrices where one (or both111When considering two diagonal matrices, we will be considering the sum with uniform over , such that and are asymptotically free and the spectrum of the eigenvalues of the sum (respectively of the product) is given asymptotically by the free convolution described in Sec. 4.1 (resp. the multiplicative free convolution described in Sec. 5.1). ) matrix is a fixed diagonal matrix:

| (10) |

The are ’frozen’ sequences of numbers such that as we increase the size of the matrix, their empirical distribution converges to the same :

| (11) |

and importantly the minimum and the maximum of the converge to the edges and of (that is, in the large limit, no outlier survives). To be more concrete, a typical example for the choice of the is to take them as the quantiles of the distribution , sometimes called the ”classical positions” of the particles. For a given and for each ranging from to , this means that is solution of the integral equation:

| (12) |

and by construction their empirical distribution converge to . Another natural choice is to draw independently each from the distribution . Now in general, diagonal matrices of the form of Eq. (10) are very different from random matrices taken from an invariant ensemble since their eigenvalues are fixed and don’t have a true repulsion as in Eq. (5). However, when one consider the problem of large deviation of the top eigenvalue, we will see that they behave as an invariant ensemble with a wall exactly at the edge (). This will be made more precise later on, but one can already see that if there is a wall exactly at the edge, then at finite the top eigenvalue cannot fluctuate outside the support of the bulk density and hence it is in a sense fixed. This construction is superfluous when considering just one matrix (in this case the question of large deviation for the top eigenvalue of a deterministic matrix as in Eq. (10) is trivial), but turns out to be very convenient when considering the sum or product of two matrices.

Remark (wall at infinity and classical invariant ensemble): One may note that we recover the case of classical invariant ensemble of Sec. 2.1 by sending .

2.3 Coulomb gas approach

Coming back to random symmetric matrices from an invariant ensemble, if we order the eigenvalues in decreasing order, then we have:

| (13) |

This result is valid in the formal and a natural question is to estimate the probability at large but finite , , of having the top eigenvalue at a position different from its typical value . If the density is ’non-critical’, by which we mean that it behaves as a square-root near the edge ,

| (14) |

then the small deviations of around the limiting value are given by the Tracy-Widom law for fluctuations of order , see Refs. [41, 42]. For a value of far from the edge , one is outside the scope of the Tracy-Widom regime describing typical fluctuations and one needs to estimate a very rare event dictated by a large deviation principle. This can be summarized (see Ref. [25]) by the following set of equations:

| (20) |

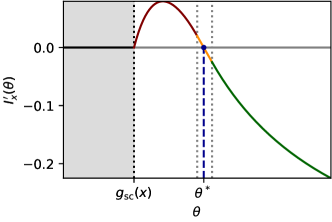

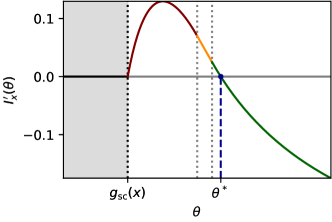

The function in Eq. (20) is the Tracy-Widom function. The scaling (or speed of convergence) of the large deviation principle is different if is either above or below the edge , and can be naturally interpreted thanks to the -Coulomb gas picture.

2.3.1 The pulled Coulomb gas ()

Let’s consider the case which is the main subject of this note. Integrating the joint density in Eq. (5), one has that computing the (logarithm of the) probability is equivalent to computing the difference of energy between the configuration of a -Coulomb gas where the top particle is pulled at the position and the configuration of the unperturbed -Coulomb gas. For the perturbed gas, we are just moving one particle away from the bulk, and thus we expect that this perturbation does not change the equilibrium density of the other particles inside the bulk. This induces the scaling in Eq. (20) for , and the right rate function is given by:

| (21) |

which can be written in integral form as:

| (22) |

where is the Stieltjes transform of :

| (23) |

It will be convenient to introduce the second branch of the Stieltjes transform, (see App. A.1), which, in the case of invariant ensemble, is given for by:

| (24) |

so that from Eq. (22) we can interpret the rate function as (half) the area between the two branches of the Stieltjes transform up to the position :

| (25) |

Note that for , the rate function is finite. Remark (Recovering the potential): From the eigenvalue density and the rate function , one can recover the potential (up to an arbitrary constant) over the whole range of possible eigenvalues. Indeed, from the density one can compute the Stieltjes transform using Eq. (23) and rewrite Eqs. (7) and (22) as222The potential for can be recovered similarly using the rate function for .

| (29) |

For random matrices that are not necessarily drawn from an invariant ensemble, we can use this formula to define an effective potential, i.e. the potential of the invariant ensemble that has the same density and rate functions. In particular, for a fixed diagonal matrix with eigenvalue density the rate function is infinite, and the effective potential is infinite beyond exactly as described in Sec. 2.2.

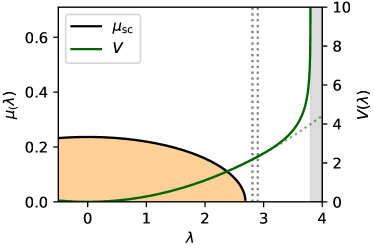

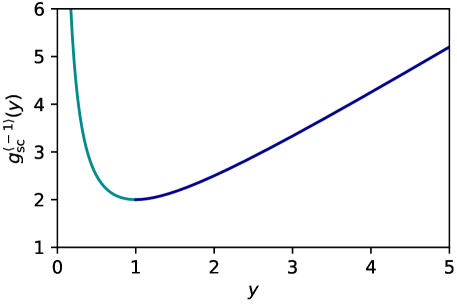

Example (Rate function for GOE matrices): for a GOE matrix, whose limiting spectrum is the semi-circle distribution of Eq. (8), the Stieltjes transform is given by:

| (30) |

and the second branch of the Stieltjes is given by:

| (31) |

and therefore integrating according to Eq. (22), the right large deviation of the top eigenvalue is given by the rate function:

| (32) |

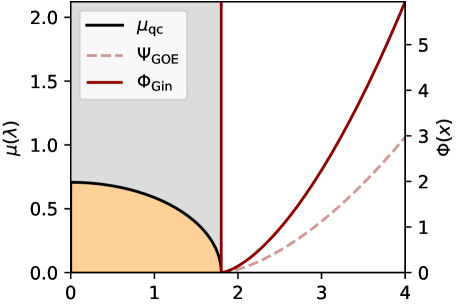

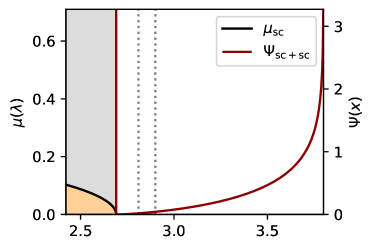

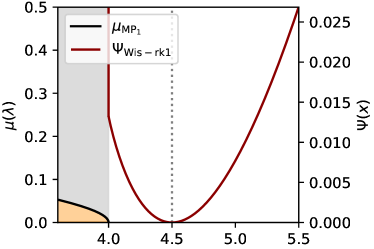

The two branches of the Stieltjes transform and the rate function are given in Fig. 3 (Left). Example (Rate function for Wishart matrices): For a (Gaussian White) Wishart matrix, whose limiting spectrum is the Marčenko-Pastur distribution of Eq. (9), the Stieltjes transform is given by:

| (33) |

with , and the second branch is given by:

| (34) |

The two branches of the Stieltjes transform are illustrated in Fig. 3 (Right). The right rate function is given by:

| (35) |

and is also represented in Fig. 3 (Right). Note that in integral in Eq. (35) can be computed analytically, but the result is not very enlightening. For the rate function simplifies considerably, and we have:

| (36) |

In this case, one may notice the following identity:

| (37) |

which will be discussed in more detail in Sec. 2.4.2 concerning bi-invariant rectangular matrices.

Remark (Behavior near the edge and the Tracy-Widom ’3/2’ scaling): If one is looking at a non-critical density satisfying the condition of Eq. (14) near the edge, then both the Stieltjes and its second branch behaves near the top edge as:

| (40) |

so approximating the integral of Eq. (25) by Euler method, at first order one has for the rate function:

| (41) |

and hence the probability behaves as

| (42) |

The scaling of the reduced variable and the asymptotic behavior matches the large argument behavior of the Tracy-Widom regime which describes the probability of finding an eigenvalue near the edge, see Ref. [25].

2.3.2 A word on the pushed Coulomb gas ()

For , one can still use the Coulomb gas analogy, but now the perturbed -Coulomb gas is compressed such that its top particle is at the position . Unlike the case , the equilibrium measure in the bulk is modified, since one needs to push a large fraction of the particles to satisfy this constraint. This explains the different scaling in Eq. (20) in this scenario, and we refer to Ref. [25] for a description of the rate function in this case. This left large deviation will not be discussed in the rest of this note.

2.4 The case of one rectangular random matrices

In this paragraph, we describe the case of rectangular random matrices. The reader only interested in symmetric random matrices may skip this section and jump directly to Sec. 3.

2.4.1 Singular value decomposition

Let be a real matrix. Without loss of generality, we consider . We will be interested in the double scaling limit where and but the ratio stays finite:333In the rest of this section and when we are considering rectangular matrices, all limits are assumed to be taken under this setting.

| (43) |

The singular value decomposition (SVD) of is given by:

| (44) |

where (resp. ) is a (resp. ) orthogonal matrix, is a diagonal rectangular matrix:

| (45) |

and the are the singular values of . They are related to the eigenvalues of the matrix by the relation:

| (46) |

2.4.2 Bi-invariant ensemble

We say that a rectangular matrix is taken from a bi-invariant ensemble if its law can be written as:

| (47) |

for an analytic potential , since it satisfies the property:

| (48) |

for any and any . The change of variable introduces a Jacobian [43] which is equal to:

| (49) |

In this case, the matrix admits the SVD of Eq. (44) where (resp. ) is taken uniformly over (resp. over ) and the singular values admit the following joint density:

| (50) |

If we introduce the modified potential

| (51) |

with , this can be written as:

| (52) |

Note that if we do the change of variable given by Eq. (48) in the joint law of Eq. (52), we have that the matrix is taken from an invariant ensemble with the modified potential (plus a vanishing term coming from the change of variable).444Taking into account the Jacobian amounts to do the change . In particular, this vanishing term prevents the eigenvalues of the matrix to be negative for where the coefficient in front of the logarithm in Eq. (51) is null in this case. For , one has to consider as being infinite for negative values. As a consequence, in the large double scaling limit of Eq. (43), the empirical singular value distribution converges to a smooth limit:

where the limiting singular value distribution (LSVD) is given as:

| (53) |

where is solution of the Tricomi problem of Eq. (7) with the potential replaced by of Eq. (51):

| (54) |

The edges of the LSVD are the square root of the edges of the distribution . Equivalently, the LSVD is the solution of the following equation:

| (55) |

which can be directly seen from the joint law of Eq (52).

Example (Gaussian rectangular random matrices and Ginibre matrices): Let’s consider a matrix with Gaussian i.i.d entries with mean zero and variance . This corresponds to . The matrix is a Gaussian white Wishart matrix with density given by Eq. (9). Since The LSVD of the matrix is related to the spectrum of Marčenko-Pastur distribution by , one gets:

| (56) |

In particular the case corresponds to Ginibre random matrices and Eq. (56) becomes the so-called quarter-circle distribution:

| (57) |

2.4.3 Bi-invariant ensemble with a wall and fixed diagonal rectangular matrices

Similarly to the symmetric case, we say that a rectangular random matrix is taken from a bi-invariant ensemble with a wall at the position if its SVD is given by Eq. (44) with (resp. ) taken uniformly over (resp. over ) and the singular values follow the law of Eq. (52) with now , such that no singular value can be higher than the position . The introduction of this wall will allow us to study the sum of rectangular matrices where one (or both555When considering two diagonal rectangular matrices, we will be considering the sum with and uniform over and respectively, such that and are asymptotically bi-free, and the spectrum of the singular values of the sum is given asymptotically by the rectangular free convolution described in Sec. 6.1. ) of them is a fixed diagonal rectangular matrix of the form:

| (58) |

where the are frozen sequence of number such that at large , the empirical distribution of the converges to the same :

2.4.4 Right large deviation of the top singular value

As in the symmetric case, the goal is to estimate for large , the probability of finding the top singular value at a position above its typical value given by the edge of :

| (59) |

From the relation (48), we have:

| (60) |

and hence

| (61) |

where is the rate function associated with the invariant matrix in the potential . Namely, using Eq. (25), we have:

| (62) |

where and are respectively the Stieltjes and second branch of the Stieltjes of . Equivalently, we can write the rate function as:

| (63) |

Remark (square matrix and symmetrized density): In the case where , corresponding to the case where is an (asymptotic) square matrix but not necessarily symmetric, there exist a nice relation with the symmetric case of Sec. 2.1. Let’s consider a symmetric matrix , where its potential is related to the potential of Eq. (47) of the square (but non-symmetric) matrix by:

| (64) |

In the large limit, the limiting density of satisfies Eq. (7) with replaced by , that is using Eq. (64):

| (65) |

On the other hand, for since (see Eq. (51)), Eq. (55) reads:

| (66) |

so using the identity:

| (67) |

we have:

| (68) |

and hence by comparing Eq. (65) and (68), we have that the distribution is the symmetrized distribution of :

| (69) |

Furthermore, using again the identity Eq. (67) in Eq. (63) for with the definition of given by Eq. (64), we can write the rate function as:

| (70) |

where is the Stieltjes transform of , and is the rate function associated to the large deviation of the largest eigenvalue of . In other words, for a bi-invariant square matrix, the rate function associated to the largest singular value is twice the one associated to the largest eigenvalue of the invariant symmetric matrix whose limiting eigenvalue density is equal to the symmetrized distribution of . This can be heuristically guessed by remarking that for , we can express Eq. (52) as:

| (71) |

where the potential is symmetric by construction. The joint law of the (positive) singular values can be interpreted as the law of eigenvalues following the usual Eq. (5) where the first variables are constraint to be positive and each of the last is constraint to equal minus its positive counterpart. In the large limit, these constraints are irrelevant: the two problems have the same density (which does not depend on ) and differ by a factor of two for the rate function (which as an explicit factor).

Example (Rate function for Ginibre matrices): If is a Ginibre matrix, the LSVD is the quarter-circle law of Eq. (57) and its symmetrized density is the semi-circle law of Eq. (8). As a consequence, the rate function of the largest singular value of a Ginibre matrix is given by:

| (72) |

For , is a Wishart with shape parameter , so Eq. (72) and Eq. (61) give the relation (37).

3 The tilting method

3.1 Notation

In the previous section, we have reviewed the results concerning the right large deviation of the top eigenvalue (or singular value) of one random matrix. The goal of this section is to describe the general framework to tackle the case of the large deviation of the largest eigenvalue (resp. singular value) of a matrix given as the (free) sum or product of two symmetric (resp. rectangular) random matrices and . In the large limit, the limiting density (resp. ) of eigenvalues (resp. singular values) of the matrix is given by free probability theory and depends precisely on the operation (sum of symmetric matrices, product of symmetric matrices or sum of rectangular matrices666As we will see, the case of the product of two rectangular matrices can be deduced from the symmetric case.) one is considering. This will be discussed in each dedicated section, see Secs. 4, Sec. 5 and Sec. 6 respectively, but we argue that the strategy to get the right large deviation is the same. To put everything in the same framework we denote by

| (76) |

In any case, if we denote by the edge of the spectrum of (resp. ), we have:

| (77) |

and similar to the one-random matrix model, the natural question is to estimate the probability at large but finite . Since one recovers the original setting by taking the limit (the null matrix) in the additive case or (the identity matrix) in the multiplicative case, one should expect again to have the same different scaling as before for . As before, to tackle both the symmetric and rectangular cases at the same time, let’s denote by:

| (81) |

such that is the rate function we want to compute:

| (82) |

from the knowledge of the laws of the matrices and .

3.2 Idea of the tilting method and general expression for the rate function

The starting point for the derivation of the large deviation of one random matrix is the joint law density of the eigenvalues/singular values , from which we can use the Coulomb gas approach. For the sum or the product of matrices, one does not have a simple expression for the joint density of the eigenvalues/singular values, except in some specific cases, see Ref. [44]. Instead of directly looking at the matrix , the idea introduced in Ref. [1] in the context of RMT, is to look at a weighted realization of this matrix. If we denote by the probability density of the random matrix in the space of symmetric/rectangular matrix, let’s consider another random matrix whose probability density is given by:

| (83) |

where is a function whose precise expression will be given later on. For now, let us note that this function depends on only through its eigenvalues/singular values in addition to the free parameter . The expectation in the denominator of the RHS of Eq. (83) is an average over (and hence an average over both and ): such that is well normalized. Because only depends on the we can relate the joint density of the eigenvalues/singular values of to the (unknown) joint density of eigenvalues/singular values of :

| (84) |

by integrating Eq. (84) we have:

| (85) |

Now if we choose such that for large this function explicitly depend on the position of the largest eigenvalue/singular value but is self-averaging with respect to the other and thus independent of them, then the integral over these variables is nothing else than the probability of Eq. (82) we want to estimate. At large the density of eigenvalues (or singular values) of is the same as , but the position of top eigenvalue/singular value might different. In other words, we have:

| (86) |

where we have introduced the quenched free energy as the large limit

| (87) |

where indicates that the limit is taken with the constraint that the top eigenvalue (or singular value) is fixed at ; and similarly the annealed free energy as:

| (88) |

Given a value of the free parameter , what is the typical value of the largest eigenvalue (or singular value) of the matrix as goes to infinity? By Jensen inequality, the function in the bracket of the RHS of Eq. (85) is always non-positive (otherwise the probability would be higher than one) and so the typical value corresponds to the case where this function is exactly zero, namely is given as the solution of:

| (89) |

Now the idea of the tilting method is to look at Eq. (89) the other way: fix any , can we vary the free parameter until it reaches a value such that now the event becomes typical? If so, we can relate the unknown rate function to the annealed and quenched free energies:

| (90) |

Since the LHS of (85) is a probability measure, it is always bounded by one, so this optimal - if it exists - is given by:

| (91) |

In particular, if the supremum is a maximum, one has that is solution of:

| (92) |

Next since we have Eq. (77), by construction . One can therefore take the derivative of Eq. (90) with respect to to get the following integral representation for the rate function:

| (93) |

but by Eq. (92) the second term is null, so that we have the following simple formula:

| (94) |

3.3 Spherical Integrals as tilting functions

To summarize, we need to find a tilting function which in the large limit only depends on the limiting distribution of the matrix and the position of its top eigenvalue/singular value and such that:

-

1.

we can compute the partial derivatives of the quenched free energy Eq. (87),

-

2.

we can compute the derivative of the annealed free energy of Eq. (88),

-

3.

we can show that for each , there is one optimal temperature solution of Eq. (92) and we compute it,

then we get the rate function thanks to Eq. (94). Based on this necessary properties, we argue that a natural candidate for the tilting function is given by the spherical integral of the operation we are considering. The reason is twofold:

-

•

On the one hand, the quenched free energy associated to each spherical integral has been computed before in the literature, see Refs. [36, 37, 38, 39, 40], and is known to satisfy a transition depending on the parameter , between a phase where it does not depend explicitly on the position of the top eigenvalue/singular value and a phase where it does. The asymptotics of the quenched free energy is summarized in Sec. 4.3, in Sec. 5.3 and in Sec. 6.3 for respectively the additive spherical integral, the multiplicative spherical integral, and the rectangular spherical integral.

-

•

On the other hand, the spherical functions satisfy (by construction, as we will see later on) the following decomposition property:

(95) Applying the logarithm function and dividing by Eq. (95), this means that the annealed free energy is given by:

(96) where for (and similarly for ), we have defined

(97) and put explicitly the dependence in the position of the wall (resp. ). Since we have a precise description for the law of each matrix and separately but not for , this allows us to compute the annealed free energy and the results are also given in Sec. 4.3, in Sec. 5.3 and in Sec. 6.3.

As a consequence, once we have an expression for the (derivatives of) the annealed and quenched free energies, we only need to prove that the optimal is well defined for each (attainable) and compute it. This is done for each case in Sec. 4.5; Sec 5.4 and Sec. 6.4 . Injecting this expression in Eq. (94), we can then get an expression for the rate function and the results are given in in Sec. 4.6, in Sec. 5.5 and in Sec. 6.5.

Remark (Spherical function as partition function of spherical spin glass model): We have used the notations of statistical physics to denote the quantities of Eq. (87) and (88) as respectively the quenched and annealed free energies. The reason is that the spherical integral can be seen as the partition function over configuration living on the sphere, with disorder and inverse temperature :

| (98) |

The precise description of the spin glass model will depend on the nature of the operation we are considering and be given explicitly in Sec. 4.2 for the case of the sum, in 5.2 for the case of the product, and in Sec. 6.2 for the rectangular case. Let us mention that the rate function is given as the highest difference between the quenched and the annealed free energy for a value of the top eigenvalue/singular value being fixed. Since for such systems it is known that both the quenched and annealed free energies are equal (this is the so-called ’paramagnetic phase’) below a certain threshold of the inverse temperature, the optimal inverse temperature in Eq. (91) is necessarily attained after this threshold (in the so-called ’spin-glass phase’).

Remark (the case of diagonal matrices and wall at the edge): If one of the matrix, say , is replaced by a diagonal (resp. rectangular diagonal) matrix, as described in Sec. 2.2 (resp. as described in Sec. 2.4.3), then the decomposition property (95) is now given by:

| (99) |

Since there is no constraint on the top eigenvalue/singular value, and the limiting density of is the same as the one of , we have for the free energy

| (100) |

Now we argue that in each case, we have the following property:

| (101) |

such that the derivative of the annealed free energy of Eq. (96) and Eq. (100) are equal. Since no other quantity is modified, from the point of view of large deviation, it is equivalent to replacing the diagonal matrix by a random matrix from an invariant ensemble with the same limiting density , but with a wall at the edge. The same argument holds if one considers the free sum of two diagonal matrices.

4 Large deviation for the sum of symmetric matrices

In this section, we consider the case where the matrix is given as

| (102) |

where and are two symmetric matrices, each taken from an invariant ensemble with a wall as defined in Sec. 2.2. We aim at computing the rate function777We recall that since we are studying the symmetric case, one needs to replace the notation and in Sec. 3 by and respectively. :

| (103) |

where is the edge of the limiting spectrum of , and is described by free probability, see the next paragraph.

4.1 The sum of invariant matrices: free convolution and the R-transform

The limiting spectral distribution is a smooth density with right edge and is given as the unique probability distribution solution of:

| (104) |

for all in the complex plane close enough to the origin, where (resp. ) is the R-transform of the limiting spectral distribution (resp. ):

| (105) |

where denotes the (functional) inverse of the Stieltjes transform of Eq. (23). This inverse, and hence also the R-transform, is only defined between . However, for invariant ensemble, one can extend analytically this function for values beyond . In this case, this corresponds to inverting the second branch of the Stieltjes transform given by Eq. (24) and not the Stieltjes branch itself, see App. A.1. In the following, the R-transform has to be understood with this analytical continuation procedure. Eq. (104) shows that the R-transform linearizes the sum, and hence it is the random matrix analogous of the cumulant generating function of classical probability. The limiting spectral distribution is therefore called the free (additive) convolution of and and is usually denoted by in the RMT literature. We refer the reader to Ref. [45, 46, 47] for more detail on the free convolution. We will be using the two following properties of the additive free convolution:

- •

-

•

The Stieltjes transform at the edge of the spectrum of the matrix satisfies the following inequality:

(107)

see App. A.3.

Example (R-transform of GOE matrices): For a GOE matrix inverting Eq. (30), one has that the inverse of the Stieljes is given by:

| (108) |

and so the R-transform is given by:

| (109) |

Example (R-transform of Wishart matrices): For a Wishart matrix inverting Eq. (33), one has its R-transform is given by:

| (110) |

4.2 The additive spherical integral and the SSK model

Based on what we have discussed in Sec. 3.3, we argue that a natural candidate for the tilt function of Eq. (83) is given by the additive spherical function , where for any symmetric matrix and positive, it is defined by:

| (111) |

where is the hypersphere of radius one and is the compact notation for the uniform measure over normalized to one. It is clear that this function only depends on the eigenvalues of , because we can always absorb the matrix of eigenvectors in the variable of integration by a change of variable. Equivalently, the additive spherical integral can be written as

| (112) |

where is the normalized uniform Haar measure over . In RMT, is also known as the rank-one Harish-Chandra-Itzykson-Zuber (HCIZ) integral, see Ref. [48, 49]. The asymptotic behavior of this spherical integral is related to the -transform, as we will see later. Note that if one replaces the rank one matrix in Eq. (112) by a full rank matrix, then the asymptotic is governed by a different complex variational principle that was first derived by Matytsin, see Refs. [50, 51, 52] and it is an open problem to understand the crossover between the two different regimes. By Haar invariance, for any symmetric matrices and , we have the following property:

| (113) |

If we now apply this relation for and , since by Eq. (2) we have , and and are independent, we have after taking the average over both and , the desired property (95).

As we have argued in Sec. 3.3, we can interpret the additive spherical as the partition function of spherical model. Indeed, we can always write Eq. (111) as

| (114) |

where to follow the standard notation in statistical physics, we have denoted by the uniform average over the spins living in the sphere of radius one and the Hamiltonian is given by the quadratic form:

| (115) |

This model is known (see Refs. [53, 54, 55, 56]) as the () Spherical Sherrington-Kirkpatrick (SSK in short) model888The SSK is usually introduced with a different convention by absorbing the in the spin variable: so that the spins lives on a sphere with radius , which does not change the spherical integral.. The matrix is the disordered pairwise interaction and the parameter is the inverse temperature of the model. The SSK model has been studied in detail in the literature, and in particular the case where is a GOE matrix has received a lot of attention. In this paper, we are interested in the case where given by Eq. (102). Qualitatively, for high temperature it is known that the system is in a paramagnetic phase and all eigenvalue of the matrix contributes roughly equally to the partition function while for low temperature the situation is drastically different and the system is in a spin glass phase where the partition function is dominated by rare configurations which put more weight on the top eigenvalue .

4.3 Asymptotic behavior of the annealed and quenched free energies of the SSK model

As explained in Sec. 3, in order to get the rate function of the largest eigenvalue of , we need to compute the derivatives of the quenched and annealed free energies of Eq. (87) and Eq. (88) with the partition function given by Eq. (111). For a matrix with limiting density conditioned to have its largest eigenvalue fixed at the position , the partial derivatives of the quenched free energy are known [36] to be given by:

| (119) |

and by:

| (123) |

Thanks to Eq. (96), the computation of the (derivative of the) annealed free energy reduced to the computation of the annealed free energies and given by Eq. (97). Those annealed free energies can be computed based on (an extension of) recent ideas developed in Ref. [35] in the case of GOE. The proof is left in the App. B. For (and similarly for ), the annealed free energy is given by

| (127) |

where is the second branch of the Stieltjes transform from Eq.(24). Let us mention two important remarks:

Remark (wall at the edge and diagonal matrices): If we choose the position of the wall to be exactly at the edge: , since we have the relation

| (128) |

Eq. (127) reads in this case:

| (132) |

Comparing Eq. (132) and Eq. (119) (with the index replaced by the index and for ), we see that we have indeed the relation (101) such that from the point of large deviation we can consider a fixed diagonal matrix as an invariant matrix with a wall at the edge of its distribution.

Remark (wall at infinity and classical invariant ensemble): Since classical ensembles are obtained by taking the limit , we have for the corresponding annealed free energy:

| (136) |

where we recall that is defined as the limit of the second branch of Stieltjes transform, see Eq. (106). One may note that the second line of Eq. (136) is removed if (which is for example is the case for a GOE matrix, see Eq. (31) for ) but is present otherwise (which is for example is the case for a Wishart matrix for which , see Eq. (34) for ).

4.4 Retrieving the right large deviation for one random matrix

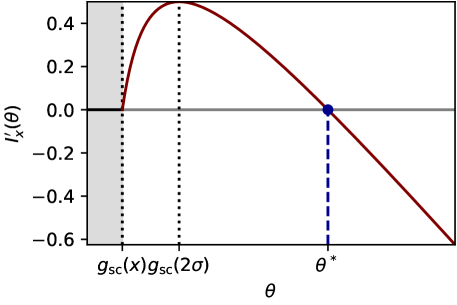

The next step in order to get the rate function is to show that there exist an optimal temperature and compute it. Let’s consider the case of one random matrix in a classical invariant ensemble, and let’s retrieve the expression of Eq. (25) with the tilting method as a warm-up exercise. For any , the optimal inverse temperature is given as the supremum of Eq. (91) with the notation and replaced by and .

One may notice by integrating Eqs. (119) and (136) with respect to , that for between and , we have:

| (137) |

This corresponds to the high temperature regime (or paramagnetic phase) of the system where both the annealed and quenched free energy are equal. Necessarily, the optimal temperature , if there is one, cannot be in this region since from Eq. (91), we want precisely the difference between the two free energies to be as high as possible. We can therefore restrict the range of possible optimal temperature to be in the spin glass phase, :

| (138) |

Let’s compute the derivative with respect to of this function . According to Eq. (119) and Eq. (136), and the definition of the -transform given by Eq. (105), it is simply given by:

| (139) |

Here the function contains the inverse of both branch of the Stieltjes transform. It is decreasing until it reaches the value and then it is increasing until it reaches the (possible infinite) value, where it goes to infinity. Conversely, the function of Eq. (139), seen as function of for fixed, starts at zero at and then is increasing until it reaches the point and then decreasing again, and goes to as . Thus, as one varies starting at , this function is positive and then negative and only crosses the real axis once. As a consequence, the supremum in Eq. (138) is a maximum and this maximum is unique. This maximum is given at the unique point where the function of Eq. (139) crosses the real axis in the region . In other words, finding amounts to solve the equation:

| (140) |

which is nothing else than the definition of the second branch of the Stieltjes transform, that is we have:

| (141) |

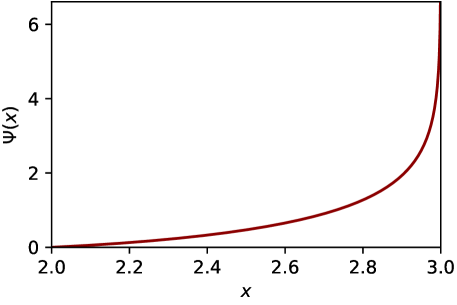

If we now use the integral representation Eq. (94) of the rate function, with the expression of Eq. (123) for the partial derivative of the quenched free energy, together with Eq. (141) for the expression of , we recover Eq. (25) as expected. A plot of the function , for a GOE matrix, is given in Fig. 5.

4.5 Optimal inverse temperature for the sum

Let’s now consider the general case given by Eq. (102). Without loss of generality, we can consider999For general and , having does not imply nor its converse. One can even come up with examples where has a no wall () while has a finite wall but still .

| (142) |

We further assume the non-trivial condition:

| (143) |

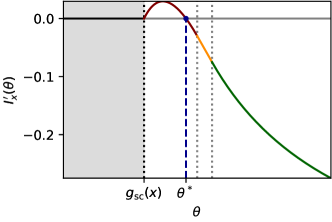

as for (which necessarily implies by Eq. (107)), the right large deviation is infinite for any . As in the previous section, we first want to show that the supremum in Eq. (91) is attained at a unique point, where is given by the sum of Eq. (96) and the annealed free energies and are given by Eq. (127). Since the function is given as the sum of three piece-wise functions, let’s first note that we have the following set of inequalities:

| (144) |

The first inequality is due to the fact that the Stieltjes is decreasing for . The second inequality is the property (107) of the free convolution. The third is due to the second branch of the Stieltjes transform being monotonically increasing. The fourth is the previously mentioned convention of Eq. (142). Using the asymptotics of Eqs. (119) (127) for the quenched and annealed free energies, together with the linearizing property (104) of the R-transform, one has the following behavior for the difference between the derivative of the annealed and quenched free energy:

| (152) |

where if one has to remove the last line and similarly if , one has to remove the last two lines. This function is represented in Fig. 6 for different values of . Let’s look at each interval separately.

-

1.

For , we are in the paramagnetic phase where both the annealed and the free energy are equal. Since for each , we want again the difference between the two to be as high as possible, the optimal inverse temperature is not in this region of the phase space.

-

2.

For , as we have seen in the simple case of one invariant matrix, the function is increasing until it reaches and then decreasing.

-

3.

For , since the R-transform is increasing, the function is decreasing.

-

4.

For , the function is decreasing.

One can easily check that the function of Eq. (152) is continuous at each point where its behavior changes. At it is equal to:

| (153) |

and at , it is equal to:

| (154) |

To summarize, in the spin glass phase the function of Eq. (152) is continuously increasing until and then it is continuously decreasing. For , it is easy to check that this function never crosses the real axis for values of , as a consequence,

| (155) |

This is expected because for the sum of two matrices we have the classical inequality:

| (156) |

and since by definition of the walls, and , the top eigenvalue of cannot exceed . So we find that the rate function is infinite for . Otherwise, for values of , this function always crosses the real axis once in this region. The correct equation for - the point where the function touches the real axis, see Eq. (92) - depends on if the value of this function at or is above or below zero, and hence on the value of . There exist three possible cases, separated by two critical points, and defined respectively as the solution of the RHS of Eq. (153) and the RHS of Eq. (154)) being equal to zero, that is:

| (157) |

and

| (158) |

Note that as we have postulated Eq. (142). We have:

-

1.

for , the optimal inverse temperature is attained in the region and so replacing in Eq. (92) the expression of the difference of the free energies by the top line of Eq. (152), it is solution of the same equation (140) as the one in the simple one invariant random matrix case (with replaced by ) and thus we have:

(159) where is defined as the inverse of for values beyond .

-

2.

For , the optimal inverse temperature is attained in the region and so from the expression of the second line of the RHS of Eq. (152), it is solution of:

(160) since the R-transform is continuously increasing, it has an inverse which we denote by so that the optimal temperature is given by:

(161) -

3.

For , is attained in the region and so solving the third line of Eq. (152) being equal to zero, we have:

(162)

One can check that the piecewise function is actually continuously increasing.

4.6 Expression for the rate function

Now that we have the expression for the optimal temperature, we can get the expression for the (right) rate function thanks to Eq. (94). This gives:

| (168) |

and is infinite for values of outside . The constant (resp. ) is given when (resp. when ) by:

| (169) |

and by:

| (170) |

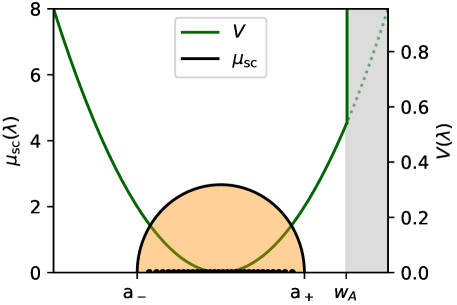

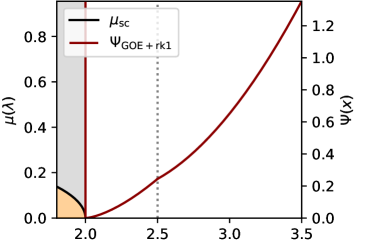

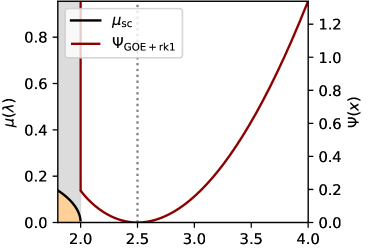

such that the rate function is continuous (and actually at least ) at each critical point. Remark (Effective potential): The effective potential Eq. (29) can be computed from the rate function and gives that is equal to the same expression as Eq. (168) with a plus sign instead of a minus sign in front of (including in the constants Eqs. (169) and (169)). The potential is only defined up to an arbitrary constant chosen here such that . An example of effective potential in plotted in Fig.7.

Remark (Tracy-Widom ’3/2’-scaling near the edge): Since the first regime matches the ones of the classical case of one random matrix given by Eq. (25), we retrieve in particular the Tracy-Widom ’3/2’-scaling of Eq. (42) near the edge for the free convolution of non-degenerate densities, as recently investigated in Ref. [57].

Remark (Number of critical points): In general, if one is considering the sum of two random matrices taken from an invariant ensemble with a wall, then the rate function has two possible critical points. However, if , then from Eqs. (157) (158), one can see that two critical points merge, and we have at most one critical point. In particular, this happens when one is considering the free sum , where is a fixed diagonal matrix. Since diverges if while diverges if either or , the free sum of a two fixed diagonal and a fluctuating matrix (no wall) has at most one critical point while the sum of two fluctuating matrices never has a critical point, in this case the rate function is the same as that of an invariant ensemble Eq. (25).

Remark (Interpretation of the three regimes): For the rate function is the same as the one from an invariant ensemble. In this regime, the eigenvalues (including rare large ones) of the matrix behave exactly as an invariant ensemble with the potential (and its analytical continuation outside the segment ) compatible with the limiting density , that is, is given by Eq. (7). In particular, walls (if any) do not modify the rate function in this regime. For , the wall starts to matter, the derivative of the rate function is now the same as if the matrix were replaced by a rank-1 matrix with eigenvalue but with the still correct (see App. C). Finally, for , both walls matter and the derivative of the rate function is now the same as for the sum of two rank-one matrices with eigenvalues and , again up to the correct (see App. D). In particular, very close to the maximal value , we have:

| (171) |

which is the asymptotic probability of two random vectors of having a squared overlap of order in dimension .

Example (Free sum of two diagonal semi-circle matrices): In this paragraph, we will compute explicitly the rate function for a matrix , where and are two fixed diagonal matrices with the semi-circle distribution of Eq. (8) as their limiting spectrum. Without loss of generality, let’s consider that their variance are given by and by respectively. The computation is equivalent to the sum of two invariant random matrices in quadratic potentials and a wall at for respectively. The free convolution of two semi-circle distributions is again a semi-circle distribution, with variance the sum of the variance. In other words, the limiting law and Stieltjes transform of the matrix is given respectively by Eq. (8) and Eq. (30) with . Since we have and the R-transform of the semi-circle distribution is given by Eq. (109), the optimal inverse temperature is given by:

| (177) |

and so the rate function is given for by

| (186) |

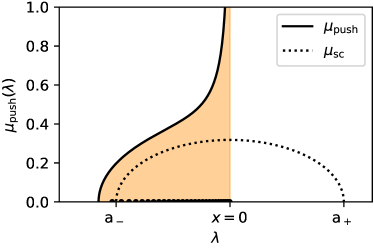

and is infinite otherwise. This function has been plotted in Fig. 7 for .

5 Large deviation for the product of symmetric matrices

In this section we consider the case where the matrix is given as the symmetric product:101010One may note that since we are interested in the eigenvalues, we can equivalently consider the product since this matrix is similar to the matrix and hence has the same eigenvalues. However, unlike , the matrix is a priori not symmetric.

| (187) |

where and are two positive semi-definite random matrices. In the large limit, the limiting density of is described by the multiplicative free convolution of the next section and our goal is to compute the rate function :111111We recall once again that since we are studying the case of symmetric matrices, one needs to replace the notation and by respectively and in Sec. 3.

| (188) |

describing the right large deviation of the top eigenvalue of far from its typical value given by the edge of . Let us make the following important remark concerning the case of the product of rectangular matrices. Remark (product of rectangular random matrices): We argue that the case of the product of two rectangular matrices reduced to the symmetric cases. Indeed, if we have two rectangular matrices and of size and respectively, then the non-zero singular values of the product are given by:

| (189) |

Since and are two symmetric matrices we recover the case of Eq. (187).

5.1 Product of invariant matrices: the multiplicative free convolution and the S-transform

The limiting density is given as the unique probability distribution solution of:

| (190) |

for all in the complex plane close enough to the origin, where (resp. ) is the (modified) S-transform121212The standard S-transform is usually defined in the literature as the reciprocal of our S-transform: . As we will see, the convention will appear more naturally. of the limiting spectral distribution (resp. ):

| (191) |

where (resp. ), is the T-transform of the limiting distribution (resp. ), which is defined for all by:

| (192) |

Similarly, we define the second branch of the T-transform as:

| (193) |

The function is the inverse of continued to values higher than . As a consequence of Eq. (190), the logarithm of the S-transform linearizes the multiplication and hence it is the random matrix analogous of the (log of the) Mellin transform of classical probability. The limiting spectral distribution is therefore called the free multiplicative convolution of and and is usually denoted by in the RMT literature. We will be using the following properties of the multiplicative free convolution:

- •

- •

5.2 The multiplicative spherical integral and the LSSK model

For the multiplicative case, we argue that a good candidate for the tilt is the multiplicative spherical integral , where for any positive semi-definite matrix and , this spherical integral is given by:

| (197) |

where we recall that is the hyper-sphere of radius one and is the unit uniform measure over . By Haar property, for any two positive semi-definite matrices and , this function satisfies:

| (198) |

which gives for and taken from an invariant ensemble and after averaging, the desired decomposition property of Eq. (95).

We can again interpret as the partition function of a spherical model:

| (199) |

with the Hamiltonian:

| (200) |

Since is the symmetric product of definite positive matrices, its eigenvalues are positive, so this Hamiltonian is well defined. In this paper, we are interested in the case given by Eq. (187). Due to the logarithmic term, we denote this model as the Logarithmic Spherical Sherrington-Kirkpatrick (LSSK for short) model. The behavior of for large has been recently investigated in Refs. [38, 39] and are given in the following section. Due to its similarity with the original SSK model, one should expect to have a similar behavior, with a paramagnetic phase at high temperature and a spin glass phase at low temperature.

5.3 Asymptotic behavior of the quenched and annealed free energies of the LSSK model

We summarize here the asymptotic behavior of (the derivatives of) the quenched and annealed free energies.

For conditioned to have its largest eigenvalue fixed at the position , the partial derivatives of the quenched free energy of Eq. (87) with given by Eq. (197) satisfy a phase transition. In the high temperature regime, it has been shown in Refs. [38, 39] that the derivative with respect to the parameter of the quenched free energy is for small enough the logarithm of the S-transform. One can also get the behavior for low temperature where there is a saturation, and we have:

| (204) |

Similarly, the partial derivative with respect to is given by:

| (208) |

For the derivative of the annealed free energy , one only needs the of and separately since we have the decomposition of Eq. (96), which are given by (see App. B.2 for a derivation):

| (212) |

and similarly for . Note that if the wall is at the edge , since , we have Eq. (101) and hence form the large deviation of the top eigenvalue, we can indeed consider fixed diagonal matrices as invariant matrices with a wall at the edge. Conversely, classical invariant ensembles correspond to the limit from which we see that the annealed free energy is equal to the logarithm of the S-transform for , with given by the limit of (194), and is otherwise infinite.

5.4 Optimal temperature for the product

Without any loss of generality, let’s assume

| (213) |

and

| (214) |

Our goal is to show that the supremum in Eq. (91) is attained at a unique point by looking at the derivative with respect to . Paying attention to the bounds in Eqs. (204) and (212), one has the following behavior:

| (222) |

Based on similar monotonous argument as in the additive case of Sec. 4.5 , one can show that for this function is continuously increasing until it reaches the point and then it is continuously decreasing. For values of , it never crosses the real axis, and we have . Otherwise, it crosses the real axis exactly one time and the equation determining depends on the position of with respect to the two critical points and defined by

| (223) |

and by:

| (224) |

-

1.

for , is attained in and so setting the second line of the RHS of Eq. (222) being equals to zero, gives:

(225) -

2.

for , the optimal inverse temperature is attained in the region and is solution of the third line of the RHS of Eq.(222) being equal to zero, that is:

(226) -

3.

for , is attained in the region and so from Eq. (222) it is given by:

(227)

5.5 Expression for the rate function

Using the expressions of the previous section for the optimal temperature together with the expression of the partial derivative of the quenched free energy of Eq. (208) in Eq. (94), we have that the rate function is given by:

| (233) |

and is infinite for other values of . The constant is again given by Eq. (169) with now given Eq. (223) (if and is defined by:

| (234) |

if .

Example (Rate Function for Generalized Wishart): Let’s consider the case in Eq. (187) where is a (White) Wishart with shape ratio and is a fixed diagonal (positive semi-definite) matrix. In this case, we have and . As a consequence, there is just one critical point and using the expression (191) for the S-transform of the Wishart matrix, it is given by:

| (235) |

and using Eq. (196) for the S-transform, we have for the rate function:

| (239) |

which is up to a change in the notation, the results obtained in Ref. [34].

6 Large deviation for the top singular value of sum of rectangular matrices

In this section, we consider the case where the matrix is given as

| (240) |

where and are two rectangular matrices, each taken from a bi-invariant ensemble with a wall as defined in Sec. 2.4.3. We aim at computing the rate function :131313We recall that since we are studying the rectangular case, one needs to replace the notation and in Sec. 3 by and respectively.

| (241) |

where is the edge of the limiting density of singular values of , described by the rectangular free convolution, see the next paragraph. Note that unlike the case of the product of rectangular matrices, this case does not boil down to consider the sum of symmetric matrices, since:

| (242) |

For specific values of (namely , corresponding to long matrices and , corresponding to square matrices), it is known - as we will see - that this rectangular free convolution is related to the additive free convolution of Sec. 4.1.

6.1 Rectangular free convolution

The LSVD of of Eq. (240) is given by the rectangular free convolution (with shape ratio ) [58, 59], denoted by in the RMT literature, which is – similarly to the additive and multiplicative free convolution – defined via a linearizing transform called the (modified)141414The standard convention for the rectangular R-transform, , is related to our rectangular C-transform , via . As we will see, the convention will appear more naturally. rectangular C-transform (with shape ratio ):

| (243) |

This transform is given by the formula:

| (244) |

where is defined by:

| (245) |

Note that is an increasing function of whose inverse transform is given by the simple formula:

| (246) |

The function in Eq. (244) is the inverse functional of the D-transform, which is the rectangular counterpart of the Stieltjes transform (resp. T-transform) in the additive (resp. multiplicative) case, defined by:

| (247) |

Note that if we denote by the Stieltjes transform of the measure , the limiting Stieltjes of the matrix , then we have:

| (248) |

Remark (long matrices () and additive free convolution): In the limit , corresponding to the case of ( rectangular long matrices with , we have for the function and the D-transform,

| (249) |

and

| (250) |

and so the inverse of the D-transform is given by:

| (251) |

As a consequence, the rectangular C-transform is related to the R-transform by

| (252) |

and so by the linearizing property of the C-transform and the R-transform we have:

| (253) |

In other words for long matrices, if one is looking at the LSVD of the sum, one can replace the symbol ’’ in Eq. (242) by an equality! Remark (square matrices () and symmetrized density): For , corresponding to (asymptotic) square matrices, the function is simply given by:

| (254) |

and the D-transform of Eq. (247) considerably simplifies (for ) into:

| (255) |

where we recall that is the symmetrized density of , given by Eq. (69). The C-transform of Eq. (244) reads in this case:

| (256) |

and by linearizing property, we have that the LSVD of the matrix is given as the unique probability measure on such that:

| (257) |

In other words, the singular values of the sum of two (bi-free) square matrices is given asymptotically by the additive free convolution of Sec. 4.1 of their respective symmetrized singular value densities. Example (Gaussian rectangular random matrices): Let’s consider the case of Gaussian rectangular matrices with LSVD given Eq. (56). Using Eq. (248) with the expression of Eq. (196) for the Stieltjes transform of the Marčenko-Pastur distribution, one gets the following expression for the D-transform (for ):

| (258) |

whose inverse is given by

| (259) |

The argument inside the square-root function is nothing else than the inverse evaluated at , see Eq. (246). Using Eq. (244), the rectangular C-transform of the Gaussian rectangular matrix is given simply by:

| (260) |

In the following, we will be using the two following properties of the rectangular free convolution:

-

•

we argue that the function is a continuous increasing function see App. A.2

- •

6.2 Rectangular spherical integral and the BSSK model

Similar to the cases of the sum of symmetric matrices, we choose the tilt function for the problem of the sum of rectangular matrices to be given by the rectangular spherical integral defined for any rectangular matrix and by:

| (262) |

For any rectangular matrices and , this function satisfies the following property:

| (263) |

which evaluated for and given as rectangular bi-invariant random matrices, gives after integration over the laws of and , the decomposition property of Eq. (95). This rectangular spherical can again be understood as the partition function of a spherical model with inverse temperature . Indeed, if we denote by

| (264) |

can be written as:

| (265) |

with the Hamiltonian

| (266) |

and by bi-invariance, this can be also written as:

| (267) |

This model is known [60, 61, 62] as the Bipartite Spherical Sherrington-Kirkpatrick (BSSK in short) spin model, due to the graph structure of the interaction matrix: each coordinate of one family vector interacts only with members of the other family.

6.3 Asymptotic behavior of the annealed and quenched free energy of the BSSK model

To have the rate function, we first need to compute the derivatives of the quenched and annealed free energy of the BSSK model of Eq. (87) and Eq. (88) respectively with the tilt function given by Eq. (262). For conditioned to have its largest singular value at the position , the quenched annealed free energy is known to be related to the rectangular C-transform for small enough value of the inverse temperature . For higher value, it depends also on the position , see the derivation in the Appendix, and we have in full generality:

| (271) |

Similarly, the partial derivative with respect to is given by:

| (275) |

The derivative of the annealed free energy is the sum of the derivative of the annealed free energy and which are given by:

| (279) |

and similarly for . If the wall is at the edge , since , we have Eq. (101) and hence form the large deviation of the top singular value, we can consider fixed rectangular diagonal matrices as bi-invariant matrices with a wall at the edge.

6.4 Optimal temperature for the rectangular case

Without loss of generality, we assume:

| (280) |

and the non-trivial condition:

| (281) |

In this case, the derivative with respect to of the function in the supremum of Eq. (91) is given by:

| (289) |

By property of the rectangular free convolution, for , this function is first increasing with until it reaches the value and then it is decreasing with . One can check that it crosses the real axis if is in the interval , and in this case, the position of the optimal inverse temperature depends on two critical points and . The first one is given by

| (290) |

Unfortunately, unlike the sum and the product of symmetric matrices, the expression for in terms of the rectangular C-transform is quite involved. if we introduce the function:

| (291) |

to ease the notation, then we have:

| (292) |

The other critical point is given by:

| (293) |

where we recall that is given by Eq. (246). Eq. (293) can be written in semi-explicit form with the function of Eq. (291):

| (294) |

-

1.

for , is attained in and hence is solution of the second line of the RHS of Eq. (289) being equals to zero. Using Eq. (244) to express the C-transform in terms of the function , one gets:

(295) and so by applying the (monotonous) function to this equation and dividing by , one gets to solve the equation:

(296) The solution is given by the second branch of the D-transform:

(297) -

2.

for , the optimal inverse temperature is attained in the region . is solution of the third line of the RHS of Eq.(289) being equal to zero so that it satisfies:

(298) If one applies the function on each side, one gets after simplification an analytical expression for the function :

(299) which is by definition the inverse of the function . Now unfortunately for general values of the parameter , we do not have a simple analytical formula for the optimal inverse temperature function of the position and so we simply denote by the solution of Eq. (299) with unknown for between and .

-

3.

for , is attained in the region and so from Eq. (289) and after simplification, one gets the following analytical expression for the function :

(300) In full generality, one can isolate one of the radical functions and take the square of the newly obtain equation and repeat the process until it becomes a polynomial equation. In our setting and for general , one would obtain that is one of the zeros of a polynomial of degree , and hence there is no hope of finding an analytical expression for . As a consequence, we simply denote by the solution (in of Eq. (300) for higher than . Now for specific values of and , for example , or , for example or , Eq. (300) becomes, after some work, a quadratic or even linear equation for (or ), as we will see.

Remark (Simplification for the case of long () matrices):

- •

-

•

For , Eq. (300) for the optimal inverse temperature simplifies into:

(303) such that the optimal temperature is given by:

(304)

Remark (Simplification for the case of square () matrices):

- •

- •

6.5 Expression for the rate function

Using the general expression of Eq. (94) for the rate function with the expression of Eq. (275) and the expression of the optimal inverse temperature of the previous section, we have:

| (314) |

where we recall that , are defined by Eq. (290) and Eq. (293) and (resp. ) is defined as the (correct) solution with unknown of Eq. (299) (resp. Eq. (300)) and and are the constants such that this rate function is continuous. To get the top line of Eq. (314) we have the property of Eq. (248) relating the D-transform and the Stieltjes transform. Remark (Rate function for the sum of long () matrices): In this case, we have:

| (320) |

Remark (Rate function for the sum of square () matrices): In this case, we have:

| (326) |

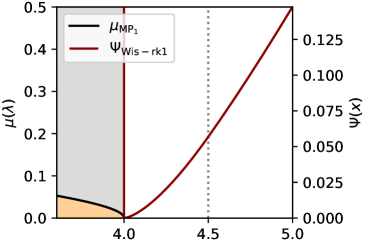

Example (Free sum of fixed diagonal quarter-circle distribution): Let’s consider two diagonal square matrices and with LSVD given by Eq. (57) where without loss of generality we take the variances to be respectively equal to and then we have that the rate function associated to the large deviation of the top singular value of the sum is given by:

| (327) |

with given by Eq. (186).

7 Conclusion

In this paper, we have derived the right large deviation function for:

-

1.

the top eigenvalue of the sum of two arbitrary symmetric matrices;

-

2.

the top eigenvalue of the product of two arbitrary symmetric matrices;

-

3.

the top singular of the sum of two arbitrary rectangular matrices;

where by arbitrary we mean that we can take the matrices to be either taken from a rotationally invariant ensemble (resp. a bi-invariant for the case of rectangular random matrices) or to be a randomly rotated fixed diagonal matrix (resp. a fixed diagonal rectangular matrices). The results rely on a direct link with spherical spin models and are summarized in Sec. 4.6 for the case of the sum of symmetric matrices, in Sec. 5.5 for the case of the product of symmetric matrices and in Sec. 6.5 for the case of the sum of rectangular matrices. In each case, we find that the rate function has up to three different regimes, and we give an interpretation of the behavior in each regime. Let us mention right away that this construction directly extends to complex matrices: for unitary invariant random matrices (resp. complex rectangular matrices), it is known that the derivatives of the quenched and annealed free energies are twice the ones of the real case and so does the rate functions. A natural question is to extend the above construction to tackle the ’left’ large deviation, for which the speed of convergence of the large deviation is . We leave this problem for future research.

Acknowledgements: P.M. would like to warmly thank Tristan Gautié for fruitful discussions at the early stage of the project. P.M. would also like to thank Florent Benaych-Georges for discussions regarding the properties of the rectangular free convolution and Satya Majumdar for several discussions regarding Coulomb gas and more generally large deviation problems in Random Matrix Theory. Both authors would like to thank Laura Foini and Jorge Kurchan for sharing their work on annealed averages.

References

- [1] A. Guionnet and M. Maïda, “Large deviations for the largest eigenvalue of the sum of two random matrices,” Electronic Journal of Probability, vol. 25, pp. 1 – 24, 2020.

- [2] J. Wishart, “The generalised product moment distribution in samples from a normal multivariate population,” Biometrika, vol. 20A, no. 1/2, pp. 32–52, 1928.

- [3] E. P. Wigner, “On the distribution of the roots of certain symmetric matrices,” Annals of Mathematics, vol. 67, no. 2, pp. 325–327, 1958.

- [4] S. F. Edwards and P. W. Anderson, “Theory of spin glasses,” Journal of Physics F: Metal Physics, vol. 5, pp. 965–974, may 1975.

- [5] D. Sherrington and S. Kirkpatrick, “Solvable model of a spin-glass,” Physical review letters, vol. 35, no. 26, p. 1792, 1975.

- [6] A. M. Tulino and S. Verdú, Random matrix theory and wireless communications. Now Publishers Inc, 2004.

- [7] J.-P. Bouchaud and M. Potters, Theory of financial risks, vol. 4. Cambridge University Press, Cambridge From Statistical Physics to Risk …, 2000.

- [8] J. Pennington and P. Worah, “Nonlinear random matrix theory for deep learning,” in Advances in Neural Information Processing Systems (I. Guyon, U. V. Luxburg, S. Bengio, H. Wallach, R. Fergus, S. Vishwanathan, and R. Garnett, eds.), vol. 30, Curran Associates, Inc., 2017.

- [9] L. Benigni and S. Péché, “Eigenvalue distribution of some nonlinear models of random matrices,” Electronic Journal of Probability, vol. 26, Jan 2021.

- [10] I. Jolliffe, “Principal component analysis,” Oct. 2005.

- [11] R. M. May, “Will a large complex system be stable?,” Nature, vol. 238, no. 5364, pp. 413–414, 1972.

- [12] S. Allesina and S. Tang, “The stability–complexity relationship at age 40: a random matrix perspective,” Population Ecology, vol. 57, no. 1, pp. 63–75, 2015.

- [13] H. Sompolinsky, A. Crisanti, and H.-J. Sommers, “Chaos in random neural networks,” Phys. Rev. Lett., vol. 61, no. 3, p. 259, 1988.

- [14] G. Wainrib and J. Touboul, “Topological and dynamical complexity of random neural networks,” Phys. Rev. Lett., vol. 110, no. 11, p. 118101, 2013.

- [15] J. Moran and J.-P. Bouchaud, “May’s instability in large economies,” Phys. Rev. E, vol. 100, no. 3, p. 032307, 2019.

- [16] Y. V. Fyodorov, “Complexity of random energy landscapes, glass transition, and absolute value of the spectral determinant of random matrices,” Phys. Rev. Lett., vol. 92, p. 240601, Jun 2004.

- [17] V. Ros, G. Ben Arous, G. Biroli, and C. Cammarota, “Complex energy landscapes in spiked-tensor and simple glassy models: Ruggedness, arrangements of local minima, and phase transitions,” Phys. Rev. X, vol. 9, p. 011003, Jan 2019.

- [18] G. Ben Arous, Y. V. Fyodorov, and B. A. Khoruzhenko, “Counting equilibria of large complex systems by instability index,” Proceedings of the National Academy of Sciences, vol. 118, no. 34, 2021.

- [19] G. B. Arous, A. Dembo, and A. Guionnet, “Aging of spherical spin glasses,” Probability Theory and Related Fields, vol. 120, pp. 1–67, May 2001.

- [20] D. S. Dean and S. N. Majumdar, “Large deviations of extreme eigenvalues of random matrices,” Phys. Rev. Lett., vol. 97, p. 160201, Oct 2006.

- [21] D. S. Dean and S. N. Majumdar, “Extreme value statistics of eigenvalues of Gaussian random matrices,” Phys. Rev. E, vol. 77, p. 041108, Apr 2008.